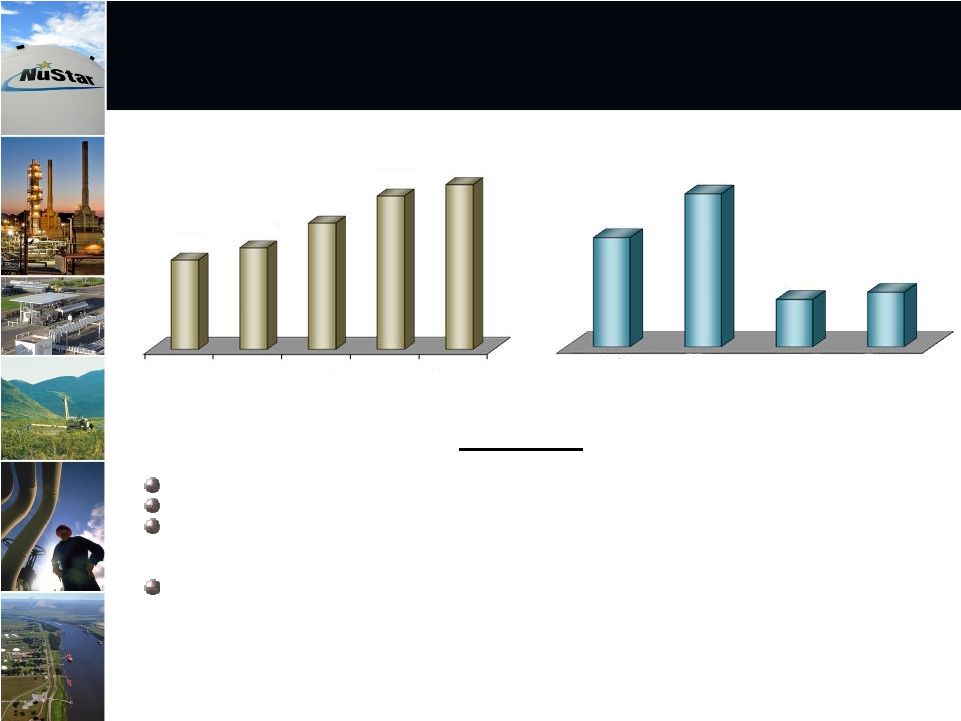

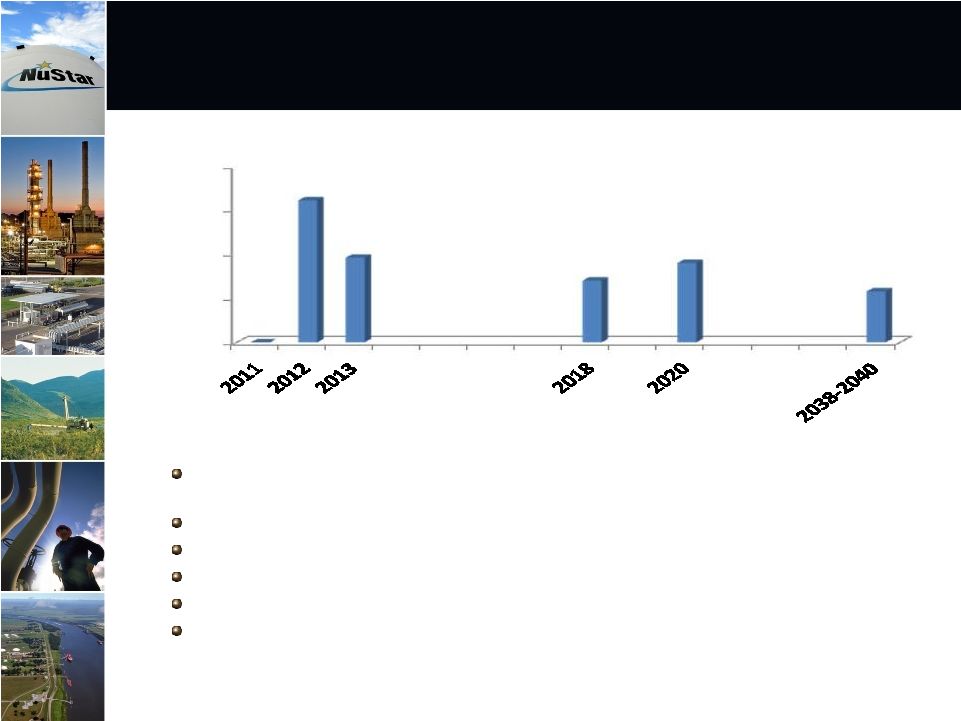

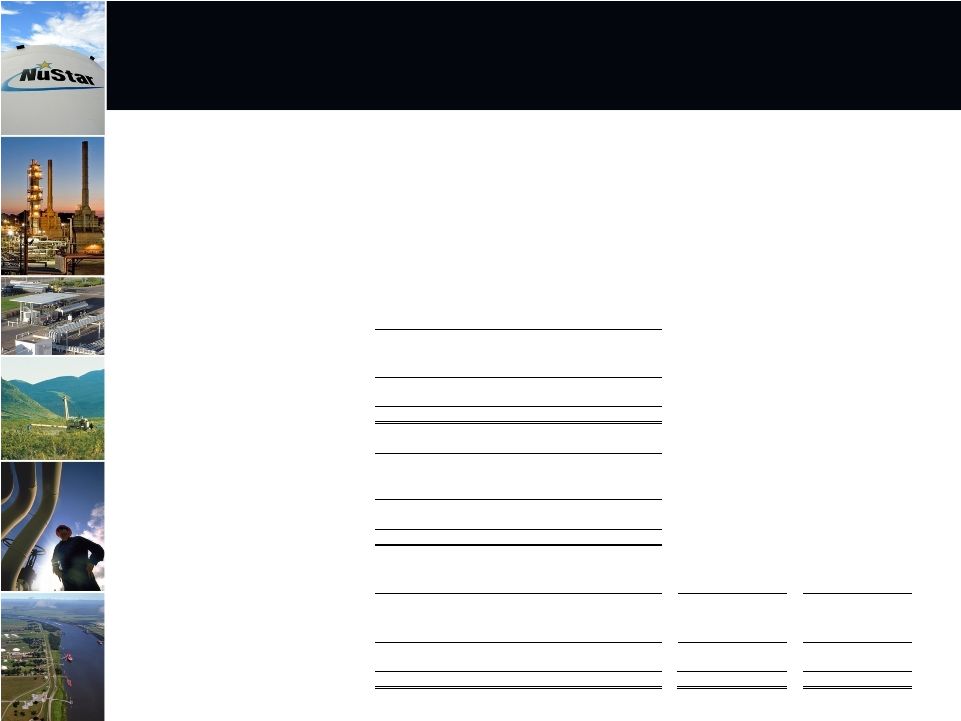

Reconciliation of Non-GAAP Financial Information: Storage Segment 27 (Unaudited, Dollars in Thousands) The following is a reconciliation of operating income to EBITDA for the Storage Segment: 2006 2007 2008 2009 2010 Operating income 108,486 $ 114,635 $ 141,079 $ 171,245 $ 178,947 $ Plus depreciation and amortization expense 53,121 62,317 66,706 70,888 77,071 EBITDA 161,607 $ 176,952 $ 207,785 $ 242,133 $ 256,018 $ Projected incremental operating income range $ 16,500 - 25,500 Plus projected incremental depreciation and amortization expense range 8,500 - 9,500 Projected incremental EBITDA range $ 25,000 - 35,000 St. James, LA Terminal Expansion Phase 1 St. Eustatius Distillate Project Projected annual operating income range $ 11,000 - 20,000 $ 4,000 - 8,000 Plus projected annual depreciation and amortization expense range 4,000 - 5,000 1,000 - 2,000 Projected annual EBITDA range $ 15,000 - 25,000 $ 5,000 - 10,000 The following is a reconciliation of projected annual operating income to projected annual EBITDA for certain projects in our storage segment related to our internal growth program: The following is a reconciliation of projected incremental operating income to projected incremental EBITDA: Year Ended December 31, Year Ended December 31, 2011 NuStar Energy L.P. utilizes two financial measures, EBITDA and distributable cash flow, which are not defined in United States generally accepted accounting principles (GAAP). Management uses these financial measures because they are widely accepted financial indicators used by investors to compare partnership performance. In addition, management believes that these measures provide investors an enhanced perspective of the operating performance of the partnership's assets and the cash that the business is generating. EBITDA in the following reconciliations relate to our reportable segments or a portion of a reportable segment. We do not allocate general and administrative expenses to our reportable segments because those expenses relate primarily to the overall management at the entity level. Therefore, EBITDA reflected in the following reconciliations excludes any allocation of general and administrative expenses consistent with our policy for determining segmental operating income, the most directly comparable GAAP measure. EBITDA should not be considered in isolation or as a substitute for a measure of performance prepared in accordance with GAAP. Neither EBITDA nor distributable cash flow are intended to represent cash flows for the period, nor are they presented as an alternative to net income. They should not be considered in isolation or as a substitute for a measure of performance prepared in accordance with GAAP. |