Preliminary View of

Fourth Quarter 2007

Financial and Operating Results

Conseco, Inc.

Forward-Looking Statements

Cautionary Statement Regarding Forward-Looking Statements. Our statements, trend analyses and other information contained in these

materials relative to markets for Conseco’s products and trends in Conseco’s operations or financial results, as well as other statements, contain

forward-looking statements within the meaning of the federal securities laws and the Private Securities Litigation Reform Act of 1995. Forward-

looking statements typically are identified by the use of terms such as “anticipate,” “believe,” “plan,” “estimate,” “expect,” “project,” “intend,”

“may,” “will,” “would,” “contemplate,” “possible,” “attempt,” “seek,” “should,” “could,” “goal,” “target,” “on track,” “comfortable with,” “optimistic” and

similar words, although some forward-looking statements are expressed differently. You should consider statements that contain these words

carefully because they describe our expectations, plans, strategies and goals and our beliefs concerning future business conditions, our results

of operations, financial position, and our business outlook or they state other ‘‘forward-looking’’ information based on currently available

information. Assumptions and other important factors that could cause our actual results to differ materially from those anticipated in our forward-

looking statements include, among other things: (i) our ability to obtain adequate and timely rate increases on our supplemental health products

including our long-term care business; (ii) mortality, morbidity, usage of health care services, persistency, the adequacy of our previous reserve

estimates and other factors which may affect the profitability of our insurance products; (iii) changes in our assumptions related to the cost of

policies produced or the value of policies inforce at the Effective Date; (iv) the recoverability of our deferred tax asset; (v) changes in accounting

principles and the interpretation thereof; (vi) our ability to achieve anticipated expense reductions and levels of operational efficiencies including

improvements in claims adjudication and continued automation and rationalization of operating systems; (vii) performance of our investments;

(viii) our ability to identify products and markets in which we can compete effectively against competitors with greater market share, higher

ratings, greater financial resources and stronger brand recognition; (ix) the ultimate outcome of lawsuits filed against us and other legal and

regulatory proceedings to which we are subject; (x) our ability to remediate the material weakness in internal controls over the actuarial reporting

process that we identified at year-end 2006 and to maintain effective controls over financial reporting; (xi) our ability to continue to recruit and

retain productive agents and distribution partners and customer response to new products, distribution channels and marketing initiatives; (xii)

our ability to achieve eventual upgrades of the financial strength ratings of Conseco and our insurance company subsidiaries as well as the

potential impact of rating downgrades on our business; (xiii) the risk factors or uncertainties listed from time to time in our filings with the

Securities and Exchange Commission; (xiv) regulatory changes or actions, including those relating to regulation of the financial affairs of our

insurance companies, such as the payment of dividends to us, regulation of financial services affecting (among other things) bank sales and

underwriting of insurance products, regulation of the sale, underwriting and pricing of products, and health care regulation affecting health

insurance products; (xv) general economic conditions and other factors, including prevailing interest rate levels, stock and credit market

performance and health care inflation, which may affect (among other things) our ability to sell products and access capital on acceptable terms,

the returns on and the market value of our investments, and the lapse rate and profitability of policies; and (xvi) changes in the Federal income

tax laws and regulations which may affect or eliminate the relative tax advantages of some of our products. Other factors and assumptions not

identified above are also relevant to the forward-looking statements, and if they prove incorrect, could also cause actual results to differ

materially from those projected. All written or oral forward-looking statements attributable to us are expressly qualified in their entirety by the

foregoing cautionary statement. Our forward-looking statements speak only as of the date made. We assume no obligation to update or to

publicly announce the results of any revisions to any of the forward-looking statements to reflect actual results, future events or developments,

changes in assumptions or changes in other factors affecting the forward-looking statements.

2

Preliminary Results

As previously announced, the Company has been consulting with the staff of the SEC’s Office of the Chief Accountant

(the “SEC staff”) regarding its accounting policy for long-term care premium rate increases, as described in the Summary

of Significant Accounting Policies in Conseco’s 2006 Form 10-K. As previously disclosed, Conseco has used a method

which prospectively changes reserve assumptions for long-term care policies when premium rate increases differ from

original assumptions. On February 28, 2008, the SEC staff informed Conseco of their view that the use of this method is

not consistent with the guidance of Statement of Financial Accounting Standards No. 60, “Accounting and Reporting by

Insurance Enterprises.” The Company is continuing to evaluate the SEC staff’s view, including its effects on the

preliminary earnings reported herein and the possible effects in prior periods. Due to this ongoing evaluation, the

Company has not completed its financial statements for the year ended December 31, 2007. As a result, all financial

results described herein should be considered preliminary, and are subject to change to reflect any necessary adjustments

that are identified before the Company completes its financial statements and files its Form 10-K for the year ended

December 31, 2007.

This presentation contains the following financial measures that differ from the comparable measures under Generally

Accepted Accounting Principles (GAAP): operating earnings measures; and earnings before net realized investment

gains (losses). Reconciliations between those non-GAAP measures and the comparable GAAP measures are included in

the Appendix or the page such measure is presented.

While management believes these measures are useful to enhance understanding and comparability of our financial

results, these non-GAAP measures should not be considered substitutes for the most directly comparable GAAP

measures.

Additional information concerning non-GAAP measures is included in our periodic filings with the Securities and Exchange

Commission that are available in the “Investor – SEC Filings” section of Conseco’s website, www.conseco.com.

Non-GAAP Measures

3

Q4 2007

Preliminary Financial Summary

CNO

BLC and CP continue to have strong results

CP results negatively impacted by cost of expanding product

line with PFFS

CIG results negatively affected by unlocking adjustment in

interest-sensitive life block and other non-recurring

adjustments

LTC Closed Block: second stable quarter as a result of Q2

2007 reserve strengthening; approaching breakeven

No change in net NOL for 2007, nor in earnings outlook;

deferred tax valuation allowance increased by $68 million as a

result of 2007 operating and capital losses

Share repurchases

Q4 2007: $22.9 million (1.7 million shares at average of $13.29/share)

4

Financial Statement Status

Resolution outstanding on accounting for long-term care future loss reserves

Form 10-K will be filed as soon as practical (no later than 3/28)

Long-Term Care Reserves

Overall reserve adequacy (Gross Premium Valuation is positive)

Prospective unlocking: reserve pivot

Relates to additional Active Life Reserves which were set up corresponding to LTC rate

increases

SEC staff has indicated that pivoting is not consistent with FAS 60

Affected Bankers LTC for 2006 and 2007, and LTC Closed Block for 2007

Adjustments have been made back to 2006 as part of restatement

Future loss reserves under FAS 60 Paragraph 37

No impact on underlying economics

Impact relates to incidence of profits over the life of the business

The combination of releasing the previously established pivot reserve and recognition of a

future loss reserve is expected to be marginally accretive to our earnings

The Company currently estimates that adjustments to reflect the SEC staff’s view may have

the effect of reducing the preliminary loss reported for Q4 2007 by up to $5 million (or 3

cents per share)

Q4 2007

Summary of Other Issues

CNO

5

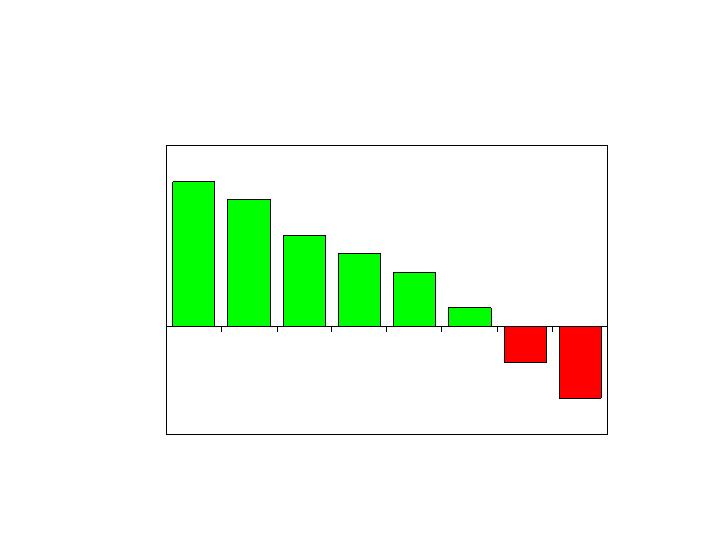

Before Effect of

Future Loss Reserve

CNO

Profit

Breakeven

Loss

Policy Year

1

2

3

4

5

6

7

8

Illustrative Example

6

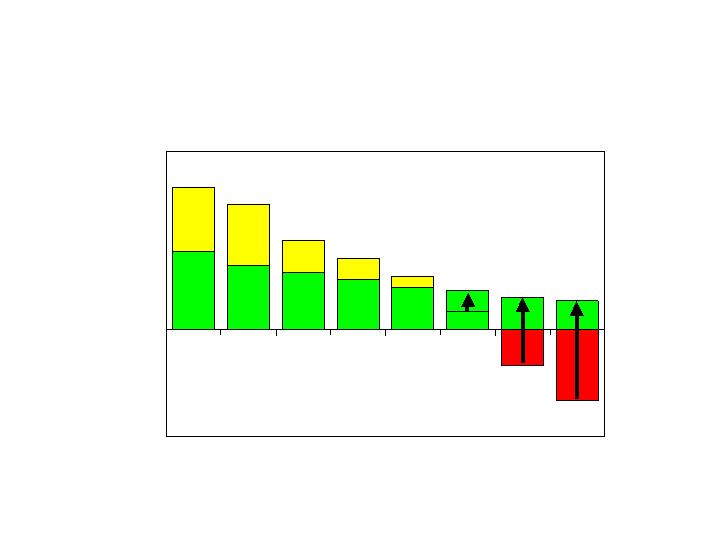

Profit

Pivoting

CNO

Breakeven

Loss

Policy Year

1

2

3

4

5

6

7

8

Illustrative Example

7

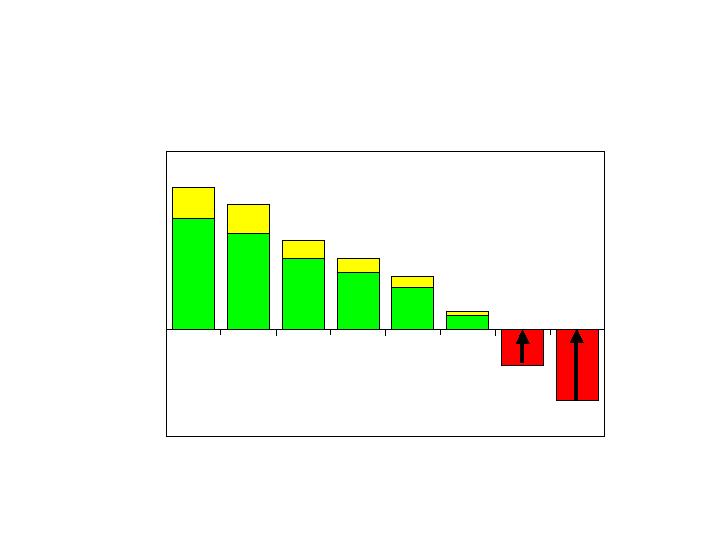

Profit

After Effect of

Future Loss Reserve

CNO

Breakeven

Loss

Policy Year

1

2

3

4

5

6

7

8

Illustrative Example

8

Profit

Pivot vs Future Loss Reserve

CNO

Breakeven

Loss

Policy Year

1

2

3

4

5

6

7

8

Illustrative Example

FLR

Pivot

9

Remediation

Material control weakness first disclosed in 2006 Form 10-K

2007 plan has been completed, plus additional items from scope

expansion

Examined more than 2,400 policy forms: Specified Disease, LTC, Life

Adjustments have been pushed back to corresponding periods with

restatement

2008 focus on sustainable, systematic control improvements

Restatement

Annual financial statements for 2005 and 2006

Quarterly financial information for 2006 and 2007

Selected consolidated financial data for 2003 and 2004

Primarily based upon the cumulative impact of errors identified in 2007

during the procedures performed in an effort to remediate the material

internal control weakness

Will provide a better basis for comparisons between periods

Q4 2007

Summary of Other Issues (cont.)

CNO

10

Bankers Life*

Colonial Penn

Conseco Insurance Group

LTC Closed Block*

Corporate and interest expense

Income before net realized investment losses***

Net realized investment losses

Total*

Earnings before net realized investment losses and

valuation allowance for deferred tax assets, per

diluted share (a non-GAAP measure)****

Q4 2007

Preliminary Summary of Results

CNO

$58.3

(0.2)

7.7

(11.3)

(22.0)

32.5

(35.4)

$(2.9)

Pre-Tax

After Tax**

EPS**

($ millions, except per share amounts)

$(49.2)

(23.0)

$(72.2)

$(0.27)

(0.12)

$(0.39)

$0.10

*Pending finalization of future loss reserves under FAS 60 Paragraph 37. The Company currently

estimates that adjustments to reflect the SEC staff’s view may have the effect of reducing the preliminary loss

reported for Q4 2007 by up to $5 million (or 3 cents per share).

**Income tax expense includes $68 million ($0.37 per share) increase in deferred tax valuation allowance.

***Management believes that an analysis of earnings before net realized investment gains (losses) and taxes (a

non-GAAP financial measure) provides an alternative measure of the operating results of the company

because it excludes net realized gains (losses) that are unrelated to the company’s underlying fundamentals.

The chart above provides a reconciliation to the corresponding GAAP measure.

****See the Appendix for a reconciliation to the corresponding GAAP measure.

11

Bankers Life*

Colonial Penn

Conseco Insurance Group

LTC Closed Block*

Corporate and interest expense

Cost related to litigation settlement

Loss related to coinsurance transaction

Income before net realized investment losses***

Net realized investment losses

Total*

Net operating income before: (1) refinements to a litigation

settlement; (2) a Q3 2007 charge related to a coinsurance

transaction; and (3) the Q4 2007 valuation allowance for

deferred tax assets per diluted share (a non-GAAP

measure)****

2007 Full Year

Preliminary Summary of Results

CNO

$233.0

18.1

102.7

(202.4)

(89.1)

(64.4)

(76.5)

(78.6)

(119.7)

$(198.3)

Pre-Tax

After Tax**

EPS**

($ millions, except per share amounts)

$(132.3)

(77.8)

$(210.1)

$(0.76)

(0.45)

$(1.21)

$0.16

*Pending finalization of future loss reserves under FAS 60 Paragraph 37. The Company currently estimates

that adjustments to reflect the SEC staff’s view may have the effect of reducing the preliminary loss

reported for the year ended December 31, 2007 by up to $15 million (or 9 cents per share).

**Income tax expense includes $68 million ($0.39 per share) increase in deferred tax valuation allowance.

***Management believes that an analysis of earnings before net realized investment gains (losses) and taxes (a

non-GAAP financial measure) provides an alternative measure of the operating results of the company

because its excludes net realized gains (losses) that are unrelated to the company’s underlying fundamentals.

The chart above provides a reconciliation to the corresponding GAAP measure.

****See the Appendix for a reconciliation to the corresponding GAAP measure.

12

Consolidated RBC ratio

296% at 12/31/07 vs 357% at 12/31/06

Investments

$362.7 million of investment income in Q4 2007

Earned yield of 5.95% in Q4 2007

94% of bonds investment grade at 12/31/07*

Corporate liquidity

Available holding company liquidity exceeds $90 million at 12/31/07;

plus $80 million revolver

Preliminary Financial Indicators

CNO

*Excludes investments from consolidated variable interest entity.

13

Collected Premiums

CNO

Strong, consistent

growth in Bankers

and Colonial Penn

Less consistent

growth in CIG due to

focus on more

profitable business

BLC

2004

$3,881.4

2005

$3,925.9

2006

$4,286.5

2007

$4,314.1

($ millions)

CP

CIG

Run-Off

14

Q4 2007 New Annualized Premium (NAP) of $58.3 million, 4%

above Q4 2006, total year NAP up 10%

Earnings driven by improved spreads and higher PDP/PFFS

income

Effective July 1, 2007, entered into a quota-share reinsurance

agreement related to certain group PFFS business sold by

Coventry

Adding $2.0 million of pretax earnings quarterly

LTC premium re-rates (as of 3/6/08):

Submitted: $45.6 million (100% of goal)

Approved: $20.1 million (63% of goal)

Implemented: $19.4 million (61% of goal)

Financial impact: $16.5 million (60% of goal)

Summary

Bankers

15

2007 Strong Distribution Results:

Growth in Key Metrics

Bankers

$294 million NAP = 10% growth

Strong Med Advantage and Life sales

Flat LTC

Lower Med Supp and Annuities

Improved agent productivity while growing quantity

4,480 agents at 12/31/07, up 10% vs 12/31/06

13% growth in new agent contracts

$67,000 average agent production = 4% growth

16

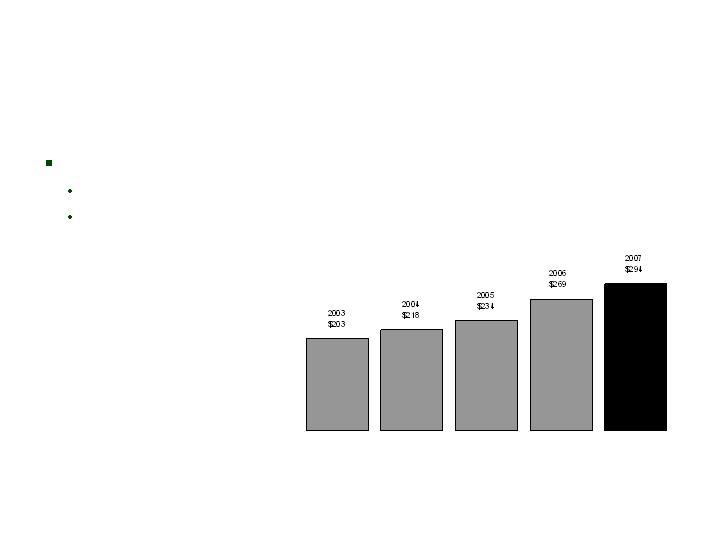

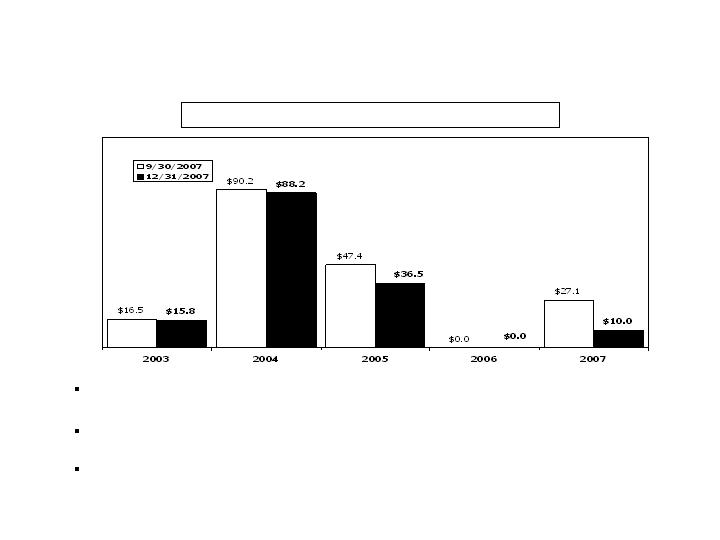

NAP Growth: 2003-2007

10% compound annual growth since 2003

Annual NAP up $90 million during period

Increases driven by agent productivity and growth plus

new product offerings (primarily Life/PDP/PFFS)

Bankers

($ millions)

17

Q4 2007 NAP of $9.3 million, 25% above Q4 2006, total year

NAP up 27%

Expanded product line into PFFS market in Q4 2007

$8.4 million of expenses charged to income

Agreement to recapture block of life insurance business

previously reinsured, effective 10/1/07

Recapture fee (purchase price): $63 million

Immediately accretive to income and ROE

Summary

Colonial Penn

18

Q4 2007 NAP of $19.7 million, 18% less than Q4 2006, total year NAP

down 21%

Decreases in Medicare supplement and annuities, consistent with CIG’s

focus on more profitable business

Higher value from new business compared to Q4 2006 and full year 2006,

despite lower sales

Strong sales gains in specified disease, up 30% from Q4 2006 and full year

2006

Q4 2007 earnings driven by:

Unlocking adjustments on the interest-sensitive life block of business

Slight increase in benefit ratios on health products

Loss of annuity profits from block coinsured in October 2007

Lower expenses

Summary

CIG

19

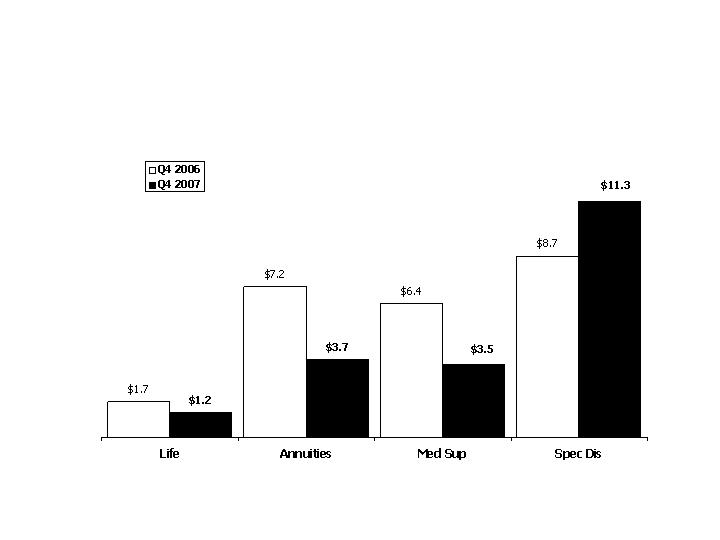

NAP: Q4 2006 vs Q4 2007

CIG

($ millions)

20

Significant reserve strengthening in Q2 2007 has stabilized

results

Active rate management, improved claims-paying practices and

expense efficiency improvements have contributed to reduced

losses

Earnings are approaching breakeven

Migration to LTCG system and processes on track

Summary

LTC Closed Block

21

Q2 2007 claims reserving actions generated stability in Q3 and Q4 2007:

Favorable prior-period development continues

Verified claims for all periods stable

Verified Incurred

Development*

*Excludes waiver-of-premium and return-of-premium benefits.

LTC Closed Block

Reported Claims

Prior Period Development

Verified Claims as of Reporting Date

Verified Claims Developed through:

12/31/04

12/31/05

12/31/06

3/31/07

6/30/07

9/30/07

12/31/07

($ millions)

Q3 2007

$100.7

3.3

104.0

104.0

102.3

Q2 2007

$212.0

(109.7)

102.3

102.3

103.0

107.1

Q1 2007

$119.7

(34.9)

84.7

84.7

104.2

103.6

106.3

2006

$433.3

(72.2)

361.1

361.1

375.1

418.3

414.4

412.2

2005

$396.0

(58.9)

337.2

337.2

365.0

368.8

389.2

388.7

391.0

2004

$370.8

(44.2)

326.6

326.6

326.0

337.7

344.2

356.5

356.6

356.6

Developed

Deficiencies

in Periods

Prior to 2004

$0.0

0

0

44.2

103.7

136.4

147.1

161.4

162.3

165.0

Q4 2007

$104.7

1.8

106.5

106.5

22

Increase in claims paid in Q4 2007 driven by inventory reduction

Claimant count estimates remain around 12,000, with paid claims continuing near $100 million

Q3 2007 termination rate reflects prior-period deaths and terminations

Operating Data

LTC Closed Block

Claims Paid (mils.)

Open Claimant Counts

In Force Policy Counts

Ann. Termination Rates

Q4 2005

$83.1

12,290

201,649

2.3%

Q1 2006

$90.4

11,805

197,585

7.8%

Q2 2006

$101.2

12,536

194,080

6.9%

Q3 2006

$96.1

12,228

190,134

7.9%

Q4 2006

$81.64

12,048

187,123

6.2%

Q1 2007

$102.0

11,870

183,655

7.2%

Q2 2007

$96.8

12,424

179,952

7.8%

Q3 2007

$99.1

12,121

175,685

8.9%

Q4 2007

$104.9

12,338

172,222

7.7%

23

Premium Re-rates

(as of 3/13/08)

LTC Closed Block

Round 1 - exceeded each goal:

Re-rates submitted: $64.0 million (115% of goal)

Re-rates approved: $45.8 million (110% of goal)

Re-rates implemented: $44.4 million (106% of goal)

Re-rates financial impact: $37.3 million (106% of goal)

Round 2 – on track to achieve goals:

Re-rates submitted: $41.8 million (98% of goal)

Re-rates approved: $16.7 million (65% of goal)

Re-rates implemented: $13.5 million (53% of goal)

Re-rates financial impact: $10.8 million (52% of goal)

24

Continue working within the regulatory environment to

achieve equitable and actuarially justified rate increases

Continue progress on claims-paying improvements and

expense efficiencies

Reduce future exposure and volatility of this block

What We Have Left to Do

LTC Closed Block

25

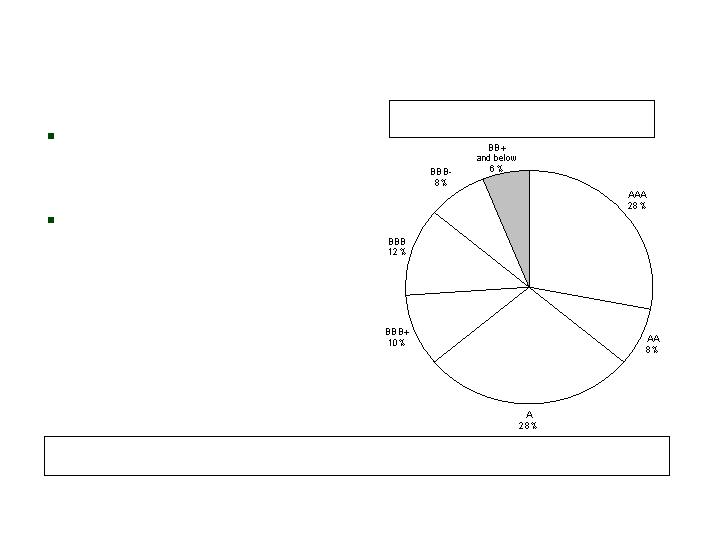

Investment Quality*

CNO

Below-investment grade

securities represent 6% of

total portfolio

Limited new money

allocation to below-

investment grade securities

Actively Managed Fixed Maturities by Rating at

12/31/07 (Market Value)

12/31/07

94%

9/30/07

94%

6/30/07

94%

3/31/07

95%

12/31/06

95%

% of Bonds which are Investment Grade:

*Consistent with prior quarters’ presentations, excludes investments from variable interest entity we are required

to consolidate for GAAP financial reporting (such assets and the related liabilities are legally separated)

26

Structured securities and

asset-backed securities

represent 25% of total

actively managed fixed

maturity securities

Over 88% “AAA” rated

Structured Securities at 12/31/07

CNO

(Market value in millions)

Pass-throughs, sequentials and

equivalent securities

$2,048.0

40.1%

Planned amortization class, target

amortization class, and accretion-

directed bonds

$1,596.1

31.3%

Commercial

mortgage-backed

securities

$965.5

18.9%

Other

$58.5

1.1%

Asset-backed securities

$440.2

8.6%

27

Sub-Prime Home Equity ABS

CNO

Market value represents 0.52% of invested assets at 12/31/07, compared to 0.57% at

9/30/07 and 0.70% at 12/31/06

Reduced sub-prime exposure by over 17% during Q4 2007, including 63% of 2007 vintage,

and over 51% during 2007

Reduction of exposure in Q4 2007 reflects dispositions of $28.3 million and writedowns of

$10.4 million for securities held at year-end

Exposure by Vintage Year (Book Value in millions)

28

Sub-Prime Home Equity ABS

at 12/31/07

CNO

AAA

AA

A

BBB

Total

$39.9

$40.8

$41.9

$0.5

$123.1

$42.5

$48.9

$58.6

$0.5

$150.5

32.4%

33.1%

34.0%

0.5%

100.0%

0.17%

0.17%

0.18%

0.00%

0.52%

Market

Value (mil.)

Book

Value (mil.)

% of

Subprime*

% of

Portfolio*

Rating

No exposure to “affordability products” – negative amortization, option ARM

collateral, etc.

Only $0.5 million (market value) rated lower than A category

Current support in structures meets original expectations

Remaining portfolio generally reflects substantial margin for adverse development

of cash flows/delinquencies

646

641

643

664

643

Avg.

FICO

41.6%

28.6%

19.4%

44.8%

28.7%

Avg.

Support

9.2%

9.0%

7.1%

23.6%

8.4%

Avg. 60+

Delinq.

*% of market value.

29

No ABS CDO investments

No hedge fund investments

No “mark to model” structured securities

No NIM securities

No CDO Squared Investments

Nominal (<$10 million par) third-party CLO/structured credit

exposure

Highly developed cashflow and default analytic models, along

with rigorous management oversight processes

Sub-Prime Home Equity ABS

and Structured Credit

CNO

30

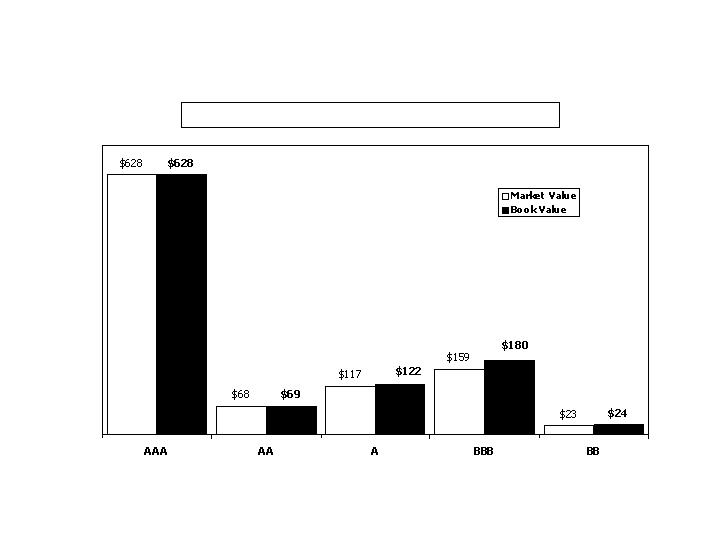

CMBS Exposure Summary

at 12/31/07

CNO

Exposure by Rating Category (in millions)

$995

$1,023

31

CNO Recap

Core businesses

Bankers Life and Colonial Penn – continued strong results, focused

on profitable growth

CIG

Greater focus on distinctive capabilities

Producing more economic value from refocused sales efforts

Run-off LTC block

Claims reserve volatility reduced

Run rate losses per quarter, trending toward breakeven

Continued progress on turnaround, increasingly visible

Stage being set to pursue reduction in LTC exposure

32

CNO Recap (cont.)

Changing the portfolios of the business

Annuity coinsurance deal with Swiss Re closed; released capital

from low-return business

Recapture of Colonial Penn life block from Swiss Re; higher-

return core business for CNO

Operations

Bulk of organizational realignment completed

Remaining real estate realignment (Chicago) to occur in Q2 2008

– expect to record pre-tax loss of approximately $15 million

33

Q4 2007

Normalization of Preliminary Earnings

CNO

Q4 2007 pre-tax income (loss) – as reported*

Loss on termination of interest-rate swaps

Cost of initial marketing of PFFS product

through direct distribution channel

Excess expense related to consolidation of

operations

Unlocking adjustments on interest-sensitive life

Other non-recurring

Q4 2007 pre-tax income (loss) - adjusted

BLC

$58.3

-

-

-

-

-

$58.3

($ millions)

CP

$(0.2)

-

8.4

-

-

-

$8.2

CIG

$7.7

4.2

-

3.3

17.0

1.4

$33.6

LTC

Run-Off

$(11.3)

-

-

-

-

-

$(11.3)

Corp.

$(22.0)

-

-

-

-

-

$(22.0)

Consol.

$32.5

4.2

8.4

3.3

17.0

1.4

$66.8

Factors impacting 2008

Expense savings

Vacating Mart

Operations consolidation

LTC re-rates

*Refer to page 11 for a reconciliation to the corresponding GAAP measure.

34

Next Steps/Expectations

Complete evaluation and calculation of future loss reserves

Filing of 10-K

Full earnings release call and investor deck presentation

35

Questions and Answers

Appendix

Information Related to Certain Non-GAAP Financial Measures

The following provides additional information regarding certain non-GAAP measures used in this presentation. A non-GAAP measure is a

numerical measure of a company’s performance, financial position, or cash flows that excludes or includes amounts that are normally excluded or

included in the most directly comparable measure calculated and presented in accordance with GAAP. While management believes these

measures are useful to enhance understanding and comparability of our financial results, these non-GAAP measures should not be considered as

substitutes for the most directly comparable GAAP measures. Additional information concerning non-GAAP measures is included in our periodic

filings with the Securities and Exchange Commission that are available in the “Investor – SEC Filings” section of Conseco’s website,

www.conseco.com.

Operating earnings measures

Management believes that an analysis of net income applicable to common stock before net realized gains or losses (“net operating income”, a

non-GAAP financial measure) is important to evaluate the performance of the Company and is a key measure commonly used in the life insurance

industry. Management uses this measure to evaluate performance because realized investment gains or losses can be affected by events that

are unrelated to the Company’s underlying fundamentals.

In addition, our results were affected by unusual and significant charges related to: (i) a litigation settlement in Q2 2006 and refinements to such

estimates recognized in subsequent periods; (ii) a Q3 2007 charge related to a coinsurance transaction; and (iii) a Q4 2007 valuation allowance for

deferred tax assets. Management does not believe that similar charges are likely to recur within two years, and there were no similar charges

recognized within the prior two years. Management believes an analysis of operating earnings before these charges is important to evaluate the

performance of the Company prior to the effect of these unusual and significant charges.

38

Information Related to Certain Non-GAAP Financial Measures

A reconciliation of net income applicable to common stock to the net operating income, excluding: (i) Q2 2006 charge related to the litigation settlement and

refinements to such estimates recognized in subsequent periods; (ii) a Q3 2007 charge related to a coinsurance transaction; and (iii) a Q4 2007 valuation

allowance for deferred tax assets (and related per share amounts) is as follows (dollars in millions, except per share amounts):

Q4 2007

YTD 2007

Net loss applicable to common stock

(72.2)

$

(210.1)

$

Net realized investment losses, net of related amortization and taxes

23.0

77.8

Net operating loss (a non-GAAP financial measure)

(49.2)

(132.3)

Q2 2006 charge related to the litigation settlement and refinements to such

estimates recognized in subsequent periods, net of taxes

-

41.9

Q3 2007 charge related to a coinsurance transaction, net of taxes

-

49.7

Q4 2007 valuation allowance for deferred tax assets

68.0

68.0

Net operating income before: (i) Q2 2006 charge related to the

litigation settlement and refinements to such estimates

recognized in subsequent periods; (ii) a Q3 2007 charge related to

a coinsurance transaction; and (iii) a Q4 2007 valuation allowance

for deferred tax assets (a non-GAAP financial measure)

18.8

$

27.3

$

Per diluted share:

Net loss

(0.39)

$

(1.21)

$

Net realized investment losses, net of related amortization and taxes

0.12

0.45

Net operating loss (a non-GAAP financial measure)

(0.27)

(0.76)

Q2 2006 charge related to the litigation settlement and refinements to such

estimates recognized in subsequent periods, net of taxes

-

0.24

Q3 2007 charge related to a coinsurance transaction, net of taxes

-

0.29

Q4 2007 valuation allowance for deferred tax assets

0.37

0.39

Net operating income before: (i) Q2 2006 charge related to the

litigation settlement and refinements to such estimates

recognized in subsequent periods; (ii) a Q3 2007 charge related to

a coinsurance transaction; and (iii) a Q4 2007 valuation allowance

for deferred tax assets (a non-GAAP financial measure)

0.10

$

0.16

$

39