It is the Funds’ policy to invest a portion of their assets in convertible securities. Although convertible securities do derive part of their value from that of the securities into which they are convertible, they are not considered derivative financial instruments. However, certain of the Funds’ investments in convertible securities include features which render them more sensitive to price changes in their underlying securities. The value of structured/synthetic convertible securities can be affected by interest rate changes and credit risks of the issuer. Such securities may be structured in ways that limit their potential for capital appreciation and the entire value of the security may be at a risk of loss depending on the performance of the underlying equity security. Consequently, the Funds are exposed to greater downside risk than traditional convertible securities, but still less than that of the underlying common stock.

In the normal course of business the Funds trade financial instruments and enter into financial transactions where risk of potential loss exists due to, among other things, changes in the market (market risk) or failure of the other party to a transaction to perform (credit/counterparty risk). The Funds are exposed to various risks such as, but not limited to, interest rate, market price and credit/counterparty risks.

Interest rate risk is the risk that fixed income securities will decline in value because of changes in interest rates. As nominal interest rates rise, the value of certain fixed income securities held by the Funds is likely to decrease. A nominal interest rate can be described as the sum of a real interest rate and an expected inflation rate. Fixed income securities with longer durations tend to be more sensitive to changes in interest rates, usually making them more volatile than securities with shorter durations. Duration is used primarily as a measure of the sensitivity of a fixed income security’s market price to interest rate (i.e. yield) movements.

The market values of equity securities, such as common and preferred stock and securities convertible into equity securities, may decline due to general market conditions which are not specifically related to a particular company, such as real or perceived adverse economic conditions, changes in the general outlook for corporate earnings, changes in interest or currency rates or adverse investor sentiment. They may also decline due to factors which affect a particular industry or industries, such as labor shortages or increased production costs and competitive conditions within an industry. Equity securities generally have greater market price volatility than fixed income securities.

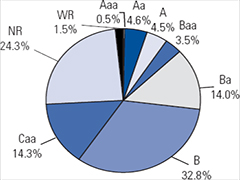

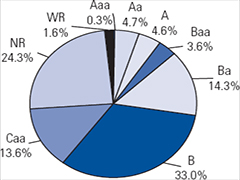

The Funds are exposed to credit risk on parties with whom they trade and will also bear the risk of settlement default. The Funds seek to minimize concentrations of credit risk by undertaking transactions with a large number of customers and counterparties on reorganized and reputable exchanges. The Funds could lose money if the issuer or guarantor of a fixed income security is unable or unwilling to make timely principal and/or interest payments, or to otherwise honor its obligations. Securities are subject to varying degrees of credit risk, which are often reflected in credit ratings.

Similar to credit risk, the Funds are exposed to counterparty risk, or the risk that an institution or other entity with which the Funds have unsettled or open transactions will default. The potential loss to the Funds could exceed the value of the financial assets recorded in the Funds’ financial statements. Financial assets, which potentially expose the Funds to counterparty risk, consist principally of cash due from counterparties and investments. The Funds’ sub-adviser, Nicholas-Applegate Capital Management LLC (the “Sub-Adviser”), an affiliate of the Investment Manager, seeks to minimize Funds’ counterparty risks by performing reviews of each counterparty. Delivery of securities sold is only made once the Funds have received payment. Payment is made on the purchase once the securities have been delivered by the counterparty. The trade will fail if either party fails to meet its obligation.

During the fiscal year ended February 28, 2010, the Funds held synthetic convertible securities with Lehman Brothers Holdings, Inc. as the counterparty. On September 15, 2008, Lehman Brothers Holdings, Inc. filed for protection under Chapter 11 of the United States Bankruptcy Code. The value of the relevant securities has been written down to their estimated recoverable values.

Each Fund has an Investment Management Agreement (each an “Agreement”) with the Investment Manager. Subject to the supervision of the Funds’ Board of Trustees, the Investment Manager is responsible for managing, either directly or through others selected by it, the Funds’ investment activities, business affairs and administrative matters. Pursuant to each Agreement, the Funds pay the Investment Manager an annual fee, payable on a monthly basis, at the annual rate of 0.70% of the Funds’ average daily total managed assets. Total managed assets refer to the total assets of each Fund (including assets attributable to any preferred shares or other forms of leverage of the Fund that may be outstanding) minus accrued liabilities (other than liabilities representing leverage).

| |

Nicholas-Applegate Convertible & Income Funds | Notes to Financial Statements |

February 28, 2010 | |

| | |

3. Investment Manager/Sub-Adviser (continued)

The Investment Manager has retained the Sub-Adviser to manage the Funds’ investments. Subject to the supervision of the Investment Manager, the Sub-Adviser is responsible for making all of the Funds’ investment decisions. The Investment Manager, and not the Funds, pays a portion of the fees it receives as Investment Manager to the Sub-Adviser in return for its services.

4. Investment in Securities

For the year ended February 28, 2010, purchases and sales of investments, other than short-term securities were:

| | | | | | | | | | | | |

| | U.S. Government Obligation | | All Other | |

| | | | | |

| | Purchases | | Sales | | Purchases | | Sales | |

| | | | | | | | | | |

Convertible & Income | | — | | $ | 25,786,094 | | $ | 504,056,045 | | $ | 487,483,943 | |

Convertible & Income II | | — | | | 22,035,000 | | | 388,168,922 | | | 378,413,805 | |

5. Income Tax Information

Convertible & Income:

For the fiscal years ended February 28, 2010 and February 28, 2009, the tax character of dividends paid of $79,507,476 and $110,164,852, respectively, were comprised entirely of ordinary income.

At February 28, 2010, the tax character of distributable earnings of $3,366,103 was comprised entirely of ordinary income.

For the year ended February 28, 2010, permanent differences are primarily attributable to the differing treatment of premium amortization, convertible preferred securities, consent payments and excise taxes. These adjustments were to increase undistributed net investment income by $6,177,842, increase accumulated net realized loss by $6,167,218 and decrease paid-in-capital in excess of par by $10,624.

At February 28, 2010, Convertible & Income had a capital loss carryforward of $401,934,705 ($1,830,527 of which will expire in 2015, $10,961,628 of which will expire in 2016, $131,342,119 of which will expire in 2017 and $257,800,431 of which will expire in 2018) available as a reduction, to the extent provided in the regulations, of any future net realized capital gains. To the extent that these losses are used to offset future realized capital gains, such gains will not be distributed.

The cost basis of portfolio securities for federal income tax purposes is $975,190,391. Aggregate gross unrealized appreciation for securities in which there is an excess value over tax cost is $89,965,922; aggregate gross unrealized depreciation for securities in which there is an excess of tax cost over value is $82,803,912; net unrealized appreciation for federal income tax purposes is $7,162,010. The difference between book and tax basis unrealized is attributable to wash sales and the differing treatment of bond premium amortization and convertible preferred securities.

Convertible & Income II:

For the years ended February 28, 2010 and February 28, 2009, the tax character of dividends paid of $69,200,358 and $88,564,571, respectively, were comprised entirely of ordinary income.

At February 28, 2010, the tax character of distributable earnings of $2,640,409 was comprised entirely of ordinary income.

For the year ended February 28, 2010, permanent differences are primarily attributable to the differing treatment of premium amortization, convertible preferred securities, consent payments and excise taxes. These adjustments were to increase undistributed net investment income by $4,664,560, increase accumulated net realized loss by $4,655,128 and decrease paid-in-capital in excess of par by $9,432.

At February 28, 2010, Convertible & Income II had a capital loss carryforward of $371,556,558 ($1,751,653 of which will expire in 2015, $11,338,190 of which will expire in 2016, $130,798,418 of which will expire in 2017 and $227,668,267 of which will expire in 2018) available as a reduction, to the extent provided in the regulations, of any future net realized capital gains. To the extent that these losses are used to offset future realized capital gains, such gains will not be distributed.

26 Nicholas-Applegate Convertible & Income Funds Annual Report | 2.28.10

| |

Nicholas-Applegate Convertible & Income Funds | Notes to Financial Statements |

February 28, 2010 | |

| | |

5. Income Tax Information (continued)

The cost basis of portfolio securities for federal income tax purposes is $743,326,398. Aggregate gross unrealized appreciation for securities in which there is an excess value over tax cost is $70,313,117; aggregate gross unrealized depreciation for securities in which there is an excess of tax cost over value is $67,943,146; net unrealized appreciation for federal income tax purposes is $2,369,971. The difference between book and tax basis unrealized is attributable to wash sales and the differing treatment of bond premium amortization and convertible preferred securities.

6. Auction-Rate Preferred Shares

Convertible & Income has 2,856 shares of Preferred Shares Series A, 2,856 shares of Preferred Shares Series B, 2,856 shares of Preferred Shares Series C, 2,856 shares of Preferred Shares Series D, and 2,856 shares of Preferred Shares Series E outstanding, each with a liquidation preference value of $25,000 per share plus any accumulated, unpaid dividends.

Convertible & Income II has 2,192 shares of Preferred Shares Series A, 2,192 shares of Preferred Shares Series B, 2,192 shares of Preferred Shares Series C, 2,192 shares of Preferred Shares Series D, and 2,192 shares of Preferred Shares Series E outstanding, each with a liquidation preference value of $25,000 per share plus any accumulated, unpaid dividends.

Dividends are accumulated daily at an annual rate (typically re-set every seven days) through auction procedures. Distributions of net realized long-term gains, if any, are paid annually.

For the fiscal year ended February 28, 2010, the annualized dividend rate ranged from:

| | | | | | |

| | High | | Low | | At February 28, 2010 |

| | | | | | | |

Convertible & Income: | | | | | | |

Series A | | 0.677% | | 0.105% | | 0.165% |

Series B | | 0.527% | | 0.105% | | 0.150% |

Series C | | 0.452% | | 0.090% | | 0.135% |

Series D | | 0.677% | | 0.060% | | 0.210% |

Series E | | 0.677% | | 0.075% | | 0.240% |

| | | | | | |

Convertible & Income II: | | | | | | |

Series A | | 0.677% | | 0.105% | | 0.165% |

Series B | | 0.527% | | 0.105% | | 0.150% |

Series C | | 0.452% | | 0.090% | | 0.135% |

Series D | | 0.677% | | 0.060% | | 0.210% |

Series E | | 0.677% | | 0.075% | | 0.240% |

The Funds are subject to certain limitations and restrictions while Preferred Shares are outstanding. Failure to comply with these limitations and restrictions could preclude the Funds from declaring any dividends or distributions to common shareholders or repurchasing common shares and/or could trigger the mandatory redemption of Preferred Shares at their liquidation preference plus any accumulated, unpaid dividends.

Preferred shareholders, who are entitled to one vote per share, generally vote with the common shareholders but vote separately as a class to elect two Trustees and on any matters affecting the rights of the Preferred Shares.

Since mid-February 2008, holders of auction-rate preferred shares (“ARPS”) issued by the Funds have been directly impacted by an unprecedented lack of liquidity, which has similarly affected ARPS holders in many of the nation’s closed-end funds. Since then, regularly scheduled auctions for ARPS issued by the Funds have consistently “failed” because of insufficient demand (bids to buy shares) to meet the supply (shares offered for sale) at each auction. In a failed auction, ARPS holders cannot sell all, and may not be able to sell any, of their shares tendered for sale. While repeated action failures have affected the liquidity for ARPS, they do not constitute a default or automatically alter the credit quality of the ARPS, and ARPS holders have continued to receive dividends at the defined “maximum rate” the 7-day “AA” Composite Commercial Paper Rate multiplied by 150% (which is a function of short-term interest rates and typically higher than the rate that would have otherwise been set through a successful auction). If the Funds’ ARPS auctions continue to fail and the “maximum rate” payable on the ARPS rises as a result of changes in short-term interest rates, returns for the Funds’ common shareholders could be adversely affected.

2.28.10 | Nicholas-Applegate Convertible & Income Funds Annual Report 27

|

Nicholas-Applegate Convertible & Income Funds Notes to Financial Statements |

February 28, 2010 |

| |

7. Legal Proceedings

In June and September 2004, the Investment Manager and certain of its affiliates (including PEA Capital LLC (“PEA”), Allianz Global Investors Distributors LLC and Allianz Global Investors of America, L.P.), agreed to settle, without admitting or denying the allegations, claims brought by the Securities and Exchange Commission (“SEC”) and the New Jersey Attorney General alleging violations of federal and state securities laws with respect to certain open-end funds for which the Investment Manager serves as investment adviser. The settlements related to an alleged “market timing” arrangement in certain open-end funds formerly sub-advised by PEA. The Investment Manager and its affiliates agreed to pay a total of $68 million to settle the claims. In addition to monetary payments, the settling parties agreed to undertake certain corporate governance, compliance and disclosure reforms related to market timing, and consented to cease and desist orders and censures. Subsequent to these events, PEA deregistered as an investment adviser and dissolved. None of the settlements alleged that any inappropriate activity took place with respect to the Funds.

Since February 2004, the Investment Manager and certain of its affiliates and their employees have been named as defendants in a number of pending lawsuits concerning “market timing,” which allege the same or similar conduct underlying the regulatory settlements discussed above. The market timing lawsuits have been consolidated in a multi-district litigation proceeding in the U.S. District Court for the District of Maryland. Any potential resolution of these matters may include, but not be limited to, judgments or settlements for damages against the Investment Manager or its affiliates or related injunctions.

The Investment Manager and the Sub-Adviser believe that these matters are not likely to have a material adverse effect on the Funds or on their ability to perform their respective investment advisory activities relating to the Funds.

8. Subsequent Events

On March 1, 2010 the following monthly dividends were declared to common shareholders, payable March 30, 2010 to shareholders of record on March 11, 2010:

| |

Convertible & Income | $0.09 per share |

Convertible & Income II | $0.085 per share |

On April 1, 2010 the following monthly dividends were declared to common shareholders, payable May 3, 2010 to shareholders of record on April 12, 2010:

| |

Convertible & Income | $0.09 per share |

Convertible & Income II | $0.085 per share |

Effective March 1, 2010, Convertible & Income Fund II adopted amended and restated by-laws (“By-laws”) that incorporate substantially revised and updated ratings criteria (the “New Fitch Criteria”) issued by Fitch, Inc. (“Fitch”) applicable to that Fund’s outstanding auction rate preferred shares (“Preferred Shares”). The New Fitch Criteria include two separate Preferred Shares asset coverage tests which differ from the single test previously applicable to Fitch’s ratings. Other key components of the New Fitch Criteria as cited by Fitch include, among others, updated asset discount factors, changes to issuer and industry concentration thresholds and guidelines, and inclusion of certain leverage and derivatives when calculating the Fitch asset coverage tests. The New Fitch Criteria are available on the Fitch website (www.fitchratings.com) and are incorporated by reference into Convertible & Income Fund II’s By-laws. Furthermore, as announced in a press release dated March 12, 2010, Fitch has reaffirmed the ‘AAA’ rating it assigned to Convertible & Income Fund II’s Preferred Shares.

28 Nicholas-Applegate Convertible & Income Funds Annual Report | 2.28.10

|

Nicholas-Applegate Convertible & Income Fund Financial Highlights |

For a share of common stock outstanding throughout each year: |

| |

| | | | | | | | | | | | | | | | |

| | Year ended | |

| | | |

| | February 28,

2010 | | February 28,

2009 | | February 29,

2008 | | February 28,

2007 | | February 28,

2006 | |

| | | | | | | | | | | |

Net asset value, beginning of year | | $ | 4.80 | | $ | 12.52 | | $ | 14.84 | | $ | 14.69 | | $ | 16.07 | |

| | | | | | | | | | | | | | | | | |

Income from Investment Operations: | | | | | | | | | | | | | | | | |

Net investment income | | | 1.07 | | | 1.56 | | | 1.62 | | | 1.66 | | | 1.51 | |

| | | | | | | | | | | | | | | | | |

Net realized and change in unrealized gain (loss) on investments and interest rate caps | | | 4.02 | | | (7.75 | ) | | (2.05 | ) | | 0.55 | | | (0.48 | ) |

| | | | | | | | | | | | | | | | | |

Total from investment operations | | | 5.09 | | | (6.19 | ) | | (0.43 | ) | | 2.21 | | | 1.03 | |

| | | | | | | | | | | | | | | | | |

Dividends and Distributions on Preferred Shares from: | | | | | | | | | | | | | | | | |

Net investment income | | | (0.01 | ) | | (0.17 | ) | | (0.39 | ) | | (0.34 | ) | | (0.25 | ) |

| | | | | | | | | | | | | | | | | |

Net realized gains | | | — | | | — | | | — | | | (0.03 | ) | | (0.02 | ) |

| | | | | | | | | | | | | | | | | |

Total dividends and distributions on preferred shares | | | (0.01 | ) | | (0.17 | ) | | (0.39 | ) | | (0.37 | ) | | (0.27 | ) |

| | | | | | | | | | | | | | | | | |

Net increase (decrease) in net assets applicable to common shareholders resulting from investment operations | | | 5.08 | | | (6.36 | ) | | (0.82 | ) | | 1.84 | | | 0.76 | |

| | | | | | | | | | | | | | | | | |

Dividends and Distributions to Common Shareholders from: | | | | | | | | | | | | | | | | |

Net investment income | | | (1.08 | ) | | (1.36 | ) | | (1.50 | ) | | (1.50 | ) | | (1.91 | ) |

| | | | | | | | | | | | | | | | | |

Net realized gains | | | — | | | — | | | — | | | (0.19 | ) | | (0.23 | ) |

| | | | | | | | | | | | | | | | | |

Total dividends and distributions to common shareholders | | | (1.08 | ) | | (1.36 | ) | | (1.50 | ) | | (1.69 | ) | | (2.14 | ) |

| | | | | | | | | | | | | | | | | |

Net asset value, end of year | | $ | 8.80 | | $ | 4.80 | | $ | 12.52 | | $ | 14.84 | | $ | 14.69 | |

| | | | | | | | | | | | | | | | | |

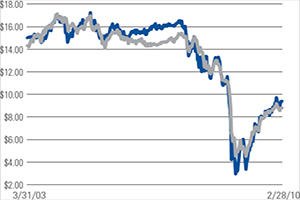

Market price, end of year | | $ | 9.39 | | $ | 4.05 | | $ | 12.50 | | $ | 16.08 | | $ | 15.69 | |

| | | | | | | | | | | | | | | | | |

Total Investment Return (1) | | | 166.37 | % | | (61.55 | )% | | (13.63 | )% | | 14.60 | % | | 14.30 | % |

| | | | | | | | | | | | | | | | | |

RATIOS/SUPPLEMENTAL DATA: | | | | | | | | | | | | | | | | |

Net assets, applicable to common shareholders, end of year (000s) | | $ | 644,408 | | $ | 348,544 | | $ | 895,043 | | $ | 1,050,149 | | $ | 1,017,779 | |

| | | | | | | | | | | | | | | | | |

Ratio of expenses to average net assets (2) | | | 1.39 | % | | 1.56 | %(3) | | 1.26 | % | | 1.27 | % | | 1.28 | %(3) |

| | | | | | | | | | | | | | | | | |

Ratio of net investment income to average net assets (2) | | | 14.21 | % | | 16.87 | % | | 11.26 | % | | 11.37 | % | | 10.03 | % |

| | | | | | | | | | | | | | | | | |

Preferred shares asset coverage per share | | $ | 70,125 | | $ | 49,406 | | $ | 67,626 | | $ | 74,981 | | $ | 73,442 | |

| | | | | | | | | | | | | | | | | |

Portfolio turnover | | | 58 | % | | 62 | % | | 33 | % | | 67 | % | | 52 | % |

| | | | | | | | | | | | | | | | | |

| |

(1) | Total investment return is calculated assuming a purchase of a share of common stock at the current market price on the first day of the period and a sale of a share of common stock at the current market price on the last day of each period reported. Dividends and distributions are assumed, for purposes of this calculation, to be reinvested at prices obtained under the Fund’s dividend reinvestment plan. Total investment return does not reflect brokerage commissions or sales charges. |

| |

(2) | Calculated on the basis of income and expenses applicable to both common shares and preferred shares relative to the average net assets of common shareholders. |

| |

(3) | Ratio of expenses to average net assets, excluding excise tax expense was 1.53% for the year ended February 28, 2009 and 1.26% for the year ended February 28, 2006. |

See accompanying Notes to Financial Statements | 2.28.10 | Nicholas-Applegate Convertible & Income Funds Annual Report 29

|

Nicholas-Applegate Convertible & Income Fund II Financial Highlights |

For a share of common stock outstanding throughout each period: |

| |

| | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | For the Period

July 1, 2005

through

February 28,

2006* | | Year ended

June 30,

2005 | |

| | Year ended | | | |

| | | | | |

| | February 28,

2010 | | February 28,

2009 | | February 29,

2008 | | February 28,

2007 | | | |

| | | | | | | | | | | | | |

Net asset value, beginning of period | | $ | 4.39 | | $ | 12.38 | | $ | 14.91 | | $ | 14.70 | | $ | 14.61 | | $ | 15.18 | |

| | | | | | | | | | | | | | | | | | | | |

Income from Investment Operations: | | | | | | | | | | | | | | | | | | | |

Net investment income | | | 0.98 | | | 1.55 | | | 1.70 | | | 1.69 | | | 1.04 | | | 1.59 | |

| | | | | | | | | | | | | | | | | | | | |

Net realized and change in unrealized gain (loss) on investments and interest rate caps | | | 3.80 | | | (8.05 | ) | | (2.17 | ) | | 0.61 | | | 0.58 | | | (0.39 | ) |

| | | | | | | | | | | | | | | | | | | | |

Total from investment operations | | | 4.78 | | | (6.50 | ) | | (0.47 | ) | | 2.30 | | | 1.62 | | | 1.20 | |

| | | | | | | | | | | | | | | | | | | | |

Dividends and Distributions on Preferred Shares from: | | | | | | | | | | | | | | | | | | | |

Net investment income | | | (0.01 | ) | | (0.20 | ) | | (0.45 | ) | | (0.38 | ) | | (0.17 | ) | | (0.21 | ) |

| | | | | | | | | | | | | | | | | | | | |

Net realized gain | | | — | | | — | | | — | | | (0.04 | ) | | (0.05 | ) | | (0.00 | )** |

| | | | | | | | | | | | | | | | | | | | |

Total dividends and distributions on preferred shares | | | (0.01 | ) | | (0.20 | ) | | (0.45 | ) | | (0.42 | ) | | (0.22 | ) | | (0.21 | ) |

| | | | | | | | | | | | | | | | | | | | |

Net increase (decrease) in net assets applicable to common shareholders resulting from investment operations | | | 4.77 | | | (6.70 | ) | | (0.92 | ) | | 1.88 | | | 1.40 | | | 0.99 | |

| | | | | | | | | | | | | | | | | | | | |

Dividends and Distributions to Common Shareholders from: | | | | | | | | | | | | | | | | | | | |

Net investment income | | | (1.14 | ) | | (1.29 | ) | | (1.61 | ) | | (1.42 | ) | | (1.05 | ) | | (1.42 | ) |

| | | | | | | | | | | | | | | | | | | | |

Net realized gains | | | — | | | — | | | — | | | (0.25 | ) | | (0.26 | ) | | (0.14 | ) |

| | | | | | | | | | | | | | | | | | | | |

Total dividends and distributions to common shareholders | | | (1.14 | ) | | (1.29 | ) | | (1.61 | ) | | (1.67 | ) | | (1.31 | ) | | (1.56 | ) |

| | | | | | | | | | | | | | | | | | | | |

Net asset value, end of period | | $ | 8.02 | | $ | 4.39 | | $ | 12.38 | | $ | 14.91 | | $ | 14.70 | | $ | 14.61 | |

| | | | | | | | | | | | | | | | | | | | |

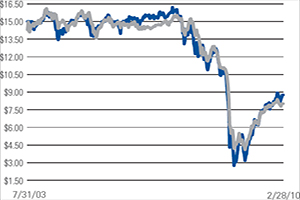

Market price, end of period | | $ | 8.76 | | $ | 3.73 | | $ | 12.09 | | $ | 15.42 | | $ | 15.14 | | $ | 14.74 | |

| | | | | | | | | | | | | | | | | | | | |

Total Investment Return (1) | | | 174.62 | % | | (63.34 | )% | | (12.08 | )% | | 13.99 | % | | 12.10 | % | | 16.44 | % |

| | | | | | | | | | | | | | | | | | | | |

RATIOS/SUPPLEMENTAL DATA: | | | | | | | | | | | | | | | | | | | |

Net assets, applicable to common shareholders, end of period (000s) | | $ | 487,130 | | $ | 263,220 | | $ | 735,359 | | $ | 879,014 | | $ | 850,769 | | $ | 834,909 | |

| | | | | | | | | | | | | | | | | | | | |

Ratio of expenses to average net assets (2) | | | 1.42 | % | | 1.71 | %(4) | | 1.35 | %(4) | | 1.34 | % | | 1.37 | %(3)(4) | | 1.35 | % |

| | | | | | | | | | | | | | | | | | | | |

Ratio of net investment income to average net assets (2) | | | 14.20 | % | | 17.26 | % | | 11.75 | % | | 11.56 | % | | 10.57 | %(3) | | 9.79 | % |

| | | | | | | | | | | | | | | | | | | | |

Preferred shares asset coverage per share | | $ | 69,445 | | $ | 49,015 | | $ | 61,410 | | $ | 68,493 | | $ | 67,096 | | $ | 66,319 | |

| | | | | | | | | | | | | | | | | | | | |

Portfolio turnover | | | 58 | % | | 57 | % | | 34 | % | | 60 | % | | 33 | % | | 67 | % |

| | | | | | | | | | | | | | | | | | | | |

| |

* | During the period the Fund’s fiscal year-end changed from June 30 to February 28. |

| |

** | Less than $0.005 per share. |

| |

(1) | Total investment return is calculated assuming a purchase of a share of common stock at the current market price on the first day of the period and a sale of a share of common stock at the current market price on the last day of each period reported. Dividends and distributions are assumed, for purposes of this calculation, to be reinvested at prices obtained under the Fund’s dividend reinvestment plan. Total investment return does not reflect brokerage commissions or sales charges. Total investment return for a period of less than one year is not annualized. |

| |

(2) | Calculated on the basis of income and expenses applicable to both common shares and preferred shares relative to the average net assets of common shareholders. |

| |

(3) | Annualized. |

| |

(4) | Ratio of expenses to average net assets, excluding excise tax expense was 1.63% for the year ended February 28, 2009, 1.34% for the year ended February 29, 2008 and 1.35% for the period July 1, 2005 through February 28, 2006. |

30 Nicholas-Applegate Convertible & Income Funds Annual Report | 2.28.10 | See accompanying Notes to Financial Statements

|

Nicholas-Applegate Convertible & Income Funds Report of Independent Registered Public Accounting Firm |

|

| |

To the Shareholders and Board of Trustees of:

Nicholas-Applegate Convertible & Income Fund

Nicholas-Applegate Convertible & Income Fund II

In our opinion, the accompanying statements of assets and liabilities, including the schedules of investments, and the related statements of operations and of changes in net assets and the financial highlights present fairly, in all material respects, the financial position of the Nicholas-Applegate Convertible & Income Fund and Nicholas-Applegate Convertible & Income Fund II (the “Funds”) at February 28, 2010, the results of each of their operations, changes in net assets and the financial highlights for each of the periods presented, in conformity with accounting principles generally accepted in the United States of America. These financial statements and financial highlights (hereafter referred to as “financial statements”) are the responsibility of the Funds’ management. Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits of these financial statements in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audits, which included confirmation of securities at February 28, 2010, by correspondence with the custodian and brokers, provide a reasonable basis for our opinion.

PricewaterhouseCoopers LLP

New York, New York

April 20, 2010

2.28.10 | Nicholas-Applegate Convertible & Income Funds Annual Report 31

|

Nicholas-Applegate Convertible & Income Funds Tax Information (unaudited) |

| |

Tax Information:

|

Convertible & Income |

Pursuant to the Jobs and Growth Tax Relief Reconciliation Act of 2003, the Fund designates 10.16% of ordinary dividends paid by the Fund during the year ended February 28, 2010 as Qualified Dividend Income (or the maximum allowable amount). |

|

The percentage of ordinary dividends paid by the Fund during the year ended February 28, 2010, which qualified for the Dividends Received Deduction available to corporate shareholders was 8.51% or the maximum allowable amount. |

|

Convertible & Income II |

Pursuant to the Jobs and Growth Tax Relief Reconciliation Act of 2003, the Fund designates 9.26% of ordinary dividends paid by the Fund during the year ended February 28, 2010 as Qualified Dividend Income (or the maximum allowable amount). |

|

The percentage of ordinary dividends paid by the Fund during the year ended February 28, 2010, which qualified for the Dividends Received Deduction available to corporate shareholders was 7.77% or the maximum allowable amount. |

|

Since the Funds’ tax year is not the calendar year, another notification will be sent with respect to calendar year 2010. In January 2011, shareholders will be advised on IRS Form 1099 DIV as to the federal tax status of dividends and distributions received during calendar 2010. The amount that will be reported will be the amount to use on your 2010 federal income tax return and may differ from the amount which must be reported in connection with the Funds’ tax year ended February 28, 2010. Shareholders are advised to consult their tax advisers as to the federal, state and local tax status of the dividend income received from the Funds. |

32 Nicholas-Applegate Convertible & Income Funds Annual Report | 2.28.10

| |

Nicholas-Applegate Convertible & Income Funds | Annual Shareholder Meeting

Results/Board of Trustees Changes

(unaudited) |

| | |

Annual Shareholder Meeting Results:

The Funds held their joint annual meeting of shareholders on July 14, 2009. Common/Preferred shareholders voted as indicated below:

| | | | | | | |

| | Affirmative | | Withheld

Authority | |

| | | | | | |

Convertible & Income | | | | | | | |

Re-election of Paul Belica—Class III to serve until 2012 | | | 64,895,145 | | | 2,608,849 | |

Re-election of John C. Maney**—Class III to serve until 2012 | | | 64,950,714 | | | 2,553,280 | |

Election of Diana L. Taylor*†—Class II to serve until 2011 | | | 10,761 | | | 312 | |

Messrs. Hans W. Kertess, James A. Jacobson***, William B. Ogden, IV and R. Peter Sullivan, III continue to serve as Trustees of the Convertible & Income Fund.

| | | | | | | |

Convertible & Income II | | | | | | | |

Re-election of Hans W. Kertess—Class III to serve until 2012 | | | 51,169,985 | | | 2,112,025 | |

Re-election of John C. Maney**—Class III to serve until 2012 | | | 51,258,807 | | | 2,023,203 | |

Election of Diana L. Taylor*†—Class II to serve until 2011 | | | 8,325 | | | 171 | |

| | | | | | | |

Messrs. Paul Belica, James A. Jacobson***, William B. Ogden, IV and R. Peter Sullivan, III continue to serve as Trustees of the Convertible & Income Fund II. |

| |

| | |

* | Preferred Shares Trustee. |

** | John C. Maney is an interested Trustee of the Funds. |

*** | Mr. Jacobson joined the Board of Trustees on December 14, 2009. |

† | Resigned from the Board of Trustees on September 10, 2009. |

| | |

| Mr. Robert E. Connor* served as a Trustee of the Funds until his death on April 8, 2010. |

| | |

Board of Trustees Changes:

On September 10, 2009, Diana L. Taylor resigned as Trustee of the Funds.

On December 14, 2009, James A. Jacobson joined the Board of Trustees.

2.28.10 | Nicholas-Applegate Convertible & Income Funds Annual Report 33

| |

Nicholas-Applegate Convertible & Income Funds | Privacy Policy/Proxy Voting

Policies & Procedures

(unaudited) |

| | |

|

Privacy Policy: |

|

Our Commitment to You |

We consider customer privacy to be a fundamental aspect of our relationship with clients. We are committed to maintaining the confidentiality, integrity, and security of our current, prospective and former clients’ personal information. We have developed policies designed to protect this confidentiality, while allowing client needs to be served. |

|

Obtaining Personel Information |

In the course of providing you with products and services, we may obtain non-public personal information about you. This information may come from sources such as account applications and other forms, from other written, electronic or verbal correspondence, from your transactions, from your brokerage or financial advisory firm, financial adviser or consultant, and/or from information captured on our internet web sites. |

|

Respecting Your Privacy |

We do not disclose any personal or account information provided by you or gathered by us to non-affiliated third parties, except as required or permitted by law. As is common in the industry, non-affiliated companies may from time to time be used to provide certain services, such as preparing and mailing prospectuses, reports, account statements and other information, conducting research on client satisfaction, and gathering shareholder proxies. We may also retain non-affiliated companies to market our products and enter in joint marketing agreements with other companies. These companies may have access to your personal and account information, but are permitted to use the information solely to provide the specific service or as otherwise permitted by law. We may also provide your personal and account information to your brokerage or financial advisory firm and/or to your financial adviser or consultant. |

|

Sharing Information with Third Parties |

We do reserve the right to disclose or report personal information to non-affiliated third parties in limited circumstances where we believe in good faith that disclosure is required under law, to cooperate with regulators or law enforcement authorities, to protect our rights or property, or upon reasonable request by any mutual fund in which you have chosen to invest. In addition, we may disclose information about you or your accounts to a non-affiliated third party with the consent or at your request or if you consent in writing to the disclosure. |

|

Sharing Information with Affiliates |

We may share client information with our affiliates in connection with servicing your account or to provide you with information about products and services that we believe may be of interest to you. The information we share may include, for example, your participation in our mutual funds or other investment programs, your ownership of certain types of accounts (such as IRAs), or other data about your accounts. Our affiliates, in turn, are not permitted to share your information with non-affiliated entities, except as required or permitted by law. |

|

Procedures to Safeguard Private Information |

We take seriously the obligation to safeguard shareholder non-public personal information. In addition to this policy, we have also implemented procedures that are designed to restrict access to a shareholder’s non-public personal information only to internal personnel who need to know that information in order to provide products or services to you. In order to guard your non-public personal information, physical, electronic and procedural safeguards are in place. |

| |

|

Proxy Voting Policies & Procedures: |

|

A description of the policies and procedures that the Funds have adopted to determine how to vote proxies relating to portfolio securities and information about how the Funds voted proxies relating to portfolio securities held during the most recent twelve month period ended June 30, is available (i) without charge, upon request, by calling the Funds’ shareholder servicing agent at (800) 254-5197; (ii) on the Funds’ website at www.allianzinvestors.com/closedendfunds; and (iii) on the Securities and Exchange Commission’s website at www.sec.gov. |

34 Nicholas-Applegate Convertible & Income Funds Annual Report | 2.28.10

| |

Nicholas-Applegate Convertible & Income Funds | Dividend Reinvestment Plan

(unaudited) |

| | |

| |

Dividend Reinvestment Plan: |

| |

Pursuant to the Funds’ Dividend Reinvestment Plan (the “Plan”), all Common Shareholders whose shares are registered in their own names will have all dividends, including any capital gain dividends, reinvested automatically in additional Common Shares by PNC Global Investment Servicing, as agent for the Common Shareholders (the “Plan Agent”), unless the shareholder elects to receive cash. An election to receive cash may be revoked or reinstated at the option of the shareholder. In the case of record shareholders such as banks, brokers or other nominees that hold Common Shares for others who are the beneficial owners, the Plan Agent will administer the Plan on the basis of the number of Common Shares certified from time to time by the record shareholder as representing the total amount registered in such shareholder’s name and held for the account of beneficial owners who are to participate in the Plan. Shareholders whose shares are held in the name of a bank, broker or nominee should contact the bank, broker or nominee for details. All distributions to investors who elect not to participate in the Plan (or whose broker or nominee elects not to participate on the investor’s behalf), will be paid cash by check mailed, in the case of direct shareholder, to the record holder by PNC Global Investment Servicing, as the Funds’ dividend disbursement agent. |

|

Unless you elect (or your broker or nominee elects) not to participate in the Plan, the number of Common Shares you will receive will be determined as follows: |

|

(1) | If on the payment date the net asset value of the Common Shares is equal to or less than the market price per Common Share plus estimated brokerage commissions that would be incurred upon the purchase of Common Shares on the open market, the Fund will issue new shares at the greater of (i) the net asset value per Common Share on the payment date or (ii) 95% of the market price per Common Share on the payment date; or |

| |

(2) | If on the payment date the net asset value of the Common Shares is greater than the market price per Common Share plus estimated brokerage commissions that would be incurred upon the purchase of Common Shares on the open market, the Plan Agent will receive the dividend or distribution in cash and will purchase Common Shares in the open market, on the New York Stock Exchange or elsewhere, for the participants’ accounts. It is possible that the market price for the Common Shares may increase before the Plan Agent has completed its purchases. Therefore, the average purchase price per share paid by the Plan Agent may exceed the market price on the payment date, resulting in the purchase of fewer shares than if the dividend or distribution had been paid in Common Shares issued by the Funds. The Plan Agent will use all dividends and distributions received in cash to purchase Common Shares in the open market on or shortly after the payment date, but in no event later than the ex-dividend date for the next distribution. Interest will not be paid on any uninvested cash payments. |

| |

You may withdraw from the Plan at any time by giving notice to the Plan Agent. If you withdraw or the Plan is terminated, you will receive a certificate for each whole share in your account under the Plan and you will receive a cash payment for any fraction of a share in your account. If you wish, the Plan Agent will sell your shares and send you the proceeds, minus brokerage commissions. |

|

The Plan Agent maintains all shareholders’ accounts in the Plan and gives written confirmation of all transactions in the accounts, including information you may need for tax records. The Plan Agent will also furnish each person who buys Common Shares with written instructions detailing the procedures for electing not to participate in the Plan and to instead receive distributions in cash. Common Shares in your account will be held by the Plan Agent in non-certificated form. Any proxy you receive will include all Common Shares you have received under the Plan. |

|

There is no brokerage charge for reinvestment of your dividends or distributions in Common Shares. However, all participants will pay a pro rata share of brokerage commissions incurred by the Plan Agent when it makes open market purchases. |

|

Automatically reinvested dividends and distributions are taxed in the same manner as cash dividends and distributions. |

|

The Funds and the Plan Agent reserve the right to amend or terminate the Plan. There is no direct service charge to participants in the Plan; however, the Funds reserve the right to amend the Plan to include a service charge payable by the participants. Additional information about the Plan may be obtained from the Funds’ shareholder servicing agent, PNC Global Investment Servicing, P.O. Box 43027, Providence, RI 02940-3027, telephone number (800) 254-5197. |

2.28.10 | Nicholas-Applegate Convertible & Income Funds Annual Report 35

|

Nicholas-Applegate Convertible & Income Funds Board of Trustees (unaudited) |

| |

| | |

Name, Date of Birth, Position(s) Held

with Funds, Length of Service, Other

Trusteeships/Directorships Held by

Trustee; Number of Portfolios in Fund

Complex/Outside Fund Complexes

Currently Overseen by Trustee | | Principal Occupation(s) During Past 5 Years: |

| |

The address of each trustee is 1345 Avenue of the Americas, New York, NY 10105. |

| | |

Hans W. Kertess

Date of Birth: 7/12/39

Chairman of the Board of Trustees since: 2007

Trustee since: 2004—NCV/ 2003—NCZ

Term of office: Expected to stand for re-election

at 2010—NCV/ 2012—NCZ annual meeting

of shareholders.

Trustee/Director of 49 Funds in Fund Complex;

Trustee/Director of no funds outside of Fund Complex | | President, H. Kertess & Co., a financial advisory company. Formerly, Managing Director, Royal Bank of Canada Capital Markets. |

| | |

Paul Belica

Date of Birth: 9/27/21

Trustee since: 2003

Term of office: Expected to stand for re-election

at 2012—NCV/ 2010—NCZ annual meeting

of shareholders.

Trustee/Director of 49 funds in Fund Complex

Trustee/Director of no funds outside of Fund Complex | | Retired. Formerly Director, Student Loan Finance Corp., Education Loans, Inc., Goal Funding, Inc., Goal Funding II, Inc. and Surety Loan Fund, Inc. Formerly, Manager of Stratigos Fund LLC, Whistler Fund LLC, Xanthus Fund LLC & Wynstone Fund LLC. |

| | |

James A. Jacobson

Date of Birth: 2/3/45

Trustee since: 2009

Term of office: Expected to stand for election

at 2010 annual meeting of shareholders.

Trustee/Director of 44 funds in Fund Complex

Trustee/Director of 16 funds in Alpine Mutual

Funds Complex | | Retired. Formerly, Vice Chairman and Managing Director of Spear, Leeds & Kellogg Specialists, LLC, specialist firm on the New York Stock Exchange. |

| | |

William B. Ogden, IV

Date of Birth: 1/11/45

Trustee since: 2006

Term of office: Expected to stand for re-election

at 2010 annual meeting of shareholders

Trustee/Director of 49Funds in Fund Complex;

Trustee/Director of no funds outside of Fund Complex | | Asset Management Industry Consultant. Formerly, Managing Director, Investment Banking Division of Citigroup Global Markets Inc. |

| | |

R. Peter Sullivan, III

Date of Birth: 9/4/41

Trustee since: 2004—NCV/ 2006—NCZ

Term of office: Expected to stand for re-election

at 2011 annual meeting of shareholders

Trustee/Director of 49 funds in Fund Complex

Trustee/Director of no funds outside of Fund Complex | | Retired. Formerly, Managing Partner, Bear Wagner Specialists LLC, specialist firm on the New York Stock Exchange. |

36 Nicholas-Applegate Convertible & Income Funds Annual Report | 2.28.10

| |

Nicholas-Applegate Convertible & Income Funds Board of Trustees |

| (unaudited) (continued) |

| |

| | |

Name, Date of Birth, Position(s) Held

with Funds, Length of Service, Other

Trusteeships/Directorships Held by

Trustee; Number of Portfolios in Fund

Complex/Outside Fund Complexes

Currently Overseen by Trustee | | Principal Occupation(s) During Past 5 Years: |

| |

|

John C. Maney†

Date of Birth: 8/3/59

Trustee since: 2006

Term of office: Expected to stand for re-election

at 2012annual meeting of shareholders.

Trustee/Director of 78 Funds in Fund Complex

Trustee/Director of No Funds outside the Fund Complex | | Management Board of Allianz Global Investors Fund Management LLC; Management Board and Managing Director of Allianz Global Investors of America L.P. since January 2005 and also Chief Operating Officer of Allianz Global Investors of America L.P. since November 2006. |

| |

† | Mr. Maney is an “interested person” of the Funds due to his affiliation with Allianz Global Investors of America L.P. In addition to Mr. Maney’s positions set forth in the table above, he holds the following positions with affiliated persons: Management Board, Managing Director and Chief Operating Officer of Allianz Global Investors of America L.P. and Allianz Global Investors of America LLC; Member - Board of Directors and Chief Operating Officer of Allianz Global Investors of America Holdings Inc. and Oppenheimer Group, Inc.; Managing Director and Chief Operating Officer of Allianz Global Investors NY Holdings LLC; Management Board and Managing Director of Allianz Global Investors U.S. Holding LLC; Managing Director and Chief Operating Officer of Allianz Hedge Fund Partners Holding L.P. and Allianz Global Investors U.S. Retail LLC; Member – Board of Directors and Managing Director of Allianz Global Investors Advertising Agency Inc.; Compensation Committee of NFJ Investment Group LLC; Management Board of Management Board of Allianz Global Investors Fund Management LLC, Allianz Global Investors Management Partners LLC and Nicholas-Applegate Holdings LLC; Member – Board of Directors and Chief Operating Officer of PIMCO Global Advisors (Resources) Limited; Executive Vice President of PIMCO Japan Ltd; Chief Operating Officer of Allianz Global Investors U.S. Holding II LLC; and Member and Chairman – Board of Directors, President and Chief Operating Officer of PFP Holdings, Inc. |

Further information about certain of the Funds’ Trustees is available in the Funds’ Statements of Additional Information, dated May 21, 2003 (for the Nicholas-Applegate Convertible & Income Fund) and September 25, 2003 (for Nicholas-Applegate Convertible & Income Fund II), which can be obtained, without charge, by calling the Funds’ shareholder servicing agent at (800) 254-5197.

2.28.10 | Nicholas-Applegate Convertible & Income Funds Annual Report 37

|

Nicholas-Applegate Convertible & Income Funds Fund Officers (unaudited) |

| |

| | |

Name, Date of Birth, Position(s) Held with Funds | | Principal Occupation(s) During Past 5 Years: |

| |

| | |

Brian S. Shlissel

Date of Birth: 11/14/64

President & Chief Executive Officer since: 2003 | | Managing Director, Head of Mutual Fund Services, Allianz Global Investors Fund Management LLC; President and Chief Executive Officer of 33 funds in the Fund Complex; Treasurer, Principal Financial and Accounting Officer of 45 funds in the Fund Complex and The Korea Fund, Inc. Formerly, Director of 4 funds in the Fund Complex, 2002-2008. |

| | |

Lawrence G. Altadonna

Date of Birth: 3/10/66

Treasurer, Principal Financial and Accounting Officer

since: 2003 | | Senior Vice President, Director of Fund Administration, Allianz Global Investors Fund Management LLC; Treasurer, Principal Financial and Accounting Officer of 33 funds in the Fund Complex; Assistant Treasurer of 45 funds in the Fund Complex and The Korea Fund, Inc. |

| | |

Thomas J. Fuccillo

Date of Birth: 3/22/68

Vice President, Secretary & Chief Legal Officer

since: 2004 | | Executive Vice President, Chief Legal Officer and Secretary of Allianz Global Investors Fund Management LLC; Executive Vice President of Allianz Global Investors of America L.P; Vice President, Secretary and Chief Legal Officer of 78 funds in the Fund Complex; Secretary and Chief Legal Officer of The Korea Fund, Inc. |

| | |

Scott Whisten

Date of Birth: 3/13/71

Assistant Treasurer since: 2007 | | Senior Vice President, Allianz Global Investors Fund Management LLC; Assistant Treasurer of 78 funds in the Fund Complex. Formerly, Accounting Manager, Prudential Investments, 2000-2005. |

| | |

Richard J. Cochran

Date of Birth: 1/23/61

Assistant Treasurer since: 2008 | | Vice President, Allianz Global Investors Fund Management LLC; Assistant Treasurer of 78 funds in the Fund Complex; Formerly, Tax Manager, Teachers Insurance Annuity Association/College Retirement Equity Fund (TIAA-CREF), 2002-2008. |

| | |

Youse E. Guia

Date of Birth: 9/3/72

Chief Compliance Officer since: 2004 | | Senior Vice President and Chief Compliance Officer of Allianz Global Investors of America L.P.; Chief Compliance Officer of 78 funds in the Fund Complex and The Korea Fund, Inc. |

| | |

Kathleen A. Chapman

Date of Birth: 11/11/54

Assistant Secretary since: 2006 | | Assistant Secretary of 78 funds in the Fund Complex. Formerly, Manager – Individual Investor Group Advisory Law, Morgan Stanley, 2004-2005. |

| | |

Lagan Srivastava

Date of Birth: 9/20/77

Assistant Secretary since: 2006 | | Assistant Secretary of 78 funds in the Fund Complex and The Korea Fund, Inc. Formerly, Research Assistant, Dechert LLP, 2004-2005. |

Officers hold office at the pleasure of the Board and until their successors are appointed and qualified or until their earlier resignation or removal.

38 Nicholas-Applegate Convertible & Income Funds Annual Report | 2.28.10

| |

Trustees | Fund Officers |

Hans W. Kertess | Brian S. Shlissel |

Chairman of the Board of Trustees | President & Chief Executive Officer |

Paul Belica | Lawrence G. Altadonna |

James A. Jacobson | Treasurer, Principal Financial & Accounting Officer |

John C. Maney | Thomas J. Fuccillo |

William B. Ogden, IV | Vice President, Secretary & Chief Legal Officer |

R. Peter Sullivan III | Scott Whisten |

| Assistant Treasurer |

| Richard J. Cochran |

| Assistant Treasurer |

| Youse E. Guia |

| Chief Compliance Officer |

| Kathleen A. Chapman |

| Assistant Secretary |

| Lagan Srivastava |

| Assistant Secretary |

| |

Investment Manager | |

Allianz Global Investors Fund Management LLC | |

1345 Avenue of the Americas | |

New York, NY 10105 | |

| |

Sub-Adviser | |

Nicholas-Applegate Capital Management LLC | |

600 West Broadway, 30th Floor | |

San Diego, CA 92101 | |

| |

Custodian & Accounting Agent | |

Brown Brothers Harriman & Co. | |

40 Water Street | |

Boston, MA 02109 | |

| |

Transfer Agent, Dividend Paying Agent and Registrar | |

PNC Global Investment Servicing | |

P.O. Box 43027 | |

Providence, RI 02940-3027 | |

| |

Independent Registered Public Accounting Firm | |

PricewaterhouseCoopers LLP | |

300 Madison Avenue | |

New York, NY 10017 | |

| |

Legal Counsel | |

Ropes & Gray LLP | |

One International Place | |

Boston, MA 02110-2624 | |

This report, including the financial information herein, is transmitted to the shareholders of Nicholas-Applegate Convertible & Income Fund and Nicholas-Applegate Convertible & Income Fund II for their information. It is not a prospectus, circular or representation intended for use in the purchase of shares of the Funds or any securities mentioned in this report.

Notice is hereby given in accordance with Section 23(c) of the Investment Company Act of 1940, as amended, that from time to time the Funds may purchase shares of their common stock in the open market.

The Funds file their complete schedule of portfolio holdings with the Securities and Exchange Commission (“SEC”) for the first and third quarters of their fiscal year on Form N-Q. The Funds’ Form N-Q is available on the SEC’s website at www.sec.gov and may be reviewed and copied at the SEC’s Public Reference Room in Washington, DC. Information on the operation of the Public Reference Room may be obtained by calling (800) SEC-0330. The information on Form N-Q is also available on the Funds’ website at www.allianzinvestors.com/closedendfunds.

Information on the Funds is available at www.allianzinvestors.com/closedendfunds or by calling the Funds’ shareholder servicing agent at (800) 254-5197.

Receive this report electronically and eliminate paper mailings.

To enroll, go to www.allianzinvestors.com/edelivery.

ITEM 2. CODE OF ETHICS

| | |

| (a) | As of the end of the period covered by this report, the registrant has adopted a code of ethics (the “Section 406 Standards for Investment Companies — Ethical Standards for Principal Executive and Financial Officers”) that applies to the registrant’s Principal Executive Officer and Principal Financial Officer; the registrant’s Principal Financial Officer also serves as the Principal Accounting Officer. The registrant undertakes to provide a copy of such code of ethics to any person upon request, without charge, by calling 1-800-254-5197. The code of ethics is included as an Exhibit 99.CODEETH hereto. |

| | |

| (b) | During the period covered by this report, there were not any amendments to a provision of the code of ethics adopted in 2(a) above. |

| | |

| (c) | During the period covered by this report, there were not any waivers or implicit waivers to a provision of the code of ethics adopted in 2(a) above. |

ITEM 3. AUDIT COMMITTEE FINANCIAL EXPERT

The registrant’s Board has determined that Mr. Paul Belica, a member of the Board’s Audit Oversight Committee is an “audit committee financial expert,” and that he is “independent,” for purposes of this Item.

ITEM 4. PRINCIPAL ACCOUNTANT FEES AND SERVICES

| | |

| a) | Audit fees. The aggregate fees billed for each of the last two fiscal years (the “Reporting Periods”) for professional services rendered by the Registrant’s principal accountant (the “Auditor”) for the audit of the Registrant’s annual financial statements, or services that are normally provided by the Auditor in connection with the statutory and regulatory filings or engagements for the Reporting Periods were $54,000 in 2009 and $54,000 in 2010. |

| | |

| b) | Audit-Related Fees. The aggregate fees billed in the Reporting Periods for assurance and related services by the principal accountant that are reasonably related to the performance of the audit registrant’s financial statements and are not reported under paragraph (e) of this Item were $40,000 in 2009 and $10,000 in 2010. These services consist of accounting consultations, agreed upon procedure reports (inclusive of review of basic maintenance testing associated with the Preferred Shares), attestation reports and comfort letters. |

| | |

| c) | Tax Fees. The aggregate fees billed in the Reporting Periods for professional services rendered by the Auditor for tax compliance, tax service and tax planning (“Tax Services”) were $13,650 in 2009 and $13,650 in 2010. These services consisted of review or preparation of U.S. federal, state, local and excise tax returns and calculation of excise tax distributions. |

| | |

| d) | All Other Fees. There were no other fees billed in the Reporting Periods for products and services provided by the Auditor to the Registrant. |

| | |

| e) | 1. Audit Committee Pre-Approval Policies and Procedures. The Registrant’s Audit Committee has established policies and procedures for pre-approval of all audit and permissible non-audit services by the Auditor for the Registrant, as well as the Auditor’s engagements related directly to the operations and financial reporting of the Registrant. The Registrant’s policy is stated below. |

| | |

| | Nicholas-Applegate Convertible & Income Fund (The “Fund”) |

AUDIT OVERSIGHT COMMITTEE POLICY FOR PRE-APPROVAL OF SERVICES PROVIDED BY THE INDEPENDENT ACCOUNTANTS

The Fund’s Audit Oversight Committee (“Committee”) is charged with the oversight of the Fund’s financial reporting policies and practices and their internal controls. As part of this responsibility, the Committee must pre-approve any independent accounting firm’s engagement to render audit and/or permissible non-audit services, as required by law. In evaluating a proposed engagement by the independent accountants, the Committee will assess the effect that the engagement might reasonably be expected to have on the accountant’s independence. The Committee’s evaluation will be based on:

| |

| a review of the nature of the professional services expected to provided, |

| |

| the fees to be charged in connection with the services expected to be provided, a |

| |

| review of the safeguards put into place by the accounting firm to safeguard independence, and |

| |

| periodic meetings with the accounting firm. |

POLICY FOR AUDIT AND NON-AUDIT SERVICES TO BE PROVIDED TO THE FUNDS

On an annual basis, the Fund’s Committee will review and pre-approve the scope of the audits of the Funds and proposed audit fees and permitted non-audit (including audit-related) services that may be performed by the Fund’s independent accountants. At least annually, the Committee will receive a report of all audit and non-audit services that were rendered in the previous calendar year pursuant to this Policy. In addition to the Committee’s pre-approval of services pursuant to this Policy, the engagement of the independent accounting firm for any permitted non-audit service provided to the Fund will also require the separate written pre-approval of the President of the Fund, who will confirm, independently, that the accounting firm’s engagement will not adversely affect the firm’s independence. All non-audit services performed by the independent accounting firm will be disclosed, as required, in filings with the Securities and Exchange Commission.

AUDIT SERVICES

The categories of audit services and related fees to be reviewed and pre-approved annually by the Committee are:

| |

| Annual Fund financial statement audits |

| Seed audits (related to new product filings, as required) |

| SEC and regulatory filings and consents |

AUDIT-RELATED SERVICES

The following categories of audit-related services are considered to be consistent with the role of the Fund’s independent accountants and services falling under one of these categories will be pre-approved by the Committee on an annual basis if the Committee deems those services to be consistent with the accounting firm’s independence:

| |

| Accounting consultations |

| Fund merger support services |

| Agreed upon procedure reports (inclusive of the annual review of Basic Maintenance testing associated with issuance of Preferred Shares) |

| Other attestation reports |

| Comfort letters |

| Other internal control reports |

Individual audit-related services that fall within one of these categories and are not presented to the Committee as part of the annual pre-approval process described above, may be pre-approved, if deemed consistent with the accounting firm’s independence, by the Committee Chair (or any other Committee member who is a disinterested trustee under the Investment Company Act to whom this responsibility has been delegated) so long as the estimated fee for those services does not exceed $250,000. Any such pre-approval shall be reported to the full Committee at its next regularly scheduled meeting.

TAX SERVICES

The following categories of tax services are considered to be consistent with the role of the Fund’s independent accountants and services falling under one of these categories will be pre-approved by the Committee on an annual basis if the Committee deems those services to be consistent with the accounting firm’s independence:

Tax compliance services related to the filing or amendment of the following:

| |

| Federal, state and local income tax compliance; and, sales and use tax compliance |

| Timely RIC qualification reviews |

| Tax distribution analysis and planning |

| Tax authority examination services |

| Tax appeals support services |

| Accounting methods studies

Fund merger support service |

| Other tax consulting services and related projects |

Individual tax services that fall within one of these categories and are not presented to the Committee as part of the annual pre-approval process described above, may be pre-approved, if deemed consistent with the accounting firm’s independence, by the Committee Chairman (or any other Committee member who is a disinterested trustee under the Investment Company Act to whom this responsibility has been delegated) so long as the estimated fee for those services does not exceed $250,000. Any such pre-approval shall be reported to the full Committee at its next regularly scheduled meeting.

PROSCRIBED SERVICES

The Fund’s independent accountants will not render services in the following categories of non-audit services:

| |

| Bookkeeping or other services related to the accounting records or financial statements of the Funds |

| Financial information systems design and implementation |

| Appraisal or valuation services, fairness opinions, or contribution-in-kind reports |

| Actuarial services |

| Internal audit outsourcing services |

| Management functions or human resources |

| Broker or dealer, investment adviser or investment banking services |

| Legal services and expert services unrelated to the audit |

| Any other service that the Public Company Accounting Oversight Board determines, by regulation, is impermissible |

PRE-APPROVAL OF NON-AUDIT SERVICES PROVIDED TO OTHER ENTITIES WITHIN THE FUND COMPLEX

The Committee will pre-approve annually any permitted non-audit services to be provided to Allianz Global Investors Fund Management LLC or any other investment manager to the Funds (but not including any sub-adviser whose role is primarily portfolio management and is sub-contracted by the investment manager) (the “Investment Manager”) and any entity controlling, controlled by, or under common control with the Investment Manager that provides ongoing services to the Fund (including affiliated sub-advisers to the Fund), provided, in each case, that the engagement relates directly to the operations and financial reporting of the Fund (such entities, including the Investment Manager, shall be referred to herein as the “Accounting Affiliates”). Individual projects that are not presented to the Committee as part of the annual pre-approval process, may be pre-approved, if deemed consistent with the accounting firm’s independence, by the Committee Chairman (or any other Committee member who is a disinterested trustee under the Investment Company Act to whom this responsibility has been delegated) so long as the estimated fee for those services does not exceed $250,000. Any such pre-approval shall be reported to the full Committee at its next regularly scheduled meeting.

Although the Committee will not pre-approve all services provided to the Investment Manager and its affiliates, the Committee will receive an annual report from the Funds’ independent accounting firm showing the aggregate fees for all services provided to the Investment Manager and its affiliates.

DE MINIMUS EXCEPTION TO REQUIREMENT OF PRE-APPROVAL OF NON-AUDIT SERVICES

With respect to the provision of permitted non-audit services to a Fund or Accounting Affiliates, the pre-approval requirement is waived if:

| | | |

| | (1) | The aggregate amount of all such permitted non-audit services provided constitutes no more than (i) with respect to such services provided to the Fund, five percent (5%) of the total amount of revenues paid by the Fund to its independent accountant during the fiscal year in which the services are provided, and (ii) with respect to such services provided to Accounting Affiliates, five percent (5%) of the total amount of revenues paid to the Fund’s independent accountant by the Fund and the Accounting Affiliates during the fiscal year in which the services are provided; |

| | | |

| | (2) | Such services were not recognized by the Fund at the time of the engagement for such services to be non-audit services; and |

| | | |

| | (3) | Such services are promptly brought to the attention of the Committee and approved prior to the completion of the audit by the Committee or by the Committee Chairman (or any other Committee member who is a disinterested trustee under the Investment Company Act to whom this Committee Chairman or other delegate shall be reported to the full Committee at its next regularly scheduled meeting. |

| | | |

| | | e) 2. No services were approved pursuant to the procedures contained in paragraph (C) (7) (i) (C) of Rule 2-01 of Registration S-X. |

| | | |

| f) | Not applicable |

| | | |

| g) | Non-audit fees. The aggregate non-audit fees billed by the Auditor for services rendered to the Registrant, and rendered to the Adviser, for the 2009 Reporting Period was $361,835 and the 2010 Reporting Period was $566,790. |

| | | |

| h) | Auditor Independence. The Registrant’s Audit Oversight Committee has considered whether the provision of non-audit services that were rendered to the Adviser which were not pre-approved is compatible with maintaining the Auditor’s independence. |

ITEM 5. AUDIT COMMITTEE OF LISTED REGISTRANT

The Fund has a separately designated standing audit committee established in accordance with Section 3(a)(58)(A) of the Securities Exchange Act of 1934. The audit committee of the Fund is comprised of Paul Belica, Hans W. Kertess, R. Peter Sullivan III, William B. Ogden, IV and James A. Jacobson.

ITEM 6. SCHEDULE OF INVESTMENTS

Schedule of Investments is included as part of the report to shareholders filed under Item 1 of this form.

ITEM 7. DISCLOSURE OF PROXY VOTING POLICIES AND PROCEDURES FOR CLOSED-END MANAGEMENT INVESTMENT COMPANIES.

Nicholas-Applegate Convertible & Income Fund (NCV)

(the “trust”)

PROXY VOTING POLICY

| |

1. | It is the policy of the Trust that proxies should be voted in the interest of its shareholders, as determined by those who are in the best position to make this determination. The Trust believes that the firms and/or persons purchasing and selling securities for the Trust and analyzing the performance of the Trust’s securities are in the best position and have the information necessary to vote proxies in the best interests of the Trust and its shareholders, including in situations where conflicts of interest may arise between the interests of shareholders, on one hand, and the interests of the investment adviser, a sub-adviser and/or any other affiliated person of the Trust, on the other. Accordingly, the Trust’s policy shall be to delegate proxy voting responsibility to those entities with portfolio management responsibility for the Trust. |

| |

2. | The Trust delegates the responsibility for voting proxies to Allianz Global Investors Fund Management LLC (“AGIFM”), which will in turn delegate such responsibility to the sub-adviser of the Trust. AGIFM’s Proxy Voting Policy Summary is attached as Appendix A hereto. A summary of the detailed proxy voting policy of the Trust’s current sub-adviser is set forth in Appendix B attached hereto. Such summary may be revised from time to time to reflect changes to the sub-adviser’s detailed proxy voting policy. |

| |

3. | The party voting the proxies (i.e., the sub-adviser) shall vote such proxies in accordance with such party’s proxy voting policies and, to the extent consistent with such policies, may rely on information and/or recommendations supplied by others. |

| |

4. | AGIFM and the sub-adviser of the Trust with proxy voting authority shall deliver a copy of its respective proxy voting policies and any material amendments thereto to the applicable Board of the Trust promptly after the adoption or amendment of any such policies. |

| |

5. | The party voting the proxy shall: (i) maintain such records and provide such voting information as is required for the Trust’s regulatory filings including, without limitation, Form N-PX and the required disclosure of policy called for by Item 18 of Form N-2 and Item 7 of Form N-CSR; |

| |

| and (ii) shall provide such additional information as may be requested, from time to time, by the Board or the Trust’s Chief Compliance Officer. |

| |

6. | This Proxy Voting Policy Statement (including Appendix B), the Proxy Voting Policy Summary of AGIFM and summary of the detailed proxy voting policy of the sub-adviser of the Trust with proxy voting authority, shall be made available (i) without charge, upon request, by calling 1-800-254-5197 and (ii) on the Trust’s website at www.allianzinvestors.com. In addition, to the extent required by applicable law or determined by the Trust’s Chief Compliance Officer or Board of Trustees, the Proxy Voting Policy Summary of AGIFM and summary of the detailed proxy voting policy of the Trust’s sub-adviser with proxy voting authority shall also be included in the Trust’s Registration Statements or Form N-CSR filings. |

Appendix A

ALLIANZ GLOBAL INVESTORS FUND MANAGEMENT LLC (“AGIFM”)

| |

1. | It is the policy of AGIFM that proxies should be voted in the interest of the shareholders of the applicable fund, as determined by those who are in the best position to make this determination. AGIFM believes that the firms and/or persons purchasing and selling securities for the funds and analyzing the performance of the funds’ securities are in the best position and have the information necessary to vote proxies in the best interests of the funds and their shareholders, including in situations where conflicts of interest may arise between the interests of shareholders, on one hand, and the interests of the investment adviser, a sub-adviser and/or any other affiliated person of the fund, on the other. Accordingly, AGIFM’s policy shall be to delegate proxy voting responsibility to those entities with portfolio management responsibility for the funds. |

| |

2. | AGIFM, for each fund which it acts as an investment adviser, delegates the responsibility for voting proxies to the sub-adviser for the respective fund, subject to the terms hereof. |

| |

3. | The party voting the proxies (e.g., the sub-adviser) shall vote such proxies in accordance with such party’s proxy voting policies and, to the extent consistent with such policies, may rely on information and/or recommendations supplied by others. |

| |

4. | AGIFM and each sub-adviser of a fund shall deliver a copy of its respective proxy voting policies and any material amendments thereto to the board of the relevant fund promptly after the adoption or amendment of any such policies. |

| |

5. | The party voting the proxy shall: (i) maintain such records and provide such voting information as is required for such funds’ regulatory filings including, without limitation, Form N-PX and the required disclosure of policy called for by Item 18 of Form N-2 and Item 7 of Form N-CSR; and (ii) shall provide such additional information as may be requested, from time to time, by such funds’ respective boards or chief compliance officers. |

| |

6. | This Proxy Voting Policy Summary and summaries of the proxy voting policies for each sub-adviser of a fund advised by AGIFM shall be available (i) without charge, upon request, by calling 1-800-426-0107 and (ii) at www.allianzinvestors.com. In addition, to the extent required by applicable law or determined by the relevant fund’s board of directors/trustees or chief compliance officer, this Proxy Voting Policy Summary and summaries of the detailed proxy voting policies of each sub-adviser and each other entity with proxy voting authority for a fund advised by AGIFM shall also be included in the Registration Statement or Form N-CSR filings for the relevant fund. |

Appendix B

Nicholas-Applegate Capital Management LLC (“NACM”)

Description of Proxy Voting Policy and Procedures

NACM votes proxies on behalf of its clients pursuant to its written Proxy Policy Guidelines and Procedures (the “Proxy Guidelines”), unless a client requests otherwise. The Proxy Guidelines are designed to honor NACM’s fiduciary duties to its clients and protect and enhance its clients’ economic welfare and rights.

The Proxy Guidelines are established by a Proxy Committee consisting of executive, investment, sales, marketing, compliance and operations personnel. The Proxy Guidelines reflect NACM’s normal voting positions on specific corporate actions, including but not limited to those relating to social and corporate responsibility issues, stock option plans and other management compensation issues, changes to a portfolio company’s capital structure and corporate governance. For example, NACM generally votes for proposals to declassify boards and generally supports proposals that remove restrictions on shareholders’ ability to call special meetings independently of management. Some issues will require a case-by-case analysis.

The Proxy Guidelines largely follow the recommendations of Glass, Lewis & Co. LLC (“Glass Lewis”), an investment research and proxy advisory firm. The Proxy Guidelines may not apply to every situation and NACM may vote differently than specified by the Proxy Guidelines and/or contrary to Glass Lewis’ recommendation if NACM reasonably determines that to do so is in its clients’ best interest. Any variance from the Proxy Guidelines is documented.

In the case of a potential conflict of interest, NACM’s Proxy Committee will be responsible for reviewing the potential conflict and will have the final decision as to how the relevant proxy should be voted.

Under certain circumstances, NACM may in its reasonable discretion refrain from voting clients’ proxies due to cost or other factors.

ITEM 8.

(a)(1) Nicholas-Applegate Capital Management LLC (“Nicholas-Applegate” or the “Investment Adviser”)

As of April 29, 2010, the following individuals constitute the team that has primary responsibility for the day-to-day implementation of the Nicholas-Applegate Convertible & Income Fund (NCV) with Mr. Forsyth serving as the lead portfolio manager:

Douglas G. Forsyth, CFA

Managing Director, Portfolio Manager

Doug Forsyth has been the lead portfolio manager since inception (March 2003 - NCV) and (July 2003 - NCZ) and oversees Nicholas-Applegate’s Income and Growth Strategies portfolio management and research teams and is a member of the firm’s Executive Committee. Prior to joining Nicholas-Applegate in 1994, Doug was a securities analyst at AEGON USA, where he was responsible for financial and strategic analysis of high yield securities. Mr. Forsyth

was previously a research assistant at The University of Iowa, where he earned his B.B.A. in finance. He has eighteen years of investment industry experience.

Justin Kass, CFA

Managing Director, Portfolio Manager