QuickLinks -- Click here to rapidly navigate through this document

As filed with the Securities and Exchange Commission on January 15, 2004

Registration No. 333-

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-4

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Compass Minerals International, Inc.

(formerly Salt Holdings Corporation)

(Exact name of registrant as specified in its charter)

| Delaware | 1400 | 36-3972986 | ||

| (State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification No.) |

8300 College Boulevard

Overland Park, Kansas 66210

(913) 344-9200

(Address, including zip code, and telephone number, including area code,

of the registrant's principal executive offices)

Michael E. Ducey

Chief Executive Officer and President

8300 College Boulevard

Overland Park, Kansas 66210

(913) 344-9200

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

Gregory A. Ezring, Esq.

Latham & Watkins LLP

885 Third Avenue, Suite 1000

New York, New York 10022

(212) 906-1200

Approximate date of commencement of proposed exchange offer: As soon as practicable after the effective date of this registration statement.

If the securities being registered on this form are being offered in connection with the formation of a holding company and there is compliance with General Instruction G, check the following box. o

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

CALCULATION OF REGISTRATION FEE

| Title of Each Class of Securities to be Registered | Amount to be Registered | Proposed Maximum Offering Price per Exchange Note(1)(2) | Proposed Maximum Aggregate Offering Price(1)(2) | Amount of Registration Fee(1)(2) | ||||

|---|---|---|---|---|---|---|---|---|

| 12% Senior Subordinated Discount Notes due 2013 | $179,600,000 | 60.073% | $107,891,190 | $8,729 | ||||

- (1)

- The registration fee has been calculated pursuant to Rule 457 under the Securities Act of 1933. The Proposed Maximum Aggregate Offering Price is estimated solely for the purpose of calculating the registration fee.

- (2)

- The Proposed Maximum Aggregate Offering Price is based on the book value of the notes, as of January 15, 2004, in the absence of a market for them as required by Rule 457(f)(2) under the Securities Act.

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Subject to completion, dated January 15, 2004

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not an offer to buy these securities in any state where the offer or sale is not permitted.

PROSPECTUS

COMPASS MINERALS INTERNATIONAL, INC.

(FORMERLY SALT HOLDINGS CORPORATION)

OFFER TO EXCHANGE

$179,600,000 aggregate principal amount at maturity of its 12% Series B Senior Subordinated Discount Notes due 2013, which have been registered under the Securities Act, for any and all of its outstanding 12% Series A Senior Subordinated Discount Notes due 2013.

We are offering to exchange our 12% series B senior subordinated discount notes due 2013, or the "exchange notes," for our currently outstanding 12% series A senior subordinated discount notes due 2013, or the "outstanding notes." We refer to the outstanding notes and the exchange notes collectively in this prospectus as the "notes." The exchange notes are substantially identical to the outstanding notes, except that the exchange notes have been registered under the federal securities laws and will not bear any legend restricting their transfer. The exchange notes will represent the same debt as the outstanding notes and we will issue the exchange notes under the same indenture.

We may redeem up to 35% of the exchange notes using proceeds from one or more equity offerings on or prior to June 1, 2006. We may redeem the exchange notes on or after June 1, 2008 at the prices set forth in this prospectus. Additionally, we may redeem the notes, in whole but not in part, upon a change of control prior to June 1, 2008. Holders may require us to repurchase the exchange notes upon a change of control. There is no sinking fund for the exchange notes. The exchange notes will be our senior subordinated obligations and will rank junior to all of our existing and future senior debt. As of September 30, 2003, the exchange notes would have been subordinated to $169.3 million of our debt. The notes are not guaranteed by any of our subsidiaries and will be effectively subordinated to the existing and future debt of our subsidiaries.

The principal features of the exchange offer are as follows:

- •

- The exchange offer expires at 5:00 p.m., New York City time, on , 2004, unless extended.

- •

- We will exchange all outstanding notes that are validly tendered and not validly withdrawn prior to the expiration of the exchange offer.

- •

- You may withdraw tendered outstanding notes at any time prior to the expiration of the exchange offer.

- •

- The exchange of outstanding notes for exchange notes pursuant to the exchange offer should not be a taxable event for U.S. federal income tax purposes.

- •

- We will not receive any proceeds from the exchange offer.

- •

- We do not intend to apply for listing of the exchange notes on any securities exchange or automated quotation system.

Broker-dealers receiving exchange notes in exchange for outstanding notes acquired for their own account though market making or other trading activities must deliver a prospectus in any resale of the exchange notes.

Investing in the exchange notes involves risks. See "Risk Factors" beginning on page 12.

Neither the U.S. Securities and Exchange Commission nor any other federal or state agency has approved or disapproved of these securities to be distributed in the exchange offer, nor have any of these organizations determined that this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The date of this prospectus is , 2004.

Each broker-dealer that receives exchange notes for its own account pursuant to the exchange offer must acknowledge that it will deliver a prospectus in connection with any resale of such exchange notes. The letter of transmittal delivered with this prospectus states that by so acknowledging and by delivering a prospectus, a broker-dealer will not be deemed to admit that it is an "underwriter" within the meaning of the Securities Act of 1933, as amended. This prospectus, as it may be amended or supplemented from time to time, may be used by a broker-dealer in connection with resales of exchange notes received in exchange for outstanding notes where such outstanding notes were acquired by such broker-dealer as a result of market making activities or other trading activities. We have agreed that, for a period of 180 days after the completion of the exchange offer, we will make this prospectus available to any broker-dealer for use in connection with any such resale. See "Plan of Distribution."

We have not authorized any dealer, salesman or other person to give any information or to make any representation other than those contained or incorporated by reference in this prospectus. You must not rely upon any information or representation not contained or incorporated by reference in this prospectus as if we had authorized it. This prospectus does not constitute an offer to sell or a solicitation of an offer to buy any securities other than the registered securities to which it relates, nor does this prospectus constitute an offer to sell or a solicitation of an offer to buy securities in any jurisdiction to any person to whom it is unlawful to make such offer or solicitation in such jurisdiction.

CAUTIONARY NOTE REGARDING

FORWARD-LOOKING STATEMENTS

This prospectus, including the sections entitled "Prospectus Summary" and "Business," contains forward-looking statements. These statements relate to future events or our future financial performance, and involve known and unknown risks, uncertainties and other factors that may cause our actual results, levels of activity, performance or achievements to be materially different from any future results, levels of activity, performance or achievements, expressed or implied, by these forward-looking statements. These risks and other factors include, among other things, those listed in "Risk Factors" and elsewhere in this prospectus. In some cases, you can identify forward-looking statements by terminology such as "may," "will," "should," "expects," "intends," "plans," "anticipates," "believes," "estimates," "predicts," "potential," "continue" or the negative of these terms or other comparable terminology. These statements are only predictions. Actual events or results may differ materially. In evaluating these statements, you should specifically consider various factors, including the risks outlined in "Risk Factors." These factors may cause our actual results to differ materially from any forward-looking statement.

Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, performance or achievements. We are under no duty to update any of the forward-looking statements after the date of this prospectus.

i

MARKET AND INDUSTRY DATA AND FORECASTS

This prospectus includes market share and industry data and forecasts that we obtained from internal company surveys, market research, consultant surveys, publicly available information and industry publications and surveys. Industry surveys, publications, consultant surveys and forecasts generally state that the information contained therein has been obtained from sources believed to be reliable, but there can be no assurance as to the accuracy and completeness of such information. We have not independently verified any of the data from third-party sources nor have we ascertained the underlying economic assumptions relied upon therein. Similarly, internal company surveys, industry forecasts and market research, which we believe to be reliable based upon management's knowledge of the industry, have not been verified by any independent sources. In addition, we do not know what assumptions regarding general economic growth were used in preparing the forecasts we cite. Except where otherwise noted, references to North America include only the continental United States and Canada, and statements as to our position relative to our competitors or as to market share refer to the most recent available data. Statements concerning (a) North America general trade salt are generally based on historical sales volumes, (b) North America highway deicing salt are generally based on historical production capacity, (c) sulfate of potash are generally based on historical sales volumes and (d) United Kingdom salt sales (general trade and highway deicing) are generally based on sales volumes. Except where otherwise noted, all references to tons refer to "short tons." One short ton equals 2,000 pounds.

The following items referred to in this prospectus are fiduciary registered and other trademarks pursuant to applicable intellectual property laws and are the property of our wholly owned subsidiary Compass Minerals Group, Inc. or its subsidiaries: "Sifto®," "American Stockman®," "Safe Step®," "Winter Storm®," "Guardian®," "FreezGard®," "Nature's Own®" and "K-Life®."

ii

WHERE YOU CAN FIND MORE INFORMATION

We have filed with the U.S. Securities and Exchange Commission, or the "SEC," a registration statement on Form S-4, the "exchange offer registration statement," which term shall encompass all amendments, exhibits, annexes and schedules thereto, pursuant to the Securities Act of 1933, as amended, and the rules and regulations thereunder, which we refer to collectively as the "Securities Act," covering the exchange notes being offered. This prospectus does not contain all the information in the exchange offer registration statement. For further information with respect to Compass Minerals International, Inc. and the exchange offer, reference is made to the exchange offer registration statement. Statements made in this prospectus as to the contents of any contract, agreement or other documents referred to are not necessarily complete. For a more complete understanding and description of each contract, agreement or other document filed as an exhibit to the exchange offer registration statement, we encourage you to read the documents contained in the exhibits.

We are currently obligated to file annual, quarterly and current reports, proxy statements and other information with the SEC. We intend to make these filings available on our website upon each filing. Furthermore, the indenture governing the notes provides that we will furnish to the holders of the notes copies of the periodic reports required to be filed by us with the SEC under the Securities Exchange Act of 1934, as amended, and the rules and regulations thereunder, which we refer to collectively as the "Exchange Act." In addition, we will provide the trustee for the notes within 15 days after such filings with annual reports containing the information required to be contained in Form 10-K and quarterly reports containing the information required to be contained in Form 10-Q promulgated by the Exchange Act. If the filing of such information is not accepted by the SEC or is prohibited by the Exchange Act, you can obtain a copy of such report, at no cost, by writing or telephoning us at the following address:

Compass Minerals International, Inc.

8300 College Boulevard

Overland Park, Kansas 66210

Attention: Chief Financial Officer

(913) 344-9200

To ensure timely delivery, please make your request as soon as practicable and, in any event, no later than five business days prior to the expiration of the exchange offer.

You may read and copy any document we file with the SEC at the SEC's public reference room at 450 Fifth Street, N.W., Washington, D.C. 20549. Please call the SEC at 1-800-SEC-0330 for further information on the public reference room. Our SEC filings are also available to the public at the SEC's web site athttp://www.sec.gov.

iii

This summary highlights important information about this offering and our business. It does not include all information you should consider before investing in the exchange notes. Please review this prospectus in its entirety, including the risk factors and our financial statements and the related notes, before you decide to invest. Unless otherwise noted, the terms the "Company," "Compass Minerals," "we," "us" and "our" refer to Compass Minerals International, Inc. (formerly known as Salt Holdings Corporation) and its consolidated subsidiaries, collectively, and "Compass Minerals Group" refers to Compass Minerals Group, Inc., a wholly owned subsidiary of the Company.

Summary of the Terms of the Exchange Offer

The following is a brief summary of terms of the exchange offer. For a more complete description of the exchange offer, see "The Exchange Offer."

| Securities Offered | $179,600,000 in aggregate principal amount at maturity of 12% Series B Senior Subordinated Discount Notes due 2013. | |

Exchange Offer | We are offering to exchange $1,000 principal amount at maturity of our 12% Series B Senior Subordinated Discount Notes due 2013, which have been registered under the Securities Act, for each $1,000 principal amount at maturity of our currently outstanding 12% Series A Senior Subordinated Discount Notes due 2013. We will accept any and all outstanding notes validly tendered and not withdrawn prior to 5:00 p.m., New York City time, on , 2004. Holders may tender some or all of their outstanding notes pursuant to the exchange offer. However, notes may be tendered only in integral multiples of $1,000 in principal amount at maturity. The form and terms of the exchange notes are the same as the form and terms of the outstanding notes except that: | |

• the exchange notes have been registered under the federal securities laws and will not bear any legend restricting their transfer; | ||

• the exchange notes bear a series B designation and a different CUSIP number than the outstanding notes; and | ||

• the holders of the exchange notes will not be entitled to certain rights under the registration rights agreement, including the provisions for an increase in the interest rate on the outstanding notes in some circumstances relating to the timing of the exchange offer. | ||

See "The Exchange Offer." |

1

Transferability of Exchange Notes | We believe that you will be able to freely transfer the exchange notes without registration or any prospectus delivery requirement so long as you may accurately make the representations listed under "The Exchange Offer—Transferability of the Exchange Notes." If you are a broker-dealer that acquired outstanding notes as a result of market making or other trading activities, you must deliver a prospectus in connection with any resale of the exchange notes. See "Plan of Distribution." | |

Expiration Date | The exchange offer will expire at 5:00 p.m., New York City time, on , 2004, unless we decide to extend the exchange offer. | |

Conditions to the Exchange Offer | The exchange offer is subject to customary conditions, including our determination that the exchange offer does not violate any law, statute, rule, regulation or interpretation by the staff of the SEC or any other government agency or court of competent jurisdiction, some of which may be waived by us. See "The Exchange Offer—Conditions to the Exchange Offer." | |

Procedures for Tendering Outstanding Notes | If you wish to accept the exchange offer, you must complete, sign and date the letter of transmittal, or a facsimile of the letter of transmittal, in accordance with the instructions contained in this prospectus and in the letter of transmittal. You should then mail or otherwise deliver the letter of transmittal, or facsimile, together with the outstanding notes to be exchanged and any other required documentation, to the exchange agent at the address set forth in this prospectus and in the letter of transmittal. | |

By executing the letter of transmittal, you will represent to us that, among other things: | ||

• you, or the person or entity receiving the related exchange notes, are acquiring the exchange notes in the ordinary course of business; | ||

• neither you nor any person or entity receiving the related exchange notes is engaging in or intends to engage in a distribution of the exchange notes within the meaning of the federal securities laws; | ||

• neither you nor any person or entity receiving the related exchange notes has an arrangement or understanding with any person or entity to participate in any distribution of the exchange notes; | ||

• neither you nor any person or entity receiving the related exchange notes is an "affiliate" of Compass Minerals, as that term is defined under Rule 405 of the Securities Act; and | ||

• you are not acting on behalf of any person or entity who could not truthfully make these statements. |

2

See "The Exchange Offer—Procedures for Tendering Outstanding Notes" and "Plan of Distribution." | ||

Effect of Not Tendering | Any outstanding notes that are not tendered, or that are tendered but not accepted, will remain subject to the restrictions on transfer. Since the outstanding notes have not been registered under the federal securities laws, they bear a legend restricting their transfer absent registration or the availability of a specific exemption from registration. Upon the completion of the exchange offer, we will have no further obligations, except under limited circumstances, to provide for registration of the outstanding notes under the federal securities laws. See "The Exchange Offer—Effect of Not Tendering." | |

Withdrawal Rights | Tenders of outstanding notes may be withdrawn at any time prior to 5:00 p.m., New York City time, on the Expiration Date. | |

United States Federal Income Tax Consequences | The exchange of the exchange notes for the outstanding notes in the exchange offer should not be treated as an "exchange" for U.S. federal income tax purposes. See "Material United States Federal Income Tax Consequences." | |

Use of Proceeds | We will not receive any proceeds from the issuance of exchange notes pursuant to the exchange offer. See "Use of Proceeds." | |

Exchange Agent | The Bank of New York, the trustee under the indenture, is serving as exchange agent in connection with the exchange offer. |

3

The following is a brief summary of the terms of the exchange notes. The financial terms and covenants of the exchange notes are the same as the outstanding notes. For a more complete description of the terms of the exchange notes, see "Description of the Exchange Notes."

| Issuer | Compass Minerals International, Inc. | |

Securities Offered | $179,600,000 in aggregate principal amount at maturity of our 12% Series B Senior Subordinated Discount Notes due 2013. | |

Maturity Date | June 1, 2013. | |

Interest | Prior to June 1, 2008, interest will accrue on the exchange notes in the form of an increase in the accreted value of the exchange notes. Thereafter, cash interest on the exchange notes will accrue and be payable semiannually in arrears on June 1 and December 1 of each year, commencing on December 1, 2008, at a rate of 12% per annum. The accreted value of each exchange note will increase from the date of issuance until June 1, 2008 at a rate of 12% per annum, reflecting the accrual of non-cash interest, such that the accreted value will equal the principal amount at maturity on June 1, 2008. | |

Original Issue Discount | The exchange notes are being offered with original issue discount for U.S. federal income tax purposes. Thus, although cash interest will not be payable on the exchange notes prior to December 1, 2008, interest will accrue from the issue date of the exchange notes based on the yield to maturity of the exchange notes and will be included as interest income (including for periods ending prior to June 1, 2008) for U.S. federal income tax purposes in advance of receipt of the cash payments to which the income is attributable. See "Material United States Federal Income Tax Consequences." | |

Ranking | The exchange notes are unsecured senior subordinated obligations of ours. Accordingly, they will rank: | |

• subordinated in right of payment to all of our existing and future senior indebtedness, including our guarantee of our senior credit facilities and the 123/4% senior discount notes due 2012, or the "senior discount notes;" | ||

• equally with any of our future unsecured senior subordinated indebtedness; | ||

• ahead of any of our current and future debt that expressly provides for subordination to the exchange notes; and | ||

• senior to any of our future indebtedness that is expressly subordinated in right of payment to the notes. | ||

As of September 30, 2003, the notes would have ranked junior to approximately $169.3 million of our senior indebtedness. |

4

The exchange notes will be effectively subordinated to all of the existing and future indebtedness of our subsidiaries. As of September 30, 2003, our subsidiaries had total liabilities of $619.2 million. | ||

Optional Redemption | We may redeem any of the exchange notes at any time on or after June 1, 2008, in whole or in part, in cash at the redemption prices described in this prospectus, plus accrued and unpaid interest to the date of redemption. At any one or more times on or before June 1, 2006, we may choose to repurchase up to 35% of the exchange notes with the money that we raise in one or more equity offerings, as long as we pay 112% of the accreted value of the exchange notes and at least 65% of the original aggregate principal amount at maturity of notes remains outstanding afterwards. See "Description of the Exchange Notes—Optional Redemption." | |

Change in Control | Upon a change in control, we may be required to make an offer to purchase each holder's exchange notes at a price equal to 101% of the principal amount thereof (or accreted value, as applicable), plus accrued and unpaid interest, if any, to the date of purchase. | |

In addition, upon a change in control prior to June 1, 2008, we may redeem the exchange notes, in whole but not in part, at a redemption price equal to the accreted value of the exchange notes plus an applicable premium. | ||

Basic Covenants of the Indenture | The indenture contains covenants that will, among other things, limit our ability and the ability of our restricted subsidiaries to: | |

• incur additional indebtedness; | ||

• pay dividends on, redeem or repurchase our capital stock; | ||

• make investments; | ||

• permit payment or dividend restrictions on our restricted subsidiaries; | ||

• sell assets; | ||

• create liens; | ||

• engage in transactions with affiliates; and | ||

• consolidate or merge or sell all or substantially all of our assets and the assets of our restricted subsidiaries. | ||

In addition, we will be obligated to offer to repurchase the exchange notes at 100% of their accreted value, plus accrued and unpaid interest, if any, to the date of repurchase, in the event of certain asset sales. | ||

These restrictions and prohibitions are subject to a number of important qualifications and exceptions. See "Description of the Exchange Notes—Certain Covenants." |

5

Absence of a Public Market for the Exchange Notes | The exchange notes are new securities, for which there is currently no established trading market and none may develop. Accordingly, there can be no assurance as to the development or liquidity of any market for the exchange notes. The initial purchasers of the outstanding notes have advised us that they intend to make a market in the exchange notes. However, they are not obligated to do so and may discontinue any market making activities with respect to the exchange notes at any time without notice. We do not intend to apply for listing of the exchange notes on any securities exchange or to arrange for any quotation system to quote them. |

See the section entitled "Risk Factors" beginning on page 12 for a discussion of factors you should carefully consider before deciding to invest in the exchange notes.

6

We are the largest producer of rock, or highway deicing, salt in North America and the United Kingdom, and operate the largest highway deicing salt mines in these regions. We are also the third largest producer of general trade salt in North America and the second largest in the United Kingdom, serving major retailers, agricultural cooperatives and food producers. In addition, we are the largest producer of sulfate of potash, or "SOP," in North America, which is used in the production of specialty fertilizers. Salt is one of the most widely used minerals in the world and has a wide variety of end-use applications, including highway deicing, food grade applications, water conditioning and various industrial uses. Our business also includes the following key characteristics:

• We believe that our cash flows are not materially impacted by economic cycles due to the stable end-use markets of salt and the absence of cost-effective alternatives.

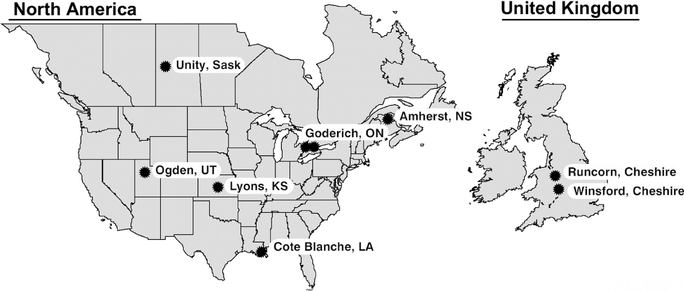

• We operate eleven facilities in North America and the United Kingdom, including the largest rock salt mine in the world in Goderich, Ontario and the largest salt mine in the United Kingdom in Winsford, Cheshire.

• We believe that we are among the lowest cost rock salt producers in our markets. Our cost advantage is due to the size and quality of our reserves, effective mining techniques and efficient production processes. In addition, our salt mines in North America are located near either rail or water transport systems, thereby minimizing shipping and handling costs, which constitute a significant portion of the overall delivered cost of salt.

For the year ended December 31, 2002, and the nine months ended September 30, 2003, we sold approximately 11.0 million and 8.6 million tons of salt and other minerals, generating sales of $502.6 million and $398.5 million and net income of $77.6 million and $11.3 million, respectively.

We operate through the following product lines:

Highway Deicing

We are the largest producer of rock, or highway deicing, salt in North America. We also operate the largest highway deicing salt mine in the United Kingdom at Winsford, Cheshire and provide an estimated 55% of the United Kingdom's highway deicing salt requirements. We believe we are the only local supplier of highway deicing salt capable of meeting peak winter demand in the United Kingdom. In addition, our highway deicing product line includes the following characteristics:

• We sell primarily to state, provincial, county and municipal highway departments for deicing applications for which demand depends largely on the number of snowfall days.

• While subject to seasonal variations in demand, highway-deicing salt is not materially affected by an economic downturn, as it is an essential part of highway maintenance to ensure public safety and continued personal and commercial mobility.

• Due to the lack of cost-effective alternatives and the steadily expanding highway infrastructure, the production of highway deicing salt in the United States has increased over time at a historical average of approximately 1% per annum during the thirty year period ending 2002, while prices have increased at a historical average of approximately 4% per annum during the same period.

General Trade Salt

We are the third largest producer of general trade salt in North America and the second largest in the United Kingdom, serving major retailers, agricultural cooperatives and food producers. Our general trade salt product line includes the following key characteristics:

• We offer a full range of salt products distributed to several end use markets, including consumer applications such as table salt, water conditioning, consumer ice control, food processing, agricultural applications and a variety of industrial applications.

7

• We believe we are the largest private label producer of water conditioning salt and the largest producer of salt-based agricultural products in North America based on tonnage.

• We manufacture more than 70 private labels of table salt for grocers and major retailers and, in Canada, we market salt under the popular Sifto® brand name.

• We are the market leader in the United Kingdom for evaporated salt used for water conditioning.

• Our operations are generally not susceptible to economic cycles as a result of the non-discretionary need for, and low cost of, salt. During the thirty year period ending 2002, the production of general trade salt products in the United States has increased at a historical average of over 1% per annum, while prices for general trade products has increased at a historical average of approximately 5% per annum over the same period.

Sulfate of Potash

We are the market leader in North American sales of SOP. Approximately 62% of our SOP sales in 2002 were made to domestic customers, which include fertilizer manufacturers, dealers and distributors. Our SOP product line includes the following key characteristics:

• SOP is primarily used as a specialty fertilizer, providing essential potassium to high-value, chloride-sensitive crops, such as vegetables, fruits, tea, tobacco and turf grass. We believe that there are growth opportunities for SOP both domestically and internationally because of its favorable impact on crop yield and quality.

�� We believe we are the low cost producer of SOP in North America. We leverage our abundant mineral resources and unique low cost manufacturing process to achieve margins that are attractive compared to other fertilizer products.

We believe that SOP requires more intense focus and active marketing efforts to sell the benefits of utilizing this product compared to other fertilizer products. In addition, we believe that SOP, as a specialty fertilizer was a non-core product of IMC Global and did not receive sufficient focus to realize its market potential. As we continue our market development of our SOP product line, we believe that we can take advantage of the significant growth opportunities arising from SOP's superior performance over commodity potash. See "Business—Specialty Potash Segment."

On December 17, 2003, the Company completed an initial public offering of 16,675,000 shares of its common stock, par value $.01 per share, at an initial public offering price of $13.00 per share. In connection with the offering, the Company changed its name from Salt Holdings Corporation to Compass Minerals International, Inc. The shares were sold by certain stockholders of the Company and the Company did not receive any proceeds from the sale of the shares. Apollo Management V, L.P., or "Apollo," and IMC Global each sold more than one-half of their beneficial holdings of the Company's common stock, which reduced Apollo's beneficial ownership of the Company's common stock from 87.73% to 35.97% and reduced IMC Global's beneficial ownership of the Company's common stock from 5.76% to 2.36%. Certain members of management, including the president and chief executive officer, also sold approximately 10% of their holdings of the Company's common stock in the initial public offering. There was no change in the Company's management as a result of the initial public offering and the initial public offering does not constitute a change of control under the indenture governing the notes.

The Company intends to pay quarterly cash dividends on its common stock at an initial annual rate of $0.75 per share. The declaration and payment of future dividends to holders of the Company's common stock will be at the discretion of our board of directors and will depend upon many factors, including our financial condition, earnings, legal requirements, restrictions in our debt agreements and other factors our board of directors deems relevant.

8

Post-Recapitalization Organization

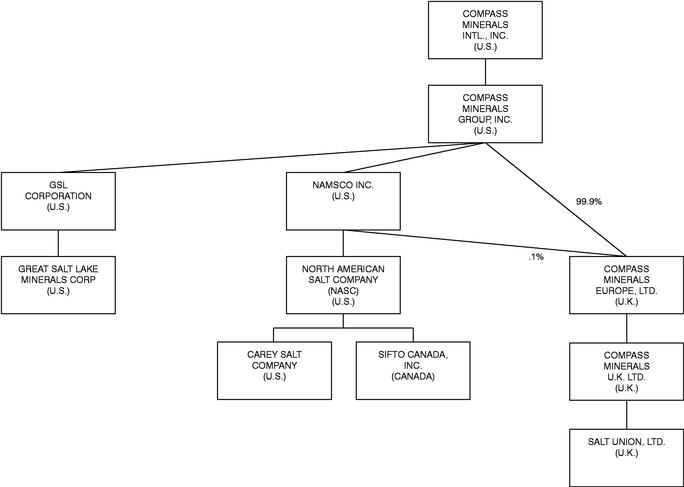

On November 28, 2001, Apollo, a managed investment fund, through its subsidiary YBR Holdings LLC, or "YBR Holdings," acquired a controlling interest in our common stock from IMC Global and has effective control over our business and affairs pursuant to a recapitalization of the Company, or the "Recapitalization." See "Risk Factors—We are controlled by our principal stockholder whose interests may conflict with or differ from your interests" and "Principal Stockholders." We were ultimately structured as a holding company, with no operations of our own and derive substantially all of our revenue and cash flow from our operating subsidiaries. All of our operating subsidiaries are wholly owned subsidiaries of GSL Corporation, NAMSCO Inc. and Compass Minerals (Europe) Limited, which are wholly owned by Compass Minerals Group. The diagram below summarizes our corporate organization as a result of the consummation of the Recapitalization.

9

Summary Combined and Consolidated Financial Information

The following table presents summary combined and consolidated financial information. The statement of operations data for the years ended December 31, 2002, 2001 and 2000 and the balance sheet data as of December 31, 2002 and 2001 have been derived from our audited combined and consolidated financial statements included elsewhere in this prospectus. The statement of operations data for the year ended December 31, 1999 and for the nine months ended December 31, 1998 and the balance sheet data as of December 31, 2000 and 1999 have been derived from our audited combined financial statements that are not included herein. The historical statement of operations data for the nine months ended September 30, 2003 and 2002, and the historical balance sheet data as of September 30, 2003 and 2002 and December 31, 1998 have been derived from unaudited combined and consolidated financial statements that, in the opinion of management, include all adjustments, consisting only of normal recurring adjustments, necessary to present fairly the data for such periods. The results of operations for the interim periods are not necessarily indicative of the operating results for the entire year or any future period.

Prior to November 28, 2001, Compass Minerals was incorporated as IMC Potash Corporation, an inactive wholly owned subsidiary of IMC Global. On November 28, 2001, Apollo, through its subsidiary YBR Holdings, acquired control of our business from IMC Global pursuant to the Recapitalization. Accordingly, prior to November 28, 2001, the combined and consolidated financial data reflect only the results of our wholly owned subsidiary Compass Minerals Group and its subsidiaries which were included in the Recapitalization. As part of the Recapitalization, IMC Potash Corporation was reincorporated as Salt Holdings Corporation, which is now known as Compass Minerals International, Inc. At November 28, 2001, IMC Global contributed the net assets of Compass Minerals Group to the Company.

The information included in this table should be read in conjunction with "Management's Discussion and Analysis of Financial Condition and Results of Operations" and the audited and unaudited combined and consolidated financial statements and accompanying notes thereto included elsewhere in this prospectus.

| | For the nine months ended December 31, | For the years ended December 31, | For the nine months ended September 30, | |||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | 1998 | 1999 | 2000 | 2001 | 2002 | 2002 | 2003 | |||||||||||||||

| | (dollars in millions) | |||||||||||||||||||||

| Statement of Operations Data: | ||||||||||||||||||||||

| Sales | $ | 277.7 | $ | 494.4 | $ | 509.2 | $ | 523.2 | $ | 502.6 | $ | 336.9 | $ | 398.5 | ||||||||

| Cost of sales—shipping and handling | 55.8 | 126.9 | 140.0 | 143.2 | 137.5 | 91.2 | 109.3 | |||||||||||||||

| Cost of sales—products(1) | 111.8 | 213.1 | 227.7 | 224.4 | 202.1 | 144.6 | 168.3 | |||||||||||||||

| Depreciation and amortization(2) | 34.3 | 55.1 | 44.3 | 32.6 | 37.1 | 28.7 | 31.2 | |||||||||||||||

| Selling, general and administrative expenses | 36.7 | 37.2 | 35.5 | 38.9 | 40.6 | 30.1 | 34.3 | |||||||||||||||

| Goodwill write-down(3) | — | 87.5 | 191.0 | — | — | — | — | |||||||||||||||

| Restructuring and other charges(3)(4) | 20.3 | 13.7 | 425.9 | 27.0 | 7.7 | 6.8 | — | |||||||||||||||

| Operating earnings (loss) | 18.8 | (39.1 | ) | (555.2 | ) | 57.1 | 77.6 | 35.5 | 55.4 | |||||||||||||

| Interest expense(5) | 17.4 | 19.0 | 16.4 | 14.4 | 42.4 | 31.8 | 40.5 | |||||||||||||||

| Net income (loss) | (14.4 | ) | (67.5 | ) | (467.7 | ) | 19.0 | 18.9 | 0.3 | 11.3 | ||||||||||||

Balance Sheet Data (at period end): | ||||||||||||||||||||||

| Total cash and cash equivalents | $ | 4.9 | $ | 4.3 | $ | 0.3 | $ | 15.9 | $ | 11.9 | $ | 7.5 | $ | 3.6 | ||||||||

| Total assets | 1,423.0 | 1,290.5 | 636.0 | 655.6 | 644.1 | 598.0 | 620.3 | |||||||||||||||

| Series A redeemable preferred stock(6) | — | — | — | 74.6 | 19.1 | 83.1 | 1.8 | |||||||||||||||

| Total debt(7) | 264.7 | 196.0 | 152.4 | 526.5 | 507.8 | 451.2 | 601.6 | |||||||||||||||

Other Financial Data: | ||||||||||||||||||||||

| Cash flows provided by operating activities | $ | 25.7 | $ | 78.4 | $ | 72.1 | $ | 112.4 | $ | 82.4 | $ | 57.8 | $ | 51.4 | ||||||||

| Cash flows used for investing activities | (39.3 | ) | (48.1 | ) | (34.0 | ) | (43.6 | ) | (19.1 | ) | (11.8 | ) | (31.0 | ) | ||||||||

| Cash flows (used for) provided by financing activities | 6.4 | (33.6 | ) | (43.3 | ) | (53.7 | ) | (69.8 | ) | (56.5 | ) | (30.1 | ) | |||||||||

| Ratio of earnings to fixed charges(8) | — | — | — | 3.69 | x | 1.67 | x | — | 1.29 | x | ||||||||||||

| Capital expenditures | $ | 39.6 | $ | 45.6 | $ | 33.7 | $ | 43.0 | $ | 19.5 | $ | 12.1 | $ | 9.7 | ||||||||

10

- (1)

- "Cost of sales—products" is presented net of depreciation and amortization.

- (2)

- "Depreciation and amortization" for purposes of this table excludes amortization of deferred financing costs.

- (3)

- Based on anticipated proceeds from the sale of the Company by IMC Global, we recorded an asset impairment charge of $616.6 million, $482.1 million after tax, in the fourth quarter of 2000. In connection with this non-cash charge, goodwill was reduced $191.0 million and intangible assets—mineral interests was reduced $425.6 million. The goodwill write-down in 1999 was the result of lowering goodwill to its recoverable value based on estimated future discounted cash flows of the business.

- (4)

- "Restructuring and other charges" include primarily those charges related to the impairment of idled assets in December of 1998, the restructuring of our business in the fourth quarter of 1999 designed to reduce employee headcount and an asset impairment in the fourth quarter of 2000 related to the planned disposition of the Company by IMC Global as described in (3) above. During 2001, we incurred $27.0 million of transaction and transition costs in connection with the Recapitalization. During 2002, we incurred $7.7 million of transition costs in connection with separating the Company from IMC Global. Substantially all cash payments related to these charges have been made.

- (5)

- As we have incurred substantial indebtedness in connection with the Recapitalization, we believe it is helpful to provide a measure describing the cash requirements necessary to satisfy our debt service in terms of "cash interest expense," which is interest expense less non-cash interest related to the outstanding notes, the senior discount notes, the Seller Notes and the amortization of debt issuance costs, plus amortization of the original issuance premium. For a discussion of our indebtedness, see Note 8 to our audited combined and consolidated financial statements and "Description of Other Indebtedness." For a discussion of the Seller Notes, see Note 11 to our audited combined and consolidated financial statements. Cash interest expense was $39.6 million, $29.7 million and $28.1 million for the year ended December 31, 2002 and the nine months ended September 30, 2002 and 2003, respectively. Cash interest expense is not calculated under GAAP. While cash interest expense and similar variations thereof is commonly used as a measure of the ability to meet debt service requirements, it is not necessarily comparable to other similarly titled captions of other companies due to potential inconsistencies in the method of calculation. The following table reconciles the differences between cash interest expense and interest expense, calculated in accordance with GAAP.

| | | For the nine months ended September 30, | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| | For the year ended December 31, 2002 | ||||||||||

| | 2002 | 2003 | |||||||||

| | (dollars in millions) | ||||||||||

| Interest expense | $ | 42.4 | $ | 31.8 | $ | 40.5 | |||||

Less non-cash interest expense: | |||||||||||

| Outstanding notes | — | — | 4.3 | ||||||||

| Senior discount notes | 0.2 | — | 6.4 | ||||||||

| Seller Notes | 0.8 | 0.8 | 0.2 | ||||||||

Less (plus) amortization: | |||||||||||

| Deferred financing costs | 1.9 | 1.4 | 1.7 | ||||||||

| Amortization of premium on senior subordinated notes | (0.1 | ) | (0.1 | ) | (0.2 | ) | |||||

| Cash interest expense | $ | 39.6 | $ | 29.7 | $ | 28.1 | |||||

- (6)

- In connection with the Company's initial public offering, we redeemed all of the outstanding shares of series A redeemable preferred stock on December 17, 2003 for $1.9 million (which includes an additional $0.1 million in accrued interest to the date of redemption).

- (7)

- "Total debt" does not include $9.3 million and $10.1 million of our senior subordinated debentures, or the "Settlement Notes," as of December 31, 2002 and September 30, 2003, respectively, including interest, currently held by a wholly owned subsidiary subject to reissuance if expected future levels of equity returns are not achieved (see Note 11 to our combined and consolidated financial statements). See "Management's Discussion and Analysis of Financial Condition and Results of Operations—Management's Discussion on Critical Accounting Policies—Seller Notes and Settlement Notes."

- (8)

- For the purposes of computing the ratio of earnings to fixed charges, earnings consist of earnings before income taxes and fixed charges. Fixed charges consist of net interest expense including the amortization of deferred debt issuance costs and the interest component of our operating rents. The ratio of earnings to fixed charges on a historical basis is not meaningful because we participated in a credit facility with IMC Global and its affiliates and the level of third-party debt was not comparable to the level of third-party debt in place upon consummation of the Recapitalization, the offering by Compass Minerals Group of an additional $75.0 million in aggregate principal amount of its 10% senior subordinated notes due 2011 on April 10, 2002, or the "April 2002 senior subordinated notes," the offering of the notes, the offering of the senior discount notes and the amendment to the senior credit facilities. Earnings were insufficient to cover fixed charges by approximately $1.5 million, $55.6 million, $572.5 million and $0.4 million, respectively, for the nine months ended December 31, 1998, the fiscal years ended December 31, 1999 and 2000, and for the nine months ended September 30, 2002.

11

You should carefully consider the following risks and all of the information set forth in this prospectus before participating in the exchange offer. The risks described below are not the only ones facing our company. Additional risks and uncertainties not currently known to us or that we currently deem to be immaterial may also materially and adversely affect our business, financial condition or results of operations.

Risks Relating to the Exchange Notes and the Exchange Offer

If you do not properly tender your outstanding notes, your ability to transfer such outstanding notes will be adversely affected.

We will only issue exchange notes in exchange for outstanding notes that are timely received by the exchange agent, together with all required documents, including a properly completed and signed letter of transmittal. Therefore, you should allow sufficient time to ensure timely delivery of the outstanding notes and you should carefully follow the instructions on how to tender your outstanding notes. If you do not tender your outstanding notes or if we do not accept your outstanding notes because you did not tender your outstanding notes properly, then, after we consummate the exchange offer, you may continue to hold outstanding notes that are subject to the existing transfer restrictions. In addition, if you tender your outstanding notes for the purpose of participating in a distribution of the exchange notes, you will be required to comply with the registration and prospectus delivery requirements of the Securities Act in connection with any resale of the exchange notes. If you are a broker-dealer that receives exchange notes for your own account in exchange for outstanding notes that you acquired as a result of market making activities or any other trading activities, you will be required to acknowledge that you will deliver a prospectus in connection with any resale of such exchange notes. After the exchange offer is consummated, if you continue to hold any outstanding notes, you may have difficulty selling them because there will be a smaller market for the remaining outstanding notes not tendered in the exchange offer. In addition, if a large amount of outstanding notes are not tendered or are tendered improperly, the limited amount of exchange notes that would be issued and outstanding after we consummate the exchange offer could lower the market price of such exchange notes.

Our substantial indebtedness could adversely affect our financial condition and prevent us from fulfilling our obligations under the exchange notes.

As of September 30, 2003, we had $601.6 million of outstanding indebtedness, including approximately $78.5 million under our senior credit facilities, $17.5 million under our revolving credit facility, $328.0 million of Compass Mineral Group's senior subordinated notes, $73.3 million of our senior discount notes, $104.3 million of our outstanding notes and a stockholders' deficit of $174.9 million. In addition, our outstanding indebtedness does not include $10.1 million of our Settlement Notes, including interest, currently held by a wholly owned subsidiary subject to reissuance if expected future levels of equity returns are not achieved (see Note 11 to our combined and consolidated financial statements). As a result, we are a highly leveraged company.

This level of leverage could have important consequences for you, including the following:

- •

- it may limit our ability to borrow money or sell stock to fund our working capital, capital expenditures and debt service requirements;

- •

- it may limit our flexibility in planning for, or reacting to, changes in our business;

- •

- we may be more highly leveraged than some of our competitors, which may place us at a competitive disadvantage;

- •

- it may make us more vulnerable to a downturn in our business or the economy;

12

- •

- it will require us to dedicate a substantial portion of our cash flow from operations to the repayment of our indebtedness, including the exchange notes, thereby reducing the availability of cash flow for other purposes; and

- •

- it may materially and adversely effect our business and financial condition if we are unable to service our indebtedness or obtain additional financing, as needed.

In addition, the indenture governing the notes, the indenture governing the senior discount notes and our senior credit facilities contain financial and other restrictive covenants discussed below that may limit our ability to engage in activities that may be in our long-term best interests. Our failure to comply with those covenants could result in an event of default which, if not cured or waived, could result in the acceleration of all of our debt. See "—Restrictive covenants in the agreements governing our indebtedness and certain indebtedness of Compass Minerals Group may restrict our ability to pursue business strategies. A default under our senior credit facilities may also prohibit us from making any payments on the exchange notes," "Description of Other Indebtedness" and "Description of the Exchange Notes."

Despite our substantial indebtedness we may still incur significantly more debt. This could exacerbate the risks described above.

The terms of the indenture governing the notes, the indenture governing the senior discount notes and our senior credit facilities permit us and our subsidiaries to incur significant additional indebtedness in the future. As of September 30, 2003, we had approximately $108.5 million available for additional borrowing under the revolving credit facility, subject to the satisfaction of customary conditions, including absence of a default and accuracy of representations and warranties. All borrowings under our senior credit facilities are effectively senior to the exchange notes.

We are a holding company with no operations of our own and depend on our subsidiaries for cash. Our ability to access the cash flow of our subsidiaries may be contingent upon our ability to refinance the debt of our subsidiaries.

We have no operations of our own and derive substantially all of our revenue and cash flow from our subsidiaries. None of our subsidiaries guaranteed these notes. Creditors of our subsidiaries (including trade creditors) will generally be entitled to payment from the assets of those subsidiaries before those assets can be distributed to us. As a result, these notes will effectively be subordinated to the prior payment of all of the debts (including trade payables) of our subsidiaries.

As of September 30, 2003, the aggregate amount of indebtedness and other liabilities of our subsidiaries was approximately $619.2 million, or approximately 78% of our total indebtedness and other liabilities. Further, approximately $108.5 million was available to our subsidiaries for additional borrowing under the revolving credit facility. Our subsidiaries who have their debt accelerated may not be able to repay such indebtedness. As a result of general economic, financial, competitive and other factors we can also not assure you that our assets and our subsidiaries' assets will be sufficient to fully repay the exchange notes and our other indebtedness. See "Description of Other Indebtedness."

We may not have access to the cash flow and other assets of our subsidiaries that may be needed to make payment on the exchange notes.

Although our operations are conducted through our subsidiaries, none of our subsidiaries are obligated to make funds available to us for payment on the exchange notes. Accordingly, our ability to make payments on the exchange notes is dependent on the earnings and the distribution of funds from our subsidiaries. The terms of our senior credit facilities and the indenture governing the senior subordinated notes of Compass Minerals Group significantly restrict our subsidiaries from paying dividends and otherwise transferring assets to us. Furthermore, our subsidiaries will be permitted under

13

the terms of our senior credit facilities and other indebtedness to incur additional indebtedness that may severely restrict or prohibit the making of distributions, the payment of dividends or the making of loans by such subsidiaries to us. The terms of our senior credit facilities also restrict our subsidiaries from paying dividends to us in order to fund cash interest on the exchange notes after June 1, 2008, if we do not maintain an adjusted senior indebtedness leverage ratio of 5.25 or less (as of September 30, 2003) or if a default or event of default has occurred and is continuing under our senior credit facilities. As of September 30, 2003, our adjusted senior indebtedness leverage ratio was 3.02. We cannot assure you that we will maintain this ratio. This ratio is not necessarily comparable to other similarly titled ratios of other companies due to inconsistencies in the method of calculation and we encourage you to read our amended and restated credit agreement contained in the exhibits to the registration statement of which this prospectus is a part.

We cannot assure you that the agreements governing the current and future indebtedness of our subsidiaries will permit our subsidiaries to provide us with sufficient dividends, distributions or loans to fund scheduled interest and principal payments on these exchange notes when due. See "Description of Other Indebtedness."

Your right to receive payments on the exchange notes is junior to our existing senior indebtedness and possibly all of our future borrowings.

The exchange notes rank behind all of our existing senior indebtedness, including the senior credit facilities and the senior discount notes, and all of our future indebtedness except any future indebtedness that expressly provides that it ranks equal with, or subordinated in right of payment to, the exchange notes. As a result, upon any distribution to our creditors in a bankruptcy, liquidation or reorganization or similar proceeding relating to us or our property, the holders of our senior indebtedness will be entitled to be paid in full before any payment may be made with respect to the exchanges notes.

In addition, all payments on the exchange notes will be blocked in the event of a payment default on senior indebtedness and may be blocked for up to 179 of 360 consecutive days in the event of certain non-payment defaults on senior indebtedness.

In the event of a bankruptcy, liquidation or reorganization or similar proceeding relating to us, holders of the exchange notes will participate with trade creditors and all other holders of our subordinated indebtedness in the assets remaining after we have paid all of our senior indebtedness. However, because the indenture governing the exchange notes requires that amounts otherwise payable to holders of the exchange notes in a bankruptcy or similar proceeding be paid to holders of senior indebtedness instead, holders of the exchange notes may receive less, ratably, than holders of trade payables in any such proceeding. In any of these cases, we may not have sufficient funds to pay all of our creditors and holders of exchange notes may receive less, ratably, than the holders of our senior indebtedness.

Assuming we had completed this offering on September 30, 2003, the exchange notes would have been subordinated to $169.3 million of senior indebtedness and approximately $108.5 million would have been available for borrowing as additional senior indebtedness under our revolving credit facility. The terms of indenture, the indenture governing the senior discount notes and our senior credit facilities permit us and our subsidiaries to incur significant additional indebtedness, including senior indebtedness, in the future.

14

Restrictive covenants in the agreements governing our indebtedness and certain indebtedness of Compass Minerals Group may restrict our ability to pursue our business strategies. A default under our senior credit facilities may also prohibit us from making any payments on the exchange notes.

Our senior credit facilities, the indenture governing the notes, the indenture governing the senior discount notes and the indenture governing the senior subordinated notes of Compass Minerals Group limit our ability and the ability of our restricted subsidiaries, among other things, to:

- •

- incur additional indebtedness or contingent obligations;

- •

- pay dividends or make distributions to our stockholders;

- •

- repurchase or redeem our stock;

- •

- make investments;

- •

- grant liens;

- •

- make capital expenditures;

- •

- enter into transactions with our stockholders and affiliates;

- •

- sell assets; and

- •

- acquire the assets of, or merge or consolidate with, other companies.

In addition, our senior credit facilities require us to maintain financial ratios. These financial ratios include an interest coverage ratio and a consolidated indebtedness leverage ratio. Although we have historically always been able to maintain these financial ratios, we may not be able to maintain these ratios in the future. Covenants in our senior credit facilities may also impair our ability to finance future operations or capital needs or to enter into acquisitions or joint ventures or engage in other favorable business activities.

If we default under our senior credit facilities, we could be prohibited from making any payments on the exchange notes. In addition, if we default under our senior credit facilities under certain circumstances the lenders could require immediate repayment of the entire principal. These circumstances include a change of control, default under agreements governing our other indebtedness, material judgments in excess of $5,000,000 or breach of representations and warranties. Any default under our senior credit facilities or agreements governing our other indebtedness could lead to an acceleration of debt under our other debt instruments that contain cross-acceleration or cross-default provisions. If the lenders under our senior credit facilities require immediate repayment, we will not be able to repay them and also repay the exchange notes in full. Our ability to comply See "Description of Other Indebtedness—The Senior Credit Facilities." We also encourage you to read our amended and restated credit agreement contained in the exhibits to the registration statement of which this prospectus is a part.

To service our indebtedness, including the exchange notes, we will require a significant amount of cash. The ability to generate cash depends on many factors beyond our control.

Our ability to make payments on and to refinance our indebtedness, including the exchange notes, and to fund planned capital expenditures and research and development efforts will depend on our ability to generate cash in the future. This is subject to general economic, financial, competitive, legislative, regulatory and other factors that are beyond our control. As a result, we cannot assure you that our business will generate sufficient cash flow from operations, that currently anticipated cost savings and operating improvements will be realized on schedule or that future borrowings will be available to us in an amount sufficient to enable us to pay our indebtedness, including the exchange notes, or to fund our other liquidity needs. If we consummate an acquisition, our debt service

15

requirements could increase. We may need to refinance all or a portion of our indebtedness, including the exchange notes on or before maturity. Depending on prevailing general economic and financial conditions, competition and other factors, we cannot assure you that we will be able to refinance any of our indebtedness, including our senior credit facilities and the exchange notes, on commercially reasonable terms or at all.

We may not have the ability to raise the funds necessary to finance any change of control offer required by the indenture governing the exchange notes.

If we undergo a change of control (as defined in the indenture governing the exchange notes) we may need to refinance large amounts of our debt, including the exchange notes, the senior discount notes and borrowings under our senior credit facilities. If a change of control occurs, we must offer to buy back the exchange notes for a price equal to 101% of the accreted value of the exchange notes, plus any accrued and unpaid interest. We may not have sufficient funds available to make any required repurchases of the exchange notes and our other indebtedness with similar provisions upon a change of control. In addition, our senior credit facilities prohibit us from repurchasing the exchange notes until we first repay our senior credit facilities in full. If we fail to repurchase the exchange notes in that circumstance, we will go into default under the indentures governing the exchange notes and the senior discount notes, as well as our senior credit facilities. Any future debt which we incur may also contain restrictions on repayment upon a change of control. If any change of control occurs, we cannot assure you that we will have sufficient funds to satisfy all of our debt obligations. The buyback requirements also delay or make it harder for others to effect a change of control. However, certain other corporate events, such as a leveraged recapitalization that would increase our level of indebtedness, would not constitute a change of control under the indenture governing the exchange notes. See "Description of the Exchange Notes—Change of Control."

You will be required to pay U.S. federal income tax on accrual of original issue discount on the exchange notes even if we do not pay cash interest.

The exchange notes will be issued at a substantial discount from their principal amount at maturity. Although cash interest will not accrue on the exchange notes prior to June 1, 2008, and there will be no periodic payments of cash interest on the exchange notes prior to December 1, 2008, original issue discount (the difference between the stated redemption price at maturity and the issue price of the exchange notes) will accrue from the issue date of the exchange notes. Consequently, purchasers of the exchange notes generally will be required to include amounts in gross income for United States federal income tax purposes in advance of their receipt of the cash payments to which the income is attributable. Such amounts in the aggregate will be equal to the difference between the stated redemption price at maturity (inclusive of stated interest on the exchange notes) and the issue price of the exchange notes. See "Material United States Federal Income Tax Consequences."

You may be unable to sell your exchange notes if a trading market for the exchange notes does not develop.

The exchange notes will be new securities for which there is currently no established trading market and none may develop. We do not intend to apply for listing of the exchange notes on any securities exchange or for quotation on any automated dealer quotation system. The liquidity of any market for the exchange notes will depend on the number of holders of the exchange notes, the interest of securities dealers in making a market in the exchange notes and other factors. The initial purchasers of the outstanding notes have indicated to us that they intend to make a market in the exchange notes, as permitted by applicable laws and regulations. However, the initial purchasers are under no obligation to do so. At their discretion, the initial purchasers could discontinue their market making efforts at any time without notice. Accordingly, we cannot assure you as to the development or liquidity of any market for the exchange notes. If an active trading market does not develop, the

16

market price and liquidity of the exchange notes may be adversely affected. If the exchange notes are traded, they may trade at a discount from their initial offering price depending upon prevailing interest rates, the market for similar securities, general economic conditions, our performance and business prospects and other factors.

The market price for the exchange notes may be volatile.

Historically, the market for non-investment grade debt has been subject to disruptions that have caused substantial volatility in the prices of securities similar to the exchange notes. Although we have not experienced any substantial disruptions or volatility with respect to our non-investment grade debt, including the outstanding notes, the market for the exchange notes, if any, may be subject to disruptions and price volatility. Any such disruptions may adversely affect the market price of your exchange notes.

Risks Relating to Our Business

The seasonal demand for our products and the variations in our cash flows from quarter to quarter as a result of weather conditions may have an adverse effect on our ability to make payments on our indebtedness, including the exchange notes.

Our highway deicing product line is seasonal, with operating results varying from quarter to quarter. Over the last four years, our North American highway deicing product line has generated over 65% of its annual sales during the months of December through March when the need for highway deicing is at its peak. We need to stockpile sufficient highway deicing salt in the first two fiscal quarters to meet estimated demand for the winter season. Weather conditions that impact our highway deicing product line include temperature, levels of precipitation, number of snow days and duration and timing of snow fall in our relevant geographic markets. Lower than expected sales by us during this period could have a material adverse effect on the timing of our cash flows and therefore our ability to service our obligations with respect to our indebtedness.

Our SOP operating results are dependent in part upon conditions in the agriculture markets. The agricultural products business can be affected by a number of factors, the most important of which for U.S. markets are weather patterns and field conditions (particularly during periods of traditionally high crop nutrients consumption) and quantities of crop nutrients imported to and exported from North America.

Economic and other risks associated with international sales and operations could adversely affect our business, including economic loss and a negative impact on earnings.

Since we manufacture and sell our products primarily in the United States, Canada and the United Kingdom, our business is subject to risks associated with doing business internationally. Our sales outside the United States, as a percentage of our total sales, were 34% and 36% for the year ended December 31, 2002 and the nine months ended September 30, 2003, respectively. Accordingly, our future results could be harmed by a variety of factors, including:

- •

- changes in foreign currency exchange rates;

- •

- exchange controls;

- •

- tariffs, other trade protection measures and import or export licensing requirements;

- •

- potentially negative consequences from changes in tax laws;

- •

- differing labor regulations;

- •

- requirements relating to withholding taxes on remittances and other payments by subsidiaries;

17

- •

- restrictions on our ability to own or operate subsidiaries, make investments or acquire new businesses in these jurisdictions;

- •

- restrictions on our ability to repatriate dividends from our subsidiaries; and

- •

- unexpected changes in regulatory requirements.

Fluctuations in the value of the U.S. dollar may adversely affect our results of operations. Because our consolidated financial results are reported in U.S. dollars, if we generate sales or earnings in other currencies the translation of those results into dollars can result in a significant increase or decrease in the amount of those sales or earnings. In addition, our debt service requirements are primarily in U.S. dollars even though a significant percentage of our cash flow is generated in Canadian dollars and pound sterling. Significant changes in the value of Canadian dollars and pound sterling relative to the U.S. dollar could have a material adverse effect on our financial condition and our ability to meet interest and principal payments on U.S. dollar denominated debt, including the exchange notes and borrowings under our senior credit facilities.

In addition to currency translation risks, we incur currency transaction risk whenever we or one of our subsidiaries enter into either a purchase or a sales transaction using a currency other than the local currency of the transacting entity. Given the volatility of exchange rates, we cannot assure you that we will be able to effectively manage our currency transaction and/or translation risks. It is possible that volatility in currency exchange rates will have a material adverse effect on our financial condition or results of operations. We have in the past experienced and expect to continue to experience economic loss and a negative impact on earnings as a result of foreign currency exchange rate fluctuations. We expect that the amount of our revenues denominated in non-U.S. dollar currencies will continue to increase in future periods. See "Management's Discussion and Analysis of Financial Condition and Results of Operations—Effects of Currency Fluctuations and Inflation" and "Management's Discussion and Analysis of Financial Condition and Results of Operations—Market Risk."

Our overall success as a global business depends, in part, upon our ability to succeed in differing economic and political conditions. We cannot assure you that we will continue to succeed in developing and implementing policies and strategies that are effective in each location where we do business.

Our operations are dependent on natural gas and a significant interruption in the supply or increase in the price of natural gas could have a material adverse affect on our financial condition or results of operations.

Energy costs, including primarily natural gas and electricity, represented approximately 12% of the costs of our North American salt production in 2002. Natural gas is a primary fuel source used in the salt production process. Our profitability is impacted by the price and availability of natural gas we purchase from third parties. We have not entered into any long-term contracts for the purchase of natural gas. Our contractual arrangements for the supply of natural gas do not specify quantities and are automatically renewed annually unless either party elects not to do so. We do not have arrangements in place with back-up suppliers. A significant increase in the price of natural gas that is not recovered through an increase in the price of our products or covered through our hedging arrangements, or an extended interruption in the supply of natural gas to our production facilities, could have a material adverse effect on our business, financial condition or results of operations.

Competition in our markets could limit our ability to attract and retain customers, force us to continuously make capital investments and put pressure on the prices we can charge for our products.

We encounter competition in all areas of our business. Competition in our product lines is based on a number of considerations, including product performance, transportation costs in salt distribution, brand reputation, quality of client service and support and price. Additionally, customers for our products are attempting to reduce the number of vendors from which they purchase in order to

18

increase their efficiency. Our customers increasingly demand a broad product range and we must continue to develop our expertise in order to manufacture and market these products successfully. To remain competitive, we will need to invest continuously in manufacturing, marketing, customer service and support and our distribution networks. We may have to adjust the prices of some of our products to stay competitive. We may not have sufficient resources to continue to make such investments or maintain our competitive position. Some of our competitors have greater financial and other resources than we do.

Environmental laws and regulation may subject us to significant liability and require us to incur additional costs in the future.

We are subject to numerous environmental, health and safety laws and regulations in the United States, Canada and Europe, including laws and regulations relating to land reclamation and remediation of hazardous substance releases, and discharges to air and water. For example, the U.S. Comprehensive Environmental Response, Compensation, and Liability Act, or "CERCLA," imposes liability, without regard to fault or to the legality of a party's conduct, on certain categories of persons (known as "potentially responsible parties") who are considered to have contributed to the release of "hazardous substances" into the environment. Although we are not currently incurring material liabilities pursuant to CERCLA, we may in the future incur material liabilities under CERCLA and other environmental cleanup laws, with regard to our current or former facilities, adjacent or nearby third party facilities or off-site disposal locations. Under CERCLA, or its various state analogues, one party may, under some circumstances, be required to bear more than its proportional share of cleanup costs at a site where it has liability if payments cannot be obtained from other responsible parties. Liability under these laws involves inherent uncertainties. Violations of environmental, health and safety laws are subject to civil, and in some cases criminal, sanctions.