Pioneer Municipal High Income Trust

Semiannual Report | October 31, 2020

Ticker Symbol: MHI

Beginning in or after April 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Trust’s shareholder reports like this one will no longer be sent by mail, unless you specifically request paper copies of the reports from the Trust or from your financial intermediary, such as a broker-dealer, bank or insurance company. Instead, the reports will be made available on the Trust’s website, and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications electronically by contacting your financial intermediary or, if you invest directly with the Trust, by calling 1-800-710-0935.

You may elect to receive all future reports in paper free of charge. If you invest directly with the Trust, you can inform the Trust that you wish to continue receiving paper copies of your shareholder reports by calling 1-800-710-0935. If you invest through a financial intermediary, you can contact your financial intermediary to request that you continue to receive paper copies of your shareholder reports. Your election to receive reports in paper will apply to all funds held in your account if you invest through your financial intermediary or all funds held within the Pioneer Fund complex if you invest directly.

visit us: www.amundipioneer.com/us

Pioneer Municipal High Income Trust | Semiannual Report | 10/31/20 1

President’s LetterDear Shareholders,

The new decade has arrived delivering a calendar year that will go down in the history books. The beginning of 2020 seemed to extend the positive market environment of 2019. Then, March roared in like a lion and the COVID-19 pandemic became a global crisis impacting lives and life as we know it. As the fourth quarter of 2020 got underway, it appeared that the long-anticipated “second wave” of COVID-19 cases was occurring, both in some U.S. states and in Europe. In response, some governments began retightening restrictions on both business and personal activities.

However, as the fourth quarter continued, we began to read some encouraging news on the vaccine front, as multiple pharmaceutical companies announced successful clinical trials for their COVID-19 vaccinations and applied for emergency-use approval for the drugs with the Food and Drug Administration. Government officials followed up on the positive news by announcing that deployment of at least one of the vaccines to frontline workers could begin even before the end of this calendar year, with the potential for widespread distribution by mid-2021.

While there may finally be a light visible at the end of the pandemic tunnel as 2020 comes to a close, the long-term impact on the global economy from COVID-19, while currently unknown, is likely to be considerable. It is clear that several industries have already felt greater effects than others, and the markets, which do not thrive on uncertainty, have been volatile, delivering significantly negative performance in the first quarter, and then recovering most of those losses throughout the following quarters. Despite the rebound, volatility has remained elevated, with momentum rising and falling on seemingly every bit of positive or negative news about the virus, from vaccines to spikes in the number of cases as well as rising hospitalization rates in some areas. In addition, the U.S. Presidential Election was in high gear as we entered the fourth quarter. This election contributed to the market volatility as investors pondered the possible outcomes and their potential effects on the economic outlook.

With the advent of COVID-19 last winter, we implemented our business continuity plan according to the new COVID-19 guidelines, and most of our employees have been working remotely since March. To date, our operating environment has faced no interruption. I am proud of the careful planning that has taken place and confident we can maintain this environment for as long as is prudent. History in the making for a company that first opened its doors way back in 1928.

2 Pioneer Municipal High Income Trust | Semiannual Report | 10/31/20

Since 1928, Amundi’s investment process has been built on a foundation of fundamental research and active management, principles which have guided our investment decisions for more than 90 years. We believe active management – that is, making active investment decisions – can help mitigate the risks during periods of market volatility. As 2020 has reminded us, investment risk can arise from a number of factors in today’s global economy, including slower or stagnating growth, changing U.S. Federal Reserve policy, oil price shocks, political and geopolitical factors and, unfortunately, major public health concerns such as a viral pandemic.

At Amundi, active management begins with our own fundamental, bottom-up research process. Our team of dedicated research analysts and portfolio managers analyzes each security under consideration, communicating directly with the management teams of the companies issuing the securities and working together to identify those securities that best meet our investment criteria for our family of funds. Our risk management approach begins with each and every security, as we strive to carefully understand the potential opportunity, while considering any and all risk factors.

Today, as investors, we have many options. It is our view that active management can serve shareholders well, not only when markets are thriving, but also during periods of market stress.

As you consider your long-term investment goals, we encourage you to work with your financial professional to develop an investment plan that paves the way for you to pursue both your short-term and long-term goals.

We remain confident that the current crisis, like others in human history, will pass, and we greatly appreciate the trust you have placed in us and look forward to continuing to serve you in the future.

Sincerely,

Lisa M. Jones

Head of the Americas, President and CEO of U.S.

Amundi Pioneer Asset Management USA, Inc.

December 18, 2020

Any information in this shareowner report regarding market or economic trends or the factors influencing the Trust’s historical or future performance are statements of opinion as of the date of this report. Past performance is no guarantee of future results.

Pioneer Municipal High Income Trust | Semiannual Report | 10/31/20 3

Portfolio Management Discussion |

10/31/20 During the six-month period ended October 31, 2020, the municipal bond market staged a steady and strong recovery from the disruptions and volatility that had beset global financial markets earlier this year with the onset of the COVID-19 pandemic and the resulting economic downturn. In the following interview, David Eurkus and Jonathan Chirunga discuss the factors that influenced the performance of Pioneer Municipal High Income Trust during the six-month period. Mr. Eurkus, Director of Municipals, U.S., a senior vice president, and a portfolio manager at Amundi Pioneer Asset Management, Inc. (Amundi)*, and Mr. Chirunga, a Managing Director, Deputy Director of Municipals, and a portfolio manager at Amundi, are responsible for the day-to-day management of the Trust.

Q How did Pioneer Municipal High Income Trust perform during the six-month period ended October 31, 2020?

A Pioneer Municipal High Income Trust returned 7.16% at net asset value (NAV) and 7.26% at market price during the six-month period ended October 31, 2020. During the same six-month period, the Trust’s benchmarks, the Bloomberg Barclays U.S. Municipal High Yield Bond Index and the Bloomberg Barclays Municipal Bond Index, returned 11.74% and 4.99% at NAV, respectively. The Bloomberg Barclays U.S. Municipal High Yield Bond Index is an unmanaged measure of the performance of lower-rated municipal bonds, while the Bloomberg Barclays Municipal Bond Index is an unmanaged measure of the performance of investment-grade municipal bonds. Unlike the Trust, the two indices do not use leverage. While use of leverage increases investment opportunity, it also increases investment risk.

During the same six-month period, the average return at NAV of the 19 closed-end funds in Morningstar’s High Yield Municipal Debt Closed End Funds category (which may or may not be leveraged) was 9.90%, while the average return at market price in the same closed-end funds Morningstar category was 10.22%.

The shares of the Trust were selling at a 12.0% discount to NAV on October 31, 2020. Comparatively, the shares of the Trust were selling at a 12.1% discount to NAV on April 30, 2020.

* See Notes to Financial Statements Note 6.

4 Pioneer Municipal High Income Trust | Semiannual Report | 10/31/20

On October 31, 2020, the standardized 30-day SEC yield of the Trust’s shares was 2.07%**.

Q How would you describe the investment environment in the municipal bond market during the six-month period ended October 31, 2020?

A Early this year, the environment for municipal bonds was largely favorable. Declines in U.S. Treasury medium- and longer-term interest rates, the U.S. Federal Reserve System’s (Fed’s) accommodative stance on monetary policy, healthy demand for tax-free bonds with limited supply, as well as the longer-term effects on the municipal market from the federal tax overhaul legislation passed in late 2017, all combined to support performance in the municipal bond market. The federal tax overhaul passed in 2017 has boosted the performance of tax-free bonds given the fact that, under the law, income earned by investors on advance-refunding bonds, formerly treated as tax-exempt, is now treated as taxable income. (An advance-refunding bond is issued to retire, or pre-refund, another outstanding bond more than 90 days in advance of the original bond’s maturity date.) This change in the law has served to remove approximately one quarter of the prior municipal supply from the tax-exempt marketplace, which in turn has helped to boost tax-free bond prices. In addition, the concurrently enacted federal limits on state and local tax deductions have significantly increased demand for municipal investments in high tax states.

In March 2020, however, the investment environment for tax-exempt bonds as well as in the financial markets in general turned swiftly and dramatically negative. News of a number of emerging “hot spots” for the spread of the COVID-19 virus, which had emerged in China, then spread through Asia and Europe before eventually landing in the United States, roiled the markets as Americans began focusing on the serious public health implications of what quickly became a global pandemic. In fact, the COVID-19 outbreak had already begun to have a negative impact on U.S. economic activity as early as the middle of February. While public health officials provided guidance on how to deal with the outbreak, many governors and mayors in U.S. states and cities shut down businesses deemed non-essential and directed “shelter-in-place” and other quarantine-like efforts for individuals. Those measures, along with swift public recognition of the need for staying at home, working from

** The 30-day SEC yield is a standardized formula that is based on the hypothetical annualized earning power (investment income only) of the Trust’s portfolio securities during the period indicated.

Pioneer Municipal High Income Trust | Semiannual Report | 10/31/20 5

home, and social distancing, dramatically curtailed activities in the U.S. transportation, retail sales, manufacturing, and services industries. Financial markets, including the municipal bond market, experienced intense volatility at times as investors looked for so-called “safe havens,” such as U.S. Treasuries, and tried to ascertain some levels of certainty regarding the near-term and medium-term paths for the U.S. economy during a very uncertain time.

In an attempt to mitigate the very serious economic effects from COVID-19 on individuals, states, municipalities, and the United States overall, the Fed as well as Congress and the White House undertook a large number of monetary and fiscal measures. In short order, the Fed reduced the federal funds rate’s target range to near zero, reintroduced lending facilities from the 2008-2009 financial crisis-era, instituted new lending facilities, and rebooted quantitative easing (that is, injecting massive liquidity into the economy by purchasing Treasury, agency, mortgage, and taxable corporate bonds in significant quantities). Federal lawmakers also approved two large aid packages in the form of loans and grants to individuals, small businesses, medical systems, and higher-education institutions in light of the sudden freeze-up in economic activity and continuously rising unemployment figures. Taken together, those measures helped to calm financial markets, including the municipal bond market, to some degree. However, investments considered higher risk, including high-yield municipal bonds, continued to weather persistent market volatility.

At the end of March, following significant forced selling and fund outflows industry-wide, tax-equivalent yields for investment-grade municipal bonds rose to as much as 200 basis points (bps) higher than Treasury securities of similar maturity, triggering significant tax-exempt bond purchases from domestic and global investors, and providing substantial relief to the municipal bond market. (A basis point is equal to 1/100th of a percentage point.)

Through the Trust’s most recent six-month period, the tax-exempt bond market generally continued its recovery, as domestic and global investors were aggressive purchasers of these bonds, and recent yield increases reversed themselves as municipal bond prices rose. At the same time, the stunning contraction in economic activity across the country due to COVID-19 – especially within the tourism, transportation, retail, and service industries – as well as dramatic reductions in federal, state, and

6 Pioneer Municipal High Income Trust | Semiannual Report | 10/31/20

local tax revenues, continued to overshadow the municipal bond market. Toward the end of the six-month period, amid robust demand from buyers, the municipal market experienced a rush of tax-exempt and taxable issuance in advance of the presidential election.

During the past six months, the tax-exempt high-yield bond market received solid support from demand from traditional investors, but also demand from non-traditional buyers looking for relative safety, a lower default rate, and attractive bond valuations as compared with taxable bonds.

Q What factors affected the Trust’s performance relative to the Bloomberg Barclays municipal bond indices during the six-month period ended October 31, 2020?

A We maintained a well-diversified*** portfolio during the six-month period, with exposures to both investment-grade and high-yield municipal bonds.

The portfolio’s holdings of tobacco settlement bonds issued by California, Massachusetts Development Authority bonds, and North Carolina Turnpike Authority bonds were among the top positive contributors to the Trust’s relative performance during the six-month period, while positions in Carmel (Indiana) Continuing Care Facility bonds, Rhode Island Detention Center bonds, and State of Illinois Continuing Care Facility bonds were some of the largest detractors from benchmark-relative returns.

Q Did the Trust’s distributions**** to shareholders change during the six-month period ended October 31, 2020?

A No, during the six-month period, the Trust’s distributions remained stable at $0.045 per share/per month.

Q Did the level of leverage in the Trust change during the six-month period ended October 31, 2020?

A The level of leverage in the Trust remained consistent during the six-month period. As of October 31, 2020, 29.9% of the Trust’s total managed assets were financed by leverage obtained through the issuance of Variable Rate Muni Fund Term Preferred Shares, compared with 30.3% of the Trust’s total managed assets financed by leverage at the start of the period on May 1, 2020. The change in the percentage of the Trust's total managed assets financed by leverage during the six-month period was the result of an increase in the value of the Trust's total managed assets.

*** Diversification does not assure a profit nor protect against loss.

**** Distributions are not guaranteed.

Pioneer Municipal High Income Trust | Semiannual Report | 10/31/20 7

Q Did the Trust have any exposure to derivative securities during the six-month period ended October 31, 2020?

A No, the Trust’s portfolio had no exposure to derivative securities during the six-month period.

Q What is your investment outlook?

A Because of the lack of any resurgence in U.S. inflation, as well as the clear pronouncements from the Fed that it plans to keep short-term interest rates at or near zero for the next few years, at least, we are optimistic regarding the path of interest rates going forward. Additionally, in light of the continued low default rate for the municipal bond asset class, and a favorable supply/demand environment, given the ongoing shrinking of supply and persistently strong demand from various categories of investors, we believe that current prospects for the tax-exempt bond market are favorable. Lastly, given the enormous and continued need for economic assistance of all sorts in order to help businesses and individuals cope with the effects of the COVID-19 situation, the U.S. government may eventually need to face the reality of its rising debt levels, in part by raising taxes, which, in our view, would likely further increase demand for municipal bonds.

With regard to the Trust’s positioning, we have continued to identify opportunities created by large investors having to sell strong credit bonds out of their portfolios, particularly sales related to weak-credit purchases of bonds issued in the summer of 2017. We also have been exploring opportunities in areas of the tax-exempt market that have felt significant effects from the recent COVID-19-related economic slowdown, including municipal issues in the transportation and senior living center segments.

Consistent with our investment discipline in managing the Trust, we intend to continue to focus on intensive, fundamental research into individual bond issues, while maintaining a close watch on any economic factors that could influence the high-yield and investment-grade municipal markets. Based on those factors, we do not anticipate making any significant changes to the portfolio’s positioning and structure in the near future.

8 Pioneer Municipal High Income Trust | Semiannual Report | 10/31/20

Please refer to the Schedule of Investments on pages 15–25 for a full listing of Trust securities.

All investments are subject to risk, including the possible loss of principal. In the past several years, financial markets have experienced increased volatility and heightened uncertainty. The market prices of securities may go up or down, sometimes rapidly or unpredictably, due to general market conditions, such as real or perceived adverse economic, political, or regulatory conditions, recessions, inflation, changes in interest or currency rates, lack of liquidity in the bond markets, the spread of infectious illness or other public health issues or adverse investor sentiment. These conditions may continue, recur, worsen or spread.

Investments in high-yield or lower-rated securities are subject to greater-than-average risk.

The Trust may invest in securities of issuers that are in default or that are in bankruptcy.

A portion of income may be subject to state, federal, and/or alternative minimum tax. Capital gains, if any, are subject to a capital gains tax.

When interest rates rise, the prices of debt securities held by the Trust will generally fall. Conversely, when interest rates fall the prices of debt securities held by the Trust generally will rise.

A general rise in interest rates could adversely affect the price and liquidity of fixed income securities.

By concentrating in municipal securities, the Trust is more susceptible to adverse economic, political or regulatory developments than is a portfolio that invests more broadly.

Investments in the Trust are subject to possible loss due to the financial failure of the issuers of the underlying securities and the issuers’ inability to meet their debt obligations.

The Trust may invest up to 20% of its total assets in illiquid securities. Illiquid securities may be difficult to dispose of at a price reflective of their value at the times when the Trust believes it is desirable to do so, and the market price of illiquid securities is generally more volatile than that of more liquid securities. Illiquid securities are also more difficult to value and investment of the Trust’s assets in illiquid securities may restrict the Trust’s ability to take advantage of market opportunities.

The Trust uses leverage through the issuance of preferred shares. Leverage creates significant risks, including the risk that the Trust’s incremental income or capital appreciation for investments purchased with the proceeds of leverage will not be sufficient to cover the cost of the leverage, which may adversely affect the return for the holders of common shares.

Pioneer Municipal High Income Trust | Semiannual Report | 10/31/20 9

The Trust is required to maintain certain regulatory, rating agency and other asset coverage requirements in connection with its outstanding preferred shares. In order to maintain required asset coverage levels, the Trust may be required to alter the composition of its investment portfolio or take other actions, such as redeeming preferred shares with the proceeds from portfolio transactions, at what might be inopportune times in the market. Such actions could reduce the net earnings or returns to holders of the Trust’s common shares over time, which is likely to result in a decrease in the market value of the Trust’s shares.

These risks may increase share price volatility.

Any information in this shareholder report regarding market or economic trends or the factors influencing the Trust’s historical or future performance are statements of opinion as of the date of this report. Past performance is no guarantee of future results.

10 Pioneer Municipal High Income Trust | Semiannual Report | 10/31/20

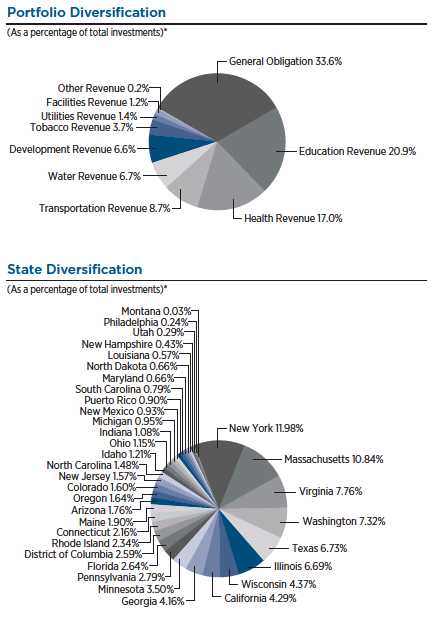

Portfolio Summary |

10/31/20 Pioneer Municipal High Income Trust | Semiannual Report | 10/31/20 11

Portfolio Summary | 10/31/20 (continued)

10 Largest Holdings

(As a percentage of total investments)*

| | | |

| 1. | Metropolitan Pier & Exposition Authority, McCormick Place, 5.65%, | |

| 6/15/22 (NATL-RE Insured) | 3.92% |

| 2. | State of Washington, Motor Vehicle Sales Tax, Series C, 6/1/22 (NATL Insured) | 3.42 |

| 3. | Massachusetts Development Finance Agency, WGBH Foundation, | |

| Series A, 5.75%, 1/1/42 (AMBAC Insured) | 2.66 |

| 4. | New York State Dormitory Authority, Series A, 4.0%, 7/1/41 | 2.17 |

| 5. | New York State Dormitory Authority, Series C, 5.0%, 3/15/39 | 2.03 |

| 6. | Brookhaven Development Authority, 4.0%, 7/1/49 | 1.91 |

| 7. | New York State Dormitory Authority, 5.0%, 10/1/50 | 1.89 |

| 8. | Massachusetts Development Finance Agency, Harvard University, | |

| Series A, 5.0%, 7/15/40 | 1.79 |

| 9. | State of Minnesota, Series B, 4.0%, 8/1/27 | 1.74 |

| 10. | Massachusetts Bay Transportation Authority, Series A, 7/1/28 | 1.50 |

* Excludes temporary cash investments and all derivative contracts except for options purchased. The Trust is actively managed, and current holdings may be different. The holdings listed should not be considered recommendations to buy or sell any securities.

12 Pioneer Municipal High Income Trust | Semiannual Report | 10/31/20

Prices and Distributions |

10/31/20 Market Value per Common Share^

| | | |

| 10/31/20 | 4/30/20 |

Market Value | $11.34 | $10.82 |

Discount | (12.02)% | (12.10)% |

Net Asset Value per Common Share^

| | | |

| 10/31/20 | 4/30/20 |

Net Asset Value | $12.89 | $12.31 |

Distributions per Common Share:

| | | | |

| Net | | |

| Investment | Short-Term | Long-Term |

| Income | Capital Gains | Capital Gains |

5/1/20 – 10/31/20 | $0.2700 | $ — | $ — |

Yields

| | | |

| 10/31/20 | 4/30/20 |

30-Day SEC Yield | 2.07% | 2.67% |

The data shown above represents past performance, which is no guarantee of future results.

^ Net asset value and market value are published in Barron’s on Saturday, The Wall Street Journal on Monday and The New York Times on Monday and Saturday. Net asset value and market value are published daily on the Trust's website at www.amundipioneer.com/us.

Pioneer Municipal High Income Trust | Semiannual Report | 10/31/20 13

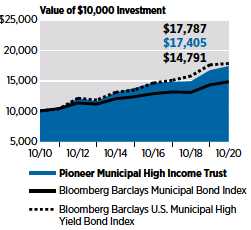

Performance Update |

10/31/20 Investment Returns

The mountain chart on the right shows the change in market value, including reinvestment of dividends and distributions, of a $10,000 investment made in common shares of Pioneer Municipal High Income Trust during the periods shown, compared to that of the Bloomberg Barclays Municipal Bond Index and Bloomberg Barclays U.S. Municipal High Yield Bond Index.

| | | | | |

| Average Annual Total Returns | |

(As of October 31, 2020) | | |

| | | | BBG |

| | | BBG | Barclays |

| Net | | Barclays | U.S. |

| Asset | | Municipal | Municipal

|

| Value | Market | Bond

| High Yield |

| Period | (NAV) | Price

| Index | Bond Index |

10 years | 5.70%

| 3.76% | 3.99% | 5.93% |

5 years | 4.76 | 2.34 | 3.70 | 5.78 |

1 year | 4.15 | -2.10 | 3.59 | 1.23 |

Call 1-800-225-6292 or visit www.amundipioneer.com/us for the most recent month-end performance results. Current performance may be lower or higher than the performance data quoted.

Performance data shown represents past performance. Past performance is no guarantee of future results. Investment return and market price will fluctuate, and your shares may trade below NAV due to such factors as interest rate changes and the perceived credit quality of borrowers.

Total investment return does not reflect broker sales charges or commissions. All performance is for common shares of the Trust.

Shares of closed-end funds, unlike open-end funds, are not continuously offered. There is a one-time public offering and, once issued, shares of closed-end funds are bought and sold in the open market through a stock exchange and frequently trade at prices lower than their NAV. NAV per common share is total assets less total liabilities, which include preferred shares or borrowings, as applicable, divided by the number of common shares outstanding.

When NAV is lower than market price, dividends are assumed to be reinvested at the greater of NAV or 95% of the market price. When NAV is higher, dividends are assumed to be reinvested at prices obtained through open-market purchases under the Trust’s dividend reinvestment plan.

The performance table and graph do not reflect the deduction of fees and taxes that a shareowner would pay on Trust distributions or the sale of Trust shares. Had these fees and taxes been reflected, performance would have been lower.

The Bloomberg Barclays Municipal Bond Index is an unmanaged, broad measure of the municipal bond market. The Bloomberg Barclays High Yield Municipal Bond Index is unmanaged, totals over $26 billion in market value and maintains over 1,300 securities. Municipal bonds in this index have the following requirements: maturities of one year or greater, sub investment grade (below Baa or non-rated), fixed coupon rate, issued after 12/31/90, deal size over $20 million, and maturity size of at least $3 million. Index returns are calculated monthly, assume reinvestment of dividends and, unlike Trust returns, do not reflect any fees, expenses or sales charges. The indices do not use leverage. It is not possible to invest directly in the indices.

Please refer to the financial highlights for a more current total return ratio.

14 Pioneer Municipal High Income Trust | Semiannual Report | 10/31/20

Schedule of Investments |

10/31/20 (unaudited)

| | | | |

| Principal | | | |

| Amount | | | |

| USD ($) | | | Value |

| | | UNAFFILIATED ISSUERS — 141.2% | |

| | | COLLATERALIZED MORTGAGE OBLIGATION — | |

| | | 0.3% of Net Assets | |

| 996,387 | | Texas Department of Housing & Community Affairs, | |

| | | 2.3%, 7/1/37 (FNMA HUD SECT 8 Insured) | $ 991,364 |

| | | TOTAL COLLATERALIZED MORTGAGE OBLIGATION | |

| | | (Cost $996,386) | $ 991,364 |

| | | MUNICIPAL BONDS — 140.9% of Net Assets(a) | |

| | | Arizona — 2.5% | |

| 4,000,000(b) | | City of Phoenix, 5.0%, 7/1/27 | $ 4,948,240 |

| 2,230,000 | | City of Phoenix, Industrial Development Authority, | |

| | 3rd & Indian School Assisted Living Project, | |

| | | 5.4%, 10/1/36 | 2,304,884 |

| 24,000 | | County of Pima, Industrial Development Authority, | |

| | Arizona Charter Schools Project, Series C, | |

| | | 6.75%, 7/1/31 | 24,080 |

| | | Total Arizona | $ 7,277,204 |

| | | California — 6.1% | |

| 1,000,000 | | California County Tobacco Securitization Agency, | |

| | | 5.0%, 6/1/49 | $ 1,177,220 |

| 10,000,000(c) | | California County Tobacco Securitization Agency, | |

| | | Capital Appreciation, Stanislaus County, Subordinated, | |

| | | Series A, 6/1/46 | 2,290,000 |

| 2,000,000 | | California Educational Facilities Authority, Stanford | |

| | | University, Series U-7, 5.0%, 6/1/46 | 3,090,900 |

| 1,450,000 | | California Enterprise Development Authority, | |

| | | Sunpower Corp., 8.5%, 4/1/31 | 1,468,386 |

| 530,000 | | California Municipal Finance Authority, Santa Rosa | |

| | | Academy Project, Series A, 5.75%, 7/1/30 | 550,097 |

| 1,590,000(d) | | California School Finance Authority, Classical | |

| | | Academies Project, Series A, 7.375%, 10/1/43 | 1,807,528 |

| 1,400,000 | | California Statewide Communities Development | |

| | | Authority, Lancer Plaza Project, 5.625%, 11/1/33 | 1,411,592 |

| 2,000,000(b) | | Los Angeles Community College District, Series G, | |

| | | 4.0%, 8/1/39 | 2,236,780 |

| 1,605,000 | | Los Angeles County Metropolitan Transportation | |

| | | Authority, Series A, 5.0%, 7/1/30 | 2,053,389 |

| 1,500,000(b) | | State of California, 3.0%, 10/1/33 | 1,686,210 |

| | | Total California | $ 17,772,102 |

The accompanying notes are an integral part of these financial statements.

Pioneer Municipal High Income Trust | Semiannual Report | 10/31/20 15

Schedule of Investments | 10/31/20

(unaudited) (continued)

| | | | |

| Principal | | | |

| Amount | | | |

| USD ($) | | | Value |

| | | Colorado — 2.3% | |

| 2,180,000 | | Board of Water Commissioners City & County of | |

| | | Denver, 4.0%, 9/15/42 | $ 2,471,270 |

| 1,500,000(d) | | Colorado Educational & Cultural Facilities Authority, | |

| | Rocky Mountain Classical Academy Project, | |

| | | 8.0%, 9/1/43 | 1,826,685 |

| 1,665,000(e) | | Tender Option Bond Trust Receipts/Certificates, | |

| | | RIB, 0.0%, 6/1/39 (144A) | 2,331,399 |

| | | Total Colorado | $ 6,629,354 |

| | | Connecticut — 3.1% | |

| 3,470,000 | | Mohegan Tribal Finance Authority, 7.0%, 2/1/45 (144A) | $ 3,498,801 |

| 5,000,000(b) | | State of Connecticut, Series E, 4.0%, 9/1/30 | 5,458,350 |

| | | Total Connecticut | $ 8,957,151 |

| | | District of Columbia — 3.7% | |

| 2,380,000 | | District of Columbia Tobacco Settlement Financing | |

| | | Corp., Asset-Backed, 6.5%, 5/15/33 | $ 2,551,027 |

| 6,000,000 | | District of Columbia Tobacco Settlement Financing | |

| | | Corp., Asset-Backed, 6.75%, 5/15/40 | 6,120,000 |

| 10,000,000(c) | | District of Columbia Tobacco Settlement Financing | |

| | Corp., Capital Appreciation, Asset-Backed, | |

| | | Series A, 6/15/46 | 2,047,000 |

| | | Total District of Columbia | $ 10,718,027 |

| | | Florida — 3.7% | |

| 5,000,000 | | County of Miami-Dade, Water & Sewer System | |

| | | Revenue, Series A, 4.0%, 10/1/44 | $ 5,574,700 |

| 5,000,000 | | Florida’s Turnpike Enterprise, Department of | |

| | | Transportation, Series A, 4.0%, 7/1/34 | 5,366,450 |

| | | Total Florida | $ 10,941,150 |

| | | Georgia — 5.9% | |

| 7,010,000 | | Brookhaven Development Authority, 4.0%, 7/1/49 | $ 7,907,981 |

| 2,333,423 | | Clayton County Development Authority, Delta Air | |

| | | Lines, Series A, 8.75%, 6/1/29 | 2,350,597 |

| 2,500,000 | | County of Fulton GA Water & Sewerage Revenue, | |

| | | 2.25%, 1/1/42 | 2,502,025 |

| 4,000,000 | | Private Colleges & Universities Authority, Emory | |

| | | University, Series A, 5.0%, 10/1/43 | 4,462,800 |

| | | Total Georgia | $ 17,223,403 |

| | | Idaho — 1.7% | |

| 5,000,000 | | Power County Industrial Development Corp., FMC Corp. | |

| | | Project, 6.45%, 8/1/32 | $ 5,030,300 |

| | | Total Idaho | $ 5,030,300 |

The accompanying notes are an integral part of these financial statements.

16 Pioneer Municipal High Income Trust | Semiannual Report | 10/31/20

| | | | |

| Principal | | | |

| Amount | | | |

| USD ($) | | | Value |

| | | Illinois — 9.5% | |

| 2,087,000(e)(g) | | Illinois Finance Authority, Clare Oaks Project, Series B, | |

| | | 4.0%, 11/15/52 | $ 1,460,900 |

| 1,305,000(c) | | Illinois Finance Authority, Clare Oaks Project, | |

| | | Series C-1, 11/15/52 | 6,525 |

| 261,000 | | Illinois Finance Authority, Clare Oaks Project, | |

| | | Series C-2, 4.0%, 11/15/52 | 1,305 |

| 261,000(g) | | Illinois Finance Authority, Clare Oaks Project, | |

| | | Series C-3, 0.0%, 11/15/52 | 1,305 |

| 3,500,000 | | Illinois Finance Authority, The Admiral at the Lake | |

| | | Project, 5.25%, 5/15/42 | 3,125,570 |

| 4,000,000 | | Illinois Finance Authority, The Admiral at the Lake | |

| | | Project, 5.5%, 5/15/54 | 3,559,960 |

| 1,610,000(f) | | Metropolitan Pier & Exposition Authority, McCormick | |

| | | Place, 5.65%, 6/15/22 (NATL-RE Insured) | 1,745,932 |

| 13,785,000 | | Metropolitan Pier & Exposition Authority, McCormick | |

| | | Place, 5.65%, 6/15/22 (NATL-RE Insured) | 14,506,645 |

| 1,000,000 | | Metropolitan Pier & Exposition Authority, McCormick | |

| | | Place, Series B, 5.0%, 6/15/52 (ST APPROP Insured) | 1,026,350 |

| 1,485,000(f) | | Metropolitan Pier & Exposition Authority, McCormick | |

| | | Place, Series B, 5.65%, 6/15/22 (NATL-RE Insured) | 1,625,080 |

| 695,000 | | Southwestern Illinois Development Authority, Village of | |

| | | Sauget Project, 5.625%, 11/1/26 | 660,264 |

| | �� | Total Illinois | $ 27,719,836 |

| | | Indiana — 1.5% | |

| 250,000(g) | | City of Carmel, Barrington Carmel Project, Series A, | |

| | | 7.0%, 11/15/32 | $ 7,187 |

| 750,000(g) | | City of Carmel, Barrington Carmel Project, Series A, | |

| | | 7.125%, 11/15/42 | 21,563 |

| 500,000(g) | | City of Carmel, Barrington Carmel Project, Series A, | |

| | | 7.125%, 11/15/47 | 14,375 |

| 2,000,000 | | City of Evansville, Silver Birch Evansville Project, | |

| | | 5.45%, 1/1/38 | 1,889,920 |

| 1,500,000 | | City of Mishawaka, Silver Birch Mishawaka Project, | |

| | | 5.375%, 1/1/38 (144A) | 1,501,200 |

| 1,000,000 | | Indiana Finance Authority, Multipurpose Educational | |

| | | Facilities, Avondale Meadows Academy Project, | |

| | | 5.375%, 7/1/47 | 1,034,110 |

| | | Total Indiana | $ 4,468,355 |

| | | Louisiana — 0.8% | |

| 2,260,000(d) | | Jefferson Parish Hospital Service District No. 2, East | |

| | | Jefferson General Hospital, 6.375%, 7/1/41 | $ 2,346,807 |

| | | Total Louisiana | $ 2,346,807 |

The accompanying notes are an integral part of these financial statements.

Pioneer Municipal High Income Trust | Semiannual Report | 10/31/20 17

Schedule of Investments | 10/31/20

(unaudited) (continued)

| | | | |

| Principal | | | |

| Amount | | | |

| USD ($) | | | Value |

| | | Maine — 2.7% | |

| 1,400,000 | | City of Portland ME General Airport Revenue, | |

| | | 4.0%, 1/1/40 | $ 1,564,878 |

| 1,500,000 | | Maine Health & Higher Educational Facilities Authority, | |

| | | Maine General Medical Center, 7.5%, 7/1/32 | 1,539,765 |

| 4,480,000 | | Maine Turnpike Authority, Series A, 5.0%, 7/1/42 | 4,760,448 |

| | | Total Maine | $ 7,865,091 |

| | | Maryland — 0.9% | |

| 1,350,000 | | Maryland Health & Higher Educational Facilities | |

| | | Authority, City Neighbors, Series A, 6.75%, 7/1/44 | $ 1,433,619 |

| 1,250,000 | | Washington Suburban Sanitary Commission, 3.0%, | |

| | | 6/1/47 (CNTY GTD Insured) | 1,314,463 |

| | | Total Maryland | $ 2,748,082 |

| | | Massachusetts — 15.3% | |

| 2,000,000(b) | | City of Boston, Series A, 5.0%, 3/1/39 | $ 2,527,640 |

| 4,000,000(b) | | Commonwealth of Massachusetts, 3.0%, 3/1/49 | 4,231,360 |

| 7,000,000(c) | | Massachusetts Bay Transportation Authority, | |

| | | Series A, 7/1/28 | 6,210,680 |

| 1,550,000 | | Massachusetts Development Finance Agency, Harvard | |

| | | University, Series A, 5.0%, 7/15/36 | 2,243,920 |

| 5,000,000 | | Massachusetts Development Finance Agency, Harvard | |

| | | University, Series A, 5.0%, 7/15/40 | 7,422,950 |

| 1,000,000 | | Massachusetts Development Finance Agency, Partners | |

| | | Healthcare System, 4.0%, 7/1/41 | 1,097,310 |

| 5,000,000 | | Massachusetts Development Finance Agency, Partner’s | |

| | | Healthcare System, Series S-1, 4.0%, 7/1/41 | 5,532,050 |

| 7,100,000 | | Massachusetts Development Finance Agency, WGBH | |

| | | Foundation, Series A, 5.75%, 1/1/42 (AMBAC Insured) | 11,037,589 |

| 115,000 | | Massachusetts Educational Financing Authority, Series I, | |

| | | 6.0%, 1/1/28 | 115,555 |

| 3,100,000 | | Massachusetts Health & Educational Facilities Authority, | |

| | | Massachusetts Institute of Technology, Series K, | |

| | | 5.5%, 7/1/32 | 4,502,006 |

| | | Total Massachusetts | $ 44,921,060 |

| | | Michigan — 1.3% | |

| 1,000,000 | | David Ellis Academy, 5.25%, 6/1/45 | $ 1,000,000 |

| 2,640,000 | | Michigan State University, Series A, 5.0%, 8/15/41 | 2,916,830 |

| | | Total Michigan | $ 3,916,830 |

| | | Minnesota — 4.9% | |

| 1,840,000 | | Bloomington Port Authority, Radisson Blu Mall of | |

| | | America, 9.0%, 12/1/35 | $ 1,840,110 |

| 1,000,000 | | City of Ham Lake, DaVinci Academy, Series A, | |

| | | 5.0%, 7/1/47 | 1,006,790 |

The accompanying notes are an integral part of these financial statements.

18 Pioneer Municipal High Income Trust | Semiannual Report | 10/31/20

| | | | |

| Principal | | | |

| Amount | | | |

| USD ($) | | | Value |

| | | Minnesota — (continued) | |

| 1,000,000 | | City of Rochester, Health Care Facilities, Mayo Clinic, | |

| | | 4.0%, 11/15/48 | $ 1,111,990 |

| 2,300,000 | | City of Rochester, Mayo Clinic, Series B, 5.0%, 11/15/35 | 3,348,892 |

| 6,000,000(b) | | State of Minnesota, Series B, 4.0%, 8/1/27 | 7,195,560 |

| | | Total Minnesota | $ 14,503,342 |

| | | Montana — 0.1% | |

| 1,600,000(g) | | Two Rivers Authority, Inc., 7.375%, 11/1/27 | $ 122,560 |

| | | Total Montana | $ 122,560 |

| | | New Hampshire — 0.6% | |

| 1,000,000 | | New Hampshire Health & Education Facilities Authority | |

| | | Act, 5.0%, 8/1/59 | $ 1,420,940 |

| 375,000 | | New Hampshire Health & Education Facilities Authority | |

| | | Act, Catholic Medical Centre, 3.75%, 7/1/40 | 381,518 |

| | | Total New Hampshire | $ 1,802,458 |

| | | New Jersey — 2.2% | |

| 1,000,000 | | New Jersey Economic Development Authority, Charter | |

| | | Marion P Thomas, 5.375%, 10/1/50 (144A) | $ 1,031,460 |

| 3,000,000 | | New Jersey Economic Development Authority, | |

| | | Continental Airlines, 5.25%, 9/15/29 | 3,059,910 |

| 2,500,000 | | New Jersey Economic Development Authority, | |

| | | Continental Airlines, 5.75%, 9/15/27 | 2,402,775 |

| | | Total New Jersey | $ 6,494,145 |

| | | New Mexico — 1.3% | |

| 955,000 | | County of Otero, Otero County Jail Project, | |

| | | 9.0%, 4/1/23 | $ 943,072 |

| 2,960,000(e) | | County of Otero, Otero County Jail Project, | |

| | | 9.0%, 4/1/28 | 2,923,000 |

| | | Total New Mexico | $ 3,866,072 |

| | | New York — 16.9% | |

| 3,000,000 | | Metropolitan Transportation Authority, 4.0%, 11/15/45 | $ 2,990,580 |

| 2,000,000 | | Metropolitan Transportation Authority, 4.0%, 11/15/48 | 1,973,400 |

| 2,500,000 | | Metropolitan Transportation Authority, 5.0%, 11/15/33 | 2,728,175 |

| 2,000,000 | | Metropolitan Transportation Authority, 5.25%, 11/15/55 | 2,189,880 |

| 2,500,000 | | New York State Dormitory Authority, 3.0%, 3/15/41 | 2,589,350 |

| 4,865,000 | | New York State Dormitory Authority, 5.0%, 10/1/50 | 7,810,952 |

| 8,000,000 | | New York State Dormitory Authority, Series A, | |

| | | 4.0%, 7/1/41 | 8,976,400 |

| 2,500,000 | | New York State Dormitory Authority, Series A, | |

| | | 5.0%, 3/15/41 | 3,038,800 |

| 7,500,000 | | New York State Dormitory Authority, Series C, | |

| | | 5.0%, 3/15/39 | 8,400,525 |

The accompanying notes are an integral part of these financial statements.

Pioneer Municipal High Income Trust | Semiannual Report | 10/31/20 19

Schedule of Investments | 10/31/20

(unaudited) (continued)

| | | | |

| Principal | | | |

| Amount | | | |

| USD ($) | | | Value |

| | | New York — (continued) | |

| 1,500,000 | | New York State Dormitory Authority, Trustees of | |

| | | Columbia University, 5.0%, 10/1/45 | $ 2,333,445 |

| 3,000,000 | | New York State Urban Development Corp., | |

| | | 3.0%, 3/15/49 | 3,079,080 |

| 1,000,000 | | Troy Capital Resource Corp., 4.0%, 9/1/40 | 1,076,240 |

| 2,312,177 | | Westchester County Healthcare Corp., Series A, | |

| | | 5.0%, 11/1/44 | 2,464,619 |

| | | Total New York | $ 49,651,446 |

| | | North Carolina — 2.1% | |

| 4,225,000(e) | | Tender Option Bond Trust Receipts/Certificates, | |

| | | RIB, 0.0%, 1/1/38 (144A) | $ 6,129,799 |

| | | Total North Carolina | $ 6,129,799 |

| | | North Dakota — 0.9% | |

| 2,525,000(d) | | County of Burleigh, St. Alexius Medical Center, | |

| | | 5.0%, 7/1/38 | $ 2,714,122 |

| | | Total North Dakota | $ 2,714,122 |

| | | Ohio — 1.6% | |

| 1,000,000 | | Buckeye Tobacco Settlement Financing Authority, | |

| | | 4.0%, 6/1/48 | $ 1,083,750 |

| 1,000,000 | | Ohio Housing Finance Agency, Sanctuary Springboro | |

| | | Project, 5.45%, 1/1/38 (144A) | 990,030 |

| 2,500,000(b)(d) | | State of Ohio, Common Schools, Series B, 5.0%, 6/15/29 | 2,693,975 |

| | | Total Ohio | $ 4,767,755 |

| | | Oregon — 2.3% | |

| 1,000,000 | | Oregon Health & Science University, Series A, | |

| | | 5.0%, 7/1/42 | $ 1,220,210 |

| 5,190,000(d) | | Oregon Health & Science University, Series E, | |

| | | 5.0%, 7/1/32 | 5,582,779 |

| | | Total Oregon | $ 6,802,989 |

| | | Pennsylvania — 3.9% | |

| 3,000,000 | | Geisinger Authority, Geisinger Health System, | |

| | | series A-1, 5.0%, 2/15/45 | $ 3,519,180 |

| 1,500,000 | | Pennsylvania Turnpike Commission, 5.25%, 12/1/44 | 1,874,505 |

| 500,000 | | Philadelphia Authority for Industrial Development, 5.5%, | |

| | | 6/1/49 (144A) | 514,465 |

| 460,000 | | Philadelphia Authority for Industrial Development, | |

| | | Greater Philadelphia Health Action, Inc., Project, | |

| | | Series A, 6.625%, 6/1/50 | 474,297 |

| 2,000,000 | | Philadelphia Authority for Industrial Development, | |

| | | Nueva Esperanze, Inc., 8.2%, 12/1/43 | 2,151,020 |

The accompanying notes are an integral part of these financial statements.

20 Pioneer Municipal High Income Trust | Semiannual Report | 10/31/20

| | | | |

| Principal | | | |

| Amount | | | |

| USD ($) | | | Value |

| | | Pennsylvania — (continued) | |

| 1,000,000 | | Philadelphia Authority for Industrial Development, | |

| | Performing Arts Charter School Project, 6.5%, | |

| | | 6/15/33 (144A) | $ 1,003,070 |

| 2,000,000 | | Philadelphia Authority for Industrial Development, | |

| | Performing Arts Charter School Project, 6.75%, | |

| | | 6/15/43 (144A) | 2,006,320 |

| | | Total Pennsylvania | $ 11,542,857 |

| | | Philadelphia — 0.3% | |

| 1,000,000 | | Philadelphia Authority for Industrial Development, | |

| | | 5.0%, 11/15/50 | $ 999,990 |

| | | Total Philadelphia | $ 999,990 |

| | | Puerto Rico — 1.3% | |

| 6,255,000(b)(g) | | Commonwealth of Puerto Rico, 8.0%, 7/1/35 | $ 3,737,363 |

| | | Total Puerto Rico | $ 3,737,363 |

| | | Rhode Island — 3.3% | |

| 5,900,000(g) | | Central Falls Detention Facility Corp., 7.25%, 7/15/35 | $ 1,062,000 |

| 2,000,000 | | Rhode Island Health & Educational Building Corp., | |

| | | Brown University, Series A, 4.0%, 9/1/37 | 2,304,360 |

| 1,500,000(d) | | Rhode Island Health & Educational Building Corp., | |

| | | Tockwatten Home Issue, 8.375%, 1/1/46 | 1,520,385 |

| 1,000,000 | | Rhode Island Turnpike & Bridge Authority, 4.0%, 10/1/44 | 1,152,790 |

| 2,500,000(e) | | Tender Option Bond Trust Receipts/Certificates, | |

| | | RIB, 0.0%, 9/1/47 (144A) | 3,671,400 |

| | | Total Rhode Island | $ 9,710,935 |

| | | South Carolina — 1.1% | |

| 2,850,000 | | City of Charleston SC Waterworks & Sewer System | |

| | | Revenue, 4.0%, 1/1/49 | $ 3,293,945 |

| | | Total South Carolina | $ 3,293,945 |

| | | Texas — 9.2% | |

| 500,000 | | Arlington Higher Education Finance Corp., 5.45%, | |

| | | 3/1/49 (144A) | $ 531,515 |

| 1,000,000 | | Arlington Higher Education Finance Corp., Universal | |

| | | Academy, Series A, 7.0%, 3/1/34 | 1,084,420 |

| 2,500,000(d) | | Central Texas Regional Mobility Authority, Sub Lien, | |

| | | 6.75%, 1/1/41 | 2,528,200 |

| 1,250,000 | | City of Houston TX Combined Utility System Revenue, | |

| | | 4.0%, 11/15/35 | 1,510,062 |

| 1,490,000(b) | | County of Harris, Series A, 5.0%, 10/1/26 | 1,828,126 |

| 5,000,000(b) | | Goose Creek Consolidated Independent School District, | |

| | | Series C, 4.0%, 2/15/26 (PSF-GTD Insured) | 5,577,650 |

| 3,785,000 | | North Texas Tollway Authority, Series A, 5.0%, 1/1/35 | 4,355,702 |

| 1,500,000(d) | | Red River Health Facilities Development Corp., MRC | |

| | | Crestview, Series A, 8.0%, 11/15/41 | 1,620,645 |

The accompanying notes are an integral part of these financial statements.

Pioneer Municipal High Income Trust | Semiannual Report | 10/31/20 21

Schedule of Investments | 10/31/20

(unaudited) (continued)

| | | | |

| Principal | | | |

| Amount | | | |

| USD ($) | | | Value |

| | | Texas — (continued) | |

| 3,960,000(g) | | Sanger Industrial Development Corp., Texas Pellets | |

| | | Project, Series B, 8.0%, 7/1/38 | $ 975,150 |

| 1,000,000(g) | | Tarrant County Cultural Education Facilities Finance | |

| | | Corp., Mirador Project, Series A, 4.875%, 11/15/48 | 100 |

| 1,000,000(g) | | Tarrant County Cultural Education Facilities Finance | |

| | | Corp., Mirador Project, Series A, 5.0%, 11/15/55 | 100 |

| 2,000,000(d) | | Tarrant County Cultural Education Facilities Finance | |

| | | Corp., MRC Crestview Project, 8.0%, 11/15/34 | 2,005,240 |

| 2,000,000 | | Texas Water Development Board, 4.0%, 10/15/44 | 2,366,200 |

| 2,500,000(d) | | Travis County Health Facilities Development Corp., | |

| | | Longhorn Village Project, 7.125%, 1/1/46 | 2,529,425 |

| | | Total Texas | $ 26,912,535 |

| | | Utah — 0.4% | |

| 1,000,000 | | Salt Lake City Corp., Airport Revenue, Series B, | |

| | | 5.0%, 7/1/35 | $ 1,215,400 |

| | | Total Utah | $ 1,215,400 |

| | | Virginia — 11.0% | |

| 5,000,000(b) | | City of Alexandria VA, 3.0%, 7/15/46 (ST AID | |

| | | WITHHLDG Insured) | $ 5,378,400 |

| 1,000,000 | | City of Richmond VA Public Utility Revenue, | |

| | | 3.0%, 1/15/45 | 1,077,870 |

| 2,200,000(b) | | County of Arlington, 4.0%, 8/15/35 | 2,524,214 |

| 1,415,000(b) | | County of Fairfax, Series A, 4.0%, 10/1/33 (ST AID | |

| | | WITHHLDG Insured) | 1,627,363 |

| 5,000,000 | | University of Virginia, Series A, 5.0%, 4/1/42 | 6,179,450 |

| 4,000,000 | | Upper Occoquan Sewage Authority, 4.0%, 7/1/41 | 4,409,760 |

| 5,000,000 | | Virginia College Building Authority, Series A, | |

| | | 3.0%, 2/1/36 | 5,413,800 |

| 4,000,000 | | Virginia Commonwealth Transportation Board, Capital | |

| | | Projects, 3.0%, 5/15/37 | 4,343,440 |

| 1,000,000 | | Virginia Public Building Authority, 4.0%, 8/1/39 | 1,194,320 |

| | | Total Virginia | $ 32,148,617 |

| | | Washington — 10.3% | |

| 3,745,000 | | City of Seattle, Water System Revenue, 4.0%, 8/1/32 | $ 4,290,197 |

| 2,500,000(b) | | King County, Issaquah School District No. 411, | |

| | | 4.0%, 12/1/31 (SCH BD GTY Insured) | 2,862,300 |

| 14,315,000(b)(c) | | State of Washington, Motor Vehicle Sales Tax, | |

| | | Series C, 6/1/22 (NATL Insured) | 14,162,545 |

| 3,285,000(e) | | Tender Option Bond Trust Receipts/Certificates, | |

| | | RIB, 0.0%, 1/1/45 (144A) | 4,823,628 |

| 2,500,000 | | University of Washington, Series B, 5.0%, 6/1/29 | 2,992,200 |

| 1,150,000 | | Washington State Housing Finance Commission, | |

| | | Mirabella Project, Series A, 6.75%, 10/1/47 (144A) | 1,192,631 |

| | | Total Washington | $ 30,323,501 |

The accompanying notes are an integral part of these financial statements.

22 Pioneer Municipal High Income Trust | Semiannual Report | 10/31/20

| | | | |

| Principal | | | |

| Amount | | | |

| USD ($) | | | Value |

| | | Wisconsin — 6.2% | |

| 1,500,000 | | Public Finance Authority, Gardner Webb University, | |

| | | 5.0%, 7/1/31 (144A) | $ 1,612,920 |

| 5,000,000 | | Public Finance Authority, Glenridge Palmer Ranch, | |

| | | Series A, 8.25%, 6/1/46 (144A) | 5,238,250 |

| 750,000 | | Public Finance Authority, Roseman University Health | |

| | | Sciences Project, 5.875%, 4/1/45 | 779,857 |

| 1,000,000 | | Public Finance Authority, SearStone CCRC Project, | |

| | | Series A, 5.3%, 6/1/47 | 1,001,600 |

| 1,465,000(d) | | Public Finance Authority, SearStone CCRC Project, | |

| | | Series A, 8.625%, 6/1/47 | 1,645,825 |

| 5,000,000 | | Wisconsin Department of Transportation, Series A, | |

| | | 5.0%, 7/1/28 | 5,769,850 |

| 2,000,000 | | Wisconsin Housing & Economic Development Authority, | |

| | | 2.95%, 3/1/42 (FNMA COLL Insured) | 2,056,981 |

| | | Total Wisconsin | $ 18,105,283 |

| | | TOTAL MUNICIPAL BONDS | |

| | | (Cost $397,391,247) | $ 413,379,866 |

| | | TOTAL INVESTMENTS IN UNAFFILIATED ISSUERS — 141.2% | |

| | | (Cost $398,387,633) | $ 414,371,230 |

| | | OTHER ASSETS AND LIABILITIES — (41.2)% | $ (120,871,033) |

| | | NET ASSETS APPLICABLE TO COMMON | |

| | | SHAREOWNERS — 100.0% | $ 293,500,197 |

| | |

RIB | Residual Interest Bond is purchased in a secondary market. The interest rate is subject to |

| change periodically and inversely based upon prevailing market rates. The interest rate |

| shown is the rate at October 31, 2020. |

(144A) | Security is exempt from registration under Rule 144A of the Securities Act of 1933. Such |

| securities may be resold normally to qualified institutional buyers in a transaction exempt |

| from registration. At October 31, 2020, the value of these securities amounted to |

| $36,076,888, or 12.3% of net assets applicable to common shareowners. |

(a) | Consists of Revenue Bonds unless otherwise indicated. |

(b) | Represents a General Obligation Bond. |

(c) | Security issued with a zero coupon. Income is recognized through accretion of discount. |

(d) | Prerefunded bonds have been collateralized by U.S. Treasury or U.S. Government |

| Agency securities which are held in escrow to pay interest and principal on the tax |

| exempt issue and to retire the bonds in full at the earliest refunding date. |

(e) | The interest rate is subject to change periodically. The interest rate and/or reference |

| index and spread shown at October 31, 2020. |

(f) | Escrow to maturity. |

(g) | Security is in default. |

The accompanying notes are an integral part of these financial statements.

Pioneer Municipal High Income Trust | Semiannual Report | 10/31/20 23

Schedule of Investments | 10/31/20

(unaudited) (continued)

Purchases and sales of securities (excluding temporary cash investments) for the six months ended October 31, 2020, aggregated $32,604,038 and $25,440,427, respectively.

The Trust is permitted to engage in purchase and sale transactions (“cross trades”) with certain funds and accounts for which Amundi Pioneer Asset Management, Inc. (the “Adviser”) serves as the Trust’s investment adviser, as set forth in Rule 17a-7 under the Investment Company Act of 1940, pursuant to procedures adopted by the Board of Trustees. Under these procedures, cross trades are effected at current market prices. During the six months ended October 31, 2020, the Trust did not engage in any cross trade activity.

At October 31, 2020, the net unrealized appreciation on investments based on cost for federal tax purposes of $396,420,712 was as follows:

| | | | |

| Aggregate gross unrealized appreciation for all investments in which | | | |

| there is an excess of value over tax cost | | $ | 30,753,899 | |

| Aggregate gross unrealized depreciation for all investments in which | | | | |

| there is an excess of tax cost over value | | | (12,803,381 | ) |

| Net unrealized appreciation | | $ | 17,950,518 | |

Various inputs are used in determining the value of the Trust’s investments. These inputs are summarized in the three broad levels below.

Level 1 – quoted prices in active markets for identical securities.

Level 2 – other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risks, etc.). See Notes to Financial Statements — Note 1A.

Level 3 – significant unobservable inputs (including the Trust’s own assumptions in determining fair value of investments). See Notes to Financial Statements — Note 1A.

The following is a summary of the inputs used as of October 31, 2020, in valuing the Trust’s investments:

| | | | | | | | | | | | | |

| | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

| Collateralized Mortgage Obligation | | $ | — | | | $ | 991,364 | | | $ | — | | | $ | 991,364 | |

Municipal Bonds | | | — | | | | 413,379,866 | | | | — | | | | 413,379,866 | |

| Total Investments in Securities | | $ | — | | | $ | 414,371,230 | | | $ | — | | | $ | 414,371,230 | |

| Other Financial Instruments | | | | | | | | | | | | | | | | |

Variable Rate MuniFund Term | | | | | | | | | | | | | | | | |

Preferred Shares(a) | | $ | — | | | $ | (125,000,000 | ) | | $ | — | | | $ | (125,000,000 | ) |

| Total Other | | | | | | | | | | | | | | | | |

| Financial Instruments | | $ | — | | | $ | (125,000,000 | ) | | $ | — | | | $ | (125,000,000 | ) |

(a) The Trust may hold liabilities in which the fair value approximates the carrying amount for financial statement purposes.

During the six months ended October 31, 2020, there were no transfers between Levels 1, 2 and 3.

The accompanying notes are an integral part of these financial statements.

24 Pioneer Municipal High Income Trust | Semiannual Report | 10/31/20

Statement of Assets and Liabilities |

10/31/20 (unaudited)

| | | | |

| ASSETS: | | | |

| Investments in unaffiliated issuers, at value (cost $398,387,633) | | $ | 414,371,230 | |

| Cash | | | 6,479,118 | |

| Receivables — | | | | |

| Investment securities sold | | | 150,007 | |

| Interest | | | 5,173,434 | |

| Due from the Adviser | | | 158,981 | |

| Other assets | | | 14,964 | |

| Total assets | | $ | 426,347,734 | |

| LIABILITIES: | | | | |

| Variable Rate MuniFund Term Preferred Shares* | | $ | 125,000,000 | |

| Payables — | | | | |

| Investment securities purchased | | | 7,718,755 | |

| Interest expense | | | 1,061 | |

| Distributions | | | 25 | |

| Trustees’ fees | | | 2,147 | |

| Due to affiliates | | | 3,125 | |

| Accrued expenses | | | 122,424 | |

| Total liabilities | | $ | 132,847,537 | |

| NET ASSETS APPLICABLE TO COMMON SHAREOWNERS: | | | | |

| Paid-in capital | | $ | 300,996,046 | |

| Distributable earnings (loss) | | | (7,495,849 | ) |

| Net assets applicable to common shareowners | | $ | 293,500,197 | |

| NET ASSET VALUE PER COMMON SHARE: | | | | |

| No par value | | | | |

| Based on $293,500,197/22,771,349 common shares | | $ | 12.89 | |

* $100,000 liquidation value per share applicable to 1,250 shares. |

The accompanying notes are an integral part of these financial statements.

Pioneer Municipal High Income Trust | Semiannual Report | 10/31/20 25

Statement of Operations (unaudited)

FOR THE SIX MONTHS ENDED 10/31/20

| | | | | | | |

| INVESTMENT INCOME: | | | | | | |

| Interest from unaffiliated issuers | | $ | 8,823,142 | | | | |

| Total investment income | | | | | | $ | 8,823,142 | |

| EXPENSES: | | | | | | | | |

| Management fees | | $ | 1,268,966 | | | | | |

| Administrative expense | | | 98,575 | | | | | |

| Transfer agent fees | | | 5,779 | | | | | |

| Distribution fees | | | | | | | | |

| Shareowner communications expense | | | 15,098 | | | | | |

| Custodian fees | | | 2,525 | | | | | |

| Registration fees | | | 7,356 | | | | | |

| Professional fees | | | 177,817 | | | | | |

| Printing expense | | | 6,653 | | | | | |

| Pricing fees | | | 3,425 | | | | | |

| Trustees’ fees | | | 10,615 | | | | | |

| Insurance expense | | | 2,461 | | | | | |

| Interest expense | | | 660,600 | | | | | |

| Miscellaneous | | | 44,630 | | | | | |

| Total expenses | | | | | | $ | 2,304,500 | |

| Net investment income | | | | | | $ | 6,518,642 | |

| REALIZED AND UNREALIZED GAIN (LOSS) ON INVESTMENTS: | | | | | |

| Net realized gain (loss) on: | | | | | | | | |

| Investments in unaffiliated issuers | | $ | 2,207,584 | | | | | |

| Change in net unrealized appreciation (depreciation) on: | | | | | | | | |

| Investments in unaffiliated issuers | | | 10,664,448 | | | | | |

| Net realized and unrealized gain (loss) on investments | | | | | | $ | 12,872,032 | |

| Net increase in net assets resulting from operations | | | | | | $ | 19,390,674 | |

The accompanying notes are an integral part of these financial statements.

26 Pioneer Municipal High Income Trust | Semiannual Report | 10/31/20

Statements of Changes in Net Assets

| | | | | | | |

| | Six Months | | | | |

| | Ended | | | Year | |

| | 10/31/20 | | | Ended | |

| | (unaudited) | | | 4/30/20 | |

| FROM OPERATIONS: | | | | | | |

Net investment income (loss) | | $ | 6,518,642 | | | $ | 12,469,533 | |

Net realized gain (loss) on investments | | | 2,207,584 | | | | 1,931,953 | |

Change in net unrealized appreciation (depreciation) | | | | | | | | |

| on investments | | | 10,664,448 | | | | (9,109,466 | ) |

| Net increase in net assets resulting from operations | | $ | 19,390,674 | | | $ | 5,292,020 | |

| DISTRIBUTIONS TO COMMON SHAREOWNERS: | | | | | | | | |

($0.27 and $0.57 per share, respectively) | | $ | (6,148,264 | ) | | $ | (12,979,669 | ) |

| Total distributions to common shareowners | | $ | (6,148,264 | ) | | $ | (12,979,669 | ) |

| Net increase (decrease) in net assets | | | | | | | | |

| applicable to common shareowners | | $ | 13,242,410 | | | $ | (7,687,649 | ) |

| NET ASSETS APPLICABLE TO COMMON SHAREOWNERS: | | | | | | | | |

Beginning of period | | $ | 280,257,787 | | | $ | 287,945,436 | |

End of period | | $ | 293,500,197 | | | $ | 280,257,787 | |

The accompanying notes are an integral part of these financial statements.

Pioneer Municipal High Income Trust | Semiannual Report | 10/31/20 27

Statement of Cash Flows

FOR THE SIX MONTHS ENDED 10/31/20

| | | | |

| Cash Flows From Operating Activities: | | | |

| Net Increase in net assets resulting from operations | | $ | 19,390,674 | |

| Adjustments to reconcile net decrease in net assets resulting | | | | |

| from operations to net cash, restricted cash and foreign | | | | |

| currencies from operating activities: | | | | |

| Purchases of investment securities | | $ | (27,978,734 | ) |

| Proceeds from disposition and maturity of investment securities | | | 26,290,401 | |

| Net (accretion) and amortization of discount/premium on investment securities | | | 219,909 | |

| Change in unrealized depreciation on investments in unaffiliated issuers | | | (10,664,448 | ) |

| Net realized gain on investments in unaffiliated issuers | | | (2,207,584 | ) |

| Decrease in interest receivable | | | 358,837 | |

| Decrease in other assets | | | 92,330 | |

| Decrease in due from advisor | | | 7,551 | |

| Increase in due to affiliates | | | 384 | |

| Increase in trustees’ fees payable | | | 2,101 | |

| Increase in accrued expenses payable | | | 33,566 | |

| Decrease in interest expense payable | | | (27,489 | ) |

| Net cash provided by operating activities | | $ | 5,517,498 | |

| Cash Flows Used in Financing Activities: | | | | |

| Distributions to shareowners | | $ | (6,148,264 | ) |

| Net cash and foreign currencies used in financing activities | | $ | (6,148,264 | ) |

| Cash, restricted cash and foreign currencies: | | | | |

| Beginning of the period | | $ | 7,109,884 | |

| End of the period | | $ | 6,479,118 | |

| Cash Flow Information: | | | | |

| Cash paid for interest | | $ | 660,600 | |

The accompanying notes are an integral part of these financial statements.

28 Pioneer Municipal High Income Trust | Semiannual Report | 10/31/20

| | | | | | | | | | | | | | | | | | | |

| | Six Months | | | | | | | | | | | | | | | | |

| | Ended | | | Year | | | Year | | | Year | | | Year | | | Year | |

| | 10/31/20 | | | Ended | | | Ended | | | Ended | | | Ended | | | Ended | |

| | (unaudited) | | | 4/30/20 | | | 4/30/19 | | | 4/30/18 | | | 4/30/17* | | | 4/30/16* | |

| Per Share Operating Performance | | | | | | | | | | | | | | | | | | |

Net asset value, beginning of period | | $ | 12.31 | | | $ | 12.65 | | | $ | 12.50 | | | $ | 12.72 | | | $ | 13.49 | | | $ | 13.31 | |

Increase (decrease) from investment operations: (a) | | | | | | | | | | | | | | | | | | | | | | | | |

| Net investment income | | $ | 0.29 | | | $ | 0.55 | | | $ | 0.74 | | | $ | 0.78 | | | $ | 0.73 | | | $ | 0.83 | |

| Net realized and unrealized gain (loss) on investments | | | 0.56 | | | | (0.32 | ) | | | 0.19 | | | | (0.29 | ) | | | (0.76 | ) | | | 0.20 | |

Distributions to preferred shareowners from: | | | | | | | | | | | | | | | | | | | | | | | | |

| Net investment income | | $ | — | | | $ | — | | | $ | (0.15 | ) | | $ | (0.09 | ) | | $ | (0.05 | ) | | $ | (0.01 | ) |

| Net increase (decrease) from investment operations | | $ | 0.85 | | | $ | 0.23 | | | $ | 0.78 | | | $ | 0.40 | | | $ | (0.08 | ) | | $ | 1.02 | |

Distributions to shareowners from: | | | | | | | | | | | | | | | | | | | | | | | | |

| Net investment income and previously undistributed | | | | | | | | | | | | | | | | | | | | | | | | |

| net investment income | | $ | (0.27 | ) | | $ | (0.57 | ) | | $ | (0.63 | ) | | $ | (0.62 | ) | | $ | (0.69 | ) | | $ | (0.84 | )** |

| Net increase (decrease) in net asset value | | $ | 0.58 | | | $ | (0.34 | ) | | $ | 0.15 | | | $ | (0.22 | ) | | $ | (0.77 | ) | | $ | 0.18 | |

Net asset value, end of period | | $ | 12.89 | | | $ | 12.31 | | | $ | 12.65 | | | $ | 12.50 | | | $ | 12.72 | | | $ | 13.49 | |

Market value, end of period | | $ | 11.34 | | | $ | 10.82 | | | $ | 11.91 | | | $ | 11.25 | | | $ | 11.75 | | | $ | 14.07 | |

| Total return at net asset value (b) | | | 7.16 | %(c) | | | 2.00 | %(d) | | | 6.93 | % | | | 3.53 | % | | | (0.45 | )% | | | 8.12 | % |

| Total return at market value (b) | | | 7.26 | %(c) | | | (4.77 | )% | | | 11.86 | % | | | 0.87 | % | | | (11.83 | )% | | | 1.75 | % |

Ratios to average net assets of shareowners: | | | | | | | | | | | | | | | | | | | | | | | | |

| Total expenses plus interest expense (e) | | | 1.55 | %(f) | | | 2.13 | % | | | 1.03 | % | | | 1.01 | % | | | 1.00 | % | | | 1.05 | % |

| Net investment income before preferred share distributions | | | 4.39 | %(f) | | | 4.24 | % | | | 5.92 | % | | | 6.14 | % | | | 5.54 | % | | | 6.24 | % |

| Preferred share distributions | | | — | % | | | — | % | | | (1.23 | )% | | | 0.71 | % | | | 0.38 | % | | | 0.10 | % |

| Net investment income available to shareowners | | | 4.39 | %(f) | | | 4.24 | % | | | 4.69 | % | | | 5.44 | % | | | 5.16 | % | | | 6.14 | % |

Portfolio turnover rate | | | 6 | % | | | 17 | % | | | 16 | % | | | 20 | % | | | 19 | % | | | 9 | % |

Net assets, end of period (in thousands) | | $ | 293,500 | | | $ | 280,258 | | | $ | 287,945 | | | $ | 284,596 | | | $ | 289,741 | | | $ | 307,027 | |

The accompanying notes are an integral part of these financial statements.

Pioneer Municipal High Income Trust | Semiannual Report | 10/31/20 29

Financial Highlights (continued)

| | | | | | | | | | | | | | | | | | | |

| | Six Months | | | | | | | | | | | | | | | | |

| | Ended | | | Year | | | Year | | | Year | | | Year | | | Year | |

| | 10/31/20 | | | Ended | | | Ended | | | Ended | | | Ended | | | Ended | |

| | (unaudited) | | | 4/30/20 | | | 4/30/19 | | | 4/30/18 | | | 4/30/17* | | | 4/30/16* | |

Preferred shares outstanding (in thousands) (g)(h) | | $ | 125,000 | | | $ | 125,000 | | | $ | 125,000 | | | $ | 125,000 | | | $ | 101,000 | | | $ | 101,000 | |

Asset coverage per preferred share, end of period | | $ | 334,801 | | | $ | 324,229 | | | $ | 330,370 | | | $ | 327,672 | | | $ | 96,723 | | | $ | 100,998 | |

Average market value per preferred share (i) | | $ | 100,000 | | | $ | 100,000 | | | $ | 100,000 | | | $ | 100,000 | | | $ | 25,000 | | | $ | 25,000 | |

Liquidation value, including dividends payable, per preferred share | | $ | 100,001 | | | $ | 100,023 | | | $ | 100,014 | | | $ | 99,996 | | | $ | 25,006 | | | $ | 25,001 | |

| | |

* | The Trust was audited by an independent registered public accounting firm other than Ernst & Young LLP. |

** | The amount of distributions made to shareowners during the year were in excess of the net investment income earned by the Trust during the year. The Trust has accumulated undistributed net investment income which is part of the Trust’s NAV. A portion of the accumulated net investment income was distributed to shareowners during the year. |

(a) | The per common share data presented above is based upon the average common shares outstanding for the periods presented. |

(b) | Total investment return is calculated assuming a purchase of common shares at the current net asset value or market value on the first day and a sale at the current net asset value or market value on the last day of the periods reported. Dividends and distributions, if any, are assumed for purposes of this calculation to be reinvested at prices obtained under the Trust’s dividend reinvestment plan. Total investment return does not reflect brokerage commissions. Past performance is not a guarantee of future results. |

(c) | Not annualized. |

(d) | If the Fund had not recognized gains in settlement of class action lawsuits during the year ended April 30, 2020, the total return would have been 1.73%. |

(e) | Expense ratios do not reflect the effect of distribution payments to preferred shareowners. |

(f)

| Annualized.

|

(g) | Prior to February 9, 2018 there were 4,040 Auction Preferred Shares (“APS”) outstanding with a liquidation preference of $25,000 per share. The Trust redeemed all 2,000 outstanding Series A APS on February 14, 2018 and all 2,040 outstanding Series B APS on February 15, 2018. |

(h) | The Trust issued 1,250 Variable Rate MuniFund Term Preferred Shares, with a liquidation preference of $100,000 per share, on February 9, 2018. |

(i) | Market value is redemption value without an active market. |

The accompanying notes are an integral part of these financial statements.

30 Pioneer Municipal High Income Trust | Semiannual Report | 10/31/20

Notes to Financial Statements |

10/31/20 (unaudited)

1. Organization and Significant Accounting Policies

Pioneer Municipal High Income Trust (the “Trust”) was organized as a Delaware statutory trust on March 13, 2003. Prior to commencing operations on July 21, 2003, the Trust had no operations other than matters relating to its organization and registration as a diversified, closed-end management investment company under the Investment Company Act of 1940, as amended. The investment objective of the Trust is to seek a high level of current income exempt from regular federal income tax, and the Trust may, as a secondary objective, also seek capital appreciation to the extent that it is consistent with its primary investment objective.

Amundi Pioneer Asset Management, Inc., an indirect, wholly owned subsidiary of Amundi and Amundi’s wholly owned subsidiary, Amundi USA, Inc., serves as the Trust’s investment adviser (the “Adviser”). Amundi Pioneer Distributor, Inc., an affiliate of Amundi Pioneer Asset Management, Inc., serves as the Trust’s distributor (the “Distributor”).

During March 2017, the Financial Accounting Standards Board (FASB) issued an Accounting Standard Update, ASU 2017-08, Receivables-Nonrefundable Fees and Other Costs (Subtopic 310-20), Premium Amortization on Purchased Callable Debt Securities (“ASU 2017-08”), which shortens the amortization period for purchased non-contingently callable debt securities held at a premium. ASU 2017-08 specifies that the premium amortization period ends at the earliest call date, for certain purchased non-contingently callable debt securities. ASU 2017-08 is effective for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2018. The Trust has adopted ASU 2017-08 as of April 30, 2020. The implementation of ASU 2017-08 did not have a material impact on the Trust’s Financial Statements.

In March 2020, FASB issued an Accounting Standard Update, ASU 2020-04, Reference Rate Reform (Topic 848) -- Facilitation of the Effects of Reference Rate Reform on Financial Reporting ("ASU 2020-04"), which provides optional, temporary relief with respect to the financial reporting of contracts subject to certain types of modifications due to the planned discontinuation of the London Interbank Offered Rate ("LIBOR") and other LIBOR-based reference rates at the end of 2021. The temporary relief provided by ASU 2020-04 is effective for certain reference rate-related contract modifications that occur during the period from March 12, 2020

Pioneer Municipal High Income Trust | Semiannual Report | 10/31/20 31

through December 31, 2022. Management is evaluating the impact of ASU 2020-04 on the Fund's investments, derivatives, debt and other contracts that will undergo reference rate-related modifications as a result of the reference rate reform.

The Trust is an investment company and follows investment company accounting and reporting guidance under U.S. Generally Accepted Accounting Principles (“U.S. GAAP”). U.S. GAAP requires the management of the Trust to make estimates and assumptions that affect the reported amounts of assets and liabilities, the disclosure of contingent assets and liabilities at the date of the financial statements, and the reported amounts of income, expenses and gain or loss on investments during the reporting period. Actual results could differ from those estimates.

The following is a summary of significant accounting policies followed by the Trust in the preparation of its financial statements:

A. Security Valuation

The net asset value of the Trust is computed once daily, on each day the New York Stock Exchange (“NYSE”) is open, as of the close of regular trading on the NYSE.

Fixed-income securities are valued by using prices supplied by independent pricing services, which consider such factors as market prices, market events, quotations from one or more brokers, Treasury spreads, yields, maturities and ratings, or may use a pricing matrix or other fair value methods or techniques to provide an estimated value of the security or instrument. A pricing matrix is a means of valuing a debt security on the basis of current market prices for other debt securities, historical trading patterns in the market for fixed-income securities and/or other factors. Non-U.S. debt securities that are listed on an exchange will be valued at the bid price obtained from an independent third party pricing service. When independent third party pricing services are unable to supply prices, or when prices or market quotations are considered to be unreliable, the value of that security may be determined using quotations from one or more broker-dealers

Securities for which independent pricing services or broker-dealers are unable to supply prices or for which market prices and/or quotations are not readily available or are considered to be unreliable are valued by a fair valuation team comprised of certain personnel of the Adviser pursuant to procedures adopted by the Trust’s Board of Trustees. The Adviser’s fair valuation team uses fair value methods approved by the Valuation

32 Pioneer Municipal High Income Trust | Semiannual Report | 10/31/20

Committee of the Board of Trustees. The Adviser’s fair valuation team is responsible for monitoring developments that may impact fair valued securities and for discussing and assessing fair values on an ongoing basis, and at least quarterly, with the Valuation Committee of the Board of Trustees.

Inputs used when applying fair value methods to value a security may include credit ratings, the financial condition of the company, current market conditions and comparable securities. The Trust may use fair value methods if it is determined that a significant event has occurred after the close of the exchange or market on which the security trades and prior to the determination of the Trust’s net asset value. Examples of a significant event might include political or economic news, corporate restructurings, natural disasters, terrorist activity or trading halts. Thus, the valuation of the Trust’s securities may differ significantly from exchange prices, and such differences could be material.

At October 31, 2020, no securities were valued using fair value methods (other than securities valued using prices supplied by independent pricing services, broker-dealers or using a third party insurance industry pricing model).

B. Investment Income and Transactions

Interest income, including interest on income-bearing cash accounts, is recorded on the accrual basis. Dividend and interest income are reported net of unrecoverable foreign taxes withheld at the applicable country rates and net of income accrued on defaulted securities.

Discounts and premiums on purchase prices of debt securities are accreted or amortized, respectively, daily, into interest income on an effective yield to maturity basis with a corresponding increase or decrease in the cost basis of the security. Premiums and discounts related to certain mortgage-backed securities are amortized or accreted in proportion to the monthly paydowns.

Interest and dividend income payable by delivery of additional shares is reclassified as PIK (payment-in-kind) income upon receipt and is included in interest and dividend income, respectively.

Security transactions are recorded as of trade date. Gains and losses on sales of investments are calculated on the identified cost method for both financial reporting and federal income tax purposes.

Pioneer Municipal High Income Trust | Semiannual Report | 10/31/20 33

C. Federal Income Taxes