FILED BY EQUITY BANCSHARES, INC. PURSUANT TO RULE 425 UNDER THE SECURITIES ACT OF 1933 AND DEEMED FILED PURSUANT TO RULE 14a-12 UNDER THE SECURITIES EXCHANGE ACT OF 1934 SUBJECT COMPANY: COMMUNITY FIRST BANCSHARES, INC. COMMISSION FILE NO. FOR REGISTRATION STATEMENT ON FORM S-4 FILED BY EQUITY BANCSHARES, INC.: 333-213283 The following letter was mailed to the customers of Community First Bank, the banking subsidiary of Community First Bancshares, Inc., on or about October 14, 2016.

Your guide to community banking with equity Bank. Equity Bank Community First Bank 2016

October 13, 2016 We’re excited to welcome you to Equity Bank! Thank you for your business, and your continued support of Community First Bank. I’m pleased to inform you that beginning November 12, all Community First Bank accounts and services will officially be Equity Bank accounts and services. Thank you for banking with a community bank dedicated to local service. We’re proud to continue serving you. At Equity Bank, our slogan is: We never forget it’s your money, and we take that to heart. Equity Bank is a community bank committed to going the extra mile for your business and family, just like Community First. Equity Bank’s branch network will grow to 34 with the addition of our five Community First locations, including 29 branches currently in Kansas and Missouri. Equity Bank offers a full range of financial solutions, including commercial loans, consumer banking, mortgage loans, and treasury management. Like Community First, our Equity Bank focus will remain on our local communities. Many bank leaders, board members, and advisory boards are remaining in place in your communities. In addition, as outlined in this booklet, beginning November 12, you will have access to the best of Equity Bank! This includes business solutions customized for your company, the Equity Bank mobile app with remote check deposit, online banking and bill pay. Plus—you’ll never pay an ATM fee again. ATM usage at all ATMs, anywhere in the U.S. is complimentary, for all Equity Bank customers! For the past few months, Equity Bank and Community First Bank staff have worked together to ensure a seamless transition for you. This guidebook serves as your handy reference for Equity Bank accounts, services, and procedures following our transition from Community First Bank. Names of accounts may change, but your service will continue to be top notch. Please do not hesitate to contact us with any questions at any time, at our toll free number, 888-733-5041. You can also find this guidebook at EquityBank.com and CommunityFirstBank.com.Thank you for your patience, your business, and your trust in the years ahead. We think you’ll like what you find.ImportantEquity Bank Routing Number101105354Equity Service Bank Center Customer 1 (888) 733-5041Lost or Stolen Card1 (800) 383-8000and Your Debit Checking Card Account Number In almost all cases, your checking account number will remain the same. Continue using your Community First debit card until it expires!customerservice@equitybank.comequitybank.com2 equitybank.com/community-first

Getting Started Equity Bank Online, Mobile, Bill Pay Starting Monday, November 14, 2016, please visit EquityBank.com to enroll in online banking as though you are a new user. Use your existing account number to enroll. You may choose the same user ID used with your CommunityFirstBank.com online banking, if it is not already being used within the EquityBank.com system. Once logged in, we will confirm your enrollment, and your account history, current balance and transaction details will be available at EquityBank.com. Visit EquityBank.com for more details, demonstrations, and more. Online Bill Pay Great news! Your Online Bill Payees, Scheduled Payments, and recurring online bill payments will transfer to Equity Bank! Equity Bank’s Online Bill Pay is available within online banking, and you may also use our mobile app to pay bills. There is no need to cancel online bill payments within your Community First Bank online banking account. This payee activity should be available to you within 48 hours of online banking enrollment. Mobile App Equity Bank’s mobile app is available on the iOS App Store and in Google Play, and is free for download. After confirmation of enrollment in Equity Bank Online Banking, you will be able to use your user ID and password to access full functionality of the app, including transaction history, mobile deposit, and mobile bill pay. Thursday, November 10, 2016 Last day of Community First Bank operation. Friday, November 11, 2016 Veteran’s Day—bank locations closed. Customer Service Center available from 8a—6p at 1 (888) 733- 5041. Saturday, November 12, 2016 First day as Equity Bank. Monday, November 14, 2016 Enroll in Equity Bank Online Banking & Bill Pay. Mobile Deposit Within the Equity Bank mobile app, you will have the ability to deposit checks via your mobile phone, subject to approval. Please follow the prompts within the app to request activation. Statement History Equity Bank will retain statement history for 24 months. For items older than 24 months, you may choose to print, save, or download from CommunityFirstBank.com before November 10. TransfersEquity Bank Online Banking and the Equity BankMobile App feature the ability to transfer money between accounts. Online account transfers using Community First Online Banking must be completed by Wednesday, November 9 at 3 p.m. Recurring or scheduled transfers will not automatically transfer to Equity Bank Online Banking. 3 equitybank.com/community-first

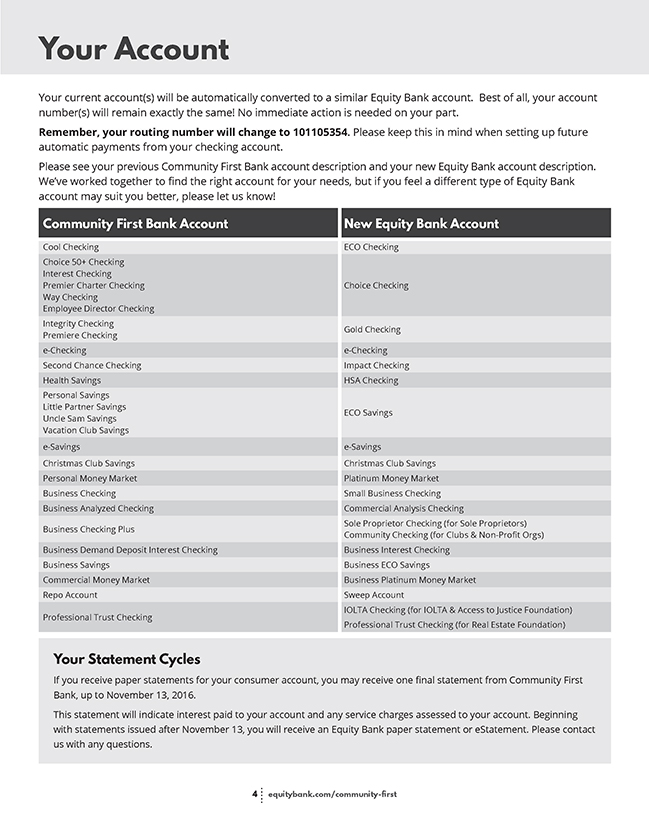

Your Account Your current account(s) will be automatically converted to a similar Equity Bank account. Best of all, your account number(s) will remain exactly the same! No immediate action is needed on your part. Remember, your routing number will change to 101105354. Please keep this in mind when setting up future automatic payments from your checking account. Please see your previous Community First Bank account description and your new Equity Bank account description. We’ve worked together to find the right account for your needs, but if you feel a different type of Equity Bank account may suit you better, please let us know! Community First Bank Account New Equity Bank Account Cool Checking ECO Checking Choice 50+ Checking Interest Checking Premier Charter Checking Choice Checking Way Checking Employee Director Checking Integrity Checking Gold Checking Premiere Checking e-Checking e-Checking Second Chance Checking Impact Checking Health Savings HSA Checking Personal Savings Little Partner Savings ECO Savings Uncle Sam Savings Vacation Club Savings e-Savings e-Savings Christmas Club Savings Christmas Club Savings Personal Money Market Platinum Money Market Business Checking Small Business Checking Business Analyzed Checking Commercial Analysis Checking Business Checking Plus Sole Proprietor Checking (for Sole Proprietors) Community Checking (for Clubs & Non-Profit Orgs) Business Demand Deposit Interest Checking Business Interest Checking Business Savings Business ECO Savings Commercial Money Market Business Platinum Money Market Repo Account Sweep Account IOLTA Checking (for IOLTA & Access to Justice Foundation) Professional Trust Checking Professional Trust Checking (for Real Estate Foundation) Your Statement CyclesIf you receive paper statements for your consumer account, you may receive one final statement from Community FirstBank, up to November 13, 2016.This statement will indicate interest paid to your account and any service charges assessed to your account. Beginning with statements issued after November 13, you will receive an Equity Bank paper statement or eStatement. Please contact us with any questions.4 equitybank.com/community-first

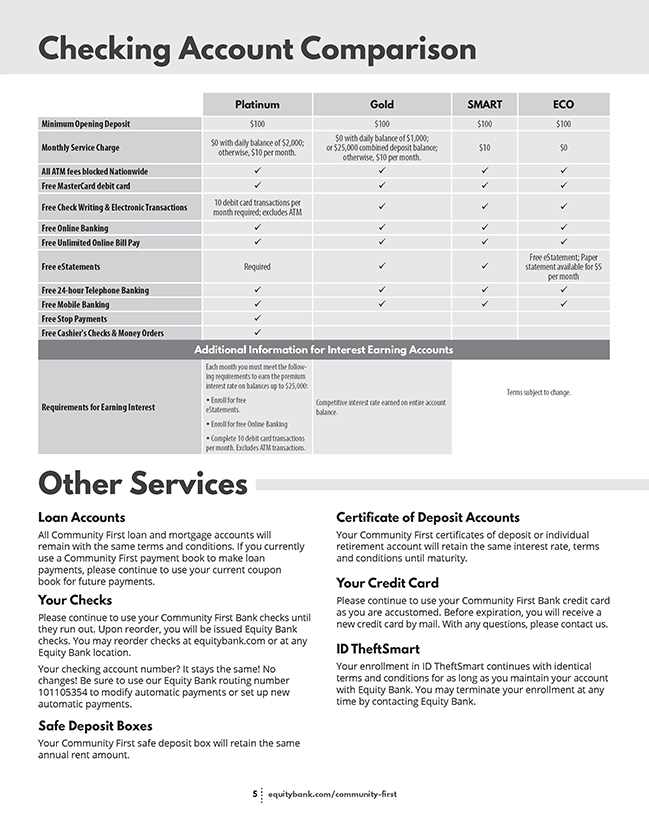

Checking Account Comparison Platinum Gold SMART ECO Minimum Opening Deposit $100 $100 $100 $100 $0 with daily balance of $2,000; $0 with daily balance of $1,000; Monthly Service Charge or $25,000 combined deposit balance; $10 $0 otherwise, $10 per month. otherwise, $10 per month. All ATM fees blocked Nationwideüüüü Free MasterCard debit cardüüüü 10 debit card transactions per Free Check Writing & Electronic Transactions üüü month required; excludes ATM Free Online Bankingüüüü Free Unlimited Online Bill Payüüüü Free eStatement; Paper Free eStatements Requiredüü statement available for $5 per month Free 24-hour Telephone Bankingüüüü Free Mobile Bankingüüüü Free Stop Paymentsü Free Cashier’s Checks & Money Ordersü Additional Information for Interest Earning Accounts Each month you must meet the follow- ing requirements to earn the premium interest rate on balances up to $25,000: Terms subject to change. • Enroll for free Competitive interest rate earned on entire account Requirements for Earning Interest eStatements. balance. • Enroll for free Online Banking • Complete 10 debit card transactions per month. Excludes ATM transactions. Other Services Loan Accounts All Community First loan and mortgage accounts will remain with the same terms and conditions. If you currently use a Community First payment book to make loan payments, please continue to use your current coupon book for future payments.Your ChecksPlease continue to use your Community First Bank checks until they run out. Upon reorder, you will be issued Equity Bank checks. You may reorder checks at equitybank.com or at any Equity Bank location. Your checking account number? It stays the same! No changes! Be sure to use our Equity Bank routing number101105354 to modify automatic payments or set up new automatic payments.Safe Deposit BoxesYour Community First safe deposit box will retain the same annual rent amount. Certificate of Deposit AccountsYour Community First certificates of deposit or individual retirement account will retain the same interest rate, terms and conditions until maturity.Your Credit CardPlease continue to use your Community First Bank credit card as you are accustomed. Before expiration, you will receive a new credit card by mail. With any questions, please contact us. ID TheftSmartYour enrollment in ID TheftSmart continues with identical terms and conditions for as long as you maintain your account with Equity Bank. You may terminate your enrollment at any time by contacting Equity Bank.5 equitybank.com/community-first

Your Debit Card Please continue to use your Community First Bank debit card. Before its expiration, we will issue you a new Equity Bank debit card. This means your existing bill payments, automatic payments, and service with your current debit card should continue uninterrupted, with no need for action from you. Please continue to use your Community First debit card until it expires. Once you receive your new Equity Bank debit card, you may activate your new card by calling the number provided on the sticker on the front of the card. Additional Account Information Equity ECO Checking Minimum Balance Requirements None. Dormant/Inactive Account Information A and dormant your balance service is charge lower than of $5 $ per 500. month will be charged after 12 months of no activity or communication Processing Order as All follows: credit transactions ATM/Debit Card are processed transactions, first. checks Debits, and or then withdrawals, Preauthorized from transactions your account (i. e. will ACH be Payments) processed. Items are processed from highest to lowest within each category.Transaction LimitationsNo transaction limitations apply to this account.Additional Information Regarding Your AccountStatements be shown. received Check and on deposit this account ticket will images be truncated can be statements, obtained through no check Online or deposit Banking ticket at images no charge. will Electronic Checking customers statements who through currently Online receive Banking complimentary are free; paper paper statements statements are will $ not 5 per be assessed month. Cool the $5.00 monthly fee.Choice CheckingVariable Rate InformationThe interest rate on your account is 0.08%, with an annual percentage yield (APY) of 0.08%. Your interest rate and annual percentage yield may change.Determination of RateAt our discretion, we may change the interest rate on your account.Frequency of Rate ChangesWe may change the interest rate on your account at any time.Limitations on Rate ChangesThere are no maximum or minimum interest rate limits for this account.Compounding and CreditingInterest will be compounded monthly and will be credited to your account monthly. If you close your account before interest is credited, you will not receive the accrued interest.Minimum Balance RequirementsYou must maintain a minimum average daily balance of $500 in your account to obtain the disclosed annual percentage yield. The average daily balance is calculated by adding the balance in the account for each day of the period and dividing that figure by the number of days in the period. The period we use to make this calculation is monthly.Dormant/Inactive Account Information A dormant service charge of $5 per month will be charged after 12 months of no activity or communication and your balance is lower than $500.Processing OrderAll credit transactions are processed first. Debits, or withdrawals, from your account will be processed as follows: ATM/Debit Card transactions, checks and then Preauthorized transactions (i.e. ACH Payments). Items are processed from highest to lowest within each category.Balance Computation MethodWe use the daily balance method to calculate interest on your account. This method applies a daily periodic rate to the principal in the account each day.Accrual on Noncash DepositsInterest begins to accrue on the business day you deposit noncash items (for example, checks).Your School-Sponsored Debit Card!Your custom card design isn’t going away! Upload an image of your choice to your new Equity Bank debit card, or continue to choose from one of our local school-sponsored debit cards, as well as numerous other designs. Visit www.mydebitcarddesign.com for more!Transaction LimitationsNo transaction limitations apply to this account.Additional Information Regarding Your AccountCustomers may request one free box of logo checks per year. Wallet style only.Gold CheckingVariable Rate InformationThe interest interest rate and rate annual on your percentage account is yield 0.20%, may with change. an annual percentage yield (APY) of 0.20%. Your Determination of RateAt our discretion, we may change the interest rate on your account.Frequency of Rate ChangesWe may change the interest rate on your account at any time.Limitations on Rate ChangesThere are no maximum or minimum interest rate limits for this account.Compounding and CreditingInterest account will before be interest compounded is credited, monthly you and will will not be receive credited the accrued to your account interest. monthly. If you close your Minimum Balance RequirementsA falls monthly below service $1,000 charge any day of of $10 the will statement be imposed cycle. every statement cycle if the daily balance in the account The deposit monthly accounts service with charge Equity will Bank be (including waived if checking, you keep savings, $25,000 money or more market combined and CDs) in your . personal Dormant/Inactive Account Information A and dormant your balance service charge is lower of than $5 per $500. month will be charged after 12 months of no activity or communication Processing Order as All follows: credit transactions ATM/Debit Card are processed transactions, first. checks Debits, and or then withdrawals, Preauthorized from transactions your account (i. e. will ACH be Payments) processed. Items are processed from highest to lowest within each category.Balance Computation Method periodic We use the rate daily to the balance principal method in the to account calculate each interest day. on your account. This method applies a daily Accrual on Noncash DepositsInterest begins to accrue on the business day you deposit noncash items (for example, checks).Transaction LimitationsNo transaction limitations apply to this account.E-CheckingMinimum Balance RequirementsNone.Dormant/Inactive Account Information A and dormant your balance service charge is lower of than $5 per $500. month will be charged after 12 months of no activity or communication Processing Order as All follows: credit transactions ATM/Debit Card are processed transactions, first. checks Debits, and or then withdrawals, Preauthorized from transactions your account (i. e. will ACH be Payments) processed. 6 equitybank.com/community-first

Items are processed from highest to lowest within each category.Transaction LimitationsNo transaction limitations apply to this account.Additional Information Regarding Your AccountAn rate e-Savings and annual account percentage is required yield to on have the this e-Saving checking account account. you In must order conduct to receive 15 the Debit disclosed Card point interest of Each sale purchases Debit Card and transaction have at least must one be (1) hard direct posted deposit to the or ACH account debit to transaction be included per in statement the 15 required cycle. per deposit statement or ACH cycle. debit transaction ATM transactions must be do hard not posted qualify to as the Debit account Card transactions. per statement At cycle. least one direct In Banking addition within to the 10 above, days of both account the e-Checking opening. Electronic and e-Savings statements accounts are must the only be enrolled type of statement in Online allowed on these accounts.If rate account of the Eco requirements Savings account. are not This met, is determined the interest by rate the transactions on the e-Savings posted account and cleared will each drop statement to the fallback cycle. If the e-Savings account is closed, this e-Checking account will convert to the Eco Checking account. bearing, Eco Checking no monthly Account –– service No minimum charge, balance electronic requirements, statements no through transaction Online requirements, Banking are non-interest free; paper statements are $5 per month. Impact CheckingMinimum Balance RequirementsNone.Dormant/Inactive Account Information A and dormant your balance service charge is lower of than $5 per $500. month will be charged after 12 months of no activity or communication Processing Order as All follows: credit transactions ATM/Debit Card are processed transactions, first. checks Debits, and or then withdrawals, Preauthorized from transactions your account (i. e. will ACH be Payments) processed. Items are processed from highest to lowest within each category.Transaction LimitationsNo transfers, checks ATM/Debit are issued Card on this purchases, account. ATM All clearing Withdrawals items or must ACH be Payments. electronic In through person withdrawals Online Banking can be made at any Equity Bank branch location. Account is subject to closure if a check clears account. Bill Payment through Online Banking is not offered with this account. Overdrafts closure. are not allowed on this account, should an overdraft occur the account will be subject to Additional Fee InformationYour account will incur a Service Charge of $10.00 per month.HSA CheckingVariable Rate InformationThe interest rate on your account is 0.09%, with an annual percentage yield (APY) of 0.09%. Your interest rate and annual percentage yield may change.Determination of RateAt our discretion, we may change the interest rate on your account.Frequency of Rate ChangesWe may change the interest rate on your account at any time.Limitations on Rate ChangesThere are no maximum or minimum interest rate limits for this account.Compounding and CreditingInterest will be compounded monthly and will be credited to your account monthly. If you close your account before interest is credited, you will not receive the accrued interest.Minimum Balance RequirementsYou must maintain a minimum daily balance of $2,500 in the account each day to obtain the disclosed annual percentage yield. You will earn interest for every day during the period that your account equals or exceeds the minimum daily balance requirement. Balance Computation MethodWe use the daily balance method to calculate the interest on your account. This method applies a daily periodic rate to the principal in the account each day.Accrual on Noncash Deposits Interest begins to accrue on the business day you deposit noncash items (for example, checks).Fees and ChargesPaper debit transactions, such as checks and in person withdrawals, in excess of one per month will be charged $1 per transaction.Transaction LimitationsThe minimum amount you may deposit is $25. Contributions are limited to the max allowed under IRS rules for the tax year unless the contribution is a rollover contribution. For individuals who have attained age 55 before the close of the taxable year, the contribution limit is increased by an additional $ most 1,000. current You agree information not to exceed on contributions, the limits. please Limits see may www. change irs.gov and Publication are not controlled 969. by us. For the Health Savings AccountHealth Revenue Savings Service. Accounts Please see (HSAs) your are HSA subject Agreement to limitations or your tax and/or advisor penalties for additional imposed information. by the Internal Additional Information Regarding Your AccountIf the balance falls below $100 at any time during the statement cycle the account will be closed. We have the right to amend the Health Savings Trust Agreement at any time. Any amendments deemed we make to to have comply consented with the to Code any other and related amendment Regulations unless, do within not 30 require days your from consent the date . we You mail will the be amendment, you notify us in writing that you do not consent. you, IRS Regulations your spouse and allow your non dependent(s) -taxable withdrawals . The Trustee from is not an required HSA to to pay monitor qualified withdrawals medical. expenses Withdrawals for not spouse made due to to pay death, qualified will result medical in a taxable expenses, event except . Consult in the your case tax of advisor a rollover . or disbursement to a ECO SavingsEligibility RequirementsThe Minimum Balance Requirements will be waived for students under the age of 18.Variable Rate InformationThe interest interest rate and rate annual on your percentage account is yield 0.09%, may with change an annual . percentage yield (APY) of 0.09%. Your Determination of RateAt our discretion, we may change the interest rate on your account.Frequency of Rate ChangesWe may change the interest rate on your account at any time.Limitations on Rate ChangesThere are no maximum or minimum interest rate limits for this account.Compounding and CreditingInterest account will before be compounded interest is credited, quarterly you and will will not be receive credited the accrued to your account interest quarterly . . If you close your Minimum Balance RequirementsA below monthly $200 service any day charge of the of month $5 will . be imposed every month if the daily balance in the account falls Dormant/Inactive Account Information A and dormant your balance service charge is lower of than $5 per $500 month . will be charged after 36 months of no activity or communication Processing OrderAll as follows: credit transactions ATM/Debit Card are processed transactions, first checks . Debits, and or then withdrawals, Preauthorized from transactions your account (i. e will . ACH be Payments) processed. Items are processed from highest to lowest within each category.Balance Computation MethodWe a periodic use the rate average to the daily average balance daily method balance to in calculate the account interest for the on period your .account The average . This method daily balance applies is calculated the number by of adding days in the the principal period. in the account for each day of the period and dividing that figure by Accrual on Noncash Deposits Interest begins to accrue on the business day you deposit noncash items (for example, checks).Transaction LimitationsTransfers or telephone from transfers a savings are account limited to to another six per month account . A or service to third charge party of by $ 1 preauthorized, will be charged automatic, for each withdrawal in excess of two during a month.E-SavingsTired Variable Rate Information portion If your average will be 0 daily .11% balance .. The annual is equal percentage to or greater yield than (APY) $75,000 for this .01, tier the will interest range from rate paid 0.45% only to for 0.11%, that depending on the balance in the account.If the your interest average rate daily paid balance only for is that equal portion to or greater will be than 0.16% $15,000 . The annual .01 but percentage less than or yield equal (APY) to $ 75,000, for this tier will range from 1.62% to 0.45%, depending on the balance in the account.If be your 1.61% average . The annual daily balance percentage is less yield than (APY) $15,000 for .this 01, tier the is interest 1.62% rate paid on the entire portion will Your interest rate and annual percentage yield may change.Determination of RateAt our discretion, we may change the interest rate on your account.Frequency of Rate ChangesWe may change the interest rate on your account at any time.Limitations on Rate ChangesThere are no maximum or minimum interest rate limits for this account.Additional Rate InformationAn rate e——and Checking annual account percentage is required yield you to have must this conduct savings 15 account Debit .Card In order point to of receive sale purchases the disclosed and interest have at Each least Debit one (1) Card direct transaction deposit or must ACH be debit hard transaction posted to per the statement e-Checking cycle account on your to be e-included Checking in account the 15 . direct required deposit per statement or ACH debit cycle transaction . ATM transactions must be hard do posted not qualify to the as e- Checking Debit Card account transactions per statement . At least cycle one . In Banking addition within to the 10 above, days of both account the e opening -Checking . Electronic and e-Savings statements accounts are must the only be enrolled type of statement in Online allowed on these accounts.If of account the Eco r equirements Savings account are for not that met, statement the interest cycle rate on on the this entire account balance will in drop the to account the fallback . Account rate requirements are determined by the transactions posted and cleared each statement cycle.If the e-Checking account is closed, this e-Savings account will convert to the Eco Savings account. Eco Savings Account——A monthly service charge of $5 will be imposed every statement cycle if the daily 7 equitybank.com/community-first

the balance same in . the A service account charge falls of below $1 will $200 be any charged day of for the each statement withdrawal cycle in . Transaction excess of two limitations during a month remain . Compounding and CreditingInterest account will before be interest compounded is credited, monthly you and will will not be receive credited the accrued to your account interest .monthly. If you close your Minimum Balance RequirementsNone.Dormant/Inactive Account Information A and dormant your balance service charge is lower of than $5 per $500 month . will be charged after 36 months of no activity or communication Processing OrderAll as follows: credit transactions ATM/Debit Card are processed transactions, first checks . Debits, and or then withdrawals, Preauthorized from transactions your account (i. e will . ACH be Payments) processed. Items are processed from highest to lowest within each category.Balance Computation MethodWe a periodic use the rate average to the daily average balance daily method balance to in calculate the account interest for the on period your .account The average . This method daily balance applies is calculated the number by of adding days in the the principal period. in the account for each day of the period and dividing that figure by Accrual on Noncash Deposits Interest begins to accrue on the business day you deposit noncash items (for example, checks).Transaction LimitationsTransfers or telephone from transfers a savings are account limited to to another six per month account . A or service to third charge party of by $ 2 preauthorized, will be charged automatic, for each withdrawal in excess of six during a month.Christmas Club SavingsVariable Rate InformationThe interest interest rate and rate annual on your percentage account is yield 0.09%, may with change an annual . percentage yield (APY) of 0.09%. Your Determination of RateAt our discretion, we may change the interest rate on your account.Frequency of Rate ChangesWe may change the interest rate on your account at any time.Limitations on Rate ChangesThere are no maximum or minimum interest rate limits for this account.Compounding and CreditingInterest account will before be interest compounded is credited, annually you and will will not be receive credited the accrued to your account interest .annually. If you close your Minimum Balance RequirementsNone.Dormant/Inactive Account Information A and dormant your balance service charge is lower of than $5 per $500 month . will be charged after 12 months of no activity or communication Processing OrderAll as follows: credit transactions ATM/Debit Card are processed transactions, first checks . Debits, and or then withdrawals, Preauthorized from transactions your account (i. e will . ACH be Payments) processed. Items are processed from highest to lowest within each category.Balance Computation MethodWe a periodic use the rate average to the daily average balance daily method balance to in calculate the account interest for the on period your account . The average . This method daily balance applies is calculated the number by of adding days in the the balance period. in the account for each day of the period and dividing the figure by Accrual on Noncash DepositsInterest begins to accrue on the business day you deposit noncash items (for example, checks).Transaction LimitationsThis account is only allowed one annual withdrawal completed by Equity Bank. Withdrawals from this account prior to the annual payout will subject the account to closure. A $10 service charge will be assessed if the account is closed before the annual statement cycle or if any type of withdrawal is made.This account is not allowed to have electronic withdrawals, checks, ATM/Debit Card, or bill pay access. You may make an unlimited number of deposits into your account.Additional Information Regarding Your AccountYou Christmas will receive Club Savings a check account for the balance with an of automatic the account deposit annually will automatically during the first remain week open of November . . A Platinum Money MarketTired Variable Rate InformationIf account your average will be 0 daily .10%, balance with an is annual below percentage $25,000, the yield interest (APY) rate of 0 paid .10% on . the entire balance in your If rate your paid average on the daily entire balance balance is in equal your to account or greater will be than 0.15%, $25,000 with but an less annual than percentage $50,000, the yield interest (APY) of 0.15%.If rate your paid average on the daily entire balance balance is in equal your to account or greater will than be 0 .$ 20%, 50,000 with but an less annual than percentage $100,000, the yield interest (APY) of 0.20%.If balance your average in your daily account balance will be is equal 0.20%, to with or greater an annual than percentage $100,000, the yield interest (APY) of rate 0. 20% paid. on the entire Your interest rate and annual percentage yield may change.Determination of RateAt our discretion, we may change the interest rate on your account.Frequency of Rate ChangesWe may change the interest rate on your account at any time.Limitations on Rate ChangesThere are no maximum or minimum interest rate limits for this account.Compounding and CreditingInterest account will before be interest compounded is credited, monthly you and will will not be receive credited the accrued to your account interest .monthly. If you close your Minimum Balance RequirementsA falls monthly below service $5,000 charge any day of of $5 the will statement be imposed cycle every . statement cycle if the daily balance in the account Dormant/Inactive Account Information A and dormant your balance service charge is lower of than $5 per $500 month . will be charged after 36 months of no activity or communication Processing OrderAll as follows: credit transactions ATM/Debit Card are processed transactions, first checks . Debits, and or then withdrawals, Preauthorized from transactions your account (i. e will . ACH be Payments) processed. Items are processed from highest to lowest within each category.Balance Computation MethodWe a periodic use the rate average to the daily average balance daily method balance to in calculate the account interest for the on period your .account The average . This method daily balance applies is calculated the number by of adding days in the the principal period. in the account for each day of the period and dividing that figure by Accrual on Noncash DepositsInterest begins to accrue on the business day you deposit noncash items (for example, checks).Transaction LimitationsTransfers check, automatic, from an Equity or telephone Platinum Money transfer Market are limited account to to six another per month account . A or service third party charge by preauthorized, of $5 will be charged for each debit transaction in excess of six per month.Current Rate Information most The rate(s) recent and seven annual calendar percentage days, and yield(s) were disclosed accurate on as the of 10/01/2016 above accounts . To were obtain offered current within rate and the annual percentage yield information, please contact your local branch or call us at 888-733-5041.Courtesy Pay(For consumer accounts only. Excluding Impact Checking.)There funds are transfers several or ways other your withdrawal account can requests; become (2) overdrawn, payments such authorized as (1) the by payment you (i .of e. checks, signature electronic -based or point (5) of the sale deposit transactions); of items which, (3) the according return of unpaid to the bank’s items deposited Funds Availability by you; (4) Policy, bank are service treated charges; as not yet available or finally paid. While enough we money, are not as obligated long as you to maintain pay any your item account presented in “good for payment standing,” if your we may account approve does your not overdraft contain items privilege within consideration, your current your available account Courtesy is in “good Pay standing” limit as a if non you -(1) contractual deposit enough courtesy money . For overdraft to bring your payment account of all to bank a positive fees and end charges); -of-day balance (2) avoid at excessive least once overdrafts every 30 suggesting calendar days the use (including of Courtesy the Pay as a continuing line of credit; and (3) have no legal orders, levies or liens against your account. low, In the per normal the bank’s course policy of business, . We reserve we generally the right pay to change electronic the transactions order of payment first and without then checks notice high to you to order if we suspect we pay your fraud items or possible in may illegal create activity multiple affecting overdraft your items account in a single . Also, banking please be day aware and that you will the be according charged to our our Overdraft records, is Charge $5 or less of $ overdrawn, 33.98 for each you overdraft will not incur item an paid overdraft . If your charge end-of . -A day continuous balance, days Overdraft and bank Fee of holidays $5 per day . There will is be a charged daily cap beginning of $169.90 the per eighth day (five day overdrawn, transactions) excluding on overdraft weekend and return check charges. You time may of opting opt out out of. the Normally, privilege we at will any not time, approve but you an are overdraft responsible for you for in any excess overdrawn of the predetermined balances at the amount the overdraft assigned plus to the your bank’s account Overdraft type. Charge So as not of $ to 33 exceed .98 per your item limit, and the please continuous note that Overdraft the amount Fee of of $5 per day will be deducted from the overdraft limit. for We you may . For refuse example, to pay an we overdraft typically item do not at pay any overdraft time even items though if your we may account have is previously not in good paid standing overdrafts as using defined Courtesy above, Pay or, if excessively based upon or our seem review to be of using your Courtesy account management, Pay as a regular we line determine of credit that . You you will are be charged a Returned Check Charge of $33.98 for each item returned. 8 equitybank.com/community-first

We will notify you promptly of any non-sufficient funds items paid or returned that you may have; however, we have no obligation to notify you before we pay or return any item. The amount of any overdraft including our Overdraft Charge of $33.98, the continuous Overdraft Fee of $5 per day will be deducted from the overdraft limit and/or a Returned Check Charge of $33.98 that you owe us is due and payable upon demand. Even if we do not ask you for payment, you must repay us, no later than 30 calendar days after the creation of the overdraft. If there is an overdraft on an account with more than one owner on the signature card, each owner and agent, if applicable, is jointly and severally liable for all overdrafts including all fees charged.Courtesy Pay should not be viewed as an encouragement to overdraw your account. To avoid fees, we encourage you to keep track of your account balance by entering all items in your check register, reconcile your checkbook regularly, and manage your finances responsibly. If you would like to have this service removed from your account, please call 1-888-733-5041.Customers who are currently enrolled in Community First Bank’s Overdraft Privilege program will automatically be enrolled in Courtesy Pay. Your overdraft limit will remain the same. Please note that your Courtesy Pay limit may be available for each item paid under the limit created by checks and other transactions made using your checking account number, such as a teller withdrawal, an automatic payment (ACH) transaction, or automatic bill payment and recurring debit card payment. Also, at your request, we may authorize and pay ATM transfers or withdrawals and everyday debit card purchases using your limit. If you requested Community First Bank to authorize and pay ATM transfers or withdrawals and everyday debit card purchases this authorization will continue. Your available balance may be affected by authorizations which could create additional overdrafts and associated fees. When you ask for your account balance, please remember the amount we show you does not include your overdraft limit.LIMITATIONS: Courtesy Pay is a non-contractual courtesy that is available to individually/jointly owned accounts in good standing for personal use. Equity Bank reserves the right to limit participation to one account per household and to suspend, revoke or discontinue this service without prior notice. If your limit is suspended, unless we notify you otherwise or you request this service be removed from your account, your limit will be made available to cover overdrafts again the first business day after you bring your account to a positive end-of-day balance. If you receive a direct deposit of your monthly Social advise Security us to prevent payment us paying into your your checking overdrafts account with these and do funds not want . Courtesy Pay eligibility, you must Electronic Fund Transfer ServicesFor purposes of this disclosure and agreement the terms “we”, “us” and “our” refer to Equity Bank. The terms “you” and “your” refer to the recipient of this disclosure and agreement.The Electronic Fund Transfer Act and Regulation E require institutions to provide certain information to customers regarding electronic fund transfers (EFTs). This disclosure applies to any EFT service you receive from us related to an account established primarily for personal, family or household purposes. This disclosure does not apply business accounts or accounts used for business purposes. Examples of EFT services include direct deposits to your account, automatic regular payments made from your account to a third party and one-time electronic payments from your account using information from your check to pay for purchases or to pay bills. This disclosure also applies to the use of your ATM Card, Standard Debit Card, Student Debit Card or Premier Debit Card at automated teller machines (ATMs) and any networks described below.TERMS AND CONDITIONS. The following provisions govern the use of electronic fund transfer (EFT) services through accounts held by Equity Bank which are established primarily for personal, family or household purposes. If you use any EFT services provided, you agree to be bound by the applicable terms and conditions listed below. Please read this document carefully and retain it for future reference.Electronic Fund Transfer Services ProvidedSERVICES CARD OR PREMIER PROVIDED DEBIT THROUGH CARD USE OF ATM CARD, STANDARD DEBIT CARD, STUDENT DEBIT If you have received an electronic fund transfer card (“ATM Card,” “Standard Debit Card,” “Student Debit Card” or “Premier Debit Card”- hereinafter referred to collectively as “ATM Card or Debit Card”) from us you may use it for the type(s) of services noted below, and the following provisions are applicable:USING YOUR CARD AND PERSONAL IDENTIFICATION NUMBER (“PIN”). In order to assist us in maintaining the security of your account and the terminals, the ATM Card or Debit Card remains our property and may be revoked or canceled at any time without giving you prior notice. You agree not to use your ATM Card or Debit Card for a transaction that would cause your account balance to go below zero, or to access an account that is no longer available or lacks sufficient funds to complete the transaction, including any available line of credit. We will not be required to complete any such transaction, but if we do, we may, at our sole discretion, charge or credit the transaction to another account; you agree to pay us the amount of the improper withdrawal or transfer upon request.Your ATM Card may only be used with your PIN. Certain transactions involving your Debit Card require use of your PIN. Your PIN is used to identify you as an authorized user. Because the PIN is used for identification purposes, you agree to notify Equity Bank immediately if your ATM Card or Debit Card is lost or if the secrecy of your PIN is compromised. You also agree not to reveal your PIN to any person not authorized by you to use your ATM Card or Debit Card or to write your PIN on your ATM Card or Debit Card or on any other item kept with your ATM Card or Debit Card. We have the right to refuse a transaction on your account when your ATM Card or Debit Card or PIN has been reported lost or stolen or when we reasonably believe there is unusual activity on your account.The security of your account depends upon your maintaining possession of your ATM Card or Debit Card and the secrecy of your PIN. You may change your PIN if you feel that the secrecy of your PIN has been compromised. You may change your PIN by requesting an Easy PIN Reference Number at any Equity Bank branch location.ATM ServicesATM CARD SERVICES. The services available through use of your ATM Card are described below. You may withdraw cash from your checking account(s), savings account(s), money market account(s), and NOW account(s).You may transfer funds between your checking and savings accounts, checking and money market accounts, checking and NOW accounts, savings and money market accounts, savings and NOW accounts, and NOW accounts and money market accounts.You may make balance inquiries on your checking account(s), savings account(s), money market account(s), and NOW account(s).DEBIT CARD SERVICES. The services available through use of your Standard Debit Card, Student Debit Card and Premier Debit Card are described below.STANDARD DEBIT CARD SERVICES—The following services are available through use of your Standard Debit Card: You may withdraw cash from your checking account(s), savings account(s), money market account(s), and NOW account(s).You may transfer funds between your checking and savings accounts, checking and money market accounts, checking and NOW accounts, savings and money market accounts, savings and NOW accounts, and NOW accounts and money market accounts.You may make balance inquiries on your checking account(s), savings account(s), money market account(s), and NOW account(s).STUDENT DEBIT CARD SERVICES—The following services are available through use of your Student Debit Card: You may withdraw cash from your checking account(s), savings account(s), money market account(s), and NOW account(s).You may transfer funds between your checking and savings accounts, checking and money market accounts, checking and NOW accounts, savings and money market accounts, savings and NOW accounts, and NOW accounts and money market accounts.You may make balance inquiries on your checking account(s), savings account(s), money market account(s), and NOW account(s).NETWORK. Your ability to perform the transactions or access the accounts set forth above depends on the location and type of ATM you are using and the network through which the transaction is being performed. A specific ATM or network may not perform or permit all of the above transactions. Besides being able to use your ATM Card or Debit Card at our ATM terminals, you may access your accounts through the following network(s): Pulse, PLUS, and Cirrus.POINT OF SALE TRANSACTIONSYou may use your ATM Card, Standard Debit Card, Student Debit Card or Premier Debit Card (‘‘POS Access Card’’) to purchase goods and services from merchants that have arranged to accept your POS Access Card as a means of payment (these merchants are referred to as “Participating Merchants”). Some Participating Merchants may permit you to receive cash back as part of your purchase. Purchases made with your POS Access Card, including any purchase where you receive cash, are referred to as “Point of Sale” transactions and will cause your “designated account” to be debited for the amount of the purchase. The designated account for ATM Card transactions is your Checking, NOW, Money Market or Savings Account. The designated account for Standard Debit Card transactions is your Checking, NOW, Money Market or Savings Account. The designated account for Student Debit Card transactions is your Checking, NOW, Money Market or Savings Account. The designated account for Premier Debit Card transactions is your Checking, NOW, Money Market or Savings Account.In addition, your Standard Debit Card, Student Debit Card or Premier Debit Card may be used at any merchant that accepts MasterCard® debit cards for the purchase of goods and services. Your card may also be used to obtain cash from your designated account at participating financial institutions. Each time you use your POS Access Card, the amount of the transaction will be debited from your designated account. We have the right to return any check or other item drawn against your account to ensure there are funds available to pay for the transactions. We may, but do not have to, allow transactions which exceed your available account balance or, if applicable, your available overdraft protection. If we do, you agree to pay the overdraft.CURRENCY CONVERSION—MasterCard®. If you perform transactions with your card with the MasterCard® logo in a currency other than US dollars, MasterCard International Inc. will convert the charge into a US dollar amount. At MasterCard International they use a currency conversion procedure, which is disclosed to institutions that issue MasterCard®. Currently the currency conversion rate used by MasterCard® International to determine the transaction amount in US dollars for such transactions is generally either a government mandated rate or wholesale rate, determined by MasterCard International for the processing cycle in which the transaction is processed, increased by an adjustment factor established from time to time by MasterCard International. The currency conversion rate used by MasterCard International on the processing date may differ from the rate that would have been used on the purchase date or the cardholder statement posting date.IMPORTANT ADDITIONAL FEE NOTICE: MasterCard charges an Internal Service Fee on all international transactions. Therefore, transactions completed with your MasterCard debit card will be subject to an International Service Assessment (ISA) Fee of 1.100% of the transaction amount when there is a currency conversion. If there is no currency conversion (the transaction is completed in the same currency as your country as cardholder), the ISA Fee will be 0.900% of the transaction amount.9 equitybank.com/community-first

SERVICES PROVIDED THROUGH USE OF EQUITY BANK INFO LINEYou may perform the following functions through use of Equity Bank Info Line.You may initiate transfers of funds between your checking and savings accounts, checking and money market accounts, checking and NOW accounts, savings and money market accounts, savings and NOW accounts, and NOW accounts and money market accounts.You may make balance inquiries on your checking account(s), savings account(s), money market account(s), and NOW account(s).You may change your PIN via the telephone.PREAUTHORIZED TRANSFER SERVICESYou may arrange for the preauthorized automatic deposit of funds to your checking account(s), savings account(s), money market account(s), and NOW account(s).You may arrange for the preauthorized automatic payment of bills from your checking account(s), savings account(s), money market account(s), and NOW account(s).SERVICES PROVIDED THROUGH USE OF EQUITY BANK ON-LINE BANKINGEquity Bank offers its customers use of our Equity Bank On-Line Banking service. You may transfer funds between your checking and savings account(s), checking and money market account(s), checking and NOW account(s), savings and money market account(s), savings and NOW account(s), and NOW account(s) and money market account(s). You may make loan payments to your Equity Bank loan from your Equity Bank deposit account. You may make balance inquiries on your checking account(s), savings account(s), money market account(s), NOW account(s), and any loans. You may view checks that have been presented for payment against your account. You may retrieve account statements on your accounts. You may change your account password. You may pay bills to businesses or individuals. You may initiate payments from your checking account(s), savings account(s), money market account(s), or NOW account(s).For more information about Internet Bill Pay and Internet Banking please visit www.equitybank.com, the Equity Bank location nearest you, or call the Bank at 1-888-733-5041.ELECTRONIC CHECK CONVERSIONYou may authorize a merchant or other payee to make a one-time electronic payment from your checking account using information from your check to pay for purchases or to pay bills.Limitations on TransactionsTRANSACTION LIMITATIONS – ATM CARDCASH WITHDRAWAL LIMITATIONS—You may withdraw up to $505.00 through use of ATMs in any one day. POINT OF SALE LIMITATIONS—You may buy up to $100.00 worth of goods or services in any one day through use of our Point of Sale service.TRANSACTION LIMITATIONS—STANDARD DEBIT CARDCASH WITHDRAWAL LIMITATIONS—You may withdraw up to $505.00 through use of ATMs in any one day. POINT OF SALE LIMITATIONS—You may buy up to $2,500.00 worth of goods or services in any one day through use of our Point of Sale service.TRANSACTION LIMITATIONS—STUDENT DEBIT CARDCASH WITHDRAWAL LIMITATIONS—You may withdraw up to $255.00 through use of ATMs in any one day. POINT OF SALE LIMITATIONS—You may buy up to $250.00 worth of goods or services in any one day through use of our Point of Sale service.OTHER LIMITATIONSConsumers with an Impact Checking or Impact Savings account are not allowed Bill Payment services through On-line Banking.The terms of your account(s) may limit the number of withdrawals you may make each month. Restrictions disclosed at the time you opened your account(s), or sent to you subsequently will also apply to your electronic withdrawals and electronic payments unless specified otherwise. Your standard, student or premier debit card can not be used at rental car companies. These types of transactions have been blocked for your security.We reserve the right to impose limitations for security purposes at any time.LIMITS ON TRANSFERS FROM CERTAIN ACCOUNTS. Federal regulation limits the number of checks, telephone transfers, online transfers and preauthorized electronic transfers to third parties (including Point of Sale transactions) from money market and savings type accounts. You are limited to six such transactions from each money market and/or savings type account(s) you have each statement period for purposes of making a payment to a third party or by use of a telephone or computer.Notice of Rights and ResponsibilitiesThe use of any electronic fund transfer services described in this document creates certain rights and responsibilities regarding these services as described below.RIGHT TO RECEIVE DOCUMENTATION OF YOUR TRANSFERSTRANSACTION RECEIPTS. Depending on the location of an ATM, you may not be given the option to receive a receipt if your transaction is $15.00 or less. Upon completing a transaction of more than $15.00, you will receive a printed receipt documenting the transaction (unless you choose not to get a paper receipt). These receipts (or the transaction number given in place of the paper receipt) should be retained to verify that a transaction was performed. A receipt will be provided for any transaction of more than $15.00 made with your ATM Card or Debit Card at a Participating Merchant. If the transaction is $15.00 or less, the Participating Merchant is not required to provide a receipt.PERIODIC STATEMENTS. If your account is subject to receiving a monthly statement, all EFT transactions will be reported on it. If your account is subject to receiving a statement less frequently than monthly, then you will continue to receive your statement on that cycle, unless there are EFT transactions, in which case you will receive a monthly statement. In any case you will receive your statement at least quarterly. PREAUTHORIZED DEPOSITS. If you have arranged to have direct deposits made to your account at least once every 60 days from the same person or company:? You can call us at 1-888-733-5041 to find out whether or not the deposit has been made.RIGHTS REGARDING PREAUTHORIZED TRANSFERSRIGHTS AND PROCEDURES TO STOP PAYMENTS. If you have instructed us to make regular preauthorized transfers out of your account, you may stop any of the payments. To stop a payment, Call us at: Or write to: 1-888-733-5041 Equity Bank Po Box 730 Andover, KS 67002 We must receive your call or written request at least three (3) business days prior to the scheduled payment. If you call, please have the following information ready: your account number, the date the transfer is to take place, to whom the transfer is being made and the amount of the scheduled transfer. If you call, we will require you to put your request in writing and deliver it to us within fourteen (14) days after you call. NOTICE OF VARYING AMOUNTS. If you have arranged for automatic periodic payments to be deducted from your checking or savings account and these payments vary in amount, you will be notified by the person or company you are going to pay ten days prior to the payment date of the amount to be deducted. You may choose instead to get this notice only when the payment would differ by more than a certain amount from the previous payment, or when the amount would fall outside certain limits that you set.OUR LIABILITY FOR FAILURE TO STOP PREAUTHORIZED TRANSFER PAYMENTS. If you order us to stop one of the payments and have provided us with the information we need at least three (3) business days prior to the scheduled transfer, and we do not stop the transfer, we will be liable for your losses or damages.YOUR RESPONSIBILITY TO NOTIFY US OF LOSS OR THEFTIf you believe your ATM Card or Debit Card or PIN or internet banking access code has been lost or stolen, call us at: 1-888-733-5041 (9:00 am—5:00 pm M-F) Or write to: Equity Bank PO Box 730 Andover, KS 67002 You should also call the number or write to the address listed above if you believe a transfer has been made using the information from your check without your permission.CONSUMER LIABILITYTell us at once if you believe your ATM Card or Debit Card or PIN or internet banking access code has been lost or stolen, or if you believe that an electronic fund transfer has been made without your permission using information from your check. Telephoning is the best way of keeping your possible losses down.FOR CARDS. If someone uses your ATM Card or Debit Card without your permission, your liability will not exceed $50.00 if you notify us within two(2) business days after learning of the loss or theft of the ATM Card or Debit Card If you fail to notify us within this time frame, you can lose as much as $500.00. FOR UNAUTHORIZED TRANSFERS. If your statement shows transfers you did not make, including those made by card, code, or other means, tell us at once. If you do not tell us within sixty (60) days after the periodic statement or receipt was transmitted to you, you may not receive back any of the money you lost after the sixty (60) days, and therefore, you could lose all the money in your account (plus your maximum overdraft line of credit, if applicable), if we can prove that we could have stopped someone from taking the money had you given us notice in time.If a good reason (such as a long trip or hospital stay) keeps you from giving the notice, we will extend the time period.CONSUMER LIABILITY FOR UNAUTHORIZED TRANSACTIONS INVOLVING STANDARD DEBIT CARD, STUDENT DEBIT CARD OR PREMIER DEBIT CARDThe limitations on your liability for unauthorized transactions described above generally apply to all electronic fund transfers. However, different limitations apply to transactions involving your card with the MasterCard® logo. These limits apply to all unauthorized transactions processed through your MasterCard® logo card.If you notify us about an unauthorized transaction involving your Standard Debit Card, Student Debit Card or Premier Debit Card within (4) business days after learning of the loss or theft, zero liability will be imposed on you for the unauthorized transaction. In order to qualify for the zero liability protection, you must have exercised reasonable care in safeguarding your card from the risk of loss or theft, you must not have reported two or more incidents of unauthorized use within the preceding twelve (12) months, and your account must be in good standing. Otherwise your liability for unauthorized transactions will not exceed the liability described under “Consumer Liability” above.ILLEGAL USE OF DEBIT CARD. You agree not to use your Debit Card for any illegal transactions, including internet gambling and similar activities.IN CASE OF ERRORS OR QUESTIONS ABOUT YOUR TRANSACTIONSIn case of errors or questions about your electronic fund transfers, call us at: 1-888-733-504110 equitybank.com/community-first

Or write to: Equity Bank PO Box 730 Andover, KS 67002Or email us at: depositops@equitybank.comOr use the current information on your most recent account statement.Notification should be made as soon as possible if you think your statement or receipt is wrong or if you need more information about a transaction listed on the statement or receipt. You must contact Equity Bank no later than 60 days after it sent you the first statement on which the problem or error appears. You must be prepared to provide the following information:‰ Your name and account number.‰ A description of the error or transaction you are unsure about along with an explanation as to why you believe it is an error or why you need more information.‰ The dollar amount of the suspected error.If you provide oral notice, you will be required to send in your complaint or question in writing within ten (10) business days.We will determine whether an error occurred within ten (10) business days (twenty (20) business days for new accounts) after we hear from you and will correct any error promptly. If we need more time, however, we may take up to forty-five (45) days (ninety (90) days for new accounts and foreign initiated or Point of Sale transfers) to investigate your complaint or question. If we decide to do this, we will credit your account within ten (10) business days (twenty (20) business days for new accounts) for the amount which you think is in error, so that you will have the use of the money during the time it takes to complete our investigation. If we ask you to put your complaint or question in writing and we do not receive it within ten (10) business days, we may not credit your account. The extended time periods for new accounts apply to all electronic fund transfers that occur within the first thirty (30) days after the first deposit to the account is made, including those for foreign initiated or Point of Sale transactions.We will tell you the results within three (3) business days after completing our investigation. If we decide that there was no error, we will send you a written explanation.You may ask for copies of the documents that we used in our investigation.LIABILITY FOR FAILURE TO COMPLETE TRANSACTIONIf we do not complete a transfer to or from your account on time or in the correct amount according to our agreement with you, we will be liable for your losses or damages as provided by law. However, there are some exceptions. We will NOT be liable, for instance:‰ If through no fault of ours, you do not have enough money in your account to make the transfer.‰ If the transfer would result in your exceeding the credit limit on your line of credit, if you have one.‰ If the electronic terminal was not working properly and you knew about the breakdown before you started the transfer.‰ If circumstances beyond our control (such as fire or flood, computer or machine breakdown, or failure or interruption of communications facilities) prevent the transfer, despite reasonable precautions we have taken.‰ If we have terminated our Agreement with you.‰ When your ATM Card or Debit Card has been reported lost or stolen or we have reason to believe that something is wrong with a transaction.‰ If we receive inaccurate or incomplete information needed to complete a transaction.‰ In the case of preauthorized transfers, we will not be liable where there is a breakdown of the system which would normally handle the transfer.‰ If the funds in the account are subject to legal action preventing a transfer to or from your account.‰ If the electronic terminal does not have enough cash to complete the transaction. There may be other exceptions provided by applicable law.CHARGES FOR TRANSFERS OR THE RIGHT TO MAKE TRANSFERS Overdraft Transfer from Line of Credit—per transfer $11.00 Automatic Loan Transfer Payment FREE CARD FEES The following fees and charges may be imposed on your attached account. ATM Card Replacement $5.00 Debit Card Replacement $5.00 PIN Replacement for ATM or Debit Cards $5.00 Swipe with Style Debit Cards FREE Swipe with Style Debit Card Replacements $5.00 My Debit Card Design FREE My Debit Card Design Replacement $5.00 DISCLOSURE OF ACCOUNT INFORMATIONYou agree that merchant authorization messages transmitted in connection with Point of Sale transactions are permissible disclosures of account information, and you further agree to release Equity Bank and hold it harmless from any liability arising out of the transmission of these messages.We will disclose information to third parties about your account or electronic fund transfers made to your account:1. Where necessary to complete a transfer or to investigate and resolve errors involving the transfer(s); or 2. In order to verify the existence and condition of your account for a third party such as a credit bureau or merchant; or 3. In order to comply with government agency or court orders; or 4. With your consent.DEFINITION OF BUSINESS DAYBusiness days are Monday through Friday excluding holidays.AMENDING OR TERMINATING THE AGREEMENTWe may change or amend any of the terms and conditions of the Agreement and those portions of the applicable fee schedules which relate to EFT services, at any time upon at least 21 days written notice to you prior to the effective date of the change or amendment. Your failure to timely furnish notice as set forth in the written notice shall be deemed to be your acceptance of such change or amendment. If you do not agree to abide by a change or amendment, you must notify Equity Bank of the fact prior to the effective date of the change or amendment and cancel this Agreement. Equity Bank may cancel this Agreement at any time, without giving you prior notice. If you or Equity Bank cancels this Agreement at any time, you shall surrender your ATM Card or Debit Card and you may no longer use any of Equity Bank’s EFT services other than the automated clearing house transfer services set forth above.NOTICE OF ATM SAFETY PRECAUTIONSSAFETY PRECAUTIONS FOR ATM TERMINAL USAGE. Please keep in mind the following basic safety tips whenever you use an ATM:‰ Have your ATM Card or Debit Card ready to use when you reach the ATM. Have all of your forms ready before you get to the machine. Keep some extra forms (envelopes) at home for this purpose.‰ If you are new to ATM usage, use machines close to or inside a financial institution until you become comfortable and can conduct your usage quickly.‰ If using an ATM in an isolated area, take someone else with you if possible. Have them watch from the car as you conduct your transaction.‰ Do not use ATMs at night unless the area and machine are well-lighted. If the lights are out, go to a different location.‰ If someone else is using the machine you want to use, stand back or stay in your car until the machine is free. Watch out for suspicious people lurking around ATMs, especially during the times that few people are around.‰ When using the machine, stand so you block anyone else’s view from behind.‰ If anything suspicious occurs when you are using a machine, cancel what you are doing and leave immediately. If going to your car, lock your doors.‰ Do not stand at the ATM counting cash. Check that you received the right amount later in a secure place, and reconcile it to your receipt then.‰ Keep your receipts and verify transactions on your account statement. Report errors immediately. Do not leave receipts at an ATM location.Additional ProvisionsYour account is also governed by the terms and conditions of other applicable agreements between you and Equity Bank.You agree not to reveal your PIN to any person not authorized by you to access your account.We may offer a discretionary, non contractual means of paying your overdrafts. However, we DO NOT authorize and pay overdrafts for any of the following types of transactions unless you ask us to:‰ ATM Transactions, including cash withdrawals and transfers between accounts, or‰ Everyday debit card transactions, such as purchasing items at a store.If you authorize us to pay overdrafts, you agree to repay any overdraft and any overdraft fees caused by using your card. Unless stated on your ATM’s screen, a sign near the ATM, and/or your transaction receipt, your stated balance does not include this overdraft protection. You understand that even if you check your account balance immediately prior to using your card, items such as checks you have written or recent credit/debit activities may not yet have been posted to your account. You may also, for example, have sufficient funds to use your card, but still cause an overdraft on a check that has not yet been processed. If you want to avoid an overdraft, you agree to reconcile your account by checking your periodic statements and any outstanding unpaid items before using your card.11 equitybank.com/community-first

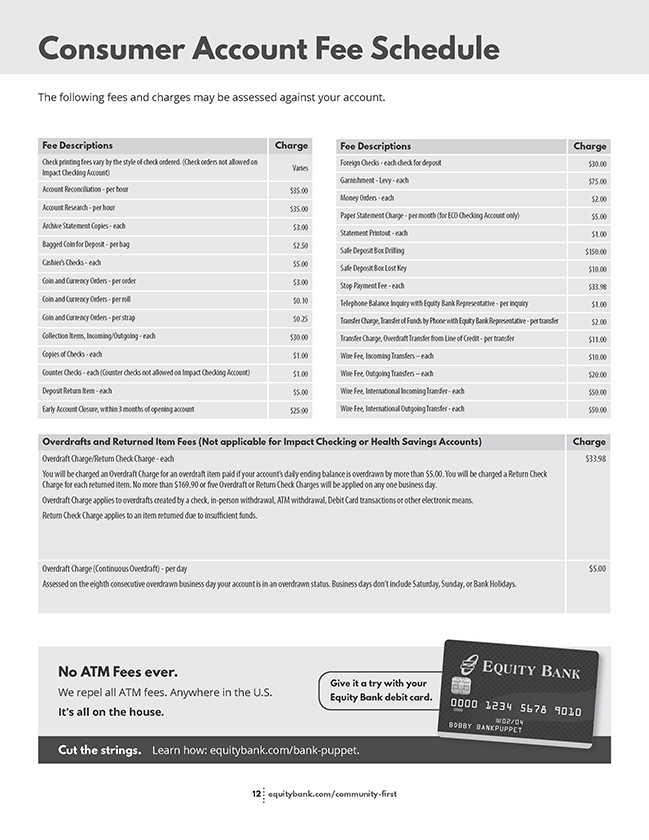

Consumer Account Fee ScheduleThe following fees and charges may be assessed against your account. Fee Descriptions Charge Check printing fees vary by the style of check ordered. (Check orders not allowed on Impact Checking Account) Varies Account Reconciliation - per hour $35.00 Account Research - per hour $35.00 Archive Statement Copies - each $3.00 Bagged Coin for Deposit - per bag $2.50 Cashier’s Checks - each $5.00 Coin and Currency Orders - per order $3.00 Coin and Currency Orders - per roll $0.10 Coin and Currency Orders - per strap $0.25 Collection Items, Incoming/Outgoing - each $30.00 Copies of Checks - each $1.00 Counter Checks - each (Counter checks not allowed on Impact Checking Account) $1.00 Deposit Return Item - each $5.00 Early Account Closure, within 3 months of opening account $25.00 Fee Descriptions Charge Foreign Checks - each check for deposit $30.00 Garnishment - Levy - each $75.00 Money Orders - each $2.00 Paper Statement Charge - per month (for ECO Checking Account only) $5.00 Statement Printout - each $1.00 Safe Deposit Box Drilling $150.00 Safe Deposit Box Lost Key $10.00 Stop Payment Fee - each $33.98 Telephone Balance Inquiry with Equity Bank Representative - per inquiry $1.00 Transfer Charge, Transfer of Funds by Phone with Equity Bank Representative - per transfer $2.00 Transfer Charge, Overdraft Transfer from Line of Credit - per transfer $11.00 Wire Fee, Incoming Transfers – each $10.00 Wire Fee, Outgoing Transfers – each $20.00 Wire Fee, International Incoming Transfer - each $50.00 Wire Fee, International Outgoing Transfer - each $50.00 Overdrafts and Returned Item Fees (Not applicable for Impact Checking or Health Savings Accounts) Charge Overdraft Charge/Return Check Charge - each $33.98 You will be charged an Overdraft Charge for an overdraft item paid if your account’s daily ending balance is overdrawn by more than $5.00. You will be charged a Return Check Charge for each returned item. No more than $169.90 or five Overdraft or Return Check Charges will be applied on any one business day. Overdraft Charge applies to overdrafts created by a check, in-person withdrawal, ATM withdrawal, Debit Card transactions or other electronic means. Return Check Charge applies to an item returned due to insufficient funds. Overdraft Charge (Continuous Overdraft) - per day $5.00 Assessed on the eighth consecutive overdrawn business day your account is in an overdrawn status. Business days don’t include Saturday, Sunday, or Bank Holidays. No ATM Fees ever.We repel all ATM fees. Anywhere in the U.S.It’s all on the house.Cut the strings. Learn how: equitybank.com/bank-puppet.12 equitybank.com/community-first

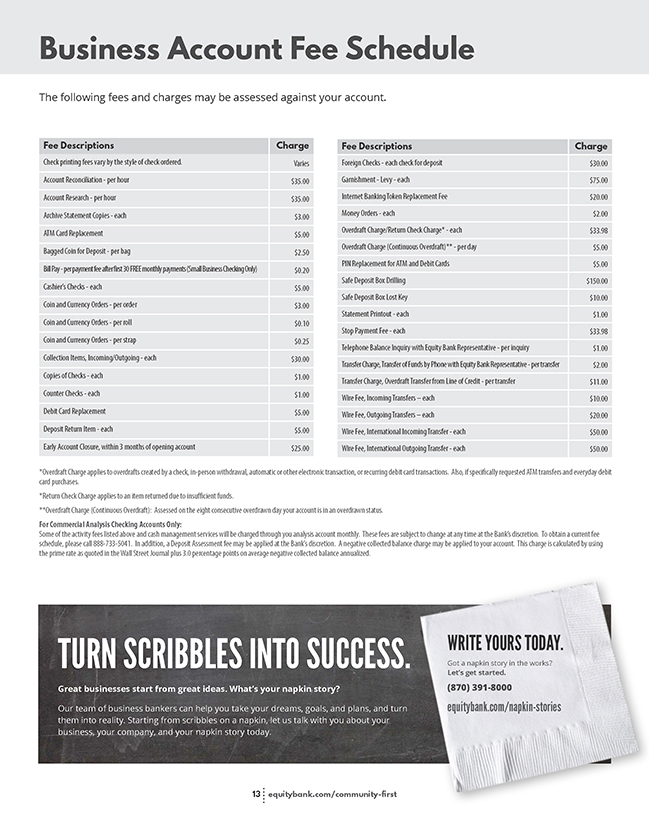

Business Account Fee ScheduleThe following fees and charges may be assessed against your account. Fee Descriptions Charge Check printing fees vary by the style of check ordered. Varies Account Reconciliation - per hour $35.00 Account Research - per hour $35.00 Archive Statement Copies - each $3.00 ATM Card Replacement $5.00 Bagged Coin for Deposit - per bag $2.50 Bill Pay - per payment fee after first 30 FREE monthly payments (Small Business Checking Only) $0.20 Cashier’s Checks - each $5.00 Coin and Currency Orders - per order $3.00 Coin and Currency Orders - per roll $0.10 Coin and Currency Orders - per strap $0.25 Collection Items, Incoming/Outgoing - each $30.00 Copies of Checks - each $1.00 Counter Checks - each $1.00 Debit Card Replacement $5.00 Deposit Return Item - each $5.00 Early Account Closure, within 3 months of opening account $25.00 Fee Descriptions Charge Foreign Checks - each check for deposit $30.00 Garnishment - Levy - each $75.00 Internet Banking Token Replacement Fee $20.00 Money Orders - each $2.00 Overdraft Charge/Return Check Charge* - each $33.98 Overdraft Charge (Continuous Overdraft)** - per day $5.00 PIN Replacement for ATM and Debit Cards $5.00 Safe Deposit Box Drilling $150.00 Safe Deposit Box Lost Key $10.00 Statement Printout - each $1.00 Stop Payment Fee - each $33.98 Telephone Balance Inquiry with Equity Bank Representative - per inquiry $1.00 Transfer Charge, Transfer of Funds by Phone with Equity Bank Representative - per transfer $2.00 Transfer Charge, Overdraft Transfer from Line of Credit - per transfer $11.00 Wire Fee, Incoming Transfers – each $10.00 Wire Fee, Outgoing Transfers – each $20.00 Wire Fee, International Incoming Transfer - each $50.00 Wire Fee, International Outgoing Transfer - each $50.00 *Overdraft Charge applies to overdrafts created by a check, in-person withdrawal, automatic or other electronic transaction, or recurring debit card transactions. Also, if specifically requested ATM transfers and everyday debit card purchases. *Return Check Charge applies to an item returned due to insufficient funds. **Overdraft Charge (Continuous Overdraft): Assessed on the eight consecutive overdrawn day your account is in an overdrawn status.For Commercial Analysis Checking Accounts Only: Some of the activity fees listed above and cash management services will be charged through you analysis account monthly. These fees are subject to change at any time at the Bank’s discretion. To obtain a current fee schedule, please call 888-733-5041. In addition, a Deposit Assessment fee may be applied at the Bank’s discretion. A negative collected balance charge may be applied to your account. This charge is calculated by using the prime rate as quoted in the Wall Street Journal plus 3.0 percentage points on average negative collected balance annualized. TURN SCRIBBLES INTO SUCCESSGreat businesses start from great ideas. What’s your napkin story?Our team of business bankers can help you take your dreams, goals, and plans, and turn them into reality. Starting from scribbles on a napkin, let us talk with you about your business, your company, and your napkin story tWRITE YOURS TODAY.Got a napkin story in the works? Let’s get started.(870) 391-8000equitybank.com/napkin-stories13 equitybank.com/community-first

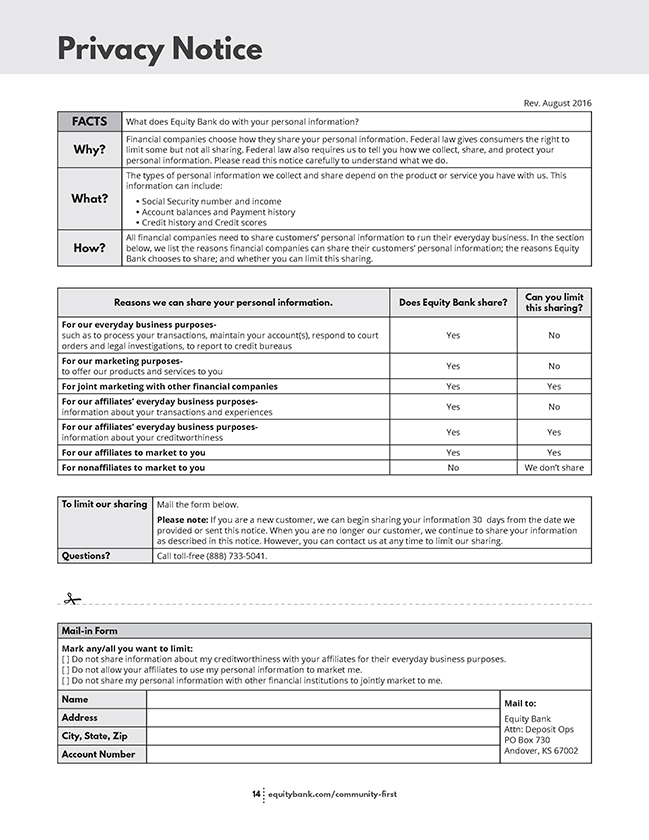

Privacy NoticeRev. August 2016 FACTS What does Equity Bank do with your personal information Financial companies choose how they share your personal information. Federal law gives consumers the right to Why limit some but not all sharing. Federal law also requires us to tell you how we collect, share, and protect your personal information. Please read this notice carefully to understand what we do. The types of personal information we collect and share depend on the product or service you have with us. This information can include: What • Social Security number and income • Account balances and Payment history • Credit history and Credit scores All financial companies need to share customers’ personal information to run their everyday business. In the section How below, we list the reasons financial companies can share their customers’ personal information; the reasons Equity Bank chooses to share; and whether you can limit this sharing. Reasons we can share your personal information. Does Equity Bank share Can you limit this sharing For our everyday business purposes- such as to process your transactions, maintain your account(s), respond to court Yes No orders and legal investigations, to report to credit bureaus For our marketing purposes- Yes No to offer our products and services to you For joint marketing with other financial companies Yes Yes For our affiliates’ everyday business purposes- Yes No information about your transactions and experiences For our affiliates’ everyday business purposes- Yes Yes information about your creditworthiness For our affiliates to market to you Yes Yes For nonaffiliates to market to you No We don’t share To limit our sharing Mail the form below. Please note: If you are a new customer, we can begin sharing your information 30 days from the date we provided or sent this notice. When you are no longer our customer, we continue to share your information as described in this notice. However, you can contact us at any time to limit our sharing. Questions Call toll-free (888) 733-5041. Mail-in FormMark any/all you want to limit: [ ] Do not share information about my creditworthiness with your affiliates for their everyday business purposes. [ ] Do not allow your affiliates to use my personal information to market me. [ ] Do not share my personal information with other financial institutions to jointly market to me. Name Mail to: Address Equity Bank Attn: Deposit Ops City, State, Zip PO Box 730 Account Number Andover, KS 67002 14 equitybank.com/community-first

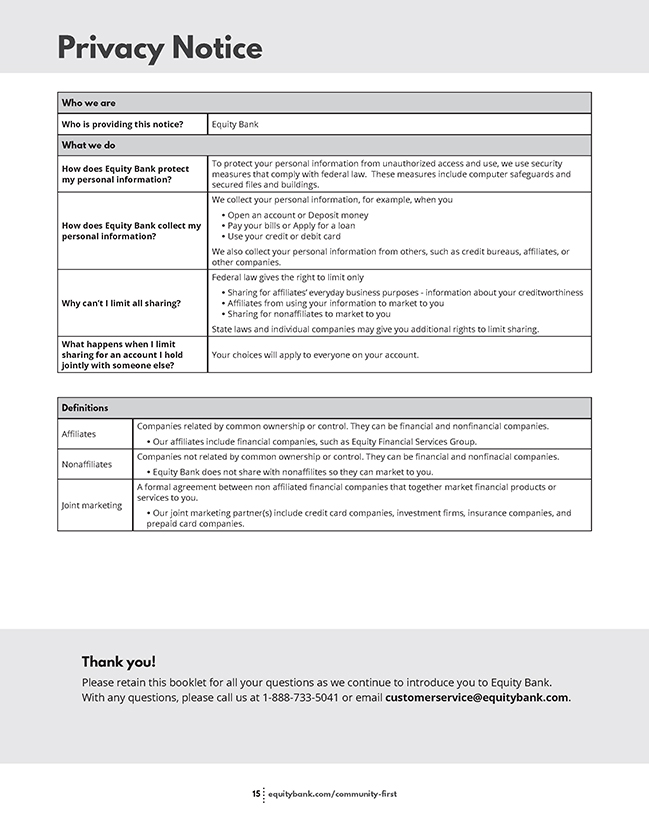

Privacy Notice Who we are Who is providing this notice Equity Bank What we do How does Equity Bank protect To protect your personal information from unauthorized access and use, we use security my personal information measures that comply with federal law. These measures include computer safeguards and secured files and buildings. We collect your personal information, for example, when you • Open an account or Deposit money How does Equity Bank collect my • Pay your bills or Apply for a loan personal information • Use your credit or debit card We also collect your personal information from others, such as credit bureaus, affiliates, or other companies. Federal law gives the right to limit only • Sharing for affiliates’ everyday business purposes - information about your creditworthiness Why can’t I limit all sharing • Affiliates from using your information to market to you • Sharing for nonaffiliates to market to you State laws and individual companies may give you additional rights to limit sharing. What happens when I limit sharing for an account I hold Your choices will apply to everyone on your account. jointly with someone else Definitions Companies related by common ownership or control. They can be financial and nonfinancial companies. Affiliates • Our affiliates include financial companies, such as Equity Financial Services Group. Companies not related by common ownership or control. They can be financial and nonfinacial companies. Nonaffiliates • Equity Bank does not share with nonaffilites so they can market to you. A formal agreement between non affiliated financial companies that together market financial products or services to you. Joint marketing • Our joint marketing partner(s) include credit card companies, investment firms, insurance companies, and prepaid card companies. Thank you!Please retain this booklet for all your questions as we continue to introduce you to Equity Bank. With any questions, please call us at 1-888-733-5041 or email customerservice@equitybank.com.15 equitybank.com/community-first