UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

________

FORM N-CSR

________

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act File Number 811-21364

Schroder Global Series Trust

(Exact name of registrant as specified in charter)

________

SEI Investments

One Freedom Valley Drive

Oaks, PA 19456

(Address of principal executive offices) (Zip code)

Michael Beattie

C/O SEI Investments

One Freedom Valley Drive

Oaks, PA 19456

(Name and address of agent for service)

Registrant’s telephone number, including area code: 1-800-464-3108

Date of fiscal year end: October 31, 2019

Date of reporting period: October 31, 2019

Item 1. Reports to Stockholders.

A copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Investment Company Act of 1940, as amended (the “Act”) (17 CFR § 270.30e-1), is attached hereto.

| | October 31, 2019 | Annual Report | |

| | | | |

| | | Domestic Equity | |

| | | Schroder North American Equity Fund | |

| | | | |

| | | International Equity | |

| | | Schroder Emerging Markets Small Cap Fund | |

| | | | |

| | | Fixed Income | |

| | | Schroder Core Bond Fund | |

| | | Schroder Long Duration Investment-Grade Bond Fund | |

| | | Schroder Short Duration Bond Fund | |

| | | Schroder Total Return Fixed Income Fund | |

| | Beginning on March 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of a Fund’s shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports from the Fund or from your financial intermediary, such as a broker-dealer or bank. Instead, the reports will be made available on a website, and you will be notified by mail each time a report is posted and provided with a website link to access the report. If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from a Fund electronically by contacting your financial intermediary. You may elect to receive all future reports in paper free of charge. If you invest through a financial intermediary, you can follow the instructions included with this disclosure, if applicable, or you can contact your financial intermediary to inform it that you wish to continue receiving paper copies of your shareholder reports. If you invest directly with a Fund, you can inform the Fund that you wish to continue receiving paper copies of your shareholder reports by calling (800) 464-3108. Your election to receive reports in paper will apply to all funds held with your financial intermediary if you invest through a financial intermediary or all Schroder Funds if you invest directly with a Fund. | |

| |  |

| |

Table of Contents

| |

| Management Discussion and Analysis | 1 |

| Schedules of Investments | |

| North American Equity Fund | 19 |

| Emerging Markets Small Cap Fund | 24 |

| Core Bond Fund | 26 |

| Long Duration Investment-Grade Bond Fund | 30 |

| Short Duration Bond Fund | 34 |

| Total Return Fixed Income Fund | 38 |

| Statements of Assets and Liabilities | 44 |

| Statements of Operations | 46 |

| Statements of Changes in Net Assets | 48 |

| Financial Highlights | 52 |

| Notes to Financial Statements | 56 |

| Report of Independent Registered Public Accounting Firm | 73 |

| Information Regarding Review and Approval of Investment Advisory Contracts | 75 |

| Disclosure of Fund Expenses | 80 |

| Trustees and Officers | 82 |

| Notice to Shareholders | 85 |

| | |

Proxy Voting (Unaudited)

A description of the Funds’ proxy voting policies and procedures is available upon request, without charge, by visiting the Securities and Exchange Commission’s (“SEC”) website at http://www.sec.gov, or by calling 1-800-464-3108 and requesting a copy of the applicable Fund’s Statement of Additional Information or on the Schroder Funds website at http://www.schroderfunds.com, by downloading the Funds’ Statement of Additional Information. Information regarding how the Funds voted proxies related to portfolio securities during the most recent 12-month period ended June 30 is available without charge, upon request by calling 1-800-464-3108 and on the SEC’s website at http://www.sec.gov.

Form N-PORT (Unaudited)

The Funds file their complete schedules of portfolio holdings with the SEC for the first and third quarters of each fiscal year as an exhibit to its report on Form N-PORT. The Funds’ Form N-PORT reports are available on the SEC’s website at http://www.sec.gov, and may be reviewed and copied at the SEC’s Public Reference Room in Washington, DC. Information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330.

Important Information Concerning Management Discussion and Analysis and Performance

Except as otherwise specifically stated, all information and investment team commentary, including portfolio security positions, is as of October 31, 2019. The views expressed in the Management Discussion and Analysis sections (the “MD&As”) are those of the respective Fund’s portfolio manager(s) and are subject to change without notice. They do not necessarily represent the views of Schroder Investment Management North America Inc. (“SIMNA”). The MD&As contain some forward-looking statements providing current expectations or forecasts of future events; they do not necessarily relate to historical or current facts. There can be no guarantee that any forward-looking statement will be realized. We undertake no obligation to publicly update forward-looking statements, whether as a result of new information, future events, or otherwise. Any discussions of specific securities should not be considered a recommendation to buy or sell those securities. A Fund may buy, sell, or hold any security discussed herein, on the basis of factors described herein or the basis of other factors or other considerations. Fund holdings will change.

Performance quoted represents past performance and does not guarantee or predict future results. Investment return and principal value will fluctuate, so shares, when redeemed, may be worth more or less than their original cost. Please keep in mind that any double digit returns are highly unusual and cannot be sustained. Fees and expenses are factored into the net asset value of your shares and any performance numbers we release. Total return figures reflect expense limitations in effect during the periods shown; without such limitations, the performance shown would have been lower. Performance results assume the reinvestment of dividends and capital gains. The return figures shown do not reflect the deduction of taxes that a shareholder may pay on Fund distributions or the redemption of Fund shares. Current and month-end performance and other information, which may be lower or higher than that cited, is available by contacting SIMNA at (212) 641-3800 and is periodically updated on our website: www.schroderfunds.com.

Schroder North American Equity Fund |

MANAGEMENT DISCUSSION AND ANALYSIS (As of December 5, 2019)

Performance

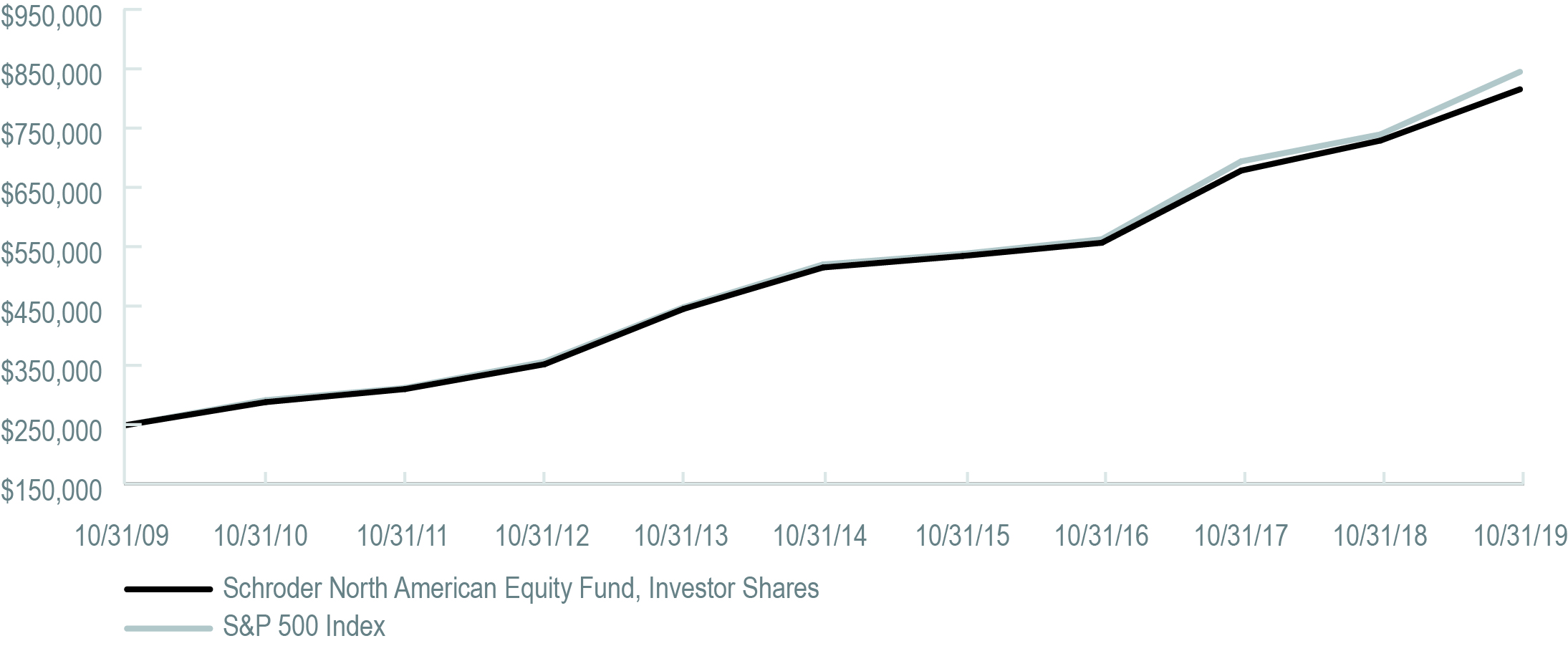

For the twelve-month period ended October 31, 2019, the Schroder North American Equity Fund (the “Fund”) gained 11.88% (Investor Shares), compared to the S&P 500 Index (the “Index”), a market index based on the market capitalizations of 500 large companies having common stock listed on the NYSE or NASDAQ, which rose 14.33% during the same period.

Market Background

The path of U.S. interest rates, Brexit, and the ebb and flow of U.S.-Chinese trade talks were prominent concerns for much of the twelve-month period. U.S. equities retreated sharply towards the end of 2018, with the selling pressure intensifying during the period as investors reacted to concerns about a slowing global economy and the uncertainty surrounding U.S.-China trade relations.

Global equities have risen in 2019 through October as the U.S. and Chinese governments have edged closer to agreeing to a partial trade deal, and the UK once again edged back from the precipice of a no-deal Brexit. Global central banks have accommodated soft economic data with the U.S. Federal Reserve (the “Fed”) cutting interest rates three times in 2019.

From a Style perspective, investors have maintained their preference for Quality Growth stocks, as evidenced by the strength of ongoing U.S. technology stocks. The MSCI Value Index lagged the MSCI Growth Index by 8.40% over the twelve-month period in review.

Portfolio Review

Against this backdrop, the Fund underperformed the benchmark. The main positive influence was stock selection within the consumer staples sector. Our long held positions within food and drink stocks were notable tailwinds for the Fund over the period. Our avoidance of Kraft Heinz supported relative performance as the stock’s price fell significantly in February.

Negative contributions were widely spread rather than being specific to individual stocks. The main detractors were in health care and in our underweight positions in rate sensitives (e.g., utilities and real estate). Exposure to stocks negatively impacted by the U.S.-China trade war (e.g., industrials) was also a headwind.

Outlook

We continue to find an abundance of attractively valued and high quality opportunities across the market. One of the Fund’s most significant exposures remains in health care, particularly pharmaceuticals, which we believe is the best example of an industry offering both value and quality. We also have a higher than Index allocation to industrials (e.g., electrical equipment, transport and machinery) and technology.

Within technology, our preferred areas remain high quality, proven companies with strong balance sheets and rising dividends. We remain underweight in utilities as we find most of these companies are highly leveraged and unattractive from a valuation perspective. We have found some opportunities in real estate over the past few months, although we still maintain lower than Index allocation to the sector.

Comparison of Change in the Value of a $250,000 Investment in the Schroder North American Equity Fund

Investor Shares vs. the Standard & Poor’s (S&P) 500 Index.

The S&P 500 Index is a market capitalization value weighted composite index of 500 large capitalization U.S. companies and reflects the reinvestment of dividends.

Performance Information

| | One Year Ended

October 31, 2019 | Five Years Ended

October 31, 2019(a) | Ten Years Ended

October 31, 2019 (a) |

| Schroder North American Equity Fund |

| Investor Shares | 11.88% | 9.66% | 12.66% |

| S&P 500 Index | 14.33% | 10.78% | 13.70% |

| (a) | Average annual total returns. |

“Total Return” is calculated including reinvestment of all dividends and distributions. Results do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Returns for certain periods reflect fee waivers and/or reimbursements in effect for that period; absent fee waivers and reimbursements, performance would have been lower. Results represent past performance and do not indicate future results. The value of an investment in the Fund and the return on investment both will fluctuate and redemption proceeds may be higher or lower than an investor’s original cost.

| Top 5 Holdings |

| Security | % of Net Assets |

| Microsoft | 4.5% |

| Apple | 4.0 |

| Amazon.com | 2.6 |

| Johnson & Johnson | 1.9 |

| Alphabet Class C | 1.7 |

| Sector Allocation |

| Sector | % of Net Assets |

| Information Technology | 22.8% |

| Healthcare | 16.2 |

| Financials | 13.3 |

| Industrials | 11.5 |

| Consumer Discretionary | 10.1 |

| Communication Services | 9.5 |

| Consumer Staples | 7.8 |

| Energy | 3.9 |

| Real Estate | 2.2 |

| Utilities | 1.1 |

| Materials | 0.7 |

| Other Assets less Liabilities | 0.9 |

Schroder Emerging Markets Small Cap Fund |

MANAGEMENT DISCUSSION AND ANALYSIS (As of December 5, 2019)

Performance

For the twelve-month period ended October 31, 2019, the Schroder Emerging Markets Small Cap Fund (the “Fund”) returned 19.60% (R6 Shares) and 19.73% (Investor Shares), compared to the Morgan Stanley Capital International (MSCI) Emerging Markets Small Cap Index (the “Index”) (a broad-based basket of emerging market stocks covering 1,660 securities across 26 markets), which returned 9.69%.

Market Backdrop

Global equities recorded a positive return over the twelve-month period. U.S.-China trade tensions escalated despite a short truce, and concerns over global growth continued to build. At the end of the period, the U.S. and China indicated that a phase one trade deal was close, but no final agreement has yet been announced. The U.S. Federal Reserve (the “Fed”) responded to the weaker outlook by ending policy normalization and began to cut interest rates. The European Central Bank followed suit, lowering its deposit rate further into negative territory, while also announcing the restart of its quantitative easing program. Against this backdrop, a number of emerging market central banks began to ease monetary policy. The MSCI Emerging Markets Small Cap Index (total return) gained 9.69% (in USD terms) and underperformed the MSCI World Index, which increased by 11.64% (in USD terms).

Greece was the best-performing index market as its economy continued to recover. The outlook was boosted by the election of the centre-right New Democracy party, which is expected to accelerate the reform agenda. Taiwan outperformed, supported by strong performance from technology sector names later in the period, as earnings expectations were revised upwards.

Brazil posted a robust return and finished ahead of the Index. Equities rallied following Jair Bolsonaro’s election to the presidency in October 2018. Economic growth disappointed but sentiment was boosted by the approval of the long-awaited pension reform bill. With inflation controlled, the central bank continued to ease policy later in the period. Mexico posted a strong gain and outperformed, despite a slowdown in economic growth that was due in part to the government transition and a slower rate of government spending, but also as congressional initiatives threatened the country’s historically stable business framework. The central bank responded by reducing interest rates. Russia also outperformed. Although economic growth disappointed, later in the period inflation eased and the central bank began to loosen monetary policy.

By contrast, South Korea recorded a negative return and underperformed, negatively impacted by slower global trade. Chilean equities fell as civil unrest towards the end of the period, amid wider concerns over inequality, increased uncertainty over the policy outlook. China finished in positive territory but underperformed. Economic growth continued to slow, reaching 6% year-on-year in Q3 2019. In response to slowing activity, the authorities deployed stimulus measures. The U.S. implemented further tariffs, with $550 billion of Chinese imports subject to tariffs. The U.S. also added Chinese telecommunications group Huawei to a trade blacklist, citing security concerns. In retaliation, China extended tariffs on U.S. goods to cover $185 billion of imports. It also allowed the renminbi to depreciate beyond the symbolic 7 threshold, leading the U.S. Treasury to label China a currency manipulator.

Portfolio Review

The Fund outperformed the Index over the reporting period.

Stock selection in China underpinned excess returns. This included positions in sportswear manufacturer Li Ning, spirits producer Anhui Gujing Distillery, property management services provider A-Living Services, and pharmaceuticals company Wuxi AppTec. The Fund’s holdings in technology companies ASM Pacific Technology and Hefei Meiya Optoelectronic Technology were also among the largest contributors. In

Brazil, positions in retailer Alpargatas and insurance company IRB Brasil Resseguros worked well. In India, holdings in Indraprastha Gas Limited and Apollo Hospitals were beneficial. Stock selection in Poland, in particular the position in Dino Polska, and in Russia, including the holding in Polymetal International, also added value. By contrast, stock selection in Taiwan was negative, most notably the Fund’s position in food and beverage business Gourmet Master.

Outlook

In our view the strategic case for an investment in emerging market smaller companies is compelling. This is in large part due to their rich opportunity set and their generally under researched nature relative to larger capitalization companies. We believe valuations are reasonably attractive, and we continue to find compelling investment opportunities in well-managed smaller companies given the breadth of the universe.

Comparison of Change in the Value of a $250,000 Investment in the Schroder Emerging Markets Small Cap Fund —

R6 and Investor Shares vs. the Morgan Stanley Capital International (MSCI) Emerging Markets Small Cap Index.

The MSCI Emerging Markets Small Cap Index includes small cap representation across 26 emerging market countries. With 1,660 constituents, the index covers approximately 14% of the free float-adjusted market capitalization in each country. The small cap segment tends to capture more local economic and sector characteristics relative to larger emerging market capitalization segments.

Performance Information

| | One Year Ended

October 31, 2019 | Annualized

Since Inception (a) |

| Schroder Emerging Markets Small Cap Fund |

| R6 Shares | 19.60% | 8.83% |

| Investor Shares | 19.73% | 8.82% |

| MSCI Emerging Markets Small Cap Index | 9.69% | 5.63% |

| (a) | From commencement of fund operations on August 26, 2015. |

“Total Return” is calculated including reinvestment of all dividends and distributions. Results do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Returns for certain periods reflect fee waivers and/or reimbursements in effect for that period; absent fee waivers and reimbursements, performance would have been lower. Results represent past performance and do not indicate future results. The value of an investment in the Fund and the return on investment both will fluctuate and redemption proceeds may be higher or lower than an investor’s original cost.

| Top 5 Holdings |

| Security | % of Net Assets |

| IRB Brasil Resseguros S | 2.9% |

| Chroma ATE | 2.7 |

| Eurobank Ergasias | 2.4 |

| ASM Pacific Technology | 2.3 |

| International Container Terminal Services | 2.3 |

| Geographic Allocation |

| | % of Net Assets |

| Asia/Far East | 62.1% |

| Latin America | 18.0 |

| Europe | 10.2 |

| Africa | 3.0 |

| Middle East | 2.4 |

| Other Assets less Liabilities | 4.3 |

MANAGEMENT DISCUSSION AND ANALYSIS (As of December 5, 2019)

Performance

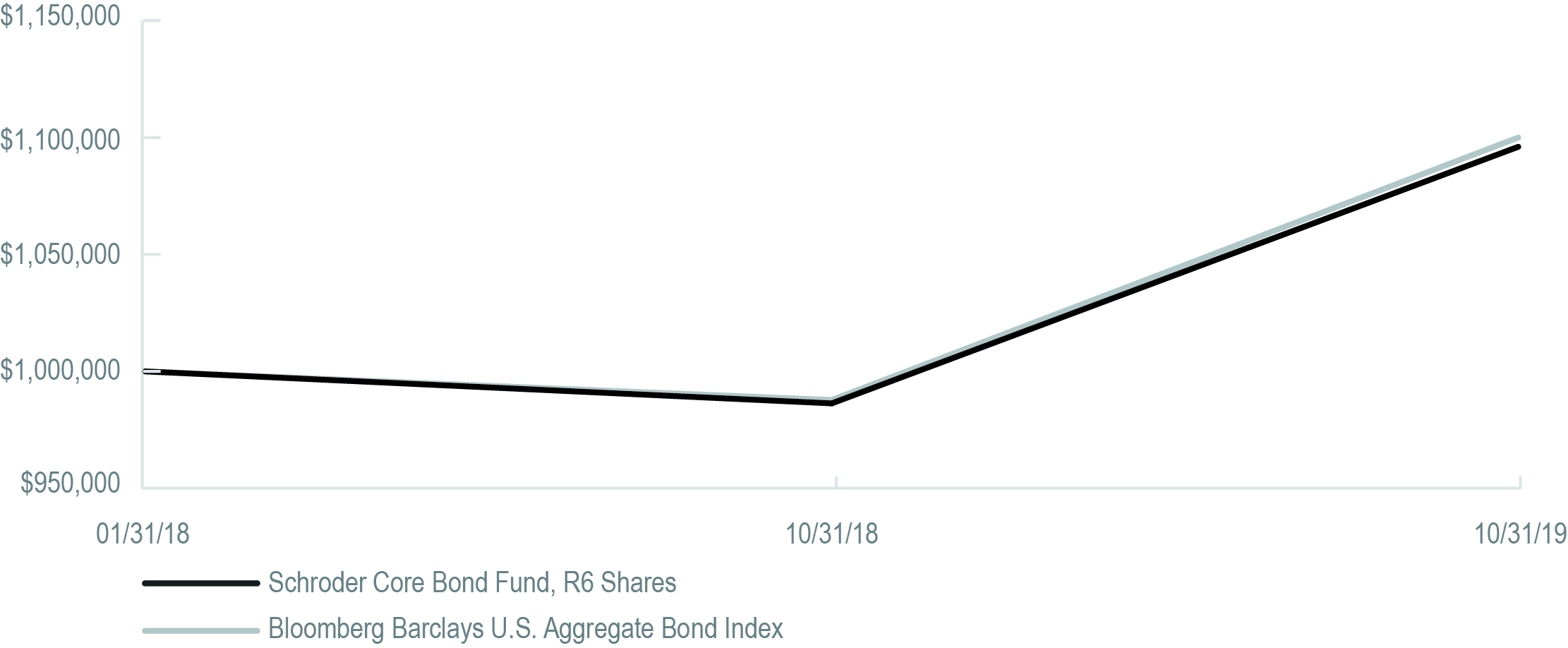

For the twelve-month period ended October 31, 2019, the Schroder Core Bond Fund (the “Fund”) returned 11.27% (R6 Shares) compared to the Bloomberg Barclays U.S. Aggregate Bond Index (the “Index”), which returned 11.51% during the same period.

Market Backdrop

Following a disappointing end to 2018, bond markets opened 2019 with strong performance across the board. In the U.S., risk assets rallied to start the year spurred by better than expected economic data and a sudden dovish turn by the U.S. Federal Reserve (the “Fed”). A massive increase in non-farm payrolls drove the rally in January and was further bolstered by the Fed’s decision at their January meeting to leave rates unchanged. Risk assets continued on a positive trajectory for the remainder of the quarter, although to a lesser degree. Later, in March, any lingering concerns that the Fed might take a hawkish turn were put to rest as they announced no rate hikes for the remainder of the year and an end to balance sheet run-off in September. The unexpected dovish sentiment provided a short-term spark to the market that was stifled by fears of a global slowdown and trade wars. However, the pivot to easing rate policy remained a constant theme through the rest of the year and globally for major Central Banks. Investor concern subsequently shifted from the trade war to the U.S. yield curve, as the curve inverted in March for the first time since 2007. Given the slowdown in activity, particularly across Europe and Asia, the curve inversion was not surprising and despite this development, many risk assets continued the strong rally beginning in late December through March.

Going into the second quarter of 2019, the remaining global central banks came to the rescue. At the macro level, weaker global growth and growing concerns about the global economy resulted in periods of weakness during the quarter. As a result, central banks made seemingly coordinated dovish comments reassuring investors that they were ready to act in order to sustain the economic expansion. Risk assets and traditional safe haven assets both rallied in response. Somewhat surprisingly, the U.S.’s escalation of the trade war with China, as well its smaller spats with Mexico and Europe, did little to interrupt this rally.

The third quarter began quietly with positive excess returns across most fixed income sectors. Despite a widely expected rate cut by the Fed in late July, investors were left to consider if the cut was sufficient. This was followed by a volatile month in August as market participants reacted to a growing list of stresses. Escalating rhetoric in the trade war with China, soft economic data out of Germany, the rising probability of a “hard Brexit,” and surprise election results in Argentina all contributed to a general risk-off sentiment. Treasuries rallied as a result, with yields approaching historical lows in August. Fixed income assets rebounded in early September, spurred by positive consumer data and an additional rate cut by the Fed. However, due to repo market turmoil, sentiment towards end the third quarter reinforced concerns about global growth, and a spike in political risk. Positive headlines from the usual suspects led both equity and fixed income markets higher in October. Market volatility fell precipitously during the month as positive developments with the Brexit resolution and U.S.-China trade deal caused risk assets to rally. The influx of generally soft economic data (e.g., September retail sales, ISM and CPI all below consensus estimates) seemed to support the market’s belief that the Fed would once again cut rates at the end of October. However, given stronger housing and the Atlanta Fed’s Q3 GDP tracker pointing to an on-trend 1.8%, there was very little to suggest that a recession is imminent. Nevertheless, the Fed cut rates for the third time this year, with forward guidance signaling no further cuts. Fixed income markets reacted accordingly, with Treasury yields dropping and spreads widening. Overall, October was a positive month for risk assets as the Fed continues to be a dominant force supporting investor sentiment, as it has throughout 2019.

Portfolio Review

The Fund underperformed the Index for the twelve-month period ended October 31, 2019. The Fund’s overweight to Agency Mortgage-Backed Securities (“MBS”) was a major factor in underperformance. Agency MBS posted excess returns of 8.87% through October 31, according to the Bloomberg Barclays Mortgage Backed Securities Index, lagging both corporates and Treasuries. Security selection within the Agency MBS sector was also a modest detractor. However, out-of-benchmark Prime MBS exposure was a positive contributor within the securitized sector. Yield curve and duration positioning had a modestly negative effect, mostly due to shorter duration corporate bonds underperforming longer duration Treasury bonds.

Positive sector allocation further mitigated negative returns, mainly due to the Fund’s overweight to the corporate sector. Within corporates, the Fund’s overweight to financials was the leading contributor, as the financial sector posted positive excess returns of 13.33%, as measured by the Bloomberg Barclays Corporate Index. Issue selection within industrials also contributed positively to performance, with names like AT&T and Apache standing out.

Outlook

Looking forward to the upcoming year, risk assets appear to believe in the omnipotence of central banks. With flows rather than fundamentals driving returns we would suggest investors proceed with caution at this juncture. Markets will need to navigate various cross-currents in the coming months: uncertainty with regards to trade, a Fed that is easing amidst a cyclical slowdown, Brexit, and the ramp-up of the 2020 U.S. election cycle, just to name a few. Our view is that the easy money in most markets has been made and that risk assets will face some challenges ahead. This is particularly true as we believe valuations in the credit sectors are now approaching the more expensive end of their cyclical range. The liquidity environment will likely keep risk assets supported, but it’s difficult to see material appreciation from here absent a change in the underlying fundamentals.

So where does this leave us in our asset allocation? With headwinds building and valuations full, we remain cautious on riskier segments of fixed income. Our allocation to the corporate sector remains as low as it has been in a number of years. Conversely, our allocations to highly liquid Treasuries and mortgages are at their highest levels. We prefer mortgages over other spread markets, as valuations are near their cheapest levels of the post-crisis period. Fundamentals are also preferable, in our opinion, as debt growth in the mortgage market has significantly lagged that of the corporate market. We believe that exposure to collateralized loan obligations is an additional way to diversify corporate exposure while maintaining an income advantage and more defensive positioning in the AAA class only. Our view is that the ensuing months will present opportunity in markets, and we want to have the liquidity available to take advantage of it.

With regard to rates, we believe the peak in yields was seen in 2018. A Fed in easing mode and slower growth suggest that fixed income assets are likely to remain well supported. Higher quality fixed income products should still offer value in both absolute terms and relative to other asset classes, especially in an environment where volatility is likely to remain high and central banks globally are continuing to embrace easy money.

Comparison of Change in the Value of a $1,000,000 Investment in the

Schroder Core Bond Fund R6 Shares vs. the Bloomberg Barclays U.S. Aggregate Bond Index.

The Bloomberg Barclays U.S. Aggregate Bond Index provides a measure of the performance of the U.S. investment grade bonds market, which includes investment grade U.S. Government bonds, investment grade corporate bonds, mortgage pass-through securities and asset-backed securities that are publicly offered for sale in the United States. The securities in the Index must have a least one year remaining to maturity. The Index is not managed.

Performance Information

| | One Year Ended October 31, 2019 | Annualized

Since Inception (a) |

| Schroder Core Bond Fund | | |

| R6 Shares | 11.27% | 5.45% |

| Bloomberg Barclays U.S. Aggregate Bond Index | 11.51% | 5.67% |

| (a) | From commencement of fund operations January 31, 2018. |

“Total Return” is calculated including reinvestment of all dividends and distributions. Results do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Returns for certain periods reflect fee waivers and/or reimbursements in effect for that period; absent fee waivers and reimbursements, performance would have been lower. Results represent past performance and do not indicate future results. The value of an investment in the Fund and the return on investment both will fluctuate and redemption proceeds may be higher or lower than an investor’s original cost.

| Top 5 Holdings |

| Security | % of Net Assets |

| United States Treasury Note 1.500%, 08/15/22 | 8.4% |

| United States Treasury Note 1.500%, 09/30/24 | 6.5 |

| FNMA 3.500%, 11/01/47 | 3.1 |

| United States Treasury Note 1.625%, 09/30/26 | 2.7 |

| United States Treasury Bond 4.500%, 02/15/36 | 2.7 |

| Sector Allocation |

| Sector | % of Net Assets |

| Corporate Obligations | 38.9% |

| U.S. Treasury Obligations | 34.3 |

| U.S. Government Mortgage-Backed Obligations | 22.3 |

| Collateralized Mortgage Obligations | 2.3 |

| Commercial Mortgage-Backed Obligations | 0.4 |

| Taxable Municipal Bond | 0.2 |

| Other Assets less Liabilities | 1.6 |

Schroder Long Duration Investment-Grade Bond Fund |

MANAGEMENT DISCUSSION AND ANALYSIS (As of December 5, 2019)

Performance

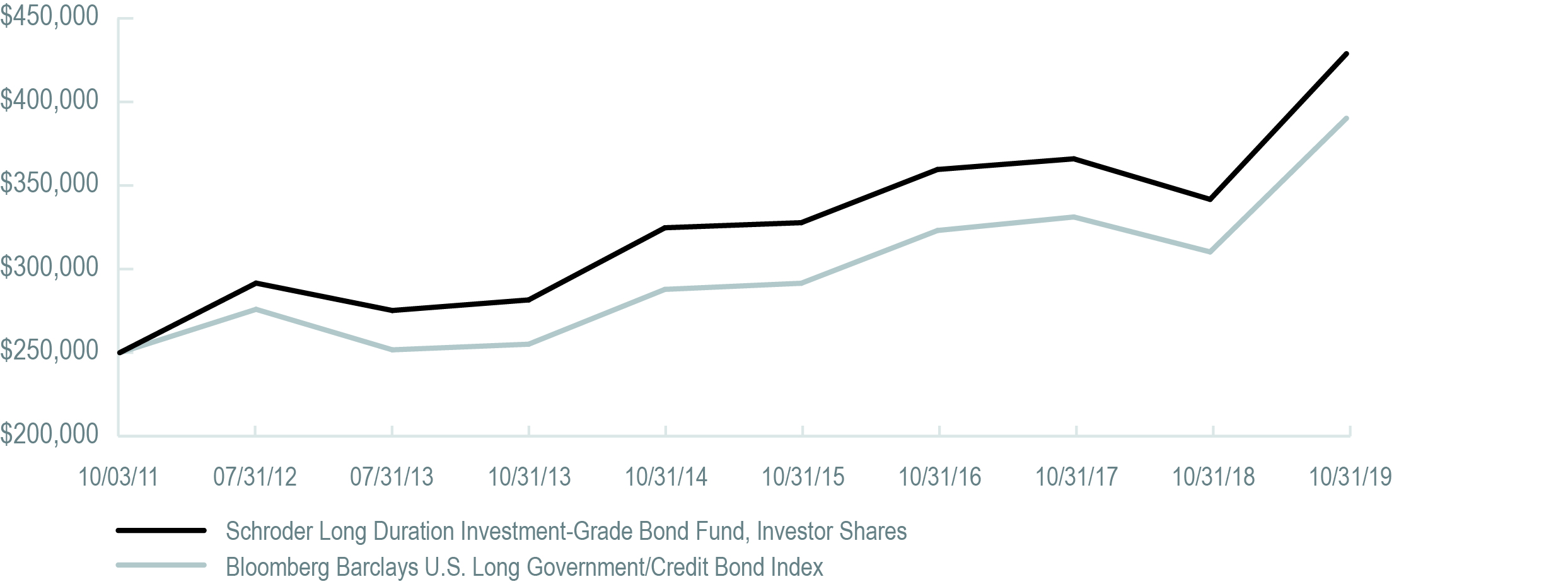

For the twelve-month period ended October 31, 2019, the Schroder Long Duration Investment-Grade Bond Fund (the “Fund”) returned 25.74% (Investor Shares), compared to the Bloomberg Barclays Long Government/Credit Bond Index (the “Index”), a broad-based basket of debt securities, which returned 26.03% during the same period.

Market background

Following a disappointing end to 2018, bond markets opened 2019 with strong performance across the board. In the U.S., risk assets rallied to start the year spurred by better than expected economic data and a sudden dovish turn by the U.S. Federal Reserve (the “Fed”). A massive increase in non-farm payrolls drove the rally in January and was further bolstered by the Fed’s decision at their January meeting to leave rates unchanged. Risk assets continued on a positive trajectory for the remainder of the quarter, although to a lesser degree. Later in March, any lingering concerns that the Fed might take a hawkish turn were put to rest as they announced no rate hikes for the remainder of the year and an end to balance sheet run-off in September. The unexpected dovish sentiment provided a short-term spark to the market that was stifled by fears of a global slowdown and trade wars. however, the pivot to easing rate policy remained a constant theme through the rest of the year and globally for major Central Banks. Investor concern subsequently shifted from the trade war to the U.S. yield curve, as the curve inverted in March for the first time since 2007. Given the slowdown in activity, particularly across Europe and Asia, the curve inversion was not surprising and despite this development many risk assets continued the strong rally beginning in late December through March.

Going into the second quarter of 2019, the remaining global central banks came to the rescue. At the macro level, weaker global growth and growing concerns about the global economy resulted in periods of weakness during the quarter. As a result, central banks made seemingly coordinated dovish comments reassuring investors that they were ready to act in order to sustain the economic expansion. Risk assets and traditional safe haven assets both rallied in response. Somewhat surprisingly, the U.S.’s escalation of the trade war with China, as well as its smaller spats with Mexico and Europe, did little to interrupt this rally.

The third quarter began quietly with positive excess returns across most fixed income sectors. Despite a widely expected rate cut by the Fed in late July, investors were left to consider if the cut was sufficient. This was followed by a volatile month in August as market participants reacted to a growing list of stresses. Escalating rhetoric in the trade war with China, soft economic data out of Germany, the rising probability of a “hard Brexit,” and surprise election results in Argentina all contributed to a general risk-off sentiment. Treasuries rallied as a result, with yields approaching historical lows in August. Fixed income assets rebounded in early September, spurred by positive consumer data and an additional rate cut by the Fed. However, due to repo market turmoil, sentiment towards end the third quarter reinforced concerns about global growth, and a spike in political risk. Positive headlines from the usual suspects led both equity and fixed income markets higher in October. Market volatility fell precipitously during the month as positive developments with the Brexit resolution and U.S.-China trade deal caused risk assets to rally. The influx of generally soft economic data (e.g., September retail sales, ISM and CPI all below consensus estimates) seemed to support the market’s belief that the Fed would once again cut rates at the end of October. However, given stronger housing and the Atlanta Fed’s Q3 GDP tracker pointing to an on-trend 1.8%, there was very little to suggest that a recession is imminent. Nevertheless, the Fed cut rates for the third time this year, with forward guidance signaling no further cuts. Fixed income markets reacted accordingly, with Treasury yields dropping and spreads widening. Overall, October was a positive month for risk assets as the Fed continues to be a dominant force supporting investor sentiment, as it has throughout 2019.

Portfolio Review

The Fund underperformed the Index for the twelve-month period ended October 31, 2019. Sector allocation was a major factor in underperformance. Within corporates, overweighting financials and slightly underweighting utilities led to outperformance, but emerging markets sovereign exposure was a major detractor. Issuer selection within corporates, particularly industrials, mitigated some underperformance. Industrial names like Cigna Corporation, Telecom Communications, and Newell stood out as top contributors. The Fund’s slightly short duration relative to the benchmark also detracted from returns.

Outlook

Looking forward to the upcoming year, risk assets appear to believe in the omnipotence of central banks. With flows rather than fundamentals driving returns we would suggest investors proceed with caution at this juncture. Markets will need to navigate various cross-currents in the coming months: uncertainty with regards to trade, a Fed that is easing amidst a cyclical slowdown, Brexit, and the ramp-up of the 2020 U.S. election cycle, just to name a few. Our view is that the easy money in most markets has been made and that risk assets will face some challenges ahead. This is particularly true as we believe valuations in the credit sectors are now approaching the more expensive end of their cyclical range. The liquidity environment will likely keep risk assets supported, but it’s difficult to see material appreciation from here absent a change in the underlying fundamentals.

So where does this leave us in our asset allocation? With headwinds building and valuations full, we remain cautious on riskier segments of fixed income. Our allocation to the corporate sector remains as low as it has been in a number of years. Conversely, our allocations to highly liquid Treasuries are at their highest levels. We believe the ensuing months will present opportunity in markets and we want to have the liquidity available to take advantage of it.

With regard to rates, we believe the peak in yields was seen in 2018. A Fed in easing mode and slower growth suggest that fixed income assets are likely to remain well supported. Higher quality fixed income products should still offer value in both absolute terms and relative to other asset classes, especially in an environment where volatility is likely to remain high and central banks globally are continuing to embrace easy money.

Comparison of Change in the Value of a $250,000 Investment in

the Schroder Long Duration Investment-Grade Bond Fund, Investor Shares

vs. the Bloomberg Barclays U.S. Long Government/Credit Bond Index.

The Bloomberg Barclays U.S. Long Government/Credit Bond Index is a bond market index covering the U.S. investment-grade fixed corporate and government bond market. The index consists of publicly issued corporate, U.S. government and specified foreign debentures and secured notes. All securities must have at least ten years to maturity and be rated investment-grade by at least two of the following ratings agencies: Moody’s, S&P and Fitch, and be dollar-denominated, fixed rate and nonconvertible.

Performance Information

| | One Year Ended

October 31, 2019 | Five Years Ended

October 31, 2019 (a) | Annualized

Since Inception (b) |

| Schroder Long Duration Investment-Grade Bond Fund | | | |

| Investor Shares | 25.74% | 5.77% | 6.98% |

| Bloomberg Barclays U.S. Long Government/Credit Bond Index | 26.03% | 6.34% | 5.72% |

| (a) | Average annual total returns. |

| (b) | From commencement of fund operations on October 3, 2011. |

“Total Return” is calculated including reinvestment of all dividends and distributions. Results do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Returns for certain periods reflect fee waivers and/or reimbursements in effect for that period; absent fee waivers and reimbursements, performance would have been lower. Results represent past performance and do not indicate future results. The value of an investment in the Fund and the return on investment both will fluctuate and redemption proceeds may be higher or lower than an investor’s original cost.

| Top 5 Holdings |

| Security | % of Net Assets |

| United States Treasury Bond 2.875%, 05/15/43 | 10.6% |

| United States Treasury Bond 2.750%, 08/15/47 | 7.6 |

| United States Treasury Bond 4.500%, 02/15/36 | 5.9 |

| United States Treasury Bond 2.750%, 11/15/47 | 3.3 |

| United States Treasury Bond 3.000%, 08/15/48 | 2.9 |

| Sector Allocation |

| Sector | % of Net Assets |

| Corporate Obligations | 59.6% |

| U.S. Treasury Obligations | 38.5 |

| Taxable Municipal Bond | 0.8 |

| Other Assets less Liabilities | 1.1 |

Schroder Short Duration Bond Fund |

MANAGEMENT DISCUSSION AND ANALYSIS (As of December 5, 2019)

Performance

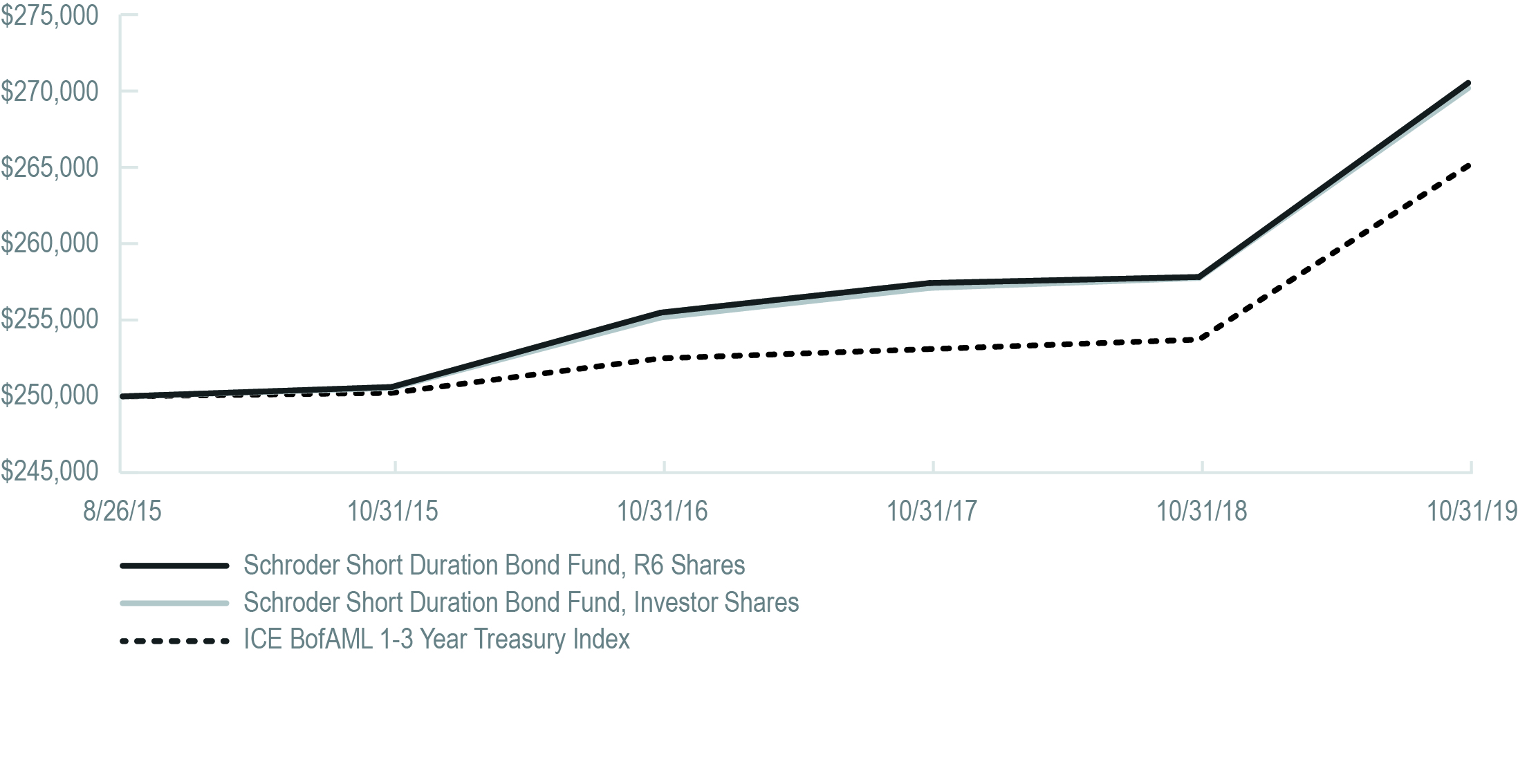

For the twelve-month period ended October 31, 2019, the Schroder Short Duration Bond Fund (the “Fund”) returned 4.88% (Investor Shares) and 4.99% (R6 Shares), compared to the ICE BofAML 1-3 Year Treasury Index (the “Index”), which returned 4.54% during the same period.

Market Backdrop

Following a disappointing end to 2018, bond markets opened 2019 with strong performance across the board. In the U.S., risk assets rallied to start the year spurred by better than expected economic data and a sudden dovish turn by the U.S. Federal Reserve (the “Fed”). A massive increase in non-farm payrolls drove the rally in January and was further bolstered by the Fed’s decision in their January meeting to leave rates unchanged. Risk assets continued on a positive trajectory for the remainder of the quarter, although to a lesser degree. Later, in March, any lingering concerns that the Fed might take a hawkish turn were put to rest as they announced no rate hikes for the remainder of the year and an end to balance sheet run-off in September. The unexpected dovish sentiment provided a short-term spark to the market that was stifled by fears of a global slowdown and trade wars. However, the pivot to easing rate policy remained a constant theme through the rest of the year and globally for major Central Banks. Investor concern subsequently shifted from the trade war to the U.S. yield curve, as the curve inverted in March for the first time since 2007. Given the slowdown in activity, particularly across Europe and Asia, the curve inversion was not surprising and despite this development many risk assets continued the strong rally beginning in late December through March.

Going into the second quarter of 2019, the remaining global central banks came to the rescue. At the macro level, weaker global growth and growing concerns about the global economy resulted in periods of weakness during the quarter. As a result, central banks made seemingly coordinated dovish comments reassuring investors that they were ready to act in order to sustain the economic expansion. Risk assets and traditional safe haven assets both rallied in response. Somewhat surprisingly, the escalation of the U.S.’s trade war with China, as well as its smaller spats with Mexico and Europe, did little to interrupt this rally.

The third quarter began quietly with positive excess returns across most fixed income sectors. Despite a widely expected rate cut by the Fed in late July, investors were left to consider if the cut was sufficient. This was followed by a volatile month in August as market participants reacted to a growing list of stresses. Escalating rhetoric in the U.S.-China trade war, soft economic data out of Germany, the rising probability of a “hard Brexit,” and surprise election results in Argentina all contributed to a general risk-off sentiment. Treasuries rallied as a result, with yields approaching historical lows in August. Fixed income assets rebounded in early September, spurred by positive consumer data and an additional rate cut by the Fed. However, due to repo market turmoil sentiment towards end the third quarter, reinforced concerns about global growth, and a spike in political risk. Positive headlines from the usual suspects led both equity and fixed income markets higher in October. Market volatility fell precipitously during the month as positive developments with the Brexit resolution and U.S.-China trade deal caused risk assets to rally. The influx of generally soft economic data (e.g., September retail sales, ISM and CPI all below consensus estimates) seemed to support the market’s belief that the Fed would once again cut rates at the end of October. However, given stronger housing and the Atlanta Fed’s Q3 GDP tracker pointing to an on-trend 1.8%, there was very little to suggest that a recession is imminent. Nevertheless, the Fed cut rates for the third time this year, with forward guidance signaling no further cuts. Fixed income markets reacted accordingly, with Treasury yields dropping and spreads widening. Overall, October was a positive month for risk assets as the Fed continues to be a dominant force supporting investor sentiment, as it has throughout 2019.

Portfolio Review

The Fund outperformed the Index for the twelve-month period ended October 31, 2019. Sector allocation drove performance, with issue selection having no positive or negative impact on returns given the 100% Treasury benchmark. Overweighting industrials and financials to the benchmark was the main driver due to the strong corporate rally since Q4 2018. Out-of-benchmark exposure to the securitized sector, Prime Mortgage-Backed Securites (“MBS”) and Collateralized Loan Obligations (“CLOs”), was also a strong driver of outperformance. Agency MBS exposure slightly detracted from outperformance as lower rates and increasing prepayments left the sector lagging corporates and Treasuries over the period in terms of excess returns. The Fund’s modestly short duration relative to the benchmark also slightly detracted from overall returns due to rates moving lower.

Although the Fund is positioned with exposure to corporates, which are not in the Index, this allocation has low sensitivity to spread risk, as measured by duration times spread. Throughout the period we reduced the overall corporate exposure in lieu of defensive, high quality securitized bonds, which we believe has diversified risk in the Fund.

Outlook

Looking forward to the upcoming year, risk assets appear to believe in the omnipotence of central banks. With flows rather than fundamentals driving returns we would suggest investors proceed with caution at this juncture. Markets will need to navigate various cross-currents in the coming months: uncertainty with regards to trade, a Fed that is easing amidst a cyclical slowdown, Brexit, and the ramp-up of the 2020 U.S. election cycle just to name a few. Our view is that the easy money in most markets has been made and that risk assets will face some challenges ahead. This is particularly true as we believe valuations in the credit sectors are now approaching the more expensive end of their cyclical range. The liquidity environment will likely keep risk assets supported, but it’s difficult to see material appreciation from here absent a change in the underlying fundamentals.

So where does this leave us in our asset allocation? With headwinds building and valuations full, we remain cautious on riskier segments of fixed income. Our allocation to the corporate sector remains as low as it has been in a number of years. Conversely, our allocations to highly liquid Treasuries and mortgages are at their highest levels. We prefer mortgages over other spread markets, as valuations are near their cheapest levels of the post-crisis period. Fundamentals are also preferable, in our opinion, as debt growth in the mortgage market has significantly lagged that of the corporate market. We believe exposure to collateralized loan obligations is an additional way to diversify corporate exposure while maintaining an income advantage and more defensive positioning in the AAA class only. Our view is that the ensuing months will present opportunity in markets and we want to have the liquidity available to take advantage of it.

With regard to rates, we believe the peak in yields was seen in 2018. A Fed in easing mode and slower growth suggest that fixed income assets are likely to remain well supported. Higher quality fixed income products should still offer value in both absolute terms and relative to other asset classes, especially in an environment where volatility is likely to remain high and central banks globally are continuing to embrace easy money.

Comparison of Change in the Value of a $250,000 Investment in the Schroder Short Duration Bond Fund —

R6 and Investor Shares vs. the ICE BofAML 1-3 Year Treasury Index.

The ICE BofAML 1-3 Year Treasury Index is an unmanaged index that tracks the performance of the direct sovereign debt of the U.S. Government having a maturity of at least one year and less than three years.

| | One Year Ended

October 31, 2019 | Annualized

Since Inception (a) |

| Schroder Short Duration Bond Fund | | |

| R6 Shares | 4.99% | 1.93% |

| Investor Shares | 4.88% | 1.90% |

| ICE BofAML 1-3 Year Treasury Index | 4.54% | 1.43% |

| (a) | From commencement of fund operations on August 26, 2015. |

“Total Return” is calculated including reinvestment of all dividends and distributions. Results do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Returns for certain periods reflect fee waivers and/or reimbursements in effect for that period; absent fee waivers and reimbursements, performance would have been lower. Results represent past performance and do not indicate future results. The value of an investment in the Fund and the return on investment both will fluctuate and redemption proceeds may be higher or lower than an investor’s original cost.

| Top 5 Holdings |

| Security | % of Net Assets |

| United States Treasury Note 2.25%, 04/15/22 | 13.9% |

| United States Treasury Bill 1.572%, 02/27/20 | 11.3 |

| United States Treasury Note 2.25%, 03/31/20 | 4.9 |

| United States Treasury Note 2.5%, 02/28/21 | 3.0 |

| Microsoft | 2.3 |

| Sector Allocation |

| Sector | % of Net Assets |

| U.S. Treasury Obligations | 39.1% |

| Corporate Obligations | 37.2 |

| U.S. Government Mortgage-Backed Obligations | 9.6 |

| Asset-Backed Securities | 8.9 |

| Collateralized Mortgage Obligations | 2.7 |

| Commercial Mortgage-Backed Obligations | 1.0 |

| Taxable Municipal Bond | 0.2 |

| Other Assets less Liabilities | 1.3 |

Schroder Total Return Fixed Income Fund |

MANAGEMENT DISCUSSION AND ANALYSIS (As of December 5, 2019)

Performance

For the twelve-month period ended October 31, 2019, the Schroder Total Return Fixed Income Fund (the “Fund”) returned 10.93% (Investor Shares), compared to the Bloomberg Barclays U.S. Aggregate Bond Index (the “Index”), which returned 11.51% during the same period.

Market Background

Following a disappointing end to 2018, bond markets opened 2019 with strong performance across the board. In the U.S., risk assets rallied to start the year spurred by better than expected economic data and a sudden dovish turn by the U.S. Federal Reserve (the “Fed”). A massive increase in non-farm payrolls drove the rally in January and was further bolstered by the Fed’s decision at their January meeting to leave rates unchanged. Risk assets continued on a positive trajectory for the remainder of the quarter, although to a lesser degree. Later in March, any lingering concerns that the Fed might take a hawkish turn were put to rest as they announced no rate hikes for the remainder of the year and an end to balance sheet run-offs in September. The unexpected dovish sentiment provided a short-term spark to the market that was stifled by fears of a global slowdown and trade wars. However, the pivot to easing rate policy remained a constant theme through the rest of the year and globally for major Central Banks. Investor concern subsequently shifted from the trade war to the U.S. yield curve, as the curve inverted in March for the first time since 2007. Given the slowdown in activity, particularly across Europe and Asia, the curve inversion was not surprising and despite this development many risk assets continued the strong rally beginning in late December through March.

Going into the second quarter of 2019, the remaining global central banks came to the rescue. At the macro level, weaker global growth and growing concerns about the global economy resulted in periods of weakness during the quarter. As a result, central banks made seemingly coordinated dovish comments reassuring investors that they were ready to act in order to sustain the economic expansion. Risk assets and traditional safe haven assets both rallied in response. Somewhat surprisingly, the escalation of the U.S.’s trade war with China, as well as its smaller spats with Mexico and Europe, did little to interrupt this rally.

The third quarter began quietly with positive excess returns across most fixed income sectors. Despite a widely expected rate cut by the Fed in late July, investors were left to consider if the cut was sufficient. This was followed by a volatile month in August as market participants reacted to a growing list of stresses. Escalating rhetoric in the U.S.-China trade war, soft economic data out of Germany, the rising probability of a “hard Brexit,” and surprise election results in Argentina all contributed to a general risk-off sentiment. Treasuries rallied as a result, with yields approaching historical lows in August. Fixed income assets rebounded in early September, spurred by positive consumer data and an additional rate cut by the Fed. However, due to repo market turmoil, sentiment towards end the third quarter, reinforced concerns about global growth and a spike in political risk. Positive headlines from the usual suspects led both equity and fixed income markets higher in October. Market volatility fell precipitously during the month as positive developments with the Brexit resolution and U.S.-China trade deal caused risk assets to rally. The influx of generally soft economic data (e.g., September retail sales, ISM and CPI all below consensus estimates) seemed to support the market’s belief that the Fed would once again cut rates at the end of October. However, given stronger housing and the Atlanta Fed’s Q3 GDP tracker pointing to an on-trend 1.8%, there was very little to suggest that a recession is imminent. Nevertheless, the Fed cut rates for the third time this year, with forward guidance signaling no further cuts. Fixed income markets reacted accordingly, with Treasury yields dropping and spreads widening. Overall, October was a positive month for risk assets as the Fed continues to be a dominant force supporting investor sentiment, as it has throughout 2019.

Portfolio Review

The Fund underperformed the Index for the twelve-month period ended October 31, 2019. Issue selection was the main detractor of performance, with sector selection mitigating negative returns. Issuer selection within corporates, particularly industrials, was the main negative driver. L Brands, the personal apparel, beauty, and personal care brand, faced a decline in earnings due to increased competition and changing consumer preferences. Issue selection with Agency Mortgage-Backed Securities (“MBS”) was also a detractor, as was exposure to Argentina bonds, where unexpected presidential election results significantly increased risk on the sovereign bond. Strong sector selection was primarily driven by the Fund’s overweight to corporates and corresponding underweight to U.S. Treasuries.

Although the Fund is positioned with an overweight to corporates, this allocation has low sensitivity to spread risk as measured by duration times spread. Throughout the period we reduced the overall corporate exposure in lieu of defensive, high quality securitized bonds, which we believe has diversified risk in the Fund.

Outlook

Looking forward to the upcoming year, risk assets appear to believe in the omnipotence of central banks. With flows rather than fundamentals driving returns we would suggest investors proceed with caution at this juncture. Markets will need to navigate various cross-currents in the coming months: uncertainty with regards to trade, a Fed that is easing amidst a cyclical slowdown, Brexit, and the ramp-up of the 2020 U.S. election cycle, just to name a few. Our view is that the easy money in most markets has been made and that risk assets will face some challenges ahead. This is particularly true as we believe valuations in the credit sectors are now approaching the more expensive end of their cyclical range. The liquidity environment will likely keep risk assets supported, but it’s difficult to see material appreciation from here absent a change in the underlying fundamentals.

So where does this leave us in our asset allocation? With headwinds building and valuations full, we remain cautious on riskier segments of fixed income. Our allocation to the corporate sector remains as low as it has been in a number of years. Conversely, our allocations to highly liquid Treasuries and mortgages are at their highest levels. We prefer mortgages over other spread markets as valuations are near their cheapest levels of the post-crisis period. Fundamentals are also preferable, in our opinion, as debt growth in the mortgage market has significantly lagged that of the corporate market. We believe exposure to collateralized loan obligations is an additional way to diversify corporate exposure while maintaining an income advantage and more defensive positioning in the AAA class only. Our view is that the ensuing months will present opportunity in markets, and we want to have the liquidity available to take advantage of it.

With regard to rates, we believe the peak in yields was seen in 2018. A Fed in easing mode and slower growth suggest that fixed income assets are likely to remain well supported. Higher quality fixed income products should still offer value in both absolute terms and relative to other asset classes, especially in an environment where volatility is likely to remain high and central banks globally are continuing to embrace easy money.

Comparison of Change in the Value of a $250,000 Investment in the Schroder Total Return Fixed Income Fund —

Investor Shares vs. the Bloomberg Barclays U.S. Aggregate Bond Index.

The Bloomberg Barclays U.S. Aggregate Bond Index provides a measure of the performance of the U.S. investment grade bonds market, which includes investment grade U.S. Government bonds, investment grade corporate bonds, mortgage pass-through securities and asset-backed securities that are publicly offered for sale in the United States. The securities in the Index must have a least one year remaining to maturity. The Index is not managed.

Performance Information

| | One Year Ended

October 31, 2019 | Five Years Ended

October 31, 2019 (a) | Ten Years Ended

October 31, 2019 (a) |

| Schroder Total Return Fixed Income Fund |

| Investor Shares | 10.93% | 2.77% | 3.87% |

| Bloomberg Barclays U.S. Aggregate Bond Index | 11.51% | 3.24% | 3.73% |

| (a) | Average annual total returns. |

“Total Return” is calculated including reinvestment of all dividends and distributions. Results do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Returns for certain periods reflect fee waivers and/or reimbursements in effect for that period; absent fee waivers and reimbursements, performance would have been lower. Results represent past performance and do not indicate future results. The value of an investment in the Fund and the return on investment both will fluctuate and redemption proceeds may be higher or lower than an investor’s original cost.

| Top 5 Holdings |

| Security | % of Net Assets |

| United States Treasury Note 2.625%, 07/31/20 | 3.9% |

| United States Treasury Inflation Indexed Bond 0.750%, 07/15/28 | 2.4 |

| FNMA 4.500%, 11/01/48 | 2.1 |

| GNMA 4.000%, 06/20/49 | 1.9 |

| Madison Park Funding XVIII, Ser 2017-18A, Class A1R 3.156%, 10/21/30 | 1.9 |

| Sector Allocation |

| Sector | % of Net Assets |

| Corporate Obligations | 38.4% |

| U.S. Government Mortgage-Backed Obligations | 23.9 |

| U.S. Treasury Obligations | 16.3 |

| Asset-Backed Securities | 10.7 |

| Collateralized Mortgage Obligations | 5.7 |

| Taxable Municipal Bonds | 1.3 |

| Commercial Mortgage-Backed Obligations | 1.2 |

| Sovereign Governments | 1.1 |

| Other Assets less Liabilities | 1.4 |

Schroder North American Equity Fund |

Schedule of Investments

October 31, 2019

| | | | | |

| | | COMMON STOCK – 99.1% | |

| | | Canada – 1.5% | |

| | 231,900 | | Birchcliff Energy | | | 353,898 | |

| | 29,500 | | Canadian National Railway | | | 2,638,448 | |

| | 7,800 | | Canadian Pacific Railway | | | 1,773,729 | |

| | 16,600 | | CGI Class A (1) | | | 1,290,341 | |

| | 7,783 | | CI Financial | | | 113,279 | |

| | 134,800 | | Crew Energy (1) | | | 49,126 | |

| | 12,100 | | Dollarama | | | 407,069 | |

| | 23,800 | | Enerflex | | | 186,482 | |

| | 11,400 | | Genworth MI Canada | | | 460,466 | |

| | 12,300 | | Gildan Activewear | | | 314,247 | |

| | 37,300 | | Husky Energy | | | 260,542 | |

| | 23,300 | | Imperial Oil | | | 580,245 | |

| | 34,700 | | Magna International Class A | | | 1,865,807 | |

| | 137,800 | | Manulife Financial | | | 2,566,422 | |

| | 13,100 | | Open Text | | | 529,331 | |

| | 36,300 | | Teck Resources Class B | | | 573,811 | |

| | 31,700 | | TransAlta Renewables | | | 341,285 | |

| | 16,400 | | Westshore Terminals Investment | | | | |

| | | | | | | 14,588,922 | |

| | | | Israel – 0.3% | |

| | 26,300 | | Check Point Software Technologies (1) | | | | |

| | | | | | | | |

| | | | United States – 97.3% | |

| | | | Communication Services – 9.5% | |

| | 12,549 | | Alphabet Class A (1) | | | 15,796,681 | |

| | 13,094 | | Alphabet Class C (1) | | | 16,499,880 | |

| | 12,000 | | AMC Networks Class A (1) | | | 522,600 | |

| | 221,127 | | AT&T | | | 8,511,178 | |

| | 600 | | Cable One | | | 795,222 | |

| | 108,500 | | Comcast Class A | | | 4,862,970 | |

| | 24,000 | | Discovery Class A (1) | | | 646,920 | |

| | 81,700 | | Facebook Class A (1) | | | 15,657,805 | |

| | 50,700 | | Fox | | | 1,624,428 | |

| | 5,000 | | Netflix (1) | | | 1,437,050 | |

| | 45,900 | | Omnicom Group | | | 3,543,021 | |

| | 184,630 | | Verizon Communications | | | 11,164,576 | |

| | 38,100 | | Viacom Class B | | | 821,436 | |

| | 68,972 | | Walt Disney | | | | |

| | | | | | | 90,844,609 | |

| | | | Consumer Discretionary – 10.0% | |

| | 14,206 | | Amazon.com (1) | | | 25,239,232 | |

| | 1,900 | | AutoZone (1) | | | 2,174,322 | |

| | 7,000 | | Best Buy | | | 502,810 | |

| Shares | | | | | |

| | 288 | | Booking Holdings (1) | | | 590,046 | |

| | 28,600 | | Buckle | | | 598,312 | |

| | 30,400 | | Capri Holdings (1) | | | 944,528 | |

| | 21,100 | | Carnival | | | 904,979 | |

| | 7,200 | | Carter’s | | | 721,728 | |

| | 25,500 | | CBS Class B | | | 919,020 | |

| | 20,400 | | Choice Hotels International | | | 1,804,992 | |

| | 91,800 | | eBay | | | 3,235,950 | |

| | 24,400 | | Foot Locker | | | 1,061,644 | |

| | 20,000 | | GameStop Class A (1) | | | 108,800 | |

| | 24,600 | | Gap | | | 399,996 | |

| | 29,900 | | Garmin | | | 2,803,125 | |

| | 25,500 | | General Motors | | | 947,580 | |

| | 79,400 | | Gentex | | | 2,227,170 | |

| | 149,000 | | H&R Block | | | 3,723,510 | |

| | 3,400 | | Helen of Troy (1) | | | 509,184 | |

| | 12,600 | | Hasbro | | | 1,226,106 | |

| | 45,493 | | Home Depot | | | 10,671,748 | |

| | 12,100 | | Kohl’s | | | 620,246 | |

| | 3,628 | | Kontoor Brands | | | 137,864 | |

| | 12,000 | | Lear | | | 1,413,240 | |

| | 7,400 | | Lowe’s | | | 825,914 | |

| | 22,400 | | MasterCraft Boat Holdings (1) | | | 352,800 | |

| | 33,181 | | McDonald’s | | | 6,526,703 | |

| | 39,300 | | Michaels (1) | | | 343,089 | |

| | 55,800 | | Nike Class B | | | 4,996,890 | |

| | 350 | | NVR (1) | | | 1,272,806 | |

| | 5,200 | | O’Reilly Automotive (1) | | | 2,264,652 | |

| | 27,000 | | PulteGroup | | | 1,059,480 | |

| | 19,400 | | Ross Stores | | | 2,127,598 | |

| | 59,900 | | Starbucks | | | 5,065,144 | |

| | 16,200 | | Tapestry | | | 418,932 | |

| | 4,500 | | Tiffany | | | 560,295 | |

| | 59,000 | | TJX | | | 3,401,350 | |

| | 2,600 | | UniFirst | | | 522,184 | |

| | 25,400 | | VF | | | | |

| | | | | | | 95,314,135 | |

| | | | Consumer Staples – 7.8% | |

| | 84,500 | | Altria Group | | | 3,784,755 | |

| | 11,900 | | Brown-Forman Class B | | | 779,688 | |

| | 33,300 | | Church & Dwight | | | 2,329,002 | |

| | 14,800 | | Clorox | | | 2,185,812 | |

| | 198,616 | | Coca-Cola | | | 10,810,669 | |

| | 60,782 | | Colgate-Palmolive | | | 4,169,645 | |

| | 1,300 | | Costco Wholesale | | | 386,243 | |

Schedule of Investments (continued)

October 31, 2019

| Shares | | | | | |

| | 13,100 | | Estee Lauder Class A | | | 2,440,137 | |

| | 26,200 | | Hershey | | | 3,847,994 | |

| | 34,900 | | Kimberly-Clark | | | 4,637,512 | |

| | 34,600 | | Lamb Weston Holdings | | | 2,700,184 | |

| | 6,200 | | Lancaster Colony | | | 862,916 | |

| | 38,400 | | Monster Beverage (1) | | | 2,155,392 | |

| | 68,024 | | PepsiCo | | | 9,330,852 | |

| | 66,691 | | Philip Morris International | | | 5,431,315 | |

| | 115,911 | | Procter & Gamble | | | 14,432,079 | |

| | 7,800 | | USANA Health Sciences (1) | | | 578,058 | |

| | 15,900 | | Walgreens Boots Alliance | | | 871,002 | |

| | 20,723 | | Walmart | | | 2,429,979 | |

| | 1,900 | | WD-40 | | | | |

| | | | | | | 74,519,294 | |

| | | | Energy – 3.8% | |

| | 53,700 | | Antero Resources (1) | | | 134,250 | |

| | 46,300 | | Cabot Oil & Gas | | | 863,032 | |

| | 90,200 | | Callon Petroleum (1) | | | 342,760 | |

| | 75,463 | | Chevron | | | 8,764,273 | |

| | 62,500 | | ConocoPhillips | | | 3,450,000 | |

| | 91,300 | | Diamond Offshore Drilling (1) | | | 482,977 | |

| | 8,500 | | Diamondback Energy | | | 728,960 | |

| | 18,800 | | EOG Resources | | | 1,303,028 | |

| | 173,990 | | ExxonMobil | | | 11,756,504 | |

| | 61,100 | | Gulfport Energy (1) | | | 170,164 | |

| | 11,200 | | HollyFrontier | | | 615,328 | |

| | 76,400 | | Laredo Petroleum Holdings (1) | | | 180,304 | |

| | 33,800 | | Marathon Petroleum | | | 2,161,510 | |

| | 99,000 | | Northern Oil and Gas (1) | | | 194,040 | |

| | 21,700 | | Phillips 66 | | | 2,534,994 | |

| | 43,600 | | ProPetro Holding (1) | | | 337,900 | |

| | 19,500 | | Valero Energy | | | 1,891,110 | |

| | 26,300 | | Whiting Petroleum (1) | | | | |

| | | | | | | 36,077,876 | |

| | | | Financials – 13.0% | |

| | 20,200 | | Affiliated Managers Group | | | 1,613,576 | |

| | 80,300 | | Aflac | | | 4,268,748 | |

| | 11,500 | | American Equity Investment Life Holding | | | 283,820 | |

| | 10,627 | | American Express | | | 1,246,335 | |

| | 30,000 | �� | American Financial Group | | | 3,121,200 | |

| | 3,800 | | American National Insurance | | | 455,924 | |

| | 15,200 | | Ameriprise Financial | | | 2,293,528 | |

| | 16,600 | | Athene Holding Class A (1) | | | 719,610 | |

| | 239,250 | | Bank of America | | | 7,481,348 | |

| | 15,000 | | BB&T | | | 795,750 | |

| Shares | | | | | |

| | 57,200 | | Berkshire Hathaway Class B (1) | | | 12,159,576 | |

| | 2,100 | | BlackRock Class A | | | 969,570 | |

| | 18,436 | | Brighthouse Financial (1) | | | 696,143 | |

| | 25,000 | | Capital One Financial | | | 2,331,250 | |

| | 11,300 | | CBOE Holdings | | | 1,301,195 | |

| | 97,342 | | Citigroup | | | 6,994,996 | |

| | 57,300 | | Citizens Financial Group | | | 2,014,668 | |

| | 24,100 | | Eaton Vance | | | 1,098,960 | |

| | 5,700 | | FactSet Research Systems | | | 1,445,064 | |

| | 37,700 | | Federated Investors Class B | | | 1,204,138 | |

| | 13,800 | | Fidelity National Information Services | | | 1,818,288 | |

| | 1,100 | | First Citizens BancShares Class A | | | 541,112 | |

| | 4,800 | | First Interstate BancSystem Class A | | | 201,408 | |

| | 72,000 | | Franklin Resources | | | 1,983,600 | |

| | 17,400 | | Globe Life | | | 1,693,542 | |

| | 19,004 | | Goldman Sachs Group | | | 4,055,073 | |

| | 10,500 | | International Bancshares | | | 430,080 | |

| | 50,000 | | Invesco | | | 841,000 | |

| | 131,663 | | JPMorgan Chase | | | 16,447,342 | |

| | 23,000 | | Lincoln National | | | 1,299,040 | |

| | 9,100 | | Loews | | | 445,900 | |

| | 6,300 | | M&T Bank | | | 986,139 | |

| | 56,200 | | MetLife | | | 2,629,598 | |

| | 14,200 | | Moody’s | | | 3,133,798 | |

| | 76,900 | | Morgan Stanley | | | 3,541,245 | |

| | 13,700 | | National Retail Properties REIT | | | 807,067 | |

| | 34,400 | | PNC Financial Services Group | | | 5,046,480 | |

| | 5,100 | | Popular | | | 277,746 | |

| | 57,800 | | Principal Financial Group | | | 3,085,364 | |

| | 26,000 | | Prudential Financial | | | 2,369,640 | |

| | 24,800 | | Raymond James Financial | | | 2,070,552 | |

| | 5,500 | | S&P Global | | | 1,418,945 | |

| | 57,300 | | Synchrony Financial | | | 2,026,701 | |

| | 21,000 | | T. Rowe Price Group | | | 2,431,800 | |

| | 73,400 | | Unum Group | | | 2,021,436 | |

| | 195,372 | | Wells Fargo | | | | |

| | | | | | | 124,185,351 | |

| | | | Healthcare – 16.2% | |

| | 41,300 | | Abbott Laboratories | | | 3,453,093 | |

| | 114,781 | | AbbVie | | | 9,130,829 | |

| | 8,700 | | Alexion Pharmaceuticals (1) | | | 916,980 | |

| | 9,600 | | Allergan | | | 1,690,656 | |

| | 44,817 | | Amgen | | | 9,557,225 | |

| | 28,300 | | Baxter International | | | 2,170,610 | |

| | 12,562 | | Biogen (1) | | | 3,752,395 | |

Schedule of Investments (continued)

October 31, 2019

| Shares | | | | | |

| | 136,171 | | Bristol-Myers Squibb | | | 7,812,130 | |

| | 26,700 | | Cerner | | | 1,792,104 | |

| | 4,000 | | Cooper | | | 1,164,000 | |

| | 30,100 | | Danaher | | | 4,148,382 | |

| | 9,900 | | Edwards Lifesciences (1) | | | 2,359,962 | |

| | 67,261 | | Eli Lilly | | | 7,664,391 | |

| | 72,104 | | Gilead Sciences | | | 4,593,746 | |

| | 5,400 | | Idexx Laboratories (1) | | | 1,539,054 | |

| | 20,500 | | Innoviva (1) | | | 238,210 | |

| | 4,800 | | Jazz Pharmaceuticals (1) | | | 603,024 | |

| | 134,784 | | Johnson & Johnson | | | 17,796,879 | |

| | 6,700 | | McKesson | | | 891,100 | |

| | 21,700 | | MEDNAX (1) | | | 476,532 | |

| | 85,169 | | Medtronic | | | 9,274,904 | |

| | 144,507 | | Merck | | | 12,522,977 | |

| | 2,400 | | Mettler-Toledo International (1) | | | 1,691,856 | |

| | 95,700 | | Mylan (1) | | | 1,832,655 | |

| | 324,747 | | Pfizer | | | 12,460,542 | |

| | 44,384 | | Quest Diagnostics | | | 4,493,880 | |

| | 11,600 | | ResMed | | | 1,715,872 | |

| | 33,600 | | SIGA Technologies (1) | | | 186,480 | |

| | 5,800 | | STERIS | | | 821,106 | |

| | 15,999 | | Stryker | | | 3,460,104 | |

| | 21,200 | | Thermo Fisher Scientific | | | 6,401,976 | |

| | 47,400 | | UnitedHealth Group | | | 11,977,980 | |

| | 24,800 | | Varian Medical Systems (1) | | | 2,996,088 | |

| | 12,308 | | Waters (1) | | | 2,604,619 | |

| | 2,800 | | West Pharmaceutical Services | | | | |

| | | | | | | 154,595,093 | |

| | | | Industrials – 10.8% | |

| | 29,535 | | 3M | | | 4,872,980 | |

| | 24,300 | | Allegion | | | 2,819,772 | |

| | 49,300 | | Allison Transmission Holdings Class A | | | 2,149,973 | |

| | 36,600 | | AMETEK | | | 3,354,390 | |

| | 11,700 | | Boeing | | | 3,976,947 | |

| | 7,900 | | Brady Class A | | | 445,086 | |

| | 24,400 | | Caterpillar | | | 3,362,320 | |

| | 21,900 | | CH Robinson Worldwide | | | 1,656,516 | |

| | 7,800 | | Cintas | | | 2,095,626 | |

| | 15,000 | | Copart (1) | | | 1,239,600 | |

| | 15,300 | | Cummins | | | 2,638,944 | |

| | 26,900 | | Delta Air Lines | | | 1,481,652 | |

| | 14,200 | | Deluxe | | | 735,986 | |

| | 14,100 | | Donaldson | | | 743,634 | |

| | 20,300 | | Dover | | | 2,108,967 | |

| Shares | | | | | |

| | 26,100 | | Eaton | | | 2,273,571 | |

| | 64,271 | | Emerson Electric | | | 4,508,611 | |

| | 9,600 | | Ennis | | | 188,064 | |

| | 42,500 | | Expeditors International of Washington | | | 3,099,950 | |

| | 60,600 | | Fastenal | | | 2,177,964 | |

| | 37,950 | | Fortive | | | 2,618,550 | |

| | 17,200 | | Graco | | | 777,440 | |

| | 41,600 | | GrafTech International | | | 502,528 | |

| | 32,191 | | Honeywell International | | | 5,560,351 | |

| | 16,000 | | Hubbell Class B | | | 2,267,200 | |

| | 10,700 | | IDEX | | | 1,664,171 | |

| | 22,400 | | Illinois Tool Works | | | 3,776,192 | |

| | 21,700 | | Landstar System | | | 2,455,355 | |

| | 10,659 | | Lincoln Electric Holdings | | | 954,727 | |

| | 9,900 | | Lockheed Martin | | | 3,729,132 | |

| | 29,000 | | Meritor (1) | | | 638,870 | |

| | 3,400 | | MSA Safety | | | 408,238 | |

| | 19,600 | | MSC Industrial Direct Class A | | | 1,434,916 | |

| | 23,600 | | Norfolk Southern | | | 4,295,200 | |

| | 2,500 | | Old Dominion Freight Line | | | 455,200 | |

| | 9,200 | | Parker Hannifin | | | 1,688,108 | |

| | 10,500 | | Regal-Beloit | | | 777,525 | |

| | 34,400 | | Robert Half International | | | 1,970,088 | |

| | 5,500 | | Rockwell Automation | | | 945,945 | |

| | 10,200 | | Roper Technologies | | | 3,436,992 | |

| | 14,900 | | Snap-on | | | 2,423,783 | |

| | 8,700 | | Timken | | | 426,300 | |

| | 13,300 | | Toro | | | 1,025,829 | |

| | 37,500 | | Union Pacific | | | 6,204,750 | |

| | 4,000 | | United Rentals (1) | | | 534,280 | |

| | 11,095 | | United Technologies | | | 1,593,020 | |

| | 15,000 | | Verisk Analytics Class A | | | 2,170,500 | |

| | 22,100 | | Waste Management | | | | |

| | | | | | | 103,145,584 | |

| | | | Information Technology – 22.3% | |

| | 19,352 | | Accenture Class A | | | 3,588,248 | |

| | 12,600 | | Adobe (1) | | | 3,501,918 | |

| | 27,800 | | Amdocs | | | 1,812,560 | |

| | 22,400 | | Amphenol Class A | | | 2,247,392 | |

| | 19,100 | | Analog Devices | | | 2,036,633 | |

| | 6,500 | | ANSYS (1) | | | 1,430,975 | |

| | 153,373 | | Apple | | | 38,153,067 | |

| | 28,000 | | Automatic Data Processing | | | 4,542,440 | |

| | 7,200 | | Broadcom | | | 2,108,520 | |

| | 21,200 | | Broadridge Financial Solutions | | | 2,654,664 | |

Schedule of Investments (continued)

October 31, 2019

Shares

| | | | | |

| | 244,985 | | Cisco Systems | | | 11,639,237 | |

| | 27,800 | | Citrix Systems | | | 3,026,308 | |

| | 62,523 | | Cognizant Technology Solutions Class A | | | 3,810,152 | |

| | 20,900 | | DXC Technology | | | 578,303 | |

| | 1,600 | | Fair Isaac (1) | | | 486,464 | |

| | 40,500 | | Fiserv (1) | | | 4,298,670 | |

| | 104,800 | | HP | | | 1,820,376 | |

| | 229,974 | | Intel | | | 13,000,430 | |

| | 64,894 | | International Business Machines | | | 8,678,275 | |

| | 14,100 | | Intuit | | | 3,630,750 | |

| | 8,500 | | Jack Henry & Associates | | | 1,203,260 | |

| | 5,700 | | Lam Research | | | 1,544,928 | |

| | 28,900 | | Mastercard Class A | | | 7,999,809 | |

| | 34,700 | | Maxim Integrated Products | | | 2,035,502 | |

| | 45,200 | | Micron Technology (1) | | | 2,149,260 | |

| | 301,450 | | Microsoft | | | 43,218,886 | |

| | 6,600 | | NVIDIA | | | 1,326,732 | |

| | 114,581 | | Oracle | | | 6,243,519 | |

| | 35,400 | | Paychex | | | 2,960,856 | |

| | 60,700 | | PayPal Holdings (1) | | | 6,318,870 | |

| | 8,000 | | Progress Software | | | 319,040 | |

| | 12,277 | | QUALCOMM | | | 987,562 | |

| | 9,400 | | salesforce.com (1) | | | 1,471,006 | |

| | 10,000 | | TE Connectivity | | | 895,000 | |

| | 42,922 | | Texas Instruments | | | 5,064,367 | |

| | 70,900 | | Visa Class A | | | 12,681,174 | |

| | 64,100 | | Xerox Holdings | | | 2,174,913 | |

| | 19,600 | | Xilinx | | | | |

| | | | | | | 213,418,570 | |

| | | | Materials – 0.6% | |

| | 1,700 | | Air Products & Chemicals | | | 362,542 | |

| | 6,400 | | Eastman Chemical | | | 486,656 | |

| | 14,100 | | LyondellBasell Industries Class A | | | 1,264,770 | |

| | 17,300 | | Newmont Mining | | | 687,329 | |

| | 21,200 | | Packaging Corp. of America | | | 2,320,552 | |

| | 3,649 | | Sonoco Products | | | 210,547 | |

| | 13,900 | | Steel Dynamics | | | 422,004 | |

| | | | | | | 5,754,400 | |

| | | | Real Estate – 2.2% | |

| | 117,600 | | Apple Hospitality REIT | | | 1,938,048 | |

| | 12,700 | | CareTrust REIT | | | 307,848 | |

| | 5,700 | | Essex Property Trust REIT | | | 1,864,641 | |

| | 19,900 | | Highwoods Properties REIT | | | 931,320 | |

| | 127,800 | | Host Hotels & Resorts REIT | | | 2,094,642 | |

| | Shares | | | | | | |

| | 49,400 | | Kimco Realty REIT | | | 1,065,064 | |

| | 7,900 | | Life Storage REIT | | | 860,468 | |

| | 3,649 | | LTC Properties REIT | | | 189,201 | |

| | 32,800 | | Newmark Group Class A | | | 348,336 | |

| | 11,200 | | Omega Healthcare Investors REIT | | | 493,248 | |

| | 90,400 | | Park Hotels & Resorts REIT | | | 2,101,800 | |

| | 2,600 | | PS Business Parks REIT | | | 469,430 | |

| | 11,100 | | Public Storage REIT | | | 2,473,746 | |

| | 19,200 | | Regency Centers REIT | | | 1,291,008 | |

| | 31,100 | | RLJ Lodging Trust REIT | | | 510,351 | |

| | 21,800 | | Simon Property Group REIT | | | 3,284,824 | |

| | 15,600 | | Tanger Factory Outlet Centers REIT | | | 251,472 | |

| | 25,700 | | Weingarten Realty Investors REIT | | | | |

| | | | | | | 21,290,908 | |

| | | | Utilities – 1.1% | |

| | 28,000 | | AES | | | 477,400 | |

| | 3,700 | | Ameren | | | 287,490 | |

| | 3,700 | | American Electric Power | | | 349,243 | |

| | 3,600 | | American Water Works | | | 443,772 | |

| | 4,500 | | Atmos Energy | | | 506,160 | |

| | 18,000 | | Centerpoint Energy | | | 523,260 | |

| | 13,199 | | Consolidated Edison | | | 1,217,212 | |

| | 6,000 | | Dominion Resources | | | 495,300 | |

| | 2,300 | | DTE Energy | | | 292,836 | |

| | 5,000 | | Eversource Energy | | | 418,700 | |

| | 40,300 | | Exelon | | | 1,833,247 | |

| | 8,200 | | NextEra Energy | | | 1,954,388 | |

| | 27,200 | | PPL | | | 910,928 | |

| | 1,800 | | Sempra Energy | | | | |

| | | | | | | | |

| | | | Total United States | | | | |

| | | | TOTAL COMMON STOCK | | | | |

| | | | (Cost $598,897,258) | | | | |

| | | | TOTAL INVESTMENTS IN SECURITIES – 99.1% | |

| | | | (Cost $598,897,258) | | | | |

| | | | OTHER ASSETS LESS LIABILITIES – 0.9% | | | | |

| | | | NET ASSETS – 100% | | | | |

| (1) | Denotes non-income producing security. |

Schedule of Investments (concluded)

October 31, 2019

The open futures contracts held by the Fund at October 31, 2019, are as follows:

Type of

Contract | | Number of

Contracts

Long | | Expiration

Date | | Notional

Amount | | | Value | | | Unrealized

Appreciation | |

| S&P 500 Index E-MINI | | | 25 | | Dec-2019 | | | | | | | | | | | | |

A summary of the outstanding forward foreign currency contracts held by the Fund at October 31, 2019, is as follows:

| Counterparty | Settlement

Date | Currency

to Deliver | Currency

to Receive | | Unrealized Appreciation | |

| Royal Bank of Canada | 12/11/19 | CAD 14,853,935 | USD 11,346,790 | | | | |

CAD — Canadian Dollar