Roth 2008 OC Growth Stock

Conference

February 19, 2008

1

1

Safe Harbor Statement

The Private Securities Litigation Reform Act of 1995 provides a safe

harbor for forward-looking information made on the Company's

behalf. All statements, other than statements of historical facts which

address the Company's expectations of sources of capital or which

express the Company's expectation for the future with respect to

financial performance or operating strategies, can be identified as

forward-looking statements. Such statements made by the company

are based on knowledge of the environment in which it operates, but

because of the factors previously listed, as well as other factors

beyond the control of the Company, actual results may differ

materially from the expectations expressed in the forward-looking

statements.

2

2

BooKoo Snapshot

BooKoo energy drinks launched in 2004

Among the leaders in sales and sales per point of distribution

Distributed in parts of the US and Canada

Coca-Cola, Pepsi, Cadbury, beer and others

Recent issues with Tier 1 Coke distribution strategy

Nielsen ACV coverage - 13%

Track record of innovation

Recognized taste leader in category

First 24 oz. can

First and only 5.75 oz. “shot”

Ready to launch the first energy ‘protein’ drink

3

3

In discussions with several larger independent beverage and beer distributors.

Focus on supporting existing distributors with “pull” marketing.

Distribution Partners

Mineral

Nye

4

4

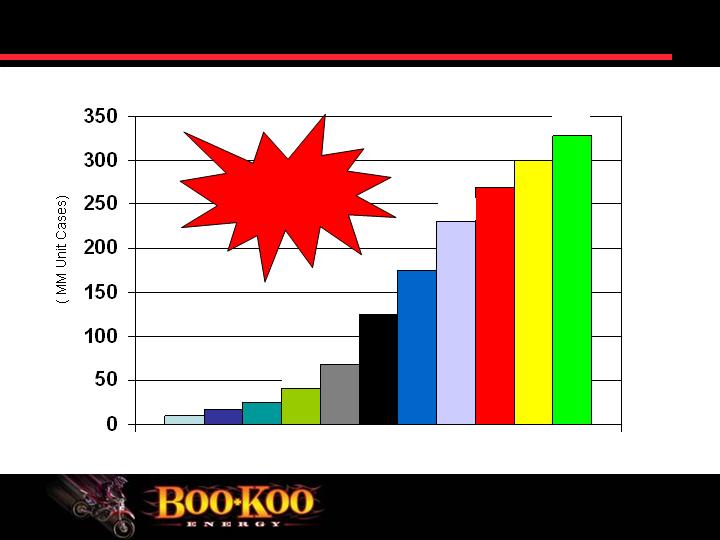

Source: Goldman Sachs Global Investment Research May 2006

2000 2001 2002 2003 2004 2005 2006E 2007E 2008E 2009E 2010E

136%

85%

74%

83%

51%

33%

18%

11%

10%

62%

Double digit volume

increases are expected

thru 2010

Energy Drink Volume and % Volume Change

5

5

AC Nielsen Sales Data

29.3

2,354,969,601

3,045,731,460

TOTAL ENERGY DRINK

Anheuser

9.6

8,858,180

9,712,422

180 R

Hansen

-35.5

17,725,960

11,436,650

LOST R

Rip It

62.5

8,049,648

13,081,042

RIP IT R

Coca-Cola

-48.6

26,093,654

13,414,265

FULL THROTTLE DT

Pepsi

N/A

0

13,895,898

JEFF GORDON 24 ENERGY R

Boo Koo

-7.7

23,070,542

21,286,537

BOO+KOO R

Pepsi

N/A

0

21,543,508

SOBE ESSENTIAL

Pepsi

7.6

37,083,427

39,886,599

SOBE DT

Coca-Cola

200.7

15,482,148

46,561,061

NOS R

Hansen

32.1

41,262,884

54,497,854

MONSTER ASSAULT R

Coca-Cola

56.0

64,332,025

100,354,229

ROCKSTAR DT

Pepsi

-22.9

206,214,831

159,028,839

SOBE R

Coca-Cola

6.1

167,860,499

178,165,668

ROCKSTAR R

Pepsi

43.1

126,679,661

181,286,580

AMP R

Coca-Cola

47.5

142,722,731

210,467,505

FULL THROTTLE R

Red Bull

41.9

152,044,091

215,719,565

RED BULL DT

Hansen

39.5

458,860,158

639,998,470

MONSTER R

Red Bull

36.8

716,206,508

979,674,235

RED BULL R

Affiliation

% Change

Last Year $

Retail Sales $

BRAND

AC Nielsen Total U.S.-CTMM 52 weeks 12-29-07

6

6

Source: AC Nielsen

¹ All Commodity Volume (“ACV”) is a measure of retail distribution that represents the percent of total stores that carry the product

Distribution Opportunity

AC Nielsen Total U.S.-CTMM 52 weeks 12-29-07

Pepsi

243,788

57

13,895,898

JEFF GORDON 24 ENERGY R

Hansen

408,452

28

11,436,650

LOST R

Coca-Cola

462,561

29

13,414,265

FULL THROTTLE DT

Pepsi

512,941

42

21,543,508

SOBE ESSENTIAL

Anheuser

647,495

15

9,712,422

180 R

Pepsi

848,651

47

39,886,599

SOBE DT

Hansen

908,298

60

54,497,854

MONSTER ASSAULT R

Coca-Cola

1,108,597

42

46,561,061

NOS R

Boo Koo

1,637,426

13

21,286,587

BOO+KOO R

Coca-Cola

2,007,085

50

100,354,229

ROCKSTAR DT

Pepsi

2,149,038

74

159,028,839

SOBE R

Rip It

2,180,174

6

13,081,042

RIP IT R

Pepsi

2,266,082

80

181,286,580

AMP R

Coca-Cola

2,440,626

73

178,165,668

ROCKSTAR R

Coca-Cola

2,664,146

79

210,467,505

FULL THROTTLE R

Red Bull

2,696,495

80

215,719,565

RED BULL DT

Hansen

7,190,994

89

639,998,470

MONSTER R

Red Bull

10,648,633

92

979,674,235

RED BULL R

Affiliation

$ Sales per Point of

Distribution

ACV %

Retail Sales $

BRAND

7

7

Milestones in 2007

Consistent pricing structure

Renegotiated vendor/supplier agreements

Improved quality of distributor network

Coca-Cola Consolidated (2nd largest Coke Bottler – NASDAQ:COKE)

Leading Brands of Canada (NASDAQ: LBIX)

Formed strategic partnerships

Circle K

Focus on innovation

Fruit Punch

Burner

Wet Vitamin

Took Company public through a reverse merger in conjunction with

a PIPE

8

8

The Boo Koo Brand Position Hierarchy

For: Older Millennia and

Generation X-ers who have more

mainstream values and

entertainment lifestyles

Boo Koo is: An alternative to the

traditional bad tasting energy

drinks and comes in five great

flavors.

Overall positioning: Boo Koo has

more energy, great taste and

provides better performance when

you need it.

Target/insight : Who the

brand needs to be most

relevant to and they’re

needs

Frame of Reference:

Categorization and

differentiated relative to

the competition

Brand offers unique and

relevant benefits to its

target audience – for

consumers who want to

be their best

9

9

Q1 “Pull” Marketing Campaign

Coke Consolidated and Coke United promotion – 9 markets – 6

week promotion

Raleigh, Charlotte, Birmingham, Nashville, plus 5 more markets

Consumer have a chance to win up to $1m – many other prizes

Promoted through local radio stations and retailers

“Large Crowd” events – basketball games, concerts, etc.

Trial/volume generating program

Sampling teams will be in place to sample product

In store POS tie in

Start date February 4, ends in mid-March

10

10

Continuing Innovation

Burner

Energy + Protein

First in class hybrid

20 grams of Whey Protein per

Bottle

2 grams of Carbs per Bottle

Sugar Free

With Taurine, Ginseng and B

Vitamins

3 Flavors

‘Charger’

2 oz Energy Supplement

Hot category

Alternative distribution

11

11

New Products

Custom Packaging

Retail Specific

New Benefits

Expanded Offering

New Distribution

Marketing

Innovation

Sampling

Market Research

Chain authorizations:

Pantry

Circle K

Growth Opportunities

12

12

Natural and organic search

engine optimization (SEO)

On-line promotions

Viral videos

User-friendly, interactive website

Viral Marketing

13

13

Seasoned Management Team and Board

14

14

Name

Position

Experience

Years

Steve Solomon

Executive Chairman

• Citadel Security Software

20+

• CT Holdings,Inc.

• Parago, Inc.

Steve Ruffini

COO/CFO

• Hit Entertainment

25+

- Sold to Apax for $1.4B

• Big Four Public Accounting

Chuck Jarvie

Director

• Procter & Gamble

40+

• Dr. Pepper

• Guiness America

Jim Carreker

Director

• Wyndham Hotels & Resorts

35+

• Trammell Crow Company

• Bombay Company

Ken Johnsen

Director

• HG Food

30+

• Parago, Inc.

• IBM

Steve Johnson

Director

• Aspen Advisors, LP

30+

• Gibson, Dunn & Crutcher

2007 Revenue down roughly 40% from 2006

$11.3 million private placement in August/September 2007

Business model has significant operating leverage

Potential to significantly grow sales through independent distributor

network

Financial Information

15

15

Participation in the large and fast-growing Energy Drink category.

Change in distribution strategy from Coca Cola to independent and beer

distributors.

Seasoned Management and Board with significant experience in

beverages and consumer products.

Increased emphasis on “pull marketing” to support brand at retail.

Line extensions and innovation.

Burner Launch in Q2.

Summary

16

16