UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-21359

MBIA Capital/Claymore Managed Duration Investment Grade Municipal Fund

(Exact name of registrant as specified in charter)

2455 Corporate West Drive, Lisle, IL 60532

(Address of principal executive offices) (Zip code)

Nicholas Dalmaso

2455 Corporate West Drive, Lisle, IL 60532

(Name and address of agent for service)

Registrant’s telephone number, including area code: (630) 505-3700

Date of fiscal year end: July 31

Date of reporting period: July 31, 2006

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. Section 3507.

| Item 1. | Reports to Stockholders. |

The registrant’s annual report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940, as amended, is as follows:

www.mbiaclaymore.com

... your stream to the LATEST,

most up-to-date INFORMATION about the

MBIA Capital/Claymore Managed Duration

Investment Grade Municipal Fund

The shareholder report you are reading right now is just the beginning of the story. Online at www.mbiaclaymore.com, you will find:

| | • | | Daily, weekly and monthly data on share prices, distributions and more |

| | • | | Portfolio overviews and performance analyses |

| | • | | Announcements, press releases, special notices and tax characteristics |

MBIA Capital Management and Claymore are continually updating and expanding shareholder information services on the Fund’s website, in an ongoing effort to provide you with the most current information about how your Fund’s assets are managed, and the results of our efforts. It is just one more way we are working to keep you better informed about your investment in the Fund.

| | |

2 | Annual Report | July 31, 2006 | | |

MZF | MBIA Capital/Claymore Managed Duration Investment Grade Municipal Fund

Dear Shareholder

I am pleased to submit the annual shareholder report for the MBIA Capital/Claymore Managed Duration Investment Grade Municipal Fund (the “Fund”). This report covers performance for the fiscal year ended July 31, 2006. As you may know, the Fund’s investment objective is to provide high current income exempt from regular Federal income tax while seeking to protect the value of the Fund’s assets during periods of interest rate volatility. The Fund seeks to achieve these objectives by investing at least 80% of its assets in municipal bonds of investment grade quality and normally investing substantially all of its assets in securities of investment grade quality.

MBIA Capital Management Corp. (“MBIA”) is the Fund’s Investment Adviser and is owned by MBIA Asset Management Group, a $55 billion dollar manager of fixed-income products. Its parent company, MBIA Inc., is listed on the New York Stock Exchange and is a component stock of the S&P 500 Index.

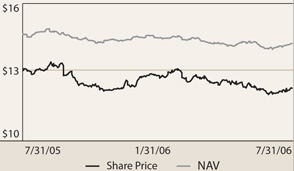

In the fiscal year ended July 31, 2006, the Fund produced a total return of 1.57% at net asset value (“NAV”). This represents a change in NAV to $14.25 on July 31, 2006 from $14.68 at the start of the period, plus the reinvestment of monthly dividends. During the fiscal year, the Fund generated a negative total return of 1.60% on a market value basis. This represents a change in the Fund’s market price to $12.29 on July 31, 2006 from $13.15 on July 31, 2005, plus the reinvestment of monthly dividends.

As was the case with many of the Fund’s peers, the Fund reduced its monthly dividend. Effective in June 2006, the monthly dividend was reduced to $0.047 per share from $0.056 per share. The increased costs of the Fund’s leveraging strategy due to rising short-term interest rates coupled with relatively flat long-term interest rates have continued to apply pressure on the Fund’s dividend. In light of the prevailing interest rate conditions, this new dividend rate more accurately reflects the earning power of the Fund’s underlying portfolio.

Over the course of the Fund’s fiscal year, the Federal Reserve Board (the “Fed”) raised the federal funds interest rate eight times. At the end of the fiscal year, the short-term interest rate was 5.25%, up from 3.25% at the start of the fiscal year. The federal funds rate now stands at 5.25% versus 1.00% when the Fund came to market in August 2003. These continued short-term interest rate increases have produced a flat U.S. Treasury yield curve which was inverted for a portion of the fiscal year. Essentially, short-term interest rates rose significantly while long-term rates rose more modestly, causing shorter-term securities to underperform longer-term securities. As investors looked for yield, they favored lower quality and non-investment grade securities that were generally producing higher yields than higher quality and investment-grade securities. This provided a challenging environment for the Fund as it invests primarily in investment-grade securities with varying maturities.

| | |

| | Annual Report | July 31, 2006 | 3 |

MZF | MBIA Capital/Claymore Managed Duration Investment Grade Municipal Fund | Dear Shareholder continued

The Fund employs a long-term hedging strategy to manage duration and to attempt to reduce volatility as long-term interest rates trend higher. We initiated this hedging strategy at the time of the Fund’s inception because we believed that long-term interest rates were poised to rise. Historically, long-term rates have risen during periods when the Fed has executed a fed funds interest rate tightening program. The flattening yield curve that we’ve witnessed over the past two years is highly unusual given the ongoing hikes in short-term interest rates. While the hedge cost performance during this fiscal year, we continue to believe that our hedging strategy is prudent as the future direction of interest rates remains uncertain.

Municipal securities generally outperformed U.S. Treasury securities during the Fund’s fiscal year. The issuance of municipal securities has slowed in 2006, but demand remains strong. We believe that municipal securities continue to represent good relative value and continue to be a prudent fixed-income investment. While lower quality securities outperformed higher quality, investment grade municipal securities during the Fund’s fiscal period, we expect to see movement into higher quality investment-grade securities when long-term interest rates begin to rise more significantly and credit spreads begin to widen.

|

Sincerely, |

|

|

Clifford D. Corso |

| MBIA Capital/Claymore Managed Duration Investment Grade Municipal Fund |

| | |

4 | Annual Report | July 31, 2006 | | |

MZF | MBIA Capital/Claymore Managed Duration Investment Grade Municipal Fund

Questions & Answers

Clifford D. Corso – Portfolio Manager

Mr. Corso is President of MBIA Capital Management Corp. which is owned by MBIA Asset Management Group. Mr. Corso joined the firm in 1994 and developed its fixed-income asset management platform and now directs the investment of more than $55 billion in fixed-income assets. Throughout his 20-year career, he has managed a wide array of fixed-income products, including corporate, asset-backed, government, mortgage and derivative products. Mr. Corso holds an MBA degree from Columbia University.

E. Gerard Berrigan – Portfolio Manager

Mr. Berrigan is a Managing Director and heads portfolio management for MBIA Capital Management Corp. He joined the firm in 1994 and is a member of the Investment Strategy Committee, the Investment Review Committee and Market Risk Committee. Mr. Berrigan has more than 15 years of experience in securities trading and portfolio management. He holds an MBA degree from Columbia University.

The MBIA Capital/Claymore Managed Duration Investment Grade Municipal Fund portfolio management team continues to be led by Clifford Corso. Mr. Corso has led the portfolio management team since the Fund’s inception. E. Gerard Berrigan assists Mr. Corso in the management of the Fund’s portfolio. During the most recent reporting period, Sue Voltz and Patrick Tucci left MBIA to pursue other opportunities. The Fund continues to be managed by a team concept and there has been no change in the team’s investment philosophy, objective or strategy.

In the following interview Portfolio Managers Clifford D. Corso and E. Gerard Berrigan discuss the market environment and the performance of the MBIA Capital/Claymore Managed Duration Investment Grade Municipal Fund (the “Fund”) for the Fund’s fiscal year ended July 31, 2006.

Will you please provide a brief overview of the municipal market during the 12-month period ended July 31, 2006?

During the period the Federal Reserve Board (the “Fed”) continued its interest rate tightening cycle and raised short-term interest rates eight times – from 3.25% at the start of the fiscal year to 5.25% by July 31, 2006. The federal funds rate now stands at 5.25% versus 1.00% when the Fund came to market in August 2003. The economy grew at a moderate pace throughout most of the fiscal year, but the slowdown in the housing market and lagging effects of higher interest rates and energy prices could suggest a downturn in future economic growth. At the same time inflation continues to be a concern. The Fed has recently decided to pause in its interest rate tightening cycle to see whether or not recent signs of a slowing economy will, by itself, remove inflationary pressures.

Municipal bonds generally outperformed Treasury bonds during the period. While the municipal bond yield curve continued to flatten (yields on short-maturity bonds rose faster than yields on long-maturity bonds), the Treasury yield curve flattened more dramatically and even inverted for a portion of the fiscal year.

After a record high level of issuance of more than $408 billion in 2005, new issuance of municipal securities slowed in the first seven months of 2006. Demand for municipal securities, however, remained strong and continued to provide support for the municipal bond market. Demand came from property and casualty insurers and non-traditional municipal investors such as hedge fund managers who invested across all maturities and were attracted to the asset class due to attractive valuations versus taxable bonds. As investors continued to search for favorable income levels, non-investment grade and lower quality investment grade municipal bonds were the strongest performers during the year as were bonds with longer maturities and durations.

How did this backdrop affect the Fund’s performance?

This backdrop created a challenging environment for the Fund, which invests, by objective at least 80% of its assets in investment grade municipal securities and substantially all of its assets in investment grade quality investments. The Fund also maintains a generally shorter duration than most of its peers. The Fund provided a negative market price total return of 1.60%, which includes the reinvestment of the Fund’s monthly dividends. The Fund gained on a net asset value (“NAV”) basis, generating a total return of 1.57%, which includes the reinvestment of the Fund’s monthly dividends. For NAV performance comparison purposes, the Lehman Brothers Municipal Bond Index returned 2.55% for the 12-month period. The Fund’s hedging strategy, which was put into place to help protect the Fund from rising long-term interest rates, detracted from relative performance as long bond rates rose modestly during the fiscal year.

| | |

| | Annual Report | July 31, 2006 | 5 |

MZF | MBIA Capital/Claymore Managed Duration Investment Grade Municipal Fund | Questions & Answers continued

Which issues or trends most helped the Fund’s performance and why?

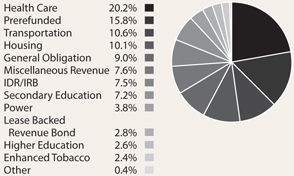

The Fund’s positions in housing bonds and hospital bonds continued to help performance. The Fund held an overweight position in these sectors relative to the Lehman Brothers Municipal Bond Index and both sectors posted strong returns and outperformed the index. The housing bonds, which are backed by pools of mortgages, benefited primarily due to their longer final maturities. The Fund’s hospital bonds were supported by the improving credit quality of the sector as well as the market’s continued high demand for higher yielding assets.

Which areas of the Fund hurt performance during the period?

The Fund’s investment grade objective and shorter duration hurt performance relative to its peers. The Fund’s long-term hedging strategy also cost performance. We initiated this hedging strategy at the time of the Fund’s inception because we believed that long-term interest rates were poised to rise. Historically, long-term rates have risen during periods when the Fed has executed a fed funds rate tightening program. The flattening yield curve that we’ve witnessed over the past two years is highly unusual given the ongoing hikes in short-term interest rates. In the second half of this 12-month period, interest rates on long-term municipal bonds began to rise modestly. Unfortunately long-term rates did not rise enough for the hedging strategy to add value, and the Fund lost money on the hedge.

We have maintained the hedge because we believe that long-term rates will increase more significantly in the coming year. If that happens, the strategy should benefit the Fund by providing capital appreciation on the hedge. Of course, the risk remains that long rates could reverse course, but we don’t anticipate that to occur in any substantive or consistent fashion.

Did you make any structural changes to the Fund’s portfolio?

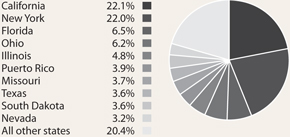

We made no meaningful changes in terms of the Fund’s positioning on the yield curve or from a duration standpoint, believing that this is the correct position in the context of our outlook. From a credit standpoint, we did elect to reduce our exposure to issuers in the Commonwealth of Puerto Rico due to a negative credit trend. We reduced such holdings in half to about 4% of long-term investments. Spreads did indeed widen in the period, and have since begun to tighten moderately, but remain historically wide.

Will you tell us about the duration of the Fund and how you manage it?

The Fund’s duration moved lower throughout the fiscal year. Duration is a measure of the interest rate sensitivity of a fixed-income portfolio which incorporates time-to-maturity and coupon size. The larger the duration number, the greater the interest rate risk.

At the start of the period, the Fund’s option-adjusted duration was 8.9 years. At the end of the period duration stood at 8.2 years. The duration declined for several reasons. First, was the result of the natural aging of the portfolio, meaning bonds are moving closer to their maturity dates. The duration also declined as the result of some issues having been pre-refunded, which moved a portion of the portfolio to a 10-year maturity range from a 20-year maturity range. We’re comfortable with the Fund’s current duration stance in a time when we expect to see long-term interest rates begin to rise. The Fund’s hedging strategy is structured as another way to manage duration and attempt to reduce portfolio volatility as interest rates trend higher. Should we see a major shift in the interest-rate environment, we’d adjust the Fund’s duration to reflect our revised outlook.

Please tell us about the Fund’s distributions during the period.

As was the case with many of the Fund’s peers, the Fund reduced its monthly dividend. Effective in June 2006, the dividend was reduced to $0.047 per share from $0.056 per share. The increased costs of the Fund’s leveraging strategy due to rising short-term interest rates coupled with relatively flat long-term interest rates have continued to apply pressure on the Fund’s dividend. The new dividend rate more accurately reflects the earning power of the Fund’s underlying portfolio.

How have higher short-term interest rates impacted the Fund’s leverage?

The Fund, like many closed-end funds, utilizes leverage as part of its investment strategy. The purpose of leverage is to fund the purchase of additional securities that provide increased income and

| | |

6 | Annual Report | July 31, 2006 | | |

MZF | MBIA Capital/Claymore Managed Duration Investment Grade Municipal Fund | Questions & Answers continued

potentially greater appreciation to common shareholders than could be achieved from an un-leveraged portfolio. Of course, leverage results in greater NAV volatility and entails more downside risk than an un-leveraged portfolio. The use of leverage also makes the Fund more vulnerable to rising interest rates. During the period, rising short-term interest rates increased the Fund’s cost of leverage. While our cost of leverage increased, it still added overall value. We will continue to employ a leveraged strategy as long as there is a benefit to doing so.

What is your outlook for the municipal market in 2006?

We have a favorable outlook for the municipal market. While we believe that the Fed is nearing the end of its rate tightening cycle, we would not be surprised by some additional rate hikes this year. We also expect to see the yield curve begin to steepen modestly and long rates to rise further by year’s end. Longer-maturity, lower-quality municipal bonds are expensive on a historical basis, but demand remains strong and appears able to support current levels. Over time, however, we believe that higher quality issues with more defensive durations will perform well. Spreads in the municipal market are very tight and we expect to see investors begin returning to higher quality securities.

New municipal issuance is anticipated to decline from record 2005 levels, but we expect that demand will remain strong which would of course support municipal valuations. Municipal bonds have outperformed Treasuries in the first seven months of 2006, and we expect it to continue as supply and demand characteristics remain attractive.

The views expressed in this report reflect those of the portfolio managers only through the report period as stated on the cover. These views are subject to change at any time, based on market and other conditions and should not be construed as a recommendation of any kind. The material may also include forward looking statements that involve risk and uncertainty, and there is no guarantee that any predictions will come to pass.

MZF Risks and Other Considerations

There can be no assurance that the Fund will achieve its investment objective. The value of the Fund will fluctuate with the value of the underlying securities. Historically, closed-end funds often trade at a discount to their net asset value. An investment in this Fund may not be suitable for investors who are, or as a result of this investment would become, subject to the federal alternative minimum tax because the securities in the Fund may pay interest that is subject to taxation under the federal alternative minimum tax. Special rules apply to corporate holders. Additionally, any capital gains dividends will be subject to capital gains taxes.

There can be no guarantee that hedging strategies will be employed or will be successful. The premium paid for entering into such hedging strategies will result in a reduction in the net asset value of the Funds and a subsequent reduction of income to the Fund. Any income generated from hedging transactions will not be exempt from income taxes.

Certain risks are associated with the leveraging of common stock. Both the net asset value and the market value of shares of common stock may be subject to higher volatility and a decline in value.

There are also specific risks associated with investing in municipal bonds. The secondary market for Municipal Bonds is less liquid than many other securities markets, which may adversely affect the Fund’s ability to sell its bonds at prices approximating those at which the Fund currently values them. The ability of municipal issuers to make timely payments of interest and principal may be diminished during general economic downturns. In addition, laws enacted in the future by Congress or state legislatures or referenda could extend the time for payment of principal and/or interest. In the event of bankruptcy of an issuer, the Fund could experience delays in collecting principal and interest.

There are also risks associated with investing in Auction Market Preferred Shares or AMPS. The AMPS are redeemable, in whole or in part, at the option of the Fund on any dividend payment date for the AMPS, and will be subject to mandatory redemption in certain circumstances. The AMPS will not be listed on an exchange. You may only buy or sell AMPS through an order placed at an auction with or through a broker-dealer that has entered into an agreement with the auction agent and the Fund or in a secondary market maintained by certain broker-dealers. These broker-dealers are not required to maintain this market, and it may not provide you with liquidity.

| | |

| | Annual Report | July 31, 2006 | 7 |

MZF | MBIA Capital/Claymore Managed Duration Investment Grade Municipal Fund

Fund Summary | As of July 31, 2006 (unaudited)

Fund Information

| | | | |

Symbol on New York Stock Exchange: | | | MZF | |

Initial Offering Date: | | | August 27, 2003 | |

Closing Market Price as of 07/31/06: | | $ | 12.29 | |

Net Asset Value as of 07/31/06: | | $ | 14.25 | |

Yield on Closing Market Price as of 07/31/06: | | | 4.59 | % |

Taxable Equivalent Yield on Closing Market Price as of 07/31/061: | | | 7.06 | % |

Current Monthly Distribution Per Common Share2: | | $ | 0.047 | |

Annualized Monthly Distribution Per Common Share: | | $ | 0.564 | |

Leverage as of 07/31/063: | | | 38 | % |

| 1 | Taxable equivalent yield is calculated assuming a 35% federal income tax bracket. |

| 2 | Monthly distribution is subject to change. |

| 3 | As a percentage of managed assets. |

Total Returns

| | | | | | |

(Inception 8/27/03) | | Market | | | NAV | |

One Year | | -1.60 | % | | 1.57 | % |

Since Inception – average annual | | -1.48 | % | | 4.81 | % |

Share Price & NAV Performance

State/Territory Allocation*

| * | As a percentage of long-term municipal bonds and notes. |

Portfolio Concentration*

| * | As a percentage of long-term municipal bonds and notes, preferred shares and swaptions. |

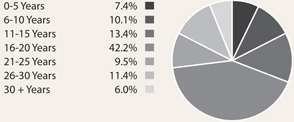

Maturity Breakdown*

| * | As a percentage of long-term municipal bonds and notes, preferred shares and swaptions. |

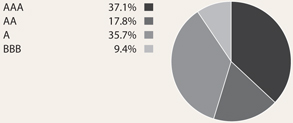

Credit Quality*

| * | As a percentage of long-term municipal bonds and notes and preferred shares. Based on Standard & Poor’s or other equivalent rating. |

| | |

8 | Annual Report | July 31, 2006 | | |

MZF | MBIA Capital/Claymore Managed Duration Investment Grade Municipal Fund

Portfolio of Investments | July 31, 2006

| | | | | | | | | | |

Rating (S&P)* | | Principal

Amount (000) | | Description | | Optional Call Provisions** | | Value |

| | | | | Municipal Bonds & Notes – 154.7% | | | | | |

| | | | | Alabama – 0.8% | | | | | |

BBB | | $ | 845 | | Courtland, AL Industrial Dev Brd | | | | | |

| | | | | Environ Imp Rev, AMT, Ser B, | | | | | |

| | | | | 6.25%, 08/01/25 | | 08/01/13 @ 100 | | $ | 914,983 |

| | | | | | | | | | |

| | | | |

| | | | | Arizona – 2.3% | | | | | |

Aaa | | | 2,500 | | Phoenix, AZ Civic Impt Corp Excise Tax Rev, | | | | | |

| | | | | 6.10%, 07/01/41 (FGIC)†† | | 07/01/15 @ 100 | | | 2,607,950 |

| | | | | | | | | | |

| | | | |

| | | | | California – 34.2% | | | | | |

A- | | | 4,000 | | California Dept of Water Res, | | | | | |

| | | | | Power Supply Rev, Ser A, | | | | | |

| | | | | 5.125%, 05/01/19 | | | | | |

| | | | | (Prerefunded @ 05/01/12)† | | 05/01/12 @ 101 | | | 4,318,240 |

| | | | |

A+ | | | 350 | | California Gen Oblig, | | | | | |

| | | | | 5.50%, 04/01/30 | | | | | |

| | | | | (Prerefunded @ 04/01/14)† | | 04/01/14 @ 100 | | | 387,002 |

| | | | |

A+ | | | 2,150 | | California Gen Oblig, | | | | | |

| | | | | 5.50%, 04/01/30 | | 04/01/14 @ 100 | | | 2,309,487 |

| | | | |

AAA | | | 4,000 | | California Infrastructure & Econ Dev Rev, | | | | | |

| | | | | Bay Area Toll Brdgs, Ser A, 5.00%, 07/01/26 | | | | | |

| | | | | (FGIC) (Escrowed to maturity) | | No call provision | | | 4,343,840 |

| | | | |

A | | | 5,000 | | California Public Works Brd | | | | | |

| | | | | Dept Mental Health Lease Rev, Ser A, | | | | | |

| | | | | 5.00%, 06/01/24 | | 06/01/14 @ 100 | | | 5,120,000 |

| | | | |

AA- | | | 3,500 | | California Statewide Cmntys Dev | | | | | |

| | | | | Auth Rev, Sutter Health, Ser A, | | | | | |

| | | | | 5.00%, 11/15/43 | | 11/15/15 @ 100 | | | 3,525,585 |

| | | | |

A+ | | | 6,000 | | California Various Purpose Gen Oblig, | | | | | |

| | | | | 5.125%, 11/01/24 | | 11/01/13 @ 100 | | | 6,232,980 |

| | | | |

A- | | | 2,500 | | Chula Vista, CA Ind Dev Rev, Ser B | | | | | |

| | | | | AMT, 5.50% 12/01/21 | | 06/02/14 @ 102 | | | 2,659,875 |

| | | | |

AAA | | | 2,750 | | Golden State Tobacco Settlement | | | | | |

| | | | | Rev, Ser B, 5.375%, 06/01/28 | | | | | |

| | | | | (Prerefunded @ 06/01/10)† | | 06/01/10 @ 100 | | | 2,905,815 |

| | | | |

AAA | | | 4,000 | | Port of Oakland, CA Rev, AMT, | | | | | |

| | | | | Ser L, 5.00%, 11/01/22 (FGIC) | | 11/01/12 @ 100 | | | 4,103,160 |

| | | | |

AAA | | | 2,500 | | San Diego, CA Unified School Dist, | | | | | |

| | | | | Ser D, 5.25%, 07/01/25 (FGIC) | | 07/01/12 @ 101 | | | 2,698,825 |

| | | | | | | | | | |

| | | | | | | | | | 38,604,809 |

| | | | | | | | | | |

| | | | |

| | | | | Colorado – 4.1% | | | | | |

AA | | | 4,500 | | Colorado Health Facs Auth Rev, | | | | | |

| | | | | 5.25%, 09/01/21 | | 09/01/11 @ 100 | | | 4,647,375 |

| | | | | | | | | | |

| | | | | District of Columbia – 1.8% | | | | | |

Aaa | | | 2,000 | | District of Columbia FHA Multi | | | | | |

| | | | | Henson Ridge-Rmkt, AMT, | | | | | |

| | | | | 5.10%, 06/01/37 (FHA) | | 06/01/15 @ 102 | | | 2,014,760 |

| | | | | | | | | | |

See notes to financial statements.

| | |

| | Annual Report | July 31, 2006 | 9 |

MZF | MBIA Capital/Claymore Managed Duration Investment Grade Municipal Fund | Portfolio of Investments continued

| | | | | | | | | | |

Rating

(S&P)* | | Principal

Amount (000) | | Description | | Optional Call Provisions** | | Value |

| | | | | Florida – 10.0% | | | | | |

A+ | | $ | 2,500 | | Highlands Co., FL Health Facs | | | | | |

| | | | | Auth Rev, Ser B, 5.25%, 11/15/23 | | 11/15/12 @ 100 | | $ | 2,576,625 |

A+ | | | 3,000 | | Highlands Co., FL Health Facs | | | | | |

| | | | | Auth Rev, Ser D, 5.875%, 11/15/29 | | 11/15/13 @ 100 | | | 3,211,230 |

AAA | | | 2,500 | | Miami-Dade Co., FL Aviation Rev, AMT, | | | | | |

| | | | | 6.07%, 10/01/38 (CIFG)†† | | 10/01/15 @ 100 | | | 2,576,800 |

AA- | | | 2,750 | | South Broward Co., FL Hosp Dist | | | | | |

| | | | | Rev, 5.60%, 05/01/27 | | 05/01/12 @ 101 | | | 2,942,885 |

| | | | | | | | | | |

| | | | | | | | | | 11,307,540 |

| | | | | | | | | | |

| | | | | Illinois – 7.4% | | | | | |

AAA | | | 3,000 | | Chicago IL, O’Hare Intl Airport Rev, | | | | | |

| | | | | 6.10%, 01/01/33 (FGIC)†† | | 01/01/16 @100 | | | 3,149,160 |

A2 | | | 3,000 | | Illinois Dev Fin Auth Hosp Rev, | | | | | |

| | | | | 5.65%, 11/15/24 | | | | | |

| | | | | (Prerefunded @ 11/15/09)† | | 11/15/09 @ 101 | | | 3,187,530 |

AA | | | 2,000 | | Illinois Hsg Dev Auth Homeowner Mtg, | | | | | |

| | | | | AMT, Ser A-2, 5.00%, 08/01/36 | | 02/01/16 @ 100 | | | 1,996,900 |

| | | | | | | | | | |

| | | | | | | | | | 8,333,590 |

| | | | | | | | | | |

| | | | | Louisiana – 0.9% | | | | | |

BBB | | | 1,000 | | De Soto Parish, LA Environ Imp | | | | | |

| | | | | Rev, AMT, Ser A, 5.85%, 11/01/27 | | 11/01/13 @ 100 | | | 1,036,290 |

| | | | | | | | | | |

| | | | | Massachusetts – 4.8% | | | | | |

AAA | | | 5,000 | | Massachusetts Special Oblig | | | | | |

| | | | | Dedicated Tax Rev, 5.25%, 01/01/26 | | | | | |

| | | | | (Prerefunded 01/01/14) (FGIC) † | | 01/01/14 @ 100 | | | 5,400,600 |

| | | | | | | | | | |

| | | | | Michigan – 1.8% | | | | | |

BBB+ | | | 2,000 | | Michigan Strategic Fund Ltd Oblig | | | | | |

| | | | | Rev Ref, Ser C, 5.45%, 09/01/29 | | 09/01/11 @ 100 | | | 2,088,080 |

| | | | | | | | | | |

| | | | | Missouri – 5.7% | | | | | |

AAA | | | 6,000 | | Missouri Health & Educ Facs Auth | | | | | |

| | | | | Rev, Ser A, 5.25%, 06/01/28 | | | | | |

| | | | | (Prerefunded @ 06/01/11) (AMBAC) † | | 06/01/11 @ 101 | | | 6,432,900 |

| | | | | | | | | | |

| | | | | Nevada – 5.0% | | | | | |

A- | | | 5,410 | | Henderson, NV Health Care Fac Rev, | | | | | |

| | | | | Ser A, 5.625%, 07/01/24 | | 07/01/14 @ 100 | | | 5,704,304 |

| | | | | | | | | | |

| | | | | New York – 34.0% | | | | | |

A- | | | 4,600 | | Long Island, NY Power Auth Rev, Ser A, | | | | | |

| | | | | 5.10%, 09/01/29 | | 09/01/14 @ 100 | | | 4,753,548 |

| | | | |

AA- | | | 4,000 | | Metropolitan Trans Auth Rev, Ser A, | | | | | |

| | | | | 5.125%, 01/01/24 | | 07/01/12 @ 100 | | | 4,143,040 |

| | | | |

A+ | | | 1,500 | | New York Dorm Auth Lease Rev, Ser A, | | | | | |

| | | | | 5.375%, 05/15/22 (Prerefunded 05/15/13)† | | 05/15/13 @ 100 | | | 1,632,525 |

| | | | |

A+ | | | 2,500 | | New York Dorm Auth Lease Rev, Ser A, | | | | | |

| | | | | 5.375%, 05/15/23 (Prerefunded 05/15/13)† | | 05/15/13 @ 100 | | | 2,720,875 |

See notes to financial statements.

| | |

10 | Annual Report | July 31, 2006 | | |

MZF | MBIA Capital/Claymore Managed Duration Investment Grade Municipal Fund | Portfolio of Investments continued

| | | | | | | | | | |

Rating (S&P)* | | Principal

Amount (000) | | Description | | Optional Call Provisions** | | Value |

A3 | | $ | 1,500 | | New York Dorm Auth Rev, North Shore | | | | | |

| | | | | Long Island Jewish Group, | | | | | |

| | | | | 5.375%, 05/01/23 | | 05/01/13 @ 100 | | $ | 1,563,990 |

| | | | |

AA- | | | 5,000 | | New York, NY Gen Oblig, Ser J, | | | | | |

| | | | | 5.00%, 05/15/23 | | 05/15/14 @ 100 | | | 5,145,750 |

| | | | |

A+ | | | 3,650 | | New York Muni Bond Bank Agy Special | | | | | |

| | | | | School Purpose Rev, Ser C, | | | | | |

| | | | | 5.25%, 12/01/22 | | 06/01/13 @ 100 | | | 3,837,610 |

| | | | |

AA- | | | 4,000 | | New York Tobacco Settlement Funding | | | | | |

| | | | | Corp, Ser A1, 5.50%, 06/01/19 | | 06/01/13 @ 100 | | | 4,288,480 |

| | | | |

AAA | | | 5,000 | | Port Auth NY and NJ - Cons, 127th Rev, | | | | | |

| | | | | AMT, 5.20%, 12/15/26 (AMBAC) | | 06/15/12 @ 101 | | | 5,222,200 |

| | | | |

A | | | 5,000 | | Suffolk Co, NY Ind Dev Agy Rev, AMT, | | | | | |

| | | | | 5.25%, 06/01/27 | | 06/01/13 @ 100 | | | 5,132,250 |

| | | | | | | | | | |

| | | | | | | | | | 38,440,268 |

| | | | | | | | | | |

| | | | | North Carolina – 3.6% | | | | | |

BBB | | | 1,000 | | North Carolina Eastern Muni Power Agy | | | | | |

| | | | | Sys Rev Ref, Ser D, 5.125%, 01/01/23 | | 01/01/13 @ 100 | | | 1,021,030 |

| | | | |

BBB | | | 1,000 | | North Carolina Eastern Muni Power Agy | | | | | |

| | | | | Sys Rev Ref, Ser D, 5.125%, 01/01/26 | | 01/01/13 @ 100 | | | 1,017,160 |

| | | | |

AAA | | | 1,925 | | North Carolina Housing Fin Agy Rev, AMT, | | | | | |

| | | | | Ser 14A, 5.35%, 01/01/22 (AMBAC) | | 07/01/11 @ 100 | | | 1,974,126 |

| | | | | | | | | | |

| | | | | | | | | | 4,012,316 |

| | | | | | | | | | |

| | | | | Ohio – 9.5% | | | | | |

A+ | | | 3,000 | | Cuyahoga Co., OH Rev Ref, Ser A, | | | | | |

| | | | | 6.00%, 01/01/20 | | 07/01/13 @ 100 | | | 3,288,840 |

| | | | |

AA- | | | 5,000 | | Lorain Co., OH Hosp Rev Ref, Ser A, | | | | | |

| | | | | 5.25%, 10/01/33 | | 10/01/11 @ 101 | | | 5,163,750 |

| | | | |

Aaa | | | 2,250 | | Toledo, OH City School Dist Facs Imp | | | | | |

| | | | | Gen Oblig, 5.00%, 12/01/25 (FSA) | | 12/01/13 @ 100 | | | 2,332,215 |

| | | | | | | | | | |

| | | | | | | | | | 10,784,805 |

| | | | | | | | | | |

| | | | | Pennsylvania – 3.9% | | | | | |

BBB | | | 2,340 | | Pennsylvania Higher Education Facs Auth | | | | | |

| | | | | Rev, 5.25%, 05/01/23 | | 05/01/13 @ 100 | | | 2,403,952 |

| | | | |

BBB+ | | | 2,000 | | Pennsylvania State Higher Education, | | | | | |

| | | | | 5.00%, 07/15/39 | | 07/15/15 @ 100 | | | 2,002,800 |

| | | | | | | | | | |

| | | | | | | | | | 4,406,752 |

| | | | | | | | | | |

| | | | | Puerto Rico – 6.1% | | | | | |

AAA | | | 1,500 | | Puerto Rico Hwy & Trans Auth Rev, | | | | | |

| | | | | Ser J, 5.50%, 07/01/24 | | | | | |

| | | | | (Prerefunded @ 07/01/14)† | | 07/01/14 @ 100 | | | 1,657,665 |

| | | | |

BBB | | | 5,000 | | Puerto Rico Public Bldgs Auth Rev, | | | | | |

| | | | | Ser I, 5.50%, 07/01/25 | | 07/01/14 @ 100 | | | 5,271,650 |

| | | | | | | | | | |

| | | | | | | | | | 6,929,315 |

| | | | | | | | | | |

See notes to financial statements.

| | |

| | Annual Report | July 31, 2006 | 11 |

MZF | MBIA Capital/Claymore Managed Duration Investment Grade Municipal Fund | Portfolio of Investments continued

| | | | | | | | | | |

Rating (S&P)* | | Principal

Amount (000) | | Description | | Optional Call Provisions** | | Value |

| | | | | South Carolina – 3.2% | | | | | |

AAA | | $ | 2,500 | | Florence Co., SC Hosp Rev, Ser A, | | | | | |

| | | | | 5.25%, 11/01/27 (FSA) | | 11/01/14 @ 100 | | $ | 2,640,125 |

BBB | | | 1,000 | | Georgetown Co., SC Environ Imp Rev, | | | | | |

| | | | | AMT, Ser A, 5.30%, 03/01/28 | | 03/01/14 @ 100 | | | 1,001,190 |

| | | | | | | | | | |

| | | | | | | | | | 3,641,315 |

| | | | | | | | | | |

| | | | | South Dakota – 5.5% | | | | | |

AAA | | | 5,000 | | South Dakota Hsg Dev Auth, Ser K, AMT, | | | | | |

| | | | | 5.05%, 05/01/36 | | 11/01/15 @ 100 | | | 5,019,750 |

A+ | | | 1,200 | | South Dakota St Hlth & Edl Fac, Ser A | | | | | |

| | | | | 5.25%, 11/01/34 | | 11/01/14 @ 100 | | | 1,230,564 |

| | | | | | | | | | |

| | | | | | | | | | 6,250,314 |

| | | | | | | | | | |

| | | | | Texas – 5.5% | | | | | |

Aaa | | | 2,000 | | Bexar Co., TX Housing Fin, AMT, | | | | | |

| | | | | 5.20%, 10/20/34 (GNMA/FHA) | | 10/20/14 @ 100 | | | 2,027,860 |

AAA | | | 4,000 | | Eagle Mtn & Saginaw, TX Indep School | | | | | |

| | | | | Dist, Ser A, 5.25%, 08/15/23 (PSF) | | 08/15/13 @ 100 | | | 4,230,960 |

| | | | | | | | | | |

| | | | | | | | | | 6,258,820 |

| | | | | | | | | | |

| | | | | West Virginia – 4.6% | | | | | |

AAA | | | 5,000 | | West Virginia Housing Dev Fund Rev, | | | | | |

| | | | | Ser D, 5.20%, 11/01/21 | | 05/01/11 @ 100 | | | 5,143,350 |

| | | | | | | | | | |

| | | | | Total Municipal Bonds & Notes – 154.7% | | | |

| | | | | (Cost $167,597,436) | | | | | 174,960,436 |

| | | | | | | | | | |

Rating (Moody) | | Redemption

Value (000) | | Description | | Value |

| | | | | Preferred Shares – 3.7% | | | | | |

A3 | | | 2,000 | | Charter Mac Equity Trust, AMT, Ser A-4-1, | | | |

| | | | | 5.75%, 04/30/15 (remarketing), 144A | | | 2,113,700 |

A3 | | | 2,000 | | GMAC Municipal Mortgage Trust, AMT, | | | |

| | | | | Ser A1-3, 5.30%, 10/31/39, | | | |

| | | | | (10/31/19 remarketing), 144A | | | 2,057,440 |

| | | | | | | | | | |

| | | | | Total Preferred Shares | | | |

| | | | | (Cost - $4,000,008) | | | 4,171,140 |

| | | | | | | | | | |

| | | | |

Counterparty | | Notional

Amount (000) | | Description | | Expiration Date | | Value |

| | | | | Swaptions(1) – 0.7% | | | | | |

Goldman Sachs | | | 85,000 | | Option on a pay fixed/receive floating rate 20 year interest rate swap (pay fixed rate of 5.20% and receive BMA rate with a weekly reset) | | 09/03/08 | | | 656,010 |

Goldman Sachs | | | 7,000 | | Option on a pay fixed/receive floating rate 20 year interest rate swap (pay fixed rate of 6.50% and receive LIBOR rate with a weekly reset) | | 09/03/08 | | | 125,230 |

| | | | | | | | | | |

| | | | | Total Swaptions | | | | | |

| | | | | (Cost $5,402,500) | | | | | 781,240 |

| | | | | | | | | | |

See notes to financial statements.

| | |

12 | Annual Report | July 31, 2006 | | |

MZF | MBIA Capital/Claymore Managed Duration Investment Grade Municipal Fund | Portfolio of Investments continued

| | | | | | | | | | | |

Rating (S&P)* | | Principal

Amount (000) | | Description | | Optional Call Provisions** | | Value | |

| | | | | Short-Term Investments – 0.9% | | | | | | |

| | | | | Alabama – 0.6 % | | | | | | |

AAA | | $ | 700 | | Mobile Co., AL, Indl Dev Auth Pollution Ctl Rev, | | | | | | |

| | | | | VRDN, 3.57%, 07/15/32(2) | | No call provision | | $ | 700,000 | |

| | | | | | | | | | | |

| | | | | Illinois – 0.1% | | | | | | |

AAA | | | 125 | | Will Co., IL Exempt Facs Rev, AMT, | | | | | | |

| | | | | VRDN, 3.63%, 04/01/26(2) | | No call provision | | | 125,000 | |

| | | | | | | | | | | |

| | | | | Missouri – 0.2% | | | | | | |

AA | | | 200 | | Curators University of MO, Sys Facs Rev, | | | | | | |

| | | | | Ser B, VRDN, 3.67%, 11/01/35(2) | | No call provision | | | 200,000 | |

| | | | | | | | | | | |

| | | | | Total Short-Term Investments | | | | | | |

| | | | | (Cost - $1,025,000) | | | | | 1,025,000 | |

| | | | | | | | | | | |

| | | | | Total Investments – 160.0% | | | | | | |

| | | | | (Cost $178,024,944) | | | | | 180,937,816 | |

| | | | | | | | | | | |

| | | | | Other assets in excess of liabilities – 1.4% | | | | | 1,556,018 | |

| | | | | Preferred Shares, at redemption value – (-61.4% of Net Assets Applicable to Common Shareholders or -38.4% of Total Investments) | | | | | (69,450,000 | ) |

| | | | | | | | | | | |

| | | | | Net Assets Applicable to Common Shareholders – 100.0%(3) | | | | $ | 113,043,834 | |

| | | | | | | | | | | |

| * | Unaudited – For securities not rated by Standard & Poor’s Rating Group, the rating by Moody’s Investor Services, Inc. or Fitch Ratings is provided. |

| ** | Unaudited – Date and price of the earliest optional call or redemption provision. There may be other call provisions at varying prices at later dates. |

| † | This bond is prerefunded. U.S. government or U.S. government agency securities, held in escrow, are used to pay interest on this security, as well as to retire the bond in full at the date and price indicated under the Optional Call Provisions. |

| †† | Inverse Floating Rate Security – the coupon rate changes inversely with interest rates. The rate shown is as of July 31, 2006. |

| (1) | Non-income producing securities. |

| (2) | Security has a maturity of more than one year, but has variable rate and demand features which qualify it as a short-term security. The rate shown is as of July 31, 2006. |

| (3) | Portfolio percentages are calculated based on net assets applicable to common shareholders. |

Glossary:

| | |

| |

| AMBAC– | | Insured by Ambac Assurance Corporation |

| |

| AMT– | | Alternative Minimum Tax |

| |

| BMA– | | Bond Market Association |

| |

| CIFG– | | Insured by CIFG Assurance NA |

| |

| FGIC– | | Insured by Financial Guaranty Insurance Co. |

| |

| FHA– | | Guaranteed by Federal Housing Administration |

| |

| FSA– | | Insured by Financial Security Assurance, Inc. |

| |

| GNMA– | | Guaranteed by Ginnie Mae |

| |

| LIBOR– | | London Inter-Bank Offered Rate |

| |

| PSF– | | Guaranteed by Texas Permanent School Fund |

| |

| VRDN– | | Variable rate demand notes are instruments whose interest rates change on a specified date (such as coupon date or interest payment date) and/or whose interest rates vary with changes in a designated base rate (such as the prime interest rate). The rate shown is as of July 31, 2006. |

| |

| 144A– | | Security exempt from registration pursuant to Rule 144A under the Securities Act of 1933. The securities may be resold in transactions exempt from registration, normally to qualified institutional buyers. At July 31, 2006 these securities amounted to $4,171,140 which represents 3.7% of net assets applicable to common shareholders. |

See notes to financial statements.

| | |

| | Annual Report | July 31, 2006 | 13 |

MZF | MBIA Capital/Claymore Managed Duration Investment Grade Municipal Fund

Statement of Assets and Liabilities | July 31, 2006

| | | | |

Assets | | | | |

Investments, at value (cost $178,024,944) | | $ | 180,937,816 | |

Cash | | | 81,256 | |

Interest receivable | | | 1,862,459 | |

Other assets | | | 37,646 | |

| | | | |

Total assets | | | 182,919,177 | |

| | | | |

Liabilities | | | | |

Dividends payable - preferred shareholders | | | 65,311 | |

Investment advisory fee payable | | | 40,459 | |

Servicing agent fee payable | | | 26,947 | |

Administration fee payable | | | 3,849 | |

Accrued expenses and other liabilities | | | 288,777 | |

| | | | |

Total liabilities | | | 425,343 | |

| | | | |

Preferred Shares, at redemption value | | | | |

$.001 par value per share; 2,778 Auction Market Preferred Shares authorized, issued and outstanding at $25,000 per share liquidation preference | | | 69,450,000 | |

| | | | |

Net Assets Applicable to Common Shareholders | | $ | 113,043,834 | |

| | | | |

Composition of Net Assets Applicable to Common Shareholders | | | | |

Common stock, $.001 par value per share; unlimited number of shares authorized, 7,935,591 shares issued and outstanding | | $ | 7,936 | |

Additional paid-in capital | | | 112,471,279 | |

Net unrealized appreciation on investments and swaptions | | | 2,912,872 | |

Accumulated undistributed net investment income | | | 181,454 | |

Accumulated net realized loss on investments and swaptions | | | (2,529,707 | ) |

| | | | |

Net Assets Applicable to Common Shareholders | | $ | 113,043,834 | |

| | | | |

Net Asset Value Applicable to Common Shareholders (based on 7,935,591 common shares outstanding) | | $ | 14.25 | |

| | | | |

See notes to financial statements.

| | |

14 | Annual Report | July 31, 2006 | | |

MZF | MBIA Capital/Claymore Managed Duration Investment Grade Municipal Fund

Statement of Operations | For the year ended July 31, 2006

| | | | | | | |

Investment Income | | | | | | | |

Interest | | | | | $ | 8,977,957 | |

| | | | | | | |

Expenses | | | | | | | |

Investment advisory fee | | $ | 717,052 | | | | |

Servicing agent fee | | | 478,035 | | | | |

Professional fees | | | 299,317 | | | | |

Auction agent fees - preferred shares | | | 224,769 | | | | |

Trustees’ fees and expenses | | | 89,720 | | | | |

Printing expenses | | | 74,840 | | | | |

Fund accounting | | | 64,938 | | | | |

Administrative fee | | | 50,561 | | | | |

Transfer agent fee | | | 36,772 | | | | |

Insurance | | | 30,615 | | | | |

NYSE listing fee | | | 23,490 | | | | |

Custodian fee | | | 20,083 | | | | |

Line of credit fee | | | 3,598 | | | | |

Other | | | 46,356 | | | | |

| | | | | | | |

Total expenses | | | | | | 2,160,146 | |

Investment advisory fees waived | | | | | | (174,045 | ) |

Servicing agent fees waived | | | | | | (116,030 | ) |

| | | | | | | |

Net expenses | | | | | | 1,870,071 | |

| | | | | | | |

Net investment income | | | | | | 7,107,886 | |

| | | | | | | |

Realized and Unrealized Gain (Loss) on Investments | | | | | | | |

Net realized gain (loss) on: | | | | | | | |

Investments | | | | | | 565,843 | |

Swaptions | | | | | | (894,000 | ) |

Net change in unrealized appreciation (depreciation) on: | | | | | | | |

Investments | | | | | | (3,579,541 | ) |

Swaptions | | | | | | 626,240 | |

| | | | | | | |

Net realized and unrealized loss on investments | | | | | | (3,281,458 | ) |

| | | | | | | |

Distributions to Auction Market Preferred Shareholders from | | | | | | | |

Net investment income | | | | | | (2,103,570 | ) |

| | | | | | | |

Net Increase in Net Assets Applicable to Common Shareholders Resulting from Operations | | | | | $ | 1,722,858 | |

| | | | | | | |

See notes to financial statements.

| | |

| | Annual Report | July 31, 2006 | 15 |

MZF l MBIA Capital/Claymore Managed Duration Investment Grade Municipal Fund

Statements of Changes in Net Assets

| | | | | | | | |

| | | For the

Year Ended

July 31, 2006 | | | For the

Year Ended

July 31, 2005 | |

Increase in Net Assets Applicable to Common Shareholders Resulting from Operations: | | | | | | | | |

Net investment income | | $ | 7,107,886 | | | $ | 7,280,738 | |

Net realized loss on investments and swaptions | | | (328,157 | ) | | | (295,158 | ) |

Net change in unrealized appreciation (depreciation) on investments and swaptions | | | (2,953,301 | ) | | | 7,212,061 | |

Distributions to auction market preferred shareholders from net investment income | | | (2,103,570 | ) | | | (1,241,239 | ) |

| | | | | | | | |

Net increase in net assets applicable to common shareholders resulting from operations | | | 1,722,858 | | | | 12,956,402 | |

| | | | | | | | |

Distributions to common shareholders from | | | | | | | | |

Net investment income | | | (5,189,877 | ) | | | (6,221,503 | ) |

| | | | | | | | |

Total change in net assets applicable to common shareholders | | | (3,467,019 | ) | | | 6,734,899 | |

| | |

Net assets applicable to common shareholders: | | | | | | | | |

Beginning of period | | | 116,510,853 | | | | 109,775,954 | |

| | | | | | | | |

End of period (including undistributed net investment income of $181,454 and $367,015, respectively.) | | $ | 113,043,834 | | | $ | 116,510,853 | |

| | | | | | | | |

See notes to financial statements.

| | |

16 | Annual Report | July 31, 2006 | | |

MZF | MBIA Capital/Claymore Managed Duration Investment Grade Municipal Fund

Financial Highlights

| | | | | | | | | | | | |

Per share operating performance for one common share outstanding throughout each period | | For the

Year Ended

July 31, 2006 | | | For the

Year Ended

July 31, 2005 | | | For the Period

August 27, 2003*

through

July 31, 2004 | |

Net asset value, beginning of period | | $ | 14.68 | | | $ | 13.83 | | | $ | 14.33 | ** |

| | | | | | | | | | | | |

Investment operations | | | | | | | | | | | | |

Net investment income | | | 0.90 | | | | 0.92 | | | | 0.78 | |

Net realized and unrealized gain on investments and swaptions transactions | | | (0.41 | ) | | | 0.87 | | | | (0.42 | ) |

Distributions to preferred shareholders from net investment income

(common share equivalent basis) | | | (0.27 | ) | | | (0.16 | ) | | | (0.08 | ) |

| | | | | | | | | | | | |

Total from investment operations | | | 0.22 | | | | 1.63 | | | | 0.28 | |

| | | | | | | | | | | | |

Distributions to common shareholders from net investment income | | | (0.65 | ) | | | (0.78 | ) | | | (0.63 | ) |

| | | | | | | | | | | | |

Common share offering costs charged to paid-in-capital in excess of par | | | — | | | | — | | | | (0.03 | ) |

Preferred shares offering costs/underwriting discount charged to paid-in-capital in excess of par | | | — | | | | — | | | | (0.12 | ) |

| | | | | | | | | | | | |

Total capital share transactions | | | — | | | | — | | | | (0.15 | ) |

| | | | | | | | | | | | |

Net asset value, end of period | | $ | 14.25 | | | $ | 14.68 | | | $ | 13.83 | |

| | | | | | | | | | | | |

Market value, end of period | | $ | 12.29 | | | $ | 13.15 | | | $ | 13.11 | |

| | | | | | | | | | | | |

Total investment return(a) | | | | | | | | | | | | |

Net asset value | | | 1.57 | % | | | 12.03 | % | | | 1.11 | % |

Market value | | | -1.60 | % | | | 6.47 | % | | | -8.62 | % |

Ratios and supplemental data | | | | | | | | | | | | |

Net assets end of period (thousands) | | $ | 113,044 | | | $ | 116,511 | | | $ | 109,776 | |

Ratio of expenses to average net assets (net of fee waivers)(c) | | | 1.63 | % | | | 1.53 | % | | | 1.34 | %(b) |

Ratio of expenses to average net assets (excluding fee waivers)(c) | | | 1.89 | % | | | 1.77 | % | | | 1.56 | %(b) |

Ratio of net investment income(loss) to average net assets(c) | | | 6.21 | % | | | 6.34 | % | | | 5.85 | %(b) |

Portfolio turnover | | | 21 | % | | | 15 | % | | | 129 | % |

Preferred shares, at redemption value ($25,000 per share liquidation preference)(thousands) | | $ | 69,450 | | | $ | 69,450 | | | $ | 69,450 | |

Preferred shares asset coverage per share | | $ | 65,693 | | | $ | 66,941 | | | $ | 64,516 | |

| * | Commencement of investment operations. |

| ** | Initial public offering price of $15.00 per share less underwriting discount of $0.675 per share. |

| (a) | Total investment return is calculated assuming a purchase of a common share at the beginning of the period and a sale on the last day of the period reported either at net asset value (NAV) or market price per share. Dividends and distributions are assumed to be reinvested at NAV for returns at NAV or in accordance with the Fund’s dividend reinvestment plan for returns at market value. Total investment return does not reflect brokerage commissions. A return calculated for a period of less than one year is not annualized. |

| (c) | Calculated on the basis of income and expenses applicable to both common and preferred shares relative to average net assets of common shareholders. |

See notes to financial statements.

| | |

| | Annual Report | July 31, 2006 | 17 |

MZF | MBIA Capital/Claymore Managed Duration Investment Grade Municipal Fund

Notes to Financial Statements

Note 1 – Organization & Accounting Policies:

The MBIA Capital/Claymore Managed Duration Investment Grade Municipal Fund (the “Fund”) was organized as a Delaware statutory trust on May 20, 2003. The Fund is registered as a diversified, closed-end management investment company under the Investment Company Act of 1940, as amended. The Fund’s investment objective is to provide its common shareholders with high current income exempt from regular federal income tax while seeking to protect the value of the Fund’s assets during periods of interest rate volatility. Prior to commencing operations on August 27, 2003, the Fund had no operations other than matters relating to its organization and registration and the sale and issuance of 6,981 common shares of beneficial interest to MBIA Capital Management Corp. The following is a summary of significant accounting policies followed by the Fund.

Securities Valuation: The municipal bonds in which the Fund invests are traded primarily in the over-the-counter markets. In determining net asset value, the Fund uses the valuations of portfolio securities furnished by a pricing service approved by the Board of Trustees. The pricing service typically values portfolio securities at the bid price or the yield equivalent when quotations are readily available. Municipal bonds for which quotations are not readily available are valued at fair market value on a consistent basis as determined by the pricing service using a matrix system to determine valuations. The procedures of the pricing service and its valuations are reviewed by the officers of the Fund under the general supervision of the Board of Trustees. Positions in futures contracts, interest rate swaps and options on interest rate swaps (“swaptions”) are valued at closing prices for such contracts established by the exchange or dealer market on which they are traded, or if market quotations are not readily available, are valued at fair value on a consistent basis using methods approved in good faith by the Board of Trustees.

Securities Transactions and Investment Income: Investment transactions are accounted for on the trade date. Realized gains and losses on investments are determined on the identified cost basis. Interest income and expenses are accrued daily. All discounts/premiums are accreted/amortized for financial reporting purposes as required.

Swaptions: The Fund may engage in options transactions on interest rate swap agreements, commonly referred to as swaptions. A swaption is an agreement between two parties where one party purchases the right from the other party to enter into an interest rate swap at a specified date and for a specified “fixed rate” yield (or “exercise” yield). In a pay-fixed swaption, the holder of the swaption has the right to enter into an interest rate swap as a payer of fixed rate interest and receiver of variable rate interest, while the writer of the swaption has the obligation to enter into the other side of the interest rate swap. In a receive-fixed swaption, the holder of the swaption has the right to enter into an interest rate swap as a receiver of fixed rate interest and a payer of variable rate interest, while the writer has the obligation to enter into the opposite side of the interest rate swap. The Fund will enter into such transactions to attempt to hedge some or all of its interest rate exposure in its holdings of municipal bonds. The Fund generally purchases pay-fixed swaptions. Upon the purchase of these pay-fixed swaptions by the Fund, the total purchase price paid was recorded as an investment. The market valuation is determined as set forth in the preceding securities valuation paragraph. When the pay-fixed swaptions are exercised, the Fund has the right to enter into an interest rate swap as a payer of fixed rate interest and receiver of variable rate interest. When the pay-fixed swaptions reach their scheduled expiration dates, the Fund will record a gain or loss depending on the difference between the purchase price and the value of the swaptions on their exercise date.

Dividends and Distributions: The Fund declares on a quarterly basis and pays on a monthly basis dividends from net investment income to common shareholders. Distributions of net realized capital gains, if any, will be paid at least annually. Dividends and distributions to shareholders are recorded on the ex-dividend date. Dividends and distributions to preferred shareholders are accrued and determined as described in Note 5.

Use of Estimates: The preparation of financial statements in accordance with U.S. generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts and disclosures in the financial statements. Actual results could differ from those estimates.

Note 2 – Agreements:

Pursuant to an Investment Advisory Agreement (the “Advisory Agreement”) between MBIA Capital Management Corp. (the “Adviser”) and the Fund, the Adviser is responsible for the daily management of the Fund’s portfolio, which includes buying and selling securities for the Fund, as well as investment research, subject to the direction of the Fund’s Board of Trustees. The Adviser is a subsidiary of MBIA Asset Management, LLC which, in turn, is a wholly-owned subsidiary of MBIA, Inc. The Advisory Agreement provides that the Fund shall pay to the Adviser a monthly fee for its services at the annual rate of 0.39% of the sum of the Fund’s average daily net assets (including assets acquired from the sale of any preferred shares), plus the proceeds of any outstanding borrowings used for financial leverage (in total, the “Managed Assets”). The Adviser contractually agreed to waive a portion of the management fees it is entitled to receive from the Fund at the annual rate of 0.09% of the Fund’s average daily Managed Assets from the commencement of the Fund’s operations through September 1, 2008 and at the annual rate of 0.042% thereafter through September 1, 2009. Effective June 16, 2006, the Adviser voluntarily agreed to waive an additional 0.0375% of advisory fees. This waiver is voluntary in nature and can be discontinued at the Adviser’s discretion.

Pursuant to a Servicing Agreement, Claymore Securities, Inc. (the “Servicing Agent”) acts as servicing agent to the Fund. The Servicing Agent receives an annual fee from the Fund, payable monthly in arrears, in an amount equal to 0.26% of the average daily value of the Fund’s Managed Assets. The Servicing Agent contractually agreed to waive a portion of the servicing fee it is entitled to receive from the Fund at the annual rate of 0.06% of the average daily value of the Fund’s Managed Assets from the commencement of the Fund’s operations through September 1, 2008 and at the annual rate of 0.028% thereafter through September 1, 2009. Effective June 16, 2006, the Servicing Agent voluntarily agreed to waive an additional 0.025% of servicing fees. This waiver is voluntary in nature and can be discontinued at the Servicing Agent’s discretion.

Under a separate Fund Administration agreement, Claymore Advisors, LLC provides Fund Administration services to the Fund. For the year ended July 31, 2006, the Fund recognized expenses of approximately $50,600 for these services.

The Bank of New York (“BNY”) acts as the Fund’s custodian, accounting agent and transfer agent. As custodian, BNY is responsible for the custody of the Fund’s assets. As accounting agent, BNY is responsible for maintaining the books and records of the Fund’s securities and cash. As transfer agent, BNY is responsible for performing transfer agency services for the Fund.

Certain officers and/or trustees of the Fund are officers and/or directors of the Adviser and the Servicing Agent.

Note 3 – Investment Transactions:

Purchases and sales of investment securities, excluding short-term investments, for the year ended July 31, 2006, aggregated $37,403,610 and $37,438,298, respectively.

| | |

18 | Annual Report | July 31, 2006 | | |

MZF | MBIA Capital/Claymore Managed Duration Investment Grade Municipal Fund | Notes to Financial Statements continued

Note 4 – Federal Income Taxes:

The Fund intends to comply with the requirements of Subchapter M of the Internal Revenue Code of 1986, as amended, applicable to regulated investment companies. Accordingly, no provision for U.S. federal income taxes is required. In addition, by distributing substantially all of its ordinary income and long-term capital gains, if any, during each calendar year, the Fund intends not to be subject to U.S. federal excise tax.

Information on the tax components of investments as of July 31, 2006 is as follows:

| | | | | | | | | | |

Cost of Investments for Tax Purposes | | Gross Tax

Unrealized

Appreciation | | Gross Tax

Unrealized

Depreciation | | | Net Tax

Unrealized

Appreciation

on Investments |

$178,076,342 | | $ | 7,677,216 | | $ | (4,815,742 | ) | | $ | 2,861,474 |

The difference between book and tax basis cost of investments is due to book/tax differences on the recognition of partnership income.

As of July 31, 2006, the components of accumulated earnings/(losses) (excluding paid-in capital) on a tax basis were as follows:

| | | | | | | | | | |

| | | Undistributed

Tax-Exempt

Income | | Accumulated

Capital and

Other Losses | | | Unrealized

Appreciation/

(Depreciation) |

2006 | | $ | 295,438 | | $ | (2,526,982 | ) | | $ | 2,861,474 |

The cumulative timing differences under tax basis accumulated capital loss is due to post-October losses.

As of July 31, 2006, the Fund had a capital loss carryforward of $2,497,591 available to offset possible future capital gains. The capital loss carryforward is set to expire as follows: $8,249 on July 31, 2012, $1,863,882 on July 31, 2013 and $625,460 on July 31, 2014. Under the current tax law, capital losses realized after October 31 may be deferred and treated as occurring on the first day of the following fiscal year. For the period ended July 31, 2006, the Fund will elect to defer losses occurring between November 1, 2005 and July 31, 2006 in the amount of $29,391.

Distributions paid to shareholders during the tax years ended July 31, 2006 and 2005, were characterized as follows for tax purposes:

| | | | | | | | | | | | |

| | | Tax-exempt

income | | Ordinary

income | | Long-term

capital gain | | Total

distributions |

2006 | | $ | 7,289,998 | | $ | 3,449 | | $ | — | | $ | 7,293,447 |

2005 | | $ | 7,462,087 | | $ | 655 | | $ | — | | $ | 7,462,742 |

Note 5 – Capital:

There are an unlimited number of $.001 par value common shares of beneficial interest authorized and 7,935,591 common shares outstanding at July 31, 2006, of which the Adviser owned 6,981 shares. There were no transactions in common shares for the years ended July 31, 2006 or 2005, respectively.

On October 27, 2003, the Fund issued 1,389 shares of Auction Market Preferred Shares, Series M7 and 1,389 shares of Auction Market Preferred Shares, Series W28. The preferred shares have a liquidation value of $25,000 per share plus any accumulated unpaid dividends. As of July 31, 2006, the Fund had 1,389 shares each of Auction Market Preferred Shares, Series M7 and W28, outstanding.

Dividends on the preferred shares are cumulative at a rate that is set by auction procedures. The dividend rate range on the preferred shares of the Fund for the year ended July 31, 2006, were as follows:

| | | | | | | | | | | |

Series | | Low | | | High | | | At 7/31/06 | | | Next Auction Date |

M7 | | 2.65 | % | | 3.75 | % | | 3.55 | % | | 8/07/06 |

W28 | | 2.40 | % | | 3.78 | % | | 3.60 | % | | 8/16/06 |

The Fund is subject to certain limitations and restrictions while preferred shares are outstanding. Failure to comply with these limitations and restrictions could preclude the Fund from declaring any dividends or distributions to common shareholders or repurchasing common shares and/or could trigger the mandatory redemption of preferred shares at their liquidation value plus any accrued dividends. Preferred shares, which are entitled to one vote per share, generally vote with the common shares but vote separately as a class to elect two Trustees and on any matters affecting the rights of preferred shares.

Note 6 – Borrowings:

The Fund has an uncommitted $2,000,000 line of credit with BNY. Interest on the amount borrowed is based on the Federal Funds Rate plus a spread on outstanding balances. At July 31, 2006, there was no outstanding balance in connection with the Fund’s uncommitted line of credit. The average daily amount of borrowings during the year ended July 31, 2006 was $65,859 with a related weighted average interest rate of 5.20%.

Note 7 – Indemnifications:

In the normal course of business, the Fund enters into contracts that contain a variety of representations, which provide general indemnifications. The Fund’s maximum exposure under these arrangements is unknown, as this would require future claims that may be made against the Fund that have not yet occurred. However, the Fund expects the risk of loss to be remote.

Note 8 – Accounting Pronouncements:

On July 13, 2006, the Financial Accounting Standards Board (FASB) released FASB Interpretation No. 48 “Accounting for Uncertainty in Income Taxes” (FIN 48). FIN 48 provides guidance for how uncertain tax positions should be recognized, measured, presented and disclosed in the financial statements. FIN 48 requires the evaluation of tax positions taken or expected to be taken in the course of preparing the Fund’s tax returns to determine whether the tax positions are “more-likely-than-not” of being sustained by the applicable tax authority. Tax positions not deemed to meet the more-likely-than-not threshold would be recorded as a tax benefit or expense in the current year. Adoption of FIN 48 is required for fiscal years beginning after December 15, 2006 and is to be applied to all open tax years as of the effective date. At this time, management is evaluating the implications of FIN 48 and its impact in the financial statements has not yet been determined.

Note 9 – Subsequent Dividend Declarations – Common Shareholders:

The Fund has declared the following dividends to common shareholders:

| | | | | | | | |

Rate Per Share | | Declaration

Date | | Ex-Dividend Date | | Record

Date | | Payable

Date |

$0.047 | | 5/24/06 | | 8/04/06 | | 8/08/06 | | 8/15/06 |

$0.047 | | 8/16/06 | | 9/06/06 | | 9/08/06 | | 9/15/06 |

$0.047 | | 8/16/06 | | 10/04/06 | | 10/06/06 | | 10/16/06 |

$0.047 | | 8/16/06 | | 11/06/06 | | 11/08/06 | | 11/15/06 |

| | |

| | Annual Report | July 31, 2006 | 19 |

MZF | MBIA Capital/Claymore Managed Duration Investment Grade Municipal Fund

Report of Independent Registered Public Accounting Firm

To the Shareholders and Board of Trustees of

MBIA Capital/Claymore Managed Duration Investment Grade Municipal Fund

We have audited the accompanying statement of assets and liabilities of MBIA Capital/Claymore Managed Duration Investment Grade Municipal Fund (the “Fund”), including the portfolio of investments, as of July 31, 2006, and the related statements of operations and changes in net assets and financial highlights for the year then ended. These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audit. The financial highlights of the Fund for each of the two years in the period ended July 31, 2005, and the statement of changes in net assets for the year ended July 31, 2005, were audited by other auditors whose report dated September 27, 2005, expressed an unqualified opinion on those financial statements.

We conducted our audit in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. We were not engaged to perform an audit of the Fund’s internal control over financial reporting. Our audit included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements and financial highlights, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of July 31, 2006, by correspondence with the custodian. We believe that our audit provides a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of MBIA Capital/ Claymore Managed Duration Investment Grade Municipal Fund at July 31, 2006, the results of its operations, the changes in its net assets and financial highlights for the year then ended in conformity with U.S. generally accepted accounting principles.

Chicago, Illinois

September 13, 2006

| | |

20 | Annual Report | July 31, 2006 | | |

MZF | MBIA Capital/Claymore Managed Duration Investment Grade Municipal Fund

Supplemental Informationl | (unaudited)

Federal Income Tax Information

Subchapter M of the Internal Revenue Code of 1986, as amended, requires the Fund to advise shareholders within 60 days of the Fund’s tax year end (July 31, 2006) as to the federal tax status of dividends and distributions received by shareholders during such tax period. Accordingly, please note that the majority of dividends paid from net investment income from the Fund during the tax period ended July 31, 2006 was federally exempt interest dividends. The Fund has invested in municipal bonds containing market discount, whose accretion is taxable and accordingly, 0.049% of the dividends paid from net investment income during the tax period are attributable to this taxable income. Therefore, the Fund designated $7,289,998 as tax-exempt income.

Since the Fund’s fiscal year is not the calendar year, another notification will be sent with respect to calendar year 2006. In January 2007, you will be advised on IRS Form 1099 DIV or substitute 1099 DIV as to the federal tax status of the dividends and distributions received during calendar year 2006. The amount that will be reported will be the amount to use on your 2006 federal income tax return and may differ from the amount which must be reported in connection with the Fund’s tax year ended July 31, 2006. Shareholders are advised to consult with their tax advisers as to the federal, state and local tax status of the income received from the Funds. In January 2007, an allocation of interest by state will be provided which may be of value in reducing a shareholder’s state or local tax liability, if any.

Trustees

The Trustees of the MBIA Capital/Claymore Managed Duration Investment Grade Municipal Fund and their principal occupations during the past five years:

| | | | | | | | |

Name, Address*, Year of Birth and Position(s) held with Registrant | | Term of Office**

and Length of

Time Served | | Principal Occupation During the Past Five Years and Other Affiliations | | Number of Portfolios

in Fund Complex***

Overseen by Trustee | | Other Directorships Held by Trustee |

| | | | |

Independent Trustees: | | | | | | | | |

Randall C. Barnes Year of Birth: 1951 Trustee | | Since 2006 | | Formerly, Senior Vice President & Treasurer (1993-1997), President, Pizza Hut International (1991-1993) and Senior Vice President, Strategic Planning and New Business Development (1987-1990) of PepsiCo, Inc.(1987-1997). | | 14 | | None. |

| | | | |

Mark Jurish Year of Birth: 1959 Trustee | | Since 2003 | | Founder and Chief Executive Officer of Larch Lane Advisors. Prior to forming Larch Lane, Mr. Jurish was Managing Director at Paloma Partners, a firm that he joined in 1988. | | 1 | | Serves on Best Practices Committee of The Greenwich Roundtable. |

| | | | |

Ronald A. Nyberg Year of Birth: 1953 Trustee | | Since 2003 | | Principal of Ronald A. Nyberg, Ltd., a law firm specializing in corporate law, estate planning and business transactions (2000-present). Formerly, Executive Vice President, General Counsel and Corporate Secretary of Van Kampen Investments (1982-1999). | | 17 | | None. |

| | | | |

Ronald E. Toupin, Jr. Year of Birth: 1958 Trustee | | Since 2003 | | Formerly, Vice President, Manager and Portfolio Manager of Nuveen Asset Management (1998-1999), Vice President of Nuveen Investment Advisory Corp. (1992-1999), Vice President and Manager of Nuveen Unit Investment Trusts (1991-1999), and Assistant Vice President and Portfolio Manager of Nuveen Unit Investment Trusts (1988-1999), each of John Nuveen & Co., Inc. (1982-1999). | | 15 | | None. |

Interested Trustees: | | | | | | | | |

Clifford D. Corso† 113 King Street Armonk, NY 10504 Year of Birth: 1961 Trustee and President | | Since 2003 | | President of MBIA Asset Management LLC & MBIA Capital Management Corp.; Chief Investment Officer, MBIA Insurance Corp. | | 1 | | None. |

| | | | |

Nicholas Dalmaso Year of Birth: 1965 Trustee, Chief Executive Officer and Chief Legal Officer | | Since 2003 | | Senior Managing Director and General Counsel of Claymore Advisors, LLC and Claymore Securities, Inc. (2001-present). Formerly, Assistant General Counsel, John Nuveen and Co., Inc. (1999-2001). Former Vice President and Associate General Counsel of Van Kampen Investments, Inc. (1992-1999). | | 17 | | None. |

| * | The business address of each Trustee unless otherwise noted is c/o MBIA Capital/Claymore Managed Duration Investment Grade Municipal Fund, 2455 Corporate West Drive, Lisle, IL 60532. |

| ** | The Trustees of each class shall be elected at an annual meeting of shareholders or special meeting in lieu thereof called for that purpose, and each Trustee elected shall hold office until his or her successor shall have been elected and shall have qualified. The term of office of a Trustee shall terminate and a vacancy shall occur in the event of the death, resignation, removal, bankruptcy, adjudicated incompetence or other incapacity to perform the duties of the office, or removal, of a Trustee. |

| *** | The Claymore Fund Complex consists of U.S. registered investment companies advised or serviced by Claymore Advisors, LLC or Claymore Securities, Inc. The Claymore Fund Complex is overseen by multiple Boards of Trustees. |

| † | Mr. Corso is an “interested person” (as defined in Section 2(a)(19) of the Investment Company Act of 1940, as amended) of the Fund because of his position as an officer of MBIA Asset Management and MBIA Capital Management Co., the Fund’s Investment Adviser. |

| †† | Mr. Dalmaso is an “interested person” (as defined in Section 2(a)(19) of the Investment Company Act of 1940, as amended) of the Fund because of his position as an officer of Claymore Securities, Inc., the Fund’s Servicing Agent. |

| | |

| | Annual Report | July 31, 2006 | 21 |

MZF | MBIA Capital/Claymore Managed Duration Investment Grade Municipal Fund | Supplemental Information (unaudited) continued

Officers

The Officers of the MBIA Capital/Claymore Managed Duration Investment Grade Municipal Fund and their principal occupations during the past five years:

| | | | |

Name, Address*, Year of

Birth and Position(s) held with

Registrant | | Term of

Office** and Length of

Time Served | | Principal Occupation During the Past Five Years and Other Affiliations |

Officers: | | | | |

| | |

| Leonard I. Chubinsky 113 King Street Armonk, NY 10504 Year of Birth: 1948 Assistant Secretary and Assistant Vice President | | Since 2003 | | General Counsel and Secretary, MBIA Asset Management LLC & MBIA Capital Management Corp.; Deputy General Counsel, MBIA Insurance Corp. |

| | |

Steven M. Hill Year of Birth: 1964 Chief Financial Officer, Chief Accounting Officer and Treasurer | | Since 2006 | | Senior Managing Director and Chief Financial Officer of Claymore Advisors, LLC and Claymore Securities, Inc. (2005-present). Managing Director of Claymore Advisors, LLC and Claymore Securities, Inc. (2003-2005). Previously, Treasurer of Henderson Global Funds and Operations Manager for Henderson Global Investors (North America) Inc., (2002-2003); Managing Director, FrontPoint Partners LLC (2001-2002); Vice President, Nuveen Investments (1999-2001); Chief Financial Officer, Skyline Asset Management LP, (1999); Vice President, Van Kampen Investments and Assistant Treasurer, Van Kampen mutual funds (1989-1999). |

| | |

Jim Howley Year of Birth: 1972 Assistant Treasurer | | Since 2006 | | Vice President, Fund Administration of Claymore Securities, Inc. (2004-present). Previously, Manager, Mutual Fund Administration of Van Kampen Investments, Inc. |

| | |

Melissa Nguyen Year of Birth: 1978 Secretary | | Since 2006 | | Vice President of Claymore Securities, Inc.; Previously, Associate, Vedder, Price, Kaufman & Kammholz, P.C. (2003-2005). |

| | |

Bruce Saxon Year of Birth: 1957 Chief Compliance Officer | | Since 2006 | | Vice President – Fund Compliance Officer of Claymore Advisors, LLC (Feb 2006 – present). Chief Compliance Officer/Assistant Secretary of Harris Investment Management, Inc. (2003-2006). Director – Compliance of Harrisdirect LLC (1999-2003). |

| * | The business address of each officer unless otherwise noted is c/o MBIA Capital/Claymore Managed Duration Investment Grade Municipal Fund, 2455 Corporate West Drive, Lisle, IL 60532. |