CareDx, Inc.

1 Tower Place

South San Francisco, California 94080

August 26, 2020

VIA EDGAR

U.S. Securities and Exchange Commission

Division of Corporation Finance, Office of Life Sciences

100 F Street, N.E.

Mail Stop 3561

Washington, DC 20549

Attention: Nudrat Salik

Al Pavot

Re: CareDx, Inc.

Form 10-K for the Year Ended December 31, 2019

Filed February 28, 2020

Form 8-K

Filed April 30, 2020

File No. 001-36536

Ladies and Gentlemen:

This letter responds to the comments of the Staff (the “Staff”) of the Securities and Exchange Commission (the “Commission”) to Mr. Michael Bell, Chief Financial Officer of CareDx, Inc., a Delaware corporation (the “Company”), in the letter dated August 5, 2020 (the “Comment Letter”) relating to the Company’s Annual Report on Form 10-K (File No. 001-36536) for the fiscal year ended December 31, 2019 filed with the Commission on February 28, 2020 (the “Form 10-K”) and the Company’s Current Report on Form 8-K (File No. 001-36536) filed with the Commission on April 30, 2020 (the “Form 8-K”).

Set forth below are the Staff’s comments (in bold italics) and the Company’s response thereto, organized as set forth in the Comment Letter.

Form 10-K for the Year Ended December 31, 2019

Consolidated Statements of Operations, page 77

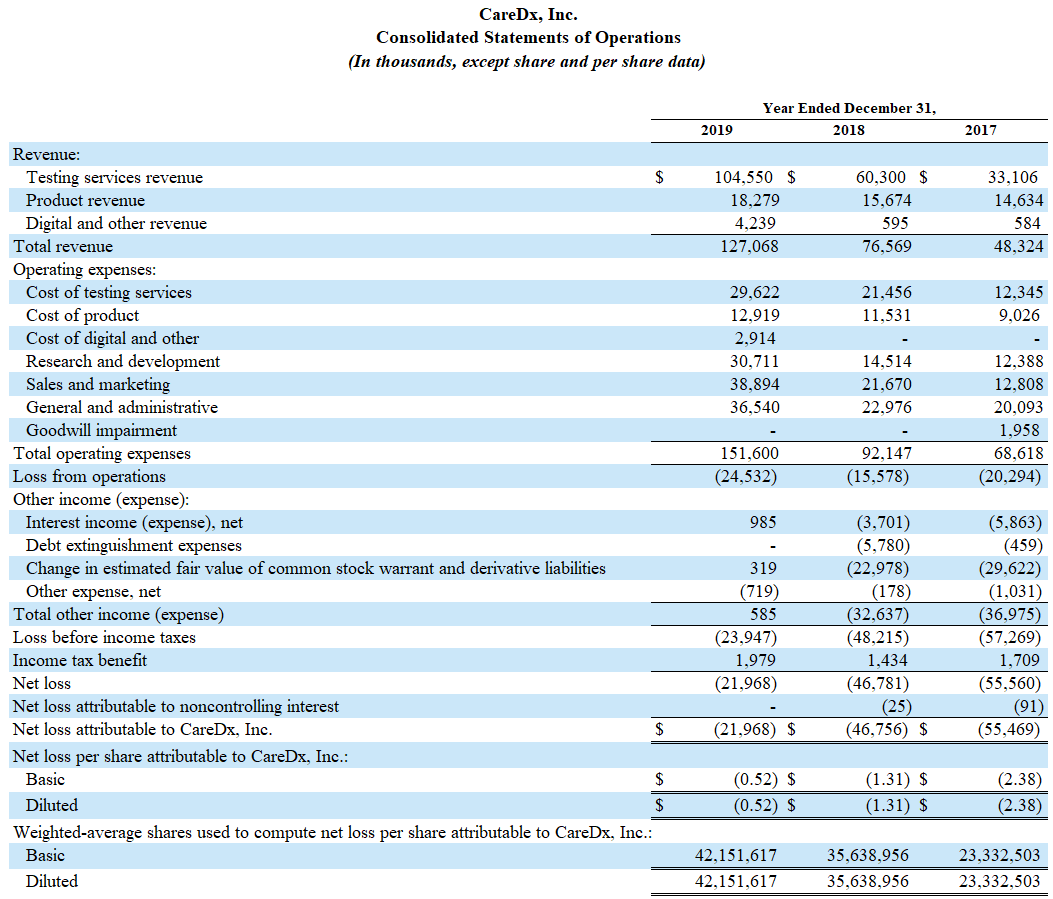

1.As disclosed on page 82, you have combined the presentation of cost of testing services, cost of product, and cost of digital and other into one cost of revenue line item. Please tell us how your current combined presentation of these cost of revenue amounts complies with Rule 5-03 of Regulation S-X. Alternatively, please revise your presentation.

We respectfully acknowledge the Staff’s comment. In future filings, the Company intends to revise its presentation of the cost of revenue to comply with Rule 5-03 of Regulation S-X. Beginning with the Form 10-Q for the quarter ending September 30, 2020, the Company will present cost of testing services, cost of product and cost of digital and other as separate line items for all periods presented. As such, in the Form 10-K for the year ended December 31, 2020, the December 31, 2019 amounts will be shown as follows:

U.S. Securities and Exchange Commission

August 26, 2020

Page 2

Form 8-K Filed April 30, 2020

Exhibit 99.1, page 7

2.You appear to present a full non-GAAP income statement when reconciling non-GAAP measures to the most directly comparable GAAP measures. Please revise your presentation to comply with the guidance in Question 102.10 of the Non-GAAP Compliance and Disclosure Interpretations.

We respectfully acknowledge the Staff’s comment. In future filings, the Company will eliminate the presentation of a full non-GAAP income statement. Beginning with the announcement of the Company’s results for its quarter ending September 30, 2020, the reconciliation of GAAP to Non-GAAP financial measures will be presented substantially in line with the following:

U.S. Securities and Exchange Commission

August 26, 2020

Page 3

U.S. Securities and Exchange Commission

August 26, 2020

Page 4

*****

Please contact me if you have any further comments or need additional information with respect to the filings or this letter.

Thank you for your assistance.

Very truly yours,

CareDx, Inc.

By: /s/ MICHAEL BELL

Name: Michael Bell

Title: Chief Financial Officer

cc: Jeffrey T. Hartlin, Paul Hastings LLP