Exhibit 99.1

Investor Meetings Post 1Q22 Reported Results

SAFE HARBOR STATEMENT CAUTIONARY NOTE REGARDING FORWARD - LOOKING STATEMENTS This presentation contains forward - looking statements within the meaning of section 27 A of the Securities Act of 1933 and section 21 E of the Securities Exchange Act of 1934 . All statements, other than statements of historical facts included in this presentation, including statements regarding our estimates, beliefs, expectations, intentions, strategies or projections are forward - looking statements . We intend these forward - looking statements to be covered by the safe harbor provisions for forward - looking statements in the United States federal securities laws . In some cases, these statements can be identified by the use of forward - looking words such as "may", "should", "could", "anticipate", "estimate", "expect", "plan", "believe", "predict", "potential", "intend" or similar expressions . These forward - looking statements are not historical facts, and are based on current expectations, estimates and projections, and various assumptions, many of which, by their nature, are inherently uncertain and beyond management's control . Forward - looking statements contained in this presentation may include, but are not limited to, information regarding our estimates for catastrophes and other weather - related losses including losses related to the COVID - 19 pandemic, measurements of potential losses in the fair market value of our investment portfolio and derivative contracts, our expectations regarding the performance of our business, our financial results, our liquidity and capital resources, the outcome of our strategic initiatives, our expectations regarding pricing and other market conditions, our growth prospects, and valuations of the potential impact of movements in interest rates, credit spreads, equity securities' prices and foreign currency exchange rates . Forward - looking statements only reflect our expectations and are not guarantees of performance . These statements involve risks, uncertainties and assumptions . Accordingly, there are or will be important factors that could cause actual events or results to differ materially from those indicated in such statements . We believe that these factors include, but are not limited to, the following : • the adverse impact of the ongoing COVID - 19 pandemic on our business, results of operations, financial condition and liquidity; • the cyclical nature of the insurance and reinsurance business leading to periods with excess underwriting capacity and unfavorable premium rates; • the occurrence and magnitude of natural and man - made disasters; • the impact of global climate change on our business, including the possibility that we do not adequately assess or reserve for the increased frequency and severity of natural catastrophes; • losses from war, including losses related to the Russian invasion of Ukraine, terrorism and political unrest or other unanticipated losses; • actual claims exceeding loss reserves; • general economic, capital and credit market conditions, including inflation, fluctuations in interest rates, credit spreads, equity securities' prices and/or foreign currency exchange rates; • the failure of any of the loss limitation methods we employ; • the effects of emerging claims, coverage and regulatory issues, including uncertainty related to coverage definitions, limits, terms and conditions; • the inability to purchase reinsurance or collect amounts due to us from reinsurance we have purchased; • the loss of business provided to us by major brokers; • breaches by third parties in our program business of their obligations to us; • difficulties with technology and/or data security; • the failure of our policyholders or intermediaries to pay premiums; • the failure of our cedants to adequately evaluate risks; • the inability to obtain additional capital on favorable terms, or at all; • the loss of one or more of our key executives; • a decline in our ratings with rating agencies; • changes in accounting policies or practices; • the use of industry models and changes to these models; • changes in governmental regulations and potential government intervention in our industry; • inadvertent failure to comply with certain laws and regulations relating to sanctions and foreign corrupt practices; • changes in the political environment of certain countries in which we operate or underwrite business, including the United Kingdom's withdrawal from the European Union; • changes in tax laws; and • other factors including but not limited to those described under Item 1A, 'Risk Factors' in our most recent Annual Report on Form 10 - K filed with the Securities and Exchange Commission ("SEC"), as those factors may be updated from time to time in our periodic and other filings with the SEC, which are accessible on the SEC's website at www.sec.gov . Readers are urged to carefully consider all such factors as the COVID - 19 pandemic may have the effect of heightening many of the other risks and uncertainties described. We undertake no obligation to update or revise publicly any forward - looking statements, whether as a result of new information, future events or otherwise. 2

Vision: Global Leadership in Specialty Risks Targeting top - quintile profitability with industry average volatility Selective participation in attractive insurance and reinsurance markets Franchise anchored in leadership positions in key markets and distribution relationships Strong relationships with distribution partners and clients based on underwriting, service, agility and claims expertise Focus on markets where we have demonstrable relevance, scale and path for profitable growth Strategic risk financing capabilities to match the right risk with the right capital Commitment to underwriting excellence, top caliber talent CONSISTENT COMMITMENT TO OUR STRATEGY STRATEGY FINANCIAL STRENGTH PROGRESS ESG & CITIZENSHIP CONCLUSION APPENDIX 3

LEADING SPECIALTY INSURER AND GLOBAL REINSURER We provide our clients and distribution partners with a broad range of risk transfer products and services, meaningful capacity and solid financial strength (1) Market data as of 5/16/22; GPW data as of YE 2021; $0.43 quarterly dividend announced 5/4/22 (2) Ratings of insurance and reinsurance subsidiaries of AXIS Capital Holdings Limited Exchange / Ticker Market Capitalization 1 Gross Premiums Written 1 Leading Global Underwriter Current Quarterly Div. / Annual Yield 1 AM Best / S&P Financial Strength Rating 2 Insurance 63% Reinsurance 37% Total FY2021 GPW: $7.7 billion Specialty Cat Liability Motor Property A&H Pro Lines Pro Lines Property Liability Marine A&H/Other Aviation Credit & Political Risk Terrorism STRATEGY FINANCIAL STRENGTH PROGRESS ESG & CITIZENSHIP CONCLUSION APPENDIX Insurance Reinsurance 4

AXIS: A PROFITABLE GROWTH ENGINE CONSISTENT MARGIN IMPROVEMENT Disciplined portfolio management should continue to drive improvements in underlying results; Core loss ratio improvement of 9.5 points since FY2017; 0.9 points improvement YoY in 1Q22 STRONG MARKET POSITION The AXIS insurance portfolio is in the most attractive growh markets around the world including E&S Property, E&S Casualty, Lloyd’s, Professional Lines as well as in many Reinsurance lines with further improvements expected in coming quarters; The Insurance segment grew GPW 20.3% in 1Q22 PRICING MOMENTUM Insurance pricing continues to improve with strong double - digit rate increases across many lines; Expected to continue through 2022 and likely beyond ; Reinsurance segment gained additional rate at 1/1 and 4/1; further momentum expected during the upcoming mid - year renewal seasons ATTRACTIVE VALUATION $100 million share repurchase program in place; Global platform with improving profitability trading at attractive levels with a 3.1% dividend yield 1 (1) Market data as of 5/16/22 STRATEGY FINANCIAL STRENGTH PROGRESS ESG & CITIZENSHIP CONCLUSION APPENDIX 5

Insurance: • Double digit rate increases continue • 18 th consecutive quarter of rate increases • Average rate increases of ~12%; 8 th consecutive quarter of double - digit rate increases • Rate increases seen in almost every line of business. AXIS is growing a number of these lines such as Excess Casualty, Renewable Energy, A&H and Marine • Cyber 2 rate increases remain in the high - double digits with further firming expected Reinsurance: • 1Q22 pricing up 9% on average; A&H pricing up 11% while Professional Lines and Casualty were up in the high single - digits and specialty lines in the low to mid - single digits • AXIS cut its property/cat book 45% at 1/1 and achieved an average rate increase of 7% • At the 4/1 renewal AXIS cut its property/cat book 27% YoY with average rate increases of 5% in property lines • Property/cat pricing remained mixed and thus underwriting discipline remains paramount Pricing momentum expected to continue through 2022 and likely beyond Pricing up in almost all lines of the Insurance segment with many lines seeing strong double - digit increases • Industry issues such as low interest rates, lower levels of favorable development, social inflation, financial inflation, the COVID - 19 pandemic and the Russia/Ukraine War should drive further pricing improvements through 2022 and likely beyond (1) Cumulative written rate indexed from 1Q18 to 1Q22 (2) Cyber is reported within Professional Lines and contributes ~$300 million of GPW per annum; There is a 65% quota share on the Cy ber book in addition to aggregate stop loss protection Cumulative Insurance Rate Improvements PRICING MOMENTUM CONTINUES 0% 10% 20% 30% 40% 50% 60% 70% Cumulative Rate Change Liability Aviation Property Marine Professional Lines Insurance 6 STRATEGY FINANCIAL STRENGTH PROGRESS ESG & CITIZENSHIP CONCLUSION APPENDIX

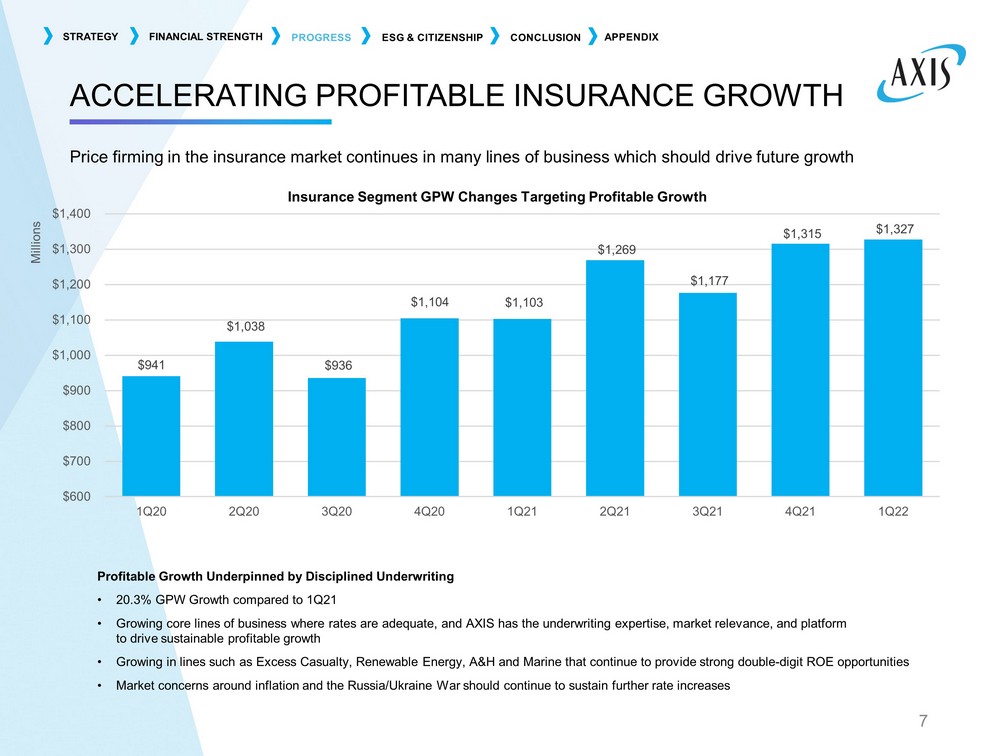

ACCELERATING PROFITABLE INSURANCE GROWTH Price firming in the insurance market continues in many lines of business which should drive future growth Millions $941 $1,038 $936 $1,104 $1,103 $1,269 $1,177 $1,315 $1,327 $600 $700 $800 $900 $1,000 $1,100 $1,200 $1,300 $1,400 1Q20 2Q20 3Q20 4Q20 1Q21 2Q21 3Q21 4Q21 1Q22 Insurance Segment GPW Changes Targeting Profitable Growth Profitable Growth Underpinned by Disciplined Underwriting • 20.3% GPW Growth compared to 1Q21 • Growing core lines of business where rates are adequate, and AXIS has the underwriting expertise, market relevance, and platf orm to drive sustainable profitable growth • Growing in lines such as Excess Casualty, Renewable Energy, A&H and Marine that continue to provide strong double - digit ROE oppo rtunities • Market concerns around inflation and the Russia/Ukraine War should continue to sustain further rate increases 7 STRATEGY FINANCIAL STRENGTH PROGRESS ESG & CITIZENSHIP CONCLUSION APPENDIX

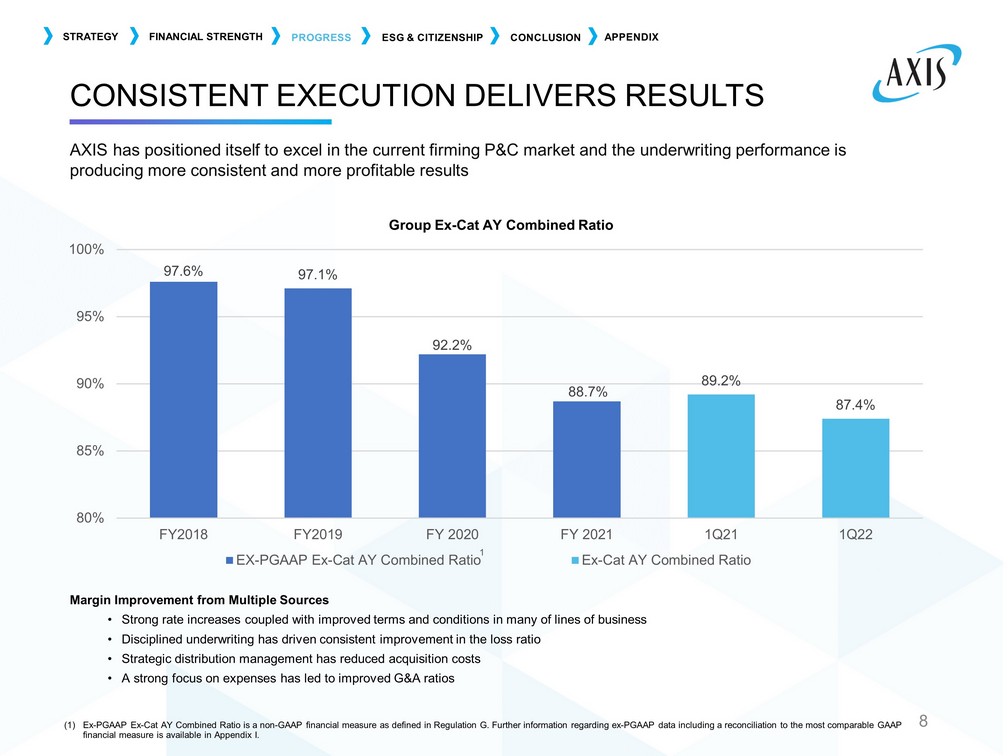

CONSISTENT EXECUTION DELIVERS RESULTS AXIS has positioned itself to excel in the current firming P&C market and the underwriting performance is producing more consistent and more profitable results (1) Ex - PGAAP Ex - Cat AY Combined Ratio is a non - GAAP financial measure as defined in Regulation G. Further information regarding ex - P GAAP data including a reconciliation to the most comparable GAAP financial measure is available in Appendix I. Margin Improvement from Multiple Sources • Strong rate increases coupled with improved terms and conditions in many of lines of business • Disciplined underwriting has driven consistent improvement in the loss ratio • Strategic distribution management has reduced acquisition costs • A strong focus on expenses has led to improved G&A ratios Group Ex - Cat AY Combined Ratio 97.6% 97.1% 92.2% 88.7% 89.2% 87.4% 80% 85% 90% 95% 100% FY2018 FY2019 FY 2020 FY 2021 1Q21 1Q22 EX-PGAAP Ex-Cat AY Combined Ratio Ex-Cat AY Combined Ratio 1 8 STRATEGY FINANCIAL STRENGTH PROGRESS ESG & CITIZENSHIP CONCLUSION APPENDIX

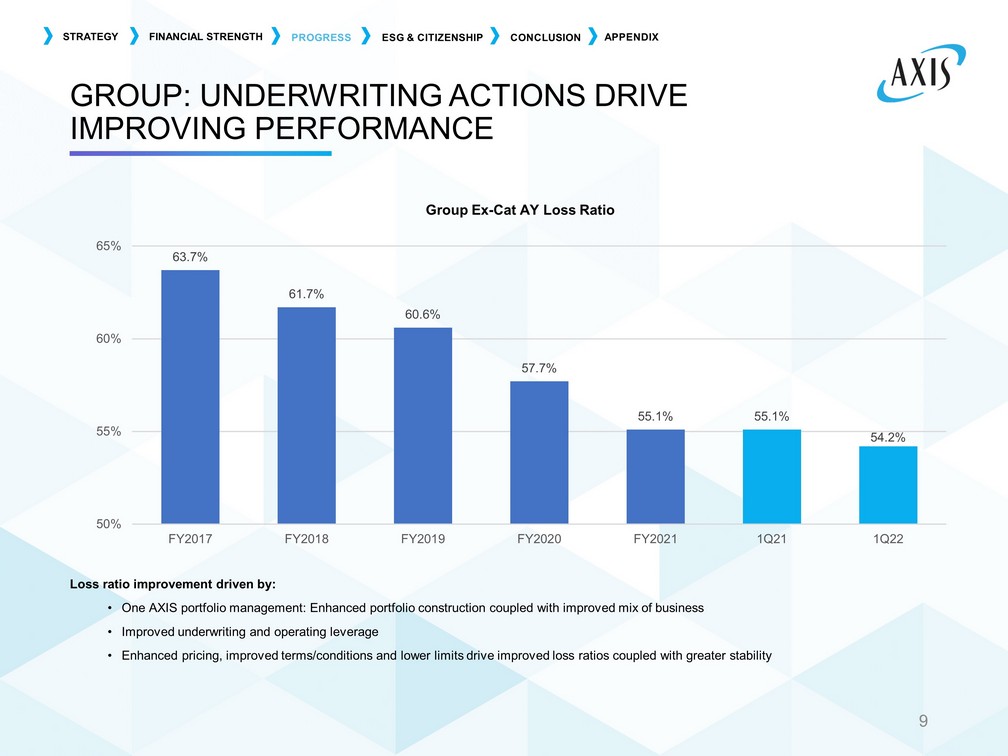

GROUP: UNDERWRITING ACTIONS DRIVE IMPROVING PERFORMANCE Loss ratio improvement driven by: • One AXIS portfolio management: Enhanced portfolio construction coupled with improved mix of business • Improved underwriting and operating leverage • Enhanced pricing, improved terms/conditions and lower limits drive improved loss ratios coupled with greater stability 63.7% 61.7% 60.6% 57.7% 55.1% 55.1% 54.2% 50% 55% 60% 65% FY2017 FY2018 FY2019 FY2020 FY2021 1Q21 1Q22 Group Ex - Cat AY Loss Ratio 9 STRATEGY FINANCIAL STRENGTH PROGRESS ESG & CITIZENSHIP CONCLUSION APPENDIX

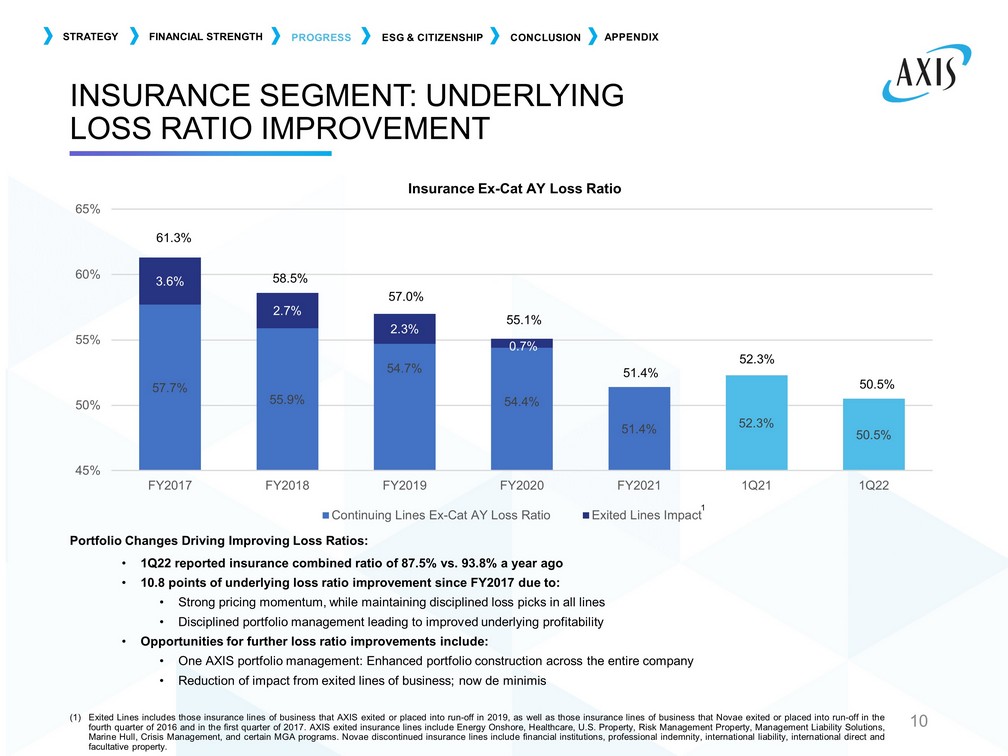

INSURANCE SEGMENT: UNDERLYING LOSS RATIO IMPROVEMENT (1) Exited Lines includes those insurance lines of business that AXIS exited or placed into run - off in 2019 , as well as those insurance lines of business that Novae exited or placed into run - off in the fourth quarter of 2016 and in the first quarter of 2017 . AXIS exited insurance lines include Energy Onshore, Healthcare, U . S . Property, Risk Management Property, Management Liability Solutions, Marine Hull, Crisis Management, and certain MGA programs . Novae discontinued insurance lines include financial institutions, professional indemnity, international liability, international direct and facultative property . Portfolio Changes Driving Improving Loss Ratios: • 1Q22 reported insurance combined ratio of 87.5% vs. 93.8% a year ago • 10.8 points of underlying loss ratio improvement since FY2017 due to: • Strong pricing momentum, while maintaining disciplined loss picks in all lines • Disciplined portfolio management leading to improved underlying profitability • Opportunities for further loss ratio improvements include: • One AXIS portfolio management: Enhanced portfolio construction across the entire company • Reduction of impact from exited lines of business; now de minimis 57.7% 55.9% 54.7% 54.4% 51.4% 52.3% 50.5% 3.6% 2.7% 2.3% 0.7% 45% 50% 55% 60% 65% FY2017 FY2018 FY2019 FY2020 FY2021 1Q21 1Q22 Insurance Ex - Cat AY Loss Ratio Continuing Lines Ex-Cat AY Loss Ratio Exited Lines Impact 61.3% 55.1% 51.4% 57.0% 52.3% 50.5% 58.5% 10 1 STRATEGY FINANCIAL STRENGTH PROGRESS ESG & CITIZENSHIP CONCLUSION APPENDIX

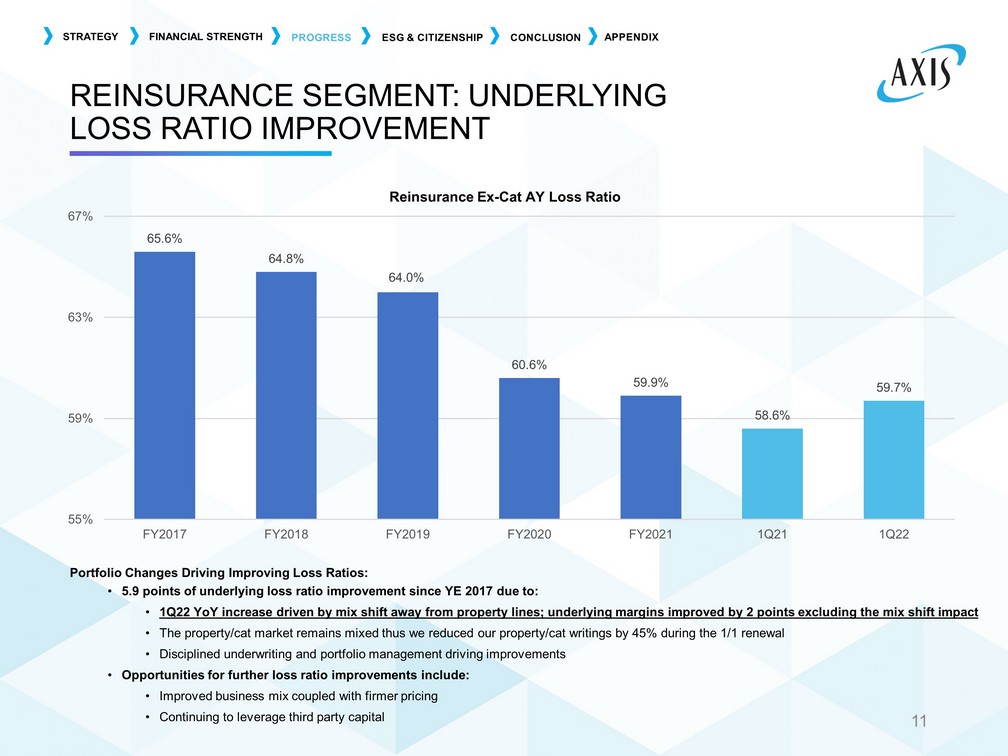

REINSURANCE SEGMENT: UNDERLYING LOSS RATIO IMPROVEMENT Portfolio Changes Driving Improving Loss Ratios: • 5.9 points of underlying loss ratio improvement since YE 2017 due to: • 1Q22 YoY increase driven by mix shift away from property lines; underlying margins improved by 2 points excluding the mix shi ft impact • The property/cat market remains mixed thus we reduced our property/cat writings by 45% during the 1/1 renewal • Disciplined underwriting and portfolio management driving improvements • Opportunities for further loss ratio improvements include: • Improved business mix coupled with firmer pricing • Continuing to leverage third party capital 65.6% 64.8% 64.0% 60.6% 59.9% 58.6% 59.7% 55% 59% 63% 67% FY2017 FY2018 FY2019 FY2020 FY2021 1Q21 1Q22 Reinsurance Ex - Cat AY Loss Ratio 11 STRATEGY FINANCIAL STRENGTH PROGRESS ESG & CITIZENSHIP CONCLUSION APPENDIX

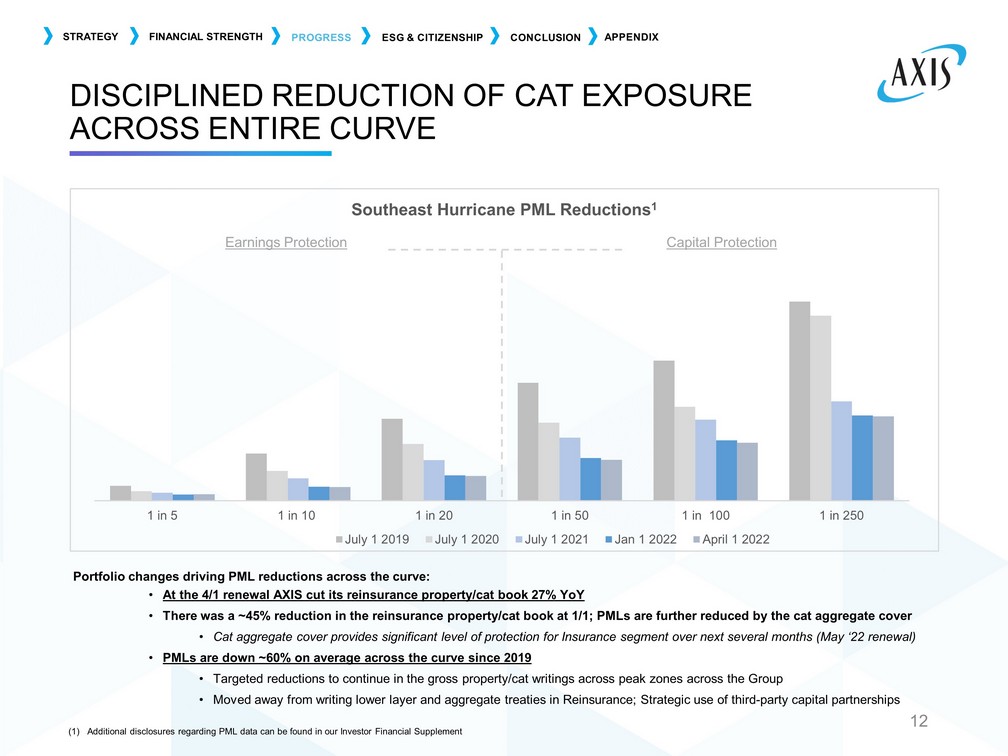

DISCIPLINED REDUCTION OF CAT EXPOSURE ACROSS ENTIRE CURVE Portfolio changes driving PML reductions across the curve: • At the 4/1 renewal AXIS cut its reinsurance property/cat book 27% YoY • There was a ~45% reduction in the reinsurance property/cat book at 1/1; PMLs are further reduced by the cat aggregate cover • Cat aggregate cover provides significant level of protection for Insurance segment over next several months (May ‘22 renewal) • PMLs are down ~60% on average across the curve since 2019 • Targeted reductions to continue in the gross property/cat writings across peak zones across the Group • Moved away from writing lower layer and aggregate treaties in Reinsurance; Strategic use of third - party capital partnerships Earnings Protection Capital Protection 12 1 in 5 1 in 10 1 in 20 1 in 50 1 in 100 1 in 250 Southeast Hurricane PML Reductions 1 July 1 2019 July 1 2020 July 1 2021 Jan 1 2022 April 1 2022 (1) Additional disclosures regarding PML data can be found in our Investor Financial Supplement STRATEGY FINANCIAL STRENGTH PROGRESS ESG & CITIZENSHIP CONCLUSION APPENDIX

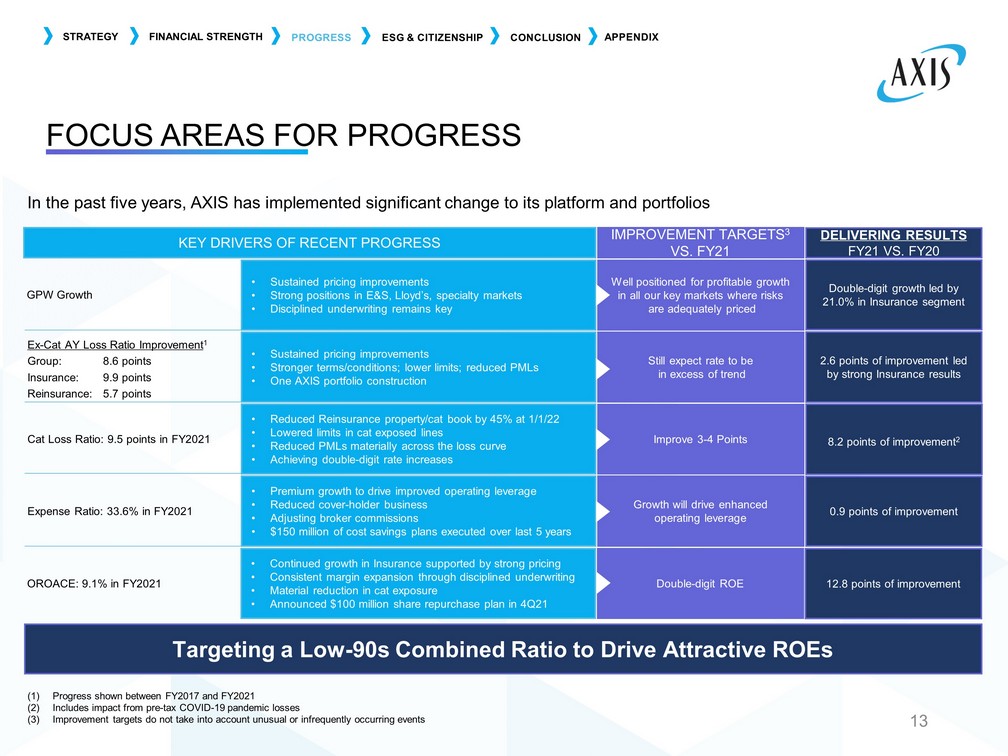

FOCUS AREAS FOR PROGRESS In the past five years, AXIS has implemented significant change to its platform and portfolios (1) Progress shown between FY 2017 and FY 2021 (2) Includes impact from pre - tax COVID - 19 pandemic losses (3) Improvement targets do not take into account unusual or infrequently occurring events KEY DRIVERS OF RECENT PROGRESS IMPROVEMENT TARGETS 3 VS. FY21 Well positioned for profitable growth in all our key markets where risks are adequately priced • Sustained pricing improvements • Strong positions in E&S, Lloyd’s, specialty markets • Disciplined underwriting remains key Still expect rate to be in excess of trend Ex - Cat AY Loss Ratio Improvement 1 Group: 8.6 points Insurance: 9 .9 points Reinsurance: 5 .7 points • Sustained pricing improvements • Stronger terms/conditions; lower l imits; reduced PMLs • One AXIS portfolio construction Cat Loss Ratio: 9.5 points in FY2021 • Reduced Reinsurance property/cat book by 45% at 1/1/22 • Lowered limits in cat exposed lines • Reduced PMLs materially across the loss curve • Achieving double - digit rate increases Improve 3 - 4 Points Expense Ratio: 33.6% in FY2021 • Premium growth to drive improved operating leverage • Reduced cover - h older business • Adjusting broker commissions • $150 million of cost savings plans executed over last 5 years Growth will drive enhanced operating leverage Targeting a Low - 90s Combined Ratio to Drive Attractive ROEs GPW Growth 13 DELIVERING RESULTS FY21 VS. FY20 Double - digit growth led by 21.0% in Insurance segment 2.6 points of improvement led by strong Insurance results 8.2 points of improvement 2 0.9 points of improvement OROACE: 9.1% in FY2021 • Continued growth in Insurance supported by strong pricing • Consistent margin expansion through disciplined underwriting • Material reduction in cat exposure • Announced $100 million share repurchase plan in 4Q21 Double - digit ROE 12.8 points of improvement STRATEGY FINANCIAL STRENGTH PROGRESS ESG & CITIZENSHIP CONCLUSION APPENDIX

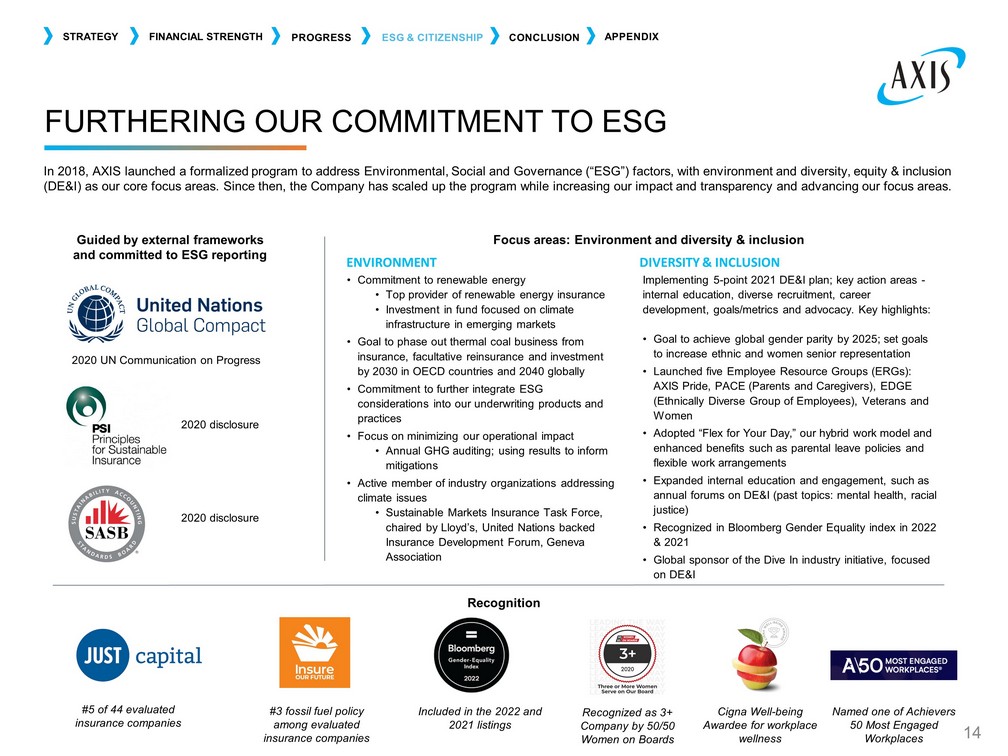

Guided by external frameworks and committed to ESG reporting Focus areas: Environment and diversity & inclusion DIVERSITY & INCLUSION Implementing 5 - point 2021 DE&I plan; key action areas - internal education, diverse recruitment, career development, goals/metrics and advocacy. Key highlights: • Goal to achieve global gender parity by 2025; set goals to increase ethnic and women senior representation • Launched five Employee Resource Groups (ERGs): AXIS Pride, PACE (Parents and Caregivers), EDGE (Ethnically Diverse Group of Employees), Veterans and Women • Adopted “Flex for Your Day,” our hybrid work model and enhanced benefits such as parental leave policies and flexible work arrangements • Expanded internal education and engagement, such as annual forums on DE&I (past topics: mental health, racial justice) • Recognized in Bloomberg Gender Equality index in 2022 & 2021 • Global sponsor of the Dive In industry initiative, focused on DE&I ENVIRONMENT • Commitment to renewable energy • Top provider of renewable energy insurance • Investment in fund focused on climate infrastructure in emerging markets • Goal to phase out thermal coal business from insurance, facultative reinsurance and investment by 2030 in OECD countries and 2040 globally • Commitment to further integrate ESG considerations into our underwriting products and practices • Focus on minimizing our operational impact • Annual GHG auditing; using results to inform mitigations • Active member of industry organizations addressing climate issues • Sustainable Markets Insurance Task Force, chaired by Lloyd’s, United Nations backed Insurance Development Forum, Geneva Association In 2018, AXIS launched a formalized program to address Environmental, Social and Governance (“ESG”) factors, with environment an d diversity, equity & inclusion (DE&I) as our core focus areas. Since then, the Company has scaled up the program while increasing our impact and transparenc y a nd advancing our focus areas. 2020 disclosure 2020 disclosure 2020 UN Communication on Progress FURTHERING OUR COMMITMENT TO ESG STRATEGY FINANCIAL STRENGTH PROGRESS ESG & CITIZENSHIP CONCLUSION APPENDIX Recognition #5 of 44 evaluated insurance companies #3 fossil fuel policy among evaluated insurance companies Included in the 2022 and 2021 listings Recognized as 3+ Company by 50/50 Women on Boards Cigna Well - being Awardee for workplace wellness Named one of Achievers 50 Most Engaged Workplaces 14

Strong Finish to 2021 and with 1Q22 this year is off to a strong start Underwriting margin improvement should continue given ongoing portfolio improvements and firm pricing Enhanced use of reinsurance, retro and third - party capital driving better risk adjusted returns with lower volatility Building a stronger, more profitable and more stable underwriter of specialty risks AXIS has a global platform with improving profitability trading at attractive levels CONCLUSION STRATEGY FINANCIAL STRENGTH PROGRESS ESG & CITIZENSHIP CONCLUSION APPENDIX 15 BA8

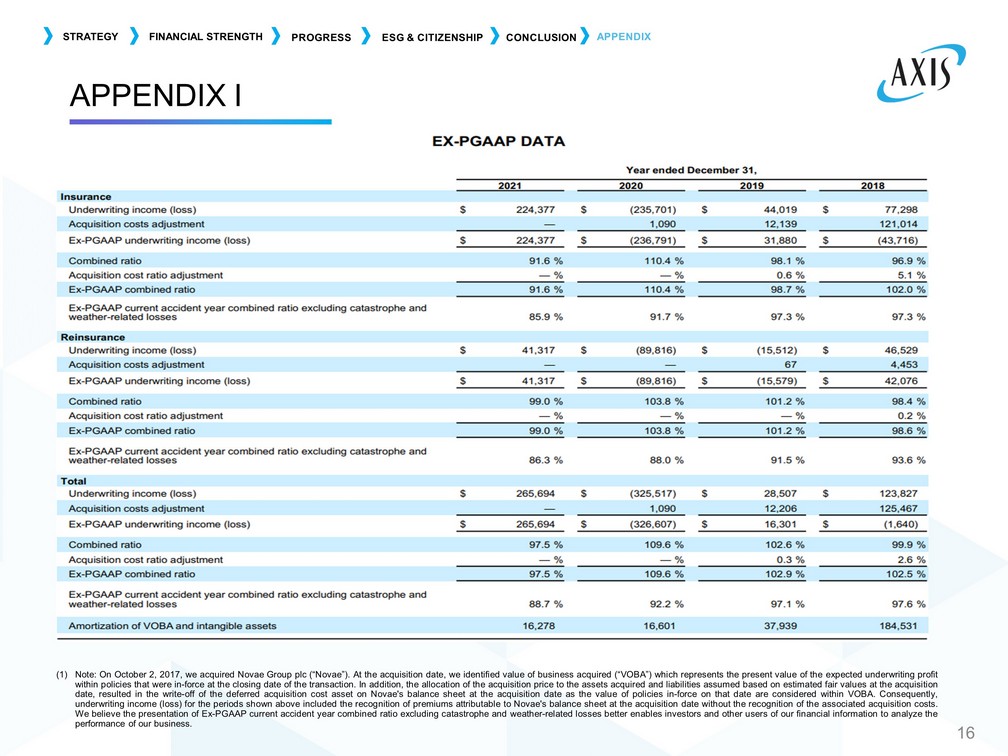

(1) Note : On October 2 , 2017 , we acquired Novae Group plc (“Novae”) . At the acquisition date, we identified value of business acquired (“VOBA”) which represents the present value of the expected underwriting profit within policies that were in - force at the closing date of the transaction . In addition, the allocation of the acquisition price to the assets acquired and liabilities assumed based on estimated fair values at the acquisition date, resulted in the write - off of the deferred acquisition cost asset on Novae's balance sheet at the acquisition date as the value of policies in - force on that date are considered within VOBA . Consequently, underwriting income (loss) for the periods shown above included the recognition of premiums attributable to Novae's balance sheet at the acquisition date without the recognition of the associated acquisition costs . We believe the presentation of Ex - PGAAP current accident year combined ratio excluding catastrophe and weather - related losses better enables investors and other users of our financial information to analyze the performance of our business . APPENDIX I STRATEGY FINANCIAL STRENGTH PROGRESS ESG & CITIZENSHIP CONCLUSION APPENDIX 16