| | OMB APPROVAL |

| | OMB Number: | 3235-0570 |

| | Expires: | January 31, 2017 |

| UNITED STATES | Estimated average burden hours per response. . . . . . . . . . . . . . . . .20.6 |

| SECURITIES AND EXCHANGE COMMISSION | |

| Washington, D.C. 20549 | |

| | | | |

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-21308 |

|

Alger Global Growth Fund |

(Exact name of registrant as specified in charter) |

|

360 Park Avenue South New York, New York | | 10010 |

(Address of principal executive offices) | | (Zip code) |

|

Mr. Hal Liebes Fred Alger Management, Inc. 360 Park Avenue South New York, New York 10010 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | 212-806-8800 | |

|

Date of fiscal year end: | October 31 | |

|

Date of reporting period: | April 30, 2014 | |

| | | | | | | | |

ITEM 1. REPORT(S) TO STOCKHOLDERS.

Alger Global Growth Fund

SEMI-ANNUAL REPORT | |

April 30, 2014 | |

(Unaudited) | |

Table of Contents

ALGER GLOBAL GROWTH FUND

Shareholders’ Letter | 1 |

| |

Fund Highlights | 8 |

| |

Portfolio Summary | 11 |

| |

Schedule of Investments | 12 |

| |

Statement of Assets and Liabilities | 20 |

| |

Statement of Operations | 22 |

| |

Statement of Changes in Net Assets | 23 |

| |

Financial Highlights | 24 |

| |

Notes to Financial Statements | 28 |

| |

Additional Information | 39 |

Go Paperless With Alger Electronic Delivery Service

Alger is pleased to provide you with the ability to access regulatory materials online. When documents such as prospectuses and annual and semi-annual reports are available, we’ll send you an e-mail notification with a convenient link that will take you directly to the fund information on our website. To sign up for this free service, simply enroll at www.icsdelivery.com/alger.

Shareholders’ Letter | | May 20, 2014 |

Dear Shareholders,

Volatility Persists as Economy Shows Signs of Growing

Equity markets in the United States and abroad produced considerable volatility during the six-month period ended April 30. In the U.S., investors assessed if economic growth in 2014 would support market levels that were driven by multiple expansion during 2013 while severe winter weather threw a cold blanket on consumer spending and real estate. Investors also struggled with uncertainty over the timing of future Federal Reserve actions to reduce fiscal stimulus. Looking abroad, Russia’s annexation of Crimea and moderating economic growth in China also supported market volatility. Yet, a combination of encouraging U.S. economic indicators, such as a strengthening labor market, supported investor sentiment. During the six-month period, the S&P 500 Index climbed 8.36% and hit a record high of 1890.90, while the MSCI ACWI ex USA Index generated a 3.12% return. Emerging market equities as measured by the MSCI Emerging Markets Index trailed both of those indexes with a -2.87% return.

Growth Scare Rattles Stocks

Perhaps the most dramatic event during the reporting period was what we call a “growth scare” that occurred in the first four months of 2014. During growth scares, investors become fearful of high-growth stocks and either liquidate their equity positions or flock to defensive stocks such as consumer names like Wal-Mart Stores, Inc. and “old” technology names such as Microsoft Corp. or International Business Machines Corp. Investors may also favor certain pharmaceutical companies. During the recent growth scare, for example, defensive stocks Wal-Mart and Johnson & Johnson generated gains. At the same time, the NYSE Arca Biotechnology Index, which consists of high-growth biotech companies, and the PowerShares Nasdaq Internet Portfolio exchange traded fund, which consists of high-growth Internet companies, each declined more than 19%. At their peaks, the Arca Biotechnology Index and the Nasdaq Internet Portfolio had forward 12-month price to earnings (P/E) ratios of 27.4 and 33 respectively. Those P/Es declined to 20.6 and 27.8 as of the end of the reporting period.

We maintain that investors who were fearful of high-growth stocks during the first four months of this year overlooked the ability of such growth companies to rapidly expand their earnings and revenues. An overview of cloud computing, one of the most important growth trends within technology, illustrates this concept. Businesses have traditionally housed databases, servers, and other technology equipment in their own facilities. In doing so, companies have been saddled with the costs of storing their technology equipment as well as the costs of committing managerial and employee time to maintaining IT facility performance; those resources generally would be better spent focused on customers, product development, marketing, and other functions that are drivers of business. With cloud computing, vendors assume the responsibility of storing and maintaining technology that customers access remotely via the Internet. By embracing cloud computing, businesses eliminate many of the costs associated with traditional on-premises technology. That can result in cutting technology costs by 30-40%. Cloud computing, therefore, has been growing rapidly as businesses seek to contain technology costs. We estimate that cloud computing technologies now capture 3.5% of the approximately $260 billion that is spent on enterprise technology annually. By 2025, we estimate that enterprise spending will total $350 billion and that providers of cloud

1

computing technology and services will capture 46% of that amount. In the process, they will take market share from traditional providers of on-premises technology.

As a result, we believe that traditional on-premises technology companies are likely to see their revenues and earnings decline as they lose market share to cloud vendors. The technology industry is at a tipping point where the growth and size of cloud computing is increasingly having a negative impact on the ability of traditional on-premises vendors to grow their businesses and profit margins. Thus, while many traditional vendors trade at low P/E multiples, we are cautious on the group as a whole and think that many of the companies are not attractive investments. Conversely, cloud vendors are likely to see their earnings grow quickly, and we believe that some—in particular those that become the new leaders of this wave of technology innovation—will be superior investments as their growth in revenues and profits over the coming years “validates” their higher valuations.

The trend of new products or technology cannibalizing older products isn’t unique to cloud computing. For example, online stores are rapidly capturing market share from traditional vendors, streaming video is replacing DVDs, online media and search are replacing magazine and newspaper advertising, and leading biotechnology companies are producing new drugs that are displacing older treatments. This is the kind of dynamic change within industries that Alger’s investment philosophy and process has, since our founding 50 years ago, perceived as opportunity for investors.

Growth scares are quite common. In fact, in recent years, we’ve seen similar market collapses in confidence or sentiment. In each case, the scares have been temporary, and as investor confidence in the strength of the U.S. economy and in corporate fundamentals returned, so did investors’ focus on companies with the strongest potential future revenue growth and fundamental business opportunities. We believe that this explains why stocks of high-growth companies have outperformed the broad market and low-growth companies in the six- and nine-month periods following the growth scares of 2012 and 2013 (See table below).

High-Growth Companies Have Outperformed the S&P 500 Index and Other Companies in the Months Following Growth Scares.

| | Growth Scare of 2012 | | Growth Scare of 2013 | |

| | Performance

(%) | | 6 Month

Performance

Following

Growth Scare

(%) | | 9 Month

Performance

Following

Growth Scare

(%) | | Performance

(%) | | 6 Month

Performance

Following

Growth Scare

(%) | | 9 Month

Performance

Following

Growth Scare

(%) | |

S&P 500 (SPX) | | -9 | | 10 | | 18 | | -4 | | 15 | | 18 | |

High-Growth Companies | | | | | | | | | | | | | |

Cloud | | -12 | | 17 | | 37 | | 3 | | 27 | | 39 | |

Biotech | | 1 | | 31 | | 61 | | -10 | | 37 | | 46 | |

Tech Growth | | -25 | | 5 | | 35 | | -15 | | 44 | | 70 | |

Consumer | | -10 | | 5 | | 16 | | -5 | | 28 | | 41 | |

Slow-Growth Companies | | | | | | | | | | | | | |

Old Tech | | -11 | | 3 | | 6 | | -6 | | 11 | | 14 | |

Consumer | | -2 | | 8 | | 11 | | -3 | | 7 | | 7 | |

Pharmaceuticals | | -4 | | 13 | | 21 | | -6 | | 7 | | 12 | |

Source: Thomson Reuters FactSet(1)

(1) To compile data in the table, we looked at the largest market declines in each of the last two years. We defined scares as the time period ranging from the start of a market decline to a market bottom. The 2012 Growth Scare occurred from May 1 to June 5. The 2013 Growth Scare occurred from May 22 to June 25.

2

Fed Watchers Drive Market Volatility

Uncertainty over the Federal Reserve’s timing for reining in stimulus also supported market volatility. Generally speaking, many investors expect the Federal Reserve to unwind its bond purchasing, or quantitative easing, later this year and to raise the federal funds rate next year. When encouraging economic data surfaced during the reporting period, however, some investors grew fearful that the central bank would rein in fiscal stimulus sooner than anticipated. Throughout the reporting period, we remained unconcerned about the potential for the Federal Reserve to speed up its pace for unwinding stimulus. Market interest rates remain lower or unchanged from levels of June of 2012 and we believe the economy still has room to grow, even though it has made considerable progress. Major economic indicators like jobs and inflation are not near levels of past cyclical peaks, and U.S. economic growth is stronger than in many other parts of the world.

Ukraine Becomes Geopolitical Hotspot

Geopolitics also drove market volatility when Russia annexed the Crimea region of the Ukraine in mid-March. The act provoked strong criticism from the U.S. and the European Union, both of which gradually increased sanctions targeting Russia while western banks cut their credit lines to the country. Conditions continued to worsen in April, with pro-Russia separatists seizing control of a regional government headquarters in Luhansk in eastern Ukraine and escalating protests. As the crisis dragged on, most analysts downgraded their already modest economic growth forecasts for Russia, while foreign investors withdrew their assets from the country. Russia’s ruble weakened, causing the country’s central bank to raise interest rates 150 basis points. Russia and the Ukraine are limited trading partners with the U.S. They account for only $13 billion in annual exports and $27.9 billion in imports, which limits our country’s ability to exert pressure through economic sanctions. Europe, however, is more closely linked to the two countries, so it has more leverage with imposing sanctions. One possible long-term benefit to the U.S. of the crisis is that Europe, which receives over 30% of its gas from Russia, may turn to the U.S. for energy commodities, which could help support our country’s already robust resurgence in the energy sector.

China Growth Moderates

The rapid growth of China’s economy in recent years has been viewed as a major driver of global economic expansion. The country’s gross domestic product (GDP) grew at a higher-than-expected rate of 7.7% in 2013, yet data in the first quarter portrayed an economy that was weakening into 2014. China’s National People’s Congress in March, furthermore, lowered the country’s official growth target for 2014 to 7.5%. The Chinese government also devalued the renminbi from 6.05 to 6.22 to the U.S. dollar, and concerns over excess manufacturing capacity and news of defaults or near-defaults in the country’s shadow banking system focused investors’ attention on a potential economic slowdown. We maintain that China’s targeted GDP growth for this year is still impressive, especially when considering that the U.S. economy grew at an annualized rate of only 2.6% during the fourth quarter of 2013. The moderation of economic expansion in China also has a silver lining. In the past, the country’s economic growth has fueled massive demand and higher prices for commodities and other resources. A slower Chinese economy, however, may reduce inflationary pressures in many important areas which, in turn, would be supportive of U.S. businesses and consumers.

Reasons for Optimism

Alger believes that issues such as Russia and the Ukraine will continue to drive market volatility that will create attractive buying opportunities for equity investors. We also maintain that the economy is stronger than commonly believed. During the reporting

3

period, unemployment dropped from 7.0% to 6.3% and the number of private-sector employees reached a record high of 116.4 million, according to Cornerstone Macro LP. The last record high of 116 million employees was set in January 2008. At the same time, total employment during April reached 138.3 million, just slightly below the January of 2008 record high of 138.4 million, and strengthening budgets for many states and municipalities suggest that public employers may increase hiring. Improvements in the job market and strong stock market gains during the past few years, meanwhile, pushed the Conference Board’s March Consumer Sentiment Index to a six-year high of 83.9. While it declined slightly in April, it is still at a high level of 82.3.

Another force is also supporting the U.S. economy—a rapidly growing energy industry that is benefiting from new technology, such as hydraulic fracturing, which is making additional reserves of oil and natural gas economically feasible for extraction and is reversing a long trend of declining production of energy commodities. From 1970 to 2008, U.S. oil production declined from 9.6 million barrels a day to only 5 million—a level not experienced since 1949. Since 2008, however, it has rapidly increased, reaching 7.4 million barrels a day as of last year. Natural gas production is also surging, climbing from 49,454 BCF (billion cubic feet) per day in 2005 to 66,768 BCF in 2013. We estimate that with growing energy production, domestic resources are on track to meet 96% of the country’s energy demand by 2020.

The surge in energy production is doing more than just creating jobs: it’s lowering energy costs for U.S. businesses, which is helping to drive a manufacturing renaissance. Just recently, the Boston Consulting Group, citing low energy costs and a lack of upward pressure on labor wages, ranked the U.S. as the second-most competitive country for manufacturing, trailing only China. Certain manufacturers, moreover, are moving their operations from China to the U.S. For example, the Keer Group, which operates a yarn spinning factory in China, plans to build a $218 million factory in North Carolina that will employ 500 workers. Its electric costs will be half of what it pays in China, according to Cornerstone Macro. The strength of manufacturing in the U.S. should not be underestimated—according to the Institute for Supply Management, economic activity in the manufacturing sector expanded in April for the eleventh consecutive month.

We are also encouraged to see the eurozone appear to be strengthening after having weathered a massive sovereign debt crisis. Markit’s eurozone Manufacturing Purchasing Managers’ Index for April rose to 53.4, up from 53 in March. It was the tenth month the index has been above the 50 level that separates growth from contraction. Manufacturing expanded in all eight of the countries tallied by the index. Granted, eurozone economies are not growing quickly, but they have clearly improved.

Across the Pacific, Japan’s economy is struggling with a recent consumption tax hike, but the Bank of Japan is continuing with its aggressive quantitative easing. The Japanese economy is only about one third the size of the U.S., but its quantitative easing program allows the Bank of Japan to spend approximately $68 million each month to buy bonds, real estate investment trusts, and exchange traded funds. In comparison, the U.S. program at its peak was $85 billion a month. The Japanese program is likely to devalue the yen, which would support the country’s exporting levels.

Going Forward

We believe the recent growth scare has created an attractive opportunity for fundamental, research-driven investors to buy equities. Our analysts and portfolio managers are working hard within our proven research-driven investment strategy to identify

4

companies that are best positioned to grow and lead their industries while delivering superior investment returns to their shareholders.

Portfolio Matters

The Alger Global Growth Fund returned 4.10% for the six-month period ended April 30, 2014, compared to the 5.54% return of the MSCI ACWI Index.

During the period, the largest sector weightings were Information Technology and Consumer Discretionary. The largest sector overweight was Information Technology and the largest sector underweight was Energy. Relative outperformance in the Industrials and Materials sectors was the most important contributor to performance, while Information Technology and Financials detracted from results.

Ireland, Mexico, China, and Brazil were among countries that provided the largest contribution to performance while Canada, Japan, Taiwan, France, Italy, and the United Kingdom were among countries that detracted from results.

Among the most important relative contributors were Facebook, Inc.; Actavis PLC; Delta Air Lines, Inc.; Blackstone Group LP; and Jones Lang LaSalle, Inc. We believe investors’ anticipation of increased advertising revenues from mobile users of Facebook supported the performance of the social network operator’s stock. As of the fourth quarter of 2013, 74% of Facebook users connected to the site with mobile devices but only accounted for 53% of the company’s advertising revenues, suggesting that revenue from mobile advertising can potentially increase.

Conversely, detracting from overall results on a relative basis were NCR Corp.; Prada SpA.; ASML Holding NV; and Great Wall Motor Co., Ltd. Also detracting from results was Doosan Heavy Industries and Construction Co., Ltd., which is an infrastructure engineering and construction company. Performance of Doosan Heavy shares was impacted by news that Korea’s National Energy Commission would reduce the role of nuclear energy within the country, even though the proposal wasn’t new and was in line with the country’s sixth electricity plan that was previously announced.

As always, we strive to deliver consistently superior investment results to you, our shareholders, and we thank you for your continued confidence in Alger.

Sincerely,

Daniel C. Chung, CFA

Chief Investment Officer

Fred Alger Management, Inc.

Investors cannot invest directly in an index. Index performance does not reflect the deduction for fees, expenses, or taxes.

This report and the financial statements contained herein are submitted for the general information of shareholders of the Fund. This report is not authorized for distribution to prospective investors in the Fund unless proceeded or accompanied by an effective prospectus for the Fund. Fund performance returns represent the fiscal six-month period return of Class A shares prior to the deduction of any sales charges and include the reinvestment of any dividends or distributions.

5

The performance data quoted represents past performance, which is not an indication or guarantee of future results.

Standardized performance results can be found on the following pages. The investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted. For performance data current to the most recent month-end, visit us at www.alger.com or call us at (800) 992-3863.

The views and opinions of the Fund’s management in this report are as of the date of the Shareholders’ Letter and are subject to change at any time subsequent to this date. There is no guarantee that any of the assumptions that formed the basis for the opinions stated herein are accurate or that they will materialize. Moreover, the information forming the basis for such assumptions is from sources believed to be reliable; however, there is no guarantee that such information is accurate. Any securities mentioned, whether owned in a fund or otherwise, are considered in the context of the construction of an overall portfolio of securities and therefore reference to them should not be construed as a recommendation or offer to purchase or sell any such security. Inclusion of such securities in a fund and transactions in such securities, if any, may be for a variety of reasons, including without limitation, in response to cash flows, inclusion in a benchmark, and risk control. The reference to a specific security should also be understood in such context and not viewed as a statement that the security is a significant holding in the Fund. Please refer to the Schedule of Investments for the Fund which is included in this report for a complete list of Fund holdings as of April 30, 2014. Securities mentioned in the Shareholders’ Letter, if not found in the Schedule of Investments, may have been held by the Fund during the fiscal period.

A Word about Risk

Growth stocks tend to be more volatile than other stocks as the price of growth stocks tends to be higher in relation to their companies’ earnings and may be more sensitive to market, political and economic developments. Investing in the stock market involves gains and losses and may not be suitable for all investors. Stocks of small- and mid-sized companies are subject to greater risk than stocks of larger, more established companies owing to such factors as limited liquidity, inexperienced management, and limited financial resources. Investing in foreign securities involves additional risk (including currency risk, risks related to political, social or economic conditions, and risks associated with foreign markets, such as increased volatility, limited liquidity, less stringent regulatory and legal system, and lack of industry and country diversification), and may not be suitable for all investors. Special risks associated with investments in emerging country issuers include exposure to currency fluctuations, less liquidity, less developed or less efficient trading markets, lack of comprehensive company information, political instability and different auditing and legal standards.

Foreign currencies are subject to risks caused by inflation, interest rates, budget deficits and low savings rates, political factors and government controls. Some of the countries where the Fund can invest may have restrictions that could limit the access to investment opportunities. The securities of issuers located in emerging markets can be more volatile and less liquid than those of issuers in more mature economies. Investing in emerging markets involves higher levels of risk, including increased information, market, and valuation risks, and may not be suitable for all investors.

6

Funds that participate in leveraging are subject to the risk that borrowing money to leverage will exceed the returns for securities purchased or that the securities purchased may actually go down in value; thus, the Fund’s net asset value can decrease more quickly than if the Fund had not borrowed.

For a more detailed discussion of the risks associated with the Fund, please see the prospectus.

Before investing, carefully consider the Fund’s investment objective, risks, charges, and expenses.

For a prospectus or a summary prospectus containing this and other information about the Alger Global Growth Fund call us at (800) 992-3863 or visit us at www.alger.com. Read it carefully before investing.

Fred Alger & Company, Incorporated, Distributor. Member NYSE Euronext, SIPC.

NOT FDIC INSURED. NOT BANK GUARANTEED. MAY LOSE VALUE.

Definitions:

· The S&P 500 Index is an unmanaged index generally representative of the U.S. stock market without regard to company size.

· The MSCI ACWI ex USA Index is a market capitalization-weighted index designed to provide a broad measure of equity market performance throughout the world, including both developed and emerging markets, but excluding the United States.

· The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance in the global emerging markets.

· The Conference Board’s Consumer Sentiment Index measures consumers’ near term outlook on the economy.

· The Boston Consulting Group is a global management consulting firm.

· Cornerstone Macro is an economic research firm.

· Markit is a global, diversified provider of financial information.

· The Institute for Supply Management is a not-for-profit organization that provides education and research on issues regarding the supply of resources that organizations need to attain their objectives.

· The MSCI ACWI Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed and emerging markets.

7

FUND PERFORMANCE AS OF 3/31/14 (Unaudited)

AVERAGE ANNUAL TOTAL RETURNS

| | 1 YEAR | | 5 YEARS | | SINCE

INCEPTION | |

Alger Global Growth Class A (Inception 11/3/03) | | 14.43 | % | 14.77 | % | 9.76 | % |

Alger Global Growth Class C (Inception 3/3/08)* | | 18.86 | % | 15.20 | % | 9.55 | % |

Alger Global Growth Class I (Inception 5/31/13) | | n/a | | n/a | | 18.12 | % |

Alger Global Growth Class Z (Inception 5/31/13) | | n/a | | n/a | | 18.36 | % |

The performance data quoted represents past performance, which is not an indication or a guarantee of future results. The Fund’s average annual total returns include changes in share price and reinvestment of dividends and capital gains. Class A returns reflect the maximum initial sales charge and Class C returns reflect the applicable contingent deferred sales charge. Beginning May 31, 2013 Alger Global Growth Fund changed its investment strategy to emphasize foreign (including emerging markets) securities and the United States, its previous investment strategy considered securities economically tied to China (including Hong Kong and Taiwan) and the United States.

* | Performance figures prior to 3/03/08, inception of Class C shares, are those of the Fund’s Class A Shares. Performance has been adjusted to remove the front-end sales charge imposed by Class A shares. Class C shares do not impose a front-end sales charge but do impose a contingent deferred sales charge of 1% on shares redeemed. If Class A sales charges were reflected, annual returns for the Class C shares would be lower. The performance figures prior to 3/03/08 have been reduced to reflect the higher operating expenses and applicable contingent deferred sales charge of Class C shares. |

8

ALGER GLOBAL GROWTH FUND

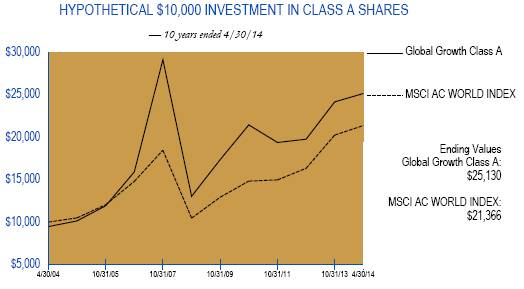

Fund Highlights Through April 30, 2014 (Unaudited)

The chart above illustrates the growth in value of a hypothetical $10,000 investment made in the Alger Global Growth Fund Class A shares, with an initial maximum sales charge of 5.25%, and the MSCI AC WORLD Index (unmanaged index of common stocks) from November 3, 2003, the inception date of the Alger Global Growth Fund Class A shares, through April 30, 2014. Beginning May 31, 2013 Alger Global Growth Fund changed its investment strategy to emphasize foreign (including emerging markets) securities and the United States, its previous investment strategy considered securities economically tied to China (including Hong Kong and Taiwan) and the United States. The figures for the Alger Global Growth Fund Class A shares, and the MSCI AC WORLD Index include reinvestment of dividends. Performance for the Alger Global Growth Fund Class C, Class I and Class Z shares will vary from the results shown above due to differences in expenses and sales charges that class bears. Investors cannot invest directly in any index. Index performance does not reflect deduction for fees, expenses, or taxes.

PERFORMANCE COMPARISON AS OF 4/30/14

AVERAGE ANNUAL TOTAL RETURNS

| | 1 YEAR | | 5 YEARS | | 10 YEARS | | Since

11/3/2003 | |

Class A (Inception 11/3/03) | | 11.28 | % | 11.80 | % | 9.65 | % | 9.52 | % |

Class C (Inception 3/3/08)* | | 15.59 | % | 12.20 | % | 9.47 | % | 9.31 | % |

MSCI AC WORLD INDEX | | 14.98 | % | 16.03 | % | 7.89 | % | 8.31 | % |

| | 1 YEAR | | 5 YEARS | | 10 YEARS | | Since

5/31/2013 | |

Class I (Inception 5/31/13) | | n/a | | n/a | | n/a | | 16.34 | % |

Class Z (Inception 5/31/13) | | n/a | | n/a | | n/a | | 16.64 | % |

MSCI AC WORLD INDEX | | n/a | | n/a | | n/a | | 15.20 | % |

9

The performance data quoted represents past performance, which is not an indication or a guarantee of future results. The Fund’s average annual total returns include changes in share price and reinvestment of dividends and capital gains. Class A returns reflect the maximum initial sales charge and Class C returns reflect the applicable contingent deferred sales charge. The chart and table above do not reflect the deduction of taxes that a shareholder would have paid on Fund distributions or on the redemption of Fund shares. Investment return and principal will fluctuate and the Fund’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted. For updated performance, visit us at www.alger.com or call us at (800) 992-3863.

* | Performance figures prior to 3/03/08, inception of Class C shares, are those of the Fund’s Class A Shares. Performance has been adjusted to remove the front-end sales charge imposed by Class A shares. Class C shares do not impose a front-end sales charge but do impose a contingent deferred sales charge of 1% on shares redeemed. If Class A sales charges were reflected, annual returns for the Class C shares would be lower. The performance figures prior to 3/03/08 have been reduced to reflect the higher operating expenses and applicable contingent deferred sales charge of Class C shares. |

10

PORTFOLIO SUMMARY†

April 30, 2014 (Unaudited)

COUNTRY | | Alger Global Growth

Fund | |

Belgium | | 1.5 | % |

Brazil | | 0.8 | |

Canada | | 1.5 | |

China | | 2.0 | |

Colombia | | 0.7 | |

France | | 1.2 | |

Germany | | 2.6 | |

Hong Kong | | 1.7 | |

India | | 0.7 | |

Indonesia | | 0.6 | |

Ireland | | 1.6 | |

Israel | | 0.5 | |

Italy | | 0.9 | |

Japan | | 4.3 | |

Mexico | | 1.5 | |

Netherlands | | 1.7 | |

Peru | | 0.9 | |

Philippines | | 0.8 | |

Singapore | | 0.8 | |

South Africa | | 0.6 | |

South Korea | | 1.7 | |

Spain | | 0.4 | |

Sweden | | 0.6 | |

Switzerland | | 4.1 | |

Taiwan | | 0.8 | |

United Kingdom | | 2.9 | |

United States | | 58.2 | |

Cash and Net Other Assets | | 4.4 | |

| | 100.0 | % |

† Based on net assets of the Fund.

11

ALGER GLOBAL GROWTH FUND

Schedule of Investments‡ April 30, 2014 (Unaudited)

| | SHARES | | VALUE | |

COMMON STOCKS—93.3% | | | | | |

BELGIUM—1.5% | | | | | |

BREWERS—1.5% | | | | | |

Anheuser-Busch InBev NV

(Cost $521,632) | | 5,371 | | $ | 584,450 | |

| | | | | |

BRAZIL—0.8% | | | | | |

MULTI-LINE INSURANCE—0.8% | | | | | |

BB Seguridade Participacoes SA

(Cost $254,875) | | 27,700 | | 324,647 | |

| | | | | |

CANADA—1.5% | | | | | |

FERTILIZERS & AGRICULTURAL CHEMICALS—0.5% | | | | | |

Potash Corporation of Saskatchewan, Inc. | | 5,500 | | 198,850 | |

| | | | | |

LEISURE PRODUCTS—1.0% | | | | | |

BRP, Inc.*(a) | | 14,914 | | 401,481 | |

| | | | | |

TOTAL CANADA

(Cost $555,290) | | | | 600,331 | |

| | | | | |

CHINA—2.0% | | | | | |

AUTOMOBILE MANUFACTURERS—0.8% | | | | | |

Great Wall Motor Co., Ltd. | | 73,229 | | 331,058 | |

| | | | | |

INTERNET SOFTWARE & SERVICES—1.2% | | | | | |

Tencent Holdings Ltd. | | 7,297 | | 454,971 | |

| | | | | |

TOTAL CHINA

(Cost $296,486) | | | | 786,029 | |

| | | | | |

COLOMBIA—0.7% | | | | | |

CONSTRUCTION MATERIALS—0.7% | | | | | |

Cementos Argos SA

(Cost $220,562) | | 50,810 | | 278,113 | |

| | | | | |

FRANCE—1.2% | | | | | |

HEALTH CARE EQUIPMENT—0.2% | | | | | |

DBV Technologies SA* | | 3,825 | | 78,957 | |

| | | | | |

PHARMACEUTICALS—1.0% | | | | | |

Sanofi | | 3,660 | | 396,134 | |

| | | | | |

TOTAL FRANCE

(Cost $487,066) | | | | 475,091 | |

| | | | | |

GERMANY—2.6% | | | | | |

APPLICATION SOFTWARE—1.5% | | | | | |

SAP AG# | | 7,400 | | 599,326 | |

| | | | | |

AUTOMOBILE MANUFACTURERS—1.1% | | | | | |

Bayerische Motoren Werke AG | | 3,328 | | 416,340 | |

| | | | | |

TOTAL GERMANY

(Cost $797,939) | | | | 1,015,666 | |

| | | | | |

HONG KONG—1.7% | | | | | |

CASINOS & GAMING—0.7% | | | | | |

Galaxy Entertainment Group Ltd.* | | 32,343 | | 254,057 | |

| | | | | | |

12

| | SHARES | | VALUE | |

COMMON STOCKS—(CONT.) | | | | | |

HONG KONG—(CONT.) | | | | | |

CONSTRUCTION & ENGINEERING—1.0% | | | | | |

China State Construction International Holdings Ltd. | | 227,534 | | $ | 378,590 | |

| | | | | |

TOTAL HONG KONG

(Cost $497,073) | | | | 632,647 | |

| | | | | |

INDIA—0.7% | | | | | |

CONSTRUCTION & FARM MACHINERY & HEAVY TRUCKS—0.7% | | | | | |

Tata Motors Ltd.#

(Cost $205,696) | | 7,752 | | 290,080 | |

| | | | | |

INDONESIA—0.6% | | | | | |

DEPARTMENT STORES—0.6% | | | | | |

Matahari Department Store Tbk PT*

(Cost $231,773) | | 177,946 | | 230,869 | |

| | | | | |

IRELAND—1.6% | | | | | |

INDUSTRIAL MACHINERY—0.9% | | | | | |

Ingersoll-Rand PLC. | | 5,631 | | 336,734 | |

| | | | | |

PHARMACEUTICALS—0.7% | | | | | |

Jazz Pharmaceuticals PLC.* | | 2,145 | | 289,361 | |

| | | | | |

TOTAL IRELAND

(Cost $571,931) | | | | 626,095 | |

| | | | | |

ISRAEL—0.5% | | | | | |

TECHNOLOGY HARDWARE STORAGE & PERIPHERALS—0.5% | | | | | |

Stratasys Ltd.*

(Cost $226,771) | | 2,000 | | 193,740 | |

| | | | | |

ITALY—0.9% | | | | | |

APPAREL RETAIL—0.9% | | | | | |

Prada SpA

(Cost $308,366) | | 44,746 | | 357,255 | |

| | | | | |

JAPAN—4.3% | | | | | |

AUTOMOBILE MANUFACTURERS—1.0% | | | | | |

Toyota Motor Corp. | | 7,004 | | 377,932 | |

| | | | | |

DIVERSIFIED BANKS—0.8% | | | | | |

Sumitomo Mitsui Financial Group, Inc. | | 7,934 | | 313,014 | |

| | | | | |

DIVERSIFIED REAL ESTATE ACTIVITIES—0.8% | | | | | |

Mitsui Fudosan Co., Ltd. | | 11,000 | | 325,077 | |

| | | | | |

ELECTRONIC COMPONENTS—0.9% | | | | | |

Murata Manufacturing Co., Ltd. | | 4,151 | | 345,155 | |

| | | | | |

PROPERTY & CASUALTY INSURANCE—0.8% | | | | | |

Tokio Marine Holdings, Inc. | | 10,837 | | 319,200 | |

| | | | | |

TOTAL JAPAN

(Cost $1,817,448) | | | | 1,680,378 | |

| | | | | | |

13

| | SHARES | | VALUE | |

COMMON STOCKS—(CONT.) | | | | | |

MEXICO—1.5% | | | | | |

DIVERSIFIED REAL ESTATE ACTIVITIES—0.7% | | | | | |

Corp Inmobiliaria Vesta SAB de CV | | 139,400 | | $ | 283,406 | |

| | | | | |

INDUSTRIAL CONGLOMERATES—0.8% | | | | | |

Alfa SAB de CV | | 112,700 | | 297,689 | |

| | | | | |

TOTAL MEXICO

(Cost $519,518) | | | | 581,095 | |

| | | | | |

NETHERLANDS—1.7% | | | | | |

SEMICONDUCTOR EQUIPMENT—1.0% | | | | | |

ASML Holding NV# | | 4,873 | | 396,613 | |

| | | | | |

SEMICONDUCTORS—0.7% | | | | | |

NXP Semiconductor NV* | | 4,850 | | 289,157 | |

| | | | | |

TOTAL NETHERLANDS

(Cost $493,782) | | | | 685,770 | |

| | | | | |

PERU—0.9% | | | | | |

DIVERSIFIED BANKS—0.9% | | | | | |

Credicorp Ltd.

(Cost $298,591) | | 2,298 | | 342,977 | |

| | | | | |

PHILIPPINES—0.8% | | | | | |

DIVERSIFIED BANKS—0.8% | | | | | |

BDO Unibank, Inc.

(Cost $345,996) | | 163,980 | | 324,649 | |

| | | | | |

SINGAPORE—0.8% | | | | | |

SEMICONDUCTORS—0.8% | | | | | |

Avago Technologies Ltd.

(Cost $244,500) | | 4,650 | | 295,275 | |

| | | | | |

SOUTH AFRICA—0.6% | | | | | |

PHARMACEUTICALS—0.6% | | | | | |

Aspen Pharmacare Holdings Ltd.

(Cost $217,592) | | 8,356 | | 222,358 | |

| | | | | |

SOUTH KOREA—1.7% | | | | | |

BUILDING PRODUCTS—0.6% | | | | | |

LG Hausys Ltd. | | 1,339 | | 235,890 | |

| | | | | |

SEMICONDUCTORS—1.1% | | | | | |

Samsung Electronics Co., Ltd. | | 314 | | 408,191 | |

| | | | | |

TOTAL SOUTH KOREA

(Cost $611,453) | | | | 644,081 | |

| | | | | |

SPAIN—0.4% | | | | | |

APPAREL RETAIL—0.4% | | | | | |

Inditex SA

(Cost $91,749) | | 950 | | 142,529 | |

| | | | | | |

14

| | SHARES | | VALUE | |

COMMON STOCKS—(CONT.) | | | | | |

SWEDEN—0.6% | | | | | |

BIOTECHNOLOGY—0.6% | | | | | |

Swedish Orphan Biovitrum AB*

(Cost $197,670) | | 20,500 | | $ | 225,081 | |

| | | | | |

SWITZERLAND—4.1% | | | | | |

APPAREL ACCESSORIES & LUXURY GOODS—1.2% | | | | | |

Cie Financiere Richemont SA | | 4,484 | | 454,895 | |

| | | | | |

OIL & GAS EQUIPMENT & SERVICES—0.7% | | | | | |

Weatherford International Ltd.* | | 13,000 | | 273,000 | |

| | | | | |

PHARMACEUTICALS—0.9% | | | | | |

Roche Holding AG | | 1,165 | | 341,460 | |

| | | | | |

SECURITY & ALARM SERVICES—1.3% | | | | | |

Tyco International Ltd. | | 12,453 | | 509,328 | |

| | | | | |

TOTAL SWITZERLAND

(Cost $1,312,663) | | | | 1,578,683 | |

| | | | | |

TAIWAN—0.8% | | | | | |

PERSONAL PRODUCTS—0.4% | | | | | |

Ginko International Co., Ltd. | | 9,000 | | 151,266 | |

| | | | | |

SEMICONDUCTORS—0.4% | | | | | |

Epistar Corp. | | 79,000 | | 172,584 | |

| | | | | |

TOTAL TAIWAN

(Cost $393,894) | | | | 323,850 | |

| | | | | |

UNITED KINGDOM—2.9% | | | | | |

DIVERSIFIED BANKS—0.2% | | | | | |

Lloyds Banking Group PLC.* | | 74,000 | | 94,150 | |

| | | | | |

HOUSEHOLD PRODUCTS—1.1% | | | | | |

Reckitt Benckiser Group PLC. | | 5,589 | | 450,565 | |

| | | | | |

INSURANCE BROKERS—0.5% | | | | | |

Aon PLC. | | 2,400 | | 203,712 | |

| | | | | |

TOBACCO—1.1% | | | | | |

British American Tobacco PLC. | | 7,384 | | 425,977 | |

| | | | | |

TOTAL UNITED KINGDOM

(Cost $1,118,008) | | | | 1,174,404 | |

| | | | | |

UNITED STATES—55.9% | | | | | |

ADVERTISING—0.0% | | | | | |

Choicestream, Inc.*(L3) | | 1,969 | | 1,575 | |

| | | | | |

AEROSPACE & DEFENSE—2.0% | | | | | |

Honeywell International, Inc. | | 5,000 | | 464,500 | |

Precision Castparts Corp. | | 1,300 | | 329,017 | |

| | | | 793,517 | |

AIRLINES—1.5% | | | | | |

Delta Air Lines, Inc. | | 16,250 | | 598,487 | |

| | | | | | |

15

| | SHARES | | VALUE | |

COMMON STOCKS—(CONT.) | | | | | |

UNITED STATES—(CONT.) | | | | | |

APPLICATION SOFTWARE—0.6% | | | | | |

Workday, Inc.* | | 3,150 | | $ | 230,170 | |

| | | | | |

AUTO PARTS & EQUIPMENT—3.1% | | | | | |

BorgWarner, Inc. | | 8,200 | | 509,548 | |

Johnson Controls, Inc. | | 9,400 | | 424,316 | |

WABCO Holdings, Inc.* | | 2,750 | | 294,277 | |

| | | | 1,228,141 | |

BIOTECHNOLOGY—3.6% | | | | | |

Biogen Idec, Inc.* | | 1,350 | | 387,612 | |

Gilead Sciences, Inc.* | | 8,300 | | 651,467 | |

Pharmacyclics, Inc.* | | 4,000 | | 378,320 | |

| | | | 1,417,399 | |

BROADCASTING—0.6% | | | | | |

CBS Corp., Cl. B | | 4,350 | | 251,256 | |

| | | | | |

BUILDING PRODUCTS—0.9% | | | | | |

Fortune Brands Home & Security, Inc. | | 9,000 | | 358,650 | |

| | | | | |

CABLE & SATELLITE—1.2% | | | | | |

Comcast Corporation, Cl. A | | 8,900 | | 460,664 | |

| | | | | |

CASINOS & GAMING—1.0% | | | | | |

Las Vegas Sands Corp. | | 5,000 | | 395,650 | |

| | | | | |

CONSTRUCTION & FARM MACHINERY & HEAVY TRUCKS—1.3% | | | | | |

Cummins, Inc. | | 3,350 | | 505,347 | |

| | | | | |

CONSUMER FINANCE—1.4% | | | | | |

American Express Co. | | 3,800 | | 332,234 | |

Discover Financial Services | | 4,100 | | 229,190 | |

| | | | 561,424 | |

DATA PROCESSING & OUTSOURCED SERVICES—0.6% | | | | | |

MasterCard, Inc., Cl. A | | 3,000 | | 220,650 | |

| | | | | |

DIVERSIFIED BANKS—1.0% | | | | | |

JPMorgan Chase & Co. | | 7,000 | | 391,860 | |

| | | | | |

DIVERSIFIED CHEMICALS—0.8% | | | | | |

The Dow Chemical Co. | | 6,500 | | 324,350 | |

| | | | | |

DRUG RETAIL—1.2% | | | | | |

CVS Caremark Corp. | | 3,400 | | 247,248 | |

Walgreen Co. | | 3,150 | | 213,885 | |

| | | | 461,133 | |

ELECTRONIC EQUIPMENT MANUFACTURERS—0.4% | | | | | |

Control4 Corp.* | | 10,000 | | 176,600 | |

| | | | | |

FOOTWEAR—1.5% | | | | | |

NIKE, Inc., Cl. B | | 8,350 | | 609,132 | |

| | | | | |

HEALTH CARE FACILITIES—1.8% | | | | | |

HCA Holdings, Inc.* | | 8,800 | | 457,600 | |

| | | | | | |

16

| | SHARES | | VALUE | |

COMMON STOCKS—(CONT.) | | | | | |

UNITED STATES—(CONT.) | | | | | |

HEALTH CARE FACILITIES—(CONT.) | | | | | |

Tenet Healthcare Corporation* | | 5,800 | | $ | 261,464 | |

| | | | 719,064 | |

HOME IMPROVEMENT RETAIL—0.8% | | | | | |

The Home Depot, Inc. | | 4,050 | | 322,015 | |

| | | | | |

HOMEBUILDING—0.9% | | | | | |

Lennar Corp., Cl. A | | 8,700 | | 335,733 | |

| | | | | |

INTERNET RETAIL—0.4% | | | | | |

Amazon.com, Inc.* | | 500 | | 152,065 | |

| | | | | |

INTERNET SOFTWARE & SERVICES—2.7% | | | | | |

Facebook, Inc.* | | 7,500 | | 448,350 | |

Google, Inc., Cl. A* | | 600 | | 320,928 | |

Google, Inc., Cl. C* | | 600 | | 315,996 | |

| | | | 1,085,274 | |

INVESTMENT BANKING & BROKERAGE—1.1% | | | | | |

Morgan Stanley | | 14,600 | | 451,578 | |

| | | | | |

LIFE & HEALTH INSURANCE—2.0% | | | | | |

Lincoln National Corp. | | 10,000 | | 485,100 | |

Prudential Financial, Inc. | | 3,800 | | 306,584 | |

| | | | 791,684 | |

MANAGED HEALTH CARE—1.3% | | | | | |

Aetna, Inc. | | 7,000 | | 500,150 | |

| | | | | |

MOVIES & ENTERTAINMENT—0.5% | | | | | |

Twenty-First Century Fox, Inc. | | 5,800 | | 185,716 | |

| | | | | |

OIL & GAS EQUIPMENT & SERVICES—1.8% | | | | | |

Halliburton Company | | 6,200 | | 391,034 | |

National Oilwell Varco, Inc. | | 4,000 | | 314,120 | |

| | | | 705,154 | |

OIL & GAS EXPLORATION & PRODUCTION—6.2% | | | | | |

Anadarko Petroleum Corp. | | 7,000 | | 693,140 | |

Cabot Oil & Gas Corp. | | 6,300 | | 247,464 | |

ConocoPhillips | | 8,350 | | 620,488 | |

Pioneer Natural Resources Co. | | 2,050 | | 396,204 | |

Whiting Petroleum Corp.* | | 6,350 | | 468,122 | |

| | | | 2,425,418 | |

OTHER DIVERSIFIED FINANCIAL SERVICES—0.5% | | | | | |

Citigroup, Inc. | | 4,000 | | 191,640 | |

| | | | | |

PHARMACEUTICALS—2.4% | | | | | |

Actavis PLC.* | | 4,550 | | 929,701 | |

| | | | | |

REAL ESTATE SERVICES—0.8% | | | | | |

Jones Lang LaSalle, Inc. | | 2,700 | | 312,903 | |

| | | | | |

REGIONAL BANKS—1.0% | | | | | |

Regions Financial Corp. | | 39,900 | | 404,586 | |

| | | | | | |

17

| | SHARES | | VALUE | |

COMMON STOCKS—(CONT.) | | | | | |

UNITED STATES—(CONT.) | | | | | |

RESTAURANTS—0.3% | | | | | |

Yum! Brands, Inc. | | 1,550 | | $ | 119,335 | |

| | | | | |

SOFT DRINKS—1.6% | | | | | |

PepsiCo, Inc. | | 7,100 | | 609,819 | |

| | | | | |

SPECIALTY CHEMICALS—2.7% | | | | | |

Rockwood Holdings, Inc. | | 10,500 | | 746,025 | |

The Sherwin-Williams Co. | | 1,500 | | 299,760 | |

| | | | 1,045,785 | |

TECHNOLOGY HARDWARE STORAGE & PERIPHERALS—4.4% | | | | | |

Apple, Inc. | | 1,600 | | 944,144 | |

NCR Corp.* | | 12,600 | | 384,426 | |

Western Digital Corp. | | 4,500 | | 396,585 | |

| | | | 1,725,155 | |

TOTAL UNITED STATES

(Cost $18,118,926) | | | | 21,998,780 | |

| | | | | |

TOTAL COMMON STOCKS

(Cost $30,957,250) | | | | 36,614,923 | |

| | | | | |

PREFERRED STOCKS—0.2% | | | | | |

UNITED STATES—0.2% | | | | | |

ADVERTISING—0.1% | | | | | |

Choicestream, Inc.*(L3) | | 16,980 | | 13,584 | |

| | | | | |

PHARMACEUTICALS—0.1% | | | | | |

Intarcia Therapeutics, Inc.*(L2) | | 1,728 | | 55,970 | |

| | | | | |

TOTAL UNITED STATES

(Cost $69,549) | | | | 69,554 | |

| | | | | |

TOTAL PREFERRED STOCKS

(Cost $69,549) | | | | 69,554 | |

| | | | | |

MASTER LIMITED PARTNERSHIP—2.1% | | | | | |

UNITED STATES—2.1% | | | | | |

ASSET MANAGEMENT & CUSTODY BANKS—2.1% | | | | | |

Blackstone Group LP.

(Cost $604,394) | | 27,550 | | 813,552 | |

| | | | | |

Total Investments

(Cost $31,631,193)(b) | | 95.6 | % | 37,498,029 | |

Other Assets in Excess of Liabilities | | 4.4 | % | 1,739,443 | |

NET ASSETS | | 100.0 | % | $ | 39,237,472 | |

18

‡ | Securities classified as Level 1 for ASC 820 disclosure purposes based on valuation inputs unless otherwise noted. |

* | Non-income producing security. |

(a) | Pursuant to Securities and Exchange Commission Rule 144A, these securities may be sold prior to their maturity only to qualified institutional buyers. These securities are deemed to be liquid and represent 1.0% of the net assets of the Portfolio. |

# | American Depositary Receipts. |

(L3) | Security classified as Level 3 for ASC 820 disclosure purposes based on valuation inputs. |

(L2) | Security classified as Level 2 for ASC 820 disclosure purposes based on valuation inputs. |

(b) | At April 30, 2014, the net unrealized appreciation on investments, based on cost for federal income tax purposes of $31,618,621, amounted to $5,879,408 which consisted of aggregate gross unrealized appreciation of $6,420,182 and aggregate gross unrealized depreciation of $540,774. |

See Notes to Financial Statements.

19

ALGER GLOBAL GROWTH FUND

Statement of Assets and Liabilities April 30, 2014 (Unaudited)

| | Alger Global Growth

Fund | |

ASSETS: | | | |

Investments in securities, at value (Identified cost below)*

see accompanying schedules of investments | | $ | 37,498,029 | |

Cash and cash equivalents | | 1,097,250 | |

Foreign cash † | | 42,848 | |

Receivable for investment securities sold | | 1,236,372 | |

Receivable for shares of beneficial interest sold | | 68,561 | |

Dividends and interest receivable | | 67,502 | |

Receivable from Investment Manager | | 8,113 | |

Prepaid expenses | | 42,753 | |

Total Assets | | 40,061,428 | |

| | | |

LIABILITIES: | | | |

Payable for investment securities purchased | | 678,386 | |

Payable for shares of beneficial interest redeemed | | 10,643 | |

Accrued investment advisory fees | | 25,922 | |

Accrued transfer agent fees | | 22,633 | |

Accrued distribution fees | | 11,182 | |

Accrued administrative fees | | 891 | |

Accrued shareholder administrative fees | | 526 | |

Accrued other expenses | | 73,773 | |

Total Liabilities | | 823,956 | |

NET ASSETS | | $ | 39,237,472 | |

| | | | |

NET ASSETS CONSIST OF: | | | |

Paid in capital (par value of $.001 per share) | | 42,876,448 | |

Undistributed net investment income | | 638,906 | |

Undistributed net realized gain (accumulated realized loss) | | (10,145,091 | ) |

Net unrealized appreciation on investments | | 5,867,209 | |

NET ASSETS | | $ | 39,237,472 | |

* Identified cost | | $ | 31,631,193 | |

† Cost of foreign cash | | $ | 42,601 | |

See Notes to Financial Statements.

20

| | Alger Global Growth

Fund | |

NET ASSETS BY CLASS: | | | |

Class A | | $ | 32,533,342 | |

Class C | | $ | 5,114,755 | |

Class I | | $ | 1,472,138 | |

Class Z | | $ | 117,237 | |

| | | | |

SHARES OF BENEFICIAL INTEREST OUTSTANDING — NOTE 6: | | | |

Class A | | 1,665,597 | |

Class C | | 271,652 | |

Class I | | 75,185 | |

Class Z | | 5,973 | |

| | | |

NET ASSET VALUE PER SHARE: | | | |

Class A — Net Asset Value Per Share | | $ | 19.53 | |

Class A — Offering Price Per Share

(includes a 5.25% sales charge) | | $ | 20.61 | |

Class C — Net Asset Value Per Share | | $ | 18.83 | |

Class I — Net Asset Value Per Share | | $ | 19.58 | |

Class Z — Net Asset Value Per Share | | $ | 19.63 | |

See Notes to Financial Statements.

21

ALGER GLOBAL GROWTH FUND

Statement of Operations for the six months ended April 30, 2014

(Unaudited)

| | Alger Global Growth

Fund | |

INCOME: | | | |

Dividends (net of foreign withholding taxes*) | | $ | 272,447 | |

Interest | | 695 | |

Total Income | | 273,142 | |

| | | |

EXPENSES: | | | |

Advisory fees — Note 3(a) | | 158,876 | |

Distribution fees — Note 3(c) | | | |

Class A | | 41,523 | |

Class C | | 24,908 | |

Class I | | 1,755 | |

Shareholder administrative fees — Note 3(f) | | 3,227 | |

Administration fees — Note 3(b) | | 5,461 | |

Custodian fees | | 24,878 | |

Transfer agent fees and expenses — Note 3(f) | | 31,754 | |

Printing fees | | 16,894 | |

Professional fees | | 61,393 | |

Registration fees | | 32,462 | |

Trustee fees — Note 3(g) | | 12,179 | |

Fund accounting fees | | 4,603 | |

Miscellaneous | | 14,011 | |

Total Expenses | | 433,924 | |

Less, expense reimbursements/waivers — Note 3(a) | | (119,221 | ) |

Net Expenses | | 314,703 | |

NET INVESTMENT LOSS | | (41,561 | ) |

| | | |

REALIZED AND UNREALIZED GAIN (LOSS) ON INVESTMENTS, OPTIONS AND FOREIGN CURRENCY: | | | |

Net realized gain on investments and purchased options | | 3,924,091 | |

Net realized (loss) on foreign currency transactions | | (3,911 | ) |

Net change in unrealized (depreciation) on investments, options and foreign currency | | (2,272,916 | ) |

Net realized and unrealized gain on investments, options, and foreign currency | | 1,647,264 | |

NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | | $ | 1,605,703 | |

* Foreign withholding taxes | | $ | 7,794 | |

See Notes to Financial Statements.

22

ALGER GLOBAL GROWTH FUND

Statements of Changes in Net Assets (Unaudited)

| | Alger Global Growth Fund | |

| | For the

Six Months Ended

April 30, 2014 | | For the

Year Ended

October 31, 2013 | |

Net investment loss | | $ | (41,561 | ) | $ | (58,548 | ) |

Net realized gain on investments, options and foreign currency | | 3,920,180 | | 7,567,251 | |

Net change in unrealized appreciation (depreciation) on investments, options and foreign currency | | (2,272,916 | ) | 755,165 | |

Net increase in net assets resulting from operations | | 1,605,703 | | 8,263,868 | |

| | | | | |

Dividends and distributions to shareholders from: | | | | | |

Net investment income: | | | | | |

Class A | | — | | (155,913 | ) |

Total dividends and distributions to shareholders | | — | | (155,913 | ) |

| | | | | |

Increase (decrease) from shares of beneficial interest transactions: | | | | | |

Class A | | (2,487,099 | ) | (14,538,080 | ) |

Class C | | 45,329 | | (5,833 | ) |

Class I | | 119,439 | | 1,190,057 | |

Class Z | | 636 | | 100,000 | |

Net decrease from shares of beneficial interest transactions — Note 6(a) | | (2,321,695 | ) | (13,253,856 | ) |

| | | | | |

Redemption Fees: | | | | | |

Class A | | 15 | | 59 | |

Class C | | — | | 115 | |

Total Redemption Fees — Note 6(b) | | 15 | | 174 | |

Total decrease | | (715,977 | ) | (5,145,727 | ) |

| | | | | |

Net Assets: | | | | | |

Beginning of period | | 39,953,449 | | 45,099,176 | |

END OF PERIOD | | $ | 39,237,472 | | $ | 39,953,449 | |

Undistributed net investment income (accumulated loss) | | $ | 638,906 | | $ | (8,903 | ) |

See Notes to Financial Statements.

23

ALGER GLOBAL GROWTH FUND

Financial Highlights for a share outstanding throughout the period (Unaudited)

Alger Global Growth Fund

| | Class A | |

| | Six months

ended

4/30/2014(i) | | Year ended

10/31/2013 | | Year ended

10/31/2012 | | Year ended

10/31/2011 | | Year ended

10/31/2010 | | Year ended

10/31/2009 | |

Net asset value, beginning of period | | $ | 18.76 | | $ | 15.42 | | $ | 15.11 | | $ | 16.74 | | $ | 13.55 | | $ | 10.18 | |

INCOME FROM INVESTMENT OPERATIONS: | | | | | | | | | | | | | |

Net investment loss(ii) | | (0.01 | ) | (0.01 | ) | (0.06 | ) | (0.08 | ) | (0.08 | ) | (0.05 | ) |

Net realized and unrealized gain (loss) on investments | | 0.78 | | 3.41 | | 0.37 | | (1.55 | ) | 3.29 | | 3.42 | |

Total from investment operations | | 0.77 | | 3.40 | | 0.31 | | (1.63 | ) | 3.21 | | 3.37 | |

Dividends from net investment income | | — | | (0.06 | ) | — | | — | | (0.02 | ) | — | |

Net asset value, end of period | | $ | 19.53 | | $ | 18.76 | | $ | 15.42 | | $ | 15.11 | | $ | 16.74 | | $ | 13.55 | |

Total return(iii) | | 4.10 | % | 22.20 | % | 2.00 | % | (9.60 | )% | 23.50 | % | 33.10 | % |

RATIOS/SUPPLEMENTAL DATA: | | | | | | | | | | | | | |

Net assets, end of period (000’s omitted) | | $ | 32,533 | | $ | 33,657 | | $ | 41,051 | | $ | 53,311 | | $ | 71,835 | | $ | 67,989 | |

Ratio of gross expenses to average net assets | | 2.07 | % | 2.35 | % | 2.29 | % | 2.15 | % | 2.12 | % | 2.31 | % |

Ratio of expense reimbursements to average net assets | | (0.57 | )% | (0.33 | )% | — | | — | | — | | — | |

Ratio of net expenses to average net assets | | 1.50 | % | 2.02 | % | 2.29 | % | 2.15 | % | 2.12 | % | 2.31 | % |

Ratio of net investment income (loss) to average net assets | | (0.13 | )% | (0.07 | )% | (0.38 | )% | (0.49 | )% | (0.56 | )% | (0.48 | )% |

Portfolio turnover rate | | 37.58 | % | 96.45 | % | 84.55 | % | 82.13 | % | 89.15 | % | 149.17 | % |

See Notes to Financial Statements.

(i) Ratios have been annualized; total return and portfolio turnover rate have not been annualized.

(ii) Amount was computed based on average shares outstanding during the period.

(iii) Does not reflect the effect of sales charges, if applicable.

24

| | Class C | |

| | Six months

ended

4/30/2014(i) | | Year ended

10/31/2013 | | Year ended

10/31/2012 | | Year ended

10/31/2011 | | Year ended

10/31/2010 | | Year ended

10/31/2009 | |

Net asset value, beginning of period | | $ | 18.15 | | $ | 14.97 | | $ | 14.79 | | $ | 16.50 | | $ | 13.43 | | $ | 10.16 | |

INCOME FROM INVESTMENT OPERATIONS: | | | | | | | | | | | | | |

Net investment loss(ii) | | (0.08 | ) | (0.13 | ) | (0.16 | ) | (0.21 | ) | (0.18 | ) | (0.14 | ) |

Net realized and unrealized gain (loss) on investments | | 0.76 | | 3.31 | | 0.34 | | (1.50 | ) | 3.25 | | 3.41 | |

Total from investment operations | | 0.68 | | 3.18 | | 0.18 | | (1.71 | ) | 3.07 | | 3.27 | |

Net asset value, end of period | | $ | 18.83 | | $ | 18.15 | | $ | 14.97 | | $ | 14.79 | | $ | 16.50 | | $ | 13.43 | |

Total return(iii) | | 3.75 | % | 21.24 | % | 1.20 | % | (10.30 | )% | 22.70 | % | 32.20 | % |

RATIOS/SUPPLEMENTAL DATA: | | | | | | | | | | | | | |

Net assets, end of period (000’s omitted) | | $ | 5,115 | | $ | 4,888 | | $ | 4,048 | | $ | 3,678 | | $ | 4,208 | | $ | 1,595 | |

Ratio of gross expenses to average net assets | | 2.87 | % | 3.13 | % | 3.06 | % | 2.95 | % | 2.91 | % | 3.03 | % |

Ratio of expense reimbursements to average net assets | | (0.62 | )% | (0.40 | )% | — | | — | | — | | — | |

Ratio of net expenses to average net assets | | 2.25 | % | 2.73 | % | 3.06 | % | 2.95 | % | 2.91 | % | 3.03 | % |

Ratio of net investment income (loss) to average net assets | | (0.87 | )% | (0.81 | )% | (1.08 | )% | (1.26 | )% | (1.25 | )% | (1.19 | )% |

Portfolio turnover rate | | 37.58 | % | 96.45 | % | 84.55 | % | 82.13 | % | 89.15 | % | 149.17 | % |

See Notes to Financial Statements.

(i) Ratios have been annualized; total return and portfolio turnover rate have not been annualized.

(ii) Amount was computed based on average shares outstanding during the period.

(iii) Does not reflect the effect of sales charges, if applicable.

25

| | Class I | |

| | Six months

ended

4/30/2014(i) | | From 5/31/2013

(commencement

of operations) to

10/31/2013(ii) | |

Net asset value, beginning of period | | $ | 18.78 | | $ | 16.83 | |

INCOME FROM INVESTMENT OPERATIONS: | | | | | |

Net investment income(iii) | | 0.01 | | 0.03 | |

Net realized and unrealized gain on investments | | 0.79 | | 1.92 | |

Total from investment operations | | 0.80 | | 1.95 | |

Net asset value, end of period | | $ | 19.58 | | $ | 18.78 | |

Total return(iv) | | 4.26 | % | 11.59 | % |

RATIOS/SUPPLEMENTAL DATA: | | | | | |

Net assets, end of period (000’s omitted) | | $ | 1,472 | | $ | 1,296 | |

Ratio of gross expenses to average net assets | | 2.07 | % | 2.97 | % |

Ratio of expense reimbursements to average net assets | | (0.82 | )% | (1.72 | )% |

Ratio of net expenses to average net assets | | 1.25 | % | 1.25 | % |

Ratio of net investment income (loss) to average net assets | | 0.13 | % | 0.47 | % |

Portfolio turnover rate | | 37.58 | % | 96.45 | % |

See Notes to Financial Statements.

(i) Ratios have been annualized; total return and portfolio turnover rate have not been annualized.

(ii) Ratios have been annualized; total return has not been annualized; portfolio turnover is for the twelve months then ended.

(iii) Amount was computed based on average shares outstanding during the period.

(iv) Does not reflect the effect of sales charges, if applicable.

26

| | Class Z | |

| | Six months

ended

4/30/2014(i) | | From 5/31/2013

(commencement

of operations) to

10/31/2013(ii) | |

Net asset value, beginning of period | | $ | 18.80 | | $ | 16.83 | |

INCOME FROM INVESTMENT OPERATIONS: | | | | | |

Net investment income(iii) | | 0.04 | | 0.04 | |

Net realized and unrealized gain on investments | | 0.79 | | 1.93 | |

Total from investment operations | | 0.83 | | 1.97 | |

Net asset value, end of period | | $ | 19.63 | | $ | 18.80 | |

Total return(iv) | | 4.41 | % | 11.71 | % |

RATIOS/SUPPLEMENTAL DATA: | | | | | |

Net assets, end of period (000’s omitted) | | $ | 117 | | $ | 112 | |

Ratio of gross expenses to average net assets | | 8.78 | % | 12.42 | % |

Ratio of expense reimbursements to average net assets | | (7.79 | )% | (11.43 | )% |

Ratio of net expenses to average net assets | | 0.99 | % | 0.99 | % |

Ratio of net investment income (loss) to average net assets | | 0.39 | % | 0.62 | % |

Portfolio turnover rate | | 37.58 | % | 96.45 | % |

See Notes to Financial Statements.

(i) Ratios have been annualized; total return and portfolio turnover rate have not been annualized.

(ii) Ratios have been annualized; total return has not been annualized; portfolio turnover is for the twelve months then ended.

(iii) Amount was computed based on average shares outstanding during the period.

(iv) Does not reflect the effect of sales charges, if applicable.

27

ALGER GLOBAL GROWTH FUND

NOTES TO FINANCIAL STATEMENTS (Unaudited)

NOTE 1 — General:

Alger Global Growth Fund (the “Fund”) is a diversified, open-end registered investment company organized as a business trust under the laws of the Commonwealth of Massachusetts. The Fund qualifies as an investment company as defined in Accounting Standards Codification 946 Financial Services — Investment Companies. The Fund’s investment objective is long-term capital appreciation. It seeks to achieve its objective by investing in equity securities in the United States and foreign countries. The Fund’s foreign investments will include securities of companies in both developed and emerging market countries. The Fund offers Class A, C, I and Z shares. Class A shares are generally subject to an initial sales charge while Class C shares are generally subject to a deferred sales charge. Class I and Z shares are sold to institutional investors without an initial or deferred sales charge. Each class has identical rights to assets and earnings except that each share class bears the cost of its plan of distribution and transfer agency and sub-transfer agency services.

NOTE 2 — Significant Accounting Policies:

(a) Investment Valuation: The Fund values its financial instruments at fair value using independent dealers or pricing services under policies approved by the Board of Trustees. Investments are valued on each day the New York Stock Exchange (the “NYSE”) is open, as of the close of the NYSE (normally 4:00 p.m. Eastern time).

Equity securities and option contracts for which valuation information is readily available are valued at the last reported sales price or official closing price as reported by an independent pricing service on the primary market or exchange on which they are traded. In the absence of reported sales, such securities are valued at the bid price or, in the absence of a recent bid price, the equivalent as obtained from one or more of the major market makers for the securities to be valued.

Securities for which market quotations are not readily available are valued at fair value, as determined in good faith pursuant to procedures established by the Board of Trustees.

Securities in which the Fund invests may be traded in foreign markets that close before the close of the NYSE. Developments that occur between the close of the foreign markets and the close of the NYSE may result in adjustments to the foreign closing prices to reflect what the investment adviser, pursuant to policies established by the Board of Trustees, believes to be the fair value of these securities as of the close of the NYSE. The Fund may also fair value securities in other situations, for example, when a particular foreign market is closed but the Fund is open.

Financial Accounting Standards Board Accounting Standards Codification 820 — Fair Value Measurements and Disclosures (“ASC 820”) defines fair value as the price that the Fund would receive upon selling an investment in a timely transaction to an independent buyer in the principal or most advantageous market of the investment. ASC 820 established a three-tier hierarchy to maximize the use of observable market data and minimize the use of unobservable inputs and to establish classification of fair value

28

ALGER GLOBAL GROWTH FUND

NOTES TO FINANCIAL STATEMENTS (Unaudited) (Continued)

measurements for disclosure purposes. Inputs refer broadly to the assumptions that market participants would use in pricing the asset or liability and may be observable or unobservable. Observable inputs are based on market data obtained from sources independent of the Fund. Unobservable inputs are inputs that reflect the Fund’s own assumptions based on the best information available in the circumstances. The three-tier hierarchy of inputs is summarized in the three broad Levels listed below.

· Level 1 — quoted prices in active markets for identical investments

· Level 2 — significant other observable inputs (including quoted prices for similar investments, interest rates, prepayment speeds, credit risk, etc.)

· Level 3 — significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of investments)

The Funds’ valuation techniques are generally consistent with either the market or income approach to fair value. The market approach considers prices and other relevant information generated by market transactions involving identical or comparable assets are used to measure fair value. The income approach converts future amounts to a current, or discounted, single amount. These fair value measurements are determined on the basis of the value indicated by current market expectations about such future events. Inputs for Level 1 include exchange-listed prices and broker quotes in an active market. Inputs for Level 2 include the last trade price in the case of a halted security, an exchange-listed price which has been adjusted for fair value factors, and prices of closely related securities. Additional Level 2 inputs include an evaluated price which is based upon a compilation of observable market information such as spreads for fixed income and preferred securities. Inputs for Level 3 include unobservable market information which can include cash flows, income and expenses, and other information obtained from a company’s financial statements, or from market indicators such as benchmarks and indices.

Valuation processes are determined by a Valuation Committee (“Committee”) established by the Fund’s Board of Trustees (“Board”) and comprised of representatives of the Fund’s investment advisor. The Committee reports its fair valuation determinations to the Board which is responsible for approving valuation policy and procedures.

While the Committee meets on an as-needed basis, the Committee formally meets quarterly to review and evaluate the effectiveness of the procedures for making fair value determinations. The Committee considers, among other things, the results of quarterly back testing of the fair value model for foreign securities, pricing comparisons between primary and secondary price sources, the outcome of price challenges put to the Fund’s pricing vendor, and variances between transactional prices and previous mark-to-markets.

The Fund will record a change to a security’s fair value level if new inputs are available or it becomes evident that inputs previously considered for leveling have changed or are no longer relevant. Transfers between Levels 1 and 2 are recognized at the end of the reporting period, and transfers into and out of Level 3 are recognized during the reporting period.

29

ALGER GLOBAL GROWTH FUND

NOTES TO FINANCIAL STATEMENTS (Unaudited) (Continued)

(b) Cash and Cash Equivalents: Cash and cash equivalents include U.S. dollars, foreign cash and overnight time deposits.

(c) Securities Transactions and Investment Income: Securities transactions are recorded on a trade date basis. Realized gains and losses from securities transactions are recorded on the identified cost basis. Dividend income is recognized on the ex-dividend date and interest income is recognized on the accrual basis.

(d) Foreign Currency Translations: The books and records of the Fund are maintained in U.S. dollars. Foreign currencies, investments and other assets and liabilities are translated into U.S. dollars at the prevailing rates of exchange on the valuation date. Purchases and sales of investment securities and income and expenses are translated into U.S. dollars at the prevailing exchange rates on the respective dates of such transactions.

Net realized gains and losses on foreign currency transactions represent net gains and losses from the disposition of foreign currencies, currency gains and losses realized between the trade dates and settlement dates of security transactions, and the difference between the amount of net investment income accrued and the U.S. dollar amount actually received. The effects of changes in foreign currency exchange rates on investments in securities are included in realized and unrealized gain or loss on investments in the Statement of Operations.

(e) Dividends to Shareholders: Dividends and distributions payable to shareholders are recorded by the Fund on the ex-dividend date. Dividends from net investment income and distributions from net realized gains are declared and paid annually after the end of the fiscal year in which earned.

Each class is treated separately in determining the amounts of dividends from net investment income payable to holders of its shares.

The characterization of distributions to shareholders for financial reporting purposes is determined in accordance with federal income tax rules. Therefore, the source of the Fund’s distributions may be shown in the accompanying financial statements as either from, or in excess of, net investment income, net realized gain on investment transactions or return of capital, depending on the type of book/tax differences that may exist. Capital accounts within the financial statements are adjusted for permanent book/tax differences. Reclassifications result primarily from the difference in tax treatment of net operating losses, passive foreign investment companies, and foreign currency transactions. The reclassifications are done annually at fiscal year end and have no impact on the net asset value of the Fund and are designed to present the Fund’s capital accounts on a tax basis.

(f) Lending of Fund Securities: The Fund may lend its securities to financial institutions, provided that the market value of the securities loaned will not at any time exceed one third of the Fund’s total assets, as defined in its prospectuses. The Fund earns fees on the securities loaned, which are included in interest income in the accompanying Statements of Operations. In order to protect against the risk of failure by the borrower to return the securities loaned or any delay in the delivery of such securities, the loan is collateralized by cash or securities that are maintained with the Custodian in an amount equal to at least 102 percent of the current market value of U.S. loaned securities or 105 percent for non-

30

ALGER GLOBAL GROWTH FUND

NOTES TO FINANCIAL STATEMENTS (Unaudited) (Continued)

U.S. loaned securities. The market value of the loaned securities is determined at the close of business of the Fund. Any required additional collateral is delivered to the Custodian and any excess collateral is returned to the borrower on the next business day. In the event the borrower fails to return the loaned securities when due, the Fund may take the collateral to replace the securities. If the value of the collateral is less than the purchase cost of replacement securities, the Custodian shall be responsible for any shortfall, but only to the extent that the shortfall is not due to any diminution in collateral value, as defined in the securities lending agreement. The Fund is required to maintain the collateral in a segregated account and determine its value each day until the loaned securities are returned. Cash collateral may be invested as determined by the Fund. Collateral is returned to the borrower upon settlement of the loan.

(f) Federal Income Taxes: It is the Fund’s policy to comply with the requirements of the Internal Revenue Code Subchapter M applicable to regulated investment companies and to distribute all of its taxable income to its shareholders. Provided that the Fund maintains such compliance, no federal income tax provision is required.

Financial Accounting Standards Board Accounting Standards Codification 740 — Income Taxes (“ASC 740”) requires the Fund to measure and recognize in its financial statements the benefit of a tax position taken (or expected to be taken) on an income tax return if such position will more likely than not be sustained upon examination based on the technical merits of the position. No tax years are currently under investigation. The Fund files income tax returns in the U.S., as well as New York State and New York City. The statute of limitations on the Fund’s tax returns remains open for the tax years 2009-2013. Management does not believe there are any uncertain tax positions that require recognition of a tax liability.

(g) Estimates: These financial statements have been prepared in accordance with accounting principles generally accepted in the United States of America, which require using estimates and assumptions that affect the reported amounts therein. Actual results may differ from those estimates. These unaudited interim financial statements reflect all adjustments which are, in the opinion of management, necessary to present a fair statement of results for the interim period. All such adjustments are of normal recurring nature.

NOTE 3 — Investment Advisory Fees and Other Transactions with Affiliates:

(a) Investment Advisory Fees: The fees incurred by the Fund, pursuant to the provisions of the Fund’s Investment Advisory Agreement with Fred Alger Management, Inc. (“Alger Management” or the “Manager”), are payable monthly and computed based on the average daily net assets of the Fund at the annual rate of 0.80%.

Effective May 31, 2013, Alger Management established expense caps for the share classes, through February 28, 2015, whereby it reimburses the share classes if annualized operating expenses (excluding interest, taxes, brokerage, and extraordinary expenses) exceed the rates, based on average daily net assets, listed below:

31

ALGER GLOBAL GROWTH FUND

NOTES TO FINANCIAL STATEMENTS (Unaudited) (Continued)

| | CLASS | | FEES WAIVED /

REIMBURSED FOR

THE SIX MONTHS

ENDED | |

| | A | | C | | I | | Z | | APRIL 30, 2014 | |

Alger Global Growth Fund | | 1.50 | % | 2.25 | % | 1.25 | % | 0.99 | % | $ | 119,221 | |

| | | | | | | | | | | | |

(b) Administration Fees: Fees incurred by the Fund, pursuant to the provisions of the Fund’s Administration Agreement with Fred Alger Management, Inc., are payable monthly and computed based on the average daily net assets of the Fund at the annual rate of 0.0275%.

(c) Distribution/Shareholder Servicing Fees: The Fund has adopted a distribution plan pursuant to which the Fund pays Alger Inc. a fee at the annual rate of 0.25% of the average daily net assets of the Class A and Class I shares and 1.00% of the average daily net assets of the Class C shares to compensate Alger Inc. for its activities and expenses incurred in distributing the Fund’s shares and shareholder servicing. Fees paid may be more or less than the expenses incurred by Alger Inc.

(d) Sales Charges: Purchases of shares of the Fund may be subject to initial sales charges or contingent deferred sales charges. For the six months ended April 30, 2014, the initial sales charges and contingent deferred sales charges imposed, all of which were retained by Fred Alger & Company, Incorporated, the Fund’s distributor (the “Distributor” or “Alger Inc.”), were approximately $1,300 and $260 respectively. The contingent deferred sales charges are used by Alger Inc. to offset distribution expenses previously incurred. Sales charges do not represent expenses of the Fund.

(e) Brokerage Commissions: During the six months ended April 30, 2014, the Fund paid Alger Inc. $2,653 in connection with securities transactions.

(f) Shareholder Administrative Fees: The Fund has entered into a shareholder administrative services agreement with Alger Management to compensate Alger Management for its liaison and administrative oversight of Boston Financial Data Services, Inc. the transfer agent, and other related services. The Fund compensates Alger Management at the annual rate of 0.0165% of the average daily net assets for Class A and Class C shares and 0.01% of the daily net assets of the Class I and Class Z shares for these services.

Alger Management makes payments to intermediaries that provide sub-accounting services to omnibus accounts, held by the Fund. A portion of the fees paid by Alger Management to intermediaries that provide sub-accounting services are charged back to the Fund, subject to certain limitations, as approved by the Fund’s Board of Trustees. For the six months ended April 30, 2014, Alger Management charged back $7,399 to the Fund for these services, which are included in the transfer agent fees and expenses in the Statement of Operations.

(g) Trustees’ Fees: From November 1, 2013 through March 5, 2014, the Fund paid each trustee who is not affiliated with Alger Management or its affiliates $880 for each meeting attended, to a maximum of $3,520 per annum, plus travel expenses incurred for attending the meeting. The Chairman of the Board received an additional annual fee of $22,500

32

ALGER GLOBAL GROWTH FUND

NOTES TO FINANCIAL STATEMENTS (Unaudited) (Continued)