As filed with the Securities and Exchange Commission on April 5, 2007

Registration No. 333-134269

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Post-Effective Amendment No. 1

to

FORM SB-2

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

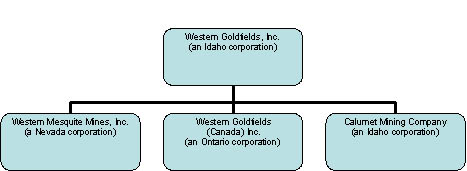

WESTERN GOLDFIELDS INC.

(Exact name of registrant as specified in its charter)

Ontario (State or other jurisdiction of incorporation or organization) | 1040 (Primary Standard Industrial Classification Code Number) | Not Applicable (I.R.S. Employer Identification No.) |

2 Bloor Street West

Suite 2102, P.O. Box 110

Toronto, Ontario

Canada M4W 3E2

(416) 324-6000

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Western Mesquite Mines, Inc.

6502 East Highway 78

Brawley, California 92227

(928) 341-4653 Extension 103

(Name, address, including zip code, and telephone number, including area code, of agent for service)

With copies to:

Cameron A. Mingay Cassels Brock & Blackwell LLP 2100 Scotia Plaza 40 King Street West Toronto, Ontario Canada, M5H 3C2 (416) 869-5300 | Christopher J. Cummings Shearman & Sterling LLP Commerce Court West 199 Bay Street, Suite 4405 Toronto, Ontario Canada M5L 1E8 (416) 360-8484 |

Approximate date of commencement of proposed sale to the public: From time to time after this post-effective amendment is declared effective.

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: o

If delivery of the prospectus is expected to be made pursuant to Rule 434, check the following box: o

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until this Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell nor is it seeking an offer to buy these securities in any state where the offer or sale is not permitted.

Subject to completion, dated April 5, 2007.

WESTERN GOLDFIELDS, INC.

49,638,450 Shares of Common Stock

$0.01 par value

We are registering up to 49,638,450 shares of our common stock, 12,624,999 shares of which are issuable upon the exercise of warrants and 13,825,950 shares of which are issuable upon the exercise of options, for sale by certain of our shareholders from time to time. The selling shareholders will receive all the proceeds from the sale of the offered shares. See “Selling Shareholders” on page 46 of this prospectus.

Our common stock is listed on the Toronto Stock Exchange under the Symbol "WGI" and quoted on the OTC Bulletin Board under the symbol “WGDF.OB.” On April 4, the last reported sale price of our common stock on the Toronto Stock Exchange was cdn$2.27 per share and on the OTC Bulletin Board was $1.96 per share.

Investing in our common stock involves a high degree of risk. See “Risk Factors” beginning on page 4 to read about certain risks you should consider before buying shares of our common stock.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

Our principal executive offices are located at 2 Bloor Street West, Suite 2012, P.O. Box 110, Toronto, Ontario, Canada, M4M 3E2. Our telephone number is (416) 324-6000.

The date of this Prospectus is , 2007.

| 1 | |

| 4 | |

| 11 | |

| 12 | |

| 12 | |

| 14 | |

| 24 | |

| 39 | |

| 41 | |

| 44 | |

| 47 | |

| 49 | |

| 51 | |

| 54 | |

| 56 | |

| 58 | |

| 58 | |

| 58 | |

| F-1 |

This prospectus is part of a registration statement we filed with the Securities and Exchange Commission. You should rely on the information provided in this prospectus. Neither we nor the selling shareholders listed in this prospectus have authorized anyone to provide you with information different from that contained in this prospectus. The selling shareholders are offering to sell, and seeking offers to buy, shares of common stock only in jurisdictions where offers and sales are permitted. The information contained in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or of any sale of common stock. Applicable SEC rules may require us to update this prospectus in the future.

The Company

We were incorporated as Bismarck Mining in the State of Idaho in 1924 and changed our name to Western Goldfields, Inc. in July 2002. We are an independent gold producer focused on completing the expansion of the Mesquite Mine (“Mesquite” or “the Mine”) in Imperial County, California and restoring the Mine to full production.

In early 2003, we commenced the process of acquiring the Mesquite Mine from Hospah Coal Company (“Hospah”), a wholly-owned subsidiary of Newmont Mining Corporation (“Newmont”). In November 2003, we acquired a 100% interest in Mesquite pursuant to an asset purchase agreement. These assets are now held by our wholly-owned subsidiary, Western Mesquite Mining Inc. The transaction included:

| · | assumption of reclamation and closure liabilities at the property, estimated at $6,000,000; |

| · | provision of approximately $7,800,000 in reclamation bonds to various governmental authorities replacing equivalent bonds previously provided by Newmont. On January 22, 2007, we were notified that the required amount of bonding had been increased to $8,600,000; |

| · | issuance of additional shares of our common stock and warrants to purchase our common stock valued at approximately $3,100,000. As a result of the transaction, Newmont acquired 3,454,468 shares of our common stock and warrants to purchase an additional 8,091,180 shares of our common stock. On April 18, 2005, Newmont surrendered warrants to purchase 2,035,000 shares of common stock; |

| · | the grant to Newmont of a perpetual net smelter return royalty ranging, according to location, from 0.5% to 2.0% on any newly mined ore; and |

| · | the grant to Newmont of a net operating cash flow royalty equal to 50% of the proceeds received from the sale of gold and silver produced from materials in place on the heap leach pads on the date of the acquisition, less certain operating costs, capital expenses and other allowances and adjustments. |

Mesquite is our most important asset, providing us with current gold production from material that was placed on the heap leach pads by Newmont and previous owners of the property. The gold produced has provided us with operating cash flow to help sustain our operations pending the reactivation of the Mine.

Our immediate priority is to finance the development of the Mesquite Mine to bring it back into full production based on the feasibility report completed in August 2006. See “Our Feasibility Study” below and “Forward-Looking Statements.”

In February 2006, we conducted a review of certain of our other exploration properties which were located in California, Idaho and Nevada. Based on the outcome of this review, we disposed of these exploration properties on June 19, 2006.

We sell our gold production to bullion dealers and refiners. In 2006, sales to two customers totaled $6,946,576 and $912,640 respectively. In 2005, sales to four customers totaled $3,911,655, $3,875,114, $1,510,030 and $501,350, respectively.

The Offering

| Common stock offered by the selling shareholders | 49,638,450 shares | |

| Common stock outstanding as of February 28, 2007 | 112,236,643 shares | |

| Use of Proceeds | We will not receive any of the proceeds from the sale of the shares by the selling shareholders. We may receive proceeds in connection with the exercise of warrants, the underlying shares of which may be sold by the selling shareholders under this prospectus. | |

| Risk Factors | An investment in our securities involves a high degree of risk and could result in a loss of your entire investment. Prior to making an investment decision, you should carefully consider all of the information in this prospectus and, in particular, you should evaluate the risk factors set forth under the caption “Risk Factors” beginning on page 4. | |

| BX Symbol | WGI | |

| OTC Bulletin Board Symbol | WGDF.OB |

An investment in our common stock involves a high degree of risk. You should carefully consider the risks described below and the other information contained in this prospectus before deciding to invest in our common stock.

Risks Related To Our Operations

If we continue to experience significant operating losses, we may need additional financing to fund our operations, which may not be available to us.

We emerged from dormancy in 1999 to pursue mineral exploration and development opportunities, and we have a limited operating history in our current form. Since we reorganized our business in 2003, we have incurred operating costs in each quarter but only began to generate any revenue in January 2004. We have incurred cumulative net losses of approximately $25.7 million through December 31, 2006, and we expect to experience additional net losses in 2007.

We have a limited history of earnings or cash flow from our operations. In addition, in our acquisition of the Mesquite Mine, we purchased an asset that had been scheduled for closure by the previous owner. Newmont Mining Corporation operated the Mesquite Mine in a limited caretaker mode with a view towards closure until our acquisition of the Mesquite Mine in November 2003. At that time, Newmont Mining Corporation did not operate the Mesquite Mine as an operating mine but as an operation to be discontinued, and we may not be able to successfully reopen and operate the mine and to execute our business strategy.

We believe that additional financing will be required in the future to fund our operations. While we may attempt to generate additional working capital through the operation, development, sale or possible joint venture development of our properties, there is no assurance that any such activity will generate funds that will be available for operations. We do not know whether additional financing will be available when needed or on acceptable terms, if at all. If we are unable to raise additional financing when necessary, we may have to delay our exploration and development efforts or any property acquisitions or be forced to cease operations.

Exploration and production may not prove successful, will involve risks and have no guaranteed outcome.

Our business operations are subject to risks and hazards inherent in the mining industry. The reactivation of the Mesquite Mine and the exploration for additional reserves involve significant risks that even a combination of careful evaluation, experience and knowledge may not eliminate.

Our exploration and production may be hampered by mining, heritage and environmental legislation, industrial accidents, industrial disputes, cost overruns, land claims and compensation and other unforeseen contingencies. Our success also depends on the delineation of economically recoverable reserves, the availability and cost of required development capital, movement in the price of commodities, as well as obtaining all necessary consents and approvals for the conduct of our production and exploration activities.

Exploration and production at the Mesquite Mine may prove unsuccessful. Mineable reserves may become depleted resulting in a reduction of the value of those tenements and a diminution in our cash flow and cash reserves as well as possible relinquishment of the exploration and mining tenements.

Risks involved in mining operations include unusual and unexpected geologic formations, seismic activity, rock bursts, cave-ins, flooding and other conditions involved in the drilling and removal of any material, any of which could result in damage to life or property, environmental damage and possible legal liability.

Whether income will result from the Mesquite Mine depends on the successful establishment of mining operations. Factors including costs, actual mineralization, consistency and reliability of ore grades and commodity prices affect successful project development. The reactivation and efficient operation of processing facilities, the existence of competent operational management and prudent financial administration, as well as the availability and reliability of appropriately skilled and experienced consultants also can affect successful project development.

We have 46 full-time employees including our executive officers, and we are dependent on our directors, officers and third-party contractors.

We have five executive officers and 41 other individuals who are full time employees. We have a small number of individuals in management. We are also dependent upon the personal efforts and abilities of our consultants who we engage from time to time. Our consultants devote less than all of their time and efforts to our operations. We are currently seeking to hire geologists and engineers on a permanent basis and unless and until we do so we must rely on consultants paid on a per diem basis. Competition for such personnel is intense, and there is no assurance that we will be able to hire and retain such personnel in the future. We are also dependent upon the efforts and abilities of our officers and directors. While much of our operations are handled by our employees, our directors and officers direct our policies and manage our operations. The loss of any one of these individuals could adversely affect our business.

Our business is dependent on good labor and employment relations.

Production at the Mesquite Mine is dependent upon the efforts of our employees. Relations between us and our employees may be impacted by changes in labor relations which may be introduced by, among others, employee groups, unions, and the relevant governmental authorities in whose jurisdictions we carry on business. Adverse changes in such legislation or in the relationship between us and our employees may have a material adverse effect on our business, results of operations, and financial condition.

If we do not continually obtain additional deposits for gold production, we will be unable to achieve or maintain targeted production levels.

We must continually replace gold deposits depleted by production. Our Mesquite Mine operation began producing gold from material that the previous owners had placed on the heap leach pads. Depleted deposits must be replaced by expanding operations on our existing property or by locating new deposits in order for us to maintain our production levels over the long term. Success in exploration for gold is uncertain. There is no assurance that additional commercially viable mineral deposit exist on any other parts of our property. As a result, our metals inventory may decline as minerals are produced without adequate replacement.

Estimates of proven and probable deposits are uncertain, and any inaccuracies could result in the estimates being overstated.

Estimates of proven and probable deposits and costs of goods sold are subject to considerable uncertainty. Such estimates are, to a large extent, based on interpretations of geologic data obtained from drill holes and other sampling techniques. Gold producers use feasibility studies to derive estimates of costs of goods sold based upon anticipated tonnage and grades of minerals to be mined and processed, the predicted configuration of the deposits, expected recovery rates, comparable facility, equipment and operating costs, and other factors. Actual costs of goods sold and economic returns on projects may differ significantly from original estimates. Further, it may take many years from the initial phase of drilling before production is possible and, during that time, the economic feasibility of exploiting a discovery may change. Any significant inaccuracies in these interpretations or assumptions or changes of conditions could cause the quantities and net present value of our deposits to be overstated. The data included and referred to in this prospectus represent only estimates. You should not assume that the present value referred to in this prospectus represents the current market value of our estimated deposits.

A shortage of equipment and supplies could adversely affect our ability to operate our business.

We are dependent on various supplies and equipment to carry out our mining operations. The shortage of such supplies, equipment and parts could have a material adverse effect on our ability to carry out our operations and therefore limit or increase the cost of production.

Increased costs could affect our financial condition.

Costs at the Mesquite Mine frequently are subject to variation from one year to the next due to a number of factors, such as changing ore grade, metallurgy and revisions to mine plans in response to the physical shape and location of the ore body. In addition, costs are affected by the price of commodities such as fuel and electricity. Such commodities are at times subject to volatile price movements, including increases that could make production at certain operations less profitable. A material increase in costs at any significant location could have a significant effect on or profitability.

Unforeseen title defects may result in a loss of entitlement to production and reserves.

Our ownership of the Mesquite Mine could be subject to prior undetected claims or interests. Although we have performed a title review of the Mesquite Mine, the review does not guarantee or certify that an unforeseen defect in the chain of title will not arise to defeat a claim by us. If any such defect were to arise, our entitlement to the reserves associated with the Mesquite Mine could be jeopardized, and could have a material adverse effect on our financial condition, results of operations and our ability to timely execute our business plan.

Our business activities are subject to extensive laws and regulations that expose us to significant compliance costs and the risk of lawsuits.

Our operations and exploration and development activities are subject to extensive United States and Canadian federal, state, provincial and local laws and regulations governing various matters, including:

| · | taxation; |

| · | mining royalties; |

| · | environmental protection; and |

| · | labor standards and occupational health and safety, including mine safety. |

The costs associated with compliance with these laws and regulations are substantial and possible future laws and regulations, changes to existing laws and regulations or more stringent enforcement of current laws and regulations by governmental authorities, could cause additional expense, capital expenditures, restrictions on or suspensions of our operations and delays in the development of the Mesquite Mine. Moreover, these laws and regulations may allow governmental authorities and private parties to bring lawsuits based upon damages to property and injury to persons resulting from the health and safety impacts of our past and current operations, and could lead to the imposition of substantial fines, penalties or other civil or criminal sanctions.

Our operations are subject to numerous governmental permits which are difficult to obtain and we may not be able to obtain or renew all of the permits we require.

In the ordinary course of business, we are required to obtain and renew governmental permits for the operation, recommissioning and expansion of the Mesquite Mine. Obtaining or renewing the necessary governmental permits is a complex and time-consuming process involving costly undertakings on our part. The duration and success of our efforts to obtain and renew permits are contingent upon many variables not within our control including the interpretation of applicable requirements implemented by the permitting authority. We may not be able to obtain or renew permits that are necessary to our operations, or the cost to obtain or renew permits may exceed our estimates. Failure to comply with applicable environmental and health and safety laws and regulations may result in injunctions, fines, suspension or revocation of permits and other penalties. There can be no assurance that the Company has been or will at all times be in full compliance with all such laws and regulations and with its environmental and health and safety permits or that the company has all required permits. The costs and delays associated with compliance with these laws, regulations and permits and with the permitting process could stop the Company from proceeding with the operation or development of the Mesquite Mine or increase the costs of development or production and may materially adversely affect the Company’s business, results of operations or financial condition.

We are subject to substantial costs for compliance with environmental laws and regulation and may be subject to substantial costs for liability related to environmental claims.

Our exploration, production and processing operations are extensively regulated under various U.S. federal, state and local laws relating to the protection of air and water quality, hazardous waste management, endangered species, and mine reclamation. We may be subject to future liability for environmental costs, including capital costs to comply with environmental laws, costs associated with the remediation of soil or groundwater contamination at our current and formerly owned or operated properties, and reclamation and closure costs upon cessation of our operations at the Mesquite Mine. In addition, we may be subject to reclamation costs for our claims, even if we have not conducted the activity on those properties. Further, the regulatory environment for our operations could change in ways that would substantially increase our liability or the costs of compliance and that could have a material adverse effect on our operations or financial position.

Various laws and permits require that financial assurances be in place for certain environmental and reclamation obligations and other potential liabilities. We have an existing insurance policy for our reclamation costs at the Mesquite Mine, but we are in the process of negotiating a supplement to that policy to cover the increase in reclamation costs due to Mesquite’s expansion. We may be unable to undertake any trenching, drilling, or development on any of our properties until we obtain financial assurances to cover potential liabilities.

Risks Related To Our Industry

We are dependent on the price of gold, which is subject to numerous factors beyond our control. A substantial or extended decline in gold prices would have a material adverse effect on our revenues, profits and cash flows.

Our business is extremely dependent on the price of gold, which is affected by numerous factors beyond our control. Factors tending to put downward pressure on the price of gold include:

| · | sales or leasing of gold by governments and central banks; |

| · | a low rate of inflation and a strong U.S. dollar; |

| · | global and regional recession or reduced economic activity; |

| · | speculative trading; |

| · | the demand for gold for industrial uses, use in jewelry, and investment; |

| · | high supply of gold from production, disinvestment, scrap and hedging; |

| · | interest rates; |

| · | sales by gold producers in forward transactions and other hedging; |

| · | the production and cost levels for gold in major gold-producing nations; and |

| · | the cost level (in local currencies) for gold in major consuming nations. |

Any drop in the price of gold would adversely impact our future revenues, profits and cash flows. In addition, sustained low gold prices can:

| · | reduce revenues further by production cutbacks due to cessation of the mining of deposits or portions of deposits that have become uneconomic at the then-prevailing gold price; |

| · | halt or delay the development of new projects; and |

| · | reduce funds available for exploration, with the result that depleted minerals are not replaced. |

During the last five years, the average annual market price of gold has fluctuated between $310 per ounce and $603 per ounce, as shown in the table below.

2002 | 2003 | 2004 | 2005 | 2006 | ||||||

| $310 | $364 | $406 | $445 | $603 | ||||||

We are subject to substantial costs for compliance with environmental laws and regulations and may be subject to substantial costs for liability related to environmental claims.

Our exploration, production and processing operations are extensively regulated under various U.S. federal, state and local laws relating to the protection of air and water quality, hazardous waste management and mine reclamation. We may have potential future liability for environmental costs. In addition, we may be subject to reclamation costs for our claims, even if we have not conducted the activity on those properties. Further, the regulatory environment for our operations could change in ways that would substantially increase our liability or the costs of compliance and that could have a material adverse effect on our operations or financial position.

Various laws and permits require that financial assurances be in place for certain environmental and reclamation obligations and other potential liabilities. We may be unable to undertake any trenching, drilling, or development on any of our properties until we obtain financial assurances to cover potential liabilities.

Our operations may be adversely affected by risks and hazards associated with the mining industry.

Our business is subject to a number of risks and hazards including adverse environmental effects, technical difficulties due to unusual or unexpected geologic formations, and pit wall failures.

Such risks could result in personal injury, environmental damage, damage to and destruction of our production facility, delays in mining and liability. For some of these risks, we maintain insurance to protect against these losses at levels consistent with our historical experience and industry practice. However, we may not be able to maintain current levels of insurance, particularly if there is a significant increase in the cost of premiums. Insurance against environmental risks is generally expensive and may not continue to be available for us and other companies in our industry. Our current policies may not cover all losses. Our existing policies may not be sufficient to cover all liabilities arising under environmental law or relating to hazardous substances. Moreover, in the event that we are unable to fully pay for the cost of remedying an environmental problem, we might be required to suspend or significantly curtail operations or enter into other interim compliance measures.

Numerous other companies compete in the mining industry, many of which have greater resources and technical capacity than us, as a result, we may be unable to effectively compete in our industry, which could have a material adverse effect on our future operations.

The mineral exploration and mining business is competitive in all of its phases. We compete with numerous other companies and individuals, including competitors with greater financial, technical and other resources than us, in the search for and the acquisition of attractive mineral properties. Our ability to operate successfully in the future will depend not only on its ability to develop the Mesquite Mine, but also on our ability to select and acquire suitable producing properties or prospects for mineral exploration. We may be unable to compete successfully with our competitors in acquiring such properties or prospects on terms we consider acceptable, if at all.

Gold producers must continually obtain additional reserves.

Gold producers must continually replace reserves depleted by production. Depleted reserves must be replaced by expanding known ore bodies or by locating new deposits in order for producers to maintain production levels over the long term. Exploration is highly speculative in nature, involves many risks and frequently is unproductive. No assurances can be given that any of our new or ongoing exploration programs will result in new mineral producing operations. Once mineralization is discovered, it may take many years from the initial phases of drilling until production is possible, during which time the economic feasibility of production may change.

Risks Related To Our Common Stock

Certain of our shareholders may have preemptive rights to acquire shares of our common stock.

We were incorporated in Idaho in 1924. Prior to July 1, 1997, Idaho law generally provided shareholders with preemptive rights unless otherwise provided in a company’s articles of incorporation. Our articles of incorporation did not address preemptive rights. Prior to July 1997, approximately 500,000 shares of our common stock were issued and outstanding, after giving effect to the one for three reverse-split of our shares in June 2002.

Preemptive rights generally give the shareholders of a corporation the right, with certain exceptions, to purchase, before they can be sold to others, (i) common stock issued by the corporation for cash and (ii) other securities issued by the corporation for cash that are convertible into or carry a right to subscribe for or acquire shares of common stock of the corporation.

Shareholders who own shares of our common stock issued prior to July 1, 1997 may have preemptive rights to purchase shares of our common stock to maintain their proportional stock ownership in the Company; however, we believe there is uncertainty with respect to the existence of such rights. In light of this uncertainty and without admitting that such rights exist, in connection with our public offering announced January 17, 2007, we provided holders of our common stock whose holdings can be traced to common stock issued prior to July 1, 1997, the opportunity to purchase shares on the same terms as such public offering.

The Company has not been able to identify all holders of the shares of our common stock issued prior to July 1, 1997. If preemptive rights exist and if shareholders to whom we do not offer the opportunity to purchase shares on the same terms as in our public offering of common stock announced January 17, 2007 or any subsequent offering were able to successfully assert preemptive rights, we could be required to issue shares of common stock to such shareholders as a result of such offerings. In addition, we could be required to issue shares or other securities convertible into our common stock as a result of past issuances and at a value which is significantly lower than the price of the shares of common stock offered to you. In such event, our share capital would be diluted significantly. During the period from January 17, 2003 through January 17, 2007, the Company issued for cash preferred shares, preferred share purchase warrants and units consisting of common shares and common share purchase warrants, all convertible or exercisable into a total of approximately 72.2 million common shares for average total consideration of $0.47 per common share. Due to the Company’s long corporate history and various changes in Idaho laws from 1924 to the present, affected shareholders may have slightly varying preemptive rights, and some affected shareholders may also have preemptive rights with respect to past issuances other than for cash.

If preemptive rights exist and if shareholders were able to successfully assert preemptive rights with respect to past or future issuances, we also could be required to pay money damages to such shareholders, which damages could be based on the difference in value of the shares or other securities between the time of issuance and the time of claim. We may not have enough cash to pay any money damages awarded with respect to such rights. In such event, we would need to finance such payments through additional debt or equity financing, which might not be available on acceptable terms, or at all. If we were unable to raise additional financing when necessary, we could be forced to delay our mine development or cease or curtail operations.

In cases primarily involving closely-held companies, courts have invalidated shares of common stock or other securities issued in violation of preemptive rights. If any shareholders were able to successfully assert preemptive rights and such remedy were granted the effect on the Company could be materially adverse.

We believe that Idaho law would bar a claim by a shareholder with respect to any issuance prior to January 17, 2003 or, alternatively January 17, 2004. As of January 17, 2003, shares issued prior to 1997 represented approximately 5.53% of the outstanding share capital of the Company, which we believe would be the aggregate ownership interest which shareholders who were able to successfully assert any preemptive rights could seek to maintain. However, we cannot assure you that a court would not reach different conclusions. If any person should seek to assert preemptive rights, the Company intends to vigorously defend the matter.

We will likely require additional capital in the future and no assurance can be given that such capital will be available at all or available on terms acceptable to us.

It is likely that we will need to raise further capital to fund aspects of the business. The success and the pricing of any such financing will be dependent upon the prevailing market conditions at that time. If additional capital is raised by an issue of securities, this may have the effect of diluting the interests of our existing shareholders. Any debt financing, if available, may involve financial covenants that limit our operations. If we cannot obtain such additional financing, we may be required to reduce the scope of any activities that could adversely affect our business, operating results and financial condition.

Failure by us to achieve and maintain effective internal control over financial reporting in accordance with the rules of the SEC could harm our business and operating results and/or result in a loss of investor confidence in our financial reports, which could have a material adverse effect on our business and stock price.

As a public company, we are required to comply with Section 404 of the Sarbanes-Oxley Act, and, beginning with the year ending December 31, 2007, we will have to obtain an annual attestation from our independent auditors regarding our internal control over financial reporting and management’s assessment of internal control over financial reporting. We cannot be certain as to the timing of completion of our internal control evaluation, testing and remediation actions or of their impact on our operations. Upon completion of this process, we may identify control deficiencies of varying degrees of severity under applicable SEC and Public Company Accounting Oversight Board rules and regulations that remain unremediated. We will be required to report, among other things, control deficiencies that constitute a “material weakness” or changes in internal controls that, or that are reasonably likely to, materially affect internal controls over financial reporting. A “material weakness” is a significant deficiency or combination of significant deficiencies that results in more than a remote likelihood that a material misstatement of the annual or interim financial statements will not be prevented or detected. If we fail to implement the requirements of Section 404 in a timely manner, we might be subject to sanctions or investigation by regulatory authorities, including the SEC. In addition, failure to comply with Section 404 or the report by us of a material weakness may cause investors to lose confidence in our financial statements, and our stock price may be adversely affected as a result. If we fail to remedy any material weakness, our financial statements may be inaccurate, we may face restricted access to the capital markets and our stock price may be adversely affected.

All of our directors and officers may not be subject to suit in the United States.

Our directors and officers reside in Canada and the United Kingdom. As a result, it may be difficult or impossible to effect service of process within the United States upon those individuals, to bring suit against any of those individuals in the United States or to enforce in the United State courts any judgment obtained there against any of those individuals predicated upon any civil liability provisions of the United States federal securities laws. Investors should not assume that Canadian or British courts will enforce judgments of United States federal securities courts against any director or officer residing in Canada or the United Kingdom, including judgments obtained in actions predicated upon the civil liability provisions of the United States federal securities laws or the securities or “blue sky” laws of any state within the United States, or will enforce, in original actions, liabilities against such directors or officers predicated upon the United States federal securities laws or any such state securities or blue sky laws.

We may experience volatility in our stock price.

The market price of our common stock may fluctuate significantly in response to a number of factors, some of which are beyond our control, including:

| · | quarterly variations in operating results; |

| · | changes in financial estimates by securities analysts; |

| · | changes in market valuations of other similar companies; |

| · | announcements by us or our competitors of new products or of significant technical innovations, contracts, acquisitions, strategic partnerships or joint ventures; |

| · | additions or departures of key personnel; |

| · | any deviations in net sales or in losses from levels expected by securities analysts; and |

| · | future sales of common stock |

As a result of any of these factors, the market price of our shares of common stock at any given point in time may not accurately reflect our long-term value. Securities class action litigation often has been brought against companies following periods of volatility in the market price of their securities. We may in the future be the target of similar litigation. Securities litigation could result in substantial costs and damages and divert management’s attention and resources.

Because our securities trade on the OTC Bulletin Board, your ability to sell your shares in the secondary market may be limited.

If you trade our securities on the OTC Bulletin Board, such trades will be subject to the rules promulgated under the Securities Exchange Act of 1934, as amended, which impose additional sales practice requirements on broker-dealers that sell securities governed by these rules to persons other than established customers and “accredited investors” (generally, individuals with a net worth in excess of $1,000,000 or annual individual income exceeding $200,000 or $300,000 jointly with their spouses). For such transactions, the broker-dealer must determine whether persons that are not established customers or accredited investors qualify under the rule for purchasing such securities and must receive that person’s written consent to the transaction prior to sale. Consequently, these rules may adversely affect the ability of purchasers to sell our securities through the OTC Bulletin Board and otherwise affect the trading market in our securities on the OTC Bulletin Board. Because our shares are deemed “penny stocks” in the United States, you may have difficulty selling them in the secondary trading market in the United States.

The Securities and Exchange Commission has adopted regulations which generally define a “penny stock” to be any equity security that has a market price (as defined in the regulations) less than $5.00 per share or with an exercise price of less than $5.00 per share, subject to certain exceptions. Additionally, if the equity security is not registered or authorized on a national securities exchange or Nasdaq, the equity security also would constitute a “penny stock.” As our common stock falls within the definition of penny stock in the United States, these regulations require the delivery, prior to any transaction in the United States involving our common stock, of a risk disclosure schedule explaining the penny stock market and the risks associated with it. Disclosure is also required to be made about compensation payable to both the broker-dealer and the registered representative and current quotations for the securities. In addition, monthly statements are required to be sent disclosing recent price information for the penny stocks. The ability of broker/dealers to sell our common stock and the ability of shareholders to sell our common stock in the secondary market would be limited. As a result, the market liquidity for our common stock would be severely and adversely affected. We can provide no assurance that trading in our common stock will not be subject to these or other regulations in the future, which would negatively affect the market for our common stock.

Any future restatement of our financial statements may adversely affect the trading price of our common stock.

In August 2006 we completed the restatement of our consolidated financial statements for the years ended December 31, 2005 and 2004, and we believe they are presented in accordance with the requirements of United States generally accepted accounting principles. However, such restatements do not prevent future changes or adjustments, including additional restatements. If there were future restatements of our consolidated financial statements, such restatements may adversely affect the trading price of the our common stock.

Our articles of incorporation contain provisions that discourage a change of control.

Our articles of incorporation contain provisions that could discourage an acquisition or change of control without our board of directors’ approval. Our articles of incorporation authorize our board of directors to issue preferred stock without shareholder approval. If our board of directors elects to issue preferred stock, it could be more difficult for a third party to acquire control of us, even if that change of control might be beneficial to our shareholders.

We have not paid dividends in the past and do not anticipate doing so in the future.

No dividends on our shares of common stock has been paid by us to date. We anticipates that we will retain all future earnings and other cash resources for the future operation and development of our business. Additionally, we do not intend to declare or pay any cash dividends in the foreseeable future. Payment of any future dividends will be at the discretion of our board of directors, after taking into account many factors, including our operating results, financial condition, and current and anticipated cash needs.

We will not receive any of the proceeds from the sale of the shares owned by the selling shareholders. We may receive proceeds in connection with the exercise of warrants, the underlying shares of which may in turn be sold by selling shareholder. Although the timing of our receipt of any such proceeds are uncertain, such proceeds, if received, will be used for general corporate purposes.

Market for Our Common Stock

Our common stock is quoted under the symbol “WGDF.OB” on the Over-the-Counter Bulletin Board and since August 28, 2006 has been quoted under the symbol “WGI.TO” on The Toronto Stock Exchange. The following tables set forth the high and low bid information for our common stock for the periods indicated in the past two fiscal years, which reflect inter-dealer prices, without retail mark-up, mark-down or commission and may not represent actual transactions:

Over-the-Counter Bulletin Board

Quarter Ended | High Bid Quotation | Low Bid Quotation | |||||

2007: | |||||||

| First quarter | $ | 2.44 | $ | 1.60 | |||

2006: | |||||||

| Fourth quarter | $ | 2.43 | $ | 1.26 | |||

| Third quarter | $ | 2.70 | $ | 1.70 | |||

| Second quarter | $ | 3.08 | $ | 0.83 | |||

| First quarter | $ | 0.92 | $ | 0.16 | |||

2005: | |||||||

| Fourth quarter | $ | 0.29 | $ | 0.16 | |||

| Third quarter | $ | 0.29 | $ | 0.15 | |||

| Second quarter | $ | 0.46 | $ | 0.26 | |||

| First quarter | $ | 0.56 | $ | 0.33 | |||

The Toronto Stock Exchange (in Canadian dollars)

Quarter Ended | High Bid Quotation | Low Bid Quotation | |||||

2007: | |||||||

| First quarter | C$ | 2.85 | C$ | 1.90 | |||

2006: | |||||||

| Fourth quarter | C$ | 2.95 | C$ | 1.40 | |||

| Third quarter (August 28, 2006 through September 30, 2006) | C$ | 3.50 | C$ | 1.92 | |||

Holders

As of February 28, 2007, there were approximately 912 shareholders on record of our common stock, however we believe that there are additional beneficial owners of our common stock who own our stock in “street name.”

Dividends

We have never declared or paid dividends on our common stock. We currently intend to retain future earnings, if any, for use in our business, and, therefore, we do not anticipate declaring or paying any dividends in the foreseeable future. Payments of future dividends, if any, will be at the discretion of our board of directors after taking into account various factors, including our financial condition, operating results, current and anticipated cash needs and plans for expansion.

We have included and from time to time may make in our public filings, press releases or other public statements, certain statements, including, without limitation, those under “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included in this prospectus. In some cases these statements are identifiable through the use of words such as “anticipate,” “believe,” “estimate,” “expect,” “intend,” “plan,” “project,” “target,” “can,” “could,” “may,” “should,” “will,” “would” and similar expressions. You are cautioned not to place undue reliance on these forward-looking statements. In addition, our management may make forward-looking statements to analysts, investors, representatives of the media and others. These forward-looking statements are not historical facts and represent only our beliefs regarding future events and by their nature, are inherently uncertain and beyond our control.

The nature of our business makes predicting the future trends of our revenues, expenses and net income difficult. The risks and uncertainties involved in our business could affect the matters referred to in such statements and it is possible that our actual results may differ materially from the anticipated results indicated in these forward looking statements. Important factors that could cause actual results to differ from those in the forward-looking statements include, without limitation:

· the effect of political, economic and market conditions and geopolitical events;

· the actions and initiatives of current and potential competitors;

· our reputation;

· investor sentiment; and

· other risks and uncertainties detailed elsewhere throughout this prospectus.

Accordingly, you are cautioned not to place undue reliance on forward-looking statements, which speak only as of the date on which they are made. We undertake no obligation to update publicly or revise any forward-looking statements to reflect the impact of circumstances or events that arise after the dates they are made, whether as a result of new information, future events or otherwise except as required by applicable law. You should, however, consult further disclosures we may make in future filings of our Annual Reports on Form 10-KSB, Quarterly Reports on Form 10-QSB and Current Reports on Form 8-K, any amendments thereto, and in the corresponding documents filed in Canada.

OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

You should read the following discussion in conjunction with our financial statements, together with the notes to those statements included elsewhere in this prospectus. The following discussion contains forward-looking statements that involve risks, uncertainties and assumptions such as statements of our plans, objectives, expectations and intentions. Our actual results may differ materially from those discussed in these forward-looking statements because of the risks and uncertainties inherent in future events.

(Dollar amounts are stated in thousands of US dollars unless otherwise stated)

Overview

We are an independent precious metals production and exploration company with operations focused in North America. In November 2003 we acquired the Mesquite Mine (“Mesquite” or “the Mine”) from a subsidiary of Newmont Mining Corporation (“Newmont”). Mesquite is our principal asset, providing us with current gold production based on leaching the material that was placed on the heap leach pads by Newmont and previous owners of the property. As a result of the current relatively high price for gold, since the acquisition from Newmont this production has provided us with operating cash flow to help sustain our operations pending completion of a feasibility study which we believed would justify resumption of mining operations.

In February 2006, we closed a $6,000 private placement financing which significantly improved our financial position, enabled us to repay all our outstanding debt and proceed towards completion of the Mesquite feasibility study. We also announced the appointment of new directors and a new management team.

On August 9, 2006 we announced the completion of the Mesquite feasibility study, which estimated proven and probable reserves of 2.36 million ounces of gold. On the basis of this study we focused our efforts on equipment specification and related financing with a view to resumption of mining operations in the second quarter of 2008. The feasibility study is more fully described under “Business - Our Feasibility Study.” In November 2006 we placed orders valued at $60,900 for the mining vehicle fleet and in January and February of 2007 we completed a common share equity financing, including an underwriter’s over-allotment option, which provided us with net proceeds of approximately $59,300. On March 30, 2007, we, through our wholly-owned subsidiary, Western Mesquite Mines, Inc. entered into a credit agreement relating to a $105,000 term loan facility, which was the final step in financing the Mine.

Selected Financial Results (in $000s)

Years ended December 31, | ||||||||||

2006 | 2005 | 2004 | ||||||||

| Revenues net | $ | 7,859 | $ | 9,798 | $ | 10,867 | ||||

| Gross profit (loss) | (1,601 | ) | (815 | ) | (1,098 | ) | ||||

| Net loss | (11,583 | ) | (3,340 | ) | (4,419 | ) | ||||

| Net loss to common shareholders | (11,600 | ) | (5,075 | ) | (4,419 | ) | ||||

| Net loss per common share, basic and diluted | $ | (0.18 | ) | $ | (0.13 | ) | $ | (0.12 | ) | |

| Gold ounces produced | 12,668 | 21,776 | 27,398 | |||||||

| Gold ounces sold | 13,210 | 23,818 | 27,357 | |||||||

| Average price received per ounce | $ | 595 | $ | 411 | $ | 397 | ||||

| Cost of sales per ounce(i) | $ | 928 | $ | 536 | $ | 502 | ||||

| (i) | Cost of sales include mine cost of sales less non-cash depreciation, amortization and accretion, and reclamation cost recovery. |

Consolidated Financial Results / Overall Performance (in $000s)

The Company’s net loss to common shareholders for the year ended December 31, 2006 (“2006”) was $11,600, or $0.18 per share, compared with $5,075, or $0.13 per share, and $4,419, or $0.12 per share, for the years ended December 31, 2005 and 2004 respectively (“2005” and “2004”).

Results for 2006, as compared with 2005, were negatively impacted by the 45% reduction in gold ounces sold from 23,818 ounces to 13,210 ounces. With no new material being placed on the leach pads, it has become increasingly difficult to extract the residual gold and maintain the solution grades coming from the leach pads. This lower production was substantially offset by the 45% increase in the average selling price per ounce from $411 to $595, reflecting the continuation of relatively strong pricing in world markets and the sale of all of our 2006 output on the spot market. During 2006, we revised the net present value of our reclamation plan obligations downward to $4,894 from $6,354, giving rise to a recovery of $1,460 in respect of accretion expense previously recorded. The reduction was primarily associated with a revision in the forecast timing of these obligations in light of the feasibility study. A similar revision in 2005 gave rise to a reduction in the forecast liability of $544 in that year. Cost of sales per ounce for 2006 were $928, as compared with $536 and $502 per ounce in 2005 and 2004 respectively.

The results for 2006 were also adversely affected by the increase in other operating expenses from $2,392 in 2005 to $9,238. General and administrative expenses were sharply higher on account of costs early in the year associated with the proposed Romarco merger, severance costs, costs of transitioning to the new management team, legal costs relating to several regulatory filings, and costs of obtaining a listing on The Toronto Stock Exchange. Non-cash stock based compensation for 2006 also increased significantly to $3,209 from $518 in 2005. The increase primarily reflects grants of options to our new management team in early 2006. We also incurred severance costs, paid in cash and through the issuance of common shares, resulting from management changes. The costs of our feasibility study in 2006 were $821.

Results for 2006 were also impacted by costs of $1,225 relating to termination of the proposed merger agreement with Romarco Minerals Inc.

The net loss to common shareholders in 2005 was adversely effected by the recognition of a conversion benefit arising to holders of our Series A Preferred stock and warrants in the amount of $1,700 and its being accounted for as a deemed dividend. The conversion benefit was triggered by our granting to Romarco Minerals Inc. an option to purchase our common stock on August 25, 2005.

As a result of the diminishing productive capacity of the leach pads, throughout 2006 we have been implementing strategies to maintain output levels and reduce costs. Ounces produced continued to decline, however, and in 2006 were 12,668 compared with 21,776 and 27,398 in 2005 and 2004 respectively. We continually monitor solution grades being produced by the leach pads with a view to optimizing output; during the third quarter of 2006 we concluded that it was no longer economic to continue leaching the Vista pad and we commenced closure operations. Under the terms of our bonding arrangement with AIG, costs of closure are reimbursable. Reimbursement claims of $201 have been made in respect of 2006 expenditures.

Years ended December 31, | ||||||||||

2006 | 2005 | 2004 | ||||||||

| Gold sales revenue | $ | 7,859 | $ | 9,798 | $ | 10,867 | ||||

| Average price realized per ounce | $ | 595 | $ | 411 | $ | 397 | ||||

| Increase (Decrease) in revenues | $ | (1,939 | ) | $ | (1,069 | ) | $ | 10,867 | ||

| Change in revenues attributable to ounces sold | $ | (4,364 | ) | $ | (1,406 | ) | $ | 10,867 | ||

| Change attributable to average selling price | $ | 2,425 | $ | 337 | $ | - | ||||

Revenues from gold sales for 2006 decreased by $1,939 or 20% compared to 2005, and by $1,069 or 10% compared with 2004, as the effect of lower ounces sold more than offset higher selling prices.

Years ended December 31, | ||||||||||

2006 | 2005 | 2004 | ||||||||

| Cost of sales | $ | 9,461 | $ | 10,613 | $ | 11,965 | ||||

| Decrease | $ | (1,152 | ) | $ | (1,352 | ) | $ | - | ||

| Cost of sales (before recognition of reclamation cost recovery) | $ | 10,921 | $ | 11,157 | $ | 11,965 | ||||

| Decrease | $ | (236 | ) | $ | (808 | ) | $ | - | ||

| Gross loss % | 20 | % | 8 | % | 10 | % | ||||

| Increase (decrease) in gross loss % | 12 | % | (2 | )% | ||||||

Cost of sales for 2006 decreased by $1,152 or 11% compared to 2005. The decrease results partially from recognition of a recovery of $1,460 in respect of reclamation plan obligations at the Mesquite Mine. The comparable recovery in 2005 was $544. On completion of the feasibility study in August 2006, we re-evaluated the net present value of closure costs in light of the extended life of the mine and the revised reserve estimates. Closure costs were estimated at $4,894 compared with $6,354 previously estimated. Excluding this element, cost sales for the year ended December 31, 2006 decreased by $236 or 2%. Cost of sales for the year ended December 31, 2006 was also impacted by a decrease in royalty expense reflecting the reduction in gold ounces sold and lower costs arising from inventory movements. Mine operating costs increased due to labour cost increases reflecting a general wage increase given to all hourly employees in July 2006, increased workmen’s compensation costs and severance payments. Costs of new hires and relocation costs for certain new employees also increased operating costs. Cyanide costs increased due to higher volumes of solution being pumped to the leach pads, and power costs increased due to utility rate increases.

Cost of sales for 2005 decreased by $1,352 or 11% compared to 2004. A recovery of $544 in respect of reclamation cost obligations was recorded in 2005. Excluding this element, cost of sales for 2005 decreased by $808 or 7%. Cost of sales for 2005 was also impacted by a decrease in royalty expense reflecting the reduction in gold ounces sold. Mine operating costs decreased due to lower cyanide costs, workmen’s compensation costs and consulting fees.

A comparison of the major components of cost of sales, excluding the reclamation cost recovery, is as follows:

Years ended December 31, | ||||||||||

2006 | 2005 | 2004 | ||||||||

| Mine operating costs | $ | 7,193 | $ | 6,551 | $ | 7,036 | ||||

| Mine site administration | $ | 1,642 | $ | 1,391 | $ | 1,837 | ||||

| Depreciation, amortization and accretion | $ | 1,352 | $ | 1,599 | $ | 1,774 | ||||

| Royalties | $ | 303 | $ | 774 | $ | 1,072 | ||||

| Inventory adjustment | $ | 399 | $ | 807 | $ | 159 | ||||

Other operating expenses for 2006 increased by $6,846 or 286% compared to 2005. The increase reflects higher general and administrative costs; early in 2006 costs were incurred for legal and travel costs in connection with the proposed merger with Romarco Minerals Inc., costs relating to warrants issued for services provided in connection with the private placement financing in February, and termination costs for several employees; later in the year we incurred significant legal costs in connection with several regulatory filings, further costs of transitioning to the expanded management team and costs in connection with our Toronto Stock Exchange listing in August. Other operating expenses for 2006 also include $3,209 in respect of stock based compensation compared with $518 in 2005. This increase was driven by the award of options to the new management team in February 2006 and by further awards made to additional hires in the second and third quarters of 2006. During 2006 we also incurred non-cash costs of $547 in respect of the value of shares issued to two former executives under the terms of their severance arrangements in 2005, and costs of $821 to complete the feasibility study.

Years ended December 31, | ||||||||||

2006 | 2005 | 2004 | ||||||||

| Other operating expenses | $ | 9,238 | $ | 2,392 | $ | 3,136 | ||||

| Increase (decrease) in other operating expenses | $ | 6,846 | $ | (744 | ) | |||||

| As % of revenues | 118 | % | 24 | % | 29 | % | ||||

| Change in % of revenues | 94 | % | (5 | )% | ||||||

A comparison of the major items included in other operating expenses is as follows:

Years ended December 31, | ||||||||||

2006 | 2005 | 2004 | ||||||||

| General and administrative | $ | 4,261 | $ | 1,653 | $ | 1, 174 | ||||

| Stock based compensation | $ | 3,209 | $ | 518 | $ | 1, 158 | ||||

| Severance costs payable in common shares | $ | 547 | $ | - | $ | - | ||||

| Exploration - Mesquite | $ | 821 | $ | 13 | $ | 508 | ||||

Other expenses for the year ended December 31, 2006 were $743 compared to $133 in 2005. The most significant item of cost occurred in February 2006, when we paid $1,225 to terminate the proposed Romarco merger. The cash infusion of $6,000 from the private placement of units in February 2006, supplemented by cash received upon exercise of preferred and common share warrants as 2006 progressed, resulted in our having positive cash balances for much of the year. Interest income for 2006 was $392 compared with $173 in 2005, and interest expense in 2006 was $20 compared with $349 in the prior year.

A comparison of the major items included in other income (expense) is as follows:

Years ended December 31, | ||||||||||

2006 | 2005 | 2004 | ||||||||

| Expenses of Romarco merger termination | $ | (1,225 | ) | $ | - | $ | - | |||

| Interest income | 392 | 173 | 115 | |||||||

| Interest expense | (20 | ) | (349 | ) | (327 | ) | ||||

Results of Operations

Year Ended December 31, 2006 (“2006”) Compared to Year Ended December 31, 2005 (“2005”).

Poured gold production for 2006 was 12,668 ounces compared with 21,776 ounces in 2005. Since no new ore has been placed on the leach pads since 2001, the productive capacity of the leach pads is diminishing and we are continuing with various strategies, initiated in the first quarter of 2006, to maintain output levels. Gold sales for 2006 were 13,210 ounces at an average selling price of $595 for revenues of $7,859 compared with 23,818 ounces at an average selling price, after hedging, of $411 for revenues of $9,798 in 2005. The higher average selling price reflects the increase in the world price for gold and our sale of all production in the spot market. We incurred no hedging losses in 2006 as compared to a loss of $687 in 2005.

Mine operating costs for 2006 were $7,193, compared to $6,551 for 2005. The increase primarily reflects higher power rates, increased costs of chemicals and increases in engineering department labour and use of consultants. During 2006 we continued our strategies aimed at lowering costs and concentrating production on the most productive areas of the leach pads. Mine site administration costs for 2006 were $1,642 compared with $1,391 in 2005, reflecting additional staffing and relocation costs. Depreciation, amortization and accretion expense for 2006 was $1,352 compared with $1,599 in 2005. The decrease reflects lower accretion expense associated with revisions to the reclamation plan at Mesquite. Costs associated with the change in metal-in-process inventories in 2006 were $399 compared with $807 in 2005 as work in process inventories declined to 441 ounces at December 31, 2006 from 1,406 ounces at December 31, 2005. In the third quarter of 2006 we recorded a cost recovery of $1,460 resulting from a reduction in the estimate of the net present value of reclamation costs at Mesquite. A re-evaluation of these costs was made on completion of the feasibility study in August 2006. The foregoing factors resulted in a gross loss of $1,601 for 2006 compared with a gross loss of $815 in 2005.

General and administrative expense increased to $4,261 for 2006 from $1,653 for 2005. We incurred significant costs early in the year associated with the proposed Romarco merger, severance costs and costs of transitioning to the new management team. We then incurred significant legal costs relating to several regulatory filings designed to facilitate the exchange of and trading in our common shares, warrants and options, and costs of obtaining a listing on The Toronto Stock Exchange. The higher costs for the year also reflect higher management salary costs, related recruiting costs and management travel costs as we completed the feasibility study and started to gear up for resumption of mining operations at Mesquite.

Stock based compensation represents the non-cash costs of options, as calculated under the Black-Scholes option pricing model, granted to directors, officers and employees. The increase in expense to $3,209 in 2006 from $518 in 2005 relates to the high initial amortization of options granted to the new management team in February and June of 2006 and their ongoing amortization thereafter.

Under the terms of severance arrangements concluded with two of our former officers in October 2005, we were required to issue a certain number of our common shares upon completion of the Mesquite feasibility study. The completion of the study was announced on August 9, 2006 and we used the closing price of the stock on that date to calculate the liability to these former officers in the amount of $547.

Exploration activities at Mesquite during 2006 were $821 and relate entirely to the completion of the mine feasibility study. Exploration activities at the Mine were minimal in 2005.

Other income (expense) for 2006 was $743 compared to $133 in 2005. The most significant item of cost occurred in February 2006, when we paid Romarco a termination fee of $1,000 and expense reimbursement costs of $225 on termination of the proposed merger agreement between us and Romarco. The proceeds of the first tranche of $3,700 of private placement units that closed on February 13, 2006 enabled us to repay the R.M.B. International, (Dublin) Limited (“RMB”) and Romarco Minerals Inc. (“Romarco”) loans outstanding at that time. Completion of the second tranche of $2,300 on February 20, 2006 and subsequent receipts of cash on exercise of common stock options and warrants as 2006 progressed, resulted in our having cash on deposit for the rest of the year. Interest income for 2006 was $392 compared with $173 in 2005, and interest expense in 2006 was $20 compared with $349 in 2005.

The net loss in 2005 was increased by the recognition of a conversion benefit arising to holders of our Series A Preferred stock and warrants in the amount of $1,700. This has been accounted for as a deemed dividend and as additional paid-in capital. The conversion benefit was triggered by our granting to Romarco an option to purchase our common stock on August 25, 2005.

The above were the major factors in our reporting a net loss to common shareholders for 2006 of $11,600 or $0.18 per share, compared with a net loss of $5,075 or $0.13 per share in 2005.

In 2005 other comprehensive income includes a gain of $679 in respect of the mark-to-market of forward gold sales contracts. We had no comparable income or expense in 2006 since all gold sales were on a spot basis.

Our net comprehensive loss in 2006 was $11,585 compared with $2,653 in 2005.

Year Ended December 31, 2005 (“2005”) Compared to Year Ended December 31, 2004 (“2004”).

Poured gold production for 2005 was 21,776 ounces compared with 27,398 ounces in 2004. This reflects the diminishing productive capacity of the leach pads with no new ore having been added since 2001. Gold sales for 2005 were 23,818 ounces at an average selling price of $411 for revenues of $9,798 compared with 27,357 ounces at an average selling price, after hedging, of $397 for revenues of $10,867 in 2004. The higher average selling price reflects the increase in the world price for gold, but this was substantially offset by the impact of hedging strategies that we adopted in connection with our credit facility agreement with RMB. We incurred hedging losses of $679 in 2005 compared with $177 in 2004.

Mine operating costs for 2005 were $6,551 compared to $7,036 in 2004. The decrease reflects refunds of, and lower rates for, Workers Compensation expense. It also reflects operating efficiencies which resulted in lower power and chemical costs. Mine site administration costs for 2005 were $1,391 compared with $1,837 in 2004. The decrease primarily relates to the termination of an outside management contract and reductions in management personnel. Depreciation, amortization and accretion expense for 2005 was $1,599 compared with $1,774 in 2004. This primarily reflects a $412 decrease in charges for amortization of deferred loan financing costs. Costs associated with the change in metal-in-process inventories in 2005 were $807 compared with $159 in 2004 as work in process inventories decreased to 1,406 ounces at December 31, 2005 from 4,004 ounces at December 31, 2004. In late 2005 we completed a review of our SFAS No. 143 reclamation and remediation liability which resulted in our recording a cost recovery of $544 due to the revised estimate being lower than previous estimates. The foregoing factors resulted in a gross loss of $815 for 2005 compared with a gross loss of $1,098 in 2004.

General and administrative expense for 2005 increased to $1,653 from $1,174 for 2005. These costs include payments to consultants, legal and accounting fees, director’s fees and general and administrative expenses for the corporate office. Stock-based compensation for 2005 was $518 compared with $1,158 in 2004. The decrease relates to there being significantly fewer options awarded and at lower exercise prices in 2005 than in 2004.

Costs for general exploration activities, primarily land fees, were $208 in 2005 compared with $295 in 2004. We also incurred expenses of $508 in connection with initial feasibility study activities in 2004.

Other expenses during 2005 totaled $133 compared with $185 in 2004. The decrease primarily reflects an increase in interest income to $173 in 2005 from $115 in 2004, partially offset by an increase in interest expense to $349 in 2005 from $327 in 2004, reflecting higher interest rates offset by lower loan balances in 2005.

The net loss to common shareholders in 2005 was adversely affected by the recognition of a conversion benefit arising to holders of our Series A Preferred stock and warrants in the amount of $1,700. This has been accounted for as a deemed dividend and as additional paid-in capital. The conversion benefit was triggered by our granting to Romarco an option to purchase our common stock on August 25, 2005.

The above were the major factors in our reporting a net loss to common shareholders for 2005 of $5,075 or $0.13 per share, compared with a net loss of $4,419 or $0.12 per share in 2004.

In 2005 other comprehensive income includes a gain of $679 in respect of the mark-to-market of forward gold sales contracts. The comparable gain in 2004 was $177.

Our net comprehensive loss in 2005 was $2,653 compared with $4,314 in 2004.

Liquidity and Capital Resources

At December 31, 2006 our cash balance was $5,503 and our working capital was $4,549. This represents a significant improvement in our financial position since December 31, 2005 when we reported cash of $52 and a working capital deficit of $2,515. At that time we were illiquid and our ability to continue as a going concern in the absence of additional financing was in question.

The working capital deficit at December 31, 2005 included the loan of $1,500 from RMB, the maturity date of which had been extended to April 26, 2006. The working capital deficit at December 31, 2005 also included short-term advances received during 2005 from Romarco of $705.

Developments in February 2006 enabled us to repay the RMB and Romarco debt and allowed us to begin work on the feasibility study for Mesquite that we had deferred for the past two years.

On February 13, 2006 we announced that we and Romarco had terminated our proposed merger and we paid Romarco a termination fee of $1,000 together with reimbursement of $225 for their out-of-pocket expenses in pursuing the merger. In addition, we repaid their promissory notes and related interest totaling $728.

In addition, on February 13, 2006 we announced the restructuring of our Board, the appointment of a new senior management team and the closing of the initial $3,700 of a non-brokered private placement financing of $6,000. On February 20, 2006, we announced the closing of the balance of $2,300 of the private placement.

With the improvement of our stock price subsequent to the developments in February 2006, our liquidity has been improved through the conversion of warrants and the exercise of stock options. In 2006, we received cash of $11,534 upon the exercise of 11,421,310 warrants at $1.00 each and 250,000 warrants at $0.45 each. In addition 500,000 preferred share warrants were exercised for proceeds of $300. Further, we received $633 in respect of the exercise of 1,135,000 options during the year. The funds were used to finance our expansion plans at Mesquite upon completion of the feasibility study.

Cash required for operating activities in 2006 was $7,316 compared with $725 in 2005. The major element in this cash requirement in 2006 was our net loss of $11,583, which amount had already been reduced by the non-cash recovery of reclamation costs of $1,460. The loss was offset in part by non-cash items such as: depreciation and accretion expense of $1,357, stock-based compensation of $3,209, and the issuance of common stock and warrants in settlement of severance obligations, for exploration asset and services, and for consultancy services, totaling $917. A change in the composition of non-cash working capital items during 2006, primarily through an increase in accounts payable, generated $515 to cash from operations. In 2005, our net loss was $3,340, which amount had already been reduced by the non-cash recovery of reclamation costs of $544. The 2005 loss was offset by non-cash depreciation, accretion and amortization of deferred loan financing costs of $1,612 and by a decrease in non-cash working capital items of $1,025. Cash requirements for operating activities in 2005 were also reduced by stock-based compensation of $518 and by the issuance of common stock for exploration assets and services in the amount of $166.

In view of the liquidity concerns in 2005 that carried over into 2006 and our focus, subsequent to the management changes and financing in February 2006, on the feasibility study, investing activities were kept to a minimum for much of 2006. Up to the end of the third fiscal quarter, capital spending was $472 and related primarily to a new “wobbler” spray system designed to enhance solution grades coming from the leach pads. During the fourth quarter we spent $2,972 on projects that had to be initiated in order to meet the time lines set out in our feasibility study for resumption of mining operations.

Net cash provided by financing activities in 2006 was $16,210. Cash receipts comprise the $6,000 proceeds of sale of 20,000,000 units in February 2006, of which $4,012 was attributed to common stock and $1,988 to warrants, the $11,534 received on exercise of common share warrants and $300 received on exercise of preferred share warrants, and the $633 received on exercise of options. Cash payments include the repayment of $2,205 principal on the RMB and Romarco loans. In 2005, net cash used for financing was $795, comprising $1,500 in respect of payments of principal on the RMB loan and the proceeds of loan advances from Romarco of $705.

The foregoing factors resulted in an increase in our cash position during 2006 of $5,450 and a decrease in our cash position during 2005 of $1,482.

On November 21, 2006, we announced that we had issued purchase orders totaling $60,900 in respect of the mining fleet required for resumption of mining operations at the Mesquite Mine. We have now issued purchase orders totaling $67,000 for the mining fleet and have incurred expenditures and other commitments of approximately $3,800. The major components of the mining fleet and their approximate cost, including all relevant taxes, are as follows: 14 haul trucks - $33,200; 2 shovels - $16,500; 1 front-end loader - $4,300; other mobile and ancillary equipment, including drills, bull-dozers, graders and water trucks - $9,500; truck tires - $3,500. During February, 2007 we took delivery of five ancillary equipment units as part of the mining fleet we had ordered in late 2006. The aggregate cost of the equipment received to date is approximately $2,900. Delivery of the larger items is expected in the period May through October of 2007. Payment terms vary; generally, payment is 10 days after commissioning, but in the case of the haul trucks, 80% is due on shipment and 20 % on completion of commissioning. Based on the delivery schedules provided by our suppliers, we anticipate paying approximately $24,000 of the cost by the end of May, a further $17,000 by the end of June, $15,000 by the end of July and the balance of $11,000 in the period August through October of 2007.