As filed with the Securities and Exchange Commission on March 3, 2003

Registration No. 333-102826

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

AMENDMENT NO. 1

TO

FORM F-1

REGISTRATION STATEMENT UNDER

THE SECURITIES ACT OF 1933

TELKOM SA LIMITED

(Exact name of registrant as specified in its charter)

The Republic of South Africa

4813

Not Applicable

(State or other jurisdiction

(Primary Standard Industrial

(I.R.S. Employer

of Incorporation or Organization)

Classification Code Number)

Identification Number)

Telkom Towers North

152 Proes Street

Pretoria 0002

The Republic of South Africa

(27) (12) 321 5808

(Address, including zip code, and telephone number of registrant's principal executive offices)

CT Corporation System

1633 Broadway

New York, New York 10019

(1) (212) 664-1666

(Name, address, including zip code, and telephone number, of agent for service)

Copies to:

Daniel G. Bergstein, Esq.

Adrian J.S. Deitz, Esq.

Tom Joyce, Esq.

Marie Censoplano, Esq.

Scott V. Simpson, Esq.

Sarah C. Murphy, Esq.

Paul, Hastings, Janofsky & Walker LLP

Skadden, Arps, Slate, Meagher & Flom LLP

Freshfields Bruckhaus Deringer

75 East 55th Street

One Canada Square

65 Fleet Street

New York, New York 10022

Canary Wharf

London EC4Y 1HS

(1) (212) 318-6000

London E14 5DS

England

England

(44) (207) 936-4000

(44) (207) 519-7000

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this

Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under

the Securities Act of 1933, please check the following box:

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act of 1933, check

the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same

offering:

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act of 1933, please check the

following box and list the Securities Act registration statement number of the earlier effective registration statement for the same

offering:

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act of 1933, check the following

box and list the Securities Act registration statement number of the earliest effective registration statement for the same

offering:

If delivery of the prospectus is expected to be made pursuant to Rule 434 under the Securities Act of 1933, check the following

box:

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date

until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter

become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become

effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

SUBJECT TO COMPLETION, DATED MARCH 3, 2003

Telkom SA Limited

incorporated in the Republic of South Africa

Registration number 1991/005476/06

139,257,954 Ordinary Shares

offered in the form of Ordinary Shares or American Depositary Shares, or ADSs, each representing 4 Ordinary Shares

This is an initial public offering of ordinary shares, having a par value of R10 each in the capital of Telkom SA Limited, by

the Government of the Republic of South Africa. This global offering is expected to be 139,257,954 ordinary shares. The

global offering is being made in the United States and the Republic of South Africa and to institutional investors outside of

those jurisdictions. 48,740,284 of the ordinary shares offered in the global offering are being registered under the US

Securities Act of 1933 for initial offer and sale in the United States and for any resales into the United States. Initial offers

and sales outside the United States are not being registered under the US Securities Act of 1933.

We currently estimate that the initial public offering price will be:

• between R27.00 and R30.00 per ordinary share; and

• between $13.30 and $14.80 per ADS, based on an exchange rate of R8.10 per $1.00, rounded down to the nearest

10 US Cents.

All of the ordinary shares to be sold in the global offering are being offered by the Government of the Republic of South

Africa. We will not receive any of the proceeds from the sale of the ordinary shares in the global offering.

Prior to this global offering, there has been no public market for the ordinary shares or ADSs. The JSE Securities

Exchange, South Africa has agreed to list all the ordinary shares in the "Telecommunications Services" sector of the list of

the JSE Securities Exchange, South Africa under the symbol "TKG" and ISIN Code "ZAE000044897," subject to the

attainment of a spread of shareholders acceptable to the JSE Securities Exchange, South Africa and the submission of all

supporting documents required by the JSE Securities Exchange, South Africa. The ADSs have been approved for listing on

the New York Stock Exchange under the symbol "TKG," subject to official notice of issuance. Please see page 174 of this

prospectus for a description of the views of the JSE Securities Exchange, South Africa on the creation of the class A

ordinary share and class B ordinary share in the share capital of Telkom on the JSE Securities Exchange, South

Africa listing date and the rights afforded to the holders thereof.

Investing in Telkom's ordinary shares and ADSs involves risks. See "Risk Factors" beginning on page 17 of this

prospectus.

Underwriting

Proceeds to the

Discounts and

Government of the

Price to Public Commissions

(1)

Republic of South Africa

Per ordinary share . . . . . . . . . . . . . .

R

R

R

Per ADS . . . . . . . . . . . . . . . . . . .

$

$

$

Total

(2)

. . . . . . . . . . . . . . . . . . . .

$

$

$

(1)

Underwriting discounts and commissions do not include fees of up to R that may be payable at the discretion of the Government of

the Republic of South Africa.

(2)

Assumes that all ordinary shares are sold in the form of ADSs.

The Government of the Republic of South Africa has granted the joint global coordinators, on behalf of the underwriters, a

30-day option to purchase up to a maximum of 20,888,693 additional ordinary shares on the same terms and conditions set

forth above solely to cover over-allotments, if any.

Neither the US Securities and Exchange Commission, the South African Registrar of Companies, the JSE nor any

other regulatory body has approved or disapproved of these securities or passed on the adequacy or accuracy of this

prospectus as truthful or complete. Any representation to the contrary is a criminal offense.

This prospectus does not constitute an offer for sale of ordinary shares or ADSs in the Republic of South Africa and

may not be distributed in South Africa.

It is expected that the ordinary shares and ADSs will be delivered on or about March 7, 2003.

Deutsche Bank Securities

JPMorgan

Prospectus dated

, 2003

The information in this prospectus is not complete and may be changed. We and the Government of the Republic of South Africa may not

We and the Go

vernment of the Republic of South

Africa ma

y not sell these securities until the

sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an

ve.

This prospectus is not an of

fer to sell t

hese securities and it is not soliciting an

offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

uy these securities in an

y jurisdiction where the of

fer or sale is not permitted.

(before expenses)

You should rely only on the information contained in this prospectus. We and the Government of the Republic of

South Africa have not authorized anyone to provide you with different information. We and the Government of the

Republic of South Africa are not offering to sell or soliciting offers to buy the ordinary shares or ADSs in places where

such offers and sales are not permitted by applicable law. You should not assume that the information in this prospectus is

accurate as of any date other than the date on the front of this prospectus.

TABLE OF CONTENTS

Page

Prospectus Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

1

Risk Factors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

17

Special Note Regarding Forward-Looking Statements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

27

Use of Proceeds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

28

Dividends and Dividend Policy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

29

Exchange Rates . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

31

Capitalization . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

32

Selected Historical Consolidated Financial and Other Data of the Telkom Group . . . . . . . . . . . . . . . . . . .

33

Management's Discussion and Analysis of Financial Condition and Results of Operations . . . . . . . . . . . . . .

39

The South African Telecommunications Industry . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

95

Business . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

98

Legal Proceedings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

130

Regulation and License Requirements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

131

Management . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

141

Relationship with Major Shareholders and Related Transactions . . . . . . . . . . . . . . . . . . . . . . . . . . . .

156

Relationship with Vodacom and Related Transactions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

164

Description of Shares . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

166

Description of American Depositary Receipts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

180

Nature of the South African Trading Market . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

185

Taxation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

186

Exchange Controls . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

192

The Global Offering . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

195

Underwriting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

201

Legal Matters . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

204

Experts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

205

Expenses Relating to the Global Offering . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

206

Enforcement of Civil Liabilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

207

Where You Can Find More Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

208

Documents Available for Inspection . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

209

Additional Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

210

Index to Financial Statements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F-1

Republic of South Africa . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

A-1

Extracts from Telkom's new memorandum and articles of association . . . . . . . . . . . . . . . . . . . . . . . . .

B-1

-ii-

1

PROSPECTUS SUMMARY

Overview

Telkom is one of the largest companies registered in the Republic of South Africa and we are the largest communications

services provider on the African continent based on operating revenue and assets. We had consolidated operating revenue of

R34.2 billion ($3.2 billion), net profit of R1.2 billion ($116 million) and cash flow from operating activities of R8.2 billion

($775 million) in the year ended March 31, 2002 and we had total assets of R55.2 billion ($5.2 billion) and shareholders'

equity of R16.8 billion ($1.6 billion) as of March 31, 2002. We had consolidated operating revenue of R18.3 billion

($1.7 billion), net profit of R0.6 billion ($61 million) and cash flow from operating activities of R3.5 billion ($328 million)

in the six months ended September 30, 2002 and we had total assets of R54.6 billion ($5.2 billion) and shareholders' equity

of R17.5 billion ($1.7 billion) as of September 30, 2002.

We offer business, residential and payphone customers a wide range of services and products, including:

•fixed-line voice services, including subscriptions and connections services, local, long distance, fixed-to-mobile and

international voice services, interconnection and transit communications services, value-added voice services,

customer premises equipment sales and directory services;

•fixed-line data services, including domestic and international data transmission services, such as leased lines and

packet-based services, managed data networking services and internet access and related information technology

services; and

•mobile communications services, including voice and data services, value-added services and handset sales through

our joint venture, Vodacom, a company incorporated in the Republic of South Africa.

We had the exclusive right to provide public switched telecommunications services, including international voice

services, in South Africa until May 7, 2002. We are currently the only national provider of these services in South Africa,

although a process has been commenced to liberalize the South African communications market, which will introduce

competition in a number of our business areas. In 1997, we embarked on an extensive five year capital investment program

in our fixed-line business. Our fixed-line capital investment for the five years ended March 31, 2002 was R41.7 billion

($4.0 billion), of which R27.9 billion ($2.6 billion) was for network modernization and line roll-out in order to comply with

our license obligations and prepare for competition. As of September 30, 2002, we had 4.9 million telephone access lines in

service and 99.8% of our telephone access lines were connected to digital exchanges.

Vodacom is our mobile communications joint venture with Vodafone Group Plc, a company incorporated in England and

Wales, and VenFin Limited, a company incorporated in the Republic of South Africa. Vodacom is the largest mobile

communications network operator in South Africa with a market share of approximately 59% as of September 30, 2002

based on total reported customers. Vodacom had 7.7 million customers as of September 30, 2002, of which 7.1 million were

in South Africa. Vodacom has investments in mobile communications network operators in Lesotho, Tanzania and the

Democratic Republic of the Congo. Vodacom had consolidated revenue of R16.2 billion ($1.5 billion), net profit of

R2.4 billion ($225 million) and cash flow from operating activities of R3.8 billion ($362 million) in the year ended March 31,

2002 and total assets of R15.4 billion ($1.5 billion) and shareholders' equity of R5.5 billion ($518 million) as of March 31,

2002. Vodacom had consolidated revenue of R9.4 billion ($895 million), net profit of R0.9 billion ($87 million) and cash

flow from operating activities of R1.6 billion ($155 million) in the six months ended September 30, 2002 and total assets of

R17.3 billion ($1.6 billion) and shareholders' equity of R6.3 billion ($601 million) as of September 30, 2002.

We believe that we have a number of competitive strengths that will enable us to increase our profitability and cash flow

and successfully meet competition. Our competitive strengths include our leading market position in the South African fixed-

line communications market, our state-of-the-art, fully digital fixed-line network and the financial, operational and

managerial expertise of our strategic equity investor, Thintana Communications LLC, a Delaware limited liability company,

which is 60% beneficially owned by SBC Communications, Inc., a Delaware corporation, and 40% beneficially owned by

Telekom Malaysia S.D.N. Berhard, a company incorporated in Malaysia. In addition, Vodacom is the leading South African

mobile communications network operator with strong brand recognition, extensive network coverage and distribution

channels, experienced local and international shareholders and management and Vodacom is expanding its operations in

other select sub-Saharan Africa countries.

2

In order to achieve our goals, we intend to pursue the following strategies:

•compete effectively in our core fixed-line markets and grow selected markets;

•continue to reduce operating expenses and enhance capital investment efficiencies in our fixed-line business;

•expand our integrated service offerings through the increased sale of existing data products and the development of

new data and fixed-mobile products;

•continue to invest in our fixed-line employees to foster a highly competitive corporate culture and to enhance skills

retention; and

•capitalize on the growing mobile communications market through Vodacom.

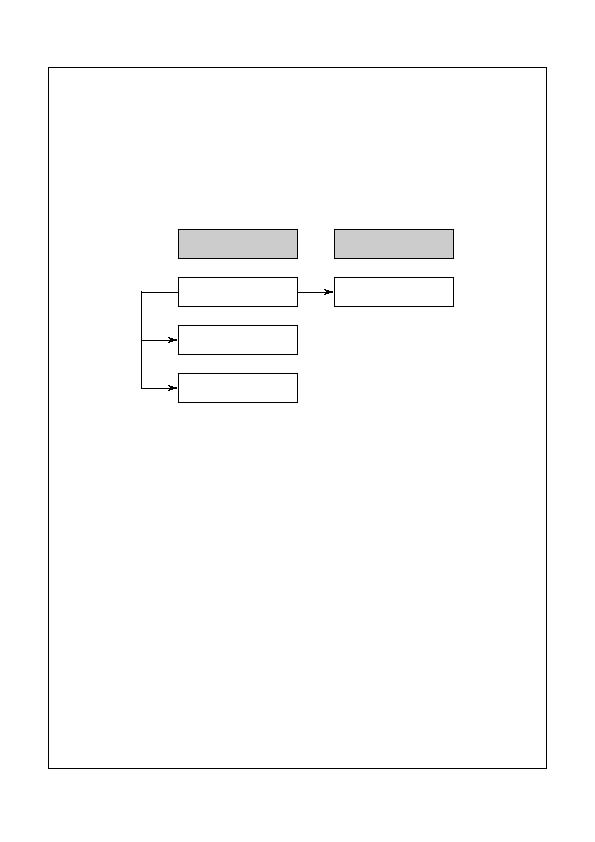

Group operational structure

Our business segments and group operational structure are as follows:

History

Telkom was incorporated on September 30, 1991 as a public limited liability company registered under the South African

Companies Act, 61 of 1973, as amended. On that same date, the Government of the Republic of South Africa transferred the

entire telecommunications enterprise of the then Department of Posts and Telecommunications of the Republic of South

Africa to Telkom. Telkom remained a wholly state-owned enterprise until May 14, 1997, when the Government sold a 30%

equity interest in Telkom to Thintana Communications as part of its policy to liberalize the telecommunications market in

South Africa. On March 30, 2001, the Government sold another 3% equity interest in Telkom from its holdings to Ucingo

Investments (Proprietary) Limited, a company incorporated in the Republic of South Africa comprising a consortium of

black empowerment investors, leaving the Government with 67% of Telkom's issued and outstanding ordinary share capital.

As part of the sale to Thintana Communications, the then Minister of Posts, Telecommunications and Broadcasting of the

Republic of South Africa entered into an agreement with Thintana Communications under which Thintana Communications

undertook significant operational and managerial responsibilities and acquired the ability to exercise effective operational

and managerial control over us until May 2002. Since May 2002, our strategic equity investors no longer exercise effective

operational and managerial control over us, but they continue to provide us with strategic direction as their nominees

continue to occupy key managerial positions and participate in Telkom's operating committee.

Upon completion of the global offering, the Government of the Republic of South Africa will own approximately 42% of

Telkom's issued and outstanding ordinary share capital, or approximately 38% if the underwriters exercise their over-

allotment option in full, and Thintana Communications will own approximately 30% of Telkom's issued and outstanding

ordinary share capital.

Telkom's registration number is 1991/005476/06. Telkom's principal executive offices are located at Telkom Towers

North, 152 Proes Street, Pretoria 0002, Gauteng Province, South Africa. Telkom's telephone number is (27) (12) 321 5808

and its internet address is www.telkom.co.za. Information contained on Telkom's website is not a part of this prospectus.

Unless the context requires otherwise, references to "we," "us," "our" and the "Telkom Group" in this prospectus refer to

Telkom SA Limited and its subsidiaries and its 50% interest in Vodacom, and references to "Telkom" in this prospectus refer

only to Telkom SA Limited. References to "Vodacom" in this prospectus refer to Telkom's 50% owned joint venture,

Vodacom Group (Proprietary) Limited, and its subsidiaries. We do not control Vodacom, the management of which requires

consensus agreement among its shareholders who are party to Vodacom's joint venture agreement.

Fixed-line

Mobile

Telkom SA Limited

Telkom Directory Services

(Proprietary) Limited

Swiftnet (Proprietary)

Limited

Vodacom Group

(Proprietary) Limited

64.9%

100.0%

50.0%

3

THE GLOBAL OFFERING

The Global Offering

A global offering of 139,257,954 ordinary shares by the Government of the Republic

of South Africa in the US and International offerings and the South African retail

offering. 48,740,284 of the ordinary shares offered in the global offering are being

registered under the US Securities Act of 1933 for initial offer and sale in the United

States and for any resales into the United States. Offers and sales of ordinary shares

and ADSs outside the United States, including all ordinary shares and ADSs offered to

South African retail and institutional investors, are being offered pursuant to Regulation

S under the US Securities Act of 1933 and are not covered by the registration statement

filed with the US Securities and Exchange Commission.

US and International Offerings

Made to retail and institutional investors in the United States and to institutional

investors outside of the United States, including institutional investors in the Republic

of South Africa, in the form of ordinary shares or ADSs.

South African Retail Offering

• Made to individuals in possession of a valid South African identity number and who

provide a South African postal address and groups of such individuals, known as

stokvels, at a 20% discount to the initial public offering price, rounded down to the

nearest SA Cent, for up to R5,000 of ordinary shares per individual and up to

R5,000 of ordinary shares per member of a stokvel, subject to a maximum of

R50,000 of ordinary shares per stokvel, in the form of ordinary shares. This offering

is referred to as the Khulisa offer. Ordinary shares purchased in this offering may

not be sold for three months following the date of the listing of the shares on the

JSE. The Government of the Republic of South Africa will also award investors

under this offer one ordinary share for every five ordinary shares purchased and held

in trust until the second anniversary of the JSE listing date.

• Made to individuals in possession of a valid South African identity number and who

provide a South African postal address at a 5% discount to the initial public offering

price, rounded down to the nearest SA Cent, in the form of ordinary shares.

See "The Global Offering" beginning on page 195 of this prospectus.

Offering Price

Between R27.00 and R30.00 per ordinary share. This is equivalent to between $13.30

and $14.80 per ADS at a ratio of 4 ordinary shares per ADS and an exchange rate of

R8.10 per $1.00, rounded down to the nearest 10 US Cents. The initial public offering

price may be outside one or both of the price range indications referred to above.

Ordinary shares sold in the South African retail offering will be at the discounts set out

above. The initial public offering price will be inclusive of uncertificated securities tax.

Over-Allotment Option

The Government of the Republic of South Africa has granted the joint global

co-ordinators, on behalf of the underwriters, a 30-day option to purchase up to a

maximum of 20,888,693 additional ordinary shares on the same terms and conditions

set forth above solely to cover over-allotments, if any.

Ownership of Controlling

Following the completion of this global offering, Telkom's controlling shareholders

Global Offering

will own the following shares:

• The Government will own the one issued and outstanding class A ordinary share and

approximately 42% of Telkom's issued and outstanding ordinary share capital, or

approximately 38% if the underwriters exercise their over-allotment option in full.

• Thintana Communications will own the one issued and outstanding class B ordinary

share and approximately 30% of Telkom's issued and outstanding ordinary share

capital.

See "Description of Shares" beginning on page 166 of this prospectus for a description

of the rights attaching to the class A ordinary share and the class B ordinary share.

In connection with the global offering, the Government of the Republic of South Africa

intends to grant to eligible current and former employees of Telkom options to

purchase up to 11,140,636 of its ordinary shares, representing 2% of Telkom's issued

and outstanding ordinary share capital, through the Diabo Share Trust established for

that purpose at R33.81 per share, which is the price at which Thintana

Communications invested in Telkom in 1997. See "Management Other employee

share ownership arrangements" beginning on page 152 of this prospectus.

4

Information in this prospectus related to the size of the global offering and the

ownership of ordinary shares by the Government of the Republic of South Africa does

not include any sale of ordinary shares through the Diabo Share Trust for the benefit of

former and current employees described above.

Voting Rights

The ordinary shares will generally vote together as a single class with the class A

ordinary share held by the Government of the Republic of South Africa and the class B

ordinary share held by Thintana Communications, except as required by law and as

provided for by Telkom's new memorandum and articles of association. However,

certain actions cannot be taken by Telkom or by its subsidiaries without the

authorization of representatives appointed by the Government of the Republic of South

Africa and Thintana Communications, as significant shareholders, respectively. See

"Management Reserved matters" beginning on page 147 of this prospectus and

"Relationship with Major Shareholders and Related Transactions Shareholder

arrangements New shareholders' agreement" beginning on page 157 of this

prospectus.

American Depositary Shares

Investors outside of South Africa may purchase ordinary shares in the form of ADSs.

Each ADS represents 4 ordinary shares and is evidenced by an American Depositary

Receipt, or ADR.

The ADS depositary is The Bank of New York.

Use of Proceeds

We will not receive any proceeds from the sale of ordinary shares or ADSs in the

global offering.

Listings

The JSE has agreed to list the ordinary shares in the "Telecommunications Services"

sector of the JSE list under the symbol "TKG," subject to the attainment of a spread of

shareholders acceptable to the JSE and the submission of all supporting documents

required by the JSE. The ADSs have been approved for listing on the New York Stock

Exchange under the symbol "TKG," subject to official notice of issuance.

Lock-Up Agreements

Telkom, Thintana Communications and the Government of the Republic of South

Africa have agreed with the underwriters that none of them will sell additional Telkom

ordinary shares for 180 days following the date of the underwriting agreement, subject

to certain exceptions. In addition, the Government has agreed with Thintana

Communications that the Government will not sell its Telkom ordinary shares for a

further 545-day period after the expiration of the lock-up period described above.

Ucingo Investments has agreed with the Government and the underwriters that it will

not sell or dispose of ordinary shares in Telkom for 180 days following the date of the

listing of Telkom's ordinary shares on the JSE Stock Exchange without approval from

the Government and the underwriters, such approval not to be unreasonably withheld.

For a further description of the lock-ups and their exceptions, see "Underwriting"

beginning on page 201 of this prospectus.

Expected Timetable

We expect the timetable for the global offering to be as follows:

January 30, 2003: South African retail offering opens and US and international

offerings commence.

March 4, 2003: Announcement of the initial public offering price and commencement

of conditional trading of the ordinary shares on the JSE and trading of the ADSs on the

New York Stock Exchange.

March 7, 2003: Payment and delivery of ordinary shares and ADSs in the US and

International Offerings.

March 11, 2003: Dispatch of shareholder statements in the South African retail

offering.

Payment and Settlement

Delivery of the ordinary shares and ADSs in the US and International Offerings is

expected to take place against payment therefor in immediately available funds on or

about March 7, 2003. As described in "The Global Offering" beginning on page 195 of

March 7, 2003: Payment and delivery of ordinary shares and ADSs in the US and

International Offerings.

March 11, 2003: Dispatch of shareholder statements in the South African retail

offering.

Payment and Settlement

Delivery of the ordinary shares and ADSs in the US and International Offerings is

expected to take place against payment therefor in immediately available funds on or

about March 7, 2003. As described in "The Global Offering" beginning on page 195 of

this prospectus, investors in the South African retail offering will have to make

payment prior to this date. The ordinary shares will be delivered in dematerialized or

electronic entry form through the facilities of Share Transactions Totally Electronic

Limited, or STRATE. The ADSs will be delivered in book entry form through the

facilities of The Depository Trust Company.

The identification numbers for the ordinary shares and the ADSs are:

Ordinary shares

ISIN: ZAE000044897

ADSs

CUSIP: 879603108

ISIN and CUSIP are codes which uniquely identify a particular securities issue.

Risk Factors

For a discussion of certain factors that should be considered in evaluating an

investment in Telkom's ordinary shares or ADSs, see "Risk Factors" beginning on

page 17 of this prospectus.

5

6

SUMMARY HISTORICAL CONSOLIDATED FINANCIAL

AND OTHER DATA OF THE TELKOM GROUP

The following table sets forth summary consolidated financial and other data of the Telkom Group as of and for each of

the three years in the period ended March 31, 2002 and as of and for each of the six month periods ended September 30,

2002 and 2001. Information in the following table includes our 50% interest in the results, assets, liabilities and

shareholders' equity of Vodacom, which we proportionately consolidate.

The following summary historical consolidated financial data of the Telkom Group as of and for each of the three years

ended March 31, 2002 was derived from the Telkom Group's historical consolidated financial statements beginning on

page F-48 of this prospectus, which have been audited by Ernst & Young, Registered Accountants and Auditors, Chartered

Accountants (SA). The following summary historical consolidated financial data of the Telkom Group as of September 30,

2002 and for each of the six month periods ended September 30, 2002 and 2001 was derived from the Telkom Group's

unaudited condensed consolidated financial statements beginning on page F-2 of this prospectus, which, in the opinion of

our management, have been prepared on the same basis as the Telkom Group's audited consolidated financial statements

and reflect all adjustments, consisting of normal recurring adjustments, necessary for a fair presentation of the Telkom

Group's results of operations and financial position for such periods. Results for the six month periods ended September 30,

2002 and 2001 are not necessarily indicative of results that may be expected for the entire year.

The consolidated financial statements of the Telkom Group have been prepared in accordance with International

Accounting Standards, or IAS, which differs in certain respects from US Generally Accepted Accounting Principles, or

US GAAP. For a description of the principal differences between IAS and US GAAP relevant to the consolidated financial

statements of the Telkom Group and a reconciliation to US GAAP of net income and profit and shareholders' equity, see

note 41 of the notes to the audited consolidated financial statements of the Telkom Group as of and for the three years

ended March 31, 2002 beginning on page F-97 of this prospectus and note 21 of the notes to the unaudited condensed

consolidated financial statements of the Telkom Group as of September 30, 2002 and for each of the six month periods

ended September 30, 2002 and 2001 beginning on page F-15 of this prospectus.

Headline earnings per share is a disclosure requirement of the JSE and is not a recognized measure under US GAAP.

Headline earnings represents net profit, excluding profit on the disposal of property, plant and equipment; profit on the

disposal of subsidiaries and joint ventures; property, plant and equipment impairment losses; goodwill amortization; and tax

and minority interest impacts. EBITDA represents operating profit before income tax, finance charges, investment income

and depreciation and amortization. We believe that EBITDA provides meaningful additional information to investors since

it is widely accepted by analysts and investors as a basis for comparing a company's underlying operating profitability with

that of other companies as it is not influenced by past capital expenditures or business acquisitions, a company's capital

structure or the relevant tax regime. This is particularly the case in a capital-intensive industry such as communications. It

is also a widely accepted indicator of a company's ability to service its long-term debt and other fixed obligations and to

fund its continued growth. EBITDA is not a US GAAP or IAS measure. You should not construe EBITDA as an alternative

to operating profit or cash flows from operating activities determined in accordance with US GAAP or IAS or as a measure

of liquidity. EBITDA is not defined in the same manner by all companies and may not be comparable to other similarly

titled measures of other companies unless the definition is the same. In addition, because the calculation of EBITDA in the

maintenance covenants contained in our credit facilities is based on accounting policies in use at the time the indebtedness

was incurred, EBITDA for purposes of those covenants is not calculated in the same manner as it is calculated in the

following table.

Fixed access lines are comprised of public switched telecommunications network lines, or PSTN lines, including

integrated services digital network, or ISDN, channels, public and private payphones and internal lines in service. We

calculate fixed-line penetration, or teledensity, based on the total number of telephone lines in service at the end of the

period per 100 persons in the population of South Africa. Population is the estimated South African population at the

mid year in the periods indicated as published by Statistics South Africa, a South African governmental department. We

calculate fixed-line traffic, other than international outgoing mobile traffic and international interconnection traffic, by

dividing traffic revenues for the particular category by the weighted average tariff for such category during the relevant

period. Fixed-line international outgoing mobile traffic and international interconnection traffic are based on the actual

traffic registered through the respective exchanges and reflected in international interconnection invoices. We calculate

revenue per fixed access line by dividing total fixed-line revenue during the period, excluding data and directories and other

revenue, by the average number of fixed lines during the period. We calculate our number of fixed lines per fixed-line

employee on the basis of fixed lines in service at period end divided by the number of employees in our fixed-line segment

at period end, excluding employees from our two subsidiaries, Telkom Directory Services and Swiftnet, which do not

provide public switched telecommunications services.

7

Rand amounts as of and for the year ended March 31, 2002 and as of and for the six months ended September 30, 2002

have been translated into Dollars solely for your convenience at R10.54 per $1.00, the Rand noon buying rate discussed in

"Exchange Rates" on page 31 of this prospectus on September 30, 2002, the date of the Telkom Group's most recent

consolidated balance sheet included in this prospectus. These translations should not be construed as representations that

the Rand amounts could actually be converted into US dollars at these rates or at all.

You should read the following information together with "Risk Factors" beginning on page 17, "Capitalization" on

page 32, "Selected Historical Consolidated Financial and Other Data of the Telkom Group" beginning on page 33,

"Management's Discussion and Analysis of Financial Condition and Results of Operations" beginning on page 39 and the

consolidated financial statements and the notes thereto of the Telkom Group and Vodacom beginning on page F-2 of this

prospectus.

8

THE TELKOM GROUP

Summary Income Statement Data

Six months ended

Year ended March 31,

September 30,

2000

2001

2002

2002

2001

2002

2002

ZAR

ZAR

ZAR

USD

ZAR

ZAR

USD

Amounts in accordance with IAS

(unaudited)

(in millions, except per share amounts)

Operating revenue . . . . . . . . . . . . . . .

27,113

31,352

34,197

3,244

16,523

18,316

1,738

Employee expenses1

. . . . . . . . . . . . .

7,713

6,590

7,166

680

3,590

3,707

352

Payments to other operators . . . . . . . . .

4,241

4,983

5,762

547

2,654

3,105

294

Selling, general and administrative2

. . . . .

5,324

6,971

8,237

781

3,794

3,795

360

Services rendered . . . . . . . . . . . . . .

1,439

1,539

2,194

208

1,091

1,108

105

Operating leases . . . . . . . . . . . . . . .

340

1,292

1,217

115

583

684

65

Depreciation and amortization . . . . . . . .

4,174

5,052

5,408

513

2,643

3,106

295

Operating expenses . . . . . . . . . . . . . .

23,231

26,427

29,984

2,844

14,355

15,505

1,471

Operating profit . . . . . . . . . . . . . . . .

3,882

4,925

4,213

400

2,168

2,811

267

Investment income . . . . . . . . . . . . . .

641

617

490

46

306

152

14

Finance charges . . . . . . . . . . . . . . .

(2,482)

(3,137)

(2,550)

(242)

(1,845)

(1,779)

(169)

Profit before tax . . . . . . . . . . . . . . . .

2,041

2,405

2,153

204

629

1,184

112

Taxation . . . . . . . . . . . . . . . . . . .

(501)

(715)

(873)

(83)

(206)

(456)

(43)

Profit after tax . . . . . . . . . . . . . . . . .

1,540

1,690

1,280

121

423

728

69

Minority interests . . . . . . . . . . . . . .

(13)

(68)

(59)

(5)

(52)

(84)

(8)

Net profit . . . . . . . . . . . . . . . . . . .

1,527

1,622

1,221

116

371

644

61

Number of ordinary shares outstanding

(millions)

Basic . . . . . . . . . . . . . . . . . . . . .

557

557

557

557

557

557

557

Diluted . . . . . . . . . . . . . . . . . . . .

557

557

557

557

557

557

557

Earnings per share (cents)

Basic . . . . . . . . . . . . . . . . . . . . .

274.1

291.2

219.2

20.8

66.6

115.6

11.0

Diluted . . . . . . . . . . . . . . . . . . . .

274.1

291.2

219.2

20.8

66.6

115.6

11.0

Dividends per share (cents) . . . . . . . . . .

59.6

-

-

-

-

-

-

Amounts in accordance with US GAAP

Net revenue . . . . . . . . . . . . . . . . . . .

n/a

26,413

27,947

2,653

13,657

14,605

1,386

Operating income . . . . . . . . . . . . . . . .

n/a

3,716

2,498

237

1,711

2,219

211

Net income . . . . . . . . . . . . . . . . . . .

n/a

1,598

1,317

125

481

757

73

Earnings per share (cents)

Basic . . . . . . . . . . . . . . . . . . . . .

n/a

286.9

236.5

22.4

86.4

135.9

12.9

Diluted . . . . . . . . . . . . . . . . . . . .

n/a

286.9

236.5

22.4

86.4

135.9

12.9

9

Summary Balance Sheet Data

As of

As of March 31,

September 30,

2000

2001

2002

2002

2002

2002

ZAR

ZAR

ZAR

USD

ZAR

USD

Amounts in accordance with IAS

(unaudited)

(in millions, except per share amounts)

Total assets . . . . . . . . . . . . . . . . . . .

47,276

53,537

55,208

5,238

54,581

5,178

Current assets . . . . . . . . . . . . . . . . . .

11,010

12,674

10,968

1,041

11,195

1,062

Cash and cash equivalents . . . . . . . . . .

1,953

1,801

724

69

1,085

103

Other current assets . . . . . . . . . . . . .

9,057

10,873

10,244

972

10,110

959

Non-current assets . . . . . . . . . . . . . . .

36,266

40,863

44,240

4,197

43,386

4,116

Total liabilities3

. . . . . . . . . . . . . . . . .

33,879

38,449

38,243

3,628

36,892

3,500

Current liabilities . . . . . . . . . . . . . . . .

14,371

15,447

12,646

1,200

15,552

1,475

Short-term debt4

. . . . . . . . . . . . . . .

6,046

6,425

2,868

272

7,322

694

Other current liabilities . . . . . . . . . . .

8,325

9,022

9,778

928

8,230

781

Non-current liabilities . . . . . . . . . . . . .

19,508

23,002

25,597

2,428

21,340

2,025

Long-term debt5

. . . . . . . . . . . . . . .

15,928

19,843

22,533

2,138

18,144

1,722

Other non-current liabilities . . . . . . . . .

3,580

3,159

3,064

290

3,196

303

Minority interests . . . . . . . . . . . . . . .

47

116

133

13

214

20

Shareholders' equity . . . . . . . . . . . . . .

13,350

14,972

16,832

1,597

17,475

1,658

Amounts in accordance with US GAAP

Total assets . . . . . . . . . . . . . . . . . . .

n/a

49,524

50,943

4,836

49,458

4,693

Total liabilities . . . . . . . . . . . . . . . . .

n/a

35,626

35,280

3,349

33,076

3,138

Shareholders' equity . . . . . . . . . . . . . .

n/a

13,776

15,535

1,475

16,220

1,539

Six months ended

Year ended March 31,

September 30,

2000

2001

2002

2002

2001

2002

2002

ZAR

ZAR

ZAR

USD

ZAR

ZAR

USD

Summary Cash Flow Data

(unaudited)

Amounts in accordance with IAS

(in millions)

Cash flow from operating activities . . . . . .

4,917

6,165

8,171

775

3,301

3,462

328

Cash flow from/(used in) investing activities . .

(9,107)

(9,964)

(9,294)

(882)

(3,653)

(2,453)

(233)

Cash flow from/(used in) financing activities .

5,051

3,439

110

10

(973)

(1,178)

(112)

Summary Other Data

Headline earnings per share (cents)6

. . . . . .

199.9

341.8

299.3

28.4

70.2

123.9

11.8

Net asset value per share (cents) (at period end)7 2,396.6

2,687.8

3,021.7

286.7

n/a

3,137.2

297.6

Net asset value per share excluding

intangibles (cents) (at period end)7 . . . . . . . 2,312.3

2,613.3

2,926.6

277.7

n/a

3,057.8

290.1

EBITDA8

. . . . . . . . . . . . . . . . . . . .

8,056

9,977

9,621

913

4,811

5,917

562

Total debt (at period end)9

. . . . . . . . . . .

21,974

26,268

25,401

2,410

25,359

25,466

2,416

Capital expenditures excluding intangibles . . .

9,461

9,889

9,004

854

3,641

2,346

223

10

Summary Fixed-Line Statistical Data

Six months ended

Year ended March 31,

September 30,

2000

2001

2002

2001

2002

Fixed access lines (thousands) (at period end)10

. . . . .

5,493

4,962

4,924

4,986

4,895

Postpaid

PSTN11

. . . . . . . . . . . . . . . . . . . . . . . . . . .

4,668

3,930

3,554

3,761

3,407

ISDN channels . . . . . . . . . . . . . . . . . . . . . . .

271

374

467

421

522

Prepaid . . . . . . . . . . . . . . . . . . . . . . . . . . . .

381

480

708

615

780

Payphones12

. . . . . . . . . . . . . . . . . . . . . . . . . .

173

178

195

189

186

Fixed-line penetration rate (%) (at period end) . . . . . . .

12.8

11.4

11.1

11.1

10.8

Revenue per fixed access line (ZAR) . . . . . . . . . . .

3,869

4,297

4,729

2,294

2,456

Total fixed-line traffic (millions of minutes) . . . . . . .

31,127

32,915

32,973

16,620

16,145

Local13

. . . . . . . . . . . . . . . . . . . . . . . . . . .

19,471

20,388

20,252

10,246

9,870

Long distance . . . . . . . . . . . . . . . . . . . . . . .

5,222

4,938

4,895

2,492

2,445

Fixed-to-mobile . . . . . . . . . . . . . . . . . . . . . .

3,659

4,319

4,390

2,221

2,079

International outgoing . . . . . . . . . . . . . . . . . .

344

357

375

184

219

Interconnection . . . . . . . . . . . . . . . . . . . . . .

2,431

2,913

3,061

1,477

1,532

Number of full-time, fixed-line employees (at period end)14

49,128

43,758

39,444

42,110

38,009

Fixed lines per fixed-line employee (at period end)14

. . . .

112

113

125

118

129

1

Employee expenses include retrenchment expenses of R373 million, R132 million and R303 million in the years ended March 31,

2002, 2001 and 2000, respectively, and R169 million and R195 million in the six months ended September 30, 2002 and 2001,

respectively.

2

Selling, general and administrative expenses include asset write-offs of R445 million and R230 million in the years ended March 31,

2002 and 2001, respectively, and provisions for potential damages related to Telkom's arbitration with Telcordia of R375 million in the

year ended March 31, 2002.

3

As of September 30, 2002, R3,621 million of our long-term debt was guaranteed by the Government of the Republic of South Africa.

4

Includes short-term portion of finance leases and utilized credit facilities.

5

Includes long-term portion of finance leases.

6

Headline earnings per share is a disclosure requirement of the JSE and is not a recognized measure under US GAAP. The following is

a reconciliation between net profit and headline earnings in accordance with IAS for the periods indicated:

Six months ended

Year ended March 31,

September 30,

2000

2001

2002

2001

2002

ZAR

ZAR

ZAR

ZAR

ZAR

(unaudited)

(in millions, except per share amounts)

Net profit

1,527

1,622

1,221

371

644

Adjustments:

Profit on disposal of property, plant and equipment . . . . . . . . . . .

(493)

(29)

(22)

(6)

(7)

Profit on disposal of subsidiaries and joint ventures . . . . . . . . . . .

(83)

-

(8)

-

-

Property, plant and equipment impairment losses . . . . . . . . . . . .

-

279

445

-

16

Goodwill amortization . . . . . . . . . . . . . . . . . . . . . . . . . .

18

75

66

26

36

Tax and outside shareholders effects . . . . . . . . . . . . . . . . . . .

145

(43)

(35)

-

1

Headline earnings . . . . . . . . . . . . . . . . . . . . . . . .

1,114

1,904

1,667

391

690

Headline earnings per share (cents) . . . . . . . . . . . . . . . . .

199.9

341.8

299.3

70.2

123.9

7

Net asset value per share including and excluding intangibles are requirements of the JSE. Net asset value per share excluding

intangibles is not a recognized measure under US GAAP. Net asset value per share including intangibles is based on net assets of

R16,832 million, R14,972 million and R13,350 million as of March 31, 2002, 2001 and 2000, respectively, and R17,475 million as of

September 30, 2002. Net asset value per share excluding intangibles is based on net assets of R16,302 million, R14,557 million and

R12,880 million as of March 31, 2002, 2001 and 2000, respectively, and R17,033 million as of September 30, 2002.

11

8

EBITDA can be reconciled to operating profit by subtracting depreciation and amortization from EBITDA as follows:

Six months ended

Year ended March 31,

September 30,

2000

2001

2002

2002

2001

2002

2002

ZAR

ZAR

ZAR

USD

ZAR

ZAR

USD

(unaudited)

(in millions)

EBITDA . . . . . . . . . . . . . . . . . . . . . .

8,056

9,977

9,621

913

4,811

5,917

562

Depreciation and Amortization . . . . . . . . . .

4,174

5,052

5,408

513

2,643

3,106

295

Operating Profit . . . . . . . . . . . . . . . . .

3,882

4,925

4,213

400

2,168

2,811

267

9

Includes short-term and long-term debt, finance lease obligations and utilized credit facilities.

10

Including Telkom internal lines of 162,460, 151,986 and 145,302 as of March 31, 2002, 2001 and 2000, respectively, and 136,459 and

157,942 as of September 30, 2002 and 2001, respectively. Each PSTN line includes one access channel, each basic ISDN line includes

two access channels and each primary ISDN line includes 30 access channels.

11

Excluding ISDN channels.

12

Includes public and private payphones.

13

Local traffic includes internet traffic.

14

Excluding employees of Telkom Directory Services and Swiftnet.

12

SUMMARY HISTORICAL CONSOLIDATED FINANCIAL

AND OTHER DATA OF VODACOM

The following table sets forth summary consolidated financial and other data of Vodacom as of and for each of the three

years in the period ended March 31, 2002 and as of and for each of the six month periods ended September 30, 2002 and

2001. Information in the Vodacom table reflects 100% of Vodacom's results of operations. Information with respect to

Vodacom's other African operations in the Vodacom table reflects 100% of the operations of Vodacom's subsidiaries in

Lesotho and Tanzania and 51% of Vodacom's joint venture in the Democratic Republic of the Congo, unless otherwise

indicated. We proportionately consolidate our 50% interest in Vodacom in the Telkom Group's consolidated financial

statements. Vodacom's direct network operating costs, depreciation, other operating income, employee expenses, marketing

expenses, administrative expenses, amortization of intangible assets and integration costs, disposals of operations and

impairment costs are presented as separate line items in Vodacom's consolidated financial statements, but have been

combined under the heading "operating expenses" in the table set forth below.

The following summary historical consolidated financial data of Vodacom as of and for each of the three years ended

March 31, 2002 have been derived from Vodacom's historical consolidated financial statements beginning on page F-115 of

this prospectus, which were audited by PricewaterhouseCoopers, Inc. and Deloitte & Touche, Registered Accountants and

Auditors, Chartered Accountants (SA). The following summary historical consolidated financial data of Vodacom as of

September 30, 2002 and for each of the six month periods ended September 30, 2002 and 2001 was derived from

Vodacom's unaudited condensed consolidated financial statements beginning on page F-25 of this prospectus, which, in the

opinion of Vodacom's management, have been prepared on the same basis as Vodacom's audited consolidated financial

statements and reflect all adjustments, consisting of normal recurring adjustments, necessary for a fair presentation of

Vodacom's results of operations and financial position for such periods. Results for the six month periods ended

September 30, 2002 and 2001 are not necessarily indicative of results that may be expected for the entire year.

The consolidated financial statements of Vodacom have been prepared in accordance with IAS, which differs in certain

respects from US GAAP. For a description of the principal differences between IAS and US GAAP relevant to the financial

statements of Vodacom and a reconciliation to US GAAP of net income and shareholders' equity, see note 45 of the notes

to the audited consolidated financial statements of Vodacom as of and for the three years ended March 31, 2002 beginning

on page F-176 of this prospectus and note 20 of the notes to the unaudited condensed consolidated financial statements of

Vodacom as of September 30, 2002 and for each of the six month periods ended September 30, 2002 and 2001 beginning

on page F-40 of this prospectus.

EBITDA represents operating profit before income tax, finance charges, investment income and depreciation and

amortization. We believe that EBITDA provides meaningful additional information to investors since it is widely accepted

by analysts and investors as a basis for comparing a company's underlying operating profitability with that of other

companies as it is not influenced by past capital expenditures or business acquisitions, a company's capital structure or the

relevant tax regime. This is particularly the case in a capital-intensive industry such as communications. It is also a widely

accepted indicator of a company's ability to service its long-term debt and other fixed obligations and to fund its continued

growth. EBITDA is not a US GAAP or IAS measure. You should not construe EBITDA as an alternative to operating profit

or cash flows from operating activities determined in accordance with US GAAP or IAS or as a measure of liquidity.

EBITDA is not defined in the same manner by all companies and may not be comparable to other similarly titled measures

of other companies unless the definition is the same.

Vodacom's customer totals are based on the total number of customers registered on Vodacom's network, which have

not been disconnected, including inactive customers, as of the end of the period indicated. See "Business - Mobile

communications - South Africa - Customers" beginning on page 122 of this prospectus for a discussion of Vodacom's

procedures with respect to disconnections and inactive customers. Vodacom's churn is calculated by dividing the average

monthly number of disconnections during the period by the average monthly total reported customer base during the

period. Vodacom calculates penetration, or teledensity, based on the total number of customers at the end of the period per

100 persons in the population of South Africa. Population is the estimated South African population at the mid-year in the

periods indicated as published by Statistics South Africa, a South African governmental department. Vodacom's traffic

comprises total traffic registered on Vodacom's network, including bundled minutes, outgoing international roaming calls

and calls to free services, but excluding national and incoming international roaming calls. Vodacom's average monthly

revenue per customer, or ARPU, is calculated by dividing the average monthly revenue during the period by the average

monthly total reported customer base during the period. ARPU excludes revenue from equipment sales, other sales and

services and revenue from national and international users roaming on Vodacom's networks. Vodacom's average monthly

minutes of use per customer, or MOU, is calculated by dividing the average monthly minutes during the period by the

average monthly total reported customer base during the period. MOU excludes calls to free services, bundled minutes and

data minutes. Cumulative network capital expenditure per customer is the cumulative network capital expenditure since the

launch of Vodacom's South African network divided by Vodacom's average customers in South Africa for the period.

Rand amounts as of and for the year ended March 31, 2002 and as of and for the six months ended September 30, 2002

have been translated into Dollars solely for your convenience at R10.54 per $1.00, the Rand noon buying rate discussed in

"Exchange Rates" on page 31 of this prospectus on September 30, 2002, the date of Vodacom's most recent balance sheet

included in this prospectus. These translations should not be construed as representations that the Rand amounts could

actually be converted into US dollars at these rates or at all.

You should read the following information together with "Risk Factors" beginning on page 17, "Selected Historical

Consolidated Financial and Other Data of the Telkom Group" beginning on page 33, "Management's Discussion and

Analysis of Financial Condition and Results of Operations" beginning on page 39 and the consolidated financial statements

and the notes thereto of the Telkom Group and Vodacom beginning on page F-2 of this prospectus.

13

14

VODACOM

Summary Income Statement Data

Six months ended

Year ended March 31,

September 30,

2000

2001

2002

2002

2001

2002

2002

ZAR

ZAR

ZAR

USD

ZAR

ZAR

USD

Amounts in accordance with IAS

(unaudited)

(in millions, except per share amounts)

Revenue . . . . . . . . . . . . . . . . . . . .

9,572

13,276

16,151

1,532

7,522

9,441

895

Operating expenses . . . . . . . . . . . . .

7,208

10,723

12,530

1,189

5,947

7,603

721

Operating profit . . . . . . . . . . . . . . .

2,364

2,553

3,621

343

1,575

1,838

174

Investment income . . . . . . . . . . . . .

32

25

32

3

17

16

2

Finance charges . . . . . . . . . . . . . . .

(567)

(504)

(60)

(5)

(123)

(315)

(30)

Profit before tax . . . . . . . . . . . . . . .

1,829

2,074

3,593

341

1,469

1,539

146

Taxation . . . . . . . . . . . . . . . . . . .

(514)

(765)

(1,190)

(113)

(445)

(525)

(50)

Profit after tax . . . . . . . . . . . . . . . .

1,315

1,309

2,403

228

1,024

1,014

96

Minority interests . . . . . . . . . . . . . .

-

9

(30)

(3)

(16)

(96)

(9)

Net profit . . . . . . . . . . . . . . . . . . .

1,315

1,318

2,373

225

1,008

918

87

Amounts in accordance with US GAAP

Net profit for the year . . . . . . . . . . . . .

n/a

1,249

2,120

201

932

839

80

Summary Balance Sheet Data

As of

As of March 31,

September 30,

2000

2001

2002

2002

2002

2002

ZAR

ZAR

ZAR

USD

ZAR

USD

Amounts in accordance with IAS

(unaudited)

(in millions)

Total assets . . . . . . . . . . . . . . . . . . . . . . .

9,864

12,342

15,359

1,457

17,319

1,643

Current assets . . . . . . . . . . . . . . . . . . . . . .

2,788

3,470

4,145

393

5,451

517

Cash and cash equivalents . . . . . . . . . . . . . .

936

798

719

68

1,564

148

Other current assets . . . . . . . . . . . . . . . . . .

1,852

2,672

3,426

325

3,887

369

Non-current assets . . . . . . . . . . . . . . . . . . . .

7,076

8,872

11,214

1,064

11,868

1,126

Total liabilities . . . . . . . . . . . . . . . . . . . . .

7,195

8,847

9,884

938

10,880

1,032

Current liabilities . . . . . . . . . . . . . . . . . . . .

5,883

7,267

7,990

758

8,080

766

Short-term debt1

. . . . . . . . . . . . . . . . . . .

3,370

2,547

3,517

334

4,207

399

Other current liabilities . . . . . . . . . . . . . . . .

2,513

4,720

4,473

424

3,873

367

Non-current liabilities . . . . . . . . . . . . . . . . . .

1,312

1,580

1,894

180

2,800

266

Long-term debt2

. . . . . . . . . . . . . . . . . . .

817

896

780

74

1,592

151

Other non-current liabilities . . . . . . . . . . . . .

495

684

1,114

106

1,208

115

Minority interests . . . . . . . . . . . . . . . . . . .

(2)

(11)

11

1

102

10

Shareholders' equity . . . . . . . . . . . . . . . . . .

2,671

3,506

5,464

518

6,337

601

Amounts in accordance with US GAAP

Shareholders' equity . . . . . . . . . . . . . . . . . .

n/a

3,195

4,874

462

5,654

536

15

Six months ended

Year ended March 31,

September 30,

2000

2001

2002

2002

2001

2002

2002

ZAR

ZAR

ZAR

USD

ZAR

ZAR

USD

Summary Cash Flow Data

Amounts in accordance with IAS

(unaudited)

(in millions)

Cash flow from operating activities . . . . .

2,341

3,610

3,815

362

n/a

1,637

155

Cash flow from/(used in) investing activities

(3,338)

(2,853)

(4,543)

(431)

n/a

(2,415)

(229)

Cash flow from/(used in) financing activities

646

(1,038)

571

54

n/a

494

47

Summary Other Data

EBITDA

3

. . . . . . . . . . . . . . . . . .

3,462

4,189

5,691

540

n/a

3,027

287

Total debt (at period end)

4

. . . . . . . . . .

4,187

3,443

4,297

408

n/a

5,799

550

Capital expenditures including intangibles

2,032

3,184

4,279

406

n/a

1,718

163

South Africa . . . . . . . . . . . . . . . .

2,011

2,830

3,291

312

n/a

1,121

106

Other African countries . . . . . . . . . .

21

354

988

94

n/a

597

57

Summary Statistical Data

Six months ended

Year ended March 31,

September 30,

2000

2001

2002

2001

2002

South Africa

Total mobile customers (thousands) (at period end)

5

. .

3,069

5,108

6,557

5,657

7,130

Contract . . . . . . . . . . . . . . . . . . . . . . . . . .

963

1,037

1,090

1,062

1,139

Prepaid . . . . . . . . . . . . . . . . . . . . . . . . . . .

2,082

4,046

5,439

4,569

5,961

Community services telephones . . . . . . . . . . . . . .

24

25

28

26

30

Churn (%) . . . . . . . . . . . . . . . . . . . . . . . . . .

31.8

23.3

27.2

31.3

30.7

Contract . . . . . . . . . . . . . . . . . . . . . . . . . .

17.4

18.7

14.5

16.6

13.2

Prepaid . . . . . . . . . . . . . . . . . . . . . . . . . . .

40.5

24.8

30.1

34.8

34.3

Mobile market share (%) (at period end) . . . . . . . . . .

59

61

61

61

59

Mobile penetration (%) (at period end) . . . . . . . . . . .

12.1

19.1

24.2

20.6

26.6

Total mobile traffic (millions of minutes) . . . . . . . . .

5,669

7,472

8,881

4,229

5,007

Outgoing . . . . . . . . . . . . . . . . . . . . . . . . . .

2,885

4,052

4,967

2,307

2,994

Incoming . . . . . . . . . . . . . . . . . . . . . . . . . .

2,784

3,420

3,914

1,922

2,013

Average monthly revenue per customer (ZAR)

6

. . . . .

266

208

182

190

181

Contract

6

. . . . . . . . . . . . . . . . . . . . . . . . . .

481

493

560

551

612

Prepaid . . . . . . . . . . . . . . . . . . . . . . . . . . .

132

98

93

94

88

Community services . . . . . . . . . . . . . . . . . . . .

n/a

1,453

1,719

1,710

1,766

Average monthly minutes of use per customer . . . . . .

158

137

111

114

102

Contract . . . . . . . . . . . . . . . . . . . . . . . . . .

274

270

264

265

269

Prepaid . . . . . . . . . . . . . . . . . . . . . . . . . . .

90

70

58

59

53

Community services . . . . . . . . . . . . . . . . . . . .

1,593

2,859

3,354

3,246

3,215

Cumulative network capital expenditure per customer (ZAR)

(at period end) . . . . . . . . . . . . . . . . . . . . . . . .

2,543

2,053

1,991

2,048

1,980

Number of mobile employees (at period end)

1

. . . . . .

4,048

4,102

3,984

4,384

3,845

Number of mobile customers per mobile employee

(at period end)

7

. . . . . . . . . . . . . . . . . . . . . . . .

758

1,245

1,646

1,290

1,854

Summary Statistical Data

Six months ended

Year ended March 31,

September 30,

2000

2001

2002

2001

2002

Other African countries

Number of mobile customers (thousands) (at period end)

12

104

306

164

540

Average monthly revenue per customer

Lesotho (ZAR) . . . . . . . . . . . . . . . . . . . . . .

n/a

n/a

144

n/a

87

Tanzania (USD) . . . . . . . . . . . . . . . . . . . . . .

n/a

31

27

n/a

23

Democratic Republic of the Congo (USD) . . . . . . . .

n/a

n/a

n/a

n/a

22

Number of mobile employees (at period end)7

. . . . . .

43

170

369

201

397

Number of customers per mobile employee (at period end)7

279

612

830

816

1,360

1

Includes short-term portion of finance leases and utilized credit facilities.

2

Includes long-term portion of finance leases.

3

EBITDA includes a net gain of R56 million, a net loss of R213 million and a net gain of R129 million in the 2002, 2001 and 2000

financial years, respectively, and a net gain of R25.5 million and nil in the six months ended September 30, 2001 and 2002,

respectively, for integration costs, disposals of operations and impairments.

4

Includes interest-bearing debt, shareholder loans and bank overdrafts.

5

13.9% of Vodacom's total reported customers, 15.9% of its prepaid customers and 3.8% of its contract customers in South Africa were

inactive as of March 31, 2002. 15.1% of Vodacom's total reported customers, 17.0% of its prepaid customers and 4.9% of its contract

customers in South Africa were inactive as of September 30, 2002.

6

Value added service revenue from previously partially owned service providers is included in contract and total average monthly

revenue per customer from October 1, 2001, at which time Vodacom consolidated these previously partially owned service providers.

7

Includes 423, 553 and 96 total temporary employees as of March 31, 2002, 2001 and 2000, respectively, and 140 and 335 total

temporary employees as of September 30, 2002 and 2001, respectively.

END OF PROSPECTUS SUMMARY

16

RISK FACTORS

You should carefully consider the risks described below and the other information in this prospectus before making a

decision to purchase the ordinary shares or ADSs, including the consolidated financial statements of the Telkom Group and

Vodacom and the related notes thereto beginning on page F-2 of this prospectus.

Risks Related to our Business

Increased competition in the South African telecommunications market may result in a reduction in overall average

tariffs and market share in our fixed-line business, which could cause our growth rates, operating revenue and net profit

to decline.

We had the exclusive right to provide public switched telecommunications services, including international telephone

services, in the Republic of South Africa until May 7, 2002, but for a number of years have competed with mobile

operators and value-added network operators in connection with the provision of other services. The Independent

Communications Authority of South Africa, or ICASA, issued an international carrier of carriers license and a multimedia

license to Sentech Limited, a company incorporated in the Republic of South Africa, in May 2002. In addition, a process

has commenced to issue an additional license to provide public switched telecommunications services to a second national

operator and to issue additional licenses to small business operators to provide telecommunications services in areas with a

teledensity of less than 5%. ICASA has indicated that it expects to issue these licenses in 2003 or early 2004. Further

competition may arise as a result of an assessment by the Minister of Communications of the feasibility of issuing

additional licenses from May 2005. As competition intensifies, the main challenges our fixed-line business faces are

continuing to improve customer loyalty and maintaining its leadership in the South African communications market. As a

result of increasing competition, we anticipate a reduction in overall average tariffs and market share in our fixed-line

business, which could cause our growth rates, operating revenue and net profit to decline.

Competition from the three existing mobile communications network operators in South Africa has resulted in

significant customer migration and substitution from fixed-line to mobile services. If this migration and substitution

continue, our growth rates, operating revenue and net profit could decline.

Telkom competes with the three existing mobile communications network operators, Vodacom, Mobile Telephone

Network Holdings (Proprietary) Limited, a company incorporated in the Republic of South Africa, or MTN, and Cell C

(Proprietary) Limited, a company incorporated in the Republic of South Africa, or Cell C, for customers. Telkom also

competes with mobile operators who use least cost routing technology that enables fixed-to-mobile calls from corporate

private branch exchanges to bypass our fixed-line network by being transferred directly to mobile networks. Telkom has

experienced significant customer migration from fixed-line services to mobile services, as well as substitution of calls

placed using mobile services rather than our fixed-line service, in recent years with the increase in mobile penetration in

South Africa. If this migration continues, our growth rates, operating revenue and net profit could decline.

Increased competition in the mobile communications market in South Africa may result in a reduction of Vodacom's

average tariffs and Vodacom's market share and increased customer acquisition and retention costs, which could cause

Vodacom's growth rates, revenue and net profit to decline.

There are currently three operators in the South African mobile communications market, Vodacom, MTN and Cell C.

At September 30, 2002, Vodacom held approximately 59%, MTN held approximately 36% and Cell C held approximately

5% of the South African mobile communications market, based on total reported customers. Cell C only commenced

operations in November 2001. In addition, ICASA has indicated that it intends to license global mobile personal

communications services in 2003 or later and to conduct a feasibility study on the licensing of a fourth mobile operator in