QuickLinks -- Click here to rapidly navigate through this document

Filed Pursuant to Rule 424(b)(3)

Registration No. 333-104874

PROSPECTUS

AmeriPath, Inc.

Offer to Exchange

$275,000,000 principal amount of its 101/2% Senior Subordinated Notes Due 2013, which have been registered under the Securities Act of 1933, for any and all of its outstanding 101/2% Senior Subordinated Notes Due 2013.

We are offering to exchange all of our outstanding 101/2% Senior Subordinated Notes due 2013, which we refer to as the old notes, for our registered 101/2% Senior Subordinated Notes due 2013, which we refer to as the exchange notes, and together with the old notes, the notes. The terms of the exchange notes are identical to the terms of the old notes except that the exchange notes have been registered under the Securities Act of 1933, and therefore, are freely transferable. We will pay interest on the notes on April 1 and October 1 of each year. The first interest payment will be made on October 1, 2003. The notes will mature on April 1, 2013.

We may redeem up to 35% of the aggregate principal amount of the notes prior to April 1, 2006 using proceeds from certain equity offerings. We may redeem the notes on or after April 1, 2008. Holders may require us to repurchase the notes upon a change of control. The notes are senior subordinated obligations and rank junior to all of our existing and future senior debt. The notes are guaranteed on a senior subordinated basis by certain of our subsidiaries.

The principal features of the exchange offer are as follows:

- •

- The exchange offer expires at 5:00 p.m., New York City time, on June 30, 2003, unless extended.

- •

- We will exchange all old notes that are validly tendered and not validly withdrawn prior to the expiration of the exchange offer.

- •

- You may withdraw tendered old notes at any time prior to the expiration of the exchange offer.

- •

- The exchange of old notes for exchange notes pursuant to the exchange offer will not be a taxable event for U.S. federal income tax purposes.

- •

- We will not receive any proceeds from the exchange offer.

- •

- We do not intend to apply for listing of the exchange notes on any securities exchange or automated quotation system.

Broker-dealers receiving exchange notes in exchange for old notes acquired for their own account through market-making or other trading activities must deliver a prospectus in any resale of the exchange notes.

Investing in the notes involves risks. See "Risk Factors" beginning on page 14.

Neither the U.S. Securities and Exchange Commission nor any other federal or state agency has approved or disapproved of the securities to be distributed in the exchange offer, nor have any of these organizations determined that this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The date of this prospectus is May 30, 2003

| | Page | |

|---|---|---|

| Prospectus Summary | 1 | |

| Risk Factors | 14 | |

| Forward Looking Statements | 28 | |

| Exchange Offer | 29 | |

| Use of Proceeds | 37 | |

| Capitalization | 38 | |

| Selected Historical Consolidated Financial Information | 39 | |

| Unaudited Pro Forma Consolidated Financial Information | 41 | |

| Management's Discussion and Analysis of Financial Condition and Results of Operations | 46 | |

| Business | 63 | |

| Government Regulation | 75 | |

| Management | 84 | |

| Security Ownership of Certain Beneficial Owners and Management | 94 | |

| The Transactions | 96 | |

| Certain Relationships and Related Transactions | 97 | |

| Description of Certain Other Indebtedness | 99 | |

| Description of the Exchange Notes | 103 | |

| Contingent Notes and the Cash Collateral Account | 147 | |

| Book Entry; Delivery and Form | 149 | |

| Certain United States Federal Tax Consequences | 151 | |

| Plan of Distribution | 156 | |

| Legal Matters | 156 | |

| Experts | 156 | |

| Where You Can Find More Information | 157 | |

| Index to Financial Statements | F-1 | |

Each broker-dealer that receives exchange notes for its own account pursuant to the exchange offer must acknowledge that it will deliver a prospectus in connection with any resale of such exchange notes. The letter of transmittal delivered with this prospectus states that by so acknowledging and by delivering a prospectus, a broker-dealer will not be deemed to admit that it is an "underwriter" within the meaning of the Securities Act of 1933. This prospectus, as it may be amended or supplemented from time to time, may be used by a broker-dealer in connection with resales of exchange notes received in exchange for old notes where such old notes were acquired by such broker-dealer as a result of market-making activities or other trading activities. We have agreed that, for a period of not less than 180 days following the effective date of the registration statement, of which this prospectus is a part, we will make this prospectus available to any broker-dealer for use in connection with any such resale. See "Plan of Distribution."

We have not authorized any dealer, salesman or other person to give any information or to make any representation other than those contained or incorporated by reference in this prospectus. You must not rely upon any information or representation not contained or incorporated by reference in this prospectus as if we had authorized it. This prospectus does not constitute an offer to sell or a solicitation of an offer to buy any securities other than the registered securities to which it relates, nor does this prospectus constitute an offer to sell or a solicitation of any offer to buy securities in any jurisdiction to any person whom it is unlawful to make such offer or solicitation in such jurisdiction.

i

This summary may not contain all of the information that may be important to you. This prospectus includes specific terms of the exchange offer, as well as information regarding our business and detailed financial data. Please review this prospectus in its entirety, including the risk factors and our financial statements and the related notes included elsewhere herein, before you decide to tender old notes for exchange notes. Unless otherwise noted, the terms "AmeriPath," "our company," "us," "we" and "our" refer to AmeriPath, Inc., together with its subsidiaries, and the terms "Holdings" and "our parent" refer to our parent company, AmeriPath Holdings, Inc. AmeriPath became a wholly owned subsidiary of Holdings on March 27, 2003 as a result of a merger of AmeriPath and Amy Acquisition Corp., a subsidiary of Holdings. In addition, unless otherwise noted, references herein to our business, our pathologists, our laboratories, our customers and payors and the hospitals we service, and all similar and related operating data, include those of a few anatomic pathology operations that we manage but whose financial results are not consolidated with ours. References to "pro forma," "EBITDA" and other financial terms have the meanings set forth in pages 12 and 13 under "—Summary Pro Forma and Historical Consolidated Financial Information."

Our Company

We are one of the leading anatomic pathology laboratory companies in the United States. We offer a broad range of anatomic pathology laboratory testing and information services used by physicians in the detection, diagnosis, evaluation and treatment of cancer and other diseases and medical conditions. During 2002, we processed and diagnosed approximately four million tissue biopsies. We believe that we are the only anatomic pathology laboratory company with substantial operations in both the outpatient and inpatient, or hospital, segments of the anatomic pathology services market.

We service an extensive referring physician base through our 15 regional laboratories and 32 satellite laboratories, and we provide inpatient diagnostic and medical director services at more than 200 hospitals. We have operations in 21 states providing us with a regional or local presence in 17 of the 30 most populous metropolitan areas of the United States. Our services are performed by over 400 pathologists, many of whom are leaders in their field. We have built our business by completing over 50 acquisitions of pathology laboratories and operations since 1996, enabling us to build regional density in attractive geographic markets and establishing a platform for organic growth. We also operate the Center for Advanced Diagnostics, or CAD, which is a leading specialty, or esoteric, testing laboratory.

Our fields of expertise include dermatopathology, in which we maintain a leading market position, women's health diagnostic services, urologic pathology and gastrointestinal pathology. We also believe that we are the leading anatomic pathology services provider to hospitals in the United States. Generally, we are the exclusive provider of anatomic pathology services for the hospitals we serve, which arrangements have historically provided us with a stable stream of revenue. In addition, through our managed care relationships, we contract with health maintenance organizations, or HMOs, and preferred provider organizations, or PPOs, that insure approximately 26 million and 83 million individuals, respectively, which represents more than half of all individuals covered by managed care in the United States.

Industry Overview

The practice of pathology consists of anatomic and clinical pathology. Anatomic pathology involves the diagnosis of cancer and other diseases and medical conditions through the examination of tissue and cell samples taken from patients. Generally, the anatomic pathology process involves the mounting of samples on slides by highly skilled technicians, which are then reviewed by anatomic pathologists. Anatomic pathologists are medical doctors who do not examine patients, but rather assist other physicians in determining the correct diagnosis of a patient's ailments. As a result, an anatomic pathologist is often referred to as a "physician's physician." Clinical pathology, on the other hand,

1

generally involves the chemical testing and analysis of body fluids utilizing standardized laboratory tests. The results of these standardized tests are provided to the referring physician for use in a patient's diagnosis. Clinical laboratory tests typically do not require the interpretive skills of a pathologist. The process is frequently routine, automated and performed by large national or regional clinical laboratory companies and hospital laboratories.

We believe the market for anatomic pathology services is approximately $7 billion per year, and we expect it to continue to grow for the following reasons:

- •

- the aging of Americans should lead to more incidences of cancer and should result in greater demand for healthcare services, including those provided by anatomic pathologists,

- •

- the increasing reliance on pathology testing by physicians to aid in the identification of risk factors and symptoms of disease, the choice of therapeutic regimen and the evaluation of treatment results, and

- •

- the increasing awareness by physicians, patients and payors of the value of preventative testing to improve the effectiveness of medical services and reduce the overall cost of healthcare.

In addition to traditional anatomic pathology services, pathologists increasingly are performing highly complex esoteric tests. Traditionally performed in academic settings, technological advancements have provided large commercial laboratories with highly specialized equipment and the means to perform these advanced tests for patients in both outpatient and inpatient settings. As these tests typically require more advanced equipment and highly skilled personnel to perform, they generally are reimbursed at rates higher than more routine tests. We believe the market for esoteric testing services is approximately $2 billion per year. The growth in the esoteric testing services market benefits from demand factors similar to those in the traditional anatomic pathology services market. In addition, we believe that emerging technologies and tests, such as gene-based tests, or genomics, should drive growth in the esoteric testing services market at a rate that exceeds the growth rate for the traditional anatomic pathology services market.

According to the American Society for Clinical Pathology, there are approximately 15,000 pathologists in the United States. Historically, the anatomic pathology industry has been highly fragmented with a majority of the services being performed by individual or small groups of pathologists working in independent laboratories, hospital laboratories or academic institutions. Recently there has been a trend among pathologists to join larger laboratories in order to offer a broader range of outpatient and inpatient services, take advantage of economies of scale and reduce the burdens of managing the administrative aspects of their operations.

Competitive Strengths

We believe that we are distinguished by the following competitive strengths:

- •

- Leadership in anatomic pathology services. We are an established and experienced leader in the highly fragmented anatomic pathology services market. We believe that we are the only anatomic pathology laboratory company with substantial operations in both the outpatient and inpatient segments of the anatomic pathology services market. Our pathologist base comprises what we believe is the largest single group of pathologists in the nation and provides us with the ability to offer services in all subspecialties of anatomic pathology. Within the subspecialty of dermatopathology, we estimate our market share to be approximately 10%, which is the largest in the industry. In addition, we have expertise in esoteric testing as well as in the anatomic pathology subspecialties of women's health diagnostic services, urologic pathology and gastrointestinal pathology. We believe our broad service offerings provide us with an advantage over most of our competitors in maintaining and developing customer relationships.

- •

- National scale with regional and local density. We believe we have the broadest national footprint within the anatomic pathology services market. We have operations in 21 states,

2

- •

- Attractive industry dynamics. The demand for traditional anatomic pathology services and esoteric testing services has created significant and growing markets. We believe the market for traditional anatomic pathology services, excluding esoteric testing services, is approximately $7 billion per year, and the market for esoteric testing services is approximately $2 billion per year. We expect these markets to continue to grow primarily due to an aging population, increasing incidences of cancer and medical advancements that allow for more accurate and earlier diagnosis and treatment of diseases. According to the U.S. Census Bureau, the number of people aged 65 and older in the United States is expected to grow 16% over the next ten years. Generally, people aged 65 or older have a greater incidence of chronic health conditions such as cancer, diabetes, heart disease, arthritis or hypertension and are heavier users of healthcare services than people under age 65. For example, according to the Surveillance, Epidemiology, and End Results (SEER) Program of the National Cancer Institute, the average annual cancer incidence rate for people aged 65 to 74 is 2,007 per 100,000 people or approximately 14 times the incidence rate of people aged 20-49 and approximately 125 times the incidence rate of people aged 20 and under. Additionally, the National Cancer Institute estimates that incidences of melanoma, a type of skin cancer, in the United States will grow 14% from 2002 to 2007. We also believe that emerging technologies and tests, such as genomics, will further drive growth in the market for esoteric testing services.

- •

- Strong cash flow generation. We believe our strong cash flow substantially enhances our competitive position in the highly fragmented anatomic pathology services market. Historically, our strong operating cash flow has been a result of low capital expenditure requirements and our ability to increase the performance of acquired operations. Our margins are a result of our enhanced laboratory utilization, our broad range of testing services, economies of scale and our success in contracting with managed care organizations. In addition, we believe our strong cash flow strengthens our ability to fund organic and external growth initiatives, which enhances our competitiveness relative to most of our smaller, regional competitors.

- •

- Favorable payor relationships. Currently, we have contractual relationships with HMOs and PPOs whose members comprise more than half of the individuals covered by managed care in the United States. These relationships provide us with access to a large number of current and potential patients. Our national scale and regional concentration have facilitated our entry into a growing number of relationships with managed care organizations, such as Blue Cross/Blue Shield plans, Aetna and United Healthcare. Since 1999, we have more than tripled the number of people covered under our managed care agreements, which we believe validates our managed care strategy. Furthermore, the overwhelming majority of our revenues from these relationships are generated from fee-for-service payments, rather than from fee-per-person, or capitated, payments. In addition, our payments from government sponsored programs, such as Medicare

providing us with a regional or local presence in 17 of the 30 most populous metropolitan areas of the United States. We also have a presence in more than 200 hospitals, which we believe makes us the leading provider of anatomic pathology services in hospitals. Furthermore, we have contractual relationships with HMOs and PPOs whose members comprise more than half of the individuals covered by managed care in the United States. We have developed a substantial presence in our target markets by forming regional operations that deliver our services locally and enable our pathologists to establish strong relationships with our referring physician base. For example, we believe we are the leading anatomic pathology laboratory company, with the largest market share and greatest number of pathologists, in Florida and Texas, our strongest regions. In Florida and Texas, for the three-year period ending December 31, 2002, our net revenues grew, on a compounded annual basis, at 13.2% and 25.0%, respectively. As a result of our regional coverage we have been able to grow our revenues, enhance our laboratory utilization, offer a broader range of testing services and benefit from economies of scale and increased managed care contracting leverage.

3

- •

- Experienced and incentivized management team. Our senior management team has an average of over ten years of healthcare industry experience and an extensive tenure with us. Our chief executive officer, James C. New, is one of our founders and has led our growth since the formation of our company in 1996. Prior to joining our company, Mr. New founded and led RehabClinics, Inc., one of the largest outpatient rehabilitation clinics in the country, a company that went public in 1992 and was merged with NovaCare in 1994. In addition, our parent has established a stock option plan, which further aligns management's interests with our performance. Under this plan, our management and employees are eligible to receive up to 12% of our parent's common stock.

and Medicaid, are relatively limited. During 2002, we derived approximately 20% of our total revenues from government-sponsored payors. We believe our diverse payor mix limits our exposure to the loss of any single source of payment for our services.

Business Strategy

We believe our business strategy will help us maintain our status as a leading provider of anatomic pathology services and increase our share of the markets in which we compete. The key elements of our strategy are to:

- •

- Capitalize on our leading market position. Through our 15 regional laboratories, 32 satellite laboratories and over 400 pathologists, we will continue to provide a comprehensive array of anatomic pathology services to primary care and specialty physicians and serve over 200 hospitals. We will further enhance our extensive expertise in the subspecialties of dermatopathology, women's health diagnostic services, urologic pathology and gastrointestinal pathology. In addition, through CAD, we will grow our esoteric testing capabilities in each of these subspecialties. We also plan to leverage our market position, regional model and broad range of services to further penetrate the markets we serve and expand our relationships with physicians, hospitals, managed care organizations and other customers.

- •

- Continue to focus on organic growth. We are focused on generating internal revenue growth. For 2002, we generated annual same store sales growth of 9.2%. We believe that our substantial organic growth has been and will continue to be a result of the following initiatives:

- •

- increasing test volume by continuing to invest in a formal sales and marketing effort,

- •

- enhancing our payor mix by pursuing additional managed care contracts,

- •

- continuing to expand our service offerings, including the offering of new, higher revenue, esoteric tests, and

- •

- improving patient care and customer service by providing more specific, informative and timely reports through the development of a standardized pathology reporting system.

- •

- Maintain quality leadership through a strong pathologist base. We believe that employing anatomic pathologists who provide accurate and efficient diagnosis is a key to our success. A pathologist's experience and reputation is critical to ensuring a successful relationship with local referring physicians. We actively recruit top anatomic pathologists by targeting practicing pathologists and medical students. In 2002, we successfully recruited 46 pathologists, each of whom is a graduate of an accredited United States pathology fellowship program. In addition, we operate one of the leading centers in the United States devoted to the diagnosis and instruction of diseases of the skin. Founded in 1999, this academy provides fellowship programs that enable students to train in various aspects of dermatopathology. We also are affiliated with three leading dermatopathology fellowship programs in the United States. Collectively, these relationships enhance our ability to attract new pathologists and allow us to more easily transfer

Collectively, these initiatives will provide us with the opportunity to grow our business organically.

4

- •

- Emphasize information technology capabilities and improve operational efficiencies.We invest in information technology enhancements to improve our services and increase efficiency. For example, in the subspecialty of women's health diagnostics, we offer customers enhanced pathology reports, including color micrographs that allow pathologists and referring physicians to more accurately view highly abnormal cell populations. In addition, to enhance efficiency, we are consolidating various internal billing systems and outsourced billing arrangements into two billing systems, which we believe will increase collections and reduce our days sales outstanding. We also are committed to increasing efficiencies and economies of scale by promoting "best practices" throughout our organization.

- •

- Selectively pursue strategic growth initiatives. We plan to invest in new outpatient laboratories and other strategic initiatives such as CAD. We believe these new facilities and programs drive revenue growth by providing national support for our existing regional and local operations and increasing our menu of testing services. We also plan to further penetrate our existing regional markets by opening new laboratory facilities, such as the new facilities we recently opened in Florida, Indiana and Pennsylvania. In addition, we expect to make additional acquisitions, as opportunities arise, in order to strategically enter new markets or further penetrate existing regional markets.

technical innovations to the anatomic pathology services market. We also believe our size and strength of reputation provide an attractive alternative for pathologists who are seeking to offer a broader range of services, take advantage of available economies of scale and reduce the burden of managing the administrative aspects of their operations.

The Transactions

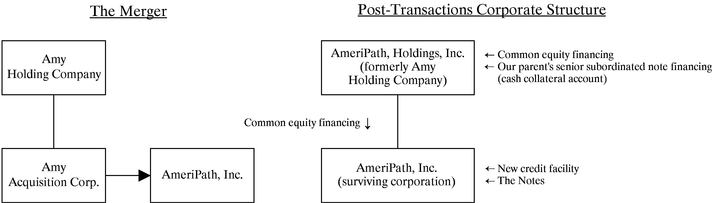

On December 8, 2002, Holdings, which was then known as Amy Holding Company, and its wholly owned subsidiary Amy Acquisition Corp. entered into a merger agreement providing for the merger of Amy Acquisition Corp. with and into our company, with our company continuing as the surviving corporation. Holdings and Amy Acquisition Corp. were each formed by Welsh, Carson, Anderson & Stowe IX, L.P. in connection with the merger. As a result of the merger, AmeriPath became a wholly owned subsidiary of Holdings. The merger was consummated on March 27, 2003 immediately following the issuance of the old notes and immediately preceding the closing of our new credit facility. We refer to the merger and the related transactions and financings, as the "Transactions." For a description of the merger, see "The Transactions."

Our Investors

As a result of the Transactions, Welsh, Carson, Anderson & Stowe IX, L.P. and its related investors, through their holdings of common stock of our parent, own 100% of our outstanding common stock (or 88% of our outstanding common stock assuming the issuance and exercise of all options reserved for issuance under our parent's new stock option plan). Welsh, Carson, Anderson & Stowe IX, L.P. also controls our board of directors.

Welsh, Carson, Anderson & Stowe is one of the largest private equity firms in the United States and is focused exclusively on investments in the healthcare, information services and communications industries. Since its founding in 1979, Welsh, Carson, Anderson & Stowe has organized investment partnerships with capital of more than $12 billion in the aggregate. Its healthcare investments include Select Medical Corporation, United Surgical Partners Holdings, Inc., Concentra Managed Care, Inc., US Oncology, Inc. and Fresenius Medical Care AG.

5

On March 27, 2003, Amy Acquisition Corp. completed an offering of $275.0 million in aggregate principal amount of 101/2% senior subordinated notes due 2013, which was exempt from registration under the Securities Act. The old notes became obligations of AmeriPath upon consummation of the merger.

Old Notes | Amy Acquisition Corp. sold the old notes to Credit Suisse First Boston LLC, Deutsche Bank Securities Inc. and Wachovia Securities, Inc., who we collectively refer to as the initial purchasers, on March 27, 2003. The initial purchasers subsequently resold the old notes to qualified institutional buyers pursuant to Rule 144A under the Securities Act and to non-U.S. persons outside the United States in reliance on Regulation S under the Securities Act. | |||

Registration Rights Agreement | In connection with the sale of the old notes, Amy Acquisition Corp. and the subsidiaries of AmeriPath who guaranteed the obligations under the old notes, who we collectively refer to as the subsidiary guarantors, entered into a registration rights agreement with the initial purchasers. Under the terms of that agreement, we agreed to: | |||

• | file a registration statement with respect to an offer to exchange the old notes for the exchange notes within 90 days of the date on which the old notes were purchased by the initial purchasers, | |||

• | cause the registration statement to be declared effective prior to 180 days after the initial purchase date, | |||

• | consummate the exchange offer within 220 days after the initial purchase date and | |||

• | file a shelf registration statement to cover resales of the old notes if we cannot effect an exchange offer and under certain other circumstances. | |||

If we and the subsidiary guarantors fail to meet any of these requirements, it will constitute a default under the registration rights agreement and we and the subsidiary guarantors must pay additional interest on the notes of up to 0.25% per annum for the first 90-day period after any such default. This interest rate will increase by an additional 0.25% per annum with respect to each subsequent 90-day period until all defaults have been cured, up to a maximum additional interest rate of 1.0% per annum. The exchange offer is being made pursuant to the registration rights agreement and is intended to satisfy the registration rights granted under the registration rights agreement, which registration rights terminate upon completion of the exchange offer.

6

The Exchange Offer

| Exchange Offer | $1,000 principal amount of exchange notes will be issued in exchange for each $1,000 principal amount of old notes validly tendered. | |||

Resale | Based upon interpretations by the staff of the SEC set forth in no-action letters issued to unrelated third parties, we believe that the exchange notes may be offered for resale, resold or otherwise transferred to you without compliance with the registration and prospectus delivery requirements of the Securities Act, unless you: | |||

• | are an "affiliate" of ours within the meaning of Rule 405 under the Securities Act, | |||

• | are a broker-dealer who purchased the old note directly from us for resale under Rule 144A or any other available exemption under the Securities Act, | |||

• | acquired the exchange notes other than in the ordinary course of your business, or | |||

• | have an arrangement with any person to engage in the distribution of exchange notes. | |||

However, we have not submitted a no-action letter and there can be no assurance that the SEC will make a similar determination with respect to the exchange offer. Furthermore, in order to participate in the exchange offer, you must make the representations set forth in the letter of transmittal that we are sending you with this prospectus. | ||||

Expiration Date | The exchange offer will expire at 5:00 p.m., New York City time, on June 30, 2003, which we refer to as the expiration date, unless we, in our sole discretion, extend it. | |||

Conditions to the Exchange Offer | The exchange offer is subject to certain customary conditions, some of which may be waived by us. See "The Exchange Offer—Conditions to the Exchange Offer." | |||

Procedure for Tendering Old Notes | If you wish to accept the exchange offer, you must complete, sign and date the letter of transmittal, or a copy of the letter of transmittal, in accordance with the instructions contained in this prospectus and in the letter of transmittal, and mail or otherwise deliver the letter of transmittal, or the copy, together with the old notes and any other required documentation, to the exchange agent at the address set forth in this prospectus and in the letter of transmittal. | |||

7

We will accept for exchange any and all old notes that are properly tendered in the exchange offer prior to the expiration date. The exchange notes issued in the exchange offer will be delivered promptly following the expiration date. See "The Exchange Offer—Terms of the Exchange Offer." | ||||

Special Procedure for Beneficial Owners | If you are the beneficial owner of old notes registered in the name of a broker, dealer, commercial bank, trust company or other nominee and wish to tender in the exchange offer, you should contact the person in whose name your notes are registered and promptly instruct the person to tender on your behalf. | |||

Guaranteed Delivery Procedures | If you wish to tender your old notes and time will not permit your required documents to reach the exchange agent by the expiration date, or the procedure for book-entry transfer cannot be completed on time, you may tender your notes according to the guaranteed delivery procedures. For additional information, you should read the discussion under "The Exchange Offer—Guaranteed Delivery Procedures." | |||

Withdrawal Rights | The tender of the old notes pursuant to the exchange offer may be withdrawn at any time prior to 5:00 p.m. New York City time on the expiration date. | |||

Acceptance of Old Notes and Delivery of Exchange Notes | Subject to the customary conditions, we will accept old notes that are properly tendered in the exchange offer and not withdrawn prior to the expiration date. The exchange notes will be delivered as promptly as practicable following the expiration date. | |||

Consequences of Not Tendering | Any old notes that are not tendered or that are tendered but not accepted will remain subject to the restrictions on transfer. Since the old notes have not been registered under the federal securities laws, they bear a legend restricting their transfer absent registration or the availability of a specific exemption from registration. Upon the completion of the exchange offer, we will have no further obligations, except under limited circumstances, to provide for registration of the old notes under the federal securities laws. See "The Exchange Offer—Consequences of Not Tendering." | |||

8

Interest on the Exchange Notes and the Old Notes | The exchange notes will bear interest from the most recent interest payment date to which interest has been paid on the old notes or, if no interest has been paid, from March 27, 2003. Interest on the old notes accepted for exchange will cease to accrue upon the issuance of the exchange notes. | |||

Certain U.S. Federal Tax Consequences | The exchange of old notes for exchange notes by tendering holders will not be a taxable exchange for federal income tax purposes, and such holders will not recognize any taxable gain or loss or any interest income for federal income tax purposes as a result of such exchange. See "Certain U.S. Federal Tax Consequences." | |||

Exchange Agent | U.S. Bank National Association, the trustee under the indenture governing the notes, is serving as exchange agent in connection with the exchange offer. | |||

Use of Proceeds | We will not receive any proceeds from the issuance of exchange notes pursuant to the exchange offer. | |||

9

Summary of the Terms of the Exchange Notes

Issuer | AmeriPath, Inc. | |||

Securities Offered | $275,000,000 in aggregate principal amount of 101/2% senior subordinated notes due 2013. | |||

Maturity Date | April 1, 2013. | |||

Interest | 101/2% per annum, payable semi-annually in arrears on April 1 and October 1, commencing on October 1, 2003. | |||

Guarantees | The exchange notes will be unconditionally guaranteed, jointly and severally and on an unsecured senior subordinated basis, by the subsidiary guarantors. | |||

Ranking | The exchange notes will be our unsecured senior subordinated obligations. The exchange notes and guarantees will rank: | |||

• | junior to all of our and the subsidiary guarantors' existing and future senior indebtedness, | |||

• | equally with any of our and the subsidiary guarantors' existing and future senior subordinated indebtedness and | |||

• | senior to any of our and the subsidiary guarantors' existing and future subordinated indebtedness. | |||

Assuming we had completed the Transactions and applied the proceeds as intended on March 31, 2003, the exchange notes would have ranked junior to approximately $230 million of senior indebtedness, virtually all of which is secured. | ||||

Optional Redemption | We may redeem any of the exchange notes at any time and from time to time on or after April 1, 2008, in whole or in part, in cash at the redemption prices described in this prospectus, plus accrued and unpaid interest to the date of redemption. In addition, at any time and from time to time, on or before April 1, 2006, we may redeem up to 35% of the exchange notes with the proceeds of certain equity offerings. | |||

Change of Control | If a change of control of our company occurs, subject to certain conditions, we must give holders of the exchange notes an opportunity to sell to us the exchange notes at a purchase price of 101% of the principal amount of the exchange notes, plus accrued and unpaid interest to the date of the purchase. See "Description of the Exchange Notes—Change of Control." | |||

10

Certain Covenants | The indenture governing the notes contains covenants that, among other things, limit our ability and the ability of our restricted subsidiaries to: | |||

• | incur or guarantee additional indebtedness, | |||

• | pay dividends or make other equity distributions, | |||

• | purchase or redeem capital stock, | |||

• | make certain investments, | |||

• | enter into arrangements that restrict dividends from subsidiaries, | |||

• | transfer and sell assets, | |||

• | engage in certain transactions with affiliates and | |||

• | effect a consolidation or merger. | |||

These limitations are subject to a number of important qualifications and exceptions. See "Description of Exchange Notes—Certain Covenants." | ||||

No Public Market for the Exchange Notes | The exchange notes are new issues of securities and will not be listed on any securities exchange or included in any automated quotation system. The initial purchasers of the old notes have advised us that they intend to make a market in the exchange notes. The initial purchasers are not obligated, however, to make a market in the exchange notes, and any such market-making may be discontinued by the initial purchasers in their discretion at any time without notice. See "Plan of Distribution." | |||

For additional information about the exchange notes, see the section of this prospectus entitled "Description of the Exchange Notes."

Risk Factors

Investment in the exchange notes involves certain risks. You should carefully consider the information under "Risk Factors" and all other information included in this prospectus before investing in the exchange notes.

Additional Information

AmeriPath was incorporated in Delaware on February 13, 1996. The principal executive offices of AmeriPath are located at 7289 Garden Road, Suite 200, Riviera Beach, Florida 33404. AmeriPath's telephone number is (561) 845-1850. Our website can be found on the Internet at www.ameripath.com. Information on our website is not deemed to be a part of this prospectus.

11

Summary Pro Forma and Historical Consolidated Financial Information

The following summary historical financial information is based on our consolidated financial statements included elsewhere in this prospectus. Our consolidated audited financial statements for the year ended December 31, 2002 have been audited by Ernst & Young LLP, our independent auditors. Our consolidated financial statements for the years ended December 31, 2000 and 2001 have been audited by Deloitte & Touche LLP. The consolidated financial information for the three months ended March 31, 2003 has not been audited. The following summary pro forma information is derived from the pro forma financial information set forth in our unaudited pro forma consolidated financial information and the notes thereto included elsewhere in this prospectus.

| | Fiscal Year ended December 31, | Pro Forma, As Adjusted Fiscal Year Ended December 31, 2002(1) | Three Months Ended March 31, 2003 | Pro Forma, As Adjusted Three Months Ended March 31, 2003(1) | |||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | 2000 | 2001 | 2002 | ||||||||||||||||||

| | (dollars in thousands) | ||||||||||||||||||||

| Statement of Operations Data: | |||||||||||||||||||||

| Net revenue | $ | 330,094 | $ | 418,732 | $ | 478,818 | $ | 497,412 | $ | 118,957 | $ | 118,957 | |||||||||

| Operating costs and expenses: | |||||||||||||||||||||

| Cost of services | 163,390 | 200,102 | 238,573 | 244,772 | 62,145 | 62,145 | |||||||||||||||

| Selling, general & administrative expense | 58,411 | 71,856 | 84,868 | 88,765 | 21,726 | 21,726 | |||||||||||||||

| Provision for doubtful accounts | 34,040 | 48,287 | 58,170 | 58,899 | 14,997 | 14,997 | |||||||||||||||

| Amortization expense | 16,172 | 18,659 | 11,389 | 12,523 | 3,107 | 3,107 | |||||||||||||||

| Merger-related charges | 6,209 | 7,103 | 2,836 | 10,010 | — | ||||||||||||||||

| Asset impairment and related charges | 9,562 | 3,809 | 2,753 | 2,753 | — | — | |||||||||||||||

| Restructuring costs | — | — | — | — | 1,196 | 1,196 | |||||||||||||||

| Write-off of deferred financing costs | — | — | — | — | 957 | — | |||||||||||||||

| Total operating costs and expenses: | 287,784 | 349,816 | 398,589 | 407,712 | 114,138 | 103,171 | |||||||||||||||

| Income from operations | 42,310 | 68,916 | 80,229 | 89,700 | 4,819 | 15,786 | |||||||||||||||

| Interest expense | (15,376 | ) | (16,350 | ) | (4,016 | ) | (45,333 | ) | (1,762 | ) | (11,135 | ) | |||||||||

| Termination of interest rate swap agreement | — | (10,386 | ) | — | — | — | — | ||||||||||||||

| Write-down of investment | — | — | (1,000 | ) | (1,000 | ) | — | — | |||||||||||||

| Other, net | 226 | 145 | 548 | 489 | 33 | 33 | |||||||||||||||

| Income before income taxes and extraordinary loss | 27,160 | 42,325 | 75,761 | 43,856 | 3,090 | 4,684 | |||||||||||||||

| Provision for income taxes | 14,068 | 18,008 | 31,120 | 16,248 | 3,565 | 1,838 | |||||||||||||||

| Income (loss) before extraordinary loss | 13,092 | 24,317 | 44,641 | 27,608 | (475 | ) | 2,846 | ||||||||||||||

| Extraordinary loss, net of tax benefit | — | (965 | ) | — | — | — | |||||||||||||||

| Net (loss) income | $ | 13,092 | $ | 23,352 | $ | 44,641 | $ | 27,608 | $ | (475 | ) | $ | 2,846 | ||||||||

Other Financial Data: | |||||||||||||||||||||

| EBITDA(2) | $ | 63,145 | $ | 94,177 | $ | 99,220 | $ | 110,179 | $ | 10,056 | $ | 21,023 | |||||||||

| Capital expenditures(3) | 9,235 | 7,773 | 8,744 | 2,553 | |||||||||||||||||

| Depreciation and amortization(4) | 21,291 | 25,675 | 19,244 | 22,951 | 5,299 | 5,867 | |||||||||||||||

| Cash paid for interest(5) | 14,645 | 17,295 | 3,888 | 42,760 | 1,141 | 10,514 | |||||||||||||||

Ratio of total debt to EBITDA | 4.57 | x | |||||||||||||||||||

| Ratio of EBITDA to cash interest expense | 2.58 | x | |||||||||||||||||||

Key Operating Data (at end of period): | |||||||||||||||||||||

| Number of pathologists | 426 | 423 | 437 | 437 | |||||||||||||||||

| Number of laboratories | 42 | 42 | 47 | 47 | |||||||||||||||||

| Net revenue per pathologist | $ | 775 | $ | 990 | $ | 1,096 | $ | 1,138 | |||||||||||||

12

| | At December 31, 2002 | At March 31, 2003 | ||||

|---|---|---|---|---|---|---|

| | (dollars in thousands) | |||||

| Balance Sheet Data: | ||||||

| Cash and cash equivalents | $ | 964 | $ | 8,578 | ||

| Working capital(6) | 63,785 | 67,589 | ||||

| Property and equipment, net | 26,126 | 26,995 | ||||

| Total intangibles and goodwill | 552,556 | 783,045 | ||||

| Total debt | 116,253 | 503,376 | ||||

| Total long-term liabilities | 196,811 | 583,788 | ||||

- (1)

- The summary pro forma, as adjusted statement of operations data for the year ended December 31, 2002 gives effect to the applicable pro forma adjustments as if the Transactions and our 2002 acquisitions had occurred on January 1, 2002. The summary pro forma, as adjusted statement of operations data for the three months ended March 31, 2003 gives effect to the applicable pro forma adjustments as if the transactions had occurred on January 1, 2003. The pro forma adjustments are described under "Unaudited Pro Forma Consolidated Financial Information" included elsewhere herein.

- (2)

- EBITDA represents income from operations plus depreciation and amortization, other than amortization of deferred financing costs. EBITDA, a non-GAAP financial measure, is presented herein because management believes it is a widely accepted financial indicator of the ability to incur and service debt. Our presentation of EBITDA is intended to supplement, and not replace our presentation of net income or other GAAP measures. Our calculation of EBITDA may not be comparable to similarly titled measures reported by other companies.

- (3)

- Capital expenditures information is not available on a pro forma basis.

- (4)

- Includes approximately $0.5 million, $0.4 million and $0.3 million of amortization of deferred financing costs for 2000, 2001 and 2002, respectively, and $0.1 million of these costs in the first quarter of 2003. Amortization of deferred financing costs for 2002 and for the three months ended March 31, 2003, on a pro forma, as adjusted basis would have been approximately $2.6 million and $0.6 million, respectively.

- (5)

- Pro forma, as adjusted cash paid for interest is an estimate of what our cash interest expense would have been in 2002 and for the three months ended March 31, 2003 had the Transactions occurred on January 1, 2002 and January 1, 2003, respectively. Timing differences relating to the payment of interest could affect this amount substantially because cash paid for interest is calculated on a cash paid basis and not an accrual basis.

- (6)

- Computed as total current assets less total current liabilities.

13

You should carefully consider the risks described below before making an investment decision. The risks described below are not the only ones facing our company. Additional risks and uncertainties not currently known to us or that we currently deem to be immaterial may also materially and adversely affect our business, financial condition or results of operations. Any of the following risks could materially and adversely affect our business, financial condition or results of operations. In such case, you may lose all or part of your original investment.

Risks Relating to the Exchange Offer and the Notes

Our substantial indebtedness could adversely affect our financial condition and prevent us from fulfilling our obligations under the notes.

We have a significant amount of indebtedness. As of March 31, 2003, our total debt was $503.4 million, excluding unused revolving loan commitments under our new credit facility, which would have represented approximately 61.2% of our total capitalization. This debt does not include our obligations under our existing contingent notes. See "Contingent Notes and the Cash Collateral Account."

Our substantial indebtedness could have important consequences for you by adversely affecting our financial condition and thus making it more difficult for us to satisfy our obligations with respect to the notes, including our repurchase obligations. Our substantial indebtedness could:

- •

- increase our vulnerability to adverse general economic and industry conditions,

- •

- require us to dedicate a substantial portion of our cash flow from operations to payments on our indebtedness, thereby reducing the availability of our cash flow to fund working capital, capital expenditures, payments under our contingent notes, research and development efforts and other general corporate purposes,

- •

- limit our flexibility in planning for, or reacting to, changes in our business and the industry in which we operate,

- •

- place us at a competitive disadvantage compared to our competitors that have less debt and

- •

- limit our ability to borrow additional funds.

Despite our level of indebtedness, we will be able to incur substantially more debt. This could further exacerbate the risks to our financial condition described above.

We will be able to incur significant additional indebtedness in the future. Although the indenture governing the notes and the credit agreement governing our new credit facility contain restrictions on the incurrence of additional indebtedness, these restrictions are subject to a number of qualifications and exceptions and the indebtedness incurred in compliance with these restrictions could be substantial. The restrictions also do not prevent us from incurring obligations that do not constitute indebtedness. Our new credit facility provides for $225.0 million of term loans and revolving loan commitments of up to an additional $65.0 million. To the extent new debt is added to our current debt levels, the substantial leverage risks described above would increase. See "Description of Certain Other Indebtedness—Description of the New Credit Facility" and "Description of the Exchange Notes."

14

The terms of our new credit facility and the indenture relating to the notes may restrict our current and future operations, particularly our ability to respond to changes or to take certain actions.

Our new credit facility contains a number of restrictive covenants that impose significant operating and financial restrictions on us and may limit our ability to engage in acts that may be in our long-term best interests. Our new credit facility includes covenants restricting, among other things, our ability to:

- •

- incur additional debt,

- •

- pay dividends and make restricted payments,

- •

- create liens,

- •

- use the proceeds from sales of assets and subsidiary stock,

- •

- enter into sale and leaseback transactions,

- •

- make capital expenditures,

- •

- change our business,

- •

- enter into transactions with affiliates and

- •

- transfer all or substantially all of our assets or enter into merger or consolidation transactions.

The indenture relating to the notes also contains numerous operating and financial covenants including, among other things, restrictions on our ability to:

- •

- incur additional debt,

- •

- pay dividends or purchase our capital stock,

- •

- make investments,

- •

- enter into transactions with affiliates,

- •

- sell or otherwise dispose of assets and

- •

- merge or consolidate with another entity.

Our new credit facility also includes financial covenants, including requirements that we maintain:

- •

- a minimum interest coverage ratio,

- •

- a minimum fixed charge coverage ratio and

- •

- a maximum leverage ratio.

These financial covenants will become more restrictive over time.

A failure by us to comply with the covenants contained in our new credit facility or the indenture could result in an event of default. In the event of any default under our new credit facility, the lenders under our new credit facility could elect to declare all borrowings outstanding, together with accrued and unpaid interest and fees, to be due and payable, enforce their security interest, require us to apply all of our available cash to repay these borrowings, even if the lenders have not declared a default, or prevent us from making debt service payments on the notes, any of which would result in an event of default under the notes. In addition, future indebtedness could contain financial and other covenants more restrictive than those applicable to our new credit facility and the notes. See "Description of Certain Other Indebtedness—Description of the New Credit Facility" and "Description of the Exchange Notes."

15

We may not be able to generate sufficient cash flow to meet our debt service obligations, including payments on the notes.

Our ability to generate sufficient cash flow from operations to make scheduled payments on our debt obligations will depend on our future financial performance, which will be affected by a range of economic, competitive, regulatory, legislative and business factors, many of which are outside of our control. If we do not generate sufficient cash flow from operations to satisfy our debt obligations, including payments on the notes, we may have to undertake alternative financing plans, such as refinancing or restructuring our debt, selling assets, reducing or delaying capital investments or seeking to raise additional capital. We cannot assure you that any refinancing would be possible or that any assets could be sold on acceptable terms or otherwise. Our inability to generate sufficient cash flow to satisfy our debt obligations, or to refinance our obligations on commercially reasonable terms, would have an adverse effect on our business, financial condition and results of operations, as well as on our ability to satisfy our obligations under the notes.

Your right to receive payments on the notes is unsecured and is junior to virtually all of our and our subsidiary guarantors' existing indebtedness and possibly all of our future borrowings.

The notes and the guarantees will be subordinated to the prior payment in full of our and our subsidiary guarantors' current and future senior debt. As of March 31, 2003, we and our subsidiary guarantors had approximately $230 million of senior debt. We also have $65.0 million in revolving loan commitments under our new credit facility. The indenture relating to the notes permits us and our subsidiary guarantors to incur additional senior debt. Because the notes are unsecured and because of the subordination provision of the notes, in the event of the bankruptcy, liquidation or dissolution of us or any subsidiary guarantor, our assets and the assets of the subsidiary guarantors would be available to pay obligations under the notes only after all payments had been made on our and the subsidiary guarantors' senior debt, including debt under our new credit facility. We cannot assure you that sufficient assets will remain after all these payments have been made to make any payments on the notes, including payments of interest when due. Because of these subordination provisions, you may recover less ratably than our other creditors in a bankruptcy, liquidation or dissolution. In addition, all payments on the notes and the guarantees will be blocked in the event of a payment default on senior debt and may be blocked for up to 179 consecutive days in the event of non-payment defaults on specified senior debt. See "Description of the Exchange Notes—Ranking."

The notes are not secured by our assets nor those of our subsidiary guarantors, and the lenders under our new credit facility will be entitled to remedies available to a secured lender, which gives them priority over you to collect amounts due to them.

In addition to being subordinated to all our existing and future senior debt, the notes and the guarantees will not be secured by any of our assets. Our obligations under our new credit facility are secured by, among other things, a first priority pledge of all our common stock, substantially all our assets, substantially all the assets of certain of our existing and subsequently acquired or organized subsidiaries and the restricted cash held by our parent in the contingent note cash collateral account. If we become insolvent or are liquidated, or if payment under our new credit facility or in respect of any other secured indebtedness is accelerated, the lenders under our new credit facility or holders of other secured indebtedness will be entitled to exercise the remedies available to a secured lender under applicable law in addition to any remedies that may be available under documents pertaining to our new credit facility or other senior debt. Upon the occurrence of any default under our new credit facility, and even without accelerating the indebtedness under our new credit facility, the lenders may be able to prohibit the payment of the notes and guarantees either by limiting our ability to access our cash flow or under the subordination provisions contained in the indenture governing the notes. See

16

"Description of Certain Other Indebtedness—Description of the New Credit Facility" and "Description of the Exchange Notes."

Not all of our subsidiaries will guarantee the notes, and the assets of our non-guarantor subsidiaries may not be available to make payments on the notes.

The guarantors of the notes will not include all of our subsidiaries. The historical consolidated financial information and the pro forma consolidated financial information included in this prospectus, however, are presented on a combined basis, including both our guarantor and non-guarantor subsidiaries. At March 31, 2003, the total debt of our non-guarantor subsidiaries was less than $10 million, including trade payables. In the event that any non-guarantor subsidiary becomes insolvent, liquidates, reorganizes, dissolves or otherwise winds up, holders of its indebtedness and its trade creditors generally will be entitled to payment on their claims from the assets of that subsidiary before any of those assets are made available to us. Consequently, your claims in respect of the notes will be effectively subordinated to all of the liabilities of our non-guarantor subsidiaries, including trade payables, and the claims, if any, of any third party holders of preferred equity interests in our non-guarantor subsidiaries.

A substantial portion of our assets are held by, and a substantial portion of our income is derived from, our subsidiaries, and the senior debt of our subsidiary guarantors may restrict payment on the notes.

We hold a substantial portion of assets through our subsidiaries and derive a substantial portion of our operating income from our subsidiaries. We are dependent on the earnings and cash flow of our subsidiaries to meet our obligations with respect to the notes. We cannot assure you that our subsidiaries will be able to, or be permitted to, pay to us amounts necessary to service the notes. In certain circumstances, the indenture governing the notes permits our subsidiary guarantors to enter into agreements that can limit our ability to receive distributions from our subsidiaries. In the event we do not receive distributions from our subsidiaries, we may be unable to make required principal and interest payments on our indebtedness, including the notes.

There may be no active trading market for the notes.

The exchange notes will constitute a new issue of securities for which there is no established trading market. We do not intend to list the exchange notes on any national securities exchange or to seek the admission of the exchange notes for quotation through the National Association of Securities Dealers Automated Quotation System. Although the initial purchasers have advised us that they currently intend to make a market in the old notes, and the exchange notes, if issued, they are not obligated to do so and may discontinue such market making activity at any time without notice. In addition, market-making activity will be subject to the limits imposed by the Securities Act and the Exchange Act and may be limited during the exchange offer and the pendency of any shelf registration statement. Although the exchange notes will be eligible for trading in The Portalsm Market, there can be no assurance as to the development or liquidity of any market for the exchange notes, the ability of the holders of the exchange notes to sell their exchange notes or the price at which the holders would be able to sell their exchange notes.

We may not be able to fulfill our repurchase obligations in the event of a change of control.

Upon the occurrence of any change of control, we will be required to make a change of control offer to repurchase the notes. Any change of control also would constitute a default under our new credit facility. Therefore, upon the occurrence of a change of control, the lenders under our new credit facility would have the right to accelerate their loans, and we would be required to prepay all of our outstanding obligations under our new credit facility. Also, as our new credit facility generally prohibits

17

us from purchasing any notes, if we do not repay all borrowings under our new credit facility first or obtain the consent of the lenders under our new credit facility, we will be prohibited from purchasing the notes upon a change of control.

In addition, if a change of control occurs, there can be no assurance that we will have available funds sufficient to pay the change of control purchase price for any or all of the notes that might be delivered by holders of the notes seeking to accept the change of control offer and, accordingly, none of the holders of the notes may receive the change of control purchase price for their notes. Our failure to make the change of control offer or pay the change of control purchase price when due would result in a default under the indenture governing the notes. See "Description of the Exchange Notes—Defaults."

Fraudulent conveyance laws could void our obligations under the notes.

The proceeds from the sale of the old notes were applied, together with other available funds, to make payments to former stockholders of AmeriPath in connection with the March 27, 2003 merger. Our incurrence of debt under the notes may be subject to review under federal and state fraudulent conveyance laws if a bankruptcy, reorganization or rehabilitation case or a lawsuit, including circumstances in which bankruptcy is not involved, were commenced by, or on behalf of, our unpaid creditors or unpaid creditors of our guarantors at some future date. Federal and state statutes allow courts, under specific circumstances, to void notes and guaranties and require noteholders to return payments received from debtors or their guarantors. As a result, an unpaid creditor or representative of creditors could file a lawsuit claiming that the issuance of the notes constituted a "fraudulent conveyance." To make such a determination, a court would have to find that we did not receive fair consideration or reasonably equivalent value for the notes and that, at the time the notes were issued, we:

- •

- were insolvent,

- •

- were rendered insolvent by the issuance of the notes,

- •

- were engaged in a business or transaction for which our remaining assets constituted unreasonably small capital or

- •

- intended to incur, or believed that we would incur, debts beyond our ability to repay those debts as they matured.

If a court were to make such a finding, it could void all or a portion of our obligations under the notes, subordinate the claim in respect of the notes to our other existing and future indebtedness or take other actions detrimental to you as a holder of the notes, including in certain circumstances, invalidating the notes.

The measure of insolvency for these purposes will vary depending upon the law of the jurisdiction being applied. Generally, a company will be considered insolvent for these purposes if the sum of that company's debts is greater than the fair value of all of that company's property, or if the present fair salable value of that company's assets is less than the amount that will be required to pay its probable liability on its existing debts as they mature. Moreover, regardless of solvency, a court could void an incurrence of indebtedness, including the notes, if it determined that the transaction was made with intent to hinder, delay or defraud creditors, or a court could subordinate the indebtedness, including the notes, to the claims of all existing and future creditors on similar grounds. We cannot determine in advance what standard a court would apply to determine whether we were "insolvent" in connection with the sale of the notes.

The making of the guaranties might also be subject to similar review under relevant fraudulent conveyance laws. A court could impose legal and equitable remedies, including subordinating the

18

obligations under the guaranties to our other existing and future indebtedness or taking other actions detrimental to you as a holder of the notes.

The market price for the notes may be volatile.

Historically, the market for non-investment grade debt has been subject to disruptions that have caused substantial volatility in the prices of securities similar to the notes. The market for the notes, if any, may be subject to similar disruptions. Any such disruptions may adversely affect the value of your notes.

If you do not properly tender your old notes, your ability to transfer your old notes will be adversely affected.

We will only issue exchange notes in exchange for old notes that are timely received by the exchange agent, together with all required documents, including a properly completed and signed letter of transmittal. Therefore, you should allow sufficient time to ensure timely delivery of the old notes and you should carefully follow the instructions on how to tender your old notes. Neither we nor the exchange agent are required to tell you of any defects or irregularities with respect to your tender of the old notes. If you do not tender your old notes or if we do not accept your old notes because you did not tender your old notes properly, then, after we consummate the exchange offer, you would continue to hold old notes that are subject to the existing transfer restrictions.

In addition, if you tender your old notes for the purpose of participating in a distribution of exchange notes, you will be required to comply with the registration and prospectus delivery requirements of the Securities Act in connection with any resale of the exchange notes. If you are a broker-dealer that receives exchange notes for your own account in exchange for old notes that you acquired as a result of market-making activities or any other trading activities, you will be required to acknowledge that you will deliver a prospectus in connection with any resale of such exchange notes.

After the exchange offer is consummated, if you continue to hold any old notes, you may have difficulty selling them because there will be fewer old notes outstanding. In addition, if a large amount of old notes are not tendered or are tendered improperly, the limited amount of exchange notes that would be issued and outstanding after we consummate the exchange offer could lower the market price of such exchange notes.

Some holders who exchange their old notes may be deemed to be underwriters.

If you exchange your old notes in the exchange offer for the purpose of participating in a distribution of the exchange notes, you may be deemed to have received restricted securities and, if so, will be required to comply with the registration and prospectus delivery requirements of the Securities Act in connection with any resale transaction.

The interests of our principal stockholders may not be aligned with your interests as a holder of the notes.

Welsh, Carson, Anderson & Stowe IX, L.P. and its related investors control all of the voting power of the outstanding common stock of our parent and control all of our affairs and policies. Circumstances may occur in which the interests of these equity holders could be in conflict with the interests of the holders of the notes. In addition, these equity holders may have an interest in pursuing acquisitions, divestitures or other transactions that, in their judgment, could enhance their equity investment, even though such transactions might involve risks to holders of the notes.

19

Risks Relating to Our Business

We conduct business in a heavily regulated industry, and changes in regulations or violations of regulations may, directly or indirectly, reduce our revenues and harm our business.

The healthcare industry is highly regulated, and there can be no assurance that the regulatory environment in which we operate will not change significantly and adversely in the future. Several areas of regulatory compliance that may affect our ability to conduct business include:

- •

- federal and state anti-kickback laws,

- •

- federal and state self-referral and financial inducement laws, including the federal physician anti-self referral law, or the Stark Law,

- •

- federal and state false claims laws,

- •

- state laws regarding prohibitions on the corporate practice of medicine,

- •

- state laws regarding prohibitions on fee-splitting,

- •

- federal and state anti-trust laws,

- •

- the Health Insurance Portability and Accountability Act of 1996, or HIPAA,

- •

- federal and state regulation of privacy, security and transmission of health information and

- •

- federal, state and local laws governing the handling and disposal of medical and hazardous waste.

These laws and regulations are extremely complex. In many instances, the industry does not have the benefit of significant regulatory or judicial interpretation of these laws and regulations. It also is possible that the courts could ultimately interpret these laws in a manner that is different from our interpretations. While we believe that we are currently in material compliance with applicable laws and regulations, a determination that we have violated these laws, or the public announcement that we are being investigated for possible violations of these laws, would have an adverse effect on our business, financial condition and results of operations. For a more complete description of these regulations, see "Government Regulation."

Our business could be materially harmed by future interpretation or implementation of state laws regarding prohibitions on the corporate practice of medicine.

The manner in which licensed physicians can be organized to perform and bill for medical services is governed by state laws and regulations. Under the laws of some states, business corporations generally are not permitted to employ physicians or to own corporations that employ physicians or to otherwise exercise control over the medical judgments or decisions of physicians.

We believe that we currently are in compliance with the corporate practice of medicine laws in the states in which we operate in all material respects. Nevertheless, there can be no assurance that regulatory authorities or other parties will not assert that we are engaged in the corporate practice of medicine or that the laws of a particular state will not change. If such a claim were successfully asserted in any jurisdiction, or as a result of such a change in law, we could be required to restructure our contractual and other arrangements, our company and our pathologists could be subject to civil and criminal penalties and some of our existing contracts, including non-competition provisions, could be found to be illegal and unenforceable. In addition, expansion of our operations to other states may require structural and organizational modification of our form of relationship with pathologists, operations or hospitals. These results or the inability to successfully restructure contractual arrangements would have an adverse effect on our business, financial condition and results of operations.

20

We could be hurt by future interpretation or implementation of federal and state anti-kickback and anti-referral laws.

Federal and state anti-kickback laws prohibit the offer, solicitation, payment and receipt of remuneration in exchange for referrals of products and services for which payment may be made by Medicare, Medicaid or other federal and state healthcare programs. Federal and state anti-referral laws, including the Stark Law, ban payments to physicians for referrals of patients to health care providers with whom the physicians or their immediate family members have a financial relationship for services for which payment may be made by Medicare or Medicaid. A violation of any of these laws could result in monetary fines, civil and criminal penalties and exclusion from participation in Medicare, Medicaid or other federal or state healthcare programs, which accounted for approximately 20% of our revenues in 2002 and for the first quarter of 2003.

Some of our physicians hold contingent notes issued in connection with acquisitions we have completed, are party to compensation arrangements with us and, prior to the merger, owned AmeriPath common stock. Although we believe that none of these constitute an unlawful kickback under federal and state anti-kickback laws, government authorities may take a contrary position. Furthermore, although we believe that our financial relationships with our physicians and our referral practices do not violate federal and state anti-referral laws, including the Stark Law, the government may take a contrary position, or a prohibited referral may be made by one of our physicians without our knowledge. If our financial relationships with our physicians were found to be unlawful or unlawful referrals were found to have been made, we or they could be fined, become subject to government recoupment of fees previously paid to us and forfeiture of revenues due to us or become subject to civil and criminal penalties. In such situations, we also may be excluded from participation in Medicare, Medicaid and other federal and state healthcare programs. Any one of these consequences could have an adverse effect on our business, financial conditions and results of operations.

Our business could be harmed by future interpretation or implementation of state law prohibitions on fee-splitting.

Many states prohibit the splitting or sharing of fees between physicians and non-physicians. We believe our arrangements with pathologists and operations comply in all material respects with the fee-splitting laws of the states in which we operate. Nevertheless, it is possible that regulatory authorities or other parties could claim we are engaged in fee-splitting. If such a claim were successfully asserted in any jurisdiction, our pathologists could be subject to civil and criminal penalties, including loss of licensure, and we could be required to restructure our contractual and other arrangements. In addition, expansion of our operations to new states with fee-splitting prohibitions may require structural and organizational modification to the form of our current relationships which may be less profitable. A claim of fee-splitting or modification of our business to avoid such a claim could have an adverse effect on our business, financial condition and results of operations.

Federal and state regulation of privacy could cause us to incur significant costs.

The Federal Trade Commission, or FTC, pursuant to consumer protection laws, and the Department of Health and Human Services, or HHS, pursuant to HIPAA, regulate the use and disclosure of information we may have about our patients. Many states also have laws regarding privacy of health information. While we believe that we are in compliance with FTC and state laws regarding privacy, as well as the HIPAA privacy regulations, these laws are complex and will have an impact upon our operations. Violations of the privacy regulations are punishable by civil and criminal penalties. In addition, while individuals do not have a private right of action under HIPAA, the privacy regulations may be viewed by the courts as setting a standard of conduct, which the failure to meet could give rise to a private claim.

21

We are subject to significant professional or other liability claims and we cannot assure you that insurance coverage will be available or sufficient to cover such claims.

We may be sued under physician liability or other liability law for acts or omissions by our pathologists, laboratory personnel and hospital employees who are under the supervision of our hospital-based pathologists. We and our pathologists periodically become involved as defendants in medical malpractice and other lawsuits, some of which are currently ongoing, and are subject to the attendant risk of substantial damage awards. We believe that we have a prudent risk management program, which includes our captive insurance arrangements and our excess liability insurance coverage as well as indemnity agreements from third parties.

Through June 30, 2002, we were insured for medical malpractice risks on a claims made basis under traditional professional liability insurance policies. In July 2002, we began using a captive insurance program to partially self-insure our medical malpractice risk. Under the captive insurance program we retain more risk for medical malpractice costs, including settlements and claims expenses, than under our prior coverage. We have no aggregate excess stop loss protection under our captive insurance arrangements, meaning there is no aggregate limitation on the amount of risk we retain under these arrangements. Because of our self-insurance arrangements and our lack of aggregate excess stop loss protection, professional malpractice claims could result in substantial uninsured losses. In addition, it is possible that the costs of our captive insurance arrangements and excess insurance coverage will rise, causing us either to incur additional costs or to further limit the amount of our coverage. Further, our insurance does not cover all potential liabilities arising from governmental fines and penalties, indemnification agreements and certain other uninsurable losses. For example, from time to time we agree to indemnify third parties, such as hospitals and national clinical laboratories, for various claims that may not be covered by insurance. As a result, we may become responsible for substantial damage awards that are uninsured. We are currently subject to indemnity claims, which if determined adversely to us, could result in substantial uninsured losses. Therefore, it is possible that pending or future claims will not be covered by or will exceed the limits of our insurance coverage and indemnification agreements or that third parties will fail or otherwise be unable to comply with their obligations to us.

Government programs account for approximately 20% of our revenues, so a decline in reimbursement rates from government programs would harm our revenues and profitability.