UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

ANNUAL REPORT

¨ REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXHANGE ACT OF 1934

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934.

For the Fiscal Year Ended December 31, 2003

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934.

For transition period from ____ to ______

Commission File Number: 0-1222108

PMI VENTURES LTD.

(Exact name of Registrant as specified in its charter)

Not Applicable

(Translation of Registrant’s name into English)

Canada

(Jurisdiction of Incorporation or Organization)

Suite 511 – 475 Howe Street, Vancouver, British Columbia V6C 2T8

(Address of Principal executive office)

Securities registered or to be registered pursuant to Section 12(b) of the Act:Not Applicable

Securities registered or to be registered pursuant to Section 12(g) of the Act:Common Shares, Without Par Value

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:None

Number of outstanding shares of each of the Company’s classes of capital or common stock as of June 22, 2004: 23,475,396Common Shares, Without Par Value

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days: Yes: x No: ¨

Indicate by check mark which financial statement item the Registrant has elected to follow: Item 17 x Item 18 ¨

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the Registrant has filed all documents and reports required to be filed by Section 12, 14 or 15(d) of the Securities Exchange Act of 1934 subsequent tot he distribution of securities under a plan confirmed by court Yes: ¨ No: ¨

INFORMATION TO BE INCLUDED IN THE REPORT

Convention

In this Annual Report all references to "Canada" are references to The Dominion of Canada. All references to the "Government" are references to the government of Canada. Unless otherwise noted all references to "shares" or "common stock" are references to the common shares of PMI Ventures Ltd.

In this document, all references to "SEC" refer to the United States Securities and Exchange Commission. The Company’s reporting currency is the Canadian dollar. References to"$", "Cdn Dollars", or “Cdn$” are to the currency of Canada and all references to "US Dollars" or "US$" are to the currency of the United States of America. Solely for the convenience of the reader, this Annual Report contains translations of certain Cdn Dollar amounts into US Dollar amounts at specified rates.

Measurement Conversion Information

In this Annual Report, metric measures are used with respect to mineral properties described herein. For ease of reference, the following conversion factors are provided:

| Imperial Measure | Metric Unit | Imperial Measure | Metric Unit |

| 1 mile | 1.609 kilometres | 2,204 pounds | 1 tonne |

| 1 yard | 0.9144 metre | 2,000 pounds/1 short ton | 0.907 tonnes |

| 1 acre | 0.405 hectare | 1 troy ounce | 31.103 grams |

| 1 US gallon | 3.785 litres | 1 imperial gallon | 4.546 litres |

Forward Looking Statements

This Annual Report includes "forward-looking statements" A shareholder or prospective shareholder should bear this in mind when assessing the Company's business. All statements, other than statements of historical facts, included in this registration statement, including, without limitation, the statements under and located elsewhere herein regarding industry prospects and the Company's financial position are forward-looking statements. Although the Company believes that the expectations reflected in such forward looking statements are reasonable, it can give no assurance that such expectation will prove to have been correct. There is significant risk that actual results will vary, perhaps materially from results projected depending on such factors as changes in general economic conditions, financial markets, copper prices and other metals, technology and exploration hazards.

GEOLOGIC TIME

The geological history of the earth is divided into Periods and sub-divided into Eras, based on ages as outlined below:

2

| Number of Years | ||

| Name of Period | Name of Era | before Present |

| (Millions) | ||

| Quaternary | Holocene | 0 to 0.4 |

| Pleistocene | 0.4 to 1.8 | |

| Tertiary | Pliocene | 1.8 to 5.0 |

| Miocene | 5.0 to 24 | |

| Oligocene | 24 to 38 | |

| Eocene | 38 to 56 | |

| Paleocene | 56 to 66 | |

| Mesozoic | Cretaceous | 66 to 140 |

| Jurassic | 140 to 200 | |

| Triassic | 200 to 250 | |

| Paleozoic | Permian | 250 to 290 |

| Carboniferous | 290 to 365 | |

| Devonian | 365 to 405 | |

| Silurian | 405 to 425 | |

| Ordovician | 425 to 500 | |

| Cambrian | 500 to 570 | |

| Precambrian | Precambrian | > 570 |

GLOSSARY OF MINING TERMS

The following are abbreviations and definitions of terms commonly used in the mining industry and this Annual Report:

| “Disseminated” or “dissemination” | is a descriptive term referring to mineral grains, which are scattered evenly throughout a rock |

| “Geological Time” | that is recorded in the succession of rocks |

| “Indicated Mineral Resource” | is that part of a Mineral Resource for which quantity, grade or quality, densities, shape and physical characteristics, can be estimated with a level of confidence sufficient to allow the appropriate application of technical and economic parameters, to support mine planning and evaluation of the economic viability of the deposit. The estimate is based on detailed and reliable exploration and testing information gathered through appropriate techniques from locations such as outcrops, trenches, pits, workings and drill holes that are spaced closely enough for geological and grade continuity to be reasonably assumed |

| “Inferred Mineral Resource” | is that part of a Mineral Resource for which quantity and grade or quality can be estimated on the basis of geological evidence and limited sampling and reasonably assumed, but not verified, geological and grade continuity. The estimate is based on limited information and sampling gathered through appropriate techniques from locations such as outcrops, trenches, pits, workings and drill holes |

3

| “Measured Mineral Resource” | is that part of a Mineral Resource for which quantity, grade or quality, densities, shape, physical characteristics are so well established that they can be estimated with confidence sufficient to allow the appropriate application of technical and economic parameters, to support production planning and evaluation of the economic viability of the deposit. The estimate is based on detailed and reliable exploration, sampling and testing information gathered through appropriate techniques from locations such as outcrops, trenches, pits, workings and drill holes that are spaced closely enough to confirm both geological and grade continuity |

| “Metallurgy” | is the science and art of extraction of metals from their ores and preparing them for use |

| “Mineral Resource” | is a concentration or occurrence of natural, solid, inorganic or fossilized organic material in or on the Earth's crust in such form and quantity and of such a grade or quality that it has reasonable prospects for economic extraction. The location, quantity, grade, geological characteristics and continuity of a Mineral Resource are known, estimated or interpreted from specific geological evidence and knowledge |

| “Mineralization” | is the process by which minerals are introduced and concentrated within a host rock, and the product of this process |

| “National Instrument 43-101” | is an instrument made under theSecurities Actof British Columbia for standards of disclosure for mineral projects |

GLOSSARY OF NON-MINING TERMS

In this Annual Report, unless there is something in the subject matter or context inconsistent therewith, the following capitalized words and terms have the following meanings:

| “Act” | means the Securities Exchange Act of 1934 |

| “affiliate” | has the meaning ascribed thereto in theSecurities Act (British Columbia), as amended |

| “BC Act” | means theBusiness Corporations Act (British Columbia), as amended |

| “Common Shares” | means the common shares in the capital of the Company as presently constituted |

| “Exchange” | means the TSX Venture Exchange of Toronto, Ontario, Canada |

PART I

Item 1. IDENTITY OF DIRECTORS SENIOR MANAGEMENT AND ADVISERS

Not Applicable

Item 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not Applicable.

4

Item 3. KEY INFORMATION

A. Selected Financial Data

Currency Exchange Rate Information:

The rate of exchange means that noon buying rate in New York City for cable transfer in Canadian dollars as certified for customs proposed by the Federal Reserve Bank of New York. The average rate means the average of the exchange rates on the last date of each month during a year.

| 2003 | 2002 | 2001 | 2000 | 1999 | |

| High | $1.5747 | $1.6003 | $1.6034 | $1.5583 | $1.5475 |

| Low | $1.3484 | $1.5593 | $1.4935 | $1.4318 | $1.4420 |

| Average for Period | $1.4615 | $1.5597 | $1.5494 | $1.4854 | $1.4857 |

| End of Period | $1.3484 | $1.5593 | $1.5928 | $1.4995 | $1.4433 |

The exchange rate on June 22, 2004 was $1.3616.

The high and low exchange rates for the most recent six months are as follows:

| Dec 2003 | Jan 2004 | Feb 2004 | March 2004 | April 2004 | May 2004 | |

| High | 1.3292 | 1.3380 | 1.3432 | 1.3476 | 1.3707 | 1.3968 |

| Low | 1.2924 | 1.2236 | 1.3102 | 1.3079 | 1.3093 | 1.3448 |

Financial Information

The following table sets forth, for the periods indicated, selected financial and operating data for the Company which information was derived from the audited financial statements of the Company which are included elsewhere herein. The selected financial data provided below are not necessarily indicative of the future results of operations or financial performance of the Company. To the best of management’s knowledge, the Company has not paid any dividends on the Common Shares and it does not expect to pay dividends in the foreseeable future.

The year end Financial Statements of the Company have been audited by Davidson & Company, independent chartered accountants. They are maintained in Canadian dollars, and have been prepared in accordance with accounting principles generally accepted in Canada. Comparison of Canadian GAAP and United States GAAP are set forth in the notes to the Financial Statements of the Company.

5

| Year Ending December 31 | ||||||||

| 2003 | 2002 | 2001 | 2000 | |||||

| Amounts in Accordance with | ||||||||

| Canadian GAAP (presented in | ||||||||

| Canadian dollars): | $17,637 | $11,188 | $5,343 | $6,192 | ||||

| Income | $4,634,113 | $189,600 | $378,953 | ($141,204 | ) | |||

| Total Assets | $2,220,161 | $161,740 | ($55,116 | ) | $4,043,780 | |||

| Net working capital | 4,388,590 | $165,362 | ($33,346 | ) | ($141,204 | ) | ||

| Shareholders’ equity | ($1,018,341 | ) | ($506,134 | ) | ($107,768 | ) | $314,668 | |

| Loss from operations | ||||||||

| Loss per share (basic and | ||||||||

| diluted) | ($0.07 | ) | ($0.09 | ) | ($0.04 | ) | $0.11 | |

| Weighted average number of | ||||||||

| common shares outstanding | ||||||||

| basic and diluted) | 14,627,645 | 5,742,082 | 2,840,718 | 2,828,390 | ||||

| Amounts in Accordance with | ||||||||

| U.S. GAAP (presented in | ||||||||

| Canadian dollars): | $2,526,223 | $189,600 | $378,953 | $6,192 | ||||

| Total assets | $2,220,161 | $161,740 | $55,116 | ($141,204 | ) | |||

| Net working capital | $2,280,700 | $165,362 | ($33,346 | ) | $4,043,780 | |||

| Shareholders’ equity | ($3,126,231 | ) | ($594,471 | ) | ($114,012 | ) | ($141,204 | ) |

| Net Loss | ||||||||

| Loss per share (basic and | ||||||||

| diluted) | ($0.21 | ) | ($0.10 | ) | ($0.04 | ) | $0.11 | |

| Weighted average number of | ||||||||

| common shares outstanding | ||||||||

| (basic and diluted) | 14,565,562 | 5,679,999 | 2,778,635 | 2,766,306 | ||||

B. Capitalization and Indebtedness

Not Applicable.

C. Reasons for Offer

Not Applicable.

D. Risk Factors

The following risks relate specifically to the Company's business and should be considered carefully. The Company's business, financial condition and results of operations could be materially and adversely affected by any of the following risks.

(1) The Company's limited operating history makes it difficult to evaluate the Company’s current business and forecast future results

The Company has only a limited operating history on which to base an evaluation of the Company's current business and prospects, each of which should be considered in light of the risks, expenses and problems frequently encountered in the early stages of development of all companies. This limited operating history leads the Company to believe that period-to-period comparisons of its operating results

6

may not be meaningful and that the results for any particular period should not be relied upon as an indication of future performance.

(2) The mineral properties of the Company are in the exploration stage only and consequently exploration of the Company’s mineral properties may not result in any discoveries of commercial bodies of mineralization

The property interests owned by the Company or in which it has an option to earn an interest are in the exploration stages only, are without known bodies of commercial mineralization and have no ongoing mining operations. Mineral exploration involves a high degree of risk and few properties which are explored are ultimately developed into producing mines. Exploration of the Company’s mineral exploration may not result in any discoveries of commercial bodies of mineralization. If the Company’s efforts do not result in any discovery of commercial mineralization, the Company will be forced to look for other exploration projects or cease operations.

(3) In order to explore its mineral properties the Company will need additional financing, failing which the Company could go out of business

If the Company wishes to retain its mineral properties, or participate in additional mineral exploration programs, it would need to raise additional financing. There is no assurance that such financing will be available on terms acceptable to the Company or at all. Failure to generate additional funds could result in the Company going out of business.

(4) The Company has no significant source of operating cash flow and failure to generate revenues in the future could cause the Company to go out of business

As none of the Company’s mineral properties currently have ore reserves the Company has no revenues from operations. The Company has limited financial resources. The Company expects that its existing capital requirements arising from the evaluation of its existing mineral properties and fulfilling its exploration commitments for the next 12 months will be met from the Company’s working capital which as at June 8, 2004 was $453,145 and from additional financing efforts. The Company’s ability to achieve and maintain profitability and positive cash flow is dependent upon the Company’s:

- ability to locate a profitable mineral property;

- ability to generate revenues; and

- ability to reduce exploration costs.

Based upon current plans, the Company expects to incur operating losses in future periods. This will happen because there are continuing expenses associated with the holding and exploration of the Company’s mineral properties. The Company may not be successful in generating revenues in the future. Failure to generate revenues could cause the Company to go out of business.

Additional funds raised by the Company through the issuance of equity or convertible debt securities will cause the Company’s current stockholders to experience dilution. Such securities may grant rights, preferences or privileges senior to those of the Company’s common stockholders.

The Company does not have any contractual restrictions on its ability to incur debt and, accordingly, the Company could incur significant amounts of indebtedness to finance its operations. Any such indebtedness could contain covenants, which would restrict the Company’s operations. The Company does not plan on entering into any debt obligations in the next twelve months.

7

(5) The possibility of any of the Company’s mineral properties ever having ore reserves is extremely remote

The Company has no known ore reserves. The possibility of any of the Company’s mineral properties ever having ore reserves is extremely remote and any funds spent on exploration will probably be lost. The Company’s success depends upon finding and developing an ore reserve. If the Company does not find an ore reserve containing gold, precious or non-precious metals, either because it does not have the money to do so or because it is not economically feasible to do it, the Company will cease operations.

(6) The Company’s mineral properties are in a foreign country and as such the Company’s business may be exposed to various levels of political, economic and other risks and uncertainties

The Company’s mineral properties are located in Ghana, West Africa. As the Company’s business is carried on in a foreign country it is exposed to various levels of political, economic and other risks and uncertainties. These risks and uncertainties include, but not limited to, terrorism, hostage taking, military repression, expropriation, changing tax laws, extreme fluctuations in currency exchange rates, high rates of inflation and labour unrest. Ghana’s status as a developing country may make it more difficult for the Company to obtain any required exploration financing for its project.

Changes, if any, in mining or investment policies or shifts in political attitude in Ghana may adversely affect the Company’s operations. Operations may be effected in varying degrees by government regulations with respect to, but not limited to restrictions on expropriation of property, foreign investment, maintenance of claims, environmental legalisation, land use and land claims of local people.

Failure to comply strictly with applicable laws, regulations and local practices relating to mineral right applications and tenure could result in loss, reduction or expropriation of entitlements, or the imposition of additional local or foreign parties as joint venture partners with carried or other interests.

The occurrence of these various factors and uncertainties cannot be accurately predicted and could have an adverse effect on the Company’s operations.

(7) As the Company is a Canadian company it may be difficult for U.S. shareholders of the Company to effect service on the Company or to realize on judgments obtained against the Company in the United States

The Company is a Canadian corporation. All of its directors and officers are residents of Canada and a significant part of its assets are, or will be, located outside of the United States. As a result, it may be difficult for shareholders resident in the United States to effect service within the United States upon the Company, directors, officers or experts who are not residents of the United States, or to realize in the United States judgments of courts of the United States predicated upon civil liability of any of the Company, directors or officers under the United States federal securities laws. If a judgment is obtained in the U.S. courts based on civil liability provisions of the U.S. federal securities laws against the Company or its directors or officers, it will be difficult to enforce the judgment in the Canadian courts against the Company and any of the Company’s non-U.S. resident executive officers or directors. Accordingly, United States shareholders may be forced to bring actions against the Company and its respective directors and officers under Canadian law and in Canadian courts in order to enforce any claims that they may have against the Company or its directors and officers. Nevertheless, it may be difficult for United States shareholders to bring an original action in the Canadian courts to enforce liabilities based on the U.S. federal securities laws against the Company and any of the Company’s non-U.S. resident executive officers or directors.

8

(8) The mineral exploitation industry is intensely competitive in all its phases and the Company competes with many companies possessing greater financial resources and technical facilities than itself

The mineral exploitation industry is intensely competitive in all its phases. The Company competes with many companies possessing greater financial resources and technical facilities than itself for the acquisition of mineral concessions, claims, leases and other mineral interests as well as for the recruitment and retention of qualified employees. In addition, there is no assurance that even if commercial quantities of minerals are discovered, a ready market will exist for their sale. Factors beyond the control of the Company may affect the marketability of any minerals discovered. These factors include market fluctuations, the proximity and capacity of natural resource markets and processing equipment, international economic and political trends, expectations of inflation, currency exchange fluctuations (specifically, the U.S. dollar relative to other currencies), interest rates and global or regional consumption patterns, speculative activities, government regulations, including regulations relating to prices, taxes, royalties, land tenure, land use, importing and exporting of minerals and environmental protection. The exact effect of these factors cannot be accurately predicted, but the combination of these factors may result in the Company not receiving an adequate return on invested capital or losing its invested capital. As the Company is in the exploration stage, the above factors have had no material impact on current operations.

(9)Substantial expenditures are required to be made by the Company to establish ore reserves and the Company may not either discover minerals in sufficient quantities or grade or may not have the necessary funds required

Substantial expenditures are required to establish ore reserves through drilling. Although substantial benefits may be derived from the discovery of a major mineralized deposit, the Company may not discover minerals in sufficient quantities or grades to justify commercial operation or that the funds required for development may not be obtained on a timely basis. Estimates of reserves and mineral deposits can also be affected by such factors as environmental factors, unforeseen technical difficulties and unusual or unexpected geological formations. In addition, the grade of ore ultimately mined may differ from that indicated by drilling results. Material changes in ore reserves, grades, stripping ratios or recovery rates may affect the economic viability of any project.

(10) Currency fluctuations of the Canadian dollar may affect the Company’s financial position

The Company presently maintains its accounts in Canadian dollars. The Company’s future operations may make the Company subject to foreign currency fluctuations and such fluctuations may materially affect its financial position and results. While, at present, monetary inflation in Ghana is relatively low, in past years the exchange value of the Ghanaian cedis has been subject to significant inflation. The Company has not in the past engaged in hedging activities.

(11) The Company does not presently have insurance covering any of its mineral properties and as a consequence could incur considerable costs

Mineral exploration involves risks, which even a combination of experience, knowledge and careful evaluation may not be able to overcome. Operations in which the Company has a direct or indirect interest may be subject to all the hazards and risks normally incidental to exploration of precious and non-precious metals, any of which could result in work stoppages, damage to property, and possible environmental damage. The Company does not presently have insurance covering any of its mining properties and does not presently intend to obtain liability insurance. As a result of not having insurance,

9

the Company could incur significant costs that could have a materially adverse effect upon its financial condition and even cause the Company to cease operations.

To date, the Company has not experienced any material losses due to hazards arising from its operations.

(12) The Company’s mineral properties may be subject to prior unregistered agreements or transfers or native land claims and as such title to some of the Company’s mineral properties may be affected

Although the Company has sought and received such representations as it has been able to achieve from vendors in connection with options to acquire an interest in its mining properties and has conducted its own investigation of legal title to each such property, the mining properties may be subject to undetected defects.

(15) The price of gold has fluctuated widely in recent years and may adversely affect the economic viability of the Company’s mineral property

The Company’s revenues, if any, are expected to be in large part derived from the mining and sale of gold and other precious and non-precious metals. The price of those commodities has fluctuated widely, particularly in recent years, and is affected by numerous factors beyond the Company’s control including international economic and political trends, expectations of inflation, currency exchange fluctuations, interest rates, consumption patterns, speculative activities and increased production due to new mine developments and improved mining and production methods. The effect of these factors on the price of gold, base and precious metals and therefore the economic viability of the Company’s mineral property cannot be accurately predicted.

(16) The Company’s future performance is dependent on key personnel The loss of the services of any of the Company’s executives or Board of Directors could have a material adverse effect on the Company business

The Company’s performance is substantially dependent on the performance and continued efforts of the Company’s executives and its Board of Directors. The loss of the services of any of the Company’s executives or Board of Directors could have a material adverse effect on the Company business, results of operations and financial condition. The Company currently does not carry any key person insurance on any of the board of directors.

(17) No dividends declared or any likely to be declared in the future

The Company has not declared any dividends and has no present intention of paying any cash dividends on its common stock in the foreseeable future. The payment by the Company of dividends, if any, in the future, rests in the discretion of the Company's Board of Directors and will depend, among other things, upon the Company's earnings, its capital requirements and financial condition, as well as other relevant factors.

(18) The possible issuance of additional shares may impact the value of the Company stock

The Company is authorized to issue up to 100,000,000 shares of common stock without par value. It is the Company's intention to issue more shares. Sales of substantial amounts of common stock (including shares issuable upon the exercise of stock options, the conversion of notes and the exercise of warrants), or the perception that such sales could occur, could materially adversely affect prevailing market prices for the common stock and the ability of the Company to raise equity capital in the future.

10

(19) Forward Looking Statements

This Annual Report includes "forward-looking statements" A shareholder or prospective shareholder should bear this in mind when assessing the Company's business. All statements, other than statements of historical facts, included in this registration statement, including, without limitation, the statements under and located elsewhere herein regarding industry prospects and the Company's financial position are forward-looking statements. Although the Company believes that the expectations reflected in such forward looking statements are reasonable, it can give no assurance that such expectation will prove to have been correct. There is significant risk that actual results will vary, perhaps materially from results projected depending on such factors as changes in general economic conditions, financial markets, gold prices and other metals, technology and exploration hazards.

(20) Conflicts of Interest of certain directors and officers of the Company

Certain of the Company's directors are also directors, officers or shareholders of other companies that are engaged in the business of acquiring, developing and exploiting natural resource properties. Such associations may give rise to conflicts of interest from time to time. Such a conflict poses the risk that the Company may enter into a transaction on terms which place the Company in a worse position than if no conflict existed.

(21) The value and transferability of the Company shares may be adversely impacted by the limited trading market for the Company’s common stock, the penny stock rules and futures share issuance. There is a limited market for the Company’s common stock in the United States

No assurance can be given that a market for the Company’s common stock will be quoted on an exchange in the U.S. or on the NASD's Over the Counter Bulletin Board.

The sale or transfer of the Company common stock by shareholders in the United States may be subject to the so-called "penny stock rules."

Under Rule 15g-9 of the Exchange Act, a broker or dealer may not sell a "penny stock" (as defined in Rule 3a51-1) to or effect the purchase of a penny stock by any person unless:

| (a) | such sale or purchase is exempt from Rule 15g-9; | |

| (b) | prior to the transaction the broker or dealer has (1) approved the person's account for transaction in penny stocks in accordance with Rule15g-9, and (2) received from the person a written agreement to the transaction setting forth the identity and quantity of the penny stock to be purchased; and | |

| (c) | the purchaser has been provided an appropriate disclosure statement as to penny stock investment. |

The SEC adopted regulations that generally define a penny stock to be any equity security other than a security excluded from such definition by Rule 3a51-1. Such exemptions include, but are not limited to (1) an equity security issued by an issuer that has (i) net tangible assets of at least $2,000,000, if such issuer has been in continuous operations for at least three years, (ii) net tangible assets of at least $5,000,000, if such issuer has been in continuous operation for less than three years, or (iii) average revenue of at least $6,000,000 for the preceding three years; (2) except for purposes of Section 7(b) of

11

the Exchange Act and Rule 419, any security that has a price of $5.00 or more; and (3) a security that is authorized or approved for authorization upon notice of issuance for quotation on the NASDAQ Stock Market, Inc.'s Automated Quotation System. It is likely that shares of the Company’s common stock, assuming a market were to develop in the US therefore, will be subject to the regulations on penny stocks; consequently, the market liquidity for the common stock may be adversely affected by such regulations limiting the ability of broker/dealers to sell the Company’s common stock and the ability of shareholders to sell their securities in the secondary market in the US.

Moreover, the Company shares may only be sold or transferred by the Company shareholders in those jurisdictions in the US in which an exemption for such "secondary trading" exists or in which the shares may have been registered.

ITEM 4. INFORMATION ON THE COMPANY

A. History and Development of the Company

The Company was incorporated by registration of its Memorandum and Articles under the BC Act on June 31, 1978 under the name “Denar Mines Ltd.”. Effective August 31st, 1987, the Company changed its name from “Denar Mines Ltd.” to “International Sinabarb Industries Ltd.”. On October 15th 1990, the Company changed its name to “Primero Industries Ltd.”. On June 27th 2001, the Company consolidated its shares on a five old for one new basis and changed its name to “PMI Ventures Ltd.”.

The head office of the Company is located at 511 – 475 Howe Street, Vancouver, British Columbia, V6C 2B3 and consists of 1,132 sq. feet. The Company has entered into a lease agreement that expires on January 1, 2006 at a cost of approximately $2,221 per month with a renewal option. The Company’s telephone number is (604) 682-8089. The registered office of the Company is located at 1100 – 888 Dunsmuir St., Vancouver, British Columbia, V6C 3K4.

The Company is a reporting issuer in the United States and the Provinces of British Columbia, Alberta and Ontario, Canada. The Company’s common stock has been listed for trading on the TSX Venture Exchange (the “Exchange”) for over 10 years under the symbol “PMI”. See “Listing Details and Markets”.

B. Business Overview

The Company is currently engaged in the acquisition and exploration of natural resource properties and currently has, pursuant to a letter agreement dated November 2002 (the “Letter Agreement”) with Goknet Mining Company Limited, a privately held Ghanaian corporation (“Goknet”), the right to acquire up to 85% of Goknet’s interest in eight exploration concessions/applications/options within the Asankrangwa Gold Belt of Southwest Ghana (the “Goknet Properties”). These prospects and properties lie within an area approximately 50 km by 10 km and comprise approximately 400 sq. km.

The mineral properties of the Company are currently in the exploration stage without any known reserves. The Company’s primary objective is to explore and develop its existing mineral properties. Its secondary objective is to locate, evaluate and acquire other mineral properties and to finance their exploration either through equity financing, by way of joint venture, option agreements or through a combination of both.

12

Three Year History

In 1999 the Company filed an assignment in bankruptcy under the Bankruptcy Act (Canada) in order to resolve and quantify claims to various creditors. This action was undertaken as a first step in the reorganization of the Company’s affairs.

Year 2000

The Company spent the year reorganizing its financial affairs.

In early 2000, the Company made a proposal to its creditors under the Bankruptcy Act (Canada) to settle all of the creditors’ claims against the Company in exchange for a dividend of $0.26 on the dollar. This proposal was accepted by the creditors and settlement was approved by the court on March 23, 2000. The funds were dispersed to the creditors on April 18, 2000. To facilitate this settlement, a director loaned the Company $50,000 on a non-interest bearing basis.

Year 2001

The Company spent most of the year finalizing its reorganization plans.

During June, April and May 2001, the Company entered into agreements with certain investors to borrow $605,200 to enable the reorganization of the Company. Shareholder approval to the reorganization was received on May 25, 2001 at the Company’s Annual General Meeting. On September 21, 2001, these loans were converted to convertible promissory notes in the principal amount of $605,200 with 6,052,000 detachable share purchase warrants. The Company issued units consisting of convertible notes in the aggregate principal amount of $605,200 together with 6,052,000 detachable share purchase warrants. The notes are non-interest bearing and mature on September 21, 2003. The holders of the convertible notes have the option to convert the notes into common shares of the Company at a conversion price of $0.10 per share until September 21, 2002 and at $0.15 per share from September 22, 2002 until September 21, 2003.

As part of its reorganization, on March 27, 2001, the Company changed its name from Primero Industries Ltd. to PMI Ventures Ltd. and consolidated its share capital on a 5:1 basis. On February 1, 2001, the Company entered into a farm-out letter agreement with Omax Resources Ltd. of Vancouver, British Columbia, Canada whereby the Company was granted an option to acquire a 60% interest in an oil and gas lease in Little Bow, Alberta. Pursuant to this agreement, the Company agreed to pay 100% of the drilling and abandonment or the drilling, completion and tie-in costs for taking of production from the well.

Year 2002

For the majority of 2002, the Company’s principal business activity continued to be the exploration and development of oil and gas properties. However, in the last quarter of the fiscal year the Company entered into negotiations and on November 22, 2002 executed the Letter Agreement with Goknet to enter into an option and joint venture agreement to further develop the Goknet Properties, located in Ghana, West Africa. The signing of this agreement signalled a change in direction for the Company, a move from oil and gas to mineral exploration.

On November 6, 2002, Mr. Arthur Fisher was appointed President of the Company and joined the Company’s Board of Directors. Mr. Fisher replaced Mr. Laurie Sadler as President of the Company.

13

Mr. Navtej S. Purewal resigned as a director of the Company on November 6, 2002.

Year 2003

On April 2, 2003, the Company completed a private placement of 1,699,845 Units to raise proceeds of $1,104,900. Each unit consisted of one common share of the Company and one share purchase warrant entitling the warrant holder to acquire one additional share of the Company for a period of one year at a price of $0.85 per share. The funds were raised to be used for exploration expenditures on the Goknet Properties and for general working capital purposes.

On May 23, 2003, the Company granted 1,205,000 common stock options to its directors and employees. The options will expire on May 23, 2008 and have an exercise price of $0.70 per share.

On May 28, 2003, the Company granted 100,000 common stock options to its employees. The options will expire on August 28, 2008 and have an exercise price of $0.70 per share.

On October 27, 2003, the Company closed two private placements. The first placement, announced on August 22, 2003, consisted of 4,444,444 Units, raised gross proceeds of $2,000,000. A finder’s fee of $72,000 plus 300,000 share purchase warrants exercisable at $0.70 per share in the first year and at $1.00 per share in the second year was paid in connection with this private placement. A second placement, announced August 28, 2003, consisted of 1,090,385 Units and raised gross proceeds of $567,000. A finder’s fee of $40,000 plus 144,231 share purchase warrants exercisable at $0.70 per share in the first year and at $1.00 per share in the second year was paid in connection with this second placement. For both placements, each Unit consists of one common share and one-half of one non-transferable share purchase warrant, each whole share purchase warrant entitling the holder to acquire one additional common share of the Company for a period of two years at a price of $0.70 per share in the first year and at $1.00 in the second year. The funds were raised to be used for exploration expenditures on the Goknet Properties and for general working capital purposes.

On October 28, 2003, the Company granted 360,000 common stock options to its employees. The options will expire on October 28, 2008 and have an exercise price of $0.70 per share.

On October 27, 2003, the Company commenced a 5,000 metre drilling program on the Goknet Properties.

On November 17, 2003, the Company received initial results from its 5,000 metre drilling program.

On December 2, 2003, the Company received additional assay results from its 5,000 metre drilling program.

2004 to date

On January 5, 2004, the Company received final results from its 5,000 metre drilling program.

On January 26, 2004, Laurie Sadler was appointed the interim President of the Company due to the untimely passing of Arthur Fisher.

On February 9, 2004, the Company commenced a next phase 2,000 metre drilling program and 80 line kilometres of deep sensing 3D IP geophysical surveys on the Goknet Properties.

On February 16, 2004, Mr. Marc Prefontaine was appointed to the Company’s Board of Directors.

14

On February 23, 2004, the Company granted 350,000 common stock options to its directors and consultants. The options will expire on February 23, 2009 and have an exercise price of $0.56 per share. In addition the Company cancelled 318,000 stock options.

On April 7, 2004, the Company received assay results from its initial 742 metres of the 2,000 metre drilling program.

On April 8, 2004, the Company announced a best-efforts brokered private placement of 2,727,273 Units of the Company at a price of $0.55 per Unit to raise gross proceeds of $1,500,000. Each Unit will consist of one common share and one-half of one non-transferable share purchase warrant, each whole share purchase warrant entitling the holder to acquire one additional common share of the Company for a period of eighteen months at a price of $0.75 per share. The financing was cancelled due to unfavourable market conditions.

On May 6, 2004, the Company completed the buyout of the Fromenda Concession one of eight concessions that comprise the Goknet Properties. Final consideration paid was US$229,000.

On June 8, 2004, Douglas MacQuarrie, formerly the Vice President of Exploration for the Company, was appointed as a Director and President, replacing Mr. Laurie Sadler who resigned both positions.

On June 15, 2004, the Company completed the buyout of the Gemap Concession one of eight concessions that comprise the Goknet Properties. Final consideration paid was US$50,000.

On June 22, 2004, the Company announced a best-efforts brokered private placement of 3,571,429 Units of the Company at a price of $0.28 per Unit to raise gross proceeds of $1,000,000. Each Unit will consist of one common share and one-half of one non-transferable share purchase warrant, each whole share purchase warrant entitling the holder to acquire one additional common share of the Company for a period of eighteen months at a price of $0.35 per share. To date the financing has not closed.

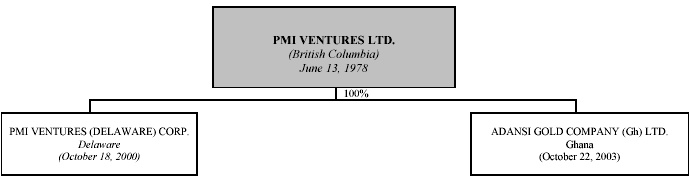

C. Organizational Structure

The following diagram shows the Company and its subsidiaries, the laws under which they were incorporated and the dates on which they came into existence:

D. Property, Plant and Equipment

Pursuant to the Letter Agreement the Company has an option to acquire an 85% interest in the Goknet Properties. See “Property Ownership”for details of the Letter Agreement.

15

Under the Letter Agreement the Company was granted an option to acquire an 85% interest in the Goknet Properties. In consideration of the grant of the option, the Company agreed to pay Goknet cash consideration of US$260,000 over three years and issue to Goknet a total of 3,000,000 of the Company's common shares in staged payments: (i) $90,000 and 500,000 common shares on the Exchange acceptance (the “Approval”); (ii) US$100,000 and 500,000 common shares on or before the second anniversary of the Approval; (iii) US$100,000 and 750,000 common shares on or before the second anniversary of the Approval; and 1,250,000 common shares on or before the third anniversary of the Approval. The Company will also be required to complete the following exploration expenditures on the Goknet Properties: (i) US$500,000 by the first anniversary of the Approval; (ii) US$1,000,000 by the second anniversary of the Approval; (iii) US$1,500,000 by the third anniversary of the Approval.

Goknet is a Ghanaian limited liability corporation formed and incorporated on April 27, 2001 with an office at #1 Switchback Crescent, Cantonments, Accra, Ghana. The directors of Goknet are G.O. Kesse, Thomas Ennison, and Douglas MacQuarrie.

The Company received Exchange Approval of the transaction on January 17, 2003.

E. Property Description and Location

The information in this Annual Report with respect to the Goknet Properties is derived from a Technical Report entitled “Technical Evaluation Report on the Asankrangwa Gold Belt of Ghana, West Africa” written by E.D. Black, M.Sc., P.Eng., an independent Consulting Geologist and dated October 28, 2002.

The Goknet Properties include eight (8) concessions/applications/options in the south western portion of Ghana along the axis of the Asankrangwa Gold Belt. Local staging point is the town of Dunkwa, approximately 200 km by road northwest of Accra. A summary of the concessions and applications comprising the Goknet Properties is listed in the following table:

| Concession | Area | Ownership | Current Status vv Goknet | |

| (sq. km) | (maximum interest %) | |||

| Gyagyatreso | 10.95 | Switchback Mining Co. | Optioned | 90% |

| Nkronua | 24.97 | Switchback Mining Co. | Optioned | 90% |

| Fromenda | 21.53 | Adansi Gold (Gh) | 100% interest | 100% |

| Diaso | 120.8 | Adansi Gold (Gh) | Application | 100% |

| Amuabaka | 28.86 | Switchback Mining Co. | Optioned | 90% |

| Gemap | 57.12 | Adansi Gold (Gh) | 100% interest | 100% |

| EJT #1 | 37.96 | EJT Exploration Ltd. | Optioned | 100% |

| Goknet#1 | 81.04 | Goynet Mining Co. Ltd. | Optioned | 100% |

| Total | 383.23 |

There can be no assurances that the Company will be successful in obtaining licenses for each of the areas for which it has made application.

16

Accessibility & Local Resources

The Goknet Properties are situated in the southwest part of Ghana, West Africa. Accra, the seacoast capital of Ghana, is a city with a population of approximately one million people, serviced daily by air from major European centers, including London, Amsterdam, Frankfurt and Rome.

The Goknet Properties are mostly contiguous and lie along the 150-km long northeasterly-trending Asankrangwa Gold Belt, centered by the village of Diaso. Diaso is approximately 50 km northwest by partially paved highway from the local staging point, Dunkwa, which, in turn, is approximately 200 km northwest of Accra.

The concessions are accessible by the all weather Dunkwa - Diaso motor road. Diaso, the largest town within the concession, has two trunk roads connecting to Bibiani and Sefwi Bekwai. A railway line running from Dunkwa to Awaso passes through the southern sector of the concession. The northern section is accessible via the main Dunkwa to Kumasi highway to the Bekwai junction, and then 37 km along the Obotan mine road, and finally along a 3rd class road 12 km. Other parts of the concessions can be easily reached by footpaths and farm tracks. In addition to Diaso, Manso, Juabo, Ntom, Agona, Moadaso and Afiefiso are large towns within the area.

Physiography

The concession area generally displays moderate relief, the highest elevation being 266m above mean sea level in the south-western area, with moderate to steep slopes. The major streams draining the area are the Ankobra river in the west and the Ofin river in the east, with numerous tributaries displaying a mature, dendritic drainage pattern.

The vegetation is mainly of the tropical rain forest type, which, with the exception of a small area of national Forest Reserves, has been actively farmed and form less densely wooded secondary forest. The concession area supports large cocoa farms and palm plantations as well as subsistence food crops such as plantain, maize and cassava.

The relative humidity is usually high. Two rainy seasons are experienced in the area - a major one from March to July followed by a minor one from September to October. The annual rainfall is in the range of 1500 - 2000 mm and the minimum and maximum temperatures are about 220 C and 360 C, respectively, with an average annual temperature of about 290 C.

Regional Geology

Ghana occupies the south eastern lobe of the Man Precambrian Shield and comprises a bedrock sequence of five north easterly trending, isoclinally folded, Proterozoic meta-sediment and meta-volcanic troughs of Upper Birimian age (2.17 Ba), with four intervening anticlinoria of meta-sediments and minor meta-volcanics, of Lower Birimian age (2.18 Ba). Locally, the former are, at times, overlain by Tarkwaian sandstones and conglomerates. This “younger” sequence lies unconformably upon a complex of intensely folded, faulted and granite intruded Archean basement.

Structurally, northeast oriented corrugated folding and thrust faulting predominates, crossed indiscriminately by north-south diabase dykes and east-west structural elements.

17

Exploration History and Mineralization

The concession area has been mined by local artisanal miners over the centuries. Significant gold production has been recorded from the alluvial dredges which worked the Ofin river – just to the east of the concessions. More recently, gold production has come from Resolute Amansies’ Obotan Mine, a recently closed 5,000 ton per day open-cut milling operation. Obotan is located 25 km north east of Diaso, along the strike of the regional geology and the concession outline.

Gold mineralization in the Asankrangwa gold belt is associated with pyrite, arsenopyrite, graphite and quartz in close proximity with northeast trending structures. Ore grade gold deposits occur along fractured, brecciated and silica invaded parts of the shear zones, which tend to parallel the Birimian fold structures; or as disseminated “stockwork” type gold deposits in favourable greywackes in and adjacent to the shear zones.

Since 1992, many of the concessions currently held by Goknet were worked by other companies with total estimated expenditures of US$9 million. Previous work consisted of over 35,000 soil samples; 115 trenchs; ground and airborne geophysics; and 27,000 metres of drilling in 559 short drill holes.

Previous best drill intersections were: 24 metres @ 5.1 g/t gold; 23 metres @ 5.65 g/t gold; 4 metres @ 27.0 g/t gold; and 9 metres @ 12.0 g/t gold. The most significant gold mineralization was noted on the Fromenda concession in the Grid “B” area, and an additional 10 target areas have been outlined elsewhere on the concessions based on the above work programs.

Legislative Overview

The legislative framework for mining in Ghana is laid down in the Minerals and Mining Law, 1986, PNDCL 153 (Law 153) as amended by the Minerals and Mining Amendment Act 1993, Act 475 (Act 475) and modified by the provisions of the Constitution of 1993 (the “Constitution”). Within this legal framework, the State is the owner of all minerals occurring in their natural state within Ghana's land and sea territory, including its exclusive economic zone. All minerals in Ghana are vested in the President on behalf of and in trust for the people of Ghana. Thus, regardless of who owns the land upon or under which minerals are situated, the exercise of any mineral right requires, by law, a licence to be granted by the Minister for Mines (the “Sector Minister”) who acts as an agent of the State for the exercise of powers relating to minerals. Mineral rights are legally defined to include the rights to reconnoitre, prospect for, and mine minerals. The sector Minister is also authorized to exercise, within defined limits, powers relating to the transfer, amendment, renewal, cancellation and surrender of mineral rights. The powers conferred upon the Minister must be exercised contingent upon the advice of the Minerals Commission (“Mincom”), which has the authority under the Constitution to regulate and manage the utilization of mineral resources and co-ordinate policies in relation to minerals. Law 153 specifies the forms of mineral rights that the sector Minister is empowered to grant, the duration of the grant, the size of the concessions, and eligibility criteria for the grantee, as well as the procedure for application for mineral rights. The law also spells out in broad terms the rights and obligations of a holder of a mineral right and the terms and conditions upon which each mineral right grant should be made. A mineral right granted is not transferable or tradable in any form except with the prior written consent of the sector Minister.

Mincom is the main promotional and regulatory agency in the minerals sector in Ghana. Under the Constitution of the republic of Ghana and Act 450 (1993), Mincom is responsible for the regulation and management of the mineral resources of Ghana and the co-ordination of policies in relation to minerals. Mincom was first established under the Minerals Commission Law (1986). Mincom functions through a Secretariat which is headed by a Chief Executive and assisted by professionals and technical personnel within the six departments of the Secretariat, namely:

18

| a. | Planning and Policy Analysis | |

| b. | Monitoring and Evaluation | |

| c. | Finance, Marketing and Research | |

| d. | Personnel and Administration | |

| e. | Legal | |

| f. | Small Scale Mining |

Under Law 153 mineral rights can be granted in the following areas:

a. Reconnaissance Licence

A Reconnaissance Licence confers on the holder the right to search for a specific mineral (or commodity) within the licence area by geochemical and photo-geological surveys or other remote sensing techniques. Except as otherwise provided in the licence, it does not permit drilling, excavation or other sub-surface techniques. The licence is normally granted for up to one year and may be renewed by the Minister from time to time for periods up to one year at a time upon application by the holder. The application for renewal must be made at least three months before the expiration of the licence. There is no legal limitation as to the size of the area over which a reconnaissance licence may be granted.

b. Prospecting Licence

A Prospecting Licence gives the holder the exclusive right to search for specific minerals (or commodities) by the conduct of geological, geochemical and geophysical investigations and to determine the extent and economic value of any deposit within the licence area. The initial grant of the licence is limited to three years and a maximum area of 150 km2. These limits may, at the direction of the President of the Republic, be exceeded in any particular grant whenever the President considers it to be in the national interest so to do. A prospecting licence may be renewed for a maximum of two terms or for further periods of up to two years each. At each renewal, half the licence area is required to be relinquished by the holder. If more than one prospecting licence is held, they may be treated as one area for purposes of relinquishment.

c. Mining Lease

The grant of a Mining Lease gives the holder the right to mine, win or extract specified minerals (or commodities) within the lease area. The lease may be granted to the holder of a prospecting licence or any person who establishes to the satisfaction of the Minister that a mineral to which the lease relates exists in commercial quantities within the proposed lease area and can be mined at a profit. The lease is issued for up to thirty years subject to renewal for a further thirty-year term. The size of the area in respect of which a lease may be granted is limited to 50 km2 for a single grant or 150 km2 for aggregate grants. These limits may be exceeded in particular cases at the direction of the President if it is in the national interest.

Exploration completed by the Company in 2003

A work program commenced in mid-February 2003 in preparation for a follow-up drill program that was comprised of approximately 1,050 metres of diamond drilling in 8 to 10 holes planned for, and initiated, in the second quarter of fiscal 2003.

The preliminary work program was carried out on the Fromenda and Gemap concessions. The program consisted of cutting of 33 line km of survey lines; rehabilitation of 10 km of drill access roads; placement of survey control pillars and the completion of 22 line km of induced polarization (“IP”) surveys.

19

The IP survey on the Fromenda property outlined two chargeability high areas which are on strike of an area previously tested by 21 reverse circulation drill holes that have also been the target of extensive recent artisan mining. Previous work in this area indicated that gold mineralization occurs over a length of 500 metres and consists of two parallel mineralized zones, each 3 to 10 metres in width. Limited drilling of this area was completed in the early 1990’s. Best intersections included 7.1 g/t Au over 4 metres at a depth of 25 metres; 3.4 g/t Au over 4 metres at a depth of 55 metres and 5.42 g/t Au over 2 metres at a depth of 24 metres.

Following are results of the diamond drill holes (1,050 metres in total) that comprise the first phase of the 2003 drill program. Drill hole 03FBDDH-1 was drilled in the Fromenda Grid “B” area to a total length of 86 metres (282 feet) at -45° using HQ drill string. The hole intersected a mineralized section of 30.0 metres (approximately true width) as shown in Table I.

The mineralized intercept is located at a depth of about 20 metres below surface. Mineralization is characterized by highly altered and oxidized greywacke crosscut by sheared quartz stringers.

| Table I | ||||||

| Fromenda Grid “B” Area | ||||||

| Drill Hole & | Drill Intercept | Drill | Assays | |||

| -inclination | From (m) | To (m) | (m) | (ft) | Au (g/t) | Au (oz/ton) |

| 03FBDDH1 | 44.0 | 74.0 | 30.0 | 98.43 | 2.63 | 0.08 |

| -45° | ||||||

| including | 52.0 | 69.0 | 17.0 | 55.78 | 3.59 | 0.11 |

| 03FBDDH2 | 82.16 | 104.85 | 22.69 | 74.44 | 0.89 | 0.03 |

| -50° | ||||||

| including | 97.41 | 104.85 | 7.44 | 24.41 | 1.44 | 0.04 |

| 03FBDDH3 | 52.0 | 77.24 | 25.24 | 82.81 | 0.86 | 0.03 |

| -60° | ||||||

| including | 72.12 | 77.24 | 5.12 | 16.80 | 1.86 | 0.05 |

This initial drilling at the Fromenda Grid “B” area has demonstrated that the shear structure that hosts the gold mineralization is approximately 25 metres (83 feet) in true width with grades of up to 3.59 g/t over a true width of 17.0 metres (56 feet).

In the Kukunapi area, four drill holes were completed. Results for the first two drill holes are shown below.

20

| Table II | ||||||

| Kukunapi Area | ||||||

| Drill Hole & | Drill Intercept | Drill | Assays | |||

| -inclination | From (m) | To (m) | (m) | (ft) | Au (g/t) | Au (oz/ton) |

| 03JGDDH1 | 30.82 | 34.40 | 4.08 | 13.39 | 1.66 | 0.05 |

| -45° | 77.55 | 83.52 | 5.97 | 19.59 | 4.67 | 0.14 |

| including | 90.22 | 91.90 | 1.68 | 5.51 | 2.21 | 0.06 |

| including | 77.55 | 78.55 | 1.00 | 3.28 | 21.59 | 0.63 |

| 03JGDDH2 | 24.00 | 27.00 | 3.00 | 9.84 | 1.34 | 0.04 |

| -60° | 41.00 | 47.00 | 6.00 | 19.68 | 1.44 | 0.04 |

| including | 95.90 | 102.41 | 6.51 | 21.36 | 2.24 | 0.07 |

The initial drilling at Kukunapi is regarded by the Company as successful since it has demonstrated the existence of the mineralized structures grading up to 4.67 g/t Au over a width of 5.97 metres (19.59 feet). During the last half of 2003, the Company commenced a second diamond drilling program on the Fromenda concession. The program, which consisted of nine holes totalling 931 metres, was intended to extend the previously reported gold mineralization to the east and to depth. The Company was encouraged by the results from the second drill (see Table III below), since they continued to demonstrate that the shear structure that hosts the gold mineralization is laterally continuous and contains near surface mineralized sections with gold grades of between 1.13 g/t gold and 4.97 g/t gold over widths ranging from 6.50 metres (21.32 feet) to 41.00 metres (134.50 feet). The deepest hole completed to date has tested the mineralized zone to a true depth of 72 metres (236 feet).

| Table III | ||||||

| Fromenda Grid “B” Area | ||||||

| Drill Hole & | Drill Intercept | Drill | Assays | |||

| -inclination | From (m) | To (m) | (m) | (ft) | Au (g/t) | Au (oz/ton) |

| 03FBDDH5 | 20.73 | 31.39 | 10.66 | 34.98 | 3.80 | 0.11 |

| -50° | ||||||

| including | 20.73 | 22.86 | 2.13 | 6.99 | 4.67 | 0.14 |

| including | 29.87 | 31.39 | 1.52 | 4.99 | 19.45 | 0.57 |

21

| Table III | ||||||

| Fromenda Grid “B” Area | ||||||

| Drill Hole & | Drill Intercept | Drill | Assays | |||

| -inclination | From (m) | To (m) | (m) | (ft) | Au (g/t) | Au (oz/ton) |

| 03FBDDH7 | 48.40 | 72.00 | 23.60 | 77.43 | 4.97 | 0.14 |

| -90° | ||||||

| including | 48.40 | 61.58 | 13.18 | 43.24 | 5.49 | 0.16 |

| including | 68.00 | 72.00 | 4.00 | 13.12 | 10.89 | 0.32 |

| 03FBDDH09 | 55.00 | 68.50 | 13.50 | 44.29 | 1.00 | 0.03 |

| -60° | ||||||

| including | 62.00 | 68.50 | 6.50 | 21.32 | 1.40 | 0.04 |

| 03FBDDH11 | 14.50 | 34.00 | 19.50 | 63.98 | 1.39 | 0.04 |

| -50° | ||||||

| including | 14.50 | 19.00 | 4.50 | 14.76 | 1.89 | 0.06 |

| including | 24.00 | 34.00 | 10.00 | 32.81 | 1.74 | 0.05 |

| 03FBDDH12 | 6.00 | 24.45 | 18.45 | 60.53 | 2.42 | 0.07 |

| -50° | ||||||

| including | 10.00 | 22.00 | 12.00 | 39.37 | 3.34 | 0.10 |

| 03FBDDH13 | 13.00 | 54.00 | 41.00 | 134.52 | 1.15 | 0.03 |

| -50° | ||||||

| including | 13.00 | 19.00 | 6.00 | 19.69 | 2.40 | 0.07 |

| 43.00 | 54.00 | 11.00 | 36.09 | 2.01 | 0.06 | |

On October 27, 2003, the Company announced commencement of a 3,000 metre drilling program. The intent of this program was to focus on the Grid "B" area of the Fromenda concession. Four other targets were slated to be drill tested on a reconnaissance basis during this program. On December 2, 2003, the Company announced that it had again intersected very significant high gold grades (27.0 g/t Au over 4.0 metres) in connection with this drill program. The results are deemed significant as they are well above the average grades found in Ghana.

22

Item 5. OPERATING AND FINANCIAL REVIEW AND PROSPECTS

A. Operating Results

This discussion should be read in conjunction with the audited financial statements of the Company and related notes included therein.

All statements other than statements of historical facts included in this Annual Report, including, without limitation, the statements under “Operating and Financial Review and Prospects,” “Information on the Company,” and “Property, Plant and Equipment” and located elsewhere herein regarding industry prospects and the Company’s financial positions are forward-looking statements. Although the Company believes that the expectations reflected in such forward-looking statements are reasonable, it cannot give any assurance that such expectations will prove to have been correct. Important factors that could cause actual results to differ materially from the Company’s expectations (“Cautionary Statements”) are disclosed in this Annual Report, including, without limitation, in conjunction with the forward-looking statements included in this Annual Report under“Risk Factors”. All subsequent written and oral forward-looking statements attributed to the Company or persons acting on their behalf are expressly qualified in their entirety by the Cautionary Statement. There is significant risk that actual results will vary, perhaps materially from results projected depending on such factors as changes in general economic conditions, financial markets, gold prices and other metals, technology and exploration hazards.

United States Generally Accepted Accounting Principles

See note 17 to the Company’s Financial Statements for a comparison of Canadian GAAP and United States GAAP as applicable to the Company’s operations. Material variations in the accounting principles, practices and methods used in preparing these financial statements from principles, practices and methods accepted under United States GAAP are described and quantified below:

Mineral property interests and deferred exploration costs

Under Canadian GAAP, mineral property interests and deferred exploration costs, including acquisition and exploration costs, are carried at cost and written down if the properties are abandoned, sold or if management determines there to be an impairment in value. Under United States GAAP, mineral property interests and deferred exploration costs are expensed as incurred. Once a final feasibility study has been completed, additional costs incurred to bring the mine into production are capitalized as development costs. Costs incurred to access ore bodies identified in the current mining plan after production has commenced are considered production costs and are expensed as incurred. Costs incurred to extend production beyond those areas identified in the mining plan where additional reserves have been established are deferred as development costs until the incremental reserves are produced. Capitalized costs are amortized using the unit-of-production method over the estimated life of the ore body based on proven and probable reserves.

Escrow shares

Under Canadian GAAP, shares issued with escrow restrictions are recorded at their issue price, with no revaluation upon release from escrow. Under United States GAAP, escrow shares which are to be released upon the Company meeting certain performance criteria are considered to be contingently issuable. Accordingly, these shares are excluded from the weighted average number of shares outstanding under United States GAAP until they are releasable, and the difference between the fair value of those shares at the time they become releasable from escrow and their original issue price is accounted for as compensation expense. The weighted average number of shares outstanding under United States

23

GAAP for the years ended December 31, 2003, 2002 and 2001 were 14,565,562, 5,679,999, and 2,778,635, respectively.

Convertible notes

Under Canadian GAAP, upon issuance of the convertible notes, the net proceeds received are allocated between the liability and equity components of the notes. Upon conversion of the note, the fair value of the note and the related equity components are transferred to capital stock.

Under United States GAAP, the beneficial conversion feature represented by the excess of the fair value of the shares issuable on conversion of the notes, measured on the commitment date, over the amount of the proceeds to be allocated to the common shares upon conversion, would be allocated to additional paid in capital and offset against the convertible notes. This results in a discount on the note that is accreted as additional interest expense over the term of the note and any unamortized balance is expensed immediately upon conversion of the note. Accordingly, for United States GAAP purposes, for the years ended December 31, 2003, 2002 and 2001 additional interest expense (including accretion) of $Nil, $88,337 and $6,244, respectively, has been recorded. The balance sheet adjustment represents the difference between the portion of the convertible debt allocated to equity under Canadian GAAP, net of accretion to date, and the portion allocated to the beneficial conversion feature under United States GAAP, also net of accretion to date.

Stock based compensation

Under United States GAAP, Statement of Financial Accounting Standards No. 123, “Accounting for Stock-based Compensation” (“SFAS 123”) requires companies to establish a fair market value based method of accounting for stock-based compensation plans. The Company has elected for the year ended December 31, 2003 to account for stock-based compensation using SFAS 123. Accordingly, compensation cost for stock options is measured at the fair value of options granted.

For the years ended December 31, 2002 and 2001, the company elected to account for stock-based compensation using Accounting Principles Board Opinion No. 25 “Accounting for Stock Issued to Employees”. Accordingly, compensation cost for stock options was measured as the excess, if any, of the quoted market price of the Company’s stock at the date of grant over the option price.

Fiscal year ended December 31, 2003 compared to fiscal year ended December 31, 2002

As at December 31, 2003, the Company held cash, cash equivalents and short-term investments of $2,367,606 and had a working capital of $2,220,161 as compared to cash, cash equivalents and short term investments of $174,375 and working capital of $161,740 as at December 31, 2002. The increased level of cash and cash equivalents at the end of year ended December 31, 2003 was due the closing of three private placements in 2003.

There was a loss of $1,018,341 for the year ended December 31, 2003. Comparatively, the loss for the year ended December 31, 2002 was $506,134. The Company recorded $8,869 in gas sales in the year ended December 31, 2003 as compared to $9,206 for the year ended December 31, 2002. Other income for the year ended December 31, 2003 was $8,768 compared to $1,982 in the year ended December 31, 2002. The increase in other income is attributable to interest on cash balances invested throughout the year ended December 31, 2003.

The Company’s costs rose dramatically in the year ended December 31, 2003, in line with the substantial increase in business activities. General & administrative expenses increased by $792,384 in the year

24

ended December 31, 2003 to $997,474 from $205,090 in the year ended December 31, 2002. Bank charges and interest increased over the year ended December 31, 2002 by $2,637. Office and miscellaneous costs increased to $115,644 in the year ended December 31 2003 from $4,170 the year ended December 31, 2002. Professional fees totalled $134,749 the year ended December 31, 2003 as compared to $21,109 in the year ended December 31, 2002.

A total of $189,535 was expended on investor relations activities in the year ended December 31, 2003 as compared to $3,504 in the year ended December 31, 2002. There was a concentrated effort made by the Company to expand awareness within the public sector, which resulted in shareholder communications expenses of $107,315 the year ended December 31, 2003 as compared to nil in the year ended December 31, 2002.

The Company incurred management fees of $81,200 during the year ended December 31, 2003 as compared to $55,600 for the year ended December 31, 2002. Wages and benefits increased substantially over the prior year to $335,450 for the year ended December 31, 2003 as compared to $24,384 during the year ended December 31 2002. This increase was as a result of the hiring of three additional employees during the year and, largely, to the inclusion of $121,093 of stock based compensation, based on the Black Scholes option pricing model resulting from the grant of 1,665,000 options to employees/directors during the year ended December 31, 2003.

Comparison of Canadian GAAP and United States GAAP

Under United States GAAP the total assets of the Company for the year ended December 31, 2003 would have been $2,526,223 as compared to $4,634,113 under Canadian GAAP as a result of the adjustment for mineral property interest and exploration costs. Total liabilities and stockholders’ equity under United States GAAP would be $2,526,223 as compared to $4,634,113 under Canadian GAAP as a result of the same adjustment.

Under United States GAAP the net loss for the year ended December 31, 2003 would have been a loss of $3,126,231 as compared to a net loss of $1,018,341 under Canadian GAAPas a result of an adjustment to mineral property interests and deferred exploration costs.

The weighted average number of shares outstanding under United States GAAP for the year ended December 31, 2003 was 14,565,562 as compared with 5,679,999 for the year ended December 31, 2002.

Fiscal year ended December 31, 2002 compared to fiscal year ended December 31, 2001

As at December 31, 2002, the Company held cash and short-term deposits of $174,375 and had a working capital of $161,740 as compared to cash and short term deposits of $59,231 and working capital of $55,116 as at December 31, 2001. The increased level of cash and cash equivalent at the end of 2002 fiscal year was due largely to the exercise of warrants related to convertible notes issued in 2001.

In the year ending December 31, 2002 the Company wrote down its interest in the Little Bow, Alberta oil and gas properties from $316,815 to a nominal value of $1. During the 2002 fiscal year the Company acquired capital assets consisting of computer equipment and furniture valued at a total of $3,705 ($3,621 net of amortization. In addition the Company entered into a lease agreement for office space with annual lease commitments under the agreement of $12,452 for each of 2003, 2004 and 2005 fiscal years. In 2001, the Company had not purchased any capital assets nor leased any office premises.

In 2002 accounts payable and accrued liabilities increased by $17,216 over 2001 as a result of increased level of business activity by the Company during 2002.

25

Comparison of Canadian GAAP and United States GAAP

Under United States GAAP the Capital Stock of the Company for the year ended December 31, 2002 would have been $4,825,986 as compared to $4,878,986 under Canadian GAAP. Additional paid-in capital under United States GAAP would be $219,343 as compared to $71,762 under Canadian GAAP and the Deficit would be $4,893,467 under United States CAAP as compared to $4,798,886 under Canadian GAAP.

Under United States GAAP the net income (loss) for the year ended December 31, 2002 would have been a loss of $594,471 as compared to a net loss of $506,134 under Canadian GAAPas a result of an adjustment for accreted interest on conversion of the convertible notes.Under United States GAAP the net income (loss) for the year ended December 31, 2001 would have been a loss of $114,012 as compared to a net loss of $107,768 under Canadian GAAPas a result of an adjustment for accreted interest on conversion of the convertible notes.

The weighted average number of shares outstanding under United States GAAP for the years ended December 31, 2002 and 2001 were 5,679,999 and 2,778,635, respectively, resulting in no effect on basic and diluted earnings (loss) per share for the years ended December 31, 2002 and 2001.

Fiscal year ended December 31, 2001 compared to the fiscal year ended December 31, 2000

The Company's expenses for the year ended December 31, 2001 were $113,111 as compared to $61,639 for the fiscal year ended December 31, 2000 reflecting the Company's increased activity in the oil and gas industry. The increase in expenses is predominantly attributable to increased professional fees from $20,890 in 2000 to $38,327 in 2001 and bank interest costs and interest on convertible notes of $202 in 2001 to $25,684 in 2001 and regulatory fees from $8,420 in 2000 to $12,515 in 2001.

The Company incurred a net loss of $107,768 for the year ended December 31, 2001. During the fiscal year ended December 31, 2000, it incurred a net gain of $314,668 arising from a gain on settlement arising from a proposal the Company made to its creditors in early 2000.

The Company had interest income of $2,526 in the year ended December 31, 2001 and interest income of $15 in the year ended December 31, 2000. The Company had miscellaneous income of $2,817 in 2001 and incurred a gain of $376,292 in 2000 arising from a proposal the Company made to its creditors in early 2000.

The Company incurred drilling costs of $312,476 and engineering costs of $4,339 in 2001 on its Little Bow oil play in Alberta Canada. The Company did not incur any mineral property acquisition or exploration costs during fiscal 2000.

Comparison of Canadian GAAP and United States GAAP

Under United States GAAP the Capital Stock of the Company for the year ended December 31, 2001 would have been $4,118,069 as compared to $4,133,780 under Canadian GAAP. Additional paid-in capital under United States GAAP would be $147,581 as compared to $125,626 under Canadian GAAP and the Deficit would be $4,298,996 under United States GAAP as compared to $4,292,752 under Canadian GAAP.

Under United States GAAP the net income (loss) for the year ended December 31, 2001 would have been a net loss of $114,012 as compared to a net loss of $107,768 under Canadian GAAP as a result of an

26

adjustment for accreted interest on conversion of the convertible notes.There was no effect on the net income (loss) of the Company for the year ended December 31, 2000.

The weighted average number of shares outstanding under United States GAAP for the years ended December 31, 2001 and 2000 were 2,778,635 and 2,766,306, respectively, resulting in no effect on basic and diluted earnings (loss) per share for the years ended December 31, 2001 and 2000.

Liquidity and Capital Resources

In management’s view, given the nature of the Company’s operation, which consists of exploration and evaluation of mining properties, the most meaningful financial information relates primarily to current liquidity and solvency. The Company’s financial success will be dependent upon the extent to which it can discover mineralization and the economic viability of developing the properties. Such development may take years to complete and the amount of resulting income, if any, is difficult to determine with any certainty. The sales value of any mineralization discovered by the Company is largely dependent upon factors beyond its control such as the market value of the metals produced.