QuickLinks -- Click here to rapidly navigate through this document

As filed with the Securities and Exchange Commission on June 25, 2004

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

| (Mark One) | |

o | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) or (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

ý | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended March 31, 2004 | |

Or | |

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to . | |

Commission file number: 001-31609

TELKOM SA LIMITED

(Exact name of Registrant as specified in its charter)

THE REPUBLIC OF SOUTH AFRICA

(Jurisdiction of incorporation or organization)

Telkom Towers North

152 Proes Street

Pretoria 0002

The Republic of South Africa

(27)(12)311-3566

(Address of principal executive offices)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |

| American Depositary Shares, each representing four (4) Ordinary Shares, par value R10 per share | New York Stock Exchange, Inc. | |

| Ordinary Shares, par value R10 per share | New York Stock Exchange, Inc.* |

- *

- Listed, not for trading, but only in connection with the registration of American Depositary Shares, pursuant to the requirements of the Securities and Exchange Commission.

Securities registered or to be registered pursuant to Section 12(g) of the Act.

NONE

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act

NONE

The number of outstanding shares of each of the issuer's classes of capital or common stock as of the close of the period covered by the annual report:

| Ordinary Shares, par value R10 per share | 553,846,083 | |

| Class A Ordinary Share, par value R10 per share | 1 | |

| Class B Ordinary Share, par value R10 per share | 1 |

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

[x] Yes [ ] No

Indicate by check mark which financial statement item the registrant has elected to follow.

[ ] Item 17 [x] Item 18

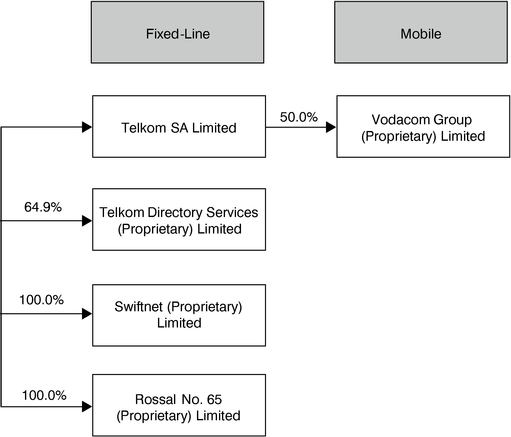

Unless the context requires otherwise, references to "we," "us," "our" and the "Telkom Group" in this annual report refer to Telkom SA Limited and its subsidiaries and its 50% interest in Vodacom, and references to "Telkom" in this annual report refer only to Telkom SA Limited. References to "Vodacom" in this annual report refer to Telkom's 50% owned joint venture, Vodacom Group (Proprietary) Limited, and its subsidiaries. We do not control Vodacom, the management of which requires consensus agreement among its shareholders who are party to Vodacom's joint venture agreement.

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

Many of the statements included in this annual report, as well as oral statements that may be made by us or by officers, directors or employees acting on behalf of us, constitute or are based on forward-looking statements within the meaning of the U.S. Private Securities Litigation Reform Act of 1995, specifically Section 21E of the U.S. Securities Exchange Act of 1934, as amended. All statements, other than statements of historical facts, including, among others, statements regarding our future financial position and plans, strategies, objectives, capital expenditures, projected costs and anticipated cost savings and financing plans, as well as projected levels of growth in the communications market, are forward-looking statements. Forward-looking statements can generally be identified by the use of terminology such as "may," "will," "should," "expect," "envisage," "intend," "plan," "project," "estimate," "anticipate," "believe," "hope," "can," "is designed to" or similar phrases, although the absence of such words does not necessarily mean that a statement is not forward-looking. These forward-looking statements involve a number of known and unknown risks, uncertainties and other factors that could cause our actual results and outcomes to be materially different from historical results or from any future results expressed or implied by such forward-looking statements. Among the factors that could cause our actual results or outcomes to differ materially from our expectations are those risks identified in Item 3. "Key Information—Risk Factors," including, but not limited to, increased competition in the South African fixed-line and mobile communications markets; continued reductions in Vodacom's and Telkom's net interconnect margins; developments in the regulatory environment; our ability to reduce expenditure; the outcome of legal or arbitration proceedings, including the outcome of Telkom's hearing before the Competition Commission related to the VANs litigation and its proceedings with Telcordia Technologies Incorporated; the impact of the Municipal Property Rates Act; Vodacom's ability to expand its operations in other African countries and the general economic, political, social and legal conditions in South Africa and in other countries where Vodacom invests; fluctuations in the value of the Rand and inflation rates; our ability to retain key personnel; customer non-payments, theft and bad debt; and other matters not yet known to us or not currently considered material by us.

We caution you not to place undue reliance on these forward-looking statements. All written and oral forward-looking statements attributable to us, or persons acting on our behalf, are qualified in their entirety by these cautionary statements. Moreover, unless we are required by law to update these statements, we will not necessarily update any of these statements after the date of this annual report, either to conform them to actual results or to changes in our expectations.

i

PART I | ||||

Item 1. | Identity of Directors, Senior Management and Advisors | 1 | ||

| Item 2. | Offer Statistics and Expected Timetable | 1 | ||

| Item 3. | Key Information | 1 | ||

| Item 4. | Information on the Company | 33 | ||

| Item 5. | Operating and Financial Review and Prospects | 105 | ||

| Item 6. | Directors, Senior Management and Employees | 163 | ||

| Item 7. | Major Shareholders and Related Party Transactions | 190 | ||

| Item 8. | Financial Information | 204 | ||

| Item 9. | The Offer and Listing | 206 | ||

| Item 10. | Additional Information | 206 | ||

| Item 11. | Quantitative and Qualitative Disclosures About Market Risk | 236 | ||

| Item 12. | Description of Securities Other than Equity Securities | 243 | ||

PART II | ||||

Item 13. | Defaults, Dividend Arrearages and Delinquencies | 244 | ||

| Item 14. | Material Modifications to the Rights of Security Holders and Use of Proceeds | 244 | ||

| Item 15. | Controls and Procedures | 244 | ||

| Item 16A. | Audit Committee Financial Expert | 244 | ||

| Item 16B | Code of Ethics | 244 | ||

| Item 16C | Principal Accountant Fees and Services | 245 | ||

| Item 16D | Exemptions From the Listing Standards for Audit Committees | 245 | ||

| Item 16E | Purchases of Equity Securities by the Issuer and Affiliated Purchasers | 245 | ||

PART III | ||||

Item 17. | Financial Statements | 246 | ||

| Item 18. | Financial Statements | 247 | ||

| Item 19. | Exhibits | 247 | ||

ii

Item 1. Identity of Directors, Senior Management and Advisors

Not applicable.

Item 2. Offer Statistics and Expected Timetable

Not applicable.

SELECTED HISTORICAL CONSOLIDATED FINANCIAL

AND OTHER DATA OF THE TELKOM GROUP

The following table sets forth selected historical consolidated financial and other data of the Telkom Group as of and for each of the five years ended March 31, 2004. Information in the following table includes our 50% interest in the results, assets, liabilities and shareholders' equity of Vodacom, which we proportionately consolidate. Unless otherwise indicated, fixed-line statistical data is derived from the results of operations of our fixed-line segment, which provides fixed-line voice and data communications services through Telkom; directory services through our 64.9% owned subsidiary, Telkom Directory Services; and wireless data services through our wholly-owned subsidiary, Swiftnet. Reclassifications to prior periods have occurred in each of the years ending March 31, 2003 and 2004. In the 2003 financial year, we reclassified some of the items previously included in selling, general and administrative operating expenses and investment income into other income, a new line item in the Telkom Group's consolidated income statements. The reclassifications in the 2003 financial year reduced operating profit and EBITDA by R22 million in the 2002 financial year and increased operating profit and EBITDA by R59 million in the 2001 financial year. In the 2004 financial year, we reclassified discounts offered on mobile-to-fixed interconnect and discounts on leased line facilities to mobile operators from payments to other operators in operating expenses to an offset to operating revenue. We also reclassified costs in respect of asset write-offs from selling, general and administrative expenses to depreciation, amortization, impairments and asset write-offs; costs in respect of losses on the disposal of property, plant and equipment and investments from selling, general and administrative expenses to other income; and insurance costs paid to Debis for our vehicle fleet from operating leases to services rendered in the 2004 financial year. In addition, we revised our presentation to remove other income from operating expense. The reclassifications in the 2004 financial year had no effect on operating profit in prior years, but reduced operating revenue by R98 million, R109 million, R110 million and R93 million and increased EBITDA by R0 million, R279 million, R445 million and R205 million in the 2000, 2001, 2002 and 2003 financial years, respectively. The Telkom Group's consolidated income statements included in this annual report and the following financial information for each of the five years ended March 31, 2004 reflect all such reclassifications.

The following selected historical consolidated financial data of the Telkom Group as of and for each of the three years ended March 31, 2004 was extracted from the Telkom Group's historical consolidated financial statements included in this annual report, which have been audited by Ernst & Young, Independent Accountants and Auditors, Chartered Accountants (SA). The following selected historical consolidated financial data of the Telkom Group as of and for each of the two years ended March 31, 2001 was extracted from the Telkom Group's consolidated financial statements not included in this annual report, which have also been audited by Ernst & Young, Independent Accountants and Auditors, Chartered Accountants (SA).

1

The consolidated financial statements of the Telkom Group have been prepared in accordance with International Financial Reporting Standards, or IFRS, which differs in certain respects from US Generally Accepted Accounting Principles, or US GAAP. For a description of the principal differences between IFRS and US GAAP relevant to the consolidated financial statements of the Telkom Group and a reconciliation to US GAAP of net income and profit and shareholders' equity, see note 47 of the notes to the audited consolidated financial statements of the Telkom Group as of and for each of the three years ended March 31, 2004 included in this annual report.

EBITDA represents net profit before minority interests, taxation, finance charges, investment income and depreciation, amortization, impairment and write-offs. We believe that EBITDA provides meaningful additional information to investors since it is widely accepted by analysts and investors as a basis for comparing a company's underlying operating profitability with that of other companies as it is not influenced by past capital expenditures or business acquisitions, a company's capital structure or the relevant tax regime. This is particularly the case in a capital-intensive industry such as communications. It is also a widely accepted indicator of a company's ability to service its long-term debt and other fixed obligations and to fund its continued growth. EBITDA is not a US GAAP or IFRS measure. You should not construe EBITDA as an alternative to operating profit or cash flows from operating activities determined in accordance with US GAAP or IFRS or as a measure of liquidity. EBITDA is not defined in the same manner by all companies and may not be comparable to other similarly titled measures of other companies unless the definition is the same. In addition, because the calculation of EBITDA in the maintenance covenants contained in our credit facilities is based on accounting policies in use, consistently applied from the time the indebtedness was incurred. EBITDA for purposes of those covenants is not calculated in the same manner as it is calculated in the table below.

Fixed access lines are comprised of public switched telecommunications network lines, or PSTN lines, including integrated services digital network channels, or ISDN channels, public and private payphones and internal lines in service. We calculate fixed-line penetration, or teledensity, based on the total number of telephone lines in service at the end of the period per 100 persons in the population of South Africa. Population is the estimated South African population at the mid year in the periods indicated as published by Statistics South Africa, a South African governmental department. We calculate fixed-line traffic, other than international outgoing mobile traffic and international interconnection traffic, by dividing traffic operating revenue for the particular category by the weighted average tariff for such category during the relevant period. Fixed-line international outgoing mobile traffic and international interconnection traffic are based on the actual traffic registered through the respective exchanges and reflected in international interconnection invoices. We calculate revenue per fixed access line by dividing total fixed-line revenue during the period, excluding data and directories and other revenue, by the average number of fixed access lines during the period. We calculate our number of fixed lines per fixed-line employee on the basis of fixed access lines in service at period end divided by the number of employees of Telkom at period end.

Rand amounts as of and for the year ended March 31, 2004 have been translated into Dollars solely for your convenience at R6.32 per $1.00, the Rand noon buying rate discussed in Item 3. "Key Information—Exchange Rates" on March 31, 2004, the date of the Telkom Group's most recent consolidated balance sheet included in this annual report. These translations should not be construed as representations that the Rand amounts could actually be converted into US dollars at these rates or at all.

You should read the following information together with Item 3. "Key Information—Risk Factors," Item 5. "Operating and Financial Review and Prospects" and the consolidated financial statements and the notes thereto of the Telkom Group and Vodacom Group included in this annual report.

2

| | Year ended March 31, | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | 2000 | 2001 | 2002 | 2003 | 2004 | 2004 | ||||||||

| | ZAR | ZAR | ZAR | ZAR | ZAR | USD | ||||||||

| | (in millions, except per share amounts) | |||||||||||||

| Income Statement Data | ||||||||||||||

| Amounts in accordance with IFRS | ||||||||||||||

| Operating revenue(1) | 27,015 | 31,243 | 34,087 | 37,507 | 40,795 | 6,455 | ||||||||

| Other income(2)(7) | 621 | 192 | 143 | 233 | 98 | 15 | ||||||||

| Operating expenses | (23,728 | ) | (26,451 | ) | (30,039 | ) | (31,226 | ) | (31,805 | ) | (5,032 | ) | ||

| Employee expenses(3) | (7,713 | ) | (6,590 | ) | (7,166 | ) | (7,208 | ) | (7,408 | ) | (1,172 | ) | ||

| Payments to other operators(4) | (4,143 | ) | (4,874 | ) | (5,652 | ) | (6,092 | ) | (5,985 | ) | (947 | ) | ||

| Selling, general and administrative(5)(6)(7) | (5,919 | ) | (6,825 | ) | (7,956 | ) | (7,682 | ) | (7,971 | ) | (1,261 | ) | ||

| Services rendered(8) | (1,439 | ) | (1,604 | ) | (2,273 | ) | (2,622 | ) | (2,269 | ) | (359 | ) | ||

| Operating leases(8) | (340 | ) | (1,227 | ) | (1,139 | ) | (1,124 | ) | (923 | ) | (146 | ) | ||

| Depreciation, amortization, impairments and write-offs(6) | (4,174 | ) | (5,331 | ) | (5,853 | ) | (6,498 | ) | (7,249 | ) | (1,147 | ) | ||

| Operating profit | 3,908 | 4,984 | 4,191 | 6,514 | 9,088 | 1,438 | ||||||||

| Investment income | 615 | 558 | 512 | 424 | 479 | 75 | ||||||||

| Finance charges | (2,482 | ) | (3,137 | ) | (2,550 | ) | (4,154 | ) | (3,264 | ) | (516 | ) | ||

| Profit before tax | 2,041 | 2,405 | 2,153 | 2,784 | 6,303 | 997 | ||||||||

| Taxation | (501 | ) | (715 | ) | (873 | ) | (1,049 | ) | (1,711 | ) | (271 | ) | ||

| Profit after tax | 1,540 | 1,690 | 1,280 | 1,735 | 4,592 | 726 | ||||||||

| Minority interests | (13 | ) | (68 | ) | (59 | ) | (105 | ) | (69 | ) | (11 | ) | ||

| Net profit | 1,527 | 1,622 | 1,221 | 1,630 | 4,523 | 715 | ||||||||

| Number of ordinary shares outstanding | ||||||||||||||

| Basic | 557 | 557 | 557 | 557 | 554 | 554 | ||||||||

| Diluted | 557 | 557 | 557 | 557 | 554 | 554 | ||||||||

| Earnings per share (cents) | ||||||||||||||

| Basic | 274.1 | 291.2 | 219.2 | 292.6 | 812.0 | 128.5 | ||||||||

| Diluted | 274.1 | 291.2 | 219.2 | 292.6 | 812.0 | 128.5 | ||||||||

| Dividends per share (cents) | 59.6 | — | — | — | 90.0 | 14.2 | ||||||||

| Amounts in accordance with US GAAP | ||||||||||||||

| Operating revenue | n/a | 26,304 | 27,837 | 29,605 | 30,541 | 4,832 | ||||||||

| Operating income | n/a | 3,775 | 2,476 | 4,595 | 6,696 | 1,059 | ||||||||

| Net income | n/a | 1,598 | 1,317 | 1,704 | 4,230 | 669 | ||||||||

| Earnings per share (cents) | ||||||||||||||

| Basic | n/a | 286.9 | 236.5 | 305.9 | 759.4 | 120.1 | ||||||||

| Diluted | n/a | 286.9 | 236.5 | 305.9 | 759.4 | 120.1 | ||||||||

3

| | Year ended March 31, | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | 2000 | 2001 | 2002 | 2003 | 2004 | 2004 | |||||||

| | ZAR | ZAR | ZAR | ZAR | ZAR | USD | |||||||

| | (in millions) | ||||||||||||

| Balance Sheet Data | |||||||||||||

| Amounts in accordance with IFRS | |||||||||||||

| Total assets(9) | 47,276 | 53,537 | 55,316 | 53,229 | 52,984 | 8,384 | |||||||

| Current assets(10) | 11,010 | 12,674 | 10,997 | 9,921 | 11,061 | 1,750 | |||||||

| Cash and cash equivalents | 1,953 | 1,801 | 724 | 1,117 | 3,218 | 509 | |||||||

| Other current assets(10) | 9,057 | 10,873 | 10,273 | 8,804 | 7,843 | 1,241 | |||||||

| Non-current assets(9)(10) | 36,266 | 40,863 | 44,319 | 43,308 | 41,923 | 6,634 | |||||||

| Total liabilities(9)(11) | 33,879 | 38,449 | 38,351 | 34,687 | 30,726 | 4,862 | |||||||

| Current liabilities(9)(12)(13) | 14,382 | 15,314 | 12,765 | 14,197 | 14,443 | 2,286 | |||||||

| Short-term debt(9)(14) | 6,046 | 6,425 | 2,976 | 5,039 | 4,473 | 708 | |||||||

| Other current liabilities(12)(13) | 8,336 | 8,889 | 9,789 | 9,158 | 9,970 | 1,578 | |||||||

| Non-current liabilities(11)(12)(13) | 19,497 | 23,135 | 25,586 | 20,490 | 16,283 | 2,576 | |||||||

| Long-term debt(11)(15) | 15,928 | 19,843 | 22,533 | 17,453 | 12,703 | 2,010 | |||||||

| Other non-current liabilities(12)(13) | 3,569 | 3,292 | 3,053 | 3,037 | 3,580 | 566 | |||||||

| Minority interests | 47 | 116 | 133 | 194 | 200 | 32 | |||||||

| Shareholders' equity | 13,350 | 14,972 | 16,832 | 18,348 | 22,058 | 3,490 | |||||||

| Amounts in accordance with US GAAP | |||||||||||||

| Total assets | n/a | 49,535 | 50,944 | 48,991 | 46,933 | 7,426 | |||||||

| Total liabilities | n/a | 35,637 | 35,281 | 31,828 | 26,408 | 4,178 | |||||||

| Shareholders' equity | n/a | 13,776 | 15,535 | 17,013 | 20,371 | 3,223 | |||||||

| | Year ended March 31, | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | 2000 | 2001 | 2002 | 2003 | 2004 | 2004 | |||||||

| | ZAR | ZAR | ZAR | ZAR | ZAR | USD | |||||||

| | (in millions) | ||||||||||||

| Cash Flow Data | |||||||||||||

| Amounts in accordance with IFRS | |||||||||||||

| Cash flow from operating activities | 4,917 | 6,165 | 8,171 | 9,748 | 13,884 | 2,197 | |||||||

| Cash flow used in investing activities(16) | (9,107 | ) | (9,964 | ) | (9,250 | ) | (5,731 | ) | (5,423 | ) | (858 | ) | |

| Cash flow (used in)/from financing activities(16) | 5,051 | 3,439 | 66 | (3,026 | ) | (6,481 | ) | (1,025 | ) | ||||

Other Data | |||||||||||||

| EBITDA(17) | 8,082 | 10,315 | 10,044 | 13,012 | 16,337 | 2,585 | |||||||

| Total debt (at period end)(9)(11)(18) | 21,974 | 26,268 | 25,509 | 22,492 | 17,176 | 2,718 | |||||||

| Capital expenditures excluding intangibles | 9,461 | 9,889 | 9,004 | 5,712 | 5,307 | 840 | |||||||

4

| | Year ended March 31, | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| | 2000 | 2001 | 2002 | 2003 | 2004 | ||||||

| Fixed-Line Statistical Data | |||||||||||

| Fixed access lines (thousands) (at period end)(19) | 5,493 | 4,962 | 4,924 | 4,844 | 4,821 | ||||||

| Postpaid | |||||||||||

| PSTN(20) | 4,668 | 3,930 | 3,554 | 3,285 | 3,134 | ||||||

| ISDN channels | 271 | 374 | 467 | 563 | 656 | ||||||

| Prepaid | 381 | 480 | 708 | 817 | 856 | ||||||

| Payphones(21) | 173 | 178 | 195 | 179 | 175 | ||||||

| Fixed-line penetration rate (%) (at period end) | 12.8 | 11.4 | 11.1 | 10.7 | 10.4 | ||||||

| Revenue per fixed access line (ZAR) | 3,859 | 4,287 | 4,722 | 4,987 | 5,169 | ||||||

| Total fixed-line traffic (millions of minutes)(22) | 31,127 | 32,863 | 33,084 | 32,868 | 32,942 | ||||||

| Local(23) | 19,471 | 20,387 | 20,538 | 20,396 | 20,547 | ||||||

| Long distance | 5,222 | 4,900 | 4,747 | 4,728 | 4,616 | ||||||

| Fixed-to-mobile | 3,659 | 4,307 | 4,364 | 4,135 | 3,980 | ||||||

| International outgoing | 344 | 356 | 374 | 439 | 427 | ||||||

| International voice over internet protocol | — | — | — | — | 25 | ||||||

| Interconnection | 2,431 | 2,913 | 3,061 | 3,170 | 3,347 | ||||||

| Data Communications Services | |||||||||||

| Managed network sites (at period end) | 3,138 | 4,634 | 5,684 | 7,729 | 9,061 | ||||||

| Retail internet customers (at period end) | 23,205 | 37,122 | 48,995 | 98,690 | 142,208 | ||||||

| Number of full-time, fixed-line employees (at period end)(24) | 49,128 | 43,758 | 39,444 | 35,361 | 32,358 | ||||||

| Fixed lines per fixed-line employee (at period end)(24) | 112 | 113 | 125 | 137 | 149 | ||||||

- (1)

- Includes an offset for discounts offered on mobile-to-fixed interconnect which had previously been included in operating expenses under payments to other operators in the 2003, 2002, 2001 and 2000 financial years. The discounts were R9 million, R11 million, R33 million, R48 million and R50 million, or 1.3%, 1.8%, 5.9%, 9.1% and 10.0% of gross interconnection revenues from domestic mobile operators for the years ended March 31, 2004, 2003, 2002, 2001 and 2000, respectively. Includes an offset for discounts on leased line facilities to mobile operators which had previously been included in operating expenses under payments to other operators in the 2003, 2002, 2001 and 2000 financial years. The discounts were R77 million, R82 million, R77 million, R61 million and R48 million, or 7.8%, 8.1%, 9.2%, 8.7% and 8.2% of leased line facilities rental from mobile operators for the years ended March 31, 2004, 2003, 2002, 2001 and 2000, respectively. Revenue for the 2003, 2002, 2001 and 2000 financial years has been revised to reflect the new presentation.

- (2)

- Other income includes profit and losses on disposal of investments and property, plant and equipment.

- (3)

- Employee expenses include retrenchment costs of R302 million, R244 million, R373 million, R132 million and R303 million in the years ended March 31, 2004, 2003, 2002, 2001 and 2000, respectively.

- (4)

- Discounts offered on mobile-to-fixed interconnect of R9 million, R11 million, R33 million, R48 million and R50 million in the 2004, 2003, 2002, 2001 and 2000 financial years, respectively, and discounts on leased line facilities to mobile operators of R77 million, R82 million, R77 million, R61 million and R48 million in the 2004, 2003, 2002, 2001 and 2000 financial years, respectively, were reclassified from payments to other operators in operating expenses to an offset to operating revenue in the 2004 financial year. Payments to other operators for the 2003, 2002, 2001 and 2000 financial years have been revised to reflect the new presentation.

5

- (5)

- Selling, general and administrative expense includes provisions for potential liabilities related to Telkom's arbitration with Telcordia of R325 million in the year ended March 31, 2002, excluding interest and legal fees. In the year ended March 31, 2003, we recorded a R117 million gain related to this provision in terms of IAS21 and IAS39 in finance charges as a result of the strengthening of the Rand. In addition, we included provisions for interest of R40 million and R50 million related to Telcordia in finance charges in the years ended March 31, 2003 and 2002, respectively, and a provision for legal fees of R58 million related to Telcordia is included in services rendered in the year ended March 31, 2003. In the year ended March 31, 2004, all of these provisions were reversed.

- (6)

- Costs in respect of asset write-offs of R350 million, R205 million, R445 million, R279 million and R0 million in the 2004, 2003, 2002, 2001 and 2000 financial years, respectively, were reclassified from selling, general and administrative expenses to depreciation, amortization, impairments and asset write-offs in the 2004 financial year. Selling, general and administrative expenses and depreciation, amortization, impairments and asset write-offs for the 2003, 2002 and 2001 financial years have been revised to reflect the new presentation.

- (7)

- Costs in respect of losses on the disposal of property, plant and equipment and investments of R6 million, R1 million, R1 million, R14 million and R9 million in the 2004, 2003, 2002, 2001 and 2000 financial years, respectively, were reclassified from selling, general and administrative expenses to other income in the 2004 financial year. Selling, general and administrative expenses and other income have been revised to reflect the new presentation.

- (8)

- Insurance costs paid to Debis for our vehicle fleet of R81 million, R81 million, R78 million and R65 million in the 2004, 2003, 2002, and 2001 financial years, respectively, were reclassified from operating leases to services rendered in the 2004 financial year. Operating leases and services rendered for the 2003, 2002, 2001 and 2000 financial years have been revised to reflect the new presentation.

- (9)

- In the 2004 financial year, Vodacom reclassified its investment in the preference shares of Vodacom Congo (RDC) s.p.r.l. Previously, the investment and short term interest bearing debt of R150.3 million and R215.8 million in the 2003 and 2002 financial years, respectively, were netted off. Vodacom has revised its presentation to move the liabilities associated with its investment to short term debt. Non-current assets and short term debt for the 2003 and 2002 financial years have been revised to reflect the new presentation.

- (10)

- Short-term investments of R29 million were reclassified from non-current assets to current assets in the year ended March 31, 2002.

- (11)

- As of March 31, 2004, R3.9 billion of our long-term debt was guaranteed by the Government of the Republic of South Africa.

- (12)

- Long-term provisions for the phantom share scheme of R144 million were reclassified from current liabilities to non-current liabilities in the year ended March 31, 2001.

- (13)

- Telephone rebate provisions of R12 million, R14 million and R11 million were reclassified from non-current to current liabilities in the years ended March 31, 2004, 2003 and 2002, respectively.

- (14)

- Includes short-term portion of finance leases and utilized credit facilities.

- (15)

- Includes long-term portion of finance leases.

- (16)

- Costs of R44 million related to our initial public offering were reclassified from cash flow used in investing activities to cash flow from financing activities in the year ended March 31, 2002.

6

- (17)

- EBITDA can be reconciled to net profit as follows:

| | Year ended March 31, | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | 2000 | 2001 | 2002 | 2003 | 2004 | 2004 | |||||||

| | ZAR | ZAR | ZAR | ZAR | ZAR | USD | |||||||

| | (in millions) | ||||||||||||

| EBITDA | 8,082 | 10,315 | 10,044 | 13,012 | 16,337 | 2,585 | |||||||

| Depreciation, amortization, impairments and write-offs | (4,174 | ) | (5,331 | ) | (5,853 | ) | (6,498 | ) | (7,249 | ) | (1,147 | ) | |

| Investment income | 615 | 558 | 512 | 424 | 479 | 75 | |||||||

| Finance charges | (2,482 | ) | (3,137 | ) | (2,550 | ) | (4,154 | ) | (3,264 | ) | (516 | ) | |

| Taxation | (501 | ) | (715 | ) | (873 | ) | (1,049 | ) | (1,711 | ) | (271 | ) | |

| Minority interests | (13 | ) | (68 | ) | (59 | ) | (105 | ) | (69 | ) | (11 | ) | |

| Net Profit | 1,527 | 1,622 | 1,221 | 1,630 | 4,523 | 715 | |||||||

- (18)

- Includes short-term and long-term debt, finance lease obligations and utilized credit facilities.

- (19)

- Including Telkom internal lines of 140,950, 134,972, 162,460, 151,986 and 145,302 as of March 31, 2004, 2003, 2002, 2001 and 2000, respectively. Each PSTN line includes one access channel, each basic ISDN line includes two access channels and each primary ISDN line includes 30 access channels.

- (20)

- Excluding ISDN channels. PSTN lines are provided using copper cable, DECT and fiber.

- (21)

- Includes public and private payphones.

- (22)

- In the 2003 financial year, we revised the calculation of the weighted average tariffs for certain prepaid calls and our ShareCall product. We have recalculated the traffic for the 2002 and 2001 financial years accordingly. Calculated on the original basis, local traffic was 20,252 and 20,388 millions of minutes, long-distance traffic was 4,895 and 4,938 millions of minutes, fixed-to-mobile traffic was 4,390 and 4,319 millions of minutes, international outgoing traffic was 375 and 357 millions of minutes and total traffic was 32,973 and 32,915 millions of minutes in the 2002 and 2001 financial years, respectively.

- (23)

- Local traffic includes internet traffic.

- (24)

- Includes employees of Telkom only.

7

SELECTED HISTORICAL CONSOLIDATED FINANCIAL

AND OTHER DATA OF VODACOM GROUP

The following table sets forth selected consolidated financial and other data of Vodacom as of and for each of the five years ended March 31, 2004. Information in the Vodacom table reflects 100% of Vodacom's results of operations. Unless otherwise indicated, information with respect to Vodacom's other African operations in the Vodacom table reflects 100% of the operations of Vodacom's subsidiaries in Lesotho, Tanzania and Mozambique and 51% of Vodacom's joint venture in the Democratic Republic of the Congo that is proportionately consolidated in Vodacom's consolidated financial statements. We proportionately consolidate our 50% interest in Vodacom in the Telkom Group's consolidated financial statements. Vodacom's other operating income, direct network operating costs, depreciation, staff expenses, marketing and advertising expenses, general administration expenses, amortization of intangible assets and integration costs, disposal of operations and impairments are presented as separate line items in Vodacom's consolidated financial statements, but have been combined under the heading "operating expenses" in the table set forth below.

The following selected historical consolidated financial data of Vodacom as of and for each of the three years ended March 31, 2004 have been extracted from Vodacom's historical consolidated financial statements included in this annual report, which were audited by Deloitte & Touche Registered Accountants and Auditors, Chartered Accountants (SA) in the 2004 financial year and were audited by each of PricewaterhouseCoopers, Inc. and Deloitte & Touche, Registered Accountants and Auditors, Chartered Accountants (SA) in the 2003 and 2002 financial years. The following selected historical consolidated financial data of Vodacom as of and for each of the two years ended March 31, 2001 have been extracted from Vodacom's historical consolidated financial statements not included in this annual report, which were also audited by PricewaterhouseCoopers, Inc. and Deloitte & Touche, Registered Accountants and Auditors, Chartered Accountants (SA).

The consolidated financial statements of Vodacom have been prepared in accordance with IFRS, which differs in certain respects from US GAAP. For a description of the principal differences between IFRS and US GAAP relevant to the financial statements of Vodacom and a reconciliation to US GAAP of net income and shareholders' equity, see note 48 of the notes to the audited consolidated financial statements of Vodacom as of and for each of the three years ended March 31, 2004 included in this annual report.

EBITDA represents net profit before minority interests, taxation, finance charges, investment income and depreciation and amortization. We believe that EBITDA provides meaningful additional information to investors since it is widely accepted by analysts and investors as a basis for comparing a company's underlying operating profitability with that of other companies as it is not influenced by past capital expenditures or business acquisitions, a company's capital structure or the relevant tax regime. This is particularly the case in a capital-intensive industry such as communications. It is also a widely accepted indicator of a company's ability to service its long-term debt and other fixed obligations and to fund its continued growth. EBITDA is not a US GAAP or IFRS measure. You should not construe EBITDA as an alternative to operating profit or cash flows from operating activities determined in accordance with US GAAP or IFRS or as a measure of liquidity. EBITDA is not defined in the same manner by all companies and may not be comparable to other similarly titled measures of other companies unless the definition is the same.

Vodacom's customer totals are based on the total number of customers registered on Vodacom's network, which have not been disconnected, including inactive customers, as of the end of the period indicated. See Item 4. "Information on the Company—Business Overview—Mobile Communications—South Africa—Customers" for a discussion of Vodacom's procedures with respect to disconnections and inactive customers. Vodacom's churn is calculated by dividing the average monthly number of disconnections during the period by the average monthly total reported customer base during the

8

period. Vodacom's market share is derived from Vodacom's total customers, MTN's total reported mobile subscribers and Cell C's total estimated mobile subscribers. Vodacom calculates penetration, or teledensity, based on the total number of customers at the end of the period per 100 persons in the population of South Africa. Population is the estimated South African population at the mid-year in the periods indicated as published by Statistics South Africa, a South African governmental department. Vodacom's traffic comprises total traffic registered on Vodacom's network, including bundled minutes, outgoing international roaming calls and calls to free services, but excluding national and incoming international roaming calls. Vodacom's average monthly revenue per customer, or ARPU, is calculated by dividing the average monthly revenue during the period by the average monthly total reported customer base during the period. ARPU excludes revenue from equipment sales, other sales and services and revenue from national and international users roaming on Vodacom's networks. Vodacom's average monthly minutes of use per customer, or average MOU, is calculated by dividing the average monthly minutes during the period by the average monthly total reported customer base during the period. MOU excludes calls to free services, bundled minutes and data minutes. Cumulative network capital expenditure per customer is the cumulative network capital expenditure since the launch of Vodacom's South African network divided by Vodacom's average customers in South Africa for the period.

Rand amounts as of and for the year ended March 31, 2004 have been translated into Dollars solely for your convenience at R6.32 per $1.00, the Rand noon buying rate discussed in Item 3. "Key Information—Exchange Rates," on March 31, 2004, the date of Vodacom's most recent balance sheet included in this annual report. These translations should not be construed as representations that the Rand amounts could actually be converted into US dollars at these rates or at all.

You should read the following information together with Item 3. "Key Information—Risk Factors," Item 5. "Operating and Financial Review and Prospects" and the consolidated financial statements and the notes thereto of the Telkom Group and Vodacom Group included in this annual report.

9

| | Year ended March 31, | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | 2000 | 2001 | 2002 | 2003 | 2004 | 2004 | ||||||||

| | ZAR | ZAR | ZAR | ZAR | ZAR | USD | ||||||||

| | (in millions) | |||||||||||||

| Income Statement Data | ||||||||||||||

| Amounts in accordance with IFRS | ||||||||||||||

Revenue | 9,572 | 13,276 | 16,151 | 19,779 | 23,478 | 3,715 | ||||||||

| Operating expenses(1) | (7,208 | ) | (10,723 | ) | (12,530 | ) | (15,449 | ) | (18,244 | ) | (2,887 | ) | ||

| Operating profit | 2,364 | 2,553 | 3,621 | 4,330 | 5,234 | 828 | ||||||||

| Investment income(2) | 32 | 28 | 840 | 742 | 657 | 104 | ||||||||

| Finance charges(2) | (567 | ) | (507 | ) | (868 | ) | (1,546 | ) | (1,108 | ) | (175 | ) | ||

| Profit before tax | 1,829 | 2,074 | 3,593 | 3,526 | 4,783 | 757 | ||||||||

| Taxation | (514 | ) | (765 | ) | (1,190 | ) | (1,199 | ) | (1,725 | ) | (273 | ) | ||

| Profit after tax | 1,315 | 1,309 | 2,403 | 2,327 | 3,058 | 484 | ||||||||

| Minority interests | — | 9 | (30 | ) | (112 | ) | (26 | ) | (4 | ) | ||||

| Net profit | 1,315 | 1,318 | 2,373 | 2,215 | 3,032 | 480 | ||||||||

Amounts in accordance with US GAAP | ||||||||||||||

Net profit for the year | n/a | 1,249 | 2,120 | 2,099 | 2,997 | 474 | ||||||||

As of March 31, | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | 2000 | 2001 | 2002 | 2003 | 2004 | 2004 | |||||||

| | ZAR | ZAR | ZAR | ZAR | ZAR | USD | |||||||

| | (in millions) | ||||||||||||

| Balance Sheet Data | |||||||||||||

| Amounts in accordance with IFRS | |||||||||||||

Total assets(3) | 9,864 | 12,342 | 15,574 | 16,966 | 20,098 | 3,180 | |||||||

| Current assets | 2,788 | 3,470 | 4,145 | 4,690 | 6,904 | 1,092 | |||||||

| Cash and cash equivalents | 936 | 798 | 719 | 1,207 | 2,370 | 375 | |||||||

| Other current assets | 1,852 | 2,672 | 3,426 | 3,483 | 4,534 | 717 | |||||||

| Non-current assets(3) | 7,076 | 8,872 | 11,429 | 12,276 | 13,194 | 2,088 | |||||||

| Total liabilities(3) | 7,195 | 8,847 | 10,099 | 10,041 | 12,402 | 1,962 | |||||||

| Current liabilities(3) | 5,883 | 7,267 | 8,205 | 7,159 | 9,833 | 1,556 | |||||||

| Short-term debt(3)(4) | 3,370 | 2,547 | 3,732 | 1,919 | 1,616 | 256 | |||||||

| Other current liabilities | 2,513 | 4,720 | 4,473 | 5,240 | 8,217 | 1,300 | |||||||

| Non-current liabilities | 1,312 | 1,580 | 1,894 | 2,882 | 2,569 | 406 | |||||||

| Long-term debt(5) | 817 | 896 | 780 | 1,732 | 1,217 | 192 | |||||||

| Other non-current liabilities | 495 | 684 | 1,114 | 1,150 | 1,352 | 214 | |||||||

| Minority interests | (2 | ) | (11 | ) | 11 | 88 | 93 | 15 | |||||

| Shareholders' equity | 2,671 | 3,506 | 5,464 | 6,837 | 7,603 | 1,203 | |||||||

Amounts in accordance with US GAAP | |||||||||||||

Shareholders' equity | n/a | 3,195 | 4,874 | 6,086 | 6,788 | 1,074 | |||||||

10

| | Year ended March 31, | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | 2000 | 2001 | 2002 | 2003 | 2004 | 2004 | ||||||||

| | ZAR | ZAR | ZAR | ZAR | ZAR | USD | ||||||||

| | (in millions) | |||||||||||||

| Cash Flow Data | ||||||||||||||

| Amounts in accordance with IFRS | ||||||||||||||

| Cash flow from operating activities | 2,341 | 3,610 | 3,815 | 4,342 | 4,790 | 758 | ||||||||

| Cash flow used in investing activities | (3,338 | ) | (2,853 | ) | (4,543 | ) | (3,243 | ) | (3,000 | ) | (475 | ) | ||

| Cash flow from (used in) financing activities | 646 | (1,038 | ) | 571 | 518 | (798 | ) | (126 | ) | |||||

Other Data | ||||||||||||||

| EBITDA(6) | 3,462 | 4,189 | 5,691 | 6,704 | 7,767 | 1,229 | ||||||||

| Total debt (at period end)(7) | 4,187 | 3,443 | 4,513 | 3,652 | 2,833 | 448 | ||||||||

| Capital expenditures including intangibles | 2,032 | 3,184 | 4,279 | 3,399 | 3,012 | 477 | ||||||||

| South Africa | 2,011 | 2,830 | 3,291 | 2,488 | 1,666 | 264 | ||||||||

| Other African countries | 21 | 354 | 988 | 911 | 1,346 | 213 | ||||||||

| | Year ended March 31, | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| | 2000 | 2001 | 2002 | 2003 | 2004 | ||||||

| Statistical Data | |||||||||||

| South Africa | |||||||||||

| Total mobile customers (thousands) (at period end)(8) | 3,069 | 5,108 | 6,557 | 7,874 | 9,725 | ||||||

| Contract | 963 | 1,037 | 1,090 | 1,181 | 1,420 | ||||||

| Prepaid | 2,082 | 4,046 | 5,439 | 6,664 | 8,282 | ||||||

| Community services telephones | 24 | 25 | 28 | 29 | 23 | ||||||

| Total inactive mobile customers (%) (at period end)(9) | n/a | n/a | 13.9 | 18.2 | 17.6 | ||||||

| Contract | n/a | n/a | 3.8 | 5.3 | 5.7 | ||||||

| Prepaid | n/a | n/a | 15.9 | 20.5 | 19.7 | ||||||

| Mobile churn (%)(10) | 31.8 | 23.3 | 27.2 | 30.4 | 36.6 | ||||||

| Contract | 17.4 | 18.7 | 14.5 | 11.9 | 10.1 | ||||||

| Prepaid | 40.5 | 24.8 | 30.1 | 34.0 | 41.3 | ||||||

| Mobile market share (%) (at period end) | 59 | 61 | 61 | 57 | 54 | ||||||

| Mobile penetration (%) (at period end) | 12.1 | 19.1 | 24.2 | 30.2 | 39.0 | ||||||

| Total mobile traffic (millions of minutes) | 5,669 | 7,472 | 8,881 | 10,486 | 12,297 | ||||||

| Outgoing | 2,885 | 4,052 | 4,967 | 6,343 | 7,772 | ||||||

| Incoming | 2,784 | 3,420 | 3,914 | 4,143 | 4,525 | ||||||

| Mobile ARPU (ZAR)(11) | 266 | 208 | 182 | 183 | 177 | ||||||

| Contract(10) | 481 | 493 | 560 | 629 | 634 | ||||||

| Prepaid | 132 | 98 | 93 | 90 | 90 | ||||||

| Community services | n/a | 1,453 | 1,719 | 1,861 | 2,155 | ||||||

| Average MOU | 158 | 137 | 111 | 101 | 96 | ||||||

| Contract | 274 | 270 | 264 | 269 | 263 | ||||||

| Prepaid | 90 | 70 | 58 | 54 | 56 | ||||||

| Community services | 1,593 | 2,859 | 3,354 | 3,162 | 3,061 | ||||||

| Cumulative network capital expenditure per customer (ZAR) (at period end) | 2,543 | 2,053 | 1,991 | 1,933 | 1,720 | ||||||

| Number of mobile employees (at period end)(12) | 4,048 | 4,102 | 3,859 | 3,904 | 3,848 | ||||||

| Number of mobile customers per mobile employee (at period end)(12) | 758 | 1,245 | 1,699 | 2,017 | 2,527 | ||||||

11

Other African countries | |||||||||||

| Number of mobile customers (thousands) (at period end)(13) | 12 | 104 | 306 | 773 | 1,492 | ||||||

| ARPU | |||||||||||

| Lesotho (ZAR) | n/a | n/a | 144 | 104 | 125 | ||||||

| Tanzania (USD) | n/a | 31 | 27 | 22 | 18 | ||||||

| Democratic Republic of the Congo (USD) | n/a | n/a | n/a | 20 | 21 | ||||||

| Mozambique (USD) | n/a | n/a | n/a | n/a | 15 | ||||||

| Number of mobile employees (at period end)(12) | 43 | 170 | 494 | 502 | 761 | ||||||

| Number of mobile customers per mobile employee (at period end)(12)(13) | 279 | 612 | 619 | 1,540 | 1,961 | ||||||

- (1)

- Includes other income of R57.6 million, R68.0 million, R29.2 million, R48.5 million and R14.5 million in the years ended March 31, 2004, 2003, 2002, 2001 and 2000, respectively.

- (2)

- Foreign exchange related items were reclassified between investment income and finance charges in the 2001 and 2002 financial years.

- (3)

- In the 2004 financial year, Vodacom reclassified its investment in the preference shares of Vodacom Congo (RDC) s.p.r.l. Previously, the investment and short term interest bearing debt of R150.3 million and R215.8 million in the 2003 and 2002 financial years, respectively, were netted off. Vodacom has revised its presentation to move the liabilities associated with its investment to short term debt. Non-current assets and short term debt for the 2003 and 2002 financial years have been revised to reflect the new presentation.

- (4)

- Includes short-term portion of finance leases, shareholder loans and non-interest bearing debt, as well as utilized credit facilities.

- (5)

- Includes long-term portion of finance leases.

- (6)

- EBITDA includes a net gain of R56 million, a net loss of R213 million and a net gain of R129 million in the 2002, 2001 and 2000 financial years, respectively, for integration costs, disposals of operations and impairments.

EBITDA can be reconciled to net profit as follows:

| | Year ended March 31, | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | 2000 | 2001 | 2002 | 2003 | 2004 | 2004 | ||||||||

| | ZAR | ZAR | ZAR | ZAR | ZAR | USD | ||||||||

| | (in millions) | |||||||||||||

| EBITDA | 3,462 | 4,189 | 5,691 | 6,704 | 7,767 | 1,229 | ||||||||

| Depreciation, amortization, impairments and asset write-offs | (1,098 | ) | (1,636 | ) | (2,070 | ) | (2,374 | ) | (2,533 | ) | (401 | ) | ||

| Investment income | 32 | 28 | 840 | 742 | 657 | 104 | ||||||||

| Finance charges | (567 | ) | (507 | ) | (868 | ) | (1,546 | ) | (1,108 | ) | (175 | ) | ||

| Taxation | (514 | ) | (765 | ) | (1,190 | ) | (1,199 | ) | (1,725 | ) | (273 | ) | ||

| Minority interests | 0 | 9 | (30 | ) | (112 | ) | (26 | ) | (4 | ) | ||||

| Net profit | 1,315 | 1,318 | 2,373 | 2,215 | 3,032 | 480 | ||||||||

- (7)

- Includes interest-bearing and non-interest bearing debt, shareholder loans and utilized credit facilities.

- (8)

- Includes inactive customers.

12

- (9)

- Vodacom's inactive customers are defined as all customers registered on Vodacom's network for which no revenue generating activity has been recorded for a period of three consecutive months.

- (10)

- Vodacom's contract customers are disconnected when they terminate their contract, or their service provider who carries the credit risk terminates their contract due to non-payment. Prepaid customers were disconnected if they did not recharge their vouchers after being in time window lock for six months for periods prior to November and December 2002, for four months for periods from November and December 2002 until April 2003 and for three months from April 2003 until December 2003. Time window lock occurs when a customer's paid active time window, or access period expires. In December 2003, Vodacom changed the deactivation rule for prepaid customers to align itself with European and industry standards. From December 2003, prepaid customers are disconnected from its network if they record no revenue generating activity within a period of 215 consecutive days. See "Item 4. "Information on the Company—Business Overview—Mobile communications—South Africa—Customers."

- (11)

- Value added service revenue from previously partially owned service providers is included in contract and total average monthly revenue per customer from October 1, 2001.

- (12)

- Vodacom had a total of 280, 219, 423, 553 and 96 temporary employees as of March 31, 2004, 2003, 2002, 2001 and 2000, respectively. The calculation of total mobile employees between South Africa and other African countries has been restated from 3,984 and 369, respectively, in the year ended March 31, 2002. Includes 100% of Vodacom's employees in the Democratic Republic of the Congo.

- (13)

- Includes 100% of mobile customers in the Democratic Republic of the Congo.

13

All of Telkom's issued and outstanding ordinary shares, including the class A ordinary share and the class B ordinary share, rank equal for dividends. No dividend may be declared to a holder of the class A ordinary share or class B ordinary share, unless the same dividend is declared to holders of all ordinary shares. The following table sets forth information with respect to the annual dividends declared. Dividends per ordinary share are based on 557,031,819 ordinary shares issued and outstanding, which includes the one class A ordinary share and the one class B ordinary share created on March 4, 2003 by the conversion of the two ordinary shares. Annual dividends are expressed in Rands and translated, solely for the convenience of the reader, into Dollars at the Rand noon buying rate described in Item 3. "Key Information—Exchange Rates" below on the relevant dividend payment date. The actual rate that cash dividends are converted to Dollars by the depositary may not equal the Rand noon buying rate on the dividend payment date.

| | Dividends paid per Ordinary Share | Dividends paid per ADS | Total dividends (millions) | Dividend cover(1) | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Year ended March 31, | SA Cents | US Cents | ZAR | US Cents | ZAR | USD | ||||||||

| 2004(2) | 90 | 14.2 | 3.60 | 57.0 | 501.3 | 79.3 | 9.0x | |||||||

| 2003 | — | — | — | — | — | — | n/a | |||||||

| 2002 | — | — | — | — | — | — | n/a | |||||||

| 2001 | — | — | — | — | — | — | n/a | |||||||

| 2000 | 59.6 | 9.7 | n/a | n/a | 331.7 | 53.9 | 4.6x | |||||||

- (1)

- Dividend cover is calculated by dividing net profit for the year after minority interest by the dividend for the year.

- (2)

- The 2004 financial year Interim dividend No.8 of 90 SA Cents per share was paid on December 29, 2003. As of March 31, 2004, we had 3,185,736 of the 557,031,819 issued shares held in treasury.

On June 3, 2004, Telkom's board of directors declared a 2004 financial year final dividend No. 9 of 110 SA cents per share to be paid on July 9, 2004.

Dividends paid by Telkom prior to listing on the JSE Securities Exchange, South Africa and the New York Stock Exchange, or NYSE, reflected its status as being majority-owned by the Government of the Republic of South Africa and should not be considered indicative of Telkom's ability to pay future dividends. Telkom did not declare any dividends in the three years ended March 31, 2003 in order to repay debt and reinvest profits in its fixed-line network modernization, rehabilitation and line-rollout program.

We cannot assure you that any dividend will actually be paid or what the timing or amount of any future dividends will be. Telkom's current dividend policy aims to provide shareholders with a competitive return on their investment, while assuring sufficient reinvestment of profits to enable us to achieve our strategy. Telkom may revise its dividend policy from time to time. The determination to pay dividends, and the amount of the dividends, will depend upon, among other things, the following:

- •

- our earnings;

- •

- our financial condition;

- •

- our capital requirements;

- •

- the impact of currency exchange rate and inflation fluctuations;

- •

- general business conditions and strategies;

14

- •

- contractual restrictions on the payment of dividends;

- •

- the possible effects on our credit worthiness;

- •

- the pay-out and dividend ratios of other major South African companies and other communications providers;

- •

- dividends received from Vodacom; and

- •

- other factors our board of directors may deem relevant, including future growth prospects.

Under South African law, a company may make payments to its shareholders if authorized thereto by its organizational documents. A company may not make any payment, in whatever form, to its shareholders if there are reasonable grounds for believing that:

- •

- the company is or would, after the payment, be unable to pay its debts as they become due in the ordinary course of business; or

- •

- the consolidated assets of the company fairly valued, after the payment, would be less than the consolidated liabilities of the company.

Under South African law, a shareholder is liable to a company for any payments received by the shareholder from the company in violation of these restrictions.

Pursuant to Telkom's memorandum and articles of association, for so long as either the Government of the Republic of South Africa or Thintana Communications is a significant shareholder, Telkom's dividend policy and all declarations of dividends and payments to shareholders will have to be approved by the directors appointed by the Government and Thintana Communications. Pursuant to Telkom's memorandum and articles of association and the shareholders' agreement, a significant shareholder is a shareholder who holds the class A ordinary share or class B ordinary share in the capital of Telkom and at least 15% of Telkom's issued ordinary shares. This percentage will be reduced from time to time to reflect the dilutive effect of issuances of new ordinary shares, but may not be less than 10%. Furthermore, in the shareholders' agreement, the Government and Thintana Communications have agreed to vote their shares together in relation to the declaration and payment of dividends.

Telkom's ability to make future dividend payments will be determined based upon its financial position under IFRS. The following table sets forth a reconciliation of retained earnings in accordance with IFRS to distributable reserves in accordance with IFRS for the periods indicated.

| | Year ended March 31, | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| | 2002 | 2003 | 2004 | 2004 | |||||

| | ZAR | ZAR | ZAR | USD | |||||

| | (in millions) | ||||||||

| Retained earnings in accordance with IFRS | 8,449 | 10,066 | 13,899 | 2,199 | |||||

| Share of non-distributable retained earnings in Vodacom | (2,678 | ) | (3,485 | ) | (3,951 | ) | (625 | ) | |

| Distributable reserves in accordance with IFRS | 5,771 | 6,581 | 9,948 | 1,574 | |||||

The distribution of retained earnings of Vodacom are restricted, as Telkom requires the consent of the other shareholders of Vodacom to declare dividends. As described in Item 10. "Additional Information—Taxation," Telkom is required to pay secondary tax on companies at a flat rate of 12.5% in respect of the amount of certain dividends declared by it net of any dividends received from our joint venture and subsidiaries. As a result of the payment of secondary tax on companies, the amount of dividends that may actually be paid is less than the amount of distributable reserves. Distributable reserves are available for distribution based on Telkom's dividend policy. Telkom's board of directors decides on an annual basis the amount of distributable reserves to be reinvested in operations and the amount of any remaining funds that are available for distribution to shareholders.

15

Telkom expects to pay any cash dividends solely in Rands. Cash dividends payable to holders of American Depository Shares, or ADSs, listed on the New York Stock Exchange will be paid to the depositary's custodian, which will convert the dividends into Dollars, at the rate of exchange applicable on the date such dividends are paid, for disbursement to holders. Fluctuations in the exchange rate between Rands and Dollars and expenses of the depositary will affect the Dollar amounts actually received by holders of ADSs upon conversion by the depositary of such cash dividends.

Provided that the relevant share certificate is endorsed "non-resident" or an entry is made to such effect in the relevant electronic register, there is currently a blanket approval under the South African exchange control regulations for the free transferability of cash dividends to holders of ordinary shares or ADSs. See Item 10. "Additional Information—Exchange Controls."

In addition to the corporate tax on taxable income of South African companies at the current rate of 30%, South African companies pay secondary tax on companies as described above. Capitalization shares or stock dividends distributed to holders of ordinary shares do not incur secondary tax on companies. Because of this tax treatment, it has become common practice in South Africa for companies to offer capitalization shares in lieu of cash dividends. Capitalization shares are shares issued by a company, the payment for which is allocated out of the company's reserves, including share premium, or unappropriated profits.

For a discussion of the material South African and US federal income tax provisions regarding the taxation of dividends on ordinary shares and ADSs, see Item 10. "Additional Information—Taxation."

Shares Repurchases

As authorized by its shareholders at an annual general meeting held on January 27, 2004, Telkom embarked on a share repurchase program for purposes of the Telkom conditional share plan.

In the year ended March 31, 2004, Rossol No 65 (Proprietary) Limited, a wholly-owned subsidiary of Telkom, repurchased 3,185,736 shares at a volume weighted averaged price of R74.58 per share, including costs, which are being held in treasury. On June 4, 2004, Telkom purchased Acajou (Pty) Limited for share repurchase activities other than repurchases for the Telkom conditional share plan. Between June 7, 2004 and June 21, 2004, Acajou (Pty) Limited purchased 2,337,000 shares at a volume weighted average price of R76.88 per share, including costs, which are also being held in treasury.

In terms of the South African Companies Act, 61 of 1973, a subsidiary company may not acquire more than 10% of the shares in its holding company.

Telkom plans on continuing its buy back strategy based on certain criteria.

Taxation

A share repurchase and subsequent cancellation of shares by a South African company is deemed to be a dividend in terms of the South African Income Tax Act, 58 of 1962, on the difference between the nominal value of the share and the value purchased, unless purchased from the share premium of the company that does not comprise capitalized profit. The tax on such a deemed dividend is payable by the company at a rate of 12.5%.

16

Unless otherwise specified, as used in this annual report:

- •

- references to "Rand," "R," "ZAR" and "SA Cents" are to South African Rand and Cents, the currency of the Republic of South Africa;

- •

- references to "Dollars," "$," "USD" and "US Cents" are to the United States Dollar and Cents, the currency of the United States; and

- •

- references to the "Rand noon buying rate" are to the noon buying rates in New York City for cable transfers in Rands as certified for customs purposes by the US Federal Reserve Bank of New York expressed in Rands per $1.00.

For your convenience, this annual report contains translations of certain Rand amounts into Dollars. You should not assume, however, that Rands could have been exchanged into Dollars at any particular rate or at all. Unless otherwise stated, translations of Rand amounts into Dollars have been made at R6.32 per $1.00, the Rand noon buying rate on March 31, 2004, the date of the Telkom Group's most recent balance sheet included in this annual report. These translations should not be construed as representations that the Rand amounts could actually be converted into US dollars at these rates or at all.

The table below shows the high, low, average and end of period Rand noon buying rates for the periods indicated. The end of period Rand noon buying rate is computed on the last business day of the relevant period and the average Rand noon buying rate is computed using the Rand noon buying rate on the last business day of each month during the period indicated for financial years and the average of the month for months.

| Year ended March 31, | High | Low | Average | End of period | ||||

|---|---|---|---|---|---|---|---|---|

| 2000 | 6.58 | 5.98 | 6.19 | 6.54 | ||||

2001 | 8.04 | 6.56 | 7.34 | 8.04 | ||||

2002 | 13.60 | 7.91 | 9.64 | 11.38 | ||||

2003 | 11.36 | 7.90 | 9.74 | 7.90 | ||||

2004 | 8.24 | 6.26 | 7.17 | 6.32 |

Year 2003 | High | Low | ||

|---|---|---|---|---|

| December | 6.94 | 6.26 |

Year 2004 | High | Low | ||

|---|---|---|---|---|

| January | 7.31 | 6.36 | ||

February | 7.07 | 6.57 | ||

March | 6.92 | 6.32 | ||

April | 6.94 | 6.27 | ||

May | 7.05 | 6.52 | ||

June (through June 18, 2004) | 6.64 | 6.40 |

On June 18, 2004, the Rand noon buying rate was R6.40 per $1.00.

Fluctuations in the exchange rate between the Rand and the Dollar will affect the Dollar amounts received by holders of American Depositary Shares, or ADSs, each representing four ordinary shares of Telkom, on conversion of dividends, if any, paid in Rands on the ordinary shares and may affect the Dollar trading price of the ADSs on the New York Stock Exchange.

17

You should carefully consider the risks described below in conjunction with the other information and the consolidated financial statements of the Telkom Group and Vodacom and the related notes thereto included elsewhere in this annual report before making an investment decision with respect to Telkom's ordinary shares or ADSs.

Risks Related to our Business

Increased competition in the South African telecommunications market may result in a reduction in overall average tariffs and market share in our fixed-line business, which could cause our growth rates, operating revenue and net profit to decline.

Telkom had the exclusive right to provide public switched telecommunications services, including international telephone services, in the Republic of South Africa until May 7, 2002, but for a number of years has competed with mobile operators and value-added network operators in connection with the provision of other services. The Independent Communications Authority of South Africa, or ICASA, issued an international carrier of carriers license and a multimedia license to Sentech Limited, formerly known as Sentech (Proprietary) Limited and referred to herein as Sentech, in May 2002. In addition, on December 18, 2003, the Minister of Communications announced that she would grant an additional license to provide public switched telecommunications services to a second national operator that will be 30% owned by two entities beneficially owned by the South African Government, 19% owned by a black economic empowerment consortium and 26% owned by two other consortiums, with the remaining 25% of the second national operator being held by the Government for sale to a strategic equity investor to be identified. The Minister of Communications has indicated that she expects ICASA to issue the second public switched telecommunications services license in 2004. A process has also commenced to issue additional licenses to small business operators to provide telecommunications services in areas with a teledensity of less than 5%. ICASA has submitted its recommendations to the Minister of Communications for the granting of licenses to successful bidders in seven of the ten areas in which licenses could have been issued. The Minister of Communications has granted licenses to four successful bidders on June 3, 2004 and it is expected that these licenses will be issued in 2004. Further competition may arise as a result of an assessment by the Minister of Communications of the feasibility of issuing additional licenses from May 2005. As competition intensifies, the main challenges our fixed-line business faces are continuing to improve customer loyalty and maintaining its leadership in the South African communications market. As a result of increasing competition, we anticipate a reduction in overall average tariffs and market share in our fixed-line business, which could cause our growth rates, operating revenue and net profit to decline.

Competition from the three existing mobile communications network operators in South Africa has resulted in significant customer migration and call substitution from fixed-line to mobile services. If this customer migration and call substitution continues, our growth rates, operating revenue and net profit could decline.

Telkom competes with the three existing mobile communications network operators, Vodacom, Mobile Telephone Network Holdings (Proprietary) Limited, or MTN, and Cell C (Proprietary) Limited or Cell C, for customers. Telkom also competes with other service providers who use least cost routing technology that enables fixed-to-mobile calls from corporate private branch exchanges to bypass our fixed-line network by being transferred directly to mobile networks. Telkom has experienced significant customer migration in recent years from fixed-line services to mobile services, as well as substitution of calls placed using mobile services rather than our fixed-line service, with the increase in mobile penetration in South Africa. If this migration continues, our growth rates, operating revenue and net profit could decline.

18

The rapid growth in the mobile market in South Africa has resulted in a significant increase in the number of Vodacom and Telkom calls terminating on other mobile networks as opposed to our fixed-line network. Vodacom's and Telkom's margins and net profit could decline if this trend continues.

Vodacom and Telkom have experienced a significant change in the traffic mix as mobile customers increased relative to fixed-line customers. This resulted in an increasing percentage of calls from Vodacom's network and our fixed-line network terminating on other mobile networks rather than our fixed-line network. Vodacom's interconnection payments have increased and its margins have decreased because the cost of terminating calls on other mobile networks is higher than the cost of terminating calls on Telkom's fixed-line network. As a result, Vodacom's South African net interconnect revenue has been declining in recent years. Similarly, Telkom has incurred increased payments to other operators as a result of the growth in interconnection traffic for fixed-line calls terminating on other mobile networks. If mobile customers continue to increase and there is little or no growth in fixed-line customers, this trend could continue and Vodacom's and Telkom's margins and net profit could decline.

Increased competition in the mobile communications market in South Africa may result in a reduction of Vodacom's average tariffs and Vodacom's market share and increased customer acquisition and retention costs, which could cause Vodacom's growth rates, revenue and net profit to decline.

There are currently three operators in the South African mobile communications market, Vodacom, MTN and Cell C. At March 31, 2004, Vodacom estimates that it held approximately 54%, MTN held approximately 35% and Cell C held approximately 11% of the South African mobile communications market, based on total estimated customers. Increased competition from Cell C in 2004 has resulted in an estimated 3% decline in market share for Vodacom. In addition, ICASA has indicated that it intends to license global mobile personal communications services by satellite and to conduct a feasibility study on the licensing of a fourth mobile operator in 2004 or later. This increased competition, together with the further liberalization of the South African telecommunications industry, may result in a reduction in Vodacom's overall average tariffs and further loss of market share and increased customer acquisition and retention costs, which could cause Vodacom's growth rates, revenue and net profit to decline.

If we are not able to implement a reduction in our existing fixed-line employees and employee expenses or if significant labor unrest results from the implementation of our fixed-line employee reduction program, our ability to compete may be harmed and our net profit could decline.

The number of our fixed-line employees of Telkom declined by approximately 24,453 positions from March 31, 1997 through March 31, 2004. We intend to continue to reduce our fixed-line headcount over the next few years. Our ability to implement optimal employee reductions is limited by South African labor laws. In addition, legal requirements make such reductions costly. We also face pressure from labor unions in South Africa who oppose employee reductions and may encounter resistance from the Government of the Republic of South Africa if the reductions conflict with the Government's social objectives at the time. If we are unable to reduce the number of our fixed-line employees and employee expenses or if significant labor unrest results from implementation of our fixed-line employee reduction program, our ability to compete may be harmed and our net profit could decline.

The value of Vodacom's investments outside of South Africa and Vodacom's revenue and net profit may decline as a result of political, economic, regulatory and legal developments in the countries where Vodacom has invested.

Vodacom currently has investments in mobile communications network operators in Lesotho, Tanzania, the Democratic Republic of the Congo and Mozambique. These countries have political,

19

economic, regulatory and legal systems that are still in the process of transformation and are less developed than those in the Republic of South Africa. Political or economic upheaval or changes in laws and regulations or in their application may harm the operations of the companies in which Vodacom invests and impair the value of these investments. The regulatory environments in these countries often lack clarity in a number of areas and are subject to varying interpretations. These countries, particularly the Democratic Republic of the Congo, suffer from extreme poverty and are experiencing civil strife, political conflict and political mismanagement, all of which could cause the value of Vodacom's investments in these countries and Vodacom's revenue and net profit to decline.

Most of the fixed-line operators in these countries are still state controlled. As a result, the mobile communications network operators in which Vodacom has invested may encounter difficulties in negotiating commercially acceptable interconnection agreements and collecting amounts due under interconnection agreements. In particular, Vodacom Tanzania has been unable to collect approximately $800,000 in outstanding interconnection payments from the Tanzania Telecommunications Company Limited, the partially government owned fixed line operator in Tanzania, and has been forced to refer the matter to formal arbitration, and there have been disagreements regarding the validity of the interconnect agreements in the Democratic Republic of the Congo. The amounts in question have been written-off even though Vodacom Tanzania continues its attempt to collect these debts. In addition, a number of jurisdictions in which Vodacom invests have imposed price controls, particularly for interconnection, which could reduce Vodacom's net profit and cause the value of Vodacom's investments in these other African countries to decline. There are also foreign exchange control restrictions in South Africa, which may restrict Vodacom's ability to fund its investments in these countries, and there are foreign exchange controls in a majority of these countries, which may restrict Vodacom's ability to extract value from these investments.

The number of mobile operators and mobile licenses available for acquisition in other African countries is limited. Moreover, Vodacom's acquisition of mobile operators and licenses in other African countries may be unsuccessful, which could have a material adverse effect on Vodacom's future growth.

A substantial part of Vodacom's future growth is expected to be from acquisitions of mobile operators or licenses in other African countries. There are a limited number of mobile operators and licenses in other African countries available for acquisition and there is substantial competition for the types of mobile operators and licenses Vodacom targets. In addition, there are significant risks associated with Vodacom's ability to acquire mobile operators in other African countries, including those discussed above under "Risk Factors—Risks Related to Our Business—The value of Vodacom's investments outside of South Africa and Vodacom's revenue and net profit may decline as a result of political, economic, regulatory and legal developments in the countries where Vodacom has invested." For instance, Vodacom spent considerable time entering into a five year management agreement with VEE Networks Limited effective April 1, 2004, pursuant to which Vodacom would have managed VEE Networks' cellular network operations in Nigeria with the intention of acquiring an equity stake in the business. On May 31, 2004, however, Vodacom announced that it had elected to terminate the management contract and abandon its plan to make an equity investment in the business of VEE networks in Nigeria. To the extent securities analysts and investors anticipate that Vodacom will continue to grow through acquisitions and Vodacom does not do so, our stock price could decline. Moreover, Vodacom could expend a substantial amount of time and capital pursuing acquisitions it does not consummate, such as happened in Nigeria, which could adversely affect its business, financial condition, results of operations and growth.

The expansion of Vodacom's other African operations may place a significant strain on its management, financial and other resources. Vodacom's ability to manage future growth in its other African operations will depend upon its ability to monitor operations, maintain effective quality controls and significantly expand its internal management, technical and accounting systems, all of

20

which will result in higher operating expenses. The integration of acquired mobile operators or licenses in other African countries may involve, among other things, integration of switching, transmission, technical, sales, marketing, billing, accounting, quality control, management, personnel, payroll, regulatory compliance and other systems and operating hardware and software, some of which may be incompatible with Vodacom's existing systems and therefore may need to be replaced. In addition, mobile operators generally experience higher customer and employee turnover rates during and after an acquisition or launch of service. We cannot assure you that Vodacom will be able to integrate successfully the mobile operators or mobile licenses it may acquire in other African countries.

If we lose key personnel or if we are unable to hire and retain highly qualified employees, our business operations could be disrupted and could impact on the company's ability to compete successfully.

Our success, including the success of Vodacom, depends in large part on our ability to hire and retain highly qualified employees who possess the requisite qualifications and technical skills. Telkom and Vodacom do not have formal employment agreements with a majority of their senior management, any of whom may terminate their employment with us at any time. The loss of key personnel could disrupt our business operations if we are unable to replace them with similarly qualified individuals. We expect that competition for employees in the South African communications industry will increase as new competitors enter the market. If we lose a number of our key employees to our competitors, our business operations could be disrupted and our ability to compete could be harmed.

We do not have the right to appoint a majority of Vodacom's directors or members of its directing committee and the Vodacom joint venture agreement contains approval rights that may limit our flexibility and ability to implement our preferred strategies.