The following items were the subject of a Form 12b-25 and are included herein: portions of Items 3, portions of Item 4, Item 5, Item 11, Item 15, Item 18 and Item 19 (Exhibits 12.1, 12.2 and 13). |

As filed with the Securities and Exchange Commission on July 17, 2007.

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F/A

(Amendment No. 1)

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2006

Commission file number 001-32555

MASISA S.A.

(formerly known as Terranova S.A.)

(Exact name of Registrant as specified in its charter)

Republic of Chile

(Jurisdiction of incorporation or organization)

Av. Apoquindo 3650, Piso 10, Las Condes, Santiago, Chile

(Address of principal executive offices)

Securities registered or to be registered pursuant to Section 12(b) or the Act:

Title of each class | Name of each exchange on which registered | |

| None | None |

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

American Depositary Shares

Common Stock

Number of outstanding shares as of December 31, 2006:

Common Stock: 5,667,750,881

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check One):

Large accelerated filer ¨ | Accelerated filer x | Non-accelerated filer ¨ |

Indicate by check mark which financial statement item the registrant has elected to follow. Item 17 ¨ Item 18 x

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

EXPLANATORY NOTE

Pursuant to Rule 12b-25 under the Securities Exchange Act of 1934, as amended, our Company, Masisa S.A., previously filed parts of this Annual Report on Form 20-F on July 2, 2007. We are amending and restating this annual report in its entirety in order to include the selected financial data, management's discussion and analysis of financial condition and results of operations, management's annual report on internal control over financial reporting, financial statements and other information required by Items 3, 4, 5, 11, 15 and 18, as well as certain exhibits to the filing. This Amendment No. 1 on Form 20-F/A does not reflect events occurring after the filing of the original Annual Report on Form 20-F on July 2, 2007.

TABLE OF CONTENTS

| Page | |

| PART I | |

| Item 1. Identity of Directors, Senior Management and Advisers | 1 |

| Item 2. Offer Statistics and Expected Timetable | 1 |

| Item 3. Key Information | 1 |

| Selected Financial Data | 1 |

| Exchange Rates | 3 |

| Risk Factors | 3 |

| Item 4. Information on the Company | 12 |

| Our Company | 12 |

| Our Competitive Strengths | 13 |

| History and Development of the Company | 14 |

| The Merger of Terranova and Masisa | 16 |

| Corporate Structure | 16 |

| The Grupo Nueva Group and Our Management Framework | 18 |

| Business Strategy | 19 |

| Operational Organization | 20 |

| Facilities and Offices | 21 |

| Description of Properties | 22 |

| Capital Expenditures | 24 |

| Principal Products | 24 |

| Wood Products Sales | 27 |

| Markets and Distribution | 28 |

| Production | 40 |

| Forestry Operations | 48 |

| Insurance | 52 |

| Raw Materials and Suppliers | 52 |

| Environmental Regulation | 55 |

| Item 4A. Unresolved Staff Comments | 59 |

| Item 5. Operating and Financial Review and Prospects | 59 |

| Introduction | 59 |

| Overview | 59 |

| Results of Operations | 62 |

| Liquidity and Capital Resources | 77 |

| Research and Development | 83 |

-ii-

Table of Contents

(continued)

| Page | |

| Trend Information | 83 |

| Off-Balance Sheet Arrangements | 83 |

| Contractual Obligations | 83 |

| Impact of Inflation and Devaluation | 84 |

| Critical Accounting Policies | 84 |

| Item 6. Directors, Senior Management and Employees | 87 |

| Directors | 87 |

| Board Committees | 88 |

| Senior Management | 90 |

| Director and Executive Officer Compensation | 92 |

| Share Ownership | 93 |

| Employees | 93 |

| Item 7. Major Shareholders and Related Party Transactions | 95 |

| Major Shareholders | 95 |

| Related Party Transactions | 97 |

| Item 8. Financial Information | 98 |

| Consolidated Financial Statements | 98 |

| Export Sales | 98 |

| Legal and Arbitration Proceedings | 98 |

| Dividend Policy | 99 |

| Significant Changes | 100 |

| Item 9. The Offer and Listing | 100 |

| Stock Price History | 100 |

| Markets | 101 |

| Item 10. Additional Information | 101 |

| Memorandum and Articles of Association | 101 |

| Material Contracts | 107 |

| Exchange Controls | 107 |

| Taxation | 108 |

| Documents on Display | 113 |

| Summary of Significant Differences between the Company’s Corporate Governance Practices and the NYSE’s Corporate Governance Standards | 114 |

| Item 11. Quantitative and Qualitative Disclosure About Market Risk | 114 |

| Qualitative Disclosure | 114 |

| Quantitative Disclosure | 114 |

-iii-

Table of Contents

(continued)

| Page | |

| Item 12. Description of Securities Other than Equity Securities | 118 |

| PART II | |

| Item 13. Defaults, Dividend Arrearages and Delinquencies | 119 |

| Item 14. Material Modifications to the Rights of Security Holders and Use of Proceeds | 119 |

| Item 15. Controls and Procedures | 119 |

| Item 16A. Audit Committee Financial Expert | 121 |

| Item 16B. Code of Ethics | 122 |

| Item 16C. Principal Accountant Fees and Services | 122 |

| Item 16D. Exemptions from the Listing Standards for Audit Committees | 122 |

| Item 16E. Purchase of Equity Securities by the Issuer and Affiliated Purchasers | 123 |

| PART III | |

| Item 17. Financial Statements | 124 |

| Item 18. Financial Statements | 124 |

| Item 19. Exhibits | 125 |

-iv-

PRESENTATION OF INFORMATION

Masisa S.A. is a publicly held corporation (sociedad anónima abierta) organized under the laws of Chile.

We changed our name to Masisa S.A. on May 31, 2005 as part of our merger with our former subsidiary, which was known as Masisa S.A. before that merger. Prior to that merger, our name was Terranova S.A. Except as otherwise specifically noted, when in this document we refer to “Terranova” or “Terranova S.A.” we are referring to ourselves and our consolidated subsidiaries prior to our merger with our former subsidiary Masisa S.A. Prior to the consummation of that merger of Masisa into and with Terranova, Terranova owned 52.43% of the shares of Masisa and Masisa was one of Terranova’s consolidated subsidiaries. When we describe Terranova we include our former subsidiary Masisa S.A. and its consolidated subsidiaries in that description.

When in this annual report we refer to “Masisa” or “Masisa S.A.” with respect to any date after the merger on May 31, 2005, those terms, together with the terms “we”, “our”, “us” and the “Company” refer to our merged company and its consolidated subsidiaries. When we refer to “Masisa” or “Masisa S.A.” with respect to any date before May 31, 2005, we mean our former subsidiary Masisa S.A. and its consolidated subsidiaries before its merger into and with us, and separate from the other businesses of Terranova S.A.

In this document, unless otherwise specified, all references to “Chilean pesos,” “pesos” or “Ch$” are to Chilean pesos, references to “U.S. dollars,” “dollars” or “US$” are to United States dollars, references to the “Consumer Price Index” or “CPI” are to the Indice de Precios al Consumidor published by the Chilean Instituto Nacional de Estadísticas (“Chilean National Institute of Statistics”) and references to “UF” or “Unidades de Fomento” are to Unidades de Fomento, a Chilean financial index adjusted for changes in the CPI. The Company publishes its financial statements in U.S. dollars. Unless otherwise specified, financial data in our consolidated financial statements and elsewhere in this document are presented in accordance with accounting principles generally accepted in Chile (“Chilean GAAP”). Chilean GAAP differs in certain significant respects from accounting principles generally accepted in the United States (“U.S. GAAP”). Note 23 of our audited consolidated financial statements appearing elsewhere in this document provides a description of the principal differences between Chilean GAAP and U.S. GAAP, and contains a reconciliation to U.S. GAAP of our total shareholders’ equity as of December 31, 2005 and 2006 and our net income for the years ended December 31, 2005 and December 31, 2006, respectively.

For the convenience of the reader, certain amounts have been translated from Chilean pesos into U.S. dollars at the rate specified herein. U.S. dollar equivalent information related to acquisitions, dispositions or other corporate transactions described in this document is based on the Dólar Observado (the “Observed Exchange Rate”) in effect at the relevant time of such transactions. No representation is made that the Ch$ or US$ amounts shown in this document could have been or could be converted into US$ or Ch$, as the case may be, at any particular rate. The Observed Exchange Rate, as would be used for accounting purposes, for December 31, 2006 was Ch$532.39= US$1.00. See “Item 3. Key Information—Exchange Rates” for information regarding historical exchange rates since January 2002. The UF on December 31, 2006 had a value of Ch$18,358.28.

Each “hectare” or “ha” equals approximately 2.471 acres, each “kilometer” equals approximately 0.621 miles, each “cubic meter” or “m3” equals approximately 35.315 cubic feet or 1.308 cubic yards and each “metric ton” equals 1,000 kilograms or approximately 2,205 pounds.

Percentages and certain amounts contained in this annual report have been rounded for ease of presentation. Any discrepancies in any figure between totals and the sums of the amounts presented are due to rounding market information.

This annual report contains statements that constitute forward looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These statements appear throughout this annual report and include statements regarding the intent, belief or current expectations of the Company and its management, including with respect to

· the Company’s business, plans and operations,

-v-

· trends affecting the Company’s financial condition or results of operations and

· the future impact of competition and regulations.

Such forward looking statements are not guarantees of future performance and involve risks and uncertainties. Actual results may differ from those described in such forward looking statements included in this annual report, depending upon a number of factors, including without limitation

· the ability of the Company to implement its business plan,

· the nature and extent of future competition in the Company’s principal markets and

· political, economic and demographic developments in Chile, Argentina, Brazil, Mexico, Venezuela and other markets.

See “Item 5. Operating and Financial Review and Prospects” for further discussion of factors that could cause such material differences.

We have prepared this annual report on the basis of information which we have or have obtained from sources we believe to be reliable. You are urged to consult your own legal, tax and business advisors regarding an investment in our shares of common stock or ADSs.

-vi-

PART I

Item 1. Identity of Directors, Senior Management and Advisers

Not applicable.

Item 2. Offer Statistics and Expected Timetable

Not applicable.

Item 3. Key Information

Selected Financial Data

The following table presents certain historical financial information about us at the dates and for each of the indicated periods. The following table should be read in conjunction with, and is qualified in its entirety by our financial statements appearing elsewhere in this document. The financial statements are prepared in accordance with Chilean GAAP, which differs in certain significant respects from U.S. GAAP. Note 23 to our audited consolidated financial statements appearing elsewhere in this document provides a description of the material differences between Chilean GAAP and U.S. GAAP and a reconciliation to U.S. GAAP of net income and shareholders’ equity as of and for the years ended December 31, 2005 and 2006.

1

SELECTED FINANCIAL INFORMATION

As of and for the year ended December 31, | ||||||||||||||||

2002 | 2003 | 2004 | 2005(1) | 2006 | ||||||||||||

| (in millions of US$, except per share and per ADS amounts) | US$ | US$ | US$ | US$ | US$ | |||||||||||

| INCOME STATEMENT DATA | ||||||||||||||||

| Chilean GAAP: | ||||||||||||||||

| Net sales | 295.0 | 480.1 | 651.0 | 744.0 | 886.5 | |||||||||||

| Operating income | 28.7 | 21.6 | 95.1 | 79.5 | 83.6 | |||||||||||

| Non-operating results, net | (6.1 | ) | (47.5 | ) | (11.2 | ) | (47.6 | ) | (41.4 | ) | ||||||

| Income taxes | 1.7 | 0.6 | (11.7 | ) | (13.1 | ) | (23.3 | ) | ||||||||

| Net income | 21.0 | (20.0 | ) | 56.8 | 24.4 | 29.5 | ||||||||||

Net earnings per share (2) | 0.007 | (0.006 | ) | 0.014 | 0.005 | 0.005 | ||||||||||

Net earnings per ADS (3) | 0.36 | (0.30 | ) | 0.72 | 0.27 | 0.26 | ||||||||||

Dividends per share (2) | — | — | — | 0.011 | 0.002 | |||||||||||

Dividends per ADS (3) | — | — | — | 0.57 | 0.10 | |||||||||||

| U.S. GAAP: | ||||||||||||||||

| Net sales | — | 485.9 | 651.0 | 744.0 | 886.5 | |||||||||||

| Operating income | — | 12.9 | 138.2 | 73.9 | 72.0 | |||||||||||

| Net income | — | (30.2 | ) | 71.4 | 24.9 | 24.5 | ||||||||||

| Basic and diluted earnings per share | — | (0.009 | ) | 0.018 | 0.005 | 0.004 | ||||||||||

Net earnings per ADS (2) | — | (0.45 | ) | 0.91 | 0.27 | 0.22 | ||||||||||

| Weighted average number of shares (in thousands) | 2,940,285 | 3,391,168 | 3,918,428 | 4,591,227 | 5,664,496 | |||||||||||

| BALANCE SHEET DATA | ||||||||||||||||

| Chilean GAAP | ||||||||||||||||

| Total assets | 1,630.1 | 1,854.5 | 1,880.5 | 1,956.5 | 2,007.5 | |||||||||||

| Long-term liabilities | 377.8 | 518.4 | 533.9 | 333.8 | 542.1 | |||||||||||

| Shareholders’ equity | 656.6 | 730.6 | 778.1 | 1,094.3 | 1,186.4 | |||||||||||

| U.S. GAAP | ||||||||||||||||

| Shareholders’ equity | — | 520.6 | 574.9 | 874.8 | 937.6 | |||||||||||

| (1) | Our consolidated financial statements under Chilean GAAP for the year ended December 31, 2005, previously issued in the Chilean market, have been restated to reflect an adjustment for inventory costing of approximately US$1.9 million. See Note 2 a) to our audited consolidated financial statements appearing elsewhere in this document. |

| (2) | Under Chilean GAAP, there are no authoritative pronouncements relating to the calculation of earnings per share. For comparative purposes, the calculation has been based on the same number of weighted average shares outstanding as used for the U.S. GAAP calculation. For more information see Note 23 to our audited consolidated financial statements appearing elsewhere in this document. |

| (3) | Per ADS amounts are determined by multiplying per share amounts by 50, because one ADS is equal to 50 shares of common stock. |

2

Exchange Rates

The following table sets forth the annual low, high, average and period-end Observed Exchange Rates for U.S. dollars, as would be used for accounting purposes, for each year beginning in 2002, as reported by the Chilean Central Bank, expressed in peso per U.S. dollar.

Daily Observed Exchange Rate Ch$ per US$ | |||||||||||||

Year | Low(1) | High(1) | Average(2) | Period End | |||||||||

| 2002 | 641.75 | 756.56 | 688.94 | 718.61 | |||||||||

| 2003 | 593.10 | 758.21 | 691.40 | 593.80 | |||||||||

| 2004 | 559.21 | 649.45 | 609.52 | 557.40 | |||||||||

| 2005 | 509.70 | 592.75 | 559.77 | 512.50 | |||||||||

| 2006 | 511.44 | 549.63 | 530.28 | 532.39 | |||||||||

Low(1) | High(1) | ||||||

2006 | |||||||

| December | 524.78 | 534.43 | |||||

2007 | |||||||

| January | 538.27 | 545.18 | |||||

| February | 535.29 | 548.67 | |||||

| March | 535.36 | 541.95 | |||||

| April | 525.96 | 539.69 | |||||

| May | 517.64 | 527.62 | |||||

Source: The Central Bank of Chile.

| (1) | Rates shown are the actual low and high, on a day-to-day basis, for each period. |

| (2) | Average of month end rates. |

The Observed Exchange Rate, as would be used for accounting purposes, on December 31, 2006 and on June 15, 2007 were Ch$532.39 = US$1.00 and Ch$526.43 = US$1.00, respectively.

Risk Factors

A decision to invest in our shares or ADSs involves certain risks. Below, we discuss significant risks, including

| · | Risks relating to our business, |

| · | Risks relating to our forestry operations, |

| · | Risks relating to our operations in Latin America, and |

| · | Risks relating to the securities markets and the ownership of our ADSs and shares. |

You should read carefully these risk factors before deciding whether to invest in our company.

Risks relating to our business

We are dependent on the furniture and construction industries and lower than expected growth or a downturn in demand for our products in those industries could adversely affect our results of operations.

The sales of our products are dependent to a significant degree on the level of activity in the furniture manufacturing and construction industries. In recent years we have expanded our production capacity for medium-density fiberboard (“MDF”), particle board, oriented strand board (“OSB”) and MDF mouldings in the expectation of growth in demand. Because of the cyclicality of demand for our products, we may have short- or long-term overcapacity as a result of this expansion and other capital expenditures, and decreased demand for wood products may result in an inability to maximize our productive resources. Furthermore, it is possible that the expected growth in demand from companies in the furniture manufacturing and construction industries may not occur. The demand for such products can be adversely affected by several factors, including decreases in the level of new residential construction activity, which is subject to changes in economic conditions, increases in interest rates, decreases in population and other factors. Additionally, weakness in the economies of countries in which we sell our products as well as any downturn or continuation of current downturns in these economies, is likely to have a material adverse effect on the construction, home building and remodeling industries, as well as on the demand for furniture items manufactured with our products.

3

We face competition in the markets in which we sell our products. Increased competition from new competitors or increased production capacity by existing competitors could adversely affect both our share of our markets as well as the price at which we sell our products.

Currently, we face competition from competitors in most of the countries and regions in which we operate. In addition, we may face increased competition as a result of existing competitors increasing their production capacity or from new competitors entering the markets in which we operate. An increase in competition in the markets in which we operate could adversely affect both our share of those markets as well as the price at which we are able to sell our products.

The majority of raw wood materials and resins used to produce our board products are supplied by outside mills and companies.

Our boards are produced by combining wood chips, wood shavings, strands and sawdust. We procure the majority of the raw wood materials that we use to manufacture our boards from unaffiliated companies in Chile, Argentina, Mexico and Brazil in accordance with long standing relationships between us and the suppliers. We may not be able to maintain these relationships and continue to secure the raw materials to produce our boards at existing commercial conditions in the future. In addition, the prices we pay for raw materials may increase as a result of higher fuel costs paid by our suppliers. An inability to secure the raw materials used in the production of our boards or to transport such materials in a cost-effective manner could have a material adverse effect on our operations.

We may experience manufacturing problems in Brazil due to a lack of supply of logs.

In Brazil, we depend on a large supply of logs to produce our wood products. Our Brazilian OSB mill and saw mills depend to a large extent on supplies of pulp log and saw log from third parties. We have experienced a tight market in Brazil in the past and we may not be able to continue to secure logs for our mills.

Adverse developments relating to maritime transport and import and export restrictions could adversely affect our results of operations.

Our ability to make, transport and sell our products in some of our key markets could be affected by import and export restrictions as well as the general market unavailability of maritime transport. If our ability to sell our products competitively in one or more of our principal export markets were to be impaired by import or export restrictions, it could be difficult for us to re-allocate our products to other markets on equally favorable terms. In addition, as we depend on maritime means to transport products to offshore markets, increases in fuel prices, other transport costs or maritime demand may also increase our shipping costs. These challenges to the maritime transport of our products and the regulation of the sale of our products in offshore markets could have a material adverse effect on our profitability.

Our dependence on a limited number of distributors and customers may affect our profitability.

We are dependent to a significant degree on a small number of third-party distributors to achieve our sales in one or more of our principal markets. For example, our eight largest customers for solid wood products accounted for approximately 82% and 84% of net sales in the United States for the years ended December 31, 2005 and 2006, respectively. Our solid wood products sales made in the United States represented approximately 22% and 23% of our total consolidated sales for the years ended December 31, 2005 and December 31, 2006, respectively. Our largest customer, Masonite International (“Masonite”), accounted for approximately 52% and 41% of such solid wood products’ sales during the years ended December 31, 2005 and 2006, respectively. We cannot assure you that, under current market conditions, the loss of our largest distributor or customer in certain markets would not have a material adverse effect on us.

4

We may not be able to maintain present favorable tax treatment or exemptions from certain tax payments in certain jurisdictions in which we operate.

We may not be able to maintain important exemptions from certain tax regimes in the various jurisdictions in which we operate. Currently, Chilean tax authorities are challenging our treatment of certain losses related to our Venezuelan subsidiaries in previous tax years. We estimate that an adverse determination by Chilean tax authorities would affect approximately US$39.2 million of our deferred taxes, recoverable taxes and tax losses already utilized. See Note 21 to our audited consolidated financial statements appearing elsewhere in this document. Unfavorable tax treatment of our company in the future or an increase in the taxes levied on us, may have a material adverse effect on our results of operations.

Currency devaluations and foreign exchange fluctuations may adversely affect us.

We are exposed, both in terms of assets and liabilities, to fluctuations in the value of the U.S. dollar versus other currencies. Changes in the value against the U.S. dollar of the Chilean peso and other currencies in which we complete transactions, such as Argentinean pesos, Brazilian reales, Mexican pesos, Venezuelan bolivares and Colombian pesos, among others, could adversely affect our financial condition and results of operations. The Chilean peso, Argentinean peso, Brazilian real, Mexican peso, Venezuelan bolivar and Colombian peso, among others, have each been subject to large nominal devaluation events in the past. The value of any of these currencies against the U.S. dollar may fluctuate significantly in the future. A significant part of our indebtedness is denominated in U.S. dollars and certain of our revenues and operating expenses are denominated in local currencies. As a result, fluctuations in the local currency/U.S. dollar exchange rate may affect our financial condition and results of operations. For example, as a result of the Chilean peso appreciation and Venezuelan bolivar devaluation during 2006, we saw a loss of US$7.0 and US$10.8 million in our consolidated financial statements related to our assets and liabilities denominated in each of these currencies, respectively. In addition, as our boards business is mostly a local business and our solid wood business is mostly an export business, part of our sales are denominated in local currencies and part are denominated in U.S. dollars. As our production cost is partially dependent on wood and resin prices, which in the medium- and long-term are correlated to the U.S. dollar, part of our costs are indexed to the U.S. dollar. As a result, a decrease in the value of the U.S. dollar against the currencies of other countries from which we export products can also negatively affect our sales margins on sales of such products.

Inflation could adversely affect the value of our ADSs and financial condition and results of operations.

In the past, Latin American countries in which we operate have experienced high levels of inflation and significant changes in the levels of inflation. For example, in the late 1980s and in 1990, Chile’s inflation rate exceeded 20%. Although recent inflation levels in Chile have been below 10% for the last 10 years and below 5% since 1999, including inflation of 3.4% in 2006, high levels of inflation in the future could adversely affect the Chilean economy and have an adverse effect on our results of operations and, indirectly, the value of our common shares and of our ADSs. We estimate, for example, that a 1% increase in the annual inflation rate in Chile not accompanied by a devaluation of the Chilean Peso against the U.S. dollar would reduce our consolidated gross margin as a percentage of sales by less than 0.3 percentage points. See “Item 5. Operating and Financial Review and Prospects.”

Changes in environmental regulations to which we are subject could adversely affect our results of operations and prospects.

We are subject to changing international, national and local environmental laws concerning, among other things, health, the handling and disposal of wastes, discharges into the air, soil and water, forestry management and endangered species. During 2004, 2005, and 2006, we spent on a consolidated basis US$3.2 million, US$3.6 million and US$3.5 million, respectively, on environmental projects related to complying with environmental regulation. We expect to continue to make the necessary expenditures to comply with such environmental requirements. Changes in such laws, or the interpretation of such laws, may require us to incur significant unforeseen capital or operating expenditures to comply with such requirements.

5

A significant percentage of our employees are unionized and work slowdowns, work stoppages or strikes could adversely affect our results of operations.

Approximately 67%, 50%, 35% and 5% of our employees in Chile, Venezuela, Mexico and Brazil, respectively, are covered by collective bargaining agreements with labor unions. Most of these collective bargaining agreements have terms of two to four years, although collective bargaining agreements in Mexico have a term of one year. If a work slowdown, a work stoppage or strike were to occur prior to or upon the expiration of our various collective bargaining agreements, that work slowdown, stoppage or strike could adversely affect our sales and cash flows and have a material adverse effect on our business, financial condition, results of operations or prospects.

Risks factors relating to our forestry operations

Wind storms, fires, disease and pests could adversely affect our forests.

Our forests are subject to naturally occurring threats such as wind and fire. Damage caused by strong windstorms in Chile, such as uprooting and stems breakage, is considered by management to be a major natural risk to our forests. Fire is a risk to all of our forests, warehouses and operations. For example, in January 2007, we suffered a forest fire in the Bio-Bio region of Chile which burned approximately 1,171 hectares. We may experience other fires in the future and such fires may materially adversely affect us. Disease or pests may also have a material adverse effect on our forests and plantations in the future. Although our business and results of operations have not been materially adversely affected by these risks in the past, there can be no assurance that this will be the case in the future.

We may experience difficulties with the quality of service provided by some of our contractors and our forestry operations could be adversely affected.

We use third-party contractors that provide us specialized services in our forestry operations such as planting, harvesting and trucking. If our service contractors do not continue to fulfill past quality levels, or if our contractual relationships become the subject of litigation or regulation, our forestry operations could be adversely affected.

Conflict with native communities or other social movements in Chile and Brazil could threaten a portion of our forestry assets.

Chilean law protects the rights of indigenous people. Since 1992, disputes have arisen among Chile’s indigenous communities and the forestry industry. We are currently named in three land disputes with communities claiming rights to ancestral lands or rights based on titles granted by decree at the beginning of the 19th century. These disputes could imply partial or total overlap with our legal titles to the land involved in such disputes. The land involved in these disputes totals 1,701 hectares, of which 351 hectares correspond to planted forests (i.e. representing less than 1% of our total planted forest holdings). Since 2002, we have been in negotiations with several communities and their representatives in order to resolve and avoid possible conflicts. It is possible that we might not be able to resolve the ongoing disputes with native communities in Chile. In addition, since 1995, the Brazilian organization “Movimiento de los Trabajadores Rurales Sin Tierra” (MST) has been initiating public action to promote agrarian reform and the expropriation of property from large land estates in Brazil. We are not currently named in any land dispute with MST. A deterioration of our relationship with indigenous peoples and other social movements could affect our forestry operations and have a material adverse effect on our company.

Risks factors relating to our operations in Latin America

Political and economic developments in Latin American countries in which we operate, may adversely affect us.

Our business strategies, financial condition and results of operations could be adversely affected by changes in government policies of the Latin American countries in which we operate, other political developments in or affecting these countries, and regulatory and legal changes or administrative practices of their authorities, over which we have no control. In addition, recent rates of gross domestic product growth in these countries may not continue in the future, and future developments in or affecting their economies could impair our ability to proceed with our business plan or materially adversely affect our business, financial condition or results of operations.

6

Energy shortages and increased energy costs in Chile could adversely affect our business.

Starting in April 2004 and continuing to the present, Argentina began restricting deliveries of natural gas to Chile due to supply and distribution problems in Argentina, Chile’s principal supplier. Such restrictions have led to reduced supplies of natural gas to Chilean electricity producers, particularly during winter months. A significant portion of Chile’s electricity is produced from natural gas. Shortages of natural gas have forced and could continue to force Chile’s electric utilities to use costlier petroleum based fuels to produce electricity or could cause disruptions in the supply of electricity. While we do not use material amounts of natural gas directly, during 2006 electricity represented approximately 9.4% of our wood board production costs in Chile compared to 9.9% in 2005. In 2007, we were unable to renew certain long-term electricity contracts related to our Cabrero industrial complex in Chile at our previous rates. As a result, we are experiencing higher electricity costs as we have had to rely on purchases in the electricity spot market. For the five months ended May 31, 2007, our electricity costs represented approximately 14.7% of our wood board production costs in Chile. In addition, Chile and Brazil have each experienced energy shortages or disruptions in the past. Higher electricity costs or disruptions in the supply of electricity or natural gas could materially adversely affect our financial condition and results of operations.

Foreign exchange controls established by the Venezuelan government may limit our ability to transfer excess funds out of Venezuela.

The Ministry of Finance and the Central Bank of Venezuela established the system for administration of foreign exchange and fixed the official exchange rate for purchases and sales of Venezuelan bolivars by the Central Bank of Venezuela. These rules restrict our access to foreign exchange and limit our ability to transfer excess funds out of Venezuela. As of December 31, 2006, foreign currency activities have not been fully normalized and requests for approval for foreign currency exchange continue to be limited. Dividend payments, debt payments and foreign transfers of income from capital and interest, to individuals and corporations must be registered with the Superintendencia de Inversiones Extranjeras (Foreign Investment Superintendency). If the Foreign Investment Superintendency denies the approval of our dividend payments, debt payments or foreign transfers of income, we will be prohibited from, or will face increased costs for, transferring such funds from our subsidiaries in Venezuela to our operations outside that country.

Adverse Argentinean political and economic conditions may have a direct and adverse impact on our Argentinean operations.

In 2002, the Argentinean economy experienced critical difficulties. During the first six months of 2002, the Argentinean government eliminated the U.S. dollar-Argentinean peso parity resulting in a devaluation of Argentina’s currency in 2002 of 237%. Additionally, the Argentinean government imposed restrictions on cash withdrawals from bank accounts, on transfers of funds from Argentinean to foreign accounts and publicly announced its inability to pay its debt to foreign lenders. During 2002, Argentina also experienced higher rates of unemployment and a general inflation of prices. Consequently, Argentina’s “country risk” rose to record high levels. In 2003, the economy began to recover and some of the government financial restrictions were lifted. Since 2004, the Argentinean economy has continued its recovery.

Because our business strategy in Argentina is to some extent focused on anticipated growth in demand for particle board and MDF, our Argentinean operations and results of operations could be negatively affected if Argentina’s economy falls back into a recession.

7

Risk factors relating to the securities markets and the ownership of our ADSs and shares

The market price of our securities may be adversely affected by developments in other emerging markets.

The market value of securities of Chilean companies is, to varying degrees, affected by economic and market conditions in other emerging market countries. Investors’ reactions to developments in any of these other countries may have an adverse effect on the market value of securities of Chilean issuers regardless of whether or not economic conditions in Chile are comparable to those countries. Events in other countries, particularly Argentina, Venezuela and other emerging market countries, could adversely affect the market value of, or market for, our common stock or ADSs.

The significant share ownership of our controlling shareholders may have an adverse effect on the future market price of our ADSs and shares.

Grupo Nueva S.A. (“Grupo Nueva”), a Chilean holding company formerly known as Compañía de Inversiones Suizandina S.A., beneficially owns directly, and indirectly through its subsidiary Inversiones Forestales Los Andes S.A., in the aggregate 53.3% of our outstanding shares of common stock. A disposition by Grupo Nueva of a significant number of our shares, or the perception that such a disposition might occur, could adversely affect the trading price of our shares on the Santiago Stock Exchange (“Bolsa de Comercio de Santiago”), the Valparaíso Stock Exchange (“Bolsa de Corredores de Valparaíso”), the Chilean Electronic Stock Exchange (“Bolsa Electrónica de Chile”) as well as the market price of our ADSs on the New York Stock Exchange.

Our controlling shareholders are able to exercise significant control over our company, and also own a significant minority interest in many of our international subsidiaries which could result in conflicts of interest.

Grupo Nueva is in a position to direct our management and to determine the result of substantially all matters to be decided by majority vote of our shareholders, including the election of a majority of the members of our board of directors, determining the amount of dividends distributed by us (subject to the legally mandated minimum of 30% of net income), adopting certain amendments to our by-laws, enforcing or waiving our rights under existing agreements, leases and contractual arrangements. As a result, circumstances may occur in which the interests of Grupo Nueva could be in conflict with your interests as a holder of our ADSs or shares of common stock.

Grupo Nueva also owns a direct 40% interest in Inversiones Internacionales Terranova S.A. (“IITSA”), which holds directly and indirectly substantially all of our interest in some of our international subsidiaries, accordingly our ability to direct these operations may be affected by the rights of Grupo Nueva as a minority shareholder. Conflicts of interest may arise between us and Grupo Nueva as a result of its ownership interest in our shares and the shares of IITSA. The Directors Committee reviews and resolves these potential conflicts of interest.

Our status as a controlled company and a foreign private issuer exempts us from certain of the corporate governance standards of the New York Stock Exchange, limiting the protections afforded to investors.

We are a “controlled company” and a “foreign private issuer” within the meaning of the New York Stock Exchange corporate governance standards and, under the New York Stock Exchange rules, we are exempt from certain New York Stock Exchange corporate governance requirements. In addition, a foreign private issuer may elect to comply with the practice of its home country and not to comply with certain New York Stock Exchange corporate governance requirements, including the requirements that (1) a majority of the board of directors consist of independent directors, (2) a nominating and corporate governance committee be established that is composed entirely of independent directors and has a written charter addressing the committee’s purpose and responsibilities, and (3) an annual performance evaluation of the nominating and corporate governance and compensation committees be undertaken. We currently use these exemptions and intend to continue using these exemptions. Accordingly, you do not have the same protections afforded to shareholders of companies that are subject to all of the New York Stock Exchange corporate governance requirements.

8

There may be a lack of liquidity and market for our shares and ADSs.

Prior to the merger of Terranova S.A. and its subsidiary Masisa S.A., in May 2005, there was no public market for our shares of common stock outside Chile or for our ADSs. In connection with the merger, our ADSs were listed on the New York Stock Exchange. Although there is a trading market for our ADSs on the NYSE, there can be no assurance that an active trading market will develop or be sustained in the future. In addition, the small size of the Chilean equities market, its low liquidity in general, its increased volatility compared to major securities markets in the United States and the concentrated ownership of our shares in particular, may impair the ability of an ADS holder to sell in the Chilean market on the Santiago Stock Exchange, the Valparaiso Stock Exchange or the Chilean Electronic Stock Exchange, on which our shares are traded, the Masisa shares obtained upon withdrawal of such shares from the Masisa ADR facility in the amount and at the price and time that ADS holder desires, and could increase the volatility of the price of our ADSs.

Chile may impose controls or other restrictions on foreign investment and repatriation of investments that may affect your investment in, and earnings from, our ADSs.

Equity investments into Chile from abroad are subject to the requirement that investors provide Chile’s Central Bank with information related to such equity investments and conduct any operations in connection with the repatriation of investments and earnings on them within Chile’s Mercado Cambiario Formal, or Formal Exchange Market. See “Item 10. Additional Information—Exchange Controls.”

Owners of ADSs are entitled to receive dividends on the underlying shares to the same extent as the holders of shares of common stock. Dividends received by holders of ADSs will be converted into U.S. dollars and distributed net of foreign currency exchange fees and expenses and fees of The Bank of New York, the depositary under the Masisa ADR program (the “Depositary”) and will be subject to Chilean withholding tax, currently imposed at a rate of 35% (subject to credits in certain cases as described under “Item 10. Taxation— Chilean tax consequences of ownership of Masisa shares or ADSs by foreign holders - Taxation of dividends”). If for any reason, including changes in Chilean laws or regulations, the Depositary were unable to convert Chilean pesos to U.S. dollars, investors may receive dividends and other distributions, if any, in Chilean pesos.

Additional Chilean restrictions applicable to the holders of our ADSs and other foreign investors in Chile could be imposed in the future. The Central Bank of Chile has the authority to impose at any time certain controls, restrictions or obligations on foreign investors in Chile. Such restrictions could include, but are not limited to, the requirement to obtain the Central Bank of Chile’s prior approval for the repatriation of the proceeds from the disposition of shares underlying the ADSs or the payment of dividends. We cannot advise you as to the duration or impact of any such restrictions if imposed.

Preemptive rights may be unavailable to ADS holders or U.S. holders of shares in certain circumstances and, as a result, U.S. owners of shares or ADSs would be subject to potential dilution.

The Ley sobre Sociedades Anónimas No. 18,046 and the Reglamento de Sociedades Anónimas, which we refer to in this document collectively as the Chilean Corporations Law, require us, whenever we issue new shares for cash and sell treasury shares, to grant preemptive rights to all of our shareholders (including shares represented by ADSs), giving them the right to purchase a sufficient number of shares to maintain their existing ownership percentage. It is possible that, in connection with any future issuances of shares, we may not be able to offer shares to U.S. holders of shares or ADSs pursuant to preemptive rights granted to our shareholders and, as a result such U.S. holders of shares or ADSs would be subject to potential dilution.

We will not be able to offer shares to ADS holders or U.S. holders of shares pursuant to preemptive rights that we grant to our shareholders in connection with any future issuance of shares or sale of treasury shares unless a registration statement under the U.S. Securities Act of 1933, as amended (the “Securities Act”), is effective with respect to such rights and shares, or an exemption from the registration requirements of the Securities Act is available.

9

ADS holders may not be able to effect service of process on, or enforce judgments or bring original actions against, us, our directors or our executive officers, which may limit the ability of holders of ADSs to seek relief against us.

We are a Chilean corporation. None of our directors are residents of the United States and most of our executive officers reside outside the United States. In addition, a substantial portion of our assets and the assets of our directors and executive officers are located outside the United States. As a result, it may be difficult for ADS holders to effect service of process outside Chile upon us or our directors and executive officers or to bring an action against us or such persons in the United States or Chile to enforce liabilities based on U.S. federal securities laws. It may also be difficult for ADS holders to enforce in the United States or in Chilean courts judgments obtained in United States courts against us or our directors and executive officers.

ADS holders may not be able to exercise withdrawal rights that are granted by the Chilean Corporations Law to registered shareholders of publicly traded Chilean corporations.

Under the Chilean Corporations Law, if any of the following resolutions are adopted by our shareholders at any extraordinary shareholders meeting, dissenting shareholders have the right to withdraw from Masisa and to require us to repurchase their shares, subject to the fulfillment of certain terms and conditions. A dissenting shareholder is a shareholder who either attends the shareholders meeting and votes against a resolution which results in a withdrawal right or, if absent from the shareholders meeting, a shareholder who notifies the company in writing within 30 days of the shareholders meeting of his opposition to the resolution and that he is exercising his right to withdraw from the company.

The resolutions that result in a shareholder’s right to withdraw are the following:

| · | the transformation of Masisa into a different type of legal entity; |

| · | the merger of Masisa with or into another company; |

| · | the disposition of 50% or more of our assets, whether or not that sale includes our liabilities or the proposal or amendment of any business plan involving the transfer of more than 50% of our assets; |

| · | the granting of security interests or personal guarantees to secure or guarantee third parties’ obligations exceeding 50% of our assets, except with regard to our subsidiaries; |

| · | the creation of preferential rights for a class of shares or an amendment to those already existing, in which case the right to withdraw only accrues to dissenting shareholders of the class or classes of shares adversely affected; |

| · | the amendment of our bylaws to correct any formal defect in our incorporation, or any amendment of our bylaws that grants a shareholder a right to withdraw; |

| · | the approval by our shareholders of our ceasing to be subject to the regulations applicable to publicly held corporations in the event we no longer meet the requirements under Chilean law to qualify as such a corporation; and |

| · | any other causes as may be established by Chilean law and our bylaws (our bylaws currently do not establish any instances). |

In addition, shareholders of a publicly held corporation, such as Masisa, have the right to withdraw if a person acquires two-thirds or more of the outstanding voting stock of the company and does not make a tender offer for the remaining shares within 30 days of that acquisition at a price not lower than the price that would be paid shareholders exercising their rights to withdraw. However, the right of withdrawal described in the previous sentence does not apply in the event the company reduces its capital as a result of not having fully subscribed and paid an increase of capital within the statutory term.

10

ADS holders own a beneficial interest in shares held by the Depositary and, accordingly, they are not listed as shareholders on the share registry of the Company. The Depositary will not exercise withdrawal rights on behalf of ADS holders. Accordingly, in order to ensure a valid exercise of withdrawal rights, an ADS holder must cancel his or her ADSs and become a registered shareholder of the Company no later than the date which is five Chilean business days before the shareholders’ meeting at which the vote which would give rise to withdrawal rights is taken, or the applicable record date for withdrawal rights that arise other than as a result of a shareholder vote. Withdrawal rights must then be exercised in the manner prescribed in the notice to shareholders that is required to be sent to shareholders of Chilean public companies advising such holders of their right of withdrawal. If an event occurs that gives rise to withdrawal rights, ADS holders will have a limited time to cancel their ADSs and to become registered shareholders of the Company prior to the record date for the shareholders meeting or other event giving rise to such withdrawal rights. If an ADS holder does not become a registered shareholder of the Company prior to such record date he or she will not be able to exercise the withdrawal rights available to registered shareholders.

Chile has different corporate disclosure and accounting standards than those you may be familiar with in the United States and you may receive less information about us, and the information about us available to you will not be the same as the information available to shareholders of a comparable U.S. company.

There are important differences between Chilean and U.S. accounting and financial reporting standards. As a result, Chilean financial statements and reported earnings generally differ in important respects from those reported based on U.S. accounting and reporting standards. As a foreign private issuer, we are permitted to present our financial statements under Chilean GAAP, with reconciliation to U.S. GAAP, in our Securities Act registration statements and in our filings under the U.S. Securities Exchange Act of 1934, as amended (the “Exchange Act”). We present our financial statements under Chilean GAAP as permitted and, accordingly, the information available to you will differ from the information that would be available to you if we prepared our financial statements under U.S. GAAP. For a description of the principal differences between Chilean GAAP and U.S. GAAP as such differences relate to us, see Note 23 to our audited consolidated financial statements contained elsewhere in this document.

In addition, Chilean disclosure requirements differ from those in the United States in some important respects. For example, Chilean law does not require us to disclose our officers’ compensation on an individual basis and, as a foreign private issuer, we are permitted to report such compensation on an aggregate basis in our Securities Act registration statements and in our Exchange Act filings. Also, Chilean legal restrictions on insider trading and price manipulation are different from those in the United States and in certain respects the Chilean securities markets are not as highly regulated and supervised as the U.S. securities markets.

U.S. securities laws do not require us to disclose as much information to investors as a U.S. issuer is required to disclose, and you may receive less information about us than you might otherwise receive from a comparable U.S. company.

The corporate disclosure requirements applicable to us may not be equivalent to the requirements applicable to a U.S. company and, as a result, you may receive less information about us than you might otherwise receive in connection with a comparable U.S. company. We are subject to the periodic reporting requirements of the Exchange Act that apply to non-U.S. issuers. The periodic disclosure required of non-U.S. issuers under the Exchange Act is more limited than the periodic disclosure required of U.S. issuers. For example:

| · | We are required only to file an annual report on Form 20-F, but we are not required to file any quarterly reports. A U.S. registrant must file an annual report on Form 10-K and three quarterly reports on Form 10-Q. |

| · | We are required to file current reports on Form 6-K, but the information that we must disclose in those reports is governed primarily by Chilean law disclosure requirements and may differ from Form 8-K’s current reporting requirements imposed on a U.S. issuer. |

| · | We are not subject to the proxy requirements of Section 14 of the Exchange Act and our officers, directors and principal shareholders are not subject to the short swing insider trading reporting and recovery requirements under Section 16 of the Exchange Act. |

11

Chilean law provides for fewer and less well-defined shareholders’ rights.

Our corporate affairs are governed by our estatutos (which serve the combined function of the articles of incorporation and the bylaws of a U.S. corporation), and the laws of Chile. Under such laws and our estatutos, our shareholders may have fewer or less well-defined rights than they might have as shareholders of a corporation incorporated in a U.S. jurisdiction. For example, our shareholders would not be entitled to appraisal rights in the event of a merger or other business combination undertaken by us. See “Item 10. Additional Information— Memorandum and Articles of Association—Shareholders’ meetings and voting rights” and “—Dividend and liquidation rights.”

Currency devaluations, foreign exchange fluctuations and foreign currency conversion costs may adversely affect the U.S. dollar value of any cash distributions made to ADS holders in respect of ADSs.

If the value of the Chilean peso falls relative to the U.S. dollar, the value of the ADSs and any distributions to be received from the Depositary for the ADSs could be adversely affected. Cash distributions made in respect of the ADSs are received by the Depositary in Chilean pesos, are then converted by the Depositary into U.S. dollars at the then prevailing exchange rate and distributed to the holders of the ADRs evidencing those ADSs. In addition, the Depositary will incur foreign currency conversion costs (to be borne by the holders of the ADSs) in connection with the foreign currency conversion and subsequent distribution of dividends or other payments with respect to ADSs.

Item 4. Information on the Company

Our Company

Masisa is a leading vertically integrated Latin American wood boards company. We also grow and harvest timber in plantations located in most of the fastest tree growth rate areas in the world and sell our manufactured products primarily to the construction and furniture industries, mainly in Latin America and the United States, as well as to customers in other markets such as Europe and Asia. Our main products include wood boards for furniture, solid wood products, sawn lumber and saw and pulp logs.

In 2006, approximately 56% of our consolidated sales were in the investment grade countries of Chile, Mexico and the United States, which accounted for 16.3%, 13.2% and 26.0%, respectively, of our consolidated sales in that year. The rest of Latin America accounted for approximately 41% of our consolidated sales in 2006 with Brazil, Venezuela, Argentina, Colombia, Peru and Ecuador accounting for 16.4%, 10.4%, 7.9%, 2.8%, 2.4% and 1.1%, respectively, of our consolidated sales in that year. The remaining 3.5% of our consolidated sales in 2006 was from exports to 50 countries outside of Latin America and the United States.

We are a leading wood board manufacturer in Latin America with an annual installed capacity of 2.3 million cubic meters, which accounts for approximately 18% of the region’s installed capacity. Our principal board products include MDF (medium density fiberboard), PB (particle board) and OSB (oriented strand board) that are mainly sold in the Latin American region. Latin American board consumption has grown in the past and is expected to continue to grow due to existing housing deficits and expected higher demand for housing in the Latin American region, particularly in Brazil and Mexico. We believe additional housing activity will generate increased demand for furniture and boards.

In sawn lumber, we have an annual installed capacity of 707,000 cubic meters. We sell our sawn lumber primarily in the Mexican and Venezuelan markets.

In addition, we produce value-added products such as MDF mouldings, finger-joint mouldings and solid wood doors and have an installed annual capacity for each product of 224,400, 168,000 and 42,000 cubic meters, respectively, as of December 31, 2006. These products are sold principally in the United States. In February 2007, as part of a cost reduction program, we closed our 36,000 cubic meter MDF moulding plant located in Charleston, South Carolina. The production line will be relocated, during 2007, to our industrial complex in Cabrero, Chile.

12

In the United States, we have our own commercialization company, Masisa USA. In 2006, Masisa sold approximately one million solid wood pine doors as well as finger-joint and MDF mouldings. We also participate in the structural panels market in the United States, selling OSB produced in our Brazilian operation. We distribute our products in the United States principally through Masonite, as well as wholesale building products distributors such as Builders First Source, OrePack and Weyerhaeuser that resell our products to retailers. Over the last year, principally due to the increase in MDF moulding sales and the increased diversification and more numerous distribution channels for our solid wood door products, we have increased the percentage of our U.S. sales that are made to new customers.

Increasing environmental concerns around the world, coupled with increased demand for wood fiber by pulp and energy producers, have made planted timber a more desirable resource in the forest products industry. We own 241,417 hectares of renewable planted forests (i.e. mainly composed of pines and eucalyptus trees) including 140,734 hectares in Chile, Brazil and Argentina, three of four of the fastest tree growth rate areas in the world, giving us access to a sustainable, low-cost source of raw material. Our forests are managed under international environmental standards, including the International Organization for Standardization’s (“ISO”) 14,001 certification and compliance certifications from the Forestry Stewardship Council (“FSC”), allowing us better access to developed world markets in which compliance with such standards is often of interest to consumers.

In Latin America, Masisa’s business is complemented by a substantial distribution network of independently owned stores selling our products called Placacentros Masisa (“Placacentros”). Board demand in Latin America is highly fragmented due to the importance of general contractors and independent furniture manufacturers. Placacentros are designed to provide services that increase these contractors’ and manufacturers’ productivity and enhance demand for our products. Placacentro stores also offer a variety of products related to furniture manufacturing and provide related services, such as computer aided furniture design, and customized board sizing and drilling, improving our customers’ productivity. The Placacentro concept has been successful in developing our customer base to include more small to medium sized businesses. The network, which is present in 10 countries in the Latin American region, has grown from 49 stores in 2000 to 232 stores in 2004 and 300 stores as of December 31, 2006. Placacentros have been an instrumental factor in allowing us to increase our market share in various Latin American board markets over the last few years, and we believe they have also contributed to the overall growth in several of the markets we have entered. Our board sales through this channel represent approximately 31% of our consolidated board sales (i.e. excluding board exports) for 2006.

Our Competitive Strengths

| · | Leading producer of wood boards for furniture in Latin America. |

We have approximately 22.7% of the total installed wood board for furniture production capacity in the region (i.e. excluding plywood, which in some Latin American countries is utilized for manufacturing furniture), and a capacity approximately 9% greater than our next closest competitor as of December 2006. We own wood board production facilities in Chile, Brazil, Argentina, Venezuela and Mexico, which coupled with our Placacentros distribution network that is present in the majority of the Latin American markets, represent a strong production and commercial network. This regional footprint provides us with commercial flexibility to optimize production and product sales destinations within the region, based on the dynamics of the different Latin American markets.

| · | Strong brand positioning |

In the markets in which we operate, we have developed into a wood products manufacturer whom customers seek out because of our focus on meeting and exceeding our customers’ needs. For example, in Mexico our particle board plant has been certified as “Green Partner,” which will allow us to target customers, such as Asian electronics manufacturers, who would otherwise have to purchase such certified particle board from Asian producers. Providing offerings such as this and continually delivering innovative products and services to our customers has lead to greater customer loyalty and interest and increased consumption of Masisa’s products.

13

| · | Established and expanding distribution network. |

Our Placacentro distribution network has proved successful in Latin America, resulting in growth from 49 stores in 2000 to 220 stores in 2004 and 300 stores as of December 31, 2006. Our Placacentro stores, which are oriented toward independent furniture manufacturers and general contractors, offer a wide range of wood panels, solid wood, accessories and services required by these customers to increase their productivity. Placacentros are an important part of Masisa’s marketing strategy to increase the per capita consumption of Masisa’s products, increase brand awareness and positioning and to create competitive advantages to address the current and future competition by other market participants.

| · | Quality low cost forest resources. |

The location of our forests in fast growth rate areas lowers our raw materials cost, providing us with an important competitive advantage compared to competitors that rely on raw materials from plantations in slower tree growth rate regions. We expect that the progressive maturity of our forests will allow us to increase our annual harvest in the future, and that our consistent forest management practices that we have followed for more than a decade will permit us to improve the quality of our harvested wood, allowing us to add higher quality products to our product mix. Due to increasing environmental concerns around the world and as industrial capacity has started to match industrial forest availability, access to fiber from planted timber plantations has become a strategic asset.

| · | Modern manufacturing facilities and competitive operations. |

48% of our board production capacity, 72% of our moulding production capacity and 86% of our saw mill capacity were built after 2000. Our primary production facilities are located in Chile, Brazil, Argentina and Venezuela where our forests are located. Modern manufacturing facilities, access to low cost raw material, economies of scale derived from the overall size of our operations, and the relatively low labor costs in the Latin American countries in which we operate, provide us with a competitive cost structure.

| · | Geographic diversification. |

We sell our products in every major economy in Latin America as well as the United States. Our largest market, the United States, represents approximately 26% of our sales and our largest Latin American market represents no more than 17% of our sales. This geographic diversification diminishes to a certain extent our vulnerability to market downturns in any one country.

| · | Significant cost advantages in value-added wood products. |

We are able to capitalize on rapid forest growth and low manufacturing costs to achieve a cost advantage in supplying the North American market compared to manufacturers that serve the North American market from other regions in the world.

History and Development of the Company

We are a sociedad anónima abierta, or publicly held corporation, organized under the laws of Chile. We were incorporated into our present form on October 31, 2003 under the name Terranova S.A. Our predecessor company, Forestal Terranova S.A. was incorporated on August 2, 1994. In April 2005, the shareholders of Terranova S.A. and Masisa S.A. approved the merger of the two companies with Terranova as the surviving entity. At the same shareholder meetings, the shareholders of each company approved changing the merged company’s name to Masisa S.A., our legal and commercial name. For additional information regarding the merger see “-The Merger of Terranova and Masisa-.”.

We are controlled by our majority shareholder, Grupo Nueva S.A., formerly known as Compañía de Inversiones Suizandina S.A. Grupo Nueva S.A. is a Chilean holding company and is part of a larger group of affiliated investment companies, held by Nueva Holding, Inc. Our legal domicile is Santiago, Chile and our principal executive office is located at Avenida Apoquindo 3650, Piso 10, Las Condes, Santiago, Chile. Our telephone number is +56 (2) 350-6000. Our agent in the United States is Masisa USA, Inc., which is located at 900 Circle Seventy-five Parkway, Suite 720, Atlanta, Georgia 30339. Masisa USA was formerly known as Terranova Forest Products, Inc.

14

Our history began in the 1970s with a sawmill operation in southern Chile. In the years up to 2002, through acquisitions and other transactions, we and our predecessor companies expanded our forestry assets in Chile, Venezuela and Brazil; acquired and established manufacturing and marketing capabilities in the markets of northern Latin America and the United States in order to allow us to more efficiently utilize our forestry resources; and worked to improve the coordination and management of those resources. During this period, we expanded our operations within Chile to include additional sawmills and facilities to manufacture MDF and market skin and moulded doors. Outside Chile, we significantly expanded to add forestry assets in Venezuela and Brazil, sawmills in Venezuela and Brazil, board manufacturing facilities in Brazil, Argentina and Venezuela, a moulding mill in the United States and distribution and marketing operations in the United States and numerous markets in northern Latin America. As of 2002, our forestry assets and manufacturing operations were held directly and indirectly through our predecessor, Forestal Terranova, with our U.S. operations being coordinated through Forestal Terranova’s subsidiary, Masisa USA, and our non-Chilean subsidiaries and affiliates being held by, and their products marketed through, Terranova Internacional S.A., also known as TISA.

In January 2001, Forestal Terranova subscribed to approximately 81 million newly issued shares of Masisa, giving it an approximate 8.8% interest in Masisa. In July 2002, Forestal Terranova acquired Maspanel’s 43.16% interest in Masisa and became Masisa’s controlling shareholder with 51.9% of Masisa’s total shares then paid and outstanding. Effective as of July 1, 2002, Forestal Terranova began consolidating Masisa into its financial results. On May 27, 2003, Forestal Terranova increased its ownership interest in Masisa to 486,861,555 shares (52.43%) of common stock through open market purchases on the Santiago Stock Exchange.

On November 15, 2005 we increased our participation share in our Chilean forestry company, Forestal Tornagaleones from 60.45% to 94.91% through the purchase of a significant minority shareholder’s interest for US$29.9 million. In addition, during the first quarter of 2006, Forestal Tornagaleones increased its participation share in Forestal Argentina S.A., our Argentinean forestry investment company, from 50.10% to 98.68% through the purchase of aggregate minority shareholders’ interests of 48.58% for approximately US$24.3 million.

At the end of 2005 and beginning of 2006 we successfully completed a capital increase, with total proceeds of US$117.5 million, divided into two phases. The first phase, which was completed on December 7, 2005, yielded proceeds of US$75 million. Of this amount, 66% was placed in the U.S. market via the Company’s ADR program. The second phase of this process was completed on January 5, 2006, upon the completion of a preemptive rights offering period. The principal objectives of the capital increase were to finance the Company’s investment projects, which include a new MDF plant in Chile.

In January 2006, we successfully issued bonds in the Chilean market for UF4.75 million (US$162.95 million). The funds obtained by this bond issuance were primarily used to pay financial obligations of the Company.

In October 2006, we reviewed our corporate strategy, including our core business and competitive strategies, (see “Item 4, - Business Strategy” and “Item 4 Operational Organization”). In this process, we determined our core business to be the production and commercialization of wood boards for furniture and interior architecture (MDF and PB) in Latin America. In addition to our core business of wood boards, we have initiated the restructuring of our forestry assets, solid wood products (i.e. MDF mouldings, finger-joint mouldings and solid wood doors) and retail operations (i.e. Placacentros) from being organized by countries to be organized by business operations, specifically into three complimentary business units that will focus their respective strategies and future investments on supporting the growth of our wood board business. We will continue to carry out the same operations as before, but now they will be organized by business units rather than country. As part of this process, we also established a financial and investment plan that will allow us to strenghthen our existing leading position within the wood board industry in Latin America.

We are committed to sustainable development and are interested in developing activities designed to provide solutions to climate change challenges which are also good business opportunities. In this regard, in December 2006 we joined the Chicago Climate Exchange (“CCX”) and have committed to reduce our carbon emissions by 6% by 2010, which offers the possibility of trading our positive carbon balance at convenient conditions.

15

We expect our new MDF plant at Cabrero, Chile, to start operations by the second half of 2007, and expect it to be operating at full capacity by the beginning of 2008. This new plant will have an installed capacity of 340,000 cubic meters of annual production, thus representing a 15% increase in our existing wood board production capacity.

In February 2007, as part of a cost reduction program, we closed the Charleston MDF moulding plant (i.e. 36,000 cubic meters, representing 9% of our total moulding capacity). Most of the industrial assets previously used at the Charleston, Sout Carolina plant will be relocated to our industrial complex in Cabrero, Chile.

The Merger of Terranova and Masisa

On April 12 and April 13, 2005, respectively, the shareholders of our former majority-owned subsidiary Masisa S.A. and Terranova S.A approved the merger by incorporation of the former Masisa into and with Terranova. At the same shareholder meetings of Masisa and Terranova at which the merger was approved, the shareholders of each company also approved changing the name of the merged company from Terranova S.A. to Masisa S.A.

The merger became effective on May 31, 2005. As a consequence, the company known as Masisa before May 31, 2005 no longer exists. Terranova’s name was changed to Masisa at the effective time of the merger and continues as the surviving entity and is the legal successor of the former Masisa for all purposes.

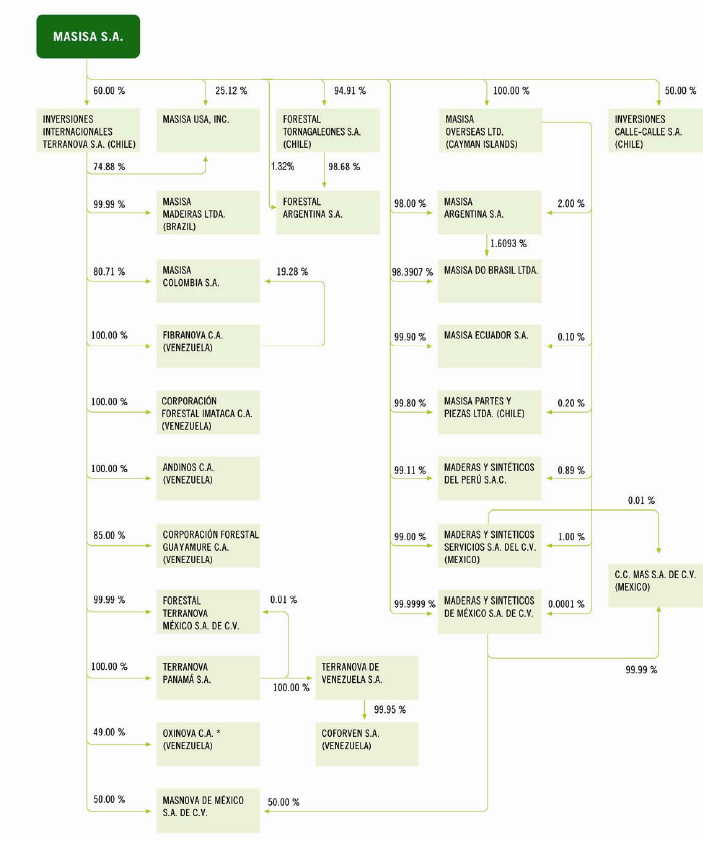

Corporate Structure

As indicated in the following charts, we and a number of our subsidiaries conduct manufacturing operations. However, most of our sales to third parties are made through Masisa USA, Maderas y Sinteticos Mexico S.A. de C.V., Forestal Terranova Mexico, Masisa Chile, Masisa Argentina, Masisa do Brazil, Masisa Madeiras Ltda., Maderas y Sinteticos del Peru S.A.C., Masisa Ecuador, Fibranova C.A.(Venezuela), Andinos C.A. (Venezuela) and Masisa Colombia. The principal exceptions are Forestal Tornagaleones and Forestal Argentina, which are directly responsible for selling their own products.

16

Our group’s business structure, as of June 15, 2007, is set forth in the following chart:

17

The following table shows on a consolidated basis our direct and indirect ownership interest in each of our subsidiaries and affiliates that formed a part of our group as of December 31, 2006 as well as the country of incorporation for each such subsidiary and affiliate. Unless specifically noted otherwise, our ownership interest in each subsidiary and affiliate as of December 31, 2006 was equal to our proportionate voting power in that entity.

Ownership interest | ||||||||||||||||

Country of | 12/31/2006 | 12/31/2005 | ||||||||||||||

Company | Incorporation | Direct | Indirect | Total | Total | |||||||||||

| Inversiones Internacionales Terranova S.A. | Chile | 60.0000 | 0.0000 | 60.0000 | 60.0000 | |||||||||||

| Forestal Tornagaleones S.A. | Chile | 94.9061 | 0.0000 | 94.9061 | 94.9061 | |||||||||||

Masisa Inversiones Limitada 1 | Chile | 0.0000 | 0.0000 | 0.0000 | 100.0000 | |||||||||||

Masisa Concepcion Limitada 2 | Chile | 0.0000 | 0.0000 | 0.0000 | 100.0000 | |||||||||||

Inversiones Coronel Limitada 3 | Chile | 0.0000 | 0.0000 | 0.0000 | 100.0000 | |||||||||||

Masisa Partes y Piezas Limitada4 | Chile | 99.8000 | 0.2000 | 100.0000 | 100.0000 | |||||||||||

| Masisa Overseas Ltd. | Cayman Islands | 100.0000 | 0.0000 | 100.0000 | 100.0000 | |||||||||||

| Maderas y Sinteticos del Perú S.A.C. | Peru | 99.0114 | 0.8897 | 99.9011 | 99.9011 | |||||||||||

| Masisa USA, Inc | U.S. | 25.1200 | 44.9280 | 70.0480 | 70.0480 | |||||||||||

| Maderas y Sinteticos Servicios S.A. de C.V. | Mexico | 99.0000 | 1.0000 | 100.0000 | 100.0000 | |||||||||||

| Masisa Ecuador S.A. | Ecuador | 99.9000 | 0.1000 | 100.0000 | 100.0000 | |||||||||||

| Masisa Do Brasil Ltda. | Brazil | 98.3907 | 1.6093 | 100.0000 | 100.0000 | |||||||||||

| Maderas y Sinteticos Mexico S.A. de C.V. | Mexico | 99.9999 | 0.0001 | 100.0000 | 100.0000 | |||||||||||

| Terranova Panama S.A. | Panama | 0.0000 | 60.0000 | 60.0000 | 60.0000 | |||||||||||

| Terranova de Venezuela S.A. | Venezuela | 0.0000 | 60.0000 | 60.0000 | 60.0000 | |||||||||||

| Coforven S.A. | Venezuela | 0.0000 | 59.9700 | 59.9700 | 59.9700 | |||||||||||

| Forestal Terranova Mexico S.A. de C.V. | Mexico | 0.0000 | 59.9940 | 59.9940 | 59.9940 | |||||||||||

| Cor.Forestal Guayamure C.A. | Venezuela | 0.0000 | 51.0000 | 51.0000 | 51.0000 | |||||||||||

| Masisa Madeiras Ltda. | Brazil | 0.0000 | 59.9940 | 59.9940 | 59.9940 | |||||||||||

| Masisa Colombia S.A. | Colombia | 0.0000 | 59.9940 | 59.9940 | 59.9940 | |||||||||||

| Cor.Forestal Imataca C.A. | Venezuela | 0.0000 | 60.0000 | 60.0000 | 60.0000 | |||||||||||

| Andinos C.A. | Venezuela | 0.0000 | 60.0000 | 60.0000 | 60.0000 | |||||||||||

Forestal Argentina S.A. 5 | Argentina | 0.0000 | 93.6530 | 93.6530 | 47.5480 | |||||||||||

| Masisa Argentina S.A. | Argentina | 98.0000 | 2.0000 | 100.0000 | 100.0000 | |||||||||||

| Fibranova C.A. | Venezuela | 0.0000 | 60.0000 | 60.0000 | 60.0000 | |||||||||||

| Masnova S.A. | Mexico | 0.0000 | 80.0000 | 80.0000 | 80.0000 | |||||||||||