Exhibit 99.1

For purposes of this Exhibit 99.1, unless the context otherwise requires: (i) “Crown” refers to Crown Holdings, Inc. and its subsidiaries on a consolidated basis; (ii) “Crown Cork” refers to Crown Cork & Seal Company, Inc. and not its subsidiaries; (iii) “Crown European Holdings” refers to Crown European Holdings SA and not its subsidiaries; (iv) “Crown Americas” refers to Crown Americas, LLC and not its subsidiaries; (v) “Crown Americas Capital” refers to Crown Americas Capital Corp. and not its subsidiaries; (vi) the description of Crown’s business and related matters gives effect to the sale of Crown’s plastic closures business in October 2005; and (vii) Crown’s historical financial results and related financial information reflect the reclassification to discontinued operations of amounts related to Crown’s plastic closures business that was sold in October 2005.

FORWARD-LOOKING STATEMENTS

Statements included herein, which are not historical facts (including any statements concerning plans and objectives of management for future operations or economic performance, or assumptions related thereto), are “forward-looking statements” within the meaning of the U.S. federal securities laws. Forward-looking statements can be identified by words, such as “believes,” “estimates,” “anticipates,” “expects” and other words of similar meaning in connection with a discussion of future operating or financial performance. These may include, among others, statements relating to:

| • | Crown’s 2005 refinancing plan, and Crown’s ability to implement it on the terms described herein; |

| • | Crown’s plans or objectives for future operations, products or financial performance; |

| • | Crown’s and its subsidiaries’ indebtedness; |

| • | the impact of an economic downturn or growth in particular regions; |

| • | anticipated uses of cash; |

| • | cost reduction efforts and expected savings; and |

| • | the expected outcome of contingencies, including with respect to asbestos-related litigation and pension liabilities. |

These forward-looking statements are made based upon Crown’s expectations and beliefs concerning future events impacting it and therefore involve a number of risks and uncertainties. Crown cautions that forward-looking statements are not guarantees and that actual results could differ materially from those expressed or implied in the forward-looking statements.

Important factors that could cause the actual results of operations or the financial condition of Crown and its subsidiaries to differ include, but are not necessarily limited to, the factors indicated under the caption “Risk Factors” and the following additional factors:

| • | their ability to repay, refinance or restructure their short and long-term indebtedness on adequate terms and to comply with the terms of their agreements relating to debt; |

| • | loss of customers, including the loss of any significant customer; |

| • | their ability to obtain and maintain adequate pricing for their products, including the impact on their revenue, margins and market share and the ongoing impact of their recent price increases; |

| • | the impact of their initiative to generate additional cash, including the reduction of working capital levels and capital spending; |

| • | restrictions on Crown’s use of available cash under its debt agreements; |

| • | their ability to realize cost savings from their restructuring programs; |

| • | changes in the availability and pricing of raw materials (including aluminum can sheet, steel tinplate, plastic resin, inks and coatings) and energy and their ability to pass raw material and energy price increases and surcharges through to their customers or to otherwise manage these commodity pricing risks; |

1

| • | the financial condition of their vendors and customers; |

| • | their ability to generate significant cash to meet their obligations and invest in their business and to maintain appropriate debt levels; |

| • | their ability to maintain adequate sources of capital and liquidity; |

| • | their ability to realize efficient capacity utilization and inventory levels; |

| • | changes in consumer preferences for different packaging products; |

| • | competitive pressures, including new product developments, industry overcapacity, or changes in competitors’ pricing for products; |

| • | their ability to maintain and develop competitive technologies for the design and manufacture of products in a cost effective manner and to withstand competitive and legal challenges to the proprietary nature of such technology; |

| • | their ability to generate sufficient production capacity; |

| • | the collectibility of receivables; |

| • | changes in governmental regulations or enforcement practices, including with respect to environmental, health and safety matters and restrictions as to foreign investment or operation; |

| • | weather conditions including their effect on demand for beverages and on crop yields for fruits and vegetables stored in food containers; |

| • | changes or differences in U.S. or international economic or political conditions, such as inflation or fluctuations in interest or foreign exchange rates and tax rates; |

| • | war or acts of terrorism that may disrupt their production or the supply or pricing of raw materials, impact the financial condition of their customers or adversely affect their ability to refinance or restructure their indebtedness; |

| • | the impact of existing and future legislation regarding refundable mandatory deposit laws in Europe for non-refillable beverage containers and the implementation of an effective return system; |

| • | energy and natural resource costs; |

| • | the costs and other effects of legal and administrative cases and proceedings, settlements and investigations; |

| • | the outcome of asbestos-related litigation, including the number and size of future claims and the terms of settlements, and the impact of bankruptcy filings by other companies with asbestos-related liabilities, any of which could increase asbestos-related costs over time, the adequacy of reserves established for asbestos-related liabilities, Crown Cork’s ability to obtain resolution without payment of asbestos related claims by persons alleging first exposure to asbestos after 1964, and the impact of Texas, Mississippi, Ohio, Florida and Pennsylvania legislation dealing with asbestos liabilities and any litigation challenging that legislation and any future state or federal legislation dealing with asbestos liabilities; |

| • | labor relations and workforce and social costs, including pension and post-retirement obligations and other employee or retiree costs; |

| • | investment performance of their pension plans; |

| • | costs and difficulties related to the integration of acquired businesses; and |

| • | the impact of any potential dispositions, acquisitions or other strategic realignments, including the recent sale of Crown’s plastic closures business and the final net proceeds therefrom. |

Crown does not intend to review or revise any particular forward-looking statement in light of future events.

2

Crown Holdings, Inc.

Crown is a worldwide leader in the design, manufacture and sale of packaging products for consumer goods with 154 plants throughout 40 countries and approximately 25,000 employees. Crown’s primary products include steel and aluminum cans for food, beverage, household and other consumer products and a wide variety of metal caps and closures. Crown believes that, based on the number of units sold, it is the largest global supplier of food cans and metal vacuum closures and the third largest global supplier of beverage cans. In addition, Crown believes that it is the second largest producer of aerosol cans in the world and the largest rigid packaging company in Europe and Asia, excluding Japan. Crown’s leadership position in these markets with premier global consumer products companies results from its commitment to be the technology leader within the industry and to provide its longstanding customers with value-added product offerings. Crown also believes that its global operations help mitigate the adverse effects of periodic, market-specific dislocations in specific countries or regions. For the fiscal year ended December 31, 2004 and the nine months ended September 30, 2005, Crown had net sales of approximately $6.5 billion and $5.3 billion, respectively, and Adjusted EBITDA (a non-GAAP measure that is defined in “—Summary Historical and Pro Forma Consolidated Condensed Financial Data”) of $750 million and $636 million, respectively. Approximately 41% of such net sales were derived from the Americas segment, 53% from the European segment and 6% from the Asia-Pacific segment in each of the fiscal year ended December 31, 2004 and the nine months ended September 30, 2005. For the twelve months ended September 30, 2005, Crown had net sales of approximately $6.9 billion and Adjusted EBITDA of approximately $793 million.

On October 11, 2005, Crown completed the sale of its plastic closures business for an aggregate purchase price of approximately $750 million, which includes the assumption of certain liabilities. Net cash proceeds from the sale were approximately $690 million, which is subject to final working capital, net debt and other adjustments. Crown expects to use the net proceeds of the sale for general corporate purposes including the repayment of debt. The plastic closures business designed, manufactured and sold plastic closures for consumer packaging worldwide primarily for the personal care, food, beverage, pharmaceutical and industrial end markets. The business had 29 facilities located in 15 countries across Europe, the United States and Asia with approximately 3,500 employees. For the twelve months ended December 31, 2004, net sales for the business were $668 million with approximately 77% derived from sales in Europe.

3

The following chart demonstrates the breadth of Crown’s product portfolio and its geographic presence:

| North America | Latin America | Europe | Middle East/ Africa | Asia- Pacific | ||||||

Metal | ||||||||||

Food cans | « | « | « | « | « | |||||

Beverage cans | « | « | « | « | « | |||||

Aerosol cans | « | « | « | « | ||||||

Specialty cans | « | « | « | |||||||

Closures | « | « | ||||||||

Bottle caps | « | « | « | « | ||||||

Other | ||||||||||

Beauty care | « | « | ||||||||

Can-making equipment | « |

Business Strengths

Crown’s principal strength lies in its ability to meet the changing needs of its global customer base with products and processes from a broad range of well-established packaging businesses. Crown believes that it is well-positioned within the packaging industry because of its:

| • | Global leadership positions. Crown is a leading producer of food, beverage and aerosol cans and of closures in North America, Europe and Asia. Crown maintains its leadership through an extensive geographic presence, with 154 plants located throughout the world. Its large manufacturing base allows Crown to service its customers locally while achieving significant economies of scale. |

| • | Strong customer base. Crown provides packaging to many of the world’s leading consumer products companies. Major customers include Anheuser-Busch, Cadbury Schweppes, Coca-Cola, Cott Beverages, Heineken, Mars, Nestlé, Pepsi-Cola, Procter & Gamble, S.C. Johnson, Scottish & Newcastle and Unilever. These consumer products companies represent stable businesses that provide consumer staples such as soft drinks, alcoholic beverages, foods and household products, which are relatively resistant to cyclicality. In addition, Crown has long-standing relationships with many of its largest customers. |

| • | Broad and diversified product base. Crown produces a wide array of products differentiated by type, purpose, size, shape and benefit to customers. Crown is not dependent on any specific product market since no product in any one geographical region represents a substantial share of total revenues. The number and type of products that Crown sells continues to increase due to increasing customer specialization and technological advances made by Crown. |

| • | Improving business and industry fundamentals. Crown’s ability to initiate fundamental changes in its business, including price increases, cost reduction initiatives and working capital reductions, has improved its business outlook. |

| • | Technological leadership resulting in superior new product and process development. Crown believes that it possesses the technology, processes and research, development and engineering capabilities to allow it to provide innovative and value-added packaging solutions to its customers, as well as to design cost-efficient manufacturing systems and materials. Recent product innovations include: the “SuperEnd™” for beverage cans, which requires less metal than existing ends without any reduction in strength; high value-added shaped beverage and aerosol cans, including, for example, Heineken’s keg can; and patented composite (metal and plastic) closures which offer improved barrier performance and tamper resistance while requiring less strength to open than standard closures. |

| • | Financially disciplined management team. Crown’s current executive leadership is focused on improving profit, increasing free cash flow, reducing debt levels and enhancing financial flexibility. |

4

Business Strategy

Crown’s principal strategic goals are to continue to improve its business operations and reduce debt in order to regain investment grade ratings on its debt securities, increase its financial flexibility and position itself for further growth. To achieve these goals, Crown has several key business strategies:

| • | Grow in targeted markets. Crown plans to capitalize on its leading food, beverage and aerosol can positions by targeting geographic areas with strong growth potential. Crown believes that it is well-positioned to take advantage of the growth potential in Southern and Eastern Europe with numerous food and beverage can plants already established in those markets. In addition, as a leading packaging supplier to the Middle Eastern, Southeast Asian and Latin American markets, Crown will work to benefit from the anticipated strong growth in the consumption of consumer goods in these regions. |

| • | Increase margins through ongoing cost reductions. Crown plans to continue to reduce manufacturing costs and enhance efficiencies through investments in equipment and technology and through improvements in productivity and material usage. |

| • | Maximize cash flow generation in order to reduce debt. Crown has implemented changes in its management of working capital, reduced capital expenditures by focusing on projects that provide an adequate return and established performance-based incentives to increase its free cash flow and operating income and reduce debt. |

| • | Serve the changing needs of the world’s leading consumer products companies through technological innovation. Crown intends to capitalize on the demand of its customers for higher value-added packaging products. By continuing to improve the physical attributes of its products, such as strength of materials and graphics, Crown plans to further improve its existing customer relationships, as well as attract new customers. |

2005 Refinancing Plan

Crown Americas and Crown Americas Capital intend to issue $1.1 billion of senior notes as part of a plan to repurchase or retire all of Crown European Holdings’ approximately $2.1 billion of outstanding second and third priority notes and to refinance Crown’s existing $400 million revolving credit facilities (under which there were $10 million of outstanding borrowings as of September 30, 2005) and $100 million revolving letter of credit facility. The purpose of the refinancing is to extend the average maturity of Crown’s indebtedness, increase operating and financial flexibility and reduce interest expense.

Crown has commenced tender offers for any and all of Crown European Holdings’ approximately $2.1 billion of outstanding second and third priority senior secured notes. In connection with the tender offers, Crown has solicited consents to amend the indentures governing the second and third priority notes to release collateral securing the notes and eliminate substantially all of the restrictive covenants, reporting requirements and certain events of default.

Under the terms of the tender offers, the consideration for tendered notes equals the sum of the price calculated to equal the present value (determined on the basis of the yield to maturity of a comparable U.S. Treasury, for dollar denominated notes, or German government, for euro denominated notes, security plus 50 basis points) on the tender offer’s payment date of the earliest redemption price and accrued interest that would apply to the applicable series of second priority or third priority notes.

The consideration includes a consent payment of $20.00 per $1,000 principal amount or €20.00 per €1,000 principal amount, as applicable, of second priority or third priority notes for notes tendered prior to the consent deadline. Each tender offer is subject to the satisfaction or waiver of various conditions, including the receipt of

5

consents from holders of at least 66 2/3% of the aggregate principal amount of the applicable notes, the execution of a supplemental indenture amending the applicable indenture, the entry into new senior credit facilities and the issuance of the new notes as part of the 2005 refinancing plan, the consummation of the other tender offer and other customary conditions. Crown may amend, extend or terminate each tender offer and consent solicitation in its sole discretion. At any time and from time to time before, during and after the expiration of the tender offers, Crown may purchase or offer to purchase second priority and third priority notes through open market purchases, privately negotiated transactions, tender offers, exchange offers, redemptions or otherwise. As of November 4, 2005, the depositaries for the tender offers have advised Crown that approximately $1,059 million aggregate principal amount, or 97.6%, of second priority dollar denominated notes, €265 million aggregate principal amount, or 93.2%, of second priority euro denominated notes and $720 million aggregate principal amount, or 99.4%, of third priority notes have been tendered and not withdrawn to date. To the extent that any second priority and third priority notes remain outstanding after consummation of the refinancing and sale of the new notes, Crown intends to reduce initial borrowings under the new senior secured revolving credit facilities.

Crown expects that the sources of funds for its 2005 refinancing plan will include:

| • | the proceeds from the new notes; |

| • | borrowings under Crown’s proposed new approximately $1.3 billion revolving and term loan senior secured credit facilities; and |

| • | approximately $690 million of proceeds from the recent sale of Crown’s plastic closures business. |

Crown expects that the new senior secured credit facilities will consist of (a) senior secured revolving credit facilities that will mature on May 15, 2011 in an aggregate principal amount of $800 million, of which up to $410 million will be available to Crown Americas in U.S. dollars, up to $350 million will be available to Crown European Holdings and certain of its subsidiaries in euros and pound sterling in amounts to be agreed and up to $40 million will be available to a Canadian subsidiary of Crown European Holdings in Canadian dollars and (b) senior term loan facilities that will mature on November 15, 2012 in an aggregate principal amount of $500 million of which $250 million will be loaned to Crown Americas in U.S. dollars and $250 million will be loaned to Crown European Holdings in euros.

The final amounts and sources of funds for Crown’s 2005 refinancing plan may change. Crown may elect to change the size of the note offering, the amount of borrowings or availability under the new credit facilities or may substitute other sources of proceeds. The receipt of at least $2.2 billion in gross proceeds (including unfunded revolving commitments) from the closing of Crown’s new senior secured credit facilities and the sale of the notes, and consummation of the tender offers for the second and third priority notes are conditions precedent to closing the note offering.

6

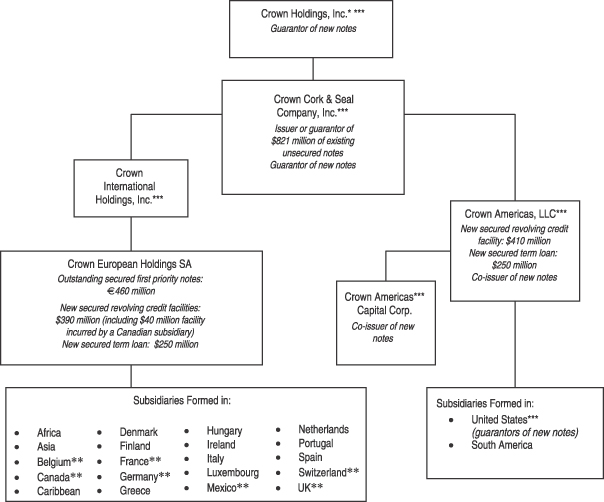

Organizational Structure

The following chart shows a summary of Crown’s current organizational structure, after giving effect to the completion of the 2005 refinancing plan. See “Capitalization.”

| * | Guarantor of Crown Cork’s obligations under the outstanding unsecured notes. See “Description of Certain Indebtedness.” |

| ** | Guarantors of outstanding secured first priority notes and new secured credit facilities to Crown European Holdings and its subsidiaries. |

| *** | Guarantors of outstanding secured first priority notes and all new secured credit facilities. |

7

Crown European Holdings is also the issuer of approximately $2.1 billion of outstanding second priority and third priority notes. As part of the 2005 refinancing plan, Crown has commenced tender offers for any and all outstanding second and third priority notes. As of November 4, 2005, the depositaries for the tender offers have advised Crown that approximately $1,059 million aggregate principal amount, or 97.6%, of second priority dollar denominated notes, €265 million aggregate principal amount, or 93.2%, of second priority euro denominated notes and $720 million aggregate principal amount, or 99.4%, of third priority notes have been tendered. Guarantors of the outstanding secured first priority notes are also guarantors of outstanding secured second priority and third priority notes. See “Description of Certain Indebtedness.”

Crown is a Pennsylvania corporation. Crown’s principal executive offices are located at One Crown Way, Philadelphia, Pennsylvania 19154, and its telephone number is (215) 698-5100. Crown Cork is a Pennsylvania corporation. Crown Americas (formerly known as Crown Americas, Inc.) is a Pennsylvania limited liability company. Crown Americas Capital is a Delaware corporation. Crown European Holdings (formerly known as CarnaudMetalbox SA) is asociété anonyme organized under the laws of France. Each of Crown Cork, Crown Americas, Crown Americas Capital and Crown European Holdings is an indirect, wholly-owned subsidiary of Crown.

8

Summary Historical and Pro Forma Consolidated Condensed Financial Data

The following table sets forth summary historical and pro forma consolidated condensed financial data for Crown. The summary of operations for each of the years in the three-year period ended December 31, 2004 and the balance sheet data as of December 31, 2003 and 2004 have been derived from Crown’s audited consolidated financial statements and the notes thereto. The summary of operations for the nine-month period ended September 30, 2005, the nine-month period ended September 30, 2004, and the balance sheet data as of September 30, 2004 and 2005 have been derived from Crown’s unaudited interim consolidated financial statements. The summary of operations for the twelve month period ended September 30, 2004 have been derived from the summary of operations and other data for the year ended December 31, 2004 and the nine month periods ended September 30, 2004 and 2005. The results of operations reflect the reclassification to discontinued operations of amounts related to Crown’s plastic closures business that was sold in October 2005. The December 31, 2002 balance sheet data has been derived from Crown’s audited consolidated financial statements which do not appear herein. The pro forma data gives effect to the consummation of the 2005 refinancing plan described under the caption “—2005 Refinancing Plan.” You should read the following financial information in conjunction with Crown’s consolidated financial statements, the related notes and the other financial information included elsewhere.

| (dollars in millions) | ||||||||||||||||||||||||

| Historical Year Ended December 31, | Nine Months Ended September 30, | Twelve Months Ended September 30, 2005 | ||||||||||||||||||||||

| 2002(1) | 2003 | 2004 | 2004 | 2005 | ||||||||||||||||||||

Summary of Operations Data: | ||||||||||||||||||||||||

Net sales | $ | 6,246 | $ | 6,007 | $ | 6,531 | $ | 4,946 | $ | 5,279 | $ | 6,864 | ||||||||||||

Cost of products sold (excluding depreciation and amortization) | 5,220 | 5,073 | 5,463 | 4,117 | 4,381 | 5,727 | ||||||||||||||||||

Depreciation and amortization | 332 | 281 | 263 | 197 | 188 | 254 | ||||||||||||||||||

Gross profit | 694 | 653 | 805 | 632 | 710 | 883 | ||||||||||||||||||

Selling and administrative expense | 277 | 292 | 318 | 236 | 262 | 344 | ||||||||||||||||||

Provision for asbestos | 30 | 44 | 35 | 35 | ||||||||||||||||||||

Provision for restructuring | 18 | 15 | 7 | 1 | 3 | 9 | ||||||||||||||||||

Provision for asset impairments and loss/(gain) on sale of assets | 247 | 76 | 47 | (22 | ) | 25 | ||||||||||||||||||

Loss/(gain) from early extinguishments of debt | (28 | ) | 12 | 39 | 37 | 2 | 4 | |||||||||||||||||

Interest expense | 342 | 379 | 361 | 270 | 283 | 374 | ||||||||||||||||||

Interest income | (11 | ) | (11 | ) | (8 | ) | (5 | ) | (6 | ) | (9 | ) | ||||||||||||

Translation and exchange adjustments | 26 | (207 | ) | (98 | ) | (7 | ) | 76 | (15 | ) | ||||||||||||||

Income/(loss) from continuing operations before income taxes, minority interests, equity earnings and cumulative effect of a change in accounting (2) | (207 | ) | 53 | 104 | 100 | 112 | 116 | |||||||||||||||||

Provision for income taxes | 9 | 71 | 61 | 37 | 13 | 37 | ||||||||||||||||||

Minority interests | (24 | ) | (39 | ) | (41 | ) | (28 | ) | (32 | ) | (45 | ) | ||||||||||||

Equity earnings/(loss) | 9 | (17 | ) | 14 | 10 | 10 | 14 | |||||||||||||||||

Income/(loss) from continuing operations before cumulative effect of a change in accounting (2) | (231 | ) | (74 | ) | 16 | 45 | 77 | 48 | ||||||||||||||||

Discontinued Operations (3) | ||||||||||||||||||||||||

Income before income taxes | 61 | 66 | 56 | 52 | 40 | 44 | ||||||||||||||||||

Provision for income taxes | 21 | 24 | 21 | 19 | 21 | 23 | ||||||||||||||||||

Income from discontinued operations | 40 | 42 | 35 | 33 | 19 | 21 | ||||||||||||||||||

Income/(loss) before cumulative effect of a change in accounting | (191 | ) | (32 | ) | 51 | 78 | 96 | 69 | ||||||||||||||||

Cumulative effect of a change in accounting, net of tax | (1,014 | ) | ||||||||||||||||||||||

Net income/(loss) | $ | (1,205 | ) | $ | (32 | ) | $ | 51 | $ | 78 | $ | 96 | $ | 69 | ||||||||||

9

| (dollars in millions) | ||||||||||||||||||||||||

| Historical Year Ended December 31, | Nine Months Ended September 30, | Twelve Months Ended September 30, 2005 | ||||||||||||||||||||||

| 2002(1) | 2003 | 2004 | 2004 | 2005 | ||||||||||||||||||||

Other Financial Data: | ||||||||||||||||||||||||

Cash flows provided by/(used in): | ||||||||||||||||||||||||

Operating activities | $ | 415 | $ | 434 | $ | 404 | $ | 30 | $ | 101 | $ | 475 | ||||||||||||

Investing activities | 591 | (100 | ) | (107 | ) | (91 | ) | (145 | ) | (161 | ) | |||||||||||||

Financing activities | (1,128 | ) | (328 | ) | (246 | ) | (43 | ) | (132 | ) | (335 | ) | ||||||||||||

EBITDA (4) | $ | 456 | $ | 702 | $ | 720 | $ | 562 | $ | 577 | $ | 735 | ||||||||||||

Adjusted EBITDA (5) | $ | 749 | $ | 642 | $ | 750 | $ | 593 | $ | 636 | $ | 793 | ||||||||||||

Capital expenditures | 115 | 120 | 138 | 97 | 115 | 156 | ||||||||||||||||||

Ratio of earnings to fixed charges (6)(7) | — | 1.2x | 1.3x | 1.4x | 1.4x | 1.3x | ||||||||||||||||||

Pro Forma Financial Data: | ||||||||||||||||||||||||

Total secured debt (8) | 1,491 | |||||||||||||||||||||||

Total debt | 3,575 | |||||||||||||||||||||||

Interest Expense (9) | 246 | |||||||||||||||||||||||

Ratio of secured debt to Adjusted EBITDA | 1.9 | x | ||||||||||||||||||||||

Ratio of total debt to Adjusted EBITDA | 4.5 | x | ||||||||||||||||||||||

Ratio of Adjusted EBITDA to Interest Expense | 3.2 | x | ||||||||||||||||||||||

Balance Sheet Data (at end of period): | ||||||||||||||||||||||||

Cash and cash equivalents | $ | 363 | $ | 401 | $ | 471 | $ | 295 | $ | 275 | $ | 275 | ||||||||||||

Working capital (10) | (246 | ) | 86 | 263 | 268 | 959 | 959 | |||||||||||||||||

Total assets | 7,505 | 7,773 | 8,125 | 7,904 | 7,728 | 7,728 | ||||||||||||||||||

Total debt | 4,054 | 3,939 | 3,872 | 3,959 | 3,705 | 3,705 | ||||||||||||||||||

Shareholders’ equity/(deficit) | (87 | ) | 140 | 277 | 233 | 207 | 207 | |||||||||||||||||

| (1) | The summary of operations and other data for the year ended December 31, 2002 includes the historical financial results of the following operations divested in 2002: |

| • | U.S. fragrance pumps business; |

| • | European pharmaceutical packaging business; |

| • | 15% shareholding in Crown Nampak (Pty) Limited; |

| • | Central and East African packaging interests; and |

| • | 89.5% of the equity interests of Constar International Inc. |

Excluding the historical financial results of these divested operations, Net Sales for 2002 would have been $5,572 million, Gross Profit for 2002 would have been $627 million, and Adjusted EBITDA for 2002 would have been $655 million. The following tables show a reconciliation of historical Net Sales, Gross Profit and Adjusted EBITDA to Net Sales, Gross Profit and Adjusted EBITDA excluding these divested operations (which is a non-GAAP measurement):

| (dollars in millions) | ||||||||||||

| Year Ended December 31, 2002 | ||||||||||||

| Historical Amounts | Disposition Adjustments | Adjusted for Dispositions | ||||||||||

Summary of Operations Data: | ||||||||||||

Net sales | $ | 6,246 | $ | (674 | ) | $ | 5,572 | |||||

Cost of products sold (excluding depreciation and amortization) | 5,220 | (558 | ) | 4,662 | ||||||||

Depreciation and amortization | 332 | (49 | ) | 283 | ||||||||

Gross profit | 694 | (67 | ) | 627 | ||||||||

Selling and administrative expense | 277 | (22 | ) | 255 | ||||||||

Provision for asbestos | 30 | — | 30 | |||||||||

Provision for restructuring | 18 | — | 18 | |||||||||

Provision for asset impairments and loss/(gain) on sale of assets | 247 | (243 | ) | 4 | ||||||||

Loss/(gain) from early extinguishments of debt | (28 | ) | — | (28 | ) | |||||||

Interest expense | 342 | (15 | ) | 327 | ||||||||

Interest income | (11 | ) | — | (11 | ) | |||||||

Translation and exchange adjustments | 26 | (1 | ) | 25 | ||||||||

Income/(loss) before income taxes, minority interests, equity earnings and cumulative effect of a change in accounting | (207 | ) | 214 | 7 | ||||||||

Provision for income taxes | 9 | (15 | ) | (6 | ) | |||||||

Minority interests and equity earnings | (15 | ) | 1 | (14 | ) | |||||||

Income/(loss) before cumulative effect of a change in accounting | $ | (231 | ) | $ | 230 | $ | (1 | ) | ||||

Adjusted EBITDA | $ | 749 | $ | (94 | ) | $ | 655 | |||||

See “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” |

| |||||||||||

10

| (2) | Excludes a charge of $1.014 billion in the first quarter of 2002 for the cumulative effect of a change in accounting for the adoption of SFAS 142, “Goodwill and Other Intangible Assets.” |

| (3) | On October 11, 2005, Crown completed the sale of its plastic closures business. The results of operations for the plastic closures business has been reported as discontinued operations for all periods presented. |

| (4) | EBITDA is a non-GAAP measurement that consists of income/(loss) from continuing operations before income taxes, minority interests, equity earnings and cumulative effect of a change in accounting plus the sum of interest expense (net of interest income) and depreciation and amortization. The reconciliation from EBITDA to income/(loss) from continuing operations before cumulative effect of a change in accounting is as follows: |

| (dollars in millions) | ||||||||||||||||||||||||

| Year Ended December 31, | Nine Months Ended September 30, | Twelve Months Ended September 30, 2005 | ||||||||||||||||||||||

| 2002 | 2003 | 2004 | 2004 | 2005 | ||||||||||||||||||||

Income/(loss) from continuing operations before cumulative effect of a change in accounting | $ | (231 | ) | $ | (74 | ) | $ | 16 | $ | 45 | $ | 77 | $ | 48 | ||||||||||

Add/(deduct): | ||||||||||||||||||||||||

Minority interests and equity earnings | 15 | 56 | 27 | 18 | 22 | 31 | ||||||||||||||||||

Provision for income taxes | 9 | 71 | 61 | 37 | 13 | 37 | ||||||||||||||||||

Interest income | (11 | ) | (11 | ) | (8 | ) | (5 | ) | (6 | ) | (9 | ) | ||||||||||||

Interest expense | 342 | 379 | 361 | 270 | 283 | 374 | ||||||||||||||||||

Depreciation and amortization | 332 | 281 | 263 | 197 | 188 | 254 | ||||||||||||||||||

EBITDA | $ | 456 | $ | 702 | $ | 720 | $ | 562 | $ | 577 | $ | 735 | ||||||||||||

| (5) | Adjusted EBITDA is a non-GAAP measurement that consists of EBITDA plus the sum of provision for asbestos, provision for restructuring, provision for asset impairments and loss/(gain) on sale of assets, loss/(gain) from early extinguishments of debt and translation and exchange adjustments. The reconciliation from EBITDA to Adjusted EBITDA is as follows: |

| (dollars in millions) | ||||||||||||||||||||||||

| Year Ended December 31, | Nine Months Ended September 30, | Twelve Ended 2005 | ||||||||||||||||||||||

| 2002 | 2003 | 2004 | 2004 | 2005 | ||||||||||||||||||||

EBITDA | $ | 456 | $ | 702 | $ | 720 | $ | 562 | $ | 577 | $ | 735 | ||||||||||||

Add/(deduct): | ||||||||||||||||||||||||

Provision for asbestos* | 30 | 44 | 35 | 35 | ||||||||||||||||||||

Provision for restructuring | 18 | 15 | 7 | 1 | 3 | 9 | ||||||||||||||||||

Provision for asset impairments and loss/(gain) on sale of assets | 247 | 76 | 47 | (22 | ) | 25 | ||||||||||||||||||

Loss/(gain) from early extinguishments of debt | (28 | ) | 12 | 39 | 37 | 2 | 4 | |||||||||||||||||

Translation and exchange adjustments | 26 | (207 | ) | (98 | ) | (7 | ) | 76 | (15 | ) | ||||||||||||||

Adjusted EBITDA | $ | 749 | $ | 642 | $ | 750 | $ | 593 | $ | 636 | $ | 793 | ||||||||||||

| * | Crown made asbestos-related payments of $114 million, $68 million, $41 million, $30 million and $18 million during 2002, 2003, 2004, the nine months ended September 30, 2004 and 2005, respectively. |

EBITDA and Adjusted EBITDA are provided for informational purposes only and should not be viewed as indicative of Crown’s actual or future results. EBITDA and Adjusted EBITDA information has been included in this offering memorandum because Crown believes that certain investors may use it as supplemental information to evaluate a company’s ability to service its indebtedness. EBITDA and Adjusted EBITDA do not represent and should not be considered as an alternative to net income, operating income, net cash provided by operating activities or any other measure for determining operating performance or liquidity that is calculated in accordance with generally accepted accounting principles. Furthermore, EBITDA and Adjusted EBITDA, as calculated by Crown, may not be comparable to calculations of similarly titled measures by other companies. For purposes of the covenants in the indenture governing the notes, EBITDA is defined differently.

| (6) | For purposes of computing the ratio of earnings to fixed charges, earnings consist of income before income taxes, equity in earnings of affiliates, minority interests and cumulative effect of accounting changes plus fixed charges (exclusive of interest capitalized during the period), amortization of interest previously capitalized and distributed income from less-than-50%-owned companies. Fixed charges include interest incurred, expensed and capitalized, amortization of debt issue costs and the portion of rental expense that is deemed representative of an interest factor. For purposes of the covenants in the indenture governing the notes, the ratio of earnings to fixed charges is defined differently. |

| (7) | Earnings did not cover fixed charges by $202 million for the year ended December 31, 2002. |

11

| (8) | Total secured debt consists of pro forma borrowings under the new term loan facility ($500 million) and revolving credit facility ($406 million), outstanding first priority notes ($553 million, based on U.S. dollar equivalents of euro as of September 30, 2005) and capitalized leases and other secured debt ($32 million). |

| (9) | The interest expense was calculated by adding $218 million of interest expense, defined as $210 million of pro forma net interest expense less $8 million of interest income, for the twelve months ended December 31, 2004, plus $169 million in interest expense, defined as pro forma net interest expense of $163 million less $6 million of interest income, for the nine months ended September 30, 2005 less $141 million in interest expense, defined as pro forma net interest expense of $136 million less $5 million in interest income for the nine months ended September 30, 2004. |

| (10) | Working capital consists of current assets less current liabilities. |

12

The following table sets forth the consolidated cash and cash equivalents and capitalization of Crown as of September 30, 2005, on an actual basis and the consolidated cash and cash equivalents and capitalization of Crown as of September 30, 2005 as adjusted to give effect to the 2005 refinancing plan, the sale of Crown’s plastic closures business and the application of the net proceeds therefrom. Crown’s historical financial results and related financial information reflect the reclassification to discontinued operations of amounts related to Crown’s plastic closures business that was sold in October 2005.

| (dollars in millions) | ||||||

| September 30, 2005 | ||||||

| Actual | As Adjusted | |||||

Cash and cash equivalents (1) | $ | 275 | $ | 500 | ||

Debt: | ||||||

Existing credit facilities | $ | 10 | — | |||

New credit facilities: | ||||||

Revolving credit facilities | — | 406 | ||||

Term loan facilities | — | 500 | ||||

6.25% First priority notes | 553 | 553 | ||||

9 1/2% Second priority notes (2) | 1,085 | — | ||||

10 1/4% Second priority notes (2) | 343 | — | ||||

10 7/8% Third priority notes (2) | 725 | — | ||||

% senior notes due 2013 | — | 500 | ||||

% senior notes due 2015 | — | 600 | ||||

Outstanding unsecured notes: | ||||||

Notes due through 2006 | 157 | 157 | ||||

Notes due 2023 through 2096 | 700 | 700 | ||||

Capital lease obligations and other secured debt | 32 | 32 | ||||

Other unsecured indebtedness (3) | 100 | 127 | ||||

Total debt | $ | 3,705 | $ | 3,575 | ||

Minority interests | 236 | 236 | ||||

Shareholders’ equity (4) | 207 | (190) | ||||

Total capitalization | $ | 4,148 | $ | 3,621 | ||

| (1) | The as adjusted cash and cash equivalents have increased by $225 million to reflect the receipt of the $690 million of proceeds from the sale of Crown’s plastic closures business, less (a) the cash used to pay the assumed tender offer premium of $283 million, less (b) $25 million in estimated fees and expenses paid in connection with the 2005 refinancing plan, less (c) $157 million of cash used for the repayment of outstanding indebtedness. In the fourth quarter of 2005 the Company expects to contribute approximately $260 million (including $200 million contributed in October 2005) to its pension plans to complete its expected $420 million aggregate contribution during 2005. Holders of repurchased second and third priority notes will also receive payment from Crown for accrued but unpaid interest to the date of the repayment, which Crown estimates to be approximately $45 million (assuming a repayment date of November 18, 2005). |

| (2) | Crown has commenced tender offers for any and all outstanding secured second and third priority notes as part of the refinancing. To the extent that any of such notes remain outstanding after consummation of the refinancing and sale of the new notes, the amount of adjusted indebtedness associated with such notes would increase and Crown intends to reduce initial borrowings under the new senior secured revolving credit facilities. |

| (3) | The as adjusted other unsecured indebtedness reflects the write off of $27 million of unamortized interest rate swap termination costs. |

| (4) | As adjusted, shareholders’ equity has been decreased by $397 million to reflect the write off of (a) $283 million premium paid, plus (b) $84 million of unamortized debt issuances fees, plus (c) $27 million of unamortized interest rate swap termination costs, plus (d) $3 million of estimated fees and expenses paid in connection with the tender offers. |

13

UNAUDITED PRO FORMA CONSOLIDATED CONDENSED FINANCIAL INFORMATION

The following unaudited pro forma consolidated condensed financial statements are presented to illustrate the effects of the 2005 refinancing plan and the sale of Crown’s plastic closures business on the historical financial position and results of operations of Crown. Historical amounts for the year ended December 31, 2004 are derived from Crown’s audited 2004 consolidated financial statements. Historical amounts as of and for the nine months ended September 30, 2005 and September 30, 2004 are derived from Crown’s unaudited consolidated financial statements.

The statements reflect adjustments for the completion of Crown’s 2005 refinancing plan and the sale of Crown’s plastic closures business. The pro forma adjustments are based upon available information and certain assumptions that Crown believes are reasonable under the circumstances. These adjustments are more fully described in the notes to the pro forma consolidated condensed financial statements below.

The unaudited pro forma consolidated condensed balance sheet at September 30, 2005 assumes that the 2005 refinancing plan and the sale of the plastic closures business took place on that date. The unaudited pro forma consolidated condensed statement of operations for the year ended December 31, 2004 and the nine months ended September 30, 2004 assumes that the 2005 refinancing plan and the sale of the plastic closures business took place on January 1, 2004, the beginning of Crown’s 2004 fiscal year. The unaudited pro forma consolidated condensed statement of operations for the nine months ended September 30, 2005 assumes that the 2005 refinancing plan and the sale of the plastic closures business took place on January 1, 2005, the beginning of Crown’s 2005 fiscal year. Such information is not necessarily indicative of the financial position or results of operations of Crown that would have occurred if the 2005 refinancing plan and the sale of the plastic closures business had been consummated as of the dates indicated, nor should it be construed as being a representation of the future financial position or results of operations of Crown.

The unaudited pro forma consolidated condensed financial statements of Crown should be read in conjunction with Crown’s consolidated financial statements, the related notes and the other financial information.

Crown cannot assure you that Crown’s 2005 refinancing plan will be consummated as described herein.

14

Unaudited Pro Forma Consolidated Condensed Balance Sheet

As of September 30, 2005

(in millions)

| Historical Amounts | Disposition Adjustments (1) | Pro Forma for Disposition | Refinancing/ Other Adjustments | Pro Forma for Refinancing | ||||||||||||||

Assets | ||||||||||||||||||

Current assets | ||||||||||||||||||

Cash & cash equivalents | $ | 275 | $ | 690 | $ | 965 | $ | (465 | )(2) | $ | 500 | |||||||

Receivables | 944 | 944 | 944 | |||||||||||||||

Inventories | 856 | 856 | 856 | |||||||||||||||

Prepaid expenses and other current assets | 76 | 76 | 76 | |||||||||||||||

Assets held for sale | 890 | (890 | ) | — | 0 | |||||||||||||

Total current assets | 3,041 | (200 | ) | 2,841 | (465 | ) | 2,376 | |||||||||||

Goodwill, net of amortization | 2,038 | 2,038 | 2,038 | |||||||||||||||

Property, plant and equipment | 1,636 | 1,636 | 1,636 | |||||||||||||||

Other non-current assets | 1,013 | 1,013 | (62 | )(3) | 951 | |||||||||||||

Total assets | $ | 7,728 | $ | (200 | ) | $ | 7,528 | $ | (527 | ) | $ | 7,001 | ||||||

Liabilities and Shareholders’ Equity | ||||||||||||||||||

Current Liabilities | ||||||||||||||||||

Short-term debt | $ | 63 | $ | 63 | $ | 5 | (4) | $ | 68 | |||||||||

Current maturities of long-term debt | 24 | 24 | 24 | |||||||||||||||

Accounts payable and accrued liabilities | 1,749 | 1,749 | 1,749 | |||||||||||||||

Income taxes payable | 46 | 46 | 46 | |||||||||||||||

Liabilities held for sale | 200 | $ | (200 | ) | — | 0 | ||||||||||||

Total current liabilities | 2,082 | (200 | ) | 1,882 | 5 | 1,887 | ||||||||||||

Long-term debt, excluding current maturities | 3,618 | 3,618 | (135 | )(5) | 3,483 | |||||||||||||

Post-retirement and pension liabilities | 971 | 971 | 971 | |||||||||||||||

Other non-current liabilities | 614 | 614 | 614 | |||||||||||||||

Minority interests | 236 | 236 | 236 | |||||||||||||||

Shareholders’ equity | 207 | 207 | (397 | )(6) | (190 | ) | ||||||||||||

Total liabilities & shareholders’ equity | $ | 7,728 | $ | (200 | ) | $ | 7,528 | $ | (527 | ) | $ | 7,001 | ||||||

15

Unaudited Pro Forma Consolidated Condensed Statement of Operations

for the Year Ended December 31, 2004

(in millions)

| Historical Amounts | Refinancing Adjustments | Pro Forma for Refinancing | ||||||||||

Net Sales | $ | 6,531 | $ | 6,531 | ||||||||

Cost of products sold (excluding depreciation and amortization) | 5,463 | 5,463 | ||||||||||

Depreciation and amortization | 263 | 263 | ||||||||||

Selling and administrative expense | 318 | 318 | ||||||||||

Provision for asbestos | 35 | 35 | ||||||||||

Provision for restructuring | 7 | 7 | ||||||||||

Provision for asset impairments and loss/gain on sale of assets | 47 | 47 | ||||||||||

Loss/(gain) on early extinguishment of debt | 39 | $ | 410 | (7) | 449 | |||||||

Interest expense, net of interest income | 353 | (143 | )(9) | 210 | ||||||||

Translation and exchange adjustments | (98 | ) | (98 | ) | ||||||||

Income/(loss) from continuing operations before income taxes, minority interests andequity earnings | 104 | (267 | ) | (163 | ) | |||||||

Provision for income taxes | 61 | (9 | )(10) | 52 | ||||||||

Minority interests, net of equity earnings | (27 | ) | (27 | ) | ||||||||

Income from continuing operations | $ | 16 | $ | (258 | ) | $ | (242 | ) | ||||

16

Unaudited Pro Forma Consolidated Condensed Statement of Operations

for the Nine Months Ended September 30, 2005

(in millions)

| Historical Amounts | Total Refinancing Adjustments | Pro Forma for Refinancing | ||||||||||

Net Sales | $ | 5,279 | $ | 5,279 | ||||||||

Cost of products sold (excluding depreciation and amortization) | 4,381 | 4,381 | ||||||||||

Depreciation and amortization | 188 | 188 | ||||||||||

Selling and administrative expense | 262 | 262 | ||||||||||

Provision for restructuring | 3 | 3 | ||||||||||

Provision for asset impairments and loss/gain on sale of assets | (22 | ) | (22 | ) | ||||||||

Loss/(gain) on early extinguishment of debt | 2 | $ | 397 | (6) | 399 | |||||||

Interest expense, net of interest income | 277 | (114 | )(9) | 163 | ||||||||

Translation and exchange adjustments | 76 | 76 | ||||||||||

Income/(loss) from continuing operations before income taxes, minority interests andequity earnings | 112 | (283 | ) | (171 | ) | |||||||

Provision for income taxes | 13 | 13 | ||||||||||

Minority interests, net of equity earnings | (22 | ) | (22 | ) | ||||||||

Income from continuing operations | $ | 77 | $ | (283 | ) | $ | (206 | ) | ||||

17

Unaudited Pro Forma Consolidated Condensed Statement of Operations

for the Nine Months Ended September 30, 2004

(in millions)

| Historical Amounts | Total Refinancing Adjustments | Pro Forma for Refinancing | ||||||||||

Net Sales | $ | 4,946 | $ | 4,946 | ||||||||

Cost of products sold (excluding depreciation and amortization) | 4,117 | 4,117 | ||||||||||

Depreciation and amortization | 197 | 197 | ||||||||||

Selling and administrative expense | 236 | 236 | ||||||||||

Provision for restructuring | 1 | 1 | ||||||||||

Provision for asset impairments and loss/gain on sale of assets | ||||||||||||

Loss/(gain) on early extinguishment of debt | 37 | $ | 406 | (8) | 443 | |||||||

Interest expense, net of interest income | 265 | (129 | )(9) | 136 | ||||||||

Translation and exchange adjustments | (7 | ) | (7 | ) | ||||||||

Income/(loss) from continuing operations before income taxes, minority interests andequity earnings | 100 | (277 | ) | (177 | ) | |||||||

Provision for income taxes | 37 | (9 | )(10) | 28 | ||||||||

Minority interests, net of equity earnings | (18 | ) | (18 | ) | ||||||||

Income from continuing operations | $ | 45 | $ | (268 | ) | $ | (223 | ) | ||||

18

| (1) | Reflects the net proceeds of $690 million from the sale of Crown’s plastic closures business and the removal of the asset and liabilities held for sale. |

| (2) | Reflects (a) the cash used to pay the tender offer premium of $283 million (assuming repurchase of all outstanding second and third priority notes and a bid side yield of the 3.375% U.S. Treasury Note due February 28, 2007 of 4.430%, a bid side yield of the 4.0% OBL #139 due February 16, 2007 of 2.585%, and a bid side yield of the 3.375% U.S. Treasury Note due February 15, 2008 of 4.502%), (b) $22 million in estimated fees and expenses paid in connection with the refinancing, (c) $157 million of cash used for the repayment of outstanding indebtedness, (d) $3 million of estimated fees and expenses paid in connection with the tender offers. |

| (3) | Reflects $22 million of estimated fees and expenses to be paid in connection with the 2005 refinancing plan which will be amortized over the life of the notes and Crown’s new credit facilities, less the write off of $84 million of unamortized debt issuances fees on indebtedness to be repaid in connection with the 2005 refinancing plan. |

| (4) | Reflects $5 million of the current portion of the new term loan. |

| (5) | Reflects the repayment of $157 million of outstanding indebtedness, plus the write off of $27 million of unamortized interest rate swap termination costs and $5 million reclassification of the current portion of the new term loan. |

| (6) | Reflects the write off of (a) $283 million tender offer premium to be paid, (b) $84 million of unamortized debt issuances fees, (c) $27 million of unamortized interest rate swap termination costs, plus (d) $3 million of estimated fees and expenses to be paid in connection with the tender offers. |

| (7) | Reflects the write off of (a) $283 million tender offer premium to be paid, (b) $99 million of unamortized debt issuances fees, (c) $25 million to retire outstanding interest rate swap, and (d) $3 million of estimated fees and expenses to be paid in connection with the tender offers. |

| (8) | Reflects the write off of (a) $283 million premium to be paid, plus (b) $96 million of unamortized debt issuances fees, plus (c) $24 million to retire outstanding interest rate swap and (d) $3 million of estimated fees and expenses paid in connection with the tender offers. |

| (9) | Reflects the interest expense impact based on the following assumptions: |

| • | Crown borrows $250 million under the term loan facility at LIBOR plus 150 basis points. The assumed rate is 6.0%. |

| • | Crown borrows $250 million U.S. dollar euro equivalent under term loan facility at EURIBOR plus 150 basis points. The rate is assumed to be 3.9%. |

| • | Crown issues $600 million of senior notes due , 2015 at an assumed interest rate of 7.25%. |

| • | Crown issues $500 million of senior notes due , 2013 at an assumed interest rate of 7.125%. |

| • | Crown European Holdings enters into an $800 million cross-currency swap of interest and principal to hedge its U.S. dollar loan with Crown Americas. The hedge yields an interest savings of 1.83%. |

| • | Crown enters into an $800 million revolving credit facility which consist of a U.S. Facility of $410 million and a $40 million Canadian facility at LIBOR plus 150 basis points and a $350 million multicurrency facility at EURIBOR plus 150 basis points. The interest rate is assumed to be 6.0% on the U.S. and Canadian facilities on the average outstanding balances of $262 million and $270 million for the nine month periods ended September 30, 2005 and September 30, 2004, respectively, and $192 million for the twelve months ended December 31, 2004. The interest rate is assumed to be 3.9% on the multicurrency facility on the average outstanding balances of $262 million and $270 million for the nine month periods ended September 30, 2005 and September 30, 2004, respectively, and $192 million for the twelve months ended December 31, 2004. |

| • | Crown pays a commitment fee of 37.5 basis points commitment fee on the undrawn portion of the $800 million proposed new revolving credit facility of $1 million for the nine months ended September 30, 2005 and September 30, 2004, respectively, and $2 million for the twelve months ended December 31, 2004. |

19

| • | Crown pays a 150 basis point fee on $80 million, $82 million and $81 million of average outstanding letters of credit for the periods ended September 30, 2005, September 30, 2004 and December 31, 2004, respectively. |

| • | The reversal of $6 million, $9 million and $10 million in historical interest expense on borrowings under Crown’s existing credit facility at a weighted average interest rate of 6.6%, 5.9% and 5.9% for the periods ended September 30, 2005, September 30, 2004 and December 31, 2004, respectively. |

| • | The reversal of $11 million, $14 million and $19 million in historical amortization of debt issuance fees on indebtedness paid in connection with the refinancing for the nine and twelve month periods ended September 30, 2005, September 30, 2004 and December 31, 2004, respectively. |

| • | The reversal of the historical commitment and letter of credit fees of $2 million, $2 million and $3 million for the nine and twelve month periods ended September 30, 2005 and December 31, 2004, respectively. |

| • | The amortization of $2 million, $2 million and $3 million in estimated fees to be paid in connection with the 2005 refinancing plan during the periods ended September 30, 2005, September 30, 2004 and December 31, 2004, respectively. |

| • | The reversal of the historical interest expense of $164 million, $163 million and $218 million for the nine and twelve month periods ended September 30, 2005, September 30, 2004 and December 31, 2004, respectively. These adjustments assume all of the outstanding $1,085 million9 1/2% second priority notes, $725 million of10 7/8% third priority notes and €285 million ($343 million U.S. dollar equivalent) 10 1/4% second priority notes are repaid in full. |

| A 0.5% movement in LIBOR would change annual interest expense on $1.0 billion of average outstanding variable debt by $5 million as of December 31, 2004. |

| (10) | Reflects the tax benefit associated with lower interest that will be recognized outside the United States. |

20

Risks Related to Crown’s Business

Pending and future asbestos litigation and payments to settle asbestos-related claims could reduce Crown Cork’s cash flow and negatively impact Crown Cork’s financial condition.

Crown Cork is one of many defendants in a substantial number of lawsuits filed throughout the United States by persons alleging bodily injury as a result of exposure to asbestos. In 1963, Crown Cork acquired a subsidiary that had two operating businesses, one of which is alleged to have manufactured asbestos-containing insulation products. Crown Cork believes that the business ceased manufacturing such products in 1963.

Crown Cork recorded pre-tax charges of $51 million, $30 million, $44 million and $35 million to increase its accrual for asbestos-related liabilities in 2001, 2002, 2003 and 2004 respectively. As of September 30, 2005, Crown Cork’s accrual for pending and future asbestos-related claims was $215 million and Crown Cork estimates that its range of potential liability for pending and future asbestos claims that are probable and estimable is between $215 million and $333 million. Crown Cork’s accrual includes estimates for probable costs for claims through the year 2014. The upper end of Crown Cork’s estimated range of possible asbestos costs of $333 million includes claims beyond that date. Assumptions underlying the accrual and the range of potential liability include that claims for exposure to asbestos that occurred after the sale of the subsidiary’s insulation business in 1964 would not be entitled to settlement payouts and that the Texas, Florida, Pennsylvania, Mississippi and Ohio asbestos legislation described in Crown’s consolidated financial statements are expected to have a highly favorable impact on Crown Cork’s ability to settle or defend against asbestos-related claims in those states, and other states where Pennsylvania law may apply.

Crown Cork made cash payments of $114 million, $68 million, $41 million and $18 million in 2002, 2003, 2004, and the first nine months of 2005, respectively, for asbestos-related claims and it expects to make additional asbestos-related cash payments of approximately $12 million for the remainder of 2005, of which approximately $5 million will be for committed settlements. These payments have reduced and any such future payments will reduce the cash flow available to Crown Cork for its business operations and debt payments.

Asbestos-related pay-outs and defense costs may be significantly higher than those estimated by Crown Cork because the outcome of this type of litigation (and, therefore, Crown Cork’s reserve and range of potential liabilities) is subject to a number of assumptions and uncertainties, such as the number or size of asbestos-related claims or settlements, the number of financially viable responsible parties, the extent to which Texas, Florida, Ohio and Mississippi statutes relating to asbestos liability are upheld and/or applied by Texas, Florida, Ohio and Mississippi courts, respectively, the extent to which a Pennsylvania statute relating to asbestos liability is upheld and/or applied by courts in states other than Pennsylvania, Crown Cork’s ability to obtain resolution without payment of asbestos-related claims by persons alleging first exposure to asbestos after 1964, and the potential impact of any pending or future asbestos-related legislation, including potential U.S. federal legislation described

21

in Crown’s consolidated financial statements. Accordingly, Crown Cork may be required to make payments for claims substantially in excess of its accrual and range of potential liability, which could reduce Crown’s cash flow and impair Crown’s ability to satisfy its obligations under the notes. As a result of the uncertainties regarding its asbestos-related liabilities and its reduced cash flow, the ability of Crown to raise new money in the capital markets is more difficult and more costly, and Crown may not be able to access the capital markets in the future. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Results of Operations—Provision for Asbestos,” “—Critical Accounting Policies,” “Crown’s Business—Legal Proceedings,” “Note K—Provision for Asbestos” to the 2004 Consolidated Financial Statements of Crown Holdings, Inc. and “Note K—Asbestos-Related Liabilities” to the Unaudited Consolidated Financial Statements of Crown Holdings, Inc.

Crown has significant pension plan obligations worldwide and significant underfunded U.S. post-retirement obligations, which could decrease cash available to satisfy obligations under the notes.

Pension contributions and payments under Crown’s retiree medical plans may decrease cash available to pay Crown’s obligations under the notes. Crown sponsors various pension plans worldwide, with the largest funded plans in the UK, U.S. and Canada. In 2000, 2001, 2002, 2003 and 2004, Crown contributed $26 million, $118 million, $144 million, $122 million and $171 million, respectively, to these plans and currently anticipates its 2005 funding to be approximately $420 million (including $160 million contributed as of September 30, 2005, $200 million contributed in October 2005 and $60 million expected to be contributed in the remainder of 2005). Pension expense in 2005 is expected to decrease to approximately $85 million from $100 million in 2004, primarily due to higher plan assets. A 0.25% change in the expected rate of return would change 2005 pension expense by approximately $10 million. A 0.25% change in the discount rates would change 2005 pension expense by approximately $14 million.

Crown has significant current funding obligations for pension benefits. Crown contributed $125 million to its U.S. pension plan in 2004. Based on current assumptions, Crown’s minimum U.S. pension funding requirement in calendar year 2005 is $86 million. Crown intends to contribute approximately $321 million to its U.S. pension in 2005.

Crown’s U.S. pension plan is significantly underfunded, and its U.S. retiree medical plans are unfunded. As of December 31, 2004, Crown’s U.S. pension plan was underfunded on a termination basis by approximately $741 million. The Crown pension plan assets consist primarily of common stocks and fixed income securities. If the performance of investments in the plan does not meet Crown’s assumptions, the underfunding of the pension plan may increase and Crown may have to contribute additional funds to the pension plan. In addition, federal legislative proposals have been made that could, if enacted, require Crown to significantly increase its funding obligations to the plan and increase the premiums paid by Crown to the Pension Benefit Guaranty Corporation. The actual impact of this legislation would depend upon the requirements of the legislation if enacted, contributions to and distributions from the pension plan and the investment performance of the assets contributed to the pension plans. An increase in pension contributions could decrease Crown’s cash available to pay its outstanding obligations, including the notes. While its U.S. pension plan continues in effect, Crown continues to incur additional pension obligations.

The Crown pension plan is subject to the Employee Retirement Income Security Act of 1974, or ERISA. Under ERISA, the Pension Benefit Guaranty Corporation, or PBGC, has the authority to terminate an underfunded plan under certain circumstances. In the event its U.S. pension plan is terminated for any reason while the plan is underfunded, Crown will incur a liability to the PBGC that may be equal to the entire amount of the underfunding, and, under certain circumstances, the liability could be senior to the notes.

In addition, as of December 31, 2004, the unfunded “accumulated postretirement benefit obligation,” calculated in accordance with generally accepted accounting principles, for retiree medical benefits was approximately $685 million, based on assumptions set forth in Crown’s consolidated financial statements.

22

Crown could be liable for Constar’s pension obligations, which could decrease cash available to satisfy obligations under the notes.

Under certain circumstances, Crown may be liable for the pension obligations of Constar International Inc., Crown’s former subsidiary that engaged in an initial public offering in 2002, which could decrease Crown’s cash available to pay its outstanding obligations, including the notes. At the time of the Constar initial public offering, Constar assumed sponsorship of the Crown pension plan which covered all active and former hourly employees and certain former salaried employees of Constar. Such plan was underfunded by approximately $24 million when it was assumed by Constar. The Constar pension plan is subject to ERISA. Under ERISA, the PBGC has the authority to terminate an underfunded plan under certain circumstances. If the Constar pension plan is terminated within five years of the completion of the Constar initial public offering, the PBGC may bring a claim under ERISA to hold Crown liable for the Constar pension plan underfunding if it is determined that a principal purpose of the Constar initial public offering was to evade pension liability. Crown does not believe that is the case. The actual amount for which Crown may become liable in the future depends on the future funding status of the Constar pension plan. In any case, if this claim is brought against Crown in the future, it may be costly to defend and the claim may reduce Crown’s liquidity.

Crown has had net operating losses in the past and may not generate profits in the future.

Operating losses could limit Crown’s ability to service its debt and fund its operations. For the fiscal years ended December 31, 2001, 2002 and 2003, Crown had consolidated losses before cumulative effect of a change in accounting of approximately $976 million, $191 million and $32 million. Crown had net income of $51 million for the fiscal year ended December 31, 2004. For the nine months ended September 30, 2005, Crown had net income of $96 million. However, Crown may not generate net income in the future.

Crown’s principal markets are subject to overcapacity and intense competition, which could reduce Crown’s net sales and net income.

The worldwide food and beverage can markets have experienced limited growth in demand in recent years. Food and beverage cans are standardized products, allowing for relatively little differentiation among competitors. This led to overcapacity and price competition among food and beverage producers, as capacity growth outpaced the growth in demand for food and beverage cans. These market conditions reduced product prices, which contributed to declining revenue and net income and increasing debt balances that Crown experienced in the past. The North American food and beverage can market, in particular, is considered to be a mature market, characterized by slow growth and a sophisticated distribution system. Price-driven competition has increased as producers seek to capture more sales volumes in order to keep their plants operating at optimal levels and reduce unit costs.

Competitive pricing pressures, overcapacity, the failure to develop new product designs and technologies for products, as well as other factors could cause Crown to lose existing business or opportunities to generate new business and could result in decreased cash flow and net income.

Crown is subject to competition from substitute products, which could result in lower profits and reduced cash flows.

Crown is subject to substantial competition from producers of alternative packaging made from glass and plastic, particularly from producers of plastic food and beverage containers, whose market has grown substantially over the past several years. Crown’s sales depend heavily on the volumes of sales by Crown’s customers in the food and beverage markets. Changes in preferences for products and packaging by consumers of prepackaged food and beverage cans significantly influence Crown’s sales. Changes in packaging by Crown’s customers may require Crown to re-tool manufacturing operations, which could require material expenditures. In addition, a decrease in the costs of, or a further increase in consumer demand for, alternative packaging could result in lower profits and reduced cash flows for Crown.

23

Crown is subject to the effects of fluctuations in foreign exchange rates, which may reduce its net sales and cash flow.

Crown is exposed to fluctuations in foreign currencies as a significant portion of its consolidated net sales, and some of its costs, assets and liabilities, are denominated in currencies other than the U.S. dollar. For the fiscal years ended December 31, 2002, 2003 and 2004 and the nine months ended September 30, 2005, Crown derived approximately 61%, 68%, 69% and 70%, respectively, of its consolidated net sales from sales in foreign currencies. In its consolidated financial statements, Crown translates local currency financial results into U.S. dollars based on average exchange rates prevailing during a reporting period. During times of a strengthening U.S. dollar, its reported international revenue and earnings will be reduced because the local currency will translate into fewer U.S. dollars. Conversely, a weakening U.S. dollar will effectively increase the dollar-equivalent of Crown’s expenses and liabilities denominated in foreign currencies. In connection with the 2005 refinancing plan, Crown expects to enter into currency swaps to convert an aggregate of approximately $800 million into euros. Crown’s translation and exchange adjustments reduced reported income before tax by $26 million in 2002 and by $76 million in the first nine months of 2005, and increased reported income before tax by $207 million in 2003 and by $98 million in 2004. Although Crown may use currency exchange rate protection agreements from time to time to reduce its exposure to currency exchange rate fluctuations in some cases, it may not elect or have the ability to implement hedges or, if it does implement them, they may not achieve the desired effect. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Financial Position—Market Risk.”

Crown’s international operations are subject to various risks that may lead to decreases in its financial results.

The risks associated with operating in foreign countries may have a negative impact on Crown’s liquidity and net income. Crown’s international operations generated approximately 61%, 68%, 69% and 70% of its consolidated net sales in 2002, 2003 and 2004, and the first nine months of 2005, respectively. The business strategy of Crown includes continued expansion of international activities. However, Crown’s international operations are subject to various risks associated with operating in foreign countries, including:

| • | restrictive trade policies; |

| • | inconsistent product regulation or policy changes by foreign agencies or governments; |

| • | duties, taxes or government royalties, including the imposition or increase of withholding and other taxes on remittances and other payments by non-U.S. subsidiaries; |

| • | foreign exchange rate risks; |

| • | difficulty in collecting international accounts receivable and potentially longer payment cycles; |

| • | increased costs in maintaining international manufacturing and marketing efforts; |

| • | non-tariff barriers and higher duty rates; |

| • | difficulties in enforcement of contractual obligations and intellectual property rights; |

| • | exchange controls, such as those found in Thailand; |

| • | national and regional labor strikes; |

| • | political, social and economic instability; |

| • | taking of property by nationalization or expropriation without fair compensation; |

| • | imposition of limitations on conversions of foreign currencies into dollars or payment of dividends and other payments by non-U.S. subsidiaries; |

| • | hyperinflation and currency devaluation in certain foreign countries, including the countries of Eastern Europe and Turkey, where such currency devaluation could affect the amount of cash generated by operations in those countries and thereby affect Crown’s ability to service the notes; and |

| • | war, civil disturbance and acts of terrorism. |

24

In addition to the risks listed above, adverse economic conditions in Argentina and Brazil contributed to reduced sales in those jurisdictions from 2001 levels and a $25 million write down of Crown’s assets in Argentina in 2003. While the reduction in sales in Argentina and Brazil is not likely to have a material impact on noteholders, there can be no guarantee that a continued deterioration of economic conditions in those or other countries would not have a material impact.

Crown’s profits will decline if the price of raw materials or energy rises and it cannot increase the price of its products.

Crown uses various raw materials, such as aluminum and steel for metals packaging, and various types of resins, which are petrochemical derivatives, for plastics packaging in its manufacturing operations. Sufficient quantities of these raw materials may not be available in the future. Moreover, the prices of certain of these raw materials, such as aluminum, steel and resin, have historically been subject to volatility. In addition, the political situation in Iraq and other petroleum exporters, along with weather-related events in the United States may cause additional volatility in the price of petrochemicals. Supplier consolidations and recent government regulations provide additional uncertainty as to the level of prices at which Crown might be able to source raw materials in the future.

As a result of steel price increases, in 2005 Crown implemented significant price increases in all of its steel product categories. To date, the impact on Crown’s earnings has not been material as a result of the pass–through of increased costs to customers. However, there can be no assurance that Crown will be able to fully recover from its customers the impact of steel surcharges or price increases. In addition, if Crown is unable to purchase steel for a significant period of time, Crown’s steel–consuming operations would be disrupted. Crown is continuing to monitor this situation and the effect on its operations.

Crown may be subject to adverse price fluctuations and surcharges, including recent steel price increases discussed above, when purchasing raw materials and it may be unable to increase its prices to offset unexpected increases in raw material costs without suffering reductions in unit volume, revenue and operating income. If any of Crown’s principal suppliers were to increase their prices significantly, impose substantial surcharges or were unable to meet its requirements for raw materials, either or both of its revenues or profits would decline.

In addition, the manufacturing facilities of Crown are dependent, in varying degrees, upon the availability of processed energy, such as natural gas and electricity. Certain of these energy sources may become difficult or impossible to obtain on acceptable terms due to external factors, which could increase Crown’s costs or interrupt its business.

The loss of a major customer and/or customer consolidation could reduce Crown’s net sales and profitability.

Many of Crown’s largest customers have acquired companies with similar or complementary product lines. This consolidation has increased the concentration of Crown’s business with its largest customers. In many cases, such consolidation has been accompanied by pressure from customers for lower prices, reflecting the increase in the total volume of product purchased or the elimination of a price differential between the acquiring customer and the company acquired. Increased pricing pressures from Crown’s customers may reduce Crown’s net sales and net income.

The majority of Crown’s sales are to companies that have leading market positions in the sale of packaged food, beverages, aerosol and health and beauty products to consumers. Although no one customer accounted for more than 10% of its net sales in 2002, 2003, or 2004, the loss of any of its major customers could reduce Crown’s net sales and net income. A continued consolidation of Crown’s customers could exacerbate any such loss.

25

Crown’s business is seasonal and weather conditions could reduce Crown’s net sales.

Crown manufactures packaging primarily for the food and beverage can market. Its sales can be affected by weather conditions. Due principally to the seasonal nature of the soft drink, brewing, iced tea and other beverage industries, in which demand is stronger during the summer months, sales of Crown’s products have varied and are expected to vary by quarter. Shipments in the U.S. and Europe are typically greater in the second and third quarters of the year. Unseasonably cool weather can reduce consumer demand for certain beverages packaged in its containers. In addition, poor weather conditions that reduce crop yields of packaged foods can decrease customer demand for its food containers.

Crown is subject to costs and liabilities related to stringent environmental and health and safety standards.