Exhibit 99.2

Supplemental Operating and Financial Data

For the Quarter Ended

March 31, 2011

MPG Office Trust, Inc.

Supplemental Operating and Financial Data

First Quarter 2011

| Table of Contents | ||||

| PAGE | ||

| Corporate Data | ||

| Forward-Looking Statements | ||

| Quarterly Highlights | ||

| Investor Information | ||

| Common Stock Data | ||

| Consolidated Financial Results | ||

| Financial Highlights | ||

| Consolidated Balance Sheets | ||

| MMO Unconsolidated Joint Venture Condensed Balance Sheets | ||

| Consolidated Statements of Operations | ||

| Consolidated Statements of Discontinued Operations | ||

| Consolidated Statements of Operations Related to Properties in Default | ||

| MMO Unconsolidated Joint Venture Statements of Operations | ||

| Funds from Operations | ||

| Adjusted Funds from Operations | ||

| Adjusted Funds from Operations Related to Properties in Default | ||

| Reconciliation of Earnings before Interest, Taxes and Depreciation and Amortization and Adjusted Funds From Operations | ||

| Capital Structure | ||

| Debt Summary | ||

| MMO Joint Venture Debt Summary | ||

| Debt Maturities | ||

| MMO Joint Venture Debt Maturities | ||

| Portfolio Data | ||

| Same Store Analysis | ||

| Portfolio Overview | ||

| Portfolio Geographic Distribution (Excluding Properties in Default) | ||

| Portfolio Overview — Leased Percentages and Weighted Average Remaining Lease Term | ||

| Major Tenants — Office Properties (Excluding Properties in Default) | ||

| Portfolio Tenant Classification Description (Excluding Properties in Default) | ||

| Lease Expirations — Wholly Owned Portfolio | ||

| Lease Expirations — Wholly Owned Portfolio (Los Angeles County) | ||

| Lease Expirations — Wholly Owned Portfolio (Orange County) | ||

| Lease Expirations — Properties in Default | ||

| Lease Expirations — MMO Joint Venture Portfolio | ||

| Leasing Activity — Total Portfolio | ||

| Leasing Activity — Los Angeles Central Business District | ||

| Leasing Activity — Orange County | ||

| Tenant Improvements and Leasing Commissions (Excluding Properties in Default) | ||

| Historical Capital Expenditures — Office Properties | ||

| Hotel Performance and Hotel Historical Capital Expenditures | ||

| Development Properties | ||

| Management Statements on Non-GAAP Supplemental Measures | ||

| Corporate Data | ||||

1

| Forward-Looking Statements | ||||

This supplemental package contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. We caution investors that any forward-looking statements presented herein are based on management’s beliefs and assumptions and information currently available to management. Such statements are subject to risks, uncertainties and assumptions and may be affected by known and unknown risks, trends, uncertainties and factors that are beyond our control. Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those anticipated, estimated or projected. These factors include, without limitation: risks associated with our ability to dispose of properties, if and when we decide to do so, at prices or terms set by or acceptable to us; risks associated with the timing and consequences of loan defaults and related asset dispositions; risks associated with our loan modification efforts; risks associated with our liquidity situation; risks associated with our dependence on key personnel whose continued service is not guaranteed; risks associated with the continued or increased negative impact of the current credit crisis and global economic slowdown; risks associated with contingent guaranties by our Operating Partnership; general risks affecting the real estate industry (including, without limitation, the inability to enter into or renew leases at favorable rates, dependence on tenants’ financial condition, and competition from other developers, owners and operators of real estate); risks associated with the availability and terms of financing; risks associated with increases in interest rates, volatility in the securities markets and contraction in the credit markets affecting our ability to extend or refinance existing loans as they come due; risks associated with management’s focus on asset dispositions, loan defaults, cash generation and general strategic matters; risks associated with joint ventures; potential liability for uninsured losses and environmental contamination; and risks associated with our potential failure to qualify as a REIT under the Internal Revenue Code of 1986, as amended, and possible adverse changes in tax and environmental laws.

For a further list and description of such risks and uncertainties, see our Annual Report on Form 10-K filed on March 16, 2011 with the Securities and Exchange Commission. We do not update forward-looking statements and disclaim any intention or obligation to update or revise them, whether as a result of new information, future events or otherwise.

2

| Quarterly Highlights | ||||

MPG Office Trust, Inc. (the “Company”), a self-administered and self-managed real estate investment trust, is the largest owner and operator of Class A office properties in the Los Angeles central business district and is primarily focused on owning and operating high-quality office properties in the Southern California market. We are a full-service real estate company with substantial in-house expertise and resources in property management, marketing, leasing and financing.

As of March 31, 2011, our office portfolio (including Properties in Default) was comprised of whole or partial interests in 24 properties totaling approximately 15 million net rentable square feet, one 350-room hotel with 266,000 square feet, and on- and off-site structured parking plus surface parking totaling approximately 9 million square feet, which accommodates approximately 27,000 vehicles.

As used in this Supplemental Operating and Financial Data package, the term “Properties in Default” refers to our Stadium Towers Plaza, 2600 Michelson, 550 South Hope, 500 Orange Tower and City Tower properties, whose mortgage loans were in default as of March 31, 2011. We disposed of Park Place II (in third quarter 2010), and 207 Goode and Pacific Arts Plaza (both in fourth quarter 2010), which were previously classified as part of Properties in Default. The results of operations of Park Place II, 207 Goode and Pacific Arts Plaza are now included in discontinued operations for all periods presented.

In addition to the mortgage loans secured by the Properties in Default, the mortgage loan secured by Two California Plaza is also in default as of March 31, 2011. We have excluded Two California Plaza from the Properties in Default because our goal is to modify the loan with the special servicer rather than to dispose of the asset. We cannot assure you that we will be successful in modifying the loan, which may ultimately result in our inability to retain ownership of Two California Plaza.

This Supplemental Operating and Financial Data package should be read in conjunction with our consolidated financial statements for the year ended December 31, 2010 in our Annual Report on Form 10-K filed with the Securities and Exchange Commission (“SEC”) on March 16, 2011. For more information on MPG Office Trust, visit our website at www.mpgoffice.com.

3

| Quarterly Highlights (continued) | ||||

Asset Disposition: On January 27, 2011, we disposed of the 500 Orange Center development site located in Orange, California. We received proceeds from this transaction of $4.7 million, net of transaction costs. Debt: Following notices from us, the mortgage loans encumbering 700 North Central and 801 North Brand were transferred to special servicing in March 2011. The mortgage loans secured by these assets are not in default. Following notices from us, the mortgage loans encumbering U.S. Bank Tower and Wells Fargo Tower were transferred to special servicing in March 2011. This step permits us to engage in discussions with the respective special servicers. We also delivered a notice of imminent default in March 2011 to the master servicer for the mortgage loan on Gas Company Tower requesting it be placed into special servicing (which has not yet occurred). The mortgage loans secured by these assets are not in default. Following a notice from us, the mortgage loan encumbering Two California Plaza was transferred to special servicing. Subsequently in March 2011, our special purpose property-owning subsidiary that owns Two California Plaza defaulted on the mortgage loan. | Subsequent Events: On April 1, 2011, we completed the disposition of 701 North Brand located in Glendale, California to the property’s lender. As a result of the disposition, we were relieved of the obligation to repay the $33.8 million mortgage loan secured by the property and received cash consideration. On April 26, 2011, we disposed of 550 South Hope located in Los Angeles, California in cooperation with the special servicer on the mortgage loan. As a result of the disposition, we were relieved of the obligation to repay the $200.0 million mortgage loan secured by the property as well as contractual and default interest. On May 1, 2011, we extended our $109.0 million mortgage loan secured by Brea Corporate Place and Brea Financial Commons. The final maturity date of this loan is May 1, 2012, and there are no remaining extension options. No cash paydown was made to extend the loan, and the loan terms remain unchanged. On May 1, 2011, we repaid our $15.0 million unsecured term loan upon maturity using cash on hand. | |

4

| Investor Information | ||||

355 South Grand Avenue, Suite 3300

Los Angeles, CA 90071

Tel. (213) 626-3300

Fax (213) 687-4758

| Senior Management | |||

| David L. Weinstein | President and Chief Executive Officer | Jonathan L. Abrams | Senior Vice President, General Counsel and Secretary |

| Shant Koumriqian | Executive Vice President, Chief Financial Officer | Peter K. Johnston | Senior Vice President, Leasing |

| Peggy M. Moretti | Executive Vice President, Investor and Public Relations | Christopher M. Norton | Senior Vice President, Transactions |

| & Chief Administrative Officer | |||

| Corporate | |||

| Investor Relations Contact: Peggy M. Moretti at (213) 613-4558 | |||

Please visit our corporate website at: www.mpgoffice.com | |||

| Transfer Agent | Timing | ||

American Stock Transfer & Trust Company 59 Maiden Lane New York, NY 10038 (866) 668-6550 www.amstock.com | Quarterly results for 2011 will be announced according to the following schedule: | ||

| Second Quarter | August 2011 | ||

| Third Quarter | October 2011 | ||

| Fourth Quarter | February 2012 | ||

| Equity Research Coverage | |||

| Credit Suisse | Andrew Rosivach | (415) 249-7942 | |

| Deutsche Bank Securities, Inc. | Vincent Chao | (212) 250-6799 | |

| Goldman Sachs & Co. | Jay Haberman | (917) 343-4260 | |

| Green Street Advisors | Michael Knott | (949) 640-8780 | |

| KeyBanc Capital Markets | Jordan Sadler | (917) 368-2280 | |

| Raymond James Associates | Paul Puryear | (727) 567-2253 | |

| RBC Capital Markets | Dave Rodgers | (440) 715-2647 | |

| Robert W. Baird & Company | David Aubuchon | (314) 863-4235 | |

| Stifel, Nicolaus & Co., Inc. | John Guinee | (443) 224-1307 | |

MPG Office Trust, Inc. is currently followed by the sell-side analysts listed above, with the exception of Green Street Advisors, which is an independent research firm. This list may not be complete and is subject to change as firms add or delete coverage of our company. Please note that any opinions, estimates or forecasts regarding our historical or predicted performance made by these analysts are theirs alone and do not represent opinions, forecasts or predictions of MPG Office Trust, Inc. or its management. We are providing this listing as a service to our stockholders and do not by listing these firms imply our endorsement of or concurrence with such information, conclusions or recommendations. Interested persons may obtain copies of analysts' reports on their own; we do not distribute these reports. Various of these firms may from time-to-time own our stock and/or hold other long or short positions in our stock, and may provide compensated services to us.

5

| Common Stock Data | ||||

Our common stock is traded on the New York Stock Exchange under the symbol MPG. Selected information about our common stock for the past five quarters (based on NYSE prices) is as follows:

| 2011 | 2010 | ||||||||||||||||||

| 1st Quarter | 4th Quarter | 3rd Quarter | 2nd Quarter | 1st Quarter | |||||||||||||||

| High price | $ | 4.28 | $ | 3.08 | $ | 3.47 | $ | 4.60 | $ | 3.98 | |||||||||

| Low price | $ | 2.76 | $ | 1.98 | $ | 2.25 | $ | 2.38 | $ | 1.41 | |||||||||

| Closing price | $ | 3.71 | $ | 2.75 | $ | 2.50 | $ | 2.93 | $ | 3.08 | |||||||||

| Dividends per share – annualized | (1 | ) | (1 | ) | (1 | ) | (1 | ) | (1 | ) | |||||||||

| Closing dividend yield – annualized | (1 | ) | (1 | ) | (1 | ) | (1 | ) | (1 | ) | |||||||||

| Closing common shares and Operating Partnership units outstanding (in thousands) | 55,491 | 55,372 | 54,735 | 54,686 | 54,692 | ||||||||||||||

| Closing market value of common shares and Operating Partnership units outstanding (in thousands) | $ | 205,872 | $ | 152,274 | $ | 136,837 | $ | 160,229 | $ | 168,451 | |||||||||

| Dividend Information: | |||||||||||||||||||

| Common Stock | |||||||||||||||||||

| Dividend amount per share | (1 | ) | (1 | ) | (1 | ) | (1 | ) | (1 | ) | |||||||||

| Series A Preferred Stock | |||||||||||||||||||

| Dividend amount per share | (2 | ) | (2 | ) | (2 | ) | (2 | ) | (2 | ) | |||||||||

__________

| (1) | The Board of Directors did not declare a dividend on our common stock for the quarters ended March 31, 2011 and December 31, September 30, June 30 and March 31, 2010. There can be no assurance that we will make distributions on our common stock at historical levels or at all. |

| (2) | The Board of Directors did not declare a dividend on our Series A Preferred Stock during the three months ended April 30 and January 31, 2011 and October 31, July 31 and April 30, 2010. Dividends on our Series A Preferred Stock are cumulative, and therefore, will continue to accrue at an annual rate of $1.9064 per share. As of April 30, 2011, we have missed ten quarterly dividend payments totaling $47.7 million. |

6

| Consolidated Financial Results | ||||

7

Financial Highlights (unaudited and in thousands, except share, per share, percentage and ratio amounts) | ||||

| For the Three Months Ended | |||||||||||||||||||

| March 31, 2011 | December 31, 2010 | September 30, 2010 | June 30, 2010 | March 31, 2010 | |||||||||||||||

| Income Items: | |||||||||||||||||||

| Revenue (1) | $ | 95,854 | $ | 101,328 | $ | 101,913 | $ | 100,521 | $ | 103,134 | |||||||||

| Straight line rent | 460 | 1,092 | (43 | ) | 778 | 551 | |||||||||||||

| Fair value lease revenue (2) | 3,446 | 3,920 | 5,942 | 3,773 | 4,046 | ||||||||||||||

| Lease termination fees | 27 | — | 2,398 | — | 18 | ||||||||||||||

| Office property operating margin (3) | 63.1 | % | 61.6 | % | 62.9 | % | 64.5 | % | 65.6 | % | |||||||||

| Net (loss) income available to common stockholders | $ | (39,548 | ) | $ | (138,275 | ) | $ | (17,860 | ) | $ | (53,521 | ) | $ | 18,580 | |||||

| Net (loss) income available to common stockholders – basic | (0.81 | ) | (2.82 | ) | (0.36 | ) | (1.10 | ) | 0.38 | ||||||||||

| Funds from operations (FFO) available to common stockholders (4) | $ | (13,490 | ) | $ | (103,726 | ) | $ | (2,440 | ) | $ | (25,215 | ) | $ | 35,552 | |||||

| FFO per share – basic (4) | (0.28 | ) | (2.12 | ) | (0.05 | ) | (0.52 | ) | 0.73 | ||||||||||

| FFO per share – diluted (4) | (0.28 | ) | (2.12 | ) | (0.05 | ) | (0.52 | ) | 0.72 | ||||||||||

| FFO per share before specified items – basic (4) | (0.06 | ) | 0.02 | — | (0.01 | ) | 0.05 | ||||||||||||

| FFO per share before specified items – diluted (4) | (0.06 | ) | 0.02 | — | (0.01 | ) | 0.05 | ||||||||||||

| Ratios: | |||||||||||||||||||

| Interest coverage ratio (5) | 1.04 | (0.78 | ) | 1.52 | 0.78 | 2.20 | |||||||||||||

| Interest coverage ratio before specified items (6) | 1.04 | 1.14 | 1.13 | 1.08 | 1.13 | ||||||||||||||

| Fixed-charge coverage ratio (7) | 0.93 | (0.71 | ) | 1.38 | 0.71 | 2.00 | |||||||||||||

| Fixed-charge coverage ratio before specified items (8) | 0.93 | 1.03 | 1.03 | 0.98 | 1.02 | ||||||||||||||

| Capitalization: | |||||||||||||||||||

| Common stock price @ quarter end | $ | 3.71 | $ | 2.75 | $ | 2.50 | $ | 2.93 | $ | 3.08 | |||||||||

| Total consolidated debt | $ | 3,578,627 | $ | 3,576,493 | $ | 3,894,266 | $ | 3,992,724 | $ | 4,035,451 | |||||||||

| Preferred stock liquidation preference | 250,000 | 250,000 | 250,000 | 250,000 | 250,000 | ||||||||||||||

| Common equity value @ quarter end (9) | 205,872 | 152,274 | 136,837 | 160,229 | 168,451 | ||||||||||||||

| Total consolidated market capitalization | $ | 4,034,499 | $ | 3,978,767 | $ | 4,281,103 | $ | 4,402,953 | $ | 4,453,902 | |||||||||

| Company share of MMO joint venture debt | 138,842 | 138,993 | 160,355 | 160,510 | 160,663 | ||||||||||||||

| Total combined market capitalization | $ | 4,173,341 | $ | 4,117,760 | $ | 4,441,458 | $ | 4,563,463 | $ | 4,614,565 | |||||||||

| Total consolidated debt / total consolidated market capitalization | 88.7 | % | 89.9 | % | 91.0 | % | 90.7 | % | 90.6 | % | |||||||||

| Total combined debt / total combined market capitalization | 89.1 | % | 90.2 | % | 91.3 | % | 91.0 | % | 90.9 | % | |||||||||

| Total consolidated debt plus liquidation preference / total consolidated market capitalization | 94.9 | % | 96.2 | % | 96.8 | % | 96.4 | % | 96.2 | % | |||||||||

| Total combined debt plus liquidation preference / total combined market capitalization | 95.1 | % | 96.3 | % | 96.9 | % | 96.5 | % | 96.3 | % | |||||||||

8

| Financial Highlights (continued) | ||||

__________

| (1) | Excludes revenue from discontinued operations of approximately $4.5 million, $10.5 million, $8.8 million and $13.3 million for the three months ended December 31, September 30, June 30 and March 31, 2010, respectively. |

| (2) | Represents the net adjustment for above- and below-market leases, which are being amortized over the remaining term of the respective leases from the date of acquisition. |

| (3) | Calculated as follows: (rental, tenant reimbursement and parking revenues - rental property operating and maintenance, real estate taxes and parking expenses) / (rental, tenant reimbursement and parking revenues). Lease termination fees are reported as part of interest and other revenue in the consolidated statements of operations. |

| (4) | For a definition and discussion of FFO, see page 48. For a quantitative reconciliation of the differences between FFO and net (loss) income, see page 16. |

| (5) | Calculated as earnings before interest, taxes and depreciation and amortization and preferred dividends, or EBITDA, of $54,035, $(44,217), $87,299, $46,041 and $134,085, respectively, divided by cash paid for interest of $52,117, $56,353, $57,369, $58,900 and $60,894, respectively. Cash paid for interest excludes default interest accrued totaling $10.1 million, $10.5 million, $9.9 million, $10.5 million and $10.4 million related to mortgages in default for the three months ended March 31, 2011 and December 31, September 30, June 30 and March 31, 2010, respectively. For a discussion of EBITDA, see page 50. For a quantitative reconciliation of the differences between EBITDA and net (loss) income, see page 19. |

| (6) | Calculated as Adjusted EBITDA of $54,035, $64,118, $64,953, $63,594 and $68,752, respectively, divided by cash paid for interest of $52,117, $56,353, $57,369, $58,900 and $60,894, respectively. For a discussion of Adjusted EBITDA, see page 50. |

| (7) | Calculated as EBITDA of $54,035, $(44,217), $87,299, $46,041 and $134,085, respectively, divided by fixed charges of $58,050, $62,461, $63,146, $65,042 and $67,128, respectively. |

| (8) | Calculated as Adjusted EBITDA of $54,035, $64,118, $64,953, $63,594 and $68,752, respectively, divided by fixed charges of $58,050, $62,461, $63,146, $65,042 and $67,128, respectively. |

| (9) | Assumes 100% conversion of the limited partnership units in our Operating Partnership into shares of our common stock. Our limited partners have the right to redeem all or part of their Operating Partnership units at any time. At the time of redemption, we have the right to determine whether to redeem the Operating Partnership units for cash, based upon the fair market value of an equivalent number of shares of our common stock at the time of redemption, or exchange them for shares of our common stock on a one-for-one basis, subject to adjustment in the event of stock splits, stock dividends, issuance of stock rights, specified extraordinary distribution and similar events. |

.

9

Consolidated Balance Sheets (unaudited and in thousands) | ||||

| March 31, 2011 | December 31, 2010 | September 30, 2010 | June 30, 2010 | March 31, 2010 | |||||||||||||||

| Assets | |||||||||||||||||||

| Investments in real estate | $ | 3,060,737 | $ | 3,063,186 | $ | 3,532,695 | $ | 3,630,535 | $ | 3,668,916 | |||||||||

| Less: accumulated depreciation | (690,953 | ) | (668,328 | ) | (685,244 | ) | (680,262 | ) | (655,892 | ) | |||||||||

| Investments in real estate, net | 2,369,784 | 2,394,858 | 2,847,451 | 2,950,273 | 3,013,024 | ||||||||||||||

| Cash, cash equivalents and restricted cash | 171,260 | 189,659 | 214,073 | 216,808 | 229,279 | ||||||||||||||

| Rents, deferred rents and other receivables, net | 67,009 | 68,237 | 75,972 | 77,320 | 76,510 | ||||||||||||||

| Deferred charges, net | 99,608 | 105,283 | 113,315 | 116,938 | 122,514 | ||||||||||||||

| Other assets | 17,304 | 12,975 | 16,591 | 16,544 | 23,892 | ||||||||||||||

| Assets associated with real estate held for sale | — | — | — | — | 52,099 | ||||||||||||||

| Total assets | $ | 2,724,965 | $ | 2,771,012 | $ | 3,267,402 | $ | 3,377,883 | $ | 3,517,318 | |||||||||

| Liabilities and Deficit | |||||||||||||||||||

| Liabilities: | |||||||||||||||||||

| Mortgage and other loans | $ | 3,578,627 | $ | 3,576,493 | $ | 3,894,266 | $ | 3,992,724 | $ | 4,035,451 | |||||||||

| Accounts payable, accrued interest payable and other liabilities | 188,418 | 196,015 | 221,184 | 208,029 | 191,959 | ||||||||||||||

| Acquired below-market leases, net | 40,111 | 44,026 | 49,163 | 62,618 | 67,815 | ||||||||||||||

| Obligations associated with real estate held for sale | — | — | — | — | 52,656 | ||||||||||||||

| Total liabilities | 3,807,156 | 3,816,534 | 4,164,613 | 4,263,371 | 4,347,881 | ||||||||||||||

| Deficit: | |||||||||||||||||||

| Stockholders’ Deficit: | |||||||||||||||||||

| Common and preferred stock and additional paid-in capital | 705,105 | 703,145 | 705,862 | 704,129 | 703,343 | ||||||||||||||

| Accumulated deficit and dividends | (1,629,743 | ) | (1,594,407 | ) | (1,460,333 | ) | (1,446,663 | ) | (1,397,328 | ) | |||||||||

| Accumulated other comprehensive loss | (27,879 | ) | (29,079 | ) | (34,582 | ) | (36,422 | ) | (36,727 | ) | |||||||||

| Total stockholders’ deficit | (952,517 | ) | (920,341 | ) | (789,053 | ) | (778,956 | ) | (730,712 | ) | |||||||||

| Noncontrolling Interests: | |||||||||||||||||||

| Common units of our Operating Partnership | (129,674 | ) | (125,181 | ) | (108,158 | ) | (106,532 | ) | (99,851 | ) | |||||||||

| Total deficit | (1,082,191 | ) | (1,045,522 | ) | (897,211 | ) | (885,488 | ) | (830,563 | ) | |||||||||

| Total liabilities and deficit | $ | 2,724,965 | $ | 2,771,012 | $ | 3,267,402 | $ | 3,377,883 | $ | 3,517,318 | |||||||||

10

MMO Unconsolidated Joint Venture Condensed Balance Sheets (1) (unaudited and in thousands) | ||||

| March 31, 2011 | December 31, 2010 | September 30, 2010 | June 30, 2010 | March 31, 2010 | |||||||||||||||

| Assets | |||||||||||||||||||

| Investments in real estate | $ | 970,875 | $ | 968,931 | $ | 1,055,538 | $ | 1,051,355 | $ | 1,049,896 | |||||||||

| Less: accumulated depreciation | (157,675 | ) | (150,943 | ) | (163,204 | ) | (156,142 | ) | (148,632 | ) | |||||||||

| Investments in real estate, net | 813,200 | 817,988 | 892,334 | 895,213 | 901,264 | ||||||||||||||

| Cash and cash equivalents, including restricted cash | 20,151 | 18,955 | 24,751 | 21,243 | 21,882 | ||||||||||||||

| Rents, deferred rents and other receivables, net | 23,410 | 22,701 | 21,641 | 21,392 | 20,535 | ||||||||||||||

| Deferred charges, net | 29,278 | 27,875 | 28,309 | 30,086 | 31,809 | ||||||||||||||

| Other assets | 2,610 | 2,474 | 3,063 | 3,832 | 4,697 | ||||||||||||||

| Total assets | $ | 888,649 | $ | 889,993 | $ | 970,098 | $ | 971,766 | $ | 980,187 | |||||||||

| Liabilities and Members’ Equity | |||||||||||||||||||

| Mortgage loans | $ | 694,209 | $ | 694,966 | $ | 801,776 | $ | 802,551 | $ | 803,317 | |||||||||

| Accounts payable, accrued interest payable and other liabilities | 22,458 | 23,001 | 32,397 | 27,619 | 29,297 | ||||||||||||||

| Acquired below-market leases, net | 2,448 | 2,762 | 3,120 | 3,531 | 3,980 | ||||||||||||||

| Total liabilities | 719,115 | 720,729 | 837,293 | 833,701 | 836,594 | ||||||||||||||

| Members’ equity | 169,534 | 169,264 | 132,805 | 138,065 | 143,593 | ||||||||||||||

| Total liabilities and members’ equity | $ | 888,649 | $ | 889,993 | $ | 970,098 | $ | 971,766 | $ | 980,187 | |||||||||

__________

| (1) | We own 20% of the Maguire Macquarie Office (“MMO”) joint venture. |

11

Consolidated Statements of Operations (unaudited and in thousands, except share and per share amounts) | ||||

| For the Three Months Ended | |||||||||||||||||||

| March 31, 2011 | December 31, 2010 | September 30, 2010 | June 30, 2010 | March 31, 2010 | |||||||||||||||

| Revenue: | |||||||||||||||||||

| Rental | $ | 58,032 | $ | 59,410 | $ | 61,139 | $ | 61,309 | $ | 62,481 | |||||||||

| Tenant reimbursements | 21,862 | 24,876 | 22,436 | 22,483 | 23,344 | ||||||||||||||

| Hotel operations | 4,988 | 5,602 | 4,867 | 4,956 | 5,237 | ||||||||||||||

| Parking | 9,636 | 9,876 | 9,559 | 10,465 | 10,886 | ||||||||||||||

| Management, leasing and development services | 999 | 1,365 | 1,281 | 1,062 | 961 | ||||||||||||||

| Interest and other | 337 | 199 | 2,631 | 246 | 225 | ||||||||||||||

| Total revenue | 95,854 | 101,328 | 101,913 | 100,521 | 103,134 | ||||||||||||||

| Expenses: | |||||||||||||||||||

| Rental property operating and maintenance | 22,109 | 25,414 | 23,521 | 22,619 | 22,330 | ||||||||||||||

| Hotel operating and maintenance | 3,573 | 3,779 | 3,485 | 3,543 | 3,747 | ||||||||||||||

| Real estate taxes | 8,146 | 7,882 | 8,264 | 8,062 | 8,039 | ||||||||||||||

| Parking | 2,768 | 2,844 | 2,814 | 2,747 | 2,852 | ||||||||||||||

| General and administrative | 6,691 | 906 | 8,073 | 6,517 | 7,607 | ||||||||||||||

| Other expense | 1,752 | 1,779 | 1,530 | 1,593 | 1,439 | ||||||||||||||

| Depreciation and amortization | 27,862 | 28,837 | 29,412 | 28,968 | 30,962 | ||||||||||||||

| Impairment of long-lived assets | — | 210,122 | — | — | — | ||||||||||||||

| Interest | 62,628 | 61,704 | 61,376 | 58,037 | 57,634 | ||||||||||||||

| Total expenses | 135,529 | 343,267 | 138,475 | 132,086 | 134,610 | ||||||||||||||

| Loss from continuing operations before equity in net (loss) income of unconsolidated joint venture and gain on sale of real estate | (39,675 | ) | (241,939 | ) | (36,562 | ) | (31,565 | ) | (31,476 | ) | |||||||||

| Equity in (loss) income of unconsolidated joint venture | (312 | ) | 304 | 204 | 196 | 201 | |||||||||||||

| Gain on sale of real estate | — | — | — | — | 16,591 | ||||||||||||||

| Loss from continuing operations | (39,987 | ) | (241,635 | ) | (36,358 | ) | (31,369 | ) | (14,684 | ) | |||||||||

| Discontinued Operations: | |||||||||||||||||||

| Loss from discontinued operations before gains on settlement of debt and sale of real estate | — | (8,486 | ) | (2,910 | ) | (24,807 | ) | (8,507 | ) | ||||||||||

| Gains on settlement of debt | — | 97,978 | 9,030 | — | 49,121 | ||||||||||||||

| Gain on sale of real estate | — | — | 14,689 | — | — | ||||||||||||||

| Income (loss) from discontinued operations | — | 89,492 | 20,809 | (24,807 | ) | 40,614 | |||||||||||||

| Net (loss) income | (39,987 | ) | (152,143 | ) | (15,549 | ) | (56,176 | ) | 25,930 | ||||||||||

| Net loss (income) attributable to common units of our Operating Partnership | 5,205 | 18,634 | 2,455 | 7,421 | (2,584 | ) | |||||||||||||

| Net (loss) income attributable to MPG Office Trust, Inc. | (34,782 | ) | (133,509 | ) | (13,094 | ) | (48,755 | ) | 23,346 | ||||||||||

| Preferred stock dividends | (4,766 | ) | (4,766 | ) | (4,766 | ) | (4,766 | ) | (4,766 | ) | |||||||||

| Net (loss) income available to common stockholders | $ | (39,548 | ) | $ | (138,275 | ) | $ | (17,860 | ) | $ | (53,521 | ) | $ | 18,580 | |||||

| Basic (loss) income per common share: | |||||||||||||||||||

| Loss from continuing operations | $ | (0.81 | ) | $ | (4.43 | ) | $ | (0.73 | ) | $ | (0.65 | ) | $ | (0.35 | ) | ||||

| Income (loss) from discontinued operations | — | 1.61 | 0.37 | (0.45 | ) | 0.73 | |||||||||||||

| Net (loss) income available to common stockholders per share | $ | (0.81 | ) | $ | (2.82 | ) | $ | (0.36 | ) | $ | (1.10 | ) | $ | 0.38 | |||||

| Weighted average number of common shares outstanding | 49,016,989 | 48,981,822 | 48,874,308 | 48,692,588 | 48,534,283 | ||||||||||||||

12

Consolidated Statements of Discontinued Operations (unaudited and in thousands) | ||||

| For the Three Months Ended | |||||||||||||||

| December 31, 2010 | September 30, 2010 | June 30, 2010 | March 31, 2010 | ||||||||||||

| Revenue: | |||||||||||||||

| Rental | $ | 2,464 | $ | 3,751 | $ | 6,404 | $ | 10,166 | |||||||

| Tenant reimbursements | 1,025 | 1,535 | 1,879 | 1,996 | |||||||||||

| Parking | 265 | 346 | 417 | 1,063 | |||||||||||

| Interest and other | 817 | 4,846 | 68 | 84 | |||||||||||

| Total revenue | 4,571 | 10,478 | 8,768 | 13,309 | |||||||||||

| Expenses: | |||||||||||||||

| Rental property operating and maintenance | 1,729 | 1,908 | 2,199 | 3,155 | |||||||||||

| Real estate taxes | 536 | 928 | 1,229 | 1,456 | |||||||||||

| Parking | 207 | 130 | 209 | 348 | |||||||||||

| Depreciation and amortization | 1,323 | 2,070 | 2,677 | 4,102 | |||||||||||

| Impairment of long-lived assets | 4,457 | 1,373 | 17,447 | — | |||||||||||

| Interest | 4,805 | 6,979 | 9,708 | 12,376 | |||||||||||

| Loss from early extinguishment of debt | — | — | 106 | 379 | |||||||||||

| Total expenses | 13,057 | 13,388 | 33,575 | 21,816 | |||||||||||

| Loss from discontinued operations before gains on settlement of debt and sale of real estate | (8,486 | ) | (2,910 | ) | (24,807 | ) | (8,507 | ) | |||||||

| Gains on settlement of debt | 97,978 | 9,030 | — | 49,121 | |||||||||||

| Gain on sale of real estate | — | 14,689 | — | — | |||||||||||

| Income (loss) from discontinued operations | $ | 89,492 | $ | 20,809 | $ | (24,807 | ) | $ | 40,614 | ||||||

13

Consolidated Statements of Operations Related to Properties in Default (1) (unaudited and in thousands) | ||||

| For the Three Months Ended | |||||||||||||||||||

| March 31, 2011 | December 31, 2010 | September 30, 2010 | June 30, 2010 | March 31, 2010 | |||||||||||||||

| Revenue: | |||||||||||||||||||

| Rental | $ | 8,066 | $ | 9,258 | $ | 9,869 | $ | 9,887 | $ | 10,368 | |||||||||

| Tenant reimbursements | 1,357 | 2,191 | 1,537 | 1,489 | 1,479 | ||||||||||||||

| Parking | 657 | 702 | 594 | 729 | 773 | ||||||||||||||

| Interest and other | 61 | 44 | 46 | 53 | 74 | ||||||||||||||

| Total revenue | 10,141 | 12,195 | 12,046 | 12,158 | 12,694 | ||||||||||||||

| Expenses: | |||||||||||||||||||

| Rental property operating and maintenance | 3,192 | 3,511 | 3,518 | 3,393 | 3,148 | ||||||||||||||

| Real estate taxes | 1,119 | 1,034 | 1,158 | 1,134 | 1,135 | ||||||||||||||

| Parking | 225 | 232 | 294 | 241 | 237 | ||||||||||||||

| Depreciation and amortization | 3,259 | 3,507 | 3,737 | 3,728 | 3,693 | ||||||||||||||

| Interest (2) | 17,761 | 18,223 | 17,497 | 16,217 | 16,523 | ||||||||||||||

| Total expenses | 25,556 | 26,507 | 26,204 | 24,713 | 24,736 | ||||||||||||||

| Loss from operations related to Properties in Default | $ | (15,415 | ) | $ | (14,312 | ) | $ | (14,158 | ) | $ | (12,555 | ) | $ | (12,042 | ) | ||||

__________

| (1) | Properties in Default include the following: Stadium Towers Plaza, 2600 Michelson, 550 South Hope, 500 Orange Tower and City Tower. As of the date of this report, the mortgage loans on these properties are in default. |

| (2) | Includes default interest totaling $8.3 million for the three months ended March 31, 2011, default interest totaling $8.4 million for the three months ended December 31, 2010, default interest totaling $7.0 million and the writeoff of deferred financing costs totaling $0.7 million for the three months ended September 30, 2010, default interest totaling $6.6 million for the three months ended June 30, 2010, and default interest totaling $6.4 million and the writeoff of deferred financing costs totaling $0.6 million for the three months ended March 31, 2010. |

14

MMO Unconsolidated Joint Venture Statements of Operations (unaudited and in thousands) | ||||

| For the Three Months Ended | |||||||||||||||||||

| March 31, 2011 | December 31, 2010 | September 30, 2010 | June 30, 2010 | March 31, 2010 | |||||||||||||||

| Revenue: | |||||||||||||||||||

| Rental | $ | 18,497 | $ | 17,710 | $ | 18,471 | $ | 18,529 | $ | 18,547 | |||||||||

| Tenant reimbursements | 5,870 | 6,219 | 6,056 | 5,318 | 5,344 | ||||||||||||||

| Parking | 1,513 | 1,472 | 1,516 | 1,573 | 1,488 | ||||||||||||||

| Interest and other | 6 | 50 | 4 | 20 | 5 | ||||||||||||||

| Total revenue | 25,886 | 25,451 | 26,047 | 25,440 | 25,384 | ||||||||||||||

| Expenses: | |||||||||||||||||||

| Rental property operating and maintenance | 6,300 | 6,647 | 5,994 | 5,849 | �� | 5,972 | |||||||||||||

| Real estate taxes | 3,171 | 2,890 | 3,345 | 3,380 | 3,072 | ||||||||||||||

| Parking | 362 | 422 | 504 | 335 | 364 | ||||||||||||||

| Depreciation and amortization | 8,507 | 8,981 | 8,477 | 8,939 | 8,830 | ||||||||||||||

| Interest | 9,156 | 9,679 | 9,550 | 9,456 | 9,361 | ||||||||||||||

| Other | 1,219 | 1,343 | 1,218 | 1,969 | 1,263 | ||||||||||||||

| Total expenses | 28,715 | 29,962 | 29,088 | 29,928 | 28,862 | ||||||||||||||

| Loss from continuing operations | (2,829 | ) | (4,511 | ) | (3,041 | ) | (4,488 | ) | (3,478 | ) | |||||||||

| Income (loss) from discontinued operations | — | 40,969 | (2,219 | ) | (2,030 | ) | (1,587 | ) | |||||||||||

| Net (loss) income | $ | (2,829 | ) | $ | 36,458 | $ | (5,260 | ) | $ | (6,518 | ) | $ | (5,065 | ) | |||||

| Company share (1) | $ | (566 | ) | $ | 7,292 | $ | (1,052 | ) | $ | (1,304 | ) | $ | (1,013 | ) | |||||

| Intercompany eliminations | 254 | 245 | 256 | 248 | 252 | ||||||||||||||

| Unallocated (allocated) losses | — | (7,233 | ) | 1,000 | 1,252 | 962 | |||||||||||||

| Equity in net (loss) income of unconsolidated joint venture | $ | (312 | ) | $ | 304 | $ | 204 | $ | 196 | $ | 201 | ||||||||

_________

| (1) | Amount represents our 20% ownership interest in the MMO joint venture. |

15

Funds from Operations (unaudited and in thousands, except share and per share amounts) | ||||

| For the Three Months Ended | ||||||||||||||||||||

| March 31, 2011 | December 31, 2010 | September 30, 2010 | June 30, 2010 | March 31, 2010 | ||||||||||||||||

Reconciliation of net (loss) income available to common stockholders to funds from operations: | ||||||||||||||||||||

| Net (loss) income available to common stockholders | $ | (39,548 | ) | $ | (138,275 | ) | $ | (17,860 | ) | $ | (53,521 | ) | $ | 18,580 | ||||||

| Add: | Depreciation and amortization of real estate assets | 27,787 | 30,084 | 31,406 | 31,569 | 34,988 | ||||||||||||||

Depreciation and amortization of real estate assets – unconsolidated joint venture (1) | 1,701 | 1,888 | 1,823 | 1,913 | 1,898 | |||||||||||||||

| Net (loss) income attributable to common units of our Operating Partnership | (5,205 | ) | (18,634 | ) | (2,455 | ) | (7,421 | ) | 2,584 | |||||||||||

| Allocated (unallocated) losses – unconsolidated joint venture (1) | — | 7,233 | (1,000 | ) | (1,252 | ) | (962 | ) | ||||||||||||

| Deduct: | Gains on sale of real estate | — | — | 14,689 | — | 16,591 | ||||||||||||||

| Funds from operations available to common stockholders and unit holders (FFO) (2) | $ | (15,265 | ) | $ | (117,704 | ) | $ | (2,775 | ) | $ | (28,712 | ) | $ | 40,497 | ||||||

| Company share of FFO (3) | $ | (13,490 | ) | $ | (103,726 | ) | $ | (2,440 | ) | $ | (25,215 | ) | $ | 35,552 | ||||||

| FFO per share – basic | $ | (0.28 | ) | $ | (2.12 | ) | $ | (0.05 | ) | $ | (0.52 | ) | $ | 0.73 | ||||||

| FFO per share – diluted | $ | (0.28 | ) | $ | (2.12 | ) | $ | (0.05 | ) | $ | (0.52 | ) | $ | 0.72 | ||||||

| Weighted average number of common shares outstanding – basic | 49,016,989 | 48,981,822 | 48,874,308 | 48,692,588 | 48,534,283 | |||||||||||||||

| Weighted average number of common and common equivalent shares outstanding – diluted | 50,237,641 | 49,619,851 | 49,507,077 | 49,442,240 | 49,197,833 | |||||||||||||||

| Weighted average diluted shares and units | 56,684,418 | 56,149,712 | 56,116,486 | 56,101,775 | 55,872,406 | |||||||||||||||

| Reconciliation of FFO to FFO before specified items: (2) | ||||||||||||||||||||

| FFO available to common stockholders and unit holders (FFO) | $ | (15,265 | ) | $ | (117,704 | ) | $ | (2,775 | ) | $ | (28,712 | ) | $ | 40,497 | ||||||

| Add: | Loss from early extinguishment of debt | — | — | — | 106 | 379 | ||||||||||||||

| Default interest accrued on mortgages in default | 10,078 | 10,533 | 9,902 | 10,541 | 10,363 | |||||||||||||||

| Writeoff of deferred financing costs related to mortgages in default | 1,626 | — | 713 | — | 562 | |||||||||||||||

| Impairment of long-lived assets | — | 214,579 | 1,373 | 17,447 | — | |||||||||||||||

| Impairment of long-lived assets – unconsolidated joint venture (1) | — | 572 | — | — | — | |||||||||||||||

| Deduct: | Gains on settlement of debt | — | 97,978 | 9,030 | — | 49,121 | ||||||||||||||

| Gain on settlement of debt – unconsolidated joint venture (1) | — | 8,838 | — | — | — | |||||||||||||||

| FFO before specified items | $ | (3,561 | ) | $ | 1,164 | $ | 183 | $ | (618 | ) | $ | 2,680 | ||||||||

| Company share of FFO before specified items (3) | $ | (3,147 | ) | $ | 1,026 | $ | 161 | $ | (543 | ) | $ | 2,353 | ||||||||

| FFO per share before specified items – basic | $ | (0.06 | ) | $ | 0.02 | $ | — | $ | (0.01 | ) | $ | 0.05 | ||||||||

| FFO per share before specified items – diluted | $ | (0.06 | ) | $ | 0.02 | $ | — | $ | (0.01 | ) | $ | 0.05 | ||||||||

| (1) | Amount represents our 20% ownership interest in the MMO joint venture. |

| (2) | For the definition and discussion of FFO and FFO before specified items, see page 48. |

| (3) | Based on a weighted average interest in our Operating Partnership of approximately 88.4% for the three months ended March 31, 2011, 88.1% for the three months ended December 31, 2010, 87.9% for the three months ended September 30, 2010 and 87.8% for all other periods presented. |

16

Adjusted Funds from Operations (1) (unaudited and in thousands) | ||||

| For the Three Months Ended | ||||||||||||||||||||

| March 31, 2011 | December 31, 2010 | September 30, 2010 | June 30, 2010 | March 31, 2010 | ||||||||||||||||

| FFO | $ | (15,265 | ) | $ | (117,704 | ) | $ | (2,775 | ) | $ | (28,712 | ) | $ | 40,497 | ||||||

| Add: | Non-real estate depreciation | 75 | 76 | 76 | 76 | 76 | ||||||||||||||

| Straight line ground lease expense | 511 | 511 | 511 | 512 | 511 | |||||||||||||||

| Amortization of deferred financing costs | 954 | 988 | 1,321 | 1,298 | 1,393 | |||||||||||||||

| Unrealized (gain) loss due to hedge ineffectiveness | (308 | ) | 783 | 1,244 | 93 | 80 | ||||||||||||||

| Default interest accrued on mortgages in default | 10,078 | 10,533 | 9,902 | 10,541 | 10,363 | |||||||||||||||

| Writeoff of deferred financing costs related to mortgages in default | 1,626 | — | 713 | — | 562 | |||||||||||||||

| Non-cash stock compensation | 1,998 | (2,502 | ) | 1,932 | 927 | 945 | ||||||||||||||

| Impairment of long-lived assets | — | 214,579 | 1,373 | 17,447 | — | |||||||||||||||

| Loss from early extinguishment of debt | — | — | — | 106 | 379 | |||||||||||||||

| Deduct: | Gains on settlement of debt | — | 97,978 | 9,030 | — | 49,121 | ||||||||||||||

| Straight line rent | 460 | 988 | (73 | ) | 1,029 | 2,761 | ||||||||||||||

| Fair value lease revenue | 3,446 | 3,946 | 5,988 | 3,820 | 4,579 | |||||||||||||||

| Capitalized payments (2) | 624 | 637 | 1,004 | 1,638 | 2,013 | |||||||||||||||

| Capital lease principal payments | 132 | 277 | 251 | 278 | 340 | |||||||||||||||

| Scheduled principal payments on mortgage loans | 900 | 900 | 600 | 940 | 965 | |||||||||||||||

| Non-recoverable capital expenditures | 149 | 347 | 638 | 77 | 199 | |||||||||||||||

| Recoverable capital expenditures | 363 | 265 | 779 | 607 | 810 | |||||||||||||||

| Hotel improvements, equipment upgrades and replacements | 776 | 661 | 88 | 57 | 68 | |||||||||||||||

| 2nd generation tenant improvements and leasing commissions (3), (4) | 1,848 | 3,229 | 5,123 | 1,032 | 1,353 | |||||||||||||||

| MMO joint venture AFFO adjustments (5) | 583 | 8,829 | 913 | 584 | 723 | |||||||||||||||

| Adjusted funds from operations (AFFO) | $ | (9,612 | ) | $ | (10,793 | ) | $ | (10,044 | ) | $ | (7,774 | ) | $ | (8,126 | ) | |||||

__________

| (1) | For the definition and computation method of AFFO, see page 49. For a quantitative reconciliation of the differences between AFFO and cash flows from operating activities, see page 19. |

| (2) | Includes capitalized leasing and development payroll, and capitalized interest. |

| (3) | Excludes 1st generation tenant improvements and leasing commissions of $0.2 million, $0.8 million, $2.8 million, $1.6 million and $1.2 million for the three months ended March 31, 2011 and December 31, September 30, June 30 and March 31, 2010, respectively. |

| (4) | Excludes tenant improvements and leasing commissions paid using cash reserves that were funded through loan proceeds upon acquisition or debt refinancing of $0.5 million, $0.2 million, $0.6 million, $0.3 million and $1.0 million for the three months ended March 31, 2011 and December 31, September 30, June 30 and March 31, 2010, respectively. |

| (5) | Amount represents our 20% ownership interest in the MMO joint venture. |

17

Adjusted Funds from Operations Related to Properties in Default (1) (unaudited and in thousands) | ||||

| For the Three Months Ended | ||||||||||||||||||||

| March 31, 2011 | December 31, 2010 | September 30, 2010 | June 30, 2010 | March 31, 2010 | ||||||||||||||||

| FFO | $ | (12,156 | ) | $ | 80,011 | $ | (2,232 | ) | $ | (24,049 | ) | $ | (11,712 | ) | ||||||

| Add: | Amortization of deferred financing costs | — | — | 18 | 27 | 26 | ||||||||||||||

| Writeoff of deferred financing costs | — | — | 713 | — | 562 | |||||||||||||||

| Default interest accrued | 8,250 | 10,533 | 9,902 | 10,541 | 10,363 | |||||||||||||||

| Impairment of long-lived assets | — | 4,457 | 1,373 | 10,688 | — | |||||||||||||||

| Deduct: | Gains on settlement of debt | — | 97,978 | 9,030 | — | — | ||||||||||||||

| Straight line rent | 530 | 1,114 | (151 | ) | — | 1,997 | ||||||||||||||

| Fair value lease revenue | 789 | 1,168 | 1,624 | 1,413 | 1,583 | |||||||||||||||

| Capitalized payments (2) | — | — | — | 939 | 1,128 | |||||||||||||||

| Non-recoverable capital expenditures | — | 31 | — | 21 | — | |||||||||||||||

| Recoverable capital expenditures | — | — | — | — | — | |||||||||||||||

| 2nd generation tenant improvements and leasing commissions | — | — | — | — | 7 | |||||||||||||||

| Adjusted funds from operations related to Properties in Default | $ | (5,225 | ) | $ | (5,290 | ) | $ | (729 | ) | $ | (5,166 | ) | $ | (5,476 | ) | |||||

__________

| (1) | For purposes of this schedule, Properties in Default include the following: Stadium Towers Plaza, Park Place II, 2600 Michelson, Pacific Arts Plaza, 550 South Hope, 500 Orange Tower, City Tower and 207 Goode. In July 2010, we disposed of Park Place II, in October 2010, we disposed of 207 Goode and in December 2010, we disposed of Pacific Arts Plaza. |

| (2) | Includes regular principal payments related to the Park Place II mortgage loan and capitalized interest related to 207 Goode. |

18

Reconciliation of Earnings before Interest, Taxes and Depreciation and Amortization (1) and Adjusted Funds from Operations (2) (unaudited and in thousands) | ||||

| For the Three Months Ended | ||||||||||||||||||||

| March 31, 2011 | December 31, 2010 | September 30, 2010 | June 30, 2010 | March 31, 2010 | ||||||||||||||||

| Reconciliation of net (loss) income to earnings before interest, taxes and depreciation and amortization (EBITDA): | ||||||||||||||||||||

| Net (loss) income | $ | (39,987 | ) | $ | (152,143 | ) | $ | (15,549 | ) | $ | (56,176 | ) | $ | 25,930 | ||||||

| Add: | Interest expense (3) | 62,628 | 66,509 | 68,355 | 67,745 | 70,010 | ||||||||||||||

| Interest expense – unconsolidated joint venture (4) | 1,831 | 2,136 | 2,188 | 2,166 | 2,145 | |||||||||||||||

| Depreciation and amortization (5) | 27,862 | 30,160 | 31,482 | 31,645 | 35,064 | |||||||||||||||

| Depreciation and amortization – unconsolidated joint venture (4) | 1,701 | 1,888 | 1,823 | 1,913 | 1,898 | |||||||||||||||

| Deduct: | Unallocated losses from unconsolidated joint venture (4) | — | (7,233 | ) | 1,000 | 1,252 | 962 | |||||||||||||

| EBITDA | $ | 54,035 | $ | (44,217 | ) | $ | 87,299 | $ | 46,041 | $ | 134,085 | |||||||||

| EBITDA | $ | 54,035 | $ | (44,217 | ) | $ | 87,299 | $ | 46,041 | $ | 134,085 | |||||||||

| Add: | Loss from early extinguishment of debt | — | — | — | 106 | 379 | ||||||||||||||

| Impairment of long-lived assets | — | 214,579 | 1,373 | 17,447 | — | |||||||||||||||

| Impairment of long-lived assets – unconsolidated joint venture (4) | — | 572 | — | — | — | |||||||||||||||

| Deduct: | Gains on settlement of debt | — | 97,978 | 9,030 | — | 49,121 | ||||||||||||||

| Gain on settlement of debt – unconsolidated joint venture (4) | — | 8,838 | — | — | — | |||||||||||||||

| Gains on sale of real estate | — | — | 14,689 | — | 16,591 | |||||||||||||||

| Adjusted EBITDA | $ | 54,035 | $ | 64,118 | $ | 64,953 | $ | 63,594 | $ | 68,752 | ||||||||||

| Reconciliation of cash flows from operating activities to adjusted funds from operations (AFFO): | ||||||||||||||||||||

| Cash flows from operating activities | $ | (19,188 | ) | $ | 4,295 | $ | 6,348 | $ | 10,966 | $ | 436 | |||||||||

| Changes in other assets and liabilities | 12,712 | (10,586 | ) | (9,764 | ) | (16,967 | ) | (6,132 | ) | |||||||||||

| Non-recoverable capital expenditures | (149 | ) | (347 | ) | (638 | ) | (77 | ) | (199 | ) | ||||||||||

| Recoverable capital expenditures | (363 | ) | (265 | ) | (779 | ) | (607 | ) | (810 | ) | ||||||||||

| Hotel improvements, equipment upgrades and replacements | (776 | ) | (661 | ) | (88 | ) | (57 | ) | (68 | ) | ||||||||||

| 2nd generation tenant improvements and leasing commissions (6), (7) | (1,848 | ) | (3,229 | ) | (5,123 | ) | (1,032 | ) | (1,353 | ) | ||||||||||

| AFFO | $ | (9,612 | ) | $ | (10,793 | ) | $ | (10,044 | ) | $ | (7,774 | ) | $ | (8,126 | ) | |||||

__________

| (1) | For the definition and discussion of EBITDA and Adjusted EBITDA, see page 50. |

| (2) | For the definition and discussion of AFFO, see page 49. |

| (3) | Includes interest expense of $4.8 million, $7.0 million, $9.7 million and $12.4 million for the three months ended December 31, September 30, June 30 and March 31, 2010, respectively, related to discontinued operations. |

| (4) | Amount represents our 20% ownership interest in the MMO joint venture. |

| (5) | Includes depreciation and amortization of $1.3 million, $2.1 million, $2.7 million and $4.1 million for the three months ended December 31, September 30, June 30 and March 31, 2010, respectively, related to discontinued operations. |

| (6) | Excludes 1st generation tenant improvements and leasing commissions of $0.2 million, $0.8 million, $2.8 million, $1.6 million and $1.2 million for the three months ended March 31, 2011 and December 31, September 30, June 30 and March 31, 2010, respectively. |

| (7) | Excludes tenant improvements and leasing commissions paid using cash reserves that were funded through loan proceeds upon acquisition or debt refinancing of $0.5 million, $0.2 million, $0.6 million, $0.3 million and $1.0 million for the three months ended March 31, 2011 and December 31, September 30, June 30 and March 31, 2010, respectively. |

19

| Capital Structure | ||||

| Debt | ||||||

| (in thousands) | ||||||

| Balance as of | ||||||

| March 31, 2011 | ||||||

| Mortgage and other loans | $ | 3,578,627 | ||||

| Company share of MMO joint venture debt | 138,842 | |||||

| Total combined debt | $ | 3,717,469 | ||||

| Equity | ||||||

| (in thousands) | ||||||

| Shares Outstanding | Total Liquidation Preference | |||||

| Preferred stock | 10,000 | $ | 250,000 | |||

Shares & Units Outstanding | Market Value (1) | |||||

| Common stock | 49,044 | $ | 181,954 | |||

| Noncontrolling common units of our Operating Partnership | 6,447 | 23,918 | ||||

| Total common equity | 55,491 | $ | 205,872 | |||

| Total consolidated market capitalization | $ | 4,034,499 | ||||

| Total combined market capitalization (2) | $ | 4,173,341 | ||||

__________

| (1) | Value based on the NYSE closing price of $3.71 on March 31, 2011. |

| (2) | Includes our share of MMO joint venture debt. |

20

Debt Summary (in thousands, except percentages) | ||||

| Maturity Date | Principal Amount as of March 31, 2011 | % of Debt | Interest Rate as of March 31, 2011 (1) | ||||||||

| Floating-Rate Debt | |||||||||||

| Unsecured term loan (2) | May 1, 2011 | $ | 15,000 | 0.42 | % | 3.99 | % | ||||

| Variable-Rate Mortgage Loans: | |||||||||||

| Plaza Las Fuentes (3) | September 29, 2011 | 79,200 | 2.21 | % | 3.99 | % | |||||

| Brea Corporate Place (4) | May 1, 2012 | 70,468 | 1.97 | % | 2.19 | % | |||||

| Brea Financial Commons (4) | May 1, 2012 | 38,532 | 1.08 | % | 2.19 | % | |||||

| Total variable-rate mortgage loans | 188,200 | 5.26 | % | 2.95 | % | ||||||

| Variable-Rate Swapped to Fixed-Rate Loan: | |||||||||||

| KPMG Tower (5) | October 9, 2012 | 400,000 | 11.17 | % | 7.16 | % | |||||

| Total floating-rate debt | 603,200 | 16.85 | % | 5.77 | % | ||||||

| Fixed-Rate Debt | |||||||||||

| Wells Fargo Tower | April 6, 2017 | 550,000 | 15.36 | % | 5.68 | % | |||||

| Gas Company Tower | August 11, 2016 | 458,000 | 12.79 | % | 5.10 | % | |||||

| 777 Tower | November 1, 2013 | 273,000 | 7.63 | % | 5.84 | % | |||||

| US Bank Tower | July 1, 2013 | 260,000 | 7.26 | % | 4.66 | % | |||||

| Glendale Center | August 11, 2016 | 125,000 | 3.49 | % | 5.82 | % | |||||

| 801 North Brand | April 6, 2015 | 75,540 | 2.11 | % | 5.73 | % | |||||

| The City – 3800 Chapman | May 6, 2017 | 44,370 | 1.24 | % | 5.93 | % | |||||

| 701 North Brand (6) | October 1, 2016 | 33,750 | 0.94 | % | 5.87 | % | |||||

| 700 North Central | April 6, 2015 | 27,460 | 0.77 | % | 5.73 | % | |||||

| Total fixed-rate debt | 1,847,120 | 51.59 | % | 5.44 | % | ||||||

| Total debt, excluding mortgages in default | 2,450,320 | 68.44 | % | 5.52 | % | ||||||

| Mortgages in Default | |||||||||||

| Two California Plaza (7) | May 6, 2017 | 470,000 | 13.13 | % | 10.50 | % | |||||

| 550 South Hope (8) (9) | May 6, 2017 | 200,000 | 5.59 | % | 10.67 | % | |||||

| City Tower (8) | May 10, 2017 | 140,000 | 3.91 | % | 10.85 | % | |||||

| 500 Orange Tower (8) | May 6, 2017 | 110,000 | 3.07 | % | 10.88 | % | |||||

| 2600 Michelson (8) | May 10, 2017 | 110,000 | 3.07 | % | 10.69 | % | |||||

| Stadium Towers Plaza (8) | May 11, 2017 | 100,000 | 2.79 | % | 10.78 | % | |||||

| Total mortgages in default | 1,130,000 | 31.56 | % | 10.65 | % | ||||||

| Total consolidated debt | 3,580,320 | 100.00 | % | 7.14 | % | ||||||

| Debt discount | (1,693 | ) | |||||||||

| Total consolidated debt, net | $ | 3,578,627 | |||||||||

21

| Debt Summary (continued) | ||||

__________

| (1) | The March 31, 2011 one-month LIBOR rate of 0.24% was used to calculate interest on the variable-rate loans. |

| (2) | This loan bears interest at a variable rate of LIBOR plus 3.75%. This loan was repaid upon maturity on May 1, 2011. |

| (3) | This loan bears interest at a variable rate of LIBOR plus 3.75%. As required by the loan agreement, we have entered into an interest rate cap agreement that limits the LIBOR portion of the interest rate to 4.75% during the loan term, excluding extension periods. Two one-year extensions are available at our option, subject to certain conditions, some of which we may be unable to fulfill. |

| (4) | This loan bears interest at a rate of LIBOR plus 1.95%. As required by the loan agreement, we have entered into an interest rate cap agreement that limits the LIBOR portion of the interest rate to 6.50% during the loan term. This loan was extended until May 1, 2012. |

| (5) | This loan bears interest at a rate of LIBOR plus 1.60%. We have entered into an interest rate swap agreement to hedge this loan, which effectively fixes the LIBOR rate at 5.564%. |

| (6) | We disposed of 701 North Brand on April 1, 2011. |

| (7) | On March 7, 2011, our special purpose property-owning subsidiary that owns Two California Plaza defaulted on the mortgage loan secured by the property. The interest rate shown for this loan is the default rate as defined in the loan agreement. The special servicer has the contractual right to accelerate the maturity of the debt but has not done so. If we are successful in modifying the mortgage loan, the settlement date and treatment of principal will be as set forth in the modified loan agreement. |

| (8) | Our special purpose property-owning subsidiary that owns this property is in default for failing to make debt service payments due under this loan. The interest rate shown for this loan is the default rate as defined in the loan agreement. The special servicer has the contractual right to accelerate the maturity of the debt but has not done so. The actual settlement date of the loan will depend upon when the property is disposed of either by the Company or the special servicer, as applicable. Management does not intend to settle this amount with unrestricted cash. We expect that this amount will be settled in a non-cash manner at the time of disposition. |

| (9) | We disposed of 550 South Hope on April 26, 2011. |

22

MMO Joint Venture Debt Summary (in thousands, except percentages) | ||||

Maturity Date | Principal Amount as of March 31, 2011 | % of Debt | Interest Rate as of March 31, 2011 (1) | ||||||||

| Fixed-Rate Debt | |||||||||||

| Wells Fargo Center (Denver, CO) | April 6, 2015 | $ | 276,000 | 39.86 | % | 5.26 | % | ||||

| One California Plaza | July 1, 2011 | 136,556 | 19.72 | % | 4.73 | % | |||||

| San Diego Tech Center | April 11, 2015 | 133,000 | 19.21 | % | 5.70 | % | |||||

| Cerritos Corporate Center | February 1, 2016 | 94,868 | 13.70 | % | 5.54 | % | |||||

| Stadium Gateway | February 1, 2016 | 52,000 | 7.51 | % | 5.66 | % | |||||

| Total fixed-rate debt | 692,424 | 100.00 | % | 5.31 | % | ||||||

| Debt premium, net of discount | 1,785 | ||||||||||

| Total joint venture debt, net | $ | 694,209 | |||||||||

| Our portion of joint venture debt (1) | $ | 138,842 | |||||||||

__________

| (1) | We own 20% of the MMO joint venture. |

23

Debt Maturities (in thousands, except percentages) | ||||

| 2011 | 2012 | 2013 | 2014 | 2015 | Thereafter | Total | |||||||||||||||||||||

| Floating-Rate Debt | |||||||||||||||||||||||||||

| Unsecured term loan (1) | $ | 15,000 | $ | — | $ | — | $ | — | $ | — | $ | — | $ | 15,000 | |||||||||||||

| Variable-Rate Mortgage Loans: | |||||||||||||||||||||||||||

| Plaza Las Fuentes (2) | 79,200 | — | — | — | — | — | 79,200 | ||||||||||||||||||||

| Brea Corporate Place | — | 70,468 | — | — | — | — | 70,468 | ||||||||||||||||||||

| Brea Financial Commons | — | 38,532 | — | — | — | — | 38,532 | ||||||||||||||||||||

| Total variable-rate mortgage loans | 79,200 | 109,000 | — | — | — | — | 188,200 | ||||||||||||||||||||

| Variable-Rate Swapped to Fixed-Rate Loan: | |||||||||||||||||||||||||||

| KPMG Tower | — | 400,000 | — | — | — | — | 400,000 | ||||||||||||||||||||

| Total floating-rate debt | 94,200 | 509,000 | — | — | — | — | 603,200 | ||||||||||||||||||||

| Fixed-Rate Debt | |||||||||||||||||||||||||||

| Wells Fargo Tower | — | — | — | — | — | 550,000 | 550,000 | ||||||||||||||||||||

| Gas Company Tower | — | — | — | — | — | 458,000 | 458,000 | ||||||||||||||||||||

| 777 Tower | — | — | 273,000 | — | — | — | 273,000 | ||||||||||||||||||||

| US Bank Tower | — | — | 260,000 | — | — | — | 260,000 | ||||||||||||||||||||

| Glendale Center | — | — | — | — | — | 125,000 | 125,000 | ||||||||||||||||||||

| 801 North Brand | — | — | — | — | 75,540 | — | 75,540 | ||||||||||||||||||||

| The City – 3800 Chapman | — | — | — | — | — | 44,370 | 44,370 | ||||||||||||||||||||

| 701 North Brand (3) | — | — | — | — | — | 33,750 | 33,750 | ||||||||||||||||||||

| 700 North Central | — | — | — | — | 27,460 | — | 27,460 | ||||||||||||||||||||

| Total fixed-rate debt | — | — | 533,000 | — | 103,000 | 1,211,120 | 1,847,120 | ||||||||||||||||||||

Total debt, excluding mortgages in default | 94,200 | 509,000 | 533,000 | — | 103,000 | 1,211,120 | 2,450,320 | ||||||||||||||||||||

| Debt discount | — | — | (1,693 | ) | — | — | — | (1,693 | ) | ||||||||||||||||||

Total debt, excluding mortgages in default, net | 94,200 | 509,000 | 531,307 | — | 103,000 | 1,211,120 | 2,448,627 | ||||||||||||||||||||

| Mortgages in Default | |||||||||||||||||||||||||||

| Two California Plaza (4) | — | — | — | — | — | 470,000 | 470,000 | ||||||||||||||||||||

| 550 South Hope (5) (6) | — | — | — | — | — | 200,000 | 200,000 | ||||||||||||||||||||

| City Tower (5) | — | — | — | — | — | 140,000 | 140,000 | ||||||||||||||||||||

| 500 Orange Tower (5) | — | — | — | — | — | 110,000 | 110,000 | ||||||||||||||||||||

| 2600 Michelson (5) | — | — | — | — | — | 110,000 | 110,000 | ||||||||||||||||||||

| Stadium Towers Plaza (5) | — | — | — | — | — | 100,000 | 100,000 | ||||||||||||||||||||

| Total mortgages in default | — | — | — | — | — | 1,130,000 | 1,130,000 | ||||||||||||||||||||

| Total consolidated debt, net | $ | 94,200 | $ | 509,000 | $ | 531,307 | $ | — | $ | 103,000 | $ | 2,341,120 | $ | 3,578,627 | |||||||||||||

Weighted average interest rate, excluding mortgages in default | 3.99 | % | 6.10 | % | 5.27 | % | — | % | 5.73 | % | 5.49 | % | 5.52 | % | |||||||||||||

Weighted average interest rate, mortgages in default | — | % | — | % | — | % | — | % | — | % | 10.65 | % | 10.65 | % | |||||||||||||

| Weighted average interest rate, consolidated | 3.99 | % | 6.10 | % | 5.27 | % | — | % | 5.73 | % | 7.98 | % | 7.14 | % | |||||||||||||

__________

| (1) | This loan was repaid upon maturity on May 1, 2011. |

| (2) | Two one-year extensions are available at our option, subject to certain conditions, some of which we may be unable to fulfill. |

| (3) | We disposed of 701 North Brand on April 1, 2011. |

| (4) | Amounts shown in the table above for mortgages in default reflect contractual maturity dates per the loan agreements. The special servicers have the contractual right to accelerate the maturity dates of the debt but have not done so. If we are successful in modifying the mortgage loan, the settlement date and treatment of principal will be as set forth in the modified loan agreement. |

| (5) | Amounts shown in the table above for mortgages in default reflect contractual maturity dates per the loan agreements. The special servicers have the contractual right to accelerate the maturity dates of the debt but have not done so. The actual settlement date of the loan will depend upon when the property is disposed of either by the Company or the special servicer, as applicable. Management does not intend to settle this amount with unrestricted cash. We expect that this amount will be settled in a non-cash manner at the time of disposition. |

| (6) | We disposed of 550 South Hope on April 26, 2011. |

24

MMO Joint Venture Debt Maturities (in thousands, except percentages) | ||||

| 2011 | 2012 | 2013 | 2014 | 2015 | Thereafter | Total | |||||||||||||||||||||

| Fixed-Rate Debt | |||||||||||||||||||||||||||

| Wells Fargo Center (Denver, CO) | $ | — | $ | — | $ | — | $ | — | $ | 276,000 | $ | — | $ | 276,000 | |||||||||||||

| One California Plaza | 136,556 | — | — | — | — | — | 136,556 | ||||||||||||||||||||

| San Diego Tech Center | — | — | — | — | 133,000 | — | 133,000 | ||||||||||||||||||||

| Cerritos Corporate Center | 922 | 1,330 | 1,406 | 1,486 | 1,570 | 88,154 | 94,868 | ||||||||||||||||||||

| Stadium Gateway | — | — | — | — | — | 52,000 | 52,000 | ||||||||||||||||||||

| 137,478 | 1,330 | 1,406 | 1,486 | 410,570 | 140,154 | 692,424 | |||||||||||||||||||||

| Debt premium, net of discount | — | — | — | — | 1,785 | — | 1,785 | ||||||||||||||||||||

| Total joint venture debt, net | $ | 137,478 | $ | 1,330 | $ | 1,406 | $ | 1,486 | $ | 412,355 | $ | 140,154 | $ | 694,209 | |||||||||||||

| Weighted average interest rate | 4.74 | % | 5.54 | % | 5.54 | % | 5.54 | % | 5.40 | % | 5.58 | % | 5.31 | % | |||||||||||||

25

| Portfolio Data | ||||

26

Same Store Analysis (unaudited and in thousands, except percentages) | ||||

| For the Three Months Ended March 31, (1) | ||||||||||

| 2011 | 2010 | % Change | ||||||||

| Total Same Store Portfolio | ||||||||||

| Number of properties | 14 | 14 | ||||||||

| Square feet as of March 31 | 9,462,979 | 9,401,471 | ||||||||

| Percentage of wholly-owned Office Portfolio | 100.0 | % | 100.0 | % | ||||||

| Weighted average leased percentage (2) | 83.5 | % | 84.7 | % | ||||||

| GAAP | ||||||||||

| Breakdown of Net Operating Income: | ||||||||||

| Operating revenue | $ | 79,508 | $ | 84,172 | (5.5 | )% | ||||

| Operating expenses | 28,446 | 28,655 | (0.7 | )% | ||||||

| Other expense | 1,264 | 1,264 | — | % | ||||||

| Net operating income | $ | 49,798 | $ | 54,253 | (8.2 | )% | ||||

| CASH BASIS | ||||||||||

| Breakdown of Net Operating Income: | ||||||||||

| Operating revenue | $ | 76,922 | $ | 81,359 | (5.5 | )% | ||||

| Operating expenses | 28,446 | 28,656 | (0.7 | )% | ||||||

| Other expense | 743 | 743 | — | % | ||||||

| Net operating income | $ | 47,733 | $ | 51,960 | (8.1 | )% | ||||

__________

| (1) | Properties included in the Same Store analysis are the properties in our Office Portfolio, with the exception of the Properties in Default and our joint venture properties. |

| (2) | Represents weighted average leased amounts for the Same Store Portfolio. |

27

| Portfolio Overview | ||||

| Property by Submarket | Square Feet | Leased % and In-Place Rents | |||||||||||||||||||||||||||||||||

| Property | Number of Buildings | Number of Tenants | Year Built / Renovated | Ownership % | Net Building Rentable | Effective (1) | % of Net Rentable | % Leased | Total Annualized Rents (2) | Effective Annualized Rents (2) | Annualized Rent $/RSF (3) | ||||||||||||||||||||||||

| Office Properties | |||||||||||||||||||||||||||||||||||

| Los Angeles County | |||||||||||||||||||||||||||||||||||

| Los Angeles Central Business District: | |||||||||||||||||||||||||||||||||||

| Gas Company Tower | 1 | 17 | 1991 | 100 | % | 1,349,169 | 1,349,169 | 10.42 | % | 94.6 | % | $ | 34,835,671 | $ | 34,835,671 | $ | 27.30 | ||||||||||||||||||

| US Bank Tower | 1 | 54 | 1989 | 100 | % | 1,431,808 | 1,431,808 | 11.06 | % | 58.5 | % | 19,443,113 | 19,443,113 | 23.22 | |||||||||||||||||||||

| Wells Fargo Tower | 2 | 56 | 1982 | 100 | % | 1,400,531 | 1,400,531 | 10.82 | % | 92.6 | % | 28,586,764 | 28,586,764 | 22.04 | |||||||||||||||||||||

| Two California Plaza | 1 | 58 | 1992 | 100 | % | 1,327,835 | 1,327,835 | 10.26 | % | 81.1 | % | 21,975,487 | 21,975,487 | 20.40 | |||||||||||||||||||||

| KPMG Tower | 1 | 21 | 1983 | 100 | % | 1,147,421 | 1,147,421 | 8.87 | % | 95.5 | % | 26,225,833 | 26,225,833 | 23.94 | |||||||||||||||||||||

| 777 Tower | 1 | 34 | 1991 | 100 | % | 1,014,665 | 1,014,665 | 7.84 | % | 79.4 | % | 17,881,379 | 17,881,379 | 22.19 | |||||||||||||||||||||

| One California Plaza | 1 | 27 | 1985 | 20 | % | 1,022,876 | 204,575 | 7.90 | % | 77.2 | % | 16,654,906 | 3,330,981 | 21.10 | |||||||||||||||||||||

| Total LACBD Submarket | 8 | 267 | 8,694,305 | 7,876,004 | 67.17 | % | 82.6 | % | 165,603,153 | 152,279,228 | 23.07 | ||||||||||||||||||||||||

| Tri-Cities Submarket: | |||||||||||||||||||||||||||||||||||

| Glendale Center | 2 | 4 | 1973/1996 | 100 | % | 396,000 | 396,000 | 3.06 | % | 93.8 | % | 8,640,473 | 8,640,473 | 23.26 | |||||||||||||||||||||

| 801 North Brand | 1 | 30 | 1987 | 100 | % | 282,788 | 282,788 | 2.19 | % | 83.2 | % | 4,851,790 | 4,851,790 | 20.61 | |||||||||||||||||||||

| 701 North Brand | 1 | 13 | 1978 | 100 | % | 131,129 | 131,129 | 1.01 | % | 97.2 | % | 2,286,548 | 2,286,548 | 17.95 | |||||||||||||||||||||

| 700 North Central | 1 | 12 | 1979 | 100 | % | 134,168 | 134,168 | 1.04 | % | 66.7 | % | 1,560,481 | 1,560,481 | 17.45 | |||||||||||||||||||||

| Plaza Las Fuentes | 3 | 7 | 1989 | 100 | % | 193,254 | 193,254 | 1.49 | % | 93.9 | % | 5,348,886 | 5,348,886 | 29.47 | |||||||||||||||||||||

| Total Tri-Cities Submarket | 8 | 66 | 1,137,339 | 1,137,339 | 8.79 | % | 88.4 | % | 22,688,178 | 22,688,178 | 22.57 | ||||||||||||||||||||||||

| Cerritos Office Submarket: | |||||||||||||||||||||||||||||||||||

| Cerritos – Phase I | 1 | 1 | 1999 | 20 | % | 221,968 | 44,394 | 1.71 | % | 100.0 | % | 6,317,209 | 1,263,442 | 28.46 | |||||||||||||||||||||

| Cerritos – Phase II | 1 | — | 2001 | 20 | % | 104,567 | 20,913 | 0.81 | % | 100.0 | % | 2,482,421 | 496,484 | 23.74 | |||||||||||||||||||||

| Total Cerritos Submarket | 2 | 1 | 326,535 | 65,307 | 2.52 | % | 100.0 | % | 8,799,630 | 1,759,926 | 26.95 | ||||||||||||||||||||||||

| Total Los Angeles County | 18 | 334 | 10,158,179 | 9,078,650 | 78.48 | % | 83.8 | % | $ | 197,090,961 | $ | 176,727,332 | $ | 23.16 | |||||||||||||||||||||

28

| Portfolio Overview (continued) | ||||

| Property by Submarket | Square Feet | Leased % and In-Place Rents | |||||||||||||||||||||||||||||||||

| Property | Number of Buildings | Number of Tenants | Year Built / Renovated | Ownership % | Net Building Rentable | Effective (1) | % of Net Rentable | % Leased | Total Annualized Rents (2) | Effective Annualized Rents (2) | Annualized Rent $/RSF (3) | ||||||||||||||||||||||||

| Office Properties | |||||||||||||||||||||||||||||||||||

| Orange County | |||||||||||||||||||||||||||||||||||

| Central Orange Submarket: | |||||||||||||||||||||||||||||||||||

| 3800 Chapman | 1 | 2 | 1984 | 100 | % | 158,767 | 158,767 | 1.23 | % | 75.9 | % | $ | 2,642,465 | $ | 2,642,465 | $ | 21.94 | ||||||||||||||||||

| Stadium Gateway | 1 | 7 | 2001 | 20 | % | 272,826 | 54,565 | 2.10 | % | 72.2 | % | 4,326,348 | 865,270 | 21.98 | |||||||||||||||||||||

| Total Central Orange Submarket | 2 | 9 | 431,593 | 213,332 | 3.33 | % | 73.5 | % | 6,968,813 | 3,507,735 | 21.96 | ||||||||||||||||||||||||

| Other: | |||||||||||||||||||||||||||||||||||

| Brea Corporate Place | 2 | 22 | 1987 | 100 | % | 329,904 | 329,904 | 2.55 | % | 73.9 | % | 3,607,569 | 3,607,569 | 14.79 | |||||||||||||||||||||

| Brea Financial Commons | 3 | 2 | 1987 | 100 | % | 165,540 | 165,540 | 1.28 | % | 90.7 | % | 3,035,782 | 3,035,782 | 20.23 | |||||||||||||||||||||

| Total Other | 5 | 24 | 495,444 | 495,444 | 3.83 | % | 79.5 | % | 6,643,351 | 6,643,351 | 16.86 | ||||||||||||||||||||||||

| Total Orange County | 7 | 33 | 927,037 | 708,776 | 7.16 | % | 76.7 | % | $ | 13,612,164 | $ | 10,151,086 | $ | 19.14 | |||||||||||||||||||||

| San Diego County | |||||||||||||||||||||||||||||||||||

| Sorrento Mesa Submarket: | |||||||||||||||||||||||||||||||||||

| San Diego Tech Center | 11 | 23 | 1984/1986 | 20 | % | 645,449 | 129,090 | 4.99 | % | 81.3 | % | $ | 10,437,173 | $ | 2,087,435 | $ | 19.89 | ||||||||||||||||||

| Total San Diego County | 11 | 23 | 645,449 | 129,090 | 4.99 | % | 81.3 | % | $ | 10,437,173 | $ | 2,087,435 | $ | 19.89 | |||||||||||||||||||||

| Other | |||||||||||||||||||||||||||||||||||

| Denver, CO – Downtown Submarket: | |||||||||||||||||||||||||||||||||||

| Wells Fargo Center – Denver | 1 | 39 | 1983 | 20 | % | 1,212,205 | 242,441 | 9.37 | % | 93.0 | % | $ | 22,254,328 | $ | 4,450,865 | $ | 19.75 | ||||||||||||||||||

| Total Other | 1 | 39 | 1,212,205 | 242,441 | 9.37 | % | 93.0 | % | $ | 22,254,328 | $ | 4,450,865 | $ | 19.75 | |||||||||||||||||||||

| Total Office Properties | 37 | 429 | 12,942,870 | 10,158,957 | 100.00 | % | 84.0 | % | $ | 243,394,626 | $ | 193,416,718 | $ | 22.39 | |||||||||||||||||||||

| Effective Office Properties | 10,158,957 | 83.7 | % | $ | 22.75 | ||||||||||||||||||||||||||||||

29

| Portfolio Overview (continued) | ||||

| Property by Submarket | Square Feet | Leased % and In-Place Rents | |||||||||||||||||||||||||||||||||

| Property | Number of Buildings | Number of Tenants | Year Built / Renovated | Ownership % | Net Building Rentable | Effective (1) | % of Net Rentable | % Leased | Total Annualized Rents (2) | Effective Annualized Rents (2) | Annualized Rent $/RSF (3) | ||||||||||||||||||||||||

| Properties in Default | |||||||||||||||||||||||||||||||||||

| 550 South Hope Street | 1 | 34 | 1991 | 100 | % | 565,738 | 565,738 | 80.8 | % | $ | 8,699,903 | $ | 8,699,903 | $ | 19.04 | ||||||||||||||||||||

| 2600 Michelson | 1 | 18 | 1986 | 100 | % | 309,742 | 309,742 | 50.2 | % | 2,405,389 | 2,405,389 | 15.48 | |||||||||||||||||||||||

| Stadium Towers Plaza | 1 | 20 | 1988 | 100 | % | 258,575 | 258,575 | 44.4 | % | 2,329,853 | 2,329,853 | 20.29 | |||||||||||||||||||||||

| 500 Orange Tower | 3 | 28 | 1987 | 100 | % | 335,898 | 335,898 | 66.7 | % | 4,063,090 | 4,063,090 | 18.15 | |||||||||||||||||||||||

| City Tower | 1 | 24 | 1988 | 100 | % | 412,839 | 412,839 | 77.4 | % | 6,785,839 | 6,785,839 | 21.23 | |||||||||||||||||||||||

| Total Properties in Default | 7 | 124 | 1,882,792 | 1,882,792 | 67.5 | % | $ | 24,284,074 | $ | 24,284,074 | $ | 19.11 | |||||||||||||||||||||||

| Total Office and Properties in Default | 14,825,662 | 12,041,749 | 81.9 | % | |||||||||||||||||||||||||||||||

| Effective Office and Properties in Default | 12,041,749 | 81.1 | % | ||||||||||||||||||||||||||||||||

| Hotel Property | SQFT | Effective SQFT | Number of Rooms | ||||||||||||||||||||||||||||||||

Westin® Hotel, Pasadena, CA | 100 | % | 266,000 | 266,000 | 350 | ||||||||||||||||||||||||||||||

| Total Office, Properties in Default and Hotel Properties | 15,091,662 | 12,307,749 | |||||||||||||||||||||||||||||||||

| Parking Properties | SQFT | Effective SQFT | Vehicle Capacity | Effective Vehicle Capacity | Annualized Parking Revenue (4) | Effective Annualized Parking Revenue (5) | Effective Annualized Parking Revenue per Vehicle Capacity (6) | ||||||||||||||||||||||||||||

| On-Site Parking | 5,457,967 | 3,965,609 | 15,917 | 11,469 | $ | 32,982,963 | $ | 28,140,501 | $ | 2,454 | |||||||||||||||||||||||||

| Off-Site Garages | 1,714,435 | 1,714,435 | 5,729 | 5,729 | 9,368,301 | 9,368,301 | 1,635 | ||||||||||||||||||||||||||||

| Properties in Default | 1,626,436 | 1,626,436 | 5,425 | 5,425 | 2,629,597 | 2,629,597 | 485 | ||||||||||||||||||||||||||||

| Total Parking Properties | 8,798,838 | 7,306,480 | 27,071 | 22,623 | $ | 44,980,861 | $ | 40,138,399 | 1,774 | ||||||||||||||||||||||||||

| Total Office, Properties in Default, Hotel and Parking Properties | 23,890,500 | 19,614,229 | |||||||||||||||||||||||||||||||||

__________

| (1) | Includes 100% of our consolidated portfolio and 20% of our MMO joint venture portfolio. |

| (2) | Annualized rent represents the annualized monthly contractual rent under existing leases as of March 31, 2011. This amount reflects total base rent before any one-time or non-recurring rent abatements but after annually recurring rent credits and is shown on a net basis; thus, for any tenant under a partial gross lease, the expense stop, or under a fully gross lease, the current year operating expenses (which may be estimates as of such date), are subtracted from gross rent. |

| (3) | Annualized rent per rentable square foot represents annualized rent as computed above, divided by the total square footage under lease as of the same date. |

| (4) | Annualized parking revenue represents the annualized quarterly parking revenue as of March 31, 2011. |

| (5) | Effective annualized parking revenue represents the annualized quarterly parking revenue as of March 31, 2011 adjusted to include 100% of our consolidated portfolio and 20% of our MMO joint venture portfolio. |

| (6) | Effective annualized parking revenue per vehicle capacity represents the effective annualized parking revenue divided by the effective vehicle capacity. |

30

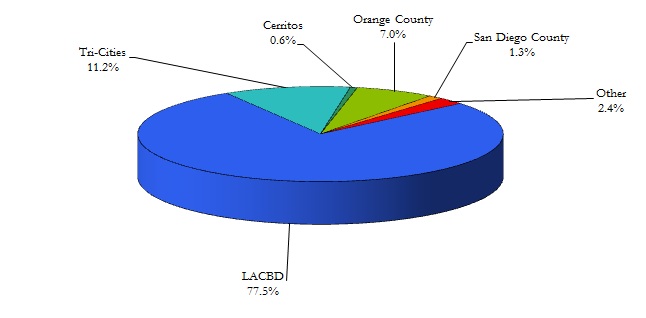

| Portfolio Geographic Distribution (Excluding Properties in Default) (1) | ||||

__________

| (1) | The Portfolio Geographic Distribution is based on effective net rentable square feet for our Office Properties and includes our pro-rata share of the MMO joint venture. |

31

| Portfolio Overview — Leased Percentages and Weighted Average Remaining Lease Term | ||||

Ownership ( % ) | Weighted Average Remaining Lease Term (in years) | ||||||||||||||||||

| % Leased | |||||||||||||||||||

| Q1 2011 | Q4 2010 | Q3 2010 | Q2 2010 | Q1 2010 | |||||||||||||||

| Office Properties | |||||||||||||||||||

| Gas Company Tower | 100 | % | 8.4 | 94.6 | % | 94.6 | % | 92.6 | % | 92.5 | % | 92.5 | % | ||||||

| US Bank Tower | 100 | % | 4.6 | 58.5 | % | 57.9 | % | 57.5 | % | 54.3 | % | 62.2 | % | ||||||

| Wells Fargo Tower | 100 | % | 4.2 | 92.6 | % | 94.3 | % | 94.4 | % | 94.3 | % | 94.1 | % | ||||||

| Two California Plaza | 100 | % | 3.9 | 81.1 | % | 81.9 | % | 82.0 | % | 83.9 | % | 83.8 | % | ||||||

| KPMG Tower | 100 | % | 7.8 | 95.5 | % | 94.3 | % | 93.9 | % | 93.8 | % | 93.9 | % | ||||||

| 777 Tower | 100 | % | 4.9 | 79.4 | % | 79.6 | % | 77.4 | % | 75.3 | % | 75.6 | % | ||||||

| One California Plaza | 20 | % | 4.3 | 77.2 | % | 76.6 | % | 76.5 | % | 76.5 | % | 76.2 | % | ||||||

| Glendale Center | 100 | % | 3.4 | 93.8 | % | 93.8 | % | 100.0 | % | 100.0 | % | 100.0 | % | ||||||

| 801 North Brand | 100 | % | 1.8 | 83.2 | % | 82.3 | % | 82.3 | % | 81.7 | % | 81.4 | % | ||||||

| 701 North Brand (1) | 100 | % | 3.4 | 97.2 | % | 97.2 | % | 97.2 | % | 97.2 | % | 97.2 | % | ||||||

| 700 North Central | 100 | % | 2.8 | 66.7 | % | 66.7 | % | 73.4 | % | 73.4 | % | 75.5 | % | ||||||

| Plaza Las Fuentes | 100 | % | 7.7 | 93.9 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | ||||||

| Cerritos – Phase I | 20 | % | 3.5 | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | ||||||

| Cerritos – Phase II | 20 | % | 5.2 | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | ||||||

| 3800 Chapman | 100 | % | 4.2 | 75.9 | % | 75.9 | % | 75.9 | % | 75.9 | % | 75.9 | % | ||||||

| Stadium Gateway | 20 | % | 4.1 | 72.2 | % | 72.2 | % | 72.2 | % | 88.0 | % | 88.0 | % | ||||||

| Brea Corporate Place | 100 | % | 3.2 | 73.9 | % | 73.9 | % | 73.3 | % | 71.6 | % | 71.6 | % | ||||||

| Brea Financial Commons | 100 | % | 3.1 | 90.7 | % | 90.7 | % | 90.7 | % | 90.7 | % | 90.7 | % | ||||||

| San Diego Tech Center | 20 | % | 3.6 | 81.3 | % | 82.3 | % | 78.5 | % | 79.3 | % | 80.0 | % | ||||||

| Wells Fargo Center – Denver | 20 | % | 6.3 | 93.0 | % | 92.5 | % | 92.0 | % | 92.4 | % | 91.7 | % | ||||||