UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-21295

JPMorgan Trust I

(Exact name of registrant as specified in charter)

270 Park Avenue

New York, NY 10017

(Address of principal executive offices) (Zip code)

Frank J. Nasta

270 Park Avenue

New York, NY 10017

(Name and Address of Agent for Service)

Registrant’s telephone number, including area code: (800) 480-4111

Date of fiscal year end: October 31

Date of reporting period: November 1, 2015 through April 30, 2016

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. Section 3507.

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

The following is a copy of the report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1).

Semi-Annual Report

J.P. Morgan Specialty Funds

April 30, 2016 (Unaudited)

JPMorgan Opportunistic Equity Long/Short Fund

JPMorgan Research Equity Long/Short Fund

JPMorgan Research Market Neutral Fund

CONTENTS

Investments in a Fund are not deposits or obligations of, or guaranteed or endorsed by, any bank and are not insured or guaranteed by the FDIC, the Federal Reserve Board or any other government agency. You could lose money if you sell when a Fund’s share price is lower than when you invested.

Past performance is no guarantee of future performance. The general market views expressed in this report are opinions based on market and other conditions through the end of the reporting period and are subject to change without notice. These views are not intended to predict the future performance of a Fund or the securities markets. References to specific securities and their issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Such views are not meant as investment advice and may not be relied on as an indication of trading intent on behalf of any Fund.

Prospective investors should refer to the Funds’ prospectus for a discussion of the Funds’ investment objective, strategies and risks. Call J.P. Morgan Funds Service Center at 1-800-480-4111 for a prospectus containing more complete information about a Fund, including management fees and other expenses. Please read it carefully before investing.

CEO’S LETTER

May 18, 2016 (Unaudited)

Dear Shareholder,

Global economic growth appeared to decelerate as 2015 ended and 2016 began. Slowing growth in China, anemic growth in Europe and falling oil prices drained momentum from the U.S. economy and put pressure on emerging market and developed market economies across the globe.

| | |

| | “Given the uncertain outlook for global growth, investors who maintain a properly diversified portfolio and an eye toward long term performance may benefit from changing economic and market conditions.” |

In December, the U.S. Federal Reserve (the “Fed”) raised interest rates for the first time in 10 years in a clear signal to financial markets that the central bank’s policymakers believed the domestic economy and, to some extent, the world economy was objectively moving in a trajectory toward self-sustaining growth.

However, economic data from China, the European Union (EU) and Japan provided a worrisome picture and the drag from weak overseas demand, and the U.S. dollar’s relative strength, reduced corporate earnings and gross domestic product (GDP) in the U.S. Meanwhile, volatility in global financial markets spiked in January and February.

Citing weakness in global economic conditions, the Fed declined to raise interest rates further at its March meeting. In the same month, the European Central Bank (ECB) unleashed a flurry of measures to bolster growth. The ECB moved deposit rates further into negative territory — an experiment that the Bank of Japan embarked upon at the end of January — and increased the size and scope of its monthly asset purchases and unveiled a program to increase bank lending. China’s central bank acted earlier, cutting bank reserve ratios in February for the second time in four months.

While the impact of all this central bank activity and accommodative policy on global growth remained uncertain at the end of April, financial markets overall responded favorably and leading central banks took no further action during the month. Moreover, fresh signs of stability in China’s economy, a modest rebound in commodities prices and the Fed’s stated cautiousness in raising U.S. interest rates further helped drive a rally in emerging market equity and bonds prices that began in March and extended into mid-April. In the EU, the unemployment rate shrank and first quarter 2016 GDP rose 0.6% to an annual rate of 2.2%, bringing it back above levels last seen before the 2008 financial crisis. The U.S. economy, which had been outpacing the rest of the world throughout 2015, turned in a lower-than-expected 0.5% rise in GDP in the first quarter of 2016, mostly

due to reductions in capital spending in the energy sector, a pullback in inventory growth and the strong U.S. dollar.

Even as global economic conditions appeared to stabilize in April, there remained worrisome aspects to the data. The upward momentum in emerging market equity and bond markets faded by the end of April as U.S. investors retreated from perceived higher risk assets. In the EU, price inflation remained consistently below the ECB’s targets despite massive central bank stimulus. The U.S. economy continued to expand through April and the employment picture remained healthy and wage growth, which had been lacking for much of the current economic recovery, also showed improvement. However, job gains slowed in April and hourly productivity failed to rise, which could hinder growth in U.S. corporate profits.

Throughout the six month period, global oil prices remained low and volatile. Prices appeared to bottom out in mid-February before strengthening ahead of the mid-April meeting of the Organization of Petroleum Exporting Countries (OPEC) and talk of a cap on production. Investment in U.S. shale oil production fell sharply in early 2016, which also supported higher oil prices. However, OPEC failed to reach an agreement to curb output and oil prices slumped but ended the month of April with the largest monthly gain in a year.

In early April, the International Monetary Fund (IMF) cut its forecast for 2016 global economic growth to 3.2% from its previous forecast of 3.4%. The IMF stated that the prolonged period of slow growth in the global economy has left it vulnerable to events that could halt growth and lead to economic stagnation. Among those risks, the IMF cited financial market turmoil, which could hurt investor confidence and demand. The IMF also noted geopolitical risks from populist movements in the U.S. and in Europe, Britain’s June referendum on exiting the EU and the strain from the large number of refugees seeking to enter Europe. However, the IMF stated that China’s economy appears to be improving amid resilient domestic demand and growth in service industries that have offset weakness in manufacturing.

Uneven economic growth and a certain measure of financial market volatility have been persistent features of the current phase of the global recovery. Given the uncertain outlook for global growth, investors who maintain a properly diversified portfolio and an eye toward long term performance may benefit from changing economic and market conditions.

Sincerely yours,

George C.W. Gatch

CEO, Investment Funds Management

J.P. Morgan Asset Management

| | | | | | | | |

| | | |

| APRIL 30, 2016 | | J.P. MORGAN SPECIALTY FUNDS | | | | | 1 | |

J.P. Morgan Specialty Funds

MARKET OVERVIEW

SIX MONTHS ENDED APRIL 30, 2016 (Unaudited)

Overall, U.S. equity markets experienced a significant increase in volatility during the six month reporting period. While equity prices rose slightly through the end of 2015, the beginning of 2016 was marked by prolonged sell-off of equities, driven by falling oil prices and investor uncertainty about both the health of China’s economy and U.S. interest rate policy.

By March, market volatility declined somewhat as economic data showed signs of stability in China, oil prices rebounded and the U.S. Federal Reserve Chairwoman Janet Yellen reassured investors that interest rate policy would remain accommodative. By the end of April, leading U.S. equity indexes returned to positive territory for the year to date. For the six months ended April 30, 2016, the Standard & Poor’s 500 Index returned 0.43%.

| | | | | | |

| | | |

| 2 | | | | J.P. MORGAN SPECIALTY FUNDS | | APRIL 30, 2016 |

JPMorgan Opportunistic Equity Long/Short Fund

FUND COMMENTARY

SIX MONTHS ENDED APRIL 30, 2016 (Unaudited)

| | | | |

| REPORTING PERIOD RETURN: | |

| Fund (Select Class Shares)* | | | -3.65% | |

| Standard & Poor’s 500 Index | | | 0.43% | |

| |

| BofA Merrill Lynch 3-Month U.S. Treasury Bill Index | | | 0.01% | |

| Net Assets as of 4/30/2016 (In Thousands) | | $ | 224,749 | |

INVESTMENT OBJECTIVE**

The JPMorgan Opportunistic Equity Long/Short Fund (the “Fund”) seeks capital appreciation.

WHAT WERE THE MAIN DRIVERS OF THE FUND’S PERFORMANCE?

The Fund (Select Class Shares) underperformed the Standard & Poor’s 500 Index (the “Benchmark”) for the six months ended April 30, 2016. Leading sector contributors to the Fund’s relative performance included its long positions in the health care and consumer discretionary sectors. Leading sector detractors from the Fund’s relative performance included its long positions in the information technology and materials sectors.

Leading individual detractors from relative performance included the Fund’s long positions in Mobileye NV, United Rentals Inc. and Alliance Data Systems Corp. Shares of Mobileye, a provider of camera-assisted driving systems that was not held in the Benchmark, fell on questions about the company’s technology and after an influential investment firm called the stock the “short of the year: 2016.” Shares of United Rentals, a provider of oil field equipment, fell on slowing capital spending in the energy sector amid continued weakness in global oil prices. Shares of Alliance Data Systems, a provider of

marketing and customer loyalty programs, fell on weaker than expected earnings.

Leading individual contributors to relative performance included the Fund’s long positions in Jarden Corp., Thermo Fisher Scientific Inc. and Raytheon Co. Shares of Jarden, a consumer products company not held in the Benchmark, rose after it agreed to be acquired by Newell Rubbermaid Inc. for $15.4 billion. Shares of Thermo Fisher, a health care technology company, rose on better than expected earnings and revenue. Shares of Raytheon, an aerospace and technology company, rose on better-than-expected revenue growth.

HOW WAS THE FUND POSITIONED?

During the six months ended April 30, 2016, the Fund invested at least 80% of its assets under management in long and short positions in equity securities, selecting from a universe of equity securities with market capitalizations similar to those included in the Russell 1000 Index and/or S&P 500 Index. The Fund’s manager sought to achieve lower volatility than the Benchmark through a disciplined research process, security selection and risk management. For the six month reporting period, the Fund’s average gross exposure was 89% and its average net exposure was 45%.

| | | | | | | | |

| | | |

| APRIL 30, 2016 | | J.P. MORGAN SPECIALTY FUNDS | | | | | 3 | |

JPMorgan Opportunistic Equity Long/Short Fund

FUND COMMENTARY

SIX MONTHS ENDED APRIL 30, 2016 (Unaudited) (continued)

| | | | | | | | |

| TOP TEN LONG POSITIONS OF THE PORTFOLIO*** | |

| | 1. | | | Newell Brands, Inc. | | | 10.2 | % |

| | 2. | | | Twenty-First Century Fox, Inc., Class B | | | 6.7 | |

| | 3. | | | Thermo Fisher Scientific, Inc. | | | 5.8 | |

| | 4. | | | Altria Group, Inc. | | | 4.9 | |

| | 5. | | | Comcast Corp., Class A | | | 4.7 | |

| | 6. | | | Alphabet, Inc., Class A | | | 3.6 | |

| | 7. | | | Norwegian Cruise Line Holdings Ltd. | | | 3.3 | |

| | 8. | | | Becton, Dickinson and Co. | | | 3.0 | |

| | 9. | | | Reynolds American, Inc. | | | 2.9 | |

| | 10. | | | Fidelity National Information Services, Inc. | | | 2.8 | |

| | | | | | | | |

| TOP TEN SHORT POSITIONS OF THE PORTFOLIO**** | |

| | 1. | | | General Electric Co. | | | 12.2 | % |

| | 2. | | | SPDR S&P 500 ETF Trust | | | 11.9 | |

| | 3. | | | iShares Russell 2000 ETF | | | 8.6 | |

| | 4. | | | Clorox Co. (The) | | | 7.3 | |

| | 5. | | | Expeditors International of Washington, Inc. | | | 6.3 | |

| | 6. | | | Bed Bath & Beyond, Inc. | | | 5.7 | |

| | 7. | | | Cisco Systems, Inc. | | | 4.2 | |

| | 8. | | | Ross Stores, Inc. | | | 3.6 | |

| | 9. | | | American Express Co. | | | 3.2 | |

| | 10. | | | Whole Foods Market, Inc. | | | 2.9 | |

| | | | |

LONG PORTFOLIO COMPOSITION BY SECTOR*** | |

| Consumer Discretionary | | | 33.6 | % |

| Consumer Staples | | | 9.4 | |

| Health Care | | | 9.0 | |

| Information Technology | | | 8.7 | |

| Materials | | | 4.0 | |

| Industrials | | | 3.2 | |

| Others (each less than 1.0%) | | | 0.3 | |

| Short-Term Investment | | | 31.8 | |

| | | | |

SHORT PORTFOLIO COMPOSITION BY SECTOR**** | |

| Exchange Traded Funds | | | 20.5 | % |

| Industrials | | | 20.5 | |

| Consumer Discretionary | | | 20.4 | |

| Consumer Staples | | | 12.5 | |

| Financials | | | 11.4 | |

| Information Technology | | | 8.1 | |

| Health Care | | | 3.0 | |

| Energy | | | 1.4 | |

| Others (each less than 1.0%) | | | 2.2 | |

| * | | The return shown is based on net asset values calculated for shareholder transactions and may differ from the return shown in the financial highlights, which reflects adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America. |

| ** | | The adviser seeks to achieve the Fund’s objective. There can be no guarantee it will be achieved. |

| *** | | Percentages indicated are based on total long investments as of April 30, 2016. The Fund’s portfolio composition is subject to change. |

| **** | | Percentages indicated are based on total short investments as of April 30, 2016. The Fund’s portfolio composition is subject to change. |

| (a) | | Amount rounds to less than 0.1%. |

| | | | | | |

| | | |

| 4 | | | | J.P. MORGAN SPECIALTY FUNDS | | APRIL 30, 2016 |

| | | | | | | | | | | | | | |

AVERAGE ANNUAL TOTAL RETURNS AS OF APRIL 30, 2016 | |

| | | | |

| | | INCEPTION DATE OF

CLASS | | 6 MONTH* | | | 1 YEAR | | | SINCE

INCEPTION | |

CLASS A SHARES | | August 29, 2014 | | | | | | | | | | | | |

With Sales Charge** | | | | | (8.82 | )% | | | (3.27 | )% | | | 3.56 | % |

Without Sales Charge | | | | | (3.78 | ) | | | 2.10 | | | | 6.96 | |

CLASS C SHARES | | August 29, 2014 | | | | | | | | | | | | |

With CDSC*** | | | | | (5.04 | ) | | | 0.62 | | | | 6.42 | |

Without CDSC | | | | | (4.04 | ) | | | 1.62 | | | | 6.42 | |

CLASS R2 SHARES | | August 29, 2014 | | | (3.91 | ) | | | 1.86 | | | | 6.69 | |

CLASS R5 SHARES | | August 29, 2014 | | | (3.59 | ) | | | 2.58 | | | | 7.46 | |

CLASS R6 SHARES | | August 29, 2014 | | | (3.58 | ) | | | 2.65 | | | | 7.50 | |

CLASS SELECT SHARES | | August 29, 2014 | | | (3.65 | ) | | | 2.41 | | | | 7.23 | |

| ** | | Sales Charge for Class A Shares is 5.25%. |

| *** | | Assumes a 1% CDSC (contingent deferred sales charge) for the 6 month and one year periods and 0% CDSC thereafter. |

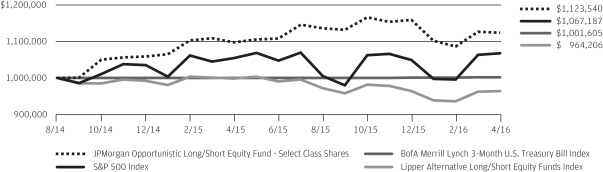

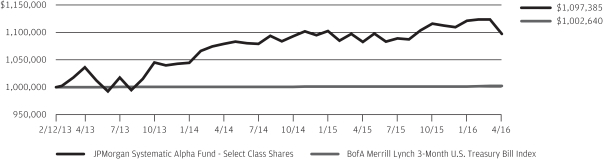

LIFE OF FUND PERFORMANCE (8/29/14 TO 4/30/16)

The performance quoted is past performance and is not a guarantee of future results. Mutual funds are subject to certain market risks. Investment returns and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data shown. For up-to-date month-end performance information please call 1-800-480-4111.

The Fund commenced operations on August 29, 2014.

The graph illustrates comparative performance for $1,000,000 invested in Select Class Shares of the JPMorgan Opportunistic Equity Long/Short Fund, the S&P 500 Index, the BofA Merrill Lynch 3-Month U.S. Treasury Bill Index and Lipper Alternative Long/Short Equity Funds Index from August 29, 2014 to April 30, 2016. The performance of the Fund assumes reinvestment of all dividends and capital gain distributions, if any, and does not include a sales charge. The performance of the S&P 500 Index and BofA Merrill Lynch 3-Month U.S. Treasury Bill Index does not reflect the deduction of expenses or a sales charge associated with a mutual fund and has been adjusted to reflect reinvestment of all dividends and capital gain distributions of securities included in the benchmarks, if applicable. The performance of the Lipper Alternative Long/Short Equity Funds Index includes expenses associated with a mutual fund, such as

investment management fees. These expenses are not identical to the expenses incurred by the Fund. The S&P 500 Index is an unmanaged index generally representative of the performance of large companies in the U.S. stock market. The BofA Merrill Lynch 3-Month U.S. Treasury Bill Index is comprised of a single issue purchased at the beginning of the month and held for a full month. Each month the index is rebalanced and the issue selected is the outstanding Treasury Bill that matures closest to, but not beyond, 3 months from the rebalancing date. The Lipper Alternative Long/Short Equity Funds Index represents the total returns of the funds in the indicated category as defined by Lipper, Inc. Investors cannot invest directly in an index.

Select Class Shares have a $1,000,000 minimum initial investment.

Fund performance may reflect the waiver of the Fund’s fees and reimbursement of expenses for certain periods since the inception date. Without these waivers and reimbursements, performance would have been lower. Also, performance shown in this section does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares.

The returns shown are based on net asset values calculated for shareholder transactions and may differ from the returns shown in the financial highlights, which reflect adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America.

| | | | | | | | |

| | | |

| APRIL 30, 2016 | | J.P. MORGAN SPECIALTY FUNDS | | | | | 5 | |

JPMorgan Research Equity Long/Short Fund

FUND COMMENTARY

SIX MONTHS ENDED APRIL 30, 2016 (Unaudited) (continued)

| | | | |

| REPORTING PERIOD RETURN: | |

| Fund (Class A Shares, without a sales charge)* | | | -1.85% | |

| BofA Merrill Lynch 3-Month U.S. Treasury Bill Index | | | 0.01% | |

| |

| Standard & Poor’s 500 Index | | | 0.43% | |

| Net Assets as of 4/30/2016 (In Thousands) | | $ | 43,499 | |

INVESTMENT OBJECTIVE**

The JPMorgan Research Equity Long/Short Fund (the “Fund”) seeks to provide long term capital appreciation.

WHAT WERE THE MAIN DRIVERS OF THE FUND’S PERFORMANCE?

The Fund’s Class A Shares, without a sales charge, underperformed the BofA Merrill Lynch 3-Month U.S. Treasury Bill Index (the “Benchmark”) and the Standard & Poor’s 500 Index for the six months ended April 30, 2016. Investors’ concerns about global economic growth as well as weakening oil prices and uncertainty over China’s economy, created a headwind for the Fund. Overall, stocks that the Fund’s portfolio managers found to be undervalued underperformed the broader market, while stocks that the portfolio managers found to be unattractively valued outperformed the broader market.

Leading detractors from the Fund’s absolute return included its security selection in the pharmaceutical & health care and consumer cyclical sectors. The Fund’s security selection in the semiconductors and media sectors was a leading positive contributor to absolute performance.

Leading individual detractors from absolute performance included the Fund’s long positions in Allergan PLC, Valeant Pharmaceuticals International Inc. and Bank of America Corp. Shares of Allergan, a pharmaceutical company, fell after its plan to merge with Pfizer Inc. collapsed in early April 2016. Shares of Valeant, a manufacture of drugs and medical devices, fell by 50% in mid-March when its chief executive said the company would not meet its earnings goals and may default on its debt. Shares of Bank of America declined amid the continuation of low, long-term interest rates.

Leading individual contributors to absolute performance included the Fund’s long positions in Broadcom Ltd., Facebook Inc. and Diamondback Energy Inc. Shares of Broadcom, a semiconductor manufacturer, rose after the company forecast strong revenue growth and gross margin expansion. Shares of Facebook, an Internet social media company, rose on a 57% increase in advertising revenue in the first three months of 2016. Shares of Diamondback Energy, an oil and natural gas producer, rose after the company announced plans to sell shares to raise cash to repay debt.

HOW WAS THE FUND POSITIONED?

The Fund’s portfolio managers used bottom-up fundamental research to construct a portfolio of long and short positions, researching companies in an attempt to determine their underlying value and potential for future earnings growth. Based on this research, the portfolio managers ranked stocks in the U.S. large-cap universe into five quintiles. The Fund’s portfolio managers looked to the top two quintiles for potential long positions in stocks that they believed were undervalued and looked to the bottom two quintiles for potential short positions in stocks that they believed were overvalued. The Fund’s portfolio managers attempted to limit the Fund’s overall market risk, holding long and short positions across a broad array of sectors. For the six month reporting period, the Fund’s average long exposure was 94% and its average short exposure was -61%.

| * | | The return shown is based on net asset values calculated for shareholder transactions and may differ from the return shown in the financial highlights, which reflects adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America. |

| ** | | The adviser seeks to achieve the Fund’s objective. There can be no guarantee it will be achieved. |

| | | | | | |

| | | |

| 6 | | | | J.P. MORGAN SPECIALTY FUNDS | | APRIL 30, 2016 |

| | | | | | | | |

| TOP TEN LONG POSITIONS OF THE PORTFOLIO* | |

| | 1. | | | Lowe’s Cos., Inc. | | | 3.4 | % |

| | 3. | | | Humana, Inc. | | | 2.7 | |

| | 4. | | | Union Pacific Corp. | | | 2.6 | |

| | 4. | | | Broadcom Ltd., (Singapore) | | | 2.4 | |

| | 5. | | | Facebook, Inc., Class A | | | 2.2 | |

| | 6. | | | Molson Coors Brewing Co., Class B | | | 2.2 | |

| | 7. | | | Alphabet, Inc., Class C | | | 2.1 | |

| | 8. | | | Amazon.com, Inc. | | | 2.1 | |

| | 9. | | | Chubb Ltd., (Switzerland) | | | 2.1 | |

| | 10. | | | NXP Semiconductors N.V., (Netherlands) | | | 2.1 | |

| | | | | | | | |

| TOP TEN SHORT POSITIONS OF THE PORTFOLIO** | |

| | 1. | | | General Electric Co. | | | 2.8 | % |

| | 2. | | | Verizon Communications, Inc. | | | 2.8 | |

| | 3. | | | Boeing Co. (The) | | | 2.5 | |

| | 4. | | | Dominion Resources, Inc. | | | 2.1 | |

| | 5. | | | Microchip Technology, Inc. | | | 2.0 | |

| | 6. | | | Kraft Heinz Co. (The) | | | 1.9 | |

| | 7. | | | Intel Corp. | | | 1.9 | |

| | 8. | | | W.R. Berkley Corp. | | | 1.7 | |

| | 9. | | | Ventas, Inc. | | | 1.7 | |

| | 10. | | | 3M Co. | | | 1.6 | |

| | | | |

LONG POSITION PORTFOLIO COMPOSITION BY SECTOR* | |

| Information Technology | | | 20.3 | % |

| Consumer Discretionary | | | 17.4 | |

| Financials | | | 15.6 | |

| Industrials | | | 14.2 | |

| Health Care | | | 10.4 | |

| Consumer Staples | | | 7.3 | |

| Materials | | | 5.1 | |

| Utilities | | | 4.6 | |

| Energy | | | 3.9 | |

| Telecommunication Services | | | 1.2 | |

| Short-Term Investment | | | 0.0 | (a) |

| | | | |

SHORT POSITION PORTFOLIO COMPOSITION BY SECTOR** | |

| Consumer Discretionary | | | 18.1 | % |

| Financials | | | 14.7 | |

| Industrials | | | 14.6 | |

| Information Technology | | | 13.7 | |

| Consumer Staples | | | 12.5 | |

| Health Care | | | 8.1 | |

| Utilities | | | 7.5 | |

| Materials | | | 5.5 | |

| Telecommunication Services | | | 3.8 | |

| Energy | | | 1.5 | |

| * | | Percentages indicated are based on total long investments as of April 30, 2016. The Fund’s portfolio composition is subject to change. |

| ** | | Percentages indicated are based on total short investments as of April 30, 2016. The Fund’s portfolio composition is subject to change. |

| | | | | | | | |

| | | |

| APRIL 30, 2016 | | J.P. MORGAN SPECIALTY FUNDS | | | | | 7 | |

JPMorgan Research Equity Long/Short Fund

FUND COMMENTARY

SIX MONTHS ENDED APRIL 30, 2016 (Unaudited) (continued)

| | | | | | | | |

AVERAGE ANNUAL TOTAL RETURNS AS OF APRIL 30, 2016 |

| | | | | | | | | | | | |

| | | | | |

| | | INCEPTION DATE OF

CLASS | | 6 MONTH* | | 1 YEAR | | 5 YEAR | | SINCE

INCEPTION |

CLASS A SHARES | | May 28, 2010 | | | | | | | | |

With Sales Charge** | | | | (7.01)% | | (8.67)% | | 0.68% | | 1.17% |

Without Sales Charge | | | | (1.85) | | (3.63) | | 1.77 | | 2.09 |

CLASS C SHARES | | May 28, 2010 | | | | | | | | |

With CDSC*** | | | | (3.10) | | (5.10) | | 1.25 | | 1.58 |

Without CDSC | | | | (2.10) | | (4.10) | | 1.25 | | 1.58 |

CLASS R5 SHARES | | May 28, 2010 | | (1.62) | | (3.14) | | 2.22 | | 2.55 |

SELECT CLASS SHARES | | May 28, 2010 | | (1.76) | | (3.35) | | 2.01 | | 2.34 |

| ** | | Sales Charge for Class A Shares is 5.25%. |

| *** | | Assumes a 1% CDSC (contingent deferred sales charge) for the 6 month and one year periods and 0% CDSC thereafter. |

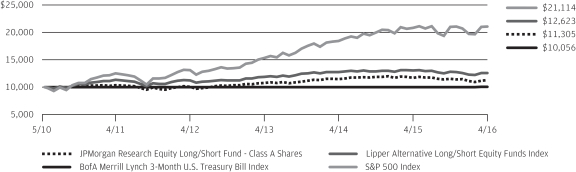

LIFE OF FUND PERFORMANCE (5/28/10 TO 4/30/16)

The performance quoted is past performance and is not a guarantee of future results. Mutual funds are subject to certain market risks. Investment returns and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data shown. For up-to-date, month-end performance information please call 1-800-480-4111.

The Fund commenced operations on May 28, 2010.

The graph illustrates comparative performance for $10,000 invested in Class A Shares of the JPMorgan Research Equity Long/Short Fund, the BofA Merrill Lynch 3-Month U.S. Treasury Bill Index, the S&P 500 Index and the Lipper Alternative Long/Short Equity Funds Index from May 28, 2010 to April 30, 2016. The performance of the Fund assumes reinvestment of all dividends and capital gain distributions, if any, and includes a sales charge. The performance of the BofA Merrill Lynch 3-Month U.S. Treasury Bill Index and the S&P 500 Index does not reflect the deduction of expenses or a sales charge associated with a mutual fund and has been adjusted to reflect reinvestment of all dividends and capital gain distributions of securities included in the benchmarks, if applicable. The performance of the Lipper Alternative Long/Short Equity Funds Index includes expenses associated with a mutual fund, such as investment management fees. These expenses are not identical to the expenses incurred by the

Fund. The BofA Merrill Lynch 3-Month U.S. Treasury Bill Index is comprised of a single issue purchased at the beginning of the month and held for a full month. Each month the index is rebalanced and the issue selected is the outstanding Treasury Bill that matures closest to, but not beyond, 3 months from the rebalancing date. The S&P 500 Index is an unmanaged index generally representative of the performance of large companies in the U.S. stock market. The Lipper Alternative Long/Short Equity Funds Index represents the total returns of the funds in the indicated category as defined by Lipper, Inc. Investors cannot invest directly in an index.

Class A Shares have a $1,000 minimum initial investment and carry a 5.25% sales charge.

Fund performance may reflect the waiver of the Fund’s fees and reimbursement of expenses for certain periods since the inception date. Without these waivers and reimbursements, performance would have been lower. Also, performance shown in this section does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares.

The returns shown are based on net asset values calculated for shareholder transactions and may differ from the returns shown in the financial highlights, which reflect adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America.

| | | | | | |

| | | |

| 8 | | | | J.P. MORGAN SPECIALTY FUNDS | | APRIL 30, 2016 |

JPMorgan Research Market Neutral Fund

FUND COMMENTARY

SIX MONTHS ENDED APRIL 30, 2016 (Unaudited)

| | | | |

| REPORTING PERIOD RETURN: | |

| Fund (Institutional Class Shares)* | | | -2.87% | |

| BofA Merrill Lynch 3-Month U.S. Treasury Bill Index | | | 0.01% | |

| |

| Net Assets as of 4/30/2016 (In Thousands) | | $ | 432,681 | |

INVESTMENT OBJECTIVE**

The JPMorgan Research Market Neutral Fund (the “Fund”) seeks to provide long-term capital appreciation from a broadly diversified portfolio of U.S. stocks while neutralizing the general risks associated with stock market investing.

WHAT WERE THE MAIN DRIVERS OF THE FUND’S PERFORMANCE?

The Fund (Institutional Class Shares) underperformed the BofA Merrill Lynch 3-Month U.S. Treasury Bill Index (the “Benchmark”) for the six months ended April 30, 2016. Investors’ concerns about global economic growth as well as weakening oil prices and uncertainty over China’s economy, created a headwind for the Fund. Overall, stocks that the Fund’s portfolio managers found to be undervalued underperformed the broader market, while stocks that the research team found to be unattractively valued outperformed the broader market.

The Fund’s security selection in the pharmaceutical & health care and consumer cyclical sectors was a leading detractor from performance relative to the Benchmark, while security selection in the semiconductors and media sectors was a leading positive contributor to relative performance.

Leading individual detractors from relative performance included the Fund’s long position in Valeant Pharmaceuticals Inc. and its short positions in Johnson & Johnson and Mattel Inc. Shares of Valeant, a manufacture of drugs and medical devices, fell by 50% in mid-March when its chief executive said the company would not meet its earnings goals and may default on its debt. Shares of Johnson & Johnson, a consumer health care products company, rose after the company reported better than expected quarterly earnings and revenue despite head-

winds in overseas markets from the relative strength of the U.S. dollar. Shares of Mattel, a toy maker, rose on better than expected quarterly sales.

Leading individual contributors to the Fund’s relative performance included its long positions in Broadcom Ltd. and Facebook Inc. and its short position in Micron Technology Inc. Shares of Broadcom, a semiconductor manufacturer, rose after the company forecast strong revenue growth and gross margin expansion. Shares of Facebook, an Internet social media company, rose on a 57% increase in advertising revenue in the first three months of 2016. Shares of Micron Technology, a maker of semiconductors, fell after the company forecast weakness in earnings.

HOW WAS THE FUND POSITIONED?

The Fund’s portfolio managers aimed to construct a portfolio of long and short positions with a low correlation to traditional investments such as stocks and bonds. The Fund’s portfolio managers used fundamental research to estimate companies’ long-term earnings forecasts, ranking approximately 600 large and mid cap stocks into five quintiles. The Fund’s portfolio managers looked to the top two quintiles for potential long positions in stocks that they believed were undervalued and the bottom two quintiles for potential short positions in stocks that they believed were overvalued.

| * | | The return shown is based on net asset values calculated for shareholder transactions and may differ from the return shown in the financial highlights, which reflects adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America. |

| ** | | The adviser seeks to achieve the Fund’s objective. There can be no guarantee it will be achieved. |

| | | | | | | | |

| | | |

| APRIL 30, 2016 | | J.P. MORGAN SPECIALTY FUNDS | | | | | 9 | |

JPMorgan Research Market Neutral Fund

FUND COMMENTARY

SIX MONTHS ENDED APRIL 30, 2016 (Unaudited) (continued)

| | | | | | | | |

| TOP TEN LONG POSITIONS OF THE PORTFOLIO* | |

| | 1. | | | Lowe’s Cos., Inc., | | | 2.7 | % |

| | 2. | | | Broadcom Ltd., (Singapore) | | | 2.5 | |

| | 3. | | | Humana, Inc., | | | 2.4 | |

| | 4. | | | Union Pacific Corp., | | | 2.4 | |

| | 5. | | | NXP Semiconductors N.V., (Netherlands) | | | 2.1 | |

| | 6. | | | Chubb Ltd., (Switzerland) | | | 2.1 | |

| | 7. | | | Lam Research Corp., | | | 2.0 | |

| | 8. | | | Molson Coors Brewing Co., Class B, | | | 1.9 | |

| | 9. | | | Twenty-First Century Fox, Inc., Class B, | | | 1.7 | |

| | 10. | | | Canadian Pacific Railway Ltd., (Canada) | | | 1.6 | |

| | | | | | | | |

| TOP TEN SHORT POSITIONS OF THE PORTFOLIO** | |

| | 1. | | | Verizon Communications, Inc., | | | 2.4 | % |

| | 2. | | | Medtronic plc, (Ireland) | | | 2.2 | |

| | 3. | | | General Electric Co., | | | 2.1 | |

| | 4. | | | Boeing Co. (The), | | | 2.1 | |

| | 5. | | | Intel Corp., | | | 1.8 | |

| | 6. | | | Kraft Heinz Co. (The), | | | 1.7 | |

| | 7. | | | Duke Energy Corp., | | | 1.6 | |

| | 8. | | | Cisco Systems, Inc., | | | 1.6 | |

| | 9. | | | Dominion Resources, Inc., | | | 1.6 | |

| | 10. | | | Taiwan Semiconductor Manufacturing Co., Ltd., ADR, (Taiwan) | | | 1.6 | |

| | | | |

LONG POSITION PORTFOLIO COMPOSITION BY SECTOR* | |

| Information Technology | | | 17.6 | % |

| Consumer Discretionary | | | 14.9 | |

| Financials | | | 13.9 | |

| Industrials | | | 12.2 | |

| Health Care | | | 9.5 | |

| Consumer Staples | | | 6.7 | |

| Utilities | | | 4.9 | |

| Materials | | | 4.8 | |

| Energy | | | 3.1 | |

| Telecommunication Services | | | 1.1 | |

| U.S. Treasury Obligations | | | 0.1 | |

| Short-Term Investment | | | 11.2 | |

| | | | |

SHORT POSITION PORTFOLIO COMPOSITION BY SECTOR** | |

| Consumer Discretionary | | | 17.6 | % |

| Financials | | | 15.3 | |

| Information Technology | | | 14.8 | |

| Industrials | | | 13.0 | |

| Consumer Staples | | | 11.4 | |

| Health Care | | | 10.1 | |

| Utilities | | | 6.2 | |

| Materials | | | 5.3 | |

| Telecommunication Services | | | 3.2 | |

| Energy | | | 3.1 | |

| * | | Percentages indicated are based on total long investments as of April 30, 2016. The Fund’s portfolio composition is subject to change. |

| ** | | Percentages indicated are based on total short investments as of April 30, 2016. The Fund’s portfolio composition is subject to change. |

| | | | | | |

| | | |

| 10 | | | | J.P. MORGAN SPECIALTY FUNDS | | APRIL 30, 2016 |

| | | | | | | | | | |

AVERAGE ANNUAL TOTAL RETURNS AS OF APRIL 30, 2016 |

TOTAL RETURNS AS OF APRIL 30, 2016

| | | | | | | | | | | | | | | | | | |

| | | INCEPTION DATE OF

CLASS | | 6 MONTH* | | | 1 YEAR | | | 5 YEAR | | | 10 YEAR | |

CLASS A SHARES | | February 28, 2002 | | | | | | | | | | | | | | | | |

With Sales Charge** | | | | | (8.18 | )% | | | (9.38 | )% | | | (2.12 | )% | | | 0.72 | % |

Without Sales Charge | | | | | (3.09 | ) | | | (4.36 | ) | | | (1.06 | ) | | | 1.26 | |

CLASS C SHARES | | November 2, 2009 | | | | | | | | | | | | | | | | |

With CDSC*** | | | | | (4.33 | ) | | | (5.88 | ) | | | (1.55 | ) | | | 0.75 | |

Without CDSC | | | | | (3.33 | ) | | | (4.88 | ) | | | (1.55 | ) | | | 0.75 | |

INSTITUTIONAL CLASS SHARES | | December 31, 1998 | | | (2.87 | ) | | | (3.89 | ) | | | (0.57 | ) | | | 1.76 | |

SELECT CLASS SHARES | | November 2, 2009 | | | (2.98 | ) | | | (4.09 | ) | | | (0.80 | ) | | | 1.60 | |

| ** | | Sales Charge for Class A Shares is 5.25%. |

| *** | | Assumes a 1% CDSC (contingent deferred sales charge) for the 6 month and one year periods and 0% CDSC thereafter. |

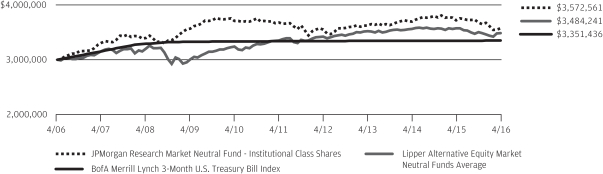

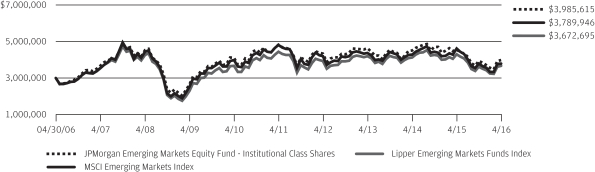

TEN YEAR FUND PERFORMANCE (4/30/06 to 4/30/16)

The performance quoted is past performance and is not a guarantee of future results. Mutual funds are subject to certain market risks. Investment returns and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data shown. For up-to-date month-end performance information please call 1-800-480-4111.

Returns for Select Class Shares prior to its inception date are based on the performance of Institutional Class Shares. The actual returns for Select Class Shares would have been lower than shown because Select Class Shares have higher expenses than Institutional Class Shares.

The graph illustrates comparative performance for $3,000,000 invested in Institutional Class Shares of the JPMorgan Research Market Neutral Fund, BofA Merrill Lynch 3-Month U.S. Treasury Bill Index and Lipper Alternative Equity Market Neutral Funds Average from April 30, 2006 to April 30, 2016. The performance of the Fund assumes reinvestment of all dividends and capital gain distributions, if any, and does not include a sales charge. The performance of the BofA Merrill Lynch 3-Month U.S. Treasury Bill Index does not reflect the deduction of expenses or a sales charge associated with a mutual fund and has been adjusted to reflect reinvestment of all dividends and capital gain distributions of the securities included in the benchmark, if applicable. The performance of the Lipper Alternative

Equity Market Neutral Funds Average includes expenses associated with a mutual fund, such as investment management fees. These expenses are not identical to the expenses incurred by the Fund. The BofA Merrill Lynch 3-Month U.S. Treasury Bill Index is comprised of a single issue purchased at the beginning of the month and held for a full month. Each month the index is rebalanced and the issue selected is the outstanding Treasury Bill that matures closest to, but not beyond, 3 months from the rebalancing date. Investors cannot invest directly in an index. The Lipper Alternative Equity Market Neutral Funds Average is an average based on the total returns of all mutual funds within the Fund’s designated category as determined by Lipper, Inc.

Institutional Class Shares have a $3,000,000 minimum initial investment.

Fund performance may reflect the waiver of the Fund’s fees and reimbursement of expenses for certain periods since the inception date. Without these waivers and reimbursements, performance would have been lower. Also, performance shown in this section does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares.

The returns shown are based on net asset values calculated for shareholder transactions and may differ from the returns shown in the financial highlights, which reflect adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America.

| | | | | | | | |

| | | |

| APRIL 30, 2016 | | J.P. MORGAN SPECIALTY FUNDS | | | | | 11 | |

JPMorgan Opportunistic Equity Long/Short Fund

SCHEDULE OF PORTFOLIO INVESTMENTS

AS OF APRIL 30, 2016 (Unaudited)

(Amounts in thousands)

| | | | | | | | |

| SHARES | | | SECURITY DESCRIPTION | | VALUE($) | |

| Long Positions — 99.0% | |

| Common Stocks — 67.5% | |

| | | | Consumer Discretionary — 33.3% | |

| | | | Auto Components — 0.0% (g) | |

| | 1 | | | BorgWarner, Inc. (j) | | | 21 | |

| | — | (h) | | Delphi Automotive plc, (United Kingdom) (j) | | | 22 | |

| | 1 | | | Johnson Controls, Inc. (j) | | | 22 | |

| | | | | | | | |

| | | | | | | 65 | |

| | | | | | | | |

| | | | Distributors — 1.2% | |

| | 86 | | | LKQ Corp. (a) (j) | | | 2,758 | |

| | | | | | | | |

| | | | Hotels, Restaurants & Leisure — 3.3% | |

| | 1 | | | Hilton Worldwide Holdings, Inc. (j) | | | 23 | |

| | 149 | | | Norwegian Cruise Line Holdings Ltd. (a) (j) | | | 7,272 | |

| | — | (h) | | Starbucks Corp. (j) | | | 22 | |

| | — | (h) | | Yum! Brands, Inc. (j) | | | 22 | |

| | | | | | | | |

| | | | | | | 7,339 | |

| | | | | | | | |

| | | | Household Durables — 12.5% | |

| | 1 | | | D.R. Horton, Inc. (j) | | | 22 | |

| | 28 | | | Mohawk Industries, Inc. (a) (j) | | | 5,358 | |

| | 496 | | | Newell Brands, Inc. (j) | | | 22,597 | |

| | | | | | | | |

| | | | | | | 27,977 | |

| | | | | | | | |

| | | | Internet & Catalog Retail — 1.5% | |

| | 5 | | | Amazon.com, Inc. (a) (j) | | | 3,391 | |

| | | | | | | | |

| | | | Media — 12.9% | |

| | 16 | | | Charter Communications, Inc., Class A (a) (j) | | | 3,500 | |

| | 172 | | | Comcast Corp., Class A (j) | | | 10,469 | |

| | — | (h) | | Time Warner, Inc. (j) | | | 22 | |

| | 499 | | | Twenty-First Century Fox, Inc., Class B (j) | | | 15,022 | |

| | | | | | | | |

| | | | | | | 29,013 | |

| | | | | | | | |

| | | | Multiline Retail — 0.0% (g) | |

| | — | (h) | | Dollar General Corp. (j) | | | 22 | |

| | | | | | | | |

| | | | Specialty Retail — 1.9% | |

| | — | (h) | | Home Depot, Inc. (The) (j) | | | 22 | |

| | — | (h) | | Lowe’s Cos., Inc. (j) | | | 23 | |

| | — | (h) | | O’Reilly Automotive, Inc. (a) (j) | | | 22 | |

| | 38 | | | Signet Jewelers Ltd. (j) | | | 4,113 | |

| | — | (h) | | TJX Cos., Inc. (The) (j) | | | 22 | |

| | | | | | | | |

| | | | | | | 4,202 | |

| | | | | | | | |

| | | | Textiles, Apparel & Luxury Goods — 0.0% (g) | |

| | — | (h) | | V.F. Corp. (j) | | | 22 | |

| | | | | | | | |

| | | | Total Consumer Discretionary | | | 74,789 | |

| | | | | | | | |

| | | | Consumer Staples — 9.3% | |

| | | | Beverages — 1.4% | |

| | 12 | | | Anheuser-Busch InBev N.V., (Belgium), ADR (j) | | | 1,500 | |

| | | | | | | | |

| SHARES | | | SECURITY DESCRIPTION | | VALUE($) | |

| | | | | | | | |

| | | | | | | | |

| | | | Beverages — continued | |

| | 17 | | | Brown-Forman Corp., Class B (j) | | | 1,597 | |

| | — | (h) | | Molson Coors Brewing Co., Class B (j) | | | 45 | |

| | | | | | | | |

| | | | | | | 3,142 | |

| | | | | | | | |

| | | | Food & Staples Retailing — 0.1% | |

| | — | (h) | | Costco Wholesale Corp. (j) | | | 44 | |

| | 1 | | | Kroger Co. (The) (j) | | | 45 | |

| | 1 | | | Walgreens Boots Alliance, Inc. (j) | | | 45 | |

| | | | | | | | |

| | | | | | | 134 | |

| | | | | | | | |

| | | | Food Products — 0.0% (g) | |

| | 1 | | | Mondelez International, Inc., Class A (j) | | | 46 | |

| | | | | | | | |

| | | | Household Products — 0.0% (g) | |

| | — | (h) | | Kimberly-Clark Corp. (j) | | | 45 | |

| | | | | | | | |

| | | | Tobacco — 7.8% | |

| | 174 | | | Altria Group, Inc. (j) | | | 10,930 | |

| | 132 | | | Reynolds American, Inc. (j) | | | 6,563 | |

| | | | | | | | |

| | | | | | | 17,493 | |

| | | | | | | | |

| | | | Total Consumer Staples | | | 20,860 | |

| | | | | | | | |

| | | | Energy — 0.1% | |

| | | | Energy Equipment & Services — 0.0% (g) | |

| | 1 | | | Halliburton Co. (j) | | | 23 | |

| | | | | | | | |

| | | | Oil, Gas & Consumable Fuels — 0.1% | |

| | 1 | | | Cabot Oil & Gas Corp. (j) | | | 23 | |

| | — | (h) | | Chevron Corp. (j) | | | 23 | |

| | — | (h) | | Diamondback Energy, Inc. (j) | | | 23 | |

| | — | (h) | | EQT Corp. (j) | | | 23 | |

| | — | (h) | | Hess Corp. (j) | | | 21 | |

| | 1 | | | Kinder Morgan, Inc. (j) | | | 22 | |

| | 1 | | | Marathon Petroleum Corp. (j) | | | 21 | |

| | — | (h) | | Occidental Petroleum Corp. (j) | | | 23 | |

| | — | (h) | | Pioneer Natural Resources Co. (j) | | | 24 | |

| | 1 | | | TransCanada Corp., (Canada) (j) | | | 23 | |

| | — | (h) | | Valero Energy Corp. (j) | | | 22 | |

| | | | | | | | |

| | | | | | | 248 | |

| | | | | | | | |

| | | | Total Energy | | | 271 | |

| | | | | | | | |

| | | | Financials — 0.2% | |

| | | | Banks — 0.1% | |

| | 2 | | | Bank of America Corp. (j) | | | 22 | |

| | — | (h) | | Citigroup, Inc. (j) | | | 22 | |

| | 2 | | | KeyCorp (j) | | | 22 | |

| | — | (h) | | Wells Fargo & Co. (j) | | | 22 | |

| | 1 | | | Zions Bancorporation (j) | | | 23 | |

| | | | | | | | |

| | | | | | | 111 | |

| | | | | | | | |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | |

| | | |

| 12 | | | | J.P. MORGAN SPECIALTY FUNDS | | APRIL 30, 2016 |

| | | | | | | | |

| SHARES | | | SECURITY DESCRIPTION | | VALUE($) | |

| Long Positions — continued | |

| Common Stocks — continued | |

| | | | Capital Markets — 0.0% (g) | |

| | — | (h) | | Ameriprise Financial, Inc. (j) | | | 22 | |

| | — | (h) | | BlackRock, Inc. (j) | | | 22 | |

| | 1 | | | Charles Schwab Corp. (The) (j) | | | 21 | |

| | 1 | | | Morgan Stanley (j) | | | 22 | |

| | | | | | | | |

| | | | | | | 87 | |

| | | | | | | | |

| | | | Consumer Finance — 0.0% (g) | |

| | 1 | | | Ally Financial, Inc. (a) (j) | | | 22 | |

| | — | (h) | | Discover Financial Services (j) | | | 23 | |

| | | | | | | | |

| | | | | | | 45 | |

| | | | | | | | |

| | | | Diversified Financial Services — 0.0% (g) | |

| | — | (h) | | Intercontinental Exchange, Inc. (j) | | | 23 | |

| | 1 | | | Voya Financial, Inc. (j) | | | 22 | |

| | | | | | | | |

| | | | | | | 45 | |

| | | | | | | | |

| | | | Insurance — 0.0% (g) | |

| | 1 | | | Arthur J. Gallagher & Co. (j) | | | 23 | |

| | — | (h) | | Chubb Ltd., (Switzerland) (j) | | | 22 | |

| | — | (h) | | Marsh & McLennan Cos., Inc. (j) | | | 23 | |

| | — | (h) | | MetLife, Inc. (j) | | | 22 | |

| | 1 | | | XL Group plc, (Ireland) (j) | | | 20 | |

| | | | | | | | |

| | | | | | | 110 | |

| | | | | | | | |

| | | | Real Estate Investment Trusts (REITs) — 0.1% | |

| | — | (h) | | American Tower Corp. (j) | | | 23 | |

| | — | (h) | | AvalonBay Communities, Inc. (j) | | | 22 | |

| | 1 | | | HCP, Inc. (j) | | | 23 | |

| | 1 | | | Kimco Realty Corp. (j) | | | 22 | |

| | 1 | | | LaSalle Hotel Properties (j) | | | 23 | |

| | 1 | | | Omega Healthcare Investors, Inc. (j) | | | 22 | |

| | — | (h) | | SL Green Realty Corp. (j) | | | 22 | |

| | | | | | | | |

| | | | | | | 157 | |

| | | | | | | | |

| | | | Total Financials | | | 555 | |

| | | | | | | | |

| | | | Health Care — 8.9% | |

| | | | Biotechnology — 0.1% | |

| | — | (h) | | Alexion Pharmaceuticals, Inc. (a) (j) | | | 40 | |

| | — | (h) | | Celgene Corp. (a) (j) | | | 42 | |

| | — | (h) | | Gilead Sciences, Inc. (j) | | | 39 | |

| | 1 | | | Incyte Corp. (a) (j) | | | 43 | |

| | 1 | | | Vertex Pharmaceuticals, Inc. (a) (j) | | | 44 | |

| | | | | | | | |

| | | | | | | 208 | |

| | | | | | | | |

| | | | Health Care Equipment & Supplies — 3.0% | |

| | 1 | | | Abbott Laboratories (j) | | | 40 | |

| | 41 | | | Becton, Dickinson and Co. (j) | | | 6,650 | |

| | | | | | | | |

| SHARES | | | SECURITY DESCRIPTION | | VALUE($) | |

| | | | | | | | |

| | | | | | | | |

| | | | Health Care Equipment & Supplies — continued | |

| | 2 | | | Boston Scientific Corp. (a) (j) | | | 50 | |

| | | | | | | | |

| | | | | | | 6,740 | |

| | | | | | | | |

| | | | Health Care Providers & Services — 0.0% (g) | |

| | — | (h) | | McKesson Corp. (j) | | | 43 | |

| | | | | | | | |

| | | | Life Sciences Tools & Services — 5.7% | |

| | — | (h) | | Illumina, Inc. (a) (j) | | | 43 | |

| | 89 | | | Thermo Fisher Scientific, Inc. (j) | | | 12,814 | |

| | | | | | | | |

| | | | | | | 12,857 | |

| | | | | | | | |

| | | | Pharmaceuticals — 0.1% | |

| | 1 | | | Bristol-Myers Squibb Co. (j) | | | 45 | |

| | 1 | | | Eli Lilly & Co. (j) | | | 44 | |

| | | | | | | | |

| | | | | | | 89 | |

| | | | | | | | |

| | | | Total Health Care | | | 19,937 | |

| | | | | | | | |

| | | | Industrials — 3.1% | |

| | | | Aerospace & Defense — 0.0% (g) | | | | |

| | — | (h) | | Honeywell International, Inc. (j) | | | 23 | |

| | — | (h) | | Northrop Grumman Corp. (j) | | | 23 | |

| | — | (h) | | United Technologies Corp. (j) | | | 22 | |

| | | | | | | | |

| | | | | | | 68 | |

| | | | | | | | |

| | | | Building Products — 0.0% (g) | |

| | — | (h) | | Lennox International, Inc. (j) | | | 22 | |

| | 1 | | | Masco Corp. (j) | | | 21 | |

| | | | | | | | |

| | | | | | | 43 | |

| | | | | | | | |

| | | | Commercial Services & Supplies — 0.0% (g) | |

| | — | (h) | | Waste Connections, Inc. (j) | | | 23 | |

| | | | | | | | |

| | | | Electrical Equipment — 0.0% (g) | |

| | — | (h) | | Eaton Corp. plc (j) | | | 23 | |

| | | | | | | | |

| | | | Machinery — 2.1% | |

| | — | (h) | | Cummins, Inc. (j) | | | 23 | |

| | — | (h) | | PACCAR, Inc. (j) | | | 23 | |

| | 39 | | | Parker-Hannifin Corp. (j) | | | 4,568 | |

| | | | | | | | |

| | | | | | | 4,614 | |

| | | | | | | | |

| | | | Road & Rail — 1.0% | |

| | 16 | | | Canadian Pacific Railway Ltd., (Canada) (j) | | | 2,257 | |

| | — | (h) | | Union Pacific Corp. (j) | | | 22 | |

| | | | | | | | |

| | | | | | | 2,279 | |

| | | | | | | | |

| | | | Trading Companies & Distributors — 0.0% (g) | |

| | 1 | | | AerCap Holdings N.V., (Ireland) (a) (j) | | | 22 | |

| | | | | | | | |

| | | | Total Industrials | | | 7,072 | |

| | | | | | | | |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | | | |

| | | |

| APRIL 30, 2016 | | J.P. MORGAN SPECIALTY FUNDS | | | | | 13 | |

JPMorgan Opportunistic Equity Long/Short Fund

SCHEDULE OF PORTFOLIO INVESTMENTS

AS OF APRIL 30, 2016 (Unaudited) (continued)

(Amounts in thousands)

| | | | | | | | |

| SHARES | | | SECURITY DESCRIPTION | | VALUE($) | |

| Long Positions — continued | |

| Common Stocks — continued | |

| | | | Information Technology — 8.6% | |

| | | | Electronic Equipment, Instruments &

Components — 0.0% (g) | |

| | 1 | | | TE Connectivity Ltd., (Switzerland) (j) | | | 44 | |

| | | | | | | | |

| | | | Internet Software & Services — 3.6% | |

| | 11 | | | Alphabet, Inc., Class A (a) (j) | | | 8,045 | |

| | — | (h) | | Facebook, Inc., Class A (a) (j) | | | 48 | |

| | | | | | | | |

| | | | | | | 8,093 | |

| | | | | | | | |

| | | | IT Services — 4.3% | |

| | — | (h) | | Accenture plc, (Ireland), Class A (j) | | | 45 | |

| | 95 | | | Fidelity National Information Services, Inc. (j) | | | 6,238 | |

| | 16 | | | MasterCard, Inc., Class A (j) | | | 1,522 | |

| | 1 | | | PayPal Holdings, Inc. (a) (j) | | | 44 | |

| | 1 | | | Vantiv, Inc., Class A (a) (j) | | | 45 | |

| | 23 | | | Visa, Inc., Class A (j) | | | 1,744 | |

| | 1 | | | WEX, Inc. (a) (j) | | | 48 | |

| | | | | | | | |

| | | | | | | 9,686 | |

| | | | | | | | |

| | | | Semiconductors & Semiconductor Equipment — 0.1% | |

| | — | (h) | | Broadcom Ltd., (Singapore) (j) | | | 44 | |

| | 1 | | | Lam Research Corp. (j) | | | 43 | |

| | 4 | | | Marvell Technology Group Ltd., (Bermuda) (j) | | | 44 | |

| | 1 | | | NXP Semiconductors N.V., (Netherlands) (a) (j) | | | 46 | |

| | 1 | | | Qorvo, Inc. (a) (j) | | | 44 | |

| | 1 | | | Skyworks Solutions, Inc. (j) | | | 43 | |

| | 1 | | | Texas Instruments, Inc. (j) | | | 44 | |

| | | | | | | | |

| | | | | | | 308 | |

| | | | | | | | |

| | | | Software — 0.1% | |

| | — | (h) | | Adobe Systems, Inc. (a) (j) | | | 45 | |

| | 1 | | | Workday, Inc., Class A (a) (j) | | | 44 | |

| | | | | | | | |

| | | | | | | 89 | |

| | | | | | | | |

| | | | Technology Hardware, Storage & Peripherals — 0.5% | |

| | 11 | | | Apple, Inc. (j) | | | 1,074 | |

| | 4 | | | HP, Inc. (j) | | | 44 | |

| | 1 | | | Western Digital Corp. (j) | | | 42 | |

| | | | | | | | |

| | | | | | | 1,160 | |

| | | | | | | | |

| | | | Total Information Technology | | | 19,380 | |

| | | | | | | | |

| | | | Materials — 3.9% | |

| | | | Chemicals — 1.7% | |

| | — | (h) | | Albemarle Corp. (j) | | | 22 | |

| | 1 | | | CF Industries Holdings, Inc. (j) | | | 22 | |

| | — | (h) | | E.I. du Pont de Nemours & Co. (j) | | | 23 | |

| | — | (h) | | Eastman Chemical Co. (j) | | | 22 | |

| | 32 | | | Ecolab, Inc. (j) | | | 3,628 | |

| | | | | | | | |

| SHARES | | | SECURITY DESCRIPTION | | VALUE($) | |

| | | | | | | | |

| | | | | | | | |

| | | | Chemicals — continued | |

| | 1 | | | Mosaic Co. (The) (j) | | | 22 | |

| | | | | | | | |

| | | | | | | 3,739 | |

| | | | | | | | |

| | | | Construction Materials — 0.0% (g) | |

| | — | (h) | | Martin Marietta Materials, Inc. (j) | | | 22 | |

| | — | (h) | | Vulcan Materials Co. (j) | | | 22 | |

| | | | | | | | |

| | | | | | | 44 | |

| | | | | | | | |

| | | | Containers & Packaging — 2.2% | |

| | 139 | | | Berry Plastics Group, Inc. (a) (j) | | | 5,001 | |

| | — | (h) | | Crown Holdings, Inc. (a) (j) | | | 22 | |

| | 1 | | | WestRock Co. (j) | | | 24 | |

| | | | | | | | |

| | | | | | | 5,047 | |

| | | | | | | | |

| | | | Total Materials | | | 8,830 | |

| | | | | | | | |

| | | | Telecommunication Services — 0.0% (g) | |

| | | | Diversified Telecommunication Services — 0.0% (g) | |

| | — | (h) | | Level 3 Communications, Inc. (a) (j) | | | 22 | |

| | — | (h) | | SBA Communications Corp., Class A (a) (j) | | | 22 | |

| | | | | | | | |

| | | | | | | 44 | |

| | | | | | | | |

| | | | Wireless Telecommunication Services — 0.0% (g) | |

| | 1 | | | T-Mobile U.S., Inc. (a) (j) | | | 22 | |

| | | | | | | | |

| | | | Total Telecommunication Services | | | 66 | |

| | | | | | | | |

| | | | Utilities — 0.1% | |

| | | | Electric Utilities — 0.1% | |

| | — | (h) | | American Electric Power Co., Inc. (j) | | | 23 | |

| | — | (h) | | Edison International (j) | | | 23 | |

| | — | (h) | | NextEra Energy, Inc. (j) | | | 23 | |

| | 1 | | | PPL Corp. (j) | | | 23 | |

| | 1 | | | Xcel Energy, Inc. (j) | | | 23 | |

| | | | | | | | |

| | | | | | | 115 | |

| | | | | | | | |

| | | | Water Utilities — 0.0% (g) | |

| | — | (h) | | American Water Works Co., Inc. (j) | | | 24 | |

| | | | | | | | |

| | | | Total Utilities | | | 139 | |

| | | | | | | | |

| | | | Total Common Stocks

(Cost $141,295) | | | 151,899 | |

| | | | | | | | |

| Short-Term Investment — 31.5% | |

| | | | Investment Company — 31.5% | | | | |

| | 70,709 | | | JPMorgan Prime Money Market Fund, Institutional Class Shares, 0.390% (b) (j) (l)

(Cost $70,709) | | | 70,709 | |

| | | | | | | | |

| | | | Total Investments — 99.0%

(Cost $212,004) | | | 222,608 | |

| | | | Other Assets in Excess of

Liabilities — 1.0% | | | 2,141 | |

| | | | | | | | |

| | | | NET ASSETS — 100.0% | | $ | 224,749 | |

| | | | | | | | |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | |

| | | |

| 14 | | | | J.P. MORGAN SPECIALTY FUNDS | | APRIL 30, 2016 |

| | | | | | | | |

| SHARES | | | SECURITY DESCRIPTION | | VALUE($) | |

| Short Positions — 16.7% | |

| Common Stocks — 13.3% | |

| | | | Consumer Discretionary — 3.4% | | | | |

| | | | Auto Components — 0.1% | | | | |

| | 1 | | | Lear Corp. | | | 170 | |

| | | | | | | | |

| | | | Automobiles — 0.4% | | | | |

| | 21 | | | Harley-Davidson, Inc. | | | 997 | |

| | | | | | | | |

| | | | Hotels, Restaurants & Leisure — 0.1% | | | | |

| | 3 | | | Darden Restaurants, Inc. | | | 165 | |

| | | | | | | | |

| | | | Media — 0.7% | | | | |

| | 3 | | | AMC Networks, Inc., Class A (a) | | | 189 | |

| | 7 | | | Discovery Communications, Inc., Class A (a) | | | 198 | |

| | 7 | | | Interpublic Group of Cos., Inc. (The) | | | 163 | |

| | 2 | | | Omnicom Group, Inc. | | | 165 | |

| | 13 | | | Scripps Networks Interactive, Inc., Class A | | | 830 | |

| | | | | | | | |

| | | | | | | 1,545 | |

| | | | | | | | |

| | | | Multiline Retail — 0.4% | | | | |

| | 20 | | | Kohl’s Corp. | | | 893 | |

| | | | | | | | |

| | | | Specialty Retail — 1.7% | | | | |

| | — | (h) | | AutoZone, Inc. (a) | | | 166 | |

| | 46 | | | Bed Bath & Beyond, Inc. (a) | | | 2,153 | |

| | 7 | | | Best Buy Co., Inc. | | | 233 | |

| | 24 | | | Ross Stores, Inc. | | | 1,358 | |

| | | | | | | | |

| | | | | | | 3,910 | |

| | | | | | | | |

| | | | Total Consumer Discretionary | | | 7,680 | |

| | | | | | | | |

| | | | Consumer Staples — 2.1% | | | | |

| | | | Food & Staples Retailing — 0.6% | | | | |

| | 1 | | | CVS Health Corp. | | | 123 | |

| | 3 | | | Sysco Corp. | | | 126 | |

| | 2 | | | Wal-Mart Stores, Inc. | | | 122 | |

| | 37 | | | Whole Foods Market, Inc. | | | 1,077 | |

| | | | | | | | |

| | | | | | | 1,448 | |

| | | | | | | | |

| | | | Food Products — 0.2% | | | | |

| | 2 | | | Campbell Soup Co. | | | 128 | |

| | 2 | | | General Mills, Inc. | | | 127 | |

| | 2 | | | Kraft Heinz Co. (The) | | | 126 | |

| | | | | | | | |

| | | | | | | 381 | |

| | | | | | | | |

| | | | Household Products — 1.3% | | | | |

| | 22 | | | Clorox Co. (The) | | | 2,755 | |

| | 2 | | | Colgate-Palmolive Co. | | | 128 | |

| | | | | | | | |

| | | | | | | 2,883 | |

| | | | | | | | |

| | | | Total Consumer Staples | | | 4,712 | |

| | | | | | | | |

| | | | | | | | |

| SHARES | | | SECURITY DESCRIPTION | | VALUE($) | |

| | | | | | | | |

| | | | | | | | |

| | | | Energy — 0.2% | | | | |

| | | | Energy Equipment & Services — 0.0% (g) | | | | |

| | 1 | | | FMC Technologies, Inc. (a) | | | 45 | |

| | — | (h) | | Helmerich & Payne, Inc. | | | 23 | |

| | | | | | | | |

| | | | | | | 68 | |

| | | | | | | | |

| | | | Oil, Gas & Consumable Fuels — 0.2% | | | | |

| | 1 | | | Apache Corp. | | | 42 | |

| | — | (h) | | Cimarex Energy Co. | | | 43 | |

| | 1 | | | Devon Energy Corp. | | | 43 | |

| | 1 | | | Enbridge, Inc., (Canada) | | | 41 | |

| | — | (h) | | Exxon Mobil Corp. | | | 43 | |

| | 1 | | | ONEOK, Inc. | | | 44 | |

| | — | (h) | | Phillips 66 | | | 39 | |

| | 3 | | | QEP Resources, Inc. | | | 49 | |

| | 1 | | | Range Resources Corp. | | | 31 | |

| | 1 | | | Spectra Energy Corp. | | | 43 | |

| | 5 | | | WPX Energy, Inc. (a) | | | 49 | |

| | | | | | | | |

| | | | | | | 467 | |

| | | | | | | | |

| | | | Total Energy | | | 535 | |

| | | | | | | | |

| | | | Financials — 1.9% | | | | |

| | | | Banks — 0.2% | | | | |

| | 5 | | | Associated Banc-Corp. | | | 83 | |

| | 4 | | | Fifth Third Bancorp | | | 81 | |

| | 6 | | | First Horizon National Corp. | | | 81 | |

| | 5 | | | People’s United Financial, Inc. | | | 80 | |

| | 2 | | | U.S. Bancorp | | | 82 | |

| | | | | | | | |

| | | | | | | 407 | |

| | | | | | | | |

| | | | Capital Markets — 0.3% | | | | |

| | 1 | | | T. Rowe Price Group, Inc. | | | 80 | |

| | 34 | | | Waddell & Reed Financial, Inc., Class A | | | 683 | |

| | | | | | | | |

| | | | | | | 763 | |

| | | | | | | | |

| | | | Consumer Finance — 0.5% | | | | |

| | 18 | | | American Express Co. | | | 1,197 | |

| | | | | | | | |

| | | | Diversified Financial Services — 0.1% | | | | |

| | 1 | | | CME Group, Inc. | | | 81 | |

| | 1 | | | Nasdaq, Inc. | | | 80 | |

| | | | | | | | |

| | | | | | | 161 | |

| | | | | | | | |

| | | | Insurance — 0.2% | | | | |

| | 1 | | | Aflac, Inc. | | | 84 | |

| | 1 | | | Aon plc, (United Kingdom) | | | 84 | |

| | 1 | | | Arch Capital Group Ltd., (Bermuda) (a) | | | 84 | |

| | 3 | | | Progressive Corp. (The) | | | 82 | |

| | 1 | | | Torchmark Corp. | | | 85 | |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | | | |

| | | |

| APRIL 30, 2016 | | J.P. MORGAN SPECIALTY FUNDS | | | | | 15 | |

JPMorgan Opportunistic Equity Long/Short Fund

SCHEDULE OF PORTFOLIO INVESTMENTS

AS OF APRIL 30, 2016 (Unaudited) (continued)

(Amounts in thousands)

| | | | | | | | |

| SHARES | | | SECURITY DESCRIPTION | | VALUE($) | |

| Short Positions — continued | |

| Common Stocks — continued | |

| | | | Insurance — continued | | | | |

| | 1 | | | W.R. Berkley Corp. | | | 83 | |

| | | | | | | | |

| | | | | | | 502 | |

| | | | | | | | |

| | | | Real Estate Investment Trusts (REITs) — 0.6% | |

| | 1 | | | Digital Realty Trust, Inc. | | | 84 | |

| | 8 | | | Extra Space Storage, Inc. | | | 667 | |

| | 1 | | | Federal Realty Investment Trust | | | 84 | |

| | 3 | | | Healthcare Realty Trust, Inc. | | | 85 | |

| | 3 | | | Healthcare Trust of America, Inc., Class A | | | 85 | |

| | 2 | | | UDR, Inc. | | | 81 | |

| | 1 | | | Ventas, Inc. | | | 85 | |

| | 1 | | | Welltower, Inc. | | | 86 | |

| | | | | | | | |

| | | | | | | 1,257 | |

| | | | | | | | |

| | | | Total Financials | | | 4,287 | |

| | | | | | | | |

| | | | Health Care — 0.5% | | | | |

| | | | Biotechnology — 0.1% | | | | |

| | 1 | | | Amgen, Inc. | | | 161 | |

| | | | | | | | |

| | | | Health Care Equipment & Supplies — 0.3% | |

| | 4 | | | Baxter International, Inc. | | | 171 | |

| | 1 | | | C.R. Bard, Inc. | | | 171 | |

| | 2 | | | Medtronic plc, (Ireland) | | | 168 | |

| | 2 | | | Varian Medical Systems, Inc. (a) | | | 159 | |

| | | | | | | | |

| | | | | | | 669 | |

| | | | | | | | |

| | | | Health Care Providers & Services — 0.0% (g) | |

| | 2 | | | Cardinal Health, Inc. | | | 151 | |

| | | | | | | | |

| | | | Pharmaceuticals — 0.1% | | | | |

| | 3 | | | Merck & Co., Inc. | | | 161 | |

| | | | | | | | |

| | | | Total Health Care | | | 1,142 | |

| | | | | | | | |

| | | | Industrials — 3.4% | | | | |

| | | | Air Freight & Logistics — 1.1% | | | | |

| | 48 | | | Expeditors International of Washington, Inc. | | | 2,369 | |

| | | | | | | | |

| | | | Electrical Equipment — 0.0% (g) | | | | |

| | — | (h) | | Acuity Brands, Inc. | | | 119 | |

| | | | | | | | |

| | | | Industrial Conglomerates — 2.0% | | | | |

| | 149 | | | General Electric Co. | | | 4,583 | |

| | | | | | | | |

| | | | Machinery — 0.2% | | | | |

| | 2 | | | AGCO Corp. | | | 127 | |

| | 2 | | | Deere & Co. | | | 126 | |

| | 4 | | | Donaldson Co., Inc. | | | 125 | |

| | 1 | | | Illinois Tool Works, Inc. | | | 124 | |

| | | | | | | | |

| | | | | | | 502 | |

| | | | | | | | |

| | | | | | | | |

| SHARES | | | SECURITY DESCRIPTION | | VALUE($) | |

| | | | | | | | |

| | | | | | | | |

| | | | Trading Companies & Distributors — 0.1% | | | | |

| | 4 | | | Air Lease Corp. | | | 119 | |

| | | | | | | | |

| | | | Total Industrials | | | 7,692 | |

| | | | | | | | |

| | | | Information Technology — 1.4% | | | | |

| | | | Communications Equipment — 0.7% | | | | |

| | 57 | | | Cisco Systems, Inc. | | | 1,567 | |

| | 5 | | | Juniper Networks, Inc. | | | 126 | |

| | | | | | | | |

| | | | | | | 1,693 | |

| | | | | | | | |

| | | | Electronic Equipment, Instruments & Components — 0.1% | |

| | 2 | | | Amphenol Corp., Class A | | | 124 | |

| | 4 | | | VeriFone Systems, Inc. (a) | | | 123 | |

| | | | | | | | |

| | | | | | | 247 | |

| | | | | | | | |

| | | | IT Services — 0.1% | | | | |

| | 1 | | | FleetCor Technologies, Inc. (a) | | | 127 | |

| | | | | | | | |

| | | | Semiconductors & Semiconductor Equipment — 0.3% | |

| | 3 | | | Linear Technology Corp. | | | 122 | |

| | 3 | | | Maxim Integrated Products, Inc. | | | 123 | |

| | 3 | | | Microchip Technology, Inc. | | | 124 | |

| | 5 | | | Taiwan Semiconductor Manufacturing Co., Ltd., (Taiwan), ADR | | | 119 | |

| | 3 | | | Xilinx, Inc. | | | 118 | |

| | | | | | | | |

| | | | | | | 606 | |

| | | | | | | | |

| | | | Software — 0.1% | | | | |

| | 2 | | | Citrix Systems, Inc. (a) | | | 124 | |

| | 2 | | | salesforce.com, Inc. (a) | | | 124 | |

| | | | | | | | |

| | | | | | | 248 | |

| | | | | | | | |

| | | | Technology Hardware, Storage & Peripherals — 0.1% | |

| | 5 | | | NetApp, Inc. | | | 124 | |

| | | | | | | | |

| | | | Total Information Technology | | | 3,045 | |

| | | | | | | | |

| | | | Materials — 0.2% | | | | |

| | | | Chemicals — 0.1% | | | | |

| | — | (h) | | Agrium, Inc., (Canada) | | | 40 | |

| | — | (h) | | Air Products & Chemicals, Inc. | | | 40 | |

| | 1 | | | Westlake Chemical Corp. | | | 39 | |

| | | | | | | | |

| | | | | | | 119 | |

| | | | | | | | |

| | | | Containers & Packaging — 0.1% | | | | |

| | 1 | | | AptarGroup, Inc. | | | 39 | |

| | 1 | | | Ball Corp. | | | 38 | |

| | 1 | | | Bemis Co., Inc. | | | 39 | |

| | 1 | | | Sonoco Products Co. | | | 40 | |

| | | | | | | | |

| | | | | | | 156 | |

| | | | | | | | |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | |

| | | |

| 16 | | | | J.P. MORGAN SPECIALTY FUNDS | | APRIL 30, 2016 |

| | | | | | | | |

| SHARES | | | SECURITY DESCRIPTION | | VALUE($) | |

| Short Positions — continued | |

| Common Stocks — continued | |

| | | | Metals & Mining — 0.0% (g) | | | | |

| | 4 | | | Alcoa, Inc. | | | 43 | |

| | | | | | | | |

| | | | Total Materials | | | 318 | |

| | | | | | | | |

| | | | Telecommunication Services — 0.1% | | | | |

| | | | Diversified Telecommunication Services — 0.1% | |

| | 4 | | | CenturyLink, Inc. | | | 121 | |

| | 2 | | | Verizon Communications, Inc. | | | 124 | |

| | | | | | | | |

| | | | Total Telecommunication Services | | | 245 | |

| | | | | | | | |

| | | | Utilities — 0.1% | | | | |

| | | | Electric Utilities — 0.0% (g) | | | | |

| | 1 | | | Duke Energy Corp. | | | 43 | |

| | 1 | | | Southern Co. (The) | | | 43 | |

| | | | | | | | |

| | | | | | | 86 | |

| | | | | | | | |

| | | | Multi-Utilities — 0.1% | | | | |

| | 1 | | | Consolidated Edison, Inc. | | | 44 | |

| | 1 | | | Dominion Resources, Inc. | | | 44 | |

| | | | | | | | |

| SHARES | | | SECURITY DESCRIPTION | | VALUE($) | |

| | | | | | | | |

| | | | | | | | |

| | | | Multi-Utilities — continued | | | | |

| | — | (h) | | DTE Energy Co. | | | 44 | |

| | | | | | | | |

| | | | | | | 132 | |

| | | | | | | | |

| | | | Total Utilities | | | 218 | |

| | | | | | | | |

| | | | Total Common Stocks

(Cost $(30,376)) | | | 29,874 | |

| | | | | | | | |

| Exchange Traded Funds — 3.4% | |

| | | | U.S. Equity — 3.4% | | | | |

| | 29 | | | iShares Russell 2000 ETF | | | 3,226 | |

| | 22 | | | SPDR S&P 500 ETF Trust | | | 4,467 | |

| | | | | | | | |

| | | | Total Exchange Traded Funds

(Cost $(7,469)) | | | 7,693 | |

| | | | | | | | |

| | | | Total Securities Sold Short

(Proceeds $37,845) | | $ | 37,567 | |

| | | | | | | | |

Percentages indicated are based on net assets.

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | | | |

| | | |

| APRIL 30, 2016 | | J.P. MORGAN SPECIALTY FUNDS | | | | | 17 | |

JPMorgan Research Equity Long/Short Fund

SCHEDULE OF PORTFOLIO INVESTMENTS

AS OF APRIL 30, 2016 (Unaudited)

(Amounts in thousands)

| | | | | | | | |

| SHARES | | | SECURITY DESCRIPTION | | VALUE($) | |

| Long Positions — 104.8% | |

| Common Stocks — 104.8% | |

| | | | Consumer Discretionary — 18.2% | | | | |

| | | | Auto Components — 0.3% | | | | |

| | 2 | | | Delphi Automotive plc, (United Kingdom) (j) | | | 132 | |

| | | | | | | | |

| | | | Hotels, Restaurants & Leisure — 4.1% | | | | |

| | 7 | | | Carnival Corp. (j) | | | 340 | |

| | — | (h) | | Chipotle Mexican Grill, Inc. (a) (j) | | | 135 | |

| | 10 | | | Hilton Worldwide Holdings, Inc. (j) | | | 217 | |

| | 1 | | | Norwegian Cruise Line Holdings Ltd. (a) (j) | | | 44 | |

| | 7 | | | Royal Caribbean Cruises Ltd. (j) | | | 513 | |

| | 2 | | | Starbucks Corp. (j) | | | 133 | |

| | 5 | | | Yum! Brands, Inc. (j) | | | 416 | |

| | | | | | | | |

| | | | | | | 1,798 | |

| | | | | | | | |

| | | | Household Durables — 1.4% | | | | |

| | 14 | | | D.R. Horton, Inc. (j) | | | 421 | |

| | 1 | | | Harman International Industries, Inc. (j) | | | 53 | |

| | 5 | | | KB Home (j) | | | 64 | |

| | 3 | | | PulteGroup, Inc. (j) | | | 55 | |

| | | | | | | | |

| | | | | | | 593 | |

| | | | | | | | |

| | | | Internet & Catalog Retail — 2.2% | | | | |

| | 1 | | | Amazon.com, Inc. (a) (j) | | | 955 | |

| | | | | | | | |

| | | | Media — 4.8% | | | | |

| | 4 | | | CBS Corp. (Non-Voting), Class B (j) | | | 232 | |

| | 1 | | | Charter Communications, Inc., Class A (a) (j) | | | 270 | |

| | 5 | | | DISH Network Corp., Class A (a) (j) | | | 257 | |

| | 29 | | | Sirius XM Holdings, Inc. (a) (j) | | | 113 | |

| | — | (h) | | Time Warner Cable, Inc. (j) | | | 94 | |

| | 3 | | | Time Warner, Inc. (j) | | | 217 | |

| | 30 | | | Twenty-First Century Fox, Inc., Class B (j) | | | 899 | |

| | | | | | | | |

| | | | | | | 2,082 | |

| | | | | | | | |

| | | | Specialty Retail — 5.4% | | | | |

| | 6 | | | Best Buy Co., Inc. (j) | | | 201 | |

| | 2 | | | Home Depot, Inc. (The) (j) | | | 324 | |

| | 20 | | | Lowe’s Cos., Inc. (j) | | | 1,538 | |

| | 1 | | | O’Reilly Automotive, Inc. (a) (j) | | | 300 | |

| | | | | | | | |

| | | | | | | 2,363 | |

| | | | | | | | |

| | | | Total Consumer Discretionary | | | 7,923 | |

| | | | | | | | |

| | | | Consumer Staples — 7.6% | | | | |

| | | | Beverages — 4.1% | | | | |

| | — | (h) | | Boston Beer Co., Inc. (The), Class A (a) (j) | | | 64 | |

| | 1 | | | Constellation Brands, Inc., Class A (j) | | | 100 | |

| | 11 | | | Molson Coors Brewing Co., Class B (j) | | | 1,008 | |

| | 6 | | | PepsiCo, Inc. (j) | | | 598 | |

| | | | | | | | |

| | | | | | | 1,770 | |

| | | | | | | | |

| | | | | | | | |

| SHARES | | | SECURITY DESCRIPTION | | VALUE($) | |

| | | | | | | | |

| | | | | | | | |

| | | | Food & Staples Retailing — 0.8% | | | | |

| | 1 | | | Costco Wholesale Corp. (j) | | | 163 | |

| | 6 | | | Kroger Co. (The) (j) | | | 199 | |

| | | | | | | | |

| | | | | | | 362 | |

| | | | | | | | |

| | | | Food Products — 1.1% | | | | |

| | 3 | | | ConAgra Foods, Inc. (j) | | | 140 | |

| | 1 | | | Hershey Co. (The) (j) | | | 89 | |

| | 3 | | | Mondelez International, Inc., Class A (j) | | | 128 | |

| | 2 | | | Post Holdings, Inc. (a) (j) | | | 136 | |

| | | | | | | | |

| | | | | | | 493 | �� |

| | | | | | | | |

| | | | Household Products — 0.7% | | | | |

| | 2 | | | Kimberly-Clark Corp. (j) | | | 279 | |

| | | | | | | | |

| | | | Personal Products — 0.2% | | | | |

| | 1 | | | Estee Lauder Cos., Inc. (The), Class A (j) | | | 103 | |

| | | | | | | | |

| | | | Tobacco — 0.7% | | | | |

| | 3 | | | Philip Morris International, Inc. (j) | | | 304 | |

| | | | | | | | |

| | | | Total Consumer Staples | | | 3,311 | |

| | | | | | | | |

| | | | Energy — 4.1% | | | | |

| | | | Energy Equipment & Services — 0.3% | | | | |

| | 3 | | | Halliburton Co. (j) | | | 142 | |

| | | | | | | | |

| | | | Oil, Gas & Consumable Fuels — 3.8% | | | | |

| | 6 | | | Cabot Oil & Gas Corp. (j) | | | 135 | |

| | 8 | | | Diamondback Energy, Inc. (j) | | | 711 | |

| | 2 | | | EOG Resources, Inc. (j) | | | 159 | |

| | 3 | | | Pioneer Natural Resources Co. (j) | | | 466 | |

| | 2 | | | TransCanada Corp., (Canada) (j) | | | 76 | |

| | 2 | | | Valero Energy Corp. (j) | | | 97 | |

| | | | | | | | |

| | | | | | | 1,644 | |

| | | | | | | | |

| | | | Total Energy | | | 1,786 | |

| | | | | | | | |

| | | | Financials — 16.4% | | | | |

| | | | Banks — 3.9% | | | | |

| | 37 | | | Bank of America Corp. (j) | | | 538 | |

| | 6 | | | Citigroup, Inc. (j) | | | 272 | |

| | 23 | | | KeyCorp (j) | | | 280 | |

| | 2 | | | Popular, Inc., (Puerto Rico) (j) | | | 73 | |

| | 13 | | | Regions Financial Corp. (j) | | | 121 | |

| | 4 | | | Wells Fargo & Co. (j) | | | 213 | |

| | 6 | | | Zions Bancorporation (j) | | | 173 | |

| | | | | | | | |

| | | | | | | 1,670 | |

| | | | | | | | |

| | | | Capital Markets — 3.3% | | | | |

| | 4 | | | Ameriprise Financial, Inc. (j) | | | 339 | |

| | 3 | | | Bank of New York Mellon Corp. (The) (j) | | | 132 | |

| | 1 | | | BlackRock, Inc. (j) | | | 272 | |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | |

| | | |

| 18 | | | | J.P. MORGAN SPECIALTY FUNDS | | APRIL 30, 2016 |

| | | | | | | | |

| SHARES | | | SECURITY DESCRIPTION | | VALUE($) | |

| Long Positions — continued | |

| Common Stocks — continued | |

| | | | Capital Markets — continued | | | | |

| | 14 | | | Charles Schwab Corp. (The) (j) | | | 398 | |

| | 8 | | | Morgan Stanley (j) | | | 228 | |

| | 2 | | | TD Ameritrade Holding Corp. (j) | | | 61 | |

| | | | | | | | |

| | | | | | | 1,430 | |

| | | | | | | | |

| | | | Consumer Finance — 0.6% | | | | |

| | 2 | | | American Express Co. (j) | | | 103 | |

| | 1 | | | Capital One Financial Corp. (j) | | | 51 | |

| | 2 | | | Discover Financial Services (j) | | | 114 | |

| | | | | | | | |