UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-21457

Name of Fund: BlackRock Allocation Target Shares

Series A Portfolio

Series C Portfolio

Series E Portfolio

Series M Portfolio

Series P Portfolio

Series S Portfolio

Fund Address: 100 Bellevue Parkway, Wilmington, DE 19809

Name and address of agent for service: John M. Perlowski, Chief Executive Officer, BlackRock Allocation Target Shares, 55 East 52nd Street, New York, NY 10055

Registrant’s telephone number, including area code: (800) 441-7762

Date of fiscal year end: 03/31/2018

Date of reporting period: 09/30/2017

Item 1 – Report to Stockholders

SEPTEMBER 30, 2017

| | | | |

SEMI-ANNUAL REPORT (UNAUDITED) | | | | BLACKROCK® |

BlackRock Allocation Target Shares

▶ Series A Portfolio

▶ Series C Portfolio

▶ Series E Portfolio

▶ Series M Portfolio

▶ Series P Portfolio

▶ Series S Portfolio

| | |

| Not FDIC Insured ◾ May Lose Value ◾ No Bank Guarantee | | |

Dear Shareholder,

In the 12 months ended September 30, 2017, risk assets, such as stocks and high-yield bonds, continued to deliver strong performance. These markets showed great resilience during a period with big surprises, including the aftermath of the U.K.’s vote to leave the European Union and the outcome of the U.S. presidential election, which brought only brief spikes in equity market volatility. These expressions of isolationism and discontent were countered by the closely watched and less surprising elections in France, the Netherlands, and Australia.

Interest rates rose, which worked against high-quality assets with more interest rate sensitivity. As a result, longer-term U.S. Treasuries posted negative returns, as rising energy prices, modest wage increases, and steady job growth led to expectations of higher inflation and anticipation of interest rate increases by the U.S. Federal Reserve (the “Fed”).

Market prices began to reflect reflationary expectations toward the end of 2016, as investors sensed that a global recovery was afoot. And those expectations have been largely realized in 2017, as many countries throughout the world experienced sustained and synchronized growth for the first time since the financial crisis. Growth rates and inflation are still relatively low, but they are finally rising together.

The Fed responded to these positive developments by increasing interest rates three times and setting expectations for additional interest rate increases. The Fed also announced its plan to begin reducing the vast balance sheet reserves that had accumulated in the wake of the financial crisis. The Fed will reduce its $4.5 trillion balance sheet by only $10 billion in October with further reductions expected in subsequent months.

By contrast, the European Central Bank and the Bank of Japan both continued to expand their balance sheets despite nascent signs of sustained economic growth. The Eurozone and Japan are both approaching the limits of central banks’ ownership share of debt issued by their respective governments, which means central bank bond purchasing plans may need to be reduced in 2018.

Emerging market growth also stabilized, as accelerating growth in China, the second largest economy in the world and the most influential of all developing economies, improved the outlook for corporate profits and economic growth across most developing nations. Chinese demand for commodities and other raw materials allayed concerns about the country’s banking system, leading to rising equity prices and foreign investment flows.

In recent months, financial markets have appeared less dependent on significant U.S. tax reform and infrastructure spending. Rising consumer confidence and improving business sentiment have generated momentum for the U.S. economy, even without the potential effects of major legislative changes. Escalating tensions with North Korea and our nation’s divided politics remain significant concerns; however, benign credit conditions, modest inflation, solid corporate earnings, and the positive outlook for growth in the world’s largest economies have kept markets relatively tranquil.

High valuations across most assets have laid the groundwork for muted returns going forward. At current valuation levels, potential equity gains will likely be closely tied to the pace of earnings growth, which has remained solid thus far in 2017, particularly in emerging markets. In this environment, investors need to think globally, extend their scope across a broad array of asset classes and be nimble as market conditions change. We encourage you to talk with your financial advisor and visit blackrock.com for further insight about investing in today’s markets.

Sincerely,

Rob Kapito

President, BlackRock Advisors, LLC

Rob Kapito

President, BlackRock Advisors, LLC

| | | | | | | | |

| Total Returns as of September 30, 2017 | |

| | | 6-month | | | 12-month | |

U.S. large cap equities

(S&P 500® Index) | | | 7.71 | % | | | 18.61 | % |

U.S. small cap equities

(Russell 2000® Index) | | | 8.27 | | | | 20.74 | |

International equities

(MSCI Europe, Australasia, Far East Index) | | | 11.86 | | | | 19.10 | |

Emerging market equities

(MSCI Emerging Markets Index) | | | 14.66 | | | | 22.46 | |

3-month Treasury bills

(BofA Merrill Lynch 3-Month U.S. Treasury Bill Index) | | | 0.47 | | | | 0.66 | |

U.S. Treasury securities

(BofA Merrill Lynch 10- Year U.S. Treasury Index) | | | 1.57 | | | | (4.61 | ) |

U.S. investment grade bonds

(Bloomberg Barclays U.S. Aggregate Bond Index) | | | 2.31 | | | | 0.07 | |

Tax-exempt municipal bonds

(S&P Municipal Bond Index) | | | 2.82 | | | | 0.84 | |

U.S. high yield bonds

(Bloomberg Barclays U.S. Corporate High Yield 2% Issuer Capped Index) | | | 4.19 | | | | 8.87 | |

|

| Past performance is no guarantee of future results. Index performance is shown for illustrative purposes only. You cannot invest directly in an index. | |

| | | | | | |

| 2 | | THIS PAGE NOT PART OF YOUR FUND REPORT | | | | |

| | | | | | |

| | | BLACKROCK ALLOCATION TARGET SHARES | | SEPTEMBER 30, 2017 | | 3 |

| | | | |

| Fund Summary as of September 30, 2017 | | | Series A Portfolio | |

Series A Portfolio’s (the “Fund”) investment objective is to seek a high level of current income consistent with capital preservation.

|

| Portfolio Management Commentary |

How did the Fund perform?

| • | | For the six-month period ended September 30, 2017, the Fund outperformed both its broad-based benchmark, the Bloomberg Barclays U.S. Universal Index, and its “Reference Benchmark,” consisting of 50% Bloomberg Barclays U.S. Asset-Backed Securities Index and 50% Bloomberg Barclays Non-Agency Investment Grade CMBS Index. Shares of the Fund can be purchased or held only by or on behalf of: (i) certain separately managed account clients; (ii) collective trust funds managed by BlackRock Institutional Trust Company, N.A., an affiliate of the investments adviser; and (iii) mutual funds advised by BlackRock Advisors, LLC or its affiliates. Comparisons of the Fund’s performance versus its benchmark index will differ from comparisons of the benchmark against the performance of the separately managed accounts and collective trust funds. |

What factors influenced performance?

| • | | The largest positive contributions to the Fund’s performance came from holdings of non-agency residential mortgage-backed securities (“RMBS”), specifically allocations within the subprime, option adjustable-rate mortgage and credit risk-transfer subsectors. Allocations to floating rate collateralized loan obligations (“CLOs”) also contributed notably to performance. |

| • | | The most significant detractor from performance was the Fund’s underweight to asset-backed securities (“ABS”) relative to the benchmark, which was most pronounced with respect to the credit |

| | | card and auto loan segments. The negative contribution was almost entirely offset by strong security selection within the ABS sector, specifically overweights to consumer loans and private label student loans. The Fund’s underweight to commercial mortgage-backed securities (“CMBS”) relative to the benchmark also detracted from performance. Strong security selection within CMBS helped offset most of this underperformance, through overweights to interest-only (“IO”) and BBB-rated issues. |

Describe recent portfolio activity.

| • | | The Fund took advantage of the robust new-issue calendar to deploy cash, increasing its allocations to non-agency RMBS, CMBS and CLOs. The Fund also added a small amount of bank loans, auto ABS and student loan ABS while reducing exposure in credit card ABS. |

Describe portfolio positioning at period end.

| • | | The Fund ended the period underweight to duration (and corresponding interest rate sensitivity) relative to the benchmark. The Fund’s allocation within non-agency RMBS favored more market sensitive, higher beta subprime issues relative to Alt-A, Option ARM and prime. Within CMBS, the Fund favored allocations to IO issues and lower beta single-asset/ single-borrower transactions. Within CLOs, the Fund maintained a barbelled approach with allocations to the top and bottom of the capital structure. Within ABS, allocations favored consumer loans and private label student loans over auto or credit card ABS. |

The views expressed reflect the opinions of BlackRock as of the date of this report and are subject to change based on changes in market, economic or other conditions. These views are not intended to be a forecast of future events and are no guarantee of future results.

| | |

| Portfolio Composition | | Percent of

Total Investments1 |

| | | | |

Asset-Backed Securities | | | 57 | % |

Non-Agency Mortgage-Backed Securities | | | 37 | |

U.S. Government Sponsored Agency Securities | | | 5 | |

Floating Rate Loan Interests | | | 1 | |

| | |

| Credit Quality Allocation2 | | Percent of

Total Investments1 |

| | | | |

AAA/Aaa3 | | | 17 | % |

AA/Aa | | | 5 | |

A | | | 10 | |

BBB/Baa | | | 11 | |

BB/Ba | | | 12 | |

B | | | 4 | |

CCC/Caa | | | 9 | |

CC/Ca | | | 4 | |

C | | | 2 | |

N/R | | | 26 | |

| | 1 | | Total investments exclude short-term securities. |

| | 2 | | For financial reporting purposes, credit quality ratings shown above reflect the highest rating assigned by either S&P Global Ratings (“S&P”) or Moody’s Investors Service (“Moody’s”) if ratings differ. These rating agencies are independent, nationally recognized statistical rating organizations and are widely used. Investment grade ratings are credit ratings of BBB/Baa or higher. Below investment grade ratings are credit ratings of BB/Ba or lower. Investments designated N/R are not rated by either rating agency. Unrated investments do not necessarily indicate low credit quality. Credit quality ratings are subject to change. |

| | 3 | | The investment adviser evaluates the credit quality of not-rated investments based upon certain factors including, but not limited to, credit ratings for similar investments and financial analysis of sectors, individual investments and/or issuers. Using this approach, the investment adviser has deemed not-rated U.S. Government Sponsored Agency Securities and U.S. Treasury Obligations as AAA/Aaa. |

| | | | | | |

| 4 | | BLACKROCK ALLOCATION TARGET SHARES | | SEPTEMBER 30, 2017 | | |

|

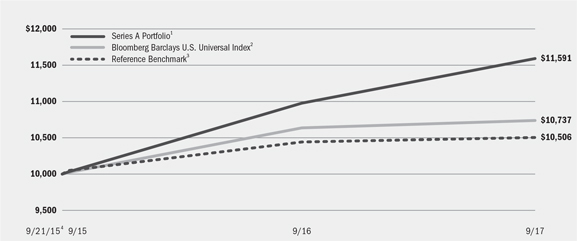

| Total Return Based on a $10,000 Investment |

| | 1 | The Fund is non-diversified and will principally invest its assets in fixed-income securities, such as asset-backed securities, commercial and residential mortgage-backed securities issued or guaranteed by the U.S. Government, various agencies of the U.S. Government or various instrumentalities that have been established or sponsored by the U.S. Government, commercial and residential mortgage-backed securities issued by banks and other financial institutions, collateralized mortgage obligations, loans backed by commercial or residential real estate, derivatives and repurchase agreements and reverse repurchase agreements. |

| | 2 | An unmanaged, market value weighted index of fixed-income securities issued in U.S. dollars, including U.S. government and investment grade debt, non-investment grade debt, asset-backed and mortgage-backed securities, Eurobonds, 144A securities and emerging market debt with maturities of at least one year. |

| | 3 | A customized weighted index comprised of the returns of the Bloomberg Barclays U.S. Asset-Backed Securities Index (50%)/Bloomberg Barclays Non-Agency Investment Grade CMBS Index (50%). The Bloomberg Barclays U.S. Asset-Backed Securities Index is composed of debt securities backed by credit card, auto and home equity loans that are rated investment grade or higher by Moody’s, S&P or Fitch Ratings, Inc. Issues must have at least one year to maturity and an outstanding par value of at least $50 million. The Bloomberg Barclays Non- Agency Investment Grade CMBS Index measures the market of conduit and fusion CMBS deals with a minimum current deal size of $300 million that are rated investment grade or higher using the middle rating of Moody’s, S&P, and Fitch after dropping the highest and lowest available ratings. Securities must have a remaining average life of at least one year and must be fixed-rate, weighted average coupon (WAC), or capped WAC securities. |

| | 4 | Commencement of operations. |

|

| Performance Summary for the Period Ended September 30, 2017 |

| | | | | | | | | | | | |

| | | | | | Average Annual Total Returns5 | |

| | | 6-Month

Total Returns | | | 1 Year | | | Since Inception6 | |

Series A Portfolio | | | 3.46 | % | | | 5.61 | % | | | 7.57 | % |

Bloomberg Barclays U.S. Universal Index | | | 2.55 | | | | 0.96 | | | | 3.58 | |

Reference Benchmark | | | 1.71 | | | | 0.62 | | | | 2.47 | |

| | 5 | | See “About Fund Performance” on page 16 for a detailed description of performance related information. |

| | 6 | | The Fund commenced operations on September 21, 2015. |

| | | | Past performance is not indicative of future results. |

| | | | Performance results may include adjustments made for financial reporting purposes in accordance with U.S. generally accepted accounting principles. |

| | | | | | | | | | | | | | |

| | | Actual | | Hypothetical8 | | |

| | | Beginning

Account Value

April 1, 2017 | | Ending

Account Value

September 30, 2017 | | Expenses Paid

During the Period7 | | Beginning

Account Value

April 1, 2017 | | Ending

Account Value

September 30, 2017 | | Expenses Paid

During the Period7 | | Annualized

Expense Ratio |

Series A Portfolio | | $1,000.00 | | $1,034.60 | | $0.00 | | $1,000.00 | | $1,025.07 | | $0.00 | | 0.00% |

| | 7 | | For shares of the Fund, expenses are equal to the annualized expense ratio, multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one-half year period shown). BlackRock has contractually agreed to waive all fees and pay or reimburse all direct expenses, except extraordinary expenses and interest expense, incurred by the Fund. This agreement has no fixed term. |

| | 8 | | Hypothetical 5% annual return before expenses is calculated by prorating the number of days in the most recent fiscal half year divided by 365. |

| | | | See “Disclosure of Expenses” on page 16 for further information on how expenses were calculated. |

| | | | | | |

| | | BLACKROCK ALLOCATION TARGET SHARES | | SEPTEMBER 30, 2017 | | 5 |

| | | | |

| Fund Summary as of September 30, 2017 | | | Series C Portfolio | |

Series C Portfolio’s (the “Fund”) investment objective is to seek to maximize total return, consistent with income generation and prudent investment management.

|

| Portfolio Management Commentary |

How did the Fund perform?

| • | | For the six-month period ended September 30, 2017, the Fund outperformed its benchmark, the Bloomberg Barclays U.S. Credit Index. Shares of the Fund can be purchased or held only by or on behalf of certain separately managed account clients. Comparisons of the Fund’s performance versus its benchmark index will differ from comparisons of the benchmark against the performance of the separately managed accounts. |

What factors influenced performance?

| • | | The Fund’s performance was helped by security selection in the wireline telecommunications industry, including a position in Verizon Corp. Security selection in financials also contributed positively, led by large U.S. banks. Exposure to the cable and satellite industry detracted from results, as did positions in capital securities and emerging markets. (Capital securities are dividend-paying securities that combine some features of both corporate bonds and preferred stocks while generally providing higher yields to compensate for being less senior in the issuers’ capital structures). |

Describe recent portfolio activity.

| • | | The Fund maintained a short duration posture due to the combination of improving economic growth and the revived prospects for tax reform. |

| | (Duration is a measure of interest rate sensitivity; prices and yields move in opposite directions). Late in the period, the Fund shifted to a neutral positioning. |

| • | | The investment adviser continued to see a supportive fundamental backdrop for corporate bonds, but retained a defensive portfolio positioning in response to elevated geopolitical risks. The investment adviser also believed that much of the improvement in fundamentals had already been reflected in prices, thereby limiting the potential upside for corporates. The Fund continued to favor the banking sector, particularly securities lower in the capital structure. The Fund maintained overweights in the pipeline and cable/telecommunications sub-sectors, but retained a defensive positioning overall within the industrials sector. |

Describe portfolio positioning at period end.

| • | | The investment adviser believed the valuations for corporate bonds were somewhat rich on a historical basis, given that yield spreads were near their lows of both 2017 and the longer-term cycle at the close of the period. However, the investment adviser also saw the continued strength in economic growth as the foundation for an extended credit cycle that could continue to support the asset class. With this as background, the Fund remained defensively positioned with a preference for taking risk through security selection. |

The views expressed reflect the opinions of BlackRock as of the date of this report and are subject to change based on changes in market, economic or other conditions. These views are not intended to be a forecast of future events and are no guarantee of future results.

| | |

| Portfolio Composition | | Percent of

Total Investments1 |

| | | | |

Corporate Bonds | | | 91 | % |

Capital Trusts | | | 5 | |

Taxable Municipal Bonds | | | 2 | |

Foreign Government Obligations | | | 1 | |

Foreign Agency Obligations | | | 1 | |

| | |

| Credit Quality Allocation2 | | Percent of Total Investments1 |

| | | | |

AAA/Aaa3 | | | 4 | % |

AA/Aa | | | 9 | |

A | | | 31 | |

BBB/Baa | | | 51 | |

BB/Ba | | | 5 | |

| | 1 | | Total investments exclude short-term securities and options purchased. |

| | 2 | | For financial reporting purposes, credit quality ratings shown above reflect the highest rating assigned by either S&P or Moody’s if ratings differ. These rating agencies are independent, nationally recognized statistical rating organizations and are widely used. Investment grade ratings are credit ratings of BBB/Baa or higher. Below investment grade ratings are credit ratings of BB/Ba or lower. Investments designated N/R are not rated by either rating agency. Unrated investments do not necessarily indicate low credit quality. Credit quality ratings are subject to change. |

| | 3 | | The investment adviser evaluates the credit quality of not-rated investments based upon certain factors including, but not limited to, credit ratings for similar investments and financial analysis of sectors, individual investments and/or issuers. Using this approach, the investment adviser has deemed not-rated U.S. Government Sponsored Agency Securities and U.S. Treasury Obligations as AAA/ Aaa. |

| | | | | | |

| 6 | | BLACKROCK ALLOCATION TARGET SHARES | | SEPTEMBER 30, 2017 | | |

|

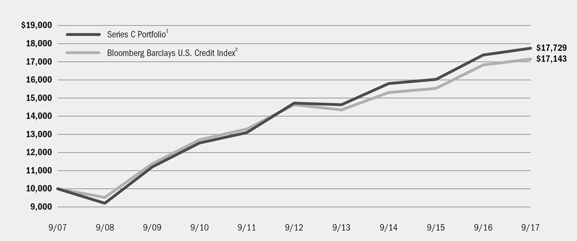

| Total Return Based on a $10,000 Investment |

| | 1 | The Fund will principally invest its assets in investment grade fixed-income securities, such as corporate bonds, notes and debentures, asset-backed securities, commercial and residential mortgage-backed securities, obligations of non-U.S. governments and supranational organizations which are chartered to promote economic development, collateralized mortgage obligations, U.S. Treasury and agency securities, cash equivalent investments, when-issued and delayed delivery securities, derivatives, repurchase agreements and reverse repurchase agreements. |

| | 2 | An unmanaged index that includes publicly issued U.S. corporate and non-corporate securities which include foreign agencies, sovereigns, supranationals and local authorities that meet the specified maturity, liquidity, and quality requirements. |

| | | | | | | | | | | | | | | | |

| Performance Summary for the Period Ended September 30, 2017 | |

| | | | | | Average Annual Total Returns3 | |

| | | 6-Month

Total Returns | | | 1 Year | | | 5 Years | | | 10 Years | |

Series C Portfolio | | | 3.97 | % | | | 2.14 | % | | | 3.79 | % | | | 5.89 | % |

Bloomberg Barclays U.S. Credit Index | | | 3.73 | | | | 1.96 | | | | 3.23 | | | | 5.54 | |

| | 3 | | See “About Fund Performance” on page 16 for a detailed description of performance related information. |

| | | | Past performance is not indicative of future results. |

| | | | Performance results may include adjustments made for financial reporting purposes in accordance with U.S. generally accepted accounting principles. |

| | | | | | | | | | | | | | |

| Expense Example |

| | | Actual | | Hypothetical5 | | |

| | | Beginning Account Value

April 1, 2017 | | Ending Account Value

September 30, 2017 | | Expenses Paid

During the Period4 | | Beginning Account Value

April 1, 2017 | | Ending Account Value

September 30, 2017 | | Expenses Paid

During the Period4 | | Annualized Expense Ratio |

Series C Portfolio | | $1,000.00 | | $1,039.70 | | $0.00 | | $1,000.00 | | $1,025.07 | | $0.00 | | 0.00% |

| | 4 | | For shares of the Fund, expenses are equal to the annualized expense ratio, multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one-half year period shown). BlackRock has contractually agreed to waive all fees and pay or reimburse all direct expenses, except extraordinary expenses and interest expense, incurred by the Fund. This agreement has no fixed term. |

| | 5 | | Hypothetical 5% annual return before expenses is calculated by prorating the number of days in the most recent fiscal half year divided by 365. |

| | | | See “Disclosure of Expenses” on page 16 for further information on how expenses were calculated. |

| | | | | | |

| | | BLACKROCK ALLOCATION TARGET SHARES | | SEPTEMBER 30, 2017 | | 7 |

| | | | |

| Fund Summary as of September 30, 2017 | | | Series E Portfolio | |

Series E Portfolio’s (the “Fund”) investment objective is to seek to maximize Federal tax-free yield with a secondary goal of total return.

|

| Portfolio Management Commentary |

How did the Fund perform?

| • | | For the six-month period ended September 30, 2017, the Fund outperformed both its broad-based benchmark, the S&P® Municipal Bond Index, and its customized “Reference Benchmark,” consisting of 50% S&P® Municipal High-Yield Index, 25% S&P® Municipal Bond A Rating Band Index (using the returns of only those A rated bonds that have maturities greater than five years) and 25% S&P® Municipal Bond BBB Rating Band Index (using the returns of only those BBB rated bonds that have maturities greater than five years). Shares of the Fund can be purchased or held only by or on behalf of certain separately managed account clients. Comparisons of the Fund’s performance versus its benchmark index will differ from comparisons of the benchmark against the performance of the separately managed accounts. |

What factors influenced performance?

| • | | The Fund was helped by having a large underweight in Puerto Rico, as the territory significantly underperformed all U.S. states during the period due to its ongoing fiscal issues and the impact of Hurricane Maria. Specifically, underweight positions in the tax-backed (state) and utilities sectors related to Puerto Rico contributed positively. |

| • | | The Fund was also aided by having a long duration posture relative to the benchmark at a time of falling yields. (Duration is a measure of interest-rate sensitivity, prices and yields move in opposite directions). The Fund’s yield curve positioning was a further contributor due to an overweight in longer-dated securities. |

| • | | Overweight positions in the health care and project-finance sectors also made positive contributions. Conversely, underweights in the school district and tax-backed (local) sectors detracted. An underweight in non-rated bonds also hurt results, as lower-rated securities outperformed. |

| • | | The Fund sought to manage interest rate risk using U.S. Treasury futures, but this aspect of its positioning had a negligible effect on returns. The Fund continued to adjust the size of this position on a tactical basis in an effort to reduce the effect of interest rate volatility. |

Describe recent portfolio activity.

| • | | Given the strong cash inflows that the Fund received during the period, portfolio activity reflected efforts to stay fully invested. In addition, the investment adviser sought to realize gains on certain securities that had benefited from falling yield spreads. The Fund also added longer-dated securities to capitalize on a flattening yield curve (i.e., outperformance for longer-term bonds relative to short-term issues). |

Describe portfolio positioning at period end.

| • | | In a reflection of its bias toward a flattening yield curve, the Fund held its largest overweight position in bonds with maturities of 20 year and above. The Fund’s leading sector overweights were in the transportation, education and project finance sectors, while its largest underweights included tax-backed local and state, school districts and utilities. |

The views expressed reflect the opinions of BlackRock as of the date of this report and are subject to change based on changes in market, economic or other conditions. These views are not intended to be a forecast of future events and are no guarantee of future results.

| | |

| Sector Allocation | | Percent of

Total Investments1 |

| | | | |

Transportation | | | 21 | % |

Health Care | | | 21 | |

Education | | | 15 | |

County/City/Special District/School District | | | 15 | |

Tobacco | | | 12 | |

Utilities | | | 7 | |

Corporate | | | 5 | |

Housing | | | 4 | |

| | |

| Credit Quality Allocation2 | | Percent of

Total Investments1 |

| | | | |

AAA/Aaa | | | 2 | % |

AA/Aa | | | 11 | |

A | | | 21 | |

BBB/Baa | | | 29 | |

BB/Ba | | | 10 | |

B | | | 7 | |

CCC/Caa | | | 1 | |

N/R | | | 19 | |

| | 1 | | Total investments exclude short-term securities. |

| | 2 | | For financial reporting purposes, credit quality ratings shown above reflect the highest rating assigned by either S&P or Moody’s if ratings differ. These rating agencies are independent, nationally recognized statistical rating organizations and are widely used. Investment grade ratings are credit ratings of BBB/Baa or higher. Below investment grade ratings are credit ratings of BB/Ba or lower. Investments designated N/R are not rated by either rating agency. Unrated investments do not necessarily indicate low credit quality. Credit quality ratings are subject to change. |

| | | | | | |

| 8 | | BLACKROCK ALLOCATION TARGET SHARES | | SEPTEMBER 30, 2017 | | |

|

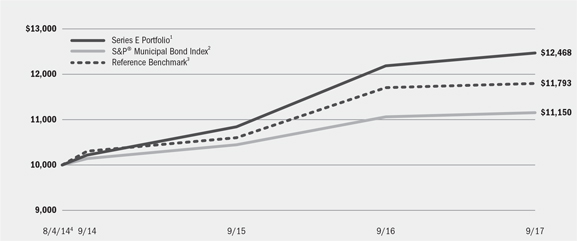

| Total Return Based on a $10,000 Investment |

| | 1 | The Fund will invest in investment grade and non-investment grade municipal bonds. Under normal circumstances, the Fund maintains an average portfolio duration that is within ±25% of the duration of the Reference Benchmark. |

| | 2 | The S&P® Municipal Bond Index is composed of bonds held by managed municipal bond fund customers of Standard & Poor’s Securities Pricing, Inc. that are priced daily. Bonds in the S&P® Municipal Bond Index must have an outstanding par value of at least $2 million and a remaining maturity of not less than one month. |

| | 3 | A customized weighted index comprised of the returns of the S&P® Municipal High-Yield Index (50%)/S&P® Municipal Bond A Rating Band Index (25%) using the returns of only those A rated bonds that have maturities greater than 5 years/S&P® Municipal Bond BBB Rating Band Index (25%) using the returns of only those BBB rated bonds that have the maturities greater than 5 years. The benchmark value used to calculate since inception return is from the close of July 31, 2014. By using this value the benchmark is using 2 extra days of performance (August 1, 2014 and August 4, 2014) compared to the Fund. |

| | 4 | Commencement of operations. |

| | | | | | | | | | | | |

| Performance Summary for the Period Ended September 30, 2017 | |

| | | | | | Average Annual Total Returns5 | |

| | | 6-Month

Total Returns | | | 1 Year | | | Since Inception6 | |

Series E Portfolio | | | 5.12 | % | | | 2.34 | % | | | 7.24 | % |

S&P® Municipal Bond Index | | | 2.82 | | | | 0.84 | | | | 3.51 | |

Reference Benchmark | | | 2.73 | | | | 0.78 | | | | 5.35 | 7 |

| | 5 | | See “About Fund Performance” on page 16 for a detailed description of performance related information. |

| | 6 | | The Fund commenced operations on August 4, 2014. |

| | 7 | | The benchmark value used to calculate since inception return is from the close of July 31, 2014. By using this value the benchmark is using 2 extra days of performance (August 1, 2014 and August 4, 2014) compared to the Fund. |

| | | | Past performance is not indicative of future results. |

| | | | Performance results may include adjustments made for financial reporting purposes in accordance with U.S. generally accepted accounting principles. |

| | | | | | | | | | | | | | | | | | |

| Expense Example |

| | | Actual | | Hypothetical10 |

| | | | | | | Including

Interest Expense

and Fees | | Excluding

Interest Expense

and Fees | | | | Including Interest Expense and Fees | | Excluding Interest Expense and Fees |

| | | Beginning

Account Value

April 1, 2017 | | Ending Account Value

September 30,

2017 | | Expenses Paid During the Period8 | | Expenses Paid During the Period9 | | Beginning

Account Value

April 1, 2017 | | Ending Account Value

September 30,

2017 | | Expenses Paid During the Period8 | | Ending Account Value September 30, 2017 | | Expenses Paid During the Period9 |

Series E Portfolio | | $1,000.00 | | $1,051.20 | | $0.31 | | $0.00 | | $1,000.00 | | $1,024.77 | | $0.30 | | $1,025.07 | | $0.00 |

| | 8 | | For shares of the Fund, expenses are equal to the annualized expense ratio of 0.06%, multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one-half year period shown). BlackRock has contractually agreed to waive all fees and pay or reimburse all direct expenses, except extraordinary expenses and interest expense, incurred by the Fund. This agreement has no fixed term. |

| | 9 | | For shares of the Fund, expenses are equal to the annualized expense ratio of 0.00%, multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one-half year period shown). BlackRock has contractually agreed to waive all fees and pay or reimburse all direct expenses, except extraordinary expenses and interest expense, incurred by the Fund. This agreement has no fixed term. |

| | 10 | | Hypothetical 5% annual return before expenses is calculated by prorating the number of days in the most recent fiscal half year divided by 365. |

| | | | See “Disclosure of Expenses” on page 16 for further information on how expenses were calculated. |

| | | | | | |

| | | BLACKROCK ALLOCATION TARGET SHARES | | SEPTEMBER 30, 2017 | | 9 |

| | | | |

| Fund Summary as of September 30, 2017 | | | Series M Portfolio | |

Series M Portfolio’s (the “Fund”) investment objective is to seek to maximize total return, consistent with income generation and prudent investment management.

|

| Portfolio Management Commentary |

How did the Fund perform?

| • | | For the six-month period ended September 30, 2017, the Fund outperformed its benchmark, the Bloomberg Barclays MBS Index. Shares of the Fund can be purchased or held only by or on behalf of certain separately managed account clients. Comparisons of the Fund’s performance versus its benchmark index will differ from comparisons of the benchmark against the performance of the separately managed accounts. |

What factors influenced performance?

| • | | The most significant positive contributors to the Fund’s performance were allocations to agency mortgage-backed securities (“MBS”), U.S. Treasuries, agency collateralized mortgage obligations (“CMOs”), and agency interest-only (“IO”) and principal-only (“PO”) obligations. Security selection within commercial mortgage-backed obligations (“CMBS”) and MBS also added to relative performance. |

| • | | An underweight to CMBS and swap/swaption-based strategies were the only material detractors from performance. |

Describe recent portfolio activity.

| • | | During the period, the Fund trimmed its allocation to pass-through agency MBS, while adding to agency CMOs. The Fund increased its overall allocation to CMBS during the period, while rotating some IO positions into AAA-rated last cash flow securities. The Fund moved from an underweight stance with respect to duration (and corresponding interest rate sensitivity) to a modest duration overweight relative to the benchmark. |

Describe portfolio positioning at period end.

| • | | The Fund’s positioning at period-end reflected a reasonably positive near-term outlook for MBS, based on supply/demand factors and valuation relative to credit-oriented sectors. The Fund was slightly underweight CMBS given tight spreads for the sector, with a tilt toward the top of the capital structure as well as toward less market sensitive, single asset/ single borrower issues. In turn, the Fund held exposure to agency CMOs, IOs and POs. Relative to the Bloomberg Barclays MBS Index, the Fund ended the period modestly overweight overall portfolio duration relative to the benchmark. |

The views expressed reflect the opinions of BlackRock as of the date of this report and are subject to change based on changes in market, economic or other conditions. These views are not intended to be a forecast of future events and are no guarantee of future results.

| | |

| Portfolio Composition | | Percent of

Total Investments1 |

| | | | |

U.S. Government Sponsored Agency Securities | | | 95 | % |

Non-Agency Mortgage-Backed Securities | | | 5 | |

| | |

| Credit Quality Allocation2 | | Percent of

Total Investments1 |

| | | | |

AAA/Aaa3 | | | 98 | % |

BBB/Baa | | | 1 | |

N/R | | | 1 | |

| | 1 | | Total investments exclude short-term securities, options purchased, TBA sale commitments and options written. |

| | 2 | | For financial reporting purposes, credit quality ratings shown above reflect the highest rating assigned by either S&P or Moody’s if ratings differ. These rating agencies are independent, nationally recognized statistical rating organizations and are widely used. Investment grade ratings are credit ratings of BBB/Baa or higher. Below investment grade ratings are credit ratings of BB/Ba or lower. Investments designated N/R are not rated by either rating agency. Unrated investments do not necessarily indicate low credit quality. Credit quality ratings are subject to change. |

| | 3 | | The investment adviser evaluates the credit quality of not-rated investments based upon certain factors including, but not limited to, credit ratings for similar investments and financial analysis of sectors, individual investments and/or issuers. Using this approach, the investment adviser has deemed not-rated U.S. Government Sponsored Agency Securities and U.S. Treasury Obligations as AAA/ Aaa. |

| | | | | | |

| 10 | | BLACKROCK ALLOCATION TARGET SHARES | | SEPTEMBER 30, 2017 | | |

|

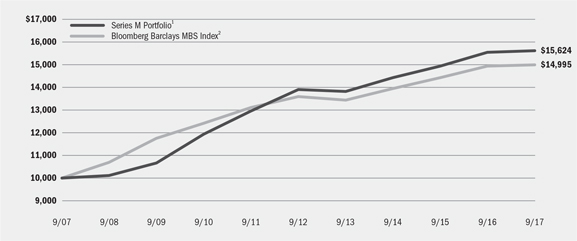

| Total Return Based on a $10,000 Investment |

| | 1 | The Fund will principally invest its assets in investment grade commercial and residential mortgage-backed securities, asset-backed securities, collateralized mortgage obligations, U.S. Treasury and agency securities, cash equivalent instruments, when-issued and delayed delivery securities, derivatives and dollar rolls. |

| | 2 | An unmanaged index that includes the mortgage-backed pass-through securities of Ginnie Mae, Fannie Mae and Freddie Mac that meet the maturity and liquidity criteria. |

| | | | | | | | | | | | | | | | |

| Performance Summary for the Period Ended September 30, 2017 | |

| | | | | | Average Annual Total Returns3 | |

| | | 6-Month

Total Returns | | | 1 Year | | | 5 Years | | | 10 Years | |

Series M Portfolio | | | 2.00 | % | | | 0.47 | % | | | 2.35 | % | | | 4.56 | % |

Bloomberg Barclays MBS Index | | | 1.84 | | | | 0.30 | | | | 1.96 | | | | 4.13 | |

| | 3 | | See “About Fund Performance” on page 16 for a detailed description of performance related information. |

| | | | Past performance is not indicative of future results. |

| | | | Performance results may include adjustments made for financial reporting purposes in accordance with U.S. generally accepted accounting principles. |

| | | | | | | | | | | | | | |

| Expense Example |

| | | Actual | | Hypothetical5 | | |

| | | Beginning Account

Value April 1, 2017 | | Ending Account

Value September 30,

2017 | | Expenses Paid

During the Period4 | | Beginning Account

Value April 1, 2017 | | Ending Account

Value September 30,

2017 | | Expenses Paid

During the Period4 | | Annualized Expense

Ratio |

Series M Portfolio | | $1,000.00 | | $1,020.00 | | $0.00 | | $1,000.00 | | $1,025.07 | | $0.00 | | 0.00% |

| | 4 | | For shares of the Fund, expenses are equal to the annualized expense ratio, multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one-half year period shown). BlackRock has contractually agreed to waive all fees and pay or reimburse all direct expenses, except extraordinary expenses and interest expense, incurred by the Fund. This agreement has no fixed term. |

| | 5 | | Hypothetical 5% annual return before expenses is calculated by prorating the number of days in the most recent fiscal half year divided by 365. |

| | | | See “Disclosure of Expenses” on page 16 for further information on how expenses were calculated. |

| | | | | | |

| | | BLACKROCK ALLOCATION TARGET SHARES | | SEPTEMBER 30, 2017 | | 11 |

| | | | |

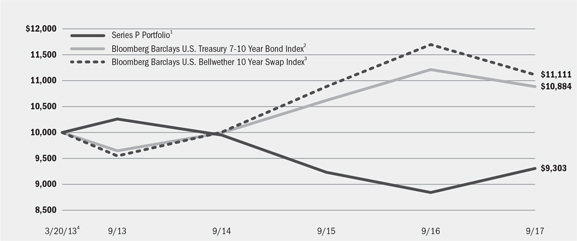

| Fund Summary as of September 30, 2017 | | | Series P Portfolio | |

Series P Portfolio’s (the “Fund”) investment objective is to seek to provide a duration that is the inverse of its benchmark.

|

| Portfolio Management Commentary |

How did the Fund perform?

| • | | For the six-month period ended September 30, 2017, the Fund underperformed both its benchmarks, the Bloomberg Barclays U.S. Treasury 7-10 Year Bond Index and the Bloomberg Barclays U.S. Bellwether 10 Year Swap Index. Shares of the Fund can be purchased or held only by or on behalf of certain separately managed account clients. Comparisons of the Fund’s performance versus its benchmark index will differ from comparisons of the benchmark against the performance of the separately managed accounts. |

What factors influenced performance?

| • | | The Fund held cash at the end of the period as collateral in conjunction with the Fund’s investments in U.S. Treasury futures and interest rate swaps. The Fund’s cash exposure had no material impact on performance. The use and cost of derivatives will result in a negative contribution to returns when interest rates fall; however, the Fund’s strategy is designed to offset these costs by holding shares of BlackRock Allocation Target Shares: Series S Portfolio (“Series S Portfolio”), a short-term proprietary fund. The use of derivatives is necessary to achieve the Fund’s objective and should therefore be evaluated in a portfolio context and not as a standalone strategy. The Fund’s use of derivatives to facilitate an inverse exposure to the 7- to 10-year part of the U.S. Treasury yield curve detracted from results given that yields fell. |

| • | | The Fund’s allocation to Series S Portfolio contributed to performance. Series S Portfolio generated positive returns from its overweight |

| | | allocations to investment-grade corporate bonds, mortgage-backed securities (“MBS”), commercial mortgage-backed securities (“CMBS”) and asset-backed securities (“ABS”). |

Describe recent portfolio activity.

| • | | The Fund actively managed interest rate risk on the 7- to 10-year part of the yield curve by using derivatives as described above. The Fund maintained its allocation to Series S Portfolio, in order to offset the cost of the derivatives. |

| • | | Series S Portfolio slightly increased the Fund’s exposure to credit risk during the course of the period. It also slightly reduced the allocation to ABS and CMBS and rotated the proceeds into agency MBS, which came under pressure from the Fed’s announcement of a plan to begin reducing the size of its balance sheet. The unknown path of privatization for Fannie Mae and Freddie Mac acted as a further headwind to the asset class. The resulting underperformance for MBS caused the category to become attractively priced relative to other spread sectors, a development the investment adviser saw as creating the potential for attractive risk-adjusted returns. |

Describe portfolio positioning at period end.

| • | | The Fund held positions in U.S. Treasury futures, interest rate swaps, Series S Portfolio, and the Bank of New York Cash Reserve money market fund. |

The views expressed reflect the opinions of BlackRock as of the date of this report and are subject to change based on changes in market, economic or other conditions. These views are not intended to be a forecast of future events and are no guarantee of future results.

| | |

| Portfolio Composition | | Percent of

Net Assets |

| | | | |

Fixed Income Funds | | | 29 | % |

Other Assets Less Liabilities | | | 71 | |

| | |

| Portfolio Holdings | | Percent of

Affiliated Investment Companies |

| | | | |

BlackRock Allocation Target Shares: Series S Portfolio | | | 100 | % |

| | | | | | |

| 12 | | BLACKROCK ALLOCATION TARGET SHARES | | SEPTEMBER 30, 2017 | | |

|

| Total Return Based on a $10,000 Investment |

| | 1 | The Fund may invest in a portfolio of securities and other financial instruments, including derivative instruments, in an attempt to provide returns that are the inverse of its benchmark index. |

| | 2 | An unmanaged index that includes all publicly issued, U.S. Treasury securities that have a remaining maturity of between 7 and 10 years, are non-convertible, are denominated in U.S. dollars, are rated Baa3 (or better) by Moody’s or BBB- (or better) by S&P, are fixed rate, and have more than $250 million par outstanding. |

| | 3 | Provides total returns for swaps with varying maturities. For example, the 10-year swap index measures the total return of investing in 10-year par swaps over time. |

| | 4 | Commencement of operations. |

| | | | | | | | | | | | |

| Performance Summary for the Period Ended September 30, 2017 | | | | | | | | | | | | |

| | | | | | Average Annual Total Returns5 | |

| | | 6-Month

Total Returns | | | 1 Year | | | Since Inception6 | |

Series P Portfolio | | | (0.82 | )% | | | 5.24 | % | | | (1.58 | )% |

Bloomberg Barclays U.S. Treasury 7-10 Year Bond Index | | | 1.86 | | | | (2.90 | ) | | | 1.89 | |

Bloomberg Barclays Bellwether 10 Year Swap Index | | | 2.21 | | | | (4.98 | ) | | | 2.35 | |

| | 4 | | See “About Fund Performance” on page 16 for a detailed description of performance related information. |

| | 5 | | The Fund commenced operations on March 20, 2013. |

| | | | Past performance is not indicative of future results. |

| | | | Performance results may include adjustments made for financial reporting purposes in accordance with U.S. generally accepted accounting principles. |

| | | | | | | | | | | | | | |

| Expense Example |

| | | Actual | | Hypothetical8 | | |

| | | Beginning Account Value

April 1, 2017 | | Ending Account Value

September 30, 2017 | | Expenses Paid

During the Period7 | | Beginning Account Value

April 1, 2017 | | Ending Account Value

September 30, 2017 | | Expenses Paid

During the Period7 | | Annualized Expense Ratio |

Series P Portfolio | | $1,000.00 | | $991.80 | | $0.00 | | $1,000.00 | | $1,025.07 | | $0.00 | | 0.00% |

| | 6 | | For shares of the Fund, expenses are equal to the annualized expense ratio, multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one-half year period shown). The fees and expenses of the underlying funds in which the Fund invests are not included in the Fund’s annualized expense ratio. BlackRock has contractually agreed to waive all fees and pay or reimburse all direct expenses, except extraordinary expenses and interest expense, incurred by the Fund. This agreement has no fixed term. |

| | 7 | | Hypothetical 5% annual return before expenses is calculated by prorating the number of days in the most recent fiscal half year divided by 365. |

| | | | See “Disclosure of Expenses” on page 16 for further information on how expenses were calculated. |

| | | | | | |

| | | BLACKROCK ALLOCATION TARGET SHARES | | SEPTEMBER 30, 2017 | | 13 |

| | | | |

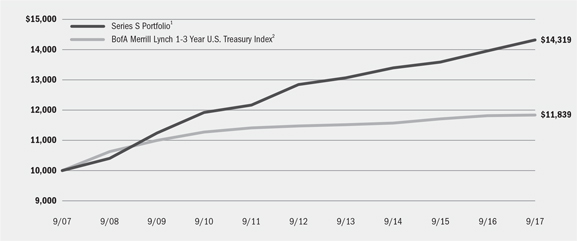

| Fund Summary as of September 30, 2017 | | | Series S Portfolio | |

Series S Portfolio’s (the “Fund”) investment objective is to seek to maximize total return, consistent with income generation and prudent investment management.

|

| Portfolio Management Commentary |

How did the Fund perform?

| • | | For the six-month period ended September 30, 2017, the Fund outperformed its benchmark, the BofA Merrill Lynch 1-3 Year U.S. Treasury Index. Shares of the Fund can be purchased or held only by or on behalf of certain separately managed account clients. Comparisons of the Fund’s performance versus its benchmark index will differ from comparisons of the benchmark against the performance of the separately managed accounts. |

What factors influenced performance?

| • | | The Fund’s overweight allocation to investment-grade corporate bonds was the leading contributor to performance. Corporate issues outpaced the benchmark, which is invested entirely in U.S. Treasuries, in a reflection of investors’ continued appetite for yield. Allocations to mortgage-backed securities (“MBS”), commercial mortgage-backed securities (“CMBS”) and asset-backed securities (“ABS”) further aided results. However, the Fund’s yield curve positioning slightly detracted from performance. |

| • | | As part of its investment strategy, the Fund employed derivatives during the period. U.S. Treasury futures are used primarily as a means of managing the portfolio’s duration risk (sensitivity to interest rate movements). The Fund also used credit default swaps against |

| | | individual securities or broad indices to manage credit risk in the portfolio. Credit default swaps against indices also help manage market risk. The use of derivatives detracted from the Fund’s six-month results. |

Describe recent portfolio activity.

| • | | The investment adviser slightly increased the Fund’s exposure to credit risk during the course of the period. It also slightly reduced the allocation to ABS and CMBS and rotated the proceeds into agency MBS, which came under pressure from the U.S. Federal Reserve’s announcement that it would begin reducing the size of its balance sheet. The unknown path of privatization for Fannie Mae and Freddie Mac acted as a further headwind to the asset class. The resulting underperformance for MBS caused the category to become attractively priced relative to other spread sectors, a development the investment adviser saw as creating the potential for attractive risk-adjusted returns. |

Describe portfolio positioning at period end.

| • | | The Fund was positioned with a duration mildly above that of its benchmark. The Fund finished the period with overweights in ABS, agency MBS and U.S. investment-grade corporates. Conversely, it was underweight in non-U.S. sovereign debt. |

The views expressed reflect the opinions of BlackRock as of the date of this report and are subject to change based on changes in market, economic or other conditions. These views are not intended to be a forecast of future events and are no guarantee of future results.

| | |

| Portfolio Composition | | Percent of

Total Investments1 |

| | | | |

Corporate Bonds | | | 42 | % |

Asset-Backed Securities | | | 27 | |

U.S. Government Sponsored Agency Securities | | | 20 | |

Non-Agency Mortgage-Backed Securities | | | 11 | |

| | |

| Credit Quality Allocation2 | | Percent of

Total Investments1 |

| | | | |

AAA/Aaa3 | | | 54 | % |

AA/Aa | | | 4 | |

A | | | 18 | |

BBB/Baa | | | 23 | |

B | | | 1 | |

| | 1 | | Total investments exclude short-term securities and options purchased. |

| | 2 | | For financial reporting purposes, credit quality ratings shown above reflect the highest rating assigned by either S&P or Moody’s if ratings differ. These rating agencies are independent, nationally recognized statistical rating organizations and are widely used. Investment grade ratings are credit ratings of BBB/Baa or higher. Below investment grade ratings are credit ratings of BB/Ba or lower. Investments designated N/R are not rated by either rating agency. Unrated investments do not necessarily indicate low credit quality. Credit quality ratings are subject to change. |

| | 3 | | The investment adviser evaluates the credit quality of not-rated investments based upon certain factors including, but not limited to, credit ratings for similar investments and financial analysis of sectors, individual investments and/or issuers. Using this approach, the investment adviser has deemed not-rated U.S. Government Sponsored Agency Securities and U.S. Treasury Obligations as AAA/ Aaa. |

| | | | | | |

| 14 | | BLACKROCK ALLOCATION TARGET SHARES | | SEPTEMBER 30, 2017 | | |

|

| Total Return Based on a $10,000 Investment |

| | 1 | The Fund will principally invest its assets in investment grade fixed-income securities, such as commercial and residential mortgage-backed securities, obligations of non-U.S. governments and supranational organizations, which are chartered to promote economic development, obligations of domestic and non-U.S. corporations, asset-backed securities, U.S. Treasury and agency securities, cash equivalent investments, when-issued and delayed delivery securities, derivatives, repurchase agreements, reverse repurchase agreements and dollar rolls. |

| | 2 | An unmanaged index comprised of Treasury securities with maturities ranging from one to three years. |

| | | | | | | | | | | | | | | | |

| Performance Summary for the Period Ended September 30, 2017 | | | | | | | | | | | | | | | | |

| | | | | | Average Annual Total Returns3 | |

| | | 6 Months

Total Returns | | | 1 Year | | | 5 Years | | | 10 Years | |

Series S Portfolio | | | 1.53 | % | | | 2.60 | % | | | 2.19 | % | | | 3.66 | % |

BofA Merrill Lynch 1-3 Year U.S. Treasury Index | | | 0.41 | | | | 0.24 | | | | 0.63 | | | | 1.70 | |

| | 3 | | See “About Fund Performance” on page 16 for a detailed description of performance related information. |

| | | | Past performance is not indicative of future results. |

| | | | Performance results may include adjustments made for financial reporting purposes in accordance with U.S. generally accepted accounting principles. |

| | | | | | | | | | | | | | | | | | |

| Expense Example |

| | | Actual | | Hypothetical6 |

| | | | | | | Including

Interest Expense | | Excluding

Interest Expense | | | | Including Interest Expense | | Excluding Interest Expense |

| | | Beginning

Account Value April 1, 2017 | | Ending Account Value

September 30, 2017 | | Expenses Paid

During the Period4 | | Expenses Paid

During the Period5 | | Beginning

Account Value April 1, 2017 | | Ending Account Value

September 30, 2017 | | Expenses Paid

During the Period4 | | Ending Account Value

September 30, 2017 | | Expenses Paid

During the Period5 |

Series S Portfolio | | $1,000.00 | | $1,015.30 | | $2.83 | | $0.00 | | $1,000.00 | | $1,022.26 | | $2.84 | | $1,025.07 | | $0.00 |

| | 4 | | For shares of the Fund, expenses are equal to the annualized expense ratio of 0.56%, multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one-half year period shown). BlackRock has contractually agreed to waive all fees and pay or reimburse all direct expenses, except extraordinary expenses and interest expense, incurred by the Fund. This agreement has no fixed term. |

| | 5 | | For shares of the Fund, expenses are equal to the annualized expense ratio of 0.00%, multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one-half year period shown). BlackRock has contractually agreed to waive all fees and pay or reimburse all direct expenses, except extraordinary expenses and interest expense, incurred by the Fund. This agreement has no fixed term. |

| | 6 | | Hypothetical 5% annual return before expenses is calculated by prorating the number of days in the most recent fiscal half year divided by 365. |

| | | | See “Disclosure of Expenses” on page 16 for further information on how expenses were calculated. |

| | | | | | |

| | | BLACKROCK ALLOCATION TARGET SHARES | | SEPTEMBER 30, 2017 | | 15 |

Performance information reflects past performance and does not guarantee future results. Current performance may be lower or higher than the performance data quoted. Performance results do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Figures shown in the performance tables on the previous pages assume reinvestment of all distributions, if any, at net asset value (“NAV”) on the ex-dividend/payable date. Investment return and principal value of shares will fluctuate so that shares, when redeemed, may be worth more or less than their original cost.

The performance information also reflects fee waivers and reimbursements that subsidize and reduce the total operating expenses of each Fund. The Funds’ returns would have been lower if there were no such waivers and reimbursements.

Shareholders of each Fund may incur the following charges: (a) transactional expenses and (b) operating expenses, including administration fees and other fund expenses. The expense examples shown on the previous pages (which are based on a hypothetical investment of $1,000 invested on April 1, 2017 and held through September 30, 2017) are intended to assist shareholders both in calculating expenses based on an investment in each Fund and in comparing these expenses with similar costs of investing in other mutual funds.

The expense examples provide information about actual account values and actual expenses. In order to estimate the expenses a shareholder paid during the period covered by this report, shareholders can divide their account value by $1,000 and then multiply the result by the number corresponding to their Fund under the headings entitled “Expenses Paid During the Period.”

The expense examples also provide information about hypothetical account values and hypothetical expenses based on a Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses. In order to assist shareholders in comparing the ongoing expenses of investing in these Funds and other funds, compare the 5% hypothetical examples with the 5% hypothetical examples that appear in shareholder reports of other funds.

The expenses shown in the expense examples are intended to highlight shareholders’ ongoing costs only and do not reflect transactional expenses, if any. Therefore, the hypothetical examples are useful in comparing ongoing expenses only, and will not help shareholders determine the relative total expenses of owning different funds. If these transactional expenses were included, shareholder expenses would have been higher.

| | | | | | |

| 16 | | BLACKROCK ALLOCATION TARGET SHARES | | SEPTEMBER 30, 2017 | | |

| | | | |

| The Benefits and Risks of Leveraging | | | | |

The Funds may utilize leverage to seek to enhance returns and NAV. However, these objectives cannot be achieved in all interest rate environments.

The Funds may utilize leverage by entering into reverse repurchase agreements.

Series E Portfolio may leverage its assets through the use of proceeds received in tender option bond (“TOB”) transactions, as described in the Notes to Financial Statements. In a TOB Trust transaction, the Fund transfers municipal bonds or other municipal securities into a special purpose entity (a “TOB Trust”). TOB investments generally provide the Fund with economic benefits in periods of declining short-term interest rates, but expose the Fund to risks during periods of rising short-term interest rates. Additionally, fluctuations in the market value of municipal bonds deposited into a TOB Trust may adversely affect the Fund’s NAV per share.

In general, the concept of leveraging is based on the premise that the financing cost of leverage, which is based on short-term interest rates, is normally lower than the income earned by each Fund on its longer-term portfolio investments purchased with the proceeds from leverage. To the extent that the total assets of each Fund (including the assets obtained from leverage) are invested in higher-yielding portfolio investments, the Funds’ shareholders benefit from the incremental net income.

The interest earned on securities purchased with the proceeds from leverage is distributed to the Funds’ shareholders, and the value of these portfolio holdings is reflected in the Funds’ per share NAV. However, in

order to benefit shareholders, the return on assets purchased with leverage proceeds must exceed the ongoing costs associated with the leverage. If interest and other ongoing costs of leverage exceed a Fund’s return on assets purchased with leverage proceeds, income to shareholders is lower than if the Fund had not used leverage.

Furthermore, the value of each Fund’s portfolio investments generally varies inversely with the direction of long-term interest rates, although other factors can also influence the value of portfolio investments. As a result, changes in interest rates can influence each Fund’s NAV positively or negatively in addition to the impact on each Fund’s performance from leverage. Changes in the direction of interest rates are difficult to predict accurately, and there is no assurance that a Fund’s leveraging strategy will be successful.

The use of leverage also generally causes greater changes in each Fund’s NAV and dividend rates than comparable portfolios without leverage. In a declining market, leverage is likely to cause a greater decline in the NAV of a Fund’s shares than if the Fund were not leveraged. In addition, each Fund may be required to sell portfolio securities at inopportune times or at distressed values in order to comply with regulatory requirements applicable to the use of leverage or as required by the terms of the leverage instruments, which may cause the Funds to incur losses. The use of leverage may limit a Fund’s ability to invest in certain types of securities or use certain types of hedging strategies. Each Fund incurs expenses in connection with the use of leverage, all of which are borne by each Fund’s shareholders and may reduce income.

|

| Derivative Financial Instruments |

The Funds may invest in various derivative financial instruments. These instruments are used to obtain exposure to a security, commodity, index, market, and/or other assets without owning or taking physical custody of securities, commodities and/or other referenced assets or to manage market, equity, credit, interest rate, foreign currency exchange rate, commodity and/or other risks. Derivative financial instruments may give rise to a form of economic leverage and involve risks, including the imperfect correlation between the value of a derivative financial instrument and the underlying asset, possible default of the counterparty to the

transaction or illiquidity of the instrument. The Funds’ successful use of a derivative financial instrument depends on the investment adviser’s ability to predict pertinent market movements accurately, which cannot be assured. The use of these instruments may result in losses greater than if they had not been used, may limit the amount of appreciation a Fund can realize on an investment and/or may result in lower distributions paid to shareholders. The Funds’ investments in these instruments, if any, are discussed in detail in the Notes to Financial Statements.

| | | | | | |

| | | BLACKROCK ALLOCATION TARGET SHARES | | SEPTEMBER 30, 2017 | | 17 |

| | | | |

| Schedule of Investments September 30, 2017 (Unaudited) | | | Series A Portfolio | |

| | | (Percentages shown are based on Net Assets) | |

| | | | | | | | |

| Asset-Backed Securities | | Par

(000) | | | Value | |

AIMCO CLO, Series 2015-AA, Class E, (3 mo. LIBOR US + 7.820%), 9.12%, 1/15/28 (a)(b) | | $ | 1,000 | | | $ | 1,015,676 | |

Ajax Mortgage Loan Trust: | | | | | | | | |

Series 2016-1, Class A, 4.25%, 7/25/47 (b)(c) | | | 257 | | | | 255,829 | |

Series 2016-B, Class A, 4.00%, 9/25/65 (b)(c) | | | 149 | | | | 149,083 | |

Allegro CLO II Ltd.: | | | | | | | | |

Series 2014-1A, Class A1R, (3 mo. LIBOR US + 1.310%), 2.62%, 1/21/27 (a)(b)(d) | | | 1,000 | | | | 1,003,576 | |

Series 2014-1A, Class CR, (3 mo. LIBOR US + 3.850%), 5.16%, 1/21/27 (a)(b)(d) | | | 250 | | | | 250,179 | |

Allegro CLO, Ltd., Series 2016-1A, Class D, (3 mo. LIBOR US + 3.850%), 5.13%, 1/15/29 (a)(b) | | | 500 | | | | 506,244 | |

ALM VI Ltd., Series 2012-6A, Class DRR, (3 mo. LIBOR US + 5.450%), 6.75%, 7/15/26 (a)(b) | | | 600 | | | | 598,077 | |

ALM VII Ltd., Series 2012-7A, Class A1R, (3 mo. LIBOR US + 1.480%), 2.78%, 10/15/28 (a)(b) | | | 1,000 | | | | 1,010,665 | |

ALM XIV Ltd., Series 2014-14A, Class BR, (3 mo. LIBOR US + 2.100%), 3.41%, 7/28/26 (a)(b) | | | 1,250 | | | | 1,251,984 | |

AMMC CLO 20 Ltd., Series 2017-20A, Class E, (3 mo. LIBOR US + 5.810%), 7.11%, 4/17/29 (a)(b) | | | 500 | | | | 481,875 | |

Anchorage Capital CLO 3 Ltd., Series 2014-3A, Class BR, (3 mo. LIBOR US + 2.650%), 3.96%, 4/28/26 (a)(b) | | | 500 | | | | 500,526 | |

Anchorage Capital CLO 4 Ltd., Series 2014-4A, Class CR, (3 mo. LIBOR US + 3.400%), 4.71%, 7/28/26 (a)(b)(d) | | | 1,000 | | | | 999,728 | |

Anchorage Capital CLO 5 Ltd., Series 2014-5A, Class CR, (3 mo. LIBOR US + 2.200%), 3.50%, 10/15/26 (a)(b) | | | 1,000 | | | | 1,002,115 | |

Anchorage Capital CLO 8 Ltd., Series 2016-8A, Class D, (3 mo. LIBOR US + 4.200%), 5.51%, 7/28/28 (a)(b) | | | 250 | | | | 252,039 | |

Anchorage Capital CLO Ltd., Series 2013-1A, Class BR, (3 mo. LIBOR US + 2.150%), 0.00%, 10/13/30 (a)(b) | | | 500 | | | | 500,000 | |

Apidos CLO XIX, Series 2014-19A, Class A1R, (3 mo. LIBOR US + 1.200%), 2.50%, 10/17/26 (a)(b) | | | 1,000 | | | | 1,001,428 | |

Apidos CLO XVIII, Series 2014-18A, Class CR, (3 mo. LIBOR US + 3.250%), 4.56%, 7/22/26 (a)(b) | | | 250 | | | | 252,897 | |

Apidos CLO XXI, Series 2015-21A, Class D, 6.85%, 7/18/27 (a) | | | 500 | | | | 500,259 | |

Apidos CLO XXII, Series 2015-22A, Class D, (3 mo. LIBOR US + 6.000%), 7.31%, 10/20/27 (a)(b)(d) | | | 500 | | | | 501,204 | |

| | | | | | | | |

| Asset-Backed Securities | | Par

(000) | | | Value | |

Apidos CLO XXIII, Series 2015-23A, Class D2, (3 mo. LIBOR US + 5.950%), 7.25%, 1/14/27 (a)(b) | | $ | 500 | | | $ | 505,705 | |

Arbor Realty Commercial Real Estate Notes Ltd.: | | | | | | | | |

Series 2016-FL1A, Class A, (1 mo. LIBOR US + 1.700%), 2.93%, 9/15/26 (a)(b)(d) | | | 190 | | | | 191,493 | |

Series 2017-FL1, Class A, (1 mo. LIBOR US + 1.300%), 2.53%, 4/15/27 (a)(b) | | | 1,920 | | | | 1,938,067 | |

Series 2017-FL1, Class B, (1 mo. LIBOR US + 2.500%), 3.73%, 4/15/27 (a)(b)(d) | | | 438 | | | | 440,051 | |

Ares XXXIII CLO Ltd.: | | | | | | | | |

Series 2015-1A, Class CR, (3 mo. LIBOR US + 4.200%), 5.52%, 12/05/25 (a)(b) | | | 250 | | | | 253,688 | |

Series 2015-1A, Class D, (3 mo. LIBOR US + 6.230%), 7.55%, 12/05/25 (a)(b) | | | 500 | | | | 503,053 | |

Ares XXXIV CLO Ltd., Series 2015-2A, Class E2, (3 mo. LIBOR US + 5.200%), 6.51%, 7/29/26 (a)(b) | | | 500 | | | | 496,879 | |

Ares XXXIX CLO Ltd., Series 2016-39A, Class E, (3 mo. LIBOR US + 7.250%), 8.55%, 7/18/28 (a)(b) | | | 250 | | | | 251,278 | |

Argent Mortgage Loan Trust, Series 2005-W1, Class A2, (1 mo. LIBOR US + 0.480%), 1.72%, 5/25/35 (a)(d) | | | 80 | | | | 61,365 | |

Atrium VIII, Series 8A, Class DR, (3 mo. LIBOR US + 4.000%), 5.31%, 10/23/24 (a)(b) | | | 325 | | | | 327,548 | |

Atrium X, Series 10A, Class E (3 mo. LIBOR US + 4.500%), 5.80%, 7/16/25 (a)(b) | | | 650 | | | | 646,923 | |

BA Credit Card Trust, Series 2015-A2, Class A 1.36%, 9/15/20 | | | 5,000 | | | | 4,997,672 | |

Babson CLO Ltd., Series 2016-1A, Class E, (3 mo. LIBOR US + 6.550%), 7.86%, 4/23/27 (a)(b) | | | 250 | | | | 251,864 | |

Ballyrock CLO LLC, Series 2014-1A, Class CR, (3 mo. LIBOR US + 3.650%), 4.96%, 10/20/26 (a)(b)(d) | | | 1,750 | | | | 1,736,142 | |

Battalion CLO IV Ltd., Series 2013-4A, Class A1R, (3 mo. LIBOR US + 1.140%), 2.45%, 10/22/25 (a)(b) | | | 1,000 | | | | 1,001,004 | |

Bayview Financial Revolving Asset Trust: | | | | | | | | |

Series 2005-E, Class A1, (1 mo. LIBOR US + 1.000%), 2.23%, 12/28/40 (a)(b) | | | 3,740 | | | | 3,311,704 | |

Series 2005-E, Class A2A, (1 mo. LIBOR US + 0.930%), 2.16%, 12/28/40 (a)(b) | | | 2,616 | | | | 2,286,801 | |

Bear Stearns Asset-Backed Securities I Trust: | | | | | | | | |

Series 2007-HE2, Class 1A4, (1 mo. LIBOR US + 0.320%), 1.56%, 3/25/37 (a) | | | 860 | | | | 620,430 | |

Series 2007-HE2, Class 23A, (1 mo. LIBOR US + 0.140%), 1.38%, 3/25/37 (a) | | | 162 | | | | 155,752 | |

| | | | | | | | | | |

| Portfolio Abbreviations |

| ABS | | Asset-Backed Security | | LIBOR | | London Interbank Offered Rate | | | | |

| AGM | | Assured Guaranty Municipal Corp. | | OTC | | Over-the-counter | | | | |

| AMT | | Alternative Minimum Tax (subject to) | | RAN | | Revenue Anticipation Notes | | | | |

| BAN | | Bond Anticipation Notes | | RB | | Revenue Bonds | | | | |

| CLO | | Collateralized Loan Obligation | | REMIC | | Real Estate Mortgage Investment Conduit | | | | |

| DAC | | Designated Activity Company | | S&P | | S&P Global Ratings | | | | |

| EDA | | Economic Development Authority | | TBA | | To-be-announced | | | | |

| GO | | General Obligation Bonds | | USD | | US Dollar | | | | |

| IDA | | Industrial Development Authority | | | | | | | | |

See Notes to Financial Statements.

| | | | | | |

| 18 | | BLACKROCK ALLOCATION TARGET SHARES | | SEPTEMBER 30, 2017 | | |

| | | | |

| Schedule of Investments (continued) | | | Series A Portfolio | |

| | | | |

| | | | | | | | |

| Asset-Backed Securities | | Par

(000) | | | Value | |

Series 2007-HE3, Class 1A4, (1 mo. LIBOR US + 0.350%), 1.59%, 4/25/37 (a) | | $ | 327 | | | $ | 255,461 | |

Bear Stearns Asset-Backed Securities Trust, Series 2005-4, Class M2, (1 mo. LIBOR US + 1.200%), 2.44%, 1/25/36 (a) | | | 367 | | | | 354,134 | |

Benefit Street Partners CLO IV Ltd., Series 2014-IVA, Class A1R, (3 mo. LIBOR US + 1.490%), 2.80%, 1/20/29 (a)(b) | | | 500 | | | | 505,533 | |

BlueMountain CLO Ltd.: | | | | | | | | |

Series 2013-2A, Class A, (3 mo. LIBOR US + 1.200%), 2.51%, 1/22/25 (a)(b) | | | 1,000 | | | | 1,000,113 | |

Series 2015-1A, Class D, (3 mo. LIBOR US + 5.450%), 6.75%, 4/13/27 (a)(b) | | | 250 | | | | 250,509 | |

Series 2015-2A, Class E, (3 mo. LIBOR US + 5.350%), 6.65%, 7/18/27 (a)(b) | | | 250 | | | | 246,795 | |

Canyon Capital CLO Ltd.: | | | | | | | | |

Series 2006-1A, Class A1, (3 mo. LIBOR US + 0.250%), 1.57%, 12/15/20 (a)(b) | | | 177 | | | | 175,962 | |

Series 2006-1A, Class C, (3 mo. LIBOR US + 0.700%), 2.02%, 12/15/20 (a)(b) | | | 250 | | | | 247,591 | |

Carlyle Global Market Strategies CLO Ltd.: | | | | | | | | |

Series 2012-3A, Class CR, (3 mo. LIBOR US + 4.100%), 5.40%, 10/14/28 (a)(b) | | | 500 | | | | 504,077 | |

Series 2012-4A, Class AR, (3 mo. LIBOR US + 1.450%), 2.76%, 1/20/29 (a)(b) | | | 935 | | | | 944,554 | |

Series 2013-3A, Class B, (3 mo. LIBOR US + 2.650%), 3.95%, 7/15/25 (a)(b) | | | 250 | | | | 250,026 | |

Series 2013-3A, Class C, (3 mo. LIBOR US + 3.400%), 4.70%, 7/15/25 (a)(b) | | | 250 | | | | 250,029 | |

Series 2014-1A, Class CR, (3 mo. LIBOR US + 2.750%), 4.05%, 4/17/25 (a)(b) | | | 500 | | | | 502,173 | |

Series 2014-3A, Class C1R, (3 mo. LIBOR US + 3.270%), 4.59%, 7/27/26 (a)(b) | | | 1,000 | | | | 1,011,506 | |

Series 2014-3A, Class D1, (3 mo. LIBOR US + 5.100%), 6.42%, 7/27/26 (a)(b) | | | 1,400 | | | | 1,402,839 | |

Series 2014-3A, Class D2R, (3 mo. LIBOR US + 5.750%), 7.07%, 7/27/26 (a)(b)(d) | | | 500 | | | | 502,265 | |

Series 2014-5A, Class A1R, (3 mo. LIBOR US + 1.140%), 2.44%, 10/16/25 (a)(b) | | | 1,000 | | | | 1,000,941 | |

Series 2015-4A, Class D, (3 mo. LIBOR US + 6.100%), 7.41%, 10/20/27 (a)(b) | | | 500 | | | | 508,620 | |

Series 2015-4A, Class SBB1, (3 mo. LIBOR US + 8.500%), 9.81%, 10/20/27 (a)(b) | | | 154 | | | | 155,701 | |

Series 2016-1A, Class D, (3 mo. LIBOR US + 7.600%), 8.91%, 4/20/27 (a)(b) | | | 250 | | | | 254,954 | |

Carrington Mortgage Loan Trust: | | | | | | | | |

Series 2006-FRE2, Class A2, (1 mo. LIBOR US + 0.120%), 1.36%, 10/25/36 (a) | | | 335 | | | | 223,170 | |

Series 2006-FRE2, Class A3, (1 mo. LIBOR US + 0.160%), 1.40%, 10/25/36 (a) | | | 178 | | | | 118,979 | |

Series 2006-FRE2, Class A4, (1 mo. LIBOR US + 0.250%), 1.49%, 10/25/36 (a) | | | 2,732 | | | | 1,851,375 | |

Series 2006-NC2, Class A3, (1 mo. LIBOR US + 0.150%), 1.39%, 6/25/36 (a) | | | 781 | | | | 767,116 | |

Series 2006-NC3, Class A4, (1 mo. LIBOR US + 0.240%), 1.48%, 8/25/36 (a) | | | 630 | | | | 410,343 | |

Series 2006-NC4, Class A3, (1 mo. LIBOR US + 0.160%), 1.40%, 10/25/36 (a) | | | 100 | | | | 85,937 | |

CBAM Ltd.: | | | | | | | | |

Series 2017-3A, Class A, (3 mo. LIBOR US + 1.230%), 2.60%, 10/17/29 (a)(b) | | | 2,500 | | | | 2,500,000 | |

Series 2017-3A, Class B1, (3 mo. LIBOR US + 1.700%), 3.07%, 10/17/29 (a)(b) | | | 500 | | | | 500,000 | |

| | | | | | | | |

| Asset-Backed Securities | | Par

(000) | | | Value | |

Series 2017-3A, Class E1, (3 mo. LIBOR US + 6.500%), 7.87%, 10/17/29 (a)(b) | | $ | 1,000 | | | $ | 1,000,000 | |

C-BASS Trust: | | | | | | | | |

Series 2006-CB9, Class A2, (1 mo. LIBOR US + 0.110%), 1.35%, 11/25/36 (a) | | | 65 | | | | 40,893 | |

Series 2006-CB9, Class A4, (1 mo. LIBOR US + 0.230%), 1.47%, 11/25/36 (a) | | | 17 | | | | 10,959 | |

Series 2007-CB1, Class AF2, 3.75%, 1/25/37 (c) | | | 323 | | | | 157,947 | |

Series 2007-CB5, Class A2, (1 mo. LIBOR US + 0.170%), 1.41%, 4/25/37 (a) | | | 65 | | | | 49,923 | |

Chase Issuance Trust, Series 2015-A5, Class A5 1.36%, 4/15/20 | | | 1,708 | | | | 1,707,205 | |

CIFC Funding Ltd.: | | | | | | | | |

Series 2012-3A, Class A3R, (3 mo. LIBOR US + 2.700%), 4.01%, 1/29/25 (a)(b) | | | 250 | | | | 250,073 | |

Series 2014-3A, Class C1R, (3 mo. LIBOR US + 1.900%), 3.21%, 7/22/26 (a)(b) | | | 250 | | | | 250,886 | |

Series 2014-4A, Class A1R, (3 mo. LIBOR US + 1.380%), 2.68%, 10/17/26 (a)(b) | | | 500 | | | | 502,134 | |

Series 2014-5A, Class CR, (3 mo. LIBOR US + 2.700%), 4.00%, 1/17/27 (a)(b) | | | 750 | | | | 753,649 | |

Series 2016-1A, Class E, (3 mo. LIBOR US + 6.750%), 8.06%, 10/21/28 (a)(b) | | | 500 | | | | 512,191 | |

Clear Creek CLO Ltd., Series 2015-1A, Class E, (3 mo. LIBOR US + 5.750%), 7.06%, 4/20/27 (a)(b) | | | 1,000 | | | | 999,979 | |

Conseco Finance Corp.: | | | | | | | | |

Series 1996-10, Class B1, 7.24%, 11/15/28 (e) | | | 64 | | | | 50,223 | |

Series 1998-4, Class M1, 6.83%, 4/01/30 (e) | | | 1,237 | | | | 1,092,334 | |

Series 1998-8, Class M1, 6.98%, 9/01/30 (e) | | | 1,190 | | | | 989,829 | |

Conseco Finance Securitizations Corp.: | | | | | | | | |

Series 2000-1, Class A5, 8.06%, 9/01/29 (e) | | | 2,465 | | | | 1,394,006 | |

Series 2000-4, Class A6, 8.31%, 5/01/32 (e) | | | 2,456 | | | | 1,351,027 | |

Countrywide Asset-Backed Certificates: | | | | | | | | |

Series 2006-11, Class 3AV2, (1 mo. LIBOR US + 0.160%), 1.40%, 9/25/46 (a) | | | 18 | | | | 17,233 | |

Series 2007-S3, Class A3, (1 mo. LIBOR US + 0.380%), 1.62%, 5/25/37 (a) | | | 191 | | | | 171,319 | |

Countrywide Revolving Home Equity Loan Trust, Series 2004-U, Class 2A, (1 mo. LIBOR US + 0.270%), 1.50%, 3/15/34 (a) | | | 71 | | | | 57,087 | |

Credit-Based Asset Servicing & Securitization LLC: | | | | | | | | |

Series 2006-CB2, Class AF4, 3.43%, 12/25/36 (c) | | | 27 | | | | 21,121 | |

Series 2006-MH1, Class B1, 6.25%, 10/25/36 (b)(c) | | | 2,900 | | | | 2,987,446 | |

Series 2006-SL1, Class A3, (1 mo. LIBOR US + 0.220%), 1.46%, 9/25/36 (a)(b) | | | 6,848 | | | | 1,259,301 | |

Series 2007-RP1, Class A, (1 mo. LIBOR US + 0.310%), 1.55%, 5/25/46 (a)(b) | | | 92 | | | | 76,053 | |

CWHEQ Home Equity Loan Trust, Series 2006-S2, Class A3, 5.84%, 7/25/27 | | | 757 | | | | 914,708 | |

CWHEQ Revolving Home Equity Loan Resuritization Trust: | | | | | | | | |

Series 2006-RES, Class 4Q1B, (1 mo. LIBOR US + 0.300%), 1.53%, 12/15/33 (a)(b)(d) | | | 56 | | | | 50,906 | |

Series 2006-RES, Class 5B1B, (1 mo. LIBOR US + 0.190%), 1.42%, 5/15/35 (a)(b)(d) | | | 22 | | | | 18,931 | |

See Notes to Financial Statements.

| | | | | | |

| | | BLACKROCK ALLOCATION TARGET SHARES | | SEPTEMBER 30, 2017 | | 19 |

| | | | |

| Schedule of Investments (continued) | | | Series A Portfolio | |

| | | | |

| | | | | | | | |

| Asset-Backed Securities | | Par

(000) | | | Value | |

CWHEQ Revolving Home Equity Loan Trust, Series 2006-G, Class 2A, (1 mo. LIBOR US + 0.150%), 1.38%, 10/15/36 (a) | | $ | 557 | | | $ | 503,121 | |

Dryden XXXI Senior Loan Fund, Series 2014-31A, Class AR, (3 mo. LIBOR US + 1.080%), 2.38%, 4/18/26 (a)(b) | | | 1,000 | | | | 1,003,973 | |

Dryden XXXVII Senior Loan Fund, Series 2015-37A, Class E, (3 mo. LIBOR US + 5.400%), 6.70%, 4/15/27 (a)(b) | | | 1,650 | | | | 1,644,515 | |

First Franklin Mortgage Loan Trust: | | | | | | | | |

Series 2006-FF5, Class 2A3, (1 mo. LIBOR US + 0.160%), 1.40%, 4/25/36 (a) | | | 67 | | | | 63,280 | |

Series 2006-FF16, Class 2A3, (1 mo. LIBOR US + 0.140%), 1.38%, 12/25/36 (a) | | | 738 | | | | 464,187 | |

Series 2006-FF17, Class A5, (1 mo. LIBOR US + 0.150%), 1.39%, 12/25/36 (a) | | | 3,563 | | | | 2,964,712 | |

Galaxy XVI CLO Ltd., Series 2013-16A, Class CR, (3 mo. LIBOR US + 2.250%), 3.56%, 11/16/25 (a)(b) | | | 1,500 | | | | 1,503,863 | |

Galaxy XXI CLO Ltd., Series 2015-21A, Class E2, (3 mo. LIBOR US + 6.500%), 7.81%, 1/20/28 (a)(b) | | | 500 | | | | 497,879 | |

GCAT LLC, Series 2017-4, Class A1, 3.23%, 5/25/22 (b)(c) | | | 1,933 | | | | 1,938,699 | |

GE-WMC Asset-Backed Pass-Through Certificates, Series 2005-2, Class A2C, (1 mo. LIBOR US + 0.250%), 1.49%, 12/25/35 (a) | | | 33 | | | | 32,458 | |

Gilbert Park CLO Ltd., Series 2017-1A, Class E, (3 mo. LIBOR US + 6.400%), 0.00%, 10/15/30 (a)(b) | | | 1,000 | | | | 1,000,000 | |

GMACM Home Equity Loan Trust, Series 2006-HE1, Class A, (1 mo. LIBOR US + 0.210%), 1.45%, 11/25/36 (a) | | | 592 | | | | 616,856 | |

GoldenTree Loan Opportunities VIII Ltd., Series 2014-8A, Class AR, (3 mo. LIBOR US + 1.210%), 2.52%, 4/19/26 (a)(b) | | | 1,000 | | | | 1,003,554 | |

Greywolf CLO IV Ltd., Series 2014-2A, Class BR, (3 mo. LIBOR US + 2.350%), 3.65%, 1/17/27 (a)(b) | | | 500 | | | | 500,289 | |