Exhibit 99.1

InterOil’s value - creating transaction with Oil Search July 2016

– 2 – – 2 – Legal Notice and Forward - Looking Statements None of the securities anticipated to be issued pursuant to the Plan of Arrangement have been or will be registered under the United States Securities Act of 1933 , as amended (the "U . S . Securities Act"), or any state securities laws, and any securities issued in the Arrangement are anticipated to be issued in reliance upon available exemptions from such registration requirements pursuant to Section 3 (a)( 10 ) of the U . S . Securities Act and applicable exemptions under state securities laws . This document does not constitute an offer to sell or the solicitation of an offer to buy any securities . There can be no assurance that the Arrangement will occur . The proposed Arrangement is subject to certain approvals and the fulfilment of certain conditions, and there can be no assurance that any such approvals will be obtained and/or any such conditions will be met . Further details regarding the terms of the transaction are set out in the Arrangement Agreement and have been provided in a management information circular which is available under the profile of InterOil Corporation at www . sedar . com This presentation includes “forward - looking statements” . All statements, other than statements of historical facts, included in this document are forward - looking statements . These statements are based on the current belief of InterOil, as well as assumptions made by, and information currently available to InterOil . No assurances can be given however, that these events will occur . Actual results could differ, and the difference may be material and adverse to the combined company and its shareholders . Such statements are subject to a number of assumptions, risks and uncertainties, many of which are beyond the control of InterOil, which may cause actual results to differ materially from those implied or expressed by the forward looking statements . These include in particular information and statements relating to InterOil’s agreement with Oil Search and the ability to realize the anticipated benefits, Oil Search’s agreement with Total and the ability to realize the anticipated benefits, the ability to complete either of the two transactions, the outcome of any potential alternative transaction proposal, either on the anticipated timeline or at all, the ability to obtain required regulatory and court approvals for the transactions , the combined company's expected growth profile, the anticipated market capitalization of the combined company, the need to integrate the two companies and related costs, business disruptions relating from the transactions, the outcome of any legal proceeding relating to the transactions, the combined company becoming a leading exploration and production champion for Papua New Guinea, the profitability of the combined company, information or statements relating to resources, hydrocarbon volumes, well test results, the estimated timing of the LNG project, the timing and quantum of the certification payment, the costs and break - even prices and potential revenues of the LNG project, the estimated drilling times of the exploration or appraisal wells and estimated 2016 budgets and expenditures, the absence of an established market for natural gas or gas condensate in Papua New Guinea and the ability to extract and sell commercially any natural gas or gas condensate, oil and gas prices, changes in market demand for oil and gas, currency fluctuations, drilling results, field performance, the timing of well work - overs and field development, reserves depletion, fiscal and other governmental issues and approvals, and the other risk factors discussed in InterOil’s publicly available filings, including but not limited to those in InterOIl’s management information circular, InterOil’s annual report for the year ended December 31 , 2015 on Form 40 - F and its Annual Information Form for the year ended December 31 , 2015 , as well as the risk that Oil Search and Total do not enter into definitive agreements relating to the MOU between such parties . InterOil disclaims any intention or obligation to update or revise any forward - looking statements, whether as a result of new information, future events or otherwise, except as expressly required by applicable laws .

– 3 – – 3 – Reference is made in this presentation to contingent resources It should be noted that InterOil has no production or reserves or future net revenue as defined in National Instrument 51 - 101 – Standards of Disclosure for Oil and Gas Activities (“NI 51 - 101 ”) or under definitions established by the SEC . Trillion cubic feet equivalent ( Tcfe ) may be misleading, particularly if used in isolation . A Tcfe conversion ratio of one barrel of oil to six thousand cubic feet of gas is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead . Well test results should be considered as preliminary and not necessarily indicative of long - term performance or of ultimate recovery . Well log interpretations indicating gas accumulations are not necessarily indicative of future production or ultimate recovery . Estimates of InterOil’s Contingent Resources are based on the independent evaluation by GLJ of Contingent Resources for the Elk - Antelope and Triceratops fields as of December 31 , 2015 (“GLJ Elk - Antelope and Triceratops Report”) and the independent evaluation by RISC of Contingent Resources for the Raptor and Bobcat discoveries as of December 31 , 2015 (“RISC Raptor and Bobcat Report”), which have each been prepared in accordance with the COGE Handbook . All of InterOil’s Contingent Resources have been classified as conventional natural gas and natural gas liquids . Contingent Resources are those quantities of natural gas and condensate estimated, as of a given date, to be potentially recoverable from known accumulations using established technology or technology under development, but which are not currently considered to be commercially recoverable due to one or more contingencies . The economic status of the resources is undetermined and there is uncertainty that it will be commercially viable to produce any portion of the resources . It should be noted that it is not certain that all fields / accumulations set out above will progress to reserves . The following classification of Contingent Resources are used in this presentation : • Low Estimate (or 1 C) means there is at least a 90 percent probability (P 90 ) that the quantities actually recovered will equal or exceed the low estimate . • Best Estimate (or 2 C) means there is at least a 50 percent probability (P 50 ) that the quantities actually recovered will equal or exceed the best estimate . • High Estimate (or 3 C) means there is at least a 10 percent probability (P 10 ) that the quantities actually recovered will equal or exceed the high estimate . The estimates of Contingent Resources provided in this presentation are estimates only and there is no guarantee that the estimated Contingent Resources will be recovered . Actual Contingent Resources may be greater than or less than the estimates provided in this in this presentation and the differences may be material . There is no assurance that the forecast price and cost assumptions applied by GLJ and RISC in evaluating InterOil’s Contingent Resources will be attained and variances could be material . There is also uncertainty that it will be commercially viable to produce any part of the Contingent Resources . For a discussion of the Contingent Resources project evaluation scenario, economics status and maturity subclass as well as the change, timing and development of Contingent Resources evaluated pursuant to the GLJ Elk - Antelope and Triceratops Report and the RISC Raptor and Bobcat Report, see Schedule A to InterOil’s Annual Information Form for the year ended December 31 , 2015 which is available on www . interoil . com or from the SEC at www . sec . gov or on SEDAR at www . sedar . com . Accuracy of resource estimates The accuracy of resource estimates is in part a function of the quality and quantity of available data and of engineering and geological interpretation and judgment . Other factors in the classification as a resource include a requirement for more appraisal wells, detailed design estimates and near - term development plans . The size of the resource estimate could be positively impacted, potentially in a material amount, if additional appraisal wells or seismic determine that the aerial extent, reservoir quality and/or the thickness of the reservoir is larger than what is currently estimated based on the interpretation of the seismic and/or well data . The size of the resource estimate could be negatively impacted, potentially in a material amount, if additional appraisal wells or seismic determine that the aerial extent, reservoir quality and/or the thickness of the reservoir are less than what is currently estimated based on the interpretation of the seismic and/or well data . Disclaimer of oil and gas information

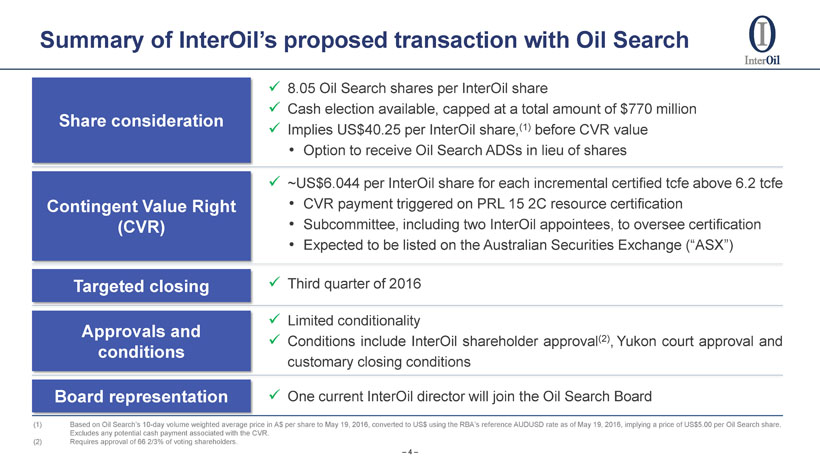

– 4 – – 4 – Summary of InterOil’s proposed transaction with Oil Search (1) Based on Oil Search’s 10 - day volume weighted average price in A$ per share to May 19, 2016, converted to US$ using the RBA’s ref erence AUDUSD rate as of May 19, 2016, implying a price of US$5.00 per Oil Search share . Excludes any potential cash payment associated with the CVR. (2) Requires approval of 66 2/3% of voting shareholders. x 8 . 05 Oil Search shares per InterOil share x Cash election available, capped at a total amount of $ 770 million x Implies US $ 40 . 25 per InterOil share, ( 1 ) before CVR value • Option to receive Oil Search ADSs in lieu of shares Share consideration x ~ US $ 6 . 044 per InterOil share for each incremental certified tcfe above 6 . 2 tcfe • CVR payment triggered on PRL 15 2 C resource certification • Subcommittee, including two InterOil appointees, to oversee certification • Expected to be listed on the Australian Securities Exchange (“ASX”) Contingent Value Right (CVR) x Third quarter of 2016 Targeted closing x Limited conditionality x Conditions include InterOil shareholder approval ( 2 ) , Yukon court approval and customary closing conditions Approvals and conditions x One current InterOil director will join the Oil Search Board Board representation

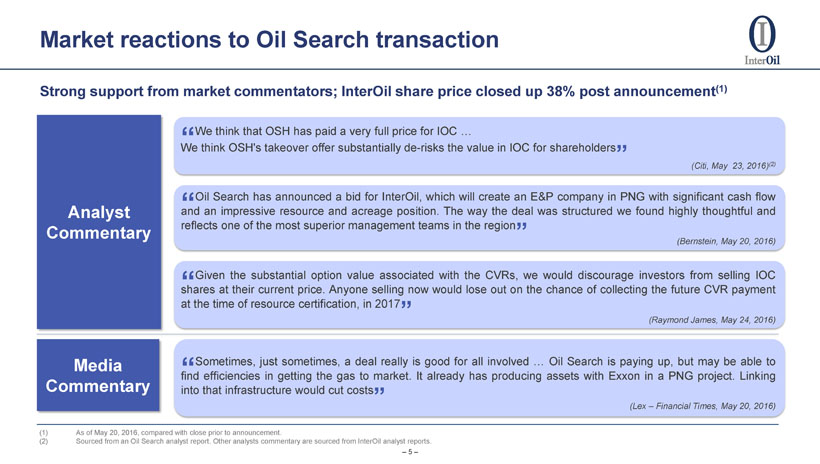

– 5 – – 5 – “ Oil Search has announced a bid for InterOil, which will create an E&P company in PNG with significant cash flow and an impressive resource and acreage position . The way the deal was structured we found highly thoughtful and reflects one of the most superior management teams in the region ” (Bernstein, May 20, 2016) Strong support from market commentators ; InterOil share price closed up 38 % post announcement ( 1 ) Analyst Commentary Media Commentary “ Sometimes, just sometimes, a deal really is good for all involved … Oil Search is paying up, but may be able to find efficiencies in getting the gas to market . It already has producing assets with Exxon in a PNG project . Linking into that infrastructure would cut costs ” (Lex – Financial Times, May 20, 2016) (1) As of May 20, 2016, compared with close prior to announcement. (2) Sourced from an Oil Search analyst report. Other analysts commentary are sourced from InterOil analyst reports. “ We think that OSH has paid a very full price for IOC … We think OSH's takeover offer substantially de - risks the value in IOC for shareholders ” ( Citi, May 23, 2016 ) (2) Market reactions to Oil Search transaction “ Given the substantial option value associated with the CVRs, we would discourage investors from selling IOC shares at their current price . Anyone selling now would lose out on the chance of collecting the future CVR payment at the time of resource certification, in 2017 ” (Raymond James, May 24, 2016)

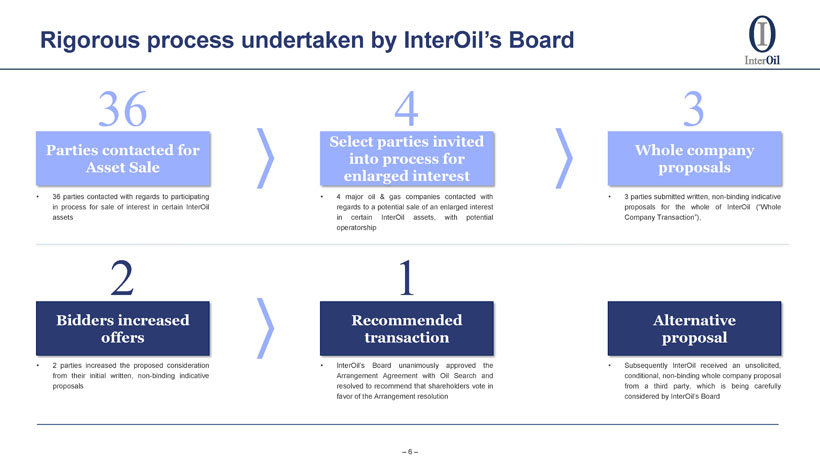

– 6 – – 6 – Parties contacted for Asset Sale 36 Select parties invited into process for enlarged interest 4 • 36 parties contacted with regards to participating in process for sale of interest in certain InterOil assets • 4 major oil & gas companies contacted with regards to a potential sale of an enlarged interest in certain InterOil assets, with potential operatorship Whole company proposals 3 • 3 parties submitted written, non - binding indicative proposals for the whole of InterOil (“Whole Company Transaction”), Bidders increased offers • 2 parties increased the proposed consideration from their initial written, non - binding indicative proposals Recommended transaction • InterOil’s Board unanimously approved the Arrangement Agreement with Oil Search and resolved to recommend that shareholders vote in favor of the Arrangement resolution Rigorous process undertaken by InterOil’s Board Alternative proposal 2 1 • Subsequently InterOil received an unsolicited, conditional, non - binding whole company proposal from a third party, which is being carefully considered by InterOil’s Board

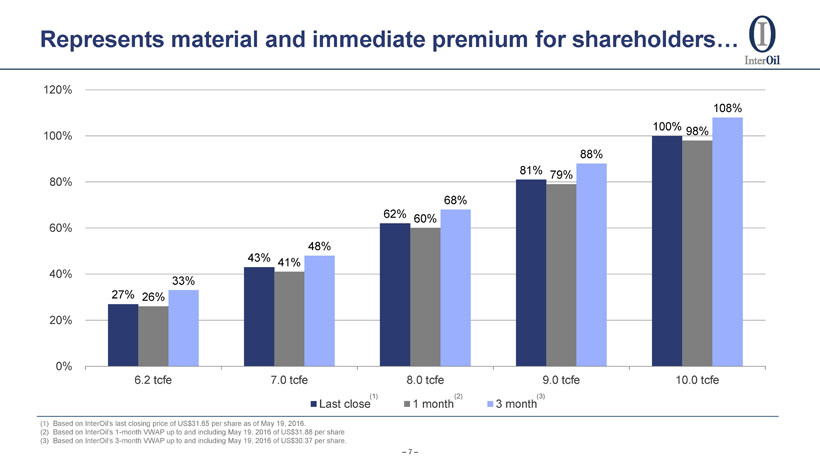

– 7 – – 7 – (1) Based on InterOil’s last closing price of US$31.65 per share as of May 19, 2016. (2) Based on InterOil’s 1 - month VWAP up to and including May 19, 2016 of US$31.88 per share (3) Based on InterOil’s 3 - month VWAP up to and including May 19, 2016 of US$30.37 per share. Represents material and immediate premium for shareholders… 27% 43% 62% 81% 100% 26% 41% 60% 79% 98% 33% 48% 68% 88% 108% 0% 20% 40% 60% 80% 100% 120% 6.2 tcfe 7.0 tcfe 8.0 tcfe 9.0 tcfe 10.0 tcfe Last close 1 month 3 month (1) (2) (3)

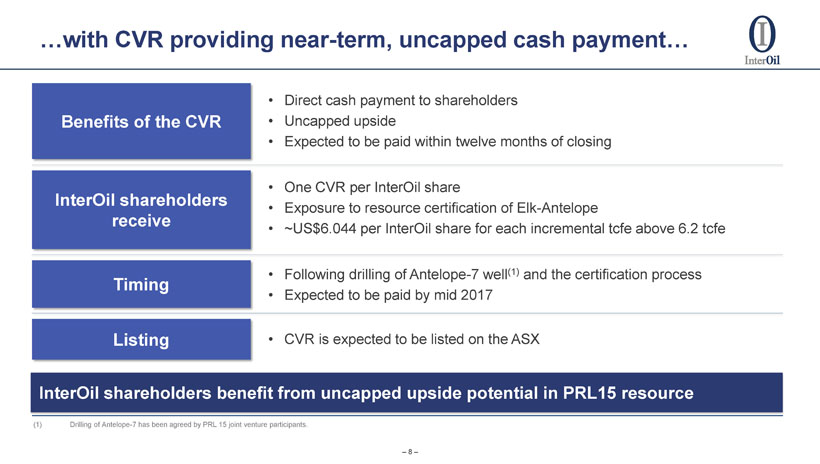

– 8 – – 8 – …with CVR providing near - term, uncapped cash payment… (1) Drilling of Antelope - 7 has been agreed by PRL 15 joint venture participants. • Direct cash payment to shareholders • Uncapped upside • Expected to be paid within twelve months of closing Benefits of the CVR • One CVR per InterOil share • Exposure to resource certification of Elk - Antelope • ~ US $ 6 . 044 per InterOil share for each incremental tcfe above 6 . 2 tcfe InterOil shareholders receive • Following drilling of Antelope - 7 well ( 1 ) and the certification process • Expected to be paid by mid 2017 Timing • CVR is expected to be listed on the ASX Listing InterOil shareholders benefit from uncapped upside potential in PRL15 resource

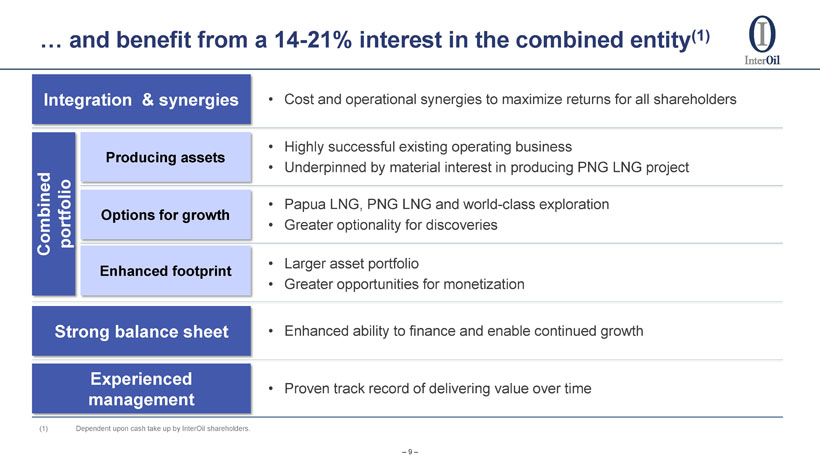

– 9 – – 9 – Producing assets • Highly successful existing operating business • Underpinned by material interest in producing PNG LNG project Options for growth • Papua LNG, PNG LNG and world - class exploration • Greater optionality for discoveries Integration & synergies • Cost and operational synergies to maximize returns for all shareholders Enhanced footprint • Larger asset portfolio • Greater opportunities for monetization Strong balance sheet • Enhanced ability to finance and enable continued growth Experienced management • Proven track record of delivering value over time Combined portfolio … and benefit from a 14 - 21% interest in the combined entity (1) (1) Dependent upon cash take up by InterOil shareholders.

– 10 – – 10 – Delivering compelling value for InterOil shareholders

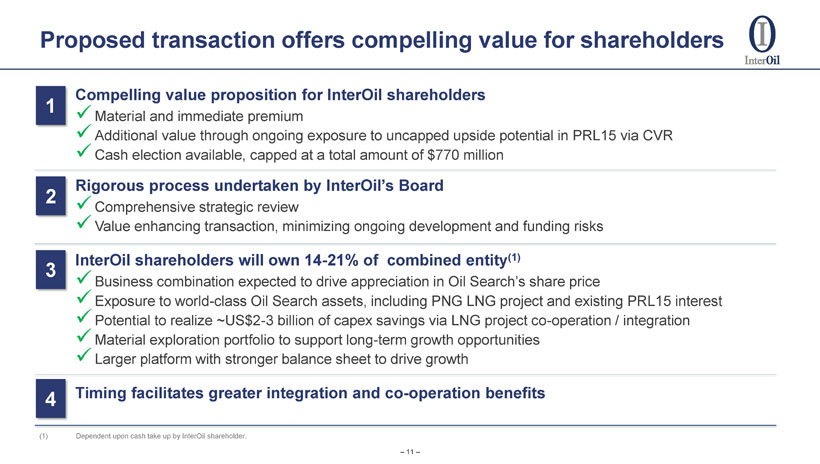

– 11 – – 11 – Compelling value proposition for InterOil shareholders x Material and immediate premium x Additional value through ongoing exposure to uncapped upside potential in PRL15 via CVR x Cash election available, capped at a total amount of $770 million 1 3 2 4 InterOil shareholders will own 14 - 21% of combined entity (1) x Business combination expected to drive appreciation in Oil Search’s share price x Exposure to world - class Oil Search assets, including PNG LNG project and existing PRL15 interest x Potential to realize ~US$2 - 3 billion of capex savings via LNG project co - operation / integration x Material exploration portfolio to support long - term growth opportunities x Larger platform with stronger balance sheet to drive growth Rigorous process undertaken by InterOil’s Board x Comprehensive strategic review x Value enhancing transaction, minimizing ongoing development and funding risks Timing facilitates greater integration and co - operation benefits Proposed transaction offers compelling value for shareholders (1) Dependent upon cash take up by InterOil shareholder.

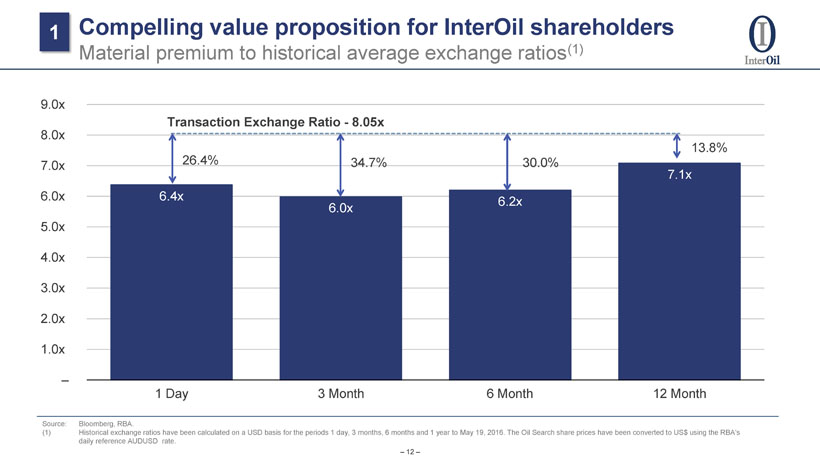

– 12 – – 12 – 6.4x 6.0x 6.2x 7.1x – 1.0x 2.0x 3.0x 4.0x 5.0x 6.0x 7.0x 8.0x 9.0x 1 Day 3 Months 6 Months 1 Year Transaction Exchange Ratio - 8.05x 26.4% 34.7% 30.0% 13.8% Compelling value proposition for InterOil shareholders Material premium to historical average exchange ratios (1) 1 Source: Bloomberg, RBA. (1) Historical exchange ratios have been calculated on a USD basis for the periods 1 day, 3 months, 6 months and 1 year to May 19, 2016. The Oil Search share prices have been converted to US$ using the RBA’s daily reference AUDUSD rate . 1 Day 3 Month 6 Month 12 Month

– 13 – – 13 – (US$ per share) 6.2 tcfe 7.0 tcfe 8.0 tcfe 9.0 tcfe 10.0 tcfe Share consideration (1) $40.25 $40.25 $40.25 $40.25 $40.25 CVR - Potential value (2) $0.00 $4.84 $10.88 $16.92 $22.97 Aggregate consideration p.s. $40.25 $45.09 $51.13 $57.17 $63.22 Premia: Premium to last close (3) 27% 43% 62% 81% 100% Premium to 1-month VWAP (4) 26% 41% 60% 79% 98% Premium to 3-month VWAP (5) 33% 48% 68% 88% 108% Uncapped upside: ~US$6.044 per InterOil share for each incremental Tcfe (3) Based on InterOil’s last closing price of US$31.65 per share as of May 19, 2016. ( 4) Based on InterOil’s 1 - month VWAP up to and including May 19, 2016 of US$31.88 per share. (5) Based on InterOil’s 3 - month VWAP up to and including May 19, 2016 of US$30.37 per share. (1) Based on Oil Search’s 10 - day volume weighted average price in AUD per share to May 19, 2016, converted daily to USD using the RBA’s reference AUDUSD rate, implying a price of US$5.00 per Oil Search share. Excluding any potential cash payment associated with the CVR. (2) Represents the estimated potential future payment at given certified resource level; not discounted to present value. Compelling value proposition for InterOil shareholders CVR provides on - going uncapped upside potential from PRL 15 1 • A certification process has been designed in order to protect InterOil shareholders ' interests in the CVR

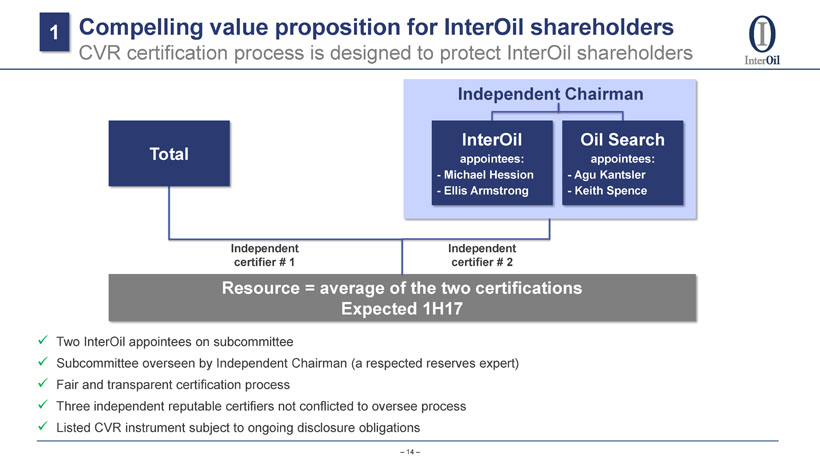

– 14 – – 14 – x Two InterOil appointees on subcommittee x Subcommittee overseen by Independent Chairman (a respected reserves expert) x Fair and transparent certification process x Three independent reputable certifiers not conflicted to oversee process x Listed CVR instrument subject to ongoing disclosure obligations InterOil appointees: - Michael Hession - Ellis Armstrong Oil Search appointees: - Agu Kantsler - Keith Spence Independent Chairman Resource = average of the two certifications Expected 1H17 Independent certifier # 1 Independent certifier # 2 Total Compelling value proposition for InterOil shareholders CVR certification process is designed to protect InterOil shareholders 1

– 15 – – 15 – Appointee Technical expertise? Biography Michael Hession (InterOil) x • Dr. Hession is a petroleum geophysicist with over 30 years’ experience in sub - surface, reserves development and LNG development • He began his career at BP in 1989 with his last position as Development Manager of the Chirag Azeri mega project, the first large - scale oil project in the Caspian Sea region • Dr Hession spent 12 - years with Woodside, where he held several high - profile roles related to the Browse LNG development and Pluto LNG mega project. Ellis Armstrong (InterOil) x • Dr. Armstrong is a former reservoir engineer with more than 30 years of international oil and gas experience with BP in the Caribbean and Latin America, Venezuela, Alaska and the North Sea • He held senior strategy, commercial and operational roles with BP and ran the company’s technology group, was the group’s Commercial Director, and was Chief Financial Officer for the group’s global exploration and production business Agu Kantsler (Oil Search) x • Dr Kantsler worked with Woodside Petroleum for 15 years, where he was Executive Vice President Exploration and New Ventures from 1995 to 2009 and Executive Vice President Health, Safety and Security • Before joining Woodside Petroleum, Dr Kantsler had extensive experience with the Shell Group of Companies working in various exploration roles in Australia and internationally Keith Spence (Oil Search) x • Mr Spence brings over thirty years of oil and gas experience to the Board, having served in senior executive positions with Woodside Petroleum Limited, including Chief Operating Officer and Acting Chief Executive • Mr Spence was with Shell for 18 years prior to Woodside Compelling value proposition for InterOil shareholders Highly experienced CVR Committee to oversee certification process 1

– 16 – – 16 – x Proposed Oil Search transaction result of a rigorous process by InterOil’s Board to identify value creating opportunities, and consistent with long - term strategy of monetising key assets x Larger number of parties contacted regarding potential sale of minority stake in certain assets x Multiple written, non - binding indicative proposals received for Whole Company Transactions Rigorous sale process x The Board of InterOil appointed an independent, highly experienced Transaction Committee to oversee the process x Comprised of independent InterOil Board members • Each committee member has > 30 years prior finance, M&A , oil & gas and governance experience Transaction Committee x InterOil has negotiated the right to nominate a current InterOil director to the Board of the combined entity Oil Search board representation x Resource certification process has been designed to protect the interests of InterOil shareholders x Two InterOil appointees on subcommittee x Subcommittee overseen by independent chairman (a respected reserves expert) x Three independent reputable certifiers not conflicted to oversee process Resource certification process 2 Rigorous process undertaken by InterOil’s Board Maximising shareholder value was key focus of the Board’s approach InterOil’s stated strategy is to Find – Enable – Develop, and the proposed transaction represents a continuation of this strategy

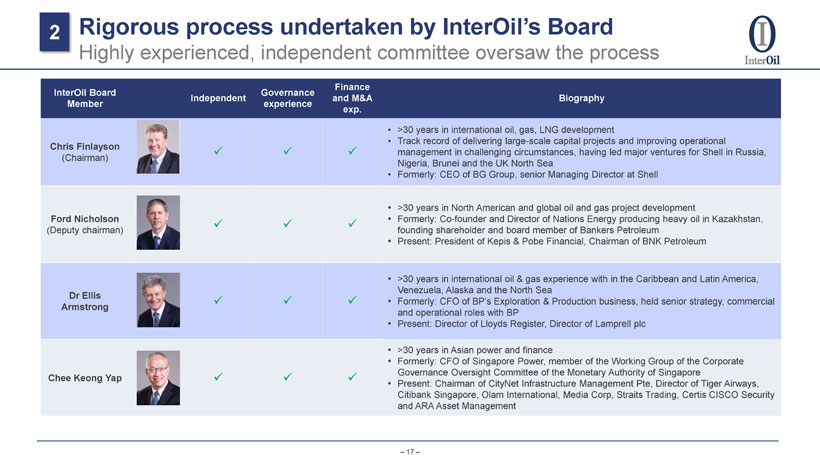

– 17 – – 17 – InterOil Board Member Independent Governance experience Finance and M&A exp. Biography Chris Finlayson (Chairman) x x x • >30 years in international oil, gas, LNG development • Track record of delivering large - scale capital projects and improving operational management in challenging circumstances, having led major ventures for Shell in Russia, Nigeria, Brunei and the UK North Sea • Formerly: CEO of BG Group, senior Managing Director at Shell Ford Nicholson (Deputy chairman) x x x • >30 years in North American and global oil and gas project development • Formerly: Co - founder and Director of Nations Energy producing heavy oil in Kazakhstan, founding shareholder and board member of Bankers Petroleum • Present: President of Kepis & Pobe Financial, Chairman of BNK Petroleum Dr Ellis Armstrong x x x • >30 years in international oil & gas experience with in the Caribbean and Latin America, Venezuela, Alaska and the North Sea • Formerly: CFO of BP’s Exploration & Production business, held senior strategy, commercial and operational roles with BP • Present: Director of Lloyds Register, Director of Lamprell plc Chee Keong Yap x x x • >30 years in Asian power and finance • Formerly: CFO of Singapore Power, member of the Working Group of the Corporate Governance Oversight Committee of the Monetary Authority of Singapore • Present: Chairman of CityNet Infrastructure Management Pte, Director of Tiger Airways, Citibank Singapore, Olam International, Media Corp, Straits Trading, Certis CISCO Security and ARA Asset Management 2 Rigorous process undertaken by InterOil’s Board Highly experienced, independent committee oversaw the process

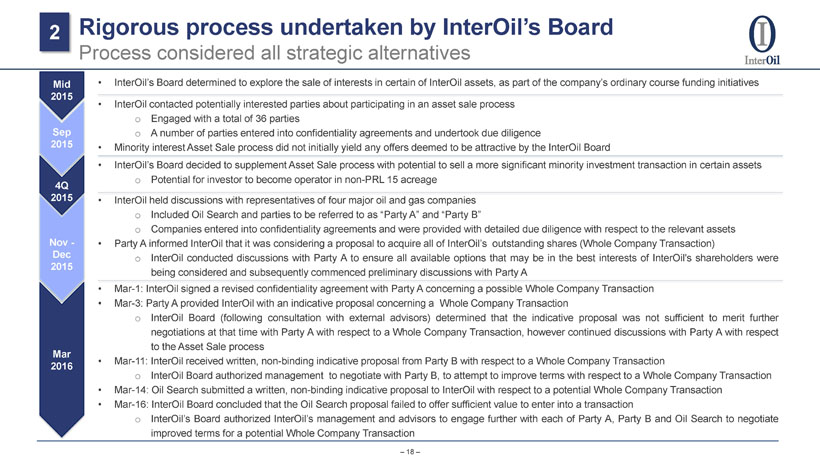

– 18 – – 18 – • InterOil’s Board determined to explore the sale of interests in certain of InterOil assets, as part of the company’s ordinary course funding initiatives Mid 2015 Sep 2015 4Q 2015 Nov - Dec 2015 • InterOil contacted potentially interested parties about participating in an asset sale process o Engaged with a total of 36 parties o A number of parties entered into confidentiality agreements and undertook due diligence • Minority interest Asset Sale process did not initially yield any offers deemed to be attractive by the InterOil Board • InterOil’s Board decided to supplement Asset Sale process with potential to sell a more significant minority investment transaction in certain assets o Potential for investor to become operator in non - PRL 15 acreage • InterOil held discussions with representatives of four major oil and gas companies o Included Oil Search and parties to be referred to as “Party A” and “Party B” o Companies entered into confidentiality agreements and were provided with detailed due diligence with respect to the relevant assets • Party A informed InterOil that it was considering a proposal to acquire all of InterOil’s outstanding shares (Whole Company Transaction) o InterOil conducted discussions with Party A to ensure all available options that may be in the best interests of InterOil's shareholders were being considered and subsequently commenced preliminary discussions with Party A Mar 2016 • Mar - 1 : InterOil signed a revised confidentiality agreement with Party A concerning a possible Whole Company Transaction • Mar - 3 : Party A provided InterOil with an indicative proposal concerning a Whole Company Transaction o InterOil Board ( following consultation with external advisors) determined that the indicative proposal was not sufficient to merit further negotiations at that time with Party A with respect to a Whole Company Transaction, however continued discussions with Party A with respect to the Asset Sale process • Mar - 11 : InterOil received written, non - binding indicative proposal from Party B with respect to a Whole Company Transaction o InterOil Board authorized management to negotiate with Party B, to attempt to improve terms with respect to a Whole Company Transaction • Mar - 14 : Oil Search submitted a written, non - binding indicative proposal to InterOil with respect to a potential Whole Company Transaction • Mar - 16 : InterOil Board concluded that the Oil Search proposal failed to offer sufficient value to enter into a transaction o InterOil’s Board authorized InterOil’s management and advisors to engage further with each of Party A, Party B and Oil Search to negotiate improved terms for a potential Whole Company Transaction 2 Rigorous process undertaken by InterOil’s Board Process considered all strategic alternatives

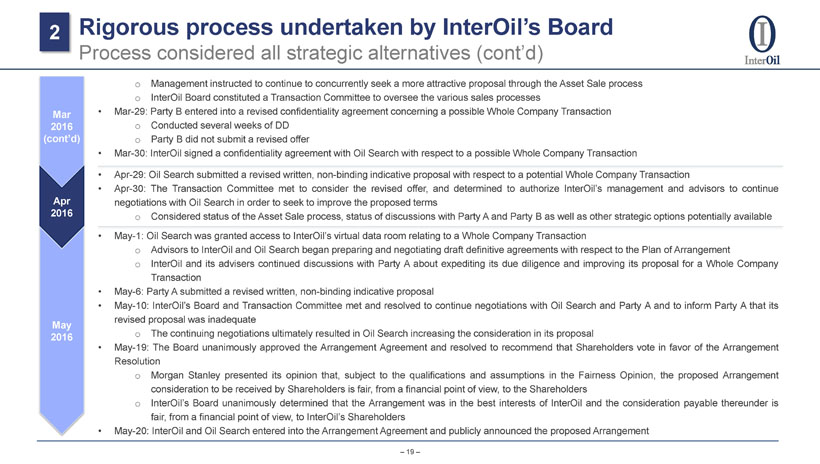

– 19 – – 19 – o Management instructed to continue to concurrently seek a more attractive proposal through the Asset Sale process o InterOil Board constituted a Transaction Committee to oversee the various sales processes • Mar - 29 : Party B entered into a revised confidentiality agreement concerning a possible Whole Company Transaction o Conducted several weeks of DD o Party B did not submit a revised offer • Mar - 30 : InterOil signed a confidentiality agreement with Oil Search with respect to a possible Whole Company Transaction Mar 2016 (cont’d) Apr 2016 May 2016 • Apr - 29 : Oil Search submitted a revised written, non - binding indicative proposal with respect to a potential Whole Company Transaction • Apr - 30 : The Transaction Committee met to consider the revised offer , and determined to authorize InterOil’s management and advisors to continue negotiations with Oil Search in order to seek to improve the proposed terms o Considered status of the Asset Sale process, status of discussions with Party A and Party B as well as other strategic options potentially available • May - 1 : Oil Search was granted access to InterOil’s virtual data room relating to a Whole Company Transaction o Advisors to InterOil and Oil Search began preparing and negotiating draft definitive agreements with respect to the Plan of Arrangement o InterOil and its advisers continued discussions with Party A about expediting its due diligence and improving its proposal for a Whole Company Transaction • May - 6 : Party A submitted a revised written, non - binding indicative proposal • May - 10 : InterOil’s Board and Transaction Committee met and resolved to continue negotiations with Oil Search and Party A and to inform Party A that its revised proposal was inadequate o The continuing negotiations ultimately resulted in Oil Search increasing the consideration in its proposal • May - 19 : T he Board unanimously approved the Arrangement Agreement and resolved to recommend that Shareholders vote in favor of the Arrangement Resolution o Morgan Stanley presented its opinion that, subject to the qualifications and assumptions in the Fairness Opinion, the proposed Arrangement consideration to be received by Shareholders is fair, from a financial point of view, to the Shareholders o InterOil’s Board unanimously determined that the Arrangement was in the best interests of InterOil and the consideration payable thereunder is fair, from a financial point of view, to InterOil’s Shareholders • May - 20 : InterOil and Oil Search entered into the Arrangement Agreement and publicly announced the proposed Arrangement 2 Rigorous process undertaken by InterOil’s Board Process considered all strategic alternatives (cont’d)

– 20 – – 20 – • Oil Search estimates potential capex savings of US $ 2 - 3 billion will be available from s haring facilities and infrastructure with PNG LNG ( 1 ) o Further significant cost savings are expected to be available through potential schedule acceleration and contingency ( 1 ) • Cooperation between Papua LNG and the PNG LNG expansion project may potentially deliver greater value for all stakeholders o RISC estimates cooperation in PNG could result in >US $ 5 billion in savings over next 20 years ( 2 ) o Next 12 - 18 months critical in pursuing development coordination ( 1 ) Base Cost Existing Contractor Rel. Contractor / Op Synergy Lessons Learned Execution experience Infrastructure Storage Marine facilities Accommodation Pipeline Corridors Access Roads Warehousing Shipping Channel Front end Pre - FID costs FEED Environmental Approvals & Surveys Liquids export Export System Improved Schedule Project PMT Improved Schedule Contractor Execution Plan Detailed Engineering Reduced Contingency Process Commissioning & Start Up Pre - treatment Sparing LNG, LPG and NGL Process Agreements pave the way for potential material capex and opex savings plus anticipated schedule acceleration of PRL 15 development InterOil shareholders will own 14 - 21% of combined entity (1) Potential to realize ~US$2 - 3bn of capex savings 3 (1) Dependent upon cash take up by InterOil shareholder (2) Oil Search Investor Presentation (June 15, 2016). (3) RISC Advisory, June 2016. Examples of potential cost savings

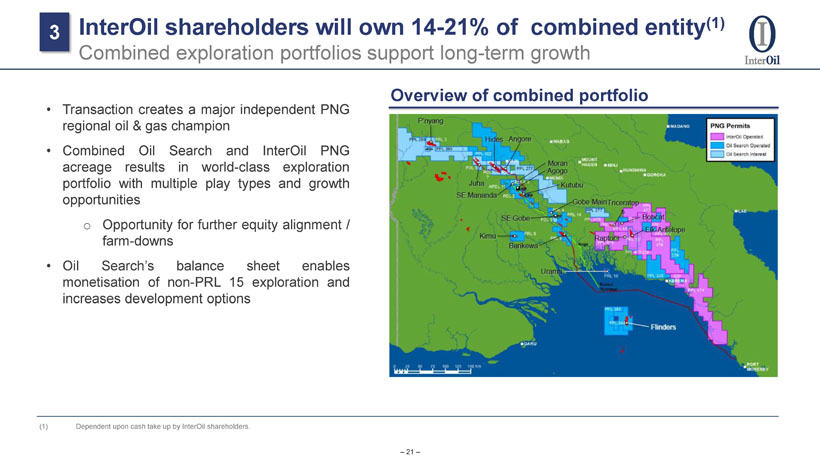

– 21 – – 21 – • Transaction creates a major independent PNG regional o il & gas champion • Combined Oil Search and InterOil PNG acreage results in world - class exploration portfolio with multiple play types and growth opportunities o Opportunity for further equity alignment / farm - downs • Oil Search’s balance sheet enables monetisation of non - PRL 15 exploration and increases development options InterOil shareholders will own 14 - 21% of combined entity (1) Combined exploration portfolios support long - term growth 3 Overview of combined portfolio (1) Dependent upon cash take up by InterOil shareholders.

– 22 – – 22 – • Balance sheet and liquidity able to support increased expenditure on development spend from higher interest in PRL 15 and larger exploration portfolio o Pro - forma net debt will decrease to ~US $ 3 . 0 billion post completion of sell down to Total, ~US $ 300 million lower than currently . ( 1 ) Receipt of Total bullet payments will improve position further o Pro - forma liquidity position of ~US $ 2 . 0 billion vs US $ 1 . 7 billion at March 31 , 2016 , including InterOil corporate debt ( 2 ) Strong balance sheet well positioned for growth Oil Search is generating positive cash - flow • Strong cash flows will help de - risk the development of PRL - 15 o Oil Search is generating positive cash flows, even at oil prices well below current levels o Cash flow breakeven ( opex plus interest) in 2016 forecast at ~US $ 19 / bbl and at low US $ 30 / bbl level after principal repayments and sustaining capex (1) Dependent upon cash take up by InterOil shareholders. (2) Pro - forma net debt based on InterOil and Oil Search net debt at March 31, 2016 and assumes Cash Alternative fully taken up by InterOil shareholders ; excludes transaction costs, pre any CVR payment, pre future fixed Total payments. InterOil shareholders will own 14 - 21% of combined entity (1) Larger platform with stronger balance sheet to drive growth 3

– 23 – – 23 – Mr RJ Lee Chairman Mr G Aopi Executive Director Executive General Manager: Stakeholder Engagement Mr PR Botten Managing Director Sir KG Constantinou Independent Director Dr EJ Doyle Independent Director Dr AJ Kantsler Independent Director Mr B Philemon Independent Director Mr KW Spenc e Independent Director Dr ZE Switkowski Independent Director + Oil Search InterOil Board representative InterOil InterOil shareholders will own 14 - 21% of combined entity (1) Combined entity’s Board of Directors 3 (1) Dependent upon cash take up by InterOil shareholders.

– 24 – – 24 – • The timing of the proposed transaction between InterOil and Oil Search is optimal to maximize cooperation and/or integration synergies ( 1 ) o Development window of PNG LNG Train 3 and Papua LNG currently aligned o Plant and infrastructure design can be appropriately sized o Construction and operations workforce optimized • Delays in the certification of Elk/Antelope and this transaction may impact ability to achieve cooperation and/or integration, with loss of upside ( 1 ) o Ability to offer these terms to InterOil would be materially diminished • Window is open for cooperation and/or integration from now until approximately mid - 2017 ( 1 ) Timing facilitates greater integration benefits 4 (1) Oil Search Investor Presentation (June 15, 2016).

– 25 – – 25 – Current status of the proposed transaction

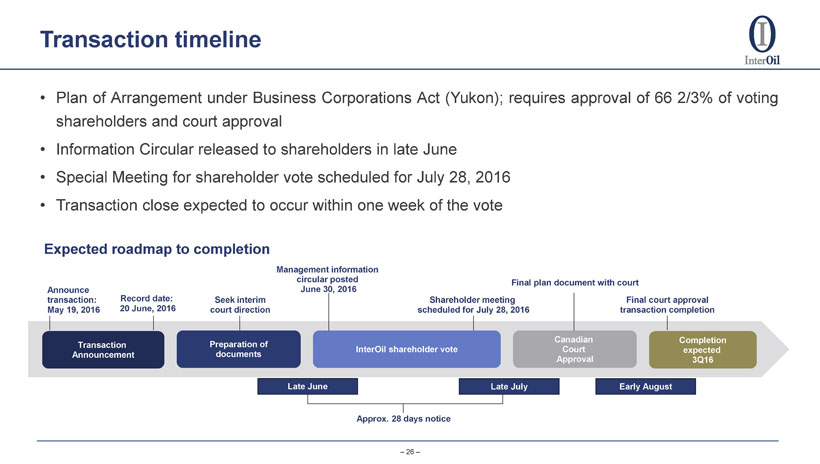

– 26 – – 26 – • Plan of Arrangement under Business Corporations Act (Yukon) ; requires approval of 66 2 / 3 % of voting shareholders and court approval • Information Circular released to shareholders in late June • Special Meeting for shareholder vote scheduled for July 28 , 2016 • Transaction close expected to occur within one week of the vote Transaction Announcement Preparation of documents InterOil shareholder vote Canadian Court Approval Completion expected 3Q16 Late June Late July Early August Announce transaction: May 19, 2016 Seek interim court direction Management information circular posted June 30, 2016 Shareholder meeting scheduled for July 28, 2016 Final court approval transaction completion Final plan document with court Expected roadmap to completion Approx. 28 days notice Record date: 20 June, 2016 Transaction timeline

– 27 – – 27 – Unsolicited, conditional, non - binding proposal • On June 30 , 2016 , InterOil announced it has received an unsolicited, conditional, non - binding whole company proposal from a third party • Proposal is subject to a number of conditions, including (among others) satisfactory completion of due diligence • InterOil’s Board, in consultation with its legal and financial advisors, is carefully reviewing and considering the unsolicited proposal • InterOil’s Board unanimously recommended the Oil Search transaction to shareholders

– 28 – – 28 – A VOTE FOR THE PROPOSED TRANSACTION IS A VOTE “FOR ” x A material and immediate premium to the InterOil share price at the time of announcement x An uncapped cash payment based on the value upside from the certification of Elk - Antelope field contingent resources x 14 - 21% ownership in the combined entity (1) and exposure to expected Oil Search share price appreciation following the transaction (1) Dependent upon cash take up by InterOil shareholders.

– 29 – – 29 – Appendix

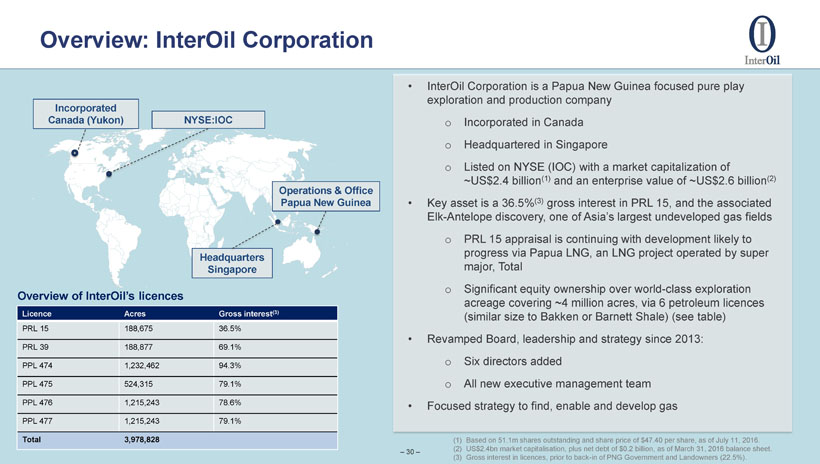

– 30 – – 30 – Overview: InterOil Corporation • InterOil Corporation is a Papua New Guinea focused pure play exploration and production company o I ncorporated in Canada o Headquartered in Singapore o Listed on NYSE (IOC) with a market capitalization of ~ US$2.4 billion (1) and an enterprise value of ~ US$2.6 billion (2) • Key asset is a 36.5 % (3) gross interest in PRL 15, and the associated Elk - Antelope discovery, one of Asia’s largest undeveloped gas fields o PRL 15 appraisal is continuing with development likely to progress via Papua LNG, an LNG project operated by super major, Total o Significant equity ownership over world - class exploration acreage covering ~4 million acres, via 6 petroleum licences (similar size to Bakken or Barnett Shale) (see table) • Revamped Board, leadership and strategy since 2013: o Six directors added o All new executive management team • Focused strategy to find, enable and develop gas NYSE:IOC Headquarters Singapore Operations & Office Papua New Guinea (1) Based on 51.1m shares outstanding and share price of $47.40 per share, as of July 11, 2016. (2) US$2.4bn market capitalisation, plus net debt of $0.2 billion, as of March 31, 2016 balance sheet. (3) Gross interest in licences , prior to back - in of PNG Government and Landowners (22.5%). Licence Acres Gross interest (3) PRL 15 188,675 36.5% PRL 39 188,877 69.1% PPL 474 1,232,462 94.3% PPL 475 524,315 79.1% PPL 476 1,215,243 78.6% PPL 477 1,215,243 79.1% Total 3,978,828 Overview of InterOil’s licences Incorporated Canada (Yukon) – 30 –

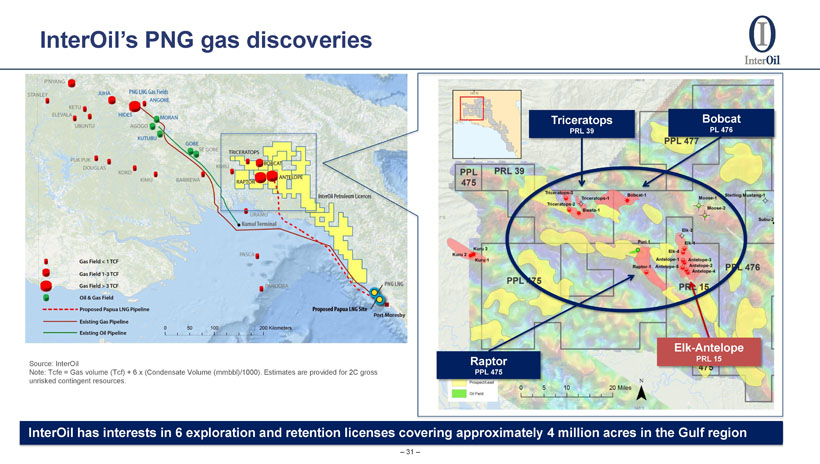

– 31 – – 31 – InterOil’s PNG gas discoveries Source: InterOil Note: Tcfe = Gas volume ( Tcf ) + 6 x (Condensate Volume ( mmbbl )/1000 ). Estimates are provided for 2C gross unrisked contingent resources. Triceratops PRL 39 Bobcat PL 476 Raptor PPL 475 Elk - Antelope PRL 15 InterOil has interests in 6 exploration and retention licenses covering approximately 4 million acres in the Gulf region

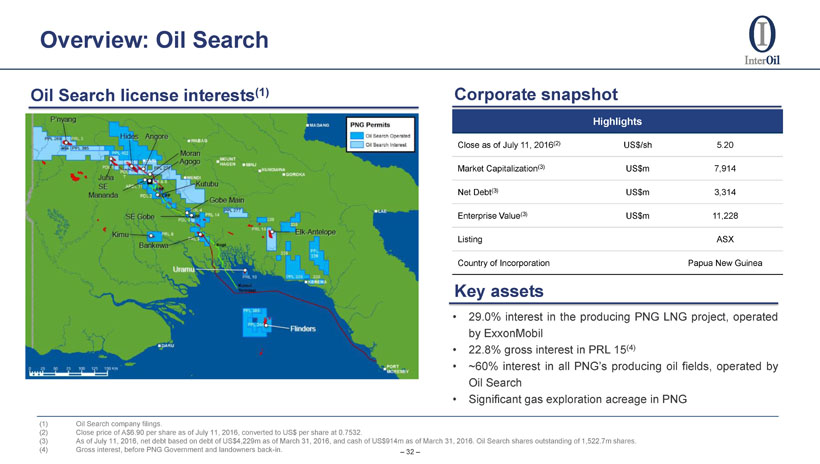

– 32 – – 32 – Overview: Oil Search Highlights Close as of July 11, 2016 (2) US$/sh 5.20 Market Capitalization (3) US$m 7,914 Net Debt (3) US$m 3,314 Enterprise Value (3) US$m 11,228 Listing ASX Country of Incorporation Papua New Guinea (1) Oil Search company filings. (2) Close price of A$6.90 per share as of July 11, 2016 , converted to US$ per share at 0.7532. (3) As of July 11, 2016, net debt based on debt of US$4,229m as of March 31, 2016, and cash of US$914m as of March 31, 2016. Oil Search shares outstanding of 1,522.7m shares. (4) Gross interest, before PNG Government and landowners back - in. • 29 . 0 % interest in the producing PNG LNG project, operated by ExxonMobil • 22 . 8 % gross interest in PRL 15 ( 4 ) • ~ 60 % interest in all PNG’s producing oil fields, operated by Oil Search • Significant gas exploration acreage in PNG Oil Search license interests (1) Corporate snapshot Key assets

– 33 – Thank You For more information, please contact: david.wu@interoil.com Senior Vice President, Investor Relations