Use these links to rapidly review the document

TABLE OF CONTENTS

INDEX TO CONSOLIDATED FINANCIAL STATEMENTS

As filed with the Securities and Exchange Commission on May 14, 2003

Registration No. 333-102428

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 3 to

FORM S-4

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

| Rexnord Corporation | Delaware | 551112 | 04-3722228 | |||

| Rexnord Industries, Inc. | Delaware | 333613 | 39-1626766 | |||

| PT Components Inc. | Delaware | 551112 | 35-1537461 | |||

| RBS Acquisition Corporation | Delaware | 551112 | 72-1538677 | |||

| Rexnord Germany-1 Inc. | Delaware | 551112 | 39-1596220 | |||

| Rexnord International Inc. | Delaware | 333613 | 39-1049617 | |||

| Winfred Berg Licensco Inc. | Delaware | 551112 | 06-1260440 | |||

| W.M. Berg Inc. | Delaware | 333613 | 11-2583091 | |||

| RAC-I, Inc. | Delaware | 551112 | 68-0532385 | |||

| RBS North America, Inc. | Delaware | 551112 | 04-3722224 | |||

| RBS Global, Inc. | Delaware | 551112 | 01-0752045 | |||

| RBS China Holdings, L.L.C. | Delaware | 551112 | 68-0532389 | |||

| Prager Incorporated | Louisiana | 333612 | 72-0291860 | |||

| Addax Inc. | Nebraska | 333613 | 47-0696432 | |||

| Clarkson Industries, Inc. | New York | 332510 | 13-1980041 | |||

| Rexnord Ltd. | Nevada | 551112 | 39-1143248 | |||

| Rexnord Puerto Rico Inc. | Nevada | 326199 | 52-1126633 | |||

| Betzdorf Chain Company Inc. | Wisconsin | 551112 | 39-1348952 | |||

| (Exact name of registrantas specified in its charter) | (State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification Number) |

| 4701 Greenfield Avenue Milwaukee, WI 53214 (414) 643-3000 | Thomas J. Jansen Chief Financial Officer 4701 Greenfield Avenue Milwaukee, WI 53214 (414) 643-3000 | |

| (Address, including zip code, and telephone number, including area code, of each of the co-registrants' principal executive offices) | (Name, address, including zip code, and telephone number, including area code, of agent for service) |

Copy to:

Marc D. Jaffe, Esq.

Latham & Watkins LLP

885 Third Avenue

New York, New York 10022

(212) 906-1200

Approximate date of commencement of proposed sale to the public: As soon as practicable after this registration statement becomes effective.

If any of the securities being registered on this Form are being offered in connection with the formation of a holding company and there is compliance with General Instruction G, check the following box. o

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and we are not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Subject to completion, dated , 2003

PROSPECTUS

Rexnord Corporation

Offer to Exchange

$225,000,000 principal amount of its 101/8% Senior Subordinated Notes due 2012,

which have been registered under the Securities Act,

for any and all of its outstanding 101/8% Senior Subordinated Notes due 2012

We are offering to exchange all of our outstanding 101/8% senior subordinated notes due 2012, which we refer to as the old notes, for our registered 101/8% senior subordinated notes due 2012, which we refer to as the exchange notes, and together with the old notes, the notes. The terms of the exchange notes are identical to the terms of the old notes except that the exchange notes have been registered under the Securities Act of 1933 and, therefore, are freely transferable. We will pay interest on the notes on June 15 and December 15 of each year. The first interest payment will be made on June 15, 2003. The notes will mature on December 15, 2012.

We may redeem up to 35% of the aggregate principal amount of the notes using proceeds from certain equity offerings completed prior to December 15, 2005. We may redeem the notes on or after December 15, 2007. Holders may require us to repurchase the notes upon a change in control. The notes will be our senior subordinated obligations and will rank junior to all of our existing and future senior debt. The notes will be guaranteed on a senior subordinated basis by our parent and certain of our current and future subsidiaries.

The principal features of the exchange offer are as follows:

- •

- The exchange offer expires at 5:00 p.m., New York City time, on , 2003, unless extended.

- •

- We will exchange all old notes that are validly tendered and not validly withdrawn prior to the expiration of the exchange offer.

- •

- You may withdraw tendered old notes at any time prior to the expiration of the exchange offer.

- •

- The exchange of old notes for exchange notes pursuant to the exchange offer will not be a taxable event for U.S. federal income tax purposes.

- •

- We will not receive any proceeds from the exchange offer.

- •

- We do not intend to apply for listing of the exchange notes on any securities exchange or automated quotation system.

Broker-dealers receiving exchange notes in exchange for old notes acquired for their own account though market-making or other trading activities must deliver a prospectus in any resale of the exchange notes.

Investing in the exchange notes involves risks. See "Risk Factors" beginning on page 15.

Neither the U.S. Securities and Exchange Commission nor any other federal or state agency has approved or disapproved of these securities to be distributed in the exchange offer, nor have any of these organizations determined that this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The date of this Prospectus is , 2003.

[Inside Front Cover]

Each broker-dealer that receives the exchange notes for its own account pursuant to the exchange offer must acknowledge that it will deliver a prospectus in connection with any resale of such exchange notes. The letter of transmittal delivered with this prospectus states that by so acknowledging and by delivering a prospectus, a broker-dealer will not be deemed to admit that it is an "underwriter" within the meaning of the Securities Act of 1933. This prospectus, as it may be amended or supplemented from time to time, may be used by a broker-dealer in connection with resales of exchange notes received in exchange for old notes where such old notes were acquired by such broker-dealer as a result of market-making activities or other trading activities. We have agreed that, for a period of not less than 180 days following the effective date of the registration statement, of which this prospectus is a part, we will make this prospectus available to any broker-dealer for use in connection with any such resale. See "Plan of Distribution."

We have not authorized any dealer, salesman or other person to give any information or to make any representation other than those contained or incorporated by reference in this prospectus. You must not rely upon any information or representation not contained or incorporated by reference in this prospectus as if we had authorized it. This prospectus does not constitute an offer to sell or a solicitation of an offer to buy any securities other than the registered securities to which it relates, nor does this prospectus constitute an offer to sell or a solicitation of an offer to buy securities in any jurisdiction to any person to whom it is unlawful to make such offer or solicitation in such jurisdiction.

TABLE OF CONTENTS

i

This summary highlights important information contained elsewhere in this prospectus. Because this is only a summary, it does not contain all of the information that may be important to you. This prospectus includes specific terms of the exchange offer, as well as information regarding our business and detailed financial data. Please review this prospectus in its entirety, including the risk factors and our financial statements and the related notes included elsewhere herein, before you decide to invest. Unless otherwise noted, references to the Company, we, us and our refer to Rexnord Corporation, formerly known as RBS Holdings, Inc., and its subsidiaries. Our fiscal year is the year ending March 31 of the corresponding calendar year. For example, our fiscal year 2002, or fiscal 2002, means the period from April 1, 2001 to March 31, 2002.

Our Company

We are one of the leading manufacturers of highly-engineered mechanical power transmission components with significant share in many of the markets we serve. Our product portfolio includes flattop chain and modular conveyer belts, industrial bearings, aerospace bearings and seals, special components, couplings and gears and industrial chain. We estimate that over 80% of our sales in fiscal year 2002 were from products for which we believe we had the number one or number two market position. Our products are used in the plants and equipment of companies in diverse industries, including food and beverage, energy, aerospace, forest products, cement and construction. We have a large and growing installed base of products that are consumed in use and have a predictable replacement cycle. In addition, due to the complexity of our customers' manufacturing operations and the high cost of process failures, our customers have demonstrated a strong preference to replace their worn Rexnord products with new Rexnord products. This replacement dynamic drives recurring replacement sales, which we refer to as aftermarket sales, that we estimate accounted for approximately 60% of our North American sales in fiscal year 2002 (excluding special components).

We manufacture our broad product portfolio of mechanical power transmission products in our 33 manufacturing facilities located around the world. Our products are either incorporated into products sold by original equipment manufacturers or sold to end-users through industrial distributors as aftermarket products. We have over 5,260 employees, and our industrial distribution customers resell our products through over 1,900 distributor branches throughout the United States. The following table displays our estimate of the primary end-markets we serve through our distributors and original equipment manufacturers.

| Percentage of Net Sales by End-Market for Fiscal Year 2002 | |||

|---|---|---|---|

| Food and Beverage | 22 | % | |

| Energy | 15 | % | |

| Aerospace | 11 | % | |

| Forest Products | 9 | % | |

| Construction | 7 | % | |

| Agri-farm | 6 | % | |

| Cement | 5 | % | |

| Air Handling | 5 | % | |

| Other | 20 | % | |

| Total | 100 | % | |

We operate in a single business segment and sell a single class of products, mechanical power transmission components. Our product portfolio consists of:

Flattop Chain. We are the leading developer and manufacturer of flattop chain and components for related conveyor systems, with approximately a 30% market share in fiscal year 2002. Our flattop chain is highly-engineered conveyor chain that provides a smooth, continuous conveying surface that is critical to high-speed operations such as those used to transport cans and bottles in beverage-filling

1

operations. We believe key end-users of our flattop chain products include Anheuser-Busch Companies, Inc., Coca-Cola Bottling Company, Nestlé S.A., Pepsi Bottling Group and The Procter & Gamble Company, and key original equipment manufacturer customers include GEBO Industries S.A., a subsidiary of Sidel SA, SIG Simonazzi and KRONES AG.

Industrial Bearings. We design and manufacture a wide variety of bearings, most of which are mounted. We estimate that we had the largest share of the U.S. mounted roller and ball bearings market, with approximately a 24% market share in fiscal year 2002. Bearings are components that support, guide and reduce the friction of motion between fixed and moving machine parts. Our key original equipment manufacturer customers for our industrial bearings products include Caterpillar Inc., Eaton Corporation, Mercury Marine International and Vermeer Manufacturing Company.

Aerospace Bearings and Seals. We believe that we are the leading supplier of rolling element airframe bearings, slotted-entry bearings and split-ball sliding bearings, and a leading supplier of aerospace seals, to the aerospace industry. We supply our aerospace bearings and seals to the commercial aircraft, military aircraft and regional jet end-markets for use in door and flight control systems, engine controls and mounts, landing gear and rotor pitch control. The majority of our sales are to engine and airframe original equipment manufacturers that specify our products for their aircraft platforms. Our key original equipment manufacturer customers for these products include The Boeing Company, the U.S. government, Allied Signal and GE Aircraft Engines.

Special Components. Our special components products are comprised of three primary product lines: electric motor brakes, miniature mechanical power transmission components and security devices for utility companies. Our key original equipment manufacturer customers include Baldor Electric Company, Cessna Aircraft Company, Vertek, Klauber Machine & Gear, Celestron International and Channel.

Couplings and Gears. We are the leading manufacturer of dry couplings in North America, and we also manufacture gearsets and gearboxes. Couplings are the interface between two shafts that permit power to be transmitted from one shaft to the other, and gearsets and gearboxes are used to reduce the output speed and increase the torque of an electric motor or engine to the level required to drive a particular piece of equipment. Our couplings and gears are sold to a variety of end-markets, including the chemical, petrochemical, food, steel, forest products and pulp and paper industries. Our key original equipment manufacturer customers include ABB Robotics, Astec Industries, Inc., Atlas Copco A.B., Stamler Machine Co., Inc. and U.S. Filter.

Industrial Chain. We are a leading supplier of industrial chain. We are a global manufacturer of highly-engineered industrial chain product, and we currently serve as a manufacturer of roller chain in Europe and reseller of commodity roller chain product in the United States. Our key original equipment manufacturer customers of industrial chain include Linde AG, The Charles Machine Works, Inc., U.S. Filter and Stamler.

Our Industry

Mechanical power transmission products are generally critical components in the machinery or plant in which they operate, yet they typically represent only a fraction of an end-user's total production cost. However, because the cost of product failure to the end-user is substantial, we believe end-users in most of the markets we serve consider a number of factors, rather than price alone, when making a purchasing decision. We believe end-users of mechanical power transmission components place a premium on factors such as quality, reliability, availability and selection. The most successful industry participants are those that can leverage their products' reputations for quality and reliability, as well as their distribution networks, to maintain attractive margins on products and gain market share. Our industry is also characterized by relatively high barriers to entry.

The mechanical power transmission industry is fragmented, containing numerous participants, most with limited product lines in specific geographies. The industry's customer base is broadly diversified across many sectors of the economy.

2

Our Competitive Strengths

- •

- Market Leadership Positions. We are one of the leading manufacturers of highly-engineered mechanical power transmission components. Specifically, we believe that we are the leading manufacturer of flattop chain and components for related conveyor systems and rolling element airframe bearings, and the leading manufacturer of dry couplings in North America. Our extensive offering of high-quality products, positive brand perception, highly-engineered product line, market experience and focus on customer satisfaction are the bases upon which we seek to maintain and grow the market share positions for our key products.

- •

- Significant Installed Base in Diversified End-markets. Almost all of our products are moving, wearing components that are consumed in use, creating a recurring aftermarket revenue stream that, on average, generates higher gross profit margins than our original equipment manufacturer sales. With our customers' demonstrated preference to replace their worn Rexnord products with new Rexnord products, our large installed base of products provides a source of recurring revenue and an additional barrier to entry for potential competitors. We serve customers across a wide array of end-markets, including sectors such as food and beverage, energy, aerospace, forest products, cement and construction.

- •

- Strong Liquidity and Attractive Margins. We generated $114.1 million of EBITDA and made capital expenditures totaling $17.3 million for the twelve months ended December 31, 2002. Our EBITDA margin was 15.7% for the twelve months ended December 31, 2002, despite a challenging economic environment. We believe our high margins are primarily attributable to the relative price stability of many of our products and our continuing restructuring efforts and cost savings initiatives.

- •

- Leading Distribution Relationships. We have established long-term relationships with original equipment manufacturers that serve a wide variety of industries. In turn these original equipment manufacturers, by incorporating our components into their products, have helped create a broad installed base for our products that generates significant aftermarket sales for us. We also have long-term relationships with several of the leading distributors in our industry. Approximately $225 million of our net sales in fiscal year 2002 were generated through our U.S. industrial distribution network.

- •

- Broad Portfolio of Highly-Engineered, Value-Added Components. We believe our product portfolio is one of the broadest in the mechanical power transmission industry. Our product portfolio features a wide range of complementary branded products that have positioned us as a one-stop supplier of choice. This product line breadth provides us leverage with distributors, creates end-user preference for our brands and allows us to pursue our cross-selling or "bundling" marketing strategy.

- •

- Strong and Experienced Management Team. We are led by an experienced management team with an average of 25 years of general industrial experience, including an average of 11 years at Rexnord or our former parent company, Invensys plc. In addition, in connection with the Acquisition, as defined below, George Sherman, the former Chief Executive Officer of Danaher Corporation, has joined us as the non-executive Chairman of the Board. As a result of the Acquisition, Mr. Sherman and other members of senior management own approximately 4% of our common equity and are eligible for additional equity incentives pursuant to a stock option plan.

Business Strategy

- •

- Drive Operational Excellence. One of the cornerstones of our business strategy is to continue to aggressively implement our operational excellence initiatives, collectively known as the Rexnord Business System. The Rexnord Business System includes the implementation at all operating levels of strategies to improve inventory management, customer delivery and plant utilization and to further improve our cost structure. Our near-term targets for improvement

3

- •

- Capitalize on Cyclical Recovery. Several of our businesses sell into industrial markets that have experienced cyclical volume declines over the past two years as a result of general economic conditions, a sharp liquidation of industrial inventories and, in the case of aerospace bearings and seals, an industry-specific downturn as a result of the events of September 11, 2001. While the timing of a recovery in cyclical markets is uncertain, we believe that we are well-positioned to experience margin improvement given the historical profitability of our business throughout the business cycle and the substantial fixed costs we have eliminated from our cost structure over the last two years.

- •

- Continue to Develop Higher Margin Business. We will focus our resources on increasing the sales of our higher margin, market-leading product lines. By strategically allocating our incremental resources to our higher margin businesses, we believe we will be able to improve the profitability of our overall business going forward.

- •

- Leverage our Sales and Distribution Network. Because we market our products directly to both original equipment manufacturers and end-users, we are able to create an expressed end-user preference for our products. This strategy of creating "pull-through" demand for our products is important in preserving our relative market power with original equipment manufacturers and distributors. Additionally, by organizing our sales and marketing organization along industry lines, we are able to leverage our industry knowledge, reputation and technical expertise to cross-sell other complementary product lines, in order to drive future sales growth.

- •

- Increase Served Market. In addition to pursuing bundling opportunities within certain industries, we are also using our extensive knowledge of these key industries to pursue similar opportunities in new markets. For example, we expect to continue to apply our extensive experience with end-users in the beverage industry to provide innovative solutions to end-users in the food industry. These cross-selling initiatives are currently underway, and we have identified this type of expansion as an area for growth. We are also pursuing the possibility of expanding our presence in Asia and Europe with certain of our product lines that have a leading market position or a demonstrated technological advantage over products currently being used in these areas.

include an additional reduction of inventory, continued improvement of on-time delivery and a significant improvement in quality metrics.

The Acquisition

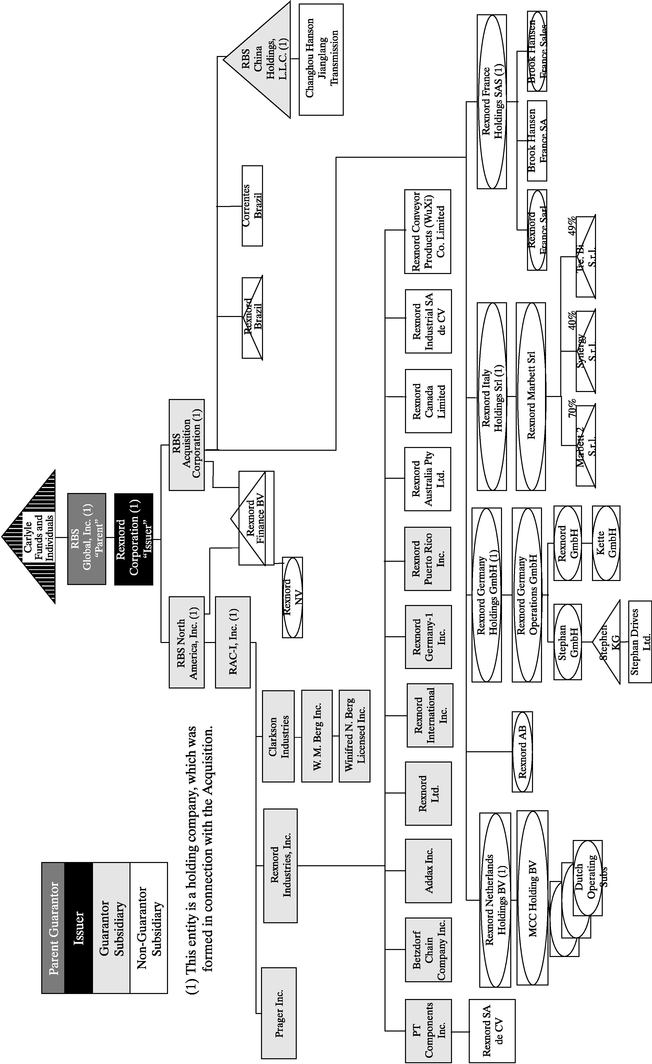

On September 27, 2002, RBS Acquisition Corporation, one of our subsidiaries, entered into a stock purchase agreement with Invensys plc and certain of its affiliates, pursuant to which RBS Acquisition and other affiliated purchasers acquired the business described in this prospectus. We refer to this transaction and the related transactions and financings, which closed on November 25, 2002, as the Acquisition. RBS Acquisition and the other purchasers are wholly-owned subsidiaries of Rexnord Corporation, which in turn is a wholly-owned subsidiary of RBS Global, Inc. Rexnord Corporation, RBS Acquisition and RBS Global are corporations formed at the direction of The Carlyle Group, certain other associated investors and Mr. George Sherman. The Acquisition closed simultaneously with the issuance of the old notes and the senior credit facilities.

Our Investors

As a result of the Acquisition, certain affiliates of The Carlyle Group, through their holdings in RBS Global, own approximately 96% and Mr. George Sherman, Mr. Robert Hitt and other senior management, through their holdings in RBS Global, own approximately 4% of our common equity. The Carlyle Group also controls our board of directors.

4

The Offering of the Old Notes

On November 25, 2002, Rexnord Corporation completed an offering of $225.0 million in aggregate principal amount of 101/8% senior subordinated notes due 2012, which was exempt from registration under the Securities Act.

| Old Notes | Rexnord Corporation sold the old notes to Credit Suisse First Boston Corporation, Deutsche Bank Securities Inc. and Wachovia Securities, Inc., the initial purchasers, on November 25, 2002. The initial purchasers subsequently resold the old notes to qualified institutional buyers pursuant to Rule 144A under the Securities Act and to non-U.S. persons outside the United States in reliance on Regulation S under the Securities Act. | |||

Registration Rights Agreement | In connection with the sale of the old notes, we, RBS Global, Inc. and the subsidiary guarantors, which together we refer to as the guarantors, entered into a registration rights agreement with the initial purchasers. Under the terms of that agreement, we agreed to: | |||

• | file a registration statement for the exchange offer and the exchange notes within 90 days after the date on which the old notes were purchased by the initial purchasers; | |||

• | use our reasonable best efforts to cause the exchange offer registration statement to become effective under the Securities Act within 180 days after the date on which the old notes were purchased by the initial purchasers; and | |||

• | file a shelf registration statement for the resales of the old notes or the exchange notes, as the case may be, under certain circumstances and use our reasonable best efforts to cause such shelf registration statement to be declared effective under the Securities Act. | |||

If we and the guarantors fail to meet any of these requirements, it will constitute a default under the registration rights agreement and we and the guarantors must pay additional interest on the notes of up to 0.50% per annum for the first 90-day period after any such default. This interest rate will increase by an additional 0.50% per annum with respect to each subsequent 90-day period until all such defaults have been cured, up to a maximun additional interest rate of 1.0% per annum. The exchange offer is being made pursuant to the registration rights agreement and is intended to satisfy the rights granted under the registration rights agreement, which rights terminate upon completion of the exchange offer. | ||||

5

The Exchange Offer

| Exchange Offer | $1,000 principal amount of exchange notes will be issued in exchange for each $1,000 principal amount of old notes validly tendered. | |||

Resale | Based upon interpretations by the staff of the SEC set forth in no-action letters issued to unrelated third parties, we believe that the exchange notes may be offered for resale, resold or otherwise transferred to you without compliance with the registration and prospectus delivery requirements of the Securities Act of 1933, unless you: | |||

• | are an "affiliate" of ours within the meaning of Rule 405 under the Securities Act; | |||

• | are a broker-dealer who purchased the old notes directly from us for resale under Rule 144A or any other available exemption under the Securities Act of 1933; | |||

• | acquired the exchange notes other than in the ordinary course of your business; or | |||

• | have an arrangement with any person to engage in the distribution of exchange notes. | |||

However, we have not submitted a no-action letter and there can be no assurance that the SEC will make a similar determination with respect to the exchange offer. Furthermore, in order to participate in the exchange offer, you must make the representations set forth in the letter of transmittal that we are sending you with this prospectus. | ||||

Expiration Date | The exchange offer will expire at 5:00 p.m., New York City time, on , 2003, which we refer to as the expiration date, unless we, in our sole discretion, extend it. | |||

Conditions to the Exchange Offer | The exchange offer is subject to certain customary conditions, some of which may be waived by us. See "The Exchange Offer—Conditions to the Exchange Offer." | |||

Procedure for Tendering Old Notes | If you wish to accept the exchange offer, you must complete, sign and date the letter of transmittal, or a copy of the letter of transmittal, in accordance with the instructions contained in this prospectus and in the letter of transmittal, and mail or otherwise deliver the letter of transmittal, or the copy, together with the old notes and any other required documentation, to the exchange agent at the address set forth in this prospectus and in the letter of transmittal. | |||

6

We will accept for exchange any and all old notes that are properly tendered in the exchange offer prior to the expiration date. The exchange notes issued in the exchange offer will be delivered promptly following the expiration date. See "The Exchange Offer—Terms of the Exchange Offer." | ||||

Special Procedures for Beneficial Owners | If you are the beneficial owner of old notes registered in the name of a broker, dealer, commercial bank, trust company or other nominee and wish to tender in the exchange offer, you should contact the person in whose name your notes are registered and promptly instruct the person to tender on your behalf. | |||

Guaranteed Delivery Procedures | If you wish to tender your old notes and time will not permit your required documents to reach the exchange agent by the expiration date, or the procedure for book-entry transfer cannot be completed on time, you may tender your notes according to the guaranteed delivery procedures. For additional information, you should read the discussion under "The Exchange Offer—Guaranteed Delivery Procedures." | |||

Withdrawal Rights | The tender of the old notes pursuant to the exchange offer may be withdrawn at any time prior to 5:00 pm, New York City time, on the expiration date. | |||

Acceptance of Old Notes and Delivery of Exchange Notes | Subject to customary conditions, we will accept old notes which are properly tendered in the exchange offer and not withdrawn prior to the expiration date. The exchange notes will be delivered promptly following the expiration date. | |||

Effect of Not Tendering | Any old notes that are not tendered or that are tendered but not accepted will remain subject to the restrictions on transfer. Since the old notes have not been registered under the federal securities laws, they bear a legend restricting their transfer absent registration or the availability of a specific exemption from registration. Upon the completion of the exchange offer, we will have no further obligations, except under limited circumstances, to provide for registration of the old notes under the federal securities laws. See "The Exchange Offer—Effect of Not Tendering." | |||

Interest on the Exchange Notes and the Old Notes | The exchange notes will bear interest from the most recent interest payment date to which interest has been paid on the notes or, if no interest has been paid, from November 25, 2002. Interest on the old notes accepted for exchange will cease to accrue upon the issuance of the exchange notes. | |||

7

Certain U.S. Federal Income Tax Considerations | The exchange of old notes for exchange notes by tendering holders will not be a taxable exchange for federal income tax purposes, and such holders will not recognize any taxable gain or loss or any interest income for federal income tax purposes as a result of such exchange. See "Certain U.S. Federal Income Tax Consequences." | |||

Exchange Agent | Wells Fargo Bank Minnesota, National Association, the trustee under the indenture, is serving as exchange agent in connection with the exchange offer. | |||

Use of Proceeds | We will not receive any proceeds from the issuance of exchange notes pursuant to the exchange offer. | |||

8

Summary of the Terms of the Exchange Notes

| Issuer | Rexnord Corporation. | |||

Notes Offered | $225.0 million aggregate principal amount of 101/8% Senior Subordinated Notes due 2012. | |||

Interest | 101/8% per annum, payable semi-annually in arrears on June 15 and December 15 of each year, beginning June 15, 2003. | |||

Maturity Date | December 15, 2012. | |||

Optional Redemption | Except in the case of certain equity offerings by us, we cannot choose to redeem the notes until December 15, 2007. At any one or more times after that date, we may choose to redeem some or all of the notes at certain specified prices, plus accrued and unpaid interest. | |||

Optional Redemption After Equity Offerings | At any one or more times before December 15, 2005, we may choose to redeem up to 35% of the original aggregate principal amount of notes with money raised in one or more equity offerings, as long as we pay 110.125% of the principal amount of the notes, plus accrued and unpaid interest, and at least 65% of the original aggregate principal amount of notes remain outstanding afterwards. See "Description of the Exchange Notes—Optional Redemption." | |||

Change In Control | Upon a change in control, we may be required to make an offer to purchase each holder's notes at a price equal to 101% of the principal amount thereof, plus accrued and unpaid interest, if any, to the date of purchase. We cannot assure you that there will be sufficient funds available for us to make any required repurchases of the exchange notes upon a change of control. In addition, our senior credit facility prohibits us from repurchasing the exchange notes until we first pay our senior credit facility in full. Our failure to repurchase the exchange notes upon a change of control will constitute an event of default under the indenture governing the exchange notes. Upon this event of default, the trustee under the indenture may declare the principal and accrued and unpaid interest on the notes immediately due and payable, which, in turn, would constitute a default under our senior credit facility. See "Description of the Exchange Notes—Defaults." Under these circumstances, the subordination provisions of the indenture would likely restrict payments to the holders of the outstanding notes until all amounts due and owing under the credit facility are paid in full. | |||

Subordination | The notes are unsecured obligations of Rexnord Corporation. The notes are subordinated in right of payment to all existing and future senior indebtedness and the guarantees are subordinated in right of payment to all existing and other indebtedness and other liabilities of the guarantors. The notes are effectively subordinated to all existing and other indebtedness and other liabilities of certain of our subsidiaries which are not guarantors. As of December 31, 2002, we had senior indebtedness of approximately $367.9 million. | |||

9

Guarantees | The notes are unconditionally guaranteed, jointly and severally, by our parent and certain of our current and future subsidiaries. | |||

Covenants | The indenture contains covenants that limit what we (and certain of our subsidiaries) may do. The indenture contains covenants that limit our ability to: | |||

• | incur or guarantee additional indebtedness; | |||

• | pay dividends on, redeem or repurchase our capital stock; | |||

• | make certain investments; | |||

• | permit payment or dividend restrictions on certain of our subsidiaries; | |||

• | sell assets; | |||

• | engage in certain transactions with affiliates; and | |||

• | consolidate or merge or sell all or substantially all of our assets and the assets of certain of our subsidiaries. | |||

In addition, we are obligated to offer to repurchase the notes at 100% of their principal amount, plus accrued and unpaid interest, if any, to the date of repurchase, in the event of certain asset sales. | ||||

These restrictions and prohibitions are subject to a number of important qualifications and exceptions. See "Description of the Exchange Notes—Certain Covenants." | ||||

Risk Factors

Investment in the exchange notes involves certain risks. You should carefully consider the information under "Risk Factors" and all other information included in this prospectus before investing in the notes.

Additional Information

Rexnord Corporation was incorporated in Delaware on September 26, 2002. Our principal executive offices are located at 4701 Greenfield Avenue, Milwaukee, Wisconsin 53214. Our telephone number is (414) 643-3000. The following items referred to in this prospectus are registered and other trademarks pursuant to applicable intellectual property laws and are the property of Rexnord Corporation or our subsidiaries: Rex®, Link-Belt®, MB®, Duralon®, Thomas®, Omega®, Rex® Viva®, MagneLink®, Addax®, ModulFlex®, Shafer® Bearing, PSI® Bearing, Cartriseal®, Brook Hansen™, Planetgear™ and Prager™.

10

Summary Pro Forma Combined Financial Information

The following summary pro forma combined financial information is based on our combined financial statements included elsewhere in this prospectus. Our combined financial statements at March 31, 2001 and 2002 and for the years ended March 31, 2000, 2001 and 2002 have been audited by Ernst & Young LLP, our independent auditors. Our condensed combined financial statements at December 31, 2002 and for the nine-month period ended December 31, 2001, the period from April 1, 2002 through November 24, 2002 and the period from November 25, 2002 through December 31, 2002 are unaudited but, in the opinion of our management, include all adjustments, consisting only of normal recurring accruals, necessary for a fair presentation. See "Unaudited Pro Forma Combined Financial Information."

| | Pro Forma Fiscal Year Ended March 31, 2002 | Pro Forma Twelve Months Ended December 31, 2002(1) | |||||

|---|---|---|---|---|---|---|---|

| | (dollars in millions) | ||||||

| Income Statement Data: | |||||||

| Net Sales | $ | 721.7 | $ | 724.7 | |||

| Cost of Sales | 451.5 | 451.7 | |||||

| Gross Profit | 270.2 | 273.0 | |||||

| Selling, General and Administrative Expenses | 170.5 | 174.9 | |||||

| Restructuring and Other Similar Costs | 55.9 | 18.1 | |||||

| Amortization of Intangible Assets | 1.7 | 1.7 | |||||

| Income from Operations | $ | 42.1 | $ | 78.3 | |||

Other Data: | |||||||

| EBITDA(2) | $ | 77.6 | $ | 114.1 | |||

| EBITDA Margin %(3) | 10.8 | % | 15.7 | % | |||

| Depreciation and Amortization | $ | 35.5 | $ | 35.8 | |||

| Capital Expenditures | $ | 21.7 | $ | 17.3 | |||

| Ratio of EBITDA to Pro Forma Cash Interest Expense(4) | 2.43 | x | |||||

| Ratio of Total Debt to EBITDA | 5.20 | x | |||||

As of December 31, 2002 | |||

|---|---|---|---|

| | (dollars in millions) | ||

| Balance Sheet Data: | |||

| Cash | $ | 37.2 | |

| Working Capital(5) | 188.9 | ||

| Total Assets | 1,275.8 | ||

| Total Debt | 592.9 | ||

| Stockholders' Equity | 362.6 | ||

- (1)

- The pro forma financial information was derived by adding historical financial information for the year ended March 31, 2002 to historical financial information for the nine months ended December 31, 2002, and subtracting historical financial information for the nine months ended December 31, 2001, and giving effect to the applicable pro forma adjustments as if the Acquisition had been effected at April 1, 2001. The pro forma adjustments are described under "Unaudited Pro Forma Combined Financial Information."

- (2)

- EBITDA represents income from operations plus depreciation and amortization. We have included information concerning EBITDA because we believe that EBITDA is generally accepted as providing useful information regarding a company's ability to service and/or incur debt. EBITDA

11

should not be considered in isolation or as an alternative to net income, cash flows, other combined income or cash flow data prepared in accordance with accounting principles generally accepted in the United States. EBITDA is calculated as follows:

| | Pro Forma Fiscal Year Ended March 31, 2002 | Pro Forma Twelve Months Ended December 31, 2002 | |||||

|---|---|---|---|---|---|---|---|

| | (in millions) | ||||||

| Income from operations | $ | 42.1 | $ | 78.3 | |||

| Depreciation and Amortization | 35.5 | 35.8 | |||||

| $ | 77.6 | $ | 114.1 | ||||

- (3)

- Represents EBITDA as a percentage of net sales.

- (4)

- Pro forma cash interest expense, which excludes amortization of deferred financing costs, for the fiscal year ended March 31, 2002 and the twelve months ended December 31, 2002 would have been $45.4 million and $46.9 million, respectively. See footnote (c) to the pro forma income statements under "Unaudited Pro Forma Combined Financial Information."

- (5)

- Represents total current assets less total current liabilities.

12

Summary Historical Combined Financial Information

The following summary historical combined financial information is based on our combined financial statements included elsewhere in this prospectus. Our combined financial statements at March 31, 2001 and 2002 and for the years ended March 31, 2000, 2001 and 2002 have been audited by Ernst & Young LLP, our independent auditors. Our condensed consolidated financial statements at December 31, 2002 and for the nine-month period ended December 31, 2001, the period from April 1, 2002 through November 24, 2002 and the period from November 25, 2002 through December 31, 2002 are unaudited but, in the opinion of our management, include all adjustments, consisting only of normal recurring accruals, necessary for a fair presentation.

| | Predecessor Basis of Accounting | | |||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | | | | | Period From April 1, 2002 through November 24, 2002 | Period From November 25, 2002 through December 31, 2002 | |||||||||||||

| | Fiscal Year Ended March 31, | Nine Months Ended December 31, 2001 | |||||||||||||||||

| | 2000 | 2001 | 2002 | ||||||||||||||||

| | (in millions) | ||||||||||||||||||

| Income Statement Data: | |||||||||||||||||||

| Net Sales | $ | 857.5 | $ | 804.6 | $ | 725.1 | $ | 528.9 | $ | 469.6 | $ | 62.0 | |||||||

| Cost of Sales | 517.3 | 462.6 | 454.5 | 334.1 | 294.7 | 39.3 | |||||||||||||

| Gross Profit | 340.2 | 342.0 | 270.6 | 194.8 | 174.9 | 22.7 | |||||||||||||

| Selling, General and Administrative Expenses | 182.7 | 183.7 | 171.7 | 129.7 | 118.8 | 15.4 | |||||||||||||

| Restructuring and Other Similar Costs | 10.6 | 21.8 | 55.9 | 44.8 | 7.0 | — | |||||||||||||

| Amortization of Intangible Assets | 18.9 | 18.5 | 18.8 | 14.1 | 1.1 | 0.2 | |||||||||||||

| Income from Operations | $ | 128.0 | $ | 118.0 | $ | 24.2 | $ | 6.2 | $ | 48.0 | $ | 7.1 | |||||||

| Other Data: | |||||||||||||||||||

| EBITDA(1) | $ | 181.1 | $ | 171.0 | $ | 76.8 | $ | 46.7 | $ | 72.2 | $ | 10.9 | |||||||

| EBITDA Margin %(2) | 21.1 | % | 21.3 | % | 10.6 | % | 8.8 | % | 15.4 | % | 17.6 | % | |||||||

| Cash provided by operating activities | $ | 169.4 | $ | 75.6 | $ | 66.0 | $ | 31.5 | $ | 15.9 | $ | 32.5 | |||||||

| Depreciation and Amortization | 53.1 | 53.0 | 52.6 | 40.5 | 24.2 | 3.8 | |||||||||||||

| Capital Expenditures | 41.7 | (3) | 33.7 | 21.7 | 17.5 | 11.8 | 1.3 | ||||||||||||

As of December 31, 2002 | |||

|---|---|---|---|

| | (in millions) | ||

| Balance Sheet Data: | |||

| Cash | $ | 37.2 | |

| Working Capital(4) | 188.9 | ||

| Total Assets | 1,275.8 | ||

| Total Debt | 592.9 | ||

| Stockholders' Equity | 362.6 | ||

- (1)

- EBITDA represents income from operations plus depreciation and amortization. We have included information concerning EBITDA because we believe that EBITDA is generally accepted as providing useful information regarding a company's ability to service and/or incur debt. EBITDA should not be considered in isolation or as an alternative to net income, cash flows, other

13

combined income or cash flow data prepared in accordance with accounting principles generally accepted in the United States. EBITDA is calculated as follows:

| | Predecessor Basis of Accounting | | ||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | | | | | Period From April 1, 2002 through November 24, 2002 | Period From November 25, 2002 through December 31, 2002 | ||||||||||||

| | Fiscal Year Ended March 31, | Nine Months Ended December 31, 2001 | ||||||||||||||||

| | 2000 | 2001 | 2002 | |||||||||||||||

| | (in millions) | |||||||||||||||||

| Income from Operations | $ | 128.0 | $ | 118.0 | $ | 24.2 | $ | 6.2 | $ | 48.0 | $ | 7.1 | ||||||

| Depreciation and Amortization | 53.1 | 53.0 | 52.6 | 40.5 | 24.2 | 3.8 | ||||||||||||

| EBITDA | $ | 181.1 | $ | 171.0 | $ | 76.8 | $ | 46.7 | $ | 72.2 | $ | 10.9 | ||||||

- (2)

- Represents EBITDA as a percentage of net sales.

- (3)

- Includes $7.9 million of capital expenditures associated with preparations for Year 2000 related systems upgrade.

- (4)

- Represents total current assets less total current liabilities.

14

You should carefully consider the risks described below before making an investment decision. The risks described below are not the only ones facing our company. Additional risks and uncertainties not currently known to us or that we currently deem to be immaterial may also materially and adversely affect our business operations. Any of the following risks could materially adversely affect our business, financial condition or results of operations. In such case, you may lose all or part of your original investment.

Risks Related to the Notes

Our substantial indebtedness could adversely affect our financial condition and prevent us from fulfilling our obligations under the notes.

We have a significant amount of indebtedness. As of December 31, 2002, our total indebtedness was $592.9 million, excluding unused commitments under our new revolving credit facility, which would have represented approximately 62.0% of our total capitalization.

Our substantial indebtedness could have important consequences for you. For example, it could:

- •

- make it more difficult for us to satisfy our obligations with respect to the notes, including our repurchase obligations;

- •

- increase our vulnerability to general adverse economic and industry conditions;

- •

- require us to dedicate a substantial portion of our cash flow from operations to payments on our indebtedness, thereby reducing the availability of our cash flow to fund working capital, capital expenditures, research and development efforts and other general corporate purposes;

- •

- limit our flexibility in planning for, or reacting to, changes in our business and the industry in which we operate;

- •

- place us at a competitive disadvantage compared to our competitors that have less debt; and

- •

- limit our ability to borrow additional funds.

In addition, the indenture and our senior credit facilities contain financial and other restrictive covenants that limit our ability to engage in activities that may be in our long-term best interests. Our failure to comply with those covenants could result in an event of default which, if not cured or waived, could result in the acceleration of all of our debts.

To service our indebtedness, including the notes, we will require a significant amount of cash.

On a pro forma basis, after giving effect to the Acquisition, cash interest expense for fiscal year 2002, the first nine months of fiscal year 2003 and for the twelve months ended December 31, 2002 would have been $45.4 million, $35.1 million and $46.9 million, respectively. On a pro forma basis, after giving effect to the Acquisition, borrowings under the senior credit facilities and the offering of the old notes, our earnings would have been insufficient to cover our fixed charges by $13.5 million for the nine months ended December 31, 2001. Our ability to make payments on our indebtedness depends on our ability to generate cash in the future. If we do not generate sufficient cash flow to meet our debt service and working capital requirements, we may need to seek additional financing or sell assets and we may be unable to obtain financing on terms that are acceptable to us or at all. Without such financing, we could be forced to sell assets to make up for any shortfall in our payment obligations under unfavorable circumstances.

Our senior credit facilities and our obligations under the notes limit our ability to sell assets and also restrict the use of proceeds from any such sale. Furthermore, the senior credit facilities are secured

15

by substantially all of our assets. Therefore, we may not be able to sell our assets quickly enough or for sufficient amounts to enable us to meet our debt service obligations.

Despite current indebtedness levels, we and our subsidiaries may still be able to incur substantially more debt, which would further exacerbate the risks associated with our substantial leverage.

We and our subsidiaries may be able to incur substantial additional indebtedness in the future because the terms of the indenture do not fully prohibit us or our subsidiaries from doing so. Our senior credit facilities permit additional borrowing of up to $75.0 million, and all of those borrowings rank senior to the notes and the subsidiary guarantees. If new debt is added to our and our subsidiaries' current debt levels, the related risks that we and they face would be magnified. In addition, the indenture does not prevent us from incurring obligations that do not constitute indebtedness.

Your right to receive payments on the notes will be subordinated to the borrowings under the senior credit facilities and possibly all future borrowings.

The notes and the guarantees rank behind all of our and the guarantors' existing senior indebtedness, including the senior credit facilities, and will rank behind all of our and their future senior indebtedness. As a result, upon any distribution to our creditors or the creditors of the guarantors in a bankruptcy, liquidation or reorganization or similar proceeding relating to us or the guarantors or our or their property, the holders of senior indebtedness of our company and the guarantors will be entitled to be paid in full in cash before any payment may be made with respect to the notes or the guarantees. In addition, the senior credit facilities are secured by substantially all of our assets and the assets of our wholly-owned domestic subsidiaries.

All payments on the notes will be blocked in the event of a payment default on senior debt and may be blocked for up to 179 consecutive days in the event of certain nonpayment defaults on certain of our senior indebtedness.

In the event of a bankruptcy, liquidation or reorganization or similar proceeding relating to us or the guarantors, holders of the notes will participate with trade creditors and all other holders of our and the guarantors' senior subordinated indebtedness in the assets remaining after we and the guarantors have paid all of the senior indebtedness. However, because the indenture requires that amounts otherwise payable to holders of the notes in a bankruptcy or similar proceeding be paid to holders of senior indebtedness instead, holders of the notes may receive less, ratably, than holders of trade payables in any such proceeding. In any of these cases, we and the guarantors may not have sufficient funds to pay all of our creditors, and holders of the notes may receive less, ratably, than the holders of senior indebtedness.

As of December 31, 2002, borrowings under the senior credit facilities and the offering of the old notes, the notes and the guarantees would have been subordinated to $367.9 million of senior indebtedness and approximately $72.0 million would have been available for borrowing as additional senior indebtedness under the senior credit facilities, subject to certain conditions. We are permitted to borrow substantial additional indebtedness, including senior indebtedness, in the future under the terms of the indenture.

Certain subsidiaries are not included as subsidiary guarantors.

In addition to our parent, the guarantors of the notes include only our wholly-owned domestic subsidiaries. However, the historical combined financial information and the pro forma combined financial information included in this prospectus are presented on a combined basis, including both our domestic and our foreign subsidiaries. The aggregate net sales and income from operations of our subsidiaries that are not guarantors for the nine months ended December 31, 2002, were $169.4 million

16

and $8.6 million, respectively. As of December 31, 2002, those subsidiaries represented 26.1% of our total assets based on book value.

Because a meaningful portion of our operations is conducted by foreign subsidiaries, our cash flow and our ability to service debt, including our and the subsidiary guarantors' ability to pay the interest on and principal of the notes when due, are dependent in part on cash dividends and distributions and other transfers of cash from our foreign subsidiaries. In addition, any payment of interest, dividends, distributions, loans or advances by our foreign subsidiaries to us and the subsidiary guarantors, as applicable, could be subject to taxation or other restrictions on dividends or repatriation of earnings under applicable local law, monetary transfer restrictions and foreign currency exchange regulations in the jurisdiction in which our foreign subsidiaries operate. Moreover, payments to us and the subsidiary guarantors by the foreign subsidiaries will be contingent upon their earnings.

Our foreign subsidiaries are separate and distinct legal entities and have no obligation, contingent or otherwise, to pay any amounts due pursuant to the notes, or to make any funds available therefor, whether by dividends, loans, distributions or other payments. Any right that we or the subsidiary guarantors have to receive any assets of any of the foreign subsidiaries upon the liquidation or reorganization of those subsidiaries, and the consequent rights of holders of notes to realize proceeds from the sale of any of those subsidiaries' assets, will be effectively subordinated to the claims of that subsidiary's creditors, including trade creditors and holders of debt of that subsidiary.

Restrictive covenants in the senior credit facilities and the indenture may restrict our ability to pursue our business strategies.

The indenture and the senior credit facilities limit our ability, among other things, to:

- •

- incur additional indebtedness or contingent obligations;

- •

- pay dividends or make distributions to our stockholders;

- •

- repurchase or redeem our stock;

- •

- make investments;

- •

- grant liens;

- •

- make capital expenditures;

- •

- enter into transactions with our stockholders and affiliates;

- •

- sell assets; and

- •

- acquire the assets of, or merge or consolidate with, other companies.

In addition, the senior credit facilities require us to maintain certain financial ratios. We may not be able to maintain these ratios. If we default under the senior credit facilities, we could be prohibited from making any payments on the notes, and the lenders under the senior credit facilities could require immediate repayment of the entire principal outstanding under these facilities. If the lenders under our senior credit facilities require immediate repayment, we will not be able to repay them and also repay the notes in full. For additional information regarding the limitations our indebtedness imposes on us, please refer to the section entitled "The Credit Facilities—Covenants and Other Matters" and "Description of the Exchange Notes—Certain Covenants."

We may not have the ability to raise the funds necessary to finance any change of control offer required by the indenture governing the notes.

If we undergo a change of control (as defined in the indenture governing the notes) we may need to refinance large amounts of our debt, including the notes and borrowings under the senior credit

17

facilities. If a change of control occurs, we must offer to buy back the notes for a price equal to 101% of the principal amount of the notes, plus any accrued and unpaid interest. We cannot assure you that there will be sufficient funds available for us to make any required repurchases of the notes upon a change of control. In addition, our senior credit facilities prohibit us from repurchasing the notes until we first repay the senior credit facilities in full in cash. If we fail to repurchase the notes in that circumstance, it would result in an event of default under the indenture, which would in turn constitute a default under the senior credit facilities. In such circumstances, the subordination provisions of the indenture would likely restrict payment to holders of the notes. The senior credit facilities contain, and future indebtedness that we incur may also contain, restrictions on repayment upon a change of control or require the repurchase of such indebtedness upon a change of control. If any change of control occurs, we cannot assure you that we will have sufficient funds to satisfy all of our debt obligations. The repurchase requirements also delay or make it harder for others to effect a change of control.

We may engage in transactions that would not be considered a change of control under the indenture, and as a result, the exchange notes could be subject to substantial additional subordination.

The definition of change in control was a result of negotiations between us and the initial purchasers in the offering of the old notes, and we believe it to be reflective of general market practice in comparable note offerings. We could, in the future, enter into certain transactions, including acquisitions, refinancings or other recapitalizations, that would not constitute a change of control under the indenture governing the exchange notes, but that could nonetheless increase the amount of indebtedness outstanding or otherwise affect our capital structure or credit rating. If a transaction falls outside the definition of change of control, and is otherwise permitted under the indenture, we are not required to offer to repurchase the exchange notes, and the exchange notes could be subject to substantial additional subordination. While there are restrictions on our ability to incur additional indebtedness, as described in the covenants set forth under "Description of the Exchange Notes—Certain Covenants—Limitation on Indebtedness" and "The Credit Facilities—Covenants and Other Matters," the indenture does not contain any other covenants or provisions that may afford holders of the exchange notes protection in the event of a highly leveraged transaction.

Federal and state laws permit a court to void the notes or the guarantees under certain circumstances.

Our payment of consideration to finance a portion of the Acquisition (including our issuance of the notes and the guarantee of the notes by our parent and certain of our wholly-owned domestic subsidiaries) may be subject to review under federal or state fraudulent transfer laws. While the relevant laws may vary from state to state, under such laws, the payment of consideration or the issuance of a guarantee will be a fraudulent conveyance if (1) we paid the consideration, or our parent or any of our subsidiaries issued guarantees, with the intent of hindering, delaying or defrauding creditors, or (2) we or any of the guarantors received less than reasonably equivalent value or fair consideration in return for paying the consideration or issuing their respective guarantees, and, in the case of (2) only, one of the following is also true:

- •

- we or any of the guarantors were insolvent, or became insolvent, when we or they paid the consideration;

- •

- paying the consideration or issuing the guarantees left us or the applicable guarantor with an unreasonably small amount of capital; or

- •

- we or the applicable guarantor, as the case may be, intended to, or believed that we or it would, be unable to pay debts as they matured.

If the payment of the consideration or the issuance of any guarantee were a fraudulent conveyance, a court could, among other things, void our obligations regarding the payment of the

18

consideration or void any of the guarantors' obligations under their respective guarantees, as the case may be, and require the repayment of any amounts paid thereunder.

Generally, an entity will be considered insolvent if:

- •

- the sum of its debts is greater than the fair value of its property;

- •

- the present fair value of its assets is less than the amount that it will be required to pay on its existing debts as they become due; or

- •

- it cannot pay its debts as they become due.

We believe, however, that as of the close of the offering of the old notes and the guarantees, we and each of the guarantors are solvent, have sufficient capital to carry on our respective businesses and are able to pay our respective debts as they mature. We cannot be sure, however, as to what standard a court would apply in making such determinations or that a court would reach the same conclusions with regard to these issues.

You cannot be sure an active trading market for the notes will develop.

The exchange notes are new issues of securities for which there is no established public market. We do not intend to have the exchange notes listed on a national securities exchange or included in any automated quotation system, although application will be made to make the exhange notes eligible for trading in the PORTAL Market. Although each initial purchaser informed us that it was its intention to make a market in the old notes and, if issued, the exchange notes, it has no obligation to do so and may discontinue making a market at any time without notice.

The liquidity of any market for the notes will depend upon the number of holders of the notes, our performance, the market for similar securities, the interest of securities dealers in making a market in the notes and other factors. A liquid trading market may not develop for the notes. If a market develops, the notes could trade at prices that may be lower than the initial offering price of the notes. See "Plan of Distribution."

The market price for the notes may be volatile.

Historically, the market for non-investment grade debt has been subject to disruptions that have caused substantial volatility in the prices of securities similar to the notes. The market for the notes, if any, may be subject to similar disruptions. Any such disruptions may adversely affect the value of your notes.

If you do not properly tender your old notes, your ability to transfer your old notes will be adversely affected.

We will only issue exchange notes in exchange for old notes that are timely received by the exchange agent, together with all required documents, including a properly completed and signed letter of transmittal. Therefore, you should allow sufficient time to ensure timely delivery of the old notes and you should carefully follow the instructions on how to tender your old notes. Neither we nor the exchange agent are required to tell you of any defects or irregularities with respect to your tender of the old notes. If you do not tender your old notes or if we do not accept your old notes because you did not tender your old notes properly, then, after we consummate the exchange offer, you may continue to hold old notes that are subject to the existing transfer restrictions. In addition, if you tender your old notes for the purpose of participating in a distribution of the exchange notes, you will be required to comply with the registration and prospectus delivery requirements of the Securities Act in connection with any resale of the exchange notes. If you are a broker-dealer that receives exchange notes for your own account in exchange for old notes that you acquired as a result of market-making

19

activities or any other trading activities, you will be required to acknowledge that you will deliver a prospectus in connection with any resale of such exchange notes. After the exchange offer is consummated, if you continue to hold any old notes, you may have difficulty selling them because there will be fewer old notes outstanding. In addition, if a large amount of old notes are not tendered or are tendered improperly, the limited amount of exchange notes that would be issued and outstanding after we consummate the exchange offer could lower the market price of such exchange notes.

Risks Related to Our Business

Our business depends upon general economic conditions, and we serve customers in cyclical industries.

Our financial performance depends, in large part, on conditions in the markets that we serve, and on the U.S. and global economy generally. Some of the industries that we serve are highly cyclical, such as the aerospace, energy and industrial equipment industries. We have experienced a downturn and a reduction in sales and margins as a result of recent recessionary conditions. While we have undertaken a consolidation and cost reduction program to mitigate the effect of these conditions, we may be unsuccessful in doing so and such actions may be insufficient. The present uncertain economic environment may result in significant quarter-to-quarter variability in our performance. Any sustained weakness in demand or continued downturn or uncertainty in the economy generally would further reduce our sales and profitability.

We face competition in our markets.

We operate in highly fragmented and very competitive markets within the mechanical power transmission industry. As a result, we compete against numerous different businesses. Some of our competitors have achieved substantially more market penetration in certain of the markets in which we operate, such as gearing. Competition in our business lines is based on a number of considerations including product performance, cost of transportation in the distribution of our products, brand reputation, quality of client service and support and price. Additionally, some of our larger more sophisticated customers are attempting to reduce the number of vendors from which they purchase in order to increase their efficiency. If we are not selected to become one of these preferred providers, we may lose access to certain sections of the markets in which we compete. Our customers increasingly demand a broad product range and we must continue to develop our expertise in order to manufacture and market these products successfully. To remain competitive, we will need to invest continuously in manufacturing, customer service and support, marketing and our distribution networks. We may have to adjust the prices of some of our products to stay competitive. We cannot assure you that we will have sufficient resources to continue to make such investments or that we will maintain our competitive position within each of the markets we serve. Some of our competitors have greater financial and other resources than we do.

We rely on independent distributors.

In addition to our own direct sales force, we depend on the services of independent distributors to sell our products and provide service and aftermarket support to our customers. We support an extensive distribution network, with over 1,900 distributor locations nationwide. Rather than serving as passive conduits for delivery of product, our industrial distributors are active participants in the overall competitive dynamic in the mechanical power transmission industry. Industrial distributors play a significant role in determining which of our products are stocked at the branch locations, and hence are most readily accessible to aftermarket buyers, and the price at which these products are sold. In fiscal year 2002, approximately 20% of our net sales were generated through sales to three of our key independent distributors: Applied Industrial Technologies, Kaman and Motion Industries. Almost all of the distributors with whom we transact business offer competitive products and services to our

20

customers. In addition, the distribution agreements we have are typically cancelable by the distributor after a short notice period. The loss of a substantial number of these distributors or an increase in the distributors' sales of our competitors' products to our customers could materially reduce our sales and profits.

We are a newly formed company with no recent operating history as a stand-alone company, which may lead to risks or unanticipated expenses similar to those of a start-up company.

Prior to the Acquisition, Invensys provided us with a number of support services, including corporate services such as certain accounting functions, internal audit, treasury, taxation, legal and intellectual property, insurance administration, certain human resource functions and certain information technology functions. While we believe we will be able to complete the arrangement of replacement services appropriate for operation as a stand-alone company, there is a risk that continuity in the performance of these functions will be affected as a result of our transition.

If we are unable to meet future capital requirements, our business may be adversely affected.

We periodically make capital investments to, among other things, maintain and upgrade our facilities and enhance our production processes. As we grow our businesses, we may have to incur significant capital expenditures. We believe that we will be able to fund these expenditures through cash flow from operations and borrowings under our senior credit facilities. However, our senior credit facilities contain limitations that could affect our ability to fund our future capital expenditures and other capital requirements. We cannot assure you that we will have, or be able to obtain, adequate funds to make all necessary capital expenditures when required, or that the amount of future capital expenditures will not be materially in excess of our anticipated or current expenditures. If we are unable to make necessary capital expenditures, our product line may become dated, our productivity may be decreased and the quality of our products may be adversely affected, which, in turn, could reduce our sales and profitability. See "Management's Discussion and Analysis of Financial Condition and Results of Operations."

We are subject to risks associated with changing technology and manufacturing techniques, which could place us at a competitive disadvantage.

The successful implementation of our business strategy requires us to continuously evolve our existing products and introduce new products to meet customers' needs in the industries we serve and want to serve. Our products are characterized by stringent performance and specification requirements that mandate a high degree of manufacturing and engineering expertise. If we fail to meet these requirements, our business could be at risk. We believe that our customers rigorously evaluate their suppliers on the basis of a number of factors, including:

- •

- product quality;

- •

- price competitiveness;

- •

- technical expertise and development capability;

- •

- new product innovation;

- •

- reliability and timeliness of delivery;

- •

- product design capability;

- •

- manufacturing expertise;

- •

- operational flexibility;

- •

- customer service; and

21

- •

- overall management.

Our success will depend on our ability to continue to meet our customers' changing specifications with respect to these criteria. We cannot assure you that we will be able to address technological advances or introduce new products that may be necessary to remain competitive within our businesses. Furthermore, we cannot assure you that we can adequately protect any of our own technological developments to produce a sustainable competitive advantage.

Our international operations are subject to uncertainties which could affect our operating results.

Our business is subject to certain risks associated with doing business internationally. Our net sales outside the United States represented 30% of our total sales for fiscal year 2002. Accordingly, our future results could be harmed by a variety of factors, including:

- •

- fluctuations in currency exchange rates;

- •

- exchange controls;

- •

- compliance with U.S. Department of Commerce export controls;

- •

- tariffs or other trade protection measures and import or export licensing requirements;

- •

- potentially negative consequences from changes in tax laws;

- •

- interest rates;

- •

- unexpected changes in regulatory requirements;

- •

- differing labor regulations;

- •

- requirements relating to withholding taxes on remittances and other payments by subsidiaries;

- •

- restrictions on our ability to own or operate subsidiaries, make investments or acquire new businesses in these jurisdictions;

- •

- restrictions on our ability to repatriate dividends from our subsidiaries; and

- •

- exposure to liabilities under the Foreign Corrupt Practices Act.

As we continue to expand our business globally, our success will depend, in large part, on our ability to anticipate and effectively manage these and other risks associated with our international operations. However, any of these factors could adversely affect our international operations and, consequently, our operating results.

Environmental regulation may impose significant environmental compliance costs and liabilities on us.

Our businesses are subject to many environmental laws and regulations. Compliance with these laws and regulations is a significant factor, and cost, in these businesses. We have incurred and expect to continue to incur significant costs to maintain or achieve compliance with applicable environmental laws and regulations. Moreover, if these environmental laws and regulations become more stringent or more stringently enforced in the future, we could incur costs beyond those currently anticipated. Our failure to comply with applicable environmental laws and regulations and permit requirements could result in civil or criminal fines, penalties or enforcement actions, third-party claims for property damage and personal injury, requirements to clean up property or to pay for the costs of cleanup, or regulatory or judicial orders enjoining or curtailing operations or requiring corrective measures, including the installation of pollution control equipment or remedial actions.

Some environmental laws and regulations impose liability for contamination on present and former owners, operators or users of facilities and sites without regard to causation or knowledge of

22

contamination. In addition, we occasionally evaluate various alternatives with respect to our facilities, including possible dispositions or closures. Investigations undertaken in connection with these activities may lead to discoveries of contamination that must be remediated, and closures of facilities may trigger remediation requirements that are not applicable to operating facilities. We currently are remediating contamination at several facilities. In addition, we have been named a potentially responsible party for contamination at contaminated sites, including for groundwater contamination under, and in the vicinity of, our Downers Grove, Illinois facility. We also face lawsuits brought by third parties which either allege property damage or personal injury as a result of, or seek reimbursement for costs associated with, such contamination.

Pursuant to the terms of the stock purchase agreement entered into in connection with the Acquisition, our former parent company, Invensys plc, has agreed to indemnify us against certain pre-existing environmental liabilities, including liabilities associated with our Downers Grove, Illinois facility. We cannot assure you, however, that Invensys will be able to satisfy its indemnification obligations. In addition, we cannot assure you that discovery of additional contamination, or the imposition of more stringent cleanup requirements, will not require significant expenditures by us. See "The Acquisition."

Our intellectual property may be misappropriated or subject to claims of infringement.