DO NOT BE MISLED, POTOMAC IS NOT SEEKING CONTROL OF SIGMA

Potomac Sets Record Straight Regarding Sigma’s Misrepresentations About Settlement Discussions

NEW YORK, June 25, 2012 /PRNewswire/ -- Potomac Capital Partners III, L.P. (“PCP III”), which together with its nominees and certain other shareholders are members of a group (the “Potomac Group”) that collectively owns 2,612,230 shares of common stock of Sigma Designs, Inc. (NASDAQ: SIGM) (the “Company” or “SIGM”), representing approximately 8.0% of the Company’s outstanding shares, today commented on the Company’s misleading statements regarding recent settlement discussions.

“Contrary to what the Company would like shareholders to believe, the Potomac Group is not trying to take over the Board and has attempted to work cooperatively with the Company to come to a mutually agreeable settlement in order to avoid a costly and protracted proxy contest,” said Eric B. Singer, the co-managing member of Potomac Capital Management III, L.L.C, the general partner of PCP III. “I traveled to California on two occasions and tried to engage management to discuss my concerns regarding the Company and the issue of Board representation. Instead, the Company ceased all communication with me until recently when they proposed a settlement that no longer would result in meaningful change,” said Mr. Singer.

Despite the Company’s claims, the Potomac Group did not inexplicably refuse its own settlement proposal. The Potomac Group’s initial proposal of a five (5) member Board, consisting of two (2) individuals nominated by the Potomac Group and three (3) incumbent directors, was originally rejected in April 2012 by William Almon, the Company’s lead independent director, because he claimed it would result in a stalemate on the Board. Mr. Almon’s rational for rejecting the proposal was that Thinh Tran, in his capacity as Chairman and CEO, would have to recuse himself from certain Board votes, leaving a tie as Mr. Almon presumed there would be disagreement between the two (2) Potomac designated directors and the two (2) remaining incumbent directors. The Potomac Group was alarmed that this view demonstrated a defensive, entrenched mentality of the existing Board. If the incumbent directors were truly engaged in pursuing business and governance practices in the best interest of all shareholders, their interests should be aligned with those of any new director, and there should be constructive and healthy Board dynamics.

The Company’s initial response was followed by five weeks of silence, despite the Potomac Group’s attempts to continue a dialogue with the Company. During such time, the Potomac Group watched as shareholder value continued to erode (e.g., reporting a $13.7 million net loss for the quarter ended April 28, 2012 and further cash depletion from operating losses and the additional $21.2 million outlay for the acquisition of Trident, as well as management giving flat guidance for the next quarter). This, in combination with the rejection of the Potomac Group’s initial proposal, led the Potomac Group to believe that without significant change on the Board it would be business as usual with a majority of incumbent directors that have overseen a dramatic deterioration of the Company's financial, operating and stock performance. Accordingly, when the Company re-initiated settlement discussions in June 2012, the Potomac Group proposed that the Board be reconstituted with five (5) directors, consisting of two (2) incumbent directors, two (2) individuals nominated by the Potomac Group, and one (1) additional independent director to be mutually agreed upon. This proposal would not result in the Potomac Group obtaining majority representation on the Board, but would result in meaningful change.

The Company immediately rejected this proposal, with the Company’s CEO claiming that if more than two incumbent directors did not stand for re-election, the existing Board would look dysfunctional. In hopes of addressing Mr. Tran’s concerns, the Potomac Group suggested that the Board be reconstituted with seven (7) directors, consisting of three (3) incumbent directors, three (3) individuals nominated by the Potomac Group and one (1) additional independent director to be mutually agreed upon. Again, this suggestion was rejected by the Company. Unless the existing Board has a different agenda, this Board should not be concerned that the addition of two or three new directors, one of which would be mutually agreed upon, would impair its ability to oversee the Company’s strategic plan unless that plan is contrary to the best interests of shareholders.

While the Potomac Group, as recently as June 17, 2012, offered to continue to discuss alternative settlement resolutions, the Company’s CEO refused to discuss any proposal that did not involve a majority of the incumbent directors maintaining control of the Board. This flies in the face of the Company’s claim that they remain willing to engage in constructive discussions.

Furthermore, SIGM has an especially abysmal governance profile which in-addition to its poor financial performance necessitates a reconstituted Board. Consider the following governance issues allowed by the current Board, which have been criticized by Institutional Shareholder Services Inc. and Glass Lewis & Co., two of the leading proxy advisory firms:

| | • | An unacceptably low number of Board members for a public company - four (4); |

| | • | An average Board tenure of 17 years, with each of the current members serving for 9 consecutive years; |

| | • | A history of poor compensation practices and approval of discretionary bonuses regardless of Company performance; and |

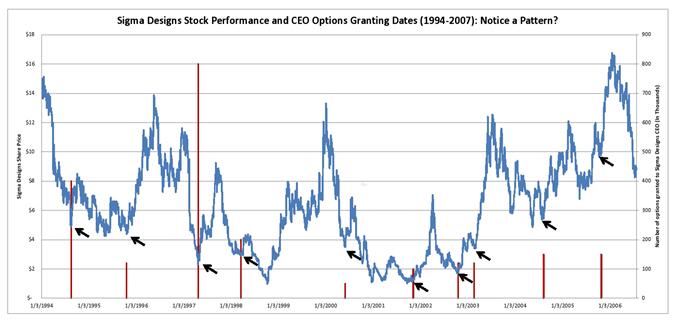

| | • | A wildly irresponsible history of option granting. |

The following chart illustrates the pattern of this incumbent Board to award stock options to the Company’s CEO when the Company’s stock price was at its lowest point:

ë - Indicates award grant date.

If the incumbent Board is reelected, or only two (2) of the Potomac Group’s nominees are elected, the incumbent directors will maintain control of the Company. The Company states that 40% representation on the Board is more than reasonable for the Potomac Group, a shareholder of approximately 8.0% of the Company’s outstanding shares, while conveniently omitting to mention that they advocate maintaining control of the Board by a group that currently owns approximately 2% of the Company’s outstanding shares (not counting interest in stock option grants, the overwhelming majority of which are under-water).

THE BEST WAY TO ENSURE THAT SIGM IS RUN WITH THE BEST INTEREST OF ALL

SHAREHOLDERS AS THE TOP PRIORITY IS TO HAVE A BOARD OF NEW,

INDEPENDENT DIRECTORS WHOSE INTERESTS ARE DIRECTLY ALIGNED WITH YOURS

This election contest is not about winning control. This election contest is simply a referendum on whether shareholders are satisfied with the performance of the Company under the incumbent Board. If elected, the Potomac Group’s nominees are committed to engaging in a search for additional independent directors mutually agreed upon by the other incumbent directors. Given the destruction of shareholder value over the tenure of the incumbent Board, the Potomac Group has no faith that the Company will return to profitability if the existing Board is permitted to remain in control.

By voting the GOLD proxy card you will be supporting new, independent directors who are dedicated to effecting improvements in both the Company’s operations and stock price and evaluating all opportunities to create value based on actions easily within the Company's control.

If you have any questions or require any assistance with your vote, please contact Okapi Partners LLC at (212) 297-0720 or (877) 566-1922 or email at info@okapipartners.com.