SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 20-F

(Mark One)

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b)

OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

| x | | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2003

OR

| ¨ | | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission file number: 1-31554

WMC RESOURCES LTD

Australian Business Number 76 004 184 598

(Exact name of Registrant as specified in its charter)

COMMONWEALTH OF AUSTRALIA

(Jurisdiction of incorporation or organization)

Level 16, IBM Centre, 60 City Road, Southbank, Victoria 3006, Australia

(Address of principal executive offices)

Securities registered or to be registered pursuant to Section 12(b) of the Act.

| | |

Title of each Class

| | Name of each exchange on which registered

|

Ordinary Shares(1) | | New York Stock Exchange |

American Depositary Shares(2) | | New York Stock Exchange |

Securities registered or to be registered pursuant to Section 12(g) of the Act.

None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act.

None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the Annual Report.

| | |

Shares outstanding: | | |

Fully Paid Ordinary Shares: | | 1,150,070,945 |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes: x No ¨

Indicate by check mark which financial statement item the registrant has elected to follow.

| (1) | | Not for trading but only in connection with the listing of the American Depositary Shares. |

| (2) | | Evidenced by American Depositary Receipts, each American Depositary Share representing four fully paid Ordinary Shares. |

CONTENTS

In this Annual Report, the terms “we”, “our”, “us”, “WMC Resources” and “WMC Resources Group” refer to WMC Resources Ltd together with its subsidiaries.

THE DEMERGER

On December 11, 2002, Alumina Limited (formerly known as WMC Limited) demerged its interest in the Alcoa World Alumina and Chemicals venture from its copper/uranium, nickel and fertilizer businesses and exploration and development interests. The demerger was effected through an Australian court-approved scheme of arrangement and associated capital reduction and dividend distribution. As a result of the demerger, Alumina Limited continues to hold its interest in AWAC, and WMC Resources now holds the nickel, copper/uranium and fertilizer businesses and exploration and development interests previously held within the WMC Limited group.

We were admitted to the official list of the Australian Stock Exchange and our shares are quoted on the stock market conducted by the Australian Stock Exchange. Our shares are also listed on the New York Stock Exchange in the form of American Depositary Receipts, or ADRs.

FORWARD-LOOKING STATEMENTS

This Annual Report contains forward-looking statements, including statements regarding (i) estimated reserves, (ii) certain plans, strategies and objectives of management, (iii) scheduled closure of certain operations or facilities, (iv) scheduled refurbishment, repair, maintenance, reconstruction and recommissioning activities, (v) anticipated production or construction commencement dates, (vi) expected costs or production output, (vii) the anticipated productive lives of projects and mines and (viii) the anticipated prices and market dynamics of commodities produced. These forward-looking statements are not guarantees of future performance and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, which may cause actual results to differ materially from those expressed in the statements contained in this Annual Report.

For example, future revenues from operations, projects or mines described in this Annual Report will be based in part on the market price of the minerals or metals produced, which may vary significantly from current levels. These variations, if materially adverse, may impact the timing or feasibility of the development of a particular project or the expansion of certain facilities or mines. Other factors that may affect the actual construction or production commencement dates, costs or production output and anticipated lives of operations, mines or facilities include:

| | • | | our ability to profitably produce and transport the minerals or metals extracted to applicable markets; |

| | • | | the impact of foreign currency exchange rates on the market prices of the minerals or metals we produce; and |

| | • | | activities of governmental authorities in certain countries where our projects, facilities or mines are being explored or developed, including increases in taxes, changes in environmental and other regulations, and political uncertainty. |

We can give no assurances that the estimated reserve figures, the scheduled closure of such operations or facilities, actual production or commencement dates, cost or production output, or anticipated lives of the projects, mines and facilities discussed herein will not differ materially from the statements contained in this Annual Report.

3

DEFINITIONS

“ADR” means an American Depositary Receipt evidencing one or more ADSs.

“ADS” means an American Depositary Share.

“ASX” means the Australian Stock Exchange.

“AWAC” means Alcoa World Alumina and Chemicals.

“Cash Flow Hedge” means a contract which hedges an exposure to changes in cash flows from an expected future transaction related to a forecast purchase or sale or an existing asset or liability.

“Combined Financial Statements” are the financial statements of WMC Limited when they incorporated both Alumina Limited and WMC Resources Ltd, prior to demerger.

“Commissioned” means the bringing into operation of plant and/or equipment at a rate approximating its design capacity.

“Consolidated” means the consolidation of entities controlled by us. Unincorporated joint ventures are consolidated on a proportionate basis.

“Counterparty Credit Risk” means the risk of financial loss arising out of holding a particular contract or portfolio of contracts as a result of one or more parties to the relevant contract(s) failing to fulfill its financial obligations under the contract.

“Cross-Currency Swap” means the exchange of cash flows in one currency for those in another, often requiring an exchange of principal.

“Currency Forward” means an agreement to exchange a specified amount of one currency for another at a future date at a certain rate.

“DAP” means di-ammonium phosphate.

“Decline” means a downwards sloping tunnel providing road access from the surface to underground mine operations.

“Demerger” means the demerger of WMC Limited’s interest in AWAC from its other operating businesses pursuant to an Australian scheme of arrangement and associated capital reduction and dividend distribution.

“Depositary” means The Bank of New York Company, Inc., 101 Barclay Street, New York, NY 10286.

“Derivative” means an instrument or product whose value changes with changes in one or more underlying market variables, such as equity or commodity prices, interest rates or foreign exchange rates. Basic derivatives include, forwards, futures, swaps, options, warrants and convertible bonds.

“Dilution” means the incorporation of waste rock with the ore during the mining process resulting in lower grade.

“Fair Value” means, in the context of commodity, currency and interest rate hedging, the current market value (mark-to-market) of financial positions.

“Fair Value Hedge” means a contract which hedges an exposure to the change in fair value of a recognized asset, liability or an unrecognized firm commitment (or a part thereof) attributable to a particular risk.

“Foreign Currency Hedge” means a contract which hedges the foreign exchange exposure of:

| | • | an unrecognized firm commitment (fair value hedge); |

| | • | an available for sale security (fair value hedge); |

| | • | a forecast transaction (cash flow hedge); or |

| | • | a net investment in a foreign operation |

4

“Grass Roots Exploration” is exploration undertaken at new sites not related to existing operations (also known as “green fields” exploration).

“Hedge” means to reduce risk by entering into transactions that reduce exposure to market fluctuations. A hedge is also the term for the transactions made to effect this reduction.

“Hedge Accounting” means the practice of deferring accounting recognition of gains and losses on financial market hedges until the corresponding gain or loss of the underlying exposure is recognized.

“HSRA” means the Australian/US dollar Hedge Settlement Rate quoted on Reuters Screen HSRA.

“Indenture” means the agreement between the Government of South Australia and WMC (Olympic Dam Corporation) Pty Ltd.

“Interest Rate Swap” means an agreement to exchange net future cash flows. Interest rate swaps most commonly change the basis on which liabilities are paid on a specified principal. They are also used to transform the interest basis of assets. In its most common form, the fixed-floating swap, one counterparty pays a fixed rate and the other pays a floating rate based on a reference rate, such as LIBOR. There is no exchange of principal – the interest rate payments are made on a notional amount.

“LME” means the London Metal Exchange.

“MAP” means mono-ammonium phosphate.

“Marking-to-Market” means to calculate the value of a financial instrument (or portfolio of such instruments) based on the current market rates or prices of the underlying instrument.

“Mineral” is a naturally occurring element or chemical compound.

“Mineralization” is a concentration of a valuable mineral or minerals.

“Nickel Matte” is the output of a nickel smelter, being predominantly nickel sulphides plus some impurities. This is typically fed to a refinery for nickel metal production. Matte can be sold as a commercial product in its own right.

“NYSE” means the New York Stock Exchange.

“Open-cut” or “Open-pit” means a mine at the earth’s surface as distinct from an underground mine.

“Option” means a contract that gives the purchaser the right, but not the obligation, to buy or sell an underlying security or instrument at a certain price (the exercise, or strike price) on or before an agreed date (the exercise period). For this right, the purchaser pays a premium to the seller. The seller (writer) of an option has a duty to buy or sell at the strike price, should the purchaser exercise his right.

“Ore” means a naturally occurring solid resource (often rock) from which a mineral or minerals can be extracted.

“Ore Reserve” means that part of a mineral deposit which could be economically mined and legally extracted or produced at the time of the reserve determination. Ore reserve estimates in this Annual Report include adjustments for dilution and mine recovery loss during the mining process but do not include adjustments for metallurgical recovery. These ore reserves comply with those prescribed by the United States Securities and Exchange Commission’s Industry Guide 7.

“Probable Ore Reserves” means reserves for which quantity and grade and/or quality are computed from information similar to that used for proven ore reserves, but the sites for inspection, sampling and measurement are farther apart or are otherwise less adequately spaced. The degree of assurance, although lower than that for proven ore reserves, is high enough to assume continuity between points of observation.

“Proven Ore Reserves” means reserves for which (a) the quantity is computed from dimensions revealed in outcrops, trenches, workings or drill holes; the grade and/or quality are computed from the results of detailed sampling and (b) the sites for inspection, sampling and measurement are spaced so closely and the geologic character is so well defined that size, shape, depth and mineral content of reserves are well-established.

“SCH” means a transfer of securities on the Clearing House Electronic Subregister System operated by ASX Settlement and Transfer Corporation Pty Ltd.

5

“SEC” means the US Securities and Exchange Commission.

“Stoping” means the extraction of ore in an underground mine, leaving behind a void.

“Sulphides” means a compound of metal elements and sulphur.

“Tailings” are the residue remaining after extraction of the valuable components from ore.

“WA Mining Act 1978” refers to legislation passed by the Government of the State of Western Australia with which all mining operations in that State must comply.

“WMC Limited” refers to the parent entity of WMC Resources prior to the demerger on December 11, 2002. WMC Limited changed its name to Alumina Limited in connection with the demerger.

“WMC Resources” means WMC Resources Ltd together with its subsidiaries. Unless indicated otherwise, references to WMC Resources prior to the effective date of the demerger are to the assets and businesses of WMC Limited that WMC Resources owned immediately upon effectiveness of the demerger.

6

WEIGHTS AND MEASURES

| | | | |

1 troy ounce | | = | | 31.103 grams |

| | |

1 kilogram | | = | | 32.15 troy ounces |

| | |

1 kilogram | | = | | 2.205 pounds |

| | |

1 tonne | | = | | 1,000 kilograms |

| | |

1 tonne | | = | | 2,205 pounds |

| | |

1 gram per tonne | | = | | 0.0292 troy ounces per (short) ton |

| | |

1 kilometer | | = | | 0.6214 miles |

Gold recovered is reported in troy ounces (expressed as “ounces” in this Annual Report), the customary market unit, whereas ore production and grades are quoted in metric units, that is tonnes and grams per tonne.

7

| | | | |

| | IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS | | |

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

| A. | | Directors and Senior Management |

Not applicable.

Not applicable.

Not applicable.

8

| | | | |

| | OFFER STATISTICS AND EXPECTED TIMETABLE | | |

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

| B. | | Method and Expected Timetable |

Not applicable.

9

| | | | |

| | KEY INFORMATION | | |

ITEM 3. KEY INFORMATION

| A. | | Selected Financial Data |

The selected financial data appearing below as at December 31, 2003 and 2002 and for the years ended December 31, 2003, 2002 and 2001 are set forth in Australian dollars (except as otherwise indicated), and are extracted, in relevant part, from our audited Consolidated Financial Statements which appear elsewhere herein. The selected financial data appearing below as at December 31, 2001, 2000 and for the year ended December 31, 2000 and 1999 are extracted, in relevant part, from audited Combined Financial Statements. The summary financial data appearing below as at December 31, 1999 is derived from unaudited consolidated financial data that is not included herein. As discussed in Note 1 to the Consolidated Financial Statements, the financial statements for 2002, 2001, 2000 and 1999 herein reflect the statements of financial performance and statements of financial position as if we were a separate entity for all periods presented. The historical financial information may not be indicative of our future performance and does not reflect what our financial position and results of operations would have been had we operated as a separate, stand-alone entity during the periods presented. These Consolidated Financial Statements have been prepared in accordance with accounting principles generally accepted in Australia (“Australian GAAP”), which differ in certain respects from accounting principles generally accepted in the United States of America (“US GAAP”). Note 45 to the Consolidated Financial Statements provides an explanation of these differences as they affect us and reconciliations from Australian GAAP to US GAAP of net income, comprehensive income, certain balance sheet items, shareholders’ equity and cashflows.

Our net income under Australian GAAP was A$245.6 million for the year ended December 31, 2003 (A$23.0 million for the year ended December 31, 2002). Under US GAAP, we would have reported a net profit of A$732.4 million for the year ended December 31, 2003 (net loss of A$109.5 million for the year ended December 31, 2002). Comprehensive income under US GAAP for the year ended December 31, 2003 was a profit of A$1,420.7 million (for the year ended December 31, 2002 a profit of A$86.2 million was reported). Our Consolidated Financial Statements are prepared in accordance with Australian GAAP. The principal differences between Australian GAAP and US GAAP that affect our net income and comprehensive income, as well as our shareholders’ equity, relate to the treatment of the following items:

| | (i) | | recognition of tax losses; |

| | (ii) | | revenue from insurance proceeds; |

| | (iv) | | exploration expenditure; |

| | (vi) | | recognition of profit on real estate disposal; |

| | (vii) | | deferral of cost of option payments; |

| | (viii) | | fair value of accounting for derivatives; |

| | (ix) | | amortization of mine development and deferred post-production waste removal costs; |

| | (x) | | transfers of net assets and exchange of shares between entities under common control; and |

| | (xi) | | accounting for asset retirement obligations. |

Differences that affect the Consolidated Statement of Cash Flows are that under US GAAP, bank overdrafts are not considered to be part of net cash equivalents, and expenditure incurred on post-production waste removal cost would be classified as part of cashflows from operating activities, rather than investing activities.

10

| | | | |

| | KEY INFORMATION | | |

The following selected financial data should be read in conjunction with, and is qualified in its entirety by reference to, the Consolidated Financial Statements, including the Notes thereto.

SELECTED FINANCIAL DATA UNDER AUSTRALIAN GAAP

| | | | | | | | | | | | | |

| | | Year Ended

December 31,

2003

| | Year Ended

December 31,

2002

| | | Year Ended

December 31,

2001

| | | Year Ended

December 31, 2000

| | Year Ended

December 31,

1999

| |

| | | (A$ million, except where indicated) | |

Net Sales Revenue from Continuing Operations | | 3,001.3 | | 2,487.2 | | | 2,364.1 | | | 2,666.0 | | 1,672.7 | |

Income/(Loss) from Continuing Operations: | | 239.1 | | (14.7 | ) | | (157.5 | ) | | 327.2 | | (5.7 | ) |

Income from Operations (before tax) | | 247.9 | | 1.8 | | | 49.7 | | | 568.6 | | 23.7 | |

Net Income | | 245.6 | | 23.0 | | | 126.0 | | | 399.9 | | 84.1 | |

Comprehensive Income | | 248.8 | | 26.1 | | | 111.9 | | | 380.7 | | 79.8 | |

Net Income per Share (A$/share)(1) | | 0.22 | | 0.02 | | | 0.11 | | | 0.35 | | 0.07 | |

Net Income/(Loss) from Continuing Operations per Ordinary Share (A$/share)(1) | | 0.21 | | (0.01 | ) | | (0.14 | ) | | 0.29 | | (0.01 | ) |

Diluted Net Income/(Loss) from Continuing Operations per Ordinary Share (A$/share)(2) | | 0.21 | | (0.01 | ) | | (0.14 | ) | | 0.29 | | (0.01 | ) |

| | |

| |

|

| |

|

| |

| |

|

|

| | | | | |

| | | At December 31,

2003

| | At December 31,

2002

| | | At December 31,

2001

| | | At December 31, 2000

| | At December 31,

1999

| |

| | | (A$ million, except where indicated) | |

Total assets | | 7,560.2 | | 7,348.1 | | | 8,242.9 | | | 8,597.0 | | 7,275.8 | |

Long-term obligations | | 2,712.9 | | 1,709.1 | | | 3,476.3 | | | 4,304.2 | | 3,053.1 | |

Net assets | | 3,949.7 | | 3,606.6 | | | 3,220.3 | | | 3,123.8 | | 3,214.3 | |

| | |

| |

|

| |

|

| |

| |

|

|

Shareholders’ equity | | 3,949.7 | | 3,606.6 | | | 3,220.3 | | | 3,123.8 | | 3,214.3 | |

| | |

| |

|

| |

|

| |

| |

|

|

| | | Millions of shares | |

Number of shares | | 1,150.1 | | 1,128.4 | | | 1,108.8 | | | 1,098.0 | | 1,149.9 | |

| | |

| |

|

| |

|

| |

| |

|

|

| (1) | | The number of our shares used in the 2002 basic net income per share calculation was determined on the basis of the weighted average number of outstanding WMC Limited shares for the 11 months to November 30, 2002 (the effective demerger date for accounting purposes) and the actual number of WMC Resources shares for the month of December 2002. For prior periods, the number of our shares used in the basic net income per share calculation was determined on the basis of the weighted average number of outstanding WMC Limited shares for the periods indicated, as in the demerger each WMC Limited shareholder received one of our shares for each share in WMC Limited it held. Refer also to Notes 1(y) and 6 to the Consolidated Financial Statements. |

| (2) | | The number of our shares used in the 2002 diluted net income per share calculation was determined on the basis of the weighted average of the number of outstanding WMC Limited shares for the 11 months to November 30, 2002 (the effective demerger date for accounting purposes) and the actual number of WMC Resources shares for the month of December 2002. For prior periods, the number of our shares used in the diluted net income per share calculation was determined on the basis of the weighted average of the number of outstanding WMC Limited shares for the periods indicated, including potential shares from the conversion of partly paid shares and options into shares of WMC Limited. Refer also to Notes 1(y) and 6 to the Consolidated Financial Statements. |

11

| | | | |

| | KEY INFORMATION | | |

SELECTED FINANCIAL DATA UNDER US GAAP

| | | | | | | | | | | | | |

| | | Year Ended

December 31,

2003

| | Year Ended

December 31,

2002

| | | Year Ended

December 31,

2001

| | | Year Ended December 31, 2000

| | Year Ended

December 31,

1999

| |

| | | (A$ million, except where indicated) | |

Net Sales Revenue | | 3,001.3 | | 2,487.2 | | | 2,364.1 | | | 2,666.0 | | 1,672.7 | |

Income/(Loss) from Continuing Operations: | | 711.7 | | (160.8 | ) | | (231.5 | ) | | 241.6 | | (22.2 | ) |

Net Income/(Loss) | | 732.4 | | (109.5 | ) | | 37.7 | | | 307.6 | | 52.1 | |

Comprehensive Income/(Loss) | | 1,420.7 | | 86.2 | | | (804.7 | ) | | 288.4 | | 2.1 | |

Net Income/(Loss) from Continuing Operations per Ordinary Share (A$/share)(1)(2) | | 0.63 | | (0.14 | ) | | (0.21 | ) | | 0.21 | | (0.02 | ) |

Diluted Net Income/(Loss) from Continuing Operations per Ordinary Share (A$/share)(3) | | 0.62 | | (0.14 | ) | | (0.21 | ) | | 0.21 | | (0.02 | ) |

| | |

| |

|

| |

|

| |

| |

|

|

| | | | | |

| | | At December 31,

2003

| | At December 31,

2002

| | | At December 31,

2001

| | | At December 31, 2000

| | At December 31,

1999

| |

| | | (A$ million, except where indicated) | |

Total assets | | 6,764.0 | | 6,478.1 | | | 6,691.4 | | | 8,368.2 | | 7,146.7 | |

Long-term obligations | | 2,712.9 | | 1,709.1 | | | 3,476.3 | | | 4,304.2 | | 3,053.1 | |

Net assets | | 3,925.7 | | 2,410.7 | | | 2,068.8 | | | 2,888.9 | | 3,071.7 | |

| | |

| |

|

| |

|

| |

| |

|

|

Shareholders’ equity | | 3,925.7 | | 2,410.7 | | | 2,068.8 | | | 2,888.9 | | 3,071.7 | |

| | |

| |

|

| |

|

| |

| |

|

|

| | | Millions of shares | |

Number of Shares | | 1,150.1 | | 1,128.4 | | | 1,108.8 | | | 1,098.0 | | 1,149.9 | |

| | |

| |

|

| |

|

| |

| |

|

|

| (1) | | The number of our shares used in the 2002 basic net income per share calculation was determined on the basis of the weighted average number of outstanding WMC Limited shares for the 11 months to November 30, 2002 (the effective demerger date for accounting purposes) and the actual number of WMC Resources shares for the month of December 2002. For prior periods, the number of our shares used in the basic net income per share calculation was determined on the basis of the weighted average number of outstanding WMC Limited shares for the periods indicated; as in the demerger each WMC Limited shareholder received one of our shares for each share in WMC Limited it held. Refer also to Notes 1(y) and 6 to the Consolidated Financial Statements. |

| (2) | | In 1999, net loss per share was A$0.04 before the cumulative effect of an accounting policy change for start-up costs. In 2002, net loss per share was $0.06 before the cumulative effect of an accounting policy change for amortization of mine development and post-production waste removal costs. In 2003, net gain per share was A$0.66 before the cumulative effect of an accounting policy change for asset retirement obligations. |

| (3) | | The number of our shares used in the 2002 diluted net income per share calculation was determined on the basis of the weighted average of the number of outstanding WMC Limited shares for the 11 months to November 30, 2002 (the effective demerger date for accounting purposes) and the actual number of WMC Resources shares for the month of December 2002. For prior periods, the number of our shares used in the diluted net income per share calculation was determined on the basis of the weighted average of the number of outstanding WMC Limited shares for the periods indicated, including potential shares from the conversion of partly paid shares and options into shares of WMC Limited. Refer also to Notes 1(y) and 6 to the Consolidated Financial Statements. |

12

| | | | |

| | KEY INFORMATION | | |

Exchange Rates

We publish our Consolidated financial statements in Australian dollars (“A$” or “$”). In this Annual Report, references to “US$” are to United States dollars.

The following table sets forth, for the periods and dates indicated, certain information concerning the rates of exchange of A$1.00 into US$ based on the noon buying rate in New York City for cable transfers in Australian dollars as certified for customs purposes by the Federal Reserve Bank of New York (the “Noon Buying Rate”).

| | | | | | | | |

Period

| | At Period End

| | Average Rate(1)

| | High

| | Low

|

| | | (all figures in US$ per A$1.00) |

Year Ended December 31, 1999 | | 0.6560 | | 0.6440 | | 0.6712 | | 0.6179 |

Year Ended December 31, 2000 | | 0.5560 | | 0.5757 | | 0.6687 | | 0.5112 |

Year Ended December 31, 2001 | | 0.5117 | | 0.5127 | | 0.5712 | | 0.4828 |

Year Ended December 31, 2002 | | 0.5625 | | 0.5447 | | 0.5748 | | 0.5060 |

Year Ended December 31, 2003 | | 0.7520 | | 0.6588 | | 0.7520 | | 0.5629 |

| | | | |

November 2003 | | | | | | 0.7238 | | 0.6986 |

December 2003 | | | | | | 0.7520 | | 0.7265 |

January 2004 | | | | | | 0.7805 | | 0.7576 |

February 2004 | | | | | | 0.7979 | | 0.7566 |

March 2004 | | | | | | 0.7725 | | 0.7325 |

April 2004 | | | | | | 0.7677 | | 0.7198 |

| | |

| |

| |

| |

|

| (1) | | The average of the exchange rates on the last day of each month during the financial period. |

On May 24, 2004, the Noon Buying Rate was A$1.00 = US$0.6982

13

| | | | |

| | KEY INFORMATION | | |

| B. | | Capitalization and Indebtedness |

Not applicable.

| C. | | Reasons for the Offer and Use of Proceeds |

Not applicable.

Risks relating to our business

We believe that, because of the international scope of our operations and the industries in which we are engaged, numerous factors have an effect on our results and operations. The following describes the material risks that could affect us.

A reduction in commodity prices could materially reduce our revenues and profits.

Our revenue is derived from sales of nickel, copper, uranium, gold and fertilizers. The prices we obtain for our products are determined by, or linked to, prices in the world markets, which have historically been subject to substantial fluctuations arising from changes in supply and demand, various Australian and international macro-economic and political conditions, the cost of substitute materials, and the speculative activities of various market participants. This will have a consequent effect on the prices we can charge for our products and the revenues we receive, including under supply contracts, the pricing terms of which track market prices, which consequently affects our profitability. The general trend in commodity prices has been characterized by an increase from 1999 through the end of 2000, followed by a decline over the course of 2001 into 2002 and increases in 2003. For further information about historical commodity price movements in the commodities we produce, please see the following sections “Qualitative and Quantitative Disclosures About Market Risk—Average Quarterly Prices”, “Business Description—Nickel—Markets and Competition”, “Business Description—Copper-uranium—Market and Competition” and “Business Description—Fertilizer—Markets and Competition”.

Material changes in the prices we receive for our products could have a significant effect on our results. Consequently, a sustained and uninterrupted period of unusually low prices of the metal and other products we sell could reduce our profitability and our ability to pay principal and interest on our debt, dividends, or meet our other obligations.

In 2003, commodity prices rose due to significant increases in economic activity in the markets we serve. However, the general volatility in commodity prices makes it difficult for us to predict the extent and duration of any decline or increase in the cyclical commodity prices relating to our products. We expect that volatility in prices and in demand for most of our products will continue for the foreseeable future. We may enter into hedging transactions with respect to nickel, gold, copper and fertilizer with a view to reducing the potentially adverse effects of commodity price fluctuations. Since 2000, any new hedging activity has been limited to securing acceptable rates of return for new projects. For a statement of our current hedging activity, and movements in the selling price of nickel, gold, copper and fertilizer over the last five years, see “Quantitative and Qualitative Disclosure about Market Risk”.

Fluctuations in foreign exchange rates could adversely affect our revenues and profits.

The products we export from Australia are predominantly sold in US$. In the year ended December 31, 2003, 92.6% of our sales revenue was denominated in or linked to US$. However, any dividend payments and the majority of our operating costs are denominated in A$. Therefore, in the absence of other changes, if the A$ strengthens in value relative to the value of the US$, our financial results will be adversely affected. Conversely, a weakening of the A$ relative to the US$ will tend to have a favorable effect on our financial results. Because much of our borrowings and the majority of our receivables are denominated in US$, movements in the A$/US$ exchange rate will also affect our net asset value. As at December 31, 2003, we had US$897.4 million of US$ repayment obligations and US$ receivables of US$192.9 million. We have from time to time sought to hedge our foreign currency exchange position. See “Quantitative and Qualitative Disclosure about Market Risk” for a more detailed discussion of our foreign exchange hedging policy.

14

| | | | |

| | KEY INFORMATION | | |

Fluctuations in the A$/US$ exchange rate will also affect the US$ equivalent of the A$ price of our ordinary shares on the ASX and, as a result, are likely to affect the market price of our ADSs in the United States. Such fluctuations would also affect the US$ amounts received by holders of ADSs on conversion of any cash dividends paid in A$ on the ordinary shares underlying the ADSs.

We may have fewer ore reserves than our estimates indicate.

There are a number of uncertainties inherent in estimating quantities of reserves, including many factors beyond our control. The reserves data included in this Annual Report are estimates. The actual volume and grade of reserves recovered and our rates of production may be less than these estimates may imply.

Our reserve estimates may change substantially if new information subsequently becomes available. Such estimates are, to a large extent, based on the interpretations of geological data obtained from drill holes and other sampling techniques, and feasibility studies which derive estimates of operating costs based upon anticipated tonnage and grades of the material to be mined and processed, expected recovery rates, equipment operating costs and other factors. Further, it may take many years from the initial phase of drilling before production is possible and, during that time, the economic feasibility of exploiting a discovery may change. Fluctuations in the price of commodities, variations in operating and capital costs, different recovery rates and other factors, including, but not limited to, short-term operating factors such as the need for sequential development of ore bodies and the processing of new or different ore grades, may ultimately result in our estimated reserves being revised. If such a revision were to indicate a substantial reduction in proven or probable reserves at one or more of our major projects, it could negatively affect our financial condition and prospects.

A decline in the market price of a particular metal or mineral may also render the exploitation of reserves containing relatively lower grades of mineralization uneconomical. If the price we realized for a particular commodity were to decline substantially below the price at which our ore reserves were estimated for a sustained period of time, we could experience reductions in reserves and asset write-downs. Under some such circumstances, we may discontinue the development of a project or mining at one or more properties.

An increase in our production costs could reduce our profitability.

Changes in our costs have a major impact on our profitability. Our main expense categories are salaries and wages, energy, transport, materials, and amortization and depreciation of property, plant and equipment. Some of our costs are also affected by government imposts and regulations. Our costs depend upon the efficient design and construction of mining and processing facilities and competent operation of those facilities. Changes in costs of mining and processing operations can occur as a result of unforeseen events or changes in reserve estimates.

Our energy costs represent a significant portion of the production costs for our operations. The principal sources of energy for our mining operations are purchased electricity and natural gas. Energy will continue to represent a significant portion of our production costs, and we may be adversely impacted if future energy sources are not available or energy prices increase. If we are unable to procure sufficient energy at reasonable prices in the future, it could reduce the earnings or cash flow that we otherwise might realize.

Our ability to sustain or increase our current levels of production in the medium to long term is partly dependent on the development of new projects and expansion of existing operations.

Our ability to sustain or increase our current levels of production, and, therefore, our potential revenues and profits, in the medium to long term is partly dependent on the development of new projects and on the expansion of existing operations. Planned development or expansion projects may not result in the entire planned additional production. The economics of any project are based upon, among other factors, estimates of non-reserve mineralization and reserves, recovery rates, production rates, capital and operating costs of these development projects and future commodity prices. The uncertainty and volatility of some or all of these factors contributes to the risks associated with project development and expansion activities.

Our business may be affected by planned and unplanned outages and other material disruptions.

Industrial disruptions, work stoppages, refurbishments, installation of new plants, geotechnical issues, accidents or sustained bad weather at our operations can result in production losses and delays in delivery of products, which may adversely affect our profitability. Production may fall below historic or estimated levels as a result of unplanned outages. For example, in 2001, we experienced a fire at both of our copper and uranium solvent extraction units at our Olympic Dam operations. We also experienced a fire in the copper solvent extraction unit in 1999. Our copper and uranium production was adversely affected following these incidents, and future incidents of this nature or other incidents resulting in unplanned outages could materially affect our production and operating profits.

15

| | | | |

| | KEY INFORMATION | | |

We are exposed to regulatory, legislative and judicial action, both in Australia and in other countries in which we conduct operations.

Our operations in each of the jurisdictions where we operate could be affected by government actions, such as controls on imports, exports and prices, variations in taxation laws (including royalties), government directions, guidelines and regulations, particularly in relation to the environment and mine operations, legislation, indigenous people’s rights and court decisions, particularly those that impact on land access and freedom to conduct mining operations. Any such government action or court decisions may require increased capital or operating expenditures or both, or could prevent or delay the development of some of our operations.

We are also subject to the requirements of Australian mining law and the conditions of leases granted to us by state or territorial governments. See “Business Description – Australian Mining Law and Leases” for a more detailed discussion of these requirements.

Some of our exploration and potential projects and activities are in developing countries where political, economic and other risks may be more acute than in developed countries, including our Corridor Sands project in Mozambique. These risks include: expropriation or nationalization of property; currency fluctuations (particularly in countries with high inflation); restrictions on the ability to pay dividends offshore; risks of loss due to civil strife, acts of war, guerilla activities, insurrection and terrorism; and other risks arising out of foreign sovereignty over the areas in which operations are conducted. Consequently, our exploration, development, and future production activities outside of Australia may be adversely affected by factors beyond our control, any of which could materially adversely affect our financial position or results of operations. Furthermore, in the event of a dispute arising from such activities, we may be subject to the exclusive jurisdiction of courts outside Australia or may not be successful in subjecting persons to the jurisdiction of the courts in Australia, which could adversely affect the outcome of a dispute.

We are subject to stringent environmental laws and regulations, which impose substantial costs and subject us to significant potential liabilities.

Compliance with environmental laws and regulations imposes substantial costs and subjects us to significant potential liabilities. Our business is subject to particular risks and liabilities associated with pollution of the environment and the disposal of waste products occurring as a result of mineral exploration and production. Our operations in Australia are subject to stringent federal, state and local laws and regulations relating to improving or maintaining environmental quality. Environmental laws often require parties to pay for remedial action or to pay damages regardless of fault. Environmental laws also often impose liability with respect to divested or terminated operations, even if the operations were terminated or divested many years ago. Costs associated with environmental and regulatory compliance have increased over time. In addition, the costs of environmental obligations may exceed the reserves we have established for these liabilities. For a discussion of our significant remediation projects in Australia, see “Business Description – Environmental Matters”.

We cannot reasonably estimate the cost of future compliance or remedial work or further investment necessitated through the introduction of further environmental regulation or by any causes of contamination, including those occurring prior to the introduction of such regulation or before or after the property in question was owned or occupied by us. Among other things, the level of these costs will be dependent upon the nature and extent of the current and future environmental regulation, the time and nature of required remedial work, the extent of any contamination, the technology available to meet the required standards, the determination of our liabilities in proportion to those of other parties and the extent to which costs are recoverable from insurance and third parties.

Service of process, enforcement of judgments and bringing of original actions in the United States may be more difficult.

Since we and our officers and directors reside outside the United States and a substantial portion of our assets are located outside the United States, there is a risk that service of process, enforcement of judgments and bringing of original actions will be more difficult.

Native Title in Australia.

“Native Title” describes the rights and interests of Aboriginal and Torres Strait Islander people in land and waters according to their traditional laws and customs that are recognized under Australian law. There are current claimant applications for native title determinations in the Federal Court of Australia over areas that include the majority of our operations. We cannot make any assessment as to whether any of our existing assets or operations will be materially affected until court determinations are made. Court decisions and various pieces of legislation make it evident that there are complex legal and factual issues affecting our existing and future interests. Accordingly, the impact of native title is being closely monitored but cannot be determined at this time. See “Item 8A. Legal Proceedings – Native Title in Australia” for a discussion of native title issues in Australia that have an impact on our operations.

16

| | | | |

| | INFORMATION ON THE COMPANY | | |

ITEM 4. INFORMATION ON THE COMPANY

A. History and Development of WMC Resources

Background

We were incorporated under the laws of the Commonwealth of Australia on March 2, 1933. Through the transactions to effect the demerger of WMC Limited’s interest in the Alcoa World Alumina and Chemicals (“AWAC”) joint venture with Alcoa Inc. from WMC Limited’s other businesses effective December 11, 2002 we became an independent diversified resources company. From 1979 until the demerger, we had been operating as a wholly-owned subsidiary of WMC Limited, holding principally the group’s nickel assets. Our main businesses consist of the discovery, development, production, processing and marketing of minerals and metals. We produce nickel, copper, phosphate fertilizers, uranium oxide, gold and a range of other intermediate products. As at December 31, 2003, we had total combined assets of approximately A$7.6 billion and we generated net sales revenue from operations of approximately A$3.1 billion in the year ended December 31, 2003.

We have our registered office and principal executive offices at Level 16, 60 City Road, Southbank, Victoria, 3006, Australia. Our telephone number is +61 3 9685 6000 and our facsimile number is +61 3 9685 3569.

The demerger

On November 21, 2001, WMC Limited announced a proposal to demerge its interests in AWAC from its other mineral businesses. The demerger was effected through an Australian court-approved scheme of arrangement and associated capital reduction and dividend distribution with an effective date of December 11, 2002 (and an effective accounting date of November 30, 2002). As a result of the demerger, WMC Limited has continued to hold its interest in AWAC (but changed its name to Alumina Limited) and we hold the nickel, copper/uranium and fertilizer businesses and exploration and development interests (other than those relating to AWAC) previously held within the WMC Limited group.

Immediately prior to effecting the demerger, through a series of share sale transactions internal to the WMC Limited group, we acquired those of WMC Limited’s subsidiaries which held its copper/uranium and fertilizer businesses and exploration and development interests (other than those relating to AWAC), together with those subsidiaries which provide administrative or financial support to, or otherwise relate to activities conducted by, us. The shares of the subsidiaries were transferred to us in return for our newly issued ordinary shares. For accounting purposes, the subsidiaries were acquired in connection with the demerger at their fair value. These fair values were determined by using discounted cash flows in accordance with Australian GAAP. (Under Australian GAAP, fair value is defined as the amount for which an asset could be exchanged, or a liability settled, between knowledgeable, willing parties in an arm’s length transaction. However, in circumstances such as these where the transaction does not take place in an active market, fair value can be determined using alternative estimation techniques such as discounted cash flows.)

The demerger was effected in two simultaneous stages. First, WMC Limited reduced its share capital by a notional cash amount of A$2.78 per share and declared a notional cash dividend of A$0.73 per share. Second, under the scheme of arrangement effected by an order of the Court and binding on all WMC Limited shareholders and WMC Limited, WMC Limited shareholders agreed to purchase all of our shares utilizing as consideration their capital reduction and dividend entitlements from WMC Limited. As a result, WMC Limited shareholders received our shares on a pro-rata basis in the demerger.

The amount of the capital reduction and dividend together represented our carrying value in the books of WMC Limited at November 30, 2002 after giving effect to the share transfers at fair value mentioned above. This carrying value amounted to A$4,007.5 million.

The demerger required the approval of a majority in number of WMC Limited shareholders present and voting, and holding at least 75% of the total number of WMC Limited shares voted, at the shareholders’ meeting held to consider the demerger. The implementation of the demerger was subject to the approval of the Australian court considering the scheme of arrangement. The approval of the ASX was also required in order to admit us to the official list of the ASX.

The information about us and our operating and financial review and prospects has been presented in this Annual Report as though we had existed as a stand-alone economic entity for all the periods presented.

17

| | | | |

| | INFORMATION ON THE COMPANY | | |

Capitalization Expenditure and Divestiture

Since January 1, 2001 we have made the following principal capital expenditure and divestiture:

| | • | | Our divestment of our Kambalda mines is part of our nickel strategy to divest mature nickel mines and seek to participate in the benefits that a small focused operator can yield from the remaining resource. Since early 2000, we have been selling various mines within our Kambalda nickel operations. To the date of this Annual Report, proceeds from these sales have totalled A$52.0 million in aggregate. We anticipate that our remaining mine in the Kambalda region will be sold over the next few years. |

| | • | | In February 2001 we purchased the Yakabindie nickel project. The Yakabindie project, situated near Mt Keith, involved an investment of A$40 million, A$25 million of which was paid at the time of acquisition with the remaining A$15 million due upon gaining approval to mine the property. While the approval process has been commenced, final approvals to mine are not expected for some years. |

| | • | | In 2002, we completed an optimization project to increase production capacity of copper cathode at our Olympic Dam operations in South Australia. The project has increased the refinery capacity and improved efficiency in the milling and hydro-metallurgy areas. The capital cost was approximately A$79 million. |

| | • | | In October 2003, we merged the operating subsidiary that held our interest in the Meliadine West gold project with Comaplex Minerals Corporation, a Canadian mining company. |

| | • | | In January 2003, we finalized our acquisition of 100% of the Corridor Sands titanium dioxide project located in Mozambique for US$62.5 million. We settled the final tranche of US$25 million by issuing 6,715,123 shares in December 2003. |

We currently have the following capital expenditure, asset purchase and divestiture activities in progress:

| | • | | Olympic Dam experienced a fire in both the copper and uranium solvent extraction circuits in 2001. The expected cost of the rebuild is approximately A$375 million. |

| | • | | An extension of the Perseverance mine at Leinster. The expected cost of the extension is approximately A$179.1 million. |

B. Business Overview

General

Our main business is the discovery, development, production, processing, and marketing of minerals and metals. We produce nickel, copper, phosphate fertilizers, uranium oxide, gold and a range of other intermediate products. Our other activities include producing, marketing and distributing fertilizers.

During 2003, we explored in Australia, China, Peru, Mongolia, Tanzania, Malawi, Turkey and the USA. During 2003, we undertook further engineering studies and secured permits for improved power supply and product export options at Corridor Sands. The Industrial Development Corporation of South Africa exercised its option over 10% of the project’s equity for US$10 million. This transaction is still subject to Reserve Bank of South Africa approval. In December 2003, we made the final payment of US$25 million to acquire the Corridor Sands project from Southern Mining Corporation by issuing 6,715,123 WMC Resources shares to that corporation. The additional US$25 million was allocated to Acquired Mineral Rights.

18

| | | | |

| | INFORMATION ON THE COMPANY | | |

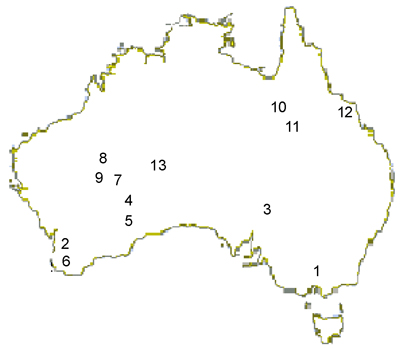

The following map shows the location of our operations and interests in Australia.

| | | | | | |

| | | CORPORATE OFFICES | | | | FERTILIZER |

1. | | Melbourne, VIC | | 10. | | Mt Isa, QLD |

2. | | Perth, WA | | 11. | | Phosphate Hill, QLD |

| | | | | 12. | | Townsville, QLD |

| | | |

| | | COPPER-URANIUM | | | | EXPLORATION |

3. | | Olympic Dam, SA | | 13. | | West Musgrave, WA |

| | | |

| | | NICKEL | | | | |

4. | | Kalgoorlie, WA | | | | |

5. | | Kambalda, WA | | | | |

6. | | Kwinana, WA | | | | |

7. | | Leinster, WA | | | | |

8. | | Mount Keith, WA | | | | |

9. | | Yakabindie, WA | | | | |

AUSTRALIA

19

| | | | |

| | INFORMATION ON THE COMPANY | | |

Segment Information

We categorize our on-going operations as follows: Nickel; Copper-Uranium (the Olympic Dam Operations which produces copper, uranium oxide, gold and silver); Fertilizers; Regional Exploration and New Business. Geographic and financial information relating to the segments of continuing operations are included under Note 7 to our Consolidated Financial Statements. The following table sets forth financial information in A$ by operating segments for each of the last three years.

FINANCIAL INFORMATION BY SEGMENT (CONTINUING OPERATIONS)

| | | | | | | | | |

| | | Year Ended

December 31,

2003

| | | Year Ended

December 31,

2002

| | | Year Ended

December 31,

2001

| |

| | | (A$ million) | |

Sales Revenue by Operating Segments(1) | | | | | | | | | |

Nickel | | 1,827.2 | | | 1,315.0 | | | 1,200.9 | |

Copper-uranium | | 719.0 | | | 723.3 | | | 810.3 | |

Fertilizers | | 428.1 | | | 420.6 | | | 352.9 | |

Unallocated corporate revenues | | 27.0 | | | 28.4 | | | — | |

| | |

|

| |

|

| |

|

|

| | | 3,001.3 | | | 2,487.3 | | | 2,364.1 | |

| | |

|

| |

|

| |

|

|

Consolidated Income/(Loss) by Operating Segments before Income Tax | | | | | | | | | |

Nickel | | 472.5 | | | 221.5 | | | 147.4 | |

Copper-uranium | | (97.5 | ) | | 53.8 | | | 47.9 | |

Fertilizers | | (25.6 | ) | | (57.4 | ) | | (89.4 | ) |

Unallocated result | | 12.7 | | | 11.4 | | | (1.0 | ) |

| | |

|

| |

|

| |

|

|

Product Operating Income | | 362.1 | | | 229.3 | | | 104.9 | |

New Business | | (19.5 | ) | | (36.5 | ) | | (35.3 | ) |

Regional Exploration | | (23.4 | ) | | (21.5 | ) | | (63.9 | ) |

Financing/Corporate | | (77.8 | ) | | (205.9 | ) | | (229.0 | ) |

| | |

|

| |

|

| |

|

|

| | | 241.4 | | | (34.6 | ) | | (223.3 | ) |

| | |

|

| |

|

| |

|

|

| (1) | | Sales revenue includes intermediate-product sales, commodity and related currency hedging. Inter-segment sales are on a commercial basis and are not significant. All revenues are considered to be generated in Australia – see Note 7 of our Consolidated Financial Statements. |

The operations and assets of our business segments are further described in Item 4D “Property, Plant and Equipment”.

20

| | | | |

| | INFORMATION ON THE COMPANY | | |

C. Organizational Structure

The WMC Resources Group consists of WMC Resources, the ultimate parent company, and its subsidiaries. Our business is split into business units based on major production commodities and activities:

| | • | | Regional Exploration and New Business; and |

The principal companies within the WMC Resources Group are:

| | • | | WMC Resources Ltd – Incorporated in Australia, WMC Resources Ltd is the parent holding company as well as an operating entity that owns the nickel mining, processing and marketing operations. |

| | • | | WMC (Olympic Dam Corporation) Pty Ltd – Incorporated in Australia, this company owns the Olympic Dam Operations which produces high quality refined copper and uranium oxide and gold and silver as co-products. It is wholly owned by WMC Resources Ltd. |

| | • | | WMC Fertilizers Pty Ltd – Incorporated in Australia, this company owns the Queensland Fertilizer Operations and fertilizer distribution arm, Hi-Fert Pty Ltd. It is wholly owned by WMC Resources Ltd. |

| | • | | WMC Finance Limited – Incorporated in Australia, this company’s principal activities are the borrowing and lending of money and other financing activities, including commodity and currency hedging and the selling of gold and silver purchased from related entities. It is wholly owned by WMC Resources Ltd. |

| | • | | WMC Finance (USA) Limited – Incorporated in Australia, the principal activity of this company is to hold debt issued in the United States markets. It is wholly owned by WMC Resources Ltd. |

D. Property, Plant and Equipment

All our assets are 100% owned, either directly or through subsidiary companies, unless otherwise stated.

Under our current life of mine plans, all reported reserves will be mined out within the period of existing leases or concessions or within the time period of assured renewal periods. All reported reserves, except for Corridor Sands, are at sites which have all required permits and government approvals. On conversion to a mining license from the existing exploration title, Corridor Sands reported reserves will be mined within the period of the mining license or within the time period of assured renewal periods.

21

| | | | |

| | INFORMATION ON THE COMPANY | | |

Our nickel business unit is a fully integrated nickel business comprising mines, concentrators, a smelter and a refinery. We produced 117,722 tonnes of contained nickel-in-concentrate extracted from 14.5 million tonnes of ore processed in the year ended December 31, 2003. This compared with production of 106,423 tonnes of contained nickel-in-concentrate in the year ended December 31, 2002 from 14.3 million tonnes of ore processed. Purchased feed from third parties was 25,940 tonnes of recovered nickel for the year ended December 31, 2003, compared to 20,900 tonnes for the year ended December 31, 2002.

Our strategy for the nickel business unit is to:

| | • | | increase output at a minimum capital cost and reduce the unit cost of production through process improvement, technology and de-bottlenecking; |

| | • | | maintain the business as a major low-cost producer; |

| | • | | pursue commercially viable growth through regional exploration in Western Australia and development of our strong resource position through projects such as Yakabindie; and |

| | • | | participate in the benefits that small, focused operators are extracting from the divested Kambalda mines. |

We commenced production of nickel-in-concentrate in 1967, following the discovery of significant nickel ore reserves at Kambalda. We currently mine nickel ore from both open-cut and underground mines at our wholly owned mines at Leinster and Mount Keith. We ceased mining at Kambalda in 2002. The mill and concentrator at Kambalda are now fed with third party ore. Nickel ore is concentrated at Kambalda, Leinster and Mount Keith and then the majority of this nickel concentrate is transported to the Kalgoorlie Nickel Smelter to be smelted into nickel matte. We sell some of the Mount Keith production directly as concentrate. In the year ended December 31, 2003, we sold 37% of nickel-in-matte produced to overseas customers compared to 28% in 2002 fiscal year and refined the balance at our Kwinana Nickel Refinery to produce LME accredited nickel briquettes, nickel powder and various other intermediate products such as ammonium sulphate.

Pursuant to an agreement with Southern Cross Energy which expires in 2013, power at the Kambalda, Mount Keith and Leinster nickel operations and at the Kalgoorlie Nickel Smelter is primarily derived from on-site third party gas fired turbines with power at the Kwinana Refinery being wheeled from the goldfields through Western Power. Under the agreement with Southern Cross Energy, we have a take or pay obligation to purchase energy. In the Goldfields region, until 2006, gas is purchased under long term contract and is sourced from North West gas fields and transported by the Goldfields Gas Pipeline. Under the gas transmission agreement, we have an 80% take or pay obligation. Since December 31, 2001 the transmission tariff has increased by approximately 30% and we are currently disputing this increase in accordance with the dispute resolution procedures under the transmission agreement. The Western Australian Independent Gas Pipeline Regulator has made a draft decision regarding tariffs payable by third parties for access to the pipeline suggesting that a lower access tariff to that currently proposed by the pipeline owners should apply. The pipeline owners have commenced proceedings in the Supreme Court of Western Australia seeking a declaration that the Regulators’ draft decision does not apply. Until 2007, gas for the Kwinana Refinery will be sourced from the north western region of Western Australia and is transported by the Dampier to Bunbury natural gas pipeline, with us having a 70% take or pay obligation.

22

| | | | |

| | INFORMATION ON THE COMPANY | | |

A summary of the production of nickel-in-concentrate from our mines and third parties, matte from its smelter and metal from its refinery for the last five years is set out below.

NICKEL PRODUCTION SUMMARY

| | | | | | | | | | |

| | | Year Ended

December 31,

2003(3)

| | Year Ended

December 31, 2002(2)

| | Year Ended

December 31,

2001

| | Year Ended

December 31,

2000

| | Year Ended

December 31,

1999(1)

|

| | | (tonnes) |

| | | Nickel-in-concentrate Produced |

Kambalda | | 25,912 | | 23,225 | | 18,653 | | 19,202 | | 11,114 |

Leinster | | 41,806 | | 40,006 | | 38,008 | | 40,724 | | 35,953 |

Mount Keith | | 50,004 | | 43,192 | | 47,930 | | 47,532 | | 41,208 |

| | |

| |

| |

| |

| |

|

Total | | 117,722 | | 106,423 | | 104,591 | | 107,458 | | 88,275 |

| | |

| |

| |

| |

| |

|

| |

| | | Kalgoorlie Smelter Production |

Concentrate treated | | 711,100 | | 640,500 | | 704,330 | | 737,244 | | 575,219 |

Matte produced | | 147,700 | | 134,400 | | 140,432 | | 148,051 | | 116,299 |

Nickel-in-matte produced | | 99,152 | | 91,574 | | 96,650 | | 103,019 | | 79,668 |

| |

| | | Kwinana Refinery Production |

Matte treated | | 92,000 | | 100,700 | | 94,208 | | 93,975 | | 79,792 |

Refined nickel produced | | 61,417 | | 65,055 | | 61,324 | | 60,532 | | 53,009 |

| | |

| |

| |

| |

| |

|

| (1) | | In 1999, the Kalgoorlie Nickel Smelter was shut down for 63 days for a major furnace rebuild following a furnace leak. |

| (2) | | In 2002, the Kalgoorlie Nickel Smelter was shut down for 24 days for repairs to the mist precipitators following a fire. |

| (3) | | In 2003, the Kwinana Nickel Refinery was shut down for 19 days for repairs following a rupture in the boiler tube. |

23

| | | | |

| | INFORMATION ON THE COMPANY | | |

The table below shows our proven and probable nickel ore reserves.

NICKEL ORE RESERVES(1), (2), (3)

As at December 31, 2003

| | | | | | | | | | | | | | | | |

Operation

| | Type of

Reserve(4)

| | Proven(5)

| | Probable(6)

| | Total

| | Assumed overall

Metallurgical

Recovery(7)

|

| | | | | Ore million tonnes

| | Grade %

| | Ore million tonnes

| | Grade %

| | Ore million tonnes

| | Grade %

| | (%)

|

Kambalda | | u/g | | — | | — | | 0.10 | | 3.30 | | 0.10 | | 3.30 | | 87 |

Leinster | | u/g | | 7.50 | | 1.80 | | 11.10 | | 1.90 | | 18.50 | | 1.80 | | 79 |

| | | o/c | | — | | — | | 0.60 | | 1.70 | | 0.60 | | 1.70 | | 76 |

| | | s/p | | 0.20 | | 1.90 | | — | | — | | 0.20 | | 1.90 | | 79 |

Mount Keith | | o/c | | 195.00 | | 0.56 | | 86.00 | | 0.57 | | 281.00 | | 0.56 | | 65 |

| | | s/p | | 27.20 | | 0.49 | | — | | — | | 27.20 | | 0.49 | | 48 |

| | | | |

| |

| |

| |

| |

| |

| |

|

| (1) | | The commodity price used to estimate the 2003 nickel ore reserves was A$5.00/lb. At the 3 year average exchange rate this equates to US$2.85/lb. |

| (2) | | Ore reserves reflect tonnages recoverable from mining. The estimates include diluting materials and allowances for losses which may occur when the material is mined but do not include adjustments for metallurgical recovery. |

| (3) | | We have a 100% interest in all operations. |

| (4) | | u/g – underground, o/c = open-cut, s/p = stockpile |

| (5) | | Approximate drill hole spacings we used to classify the proven ore reserves are: |

| | • | | Leinster (Perseverance Shoot) –£25m x 25m and |

| | • | | Mount Keith –£40m x 40m. |

| (6) | | Approximate drill hole spacings we used to classify the probable ore reserves are: |

| | • | | Leinster (Perseverance Shoot) –£50m x 50m and |

| | • | | Mount Keith –£80m x 80m. |

| (7) | | The metallurgical recovery factors included in the tabulation represent the estimated overall nickel recovery, from run-of-mine ore feed to final saleable product, assumed in the estimation of the ore reserves. The reported factors for the nickel operations are estimated primarily on the basis of the historical concentrator, smelter and refinery performance, and do not include current planned metallurgical recovery improvements. Assumed metallurgical recoveries for the individual components of the nickel business are the following: |

| | • | | Kambalda concentrator: 92%, |

| | • | | Leinster concentrator: 83% (u/g ore) and 80% (o/c ore) |

| | • | | Mount Keith concentrator: 68% (o/c ore) and 51% (s/p ore),. |

| | • | | Kalgoorlie Nickel Smelter: 97% |

| | • | | Kwinana Nickel Refinery: 98% |

In 2003, we continued our exploration work at our West Musgrave nickel-copper project in Western Australia. West Musgrave is located within the Musgrave Ranges north-east of Laverton near the South Australian border. The tenements lie entirely within Aboriginal Reserve No. A17614, administered by the Ngaanyatjarra Land Council. See discussion of West Musgrave at “Regional Exploration and New Business – Minerals Exploration – West Musgrave, Western Australia”.

Nickel Operations

Kambalda Nickel Operations

Our Kambalda operations are located 56 kilometers south of Kalgoorlie in Western Australia and comprise a concentrator and a high-grade nickel sulphide mine. Since early 2000, we have been selling our mines at Kambalda and entering into long-term nickel

24

| | | | |

| | INFORMATION ON THE COMPANY | | |

purchase agreements with the mine operators for the processing of ore and the purchase of subsequent concentrate. The divestment of the mines is part of our nickel strategy to divest mature mines where proven and probable reserves are nearly depleted and reduce the capital intensity of the operation. During the first half of 2002, we ceased mining ore at Kambalda and now rely entirely on third party ore for feed through the concentrator, some of which is sourced from mines previously owned by us. The Kambalda concentrator has a capacity of 1.5 million tonnes of ore per year. In 2003, the utilization of the Kambalda concentrator was approximately 54%. This is expected to increase to approximately 75% in 2004. The nickel concentrate, containing approximately 14% nickel, is dried at Kambalda and transported by rail to the Kalgoorlie Nickel Smelter for conversion to nickel-in-matte.

Purchases from third parties amounted to 25,940 tonnes of recovered nickel for the year ended December 31, 2003, and 20,900 tonnes for the year ended December 2002. We sold the lease containing the Miitel mine, previously on care-and-maintenance, in November 2000. During 2001 the Wannaway mine and North Widgiemooltha Block were sold to external parties. We leased land containing the Otter, Juan and Coronet North mines to third parties under a long term arrangement. We sold the Long Victor mine during September 2002. The Lanfranchi mine complex is the only mine at Kambalda we still own. We ceased mining at Lanfranchi at the end of March 2002. We anticipate that, subject to regulatory approval, we will enter into an agreement during 2004 to sublet this mine. We have entered into long-term nickel purchase agreements with the purchasers of these mines.

The net written down value of property and associated plant and equipment at Kambalda Nickel Operations at December 31, 2003 was A$15.2 million.

Leinster Nickel Operations

Leinster is approximately 375 kilometers north of Kalgoorlie in Western Australia. We purchased the Leinster Nickel Operations in 1988 from Mount Isa Mines and Western Selcast.

The site comprises underground and open pit mines and a concentrator and is supported by the nearby township of Leinster. The Leinster deposits consist of both medium-grade disseminated sulfide and sulfide mineralization with average grades of approximately 2.0%. During 2003, we sourced our Leinster production from the Perseverance underground mine and the Harmony open cut mine. The Leinster mill operating capacity is rated 2.7 million tonnes of ore per year and its utilization is currently approximately 92%. The nickel-in-concentrate, containing approximately 12% nickel, is dried at Leinster before being delivered to our Kalgoorlie Nickel Smelter for further processing.

The net written down value of our property and associated plant and equipment at Leinster Nickel Operations at December 31, 2003 was A$304.7 million. Our reserves are equivalent to approximately ten years life at current production rates.

Mount Keith Operations

Mount Keith is located in Western Australia, approximately 450 kilometers north of Kalgoorlie and 80 kilometers north of Leinster. The Mount Keith deposit is a low-grade disseminated sulphide ore body averaging some 0.6% nickel that is mined by open-cut method. The operation includes a concentrator and ancillary facilities and we officially commissioned it in January 1995.

We have an agreement to sell up to a maximum of 14,000 tonnes of nickel-in-concentrate per year to OMG Harjavalta Nickel Oy. The contract term will expire when 140,000 tonnes in total have been delivered, which is expected to occur in the first quarter of 2005. Mount Keith concentrates, containing approximately 20% nickel, not contracted for sale are transported by road to Leinster or Kambalda for drying and blending with other concentrates and then delivered to the Kalgoorlie Nickel Smelter for smelting.

The nominal capacity of the Mount Keith concentrator is 11.2 million tonnes of ore per annum. It currently has a utilization of approximately 100%. Average nickel recoveries of around 71% were achieved in 2003. We recently completed a feasibility study which indicates that the milling capacity at Mount Keith could be increased by up to 30%.

The net written down value of our property and associated plant and equipment at Mount Keith Operations at December 31, 2003 was A$531.6 million. Our reserves included in the current mine plan will be depleted in approximately 18 years at current production rates.

Kalgoorlie Nickel Smelter

We constructed the Kalgoorlie Nickel Smelter and commenced operation in 1972 to supply nickel matte under sales contracts to overseas nickel refiners and also to supply our nickel refinery at Kwinana. The smelter receives supplies of concentrate from the Kambalda, Leinster and Mount Keith treatment plants. We use a flash smelting process to produce matte containing 66% to 75% nickel and 2% to 3% copper.

25

| | | | |

| | INFORMATION ON THE COMPANY | | |

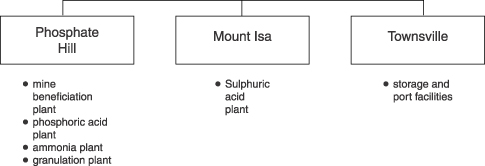

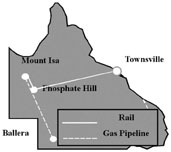

The Kalgoorlie Nickel Smelter also produces sulphuric acid. We sell most of the sulphuric acid to nickel laterite operations in the Kalgoorlie area, with some acid being used at Mount Keith and the Kwinana Nickel Refinery. In the year ended December 31, 2003, we produced 528,921 tonnes of sulphuric acid compared to 489,568 tonnes in the previous 12 months.

In the year ended December 31, 2003 approximately 63% of the nickel-in-matte we produced, and in the year ended December 31, 2002 approximately 72% of the nickel-in-matte we produced, was sent by rail to our refinery at Kwinana where we refined it to nickel metal. We exported the remainder.

The net written down value of our property and associated plant and equipment at the Kalgoorlie Nickel Smelter at December 31, 2003 was A$231.5 million.

Kwinana Nickel Refinery

The Kwinana Nickel Refinery is 30 kilometers south of Perth in Western Australia. We constructed the refinery, which commenced operation in 1970, and use the Sherritt-Gordon ammonia leach process to convert nickel matte from the Kalgoorlie Nickel Smelter into LME grade nickel briquettes and nickel powder. A small amount of higher grade nickel concentrate from Mount Keith has on occasion been used to supplement matte as feedstock. The refinery also produces a number of intermediate products, including copper sulphide, cobalt-nickel sulphide and ammonium sulphate. The cobalt-nickel sulphide is treated by a third-party processor that separates the nickel and cobalt into metal. We receive a credit for the nickel and have the cobalt metal returned for subsequent sale.

The net written down value of our property and associated plant and equipment at the Kwinana Nickel Refinery at December 31, 2003 was A$156.5 million.

Markets and Competition

Nickel is used primarily in the production of stainless steel, low alloy steels, nickel-based alloys to impart strength, toughness and corrosion resistance. It is also used for electroplating and the production of chemicals and batteries. Stainless steel accounted for approximately 67% of world primary nickel demand in 2003 and this percentage is expected to gradually increase as stainless steel is expected to grow faster than other nickel applications. In the western world, growth in demand for stainless steel has consistently outstripped growth in industrial production.

The London Metal Exchange is the central price setting market for most nickel. Having reached a cyclical low in 2001, nickel prices posted a modest recovery in 2002. Nickel prices strengthened further in 2003 due to higher stainless steel production, strong Chinese demand and tight availability of stainless steel scrap. Nickel prices in 2003 ranged from US$3.27/lb to US$7.56/lb, from a range of US$2.55/lb to US$3.50/lb in 2002 (average daily cash settlement). We believe that the medium-to long-term outlook is positive due to limited new supply coming on-stream and expected continued growth in stainless steel production as a result of substantial new capacity additions.

We sell nickel metal, nickel matte, nickel concentrate and various intermediate-products. Most of our nickel metal sales are made under short- to medium-term contractual arrangements. We sell nickel metal to a large number of customers in Europe, North America and Asia. We also maintain websites for the sale of cobalt metal.

Most of our nickel-in-matte sales are made under medium-to long-term contractual arrangements to customers in Asia and Europe. Our long-term contractual arrangements to supply 26,000 tonnes to Sumitomo progressively expires between 2003 and 2005. In 2002, we entered into a three year agreement, commencing in 2005, for 10,000 tonnes of nickel-in-matte per year with Jinchuan Non-Ferrous Metals I/E Company of China. In 2003, we concluded a second nickel-in-matte sales agreement with Jinchuan. The second contract is a six-year agreement, commencing in 2005, for 15,000 tonnes of nickel-in-matte per year.

26

| | | | |

| | INFORMATION ON THE COMPANY | | |

Our Olympic Dam Operations in South Australia are a significant Australian producer of both copper and uranium oxide. Our Olympic Dam subsidiary assumed 100% ownership of the Olympic Dam Operations on March 31, 1993 after previously holding 51% in the joint venture that established operations at Olympic Dam.

During 2002, Olympic Dam completed an optimization project to increase its production capacity to 235,000 tonnes per annum of refined copper. However, due to the rebuild of the copper and uranium solvent extraction plants, the planned reline of the smelter furnace and a failure of a heat exchanger in the acid plant, actual production in 2003 was 160,080 tonnes. We are planning production in 2004 to be approximately 230,000 tonnes of copper. Over the next two years, we will invest approximately A$50 million on the next phase of the Olympic Dam Development Study which may result in increasing copper production to in excess of 500,000 tonnes per annum.

A summary of our Olympic Dam copper, uranium oxide and gold and silver production is set out below

OLYMPIC DAM PRODUCTION SUMMARY

| | | | | | | | | | | | |

| | | | | Year Ended

December 31,

2003

| | Year Ended

December 31,

2002

| | Year Ended

December 31,

2001

| | Year Ended

December 31,

2000

| | Year Ended

December 31,

1999

|

Ore treated | | ‘000s tonnes | | 8,386 | | 8,875 | | 9,336 | | 8,901 | | 6,743 |

Grade of Ore: | | | | | | | | | | | | |

Copper | | % | | 2.42 | | 2.57 | | 2.47 | | 2.53 | | 2.69 |

Uranium oxide concentrate | | kilograms/tonne | | 0.63 | | 0.69 | | 0.72 | | 0.73 | | 0.78 |

Gold | | grams/tonne | | 0.47 | | 0.53 | | 0.59 | | 0.53 | | 0.65 |

Metal Produced: | | | | | | | | | | | | |

Refined copper | | tonnes | | 160,080 | | 178,120 | | 200,523 | | 200,423 | | 138,272 |

Uranium oxide concentrate | | tonnes | | 3,203 | | 2,891 | | 4,379 | | 4,539 | | 3,221 |

Gold | | ounces | | 86,117 | | 64,293 | | 113,412 | | 69,967 | | 30,510 |

| | | | |

| |

| |

| |

| |

|