United States Securities and Exchange Commission

Washington, D.C. 20549

Form N-CSR

Certified Shareholder Report of Registered Management Investment Companies

811-21235

(Investment Company Act File Number)

Federated Hermes Premier Municipal Income Fund

(Exact Name of Registrant as Specified in Charter)

Federated Hermes Funds

4000 Ericsson Drive

Warrendale, PA 15086-7561

(Address of Principal Executive Offices)

(412) 288-1900

(Registrant’s Telephone Number)

Peter J. Germain, Esquire

1001 Liberty Avenue

Pittsburgh, Pennsylvania 15222-3779

(Name and Address of Agent for Service)

(Notices should be sent to the Agent for Service)

Date of Fiscal Year End: 2024/11/30

Date of Reporting Period: 2024/11/30

| Item 1. | Reports to Stockholders |

Annual Shareholder Report

Federated Hermes Premier Municipal Income Fund

Dear Valued Shareholder,We are pleased to present the Annual Shareholder Report for your fund covering the period from December 1, 2023 through November 30, 2024. This report includes Management’s Discussion of Fund Performance, a complete listing of your fund’s holdings, performance information and financial statements along with other important fund information.

As a global leader in active investment management, Federated Hermes is guided by our conviction that responsible investing is the best way to create wealth over the long term. The company provides capabilities across a wide range of asset classes to investors around the world.

In addition, FederatedHermes.com/us offers quick and easy access to valuable resources that include timely fund updates, economic and market insights from our investment strategists and financial planning tools. You can also access many of those insights by following us on Twitter (@FederatedHermes) and LinkedIn.

Thank you for investing with us. We hope you find this information useful and look forward to keeping you informed.

Sincerely,

J. Christopher Donahue, President

Not FDIC Insured ▪ May Lose Value ▪ No Bank Guarantee

Management’s Discussion of Fund Performance (unaudited)

The total return of Federated Hermes Premier Municipal Income Fund (the “Fund”), based on net asset value (NAV) for the 12-month reporting period ended November 30, 2024, was 9.47% for the Fund’s Common Shares (FMN).1 This total return consisted of 3.73% of tax-exempt dividends and reinvestments and appreciation of 5.74% in the NAV of the Common Shares.2 The Fund’s broad-based securities market index, the S&P Municipal Bond Index (SPMUNI),3 had a total return of 5.52% during the reporting period. The average total return of the Morningstar US Closed End Muni National Long category (MCEMNL),4 a peer group comparison for the Fund, was 8.48% during the reporting period. The Fund’s and the MCEMNL total returns reflected the effect of leverage, transaction costs and expenses which were not reflected in the total return of the SPMUNI.

The Fund’s use of structural leverage had a positive net impact on Fund returns at NAV. Leverage amplified NAV volatility as yields fluctuated widely during the year, driving both sharp drops and increases in the Fund’s net asset value. The cost of leverage decreased moderately as the Federal Reserve (the “Fed”) cut its target short-term interest rates by 75 basis points later in the period. The dividend rate paid to preferred shareholders is linked to the Securities Industry and Financial Markets Association (SIMFA) Municipal Swap Index. This index fluctuates with market conditions and reflects the Fed’s policy changes. The four-week moving average of the SIFMA Municipal Swap Index, which smooths out the week-to-week volatility, peaked at 3.86% in April and ended the period at 3.08%.

Excluding the impact of leverage, the Fund’s portfolio outperformed the SPMUNI. Portfolio duration,5 yield curve6 positioning, allocation of exposures across different credit quality ratings7 and among municipal credit sectors, and favorable security selection each contributed favorably to relative performance.

For the Period Ended November 30, 2024:

| Total Returns (Annualized) |

| | | | | |

| | | | | |

Morningstar US Closed End Muni National Long Median | | | | | |

PERFORMANCE AT MARKET PRICE

For the Period Ended November 30, 2024:

| Total Returns (Annualized) |

| | | | | |

| | | | | |

Morningstar US Closed End Muni National Long Median | | | | | |

A closed-end fund’s market price typically differs from its NAV. If a closed-end fund’s shares trade at a price below their NAV, they are said to be trading at a discount. Conversely, if a closed-end fund’s shares trade at a price above their NAV, they are said to be trading at a premium. Market forces in the trading of the shares of a fund determine the market price, while a fund’s NAV is primarily based on the total market value of the securities held in a fund’s portfolio. The extent to which the share price and NAV diverge will affect the return for a fund’s shareholders. Below is the Premium/Discount of Market Price to NAV for the Fund and the median for its peers on the following dates:

| | | |

| | | |

Morningstar US Closed End Muni National Long Median | | | |

Annual Shareholder Report

Market OVERVIEW

Municipal bond and U.S. Treasury yields ranged widely during the 12-month reporting period. Fluctuations in U.S. growth, employment, and inflation data over the period drove sharp changes in the expected timing and amount of Fed easing. Ultimately, the Fed lowered target interest rates in both September and November. In addition, the outcome of the U.S. elections supported expectations of stimulative and potentially inflationary fiscal and immigration policies in coming years, placing upward pressure on Treasury and municipal yields late in the period.

The 30-year U.S. Treasury yield ranged from a high of 4.81% in April 2024 to a low of 3.93% in September 2024. Yields on 2-, 10- and 30-year Treasury securities ended the period lower by 53, 16 and 13 basis points, respectively, with shorter term yields falling more because of Fed’s policy easing. The Bloomberg Evaluation Services (BVAL)10 30-year AAA tax-exempt municipal yield ranged from a low of 3.40% in December 2023 to a high of 4.02% in April 2024. The 2-, 10- and 30- year AAA municipal yields ended the period down 26, up 16 and down 24 basis points, respectively. The increase in the 10-year AAA yield reflected a correction in the unusual inversion of the municipal yield curve as the Fed signaled it would lower policy rates and investor demand shifted along the yield curve.

DURATION AND Yield Curve Positioning

The portfolio maintained a duration that was long to varying degrees relative to the SPMUNI over the period, including, at times, the use of short and long positions in Treasury futures as market yields fluctuated. Overall, management of portfolio duration contributed to favorable relative performance. Yield curve positioning also contributed favorably to relative performance due to an overweight allocation in longer term municipal securities that outperformed.

Mid- and lower-quality11 municipal bonds outperformed during the period amid sustained economic expansion, strong investor demand for lower quality credits, and narrowing credit spreads. The Fund held overweight allocations relative to the SPMUNI in A-rated, BBB-rated, and below investment-grade securities and underweight allocations to high-quality (AAA- and AA-rated) securities, contributing favorably to relative performance.

The allocation of holdings across municipal sectors had a net positive impact on relative performance. For example, overweight exposure to outperforming Hospital and Senior Care revenue bonds and underweight exposure to underperforming Local GO bonds contributed to favorable relative performance.

Security selection provided a positive contribution to relative performance as gross return was above that of the SPMUNI after accounting for duration, yield curve, credit quality and sector positioning.

TENDER OFFER FOR COMMON SHARES

The Fund completed a tender offer of 32% of its outstanding Common Shares in October 2024 at 99% of the net asset value per Common Share determined as of the close of the regular trading session of the New York Stock Exchange on October 11, 2024. The tender offer provided alternative liquidity to holders of the Fund’s Common Shares.

PREFERRED SHARES AND FUND LEVERAGE

At period end, the Fund maintained one source of leverage with $67.35 million of Variable Rate Municipal Term Preferred Shares (VMTPS) outstanding. As part of the portfolio adjustments in relation to the tender offer, the amount of outstanding VMTPS was reduced in order to allow the Fund to continue to operate as a leveraged closed-end fund and to remain in compliance with regulatory and contractual leverage restrictions. The dividend rate for VMTPS resets weekly at a fixed spread (as disclosed in the notes to the attached financial statements) above the SIFMA Municipal Swap Index.12

The monthly dividend for the Fund was increased during the reporting period in June 2024. The decline in leverage costs contributed to the Fund increasing its monthly dividend during the period. The Fund maintains undistributed net investment income that may rise or fall depending upon whether distributions to common shareholders are less or greater than the Fund’s current net income after expenses and financing costs. At November 30, 2024, the Fund’s undistributed net investment income as determined in accordance with U.S. Generally Accepted Accounting Principles was $0.077 per share, up from $0.009 per share at November 30, 2023.

Annual Shareholder Report

1

The Fund offers Common Shares and Preferred Shares. The Pricing, Yield, Dividends, Fund History, Total Return and Premium/Discount of Market Price

to Net Asset Value (NAV) information provided herein relates to Common Shares only. Unlike Preferred Shares, Common Shares are not rated.

2

Income may be subject to state and local taxes.

3

Please see the footnote to the line graph below for definitions of, and further information about, the SPMUNI.

4

The MCEMNL, a peer average, is being used for comparison purposes because, although the peer group is not the Fund’s broad-based securities

market index, the Fund’s investment adviser (the “Adviser”) believes it more closely reflects the market sectors in which the Fund invests. Morningstar figures represent the average of the total returns reported by all funds designated by Morningstar as falling into the respective category and is not adjusted to reflect any sales charges.

5

Duration is a measure of a security’s price sensitivity to changes in interest rates. Securities with longer durations are more sensitive to changes in

interest rates than securities with shorter durations. For purposes of this Management’s Discussion of Fund Performance, duration is determined using a

third-party analytical system.

6

Bond prices are sensitive to changes in interest rates, and a rise in interest rates can cause a decline in their prices.

7

Credit ratings pertain only to the securities in the portfolio and do not protect Fund shares against market risk.

8

Current yield is an annualized number, calculated by multiplying the Fund’s most recent monthly dividend per share by 12 and then dividing by the

9

Dividend Yield at Market Price is an annualized number, calculated by multiplying the Fund’s most recent monthly dividend per share by 12 and then

dividing by the month-end market price per share.

10 The BVAL AAA Municipal Curves are constructed using trades from the Municipal Securities Rulemaking Board (MSRB) and contributed data. Constituents eligible for the curve must have a rating of AAA, minimum maturity and issuance sizes of $2mm and $30mm, respectively, minimum trade size of $500K for MSRB Dealer trades and $1mm for all other MSRB trades and contributed quotes. All observations are normalized for differences in credit, optionality and coupon size.

11 Investment-grade securities are securities that are rated at least BBB or unrated securities of a comparable quality. Noninvestment-grade securities are securities that are not rated at least BBB or unrated securities of a comparable quality. Credit ratings are an indication of the risk that a security will default. They do not protect a security from credit risk. Lower-rated bonds typically offer higher yields to help compensate investors for the increased risk associated with them. Among these risks are lower creditworthiness, greater price volatility, more risk to principal and income than with higher-rated securities and increased possibilities of default.

12 The Securities Industry and Financial Markets Association Municipal Swap Index is a 7-day high-grade market index comprised of tax-exempt Variable Rate Demand Obligations (VRDOs) with certain characteristics. The index is calculated and published by Bloomberg. The index is overseen by SIFMA’s Municipal Swap Index Committee. The index is unmanaged, and it is not possible to invest directly in an index.

Annual Shareholder Report

PORTFOLIO OVERVIEW AS OF NOVEMBER 30, 2024 (unaudited)

| |

| |

| |

Taxable Equivalent Dividend Yield2 | |

| |

| |

| |

| |

Weighted Average Effective Maturity | |

Weighted Average Stated Maturity | |

Weighted Average Modified Duration3 | |

Total Number of Securities | |

Tax-Free Dividends Per Share Since Inception

February 2003–August 2005 | |

September 2005–October 2006 | |

November 2006–February 2009 | |

| |

| |

| |

December 2012–August 2014 | |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

Performance and composition information is updated monthly on FederatedHermes.com/us.

Past performance is no guarantee of future results. Investment return, price, yield and NAV will fluctuate.

Annual Shareholder Report

1

Dividend Yield on market share price is an annualized number, calculated by multiplying the Fund’s most recent monthly dividend per share by 12 and

then dividing by the month-end market price per share.

2

Taxable Equivalent Dividend Yield–In calculating this yield, the dividend yield is divided by one minus the applicable tax rate. The maximum federal tax

rate (37%) is used when calculating the taxable equivalent dividend yield. Federal tax rates are based on 2018 rates as stated in the Tax Cuts and Jobs

3

Duration is a measure of a security’s price sensitivity to changes in interest rates. Securities with longer durations are more sensitive to changes in

interest rates than securities of shorter durations.

4

The ratings agencies that provided the ratings are S&P Global Ratings, Moody’s Investors Service and Fitch Ratings. When ratings vary, the highest

rating is used. Credit ratings of A or better are considered high credit quality; credit ratings of BBB are good credit quality and the lowest category of

investment grade; credit ratings BB and below are lower-rated securities (“junk bonds”); and credit ratings of CCC or below have high default risk. The

credit quality breakdown does not give effect to the impact of any credit derivative investments made by a fund.

Annual Shareholder Report

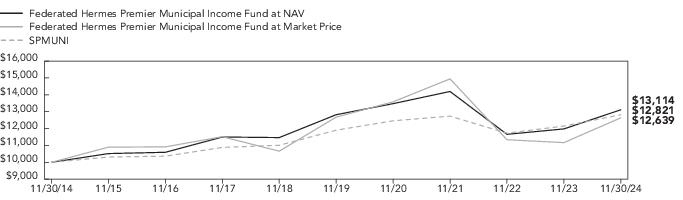

FUND PERFORMANCE AND GROWTH OF A $10,000 INVESTMENT

The graph below illustrates the hypothetical investment of $10,0001 in the Federated Hermes Premier Municipal Income Fund (the “Fund”) from November 30, 2014 to November 30, 2024, compared to the S&P Municipal Bond Index (SPMUNI).2 The Average Annual Total Returns table below shows returns for the Fund at NAV and at Market Price averaged over the stated periods.

Growth of a $10,000 Investment

Growth of $10,000 as of November 30, 2024

Average Annual Total Returns for the Period Ended 11/30/2024

Performance data quoted represents past performance which is no guarantee of future results. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Mutual fund performance changes over time and current performance may be lower or higher than what is stated. For current to the most recent month-end performance and returns, visit FederatedHermes.com/us or call 1-800-341-7400 and select option #4. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Mutual funds are not obligations of or guaranteed by any bank and are not federally insured.

1

Represents a hypothetical investment of $10,000 in the Fund. The Fund’s performance assumes the reinvestment of all dividends and distributions. The

SPMUNI has been adjusted to reflect reinvestment of dividends on securities in the index.

2

The SPMUNI is a broad, market value-weighted index that seeks to measure the performance of the U.S. municipal bond market. It tracks fixed-rate tax-

free bonds and bonds subject to the alternative minimum tax (AMT). The index includes bonds of all quality–from “AAA” to non-rated, excluding

defaulted bonds–from all sectors of the municipal bond market. The index is not adjusted to reflect sales charges, expenses and other fees that the

Securities and Exchange Commission requires to be reflected in the Fund’s performance. The index is unmanaged, and, unlike the Fund, is not affected

by cash flows. It is not possible to invest directly in an index.

Annual Shareholder Report

The Fund’s Investment Objectives, Principal Strategies and Principal Risks

The following information is a summary of certain disclosure changes since November 30, 2023. This information may not reflect all of the disclosure changes that have occurred since you purchased Common Shares of the Fund.

The Fund’s Annual Report disclosure regarding its principal strategies has been clarified to reflect that the Fund does not have a 10% limit on investments in inverse floaters in connection with its use of leverage.

The Fund’s investment objective is to provide current income exempt from federal income tax, including the alternative minimum tax (AMT).

The Fund seeks to achieve its investment objective by investing primarily in securities that, in the opinion of bond counsel to the issuer, or on the basis of another authority believed by the Adviser to be reliable, pay interest exempt from federal income tax, including AMT. The Adviser does not conduct its own analysis of the tax status of the interest paid by tax-exempt securities held by the Fund.

The Fund normally invests substantially all (at least 90%) of its total assets in tax-exempt securities, and normally invests at least 80% of its total assets in investment-grade tax-exempt securities. The Fund may invest up to 20% of its total assets in tax-exempt securities of below investment-grade quality (but not lower than B, including modifiers, sub-categories or gradations). The presence of a ratings modifier, sub-category, or gradation (for example, a (+) or (-)) is intended to show relative standing within the major rating categories and does not affect the security credit rating for purposes of the Fund’s investment parameters. Bonds of below investment-grade quality are commonly referred to as “junk bonds.”

The Adviser performs a fundamental credit analysis on tax-exempt securities that the Fund is contemplating purchasing before the Fund purchases such securities. The Adviser considers various factors, including the economic feasibility of revenue bond financings and general-purpose financings; the financial condition of the issuer or guarantor; and political developments that may affect credit quality. The Adviser monitors the credit risks of the tax-exempt securities held by the Fund on an ongoing basis by reviewing periodic financial data and credit ratings of nationally recognized statistical rating organizations (NRSROs).

The Fund maintains a dollar-weighted average stated portfolio maturity of ten to thirty years and a dollar-weighted average duration of thirteen years or less.

The Fund’s average effective portfolio maturity represents an average based on the actual stated maturity dates of the debt securities in the Fund, except that: (1) variable-rate securities are deemed to mature at the next interest-rate adjustment date, unless subject to a demand feature; (2) variable-rate securities subject to a demand feature are deemed to mature on the longer of the next interest-rate adjustment date or the date on which principal can be recovered through demand; (3) floating-rate securities subject to a demand feature are deemed to mature on the date on which the principal can be recovered through demand; and (4) securities being hedged with futures contracts may be deemed to have a longer maturity, in the case of purchases of futures contracts, and a shorter maturity, in the case of sales of futures contracts, than they would otherwise be deemed to have. The average portfolio maturity of the Fund is dollar-weighted based upon the market value of the Fund’s securities at the time of calculation. (A bond’s effective maturity takes into account the possibility that it may be called by the issuer before its stated maturity date. In this case, the bond trades as though it had a shorter maturity than its stated maturity.) The Fund’s average stated portfolio maturity is determined based on the actual stated maturity dates of the debt securities in the Fund’s portfolio whether or not a security is subject to redemption at the option of the issuer prior to the security’s stated maturity.

The Fund may use derivative contracts for risk management purposes. The Fund uses leverage to pursue its investment objective. The Fund currently utilizes leverage through the issuance of Preferred Shares. The Fund may enter into tender option bond (TOB) transactions and invest in derivative contracts, including inverse floating rate securities (inverse floaters). Inverse floaters are the residual interest in a TOB trust, which is a special purpose trust that holds one or more tax-exempt obligations. There can be no assurance that the Fund’s use of derivative contracts or hybrid instruments will work as intended. Derivative investments made by the Fund are included within the Fund’s 80% policy (as described below) and are calculated at market value. The Fund may also invest in exchange-traded funds to implement elements of its investment strategy, including for cash flow management, cost effectiveness, and gaining exposure to certain markets and securities in a quicker and/or more efficient manner.

Under normal circumstances, the Fund will invest its assets so that at least 80% of the income that it distributes will be exempt from federal regular income tax. This policy may not be changed without shareholder approval.

Annual Shareholder Report

Additional Information Regarding the Security Selection Process

As part of analysis in its security selection process, among other factors, the Adviser also evaluates whether environmental, social and governance factors could have positive or negative impact on the risk profiles of many issuers or guarantors in the universe of securities in which the Fund may invest. The Adviser may also consider information derived from active engagements conducted by its in-house stewardship team with certain issuers or guarantors on environmental, social and governance topics. This qualitative analysis does not automatically result in including or excluding specific securities but may be used by Federated Hermes as an additional input in its primary analysis.

Risks Related to Market Price, Discount and Net Asset Value of Shares

Shares of closed-end management investment companies frequently trade at a discount from their net asset value (NAV).

Prices of fixed-income securities (including tax-exempt securities) generally fall when interest rates rise. The longer the duration of a fixed-income security, the more susceptible it is to interest rate risk. Distributions on any inverse floaters paid to the Fund will be reduced or, in the extreme, eliminated as short-term interest rates rise and will increase when such interest rates fall. Inverse floaters generally respond with more volatility to interest rate changes than fixed rate, tax-exempt bonds of the same maturity. If interest rates exceed the interest paid on the underlying obligations, the TOB trust could be required to sell the obligations and distribute the proceeds to the certificate holders, which would cause the Fund to realize a loss on its investment. Recent and potential future changes in monetary policy made by central banks and/or their governments are likely to affect the level of interest rates.

It is possible that interest or principal on securities will not be paid when due. Noninvestment-grade securities generally have a higher default risk than investment-grade securities. Such non-payment or default may reduce the value of the Fund’s portfolio holdings, its share price and its performance.

The use of leverage through the issuance of Preferred Shares creates an opportunity for increased income that may be distributed as Common Share dividends, but also creates special risks for Common Shareholders. Two major types of risks created by leverage include: the likelihood of greater volatility of the NAV and market price of Common Shares, because changes in the value of the Fund’s tax-exempt security portfolio (including securities bought with the proceeds of the Preferred Shares offering) are borne entirely by Common Shareholders; and the possibility either that Common Share income will fall if the Preferred Share dividend rate rises, or that Common Share income will fluctuate because the Preferred Share dividend rate varies. Inverse floaters involve leverage risk which is substantially similar to the leverage risk associated with the Fund’s issuance of Preferred Shares. If short-term and long-term interest rates rise, the combination of the Fund’s investment in inverse floaters and its use of other forms of leverage (including the issuance of Preferred Shares) likely will adversely impact the Fund’s NAV per share and income, distributions and total returns to shareholders.

Risks Associated with Noninvestment-Grade Securities

Securities rated below investment grade may be subject to greater interest rate, credit and liquidity risks than investment-grade securities. These securities are considered speculative with respect to the issuer’s ability to pay interest and repay principal.

Tax-Exempt Securities Risks

The amount of public information available about tax-exempt securities is generally less than for corporate equities or bonds. The secondary market for tax-exempt securities also tends to be less well-developed and less liquid than many other securities markets, which may limit the Fund’s ability to sell its tax-exempt securities at attractive prices. Special factors, such as legislative changes, and state and local economic and business developments, may adversely affect the yield and/or value of the Fund’s investments in tax-exempt securities. Tax-exempt issuers can and have defaulted on obligations, been downgraded or commenced insolvency proceedings. Like other issuers and securities, the likelihood that the credit risk associated with such issuers and such securities will increase is greater during times of economic stress and financial instability.

Annual Shareholder Report

Derivative Contracts and Hybrid Instruments Risk

Derivative contracts, including inverse floaters, and hybrid instruments involve risks different from, or possibly greater than, risks associated with investing directly in securities and other traditional investments. Specific risk issues related to the use of such contracts and instruments include valuation and tax issues, increased potential for losses and/or costs to the Fund, and a potential reduction in gains to the Fund. Derivative contracts and hybrid instruments may also involve other risks, such as interest rate, credit, liquidity and leverage.

Income from the Fund’s tax-exempt security portfolio will decline if and when the Fund invests the proceeds from matured, traded or called tax-exempt securities at market interest rates that are below the portfolio’s current earnings rate. A decline in income could affect the market price or overall return of Common Shares.

In order to be tax-exempt, tax-exempt securities must meet certain legal requirements. Failure to meet such requirements may cause the interest received and distributed by the Fund to shareholders to be taxable. The federal income tax treatment of payments in respect of certain derivative contracts is unclear. Consequently, the Fund may receive payments, and make distributions, that are treated as ordinary income for federal income tax purposes.

The Fund may invest 25% or more of its total assets in tax-exempt securities of issuers in the same economic sector, such as hospitals or life care facilities and transportation-related issuers. In addition, a substantial part of the Fund’s portfolio may be comprised of securities credit enhanced by banks, insurance companies or companies with similar characteristics. As a result, the Fund will be more susceptible to any economic, business, political or other developments which generally affect these sectors and entities.

The Fund’s Agreement and Declaration of Trust includes provisions that could limit the ability of other entities or persons to acquire control of the Fund or convert the Fund to open-end status. These provisions could deprive Common Shareholders of opportunities to sell their Common Shares at a premium over the then current market price of Common Shares or at NAV. In addition, Preferred Shareholders will have voting rights that could deprive Common Shareholders of such opportunities.

Inflation risk is the risk that the value of assets or income from the Fund’s investments will be worth less in the future as inflation decreases the present value of payments at future dates.

The tax-exempt securities in which the Fund may invest can be principal investment strategies for the Fund and may be subject to call risk. Call risk is the possibility that an issuer may redeem a fixed-income security (including a tax-exempt security) before maturity (a “call”) at a price below or above its current market price. An increase in the likelihood of a call may reduce the security’s price. If a fixed-income security is called, the Fund may have to reinvest the proceeds in other fixed-income securities with lower interest rates, higher credit risks or other less favorable characteristics.

Risk Related to the Economy

The value of the Fund’s portfolio may decline in tandem with a drop in the overall value of the markets in which the Fund invests and/or other markets. Economic, political and financial conditions, industry or economic trends and developments or public health risks, such as epidemics or pandemics, may, from time to time, and for varying periods of time, cause the Fund to experience volatility, illiquidity or other potentially adverse effects. Among other investments, lower-grade bonds may be particularly sensitive to changes in the economy.

The securities in which the Fund invests may be subject to credit enhancement (for example, guarantees, letters of credit or bond insurance). If the credit quality of the credit enhancement provider (for example, a bank or bond issuer) is downgraded, the rating on a security credit enhanced by such credit enhancement provider also may be downgraded. Having multiple securities credit enhanced by the same enhancement provider will increase the adverse effects on the Fund that are likely to result from a downgrading of, or a default by, such an enhancement provider. Adverse developments in the banking or bond insurance industries also may negatively affect the Fund.

Annual Shareholder Report

Exchange-Traded Funds Risk

An investment in an exchange-traded fund (ETF) generally presents the same primary risks as an investment in a conventional fund (i.e., one that is not exchange-traded) that has the same investment objectives, strategies and policies. The price of an ETF can fluctuate up or down, and the Fund could lose money investing in an ETF if the prices of the securities owned by the ETF go down. In addition, ETFs may be subject to the following risks that do not apply to conventional funds: (i) the market price of an ETF’s shares may trade above or below their net asset value; (ii) an active trading market for an ETF’s shares may not develop or be maintained; or (iii) trading of an ETF’s shares may be halted if the listing exchange’s officials deem such action appropriate, the shares are delisted from the exchange or the activation of market-wide “circuit breakers” (which are tied to large decreases in stock prices) halts stock trading generally.

Certain securities in which the Fund invests may be less readily marketable and may be subject to greater fluctuation in price than other securities. These features may make it more difficult to sell or buy a security at a favorable price or time. Noninvestment-grade securities generally have less liquidity than investment-grade securities. Liquidity risk also refers to the possibility that the Fund may not be able to sell a security or close out a derivative contract when it wants to. Over-the-counter derivative contracts generally carry greater liquidity risk than exchange-traded contracts.

A party to a transaction involving the Fund may fail to meet its obligations. This could cause the Fund to lose money or to lose the benefit of the transaction or prevent the Fund from selling or buying other securities to implement its investment strategies.

The Adviser uses various technologies in managing the Fund, consistent with its investment objective and strategy. For example, proprietary and third-party data and systems are utilized to support decision making for the Fund. Data imprecision, software or other technology malfunctions, programming inaccuracies and similar circumstances may impair the performance of these systems, which may negatively affect Fund performance.

Annual Shareholder Report

Portfolio of Investments Summary Table (unaudited)

At November 30, 2024, the Fund’s sector composition1 was as follows:

| Percentage of

Total Investments |

| |

| |

| |

| |

| |

| |

| |

General Obligation—State Appropriation | |

Primary/Secondary Education | |

| |

Industrial Development Bond/Pollution Control Revenue | |

| |

| |

| Sector classifications, and the assignment of holdings to such sectors, are based upon the economic sector and/or revenue source of the underlying borrower, as determined by the Fund’s Adviser. For securities that have been enhanced by a third-party guarantor, such as bond insurers and banks, sector classifications are based upon the economic sector and/or revenue source of the underlying obligor, as determined by the Fund’s Adviser. Refunded securities are those whose debt service is paid from escrowed assets, usually U.S. government securities. |

| For purposes of this table, sector classifications constitute 85.4% of the Fund’s investments. Remaining sectors have been aggregated under the designation “Other.” |

Annual Shareholder Report

Portfolio of Investments

| | | |

| | | |

| | | |

| | Alabama State Corrections Institution Finance Authority (Alabama State), Revenue Bonds (Series 2022A), 5.250%, 7/1/2052 | |

| | Jefferson County, AL (Jefferson County, AL Sewer System), Sewer Revenue Warrants (Series 2024), 5.250%, 10/1/2049 | |

| | Lower Alabama Gas District, Gas Project Revenue Bonds (Series 2016A), (Goldman Sachs Group, Inc. GTD), 5.000%, 9/1/2046 | |

| | | |

| | | |

| | Maricopa County, AZ, IDA (Paradise Schools), Revenue Refunding Bonds, 5.000%, 7/1/2036 | |

| | Phoenix, AZ Civic Improvement Corp. - Wastewater System, Junior Lien Wastewater System Revenue Bonds (Series 2023), 5.250%, 7/1/2047 | |

| | Phoenix, AZ IDA (GreatHearts Academies), Education Facility Revenue Bonds (Series 2014A), 5.000%, 7/1/2034 | |

| | Pima County, AZ IDA (La Posada at Pusch Ridge), Senior Living Revenue Bonds (Series 2022A), 6.750%, 11/15/2042 | |

| | | |

| | | |

| | California Public Finance Authority (Kendal at Sonoma), Enso Village Senior Living Revenue Refunding Bonds (Series 2021A), 5.000%, 11/15/2056 | |

| | California School Finance Authority (KIPP LA), School Facility Revenue Bonds (Series 2014A), 5.000%, 7/1/2034 | |

| | California School Finance Authority (KIPP LA), School Facility Revenue Bonds (Series 2014A), 5.125%, 7/1/2044 | |

| | California School Finance Authority (KIPP LA), School Facility Revenue Bonds (Series 2015A), 5.000%, 7/1/2035 | |

| | M-S-R Energy Authority, CA, Gas Revenue Bonds (Series 2009A), (Citigroup, Inc. GTD), 7.000%, 11/1/2034 | |

| | M-S-R Energy Authority, CA, Gas Revenue Bonds (Series 2009A), (Original Issue Yield: 6.375%), (Citigroup, Inc. GTD), 6.125%, 11/1/2029 | |

| | San Francisco, CA City & County Airport Commission, Second Series Revenue Bonds (Series 2019F), 5.000%, 5/1/2050 | |

| | | |

| | | |

| | Colorado Educational & Cultural Facilities Authority (University Lab School), Charter School Refunding & Improvement Revenue Bonds (Series 2015), 5.000%, 12/15/2035 | |

| | Colorado Health Facilities Authority (Adventist Health System), Hospital Revenue Bonds (Series 2018B), 4.000%, 11/15/2048 | |

| | Colorado Health Facilities Authority (CommonSpirit Health), Revenue Bonds (Series 2022), 5.500%, 11/1/2047 | |

| | Colorado High Performance Transportation Enterprise, C-470 Express Lanes Senior Revenue Bonds (Series 2017), 5.000%, 12/31/2056 | |

| | Colorado State Health Facilities Authority (Intermountain Healthcare Obligated Group), Revenue Bonds (Series 2024A), 5.000%, 5/15/2054 | |

| | Public Authority for Colorado Energy, Natural Gas Purchase Revenue Bonds (Series 2008), (Original Issue Yield: 6.630%), (Bank of America Corp. GTD), 6.250%, 11/15/2028 | |

| | | |

| | District of Columbia—0.3% | |

| | District of Columbia (Friendship Public Charter School, Inc.), Revenue Bonds (Series 2016A), 5.000%, 6/1/2041 | |

| | | |

| | Atlantic Beach, FL Health Care Facilities (Fleet Landing Project, FL), Revenue & Refunding Bonds (Series 2013A), 5.000%, 11/15/2028 | |

| | Collier County, FL IDA (Arlington of Naples), Continuing Care Community Revenue Bonds (Series 2013A), (Original Issue Yield: 8.250%), 8.125%, 5/15/2044 | |

| | Florida Development Finance Corp. (Tampa General Hospital), Healthcare Facilities Revenue Bonds (Series 2024A), 5.250%, 8/1/2049 | |

| | Hillsborough County, FL IDA (Baycare Health System), Health System Revenue Bonds (Series 2024C), (Original Issue Yield: 4.320%), 4.125%, 11/15/2051 | |

| | Lakewood Ranch Stewardship District, FL (Taylor Ranch), Special Assessment Revenue Bonds (Series 2023), 6.125%, 5/1/2043 | |

| | Miami-Dade County, FL (Miami-Dade County, FL Transit System), Sales Surtax Revenue Bonds (Series 2020A), 4.000%, 7/1/2050 | |

| | Midtown Miami, FL CDD, Special Assessment & Revenue Refunding Bonds (Series 2014A), 5.000%, 5/1/2029 | |

| | Rivers Edge II CDD, Capital Improvement Revenue Bonds (Series 2021), 4.000%, 5/1/2051 | |

| | | |

Annual Shareholder Report

| | | |

| | MUNICIPAL BONDS—continued | |

| | | |

| | Atlanta, GA Development Authority (Westside Gulch Area Project (Spring Street Atlanta)), Senior Revenue Bonds (Series 2024A-1), 5.000%, 4/1/2034 | |

| | Fulton County, GA Residential Care Facilities (Lenbrook Square Foundation, Inc.), Retirement Facility Refunding Revenue Bonds (Series 2016), 5.000%, 7/1/2036 | |

| | Geo. L. Smith II Georgia World Congress Center Authority, Convention Center Hotel Second Tier Revenue Bonds (Series 2021B), 5.000%, 1/1/2054 | |

| | Main Street Natural Gas, Inc., GA, Gas Supply Revenue Bonds (Series 2023C), (Royal Bank of Canada GTD), 5.000%, Mandatory Tender 9/1/2030 | |

| | Municipal Electric Authority of Georgia, Plant Vogtle Units 3&4 Project J Revenue Refunding Bonds (Series 2015A), 5.500%, 7/1/2060 | |

| | Municipal Electric Authority of Georgia, Plant Vogtle Units 3&4 Project M Bonds (Series 2021A), 5.000%, 1/1/2056 | |

| | Municipal Electric Authority of Georgia, Plant Vogtle Units 3&4 Project P Revenue Refunding Bonds (Series 2023A), 5.500%, 7/1/2064 | |

| | | |

| | | |

| | Chicago, IL Board of Education, Dedicated Capital Improvement Tax Bonds (Series 2023), 5.750%, 4/1/2048 | |

| | Chicago, IL Wastewater Transmission, Second Lien Wastewater Transmission Revenue Bonds (Series 2023A), (Assured Guaranty, Inc. INS), 5.250%, 1/1/2053 | |

| | Chicago, IL Water Revenue, Second Lien Water Revenue Bonds (Series 2023A), (Assured Guaranty, Inc. INS), 5.250%, 11/1/2053 | |

| | DuPage County, IL (Naperville Campus LLC), Special Tax Bonds (Series 2006), 5.625%, 3/1/2036 | |

| | Illinois Finance Authority (Admiral at the Lake), Revenue Refunding Bonds (Series 2017), (Original Issue Yield: 5.500%), 5.250%, 5/15/2054 | |

| | Illinois State, UT GO Bonds (Series 2020B), (Original Issue Yield: 5.850%), 5.750%, 5/1/2045 | |

| | Illinois State, UT GO Bonds (Series 2022C), 5.125%, 10/1/2043 | |

| | Illinois State, UT GO Bonds (Series 2022C), 5.500%, 10/1/2045 | |

| | Illinois State, UT GO Bonds (Series of May 2014), (United States Treasury PRF 1/14/2025@100), 5.000%, 5/1/2039 | |

| | Illinois State, UT GO Refunding Bonds (Series 2018A), 5.000%, 10/1/2026 | |

| | Metropolitan Pier & Exposition Authority, IL, McCormick Place Expansion Project Bonds (Series 2015A), (Original Issue Yield: 5.060%), 5.000%, 6/15/2053 | |

| | Sales Tax Securitization Corp., IL, Sales Tax Securitization Bonds (Series 2018A), 5.000%, 1/1/2048 | |

| | Sales Tax Securitization Corp., IL, Sales Tax Securitization Bonds (Series 2022A), 4.000%, 1/1/2042 | |

| | | |

| | | |

| | Indiana Municipal Power Agency, Power Supply System Revenue Bonds (Series 2013A), 5.250%, 1/1/2038 | |

| | Indiana State Finance Authority (CWA Authority, Inc.), First Lien Wastewater Utility Revenue Bonds (Series 2022B), 5.250%, 10/1/2052 | |

| | Indianapolis, IN Local Public Improvement Bond Bank (Indiana Convention Center Hotel), Senior Revenue Bonds (Series 2023E), (Original Issue Yield: 5.880%), 5.750%, 3/1/2043 | |

| | | |

| | | |

| | Iowa Finance Authority (Iowa Fertilizer Co. LLC), Midwestern Disaster Area Revenue Refunding Bonds (Series 2022), (United States Treasury PRF 12/1/2032@100), 5.000%, 12/1/2050 | |

| | Iowa Finance Authority (Iowa Fertilizer Co. LLC), Midwestern Disaster Area Revenue Refunding Bonds (Series 2022), (United States Treasury PRF 12/1/2032@100), 5.000%, Mandatory Tender 12/1/2042 | |

| | | |

| | | |

| | Wyandotte County, KS Unified Government Utility System, Improvement & Refunding Revenue Bonds (Series 2014-A), 5.000%, 9/1/2044 | |

| | | |

| | Kentucky Economic Development Finance Authority (Miralea), Revenue Bonds (Series 2016A), 5.000%, 5/15/2031 | |

| | | |

| | Louisiana Stadium and Exposition District, Senior Revenue Bonds (Series 2023A), 5.000%, 7/1/2048 | |

| | St. James Parish, LA (NuStar Logistics LP), Revenue Bonds (Series 2011), 5.850%, Mandatory Tender 6/1/2025 | |

| | | |

Annual Shareholder Report

| | | |

| | MUNICIPAL BONDS—continued | |

| | | |

| | Baltimore, MD (East Baltimore Research Park), Special Obligation Revenue Refunding Bonds (Series 2017A), 5.000%, 9/1/2038 | |

| | Westminster, MD (Lutheran Village at Miller’s Grant, Inc.), Revenue Bonds (Series 2014A), 6.000%, 7/1/2034 | |

| | | |

| | | |

| | Commonwealth of Massachusetts, UT GO Consolidated Loan Bonds (Series 2023C), 5.000%, 8/1/2044 | |

| | | |

| | Detroit, MI, UT GO Bonds (Series 2020), 5.500%, 4/1/2045 | |

| | Michigan State Building Authority, Revenue Refunding Bonds Facilities Program (Series 2023-II), 4.000%, 10/15/2047 | |

| | Michigan State Finance Authority (Detroit, MI Public Lighting Authority), Local Government Loan Program Revenue Bonds (Series 2014B), 5.000%, 7/1/2039 | |

| | Michigan State Finance Authority (McLaren Health Care Corp.), Revenue Bonds (Series 2019A), 4.000%, 2/15/2044 | |

| | Michigan State Finance Authority (Provident Group - HFH Energy LLC), Act 38 Facilities Senior Revenue Bonds (Series 2024), 5.500%, 2/28/2049 | |

| | Michigan State Finance Authority (Trinity Healthcare Credit Group), (Series MI 2019A), 4.000%, 12/1/2049 | |

| | | |

| | | |

| | Kansas City, MO Redevelopment Authority (Kansas City Convention Center Headquarters Hotel CID), Revenue Bonds (Series 2018B), (Original Issue Yield: 5.079%), 5.000%, 2/1/2050 | |

| | Kansas City, MO Redevelopment Authority (Kansas City Convention Center Headquarters Hotel CID), Revenue Bonds (Series 2018B), 5.000%, 2/1/2040 | |

| | | |

| | | |

| | Kalispell, MT Housing and Healthcare Facilities (Immanuel Lutheran Corp.), Revenue Bonds (Series 2017A), 5.250%, 5/15/2047 | |

| | | |

| | Nevada State, LT GO Bonds (Series 2023A), 5.000%, 5/1/2042 | |

| | | |

| | National Finance Authority, NH (Attwater Project Texas MUD No. 38), Special Revenue Capital Appreciation Bonds (Series 2024), (Original Issue Yield: 6.250%), 0.000%, 4/1/2032 | |

| | National Finance Authority, NH, Municipal Certificates (Series 2024-1 Class A), (Original Issue Yield: 4.510%), 4.250%, 7/20/2041 | |

| | | |

| | | |

| | New Jersey EDA (New Jersey State), North Portal Bridge Project (Series 2022), 5.250%, 11/1/2041 | |

| | New Jersey EDA (New Jersey State), North Portal Bridge Project (Series 2022), 5.250%, 11/1/2047 | |

| | New Jersey Educational Facilities Authority (New Jersey State), Higher Education Capital Improvement Fund (Series 2023A), 4.625%, 9/1/2048 | |

| | New Jersey State Transportation Trust Fund Authority (New Jersey State), Transportation Program Bonds (Series 2023BB), 5.000%, 6/15/2046 | |

| | New Jersey State Transportation Trust Fund Authority (New Jersey State), Transportation System Bonds (Series 2018A), 5.000%, 12/15/2034 | |

| | New Jersey State Transportation Trust Fund Authority (New Jersey State), Transportation System Bonds (Series 2022CC), 5.500%, (United States Treasury PRF 12/15/2032@100), 6/15/2050 | |

| | Tobacco Settlement Financing Corp., NJ, Tobacco Settlement Asset-Backed Senior Refunding Bonds (Series 2018A), 5.000%, 6/1/2035 | |

| | | |

| | | |

| | Build NYC Resource Corporation (KIPP NYC Canal West), Revenue Bonds (Series 2022), 5.250%, 7/1/2057 | |

| | Metropolitan Transportation Authority, NY (MTA Transportation Revenue), Transportation Revenue Green Bonds (Series 2020C-1), 5.250%, 11/15/2055 | |

| | New York City Housing Development Corp., Multifamily Housing Revenue Bonds (Series 2024B-1), 4.750%, 11/1/2054 | |

| | New York City, NY Municipal Water Finance Authority, Water and Sewer System Second General Resolution Revenue Bonds (Series 2023-DD), (Original Issue Yield: 4.380%), 4.125%, 6/15/2047 | |

| | New York City, NY Municipal Water Finance Authority, Water and Sewer System Second General Resolution Revenue Bonds (Series 2024CC-1), 5.250%, 6/15/2054 | |

| | New York City, NY Transitional Finance Authority, Future Tax Secured Subordinate Bonds (Series 2015E-1), 5.000%, 2/1/2041 | |

Annual Shareholder Report

| | | |

| | MUNICIPAL BONDS—continued | |

| | | |

| | New York City, NY Transitional Finance Authority, Future Tax Secured Subordinate Bonds (Series 2023F-1), (Original Issue Yield: 4.450%), 4.000%, 2/1/2051 | |

| | New York Liberty Development Corporation (3 World Trade Center), Revenue Bonds (Series 2014 Class 1), 5.000%, 11/15/2044 | |

| | New York State Thruway Authority (New York State Thruway Authority - General Revenue), General Revenue Junior Indebtedness Obligations (Series 2016A), 5.000%, 1/1/2046 | |

| | New York Transportation Development Corporation (JFK International Air Terminal LLC), Special Facilities Revenue Bonds (Series 2020C), 4.000%, 12/1/2040 | |

| | Suffolk County, NY Off-Track Betting Corp., Revenue Bonds (Series 2024), (Original Issue Yield: 5.076%), 5.000%, 12/1/2034 | |

| | Suffolk County, NY Off-Track Betting Corp., Revenue Bonds (Series 2024), (Original Issue Yield: 5.865%), 5.750%, 12/1/2044 | |

| | | |

| | | |

| | Charlotte, NC (Charlotte, NC Douglas International Airport), Airport Revenue Bonds (Series 2017A), 5.000%, 7/1/2047 | |

| | North Carolina Medical Care Commission (United Methodist Retirement Homes), Retirement Facilities First Mortgage Revenue Bonds (Series 2024), 5.125%, 10/1/2054 | |

| | | |

| | | |

| | Cuyahoga County, OH Hospital Authority (MetroHealth System), Hospital Revenue Bonds (Series 2017), (Original Issue Yield: 5.030%), 5.000%, 2/15/2057 | |

| | Cuyahoga County, OH Hospital Authority (MetroHealth System), Hospital Revenue Bonds (Series 2017), 5.250%, 2/15/2047 | |

| | Miami County, OH Hospital Facility (Kettering Health Network Obligated Group), Hospital Facilities Revenue Refunding and Improvement Bonds (Series 2019), 5.000%, 8/1/2049 | |

| | Muskingum County, OH (Genesis Healthcare Corp.), Hospital Facilities Revenue Bonds (Series 2013), 5.000%, 2/15/2027 | |

| | | |

| | | |

| | Oregon State Housing and Community Services Department, Single Family Mortgage Program (Series 2023A), 4.600%, 7/1/2043 | |

| | | |

| | Allegheny County, PA Hospital Development Authority (Allegheny Health Network Obligated Group), Revenue Bonds (Series 2018A), 5.000%, 4/1/2047 | |

| | Cumberland County, PA Municipal Authority (Diakon Lutheran Social Ministries), Revenue Bonds (Series 2015), (United States Treasury PRF 1/1/2025@100), 5.000%, 1/1/2038 | |

| | Cumberland County, PA Municipal Authority (Diakon Lutheran Social Ministries), Revenue Bonds (Series 2015), (United States Treasury PRF 1/1/2025@100), 5.000%, 1/1/2038 | |

| | Cumberland County, PA Municipal Authority (Diakon Lutheran Social Ministries), Revenue Bonds (Series 2015), 5.000%, 1/1/2038 | |

| | Lehigh County, PA General Purpose Authority (Lehigh Valley Academy Regional Charter School), Charter School Revenue Bonds (Series 2022), 4.000%, 6/1/2057 | |

| | Northampton County, PA General Purpose Authority (Lafayette College), College Refunding and Revenue Bonds (Series 2017), 5.000%, 11/1/2047 | |

| | Northampton County, PA General Purpose Authority (St. Luke’s University Health Network), Hospital Revenue Bonds (Series 2016A), 4.000%, 8/15/2040 | |

| | Pennsylvania State Economic Development Financing Authority (UPMC Health System), Revenue Bonds (Series 2023A-2), 4.000%, 5/15/2053 | |

| | Pennsylvania State Turnpike Commission, Subordinate Revenue Bonds (Series 2019A), 5.000%, 12/1/2044 | |

| | Pennsylvania State Turnpike Commission, Turnpike Revenue Bonds (Series 2022B), 5.250%, 12/1/2052 | |

| | Philadelphia, PA Airport System, Airport Revenue and Refunding Bonds (Series 2017A), 5.000%, 7/1/2047 | |

| | Philadelphia, PA Water & Wastewater System, Water and Wastewater Revenue Bonds (Series 2020A), 5.000%, 11/1/2045 | |

| | Westmoreland County, PA Municipal Authority, Municipal Service Revenue Bonds (Series 2016), (Build America Mutual Assurance INS), 5.000%, 8/15/2042 | |

| | | |

| | | |

| | Commonwealth of Puerto Rico, UT GO Restructured Bonds (Series 2022A), 4.000%, 7/1/2041 | |

| | Puerto Rico Sales Tax Financing Corp., Restructured Sales Tax Bonds (Series 2019A), (Original Issue Yield: 5.154%), 5.000%, 7/1/2058 | |

| | Puerto Rico Sales Tax Financing Corp., Restructured Sales Tax Bonds (Series 2019A-2), 4.329%, 7/1/2040 | |

| | | |

Annual Shareholder Report

| | | |

| | MUNICIPAL BONDS—continued | |

| | | |

| | South Carolina Jobs-EDA (Novant Health, Inc.), Health Care Facilities Revenue Bonds (Series 2024A), 5.500%, 11/1/2054 | |

| | South Carolina Jobs-EDA (Prisma Health Obligated Group), Hospital Revenue Bonds (Series 2018A), 5.000%, 5/1/2048 | |

| | South Carolina Jobs-EDA (Seafields at Kiawah Island), Retirement Community Revenue Bonds TEMPS-50 (Series 2023B-2), 5.250%, 11/15/2028 | |

| | South Carolina Jobs-EDA (Seafields at Kiawah Island), Retirement Community Revenue Bonds TEMPS-75 (Series 2023B-1), 5.750%, 11/15/2029 | |

| | | |

| | | |

| | Chattanooga, TN Health, Educational & Housing Facility Board (CommonSpirit Health), Revenue Bonds (Series 2019A), 5.000%, 8/1/2049 | |

| | Metropolitan Nashville Tennessee Airport Authority, Airport Revenue Bonds (Series 2022A), 5.000%, 7/1/2052 | |

| | | |

| | | |

| | Austin, TX, Water and Wastewater System Revenue Refunding Bonds (Series 2022), 5.000%, 11/15/2052 | |

| | Harris County, TX IDC (Energy Transfer LP), Marine Terminal Refunding Revenue Bonds (Series 2023), 4.050%, Mandatory Tender 6/1/2033 | |

| | Houston, TX, Public Improvement and Refunding Bonds (Series 2024A), (Original Issue Yield: 4.380%), 4.125%, 3/1/2051 | |

| | North Texas Tollway Authority, First Tier Revenue Refunding Bonds (Series 2017A), 5.000%, 1/1/2048 | |

| | Richardson, TX ISD, UT GO School Building Bonds (Series 2024), (Original Issue Yield: 4.160%), (Texas Permanent School Fund Guarantee Program GTD), 4.000%, 2/15/2049 | |

| | San Antonio, TX Electric & Gas System, Revenue Bonds (Series 2024A), 5.250%, 2/1/2049 | |

| | San Antonio, TX Electric & Gas System, Revenue Refunding Bonds (Series 2017), 5.000%, 2/1/2047 | |

| | Texas Municipal Gas Acquisition & Supply Corp. IV, Gas Supply Revenue Bonds (Series 2023B), (BP PLC GTD), 5.500%, Mandatory Tender 1/1/2034 | |

| | Texas State Transportation Commission (State Highway 249 System), First Tier Toll Revenue Bonds (Series 2019A), 5.000%, 8/1/2057 | |

| | | |

| | | |

| | Utah State Board of Higher Education (University of Utah), General Revenue Bonds (Series 2022A), 4.000%, 8/1/2051 | |

| | | |

| | Chesapeake Bay Bridge & Tunnel District, VA, First Tier General Resolution Revenue Bonds (Series 2016), 5.000%, 7/1/2046 | |

| | James City County, VA EDA (Williamsburg Landing), Residential Care Facility Revenue Bonds (Series 2024A), 6.875%, 12/1/2058 | |

| | Virginia Beach, VA Development Authority (Westminster-Canterbury on Chesapeake Bay), Residential Care Facility Revenue Bonds (Series 2023A), 7.000%, 9/1/2053 | |

| | | |

| | | |

| | Washington State Health Care Facilities Authority (CommonSpirit Health), Revenue Refunding Bonds (Series 2019A-1), 4.000%, 8/1/2044 | |

| | Washington State Housing Finance Commission (Heron’s Key Senior Living), Nonprofit Housing Revenue Bonds (Series 2015A), (United States Treasury COL), 6.000%, 7/1/2025 | |

| | Washington State Housing Finance Commission (Presbyterian Retirement Communities Northwest), Revenue Bonds (Series 2016), 5.000%, 1/1/2031 | |

| | Washington State Housing Finance Commission (Presbyterian Retirement Communities Northwest), Revenue Bonds (Series 2016), 5.000%, 1/1/2051 | |

| | Washington State Housing Finance Commission (Rockwood Retirement Communities), Nonprofit Housing Revenue & Refunding Revenue Bonds (Series 2020A), 5.000%, 1/1/2041 | |

| | | |

| | | |

| | West Virginia State Hospital Finance Authority (Vandalia Health), Hospital Refunding and Improvement Revenue Bonds (Series 2023B), 6.000%, 9/1/2048 | |

| | | |

| | Public Finance Authority, WI (LVHN CHP JV, LLC), Revenue Bonds (Series 2022A), 7.250%, 12/1/2042 | |

| | Public Finance Authority, WI Revenue (Aurora Integrated Oncology Foundation), Revenue Bonds (Series 2023), 9.000%, 11/1/2028 | |

Annual Shareholder Report

| | | |

| | MUNICIPAL BONDS—continued | |

| | | |

| | Wisconsin Health & Educational Facilities Authority (Ascension Health Alliance Senior Credit Group), Revenue Bonds (Series 2016A), 4.000%, 11/15/2046 | |

| | | |

| | TOTAL MUNICIPAL BONDS

(IDENTIFIED COST $155,385,785) | |

| | SHORT-TERM MUNICIPALS—4.5% | |

| | | |

| | Charlotte-Mecklenburg Hospital Authority, NC (Atrium Health (previously Carolinas HealthCare) System), (Series 2018H) Daily VRDNs, (JPMorgan Chase Bank, N.A. LIQ), 3.200%, 12/2/2024 | |

| | | |

| | Ohio State Higher Educational Facility Commission (Cleveland Clinic), (Series 2008 B-4) Daily VRDNs, (Barclays Bank plc LIQ), 3.100%, 12/2/2024 | |

| | Ohio State Higher Educational Facility Commission (Cleveland Clinic), (Series 2013B-2) Daily VRDNs, (TD Bank, N.A. LIQ), 3.150%, 12/2/2024 | |

| | | |

| | | |

| | Delaware County, PA IDA (United Parcel Service, Inc.), (Series 2015) Daily VRDNs, (United Parcel Service, Inc. GTD), 3.200%, 12/2/2024 | |

| | | |

| | Shelby County, TN Health Education & Housing Facilities Board (Methodist Le Bonheur Healthcare), (Series 2008A) Daily VRDNs, (Assured Guaranty, Inc. INS)/(JPMorgan Chase Bank, N.A. LIQ), 3.250%, 12/2/2024 | |

| | TOTAL SHORT-TERM MUNICIPALS

(IDENTIFIED COST $7,450,000) | |

| | TOTAL INVESTMENT IN SECURITIES—100%

(IDENTIFIED COST $162,835,785)5 | |

| | OTHER ASSETS AND LIABILITIES - NET6 | |

| | LIQUIDATION VALUE OF VARIABLE RATE MUNICIPAL TERM PREFERRED SHARES (VMTPS) | |

| | TOTAL NET ASSETS APPLICABLE TO COMMON SHAREHOLDERS | |

At November 30, 2024, the Fund held no securities that are subject to the federal alternative minimum tax (AMT) (Unaudited).

| Denotes a restricted security that either: (a) cannot be offered for public sale without first being registered, or availing of an exemption from registration, under the Securities Act of 1933; or (b) is subject to a contractual restriction on public sales. At November 30, 2024, these restricted securities amounted to $11,528,425, which represented 11.3% of total net assets. |

| Non-income-producing security. |

| |

| Current rate and current maturity or next reset date shown for floating rate notes and variable rate notes/demand instruments. Certain variable rate securities are not based on a published reference rate and spread but are determined by the issuer or agent and are based on current market conditions. These securities do not indicate a reference rate and spread in their description above. |

| The cost of investments for federal tax purposes amounts to $162,728,692. |

| Assets, other than investments in securities, less liabilities. See Statement of Assets and Liabilities. |

Note: The categories of investments are shown as a percentage of total market value at November 30, 2024.

Various inputs are used in determining the value of the Fund’s investments. These inputs are summarized in the three broad levels listed below:

Level 1—quoted prices in active markets for identical securities.

Level 2—other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.). Also includes securities valued at amortized cost.

Level 3—significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of investments).

The inputs or methodology used for valuing securities are not an indication of the risk associated with investing in those securities.

Annual Shareholder Report

As of November 30, 2024, all investments of the Fund utilized Level 2 inputs in valuing the Fund’s assets carried at fair value.

The following acronym(s) are used throughout this portfolio: | |

| —Community Development District |

| |

| —Economic Development Authority |

| |

| |

| —Industrial Development Authority |

| —Industrial Development Corporation |

| |

| —Independent School District |

| |

| |

| |

| |

| —Tax Exempt Mandatory Paydown Securities |

| |

| —Variable Rate Demand Notes |

See Notes which are an integral part of the Financial Statements

Annual Shareholder Report

Financial Highlights

(For a Common Share Outstanding Throughout Each Period)

| |

| | | | | |

Net Asset Value, Beginning of Period | | | | | |

Income From Investment Operations: | | | | | |

| | | | | |

Net realized and unrealized gain (loss) | | | | | |

Distributions to auction market preferred shareholders from net investment income2 | | | | | |

Total from Investment Operations | | | | | |

Less Distributions to Common Shareholders: | | | | | |

Distributions from net investment income | | | | | |

Increase From Common Share Tender and Repurchase | | | | | |

Net Asset Value, End of Period | | | | | |

Market Price, End of Period | | | | | |

Total Return at Net Asset Value4 | | | | | |

Total Return at Market Price5 | | | | | |

Ratios to Average Net Assets: | | | | | |

| | | | | |

Net expenses excluding all interest and trust expenses7 | | | | | |

| | | | | |

Expense waiver/reimbursement10 | | | | | |

| | | | | |

Net assets, end of period (000 omitted) | | | | | |

| | | | | |

Annual Shareholder Report

Asset Coverage Requirements for Investment Company Act of 1940—Preferred Shares

| | | Minimum

Required

Asset

Coverage

Per Share | Involuntary

Liquidating

Preference

Per Share | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| Per share numbers have been calculated using the average shares method. |

| The amounts shown are based on Common Share equivalents. |

| Represents less than $0.01. |

| Total Return at Net Asset Value is the combination of changes in the Common Share net asset value, reinvested dividend income and reinvested capital gains distributions at net asset value, if any, and does not reflect the sales charge, if applicable. |

| Total Return at Market Price is the combination of changes in the market price per share and the effect of reinvested dividend income and reinvested capital gains distributions, if any, at the average price paid per share at the time of the reinvestment. |

| Amount does not reflect net expenses incurred by investment companies in which the Fund may invest. |

| Ratios do not reflect the effect of interest expense on variable rate municipal term preferred shares, dividend payments to preferred shareholders and any associated commission costs, or interest and trust expenses on tender option bond trusts. |

| The net expense ratio is calculated without reduction for expense offset arrangements. The net expense ratio is 0.99% for the years ended November 30, 2024, 2023, and 2020, after taking into account these expense reductions. |

| Ratios reflect reductions for dividend payments to preferred shareholders. |

| This expense decrease is reflected in both the net expense and the net investment income ratios shown above. Amount does not reflect expense waiver/ reimbursement recorded by investment companies in which the Fund may invest. |

| Securities that mature are considered sales for purposes of this calculation. |

| Represents initial public offering price. |

See Notes which are an integral part of the Financial Statements

Annual Shareholder Report

Statement of Assets and LiabilitiesNovember 30, 2024

| |

Investment in securities, at value (identified cost $162,835,785) | |

| |

| |

| |

| |

Payable for investments purchased | |

Income distribution payable - Common Shares | |

| |

Payable for portfolio accounting fees | |

Payable for auditing fees | |

Payable for investment adviser fee (Note 5) | |

Payable for administrative fee (Note 5) | |

Payable for Directors’/Trustees’ fees (Note 5) | |

Accrued expenses (Note 4) | |

TOTAL ACCRUED LIABILITIES | |

| |

Variable Rate Municipal Term Preferred Shares (VMTPS) (1,347 shares authorized and issued at $50,000 per share) | |

| |

Net assets applicable to Common Shares | |

Net Assets Applicable to Common Shares Consists of: | |

| |

Total distributable earnings (loss) | |

TOTAL NET ASSETS APPLICABLE TO COMMON SHARES | |

Net Asset Value, Offering Price and Redemption Proceeds Per Share: | |

$100,851,564 ÷ 7,818,701 shares outstanding, ($0.01 par value, unlimited shares authorized) | |

See Notes which are an integral part of the Financial Statements

Annual Shareholder Report

Statement of OperationsYear Ended November 30, 2024

| |

| |

| |

Investment adviser fee (Note 5) | |

Administrative fee (Note 5) | |

| |

| |

Directors’/Trustees’ fees (Note 5) | |

| |

| |

Portfolio accounting fees | |

| |

Interest expense - VMTPS (Note 7) | |

| |

| |

| |

Waiver of investment adviser fee (Note 5) | |

Reduction of custodian fees (Note 6) | |

TOTAL WAIVER AND REDUCTION | |

| |

| |

Realized and Unrealized Gain (Loss) on Investments and Futures Contracts: | |

Net realized loss on investments | |

Net realized gain on futures contracts | |

Net change in unrealized depreciation of investments | |

Net change in unrealized appreciation of futures contracts | |

Net realized and unrealized gain (loss) on investments and futures contracts | |

Change in net assets resulting from operations applicable to Common Shares | |

See Notes which are an integral part of the Financial Statements

Annual Shareholder Report

Statement of Changes in Net Assets

| | |

Increase (Decrease) in Net Assets | | |

| | |

| | |

| | |

Net change in unrealized appreciation/depreciation | | |

CHANGE IN NET ASSETS RESULTING FROM OPERATIONS APPLICABLE TO COMMON SHARES | | |

Distribution to Common Shareholders: | | |

Share Transactions Applicable to Common Shares: | | |

Cost of shares tendered and repurchased | | |

| | |

| | |

| | |

| | |

See Notes which are an integral part of the Financial Statements

Annual Shareholder Report

Statement of Cash FlowsNovember 30, 2024

| |

Change in net assets resulting from operations applicable to common shares | |

Adjustments to Reconcile Change in Net Assets Resulting from Operations to Net Cash Provided by Operating Activities: | |

Purchases of investment securities | |

Proceeds from sale of investment securities | |

Net purchases of short-term investment securities | |

Decrease in due from broker | |

Decrease in income receivable | |

Decrease in variation margin on futures contracts | |

Decrease in payable for investments purchased | |

Decrease in interest payable—VMTPS | |

Increase in payable for portfolio accounting fees | |

Decrease in payable for investment adviser fee | |

Increase in payable for Directors’/Trustees’ fees | |

Increase in payable for administrative fee | |

Increase in payable for auditing fees | |

Decrease in accrued expenses | |

Net amortization of premium | |

Net realized loss on investments | |

Net change in unrealized appreciation/depreciation of investments | |

Net Cash Provided By Operating Activities | |

| |

Decrease in deferred offering costs | |

Redemption of VMTPS, at liquidation value | |

Tender and repurchase of common shares | |

Income distributions to participants | |

Net Cash Used In Financing Activities | |

| |

| |

| |

| |

Supplemental disclosure of cash flow information:

Cash paid for interest expense during the period ended November 30, 2024, was $3,813,474.See Notes which are an integral part of the Financial Statements Annual Shareholder Report

Notes to Financial Statements

Federated Hermes Premier Municipal Income Fund (the “Fund”) is registered under the Investment Company Act of 1940, as amended (the “Act”), as a diversified, closed-end management investment company. The investment objective of the Fund is to provide current income exempt from federal income tax, including the federal AMT.

2. SIGNIFICANT ACCOUNTING POLICIES

The following is a summary of significant accounting policies consistently followed by the Fund in the preparation of its financial statements. These policies are in conformity with U.S. generally accepted accounting principles (GAAP).

In calculating its net asset value (NAV), the Fund generally values investments as follows:

■

Fixed-income securities are fair valued using price evaluations provided by a pricing service approved by Federated Investment Management Company (the “Adviser”).

■

Shares of other mutual funds or non-exchange-traded investment companies are valued based upon their reported NAVs, or NAV per share practical expedient, as applicable.

■

Derivative contracts listed on exchanges are valued at their reported settlement or closing price, except that options are valued at the mean of closing bid and ask quotations.

■

Over-the-counter (OTC) derivative contracts are fair valued using price evaluations provided by a pricing service approved by the Adviser.

■

For securities that are fair valued in accordance with procedures established by and under the general supervision of the Adviser, certain factors may be considered such as: the last traded or purchase price of the security, information obtained by contacting the issuer or dealers, analysis of the issuer’s financial statements or other available documents, fundamental analytical data, the nature and duration of restrictions on disposition, the movement of the market in which the security is normally traded, public trading in similar securities or derivative contracts of the issuer or comparable issuers, movement of a relevant index, or other factors including but not limited to industry changes and relevant government actions.

If any price, quotation, price evaluation or other pricing source is not readily available when the NAV is calculated, if the Fund cannot obtain price evaluations from a pricing service or from more than one dealer for an investment within a reasonable period of time as set forth in the Adviser’s valuation policies and procedures for the Fund, or if information furnished by a pricing service, in the opinion of the Adviser’s valuation committee (“Valuation Committee”), is deemed not representative of the fair value of such security, the Fund uses the fair value of the investment determined in accordance with the procedures described below. There can be no assurance that the Fund could obtain the fair value assigned to an investment if it sold the investment at approximately the time at which the Fund determines its NAV per share, and the actual value obtained could be materially different.

Fair Valuation Procedures

Pursuant to Rule 2a-5 under the Act, the Fund’s Board of Trustees (the “Trustees”) has designated the Adviser as the Fund’s valuation designee to perform any fair value determinations for securities and other assets held by the Fund. The Adviser is subject to the Trustees’ oversight and certain reporting and other requirements intended to provide the Trustees the information needed to oversee the Adviser’s fair value determinations.

The Adviser, acting through its Valuation Committee, is responsible for determining the fair value of investments for which market quotations are not readily available. The Valuation Committee is comprised of officers of the Adviser and certain of the Adviser’s affiliated companies and determines fair value and oversees the calculation of the NAV. The Valuation Committee is also authorized to use pricing services to provide fair value evaluations of the current value of certain investments for purposes of calculating the NAV. The Valuation Committee employs various methods for reviewing third-party pricing-service evaluations including periodic reviews of third-party pricing services’ policies, procedures and valuation methods (including key inputs, methods, models and assumptions), transactional back-testing, comparisons of evaluations of different pricing services, and review of price challenges by the Adviser based on recent market activity. In the event that market quotations and price evaluations are not available for an investment, the Valuation Committee determines the fair value of the investment in accordance with procedures adopted by the Adviser. The Trustees periodically review the fair valuations made by the Valuation Committee. The Trustees have also approved the Adviser’s fair valuation and significant events procedures as part of the Fund’s compliance program and will review any changes made to the procedures.

Factors considered by pricing services in evaluating an investment include the yields or prices of investments of comparable quality, coupon, maturity, call rights and other potential prepayments, terms and type, reported transactions, indications as to values from dealers and general market conditions. Some pricing services provide a single price evaluation reflecting the bid-side of the market for an investment (a “bid” evaluation). Other pricing services offer both bid evaluations and price evaluations indicative of a price between the prices bid and ask for the investment (a “mid” evaluation). The Fund normally uses bid evaluations for any U.S. Treasury and Agency securities, mortgage-backed securities and municipal securities. The Fund normally uses mid evaluations for any other types of fixed-income securities and any OTC derivative contracts. In the event that market quotations and price evaluations are not available for an investment, the fair value of the investment is determined in accordance with procedures adopted by the Adviser.

Annual Shareholder Report

Investment Income, Gains and Losses, Expenses and Distributions

Investment transactions are accounted for on a trade-date basis. Realized gains and losses from investment transactions are recorded on an identified-cost basis. Interest income and expenses are accrued daily. Distributions to common shareholders, if any, are recorded on the ex-dividend date and are declared and paid monthly. In addition, distributions of capital gains, if any, are declared and paid at least annually. Non-cash dividends included in dividend income, if any, are recorded at fair value. Amortization/accretion of premium and discount is included in investment income. The detail of the total fund expense waiver and reduction of $364,360 is disclosed in Note 5 and Note 6.

It is the Fund’s policy to comply with the Subchapter M provision of the Internal Revenue Code of 1986 (the “Code”) and to distribute to shareholders each year substantially all of its income. Accordingly, no provision for federal income tax is necessary. As of and during the year ended November 30, 2024, the Fund did not have a liability for any uncertain tax positions. The Fund recognizes interest and penalties, if any, related to tax liabilities as income tax expense in the Statement of Operations. As of November 30, 2024, tax years 2021 through 2024 remain subject to examination by the Fund’s major tax jurisdictions, which include the United States of America and the State of Delaware.

When-Issued and Delayed-Delivery Transactions

The Fund may engage in when-issued or delayed-delivery transactions. The Fund records when-issued securities on the trade date and maintains security positions such that sufficient liquid assets will be available to make payment for the securities purchased. Securities purchased on a when-issued or delayed-delivery basis are marked to market daily and begin earning interest on the settlement date. Losses may occur on these transactions due to changes in market conditions or the failure of counterparties to perform under the contract.

The Fund purchases and sells financial futures contracts to manage duration, market and yield curve risks. Upon entering into a financial futures contract with a broker, the Fund is required to deposit with a broker, either U.S. government securities or a specified amount of cash, which is shown as due from broker in the Statement of Assets and Liabilities. Futures contracts are valued daily and unrealized gains or losses are recorded in a “variation margin” account. The Fund receives from or pays to the broker a specified amount of cash based upon changes in the variation margin account. When a contract is closed, the Fund recognizes a realized gain or loss. Futures contracts have market risks, including the risk that the change in the value of the contract may not correlate with the changes in the value of the underlying securities. There is minimal counterparty risk to the Fund since futures contracts are exchange-traded and the exchange’s clearinghouse, as counterparty to all exchange-traded futures contracts, guarantees the futures contracts against default.

At November 30, 2024, the Fund had no outstanding futures contracts.

The average notional value of long futures contracts held by the Fund throughout the period was $2,739,215. This is based on amounts held as of each month-end throughout the fiscal year.