UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-21237

Unified Series Trust

2960 N. Meridian Street, Ste.300, Indianapolis, In 46208

Christopher E. Kashmerick

Unified Fund Services, Inc.

2960 N. Meridian Street, Ste. 300

Indianapolis, IN 46208

(Name and address of agent for service)

Registrant's telephone number, including area code: 317-917-7000

Date of fiscal year end: 03/31

Date of reporting period: 03/31/10

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

Dean Small Cap Value Fund (DASCX)

Management’s Discussion & Analysis – Fiscal Year ending March 31, 2010

Past Year Review

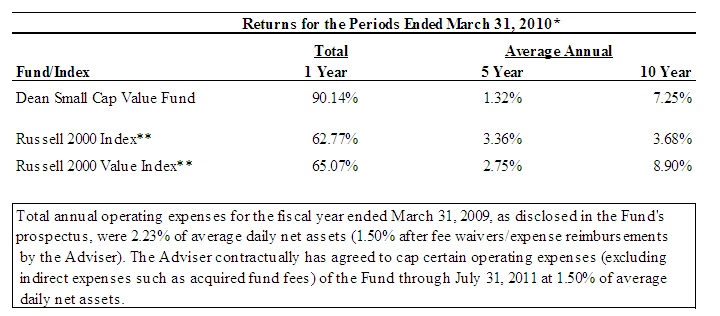

Small cap stocks have dramatically rebounded from their historic fall in late 2008 and early 2009 with an equally historic rise over the past fiscal year. For the 12 months ending March 31, 2010, the Dean Small Cap Value Fund returned a positive 90.14% net of fees compared with a positive 65.07% for the Russell 2000 Value Index and a positive 62.77% for the Russell 2000 Index.

We were extremely pleased to be up over 90% and to have outperformed our index (the Russell 2000 Value) by 25% this past fiscal year. Better yet, we accomplished this performance in an environment that was not one in which we typically would perform well.

Since the low on March 9, 2009, the market rally has been led by the lowest quality stocks; (meaning, companies that have balance sheets loaded with debt, companies that do not pay a dividend or have earnings, and companies whose stocks have historically been the most volatile). This is usually not a friendly environment for our investing style, as we tend to favor stocks with the opposite attributes: companies that have minimal debt, companies that pay a dividend and have steady earnings, and companies whose stocks have historically been less volatile than the market with a narrower range of outcomes.

So how did we outperform in such a dramatic way while operating in an unfavorable environment for our investing style? We feel it is because of our proprietary process of calculating normalized earnings.

By focusing on normalized earnings power, we felt comfortable holding large weights in high quality companies that were in the most economically sensitive industries in late 2008 and early 2009. We believed we owned asymmetrical risk versus reward situations; (meaning, we had limited downside risk, with a great deal of upside potential, as long as the business cycle eventually came back and as long as we were remotely accurate in our calculation of normalized earnings). We believe it was our disciplined process of calculating normal earnings power that led us to the economically sensitive stocks at a time when not many investors were willing to own them, thus helping us outperform this past year.

We believe that our calculation of normalized earnings is one of our competitive advantages at Dean Capital Management (DCM). Instead of using historical or next year’s projected earnings to value a company, we calculate normalized earnings (what we think a company can earn in a typical business environment over a full business cycle) for every company we purchase. We believe it is more prudent to focus on a longer time horizon by looking three to five years out versus focusing on what a company might earn in the next year. By doing this, we seek to eliminate the tendency to allow emotion to cause extrapolation of the most recent trends. We believe it provides a stable number upon which we can calculate valuations that are comparable across companies and sectors. The stabilit y of our normal earnings number was the reason we had conviction owning the most neglected stocks in March of 2009.

While we would love to have 90% absolute returns that are 25% above our benchmark every year, we recognize this will most certainly not happen. We feel it is important that we give our shareholders a sense of what they can expect from us in different types of markets.

A residual of adhering to our process is the tendency to perform well at inflection points in the market, which can be seen in our strong outperformance relative to the benchmark at the bottom of the market in March 2009 through the past fiscal year. Conversely, we tend to underperform in a momentum market; and, wherein the longer a market continues on a trend, the greater our underperformance becomes. This is evidenced by our struggles in late 2008 and early 2009 when the market had strong momentum to the downside. We held up well in the initial downturn; however, our underperformance grew as the market became more and more irrational in its behavior. Ultimately, we were rewarded for our patience and discipline when the market turned the corner in March 2009 and we more than made up fo r being a little early.

This dynamic is a function of our underemphasizing those parts of the market that are becoming popular and overvalued, while embracing those parts of the market that are becoming neglected and undervalued. By doing so, we believe we are properly being compensated for the risk we are taking in the market. We feel that continuing in the disciplined process we have always followed serves our shareholders well over the long term.

Please know that we will continue to do our best to be good stewards of your capital as we invest alongside you. You can feel comfortable that our financial interests are aligned with yours as each of our portfolio managers holds a significant portion of his investable assets in DASCX. We definitely, as the saying goes, “eat our own cooking.”

Market Perspective

Small cap stocks have historically been one of the best performing asset classes coming out of a recession, and this recession has been no different. Below is a chart comparing the Russell 2000 Index to the S&P 500 Index from the March 9, 2009 market low. The small cap outperformance has been substantial:

Even though small cap stocks have had a big run, we think they can continue to perform well going forward. Small caps could continue to benefit as the economic recovery takes hold, even if that recovery is slower than normal. They could also benefit from merger and acquisition activity picking up again after a long period of dormancy while the credit markets were frozen.

Large corporations have significant amounts of cash on their balance sheets and, given the slower growth environment the economy may be facing in the future, these companies will attempt to supplement slow organic growth through acquisitions of smaller companies. We feel this could be favorable to our investment style as the attributes we look for in companies, such as high free cash flow generation, high returns on capital, market dominance in niche businesses, and attractive valuations, are attributes that private equity buyers, as well as strategic buyers, might look for in an acquisition target.

We have already benefited from this trend with the acquisition of Foundation Coal (FCL) by Alpha Natural Resources (ANR) and the leveraged buyout of IMS Health (RX).

FCL is a coal producer in the Powder River Basin in Wyoming, as well as the North and Central Appalachian Mountains. ANR purchased FCL in order to gain access to the Powder River Basin for a 37% premium over where the stock was trading and an 85% premium from our original purchase price.

RX is a medical information and intelligence provider to large pharmaceutical companies and was a sizeable holding for DASCX in 2009. It was purchased by TPG and the CPP Investment Board for a 31% premium over where the stock was trading and a 59% premium from where we originally bought the stock. Merger and acquisition activity will likely continue to be an important performance driver of small cap stocks.

According to our work on the valuation level of the market, we see valuations of economically sensitive stocks as being stretched. We have started to rotate towards traditionally defensive stocks as they look to have much more attractive valuations. Given where we are at this point in the cycle, we feel we are getting paid more to own steady companies with good balance sheets and cash flows that are persistent regardless of the economy, versus those companies that could see a sharp rebound in earnings from an economic recovery. To put it simply, we believe an economic recovery is largely priced into the market at this point in time.

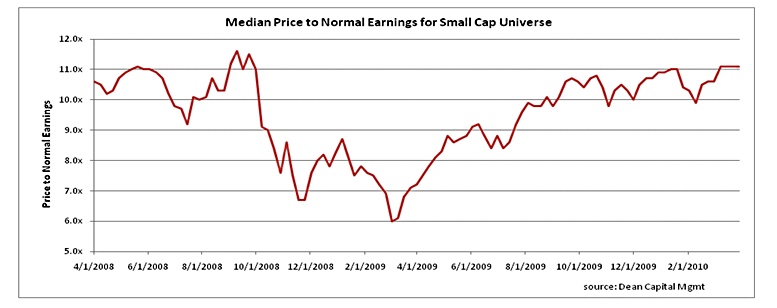

By way of reference, below is a chart of the price to DCM’s calculation of normal earnings over the last two years for the small cap universe:

As seen in the chart, the small cap market (according to DCM’s calculations) is now at a pre-credit crisis valuation level. While this level is not extremely overvalued, it isn’t irrationally cheap like it was in March 2009, and the market seems to be pricing in a normal post World War II recovery. We believe a normal recovery is still very much in question given that we are in the midst of the largest deleveraging cycle we have seen since the Great Depression. Attractive investments in the current environment will be much less broad-based and tied to the economy then they were in 2009 and will need to be more opportunistic in nature, in our opinion.

Current Opportunities

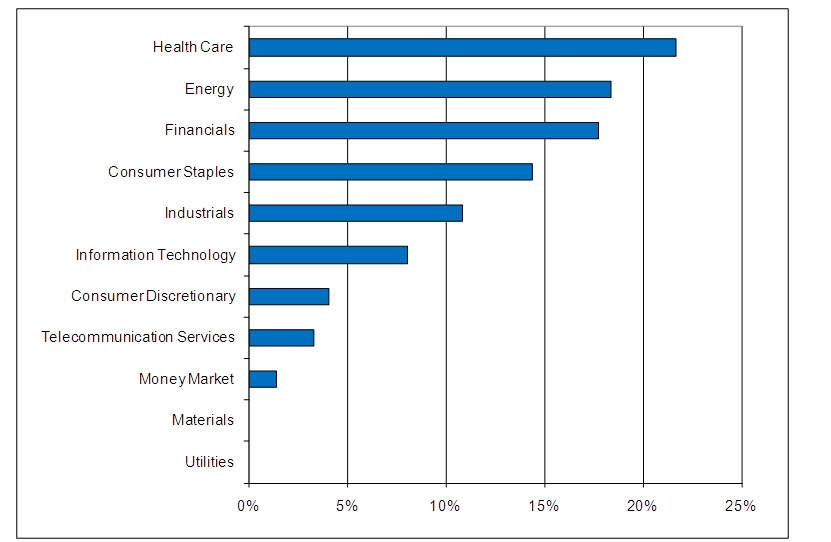

Through our bottom up, fundamental analysis, and using normal earnings as our valuation guide, we have been lowering our weight in Industrial and Consumer Discretionary companies while increasing our weight in Health Care and Consumer Staples.

Another area where we have been finding what we believe are attractive investment opportunities is in the banking industry. This is our largest industry weight with nearly 25% of the portfolio invested in small cap banks. We feel this is a large differentiating factor for DASCX relative to our benchmark and peers. It also demonstrates how we can find tremendous value in our search for good companies in neglected industries.

We own a basket of 17 bank stocks that we believe can take advantage of the current dislocations in the banking industry by acquiring failed institutions through FDIC-assisted transactions. FDIC-assisted transactions can generate a tremendous amount of value for shareholders of the acquiring firm. These types of acquisitions instantly increase the acquiring bank’s normalized earnings power, book value, and franchise value while the FDIC usually shares in 80% of the losses of the failed bank.

Our prime example to illustrate the potential from these types of situations is First Financial Bancorp (FFBC) out of Cincinnati, Ohio, which is one of our largest holdings. FFBC announced two FDIC-assisted transactions in September 2009. Prior to the acquisitions, the stock was trading around $8 per share. Following the acquisitions, and after the market recognized the earnings potential of the deals, the stock is now trading at just under $20 per share for a nearly 150% gain. This has handily outperformed the market over that time frame. We hope to have more stocks like FFBC in our basket of bank stocks.

One of our most recent purchases, GeoEye, Inc. (GEOY), is an example of an opportunistic investment, and also demonstrates how we like to find companies that dominate a niche market.

GEOY provides satellite imagery services worldwide by operating high resolution satellites. The company’s satellites support a variety of applications, including defense and military planning, agriculture and environmental monitoring, as well as general charting and mapping. One of GEOY’s applications is used in providing images to Google Earth and Google Maps. GEOY is one of two major players in the high resolution commercial satellite imagery industry and it holds significant market share. The stock sold off in December 2009 because of a glitch in one of its satellites. We felt the market overreacted to the situation, and this event provided us the opportunity to start a position in a unique company that dominates a niche market with the stock temporarily undervalued because of a transitory event.

Sector Highlights

The best performing sector relative to our benchmark in the last 12 months was the Financials sector, which accounted for nearly 50% of our outperformance. We benefited from our overweight in the sector, as well as from our stock selection, with our stocks returning 92% versus 49% for the index. As we mentioned, we are still finding excellent opportunities in the Financial sector, especially in small cap banks.

The worst performing sector in the last year was Consumer Staples. Most of this underperformance came in the last four months while we were increasing the weight in this underperforming sector. The market continues to favor economically sensitive sectors such as Consumer Discretionary, as well as commodity related industries, while neglecting Consumer Staples. This is providing us with some attractive opportunities.

The Last Year’s Standout Stocks

PZN:

Pzena Investment Management (PZN) was the largest contributing stock over the last year. PZN is an institutional boutique asset management firm that focuses solely on deep value equity investing. This investment style was out of favor through most of 2008 and early 2009, and the stock was under pressure as a result. We continued to believe in the process and niche focus of the firm and thought it would benefit from the market rotating back to Pzena’s investment style. Deep value investing usually does extremely well when the economy starts to come out of a recession. Our theory took hold in the second quarter of 2009 and, given the enormous appreciation of the stock, we felt it had gotten ahead of its fundamentals. Because of its stretched valuation, we exited the position.

BH (formerly SNS):

The second largest individual contributor for the period was Biglari Holdings (BH), formerly named Steak ‘n Shake (SNS). Steak ‘n Shake is a good example of the type of situation we think will be instrumental in driving outperformance in the future.

Steak ‘n Shake, which we have owned since June 2008, is a fast food restaurant franchise that is highly concentrated in the Midwest and the South. Steak ‘n Shake was a company with solid brand recognition, but the previous management team was more interested in “growth for growth’s sake” versus increasing return on invested capital. Activist investor, Sardar Biglari, agitated for change while garnering a seat on the Board and eventually becoming Chairman and CEO. Since gaining these titles, Mr. Biglari has dramatically slowed the store growth and rationalized the store base while turning around the operations in the existing restaurants. In addition, Mr. Biglari is attempting to turn the company into a mini Berkshire Hathaway by changing it into a holding company structure where he uses the cash flow generated from franchisee royalty streams to invest in unrelated businesses that offer what he feels are the best opportunities for return on invested capital. Meanwhile, he has changed the name to Biglari Holdings to alleviate the stigma a potential acquisition target might have from being acquired by a fast food company.

HMPR:

Our largest detractor over the last year was Hampton Roads Bankshares (HMPR). We underestimated the negative impact that two large acquisitions would have on the very solid balance sheet that Hampton Roads had always maintained. The two banks HMPR acquired were fraught with bad loans and it has begun to strain Hampton Roads’ balance sheet. Recognizing our mistake, we quickly sold the stock before it deteriorated further.

KNDL:

Our second largest detractor for the period was Kendle International (KNDL). Kendle is a contract research organization that provides Phase I through IV clinical research and drug development services to the pharmaceutical and biotechnology industries. Kendle announced that it would not meet analysts’ estimates due to pricing pressure, project delays, and cancellations, which caused the stock to plummet over 50% in one day. Many of Kendle’s competitors missed estimates because of the same issues. We waited for a small bounce in Kendle’s stock price and we exited the position because of deteriorating fundamentals and better opportunities elsewhere.

Bottom Line

Over the last year, we believe we have had a nice run in the market in general, and in the Dean Small Cap Value Fund in particular; however, we feel the market dynamic has changed meaningfully since March 2009. The market is beginning to price in a recovery, yet while much improved, the evidence of a full recovery is still in question. We feel there are still many great opportunities currently in the small cap space; there just aren’t as many extraordinary opportunities that we saw last year. More importantly, we believe that over long periods of time, the small cap value asset class is a superior asset class in which to be invested. This is why, as portfolio managers of the Fund, we hold such significant personal stakes in DASCX.

Thank you for your continued confidence in Dean.

Small-Cap investing involves greater risk not associated with investing in more established companies, such as greater price volatility, business risk, less liquidity and increased competitive threat.

Performance Summary

The performance quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Current performance may be lower or higher than the performance data quoted. For more infor mation on the Dean Small Cap Value Fund, and to obtain performance data current to the most recent month-end, or to request a prospectus, please call 1-888-899-8343.

You should carefully consider the investment objectives, potential risks, management fees, and charges and expenses of the Fund before investing. The Fund’s prospectus contains this and other information about the Fund, and should be read carefully before investing.

* Return figures reflect any change in price per share and assume the reinvestment of all distributions.

**The Russell 2000 and Russell 2000 Value Indices are unmanaged benchmarks that assume reinvestment of all distributions and exclude the effect of taxes and fees. The Indices are widely recognized unmanaged indices of equity prices and are representative of a broader market and range of securities than are found in the Fund’s portfolio. Individuals cannot invest directly in the Indices; however, an individual can invest in exchange-traded Funds or other investment vehicles that attempt to track the performance of a benchmark index.

This graph shows the value of a hypothetical initial investment of $10,000 in the Fund, the Russell 2000 Index and the Russell 2000 Value Index on March 31, 2000 and held through March 31, 2010.

The Russell 2000 Index and the Russell 2000 Value Index are widely recognized unmanaged indices of common stock prices and are representative of a broader market and range of securities than are found in the Fund’s portfolio. Individuals cannot invest directly in the Indices; however, an individual can invest in exchange-traded Funds or other investment vehicles that attempt to track the performance of a benchmark index. The Index returns do not include expenses, which have been deducted from the Fund’s return. These performance figures include the change in value of the stocks in the index plus the reinvestment of dividends and are not annualized. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. THE FUND’S RETU RN REPRESENTS PAST PERFORMANCE AND DOES NOT GUARANTEE OR PREDICT FUTURE RESULTS. Investment returns and principal values will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For more information on the Dean Small Cap Value Fund, and to obtain performance data current to the most recent month-end, or to request a prospectus, please call 1-888-899-8343.

You should carefully consider the investment objectives, potential risks, management fees, and charges and expenses of the Fund before investing. The Fund’s prospectus contains this and other information about the Fund, and should be read carefully before investing.

The Fund is distributed by Unified Financial Securities, Inc., Indianapolis, IN 46208, Member FINRA.

Dean Large Cap Value Fund (DALCX)

Management’s Discussion & Analysis – Fiscal Year ending March 31, 2010

“Many shall be restored that now are fallen and many shall fall that now are in honor.” – Horace

This quote opened the classic investment tome, Security Analysis, by Benjamin Graham and David Dodd. Among a great deal of insights from this book that we use on a daily basis, this quote may be the most applicable for the last year. During the climax of the market drop in the winter of 2009, any stock with cyclical earnings and a less than exceptionally good balance sheet fell in price far beyond the massive market move down 50% or so. In contrast, utilities, packaged food companies and similar noncyclical businesses held their value and thus may be seen to have been held in honor (at least in a relative sense). Fast forward one year and nearly the opposite is true. The market does not appear to have the s ame magnitude of froth as it then was cheap. However, cyclical businesses with generally weaker fundamentals are leading the market higher seemingly every day. The Dean Large Cap Value Fund was well-positioned for this change in sentiment. We didn’t know when it might come, but every day the market continued to fall (to seemingly irrational lows), the more confident we became in our holdings. In hindsight, it feels like we should have done much more. Our conservative nature may have helped us during the fall and restrained us somewhat on the rebound. The net result, however, is that we finished the last couple of years well ahead of our benchmark indexes, as well as many funds within the same category.

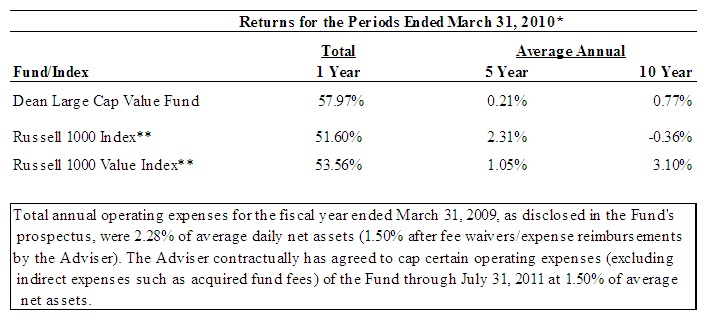

Last year, every sector in the market was up in an absolute sense. Interpreting how well an investor performed, therefore, is about comparing the results versus what he or she might have received in other opportunities (such as an index fund or peer mutual fund). In the one year period ended March 31, 2010, the Dean Large Cap Value Fund had a total return of 57.97% versus 53.56% for the benchmark Russell 1000 Value Index. The Fund performed better than 87% of Large Cap Value managers during this time, with the Morningstar median peer fund up 50.5%.

What worked in the market:

As mentioned above, the best performing stocks from March 31, 2009 to March 31, 2010 were cyclical stocks of lower quality. The market sectors led by such businesses in the period were Materials (+99%) and Consumer Discretionary (+92%). Two other leading sectors that also have a considerable cyclical nature to earnings are Industrials (+83%) and Financials (+79%).

Dean Large Cap Value suffered a little for holding a smaller portfolio weight in Materials and Consumer Discretionary. This makes sense since many of the same stocks that did so well in the period were facing the precarious fundamental position of losing money on a cash basis while being heavily indebted. In other words, bankruptcy was a very real possibility. We try to avoid such “deep value” situations where the expected payout is an all or nothing proposition. Instead, we aim to invest in the best quality businesses in these neglected groups.

The Industrial and Financials sectors were relatively profitable for us. (Remember that every sector was profitable in an absolute sense. We are discussing what worked better or worse than average). The Fund’s Industrial selections performed very well. Arguably, we rotated out of some of the winners and into more defensive names (literally and figuratively) too early. However, investments in such high-quality companies as United Technologies (UTX), Dover Corp (DOV), and Ingersoll-Rand (IR) proved very profitable.

Despite a large underweight position in Financials, the Fund did well in the group. Stocks such as Aflac (AFL) and SunTrust Banks (STI) made up for holding less Financials in total with solid returns. They are also good examples that can be argued to have been sold too soon. We feel there is a wide range of outcome situations. If the market price discounts lower value than the bottom of the wide range, then investment appears justified. However, when the price appreciates well within that implied by the range of outcomes, we are much less likely to hold on to medium quality situations. In this case, stock prices seem to have moved from below pessimistic expectations to perhaps overly optimistic fundamental expectations. The opportunity today is in avoiding suc h poor risk/reward situations.

What didn’t work:

We added significant value last year by being largely absent from poor performing sectors. In a nearly 180 degree turn from the prior period, the worst sectors last year were Telecommunications (+14%), Utilities (+22%), Energy (+28%), and Consumer Staples (+39%). We were underweight three of these for most of the year. Only in Energy did we have a modest overweight position (average 1.4% more), and this was a very small drag on performance. Consumer Staples went from being underweight to the second largest overweight late in the year.

Telecommunications was the worst performing sector and we were fortunate to hold a lower weight than the benchmark. Both AT&T (T) and Verizon (VZ) significantly underperformed the benchmark, up 9.3% and 9.2%, respectively.

The Utilities sector was the Fund’s single best group in terms of contribution to relative performance. The Fund did not own any Utilities during the year, while the benchmark holdings appreciated only 22% during this massive market recovery. Only recently have some quality utility stocks begun to be somewhat appealing from an investment point of view.

Energy was an underperforming sector last year. With an improving economic recovery underway, crude oil prices increased nearly 70% year over year. The other half of the energy commodity equation, natural gas, managed only a 2.5% increase in prices year over year. The natural gas market is suffering from a significant over-supply situation. The dynamics of the industry are somewhat different due to recent improvements in field development technology. We expect a strengthening of natural gas prices, but it may be slower in coming with improvements in the North American industrial economy. Downstream profits from refining crude oil into gasoline and other products are at decade lows. This has weighed on the stock prices, as well. The Fund’s aver age weight near 20% during the year (compared with approximately 18% for the benchmark) detracted from the Fund’s overall strong performance in the year.

The Fund’s holdings in Consumer Staples went from being more than 3% under the benchmark weight at the beginning of the year to nearly 9% over the benchmark at the end of the year. This served us well, as Consumer Staples significantly underperformed the benchmark. This massive change in sentiment (and relative value) has provided a good investment opportunity that we are positioned to take advantage of.

Other stock market return factors:

As alluded to a number of times already, the most significant event this past year has been the historic rebound in the market. It seems fitting, and perhaps predictable, that one of the largest and steepest market drops would be followed by one of the largest and steepest market recoveries. The economy most certainly has improved for most of the past year. To begin with, all the market needed was the economy to stop getting worse. In the summer of 2009, economic indicators began to move a step better by actually improving instead of simply being less bad. As such, the market recovery was very well justified by underlying fundamentals. That being said, the market finished our fiscal year end with prices up 80% from the low reached March 9, 2009. The question d u jour is whether it has gone too far, too fast. In our opinion, the answer is yes and no. There are parts of the market where prices indicate overly optimistic expectations. Still, we continue to find a number of very good companies with stock prices significantly below what we feel are justified by business fundamentals.

Value indexes outperformed growth in the year ended March 31, 2010. The simplest explanation for this deviation is that there is significantly greater weight in Financials within value benchmarks and less weight in the Consumer Staples sector.

The Russell 1000 benchmarks include the Russell Top 200 Index (largest market capitalization stocks), as well as the Russell Mid Cap Index (the next 800). Last year, mid cap stocks were up 68% compared with the Russell Top 200 Index (up 47%). As the Dean Large Cap Value Fund is predominantly large cap, this disparity was a drag on performance. Over time, this is expected to even out, but market capitalization ebbs and flows can affect performance for extended periods. We plan to remain predominately invested in the largest capitalization stocks as our name suggests.

For two years now, in our opinion, the single biggest quantitative attribute separating the winners and the losers was volatility. Volatility represents the degree of variation in the price of a stock from day to day. Usually, the greater the volatility, the more risk associated with the security or underlying business. As the economy and market were imploding, stocks with the greatest volatility led the way down, underperforming the market dramatically. When the market and economy reversed, the most volatile stocks led the way once again, this time upward. Over time, we expect the Dean Large Cap Value Fund to be invested principally in lower volatility stocks than the overall market or our benchmark index. However, when prices justify it (such as in early 2009), we will buy into the fear increasing our exposure to higher volatility stocks – while remaining in what we deem higher quality companies. The net effect for last year is that the Fund benefited significantly from buying risk (buying fear and selling safety). From the summer of 2009 through the winter of 2010 we reversed this position, which greatly reduced the exposure to higher volatility stocks more in line with historic and expected levels. This has hurt the Fund performance the last month or so of the year (March 2010), but we expect it will be a positive factor going forward.

With similar logic in opposing direction, a stock’s valuation and dividend yield was a significant factor in how stocks performed in the last couple of years. When the market was falling, higher valuation and low/no dividend yield stocks dramatically underperformed. When the market reversed, so did this factor. Last year, stocks with the highest price to earnings ratio and lowest yields led the market. A companies whose earnings were down more than other companies and that did not pay much of a dividend were deemed the most risky and sold en masse. During this past year investors changed course and flocked to weaker cyclical companies. They have led the market higher since.

Another significant event this past year is the passing of health care reform. For the first half of the year, Health Care stocks underperformed, at least partly due to investor fears over what reform might mean to their bottom line. During this time, we were buying into the fear as we felt that any bill that was passed would be significantly diluted in terms of actual change. Additionally, it was as likely as not that for many health care companies, the proposed legislation would be additive to firm value. We built the largest overweight position in the portfolio through adding medical device makers and pharmaceutical/biotech firms, in addition to the strongest health care insurer – United HealthCare (UNH). As the market’s appetite for risk has come back with a vengean ce, this group was left behind to some extent. Our stock positions have done relatively well within the group and we continue to feel that health care is one of the most opportunity rich sectors of the market.

Portfolio Positioning

Moving beyond Health Care, Dean Large Cap Value’s second largest sector overweight is in Consumer Staples. Similar to Health Care, this group is comprised of many high-quality businesses with very consistent and high returns on capital, cash generation and solid balance sheets. However, such quality is not what the market is buying today. It is our belief that the group has dramatically underperformed. The popular market strategy is to buy what could benefit most from an economic recovery. This makes sense absent the consideration of stock market prices. Much as we bought fear when it was on sale, today we are full of stocks in which we bought safety when such stocks are not popular.

On the other end of the spectrum, the Fund has relatively small weights in both Financials and Consumer Discretionary sectors. Both these groups have done very well in the market recovery. Many seem to have moved farther than justified by the fundamentals. Expectations for a complete recovery in earning power at these cyclical businesses seem premature. While there is little doubt earnings will get there, it is unlikely that it will be this year, or even next – but that is what the market prices imply expectations are. As such, we own much less than the benchmark index and what we do own are relatively higher quality and lower volatility than average.

In conclusion, we believe this has been a very good year for investors in the Dean Large Cap Value Fund. Financial disaster was largely sidestepped and the economy has started the long road back to sustained expansion. Much opportunity exists in the market and we hope and expect to profit from it. We thank you for your continued investment.

Performance Summary

The performance quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Current performance may be lower or higher than the performance data quoted. For more infor mation on the Dean Large Cap Value Fund, and to obtain performance data current to the most recent month-end, or to request a prospectus, please call 1-888-899-8343.

You should carefully consider the investment objectives, potential risks, management fees, and charges and expenses of the Fund before investing. The Fund’s prospectus contains this and other information about the Fund, and should be read carefully before investing.

* Return figures reflect any change in price per share and assume the reinvestment of all distributions.

**The Russell 1000 and Russell 1000 Value Indices are unmanaged benchmarks that assume reinvestment of all distributions and exclude the effect of taxes and fees. The Indices are widely recognized unmanaged indices of equity prices and are representative of a broader market and range of securities than are found in the Fund’s portfolio. Individuals cannot invest directly in the Indices; however, an individual can invest in exchange-traded funds or other investment vehicles that attempt to track the performance of a benchmark index.

This graph shows the value of a hypothetical initial investment of $10,000 in the Fund, the Russell 1000 Index and the Russell 1000 Value Index on March 31, 2000 and held through March 31, 2010.

The Russell 1000 Index and the Russell 1000 Value Index are widely recognized unmanaged indices of common stock prices and are representative of a broader market and range of securities than are found in the Fund’s portfolio. Individuals cannot invest directly in the Indices; however, an individual can invest in exchange-traded funds or other investment vehicles that attempt to track the performance of a benchmark index. The Index returns do not include expenses, which have been deducted from the Fund’s return. These performance figures include the change in value of the stocks in the index plus the reinvestment of dividends and are not annualized. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. THE FUND’S RETU RN REPRESENTS PAST PERFORMANCE AND DOES NOT GUARANTEE OR PREDICT FUTURE RESULTS. Investment returns and principal values will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For more information on the Dean Large Cap Value Fund, and to obtain performance data current to the most recent month-end, or to request a prospectus, please call 1-888-899-8343.

You should carefully consider the investment objectives, potential risks, management fees, and charges and expenses of the Fund before investing. The Fund’s prospectus contains this and other information about the Fund, and should be read carefully before investing.

The Fund is distributed by Unified Financial Securities, Inc., Indianapolis, IN 46208, Member FINRA.

DEAN SMALL CAP VALUE FUND HOLDINGS - (UNAUDITED)

1As a percent of total investments.

DEAN LARGE CAP VALUE FUND HOLDINGS - (UNAUDITED)

1As a percent of total investments.

PORTFOLIO HOLDINGS

The Funds file a complete schedule of portfolio holdings with the U.S. Securities and Exchange Commission (the SEC) for the first and third quarters of each fiscal year on Form N-Q. The Funds’ Forms N-Q are available on the SEC’s website at http://www.sec.gov. In addition, the Funds’ Forms N-Q may be reviewed and copied at the Commission’s Public Reference Room in Washington, D.C. Information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330.

ABOUT THE FUNDS’ EXPENSES

As a shareholder of each Fund, you incur ongoing costs, including management fees, and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in each Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning and held for the six month period, October 1, 2009 to March 31, 2010.

Actual Expenses

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on each Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not each Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in each Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds.

| Dean Small Cap Value Fund | Beginning Account Value October 1, 2009 | Ending Account Value March 31, 2010 | Expenses Paid During Period October 1, 2009 – March 31, 2010* | |||||||||

| Actual | $ | 1,000.00 | $ | 1,155.40 | $ | 8.06 | ||||||

| Hypothetical** | $ | 1,000.00 | $ | 1,017.45 | $ | 7.54 | ||||||

*Expenses are equal to the Fund’s annualized expense ratio of 1.50%, multiplied by the average account value over the period, multiplied by 182/365 (to reflect the partial year period).

** Assumes a 5% return before expenses.

| Dean Large Cap Value Fund | Beginning Account Value October 1, 2009 | Ending Account Value March 31, 2010 | Expenses Paid During Period October 1, 2009 – March 31, 2010* | |||||||||

| Actual | $ | 1,000.00 | $ | 1,119.23 | $ | 7.92 | ||||||

| Hypothetical** | $ | 1,000.00 | $ | 1,017.45 | $ | 7.54 | ||||||

*Expenses are equal to the Fund’s annualized expense ratio of 1.50%, multiplied by the average account value over the period, multiplied by 182/365 (to reflect the partial year period).

** Assumes a 5% return before expenses.

| DEAN SMALL CAP VALUE FUND | |||||||

| SCHEDULE OF INVESTMENTS | |||||||

| March 31, 2010 | |||||||

| Shares | COMMON STOCKS - 88.89% | Value | |||||

| Agricultural Production - Crops - 1.47% | |||||||

| 17,775 | Chiquita Brands International, Inc. * | $ | 279,601 | ||||

| Aircraft & Parts - 1.49% | |||||||

| 4,045 | Triumph Group, Inc. | 283,514 | |||||

| Book Printing - 2.89% | |||||||

| 33,235 | Courier Corp. | 548,710 | |||||

| Communication Services - 1.08% | |||||||

| 6,925 | GeoEye, Inc. * | 204,287 | |||||

| Crude Petroleum & Natural Gas - 4.24% | |||||||

| 9,420 | Berry Petroleum Co. - Class A | 265,267 | |||||

| 20,880 | Forest Oil Corp. * | 539,122 | |||||

| 804,389 | |||||||

| Electric Services - 3.22% | |||||||

| 31,645 | Portland General Electric Co. | 611,065 | |||||

| Fire, Marine & Casualty Insurance - 2.05% | |||||||

| 14,595 | Greenlight Capital Re., Ltd. - Class A * | 389,395 | |||||

| In Vitro & In Vivo Diagnostics Substances - 1.57% | |||||||

| 13,260 | Immucor, Inc. * | 296,891 | |||||

| Investment Companies - 2.59% | |||||||

| 40,352 | Prospect Capital Corp. | 490,277 | |||||

| Life Insurance - 5.64% | |||||||

| 26,605 | Delphi Financial Group, Inc. - Class A | 669,382 | |||||

| 7,465 | Torchmark Corp. | 399,452 | |||||

| 1,068,834 | |||||||

| National Commercial Banks - 15.95% | |||||||

| 33,645 | American National Bankshares, Inc. | 677,947 | |||||

| 19,165 | Centerstate Banks, Inc. | 234,771 | |||||

| 34,385 | First Financial Bancorp | 611,709 | |||||

| 12,220 | FirstMerit Corp. | 263,585 | |||||

| 23,555 | National Bankshares, Inc. | 641,874 | |||||

| 14,530 | NewAlliance Bancshares, Inc. | 183,369 | |||||

| 15,070 | Old National Bancorp | 180,086 | |||||

| 10,170 | PacWest Bancorp | 232,079 | |||||

| 3,025,420 | |||||||

*See accompanying notes for they are integral part of these financial statements.

| DEAN FUNDS | |||||||

| DEAN SMALL CAP VALUE FUND | |||||||

| SCHEDULE OF INVESTMENTS - continued | |||||||

| March 31, 2010 | |||||||

| Shares | COMMON STOCKS - 88.89% - continued | Value | |||||

| Oil & Gas Services - 1.38% | |||||||

| 12,465 | Superior Energy Services, Inc. * | $ | 262,014 | ||||

| Orthopedic, Prosthetic & Surgical Appliances & Supplies - 0.99% | |||||||

| 5,560 | STERIS Corp. | 187,150 | |||||

| Paperboard Containers & Boxes - 2.01% | |||||||

| 8,375 | Rock-Tenn Co. - Class A | 381,649 | |||||

| Pharmaceutical Preparations - 1.04% | |||||||

| 21,875 | Prestige Brands Holdings, Inc. * | 196,875 | |||||

| Radio & TV Broadcasting & Communications Equipment - 1.99% | |||||||

| 20,780 | Tekelec * | 377,365 | |||||

| Refuse Systems - 1.02% | |||||||

| 11,265 | IESI-BFC, Ltd. | 193,195 | |||||

| Retail - Eating & Drinking Places - 3.44% | |||||||

| 11,795 | Jack in the Box, Inc. * | 277,772 | |||||

| 16,920 | Sonic Corp. * | 186,966 | |||||

| 493 | Steak n Shake Co./The * | 187,966 | |||||

| 652,704 | |||||||

| Retail - Family Clothing - 1.00% | |||||||

| 5,140 | Buckle, Inc./The | 188,946 | |||||

| Retail - Grocery Stores - 2.08% | |||||||

| 14,045 | Village Super Market, Inc. - Class A | 393,681 | |||||

| Retail - Miscellaneous Shopping Goods Stores - 1.04% | |||||||

| 11,330 | Cabela's, Inc. * | 198,162 | |||||

| Savings Institution, Not Federally Chartered - 4.16% | |||||||

| 12,510 | First Niagara Financial Group, Inc. | 177,892 | |||||

| 13,910 | Home Federal Bancorp, Inc. | 201,834 | |||||

| 8,890 | MB Financial, Inc. | 200,292 | |||||

| 15,815 | Umpqua Holdings Corp. | 209,707 | |||||

| 789,725 | |||||||

| Services - Commercial Physical & Biological Research - 4.40% | |||||||

| 4,645 | Charles River Laboratories International, Inc. * | 182,595 | |||||

| 27,445 | Pharmaceutical Product Development, Inc. | 651,819 | |||||

| 834,414 | |||||||

| Services - Computer Processing & Data Preparation - 1.97% | |||||||

| 17,865 | CSG Systems International, Inc. * | 374,450 | |||||

| Services - Computer Programming Services - 1.32% | |||||||

| 66,665 | CIBER, Inc. * | 249,327 | |||||

| Services - Educational Services - 1.04% | |||||||

| 6,225 | Career Education Corp. * | 196,959 | |||||

| Services - Engineering Services - 1.98% | |||||||

| 26,814 | Ecology & Environment, Inc. - Class A | 375,932 | |||||

| Services - Management Consulting Services - 2.25% | |||||||

| 10,865 | FTI Consulting, Inc. * | 427,212 | |||||

*See accompanying notes for they are integral part of these financial statements.

| DEAN FUNDS | |||||||

| DEAN SMALL CAP VALUE FUND | |||||||

| SCHEDULE OF INVESTMENTS - continued | |||||||

| March 31, 2010 | |||||||

| Shares | COMMON STOCKS - 88.89% - continued | Value | |||||

| State Commercial Banks - 5.60% | |||||||

| 11,815 | Columbia Banking System, Inc. | $ | 239,963 | ||||

| 21,365 | CVB Financial Corp. | 212,154 | |||||

| 4,455 | Hancock Holding Co. | 186,264 | |||||

| 42,305 | United Community Banks, Inc. * | 186,565 | |||||

| 41,590 | Western Alliance Bancorp * | 236,647 | |||||

| 1,061,593 | |||||||

| Steel Works, Blast Furnaces, Rolling Mills - 2.38% | |||||||

| 10,915 | Commercial Metals Co. | 164,380 | |||||

| 50,060 | Friedman Industries, Inc. | 286,343 | |||||

| 450,723 | |||||||

| Surety Insurance - 1.10% | |||||||

| 16,495 | Old Republic International Corp. | 209,157 | |||||

| Surgical & Medical Instruments & Apparatus - 1.72% | |||||||

| 11,575 | Utah Medical Products, Inc. | 325,605 | |||||

| Telephone Communications - 1.45% | |||||||

| 17,145 | Neutral Tandem, Inc. * | 273,977 | |||||

| Wholesale - Groceries & Related Products - 1.34% | |||||||

| 7,565 | Nash Finch Co. | 254,562 | |||||

| TOTAL COMMON STOCKS (Cost $14,468,164) | 16,857,760 | ||||||

| EXCHANGE-TRADED NOTES - 1.40% | |||||||

| 12,690 | iPath S&P 500 VIX Short-Term Futures | 266,617 | |||||

| TOTAL EXCHANGE-TRADED NOTES (Cost $301,785) | 266,617 | ||||||

| MONEY MARKET SECURITIES - 4.38% | |||||||

| 829,919 | AIM STIT-STIC Prime Portfolio - Class I, 0.11% (a) | 829,919 | |||||

| TOTAL MONEY MARKET SECURITIES (Cost $829,919) | 829,919 | ||||||

| Principal | |||||||

| Amount | |||||||

| CONVERTIBLE CORPORATE BONDS - 5.30% | |||||||

| $ | 398,000 | ADC Telecommunications, Inc., 3.50%, 7/15/2015 | 326,857 | ||||

| 184,000 | Chemed Corp., 1.875%, 5/15/2014 | 169,050 | |||||

| 158,000 | DST Systems, Inc., 4.125%, 8/15/2023 (b) | 162,937 | |||||

| 179,000 | LifePoint Hospitals, Inc., 3.50%, 5/15/2014 | 179,448 | |||||

| 188,000 | Pantry, Inc., 3.00%, 11/15/2012 | 166,850 | |||||

| TOTAL CONVERTIBLE CORPORATE BONDS (Cost $945,723) | 1,005,142 | ||||||

| TOTAL INVESTMENTS (Cost $16,545,591) - 99.97% | $ | 18,959,438 | |||||

| Other assets less liabilities - 0.03% | 5,909 | ||||||

| TOTAL NET ASSETS - 100.00% | $ | 18,965,347 | |||||

| * Non-income producing securities. | |||||||

| (a) Variable rate security; the money market rate shown represents the rate at March 31, 2010. | |||||||

| (b) Variable rate security; the interest rate shown represents the rate at March 31, 2010. | |||||||

*See accompanying notes for they are integral part of these financial statements.

| DEAN LARGE CAP VALUE FUND | |||||||

| SCHEDULE OF INVESTMENTS | |||||||

| March 31, 2010 | |||||||

| Shares | COMMON STOCKS - 98.57% | Value | |||||

| Beverages - 2.09% | |||||||

| 4,488 | PepsiCo, Inc. | $ | 296,926 | ||||

| Biological Products - 2.29% | |||||||

| 5,448 | Amgen, Inc. * | 325,573 | |||||

| Books: Publishing or Publishing and Printing - 2.06% | |||||||

| 8,220 | McGraw-Hill Companies, Inc. | 293,043 | |||||

| Computer & Office Equipment - 1.97% | |||||||

| 5,277 | Hewlett-Packard Co. | 280,473 | |||||

| Converted Paper & Paperboard Products - 1.45% | |||||||

| 3,288 | Kimberly-Clark Corp. | 206,749 | |||||

| Crude Petroleum & Natural Gas - 4.79% | |||||||

| 4,553 | Apache Corp. | 462,130 | |||||

| 3,389 | Devon Energy Corp. | 218,353 | |||||

| 680,483 | |||||||

| Electromedical & Electrotherapeutic Apparatus - 3.37% | |||||||

| 10,645 | Medtronic, Inc. | 479,344 | |||||

| Fire, Marine & Casualty Insurance - 3.60% | |||||||

| 9,611 | Allstate Corp. | 310,531 | |||||

| 10,535 | Progressive Corp. | 201,113 | |||||

| 511,644 | |||||||

| Food & Kindred Products - 2.02% | |||||||

| 8,107 | Campbell Soup Co. | 286,582 | |||||

| Guided Missiles & Space Vehicles & Parts - 2.03% | |||||||

| 3,465 | Lockheed Martin Corp. | 288,357 | |||||

| Hospital & Medical Service Plans - 1.98% | |||||||

| 8,600 | UnitedHealth Group, Inc. | 280,962 | |||||

| Insurance Agents Brokers & Services - 1.51% | |||||||

| 4,940 | MetLife, Inc. | 214,100 | |||||

| National Commercial Banks - 8.89% | |||||||

| 14,569 | Bank of America Corp. | 260,057 | |||||

| 11,584 | JPMorgan Chase & Co. | 518,384 | |||||

| 7,815 | U.S. Bancorp | 202,252 | |||||

| 9,105 | Wells Fargo & Co. | 283,348 | |||||

| 1,264,041 | |||||||

| Oil & Gas Field Machinery & Equipment - 1.87% | |||||||

| 5,691 | Baker Hughes, Inc. | 266,566 | |||||

*See accompanying notes for they are integral part of these financial statements.

| DEAN FUNDS | |||||||

| DEAN LARGE CAP VALUE FUND | |||||||

| SCHEDULE OF INVESTMENTS - continued | |||||||

| March 31, 2010 | |||||||

| Shares | COMMON STOCKS - 98.57% - continued | Value | |||||

| Petroleum Refining - 11.73% | |||||||

| 6,070 | Chevron Corp. | $ | 460,288 | ||||

| 10,749 | ConocoPhillips | 550,026 | |||||

| 6,300 | Exxon Mobil Corp. | 421,974 | |||||

| 4,199 | Murphy Oil Corp. | 235,942 | |||||

| 1,668,230 | |||||||

| Pharmaceutical Preparations - 7.67% | |||||||

| 12,490 | Eli Lilly & Co. | 452,388 | |||||

| 5,311 | Johnson & Johnson | 346,277 | |||||

| 17,030 | Pfizer, Inc. | 292,065 | |||||

| 1,090,730 | |||||||

| Pumps & Pumping Equipment - 3.03% | |||||||

| 8,022 | ITT Corp. | 430,059 | |||||

| Radio & TV Broadcasting & Communications Equipment - 3.32% | |||||||

| 5,147 | L-3 Communications Holdings, Inc. | 471,620 | |||||

| Retail - Drug Stores and Proprietary Stores - 2.21% | |||||||

| 8,579 | CVS Caremark Corp. | 313,648 | |||||

| Retail - Grocery Stores - 2.22% | |||||||

| 12,688 | Safeway, Inc. | 315,424 | |||||

| Services - Advertising Agencies - 2.05% | |||||||

| 7,512 | Omnicom Group, Inc. | 291,541 | |||||

| Services - Computer Integrated Systems Design - 2.82% | |||||||

| 7,368 | Computer Sciences Corp. * | 401,482 | |||||

| Services - Prepackaged Software - 3.27% | |||||||

| 15,900 | Microsoft Corp. | 465,393 | |||||

| Ship & Boat Building & Repairing - 2.46% | |||||||

| 4,527 | General Dynamics Corp. | 349,484 | |||||

| Specialty Cleaning, Polishing and Sanitation Preparations - 2.44% | |||||||

| 5,419 | Clorox Co. | 347,575 | |||||

| State Commercial Banks - 3.75% | |||||||

| 7,633 | Bank of New York Mellon Corp. | 235,707 | |||||

| 5,386 | Northern Trust Corp. | 297,630 | |||||

| 533,337 | |||||||

| Surgical & Medical Instruments & Apparatus - 6.36% | |||||||

| 4,383 | C.R. Bard, Inc. | 379,655 | |||||

| 9,162 | Stryker Corp. | 524,250 | |||||

| 903,905 | |||||||

*See accompanying notes for they are integral part of these financial statements.

| DEAN FUNDS | |||||||

| DEAN LARGE CAP VALUE FUND | |||||||

| SCHEDULE OF INVESTMENTS - continued | |||||||

| March 31, 2010 | |||||||

| Shares | COMMON STOCKS - 98.57% - continued | Value | |||||

| Telephone Communications (No Radiotelephone) - 3.33% | |||||||

| 8,600 | AT&T, Inc. | $ | 222,224 | ||||

| 8,100 | Verizon Communications, Inc. | 251,262 | |||||

| 473,486 | |||||||

| Wholesale - Groceries & Related Products - 1.99% | |||||||

| 9,611 | Sysco Corp. | 283,525 | |||||

| TOTAL COMMON STOCKS (Cost $13,218,423) | 14,014,282 | ||||||

| MONEY MARKET SECURITIES - 1.45% | |||||||

| 206,108 | AIM STIT-STIC Prime Portfolio - Class I, 0.11% (a) | 206,108 | |||||

| TOTAL MONEY MARKET SECURITIES (Cost $206,108) | 206,108 | ||||||

| TOTAL INVESTMENTS (Cost $13,424,531) - 100.02% | $ | 14,220,390 | |||||

| Liabilities in excess of other assets - (0.02)% | (2,677 | ) | |||||

| TOTAL NET ASSETS - 100.00% | $ | 14,217,713 | |||||

| * Non-income producing securities. | |||||||

| (a) Variable rate security; the money market rate shown represents the rate at March 31, 2010. | |||||||

*See accompanying notes for they are integral part of these financial statements.

| DEAN FUNDS | ||||||||

| STATEMENTS OF ASSETS & LIABILITIES | ||||||||

| March 31, 2010 | ||||||||

| Small Cap | Large Cap | |||||||

| Value Fund | Value Fund | |||||||

| ASSETS | ||||||||

| Investment in securities: | ||||||||

| At cost | $ | 16,545,591 | $ | 13,424,531 | ||||

| At value | $ | 18,959,438 | $ | 14,220,390 | ||||

| Receivable for investments sold | 96,904 | - | ||||||

| Dividends receivable | 40,454 | 17,196 | ||||||

| Prepaid expenses | 10,731 | 10,816 | ||||||

| Interest receivable | 9,600 | 15 | ||||||

| Receivable for fund shares sold | 5,275 | - | ||||||

| TOTAL ASSETS | 19,122,402 | 14,248,417 | ||||||

| LIABILITIES | ||||||||

| Payable for investments purchased | 124,683 | - | ||||||

| Payable to Adviser (a) | 4,149 | 5,527 | ||||||

| Payable to Administrator | 7,874 | 6,283 | ||||||

| Payable to trustees & officers | 858 | 857 | ||||||

| Accrued expenses | 19,491 | 18,037 | ||||||

| TOTAL LIABILITIES | 157,055 | 30,704 | ||||||

| NET ASSETS | $ | 18,965,347 | $ | 14,217,713 | ||||

| NET ASSETS CONSIST OF: | ||||||||

| Paid in capital | $ | 21,684,473 | $ | 18,969,429 | ||||

| Accumulated undistributed net investment income | 249,986 | 55,456 | ||||||

| Accumulated net realized gains (losses) from security | ||||||||

| transactions | (5,382,959 | ) | (5,603,031 | ) | ||||

| Net unrealized appreciation (depreciation) on investments | 2,413,847 | 795,859 | ||||||

| NET ASSETS | $ | 18,965,347 | $ | 14,217,713 | ||||

| Shares of beneficial interest outstanding (unlimited | ||||||||

| numbers of shares authorized) | 1,981,584 | 1,437,730 | ||||||

| Net asset value, offering, and redemption price per share | $ | 9.57 | $ | 9.89 | ||||

| (a) See Note 4 in the Notes to the Financial Statements. | ||||||||

*See accompanying notes for they are integral part of these financial statements.

| DEAN FUNDS | ||||||||

| STATEMENTS OF OPERATIONS | ||||||||

| For the fiscal year ended March 31, 2010 | ||||||||

| Small Cap | Large Cap | |||||||

| Value Fund | Value Fund | |||||||

| Investment Income | ||||||||

| Dividend income (Net of foreign tax withheld of $1,212 and $0, respectively) | $ | 434,435 | $ | 286,196 | ||||

| Interest | 37,776 | 240 | ||||||

| Total Income | 472,211 | 286,436 | ||||||

| Expenses | ||||||||

| Investment advisory fees (a) | 153,007 | 124,585 | ||||||

| Administration expenses | 78,462 | 62,167 | ||||||

| Out-of-pocket expenses | 25,769 | 26,380 | ||||||

| Legal expenses | 23,823 | 22,687 | ||||||

| Registration expenses | 14,549 | 14,467 | ||||||

| Audit expenses | 13,501 | 13,501 | ||||||

| Custody expenses | 16,695 | 9,074 | ||||||

| CCO expenses | 8,081 | 8,169 | ||||||

| Trustees expenses | 8,187 | 7,760 | ||||||

| Pricing expenses | 5,216 | 4,779 | ||||||

| Miscellaneous expenses | 2,696 | 2,640 | ||||||

| Insurance expenses | 1,176 | 1,175 | ||||||

| Printing expenses | 918 | 636 | ||||||

| Total Expenses | 352,080 | 298,020 | ||||||

| Fees waived by Adviser (a) | (122,570 | ) | (111,143 | ) | ||||

| Net Expenses | 229,510 | 186,877 | ||||||

| Net Investment Income | 242,701 | 99,559 | ||||||

| Realized & Unrealized Gain (Loss) | ||||||||

| Net realized gains (losses) on security transactions | 1,265,355 | (224,534 | ) | |||||

| Change in unrealized appreciation (depreciation) on investments | 7,231,116 | 5,379,292 | ||||||

| Net realized & unrealized gains (losses) on investments | 8,496,471 | 5,154,758 | ||||||

| Net increase (decrease) in net assets resulting from operations | $ | 8,739,172 | $ | 5,254,317 | ||||

| (a) See Note 4 in the Notes to the Financial Statements. | ||||||||

*See accompanying notes for they are integral part of these financial statements.

| DEAN FUNDS | |||||||||

| STATEMENTS OF CHANGES IN NET ASSETS | |||||||||

| Small Cap Value Fund | |||||||||

| Year | Year | ||||||||

| Ended | Ended | ||||||||

| March 31, | March 31, | ||||||||

| 2010 | 2009 | ||||||||

| Increase (Decrease) in Net Assets from: | |||||||||

| Operations | |||||||||

| Net investment income (loss) | $ | 242,701 | $ | 161,637 | |||||

| Net realized gains (losses) from security transactions | 1,265,355 | (2,745,582 | ) | ||||||

| Change in unrealized appreciation (depreciation) on investments | 7,231,116 | (4,008,360 | ) | ||||||

| Net increase (decrease) in net assets from operations | 8,739,172 | (6,592,305 | ) | ||||||

| Distributions | |||||||||

| From net investment income | (161,826 | ) | (172,855 | ) | |||||

| From capital gains | - | (40,651 | ) | ||||||

| Decrease in net assets from distributions to shareholders | (161,826 | ) | (213,506 | ) | |||||

| Capital Share Transactions | |||||||||

| Proceeds from shares sold | 986,097 | 1,765,715 | |||||||

| Reinvestment of distributions | 159,822 | 209,704 | |||||||

| Amounts paid for shares redeemed | (319,340 | ) | (750,029 | ) | |||||

| Net increase (decrease) in net assets from capital share transactions | 826,579 | 1,225,390 | |||||||

| Total Increase (Decrease) in Net Assets | 9,403,925 | (5,580,421 | ) | ||||||

| Net Assets | |||||||||

| Beginning of year | 9,561,422 | 15,141,843 | |||||||

| End of year | $ | 18,965,347 | $ | 9,561,422 | |||||

| Accumulated undistributed net investment income included in net assets | $ | 249,986 | $ | 161,867 | |||||

| Capital Share Transactions | |||||||||

| Shares sold | 123,453 | 214,280 | |||||||

| Shares issued in reinvestment of distributions | 17,917 | 36,281 | |||||||

| Shares redeemed | (41,622 | ) | (89,928 | ) | |||||

| Net increase (decrease) in shares outstanding | 99,748 | 160,633 | |||||||

*See accompanying notes for they are integral part of these financial statements.

| DEAN FUNDS | ||||||||

| STATEMENTS OF CHANGES IN NET ASSETS - continued | ||||||||

| Large Cap Value Fund | ||||||||

| Year | Year | |||||||

| Ended | Ended | |||||||

| March 31, | March 31, | |||||||

| 2010 | 2009 | |||||||

| Increase (Decrease) in Net Assets from: | ||||||||

| Operations | ||||||||

| Net investment income (loss) | $ | 99,559 | $ | 211,271 | ||||

| Net realized gains (losses) from security transactions | (224,534 | ) | (3,883,676 | ) | ||||

| Change in unrealized appreciation (depreciation) on investments | 5,379,292 | (2,124,415 | ) | |||||

| Net increase (decrease) in net assets resulting from operations | 5,254,317 | (5,796,820 | ) | |||||

| Distributions | ||||||||

| From net investment income | (128,145 | ) | (193,326 | ) | ||||

| Decrease in net assets from distributions to shareholders | (128,145 | ) | (193,326 | ) | ||||

| Capital Share Transactions | ||||||||

| Proceeds from shares sold | 265,249 | 1,314,973 | ||||||

| Reinvestment of distributions | 121,983 | 183,005 | ||||||

| Amounts paid for shares redeemed | (395,251 | ) | (590,041 | ) | ||||

| Net increase (decrease) in net assets from capital share transactions | (8,019 | ) | 907,937 | |||||

| Total Increase (Decrease) in Net Assets | 5,118,153 | (5,082,209 | ) | |||||

| Net Assets | ||||||||

| Beginning of year | 9,099,560 | 14,181,769 | ||||||

| End of year | $ | 14,217,713 | $ | 9,099,560 | ||||

| Accumulated undistributed net investment income included in net assets | $ | 55,456 | $ | 84,042 | ||||

| Capital Share Transactions | ||||||||

| Shares sold | 32,049 | 142,743 | ||||||

| Shares issued in reinvestment of distributions | 12,813 | 25,069 | ||||||

| Shares redeemed | (45,869 | ) | (60,931 | ) | ||||

| Net increase (decrease) in shares outstanding | (1,007 | ) | 106,881 | |||||

*See accompanying notes for they are integral part of these financial statements.

| SMALL CAP VALUE FUND | ||||||||||||||||||||||||

| FINANCIAL HIGHLIGHTS | ||||||||||||||||||||||||

| Per Share Data for a Share Outstanding Throughout Each Period | ||||||||||||||||||||||||

| For the Years ended | ||||||||||||||||||||||||

| March 31, | March 31, | March 31, | March 31, | March 31, | ||||||||||||||||||||

| 2010 | 2009 | 2008 | 2007 | 2006 | ||||||||||||||||||||

| Net asset value, beginning of year | $ | 5.08 | $ | 8.80 | $ | 15.71 | $ | 16.01 | $ | 14.33 | ||||||||||||||

| Income (loss) from investment operations: | ||||||||||||||||||||||||

| Net investment income (loss) | 0.12 | 0.08 | 0.10 | (0.07 | ) | (0.11 | ) | |||||||||||||||||

| Net realized and unrealized gains (losses) | ||||||||||||||||||||||||

| on investments | 4.45 | (3.68 | ) | (3.17 | ) | 0.53 | 2.64 | |||||||||||||||||

| Total income (loss) from investment operations | 4.57 | (3.60 | ) | (3.07 | ) | 0.46 | 2.53 | |||||||||||||||||

| Less distributions: | ||||||||||||||||||||||||

| From net investment income | (0.08 | ) | (0.10 | ) | (0.01 | ) | - | - | ||||||||||||||||

| From net realized gains | - | (0.02 | ) | (3.83 | ) | (0.76 | ) | (0.85 | ) | |||||||||||||||

| Total distributions | (0.08 | ) | (0.12 | ) | (3.84 | ) | (0.76 | ) | (0.85 | ) | ||||||||||||||

| Net asset value, end of year | $ | 9.57 | $ | 5.08 | $ | 8.80 | $ | 15.71 | $ | 16.01 | ||||||||||||||

Total Return (a) | 90.14 | % | -41.11 | % | -21.57 | % | (b) | 2.95 | % | (b) | 18.22 | % | (b) | |||||||||||

| Ratios and Supplemental Data | ||||||||||||||||||||||||

| Net assets, end of year | $ | 18,965,347 | $ | 9,561,422 | $ | 15,141,843 | $ | 20,890,814 | $ | 19,007,165 | ||||||||||||||

| Ratio of expenses to average net assets: | ||||||||||||||||||||||||

| After fee waivers and/or expense | ||||||||||||||||||||||||

| reimbursement by Adviser | ||||||||||||||||||||||||

| and Administrator | 1.50 | % | 1.50 | % | (d) | 1.50 | % | 1.83 | % | 1.85 | % | |||||||||||||

| Before fee waivers and/or expense | ||||||||||||||||||||||||

| reimbursement by Adviser | ||||||||||||||||||||||||

| and Administrator | 2.30 | % | 2.42 | % | 2.14 | % | 2.16 | % | 2.15 | % | ||||||||||||||

| Ratio of net investment income (loss) to average net assets: | ||||||||||||||||||||||||

| After fee waivers and/or expense | ||||||||||||||||||||||||

| reimbursement by Adviser | ||||||||||||||||||||||||

| and Administrator | 1.58 | % | 1.22 | % | (d) | 0.77 | % | (0.45 | )% | (0.75 | )% | |||||||||||||

| Before fee waivers and/or expense | ||||||||||||||||||||||||

| reimbursement by Adviser | ||||||||||||||||||||||||

| and Administrator | 0.78 | % | 0.30 | % | 0.13 | % | (0.78 | )% | (c) | |||||||||||||||

| Portfolio turnover rate | 165 | % | 141 | % | 85 | % | 149 | % | 48 | % | ||||||||||||||

| (a) Total return represents the rate that the investor would have earned or lost on an investment in the Fund, assuming reinvestment of dividends. | ||||||||||||||||||||||||

| (b) Total returns shown exclude the effect of applicable sales loads. | ||||||||||||||||||||||||

| (c) Ratio not presented prior to March 31, 2007. | ||||||||||||||||||||||||

| (d) A portion of the waiver was related to 12b-1 expenses voluntarily waived by the Adviser, equal to 0.19% of average net assets. | ||||||||||||||||||||||||

*See accompanying notes for they are integral part of these financial statements.

| DEAN FUNDS | ||||||||||||||||||||||||

| LARGE CAP VALUE FUND | ||||||||||||||||||||||||

| FINANCIAL HIGHLIGHTS (Continued) | ||||||||||||||||||||||||

| Per Share Data for a Share Outstanding Throughout Each Period | ||||||||||||||||||||||||

| For the Years ended | ||||||||||||||||||||||||

| March 31, | March 31, | March 31, | March 31, | March 31, | ||||||||||||||||||||

| 2010 | 2009 | 2008 | 2007 | 2006 | ||||||||||||||||||||

| Net asset value, beginning of year | $ | 6.32 | $ | 10.65 | $ | 12.52 | $ | 11.40 | $ | 10.18 | ||||||||||||||

| Income (loss) from investment operations: | ||||||||||||||||||||||||

| Net investment income (loss) | 0.07 | 0.15 | 0.18 | (0.01 | ) | (0.01 | ) | |||||||||||||||||

| Net realized and unrealized gains (losses) | ||||||||||||||||||||||||

| on investments | 3.59 | (4.34 | ) | (1.92 | ) | 1.13 | 1.23 | |||||||||||||||||

| Total income (loss) from investment operations | 3.66 | (4.19 | ) | (1.74 | ) | 1.12 | 1.22 | |||||||||||||||||

| Less distributions: | ||||||||||||||||||||||||

| From net investment income | (0.09 | ) | (0.14 | ) | (0.13 | ) | - | - | ||||||||||||||||

| Total distributions | (0.09 | ) | (0.14 | ) | (0.13 | ) | - | - | ||||||||||||||||

| Net asset value, end of year | $ | 9.89 | $ | 6.32 | $ | 10.65 | $ | 12.52 | $ | 11.40 | ||||||||||||||

Total Return (a) | 57.97 | % | -39.52 | % | -14.02 | % | (b) | 9.85 | % | (b) | 11.98 | % | (b) | |||||||||||

| Ratios and Supplemental Data | ||||||||||||||||||||||||

| Net assets, end of year | $ | 14,217,713 | $ | 9,099,560 | $ | 14,181,769 | $ | 16,875,525 | $ | 8,167,690 | ||||||||||||||

| Ratio of expenses to average net assets: | ||||||||||||||||||||||||

| After fee waivers and/or expense | ||||||||||||||||||||||||

| reimbursement by Adviser | ||||||||||||||||||||||||

| and Administrator | 1.50 | % | 1.50 | % | (d) | 1.50 | % | 1.85 | % | 1.85 | % | |||||||||||||

| Before fee waivers and/or expense | ||||||||||||||||||||||||

| reimbursement by Adviser | ||||||||||||||||||||||||

| and Administrator | 2.39 | % | 2.47 | % | 2.23 | % | 2.44 | % | 2.73 | % | ||||||||||||||

| Ratio of net investment income (loss) to average net assets: | ||||||||||||||||||||||||

| After fee waivers and/or expense | ||||||||||||||||||||||||

| reimbursement by Adviser | ||||||||||||||||||||||||

| and Administrator | 0.80 | % | 1.73 | % | (d) | 1.46 | % | (0.69 | )% | (0.07 | )% | |||||||||||||

| Before fee waivers and/or expense | ||||||||||||||||||||||||

| reimbursement by Adviser | ||||||||||||||||||||||||

| and Administrator | (0.09 | )% | 0.76 | % | 0.73 | % | (0.10 | )% | (c) | |||||||||||||||

| Portfolio turnover rate | 62 | % | 77 | % | 24 | % | 124 | % | 62 | % | ||||||||||||||

| (a) Total return represents the rate that the investor would have earned or lost on an investment in the Fund, assuming reinvestment of dividends. | ||||||||||||||||||||||||

| (b) Total returns shown exclude the effect of applicable sales loads. | ||||||||||||||||||||||||

| (c) Ratio not presented prior to March 31, 2007. | ||||||||||||||||||||||||

| (d) A portion of the waiver was related to 12b-1 expenses voluntarily waived by the Adviser, equal to 0.19% of average net assets. | ||||||||||||||||||||||||

*See accompanying notes for they are integral part of these financial statements.

DEAN FUNDS

NOTES TO THE FINANCIAL STATEMENTS

March 31, 2010

NOTE 1. Organization

The Dean Small Cap Value Fund (the “Small Cap Fund”) and the Dean Large Cap Value Fund (the “Large Cap Fund”) (each a “Fund” and, collectively the “Funds”) were organized as diversified series of Unified Series Trust (the “Trust”) on November 13, 2006. The Trust is an open-end investment company established under the laws of Ohio by an Agreement and Declaration of Trust dated October 17, 2002 (the “Trust Agreement”).

The Small Cap Fund acquired all of the assets and liabilities of the Dean Small Cap Value Fund, a series of Dean Family of Funds, and Class A shares of the acquired funds were exchanged for shares of the identically named Fund. In the same reorganization, the Large Cap Fund acquired all of the assets and liabilities of each of the Dean Large Cap Value Fund and the Dean Balanced Fund, each a series of the Dean Family of Funds (each “Predecessor Fund”, collectively, “Predecessor Funds”), in a tax-free reorganization at the close of business on March 30, 2007. In connection with this acquisition, Class A shares of the acquired funds were exchanged for shares of the Large Cap Value Fund. The Small Cap Fund’s and Large Cap Fund’s predecessor each commenced operations on May 28, 1997. For the periods prior to March 31, 2007, the financial highlight information included herein or incorporated by reference into these Financial Statements, is that of the predecessor Dean Small Cap Value and Dean Large Cap Value Class A shares. Prior to October 28, 2006, each of the Funds’ Predecessors offered Class C shares for purchase. On October 27, 2006, the Class C shares of each Predecessor Fund were reclassified to the Class A shares of each respective Predecessor Fund.

The Trust Agreement permits the Trustees to issue an unlimited number of shares of beneficial interest of separate series. The Funds are series of funds currently authorized by the Trustees. The investment adviser to each Fund is Dean Investment Associates, LLC (“Dean Investment Associates” or “Adviser”). In addition, the Adviser has retained Dean Capital Management, LLC (“DCM” or “Sub-Adviser”) to serve as sub-adviser to the Funds. DCM is an affiliate of the Adviser. The investment objective of the Small Cap Fund and the Large Cap Fund is long-term capital appreciation and, secondarily, dividend income.

NOTE 2. Significant Accounting Policies

The following is a summary of significant accounting policies followed by the Funds in the preparation of their financial statements.

Securities Valuation – All investments in securities are recorded at their estimated fair value as described in Note 3.

Federal Income Taxes – The Funds make no provision for federal income or excise tax. The Funds intend to qualify each year as regulated investment companies (“RICs”) under subchapter M of the Internal Revenue Code of 1986, as amended, by complying with the requirements applicable to RICs and by distributing substantially all of their taxable income. The Funds also intend to distribute sufficient net investment income and net capital gains, if any, so that they will not be subject to excise tax on undistributed income and gains. If the required amount of net investment income or gains is not distributed, the Funds could incur a tax expense.

As of and during the fiscal year ended March 31, 2010, the Funds did not have a liability for any unrecognized tax benefits. The Funds recognize interest and penalties, if any, related to unrecognized tax benefits as income tax expense in the statement of operations. During the year, the Funds did not incur any interest or penalties. The Funds are not subject to examination by U.S. federal tax authorities for tax years prior to 2006.

Expenses – Expenses incurred by the Trust that do not relate to a specific fund of the Trust are allocated to the individual funds based on each fund’s relative net assets or another appropriate basis (as determined by the Board).

Security Transactions and Related Income - The Funds follow industry practice and record security transactions on the trade date. The specific identification method is used for determining gains or losses for financial statements and income tax purposes. Dividend income is recorded on the ex-dividend date and interest income is recorded on an accrual basis. Discounts and premiums on securities purchased are amortized or accreted using the effective interest method. Distributions received from investments in real estate investment trusts (“REITS”) that represent a return of capital or capital gain are recorded as a reduction of the cost of investment or as a realized gain, respectively. The calendar year-end amounts of ordinary income, capital gains, and return of capital included in distributions received from the Funds’ investments in REITS are reported to the Funds after the end of the calendar year; accordingly, the Funds estimate these amounts for accounting purposes until the characterization of REIT distributions is reported to the Funds after the end of the calendar year.

DEAN FUNDS

NOTES TO THE FINANCIAL STATEMENTS

March 31, 2010

NOTE 2. Significant Accounting Policies - continued

Estimates are based on the most recent REIT distributions information available. Distributions received from investments in publicly traded partnerships are recorded as a reduction of the cost of the investment. Withholding taxes on foreign dividends and related reclaims have been provided for in accordance with the Funds’ understanding of the applicable country’s tax rules and rates. The ability of issuers of debt securities held by the Funds to meet their obligations may be affected by economic and political developments in a specific country or region. For bonds that miss a scheduled interest payment, after the grace period, all interest accrued on the bond is written off and no additional interest will be accrued. However, for illiquid or fair valued bonds, if the Adviser’s research indicates a high recovery rate in restructuring, and the Funds expect to hold the bond until the issue is restructured, past due interest may not be written off in its entirety.

Dividends and Distributions - The Funds intend to distribute substantially all of their net investment income as dividends to their shareholders on at least an annual basis. The Funds intend to distribute their net realized long-term capital gains and their net realized short-term capital gains at least once a year. Distributions to shareholders, which are determined in accordance with income tax regulations, are recorded on the ex-dividend date. The treatment for financial reporting purposes of distributions made to shareholders during the year from net investment income or net realized capital gains may differ from their ultimate treatment for federal income tax purposes. These differences are caused primarily by differences in the ti ming of the recognition of certain components of income, expense or realized capital gain for federal income tax purposes. Where such differences are permanent in nature, they are reclassified in the components of the net assets based on their ultimate characterization for federal income tax purposes. Any such reclassifications will have no effect on net assets, results of operations or net asset values per share of the Funds. For the fiscal year ended March 31, 2010, the Small Cap Fund reclassified $5,701 from paid in capital to accumulated net investment income, and reclassified $1,543 from accumulated realized gains to accumulated net investment income, related to the tax treatment of income from certain investments.