Exhibit 99.1

|

I N V E S T O R D A Y

S E P T E M B E R 2 1 , 2 0 1 6 | T Y S O N S C O R N E R , V A

|

Forward-Looking Statements

This presentation contains “forward-looking statements” within the meaning of the safe harbor from civil liability provided for such statements by the Private Securities Litigation Reform Act of 1995

(set forth in Section 27A of the Securities Act of 1933, as amended, or the Securities Act, and Section 21E of the Securities Exchange Act of 1934, as amended, or the Exchange Act). Forward-looking

statements involve numerous risks and uncertainties and you should not rely on them as predictions of future events. Forward-looking statements depend on assumptions, data or methods which may

be incorrect or imprecise and we may not be able to realize them. We do not guarantee that the transactions and events described will happen as described (or that they will happen at all). You can

identify forward-looking statements by the use of forward-looking terminology such as “believes,” “expects,” “may,” “should,” “intends,” “plans,” “estimates” or “anticipates” and variations of such

words or similar expressions or the negative of such words. You can also identify forward-looking statements by discussions of strategies, vision, plans or intentions. Risks, uncertainties and changes

in the following factors, among others, could cause actual results and future events to differ materially from those set forth or contemplated in the forward-looking statements:

economic, business and financial conditions, and changes in our industry and changes in the real estate markets in particular;

economic and other developments in the state of Texas and in other markets where we have a high concentration of properties;

our business strategy;

our projected operating results;

rental rates and/or vacancy rates;

frequency and magnitude of defaults on, early terminations of or non-renewal of leases by tenants;

bankruptcy or insolvency of a major tenant or a significant number of smaller tenants;

interest rates or operating costs;

real estate and zoning laws and changes in real property tax rates;

real estate valuations;

our leverage;

our ability to generate sufficient cash flows to service our outstanding indebtedness;

our ability to obtain necessary outside financing;

the availability, terms and deployment of capital;

general volatility of the capital and credit markets and the market price of our Class A common stock;

risks generally associated with real estate acquisitions, dispositions and redevelopment, including the impact of construction delays and cost overruns and our ability to lease redeveloped space;

our ability to identify and pursue acquisition, disposition and redevelopment opportunities;

composition of members of our senior management team;

our ability to attract and retain qualified personnel;

our ability to continue to qualify as a real estate investment trust (REIT);

governmental regulations, tax laws and rates and similar matters;

our compliance with laws, rules and regulations;

environmental uncertainties and exposure to natural disasters;

insurance coverage;

the likelihood or actual occurrence of terrorist attacks in the U.S.; and

other risk factors, including those detailed in the section titled “Risk Factors” of our most recent Form 10-K and Form 10-Q filed with the SEC.

You should not place undue reliance on any forward-looking statements, which are based only on information currently available to us (or to third parties making the forward-looking statements). We

undertake no obligation to publicly release any revisions to such forward-looking statements to reflect events or circumstances after the date of this presentation, except as required by applicable law.

All information is presented on a consolidated basis and is as of June 30, 2016, unless otherwise noted

All 2013 information is presented on a consolidated basis, including our pro rata share of unconsolidated joint ventures, and is as of March 31, 2013, unless otherwise noted

All demographic information is sourced from The Nielsen Company, unless otherwise noted

All 2013 peer metric information is sourced from company filings as of March 31, 2013, unless otherwise noted

All 2016 peer metric information is sourced from company filings as of June 30, 2016, unless otherwise noted

2 |

|

|

OUR SPEAKERS

RPAI’s Playbook

SHANE GARRISON

EVP, COO & CIO

Balance Sheet

& Roadmap

HEATH FEAR

EVP, CFO & Treasurer

STEVE GRIMES

President and CEO

Opening & Closing Remarks

TIMOTHY STEFFAN

President—Eastern Division

Regional Experience

3

|

SENIOR LEADERSHIP

Paula Maggio

EVP, General Counsel & Secretary

Julie Swinehart

SVP, Chief Accounting Officer

Gerry Wright

President—Western Division

Maria Pope Toliopoulos

SVP, Dir. of National Retail Leasing & Services

LEASING

Greg Goldberg

VP, Leasing Director—Eastern Division

Ann Smith

VP, Sr. Leasing Director—Eastern Division

Stacy Short

VP, Leasing Director—Western Division

INVESTMENTS / DEVELOPMENT

Matthew Beverly

SVP, Dir. of Investments—Eastern Division

Mike Hazinski

VP, Dir. of Investments—Western Division

Nick Over

VP, Director of Development

CAPITAL MARKETS / INVESTOR RELATIONS

Mike Fitzmaurice

VP, Finance

4

|

O P E N I N G R E M A R K S

Steve Grimes

5 |

|

|

Our Strategy

We generate long-term shareholder value through the

ownership, operation and redevelopment of high

quality, multi-tenant retail assets in our target markets

We believe real estate is a local business and that our

approach combined with scale provides for the best

value creation over the long term

We believe in maintaining an investment grade rated

balance sheet through adhering to a simple, low

leverage model

We believe in maintaining a best-in-class operating

platform through an intense focus on talent

development and the innovative use of technology and

systems

6 |

|

|

N Y S E : R P A I

T O TA L C A P I TA L I Z AT I O N

$6.4B1

I N V E S T M E N T G R A D E

BBB- Baa3

S & P Moody’s

7 |

|

|

28.1 MILLION

SQUARE FEET

1 8 5 R E TA I L O P E R AT I N G P R O P E R T I E S

TA R G E T M A R K E T S ( R A N K B Y A B R 1 )

D A L L A S

AT L A N TA

D. C . / B A LT I M O R E

H O U S TO N

N E W YO R K

S A N A N TO N I O

C H I C AG O

P H O E N I X

S E AT T L E

A U S T I N

8

|

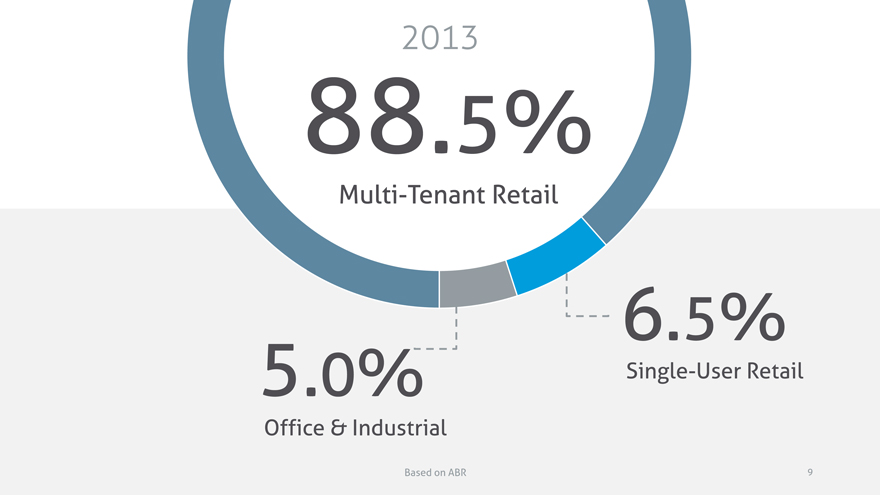

2013

88.5%

Multi-Tenant Retail

6.5%

5.0% Single-User Retail Office & Industrial

Based on ABR

9

|

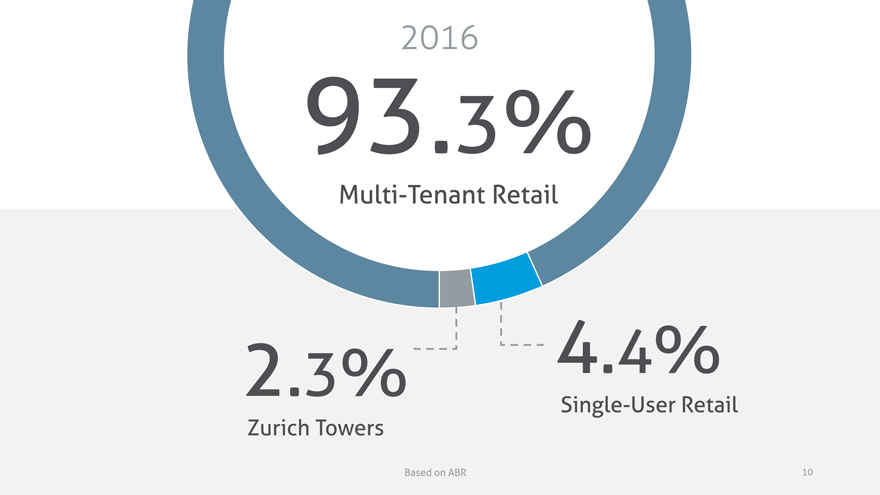

2016

93.3%

Multi-Tenant Retail

2.3% 4.4%

Single-User Retail Zurich Towers

Based on ABR 10

|

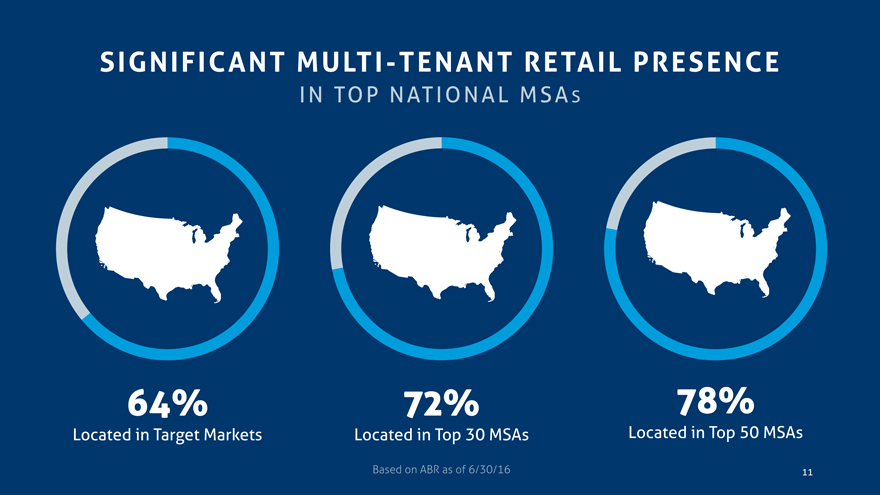

SIGNIFICANT MULTI-TENANT RETAIL PRESENCE

IN TOP NATIONAL MSA S

64% 72% 78%

Located in Target Markets Located in Top 30 MSAs Located in Top 50 MSAs

Based on ABR as of 6/30/16

11

|

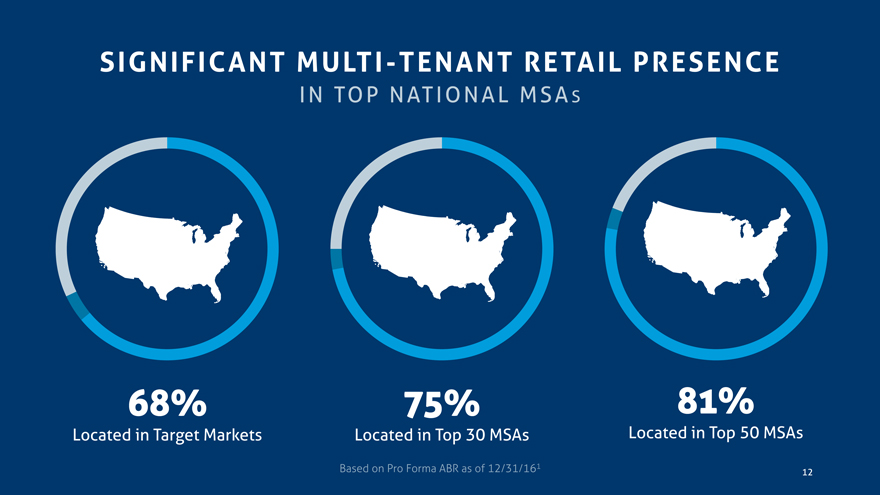

SIGNIFICANT MULTI-TENANT RETAIL PRESENCE

IN TOP NATIONAL MSA S

68% 75% 81%

Located in Target Markets Located in Top 30 MSAs Located in Top 50 MSAs

Based on Pro Forma ABR as of 12/31/161

12

|

Real Estate Driven—Evolving Multi-Tenant Retail Asset Mix

39% 35% 26%

39% 2016 45% 2016 16% 2016 2013 2013 2013

NEIGHBORHOOD/ COMMUNITY CENTERS

Avg. Household Income $88,000

Population 110,000

Est. Population Growth 5.6%

3-mile radius

POWER CENTERS

Avg. Household Income $85,000 Population 155,000

Est. Population Growth 5.4%

5-mile radius

Asset mix based on ABR

LIFESTYLE CENTERS/ MIXED-USE PROPERTIES

Avg. Household Income $108,000 Population 411,000

Est. Population Growth 5.4%

5-mile radius

13

|

2 0 1 3

INVESTOR DAY

REAL ESTATE

Reposition our multi-tenant retail portfolio into strategic target markets over a ten year period

Sold $1.4 billion1 of non-target assets, representing 23%2 of our portfolio, and redeployed $1.3 billion1 into our target markets

Improved geographic concentration in our target markets by 3.3 million square feet

Exited 8 states and 27 non-target markets

FOCUS

Simplify our business model by exiting joint ventures and reducing single-user asset exposure

Exited remaining joint ventures

representing approximately $900

million3 in transaction activity

Reduced single-user asset

exposure by 43% to 6.7%, based

on ABR, and expected to be

approximately 3.0% by year-end

2016

BALANCE SHEET

Obtain an investment grade rating

Obtained an investment grade

rating from S&P of BBB-

Obtained an investment grade

rating from Moody’s of Baa3

Completed our inaugural

unsecured public notes offering

for $250 million

14

|

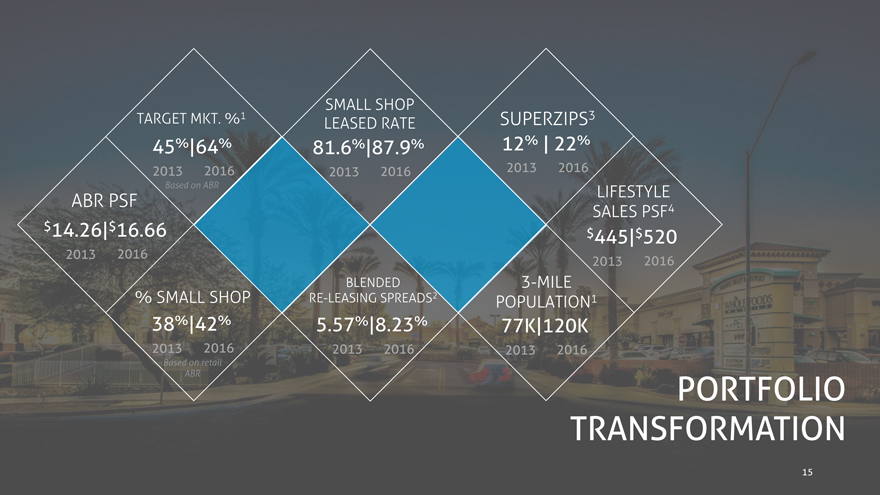

1 SMALL SHOP

TARGET MKT. % SUPERZIPS3

LEASED RATE

45%|64% 81.6%|87.9% 12% | 22%

2013 2016 2013 2016 2013 2016

Based on ABR LIFESTYLE

ABR PSF

SALES PSF4

$14.26|$16.66 $445|$520

2013 2016

2013 2016

BLENDED 3-MILE

% SMALL SHOP RE-LEASING SPREADS2 POPULATION1

38%|42% 5.57%|8.23% 77K|120K

2013 2016 2013 2016 2013 2016

Based on retail

ABR PORTFOLIO TRANSFORMATION

15

|

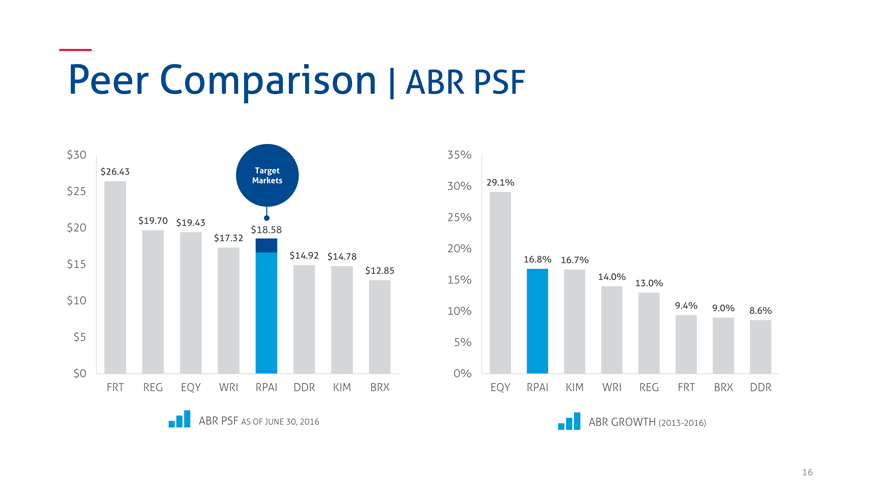

Peer Comparison | ABR PSF

$30

$26.43 Target

Markets

$25

$19.70 $19.43

$20 $18.58

$17.32

$14.92 $14.78

$15 $12.85

$10

$5

$0

FRT REG EQY WRI RPAI DDR KIM BRX

ABR PSF AS OF JUNE 30, 2016

35%

30% 29.1%

25%

20%

16.8% 16.7%

15% 14.0% 13.0%

10% 9.4% 9.0% 8.6%

5%

0%

EQY RPAI KIM WRI REG FRT BRX DDR

ABR GROWTH (2013-2016)

16

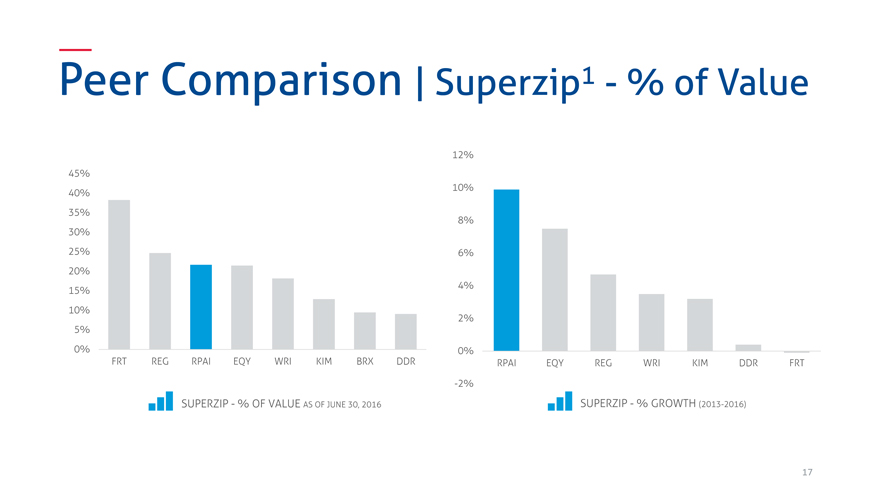

|

Peer Comparison | Superzip1—% of Value

45%

40%

35%

30%

25%

20%

15%

10%

5%

0%

FRT REG RPAI EQY WRI KIM BRX DDR

SUPERZIP—% OF VALUE AS OF JUNE 30, 2016

12%

10%

8%

6%

4%

2%

0%

RPAI EQY REG WRI KIM DDR FRT

-2%

SUPERZIP—% GROWTH (2013-2016)

17

|

MULTI-TENANT

RETAIL PORTFOLIO

2013

35 STATES, 84 MARKETS

18

|

8 S TAT E S 2 7 M S A s

I O W A BAKERSFIELD, CA SPRINGFIELD, MA WARNER ROBINS, GA COLUMBUS, IN K A N S A S COLUMBUS, OH BATON ROUGE, LA CANTON, OH LAS VEGAS, NV

M A I N E

LAWRENCE, KS DENVER, CO KANSAS CITY, MO SALT LAKE CITY, UT

M O N T A N A

SARASOTA, FL MILWAUKEE, WI OKLAHOMA CITY, OK KILLEEN, TX

N E V A D A

BANGOR, ME ST. GEORGE, UT CLEVELAND, OH POUGHKEEPSIE, NY O K L A H O M A DAVENPORT, IA BOSTON, MA KNOXVILLE, TN EAST STROUDSBURG, PA

U T A H

W I S C O N S I N MCALLEN, TX MORRISTOWN, TN PALM BAY, FL

19

|

MULTI-TENANT

RETAIL PORTFOLIO

2016

27 STATES, 58 MARKETS

Avg. 1.4 assets remaining per non-target market

20

|

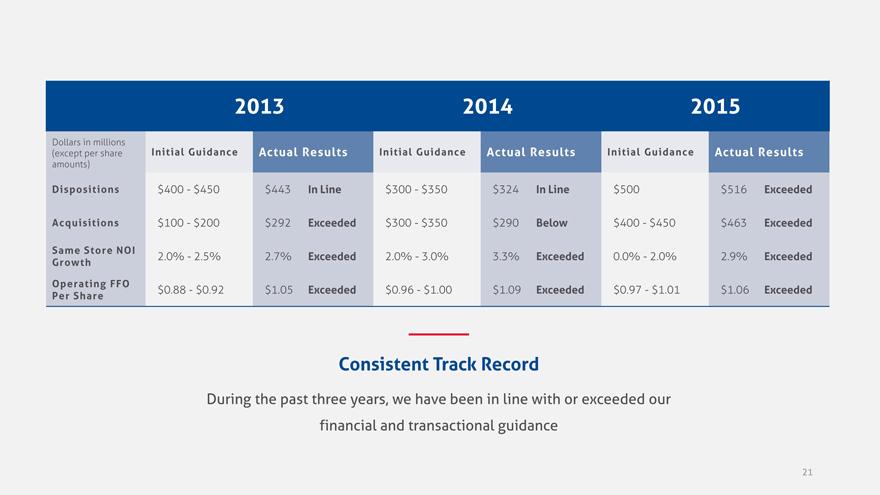

2013 2014 2015

Dollars in millions

(except per share Initial Guidance Actual Results Initial Guidance Actual Results Initial Guidance Actual Results

amounts)

Dispositions $400—$450 $443 In Line $300—$350 $324 In Line $500 $516 Exceeded

Acquisitions $100—$200 $292 Exceeded $300—$350 $290 Below $400—$450 $463 Exceeded

Same Store NOI 2.0%—2.5% 2.7% Exceeded 2.0%—3.0% 3.3% Exceeded 0.0%—2.0% 2.9% Exceeded

Growth

Operating FFO $0.88—$0.92 $1.05 Exceeded $0.96—$1.00 $1.09 Exceeded $0.97—$1.01 $1.06 Exceeded

Per Share

Consistent Track Record

During the past three years, we have been in line with or exceeded our

financial and transactional guidance

21

|

2 0 1 6

INVESTOR DAY

How does RPAI think about acquisitions, leasing and redevelopment?

How does RPAI think about its balance sheet?

What is the revised timeline for our strategic plan?

22

|

10 YEAR PLAN

2014 2015 2016 2017 2018

2019 2020 2021 2022 2023

23

|

5 YEAR PLAN

2014 2015 2016 2017 2018

2019 2020 2021 2022 2023

24

|

ONLY 2 YEARS LEFT

2014 2015 2016 2017 2018

25

|

R P A I ’ S P L A Y B O O K

Great real estate is the foundation of our future success

Shane Garrison

26

|

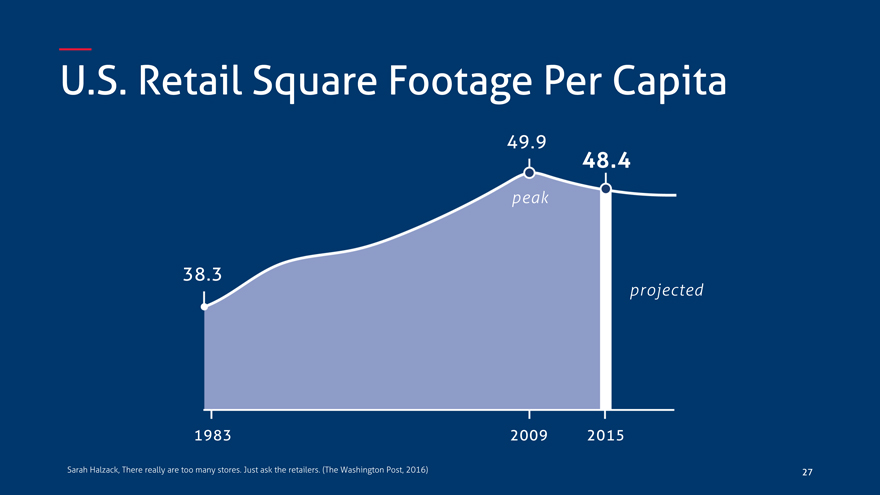

U.S. Retail Square Footage Per Capita

49.9

48.4

peak

38 projected

1983 2009 2015

Sarah Halzack, There really are too many stores. Just ask the retailers. (The Washington Post, 2016)

27

|

Retail Real Estate

is Bifurcating

RPAI’s repositioning strategy is migrating

the portfolio to the bookends

“Consumers must buy” “Consumers want to buy”

Convenience & Density Commodity Experiential

High density Outdated store spacing model Affluent demographics

Strong barriers to entry Weak relative demographic profiles Live, work, shop, play

Superior access and Markedly lower pricing power Strong daytime population

exposure

Highly educated

Strong daytime population

Lower dwell times Higher dwell times

Transit oriented

28

|

Practical Approach

Great real estate for the long term leads to… Long-Term Value Creation

More inward focus Less need to transact externally for growth Opportunities for densification

29

|

A C Q U I S I T I O N S P O T L I G H T

Shane Garrison

30

|

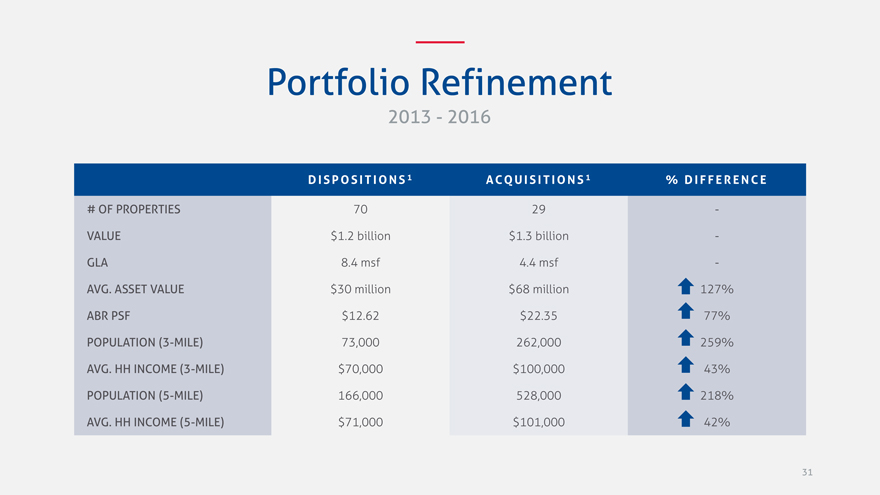

Portfolio Refinement

2013—2016

D I S P O S I T I O N S 1 ACQ U I S I T I O N S 1% D I F F E R E N C E

# OF PROPERTIES 70 29 -

VALUE $1.2 billion $1.3 billion -

GLA 8.4 msf 4.4 msf -

AVG. ASSET VALUE $30 million $68 million 127%

ABR PSF $12.62 $22.35 77%

POPULATION (3-MILE) 73,000 262,000 259%

AVG. HH INCOME (3-MILE) $70,000 $100,000 43%

POPULATION (5-MILE) 166,000 528,000 218%

AVG. HH INCOME (5-MILE) $71,000 $101,000 42%

31

|

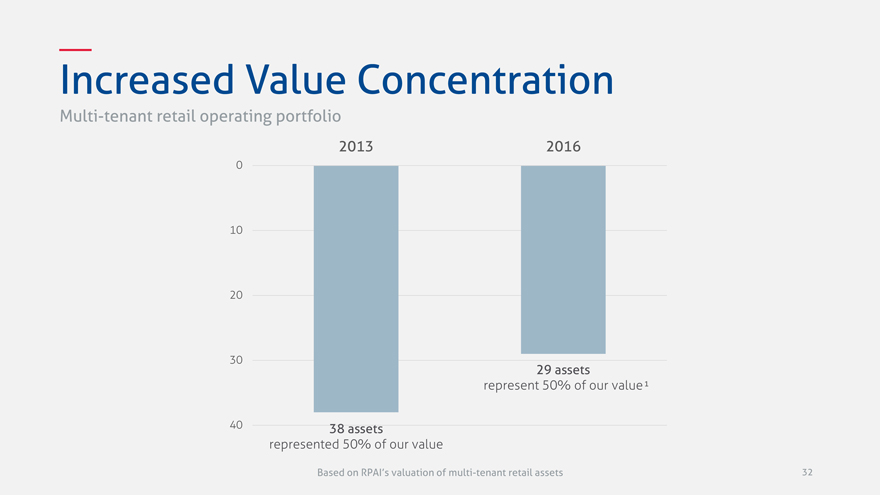

Increased Value Concentration

Multi-tenant retail operating portfolio

2013 2016

0

10

20

30

29 assets

represent 50% of our value 1

40 38 assets

represented 50% of our value

Based on RPAI’s valuation of multi-tenant retail assets

32

|

Fordham Place

33

|

Fordham Place

34

|

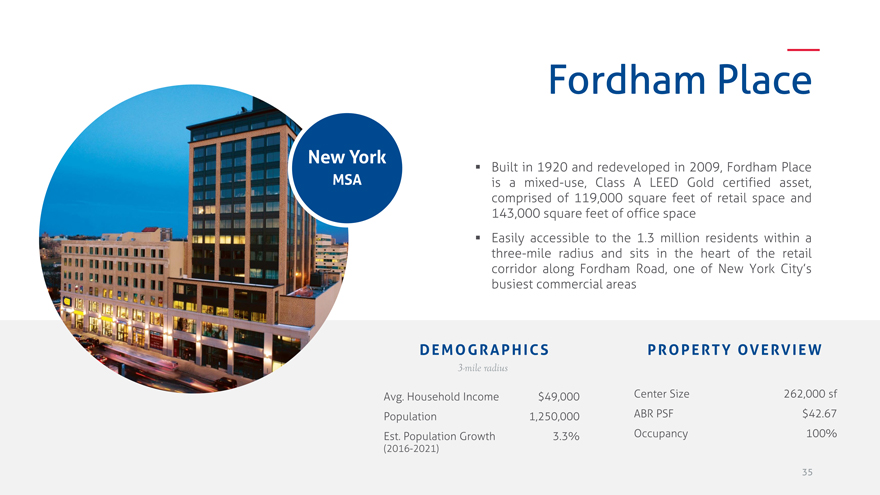

Fordham Place

New York

MSA

Built in 1920 and redeveloped in 2009, Fordham Place is a mixed-use, Class A LEED Gold certified asset, comprised of 119,000 square feet of retail space and 143,000 square feet of office space Easily accessible to the 1.3 million residents within a three-mile radius and sits in the heart of the retail corridor along Fordham Road, one of New York City’s busiest commercial areas

DEMOGRAPHICS

3-mile radius

Avg. Household Income $49,000

Population 1,250,000

Est. Population Growth 3.3%

(2016-2021)

PROPERTY OVERVIEW

Center Size 262,000 sf

ABR PSF $42.67

Occupancy 100%

35

|

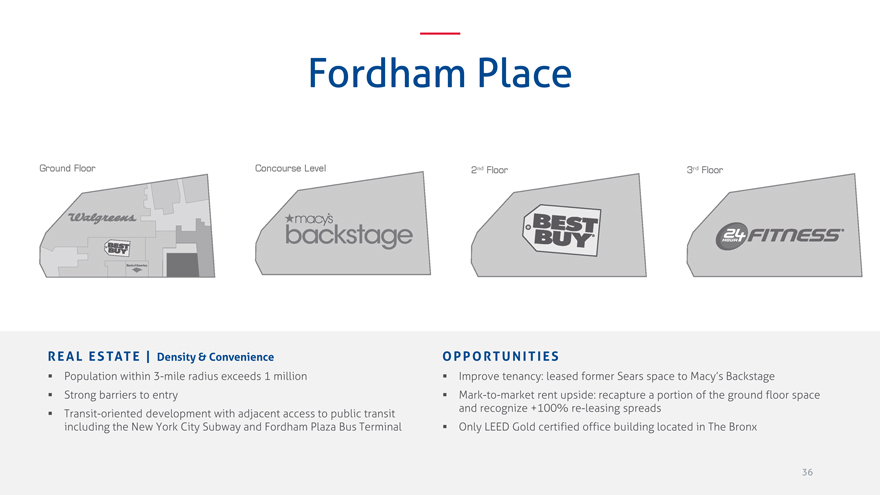

Fordham Place

REAL ESTATE | Density & Convenience

Population within 3-mile radius exceeds 1 million

Strong barriers to entry

Transit-oriented development with adjacent access to public transit

including the New York City Subway and Fordham Plaza Bus Terminal

OPPORTUNITIES

Improve tenancy: leased former Sears space to Macy’s Backstage

Mark-to-market rent upside: recapture a portion of the ground floor space

and recognize +100% re-leasing spreads

Only LEED Gold certified office building located in The Bronx

36

|

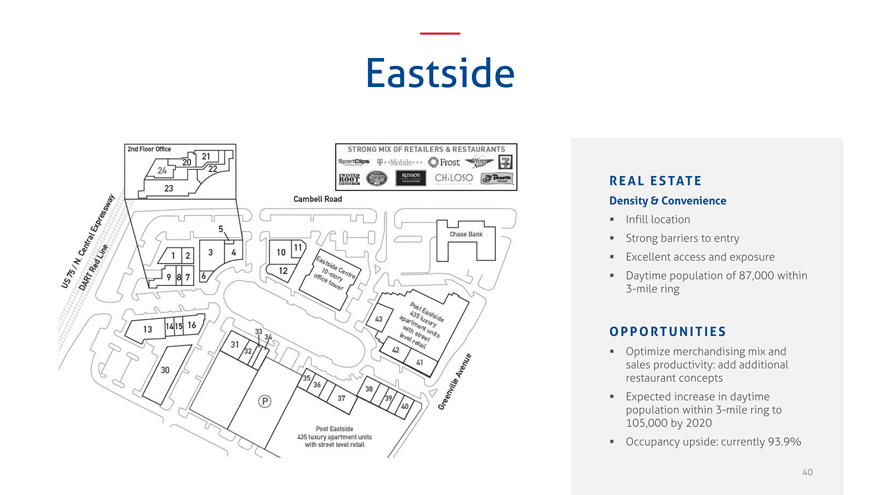

Eastside

37

|

Eastside

38

|

Eastside

Dallas

MSA

Eastside is a 67,000 square foot mixed-use center that consists of 44,000 square feet of retail space and 23,000 square feet of office space Adjacent to 435 high-end apartment units and a 10-story, 180,000 square foot Class A office tower and sits one mile from two DART Red Line Stations Surrounded by the Telecom Corridor, which includes approximately 215,000 employees within five miles, making it one of the densest high-tech areas in the U.S.

DEMOGRAPHICS

5-mile radius

Avg. Household Income $80,000

Population 354,000

Est. Population Growth 5.4%

(2016-2021)

PROPERTY OVERVIEW

Center Size 67,000 sf

Inline Sales PSF $500

Occupancy 93.9%

39

|

Eastside

REAL ESTATE

Density & Convenience

Infill location

Strong barriers to entry

Excellent access and exposure

Daytime population of 87,000 within 3-mile ring

OPPORTUNITIES

Optimize merchandising mix and sales productivity: add additional restaurant concepts

Expected increase in daytime population within 3-mile ring to 105,000 by 2020

Occupancy upside: currently 93.9%

40

|

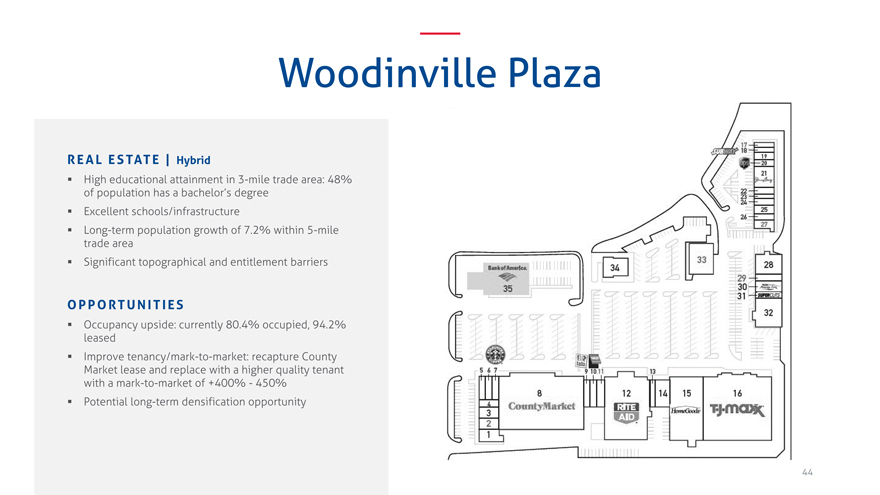

Woodinville Plaza

41

|

Woodinville Plaza

42

|

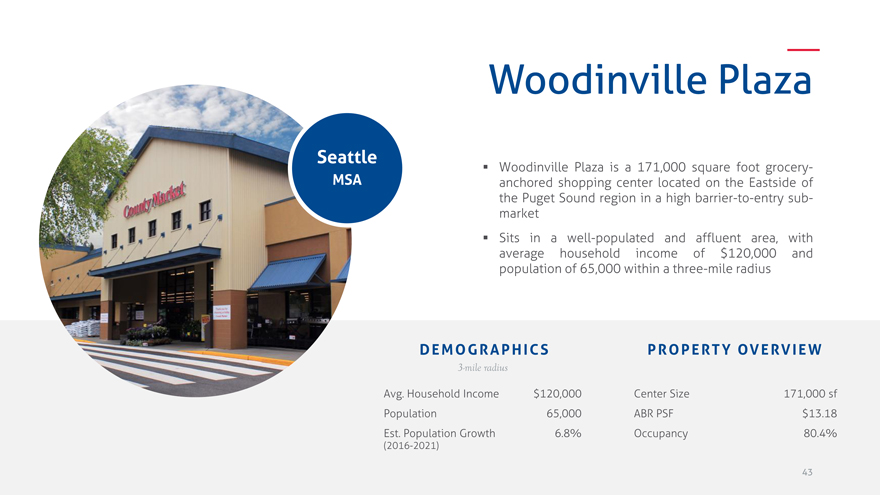

Woodinville Plaza

Seattle

MSA

Woodinville Plaza is a 171,000 square foot grocery-anchored shopping center located on the Eastside of the Puget Sound region in a high barrier-to-entry sub-market Sits in a well-populated and affluent area, with average household income of $120,000 and population of 65,000 within a three-mile radius

DEMOGRAPHICS

3-mile radius

Avg. Household Income $120,000 Population 65,000 Est. Population Growth 6.8%

(2016-2021)

PROPERTY OVERVIEW

Center Size 171,000 sf ABR PSF $13.18 Occupancy 80.4%

43

|

Woodinville Plaza

REAL ESTATE | Hybrid

High educational attainment in 3-mile trade area: 48%

of population has a bachelor’s degree

Excellent schools/infrastructure

Long-term population growth of 7.2% within 5-mile

trade area

Significant topographical and entitlement barriers

OPPORTUNITIES

Occupancy upside: currently 80.4% occupied, 94.2%

leased

Improve tenancy/mark-to-market: recapture County

Market lease and replace with a higher quality tenant

with a mark-to-market of +400%—450%

Potential long-term densification opportunity

44

|

The Shoppes at Union Hill

45

|

The Shoppes at Union Hill

46

|

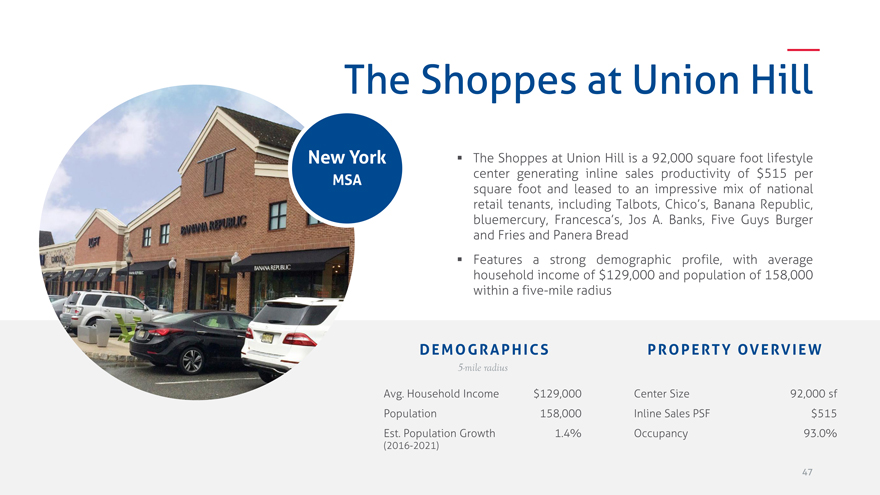

The Shoppes at Union Hill

New York

MSA

The Shoppes at Union Hill is a 92,000 square foot lifestyle center generating inline sales productivity of $515 per square foot and leased to an impressive mix of national retail tenants, including Talbots, Chico’s, Banana Republic, bluemercury, Francesca’s, Jos A. Banks, Five Guys Burger and Fries and Panera Bread Features a strong demographic profile, with average household income of $129,000 and population of 158,000 within a five-mile radius

DEMOGRAPHICS

5-mile radius

Avg. Household Income $129,000 Population 158,000 Est. Population Growth 1.4%

(2016-2021)

PROPERTY OVERVIEW

Center Size 92,000 sf Inline Sales PSF $515 Occupancy 93.0%

47

|

The Shoppes at Union Hill

REAL ESTATE | Experiential & High Discretionary Spend

High educational attainment in 5-mile trade area: 47% of population

has a bachelor’s degree

Significant discretionary spending ability

Entitlement barrier

OPPORTUNITIES

Mark-to-market rent upside: 15% over in-place rents

Occupancy upside: currently 93.0% occupied, 97.3% leased

Optimize merchandising mix and sales productivity: recently signed

lease with Soft Surroundings

Potential densification

48

|

D E V E L O P M E N T S P O T L I G H T

Shane Garrison

49

|

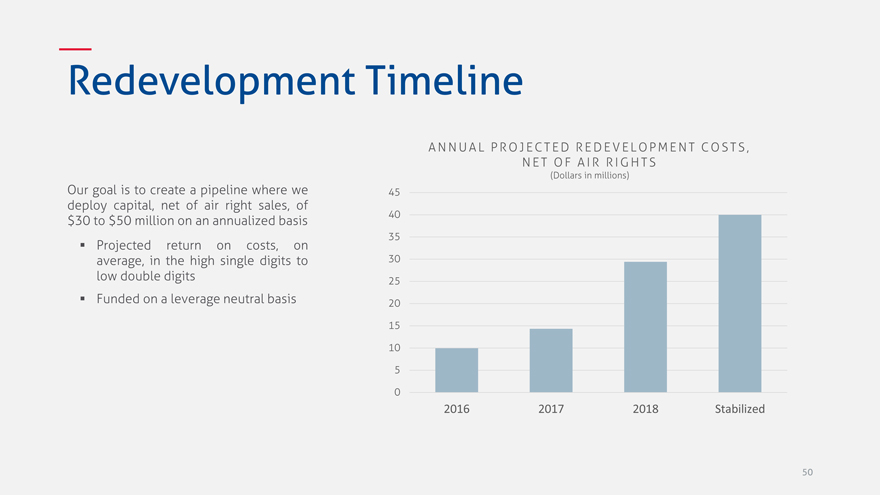

Redevelopment Timeline

Our goal is to create a pipeline where we

deploy capital, net of air right sales, of

$30 to $50 million on an annualized basis

Projected return on costs, on

average, in the high single digits to

low double digits

Funded on a leverage neutral basis

A N N U A L P R O J E C T E D R E D E V E L O P M E N T C O S T S ,

N E T O F A I R R I G H T S

(Dollars in millions)

45

40

35

30

25

20

15

10

5

0

2016 2017 2018 Stabilized

50

|

Redevelopment—Estimated Air Rights Value

160

140

$142 million1

120

millions 100

in 80

Dollars 60

40

20 $0

0

2013 2016

51

|

R E G I O N A L E X P E R I E N C E

Timothy Steffan

52

|

MARKET EXPERTISE

Timothy Steffan

President—Eastern Division

Former Senior Vice President, Asset Management and

Commercial Leasing for Macerich’s Eastern region

Greg Goldberg

Vice President, Leasing Director—Eastern Division

Former Retail Specialist for Uniwest Commercial Realty located in the

Greater Washington, D.C. area

Former Retail Specialist for Starwood Ceruzzi – Mid-Atlantic Region

Ann Smith

Vice President, Senior Leasing Director—Eastern Division

Owner and founder of Smith and Bucci Real Estate and Auctions

Former Director of Leasing for Tricor Development

Nick Over

Vice President, Director of Development

Former Development Manager at Federal Realty Investment Trust

Former Retail Development Manager and Leasing at Peterson Companies

53

|

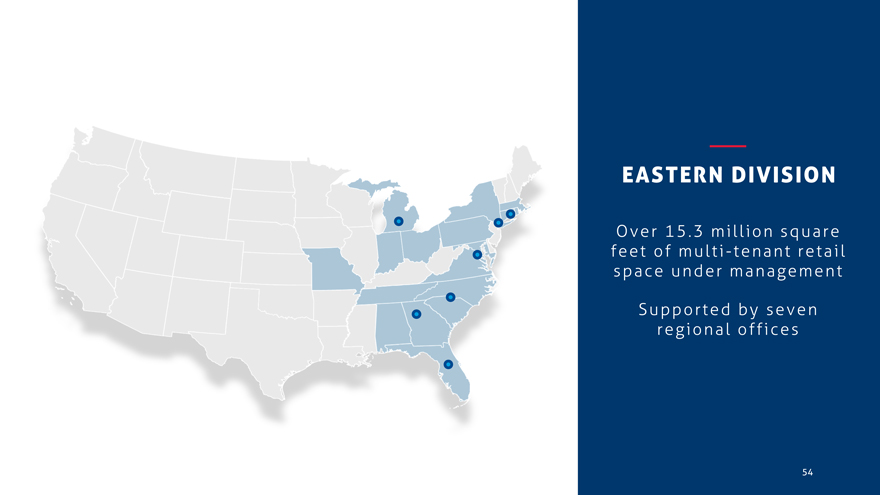

EASTERN DIVISION

Over 15.3 million square feet of multi-tenant retail space under management

Supported by seven regional offices

54

|

Local Knowledge

Ability to Play Offense and Defense

OUR

LOCAL PRESENCE

offers a unique opportunity to maximize growth within our target markets

Regional / Local Relationships

Re/Development Opportunities

55

|

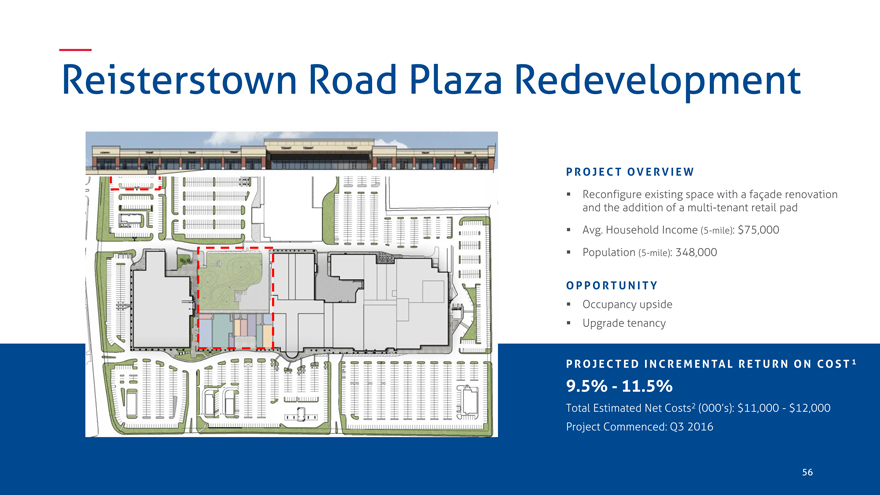

Reisterstown Road Plaza Redevelopment

P R O J E C T OV E R V I E W

Reconfigure existing space with a façade renovation

and the addition of a multi-tenant retail pad

Avg. Household Income (5-mile): $75,000

Population (5-mile): 348,000

O P P O R T U N I T Y

Occupancy upside

Upgrade tenancy

P R O J E C T E D I N C R E M E N TA L R E T U R N O N CO S T 1

9.5%—11.5%

Total Estimated Net Costs2 (000’s): $11,000—$12,000

Project Commenced: Q3 2016

56 |

|

|

Towson Circle Redevelopment

P R O J E C T OV E R V I E W

Turn the existing configuration into a mixed-use

development that will include double-sided street level

retail with approximately 390 residential units above

Avg. Household Income (5-mile): $87,000

Population (5-mile): 313,000

O P P O R T U N I T Y

Floor Area Ratio (FAR) increase of 4.6x

Integrate adjacent property Towson Square

P R O J E C T E D I N C R E M E N TA L R E T U R N O N CO S T 1

8.0%—10.0%

Total Estimated Net Costs2 (000’s): $30,000—$32,000

Targeted Commencement: Q3 2017

57 |

|

|

Merrifield Town Center II Redevelopment

P R O J E C T OV E R V I E W

Turn an existing thrift store and storage facility into a

vibrant vertically-integrated, mixed-use site with 300

– 335 vertical residential units

Avg. Household Income (5-mile): $147,000

Population (5-mile): 360,000

O P P O R T U N I T Y

Projected mark-to-market rent of 200%—250%

Integrate adjacent property Merrifield Town Center I

58 |

|

|

L O O K I N G F O R W A R D

Shane Garrison

59

|

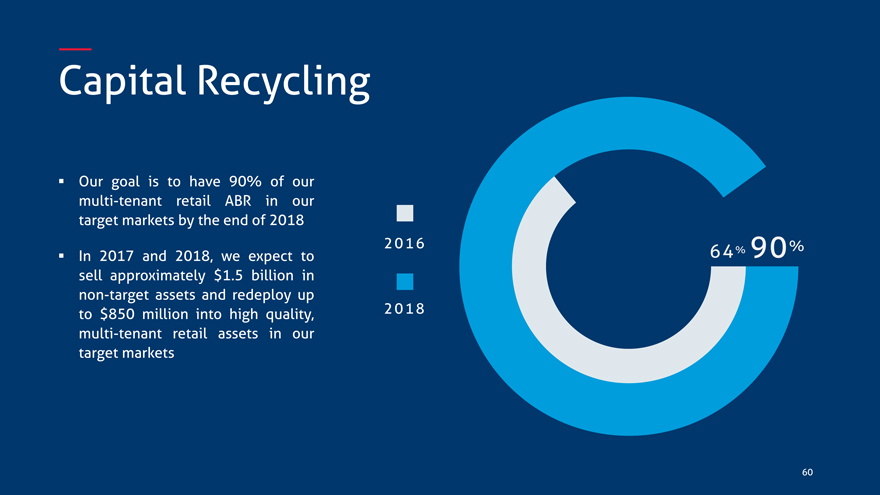

Capital Recycling

Our goal is to have 90% of our

multi-tenant retail ABR in our

target markets by the end of 2018

In 2017 and 2018, we expect to

sell approximately $1.5 billion in

non-target assets and redeploy up

to $850 million into high quality,

multi-tenant retail assets in our

target markets

2016 %

64% 90

2018

60

|

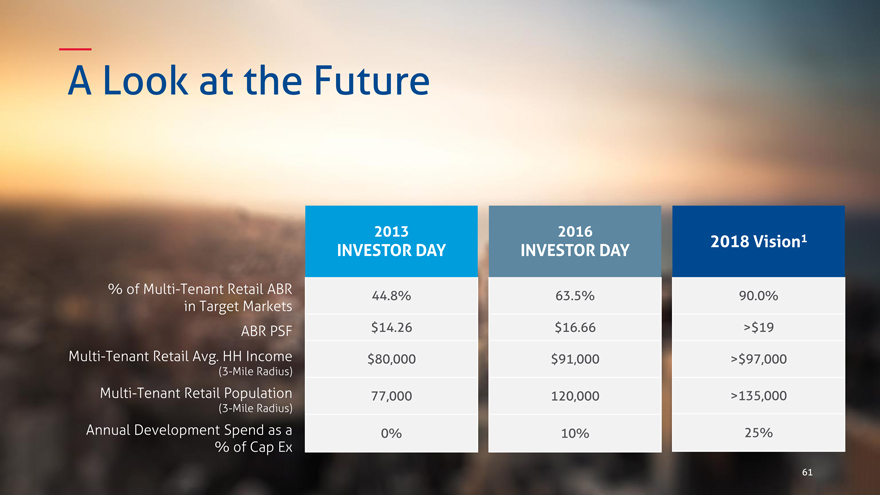

A Look at the Future

2013 2016

INVESTOR DAY INVESTOR DAY 2018 Vision1

% of Multi-Tenant Retail ABR 44.8% 63.5% 90.0%

in Target Markets

ABR PSF $14.26 $16.66 >$19

Multi-Tenant Retail Avg. HH Income $80,000 $91,000 >$97,000

(3-Mile Radius)

Multi-Tenant Retail Population 77,000 120,000 >135,000

(3-Mile Radius)

Annual Development Spend as a 0% 10% 25%

% of Cap Ex

61 |

|

|

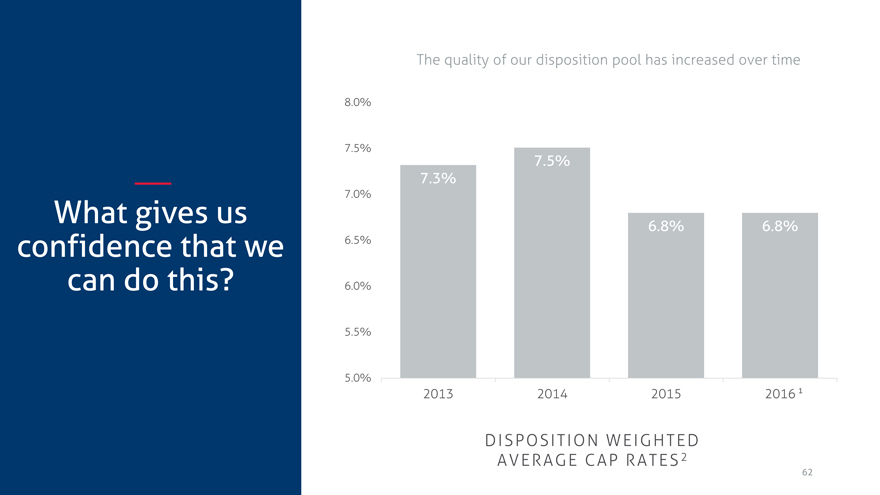

What gives us confidence that we can do this?

The quality of our disposition pool has increased over time

8.0%

7.5%

7.5%

7.3%

7.0%

6.8% |

| 6.8% |

6.5%

6.0%

5.5%

5.0%

2013 2014 2015 2016 1

DISPOSITION WEIGHTED

AVERAGE CAP RATES 2

62 |

|

|

Disposition Profile

Non-Target Multi-Tenant Retail Portfolio

Generated over 3% same store NOI growth in 2015

40% of the ABR in top 50 MSAs

Leased rate of 95.1%

$580 per square foot in grocer sales

Average 1.4 assets per MSA

63

|

S A M E S T O R E N O I G R O W T H P R O F I L E

Shane Garrison

64

|

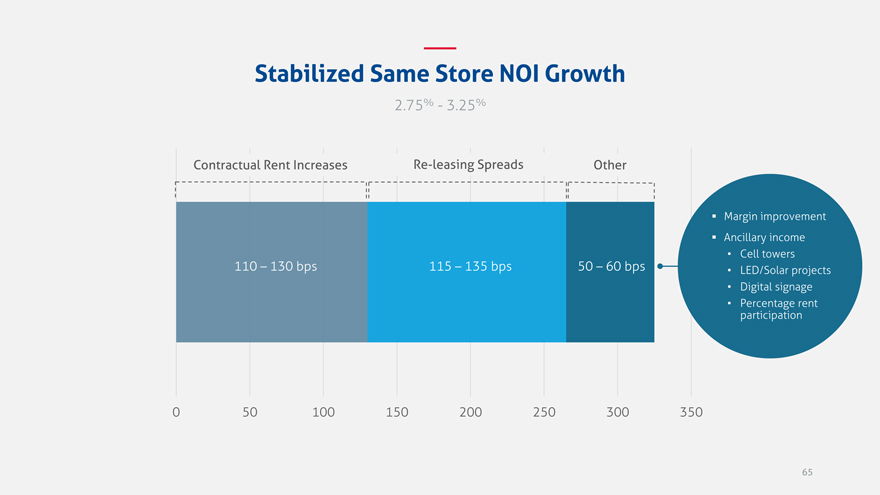

Stabilized Same Store NOI Growth

2.75%—3.25%

Contractual Rent Increases Re-leasing Spreads Other

Margin improvement

Ancillary income

Cell towers

110 – 130 bps 115 – 135 bps 50 – 60 bps LED/Solar projects

Digital signage

Percentage rent

participation

0 50 100 150 200 250 300 350

65

|

Contractual Rent Increases

150

140 135

130

120

120

110

Points 100

Basis 90 85

80 |

|

70 |

| 65 |

60 |

|

50 |

|

2013 1 2016 1 Acquisitions 2 Negotiated Leases 3

2013-2016(July 1, 2015—June 30,

2016)

66

|

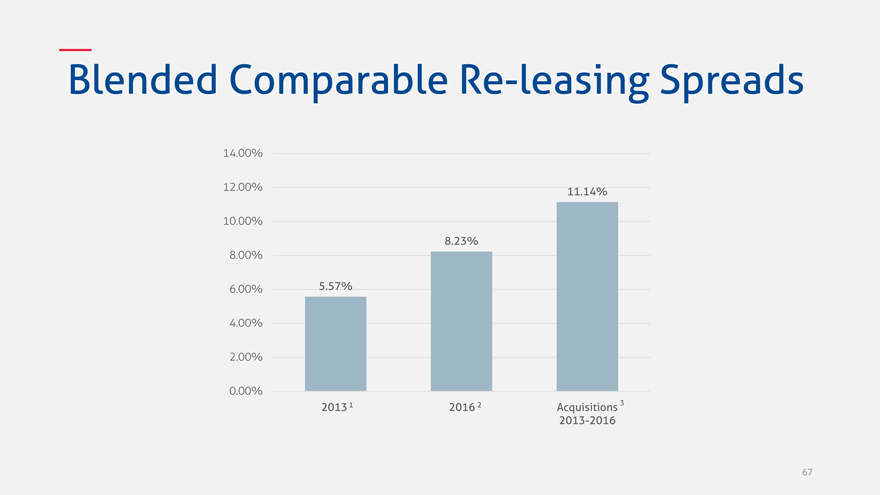

Blended Comparable Re-leasing Spreads

14.00%

12.00% 11.14%

10.00%

8.23%

8.00%

6.00% 5.57%

4.00%

2.00%

0.00%

20131 2016 2 Acquisitions 3 2013-2016

67

|

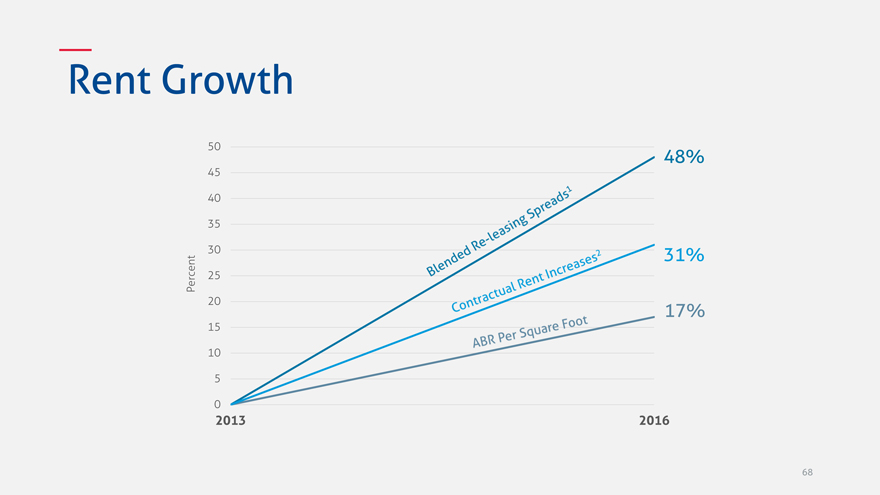

Rent Growth

50

48%

45 40 35

30 31%

Percent 25 20

17%

15 10 5

0

2013 2016

68

|

B A L A N C E S H E E T & R O A D M A P

Heath Fear

69

|

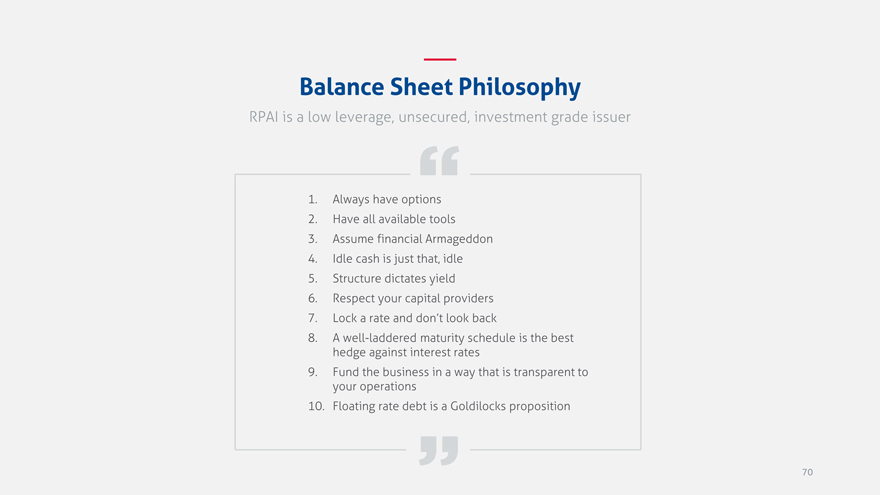

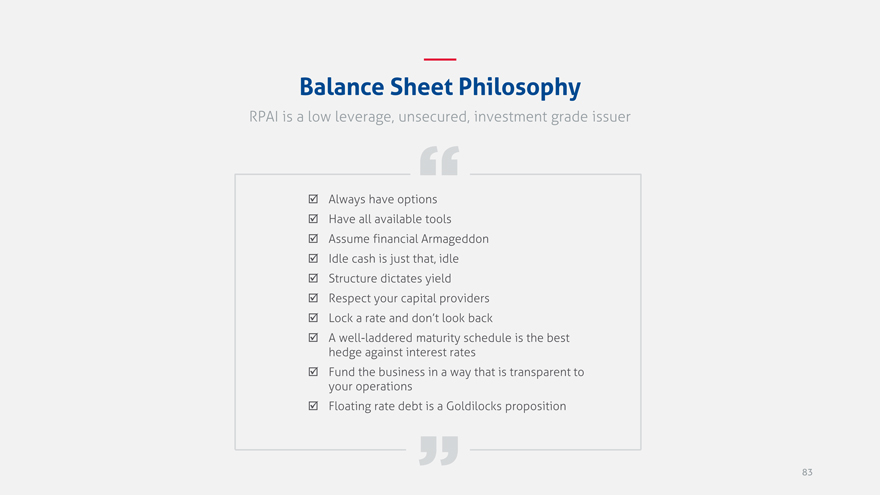

Balance Sheet Philosophy

RPAI is a low leverage, unsecured, investment grade issuer

1. Always have options

2. Have all available tools

3. Assume financial Armageddon

4. Idle cash is just that, idle

5. Structure dictates yield

6. Respect your capital providers

7. Lock a rate and don’t look back

8. A well-laddered maturity schedule is the best hedge against interest rates

9. Fund the business in a way that is transparent to your operations 10. Floating rate debt is a Goldilocks proposition

70

|

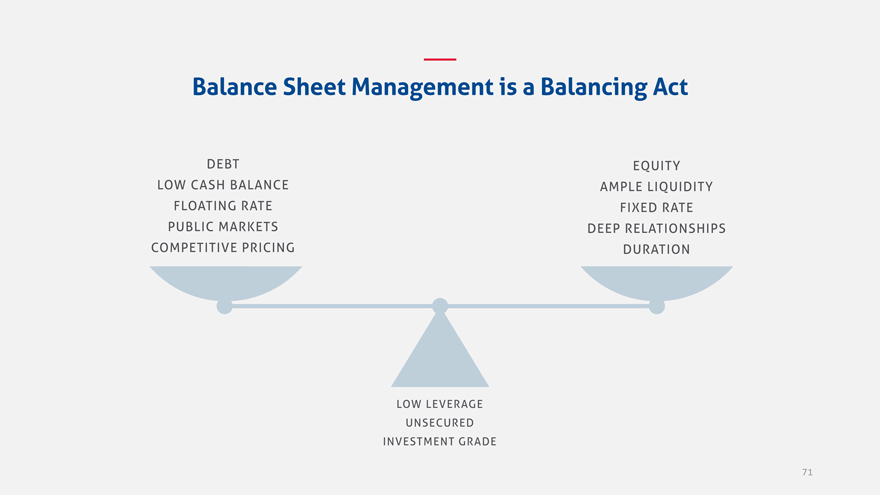

Balance Sheet Management is a Balancing Act

DEBT LOW CASH BALANCE

FLOATING RATE PUBLIC MARKETS

COMPETITIVE PRICING

EQUITY AMPLE LIQUIDITY

FIXED RATE DEEP RELATIONSHIPS

DURATION

LOW LEVERAGE UNSECURED

INVESTMENT GRADE

71

|

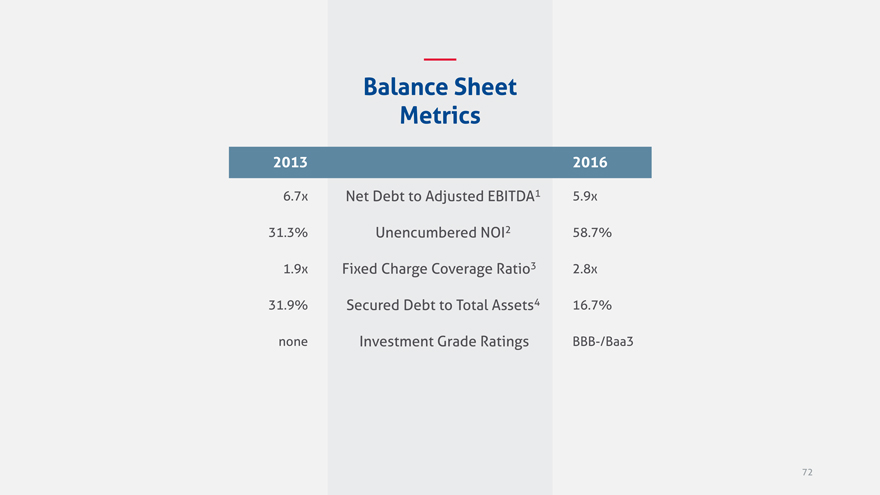

Balance Sheet Metrics

2013 2016

6.7x Net Debt to Adjusted EBITDA1 5.9x 31.3% Unencumbered NOI2 58.7% 1.9x Fixed Charge Coverage Ratio3 2.8x 31.9% Secured Debt to Total Assets4 16.7% none Investment Grade Ratings BBB-/Baa3

72

|

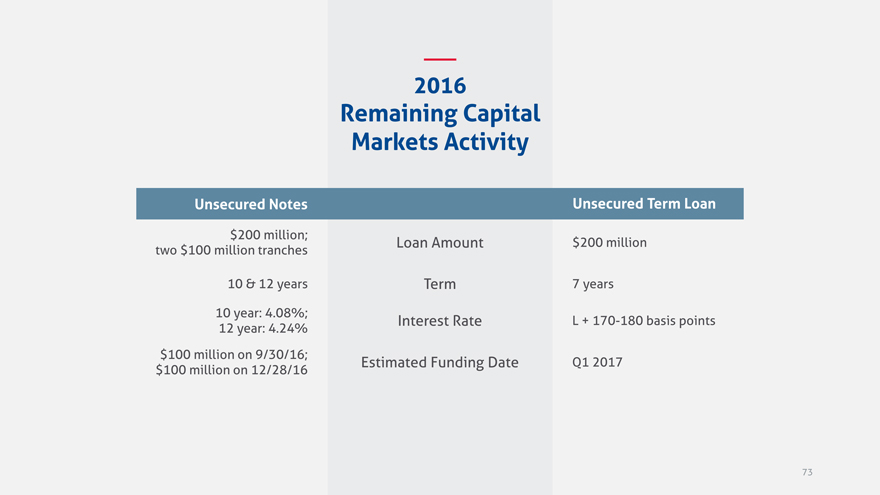

2016

Remaining Capital Markets Activity

Unsecured Notes Unsecured Term Loan

$200 million; Loan Amount $200 million

two $100 million tranches

10 & 12 years Term 7 years

10 year: 4.08%; Interest Rate L + 170-180 basis points

12 year: 4.24%

$100 million on 9/30/16; Estimated Funding Date Q1 2017

$100 million on 12/28/16

73

|

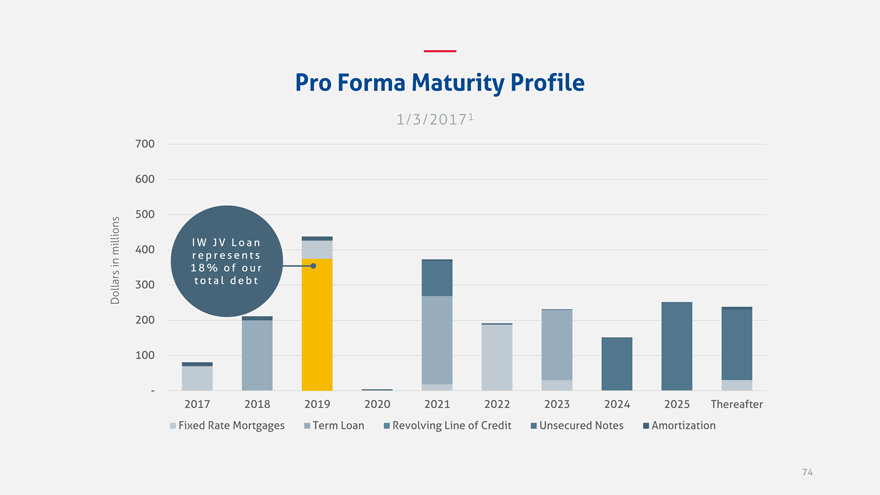

Pro Forma Maturity Profile

1/3/20171

700

600

500

millions 400 I W J V L o a n

r e p r e s e n t s

in 1 8 % o f o u r

Dollars 300 t o t a l d e b t

200

100

-

2017 2018 2019 2020 2021 2022 2023 2024 2025 Thereafter

Fixed Rate Mortgages Term Loan Revolving Line of Credit Unsecured Notes Amortization

74 |

|

|

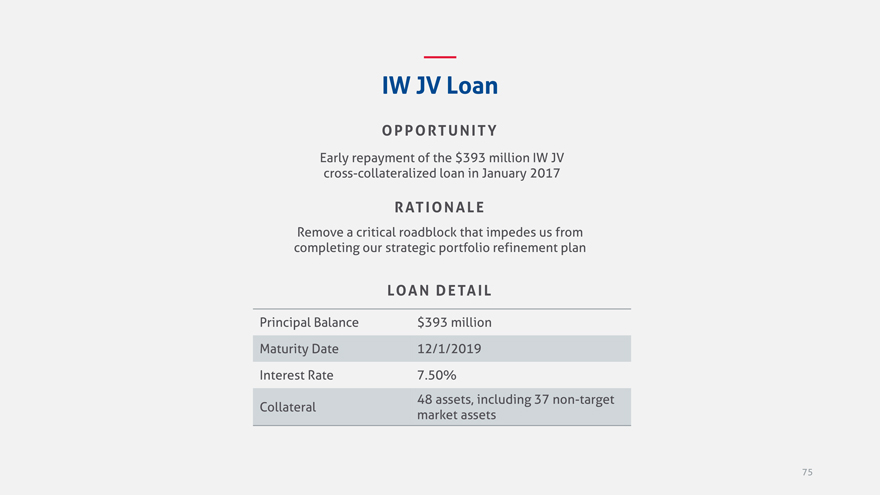

IW JV Loan

OPPORTUNITY

Early repayment of the $393 million IW JV cross-collateralized loan in January 2017

RATIONALE

Remove a critical roadblock that impedes us from completing our strategic portfolio refinement plan

LOAN DETAIL

Principal Balance $393 million

Maturity Date 12/1/2019

Interest Rate 7.50%

Collateral 48 assets, including 37 non-target

market assets

75

|

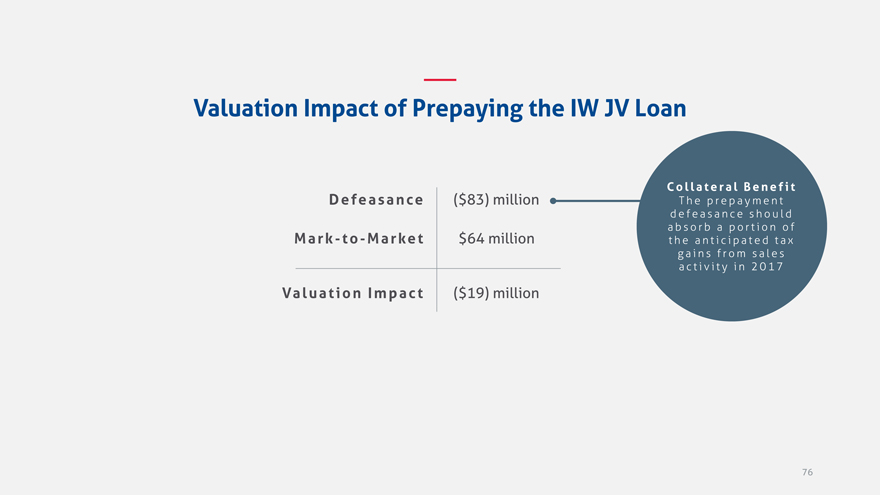

Valuation Impact of Prepaying the IW JV Loan

Defeasance ($83) million

Mark-to-Market $64 million

Valuation Impact ($19) million

C o l l a t e ra l B e n e f i t

T h e p r e p a y m e n t d e f e a s a n c e s h o u l d a b s o r b a p o r t i o n o f t h e a n t i c i p a t e d t a x g a i n s f r o m s a l e s a c t i v i t y i n 2 0 1 7

76

|

Transactional Assumptions—Roadmap

(Dollars in millions)

I N V E S T M E N T S

2H 2016 Cap Rate Timing 2017 Cap Rate Timing 2018 Cap Rate Timing Inflows Outflows

Acquisitions $1451 5.5%—6.0% Ratable $425 5.5%—6.0% Ratable $425 5.5%—6.0% Ratable $995

Dispositions $4881 6.5%—7.0% Ratable $660 6.5%—7.0% Ratable $750 6.5%—7.0% Ratable $1,898

Zurich Towers Net Proceeds $80—$100 n/a Q4 2017 $80—$100

C A P I TA L M A R K E T S

Interest

2H 2016 Interest Rate Timing 2017 Interest Rate Timing 2018 Timing Inflows Outflows

Rate

$100: 4.08% $100: 9/30/16

New—Unsecured Notes $200 $200

$100: 4.24% $100: 12/28/16

New—Unsecured Term Loan $200 L + 170-180 bps Q1 2017 $200

Scheduled Debt Payments $35 4.12% 2H 2016 $86 4.81% 2017 $5 5.41% 2018 $126

Early Debt Repayments2 $169 5.17% 2H 2016 $20 4.82% 2017 $8 7.70% 2018 $197

IW JV Loan Early Repayment3 $466 7.50% Q1 2017 $466

Preferred Equity Redemption $135 7.00% Q4 2017 $135

2018 Term Loan Early $200 1.91% 2017 $200

Repayment

2021 Term Loan Early

Repayment $100 1.97% 2018 $100

Unsecured Revolving

Line of Credit $230

Total $2.4 billion $2.4 billion

77

|

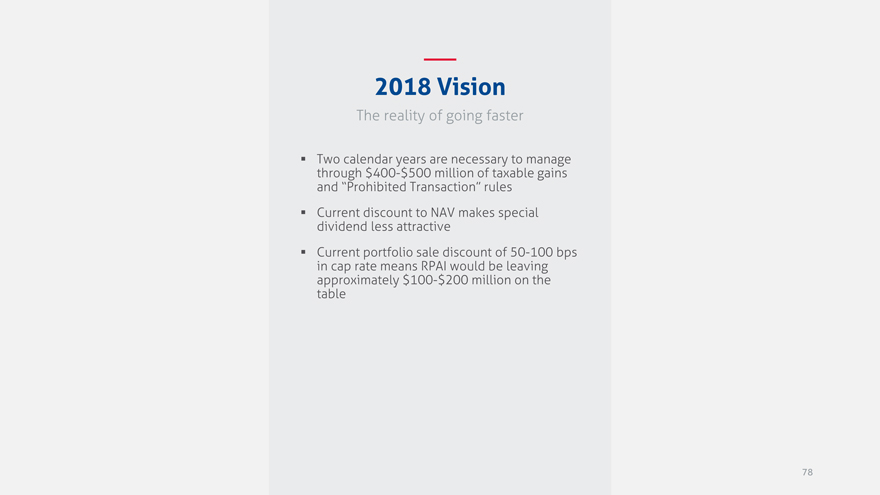

2018 Vision

The reality of going faster

Two calendar years are necessary to manage

through $400-$500 million of taxable gains

and “Prohibited Transaction” rules

Current discount to NAV makes special

dividend less attractive

Current portfolio sale discount of 50-100 bps

in cap rate means RPAI would be leaving

approximately $100-$200 million on the

table

78

|

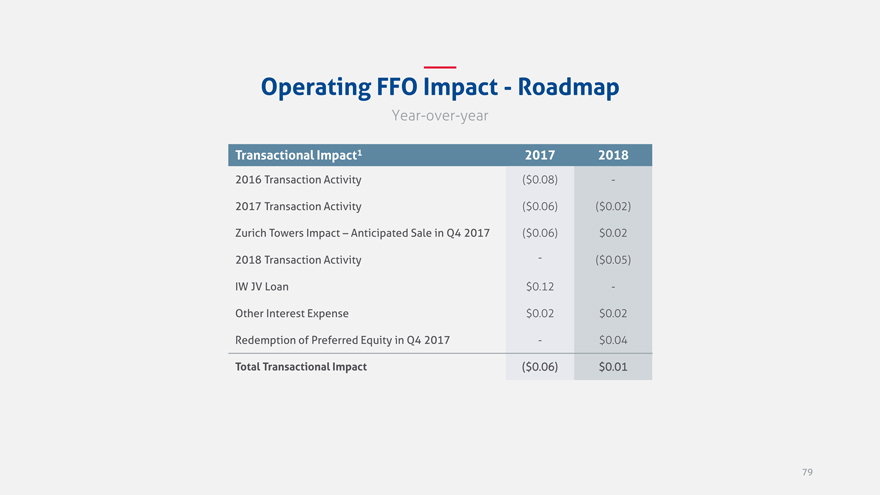

Operating FFO Impact—Roadmap

Year-over-year

Transactional Impact1 2017 2018

2016 Transaction Activity($0.08) -

2017 Transaction Activity($0.06)($0.02)

Zurich Towers Impact – Anticipated Sale in Q4 2017($0.06) $0.02

2018 Transaction Activity -($0.05)

IW JV Loan $0.12 -

Other Interest Expense $0.02 $0.02

Redemption of Preferred Equity in Q4 2017—$0.04

Total Transactional Impact($ 0.06) $ 0.01

79 |

|

|

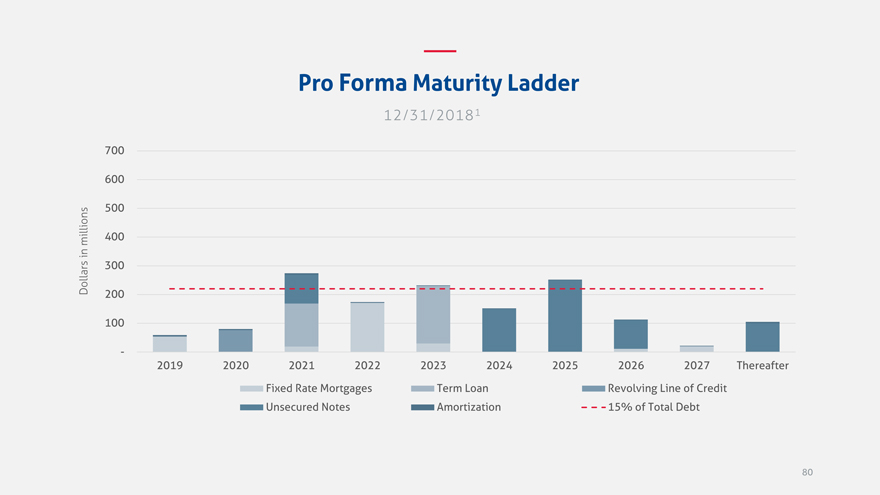

Pro Forma Maturity Ladder

12/31/2018 1

700

600

500

millions 400

in

Dollars 300

200

100

-

2019 2020 2021 2022 2023 2024 2025 2026 2027 Thereafter

Fixed Rate Mortgages Term Loan Revolving Line of Credit

Unsecured Notes Amortization 15% of Total Debt

80 |

|

|

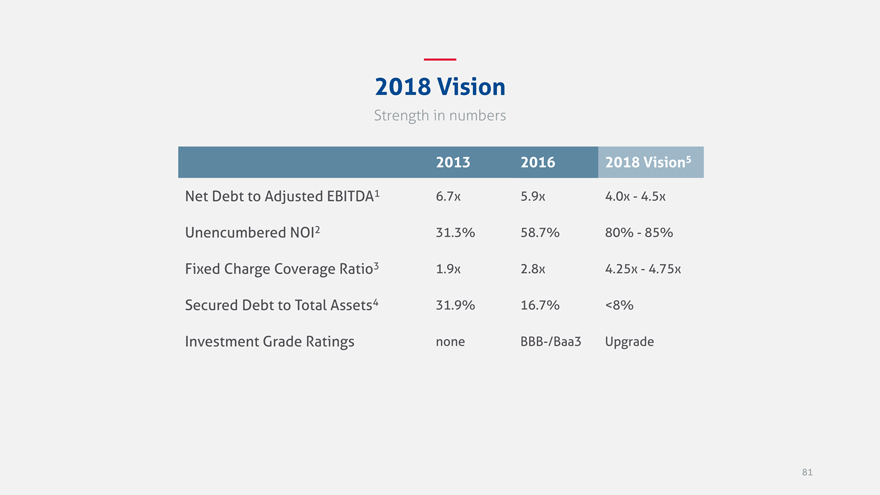

2018 Vision

Strength in numbers

2013 2016 2018 Vision5

Net Debt to Adjusted EBITDA1 6.7x 5.9x 4.0x—4.5x

Unencumbered NOI2 31.3% 58.7% 80%—85%

Fixed Charge Coverage Ratio3 1.9x 2.8x 4.25x—4.75x

Secured Debt to Total Assets4 31.9% 16.7% <8%

Investment Grade Ratings none BBB-/Baa3 Upgrade

81 |

|

|

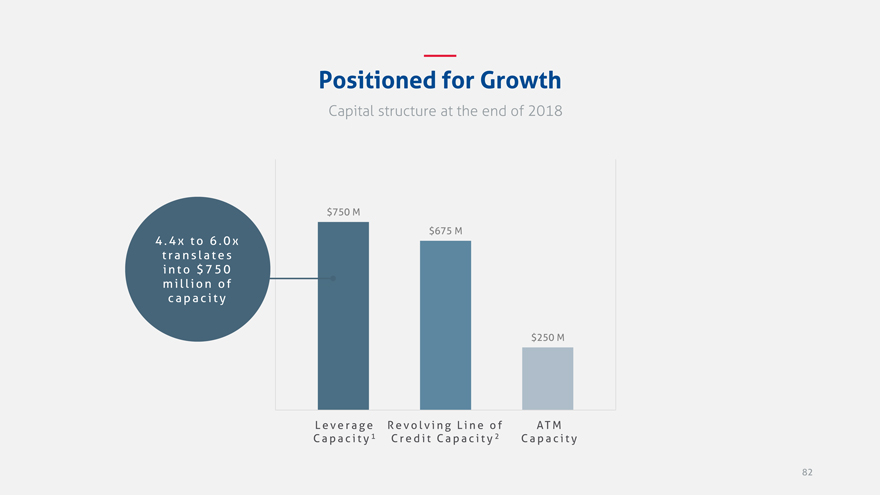

Positioned for Growth

Capital structure at the end of 2018

$750 M

$675 M

4 . 4 x t o 6 . 0 x

t r a n s l a t e s

i n t o $ 7 5 0

m i l l i o n o f

c a p a c i t y

$250 M

L e v e r a g e R e v o l v i n g L i n e o f AT M

C a p a c i t y 1 C r e d i t C a p a c i t y 2 C a p a c i t y

82

|

Balance Sheet Philosophy

RPAI is a low leverage, unsecured, investment grade issuer

Always have options

Have all available tools

Assume financial Armageddon

Idle cash is just that, idle

Structure dictates yield

Respect your capital providers

Lock a rate and don’t look back

A well-laddered maturity schedule is the best

hedge against interest rates

Fund the business in a way that is transparent to

your operations

Floating rate debt is a Goldilocks proposition

83 |

|

|

C L O S I N G R E M A R K S

Steve Grimes

84

|

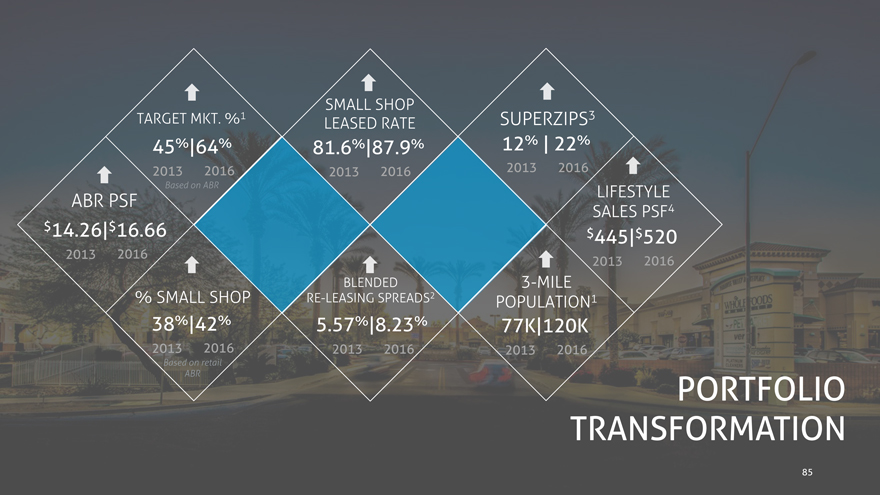

1 SMALL SHOP

TARGET MKT. % SUPERZIPS3

LEASED RATE

45%|64% 81.6%|87.9% 12% | 22%

2013 2016 2013 2016 2013 2016

Based on ABR LIFESTYLE

ABR PSF

SALES PSF4

$14.26|$16.66 $445|$520

2013 2016

2013 2016

BLENDED 3-MILE

% SMALL SHOP RE-LEASING SPREADS2 POPULATION1

38%|42% 5.57%|8.23% 77K|120K

2013 2016 2013 2016 2013 2016

Based on retail

ABR PORTFOLIO TRANSFORMATION

85

|

A Look at the Future

2013 2016

INVESTOR DAY INVESTOR DAY 2018 Vision1

% of Multi-Tenant Retail ABR 44.8% 63.5% 90.0%

in Target Markets

ABR PSF $14.26 $16.66 >$19

Multi-Tenant Retail Avg. HH Income $80,000 $91,000 >$97,000

(3-Mile Radius)

Multi-Tenant Retail Population 77,000 120,000 >135,000

(3-Mile Radius)

Annual Development Spend as a 0% 10% 25%

% of Cap Ex

Net Debt to Adjusted EBITDA2 6.7x 5.9x 4.0x – 4.5x

Investment Grade Ratings none BBB-/Baa3 Upgrade

86

|

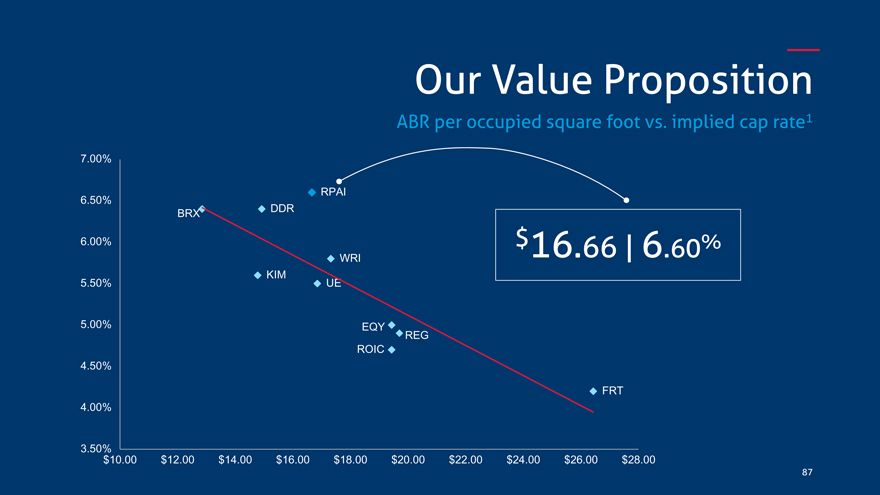

Our Value Proposition

ABR per occupied square foot vs. implied cap rate1

7.00%

6.50% RPAI DDR

BRX

6.00% $16.66 | 6.60% WRI

5.50% KIM UE

5.00% EQY REG

ROIC 4.50%

FRT 4.00%

3.50% $10.00 $12.00 $14.00 $16.00 $18.00 $20.00 $22.00 $24.00 $26.00 $28.00

87

|

THANK YOU

Today’s Takeaways

Since 2013, we have made tremendous Our local presence is at the heart of our target progress toward transforming our portfolio market strategy and our balance sheet

Our transaction thesis is solid and based on We will move faster, but not at the expense of our long-term view of the retail real estate our balance sheet philosophy and landscape transactional discipline

Good real estate densifies over time and our Our posture has moved from defensive to redevelopment pipeline has grown offensive and we are only getting stronger exponentially

88

|

Footnotes

Slide 7

1 Based on our common stock price of $16.90 as of June 30, 2016

Slide 8

1 Represents our multi-tenant retail operating portfolio

Slide 12

1 Adjusted for 2016 planned transaction activity

Slide 14

1 Represents all transactions from April 1, 2013 through June 30, 2016

2 Based on total capitalization of $6.2 billion as of March 31, 2013 3 Represents the gross value of joint ventures we have exited

Slide 15

1 Represents our multi-tenant retail operating portfolio

2 2013 represents leasing activity in our retail operating portfolio as of March 31, 2013 and for the preceding four quarters and 2016 represents leasing activity in our retail operating portfolio as of June 30, 2016 and for the preceding four quarters

3 Charles Murray, Coming Apart: The State of White America, 1960-2010 (Crown Forum, 2012). Information attributed to analysis provided by Green Street Advisors

4 Excludes three of our anticipated redevelopments, Boulevard at the Capital Centre, Reisterstown Road Plaza and Towson Circle, in addition to The Gateway which we sold during the first quarter of 2016

Slide 17

1 Charles Murray, Coming Apart: The State of White America, 1960-2010 (Crown Forum, 2012). Information attributed to analysis performed by Green Street Advisors.

Slide 31

1 Represents consolidated retail transactions from April 1, 2013 through June 30, 2016

Slide 32

1 Includes the impact of our 2016 planned transaction activity

Slide 51

1 Includes One Loudoun Downtown which is under contract

Slide 56 and 57

1 Projected Incremental Return on Cost (ROC) generally reflects only the unleveraged incremental NOI generated by the project upon stabilization and is calculated as incremental NOI divided by incremental cost. Incremental NOI is the difference between NOI expected to be generated by the stabilized project and the NOI generated prior to the commencement of active redevelopment. ROC does not include peripheral impacts, such as the impact on future lease rollover at the property or the impact on the long-term value of the property

2 Total Estimated Net Costs represent our estimated share of the project costs, net of proceeds from land sales, reimbursement from third parties and contributions from project partners, as applicable

Slide 61

1 Based on the assumptions provided in this presentation within slide 77 titled “Transactional Assumptions—Roadmap”

89

|

Footnotes (continued)

Slide 62

1 Based on the mid-point of our expected 2016 weighted average cap rate range of 6.5%—7.0%

2 All weighted average cap rates for dispositions, except for 2016, are calculated based on NOI for the trailing twelve months prior to the sale date of the disposition

Slide 66

1 Represents our multi-tenant retail operating portfolio, excluding The Gateway which we sold during the first quarter of 2016

2 Represents third-party assets acquired from April 1, 2013 through June 30, 2016

3 Represents signed new and renewal leases, excluding tenant-exercised options, from properties in our multi-tenant retail operating portfolio as of June 30, 2016

Slide 67

1 Represents leasing activity in our retail operating portfolio as of March 31, 2013 and for the preceding four quarters

2 Represents leasing activity in our retail operating portfolio as of June 30, 2016 and for the preceding four quarters

3 Represents leasing activity as of June 30, 2016 and for the preceding four quarters for third-party assets acquired from April 1, 2013 through June 30, 2016

Slide 68

1 Based on 2013 and 2016 blended comparable re-leasing spreads as reported on slide 67

2 Based on 2013 and 2016 contractual rent increases as reported on slide 66

Slide 72

1 For purposes of the Net Debt to Adjusted EBITDA ratio, EBITDA is calculated on a current quarter annualized basis and Net Debt is calculated as notional debt less cash and cash equivalents

2 For purposes of the Unencumbered NOI ratio, Unencumbered NOI is calculated based on the definitions in the agreement that governs our Unsecured Credit Facility

3 The Fixed Charge Coverage Ratio is calculated in accordance with the agreement that governs our Unsecured Credit Facility and is required to be greater than or equal to 1.50x. We include this ratio to demonstrate the extent by which we exceeded the requirement and it should not be viewed as a measure of our historical or future financial performance, financial position or cash flow

4 Secured Debt represents notional secured debt and Total Assets is calculated as GAAP book value of total assets excluding the effect of accumulated depreciation

Slide 74

1 Based on the following assumptions: unsecured private placement notes offering of $200 million, consisting of $100 million funded in September 2016 and $100 million funded in December 2016; unsecured term loan of $200 million funded in January 2017; $35 million of scheduled debt payments in the second half of 2016; $168 million of early debt repayments in the second half of 2016; and the unsecured revolving line of credit is anticipated to be zero as of 1/3/2017

Slide 77

1 2016 acquisitions and dispositions are based on the mid-point of guidance less acquisition and disposition activity during the first half of 2016

2 Includes estimate for yield maintenance of approximately $3 million and defeasance of approximately $1 million in total

3 Includes estimate for defeasance of approximately $82 million

Slide 79

1 Based on the assumptions provided in this presentation within slide 77 titled “Transactional Assumptions—Roadmap”

Slide 80

1 Based on the following assumptions: unsecured private placement notes offering of $200 million, consisting of $100 million funded in September 2016 and $100 million funded in December 2016; unsecured term loan of $200 million funded in January 2017; $35 million of scheduled debt payments in the second half of 2016, $86 million of scheduled debt payments in 2017 and $5 million of scheduled debt payments in 2018; $168 million of early debt repayments in the second half of 2016, $401 million of early debt repayments in 2017, including $384 million related to IW JV, and $7 million of early debt repayments in 2018; $200 million early repayment of the 2018 term loan in 2017; $100 million partial early repayment of the 2021 term loan in 2018; and the unsecured revolving line of credit is anticipated to be $75 million as of 12/31/2018

90

|

Footnotes (continued)

Slide 81

1 For purposes of the Net Debt to Adjusted EBITDA ratio, EBITDA is calculated on a current quarter annualized basis and Net Debt is calculated as notional debt less cash and cash equivalents

2 For purposes of the Unencumbered NOI ratio, Unencumbered NOI is calculated based on the definitions in the agreement that governs our Unsecured Credit Facility

3 The Fixed Charge Coverage Ratio is calculated in accordance with the agreement that governs our Unsecured Credit Facility and is required to be greater than or equal to 1.50x. We include this ratio to demonstrate the extent by which we exceeded and expect to exceed the requirement and it should not be viewed as a measure of our historical or future financial performance, financial position or cash flow

4 Secured Debt represents notional secured debt and Total Assets is calculated as GAAP book value of total assets excluding the effect of accumulated depreciation

5 Based on the assumptions provided in this presentation within slide 77 titled “Transaction Assumption – Roadmap”

Slide 82

1 Based on acquiring assets of similar quality to recent acquisitions

2 Our unsecured revolving line of credit has total capacity of $750 million, of which $75 million is anticipated to be drawn as of 12/31/2018

Slide 85 (see footnotes for slide 15) Slide 86

1 Based on the assumptions provided in this presentation within slide 77 titled “Transactional Assumptions—Roadmap”

2 For purposes of the Net Debt to Adjusted EBITDA ratio, EBITDA is calculated on a current quarter annualized basis and Net Debt is calculated as notional debt less cash and cash equivalents

Slide 87

1 Implied cap rates are sourced from Green Street Advisors as of September 12, 2016

91

|

Non-GAAP Financial Measures & Other Definitions

Gross Leasable Area (GLA)

Gross Leasable Area (GLA) is defined as the aggregate number of square feet available for lease. GLA excludes square footage attributable to third-party managed storage units, of which we owned 62,000 square feet as of June 30, 2016.

Occupancy

Occupancy is defined, for a property or group of properties, as the ratio, expressed as a percentage, of (a) the number of square feet of such property economically occupied by tenants under leases with an initial term of greater than one year, to (b) the aggregate number of square feet for such property.

Percent Leased Including Signed (Leased)

Percent Leased Including Signed (Leased) is defined, for a property or group of properties, as the ratio, expressed as a percentage, of (a) the sum of occupied square feet (pursuant to the definition above) of such property and vacant square feet for which a lease with an initial term of greater than one year has been signed, but rent has not yet commenced, to (b) the aggregate number of square feet for such property.

Funds From Operations (FFO) Attributable to Common Shareholders

As defined by the National Association of Real Estate Investment Trusts (NAREIT), an industry trade group, Funds From Operations (FFO) means net income (loss) computed in accordance with generally accepted accounting principles (GAAP), excluding gains (or losses) from sales of depreciable real estate, plus depreciation and amortization and impairment charges on depreciable real estate. We have adopted the NAREIT definition in our computation of FFO attributable to common shareholders. Management believes that, subject to the following limitations, FFO attributable to common shareholders provides a basis for comparing our performance and operations to those of other real estate investment trusts (REITs). We believe that FFO attributable to common shareholders, which is a supplemental non-GAAP financial measure, provides an additional and useful means to assess the operating performance of REITs. FFO attributable to common shareholders does not represent an alternative to (i) “Net income” or “Net income attributable to common shareholders” as an indicator of our financial performance, or (ii) “Cash flows from operating activities” in accordance with GAAP as a measure of our capacity to fund cash needs, including the payment of dividends.

Operating FFO Attributable to Common Shareholders

Operating FFO attributable to common shareholders is defined as FFO attributable to common shareholders excluding the impact of discrete non-operating transactions and other events which we do not consider representative of the comparable operating results of our core business platform, our real estate operating portfolio. Specific examples of discrete non-operating transactions and other events include, but are not limited to, the financial statement impact of gains or losses associated with the early extinguishment of debt or other liabilities, impairment charges to write down the carrying value of assets other than depreciable real estate, actual or anticipated settlement of litigation involving the Company and executive and realignment separation charges, which are otherwise excluded from our calculation of FFO attributable to common shareholders. We believe that Operating FFO attributable to common shareholders, which is a supplemental non-GAAP financial measure, provides an additional and useful means to assess the operating performance of REITs. Operating FFO attributable to common shareholders does not represent an alternative to (i) “Net income” or “Net income attributable to common shareholders” as an indicator of our financial performance, or (ii) “Cash flows from operating activities” in accordance with GAAP as a measure of our capacity to fund cash needs, including the payment of dividends. Comparison of our presentation of Operating FFO attributable to common shareholders to similarly titled measures for other REITs may not necessarily be meaningful due to possible differences in definition and application by such REITs.

92

|

Non-GAAP Financial Measures & Other Definitions (continued)

Net Operating Income (NOI)

We define Net Operating Income (NOI) as all revenues other than straight-line rental income, amortization of lease inducements, amortization of acquired above and below market lease intangibles and lease termination fee income, less real estate taxes and all operating expenses other than straight-line ground rent expense and amortization of acquired ground lease intangibles, which are non-cash items. NOI consists of Same Store NOI and NOI from Other Investment Properties. We believe that NOI, which is a supplemental non-GAAP financial measure, provides an additional and useful operating perspective not immediately apparent from “Operating income” or “Net income attributable to common shareholders” in accordance with GAAP. We use NOI to evaluate our performance on a property-by-property basis because this measure allows management to evaluate the impact that factors such as lease structure, lease rates and tenant base have on our operating results. NOI does not represent an alternative to “Net income” or “Net income attributable to common shareholders” in accordance with GAAP as an indicator of our financial performance. Comparison of our presentation of NOI to similarly titled measures for other REITs may not necessarily be meaningful due to possible differences in definition and application by such REITs.

Same Store NOI and NOI from Other Investment Properties

Same Store NOI for the year ended December 31, 2013 represents NOI from our same store portfolio consisting of 223 operating properties acquired or placed in service prior to January 1, 2012, excluding one operating property that was classified as held for sale as of December 31, 2013, which is accounted for within discontinued operations. NOI from Other Investment Properties for the year ended December 31, 2013 represents NOI primarily from properties acquired in 2013, our development properties and one former development property that was not classified within our operating property portfolio for both periods presented.

Same Store NOI for the year ended December 31, 2014 represents NOI from our same store portfolio consisting of 197 operating properties acquired or placed in service and stabilized prior to January 1, 2013. NOI from Other Investment Properties for the year ended December 31, 2014 represents NOI primarily from properties acquired during 2013 and 2014, our development properties, a property where we have begun activities in anticipation of future redevelopment, the investment properties that were sold or held for sale in 2014 that did not qualify for discontinued operations treatment, and the historical ground rent expense related to an existing same store investment property that was subject to a ground lease with a third party prior to our acquisition of the fee interest during 2014.

Same Store NOI for the year ended December 31, 2015 represents NOI from our same store portfolio consisting of 180 operating properties acquired or placed in service and stabilized prior to January 1, 2014. NOI from Other Investment Properties for the year ended December 31, 2015 represents NOI primarily from properties acquired during 2014 and 2015, our development property, two properties where we have begun activities in anticipation of future redevelopment, one property that was impaired below its debt balance during 2014, the properties that were sold or held for sale in 2014 and 2015 that did not qualify for discontinued operations treatment and the historical ground rent expense related to an existing same store investment property that was subject to a ground lease with a third party prior to our acquisition of the fee interest during the first quarter of 2014. In addition, the financial results reported in Other Investment Properties for the year ended December 31, 2015 include the net income from our wholly-owned captive insurance company, which was formed on December 1, 2014, and the financial results reported in Other Investment Properties for the year ended December 31, 2014 include the historical intercompany expense elimination related to our former insurance captive unconsolidated joint venture investment, in which we terminated our participation effective December 1, 2014. For the year ended December 31, 2014, the historical captive insurance expense related to our portfolio was recorded in equity in loss of unconsolidated joint ventures, net.

We believe that Same Store NOI and NOI from Other Investment Properties, which are supplemental non-GAAP financial measures, provide an additional and useful operating perspective not immediately apparent from “Operating income” or “Net income attributable to common shareholders” in accordance with GAAP. We use these measures to evaluate our performance on a property-by-property basis because they allow management to evaluate the impact that factors such as lease structure, lease rates and tenant base have on our operating results. Same Store NOI and NOI from Other Investment Properties do not represent alternatives to “Net income” or “Net income attributable to common shareholders” in accordance with GAAP as indicators of our financial performance. Comparison of our presentation of Same Store NOI and NOI from Other Investment Properties to similarly titled measures for other REITs may not necessarily be meaningful due to possible differences in definition and application by such REITs.

93

|

Non-GAAP Financial Measures & Other Definitions (continued)

Non-target market multi-tenant retail same store NOI, Target market multi-tenant retail same store NOI and Other same store NOI

Non-target market multi-tenant retail same store NOI for the year ended December 31, 2015 represents same store NOI from the multi-tenant retail same store properties located outside of our target markets. Target market multi-tenant retail same store NOI represents same store NOI from the multi-tenant retail same store properties located within our target markets. Other same store NOI represents same store NOI from our same store single-user retail properties and our one remaining office property.

We believe that non-target market multi-tenant retail same store NOI, target market multi-tenant retail same store NOI and other same store NOI, which are supplemental non-GAAP financial measures, provide an additional and useful operating perspective not immediately apparent from “Operating income” or “Net income attributable to common shareholders” in accordance with GAAP. We use these measures to evaluate our performance on a property-by-property basis because they allow management to evaluate the impact that factors such as lease structure, lease rates and tenant base have on our operating results. Non-target market multi-tenant retail same store NOI, target market multi-tenant retail same store NOI and other same store NOI do not represent alternatives to “Net income” or “Net income attributable to common shareholders” in accordance with GAAP as indicators of our financial performance. Comparison of our presentation of non-target market multi-tenant retail same store NOI, target market multi-tenant retail same store NOI and other same store NOI to similarly titled measures for other REITs may not necessarily be meaningful due to possible differences in definition and application by such REITs.

Adjusted EBITDA

Adjusted EBITDA is a supplemental non-GAAP financial measure and represents net income attributable to common shareholders before interest, income taxes, depreciation and amortization, as further adjusted to eliminate the impact of certain items that we do not consider indicative of our ongoing performance. We believe that Adjusted EBITDA is useful because it allows investors and management to evaluate and compare our performance from period to period in a meaningful and consistent manner in addition to standard financial measurements under GAAP. Adjusted EBITDA should not be considered an alternative to “Net income attributable to common shareholders” as an indicator of our financial performance. Comparison of our presentation of Adjusted EBITDA to similarly titled measures for other REITs may not necessarily be meaningful due to possible differences in definition and application by such REITs.

Net Debt to Adjusted EBITDA

Net Debt to Adjusted EBITDA is a supplemental non-GAAP financial measure and represents (i) our total notional debt, excluding unamortized premium, discount and capitalized loan fees, less cash and cash equivalents divided by (ii) Adjusted EBITDA for the prior three months, annualized. We believe that this ratio is useful because it provides investors with information regarding our total notional debt net of cash and cash equivalents, which could be used to repay debt, compared to our performance as measured using Adjusted EBITDA. Comparison of our presentation of Net Debt to Adjusted EBITDA to similarly titled measures for other REITs may not necessarily be meaningful due to possible differences in definition and application by such REITs.

Unencumbered NOI ratio

Unencumbered NOI ratio is a supplemental non-GAAP financial measure and represents (i) NOI from the unencumbered properties in our portfolio, as defined by the agreement that governs our Unsecured Credit Facility (comprised of the unsecured term loans and unsecured revolving line of credit) in effect at the end of the given period, for the trailing twelve month period, divided by (ii) total NOI, as defined by the agreement that governs our Unsecured Credit Facility in effect at the end of the given period, for the same trailing twelve month period. We believe that this ratio is useful because it allows investors and management to understand and evaluate our progress in unencumbering our portfolio. Unencumbered NOI ratio should not be considered an alternative to “Net income attributable to common shareholders” as an indicator of our financial performance. Comparison of our presentation of Unencumbered NOI ratio to similarly titled measures for other REITs may not necessarily be meaningful due to possible differences in definition and application by such REITs. For a complete listing of definitions related to our Unsecured Credit Facility, refer to the Fourth Amended and Restated Credit Agreement filed as Exhibit 10.8 to our Annual Report on Form 10-K for the year ended December 31, 2015, filed on February 17, 2016, the Third Amended and Restated Credit Agreement filed as Exhibit 10.1 to our Current Report on Form 8-K, dated May 13, 2013, and the Second Amended and Restated Credit Agreement filed as Exhibit 10.4 to Amendment No. 5 of our Form S-11, dated March 9, 2012.

94

|

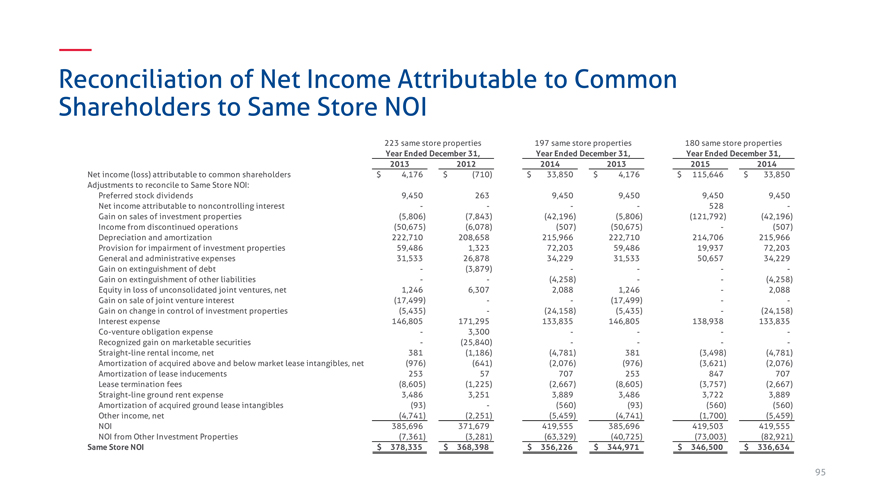

Reconciliation of Net Income Attributable to Common

Shareholders to Same Store NOI

223 same store properties 197 same store properties 180 same store properties

Year Ended December 31, Year Ended December 31, Year Ended December 31,

2013 2012 2014 2013 2015 2014

Net income (loss) attributable to common shareholders $ 4,176 $ (710) $ 33,850 $ 4,176 $ 115,646 $ 33,850

Adjustments to reconcile to Same Store NOI:

Preferred stock dividends 9,450 263 9,450 9,450 9,450 9,450

Net income attributable to noncontrolling interest — — 528 -

Gain on sales of investment properties(5,806)(7,843)(42,196)(5,806)(121,792)(42,196)

Income from discontinued operations(50,675)(6,078)(507)(50,675) -(507)

Depreciation and amortization 222,710 208,658 215,966 222,710 214,706 215,966

Provision for impairment of investment properties 59,486 1,323 72,203 59,486 19,937 72,203

General and administrative expenses 31,533 26,878 34,229 31,533 50,657 34,229

Gain on extinguishment of debt -(3,879) — —

Gain on extinguishment of other liabilities —(4,258) —(4,258)

Equity in loss of unconsolidated joint ventures, net 1,246 6,307 2,088 1,246—2,088

Gain on sale of joint venture interest(17,499) —(17,499) —

Gain on change in control of investment properties(5,435) -(24,158)(5,435) -(24,158)

Interest expense 146,805 171,295 133,835 146,805 138,938 133,835

Co-venture obligation expense—3,300 — —

Recognized gain on marketable securities -(25,840) — —

Straight-line rental income, net 381(1,186)(4,781) 381(3,498)(4,781)

Amortization of acquired above and below market lease intangibles, net(976)(641)(2,076)(976)(3,621)(2,076)

Amortization of lease inducements 253 57 707 253 847 707

Lease termination fees(8,605)(1,225)(2,667)(8,605)(3,757)(2,667)

Straight-line ground rent expense 3,486 3,251 3,889 3,486 3,722 3,889

Amortization of acquired ground lease intangibles(93) -(560)(93)(560)(560)

Other income, net(4,741)(2,251)(5,459)(4,741)(1,700)(5,459)

NOI 385,696 371,679 419,555 385,696 419,503 419,555

NOI from Other Investment Properties(7,361)(3,281)(63,329)(40,725)(73,003)(82,921)

Same Store NOI $ 378,335 $ 368,398 $ 356,226 $ 344,971 $ 346,500 $ 336,634

95 |

|

|

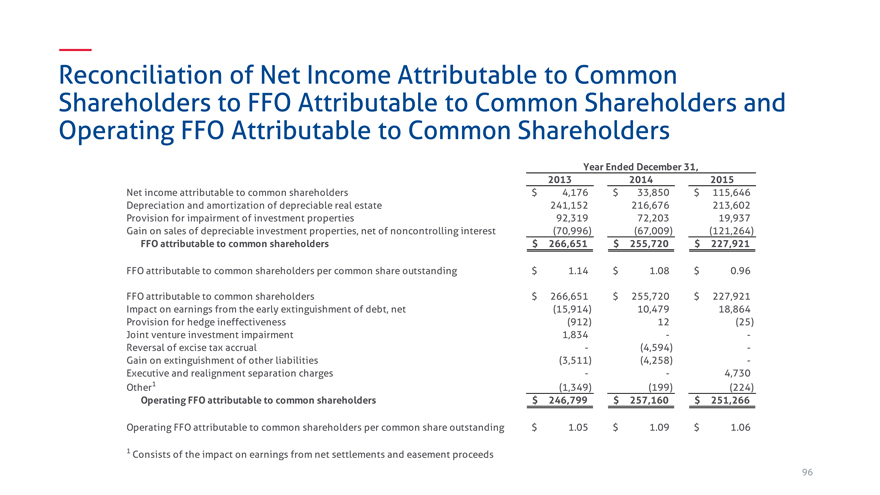

Reconciliation of Net Income Attributable to Common

Shareholders to FFO Attributable to Common Shareholders and

Operating FFO Attributable to Common Shareholders

Year Ended December 31,

2013 2014 2015

Net income attributable to common shareholders $ 4,176 $ 33,850 $ 115,646

Depreciation and amortization of depreciable real estate 241,152 216,676 213,602

Provision for impairment of investment properties 92,319 72,203 19,937

Gain on sales of depreciable investment properties, net of noncontrolling interest(70,996)(67,009)(121,264)

FFO attributable to common shareholders $ 266,651 $ 255,720 $ 227,921

FFO attributable to common shareholders per common share outstanding $ 1.14 $ 1.08 $ 0.96

FFO attributable to common shareholders $ 266,651 $ 255,720 $ 227,921

Impact on earnings from the early extinguishment of debt, net(15,914) 10,479 18,864

Provision for hedge ineffectiveness(912) 12(25)

Joint venture investment impairment 1,834 —

Reversal of excise tax accrual -(4,594) -

Gain on extinguishment of other liabilities(3,511)(4,258) -

Executive and realignment separation charges — 4,730

Other1(1,349)(199)(224)

Operating FFO attributable to common shareholders $ 246,799 $ 257,160 $ 251,266

Operating FFO attributable to common shareholders per common share outstanding $ 1.05 $ 1.09 $ 1.06

1 |

| Consists of the impact on earnings from net settlements and easement proceeds |

96 |

|

|

Reconciliation of Net Income Attributable to Common

Shareholders to Non-Target Market Multi-Tenant Retail

Same Store NOI

Year Ended December 31,

2015 2014

Net income attributable to common shareholders $ 115,646 $ 33,850

Adjustments to reconcile to Same Store NOI:

Preferred stock dividends 9,450 9,450

Net income attributable to noncontrolling interest 528 -

Gain on sales of investment properties(121,792)(42,196)

Income from discontinued operations -(507)

Depreciation and amortization 214,706 215,966

Provision for impairment of investment properties 19,937 72,203

General and administrative expenses 50,657 34,229

Gain on extinguishment of other liabilities -(4,258)

Equity in loss of unconsolidated joint ventures, net—2,088

Gain on change in control of investment properties -(24,158)

Interest expense 138,938 133,835

Straight-line rental income, net(3,498)(4,781)

Amortization of acquired above and below market lease intangibles, net(3,621)(2,076)

Amortization of lease inducements 847 707

Lease termination fees(3,757)(2,667)

Straight-line ground rent expense 3,722 3,889

Amortization of acquired ground lease intangibles(560)(560)

Other income, net(1,700)(5,459)

NOI 419,503 419,555

NOI from Other Investment Properties(73,003)(82,921)

Same Store NOI 346,500 336,634

Target market multi-tenant retail Same Store NOI(172,691)(168,485)

Other Same Store NOI(33,912)(33,333)

Non-target market multi-tenant retail Same Store NOI $ 139,897 $ 134,816

97 |

|

|

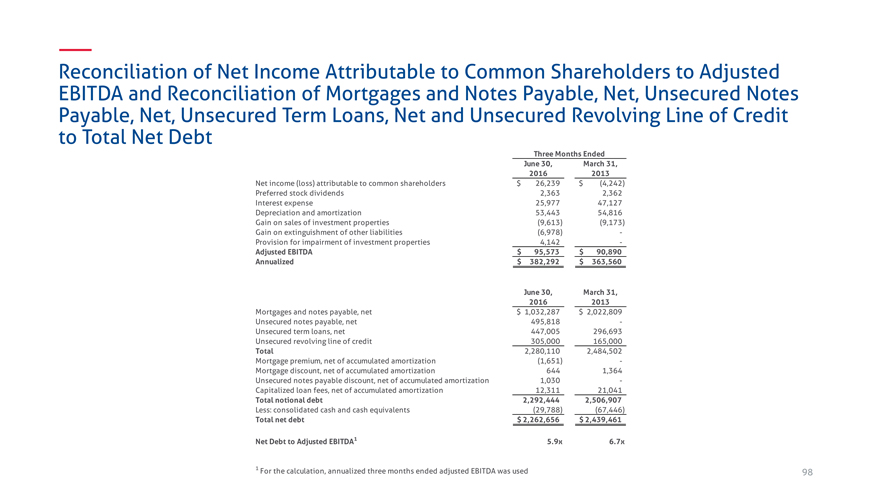

Reconciliation of Net Income Attributable to Common Shareholders to Adjusted

EBITDA and Reconciliation of Mortgages and Notes Payable, Net, Unsecured Notes

Payable, Net, Unsecured Term Loans, Net and Unsecured Revolving Line of Credit

to Total Net Debt

Three Months Ended

June 30, March 31,

2016 2013

Net income (loss) attributable to common shareholders $ 26,239 $(4,242)

Preferred stock dividends 2,363 2,362

Interest expense 25,977 47,127

Depreciation and amortization 53,443 54,816

Gain on sales of investment properties(9,613)(9,173)

Gain on extinguishment of other liabilities(6,978) -

Provision for impairment of investment properties 4,142 -

Adjusted EBITDA $ 95,573 $ 90,890

Annualized $ 382,292 $ 363,560

June 30, March 31,

2016 2013

Mortgages and notes payable, net $ 1,032,287 $ 2,022,809

Unsecured notes payable, net 495,818 -

Unsecured term loans, net 447,005 296,693

Unsecured revolving line of credit 305,000 165,000

Total 2,280,110 2,484,502

Mortgage premium, net of accumulated amortization(1,651) -

Mortgage discount, net of accumulated amortization 644 1,364

Unsecured notes payable discount, net of accumulated amortization 1,030 -

Capitalized loan fees, net of accumulated amortization 12,311 21,041

Total notional debt 2,292,444 2,506,907

Less: consolidated cash and cash equivalents(29,788)(67,446)

Total net debt $ 2,262,656 $ 2,439,461

Net Debt to Adjusted EBITDA1 5.9x 6.7x

1 |

| For the calculation, annualized three months ended adjusted EBITDA was used 98 |

|

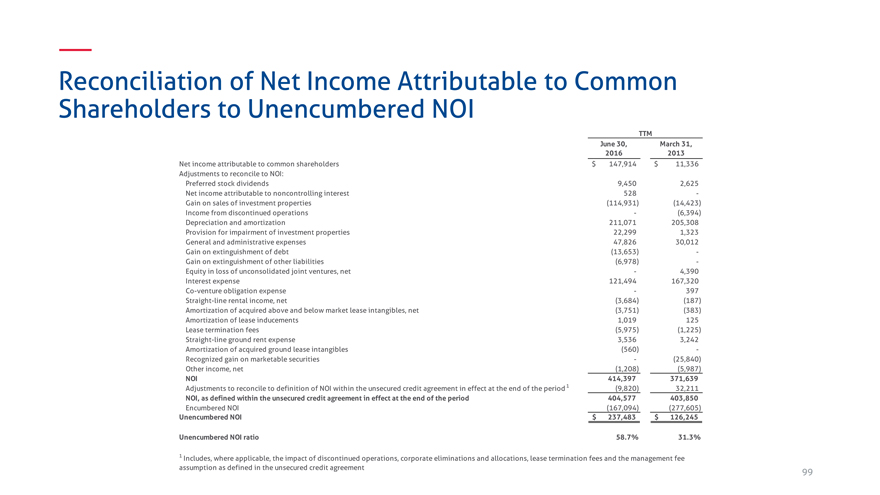

Reconciliation of Net Income Attributable to Common

Shareholders to Unencumbered NOI

TTM

June 30, March 31,

2016 2013

Net income attributable to common shareholders $ 147,914 $ 11,336

Adjustments to reconcile to NOI:

Preferred stock dividends 9,450 2,625

Net income attributable to noncontrolling interest 528 -

Gain on sales of investment properties(114,931)(14,423)

Income from discontinued operations -(6,394)

Depreciation and amortization 211,071 205,308

Provision for impairment of investment properties 22,299 1,323

General and administrative expenses 47,826 30,012

Gain on extinguishment of debt(13,653) -

Gain on extinguishment of other liabilities(6,978) -

Equity in loss of unconsolidated joint ventures, net—4,390

Interest expense 121,494 167,320

Co-venture obligation expense—397

Straight-line rental income, net(3,684)(187)

Amortization of acquired above and below market lease intangibles, net(3,751)(383)

Amortization of lease inducements 1,019 125

Lease termination fees(5,975)(1,225)

Straight-line ground rent expense 3,536 3,242

Amortization of acquired ground lease intangibles(560) -

Recognized gain on marketable securities -(25,840)

Other income, net(1,208)(5,987)

NOI 414,397 371,639

Adjustments to reconcile to definition of NOI within the unsecured credit agreement in effect at the end of the period 1(9,820) 32,211

NOI, as defined within the unsecured credit agreement in effect at the end of the period 404,577 403,850

Encumbered NOI(167,094)(277,605)

Unencumbered NOI $ 237,483 $ 126,245

Unencumbered NOI ratio 58.7% 31.3%

1 Includes, where applicable, the impact of discontinued operations, corporate eliminations and allocations, lease termination fees and the management fee

assumption as defined in the unsecured credit agreement 99

|

Reconciliation of Mortgages and Notes Payable, Net to Notional

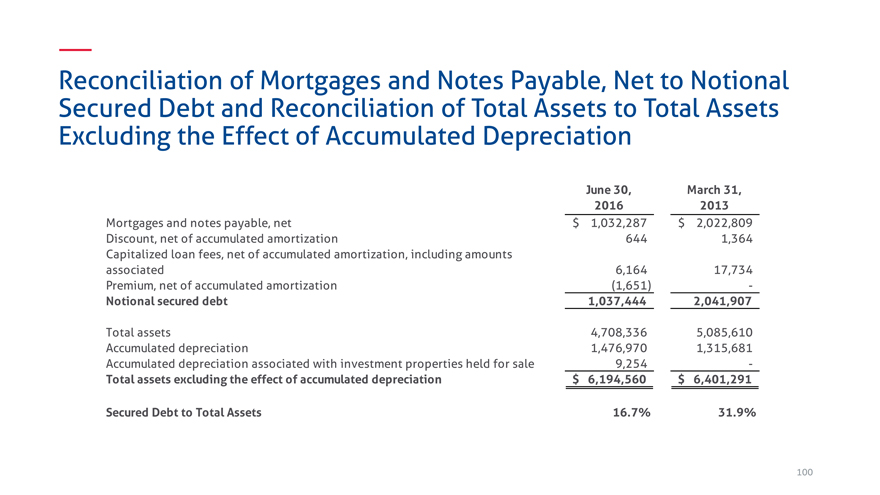

Secured Debt and Reconciliation of Total Assets to Total Assets

Excluding the Effect of Accumulated Depreciation

June 30, March 31,

2016 2013

Mortgages and notes payable, net $ 1,032,287 $ 2,022,809

Discount, net of accumulated amortization 644 1,364

Capitalized loan fees, net of accumulated amortization, including amounts

associated 6,164 17,734

Premium, net of accumulated amortization(1,651) -

Notional secured debt 1,037,444 2,041,907

Total assets 4,708,336 5,085,610

Accumulated depreciation 1,476,970 1,315,681

Accumulated depreciation associated with investment properties held for sale 9,254 -

Total assets excluding the effect of accumulated depreciation $ 6,194,560 $ 6,401,291

Secured Debt to Total Assets 16.7% 31.9%

100