AXIS Capital Bank of America Merrill Lynch Insurance Conference 2011 New York, NY John Charman, CEO and President February 15, 2011 Exhibit 99.1 |

2 Safe Harbor Disclosure Forward-looking statements only reflect our expectations and are not guarantees of performance. Accordingly, there are or will be important factors that could cause actual results to differ materially from those indicated in such statements. We believe that these factors include, but are not limited to, the following: • The occurrence of natural and man-made disasters, • Actual claims exceeding our loss reserves, • General economic, capital and credit market conditions, • The failure of any of the loss limitation methods we employ, • The effects of emerging claims and coverage issues, • The failure of our cedants to adequately evaluate risks, • Inability to obtain additional capital on favorable terms, or at all, • The loss of one or more key executives, • A decline in our ratings with rating agencies, • Loss of business provided to us by our major brokers, • Changes in accounting policies or practices, • Changes in governmental regulations, • Increased competition, • Changes in the political environment of certain countries in which we operate or underwrite business, and • Fluctuations in interest rates, credit spreads, equity prices and/or currency values. This report is for informational purposes only. It should be read in conjunction with the documents that we file with the Securities and Exchange Commission pursuant to the Securities Act of 1933 and the Securities Exchange Act of 1934. Statements in this presentation that are not historical facts, including statements regarding our estimates, beliefs, expectations, intentions, strategies or projections, may be “forward-looking statements” within the meaning of the U.S. federal securities laws, including the Private Securities Litigation Reform Act of 1995. We intend these forward-looking statements to be covered by the safe harbor provisions for forward-looking statements in the United States securities laws. In some cases, these statements can be identified by the use of forward-looking words such as “may,” “should,” “could,” “anticipate,” “estimate,” “expect,” “plan,” “believe,” “predict,” “potential,” “intend” or similar expressions. Our expectations are not guarantees and are based on currently available competitive, financial and economic data along with our operating plans. Forward-looking statements contained in this presentation may include, but are not limited to, information regarding our estimates of losses related to catastrophes and other large losses, measurements of potential losses in the fair value of our investment portfolio, our expectations regarding pricing and other market conditions and valuations of the potential impact of movements in interest rates, equity prices, credit spreads and foreign currency rates. |

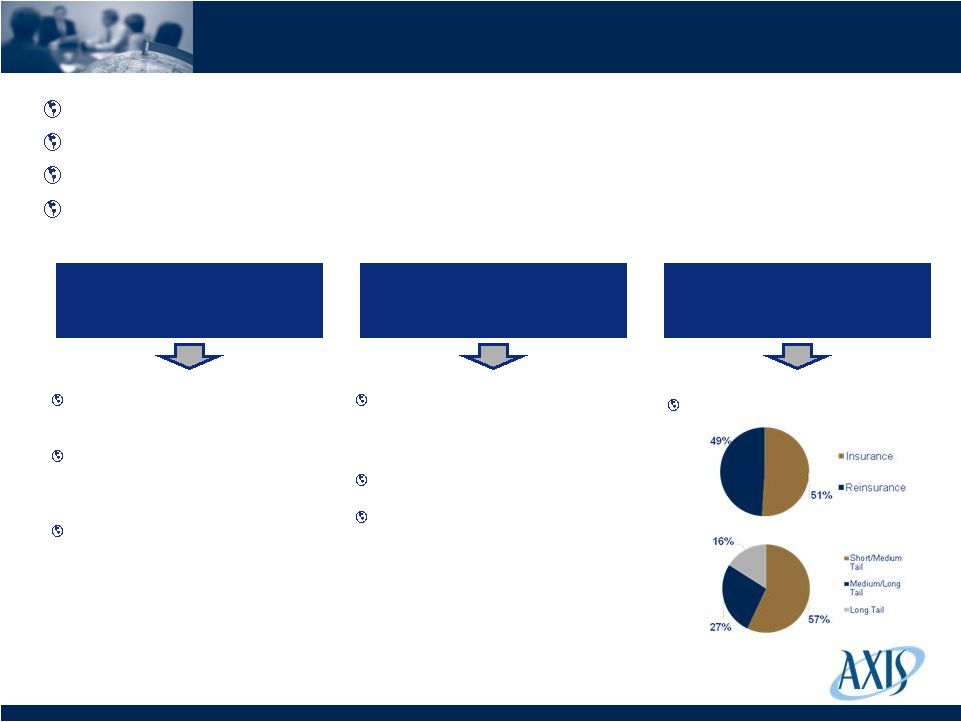

3 3 AXIS – Who we Are Bermuda-domiciled Specialty Insurer and Reinsurer Founded 2001; IPO – 2003; $4.2 Bn market capitalization at 2/11/2011 $3.75 Bn GWP in 2010 Underwriting-led, Diversified Specialty Insurer and Reinsurer with Strong Risk Management Culture Strong Balance Sheet Multi-Platform Approach Well Diversified Portfolio $5.6 Bn of shareholders’ equity as at December 31, 2010 Financial Strength Ratings of A+ (S&P), A2 (Moody’s) and A (AM Best) Diluted BVPS 13.4% CAGR since 6/30/2003 (IPO) Locations in Bermuda, U.S., Europe, Singapore, Canada and Australia Approximately 1,000 employees 32 offices in 9 countries Focus on Specialty Lines |

4 4 AXIS Insurance Development of AXIS Insurance GPW ($ in millions) |

5 5 AXIS Reinsurance Development of AXIS Reinsurance GPW ($ in millions) |

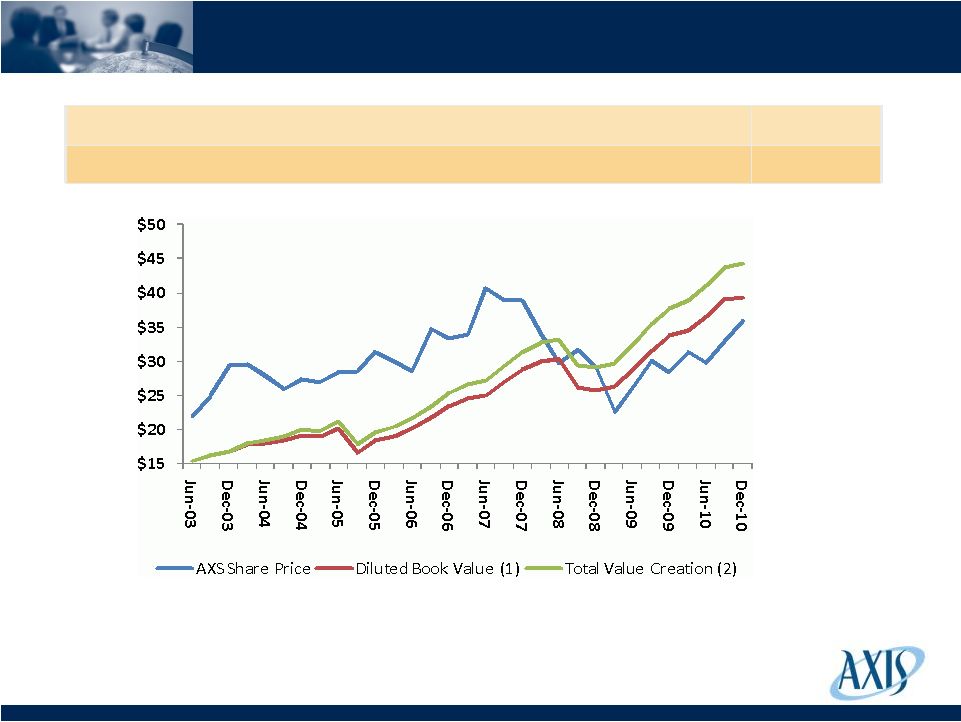

6 6 AXIS Performance – Share Price to Fully Diluted Book Value (1) Diluted book value per share calculated using Treasury stock method. Note 6/30/03 diluted book value per share is pro forma for AXIS Capital IPO. (2) Total value creation calculated as diluted book value per share plus cumulative declared dividends. Book value per share (1) CAGR since 6/30/03 (IPO) 13.4% Total value creation per share (2) CAGR since 6/30/03 (IPO) 15.2% |

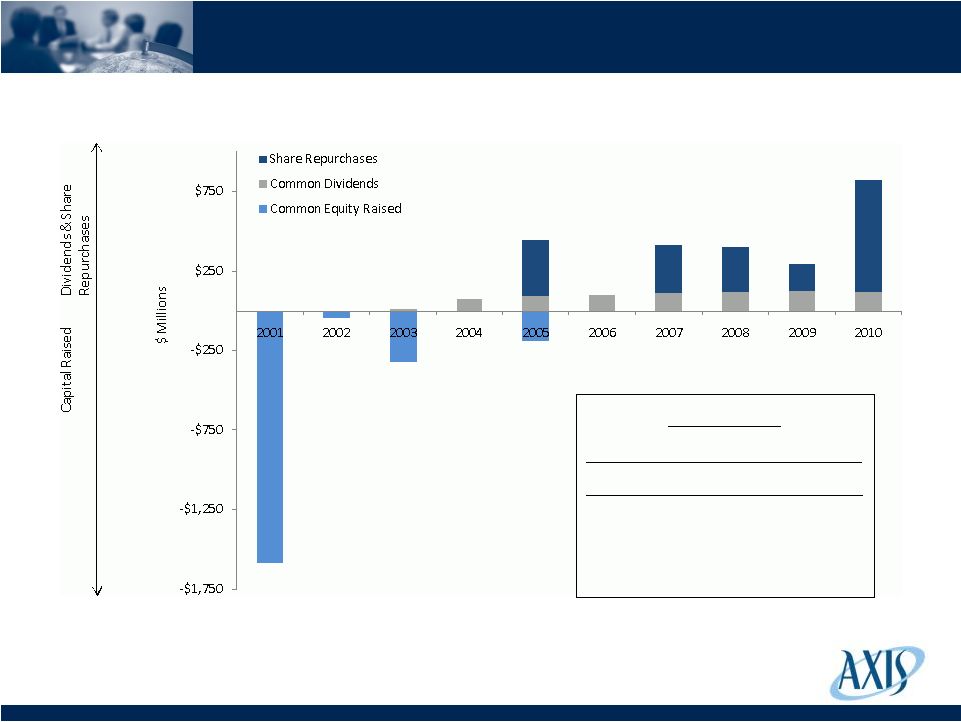

7 Key Highlights 2010 Financial Results GPW Growth 4.6% Combined Ratio 88.7% Operating ROACE 12.4% Diluted Book Value per Share Growth 17.0% Total Value Creation (1) 19.6% Managing bottom of soft P&C cycle and expecting improvement in P&C marketplace in 2012 Significant investments in Infrastructure, Geography and Product to prepare for market turn Returned $820 million to common shareholders through share repurchases and dividends (1) 2010 Total Value Creation = Growth in diluted book value per share + declared dividends |

8 8 Accident and Health Strategic Initiative Provide customized products and risk-taking solutions for (re)insurance clients Primary product focus = accident, health, travel, disability and allied personal lines insurance and reinsurance Global footprint • Growth in 2011 from accident, catastrophe and specialty health reinsurance globally • Good progress in building insurance capabilities globally • Over 60 employees globally as of year-end 2010 |

9 9 Strong Risk Management Clearly articulated objectives and risk appetite at a group and legal entity level Controlled risk taking: our financial strength and sustainable value creation are integral to our existence Clear accountability: we operate on the principle of delegated and clearly defined authority Independent risk controlling: to avoid conflicts of interests Open risk culture: risk transparency and responsiveness to change are integral to our risk control process |

10 10 Underwriting Objectives - 2011 Manage risk Maintain quality of our seasoned portfolio Prepare to accelerate when the market turns • Transformation initiative to increase productivity of intellectual capital at AXIS • Continue to build global footprint • A&H strategic initiative |

11 11 Investment and Financial Objectives - 2011 Protect Book Value and Total Returns in Rising Rate Environment Defend investment income in a low rate and spread environment • Maintain exposure to investment-grade spread assets • Take advantage of weakness in municipal markets • Maintain positions in short-duration high yield bonds Optimize risk-adjusted returns • Diversify away from interest-rate sensitive assets • Increased exposure to equities and alternatives • Monitor implementation of a hedge on fixed income assets • Limiting significant further exposure to prepayment-sensitive MBS Capital management • Maintain strength but “right size” to opportunity • Share repurchase and dividend policy characterized by consistent increase and attractive yield |

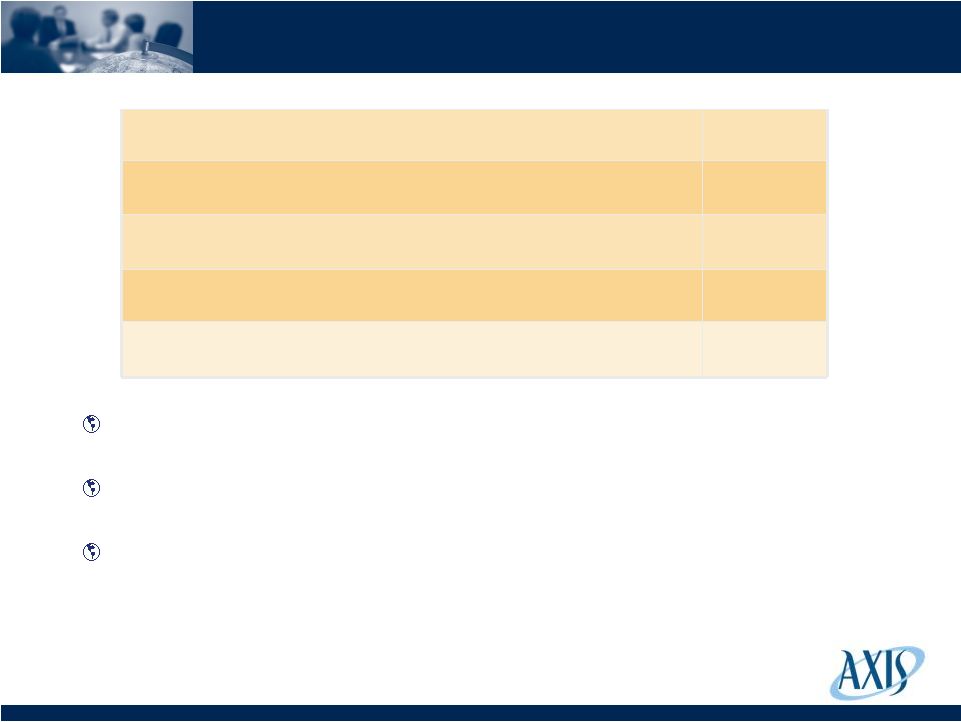

12 Efficient Capital Management Total Equity Raised $2.1 Dividends $0.8 Share Repurchases $1.8 Total Capital Returned $2.6 AXIS Market Value $5.0 IRR 2001-2010 18.2% 2001-2010 (Billions) |