POULTON & YORDAN

ATTORNEYS AT LAW

___________________________________________________________________________

RICHARD T. LUDLOW

January 16, 2008

Mark Wojciechowski

Staff Accountant

United States Securities and Exchange Commission

Division of Corporate Finance

Mail Stop 7010

100 F Street, N.E.

Washington, D.C. 20549

Re: Bekem Metals, Inc.

Form 10-KSB for the Fiscal Year Ended December 31, 2006

Filed April 2, 2007

Form 10-Q for the Quarterly Period Ended September 30, 2007

Filed November 14, 2007

Response letter dated October 15, 2007

| File No.: 0-50218 |

Dear Mr. Wojciechowski:

At the request of the management of Bekem Metals, Inc. (the “Company” or “Bekem”) we are responding to comments raised by the staff at the Securities and Exchange Commission in your letter dated November 30, 2007. Following are the responses to your comments.

General

| 1. | As noted in your response letter dated October 15, 2007, please file amended documents to include the proposed disclosure revisions without further delay. Please ensure your amended documents include an explanatory paragraph detailing the reasons you are filing an amendment. Please contact us to discuss. |

| No response required. |

POULTON & YORDAN |

| TELEPHONE: 801-355-1341 |

324 SOUTH 400 WEST, SUITE 250 |

| FAX: 801-355-2990 |

SALT LAKE CITY, UT 84101 |

| POST@POULTON-YORDAN.COM |

Mr. Mark Wojciechowski

January 16, 2008

Page 2

Form 10-KSB for the Fiscal Year Ended December 31, 2006

Management’s Discussion and Analysis, page 22

Results of Operations, page 23

| 2. | We note your response to comment one from our letter dated September 6, 2007. Within your proposed disclosure of the reasons for fluctuations in ‘Other income (expense)’ you explain that during 2006 you also “realized losses from the write off and disposal of inventory and from the disposal and impairment of property, plant and equipment in the amounts of $83,476 and $58,928, respectively.” This proposed disclosure seems inconsistent with your disclosure on page F-9 in which you state “At December 31, 2006, the Company reviewed its long-lived assets...and determined no impairment was necessary.” Please advise, and revise your disclosures to be consistent. Please also tell us why you believe it is appropriate to record your write offs of inventory and impairment of property, plant and equipment within ‘Other income (expense)’ rather than ‘Operating expenses’. See paragraph 25 of SFAS 144 for further guidance. |

The Company does not believe the disclosures as currently presented are inconsistent. While the Company realized losses from the write off and disposal of inventory and impairment of property, plant and equipment during 2006, these write offs and impairments were realized at the end of 2006. So, at December 31, 2006 no further write offs or impairments were needed. In light of the staff’s comment, however, the Company proposes to revise the disclosure contained in Note 1 as follows:

Impairment of Long-Lived Assets and Long-Lived Assets to be Disposed — Long-lived assets are reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable. Recoverability of assets to be held and used is measured by comparison of the carrying amount of an asset to future net cash flows expected to be generated by the asset. If such assets are considered to be impaired, the impairment to be recognized is measured by the amount that the carrying amount of the assets exceeds the fair value of the assets. Assets to be disposed of are reported at the lower of the carrying amount or fair value less costs to sell. During 2006, the Company realized losses from the impairment and disposal of property, plant and equipment in the amount of $58,928. At December 31, 2006, the Company reviewed its long-lived assets as disclosed above and determined no additional impairment was necessary. (See page F-10 of Exhibit A to this letter.)

Mr. Mark Wojciechowski

January 16, 2008

Page 3

The Company agrees with the staff’s position that classification of write offs of inventory and impairment of property, plant and equipment are more appropriately classified as ‘Operating expenses’ rather than ‘Other income (expense)’ and will reclassify those amounts to ‘Operating expenses.’ As a result of these changes, the Company now proposes not to include the previously proposed revision to the “Management’s Discussion and Analysis” set forth in our response to comment 1 to your comment letter dated September 6, 2007.

Nature of Business, page F-8

| 3. | Your response to comment seven focuses on the definition of production phase included within EITF 04-6, and does not address the definition of production stage in Industry Guide 7. Please note that the definition of production phase included within EITF 04-6 is limited to the context of the issue discussed in EITF 04-6. Without a “reserve,” as defined by Industry Guide 7(a)(1), the company must be in the “exploration stage,” as defined by Guide 7(a)(4)(i). As such, SEC’s Industry Guide 7 specifically requires that the filing describe the business activities as “exploration stage” activities until such time as the company has “reserves” as defined in the Guide. Therefore: |

| • | Revise the disclosure to ensure that investors are not misguided as to the actual stage of mineral-related activity. State clearly that the company is currently engaged in mineral exportation activities and that you are in the “exploration stage.” |

| • | Remove all references in the document that use the term “mining” or “mining operations,” or any term that can imply mineral production, such as “operations.” |

| • | Substitute the term “mineral exploration” for “mining/mineral operations.” |

There may be further comments concerning these points, pending your response.

The Company agrees to present itself as being in exploration stage until such time as the Company has reserves as defined by Industry Guide 7. The Company also agrees to revise its disclosure to ensure that investors are not misguided as to the actual stage of its mineral-related activities. The Company would like to point out to the staff that while it understands its disclosures are governed by Industry Guide 7, the staff certainly understands that the Ministry of Energy and Mineral Resources of the Republic of Kazakhstan (“MEMR”) is not governed by nor does it rely upon Industry Guide 7 when it grants licenses or imposes the work program requirements associated with the licenses it grants. Industry Guide 7 notwithstanding, the MEMR

Mr. Mark Wojciechowski

January 16, 2008

Page 4

on the basis of the Soviet era reserve reports, which may not conform to the standards of Industry Guide 7, determined that commercially minable reserves exist at the Company’s Kempirsai and Mamyt deposits. Accordingly, the licenses granted by the MEMR for the Kempirsai and Mamyt deposits are production licenses and require the Company to extract certain quantities of nickel, cobalt and coal in order to retain the licenses. As per my discussion with Mr. Shuler, an SEC staff engineer, to the extent the Company discusses current production, it proposes to do so in the context of exploration stage activities.

As you are aware, section (b) of Industry Guide 7 requires that the Company provide a description of the prior operations of the property. As stated in the Company’s disclosure, the Kempirsai deposit was previously a commercial mine during the 1980s and early 1990s. Therefore, in order to comply with Industry Guide 7 and to accurately portray the history of the Kempirsai deposit, the Company must use terms like “production” and “operations” when discussing the history of the Kempirsai deposit.

In order to address the staff’s concerns and to ensure the disclosure of the status of the Company’s operations is not misleading, the Company has revised its disclosure to differentiate between the historical operations of the Kempirsai deposit and the current exploration stage activities of the Company.

Please see the attached Exhibit A to this letter wherein the Company is providing its proposed revisions to Items 1 & 2 “Description of Business and Properties”, Item 6. “Management’s Discussion and Analysis” and the revised Consolidated Financial Statements and Notes to the Annual Report for the year ended December 31, 2006 on Form 10-KSB to address the staff's comments on this issue. For detail regarding the location of such revisions, please see the introduction to Exhibit A.

| 4. | We also note from your response to comment seven that you believe you are in the production stage as a result of the Republic of Kazakhstan issuing a commercial production right for these deposits, and the fact that KKM and its predecessors have extracted and sold minerals from these ore bodies since the 1980’s. Please note that the term “production stage” should be used when companies are engaged in commercial-scale, profit oriented extraction of minerals. As you do not disclose any “reserves,” as defined by Industry Guide 7, please remove the terms “develop,” “development” or “production” throughout the document, and replace this terminology, as needed with the terms “explore” or “exploration.” This includes the using of the terms in the Financial Statement head notes and footnotes. See Instruction 1 to paragraph (a), Industry Guide 7. |

Please see response to comment 3 above.

Mr. Mark Wojciechowski

January 16, 2008

Page 5

| 5. | Based on the above comments, we re-issue prior comment eight from our letter dated September 6, 2007. |

As noted in response to comment 3 above, the Company proposes to revise its disclosure consistent with Industry Guide 7 and SFAS 7.

| 6. | Please note it is the staff’s position that prior to declaring reserves, the company should obtain a “final” or “bankable” feasibility study, and employ the historic three-year average price for the economic analysis. In addition, the company should submit all necessary permits and authorizations, including environmental, to governmental authorities. |

No response needed.

Note 2 Acquisitions and Disposal, page F-12

Acquisition of Kyzyl Mamyt, LLC, page F-13

| 7. | We note your response to prior comment ten. As previously requested, please expand your disclosure to explain why you were able to acquire KKM at a price significantly below the fair value of the long term assets acquired. |

The Company proposes to expand the disclosure through revision of “NOTE 2 –ACQUISITIONS AND DISPOSAL - Kazakh Metals, Inc. acquisition of Kyzyl Kain Mamyt, LLC” as follows:

On June 1, 2005, Kazakh Metals acquired 100% of the equity interests of Kyzyl Kain Mamyt, LLC (KKM) for the cash purchase price of $100,000. The management of the Company understands that at this time KKM was not able to maintain the subsoil use contract because of financial liquidity problems. The owners of KKM, prior to its acquisition by Kazakh Metals, had incurred significant debt obligations on the property which they were unable to service and KKM’s assets were pledged as a guarantee for these debt obligations. Moreover, at the time of the acquisition of KKM by Kazakh Metals, the price of nickel was at the level where the processing of nickel ore by known and proven technologies was not considered economically feasible due to high processing costs. Therefore, the former owners of KKM sold their interests in KKM to Kazakh Metals at a price significantly below the estimated fair value to free itself from the debt obligations associated with the property. The former equity holders of KKM were not related parties. (See page F-14 of Exhibit A to this letter.)

Mr. Mark Wojciechowski

January 16, 2008

Page 6

| Form 10-Q for the Quarterly Period Ended June 30, 2007 |

| Notes to Condensed Consolidated Financial Statements, page 6 |

| Note 5 Other Assets, page 11 |

| 8. | We note your response to prior comment 15 and are unable to agree with your position. As such, we re-issue prior comment 15. |

The Company proposes to revise its financial statements and associated disclosures and appropriately expense stripping and other costs incurred while the Company is in exploration stage. For additional details please see Exhibit A to this letter.

Form 10-Q for the Quarterly Period Ended September 30, 2007

| General |

| 9. | Please note that comments one through five, and eight above, are also applicable to your |

The Company proposes to carry over all appropriate revisions to the annual report proposed herein to its quarterly report on Form 10-Q for the quarterly period ended September 30, 2007 to reflect comments one through five and eight above.

Condensed Consolidated Statements of Cash Flow, page 5

| 10. | Within your determination of ‘Net Cash from Investing Activities,’ you include an item identified as ‘Issuance of Shares.’ Please revise to present this item within the computation of ‘Net Cash from Financing Activities’ or tell us why you believe it is appropriate to include this item within investing activities. Please see paragraph 19 of SFAS 95 for further guidance. |

This was a typographical error that the Company will correct in its amendment to its quarterly report.

Thank you for your assistance in this matter. If you have any questions or require additional information, please contact me directly.

| Very truly yours, |

| POULTON & YORDAN |

| Richard T. Ludlow |

| Attorney at Law |

Exhibit A

Summary of proposed revisions to the Annual Report of Bekem Metals, Inc.

for the year ended December 31, 2006 on Form 10-KSB

I. Proposed Revisions in Response to Comments 3, 4 and 5

In response to comments 3, 4 and 5 of the staff’s comment letter dated November 30, 2007, the Company proposes revisions throughout Items 1 & 2 “Description of Business and Properties”, Item 6 “Management’s Discussion & Analysis” as appropriate, to remove terms such as “production”, “develop”, “development”, “mining/mineral operations”, “mining”, “operations” and similar terms and has replaced those statements with terms such as “explore”, “exploration”, “activities”, etc.

a) In Items 1 & 2, “Description of Business and Properties” the Company has made revisions to the following paragraphs:

| i) | paragraph 3 of “Company History” on page 3 of Exhibit A; |

| ii) | paragraphs 1 through 3 of “Title to Properties” beginning on page 8 of Exhibit A; |

| iii) | paragraph 2 of the “Kempirsai” subsection of “Geology and mineralization of deposits” on page 11 of Exhibit A; |

| iv) | paragraphs 1, 2, 5, 6 and 7 of the “Kempirsai” subsection of “History and current state of our deposits” beginning on page 12 of Exhibit A; |

| v) | paragraphs 1, 3 and 4 of “Processing” beginning on page 18 of Exhibit A; |

| vi) | paragraph 1 of the “Tax and Royalty Scheme in the Republic of Kazakhstan” on page 21 of Exhibit A; |

| vii) | the “Need for Additional Capital” risk factor on page 23 of Exhibit A; |

| viii) | the “Competition” risk factor on page 23 of Exhibit A; |

| ix) | paragraphs 2 and 5 of the “Foreign Operations” risk factor beginning on page 24 of Exhibit A; and |

| x) | the “Environmental Regulations” risk factor on page 25 of Exhibit A. |

b) In Item 6, “Management’s Discussion and Analysis” the Company has made revisions to the following paragraphs:

| i) | paragraphs 2 and 3 of the introductory paragraphs of “Management’s Discussion and Analysis” beginning on page 27 of Exhibit A; |

| ii) | the “General and Administrative Expenses” paragraph on page 28 of Exhibit A; |

| iii) | the “Exploratory Costs” paragraph on page 28 of Exhibit A; |

| iv) | the “Total Operating Expenses and Loss from Operations” paragraph on page 29 of Exhibit A; |

| v) | we added a paragraph discussing “Interest Income”, see page 29 of Exhibit A; |

1

| vi) | paragraphs 1, 3 and 5 of “Liquidity and Capital Resources” beginning on page 30 of Exhibit A; |

| vii) | the introductory paragraph to “Plan of Operations” on page 31 of Exhibit A; and |

| viii) | footnotes 2 and 3 to the “Summary of Material and Contractual Commitments” table on page 33 of Exhibit A. |

c) In the Consolidated Financial Statements and Notes the Company has made the following revisions:

| Consolidated Financial Statements |

| i) | the Company has added a separate cumulative column “For the period from March 5, 2004 (Date of Inception) through December 31, 2006” to the Consolidated Statements of Operations and the Consolidated Statements of Cash Flows, see pages F-5 and F-7 of Exhibit A. |

| Note 1 |

| i) | the Company deleted the paragraphs entitled “Kempirsai Production Stage” and “Gornostai Exploration Stage” and replaced it with a paragraph entitled “Exploration Stage Company” on page F-9 of Exhibit A; |

| ii) | the “Revenue Recognition” paragraph on page F-10 of Exhibit A; |

| iii) | paragraphs 1-3 of “Depreciation, Depletion and Amortization” on page F-11 of Exhibit A; |

| iv) | paragraphs 1-3 of “Mineral Property Rights” on page F-11 of Exhibit A; and |

| v) | the Company has added a paragraph entitled “Exploratory Costs” beginning on page F-11 of Exhibit A. |

II. Proposed Revisions in Response to Comments 8

In response to staff comment 8, the Company has revised Item 6 “Management’s Discussion and Analysis” and its Consolidated Financial Statements and Notes as follows:

| Management’s Discussion and Analysis |

| i) | as noted in our response to the September 6, 2007 letter, we have removed “Stripping Costs” from “Critical Accounting Policies.” |

2

Consolidated Financial Statements and Notes

| i) | inventories and stripping costs previously recognized as assets have now been expensed. Incidental sales previously reported as Revenues were reclassified to Exploratory costs. The Consolidated Balance Sheets, the Consolidated Statements of Operations, the Consolidated Statements of Shareholders’ Equity (Deficit), the Consolidated Statements of Cash Flows and Notes have been corrected accordingly. See Consolidated Financial Statements and Notes beginning on page F-4 of Exhibit A. |

The full text of the proposed revised Items 1 & 2 “Description of Business and Properties”, Item 6 “Management’s Discussion and Analysis” and the Consolidated Financial Statements and Notes is provided below.

PART I

Items 1 & 2. | Description of Business and Properties |

Company History

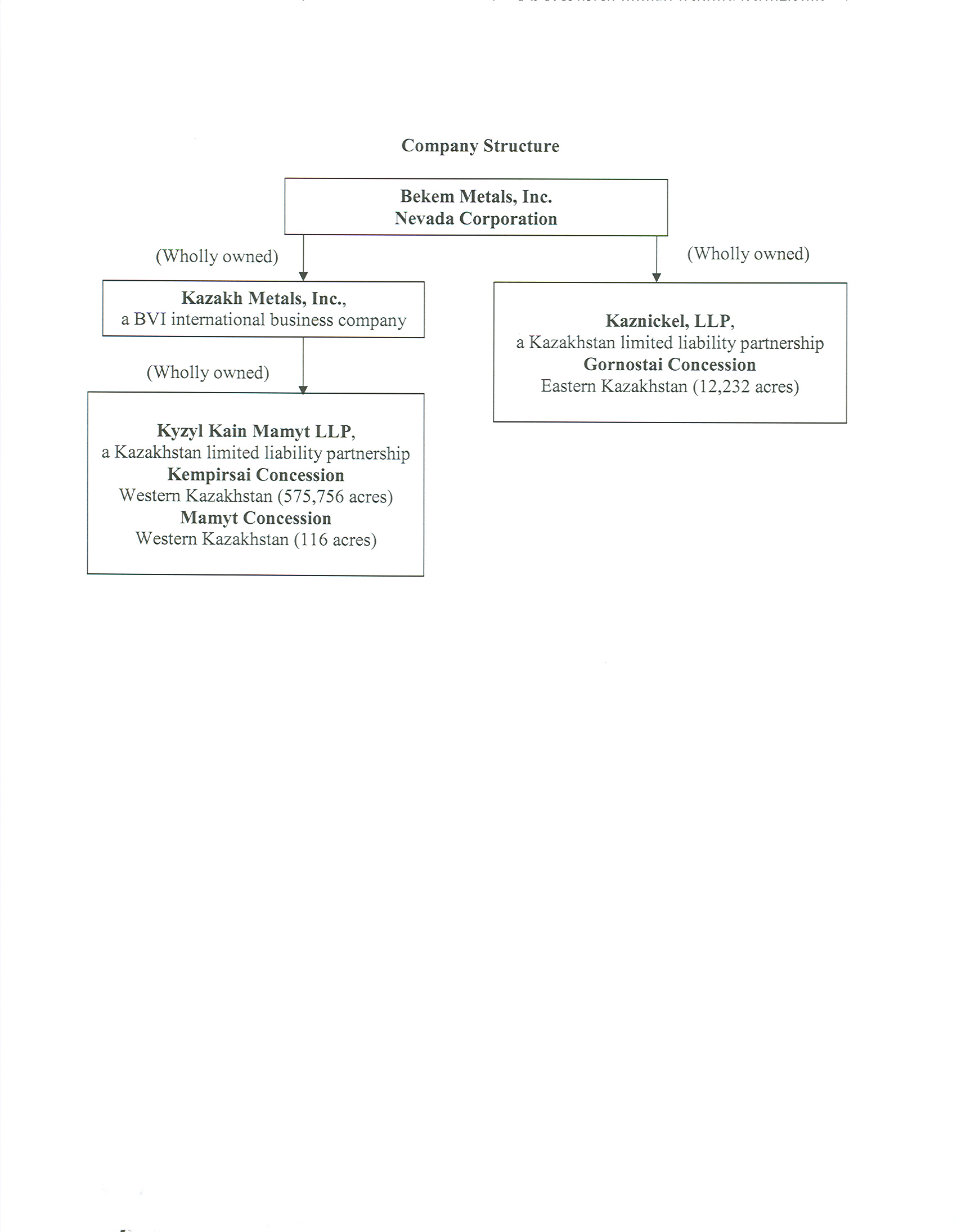

Bekem Metals, Inc., (hereinafter referred to as “us,” “we,” the “Company” or “Bekem”) is engaged in the exploration of nickel, cobalt and brown coal in the Republic of Kazakhstan.

We incorporated in the state of Utah under the name EMPS Research Corporation on January 30, 2001. Until the end of the 2004 fiscal year, our primary business focus was the development, marketing and licensing of our patented technology for use in commercially separating nonmagnetic particulate material by building and testing a high frequency eddy-current separator (“HFECS”).

We changed our name to Bekem Metals, Inc., on March 16, 2005 following our acquisition of Condesa Pacific, S.A., a British Virgin Islands international business company, and its wholly owned subsidiary Kaznickel, LLP in January of 2005. With the acquisition of Kaznickel, our primary business focus shifted from the development of our HFECS technology to exploring for nickel and cobalt in Kazakhstan. On July 24, 2006 Condesa transferred its interest in Kaznickel to Bekem, making Kaznickel a wholly-owned subsidiary of Bekem. On October 1, 2006 Bekem sold Condesa to a third party for nominal value.

The primary asset of Kaznickel is an exploration and production concession issued by the government of the Republic of Kazakhstan which grants Kaznickel the exclusive right, through February 2008, unless extended, to explore for nickel, cobalt and other minerals in a 12,232 acre area in northeastern Kazakhstan known as the Gornostayevskoye (“Gornostai”) deposit. The concession further provides that if we make a commercial discovery of nickel, cobalt or other minerals within the concession territory, we can apply for and receive the exclusive rights to commercially produce and sell nickel and cobalt ore through February 2026.

On October 24, 2005 we acquired Kazakh Metals, Inc. (“KMI”), and its wholly owned subsidiary Kyzyl Kain Mamyt (“KKM”), LLP in exchange for 61,200,000 shares of our common stock. KKM holds the exclusive subsoil use contract to extract and process nickel and cobalt ore from its Kempirsai deposit, which is comprised of the Kara-Obinskoye, and Stepninskoye sections (collectively referred to as the “Kara-Obinskoye section”) and Novo-Shandashinskoye

3

section, and brown coal from its Mamyt deposit. Unless otherwise indicated by the context of the disclosure, the Kara-Obinskoye section, the Novo-Shandashinskoye section and the Mamyt deposit are collectively referred to herein as the “Kempirsai deposit.” Under the applicable accounting reporting rules, KMI was considered the accounting acquirer.

Business of the Company

The Nickel Market

According to United States Geological Survey (“USGS”) the world mine reserves of nickel and the world mine reserves base of nickel in 2006 were 64 million tons and 140 million tons, respectively. In 2006 total nickel production was approximately 1,550,000 tons. Russia was the largest producer of nickel in the world with a 20% market share, followed by Canada with 15%, Australia with 12%, and Indonesia with 9%.

There is some debate in the market as to whether nickel prices will continue to increase. In 2006 the average price for nickel was about $24,287 per ton, up from $14,372 in 2005. The average London Metal Exchange (“LME”) price for nickel in January 2007 was $36,811 per ton.

There are several factors that can affect the overall worldwide nickel demand and prices in the future, which include the following:

4

| • | Expansion of new nickel mining capacity; |

| • | New processing technologies; |

| • | Stainless-steel worldwide demand. |

There are a number of new nickel mining projects that are projected to meet demand over the next five years. The Brazilian CVRD (former INCO) has been constructing a laterite mining complex at Goro near the southeastern tip of New Caledonia. It is anticipated that the New Caledonian nickel will be recovered onsite using pressure acid leaching technology. Australia’s leading nickel producer, BHP Billiton, is also developing a large laterite deposit near Ravensthorpe, Western Australia. Several other companies are considering employing some form of acid leaching technology to recover nickel in Cuba, Guatemala and the Philippines. The USGS has reported, however, that some nickel consumers are concerned that the global demand for nickel could outstrip supply before new mining projects can be completed. At least five automobile manufactures plan to use nickel-metal hydride batteries to power their gasoline-electric hybrid vehicle for the 2008 and 2009 model years, which would lead to a significant increase in nickel demand.

According to CRU Strategies, an independent business analysis and consultancy group focused on the mining, metals, power, cables, fertilizer and chemical sectors, the compounded annual growth rate (“CAGR”) of primary nickel consumption in the last 5 years was 4.1%. In the next five years the CAGR is expected to grow strongly up to 4.3% annually. Increasing world consumption of stainless steel is being driven in large part by China’s continued rapid economic expansion. Strong economic growth in the rest of the world will also support nickel consumption. The CRU Strategies analysis indicates that over 320,000 tons more primary nickel will be required by 2011 compared with 2006, and that supply and demand of primary nickel would be evenly matched in the next five years if the industry developed laterite ore bodies, especially limonite deposits utilizing high pressure acid leach technology.

Stainless-steel production, the single largest end use market segment of nickel, is expected to grow steadily in the next five years, relying heavily on the primary nickel supply for its expansion. Of course, high nickel prices force some steel mills to substitute chromium and manganese in place of nickel; while this lowers the cost of producing, it also lowers the corrosion-resistance of the steel. This lower-quality steel is used mainly in consumer applications where the low price of the final product is more important than corrosion resistance. Resistance to corrosion makes nickel an essential element both in alloys and as a catalyst. For aerospace, electric power and petrochemical industries, this resistance to corrosion is essential, as well as for use in gray-iron castings to toughen the iron, promote graphitization and improve machineability.

5

Our Properties

As discussed above, through our subsidiaries, we hold the rights to the Kempirsai nickel, cobalt and brown coal deposits, which are located in northwestern Kazakhstan and the Gornostai nickel and cobalt deposit located in northeastern Kazakhstan.

6

Location and access to our properties

The Kempirsai deposit is located in the Khromtausky region of northwestern Kazakhstan, approximately 130 kilometers northeast of Aktobe, Kazakhstan. The nickel and cobalt deposits are located approximately 35 kilometers south of Badamsha village, Aktobe region, Kazakhstan and the brown coal deposit is located approximately 30 kilometers east of Badamsha village, Aktobe region, Kazakhstan. Badamsha is a village of approximately 6,000 people. The Aktubinsk-Karabutak asphalt highway runs within 14 kilometers to the south of the nickel and cobalt deposit. The nickel, cobalt and brown coal deposits can be accessed through a network of country roads. The Orsk-Kanadagash state railway runs nearby the Kempirsai deposit and, through our subsidiary KKM, we own 55 kilometers of our own railway. Our railway connects the Kempirsai deposit to a reloading station and to a Russian railway.

7

The Gornostai deposit is located in the Beskaragaiskiy region of northeastern Kazakhstan, approximately 110 kilometers west of Semey, Kazakhstan and 30 kilometers east of Kurchatov, Kazakhstan. The Gornostai deposit is divided into the South and North sections by the navigable Irtysh River. The Gornostai deposit may be accessed by an asphalt highway that crosses the northern part of the South section of the deposit. The Semey-Astana railway also passes through the northern part of the South section of the deposit.

Title to Properties

We hold several subsoil use contracts that grant us the right to explore for and extract nickel, cobalt and brown coal at the Kempirsai deposit. We also hold an subsoil use contract that currently grants us the right to explore for nickel, cobalt and other minerals within the Gornostai deposit. Upon discovery of commercially producible reserves we can apply to move to commercial production. For additional information regarding our contracts please see the following table.

8

Territory | Size of | Primary Minerals | License | License or | License and |

|

|

|

|

|

|

Kempirsai | 575,756 acres | Nickel and cobalt ore | Production | MG #420 | Expires Oct, 12, 2011 unless |

|

|

|

|

|

|

Mamyt | 116 acres | Brown coal | Production | MG #9-D | Expires Dec, 11 2018 unless |

|

|

|

|

|

|

Gornostai | 12,232 acres | Nickel and cobalt ore | Exploration | 1349 | Exploration period expires |

The Kempirsai deposit was discovered and actively explored during the Soviet era. In the 1980s, the State Reserves Committee approved the reserves (based on Soviet standards) and approved the Kempirsai deposit for commercial production. The Kempirsai deposit was actively mined during the 1980s and early 1990s. Active mining at the Kempirsai deposit ceased in 1996. The working program associated with these licenses for the Kempirsai nickel, cobalt and Mamyt brown coal deposits are production contracts, those contracts do not require us to undertake significant exploration activities. While we do not have fixed exploration obligations, in order to retain our licenses we are required to engage in certain activities. For details regarding our minimum mine production requirements see “Working Programs of our Subsidiaries” in this Item 1 & 2 “Description of Business and Properties.”

The subsoil use contract to the Gornostai deposit was issued in February 2004. At the time it was issued, the Ministry of Energy and Mineral Resources of the Republic of Kazakhstan (the “MEMR”) determined that additional exploration of the deposit was necessary to determine the existence of commercially producible mineral reserves. Therefore, the subsoil use contract provides a period for exploration. Under the terms of the contract for the Gornostai deposit, we were granted the right to explore for nickel and cobalt for two years. The exploration term provides for two two-year extensions upon our request. We requested and were granted our first extension, extending the current exploration period to February 2008. Upon discovery of commercially producible nickel and/or cobalt reserves, we may notify the MEMR and convert from exploration stage to commercial production stage. If we make no commercial discoveries before the end of the exploration period, as extended, our rights to the territory will revert back to Republic of Kazakhstan. Upon completion of exploration, we will return to the Republic of Kazakhstan the rights to all areas within the licensed territory wherein no commercial discoveries of nickel and/or cobalt were made.

When we complete exploration of the Gornostai deposit, assuming we make commercial discoveries, we will apply to the MEMR to move to commercial production. At that time we will be required to pay a 0.1% commercial discovery bonus based on the initial determination of our mineral resources by the MEMR.

9

The term of each of our subsoil use contracts vary. Under our contracts we have the right to negotiate with the MEMR for extensions of the terms of those contracts. If we are unsuccessful in negotiating extensions, upon the expiration of those contracts our interest in and rights to those properties terminates and reverts back to the government of the Republic of Kazakhstan, but we retain the rights to all tangible and intangible assets we acquire for exploration, extraction and production at these deposits.

All of our subsoil use contracts are currently in good standing. Retention of our contracts, however, is contingent upon our complying with our annual minimum work program requirements and other subsoil use contract obligations. If we fail to satisfy our annual minimum working program requirements we could be subject to fines and penalties or even to the potential forfeiture of our contracts and all rights we have thereunder.

Under the terms of our subsoil use contracts we are required to provide industrial training to our employees in an amount not less than 1% of the total minimum work program expenses we incur each year.

For additional details regarding the terms and obligations associated with our subsoil use contracts and licenses please see “Tax and Royalty Scheme in the Republic of Kazakhstan” and “Working Programs of our Subsidiaries” in Item 1 & 2 “Description of Business and Properties”, “Summary of Material Contractual Commitments” in Item 6 “Management’s Discussion and Analysis” and “Note 4 – Property, Plant and Mineral Interests”, “Note 9 – Asset Retirement Obligation” and “Note 12 – Commitments and Contingencies” contained in the Notes to our Consolidated Financial Statements.

Working Programs of our Subsidiaries

For us to maintain our rights to the Kempirsai and Gornostai deposits we must satisfy the work program requirements of the MEMR for each property. Each year we must submit a proposed annual work program under each subsoil use contract or license to the MEMR. This annual work program must be reviewed and approved by the MEMR. The current work program under our KKM contracts and licenses calls for KKM to extract the following amounts of ore from the Kempirsai deposit and brown coal from the Mamyt deposit:

| Tons of Ore | Tons of Brown Coal |

2006 | -0- | 20,000 |

2007 | 175,000 | 60,000 |

2008 | 350,000 | 200,000 |

2009 | 1,000,000 | 200,000 |

2010 | 1,000,000 | 200,000 |

2011 | 1,000,000 | 200,000 |

2012 |

| 200,000 |

2013 |

| 200,000 |

2014 |

| 200,000 |

2015 |

| 200,000 |

2016 |

| 200,000 |

2017 |

| 200,000 |

2018 |

| 200,000 |

10

Under our 2006 work program for Kaznickel, we were required to drill at least 17,498 meters on the Gornostai deposit. We drilled only 12,652 meters during 2006. We have been successful in negotiating an amendment to our work program with the MEMR to allocate the balance of the 4,846 meters to the drilling program for 2007. Our total drilling requirement for the 2007 calendar year is 12,961 meters. Through February 2007, we have drilled a total of 5,990 meters.

Should we fail to complete the minimum work program in any year, the MEMR could review the work program, request an update and amendment to the work program, impose fines and penalties upon us or even revoke our subsoil use contracts and licenses.

Geology and mineralization of our deposits

Kempirsai

As mentioned above, the Kempirsai nickel and cobalt deposit is comprised of two deposits: Kara-Obinskoye, and Novo-Shandashinskoye. These deposits are located approximately 5-10 kilometers from each other. The results of exploration carried out during the Soviet era show that nickel and cobalt ore is located within the Kempirsai deposit ultramafic massif. The minerals are found in laterite form and are associated with leached nontronized serpentinites. The ore bodies have a blanket-like shape and tend to lie conformably on the underlying rocks. The depth of ore bodies from the surface is 0-40 m. In vertical section they are mainly horizontal in attitude and show variable thickness. Thickness varies from 2.0 meters to 30.0 meters, with an average thickness of 6.0 meters. Average stripping ratio is 1.5 cubic meters per ton. The nickel content of the ore within the Kempirsai deposit varies from 0.8% to 3.0% and cobalt – from 0.025% to 0.08%. The average nickel and cobalt content for the Kara-Obinskoye are 1.1% and 0.066% respectively. The average nickel and cobalt content for the Novo-Shandashinskoye deposit are 1.38% and 0.045%.

The ore reserves of the Kempirsai deposit were evaluated during the Soviet era based on Soviet standards. The Soviet standards, however, are not consistent with the standards established by the United States Securities and Exchange Commission (“SEC”). Therefore, consistent with SEC Industry Guide 7, we have included no claims as to the ore reserves that may be contained within the Kempirsai deposit. Until such time as we establish commercially producible reserves within the Kempirsai deposit you should consider the Kempirsai project to be exploratory in nature. The Kempirsai deposit is currently being evaluated by Wardell Armstrong, a qualified independent engineering firm. We anticipate they will issue a preliminary report during the second quarter 2007. For additional information regarding reserves please see “Reserves” in this Items 1 & 2 “Description of Business and Properties.”

11

Gornostai

Exploration activities conducted during the Soviet era and by us since we acquired the rights to the deposit have identified 21 ore bodies through drilling within the South section of the deposit and two ore bodies in the North section. The area of the deposit is located within the Gornostai ultramafic belt. The area of deposit is characterized by three distinct zones of ochre, nontronite, and leached and disintegrated serpentinite:

| • | Ochre zone represents the upper part of the serpentinite weathered crust. |

| • | Nontronite zone is more widespread than the ochre zone with thickness varying from 2 up to 10 m (sometimes reaching 30 m) |

| • | Zone of leached and disintegrated serpentinite is the most widespread amongst the three zones. The zone mean thickness is 15-20 m (in some cases up to 50 m). |

The minerals are found mainly in laterite form. The ore bodies have embedded form, are mainly horizontal in attitude and show variable thickness. The nickel content in the ore bodies varies from 0.7% to 2.3% and cobalt from 0.05% to 0.37%. The ore bodies are typically located at depths between 0 to 20 meters from the surface, allowing from strip mining. The lengths of the ore bodies range from 200 meters to 4,050 meters and widths range from 200 meters to 2,000 meters. Thickness varies from 0.8 meters to 15 meters. Average ore body thickness is around 4.2 meters, with an estimated average stripping ratio of 1.8 cubic meters per ton. Of the drilling done to date, the average content of nickel is 0.85% and cobalt 0.059%.

Based on the exploration activities undertaken on the deposit, we believe the size of the ore bodies, their simple form and shallow bedding will allow the deposit to be mined by open pit method with a low stripping ratio.

Despite the exploration work completed during the Soviet time and by us since acquiring this deposit, we do not have a current ore reserve estimate for the Gornostai deposit that complies with the standards established by the SEC. Accordingly, and consistent with SEC Industry Guide 7, we provide no claims as to the ore reserves that may be contained within the Gornostai deposit. Moreover, because we are currently in the exploration stage of our contract and have not yet established commercially producible reserves, the Gornostai project should be deemed exploratory in nature. This deposit is currently being evaluated by Wardell Armstrong. We expect Wardell Armstrong will complete their evaluation and issue their preliminary report during the second quarter of 2007. For additional information regarding reserves please see “Reserves” in this Items 1 & 2 “Description of Business and Properties.”

12

History and current state of our deposits

Kempirsai

The KKM subsoil use contract to the nickel and cobalt deposits covers a 575,756 acre territory, in northwestern Kazakhstan. This contract was issued by the MEMR and incorporates License series MG#420 and MG#426. These licenses to the nickel and cobalt deposits cover a period expiring on October 12, 2011. This contract may be extended upon agreement between KKM and the MEMR. KKM also holds a subsoil use contract that incorporates License series MG #9-D for a brown coal deposit located within 40 kilometers of its nickel and cobalt deposit. This contract expires on December 11, 2018 with the possibility of further extensions.

Historical exploration and production activities

Deposits in the area of the Kempirsai deposit were first discovered in the 1930s. The Kempirsai deposit was discovered in 1938 and explored during the Soviet era. During the late 1970s the Kara-Obinskoye and Novo-Shandashinskoye sections were explored by core drilling on a 12.5-25m x 25m grid. The volume of exploration works done on the deposits were as follows:

Deposit |

| Number of Holes |

| Meters |

| Samples |

|

|

|

|

|

|

|

Kara-Obinskoye |

| 4,498 |

| 79,400 |

| 46,490 |

Novo-Shandashinskoye |

| 780 |

| 7,770 |

| 6,135 |

The State Reserves Committee approved the Kara-Obinskoye and Novo-Shandashinskoye reserves for commercial production in the 1980s. These deposits, along with others in the region, were assigned to YuzhUralNickel during the Soviet era. YuzhUralNickel is a Russian company with a nickel processing plant in Russia located approximately 90 kilometers north of the Kempirsai deposit. Approximately 171 million tons of nickel ore have been mined from deposits in the area where the Kempirsai deposit is located, including 770,000 tons from the Kara-Obinskoye and Novo-Shandashinskoye sections of the Kempirsai deposit. During peak production in the late 1980s, almost five million tons of ore were mined annually from the Kempirsai deposit. Active mining of the Kempirsai deposit was discontinued in 1996.

The Kempirsai deposit remained the property of YuzhUralNickel after the break up of the Soviet Union until 1996, when a joint venture between YuzhUralNickel and the Kazakhstan State Property Committee was formed. Because of a lack of Russian interest in developing this deposit in Kazakhstan, the joint venture was unsuccessful. In 1999 the rights to the Kempirsai and Mamyt deposits were acquired by KKM from the joint venture. Due to a lack of funding and processing capability, combined with market conditions and the nickel content of Kempirsai ore, KKM has not engaged in active or significant mining activity since acquiring the deposits.

13

Historically, the Kempirsai deposit was open-pit mined, with maximum mining depths of approximately 20 meters. We anticipate that the Kempirsai deposit will be open-put mined in the future.

Plant, equipment and infrastructure

KKM owns fuel tanks, locomotives, rail cars, railway cranes, bridge cranes, railway cisterns, maintenance equipment, excavators, motor graders, passenger vehicles, passenger buses, heavy dump trucks, hoppers, scales, lathes, forging hammers, presses, grinding, milling and boring machines, boilers, electrical substations, office equipment, business machines, portable communication equipment, laboratory equipment and multiple buildings. The machinery was manufactured between 1950 and the present. The buildings were built between the 1940’s and the early 1990’s. Our equipment and infrastructure in its current state has the capacity to mine approximately 250,000 tons of ore annually. Much of our existing equipment and buildings will need repair and refurbishing prior to being put into active operation. We estimate the cost of these repairs to be approximately $1,000,000. Once repaired, we expect our infrastructure and equipment to have a standing capacity to mine up to 500,000 tons of ore annually.

In addition to the rail and road infrastructure discussed above, 220 and 110 kilovolt high voltage power lines run nearby the Kempirsai deposit and the Buhara-Ural gas pipeline runs approximately 10 km to the east of the Kempirsai deposit, (see “Kempirsai Project Location Map” included in “Location and access to our properties” in this Item 1 & 2 “Description of Business and Properties.”) We can access water from the lakes around Badamsha. In the future, we also plan to use coal from our Mamyt deposit to supply power for an ore processing plant.

Costs

Since acquiring the rights to the Kempirsai deposit in 1999, KKM has expended approximately $14,000,000 million at the Kempirsai deposit, including approximately $5,500,000 from the date we acquired KMI in October 2005 through December 31, 2006. We anticipate future planned costs to be up to $600 million, depending on technology and capacity of the processing plant we plan to build at the Kempirsai deposit as discussed herein greater detail in the “Processing” section of this Item 1 & 2. “Description of Business and Property.” We plan to spend approximately $3.4 million in 2007, depending on ore sells, in the further development of the Kempirsai deposit and in the “Plan of Operations” section of Item 6. “Management’s Discussion and Analysis.”

Gornostai

In February 2004, Kaznickel acquired a concession for exploration and development of the Gornostai nickel and cobalt deposit (contract No. 1349 registered by the MEMR), covering 12,232 acres in eastern Kazakhstan.

14

We are at the exploration stage on the Gornostai deposit. This deposit was discovered in 1958. From 1960 to 1968 a series of geological and prospecting surveys and evaluation work was performed on both sections of the deposit by the Semipalatinsk Expedition to evaluate available nickel and cobalt ore reserves. The surveys identified and explored 21 ore bodies on the South section and two ore bodies on the North section of the deposit. These exploration works tested the deposit to depths of around 50-75 meters in the South section and up to 150 meters in the North section.

In the South section, drilling was undertaken on a 200-400 meter x 100-200 meter grid. In total 2,067 shallow depth holes with a total length of about 60,000 m and several deep holes with a total length of 2,857 meters were drilled. 48 pits varying in depth between 4.3 – 24.6 meters (570 meters in total) were explored around drill hole to check core sample results. In 1965 two pits were explored for metallurgical samples. Sample weights were 1.3 and 3.6 tons. Samples were tested at the VNIITzvetmet Institute in Ust-Kamenogorsk, Kazakhstan.

In the North section, drilling was undertaken primarily on a 1600 meter x 400 meter grid. Ore bodies of significant thickness, up to 40 meters, with nickel content up to 3.64% (average 1.55%) were identified. These deposits were located at depths between 40-90 meters.

The Gornostai deposit was abandoned, however, as reserves around Norilsk in Russia were considered more attractive because of larger reserves and higher nickel content. Moreover, the Norilsk reserves were already at the production stage. In addition, a Soviet army nuclear test site, similar to the Nevada Test Site, was located near the Gornostai deposit. The surrounding territory, including the deposit, was considered a secret military zone. For these reasons, further exploration of the deposit was discontinued in 1968.

The last nuclear testing in the area was conducted more than 15 years ago. Recent tests show that the radiation levels in the soil, water and air are within normal ranges.

Exploration activities

Since acquiring Kaznickel, consistent with the terms of the current three-year work program for the deposit approved by the MEMR in 2005, we have engaged in exploration activities within the Gornostai licensed territory to determine the characteristics of this deposit. During 2006 we drilled 488 holes to a total depth of 12,652 meters, and an average depth of 30 meters per hole, and have taken 6,755 geochemical and core samples to CenterGeoAnalit LLP, a nationally accredited independent laboratory located in Karaganda, Kazakhstan, to perform spectrum and quantity analysis to identify the content of nickel, cobalt and iron. During 2005 we drilled 42 holes to a total depth of 1,065 meters, and an average depth of 30 meters and have taken 595 samples to the Institute of Nonferrous Metals, located in Oskemen, Kazakhstan. Under the three-year work program, we are required to drill an additional 12,961 meters in 2007. In addition to the drilling works that have been completed, a small area of the Gornostai deposit was strip mined in 1991.

15

As discussed above, currently the exploration stage of our license runs through February 2008. We have the option to extend exploration stage through December 31, 2009. During the exploration stage we are required to engage in certain activities to determine the existence of commercially producible mineral reserves. We have planned the following exploration activities for 2007, which we believe will be sufficient to both satisfy our minimum work program requirements and to help us establish commercially producible reserves within the Gornostai deposit. Once we establish commercially producible reserves, we plan to move to commercial production at the Gornostai deposit.

Activity |

| Quantity |

| Anticipated Timetable |

| Estimated Cost |

|

|

|

|

|

|

|

|

|

Core drilling South section including mobilization/ demobilization |

| 15,000 meters |

| January 2007 through |

| $1,315,000

|

|

|

|

|

|

|

|

|

|

Core drilling North section |

| 700 meters |

| June 2007 through |

| $62,000 |

|

|

|

|

|

|

|

|

|

Pits for checking drilling results |

|

|

| July 2007 through |

| $51,000 |

|

|

|

|

|

|

|

|

|

Core sampling |

| 8,700 samples |

| January 2007 through |

| $42,000 |

|

|

|

|

|

|

|

|

|

Survey, hydrology and engineering |

|

|

| March 2007 through |

| $58,000 |

|

|

|

|

|

|

|

|

|

Core preparation |

| 8,900 samples |

| January 2007 through |

| $52,000 |

|

|

|

|

|

|

|

|

|

Assaying and metallurgical tests |

| 9,000 samples |

| February 2007 through |

| $135,000 |

|

|

|

|

|

|

|

|

|

Interpretation of exploration results and preparation of the report and reserve estimate for submission to the State Reserves Committee (“SRC”) |

|

|

| July 2007 through |

| $50,000 |

|

|

|

|

|

|

|

|

|

Approval of report and reserve estimate by SRC |

|

|

| April 2008 to |

| $0 |

|

|

|

|

|

|

|

| |

We have retained three local drilling contractors, SemGeo LLP, Topaz and Tomai-Burservice to perform core drilling activities. Each of these drilling contractors holds a state license to provide services as a drilling contractor and has years of drilling experience in the local market.

16

Core sampling, core logging and results interpretation will be carried out by our own in-house geologists, who have 10-30 years experience in such activities. Core preparation will be conducted by the preparation laboratory of SemGeo LLP, a third party with years of experience in the local market. Assaying will be done by CenterGeoAnalit LLP.

Core sampling, assaying and quality assurance/quality control

Core sampling will be conducted over the full length of the hole. In general, sample intervals will be 1-2 meters, which will produce 2-5 kilograms of sample from each interval. The core will not be cut because the rocks are fractured. Samples will be undertaken of the whole core.

All sample preparation will be done at the SemGeo LLP laboratory, which is located approximately 120 kilometers from the Gornostai deposit. Whole core samples are sent to SemGeo in 2-5 kilogram labeled Hessian bags which are stacked in racks and dried at approximately 90° C. Samples are then sent to a small jaw crusher that reduces the whole sample to 4-5 millimeters. The sample is then sent to a roll crusher where it is reduced to 1-2 millimeters. The equipment is cleaned with compressed air between samples. Samples are then split by cone and quartering with opposite quadrants combined before being sent to the disc grinder where the sample is reduced in size to 74 micrometers. Every fifth sample is checked by sieving to see if it complies with this grain size. As an additional check, every thirtieth sample is waste rock to act as a “blank” control.

From the sample preparation facility, approximately 60 grams of pulverized sample will be sent to the CenterGeoAnalit LLP laboratory for assay, while the pulps are kept at the sample preparation facility. Assaying includes the quantitative determination of the main ore components, including nickel, cobalt and iron.

Composite samples will be produced to determine the chemical composition of slag-forming oxides, detrimental impurities and accompanying components in the ores. Composites are made up from three to five individual samples from one intersection by taking material from duplicates of analytical samples proportional to their length. The maximum weight of a composite sample will be 250 grams.

For quality control, each of 30 samples includes approximately 10% checks comprising of one blank, one duplicate and one standard. As standards, we use the certified Reference Samples from GEOSTATS PTY LTD (Australia). We have 11 standards with nickel grade varying from 0.02% to 1.51%. In the event an assay result of the Reference Sample shows >2 or <2 standard deviations from the accredited value, the whole batch will be re-assayed.

17

Submission of report and reserves estimate to the State Resources Committee

We will retain a third party to work with our in-house geologists to prepare the report and reserve estimate for submission to the State Resources Committee in connection with our application to move to the Gornostai deposit from exploration phase to commercial production phase. We have not yet selected a party to provide this service.

Infrastructure

In addition to the road and rail infrastructure discussed above, low tension power lines follow the railway are run within the Gornostai deposit. A high tension power line is located approximately 6-7 km to the south of the central part of the South deposit. We have access to water from Irtysh River. Unlike the Kempirsai deposit, there are no buildings and minimal equipment at the Gornostai deposit.

Costs

Since acquiring the rights to the Kempirsai deposit in February 2004, Kaznickel has spent approximately $3,000,000 in exploration activities at the Gornostai deposit. Of this amount, approximately $2,500,000 was spent from January 2005, when we acquired Kaznickel, to December 31, 2006. As with the Kempirsai deposit, we anticipate costs to be as high as $600,000,000, depending on capacity and technology of the type of processing plant we build at the Gornostai deposit as discussed herein greater detail in the “Processing” section of this Item 1 & 2. “Description of Business and Property.” We plan to spend approximately $1,800,000 in exploration activities within the Gornostai deposit during fiscal 2007. For additional details please see the “Plan of Operations” section of Item 6. “Management’s Discussion and Analysis”.

Processing

We currently have no processing facilities at either the Gornostai or Kempirsai deposits. Once we establish to existence of commercially producible reserves, we intend to construct a processing facility. Historically, pyrometallurgy has been the most common processing procedure utilized to process nickel and cobalt ores. Hydrometallurgical technology has improved to the point that it is now an acceptable alternative to pyrometallurgy for processing nickel and cobalt ores. Both technologies require large plants, costly construction and expensive equipment often requiring capital infusions of hundreds of millions of dollars.

The KMI acquisition gave us the rights to a proprietary technology for processing nickel and cobalt ores. While this technology has not previously been used to process nickel and cobalt ores, it is based on the same principles used to process titanium and other rare earth metals in Kazakhstan and Russia. The processing technique utilizes hydrogen chloride to leach out the nickel and cobalt ores with sublimation of the nickel and cobalt chlorides occurring at 1,050-1,100 (Degrees) Celsius. This technology utilizes a closed-circle utilization chamber, which results in no emissions while achieving extraction rates comparable to pyrometallurgy and hydrometallurgy.

18

The following table provides additional information regarding recovery rates and cost per ton of metal recovered associated with pyrometallurgical, hydrometallurgical and hydrochlorination plants:

| Pyrometallurgy | Hydrometallurgy | Hydrochlorination(1) |

|

|

|

|

Average nickel recovery rate(2) | 80% | 95-99% | 93% |

Average cobalt recovery rate( 2) | 75-80% | 90-95% | 85-88% |

Cost per ton of metal recovered | $8,000 | $4,000 | $5,000 |

(1) As this process is still in the research and development stage, all figures given are estimates based on the estimates calculated by the Mining Bureau, an independent third party research and development firm focused on mining and metallurgy in Kazakhstan. These estimates could vary materially if test works show the need for additional materials, equipment or processes needed to recover nickel and cobalt.

(2) Ore recovery rates are subject to a number of different factors, including processing techniques, ore characteristics, etc., which can cause rates of recovery actually realized to vary.

The following table provides a comparison of the estimated initial construction costs and time required to build pyrometallurgical, hydromettalurgical and hydrochlorination ore processing plants capable of processing 500,000 and 1,000,000 tons of head ore annually.

| Pyrometallurgy | Hydrometallurgy | Hydrochlorination(1) |

500,000 tons annually |

|

|

|

Initial construction cost | $100-150 million | $500-600 million | $100 million |

Estimated construction time | 24 months | 24 months | 24 months |

|

|

|

|

1,000,000 tons annually |

|

|

|

Initial construction cost | $250-$350 million | Over $650 million | $100 million |

Estimate construction time | 24-36 months | 36+ months | 24 months |

(1) As this process is still in the research and development stage, all figures given are estimates based on the estimates calculated by the Mining Bureau, an independent third party research and development firm focused on mining and metallurgy in Kazakhstan. These estimates could vary materially if test works show the need for additional materials, equipment or processes needed to recover nickel and cobalt.

We have constructed a pilot plant at our Kempirsai deposit to test our hydrochlorination process. Initially we had planned to complete the pilot plant and begin testing during the second quarter 2006. The pilot plant was completed in October 2006 and we began testing the mineral concentrating capability of our hydrochlorination processing technology at the pilot plant level in October 2006. The initial tests of the pilot plant used head ore from our Kempirsai deposit. The average nickel content of our Kempirsai head ore is approximately 1.1 percent per ton. PIT Geoanalitika, an independent Kazakh company, conducted chemical analysis of several different samples of the pilot plant concentrates and found that nickel content following the hydrochlorination process increased to 10 to 15 percent. We feel these initial results justify further research and development to optimize the process at the scale of a pilot plant with a view to employing the technology in commercial production in the future.

19

Our pilot processing plant has a processing capacity of 12.5 tons of ore per day. We processed an aggregate of 10 tons of ore through the pilot plant from October 2006 to January 2007. For reasons discussed in more detail below, we have processed no additional ore since January 2007.

Initially we estimated that we would need approximately six months to test our hydrochlorination process at the pilot plant level to determine its commercial viability. Testing, however, has progressed more slowly than initially expected due to a number of factors. First, the use of chlorides in the process and difficulties in getting isolation in the rotating kiln significantly enhances the potential risk to personnel and the environment, so we have had to proceed carefully. Second, because this process has not previously been used to commercially process nickel and cobalt, we have had to develop processes and procedures without the benefit of relying on others experience. Third, because of the use of chlorides and associated acids, the necessary equipment for the pilot plant has been difficult to design, locate and procure. Fourth, during the testing stage, following each test run we halt the pilot plant, disassemble the rotating kiln and test and replace the inner lining of the kiln to ensure the integrity of the equipment used in the process. Fifth, due to unusually harsh weather conditions at our Kempirsai deposit this winter, including up to 13 feet of snow and temperature as low as 31 to 40 degrees below zero Fahrenheit, we were forced to discontinue operations at the pilot plant in January 2007 and have not operated the pilot plant for testing of hydrochlorination since that time. The idle time at the pilot plant has been used to improve the inner lining of the rotating kiln to withstand the temperatures of more than 1,200 degrees Celsius, check and replace the pipes transporting the acids throughout the pilot plant facility, recheck, order and replace the heating and cooling system, and various other parts and blocks of the pilot plant and to investigate the possible acquisition of agglomeration and magnetic separation equipment.

Weather permitting, we plan to recommence testing at the pilot plant in April 2007. We have planned a series of tests designed to establish the economic feasibility of the processing technology and to formulate the required procedures, protocols and operational guidelines for commercial utilization of the hydrochlorination process. We expect this testing will be completed in the fourth quarter 2007 and have budgeted $200,000 for the cost of this testing and development.

Once we have completed these tests and analyzed the results, we will make a final determination as to the feasibility of our hydrochlorination technology for the commercial production of our deposits.

In light of the delays experienced to this point and the planned testing through the end of the 2007 fiscal year, coupled with the time requirements to build a commercial hydrochlorination processing plant, should the technology prove technically and economically feasible, we have been researching other options that might allow us to get to commercial production at Kempirsai more quickly. To this end, we have approached several leading design and metallurgy institutes to supply feasibility studies for a commercial processing plant utilizing pyrometallurgy as a main technology to produce ferronickel from our Kempirsai deposit.

20

We are considering proposals for the construction of a ferronickel pyrometallurgical commercial processing plant at the Kempirsai deposit. We anticipate the plant will be built in several phases. The first phase would include the construction of a plant with capacity to process up to 500,000 tons of head ore annually. Depending upon the success of the first phase of the plant, we would then have the option to increase the capacity to 1,000,000 tons of head ore processing capacity annually over several years. We anticipate this expansion would occur in additional phases. We have allocated $940,000 this year for pre-feasibility and feasibility studies upon which we can base a decision with regard to commencement of construction of phase one of a pyrometallurgical plant at the Kempirsai deposit. We expect to receive a detailed feasibility study within the next several months.

Irrespective of our decision regarding the feasibility of a pyrometallurgical processing plant at the Kempirsai deposit, we plan to continue testing and development of our hydrochlorination process as discussed above.

Reserves

We do not have a current estimate of the ore reserves contained within our concessions. While we have reserve estimates prepared during Soviet times, we do not know the accuracy of those reserve estimates and do not believe them to be to the standards established by the SEC. As disclosed herein, we are working with Wardell Armstrong, a qualified independent engineering firm, to provide us with a preliminary ore resource estimate of our deposits that will conform to the Australasian Joint Ore Reserves Committee (“JORC Code”). We anticipate this report will be completed during the second quarter 2007.

We anticipate that the preliminary Wardell Armstrong report will indicate that currently we have only ore resources. Under the SEC standard and the JORC Code, mineral deposits qualify as “reserves” only to the extent some part of the deposit can be economically and legally extracted or produced at the time of the reserve determination. At the present time, we do not know whether the ore in our deposits can be economically extracted or produced. For this purpose, we intend to retain an independent third party during 2007 to conduct a preliminary feasibility study to provide information on mining, processing, metallurgical, economic and other relevant factors to determine whether each of our deposits can be economically produced. We anticipate this preliminary feasibility study on the Kempirsai deposit will be undertaken in the second half of 2007 and should be completed sometime during the first quarter 2008. We expect a preliminary feasibility study on the Gornostai deposit will be undertaken some time in 2008. At the time these preliminary feasibility studies are conducted, we will ask Wardell Armstrong to conduct a follow up evaluation of our deposits consistent with SEC standards.

Because our deposits are without known reserves, you should consider our proposed programs to be exploratory in nature.

21

Tax and Royalty Scheme in the Republic of Kazakhstan

We are subject to the following taxes and royalties payable to the Republic of Kazakhstan:

Class of Tax or Royalty | Basis of Tax | Payable Period | Annual Rate |

Corporate Income Tax | Profits | Monthly | 30% |

Social Tax | Payroll | Monthly | 21-26% |

VAT | Value added | Monthly | 14-20% |

Property Tax | Property | Quarterly | 1% |

Royalty (ore) | Output volume | Monthly/Quarterly | 2.21% |

Royalty (brown coal) | Output volume | Monthly/Quarterly | 0.9% |

Excess Profit Tax | Net income | Annually | 4-60% |

Competition

Recent high prices for nickel and cobalt are the result of the growing demand from such economies, such as China and India, and certain industries, such as stainless steel, experienced a near 8% increase in demand in 2006 as compared to 2005. This spike in worldwide demand is not being met by current supply as the current capacity of nickel producers is limited and new plant commissions have been postponed several times. Also contributing to the price increase is the uneasy situation in New Caledonia and Indonesia, where the local populations have held protests at mines and plants, as well a series of strikes held in Canada at the CVRD and Xtrata owned properties. All of these issues have contributed to increased prices and historically low levels of the nickel held at LME-approved warehouses, reaching as low as 3,600 tons.

Cobalt prices have also reached as high as $66,000 per ton recently due to several factors. The main reason for the price increase is the deal between Norilsk Nickel, the world’s largest producer of nickel, and OM group. In exchange for selling OM’s plant in Finland to NorNickel, NorNickel has agreed to sell all of its produced cobalt to directly to OM, thus potentially limiting the volume of cobalt available on the market.

Total nickel production worldwide was approximately 1,550,000 tons in 2006, according to USGS. Norilsk Nickel is the largest nickel producer followed by CVRD, BHP Billiton Plc, Eramet Group and Xtrata. These five companies account for approximately 66% of the world’s primary nickel production, while more than 30 medium to small size companies produce the remaining 34%.

Until recently, there were no nickel-producing companies in Kazakhstan. In February 2004, Oriel Resources, a London-based company, acquired 90% of Muzbel LLC, which holds exploration and extraction rights for the Shevchenko nickel deposit in northern Kazakhstan. The Shevchenko Nickel Project Feasibility Study showed that proven and probable nickel laterite ore reserves were 104.4 million tons of 0.79% nickel.

22

In October 2006, Oriel Resources was acquired by IPH Polychrom Holding BV and Croweley International Limited. Based on the latest announcement, Oriel plans to develop its chrome deposit in Kazakhstan and review its plans for the Schevchenko nickel deposit in Kazakhstan.

Companies compete with each other generally across the globe and are best categorized by their size, reserve base, ore richness and production method, due to different extracting technologies applied, and the final product. Competition in this industry focuses largely on price and nickel content, whether it is sold in unwrought or chemical form. High nickel content material is sold at higher prices and is most sought after among customers.

We do not anticipate direct competition from Oriel Resources should they pursue the plan to build a nickel processing plant. Nickel and cobalt are part of a global market and a worldwide demand, in which the supply is limited and the number of industries that use nickel and cobalt is increasing, thus ensuring a constant demand for additional production of nickel and cobalt.

We believe that the proximity of our Gornostai deposit to China and other Asian countries will provide us a competitive advantage. We have already been approached by Chinese metal companies interested in purchasing finished product once we reach production stage. As of this date we have not entered into definitive negotiations with any party.

Risk Factors

Business Risks

Need for Additional Capital. Since focusing our efforts on nickel and cobalt exploration our capital resources have consisted almost exclusively of funds we have borrowed from related and non-related parties and from a private sale of our equity securities. In July 2006 we raised $28,000,000 through a private placement of our equity securities. As of December 31, 2006, we had cash on hand of $8,583,680. We believe this should be sufficient capital to fund our operations until the end of 2007. We currently have very limited capacity to generate revenue. Should we determine to pursue construction of an ore processing plant to produce ferronickel, we expect the cost to build a facility capable of processing 500,000 tons of head ore per year will be about $50,000,000 and the cost to construct an ore processing facility capable of processing 1,000,000 tons of head ore per year will range from $100,000,000 to $150,000,000. We will have very little ability to generate revenue until we build and begin operating this plant. We expect that it will be 2009 or later, if ever, before we have the ability to generate revenue sufficient to meet our operating needs. Therefore, we anticipate the need for substantial additional capital resources by the end of the 2007 fiscal year. And we expect to be totally dependent upon investment funds to support our operations until such time as we begin to generate sufficient revenue to fund operations. We expect these funds will consist primarily of funds raised in equity and/or debt financing activities. We currently have no firm commitment from any party to provide us additional equity or debt financing and there is no guarantee that we will obtain additional financing on acceptable terms, or at all. If we are unsuccessful in obtaining additional funding by the end of 2007, we will likely have insufficient funds to continue operations or to meet our minimum annual work program requirements. If we cannot fulfill our minimum work program requirement, we could be subjected to fines and penalties and even to the possible forfeiture of our subsoil use contracts and licenses.

23

Nickel and Cobalt Prices can be Volatile. Commodity prices for nickel and cobalt fluctuate according to the influence of diverse market conditions that can affect the supply or demand for a commodity such as political and economic conditions and uncertainties; advances in exploration and development technology; introduction of competing products; and governmental restrictions on exploration, production and export of natural resources.

Competition. Our principal competitors are large established companies with substantial financial resources and market share. If we establish commercially producible reserves and move to production stage, we will have to compete for customers with these companies.

New Technology. We are developing the proprietary technology. Although this technology has been used successfully to recover other metals, it has not been used in the commercial recovery of nickel and cobalt. We have completed construction of the pilot processing facility and continuing test operations to further establish the feasibility of the technology. There is no assurance that our pilot facility will operate as we expect. After testing of the pilot facility we will begin construction of a facility to process commercial quantities of ore. There is no assurance the technology operated in a test facility will scale to a commercial facility successfully or operate at expected extraction efficiencies and operating costs to support profitable commercial operation. In the event our technology does not work as expected, we will be required to construct a facility using other technology, which would increase our need for investment capital and would also increase our operating costs and breakeven point.

Failure to Satisfy the Terms of Our Subsoil Use Contracts. Under our subsoil use contracts, we are required to satisfy our annual minimum work program requirements. There is no guarantee that we will be able to continue to meet these commitments in the future. If we fail to satisfy these commitments we may be subject to penalties and fines and, potentially, to the loss of one or more of our subsoil use contracts. The cancellation of our contracts would have a material adverse effect on our business, results of operations and financial condition. Although we would seek waivers of any breaches or seek to renegotiate the terms of our commitments in the event we do not believe we can meet such commitments, we cannot assure you that we would be successful in doing so.

Foreign Operations. In recent years, the Republic of Kazakhstan has undergone substantial political and economic change. As an emerging market, Kazakhstan does not possess the well-developed business infrastructure that generally exists in more mature free market economies. As a result, operations carried out in Kazakhstan can involve significant risks that are not typically associated with developed markets. Instability in the market reform process could subject us to unpredictable changes in the basic business infrastructure in which we currently operate. Therefore, we face risks inherent in conducting business internationally, such as:

24

| • | Foreign currency exchange fluctuations or imposition of currency exchange controls; |

| • | Legal and governmental regulatory requirements; |

| • | Disruption of tenders resulting from disputes with governmental authorities; |

| • | Potential seizure or nationalization of assets; |

| • | Import-export quotas or other trade barriers; |

| • | Difficulties in collecting accounts receivable and longer collection periods; |

| • | Political and economic instability; |

| • | Difficulties and costs of staffing and managing international operations; and |

| • | Language and cultural differences. |

Any of these factors could materially adversely affect our business and financial condition. At this time, we are unable to estimate what, if any, changes may occur or the resulting effect of any such changes on us.

We also face a significant potential risk of unfavorable tax treatment and currency law violations. Legislation and regulations regarding taxation, foreign currency transactions and licensing of foreign currency loans in the Republic of Kazakhstan continue to evolve as the central government manages the transformation from a command to a market-oriented economy. The legislation and regulations are not always clearly written and their interpretation is subject to the opinions of local tax inspectors. Instances of inconsistent opinions between local, regional and national tax authorities are not unusual.

The current regime of penalties and interest related to reported and discovered violations of Kazakhstan’s laws, decrees and related regulations can be severe. Penalties include confiscation of the amounts at issue for currency law violations, as well as fines of generally 100% of the taxes unpaid. Interest is assessable at rates of generally 0.3% per day. As a result, penalties and interest can result in amounts that are multiples of any unreported taxes.

We may be adversely affected by Kazakh political developments, including the application of existing and future legislation and tax regulations.

Environmental Regulations. We are subject to stringent federal, state and local laws and regulations relating to the release or disposal of materials into the environment or otherwise relating to environmental protection. These laws and regulations may require the acquisition of permits before extraction activities commence, restrict the types, quantities and concentration of substances that can be released into the environment in connection with extraction and production activities and impose substantial liabilities for pollution resulting from our operations. Failure to comply with these laws and regulations may result in the assessment of administrative, civil and criminal penalties, incurrence of investigatory or remedial obligations or the imposition of injunctive relief. Changes in environmental laws and regulations occur frequently, and any changes that result in more stringent or costly waste handling, storage, transport, disposal or cleanup

25

requirements could require us to make significant expenditures to maintain compliance, and may otherwise have a material adverse effect on us as well as the industry in general. Under these environmental laws and regulations, we could be held strictly liable for the removal or remediation of previously released materials or property contamination regardless of whether we were responsible.