UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 or 15(d) of The Securities Exchange Act of 1934

Date of Report (Date of earliest event reported): July 19, 2021

EQUITY BANCSHARES, INC.

(Exact name of registrant as specified in its charter)

Kansas | 001-37624 | 72-1532188 |

(State or other jurisdiction of incorporation or organization) | (Commission File Number) | (I.R.S. Employer Identification No.) |

|

|

|

7701 East Kellogg Drive, Suite 300 Wichita, KS |

|

67207 |

(Address of principal executive offices) |

| (Zip Code) |

Registrant’s telephone number, including area code: 316.612.6000

Former name or former address, if changed since last report: Not Applicable

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

☒ | Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

☐ | Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

☐ | Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Securities registered pursuant to Section 12(b) of the Act:

Title of each class Class A, Common Stock, par value $0.01 per share | Trading Symbol EQBK | Name of each exchange on which registered The Nasdaq Stock Market LLC |

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter).

☐ Emerging growth company

☐ If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Item 2.02Results of Operations and Financial Condition.

On July 19, 2021, Equity Bancshares, Inc. (the “Company”) issued a press release announcing its financial results for the second quarter ended June 30, 2021. A copy of the press release is furnished as Exhibit 99.1 and is incorporated by reference herein.

The information in this Item 2.02, including Exhibit 99.1, is being furnished pursuant to Item 2.02 of Form 8-K and shall not be deemed “filed” for purposes of Section 18 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), or otherwise subject to liabilities of that section, nor shall it be deemed incorporated by reference into any filing under the Securities Act of 1933, as amended (the “Securities Act”), or the Exchange Act, unless specifically identified therein as being incorporated therein by reference.

Item 7.01Regulation FD Disclosure.

Branch Purchase and Assumption

On July 19, 2021, Equity Bancshares, Inc. (the ”Company”) announced that Equity Bank (“Equity Bank”), a wholly owned subsidiary of the Company, signed a definitive branch purchase and assumption agreement to acquire the assets and assume the deposits of three bank locations from Security Bank of Kansas City (“Security”), a subsidiary of Valley View Financial Co. (“Valley”) of Overland Park, Kansas. The Company anticipates closing the transaction in the fourth quarter of 2021.

Quarterly Investor Call

The Company intends to hold an investor call and webcast to discuss its financial results for the second quarter ended June 30, 2021 on Tuesday, July 20, 2021, at 9:00 a.m. Central Time. The Company’s presentation to analysts and investors contains additional information about the Company’s financial results for the second quarter ended June 30, 2021 and is furnished as Exhibit 99.2 and is incorporated by reference herein.

The information in this Item 7.01, including Exhibit 99.2, is being furnished pursuant to Item 7.01 of Form 8-K and shall not be deemed “filed” for purposes of Section 18 of the Exchange Act, or otherwise subject to liabilities of that section, nor shall it be deemed incorporated by reference into any filing under the Securities Act or the Exchange Act, unless specifically identified therein as being incorporated therein by reference.

Item 8.01Other Events.

The only information contained in this Form 8-K being filed for the purposes of Rule 425 of the Securities Act is the information relating solely to the previously announced proposed merger between the Company and American State Bancshares, Inc. contained in the press release furnished herewith as Exhibit 99.1.

Item 9.01Financial Statements and Exhibits.

(d) Exhibits

Exhibit No. |

| Description |

99.1 |

| Earnings Press Release, dated July 19, 2021 |

99.2 |

| Equity Bancshares, Inc. Investor Presentation |

104 |

| Cover Page Interactive Data File |

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| Equity Bancshares, Inc. |

|

|

Date: July 19, 2021 | By: /s/ Eric R. Newell |

| Eric R. Newell |

| Executive Vice President and Chief Financial Officer |

Exhibit 99.1

Equity Bancshares, Inc.

PRESS RELEASE - 07/19/2021

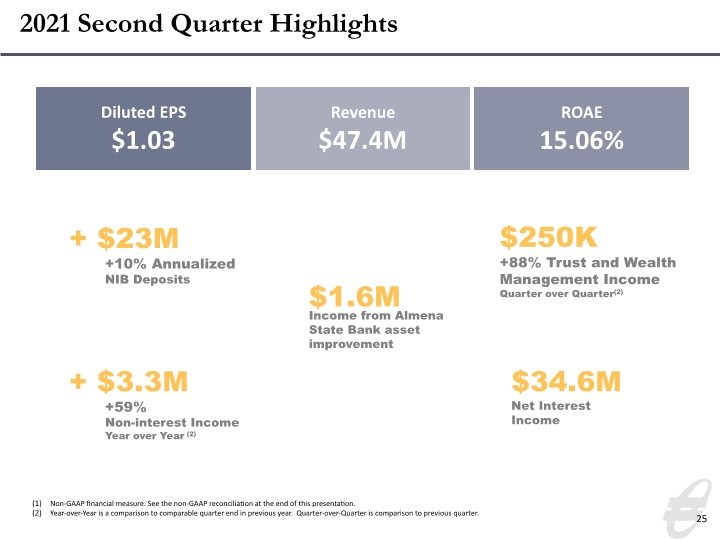

Equity Bancshares, Inc. Second Quarter Results Include Strong Organic Loan Growth, Company to Acquire St. Joseph Bank Locations, Expanding Missouri Network

Annualized organic non-PPP loan growth contributes to $1.03 per diluted share,

Company will acquire three Security Bank of KC branch locations in St. Joseph, Missouri

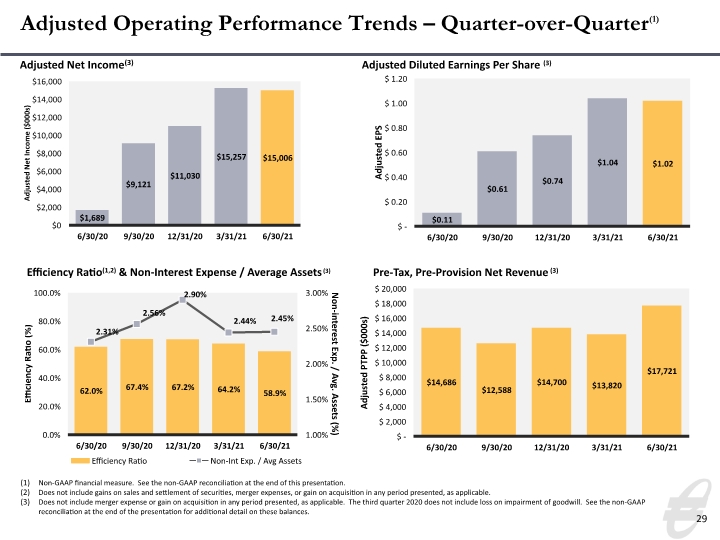

WICHITA, Kansas, July 19, 2021 (GLOBE NEWSWIRE) – Equity Bancshares, Inc. (NASDAQ: EQBK), (“Equity”, “the Company”, “we”, “us”, “our”), the Wichita-based holding company of Equity Bank, reported net income of $15.2 million and $1.03 per diluted share for the second quarter ended June 30, 2021.

“Our Equity Bank team had an excellent quarter serving our customers, expanding our delivery channels and adding shareholder value. Exclusive of the Paycheck Protection Program, we organically grew gross loans by $81.8 million, an annualized rate of 14.75%, through the focused efforts of our sales and operational teams,” said Brad S. Elliott, Chairman and CEO of Equity. “A key component of our results is growth in our core deposit customer base, with new banking products contributing to a $1.1 million increase in service fee revenue, as well as the continued addition of trust and wealth management customer relationships.”

Equity customers successfully had $99.7 million of Paycheck Protection Program (“PPP”) loans forgiven during the quarter, resulting in the recognition of fee income totaling $5.7 million in the three-month period ended June 30, 2021. At June 30, 2021, the total unrecognized fee income associated with PPP loans was $10.7 million. Through two rounds of PPP, Equity originated more than $610.0 million in PPP loans.

Further driving results this quarter was customer and relationship growth within Equity Trust and Wealth Management and Equity’s consumer deposit base, expansion of non-interest income with Equity’s debit card platform and increased transaction activity within our deposit customer base.

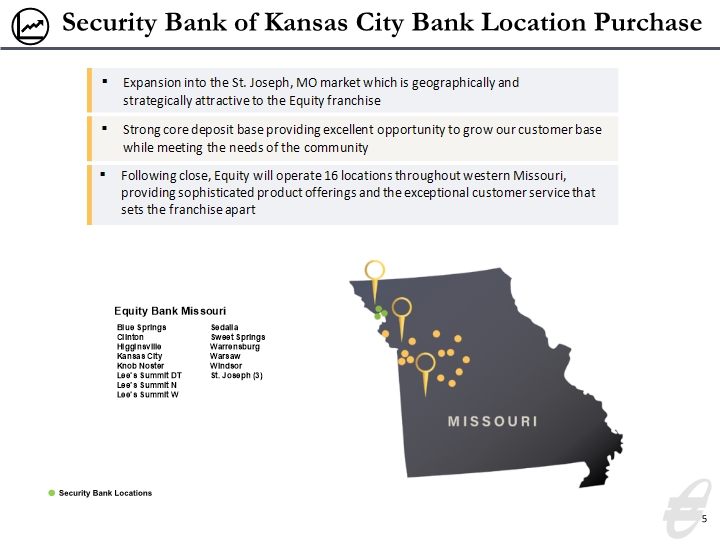

The Company has announced its expansion into St. Joseph, Missouri, with a definitive branch purchase and assumption agreement to acquire the assets and assume the deposits of three bank locations from Security Bank of Kansas City (“Security”), a subsidiary of Valley View Financial Co. (“Valley”) of Overland Park, Kansas. Equity anticipates closing the transaction in the fourth quarter of 2021.

“We are pleased with the opportunity to offer Equity Bank products and services to customers in Northwest Missouri, and St. Joseph is a great fit within our network,” said Mr. Elliott. “We have been able to grow loans, fee income and our core deposit base effectively in Western Missouri with a focus on local community banking and we believe this approach will serve customers well in our new St. Joseph region.”

“Our recent merger announcement with American State Bancshares, Inc. is a great cultural fit for us as well as an expansion of our Kansas market, and our teams have worked diligently alongside one another. We remain on target for a closing and conversion of data systems in early October,” said Mr. Elliott. “I thank everyone on both the Equity and American State Bancshares, Inc. teams for their collaboration and hard work to make sure we continue to deliver excellent customer service while increasing shareholder value.”

Notable Items:

| • | Quarter over quarter, service fee revenue, including deposit services, mortgage banking, trust and wealth and insurance services increased to $6.4 million from $5.3 million, or 20.77%. |

| • | The Company authorized a second stock repurchase program in the third quarter of 2020 totaling 800,000 shares. During the quarter ended June 30, 2021, the Company repurchased 73,070 shares at a weighted average cost of $28.94 per share, totaling $2.1 million. At the end of the quarter, capacity of 180,687 shares remained under the current repurchase program. |

Equity Bancshares, Inc.

PRESS RELEASE - 07/19/2021

| • | Additional information attained on the assets purchased through the Almena State Bank (“Almena”) transaction indicated a more positive outcome than originally expected, resulting in a net reduction in reserves on the balance sheet and an increase in gain on acquisition of $663 thousand during the quarter. |

| • | During the quarter ended June 30, 2021, there was a release of allowance for credit losses of $1.7 million as compared to a release of $5.8 million in the quarter ended March 31, 2021. The release in the second quarter was driven primarily by improvement in assets specifically assessed for impairment as asset quality improved quarter over quarter. |

Equity’s Balance Sheet Highlights:

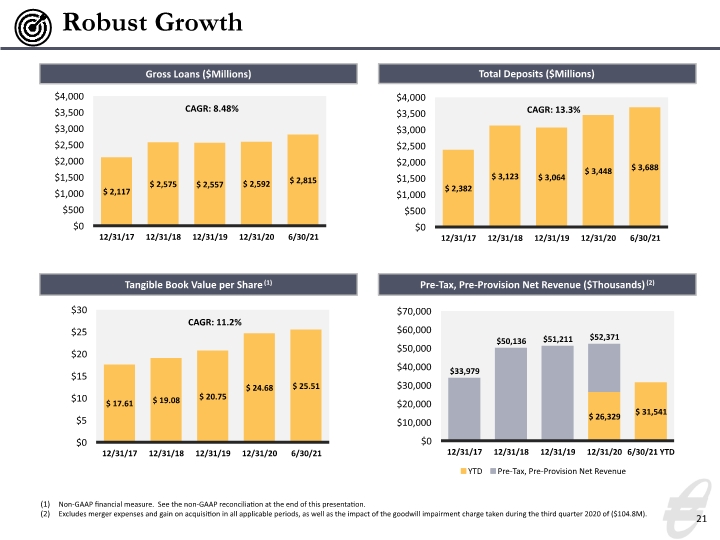

| • | Total loans held for investment of $2.82 billion at June 30, 2021, as compared to total loans held for investment of $2.80 billion at March 31, 2021. The periodic change included organic loan production of $81.8 million, or 14.75%. |

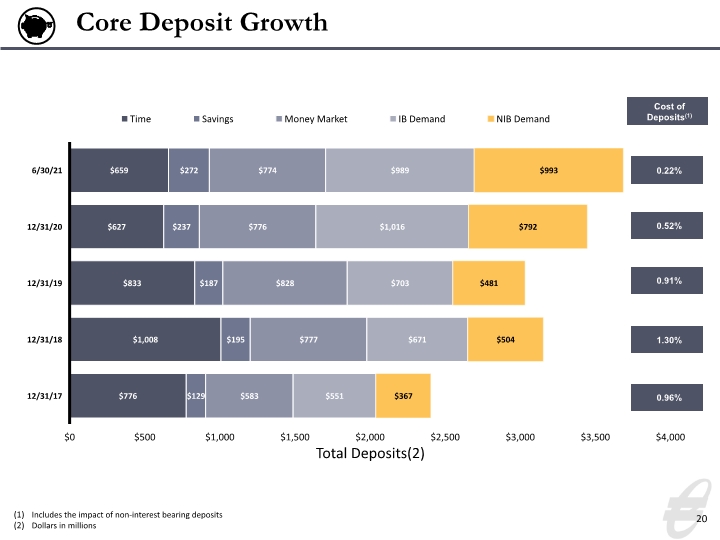

| • | Total deposits of $3.69 billion at June 30, 2021, as compared to $3.63 billion at March 31, 2021. Checking, savings and money market accounts were $3.03 billion at June 30, 2021, relative to $3.05 billion at March 31, 2021. Included in the periodic change was a $20.2 million increase in non-interest-bearing deposits. As compared to December 31, 2020, the Bank has increased non-interest-bearing deposits by $200.9 million, or 25.38%. |

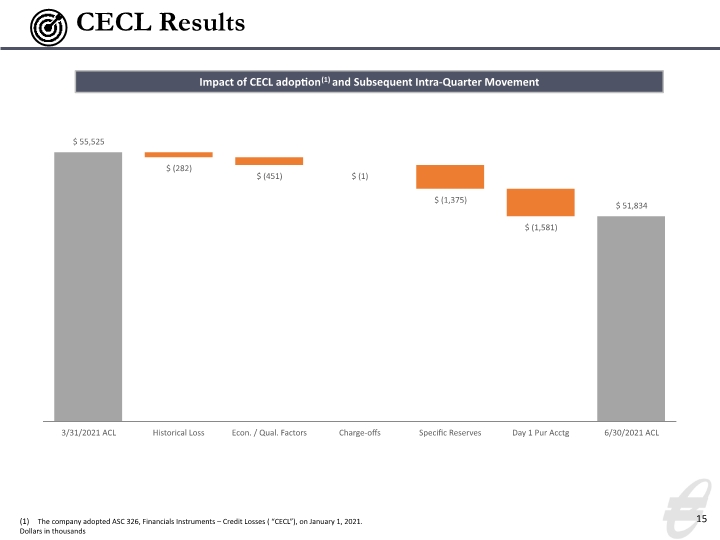

| • | The allowance for credit losses as of June 30, 2021, was $51.8 million, or 1.84% of total loans and 2.04% of total loans excluding PPP assets. |

Acquisition of Three Bank Locations in St. Joseph, Missouri

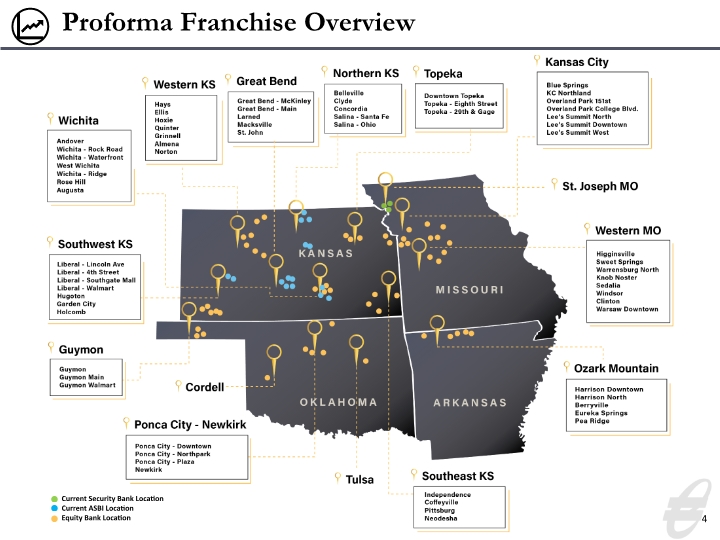

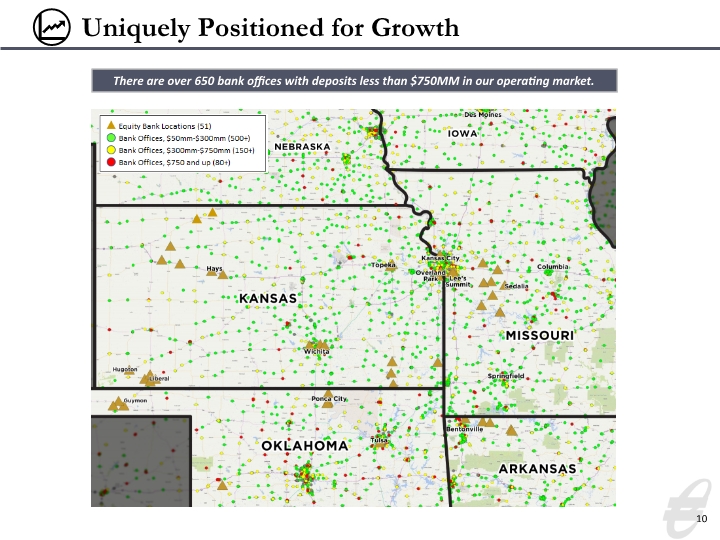

Equity will operate each of the three Security locations in St. Joseph as Equity Bank locations following completion of the acquisition, expected in December of 2021. Joshua J. Means, President of Western Missouri, will oversee the St. Joseph community bank locations. Equity will operate a total of 16 locations in Missouri, including the three Security locations, eight bank locations in legacy Western Missouri communities and five bank locations on the Missouri side of the Kansas City metropolitan area.

In Equity’s Western Missouri region, notable for communities like Warrensburg, Sedalia and Higginsville, deposits as of June 30, 2018, were $478.4 million, compared to $614.8 million as of June 30, 2021. Total loans in Equity’s Western Missouri region were $147.0 million as of June 30, 2018, compared to $218.3 million as of June 30, 2021, growing by 48.5% during the three-year period.

“Each of our Missouri locations delivers outstanding service to our consumer, mortgage and business customers and we expect St. Joseph to serve as a key market for us in Northwest Missouri. Josh Means and his regional leadership team have helped our local banks grow in loans, fee income and deposits, one relationship at a time,” said Mr. Elliott. “We are pleased to welcome talented community bankers to our Equity team and to offer St. Joseph-area consumers enhanced commercial and business banking solutions.”

Equity announced in May its merger with American State Bancshares, Inc. (“ASBI”), the holding company of American State Bank, a $779 million bank with headquarters in Wichita, Kansas, and 17 locations in its Kansas footprint. Equity expects to complete the merger with ASBI in October 2021. Pro forma Equity Bank, including ASBI and Security deposits and locations, will comprise more than 70 locations throughout our four-state footprint and hold more than $5 billion in assets.

Pursuant to the terms of the Branch Purchase and Assumption Agreement, between Equity Bank and Security, Equity will acquire certain loans and other branch-related assets and assume certain deposits and other liabilities associated with the Security branches.

Equity Bancshares, Inc.

PRESS RELEASE - 07/19/2021

Financial Results for the Quarter Ended June 30, 2021

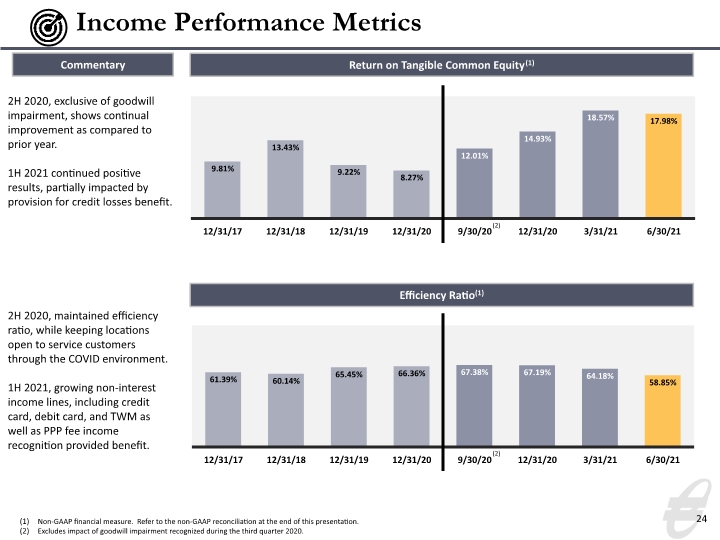

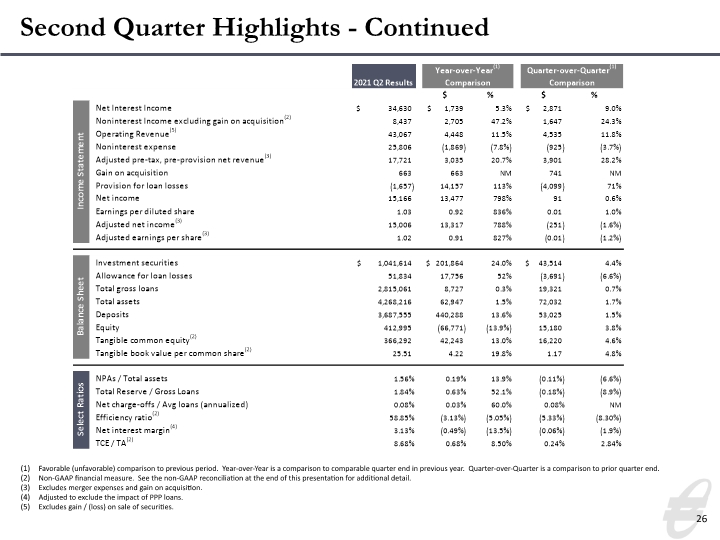

Net income allocable to common stockholders was $15.2 million, or $1.03 per diluted share, for the three months ended June 30, 2021, as compared to $15.1 million, or $1.02 per diluted share, for the three months ended March 31, 2021, an increase of $91 thousand. This second quarter increase was attributable to a net interest income increase of $2.9 million and a non-interest income increase of $2.4 million, partially offset by a $4.1 million decrease in reversal of provision for credit losses, a $925 thousand increase in non-interest expense and a $144 thousand increase in provision for income taxes.

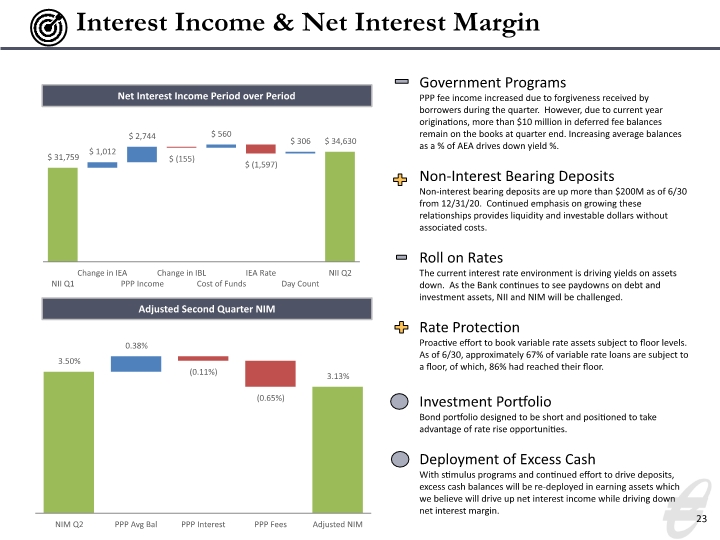

Net Interest Income

Net interest income was $34.6 million for the three months ended June 30, 2021, as compared to $31.8 million for the three months ended March 31, 2021, an increase of $2.9 million, or 9.0%. The increase in net interest income was primarily driven by a 15-basis point increase in the average yield earned on interest-earning assets, to 3.88% for the quarter ended June 30, 2021, from 3.73% for the quarter ended March 31, 2021. In addition, there was a 6-basis point decrease in average rate paid on interest-bearing liabilities, to 0.52% for the quarter ended June 30, 2021, from 0.58% for the quarter ended March 31, 2021. The cost of interest-bearing deposits declined by 5 basis points to 0.31% for the three months ended June 30, 2021 from 0.36% in the previous quarter primarily attributed to the reduction in the cost of time deposits, that slipped 19 basis points between the quarters.

Provision for Credit Losses

During the three months ended June 30, 2021, there was a net release of $1.7 million in the allowance for credit losses recognized through the provision for credit losses as compared to a net release of $5.8 million provision for credit losses for the three months ended March 31, 2021. For the three months ended June 30, 2021, we had net charge-offs of $567 thousand as compared to $65 thousand for the three months ended March 31, 2021. The release in the second quarter was driven primarily by improvement in assets individually evaluated for impairment as asset quality improved quarter over quarter.

Non-Interest Income

Total non-interest income was $9.1 million for the three months ended June 30, 2021, as compared to $6.7 million for the three months ended March 31, 2021, or $8.4 million excluding the $663 thousand net gain on the purchase and assumption of Almena State Bank. Other non-interest income was $2.1 million, an increase of $774 thousand, or 60.0%, from the quarter ended March 31, 2021. The increase in other non-interest income was primarily due to income of $917 thousand related to the reversal of potential repurchase obligation on acquired assets as Equity was able to improve our position on those assets during the quarter.

During the quarter, service fee revenue, including deposit services, mortgage banking, trust and wealth management, credit cards and insurance increased to $6.4 million from $5.3 million during the first quarter. The growth was driven by increasing balances, transaction activity and relationship development within our trust and wealth management business line.

Non-Interest Expense

Total non-interest expense for the quarter ended June 30, 2021, was $25.8 million as compared to $24.9 million for the quarter ended March 31, 2021. The $925 thousand change is primarily attributed to an increase of $811 thousand in data processing expense, as deposit accounts and activity have increased so too has the associated expense. The periodic increase also included $308 thousand in merger expense.

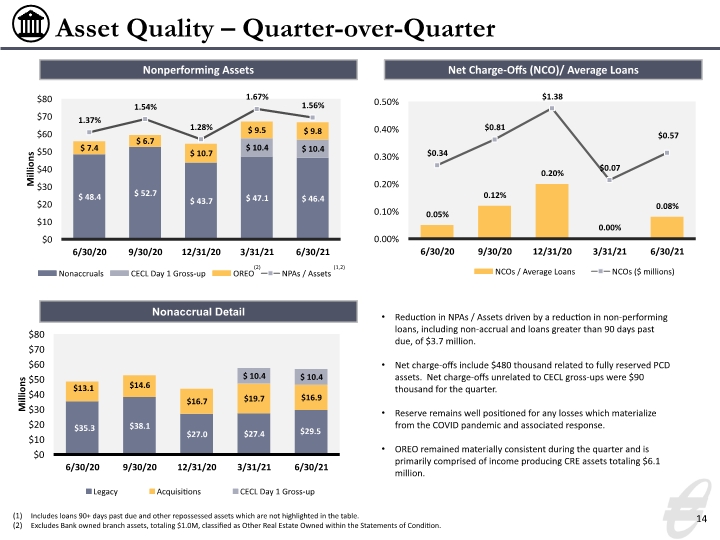

Asset Quality

As of June 30, 2021, Equity’s allowance for credit losses to total loans was 1.84%, as compared to 1.99% at March 31, 2021. Exclusive of PPP assets, the reserve to total loans was 2.04% as of June 30, 2021 as compared to 2.33% at March

Equity Bancshares, Inc.

PRESS RELEASE - 07/19/2021

31, 2021. Nonperforming assets were $66.7 million as of June 30, 2021, or 1.56% of total assets, compared to $70.1 million at March 31, 2021, or 1.67% of total assets. Total classified assets, including loans rated special mention or worse, other real estate owned and other repossessed assets were $103.1 million, or 23.11% of regulatory capital, down from $112.6 million, or 26.45% of regulatory capital as of March 31, 2021.

Regulatory Capital

The Company’s ratio of common equity tier 1 capital to risk-weighted assets was 12.4%, the total capital to risk-weighted assets was 16.7% and the total leverage ratio was 8.9% at June 30, 2021. At December 31, 2020, the Company’s common equity tier 1 capital to risk-weighted assets ratio was 12.8%, the total capital to risk-weighted assets ratio was 17.4% and the total leverage ratio was 9.3%. The Company’s subsidiary, Equity Bank, had a ratio of common equity tier 1 capital to risk-weighted assets of 14.4%, a ratio of total capital to risk-weighted assets of 15.6% and a total leverage ratio of 9.9% at June 30, 2021. At December 31, 2020, Equity Bank’s ratio of common equity tier 1 capital to risk-weighted assets was 14.5%, the ratio of total capital to risk-weighted assets was 15.7% and the total leverage ratio was 10.1%.

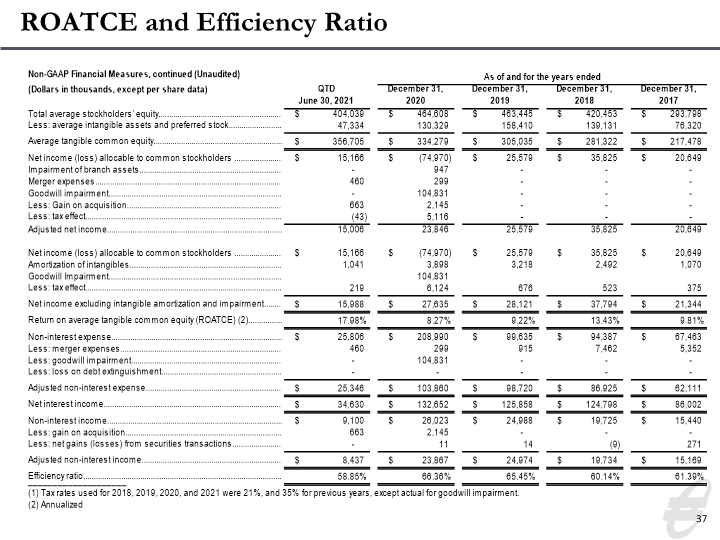

Non-GAAP Financial Measures

In addition to evaluating the Company’s results of operations in accordance with accounting principles generally accepted in the United States of America (“GAAP”), management periodically supplements this evaluation with an analysis of certain non-GAAP financial measures that are intended to provide the reader with additional perspectives on operating results, financial condition and performance trends, while facilitating comparisons with the performance of other financial institutions. Non-GAAP financial measures are not a substitute for GAAP measures, rather, they should be read and used in conjunction with the Company’s GAAP financial information.

The efficiency ratio is used as a common measure by banks as a comparable metric to understand the Company’s expense structure relative to its total revenue; in other words, for every dollar of total revenue recognized, how much of that dollar is expended. To improve the comparability of the ratio to our peers, non-core items are excluded. To improve transparency and acknowledging that banks are not consistent in their definition of the efficiency ratio, we include our calculation of this non-GAAP measure.

Return on average assets before income tax provision, provision for loan losses and goodwill impairment is a measure that the Company uses to understand fundamental operating performance before these expenses. Used as a ratio relative to average assets, we believe it demonstrates the “core” performance and can be viewed as an alternative measure of how efficiently the Company services its asset base. Used as a ratio relative to average equity, it can function as an alternative measure of the Company’s earnings performance in relationship to its equity.

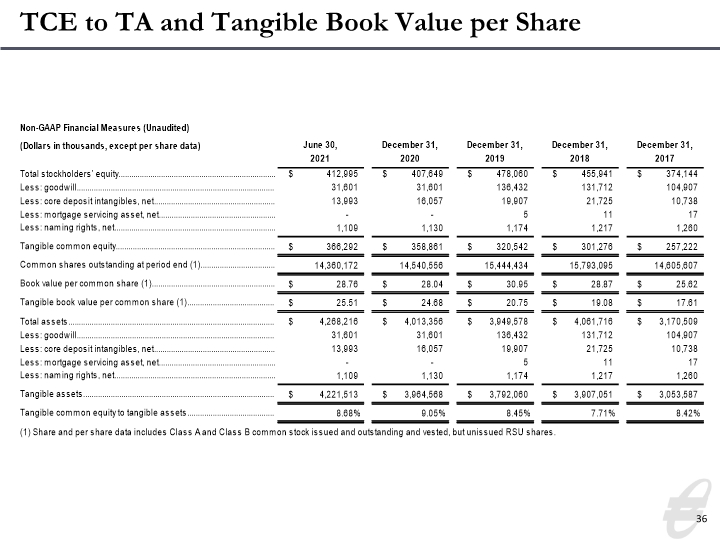

Tangible common equity and related measures are non-GAAP financial measures that exclude the impact of intangible assets, net of deferred taxes, and their related amortization. These financial measures are useful for evaluating the performance of a business consistently, whether acquired or developed internally. Return on average tangible common equity is used by management and readers of our financial statements to understand how efficiently the Company is deploying its common equity. Companies that are able to demonstrate more efficient use of common equity are more likely to be viewed favorably by current and prospective investors.

The Company believes that disclosing these non-GAAP financial measures is both useful internally and is expected by our investors and analysts in order to understand the overall performance of the Company. Other companies may calculate and define their non-GAAP financial measures and supplemental data differently. A reconciliation of GAAP financial measures to non-GAAP measures and other performance ratios, as adjusted, are included in Table 8 in the following press release tables.

Conference Call and Webcast

Equity Chairman and Chief Executive Officer, Brad Elliott, and Executive Vice President and Chief Financial Officer, Eric Newell, will hold a conference call and webcast to discuss the 2021 second quarter results on Tuesday, July 20, 2021, at 10:00 a.m. eastern time, 9:00 a.m. central time.

Equity Bancshares, Inc.

PRESS RELEASE - 07/19/2021

Investors, news media and other participants should register for the call or audio webcast at investor.equitybank.com. On Tuesday, July 20, 2021, participants may also dial into the call toll-free at (844) 534-7311 from anywhere in the U.S. or (574) 990-1419 internationally, using conference ID no. 9999830.

Participants are encouraged to dial into the call or access the webcast approximately 10 minutes prior to the start time. Presentation slides to pair with the call or webcast will be posted one hour prior to the call at investor.equitybank.com.

A replay of the call and webcast will be available two hours following the close of the call until July 27, 2021, accessible at (855) 859-2056 with conference ID no. 9999830 at investor.equitybank.com.

About Equity Bancshares, Inc.

Equity Bancshares, Inc. is the holding company for Equity Bank, offering a full range of financial solutions, including commercial loans, consumer banking, mortgage loans, trust and wealth management services and treasury management services, while delivering the high-quality, relationship-based customer service of a community bank. Equity’s common stock is traded on the NASDAQ Global Select Market under the symbol “EQBK.” Learn more at www.equitybank.com.

Important Additional Information

The information contained herein does not constitute an offer to sell or a solicitation of an offer to buy any securities or a solicitation of any vote or approval.

In connection with the proposed transaction, Equity filed with the Securities and Exchange Commission (“SEC”) a registration statement on Form S-4 to register the shares of Equity common stock to be issued to ASBI stockholders. The registration statement included a proxy statement/prospectus, which will be sent to the stockholders of ASBI seeking their approval of the proposed transaction.

WE URGE INVESTORS AND SECURITY HOLDERS TO READ THE REGISTRATION STATEMENT ON FORM S-4, THE PROXY STATEMENT/PROSPECTUS INCLUDED WITHIN THE REGISTRATION STATEMENT ON FORM S-4 AND ANY OTHER RELEVANT DOCUMENTS TO BE FILED WITH THE SEC IN CONNECTION WITH THE PROPOSED TRANSACTION BECAUSE THEY CONTAIN IMPORTANT INFORMATION ABOUT EQUITY, ASB AND THE PROPOSED TRANSACTION.

The documents filed by Equity with the SEC may be obtained free of charge at Equity’s investor relations website at investor.equitybank.com or at the SEC’s website at www.sec.gov. Alternatively, these documents, when available, can be obtained free of charge from Equity upon written request to Equity Bancshares, Inc., Attn: Investor Relations, 7701 East Kellogg Drive, Suite 300, Wichita, Kansas 67207 or by calling (316) 612-6000.

Participants in the Transaction

Equity, ASBI and certain of their respective directors and executive officers may be deemed to be participants in the solicitation of proxies from ASBI’s stockholders in connection with the proposed transaction under the rules of the SEC. Information about the directors and executive officers of Equity is set forth in the proxy statement for Equity’s 2021 annual meeting of stockholders filed with the SEC on Schedule 14A on March 18, 2021, and Equity’s annual report on Form 10-K for the year ended December 31, 2020 filed with the SEC on March 9, 2021. Free copies of these documents may be obtained free of charge as described in the preceding paragraph. Additional information regarding the interests of these participants and other persons who may be deemed participants in the transaction may be obtained by reading the proxy statement/prospectus regarding the proposed transaction when it becomes available.

No Offer or Solicitation

This press release shall not constitute an offer to sell, a solicitation of an offer to sell, or the solicitation or an offer to buy any securities. There will be no sale of securities in any jurisdiction in which such an offer, solicitation or sale would be

Equity Bancshares, Inc.

PRESS RELEASE - 07/19/2021

unlawful prior to registration or qualification under the securities laws of any such jurisdiction. No offer of securities shall be made except by means of a prospectus meeting the requirement of Section 10 of the Securities Act of 1933, as amended.

Special Note Concerning Forward-Looking Statements

This press release contains “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. These forward-looking statements reflect the current views of Equity’s management with respect to, among other things, future events and Equity’s financial performance. These statements are often, but not always, made through the use of words or phrases such as “may,” “should,” “could,” “predict,” “potential,” “believe,” “will likely result,” “expect,” “continue,” “will,” “anticipate,” “seek,” “estimate,” “intend,” “plan,” “project,” “forecast,” “goal,” “target,” “would” and “outlook,” or the negative variations of those words or other comparable words of a future or forward-looking nature. These forward-looking statements are not historical facts, and are based on current expectations, estimates and projections about Equity’s industry, management’s beliefs and certain assumptions made by management, many of which, by their nature, are inherently uncertain and beyond Equity’s control. Accordingly, Equity cautions you that any such forward-looking statements are not guarantees of future performance and are subject to risks, assumptions and uncertainties that are difficult to predict. Although Equity believes that the expectations reflected in these forward-looking statements are reasonable as of the date made, actual results may prove to be materially different from the results expressed or implied by the forward-looking statements. Factors that could cause actual results to differ materially from Equity’s expectations include COVID-19 related impacts; competition from other financial institutions and bank holding companies; the effects of and changes in trade, monetary and fiscal policies and laws, including interest rate policies of the Federal Reserve Board; changes in the demand for loans; fluctuations in value of collateral and loan reserves; inflation, interest rate, market and monetary fluctuations; changes in consumer spending, borrowing and savings habits; and acquisitions and integration of acquired businesses; and similar variables. The foregoing list of factors is not exhaustive.

For discussion of these and other risks that may cause actual results to differ from expectations, please refer to “Cautionary Note Regarding Forward-Looking Statements” and “Risk Factors” in Equity’s Annual Report on Form 10-K filed with the Securities and Exchange Commission on March 9, 2021, and any updates to those risk factors set forth in Equity’s subsequent Quarterly Reports on Form 10-Q or Current Reports on Form 8-K. If one or more events related to these or other risks or uncertainties materialize, or if Equity’s underlying assumptions prove to be incorrect, actual results may differ materially from what Equity anticipates. Accordingly, you should not place undue reliance on any such forward-looking statements. Any forward-looking statement speaks only as of the date on which it is made, and Equity does not undertake any obligation to publicly update or review any forward-looking statement, whether as a result of new information, future developments or otherwise. New risks and uncertainties arise from time to time, such as COVID-19, and it is not possible for us to predict those events or how they may affect us. In addition, Equity cannot assess the impact of each factor on Equity’s business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements. All forward-looking statements, expressed or implied, included in this press release are expressly qualified in their entirety by this cautionary statement. This cautionary statement should also be considered in connection with any subsequent written or oral forward-looking statements that Equity or persons acting on Equity’s behalf may issue.

Investor Contact:

Chris Navratil

SVP, Finance

Equity Bancshares, Inc.

(316) 612-6014

cnavratil@equitybank.com

Equity Bancshares, Inc.

PRESS RELEASE - 07/19/2021

Media Contact:

John J. Hanley

SVP, Senior Director of Marketing

Equity Bancshares, Inc.

(816) 505-4063

jhanley@equitybank.com

Unaudited Financial Tables

| • | Table 1. Consolidated Statements of Income |

| • | Table 2. Quarterly Consolidated Statements of Income |

| • | Table 3. Consolidated Balance Sheets |

| • | Table 4. Selected Financial Highlights |

| • | Table 5. Year-To-Date Net Interest Income Analysis |

| • | Table 6. Quarter-To-Date Net Interest Income Analysis |

| • | Table 7. Quarter-Over-Quarter Net Interest Income Analysis |

| • | Table 8. Non-GAAP Financial Measures |

Equity Bancshares, Inc.

PRESS RELEASE - 07/19/2021

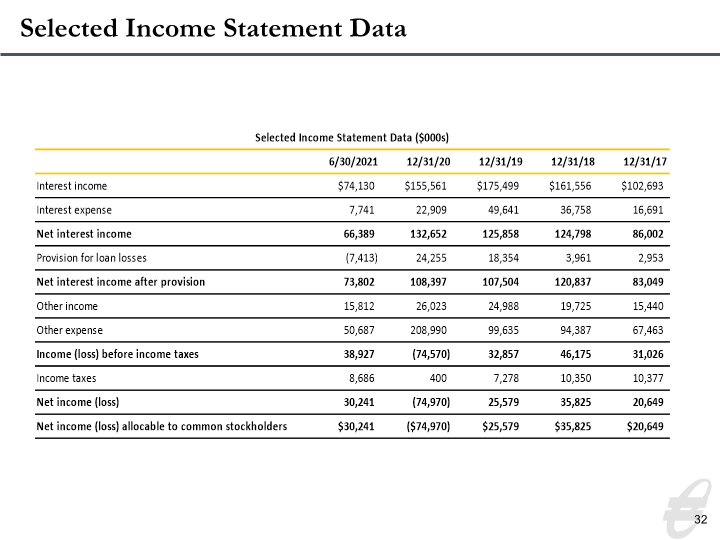

TABLE 1. CONSOLIDATED STATEMENTS OF INCOME (Unaudited)

(Dollars in thousands, except per share data)

|

| Three months ended June 30, |

|

| Six months ended June 30, |

| ||||||||||

|

| 2021 |

|

| 2020 |

|

| 2021 |

|

| 2020 |

| ||||

Interest and dividend income |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Loans, including fees |

| $ | 33,810 |

|

| $ | 32,627 |

|

| $ | 64,811 |

|

| $ | 67,003 |

|

Securities, taxable |

|

| 3,523 |

|

|

| 4,017 |

|

|

| 7,322 |

|

|

| 8,637 |

|

Securities, nontaxable |

|

| 717 |

|

|

| 880 |

|

|

| 1,441 |

|

|

| 1,846 |

|

Federal funds sold and other |

|

| 268 |

|

|

| 409 |

|

|

| 556 |

|

|

| 1,004 |

|

Total interest and dividend income |

|

| 38,318 |

|

|

| 37,933 |

|

|

| 74,130 |

|

|

| 78,490 |

|

Interest expense |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Deposits |

|

| 2,025 |

|

|

| 3,899 |

|

|

| 4,435 |

|

|

| 10,763 |

|

Federal funds purchased and retail repurchase agreements |

|

| 26 |

|

|

| 24 |

|

|

| 48 |

|

|

| 55 |

|

Federal Home Loan Bank advances |

|

| 80 |

|

|

| 552 |

|

|

| 145 |

|

|

| 1,727 |

|

Federal Reserve Bank discount window |

|

| — |

|

|

| 6 |

|

|

| — |

|

|

| 6 |

|

Bank stock loan |

|

| — |

|

|

| 306 |

|

|

| — |

|

|

| 415 |

|

Subordinated debt |

|

| 1,557 |

|

|

| 255 |

|

|

| 3,113 |

|

|

| 538 |

|

Total interest expense |

|

| 3,688 |

|

|

| 5,042 |

|

|

| 7,741 |

|

|

| 13,504 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net interest income |

|

| 34,630 |

|

|

| 32,891 |

|

|

| 66,389 |

|

|

| 64,986 |

|

Provision (reversal) for credit losses |

|

| (1,657 | ) |

|

| 12,500 |

|

|

| (7,413 | ) |

|

| 22,440 |

|

Net interest income after provision (reversal) for credit losses |

|

| 36,287 |

|

|

| 20,391 |

|

|

| 73,802 |

|

|

| 42,546 |

|

Non-interest income |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Service charges and fees |

|

| 2,169 |

|

|

| 1,365 |

|

|

| 3,765 |

|

|

| 3,391 |

|

Debit card income |

|

| 2,679 |

|

|

| 2,201 |

|

|

| 5,029 |

|

|

| 4,244 |

|

Mortgage banking |

|

| 848 |

|

|

| 831 |

|

|

| 1,783 |

|

|

| 1,421 |

|

Increase in value of bank-owned life insurance |

|

| 676 |

|

|

| 481 |

|

|

| 1,277 |

|

|

| 963 |

|

Net gain on acquisition |

|

| 663 |

|

|

| — |

|

|

| 585 |

|

|

| — |

|

Net gains (losses) from securities transactions |

|

| — |

|

|

| 4 |

|

|

| 17 |

|

|

| 12 |

|

Other |

|

| 2,065 |

|

|

| 850 |

|

|

| 3,356 |

|

|

| 1,007 |

|

Total non-interest income |

|

| 9,100 |

|

|

| 5,732 |

|

|

| 15,812 |

|

|

| 11,038 |

|

Non-interest expense |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Salaries and employee benefits |

|

| 12,769 |

|

|

| 12,695 |

|

|

| 25,491 |

|

|

| 26,199 |

|

Net occupancy and equipment |

|

| 2,327 |

|

|

| 2,119 |

|

|

| 4,695 |

|

|

| 4,354 |

|

Data processing |

|

| 3,474 |

|

|

| 2,763 |

|

|

| 6,137 |

|

|

| 5,426 |

|

Professional fees |

|

| 999 |

|

|

| 943 |

|

|

| 2,072 |

|

|

| 2,310 |

|

Advertising and business development |

|

| 799 |

|

|

| 403 |

|

|

| 1,481 |

|

|

| 1,099 |

|

Telecommunications |

|

| 512 |

|

|

| 390 |

|

|

| 1,092 |

|

|

| 877 |

|

FDIC insurance |

|

| 425 |

|

|

| 414 |

|

|

| 840 |

|

|

| 931 |

|

Courier and postage |

|

| 327 |

|

|

| 353 |

|

|

| 696 |

|

|

| 737 |

|

Free nationwide ATM cost |

|

| 513 |

|

|

| 327 |

|

|

| 985 |

|

|

| 747 |

|

Amortization of core deposit intangibles |

|

| 1,030 |

|

|

| 974 |

|

|

| 2,064 |

|

|

| 1,776 |

|

Loan expense |

|

| 181 |

|

|

| 287 |

|

|

| 419 |

|

|

| 521 |

|

Other real estate owned |

|

| (468 | ) |

|

| 269 |

|

|

| (463 | ) |

|

| 577 |

|

Merger expenses |

|

| 460 |

|

|

| — |

|

|

| 612 |

|

|

| — |

|

Other |

|

| 2,458 |

|

|

| 2,000 |

|

|

| 4,566 |

|

|

| 4,141 |

|

Total non-interest expense |

|

| 25,806 |

|

|

| 23,937 |

|

|

| 50,687 |

|

|

| 49,695 |

|

Income (loss) before income tax |

|

| 19,581 |

|

|

| 2,186 |

|

|

| 38,927 |

|

|

| 3,889 |

|

Provision for income taxes |

|

| 4,415 |

|

|

| 497 |

|

|

| 8,686 |

|

|

| 942 |

|

Net income (loss) and net income (loss) allocable to common stockholders |

| $ | 15,166 |

|

| $ | 1,689 |

|

| $ | 30,241 |

|

| $ | 2,947 |

|

Basic earnings (loss) per share |

| $ | 1.06 |

|

| $ | 0.11 |

|

| $ | 2.10 |

|

| $ | 0.19 |

|

Diluted earnings (loss) per share |

| $ | 1.03 |

|

| $ | 0.11 |

|

| $ | 2.06 |

|

| $ | 0.19 |

|

Weighted average common shares |

|

| 14,356,958 |

|

|

| 15,209,483 |

|

|

| 14,410,328 |

|

|

| 15,298,590 |

|

Weighted average diluted common shares |

|

| 14,674,838 |

|

|

| 15,304,009 |

|

|

| 14,704,240 |

|

|

| 15,449,517 |

|

Equity Bancshares, Inc.

PRESS RELEASE - 07/19/2021

TABLE 2. QUARTERLY CONSOLIDATED STATEMENTS OF INCOME (Unaudited)

(Dollars in thousands, except per share data)

|

| As of and for the three months ended |

| |||||||||||||||||

|

| June 30, 2021 |

|

| March 31, 2021 |

|

| December 31, 2020 |

|

| September 30, 2020 |

|

| June 30, 2020 |

| |||||

Interest and dividend income |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Loans, including fees |

| $ | 33,810 |

|

| $ | 31,001 |

|

| $ | 35,383 |

|

| $ | 32,278 |

|

| $ | 32,627 |

|

Securities, taxable |

|

| 3,523 |

|

|

| 3,799 |

|

|

| 3,408 |

|

|

| 3,476 |

|

|

| 4,017 |

|

Securities, nontaxable |

|

| 717 |

|

|

| 724 |

|

|

| 913 |

|

|

| 923 |

|

|

| 880 |

|

Federal funds sold and other |

|

| 268 |

|

|

| 288 |

|

|

| 285 |

|

|

| 405 |

|

|

| 409 |

|

Total interest and dividend income |

|

| 38,318 |

|

|

| 35,812 |

|

|

| 39,989 |

|

|

| 37,082 |

|

|

| 37,933 |

|

Interest expense |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Deposits |

|

| 2,025 |

|

|

| 2,410 |

|

|

| 2,755 |

|

|

| 3,064 |

|

|

| 3,899 |

|

Federal funds purchased and retail repurchase agreements |

|

| 26 |

|

|

| 22 |

|

|

| 25 |

|

|

| 25 |

|

|

| 24 |

|

Federal Home Loan Bank advances |

|

| 80 |

|

|

| 65 |

|

|

| 94 |

|

|

| 471 |

|

|

| 552 |

|

Federal Reserve Bank discount window |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 6 |

|

Bank stock loan |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 306 |

|

Subordinated debt |

|

| 1,557 |

|

|

| 1,556 |

|

|

| 1,556 |

|

|

| 1,415 |

|

|

| 255 |

|

Total interest expense |

|

| 3,688 |

|

|

| 4,053 |

|

|

| 4,430 |

|

|

| 4,975 |

|

|

| 5,042 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net interest income |

|

| 34,630 |

|

|

| 31,759 |

|

|

| 35,559 |

|

|

| 32,107 |

|

|

| 32,891 |

|

Provision (reversal) for credit losses |

|

| (1,657 | ) |

|

| (5,756 | ) |

|

| 1,000 |

|

|

| 815 |

|

|

| 12,500 |

|

Net interest income after provision (reversal) for credit losses |

|

| 36,287 |

|

|

| 37,515 |

|

|

| 34,559 |

|

|

| 31,292 |

|

|

| 20,391 |

|

Non-interest income |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Service charges and fees |

|

| 2,169 |

|

|

| 1,596 |

|

|

| 1,759 |

|

|

| 1,706 |

|

|

| 1,365 |

|

Debit card income |

|

| 2,679 |

|

|

| 2,350 |

|

|

| 2,401 |

|

|

| 2,491 |

|

|

| 2,201 |

|

Mortgage banking |

|

| 848 |

|

|

| 935 |

|

|

| 855 |

|

|

| 877 |

|

|

| 831 |

|

Increase in value of bank-owned life insurance |

|

| 676 |

|

|

| 601 |

|

|

| 489 |

|

|

| 489 |

|

|

| 481 |

|

Net gain on acquisition |

|

| 663 |

|

|

| (78 | ) |

|

| 2,145 |

|

|

| — |

|

|

| — |

|

Net gains (losses) from securities transactions |

|

| — |

|

|

| 17 |

|

|

| (1 | ) |

|

| — |

|

|

| 4 |

|

Other |

|

| 2,065 |

|

|

| 1,291 |

|

|

| 852 |

|

|

| 922 |

|

|

| 850 |

|

Total non-interest income |

|

| 9,100 |

|

|

| 6,712 |

|

|

| 8,500 |

|

|

| 6,485 |

|

|

| 5,732 |

|

Non-interest expense |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Salaries and employee benefits |

|

| 12,769 |

|

|

| 12,722 |

|

|

| 14,053 |

|

|

| 13,877 |

|

|

| 12,695 |

|

Net occupancy and equipment |

|

| 2,327 |

|

|

| 2,368 |

|

|

| 2,206 |

|

|

| 2,224 |

|

|

| 2,119 |

|

Data processing |

|

| 3,474 |

|

|

| 2,663 |

|

|

| 2,748 |

|

|

| 2,817 |

|

|

| 2,763 |

|

Professional fees |

|

| 999 |

|

|

| 1,073 |

|

|

| 1,095 |

|

|

| 877 |

|

|

| 943 |

|

Advertising and business development |

|

| 799 |

|

|

| 682 |

|

|

| 801 |

|

|

| 598 |

|

|

| 403 |

|

Telecommunications |

|

| 512 |

|

|

| 580 |

|

|

| 510 |

|

|

| 486 |

|

|

| 390 |

|

FDIC insurance |

|

| 425 |

|

|

| 415 |

|

|

| 797 |

|

|

| 360 |

|

|

| 414 |

|

Courier and postage |

|

| 327 |

|

|

| 369 |

|

|

| 338 |

|

|

| 366 |

|

|

| 353 |

|

Free nationwide ATM cost |

|

| 513 |

|

|

| 472 |

|

|

| 423 |

|

|

| 439 |

|

|

| 327 |

|

Amortization of core deposit intangibles |

|

| 1,030 |

|

|

| 1,034 |

|

|

| 1,044 |

|

|

| 1,030 |

|

|

| 974 |

|

Loan expense |

|

| 181 |

|

|

| 238 |

|

|

| 161 |

|

|

| 107 |

|

|

| 287 |

|

Other real estate owned |

|

| (468 | ) |

|

| 5 |

|

|

| 1,600 |

|

|

| 133 |

|

|

| 269 |

|

Merger expenses |

|

| 460 |

|

|

| 152 |

|

|

| 299 |

|

|

| — |

|

|

| — |

|

Goodwill impairment |

|

| — |

|

|

| — |

|

|

| — |

|

|

| 104,831 |

|

|

| — |

|

Other |

|

| 2,458 |

|

|

| 2,108 |

|

|

| 2,385 |

|

|

| 2,690 |

|

|

| 2,000 |

|

Total non-interest expense |

|

| 25,806 |

|

|

| 24,881 |

|

|

| 28,460 |

|

|

| 130,835 |

|

|

| 23,937 |

|

Income (loss) before income tax |

|

| 19,581 |

|

|

| 19,346 |

|

|

| 14,599 |

|

|

| (93,058 | ) |

|

| 2,186 |

|

Provision for income taxes (benefit) |

|

| 4,415 |

|

|

| 4,271 |

|

|

| 2,111 |

|

|

| (2,653 | ) |

|

| 497 |

|

Net income (loss) and net income (loss) allocable to common stockholders |

| $ | 15,166 |

|

| $ | 15,075 |

|

| $ | 12,488 |

|

| $ | (90,405 | ) |

| $ | 1,689 |

|

Basic earnings (loss) per share |

| $ | 1.06 |

|

| $ | 1.04 |

|

| $ | 0.85 |

|

| $ | (6.01 | ) |

| $ | 0.11 |

|

Equity Bancshares, Inc.

PRESS RELEASE - 07/19/2021

Diluted earnings (loss) per share |

| $ | 1.03 |

|

| $ | 1.02 |

|

| $ | 0.84 |

|

| $ | (6.01 | ) |

| $ | 0.11 |

|

Weighted average common shares |

|

| 14,356,958 |

|

|

| 14,464,291 |

|

|

| 14,760,810 |

|

|

| 15,040,407 |

|

|

| 15,209,483 |

|

Weighted average diluted common shares |

|

| 14,674,838 |

|

|

| 14,734,083 |

|

|

| 14,934,058 |

|

|

| 15,040,407 |

|

|

| 15,304,009 |

|

Equity Bancshares, Inc.

PRESS RELEASE - 07/19/2021

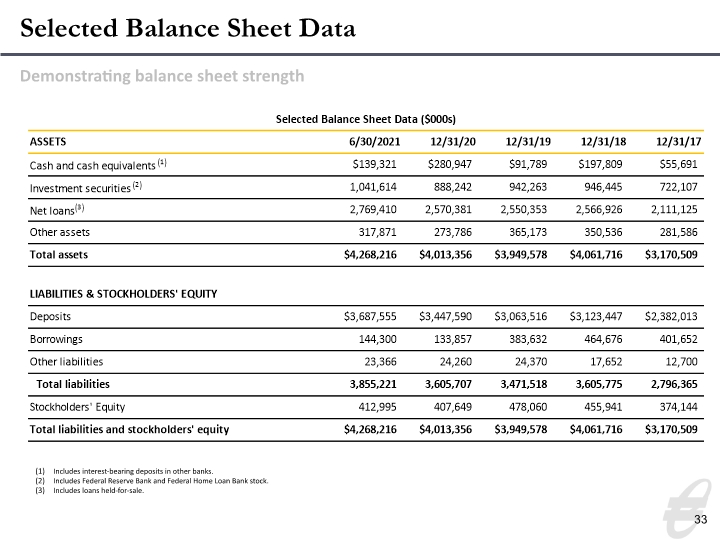

TABLE 3. CONSOLIDATED BALANCE SHEETS (Unaudited)

(Dollars in thousands)

|

| June 30, 2021 |

|

| March 31, 2021 |

|

| December 31, 2020 |

|

| September 30, 2020 |

|

| June 30, 2020 |

| |||||

ASSETS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Cash and due from banks |

| $ | 138,869 |

|

| $ | 136,190 |

|

| $ | 280,150 |

|

| $ | 65,534 |

|

| $ | 178,045 |

|

Federal funds sold |

|

| 452 |

|

|

| 498 |

|

|

| 548 |

|

|

| 305 |

|

|

| 245 |

|

Cash and cash equivalents |

|

| 139,321 |

|

|

| 136,688 |

|

|

| 280,698 |

|

|

| 65,839 |

|

|

| 178,290 |

|

Interest-bearing time deposits in other banks |

|

| — |

|

|

| 249 |

|

|

| 249 |

|

|

| 499 |

|

|

| 2,248 |

|

Available-for-sale securities |

|

| 1,041,614 |

|

|

| 998,100 |

|

|

| 871,827 |

|

|

| 798,576 |

|

|

| 177,228 |

|

Held-to-maturity securities(1) |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 662,522 |

|

Loans held for sale |

|

| 6,183 |

|

|

| 8,609 |

|

|

| 12,394 |

|

|

| 9,053 |

|

|

| 4,802 |

|

Loans, net of allowance for credit losses(2) |

|

| 2,763,227 |

|

|

| 2,740,215 |

|

|

| 2,557,987 |

|

|

| 2,691,626 |

|

|

| 2,772,256 |

|

Other real estate owned, net |

|

| 10,861 |

|

|

| 10,559 |

|

|

| 11,733 |

|

|

| 8,727 |

|

|

| 7,374 |

|

Premises and equipment, net |

|

| 90,876 |

|

|

| 90,322 |

|

|

| 89,412 |

|

|

| 86,087 |

|

|

| 87,055 |

|

Bank-owned life insurance |

|

| 103,321 |

|

|

| 102,645 |

|

|

| 77,044 |

|

|

| 76,555 |

|

|

| 76,066 |

|

Federal Reserve Bank and Federal Home Loan Bank stock |

|

| 18,454 |

|

|

| 15,174 |

|

|

| 16,415 |

|

|

| 32,545 |

|

|

| 31,832 |

|

Interest receivable |

|

| 15,064 |

|

|

| 16,655 |

|

|

| 15,831 |

|

|

| 18,110 |

|

|

| 19,598 |

|

Goodwill |

|

| 31,601 |

|

|

| 31,601 |

|

|

| 31,601 |

|

|

| 31,601 |

|

|

| 136,432 |

|

Core deposit intangibles, net |

|

| 13,993 |

|

|

| 15,023 |

|

|

| 16,057 |

|

|

| 17,101 |

|

|

| 18,131 |

|

Other |

|

| 33,701 |

|

|

| 30,344 |

|

|

| 32,108 |

|

|

| 29,252 |

|

|

| 31,435 |

|

Total assets |

| $ | 4,268,216 |

|

| $ | 4,196,184 |

|

| $ | 4,013,356 |

|

| $ | 3,865,571 |

|

| $ | 4,205,269 |

|

LIABILITIES AND STOCKHOLDERS’ EQUITY |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Deposits |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Demand |

| $ | 992,565 |

|

| $ | 972,364 |

|

| $ | 791,639 |

|

| $ | 693,967 |

|

| $ | 756,613 |

|

Total non-interest-bearing deposits |

|

| 992,565 |

|

|

| 972,364 |

|

|

| 791,639 |

|

|

| 693,967 |

|

|

| 756,613 |

|

Savings, NOW and money market |

|

| 2,035,496 |

|

|

| 2,074,261 |

|

|

| 2,029,097 |

|

|

| 1,816,307 |

|

|

| 1,800,132 |

|

Time |

|

| 659,494 |

|

|

| 587,905 |

|

|

| 626,854 |

|

|

| 623,344 |

|

|

| 690,522 |

|

Total interest-bearing deposits |

|

| 2,694,990 |

|

|

| 2,662,166 |

|

|

| 2,655,951 |

|

|

| 2,439,651 |

|

|

| 2,490,654 |

|

Total deposits |

|

| 3,687,555 |

|

|

| 3,634,530 |

|

|

| 3,447,590 |

|

|

| 3,133,618 |

|

|

| 3,247,267 |

|

Federal funds purchased and retail repurchase agreements |

|

| 47,184 |

|

|

| 40,339 |

|

|

| 36,029 |

|

|

| 46,295 |

|

|

| 51,557 |

|

Federal Home Loan Bank advances |

|

| 9,208 |

|

|

| 9,926 |

|

|

| 10,144 |

|

|

| 167,862 |

|

|

| 344,900 |

|

Subordinated debt |

|

| 87,908 |

|

|

| 87,788 |

|

|

| 87,684 |

|

|

| 87,537 |

|

|

| 55,575 |

|

Contractual obligations |

|

| 4,469 |

|

|

| 4,856 |

|

|

| 5,189 |

|

|

| 5,478 |

|

|

| 5,571 |

|

Interest payable and other liabilities |

|

| 18,897 |

|

|

| 20,930 |

|

|

| 19,071 |

|

|

| 22,609 |

|

|

| 20,633 |

|

Total liabilities |

|

| 3,855,221 |

|

|

| 3,798,369 |

|

|

| 3,605,707 |

|

|

| 3,463,399 |

|

|

| 3,725,503 |

|

Commitments and contingent liabilities |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Stockholders’ equity |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Common stock |

|

| 176 |

|

|

| 175 |

|

|

| 174 |

|

|

| 174 |

|

|

| 174 |

|

Additional paid-in capital |

|

| 389,394 |

|

|

| 387,939 |

|

|

| 386,820 |

|

|

| 386,017 |

|

|

| 384,955 |

|

Retained earnings |

|

| 68,625 |

|

|

| 53,459 |

|

|

| 50,787 |

|

|

| 38,299 |

|

|

| 128,704 |

|

Accumulated other comprehensive income, net of tax |

|

| 13,450 |

|

|

| 12,019 |

|

|

| 19,781 |

|

|

| 21,074 |

|

|

| 3,390 |

|

Employee stock loans |

|

| — |

|

|

| — |

|

|

| (43 | ) |

|

| (43 | ) |

|

| (43 | ) |

Treasury stock |

|

| (58,650 | ) |

|

| (55,777 | ) |

|

| (49,870 | ) |

|

| (43,349 | ) |

|

| (37,414 | ) |

Total stockholders’ equity |

|

| 412,995 |

|

|

| 397,815 |

|

|

| 407,649 |

|

|

| 402,172 |

|

|

| 479,766 |

|

Total liabilities and stockholders’ equity |

| $ | 4,268,216 |

|

| $ | 4,196,184 |

|

| $ | 4,013,356 |

|

| $ | 3,865,571 |

|

| $ | 4,205,269 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(1) Fair market value of held-to-maturity securities |

| $ | — |

|

| $ | — |

|

| $ | — |

|

| $ | — |

|

| $ | 689,206 |

|

(2) Allowance for credit losses |

|

| 51,834 |

|

|

| 55,525 |

|

|

| 33,709 |

|

|

| 34,087 |

|

|

| 34,078 |

|

Equity Bancshares, Inc.

PRESS RELEASE - 07/19/2021

TABLE 4. SELECTED FINANCIAL HIGHLIGHTS (Unaudited)

(Dollars in thousands, except per share data)

|

| As of and for the three months ended |

| |||||||||||||||||

|

| June 30, |

|

| March 31, |

|

| December 31, |

|

| September 30, |

|

| June 30, |

| |||||

|

| 2021 |

|

| 2021 |

|

| 2020 |

|

| 2020 |

|

| 2020 |

| |||||

Loans Held-For-Investment by Type |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Commercial real estate |

| $ | 1,261,214 |

|

| $ | 1,218,537 |

|

| $ | 1,188,696 |

|

| $ | 1,188,329 |

|

| $ | 1,191,336 |

|

Commercial and industrial |

|

| 732,126 |

|

|

| 820,736 |

|

|

| 734,495 |

|

|

| 857,244 |

|

|

| 883,355 |

|

Residential real estate |

|

| 503,110 |

|

|

| 438,503 |

|

|

| 381,958 |

|

|

| 402,242 |

|

|

| 442,486 |

|

Agricultural real estate |

|

| 129,020 |

|

|

| 134,944 |

|

|

| 133,693 |

|

|

| 127,349 |

|

|

| 129,080 |

|

Agricultural |

|

| 97,912 |

|

|

| 93,764 |

|

|

| 94,322 |

|

|

| 83,084 |

|

|

| 89,040 |

|

Consumer |

|

| 91,679 |

|

|

| 89,256 |

|

|

| 58,532 |

|

|

| 67,465 |

|

|

| 71,037 |

|

Total loans held-for-investment |

|

| 2,815,061 |

|

|

| 2,795,740 |

|

|

| 2,591,696 |

|

|

| 2,725,713 |

|

|

| 2,806,334 |

|

Allowance for credit losses |

|

| (51,834 | ) |

|

| (55,525 | ) |

|

| (33,709 | ) |

|

| (34,087 | ) |

|

| (34,078 | ) |

Net loans held-for-investment |

| $ | 2,763,227 |

|

| $ | 2,740,215 |

|

| $ | 2,557,987 |

|

| $ | 2,691,626 |

|

| $ | 2,772,256 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Asset Quality Ratios |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Allowance for credit losses on loans to total loans |

|

| 1.84 | % |

|

| 1.99 | % |

|

| 1.30 | % |

|

| 1.25 | % |

|

| 1.21 | % |

Past due or nonaccrual loans to total loans |

|

| 2.09 | % |

|

| 2.30 | % |

|

| 1.99 | % |

|

| 2.12 | % |

|

| 1.88 | % |

Nonperforming assets to total assets |

|

| 1.56 | % |

|

| 1.67 | % |

|

| 1.36 | % |

|

| 1.55 | % |

|

| 1.37 | % |

Nonperforming assets to total loans plus other real estate owned |

|

| 2.36 | % |

|

| 2.50 | % |

|

| 2.10 | % |

|

| 2.19 | % |

|

| 2.05 | % |

Classified assets to bank total regulatory capital |

|

| 23.11 | % |

|

| 26.45 | % |

|

| 25.50 | % |

|

| 18.35 | % |

|

| 20.81 | % |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Selected Average Balance Sheet Data (QTD Average) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Investment securities |

| $ | 986,986 |

|

| $ | 947,453 |

|

| $ | 814,114 |

|

| $ | 802,525 |

|

| $ | 877,308 |

|

Total gross loans receivable |

|

| 2,853,145 |

|

|

| 2,736,918 |

|

|

| 2,692,223 |

|

|

| 2,758,680 |

|

|

| 2,806,865 |

|

Interest-earning assets |

|

| 3,964,633 |

|

|

| 3,891,140 |

|

|

| 3,647,730 |

|

|

| 3,679,168 |

|

|

| 3,786,629 |

|

Total assets |

|

| 4,231,439 |

|

|

| 4,143,752 |

|

|

| 3,910,628 |

|

|

| 4,041,187 |

|

|

| 4,159,336 |

|

Interest-bearing deposits |

|

| 2,656,052 |

|

|

| 2,690,159 |

|

|

| 2,551,219 |

|

|

| 2,430,407 |

|

|

| 2,487,187 |

|

Borrowings |

|

| 171,658 |

|

|

| 139,360 |

|

|

| 172,730 |

|

|

| 377,158 |

|

|

| 384,727 |

|

Total interest-bearing liabilities |

|

| 2,827,710 |

|

|

| 2,829,519 |

|

|

| 2,723,949 |

|

|

| 2,807,565 |

|

|

| 2,871,914 |

|

Total deposits |

|

| 3,624,950 |

|

|

| 3,577,625 |

|

|

| 2,960,791 |

|

|

| 3,145,810 |

|

|

| 3,257,631 |

|

Total liabilities |

|

| 3,827,400 |

|

|

| 3,748,114 |

|

|

| 3,501,056 |

|

|

| 3,558,099 |

|

|

| 3,675,731 |

|

Total stockholders' equity |

|

| 404,039 |

|

|

| 395,638 |

|

|

| 409,572 |

|

|

| 483,088 |

|

|

| 483,605 |

|

Tangible common equity* |

|

| 356,705 |

|

|

| 347,262 |

|

|

| 355,025 |

|

|

| 329,039 |

|

|

| 327,411 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Performance ratios |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Return on average assets (ROAA) annualized |

|

| 1.44 | % |

|

| 1.48 | % |

|

| 1.27 | % |

|

| (8.90 | )% |

|

| 0.16 | % |

Return on average assets before income tax, provision for loan losses and goodwill impairment* |

|

| 1.70 | % |

|

| 1.33 | % |

|

| 1.59 | % |

|

| 1.24 | % |

|

| 1.42 | % |

Return on average equity (ROAE) annualized |

|

| 15.06 | % |

|

| 15.45 | % |

|

| 12.13 | % |

|

| (74.45 | )% |

|

| 1.40 | % |

Return on average equity before income tax, provision for loan losses and goodwill impairment* |

|

| 17.79 | % |

|

| 13.93 | % |

|

| 15.15 | % |

|

| 10.37 | % |

|

| 12.21 | % |

Return on average tangible common equity (ROATCE) annualized* |

|

| 17.98 | % |

|

| 18.57 | % |

|

| 14.93 | % |

|

| (108.31 | )% |

|

| 3.03 | % |

Return on average tangible common equity adjusted for goodwill impairment* |

|

| 17.98 | % |

|

| 18.57 | % |

|

| 14.93 | % |

|

| 12.01 | % |

|

| 3.03 | % |

Yield on loans annualized |

|

| 4.75 | % |

|

| 4.59 | % |

|

| 5.23 | % |

|

| 4.65 | % |

|

| 4.68 | % |

Cost of interest-bearing deposits annualized |

|

| 0.31 | % |

|

| 0.36 | % |

|

| 0.43 | % |

|

| 0.50 | % |

|

| 0.63 | % |

Cost of total deposits annualized |

|

| 0.22 | % |

|

| 0.27 | % |

|

| 0.37 | % |

|

| 0.39 | % |

|

| 0.48 | % |

Net interest margin annualized |

|

| 3.50 | % |

|

| 3.31 | % |

|

| 3.88 | % |

|

| 3.47 | % |

|

| 3.49 | % |

Efficiency ratio* |

|

| 58.85 | % |

|

| 64.18 | % |

|

| 67.19 | % |

|

| 67.38 | % |

|

| 61.98 | % |

Non-interest income / average assets |

|

| 0.86 | % |

|

| 0.66 | % |

|

| 0.86 | % |

|

| 0.64 | % |

|

| 0.55 | % |

Non-interest expense / average assets |

|

| 2.45 | % |

|

| 2.44 | % |

|

| 2.90 | % |

|

| 12.88 | % |

|

| 2.31 | % |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Equity Bancshares, Inc.

PRESS RELEASE - 07/19/2021

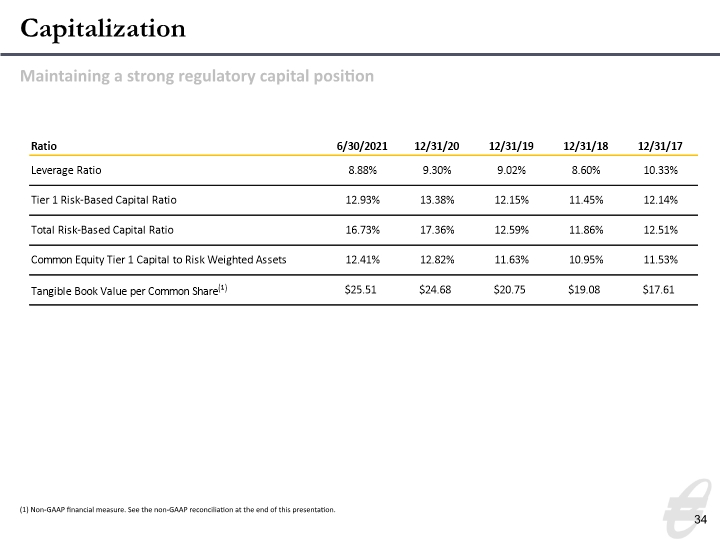

Capital Ratios |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Tier 1 Leverage Ratio |

|

| 8.88 | % |

|

| 8.73 | % |

|

| 9.30 | % |

|

| 8.76 | % |

|

| 8.52 | % |

Common Equity Tier 1 Capital Ratio |

|

| 12.41 | % |

|

| 12.53 | % |

|

| 12.82 | % |

|

| 12.76 | % |

|

| 12.02 | % |

Tier 1 Risk Based Capital Ratio |

|

| 12.93 | % |

|

| 13.08 | % |

|

| 13.37 | % |

|

| 13.32 | % |

|

| 12.57 | % |

Total Risk Based Capital Ratio |

|

| 16.73 | % |

|

| 17.02 | % |

|

| 17.35 | % |

|

| 17.35 | % |

|

| 15.33 | % |

Total stockholders' equity to total assets |

|

| 9.68 | % |

|

| 9.48 | % |

|

| 10.16 | % |

|

| 10.40 | % |

|

| 11.41 | % |

Tangible common equity to tangible assets* |

|

| 8.68 | % |

|

| 8.44 | % |

|

| 9.05 | % |

|

| 9.23 | % |

|

| 8.00 | % |

Book value per common share |

| $ | 28.76 |

|

| $ | 27.66 |

|

| $ | 28.04 |

|

| $ | 27.08 |

|

| $ | 31.53 |

|

Tangible book value per common share* |

| $ | 25.51 |

|

| $ | 24.34 |

|

| $ | 24.68 |

|

| $ | 23.72 |

|

| $ | 21.29 |

|

Tangible book value per diluted common share* |

| $ | 24.98 |

|

| $ | 23.87 |

|

| $ | 24.32 |

|

| $ | 23.57 |

|

| $ | 21.13 |

|

* The value noted is considered a Non-GAAP financial measure. For a reconciliation of Non-GAAP financial measures, see Table 8. Non-GAAP Financial Measures

Equity Bancshares, Inc.

PRESS RELEASE - 07/19/2021

TABLE 5. YEAR-TO-DATE NET INTEREST INCOME ANALYSIS (Unaudited)

(Dollars in thousands)

| For the six months ended |

|

| For the six months ended |

| ||||||||||||||||||

June 30, 2021 |

|

| June 30, 2020 |

| |||||||||||||||||||

| Average Outstanding Balance |

|

| Interest Income/ Expense |

|

| Average Yield/Rate(3)(4) |

|

| Average Outstanding Balance |

|

| Interest Income/ Expense |

|

| Average Yield/Rate(3)(4) |

| ||||||

Interest-earning assets |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Loans (1) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Commercial and industrial | $ | 814,895 |

|

| $ | 20,962 |

|

|

| 5.19 | % |

| $ | 712,115 |

|

| $ | 16,258 |

|

|

| 4.59 | % |

Commercial real estate |

| 981,482 |

|

|

| 22,873 |

|

|

| 4.70 | % |

|

| 923,625 |

|

|

| 25,134 |

|

|

| 5.47 | % |

Real estate construction |

| 254,807 |

|

|

| 4,531 |

|

|

| 3.59 | % |

|

| 260,530 |

|

|

| 6,413 |

|

|

| 4.95 | % |

Residential real estate |

| 430,123 |

|

|

| 9,093 |

|

|

| 4.26 | % |

|

| 481,716 |

|

|

| 10,156 |

|

|

| 4.24 | % |

Agricultural real estate |

| 136,366 |

|

|

| 3,384 |

|

|

| 5.00 | % |

|

| 134,098 |

|

|

| 4,046 |

|

|

| 6.07 | % |

Agricultural |

| 94,596 |

|

|

| 2,062 |

|

|

| 4.40 | % |

|

| 87,892 |

|

|

| 2,576 |

|

|

| 5.89 | % |

Consumer |

| 83,083 |

|

|

| 1,906 |

|

|

| 4.63 | % |

|

| 66,128 |

|

|

| 2,420 |

|

|

| 7.36 | % |

Total loans |

| 2,795,352 |

|

|

| 64,811 |

|

|

| 4.68 | % |

|

| 2,666,104 |

|

|

| 67,003 |

|

|

| 5.05 | % |

Securities |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Taxable securities |

| 863,801 |

|

|

| 7,322 |

|

|

| 1.71 | % |

|

| 763,992 |

|

|

| 8,637 |

|

|

| 2.27 | % |

Nontaxable securities |

| 103,529 |

|

|

| 1,441 |

|

|

| 2.81 | % |

|

| 128,616 |

|

|

| 1,846 |

|

|

| 2.89 | % |

Total securities |

| 967,330 |

|

|

| 8,763 |

|

|

| 1.83 | % |

|

| 892,608 |

|

|

| 10,483 |

|

|

| 2.36 | % |

Federal funds sold and other |

| 165,408 |

|

|

| 556 |

|

|

| 0.68 | % |

|

| 94,234 |

|

|

| 1,004 |

|

|

| 2.14 | % |

Total interest-earning assets | $ | 3,928,090 |

|

|

| 74,130 |

|

|

| 3.81 | % |

| $ | 3,652,946 |

|

|

| 78,490 |

|

|

| 4.32 | % |

Interest-bearing liabilities |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Savings, NOW and money market deposits | $ | 2,073,658 |

|

|

| 1,865 |

|

|

| 0.18 | % |

| $ | 1,739,527 |

|

|

| 4,048 |

|

|

| 0.47 | % |

Time deposits |

| 599,353 |

|

|

| 2,570 |

|

|

| 0.86 | % |

|

| 769,820 |

|

|

| 6,715 |

|

|

| 1.75 | % |

Total interest-bearing deposits |

| 2,673,011 |

|

|

| 4,435 |

|

|

| 0.33 | % |

|

| 2,509,347 |

|

|

| 10,763 |

|

|

| 0.86 | % |

FHLB advances |

| 23,911 |

|

|

| 145 |

|

|

| 1.22 | % |

|

| 283,231 |

|

|

| 1,727 |

|

|

| 1.23 | % |

Other borrowings |

| 131,687 |

|

|

| 3,161 |

|

|

| 4.84 | % |

|

| 86,784 |

|

|

| 1,014 |

|

|

| 2.35 | % |

Total interest-bearing liabilities | $ | 2,828,609 |

|

|

| 7,741 |

|

|

| 0.55 | % |

| $ | 2,879,362 |

|

|

| 13,504 |

|

|

| 0.94 | % |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net interest income |

|

|

|

| $ | 66,389 |

|

|

|

|

|

|

|

|

|

| $ | 64,986 |

|

|

|

|

|

Interest rate spread |

|

|

|

|

|

|

|

|

| 3.26 | % |

|

|