UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

ENTOURAGE MINING LTD.

¨ REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE

SECURITIES EXCHANGE ACT OF 1934

OR

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES

EXCHANGE ACT OF 1934, for the fiscal year ended: December 31, 2003

OR

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES

EXCHANGE ACT OF 1934, for the transition period from

ENTOURAGE MINING LTD.

(Exact name of registrant as specific in its charter)

Province of British Columbia, Canada

(Jurisdiction of incorporation or organization)

525 Seymour Street Suite 212

Vancouver, British Columbia, Canada V6B 3H7

(Address of principal executive offices, including Postal Code)

Registrant's area code and telephone number:778-893-4471

Securities to be registered pursuant to Section 12(g) of the Act: None

Title of each class: Common Stock without par value

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Indicate the number of outstanding shares of each of the issuer's classes of capital or common stock as of the close of the period covered by the annual report -15,130,005 shares of common stock

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

x YES ¨ NO

Indicate by check mark which financial statement item the registrant has elected to follow:

¨ ITEM 17 x ITEM 18

(APPLICABLE ONLY TO REGISTRANTS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13, or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court.

x YES ¨ NO

EXHIBIT INDEX BEGINS ON PAGE 48

Table of Contents

2

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISORS

Not Applicable

3

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable

ITEM 3. KEY INFORMATION

A. SELECTED FINANCIAL DATA

Selected Consolidated Financial Data

The selected historical data presented below has been derived from our financial statements. The financial statements for the periods ending December 31,2003, 2002, 2001, 2000 and 1999. have been audited Morgan & Company, Chartered Accountants.

Our financial statements are presented in Canadian dollars and have been prepared in accordance with generally accepted accounting principles in the United States of America ("U.S. GAAP").

The following table summarizes certain financial information and should be read in conjunction with the financial information in Item 5. We have not declared a dividend during the three months ended March 31, 2004 or the five years ended December 31, 2003, 2002, 2001, 2000 and 1999. There were no fluctuations in revenues and net income (loss) between the periods stated in the table below since we were inoperative during the applicable years. For the reasons set forth herein the information shown below may not be indicative of our future results of operation.

Condensed Statements of Operations for the three months ended March 31, 2003 and the five years ended December 31, 2003:

| For the three months | ||||||||||||||

| ended March 31, | For the years ended December 31 | |||||||||||||

| �� | ||||||||||||||

| 2004 | 2003 | 2003 | 2002 | 2001 | 2000 | 1999 | ||||||||

| PER U.S. GAAP | ||||||||||||||

| Revenues | Nil | Nil | Nil | Nil | Nil | Nil | Nil | |||||||

| Net Loss | (37,719 | ) | (24,747 | ) | (319,515 | ) | (58,749 | ) | (66,855 | ) | (70,046 | ) | ||

| Loss per share | (0.01 | ) | (0.01 | ) | (0.04 | ) | (0.01 | ) | (0.01 | ) | (0.01 | ) | (0.01 | ) |

Note: Diluted loss per share has not been presented as the effect on basic loss per share would be anti-dilutive.

4

Condensed Balance Sheet Information for the three months ended March 31, 2004 and the five years ended December 31, 2003

| As at March 31, | As at December 31, | ||||||

| 2004 | 2003 | 2003 | 2002 | 2001 | 2000 | 1999 | |

| PER U.S. GAAP | |||||||

| Total Assets | 23,972 | 186,546 | 106,702 | Nil | 3,986 | 3,870 | 2,829 |

| Net Working Capital (Deficit) | -239,583 | -186,546 | -230,498 | -161,799 | -303,042 | -244,293 | -177,438 |

| Shareholders' Deficiency | -239,583 | -186,546 | -230,498 | -161,799 | -303,042 | -244,293 | -177,438 |

| Weighted Average Number | 15,732,889 | 9,130,005 | 9,127,950 | 5,380,005 | 5,380,005 | 5,380,005 | 5,380,005 |

Exchange Rates

The following table sets forth the rate of exchange for the Canadian Dollar at the end of the five most recent fiscal periods ended December 31, the average rates for the period. Exchange rates are also disclosed for the preceding six monthly periods.

| Months | C$ to US$ |

| Jan 04 | 1.296 |

| Feb 04 | 1.329 |

| Mar 04 | 1.328 |

| Apr 04 | 1.342 |

| May 04 | 1.378 |

| June 04 | 1.358 |

| Years Ending | C$ to US$ |

| Dec 2003 | 1.401 |

| Dec 2002 | 1.570 |

| Dec 2001 | 1.548 |

| Dec 2000 | 1.485 |

| Dec 1999 | 1.486 |

For purposes of this table, the rate of exchange means the noon buying rate from the Ban of Canada. The table sets forth the number of Canadian dollars required under that formula to buy one U.S. Dollar. The average rate means the average of the exchange rates on the last day of each month during the period.

5

The exchange rate was $1.31 on March 31, 2004. The above information was obtained from the Bank of Canada and we believe closely approximate the rates certified for customs purposes by the Federal Reserve Bank in New York.

B. CAPITALIZATION AND INDEBTEDNESS

Not Applicable

C. REASON FOR THE OFFER AND USE OF PROCEEDS

Not applicable

D. RISK FACTORS

Because our auditors have issued a going concern opinion and because our officers and directors will not loan any money to us, we may not be able to achieve our objectives and may have to suspend or cease operations.Our auditors have issued a going concern opinion. This means that there is substantial doubt that we can continue as an ongoing business for the next twelve months. Because our officers and directors, at present, are unwilling to loan or advance any additional capital to us, we believe that if we do not raise additional capital, we may have to suspend or cease operations within six months.

6

Because the probability of an individual prospect ever having reserves is extremely remote, in all probability our properties do not contain any reserves, and any funds spent on exploration will be lost.Looking for mineralized material below the surface of the earth is very speculative. While equipment can detect mineralized material beneath the surface of the earth, the detection devices can not determine the type of mineralized material. The type of mineralized material can only be determined by extracting it from the ground. The likelihood of taking an unexplored piece of land and finding mineralized material is improbable. The likelihood of locating a valuable reserve is remote. Because the probability of an individual prospect ever having reserves is extremely remote, in all probability our properties do not contain any reserves, and any funds spent on exploration will be lost.

We lack an operating history and have losses that we expect to continue into the future.As a result, we may have to suspend or cease operations.We were incorporated in June 1995 and we just begun our proposed business operations and have not realized any revenues in the last 5 years. We have no operating history upon which an evaluation of our future success or failure can be made. Our net loss since inception is $958,486 as of December 31, 2003 and $996,205 as of March 31, 2004. Our ability to achieve and maintain profitability and positive cash flow is dependent upon

| * | our ability to locate, explore and develop a profitable mineral property | |

| * | our ability to generate revenues | |

| * | our ability to reduce exploration costs. |

Based upon current plans, we expect to incur operating losses in future periods. We have not generated any revenues from our operations and we don't anticipate any in the foreseeable future. This will happen because there are expenses associated with the research and exploration of our mineral properties. We may not guarantee we will be successful in generating revenues in the future. Failure to generate revenues will cause us to go out of business.

Because only one of our directors, John R. Poloni, has technical training or experience in exploring for, starting, and operating a mine, we will have to hire qualified personnel. If we cannot locate qualified personnel, we may have to suspend or cease operations that will result in the loss of your investment.Only one of our directors, John R. Poloni has experience with exploring for, starting, and operating a mine. None of our officers have any technical training or experience in exploring for, starting, and operation a mine. As such, we will have to hire qualified persons to perform surveying, exploration, and excavation of our properties. The two other officers and directors, Hart and Kennedy, have no direct training or experience in these areas and as a result may not be fully aware of many of the specific requirements related to working within the industry. Their decisions and choices may not take into account standard engineering or managerial approaches, mineral exploration companies commonly use. Consequently our operations, earnings and ultimate financial success could suffer irreparable harm due to management's lack of experience in this industry. As a result we may have to suspend or cease operations that will result in the loss of your investment.

7

We have no known mineral reserves. Without mineral reserves we can not generate income and if we cannot generate income we will have to cease operations which result in the loss your investment. We have no known mineral reserves. Without mineral reserves, we have nothing to economically remove. If we have nothing to economically remove from the property, we cannot generate income and if we cannot generate income we will have to cease operation that will result in the loss of your investment.

Weather interruptions in the Yukon Territory may delay our proposed exploration operations which will extend the time revenues will not be generated and you could lose your investment.Our proposed exploration work can only be performed approximately four to five months out of the year. This is because rain and snow cause travel to our claims to be difficult during seven to eight months of the year. During winter, we are unable to conduct exploration operations on our property. This will delay exploration and subsequent removal of any mineralized material, should any be discovered. As a result of the delay in removing mineralized material, no revenue will be generated by us and you could lose your investment.

Because we are small and do not have much capital, we must limit our exploration and as a result may not find any minerals. Without any minerals, we cannot generate revenues and you will lose your investment.Because we are small and do not have much capital, we must limit our exploration. Because we may have to limit our exploration, we may not find any minerals, even though our properties may contain mineralized material. Without any minerals we cannot generate revenues and you will lose your investment.

Because Messrs., Poloni and Hart have other outside business activities and will only be devoting 10% of their time to our operations, our operations may be sporadic which may result in periodic interruptions or suspensions of exploration.Only Mr. Kennedy devotes 100% of his time to the operations of the Company.Because Messrs., Poloni and Hart, have other outside business activities and will only be devoting 10% of their time to our operations, our operations may be sporadic and occur at times which are convenient to Messrs., Poloni, and Hart. Only Mr. Kennedy devotes 100% of his time to our operations and as a result, exploration of our properties may be periodically interrupted or suspended.

Because title to our properties are held in the name of another entity, if it transfers our properties to someone other than us, we will cease operations and you will lose your investment.Title to our properties are not held in our name. Title to our properties is recorded in the name of Expatriate Resources Ltd. Under the terms of an agreement dated November 13, 2002, we are entitled to earn a 60% interest in the properties provided we pay Expatriate Resources Ltd. a total $90,000 and spend a total $500,000 on the properties and pay YK Group $60,000 by November 1, 2007. To date, none of the $90,000 has been paid. If Expatriate Resources Ltd. transfers our properties or our interest to a third person, the third person will obtain title or the interest designated for us and we will have nothing. We are not entitled to any notice by Expatriate Resources if they decided to sell the properties or our contractual interest. If Expatriate does sell the properties or our interest therein, we will be harmed in that we will not own any properties or interests in the properties and we will have to cease operations and you will lose your investment.

8

We may not have access to all of the supplies and materials we need to begin exploration that could cause us to delay or suspend operations.Competition and unforeseen limited sources of supplies in the industry could result in occasional spot shortages of supplies, such as dynamite, and certain equipment such as bulldozers and excavators that we might need to conduct exploration. We have not attempted to locate or negotiate with any suppliers of products, equipment or materials. Our exploration efforts will be continued on the receipt of further funding. Once further funding is obtained we will attempt to locate products, equipment and materials. If we cannot find the products and equipment we need we will have to suspend our exploration plans until we do find the products and equipment we need. Suspension or operations will result in the generation of revenues.

Although our stock trades on the OTC Bulletin Board there is no guarantee of liquidity and you may not be able to resell your stockAlthough our stock trades on the OTC Bulletin Board there is no guarantee of liquidity and reselling your stock may be difficult.

Because our securities are subject to penny stock rules, you may have difficulty reselling your shares.Our shares as penny stocks are covered by Section 15(g) of the Securities Exchange Act of 1934 which imposes additional sales practice requirements on broker/dealers who sell the Company's securities including the delivery of a standardized disclosure document; disclosure and confirmation of quotation prices; disclosure of compensation the broker/dealer receives; and, furnishing monthly account statements. For sales of our securities, the broker/dealer must make a special suitability determination and receive from its customer a written agreement prior to making a sale. The imposition of the foregoing additional sales practices could adversely affect a shareholder's ability to dispose of his stock.

Because all of our assets and our officers and directors are located outside the United States of America, it may be difficult for an investor to enforce within the United States any judgments obtained against us or any of our officers and directors.All of our assets are located outside of the United States and we do not currently maintain a permanent place of business within the United States. In addition, our directors and officers are nationals and/or residents of countries other than the United States, and all or a substantial portion of such persons' assets are located outside the United States. As a result, it may be difficult for an investor to effect service of process or enforce within the United States any judgments obtained against us or our officers or directors, including judgments predicated upon the civil liability provisions of the securities laws of the United States or any state thereof. In addition, there is uncertainty as to whether the courts of Canada and other jurisdictions would recognize or enforce judgments of United States courts obtained against us or our directors and officers predicated upon the civil liability provisions of the securities laws of the United States or any state thereof, or be competent to hear original actions brought in Canada or other jurisdictions against us or our directors and officers predicated upon the securities laws of the United States or any state thereof.

We may become a passive foreign investment company, or PFIC, which could result in adverse U.S. tax consequences to U.S. investors.Since PFIC status will be determined by us on an annual basis and will depend on the composition of our income and assets from time to time (as further discussed below), we cannot assure you that we will not be considered a PFIC for any taxable year. Such a characterization could result in adverse U.S. tax consequences to you if you are a U.S. investor. In particular, absent an election described below, a U.S. investor would be subject to U.S. federal income tax at ordinary income tax rates, plus a possible interest charge, in respect of gain derived from a disposition of our shares, as well as certain distributions by us. In addition, a step-up in the tax basis of our shares would not be available upon the death of an individual shareholder. For this reason, if we are treated as a PFIC for any taxable year and you are a U.S. investor, you may desire to make an election to treat us as a "qualified electing fund" with respect to your shares (a "QEF election"), in which case you will be required to take into account apro-rata share of our earnings and net capital gain for each year, regardless of whether we make any distributions to you. As an alternative to the QEF election, a U.S. investor may be able to make an election to "mark-to-market" our shares each taxable year and recognize ordinary income pursuant to such election based upon increases in the value of our shares. We will be classified as a PFIC for U.S. federal income tax purposes if 50% or more of our assets, including goodwill (based on an annual quarterly average), are passive assets, or 75% or more of our annual gross income is derived from passive assets. The calculation of goodwill will be based, in part, on the then market value of our common shares, which is subject to change. In addition, the composition of our income and assets will be affected by how we spend the cash we raise in this offering.

9

Because we may issue additional shares of common stock in public offerings or private placements, your ownership interest is us may be diluted.Because we may issue shares of common stock in public offerings or private placements in order to raise capital for our operations, your ownership interest may be diluted which results in your percentage of ownership in us decreasing.

ITEM 4. INFORMATION ON THE COMPANY

A. HISTORY AND DEVELOPMENT OF THE COMPANY

Our Registered Office in British Columbia is located at 1111 West Hastings Street, Suite 708, Vancouver, British Columbia V6E 2J3. Our head office and principal office is located at 212-525 Seymour Street, Vancouver, British Columbia V6B 3H7.

We were originally incorporated under the name, Entourage Holdings Ltd., pursuant to the Company Act (British Columbia) on June 16, 1995. On June 25, 1996, we changed our name to Entourage Mining Ltd.

On February 18, 1998, we became a reporting Issuer as defined under the Securities Act of the Province of British Columbia in British Columbia, Canada.

We have one subsidiary company, Entourage USA Inc., located at 6121 Lakeside Drive, Suite 260, Reno, Nevada 89511. The subsidiary company will seek mineral prospects in the United States.

B. BUSINESS OVERVIEW

We are a natural resource company engaged in the acquisition and exploration of natural resource properties. We commenced operations in 1996 and currently have entered into an option agreement to acquire a 60% interest in the Finlayson Properties consisting of 2,626 un-surveyed quartz claims described below and intend to seek and acquire additional properties worthy of exploration and development.

We are an exploration stage company and there is no assurance that a commercially viable mineral deposit exists on any of the property, and further exploration will be required before a final evaluation as to the economic and legal feasibility is determined.

General

We were incorporated in the Province of British Columbia on June 16, 1995 as Entourage Holdings Ltd. On June 25, 1996, we changed our name to Entourage Mining Ltd. We changed our name because we wanted our name to reflect the business sector we intended to operate in.

We are engaged in the acquisition and exploration of mining properties. Our Registered Office in British Columbia is located at 1111 West Hastings Street, Suite 708, Vancouver, British Columbia V6E 2J3. Our head office and principal office is located at 525 Seymour Street, Vancouver, British Columbia V6B 3H7. Our telephone number is (778)-893-4471. Our offices today are shared with another mining company and our rent is $668.75 per month.

Entourage Mining Ltd. has no plans to change its business activities or to combine with another business, and is not aware of any events or circumstances that might cause its plans to change.

In March 2003, we entered into an agreement with the YK Group, a syndicate of unrelated third party comprised of Paul Shatzko, Maryl Shatzko, Carl Verley, Shirley Verley, William Weston and Margaret Weston, to acquire YK Group's interest in an option agreement dated November 13, 2002, entered into between the YK Group and Expatriate Resources Ltd. Upon the payment of $60,000 and delivery of 6,000,000 common restricted shares of our common stock, the YK Group will assign its interest to us in the November 13, 2002 option agreement. On April 26, 2003, our shareholders approved the agreement and as of May 17, 2003 we became obligated to perform the YK Group's obligations under the terms of the November 13, 2002 option agreement.

10

As of the date hereof, we have paid $ -0- of the $60,000 due the YK Group and on May 17, 2003, we issued the 6,000,000 shares of common stock to the YK Group. As of today's date we have received an assignment of YK Group's interest in the option agreement although we have not paid the YK Group $60,000.

Under the terms of our agreement with the YK Group, we are obligated to pay to the YK Group CDN$60,000 sixty days after Entourage is financed and as of today's date the $60,000 remains unpaid.

We issued the 6,000,000 shares of common stock to the individuals named below the in the amounts set forth opposite their names:

| Paul Shatzko | 1,000,000 | |

| Maryl Shatzko | 1,000,000 | |

| Carl Verley | 1,000,000 | |

| Shirley Verley | 1,000,000 | |

| William P. Weston | 1,500,000 | |

| Margaret M. Weston | 500,000 |

Under British Columbia law, the shares may not be resold for a period of four months from the date of issue, which date has now passed .

As of today's date we have raised $219,450 that was expended in our fall 2003 exploration season and for general working capital purposes; the Company has not yet paid the YK Group the $60,000-. We do not have to pay YK Group until we finance Entourage, which may never occur.

By assuming YK Group's obligations under the option agreement and subject to the performance of the terms and conditions of the option agreement, we may acquire a 60% interest in and to the Finlayson Properties. The Finlayson Properties contain two thousand six hundred twenty six (2626) un-surveyed mining claims in the Watson Lake Mining District and the Whitehorse Mining District, in the Yukon Territory.

Under the terms of the option agreement between the YK Group and Expatriate Resources, we are obligated to pay to Expatriate, CDN$90,000 in cash and expend CDN$500,000 on the properties. Payment of the cash is as follows:

| On November 13, 2002 | $10,000 paid | |

| On or before November 1, 2003 | $10,000 paid | |

| On or before November 1, 2004 | 10,000 | |

| On or before November 1, 2005 | 15,000 | |

| On or before November 1, 2006 | 15,000 | |

| On or before November 1, 2007 | 30,000 |

Aggregate expenditure on the properties is as follows:

| On or before November 1, 2003 | $100,000 spent | |

| On or before November 1, 2004 | $150,000 spent | |

| On or before November 1, 2005 | $200,000 spent | |

| On or before November 1, 2006 | $250,000 | |

| On or before November 1, 2007 | $500,000 |

Upon payment of the foregoing, we will be assigned a 60% interest in and to the Finlayson properties.

Time being the essence of agreement, if the payments or expenditures do not occur at the precise time set forth therein, the agreement will be terminated.

In Quarter 1, 2004 we raised sufficient funds to make the cash payments and the exploration expenditures from friends and relatives of current directors pursuant to exemptions in the Canadian provincial securities acts. As of today's date we have raised $219,450 by way of a private placement in Q1. If we don't raise the balance of the funds and make the payments described above the option agreement will terminate and we will cease or suspend operations.

11

Pursuant to the terms of Article 5 of the agreement, upon satisfying the provisions of Article 4 thereof, we will enter into a joint ventures agreement Expatriate. We will have a 60% participating interest and Expatriate will have a 40% working interest. Upon formation of the joint venture, the parties will form a management committee to determine the activities of the joint venture. We have not entered into a joint venture agreement as of the date hereof and will not do so until we earn our interest.

Aurora Geosciences Ltd. was paid $5,283.80 to review and make recommendations on the Finlayson Properties regarding emerald potential and for further exploration work. The amount was paid by the YK Group and will be reimbursed to the YK Group out of the $60,000 cash payment due and payable under the Assignment Agreement. These are the only services we have paid to Aurora Geosciences Ltd. to date. Aurora Geosciences Ltd. was hired by the YK Group and accepted by us because we believe they could provide expert independent advice concerning the emerald potential of the Finlayson Properties. Aurora Geosciences Ltd. has been engaged in mining exploration for the past 18 years. Michael A. Power is a registered professional engineer and geoscientist in the Province of British Columbia and a professional geophysicist with the Northwest Territories Association of Professional Engineers. Mr. Power holds a Bachelor of Science degree with honors in geology and a Masters of Science degree from the University of Alberta. Scott Casselman is a member of the Association of Professional Engineers and geoscientists of British Columbia. Mr. Casselman holds a Bachelor of Science degree in geology from Carleton University in Ottawa.

All Canadian lands and minerals, which have not been granted to private persons, are owned by either the federal or provincial governments in the name of Her Majesty. Ungranted minerals are commonly known as Crown minerals. Ownership rights to Crown minerals are vested by the Canadian Constitution in the province where the minerals are located. Most privately held mineral titles are acquired directly from the Crown. The Finlayson properties are one such acquisition. Accordingly, fee simple title to the Finlayson properties resides with the Crown and Expatriate Resources was granted a lease by the Crown to explore for minerals. The lease covering the Finlayson claims was issued pursuant to the Yukon Quartz Mining Act. The lessee, Expatriate Resources has exclusive rights to mine and recover all of the minerals contained within the surface boundaries of the lease continued vertically downward. To the best of our knowledge, there are no native land claims that affect our title.

Save and except for the terms of the November 13, 2002 option agreement, the properties are unencumbered and there are no competitive conditions which affect the properties. Further, there is no insurance covering the properties and we believe that no insurance is necessary since the properties are unimproved and contain no buildings or improvements.

To date we have retained the services of Aurora Geoscience to analyze proprietary data gathered from the claims and acquired from Expatriate Resources, as well as analyze other public domain data from the area. We are presently in the exploration stage and we cannot guarantee that a commercially viable mineral deposit or reserve exists on the properties until further exploration is done and a comprehensive evaluation concludes economic and legal feasibility.

We selected the properties at the suggestion of Aurora Geosciences, Ltd., and Carl Verley, P.Geo. and a member of the YK Group, who has informed us that emeralds were discovered nearby. He said that because emeralds were discovered nearby, there might be emeralds on our properties. We did not review any technical information prior to selecting the properties. We relied entirely on our consultants, Aurora Geosciences, Ltd. and Carl Verley. Our President, Mr. Kennedy, visited the property in September 2003 during our exploration program.

The following is a description of the claims encompassing the Finlayson Properties.

12

| Claim | Claim | Number | Record | Record | |||||

| Claim | Number | Number | of | Number | Number | Mining | |||

| Group | From | To | Fractions | claims | From | To | Expiry Date | District | Map Sheet |

| Blade | 17 | 1 | YB61574 | 17-Mar-05 | Watson Lake | 105-G-07 | |||

| BlueLine | 1 | 20 | 20 | YB60514 | YB60533 | 17-Mar-09 | Watson Lake | 105-G-07 | |

| BlueLine | 21 | 32 | 12 | YB61472 | YB61483 | 17-Mar-09 | Watson Lake | 105-G-07 | |

| BlueLine | 33 | 34 | 2 | YB89605 | YB89606 | 17-Mar-07 | Watson Lake | 105-G-07 | |

| Box | 1 | 20 | 20 | YB59163 | YB59182 | 17-Mar-09 | Watson Lake | 105-G-10 | |

| Box | 21 | 24 | 4 | YB60837 | YB60840 | 17-Mar-08 | Watson Lake | 105-G-10 | |

| Box | 39 | 40 | 2 | YB93657 | YB93658 | 17-Mar-08 | Watson Lake | 105-G-10 | |

| Box | 41 | 105 | 65 | YB94174 | YB94238 | 10-Sep-04 | Watson Lake | 105-G-10 | |

| Box | 107 | 120 | 14 | YB94239 | YB94252 | 10-Sep-04 | Watson Lake | 105-G-10 | |

| Breakaway | 1 | 10 | 10 | YB57481 | YB57490 | 16-Mar-07 | Whitehorse | 105-K-01 | |

| Breakaway | 11 | 14 | 4 | YB57645 | YB57648 | 16-Mar-07 | Whitehorse | 105-K-01 | |

| Breakaway | 15 | 40 | 26 | YB66343 | YB66368 | 16-Mar-05 | Whitehorse | 105-K-01 | |

| Bug | 1 | 22 | 22 | YB93298 | YB93319 | 26-Jul-06 | Watson Lake | 105-G-08 | |

| Bug | 23 | 24 | F | 2 | YB93320 | YB93321 | 27-Jul-06 | Watson Lake | 105-G-08 |

| Bug | 25 | 27 | 3 | YB93322 | YB93324 | 28-Jul-06 | Watson Lake | 105-G-08 | |

| Buzzer | 9 | 1 | YB69066 | 17-Mar-05 | Watson Lake | 105-G-01 | |||

| Clarence | 26 | 1 | YB61709 | 17-Mar-05 | Watson Lake | 105-G-10 | |||

| Cup | 1 | 16 | 16 | YB87695 | YB87710 | 17-Mar-06 | Watson Lake | 105-G-08 | |

| Cup | 17 | 18 | F | 2 | YB87711 | YB87712 | 17-Mar-06 | Watson Lake | 105-G-08 |

| Cup | 19 | 22 | 4 | YB87713 | YB87716 | 17-Mar-06 | Watson Lake | 105-G-08 | |

| Cup | 23 | 24 | F | 2 | YB87717 | YB87718 | 17-Mar-06 | Watson Lake | 105-G-08 |

| Dan | 1 | 16 | 16 | YB92726 | YB92741 | 02-Aug-04 | Watson Lake | 105-G-08 | |

| Goal | 1 | 24 | 24 | YB56129 | YB56152 | 17-Mar-14 | Watson Lake | 105-G-07 | |

| Goal | 25 | 44 | 20 | YB60584 | YB60603 | 17-Mar-11 | Watson Lake | 105-G-07 | |

| Goal | 45 | 54 | 10 | YB60604 | YB60613 | 17-Mar-15 | Watson Lake | 105-G-07 | |

| Goal | 55 | 94 | 40 | YB60614 | YB60653 | 17-Mar-11 | Watson Lake | 105-G-07 | |

| Goal | 95 | 96 | 2 | YB63999 | YB64000 | 17-Mar-11 | Watson Lake | 105-G-07 | |

| Goal | 97 | 98 | 2 | YB68801 | YB68802 | 17-Mar-11 | Watson Lake | 105-G-07 | |

| Goal | 99 | 121 | 23 | YB60654 | YB60676 | 17-Mar-11 | Watson Lake | 105-G-07 | |

| Goal | 122 | 129 | 8 | YB68823 | YB68830 | 17-Mar-11 | Watson Lake | 105-G-07 | |

| Goal | 130 | 165 | 36 | YB70481 | YB70516 | 17-Mar-11 | Watson Lake | 105-G-07 | |

| Goal | 166 | 168 | 3 | YB70518 | YB70520 | 17-Mar-11 | Watson Lake | 105-G-08 | |

| Goal | 169 | 1 | YB70556 | 17-Mar-11 | Watson Lake | 105-G-08 | |||

| Goal | 170 | 1 | YB70521 | 17-Mar-07 | Watson Lake | 105-G-08 | |||

| Goal | 171 | 1 | YB70522 | 17-Mar-11 | Watson Lake | 105-G-08 | |||

| Goal | 172 | 181 | 10 | YB70523 | YB70532 | 17-Mar-07 | Watson Lake | 105-G-08 | |

| Goal | 182 | 1 | YB70517 | 17-Mar-11 | Watson Lake | 105-G-08 | |||

| Goal | 183 | 1 | YB70533 | 17-Mar-07 | Watson Lake | 105-G-08 | |||

| Goal | 184 | 203 | 20 | YB68803 | YB68822 | 17-Mar-11 | Watson Lake | 105-G-08 | |

| Goal | 205 | 210 | 6 | YB70475 | YB70480 | 17-Mar-11 | Watson Lake | 105-G-07 | |

| Goal | 211 | 212 | 2 | YB76787 | YB76858 | 17-Mar-11 | Watson Lake | 105-G-07 | |

| Goal | 231 | 232 | 2 | YB76807 | YB76808 | 18-Mar-11 | Watson Lake | 105-G-08 | |

| Goal | 251 | 1 | YB76827 | 19-Mar-11 | Watson Lake | 105-G-09 | |||

| Goal | 271 | 282 | 12 | YB76846 | YB76858 | 20-Mar-11 | Watson Lake | 105-G-10 | |

| Goal | 320 | 335 | 16 | YB87595 | YB87610 | 17-Mar-09 | Watson Lake | 105-G-07 | |

| Goon | 1 | 16 | 16 | YB76681 | YB76696 | 17-Mar-14 | Watson Lake | 105-G-08 | |

| Goon | 17 | 30 | 14 | YB76697 | YB76710 | 17-Mar-07 | Watson Lake | 105-G-07 | |

| Goon | 31 | 38 | 8 | YB76711 | YB76718 | 17-Mar-08 | Watson Lake | 105-G-07 | |

| Goon | 39 | 79 | 41 | YB76719 | YB76759 | 17-Mar-05 | Watson Lake | 105-G-07 | |

| Goon | 80 | 82 | 3 | YB76760 | YB76762 | 17-Mar-05 | Watson Lake | 105-G-07 | |

| Goon | 83 | 84 | F | 2 | YB76763 | YB76764 | 17-Mar-05 | Watson Lake | 105-G-07 |

| Goon | 85 | 106 | 22 | YB76765 | YB76786 | 17-Mar-05 | Watson Lake | 105-G-07 | |

| Goon | 107 | 136 | 30 | YB76876 | YB76905 | 17-Mar-05 | Watson Lake | 105-G-07 | |

| Goon | 137 | 1 | YB92719 | 17-Mar-06 | Watson Lake | 105-G-08 | |||

| Goon | 138 | F | 1 | YB92720 | 17-Mar-06 | Watson Lake | 105-G-08 | ||

| Hat Trick | 1 | 50 | 50 | YB59061 | YB59110 | 17-Mar-05 | Watson Lake | 105-G-02 | |

| Hat Trick | 51 | 52 | 2 | YB59941 | YB59942 | 17-Mar-05 | Watson Lake | 105-G-02 | |

| Hat Trick | 53 | 60 | 8 | YB63578 | YB63585 | 17-Mar-05 | Watson Lake | 105-G-02 | |

| Hat Trick | 61 | 74 | 14 | YB59943 | YB59956 | 17-Mar-05 | Watson Lake | 105-G-02 | |

| Hat Trick | 103 | 114 | 12 | YB60472 | YB60483 | 17-Mar-05 | Watson Lake | 105-G-02 | |

| Hat Trick | 115 | 122 | 8 | YB63586 | YB63593 | 17-Mar-05 | Watson Lake | 105-G-02 |

13

| Claim | Claim | Number | Record | Record | |||||

| Claim | Number | Number | of | Number | Number | Mining | |||

| Group | From | To | Fractions | claims | From | To | Expiry Date | District | Map Sheet |

| Hat Trick | 247 | 262 | 16 | YB63718 | YB63733 | 17-Mar-05 | Watson Lake | 105-G-02 | |

| Hat Trick | 275 | 290 | 16 | YB63902 | YB63917 | 17-Mar-05 | Watson Lake | 105-G-02 | |

| Hat Trick | 303 | 316 | 14 | YB63746 | YB63759 | 17-Mar-05 | Watson Lake | 105-G-02 | |

| Ice | 1 | 16 | 16 | YB78632 | YB78647 | 06-Mar-10 | Watson Lake | 105-G-14 | |

| Ice | 17 | 48 | 32 | YB84405 | YB84436 | 06-Mar-06 | Watson Lake | 105-G-14 | |

| Ice | 49 | 165 | 117 | YB84880 | YB84996 | 06-Mar-06 | Watson Lake | 105-G-14 | |

| Ice | 166 | F | 1 | YB84997 | 06-Mar-06 | Watson Lake | 105-G-14 | ||

| Ice | 167 | 1 | YB84998 | 06-Mar-06 | Watson Lake | 105-G-14 | |||

| Ice | 168 | F | 1 | YB84999 | 06-Mar-06 | Watson Lake | 105-G-14 | ||

| Ice | 169 | 1 | YB85000 | 06-Mar-06 | Watson Lake | 105-G-14 | |||

| Ice | 170 | F | 1 | YB85001 | 06-Mar-06 | Watson Lake | 105-G-14 | ||

| Ice | 171 | 1 | YB85002 | 06-Mar-06 | Watson Lake | 105-G-14 | |||

| Ice | 172 | F | 1 | YB85003 | 06-Mar-06 | Watson Lake | 105-G-14 | ||

| Ice | 173 | 1 | YB85004 | 06-Mar-06 | Watson Lake | 105-G-14 | |||

| Ice | 174 | F | 1 | YB85005 | 06-Mar-06 | Watson Lake | 105-G-14 | ||

| Ice | 175 | 1 | YB85006 | 06-Mar-06 | Watson Lake | 105-G-14 | |||

| Ice | 176 | F | 1 | YB85007 | 06-Mar-06 | Watson Lake | 105-G-14 | ||

| Ice | 177 | 1 | YB85008 | 06-Mar-06 | Watson Lake | 105-G-14 | |||

| Ice | 178 | F | 1 | YB85009 | 06-Mar-06 | Watson Lake | 105-G-14 | ||

| Ice | 179 | 1 | YB85010 | 06-Mar-06 | Watson Lake | 105-G-14 | |||

| Ice | 180 | F | 1 | YB85011 | 06-Mar-06 | Watson Lake | 105-G-14 | ||

| Ice | 181 | 212 | 32 | YB85012 | YB85043 | 06-Mar-06 | Watson Lake | 105-G-14 | |

| Ice | 213 | F | 1 | YB85044 | 06-Mar-06 | Watson Lake | 105-G-14 | ||

| Ice | 214 | 326 | 113 | YB85045 | YB85157 | 06-Mar-06 | Watson Lake | 105-G-14 | |

| Ice | 327 | 334 | 8 | YB85158 | YB85165 | 06-Mar-06 | Watson lake | 105-G-14 | |

| Ice | 335 | 362 | 28 | YB86186 | YB86213 | 06-Mar-06 | Watson Lake | 105-G-14 | |

| Ice | 363 | 374 | 12 | YB86878 | YB86889 | 06-Mar-06 | Watson Lake | 105-G-14 | |

| Ice | 375 | 402 | 28 | YB86214 | YB86241 | 06-Mar-06 | Watson Lake | 105-G-14 | |

| Ice | 1080 | 1081 | 2 | YB87693 | YB87694 | 06-Mar-08 | Watson Lake | 105-G-14 | |

| League | 1 | 20 | 20 | YB59143 | YB59162 | 17-Mar-09 | Watson Lake | 105-G-10 | |

| League | 21 | 30 | 10 | YB60204 | YB60213 | 17-Mar-05 | Watson Lake | 105-G-10 | |

| League | 31 | 34 | 4 | YB60214 | YB60217 | 17-Mar-05 | Watson Lake | 105-G-10 | |

| League | 54 | 1 | YB60237 | 17-Mar-05 | Watson Lake | 105-G-10 | |||

| League | 57 | 1 | YB60240 | 17-Mar-05 | Watson Lake | 105-G-10 | |||

| League | 59 | 68 | 10 | YB60855 | 17-Mar-05 | Watson Lake | 105-G-10 | ||

| League | 70 | 1 | YB60866 | 17-Mar-05 | Watson Lake | 105-G-10 | |||

| League | 72 | 78 | 7 | YB60868 | YB60874 | 17-Mar-05 | Watson Lake | 105-G-10 | |

| League | 94 | 1 | YB60890 | 17-Mar-05 | Watson Lake | 105-G-10 | |||

| League | 96 | 1 | YB60892 | 17-Mar-05 | Watson Lake | 105-G-10 | |||

| League | 115 | 150 | 36 | YB61588 | YB61623 | 17-Mar-05 | Watson Lake | 105-G-10 | |

| League | 153 | 171 | 19 | YB61626 | YB61644 | 17-Mar-05 | Watson Lake | 105-G-10 | |

| League | 173 | 1 | YB61626 | 17-Mar-05 | Watson Lake | 105-G-10 | |||

| League | 176 | 1 | YB61649 | 17-Mar-05 | Watson Lake | 105-G-10 | |||

| League | 178 | 1 | YB61651 | 17-Mar-05 | Watson Lake | 105-G-10 | |||

| League | 180 | 1 | YB61653 | 17-Mar-05 | Watson Lake | 105-G-10 | |||

| League | 182 | 1 | YB61655 | 17-Mar-05 | Watson Lake | 105-G-10 | |||

| League | 249 | 256 | 8 | YB70247 | YB70254 | 17-Mar-05 | Watson Lake | 105-G-10 | |

| Light | 6 | 1 | YB92390 | 28-Feb-06 | Watson Lake | 105-G-06 | |||

| Light | 8 | 1 | YB92392 | 28-Feb-06 | Watson Lake | 105-G-06 | |||

| Light | 10 | 1 | YB92394 | 28-Feb-06 | Watson Lake | 105-G-06 | |||

| Light | 12 | 1 | YB92396 | 28-Feb-06 | Watson Lake | 105-G-06 | |||

| Light | 14 | 1 | YB92398 | 28-Feb-06 | Watson Lake | 105-G-06 | |||

| Light | 16 | 1 | YB92400 | 28-Feb-06 | Watson Lake | 105-G-06 | |||

| Light | 23 | 1 | YB92407 | 28-Feb-06 | Watson Lake | 105-G-06 | |||

| Light | 25 | 1 | YB92409 | 28-Feb-06 | Watson Lake | 105-G-06 | |||

| Light | 27 | 1 | YB92411 | 28-Feb-06 | Watson Lake | 105-G-06 | |||

| Light | 29 | 1 | YB92413 | 28-Feb-06 | Watson Lake | 105-G-06 | |||

| Light | 31 | 1 | YB92415 | 28-Feb-06 | Watson Lake | 105-G-06 | |||

| Light | 33 | 1 | YB92417 | 28-Feb-06 | Watson Lake | 105-G-06 | |||

| Light | 35 | 38 | 4 | YB92419 | YB92422 | 28-Feb-06 | Watson Lake | 105-G-06 |

14

| LIGHT | 51 | 60 | 10 | YC22637 | YC22646 | 21-Nov-04 | Watson Lake | 105-G-06 | |

| LIGHT | 65 | 68 | 4 | YC22647 | YC22650 | 21-Nov-04 | Watson Lake | 105-G-06 | |

| Mask | 1 | 38 | 38 | YB63540 | YB63577 | 17-Mar-06 | Watson Lake | 105-G-01 | |

| Mask | 39 | 48 | 10 | YB77943 | YB77952 | 17-Mar-06 | Watson Lake | 105-G-01 | |

| Mask | 55 | 56 | 2 | YB77959 | YB77960 | 17-Mar-06 | Watson Lake | 105-G-01 | |

| Mask | 67 | 76 | 10 | YB77971 | YB77980 | 17-Mar-06 | Watson Lake | 105-G-01 |

15

| Claim | Claim | Number | Record | Record | |||||

| Claim | Number | Number | of | Number | Number | Mining | |||

| Group | From | To | Fractions | claims | From | To | Expiry Date | District | Map Sheet |

| Net | 1 | 34 | 34 | YB56095 | YB56128 | 17-Mar-13 | Watson Lake | 105-G-08 | |

| Net | 35 | 58 | 24 | YB59119 | YB59142 | 17-Mar-11 | Watson Lake | 105-G-08 | |

| Net | 59 | 72 | 14 | YB60984 | YB60997 | 17-Mar-07 | Watson Lake | 105-G-08 | |

| Net | 73 | 124 | 52 | YB63472 | YB63523 | 17-Mar-07 | Watson Lake | 105-G-08 | |

| Net | 125 | 140 | 16 | YB63930 | YB63945 | 17-Mar-11 | Watson Lake | 105-G-08 | |

| Net | 141 | 156 | 16 | YB63524 | YB63539 | 17-Mar-11 | Watson Lake | 105-G-08 | |

| Net | 157 | 164 | 8 | YB70431 | YB70438 | 17-Mar-07 | Watson Lake | 105-G-08 | |

| Net | 165 | F | 1 | YB70439 | 17-Mar-07 | Watson Lake | 105-G-08 | ||

| Net | 166 | 169 | 4 | YB70440 | YB70443 | 17-Mar-07 | Watson Lake | 105-G-08 | |

| Net | 170 | F | 1 | YB70444 | 17-Mar-07 | Watson Lake | 105-G-08 | ||

| Net | 171 | 184 | 14 | YB70445 | YB70458 | 17-Mar-07 | Watson Lake | 105-G-08 | |

| Net | 185 | 195 | 11 | YB70459 | YB70469 | 17-Mar-11 | Watson Lake | 105-G-08 | |

| Net | 196 | 1 | YB70557 | 17-Mar-11 | Watson Lake | 105-G-07 | |||

| Net | 197 | 200 | 4 | YB70470 | YB70473 | 17-Mar-11 | Watson Lake | 105-G-07 | |

| Net | 201 | 204 | 4 | YB78690 | YB78693 | 17-Mar-07 | Watson Lake | 105-G-08 | |

| Net | 205 | 206 | F | 2 | YB78694 | YB78695 | 17-Mar-07 | Watson Lake | 105-G-08 |

| Net | 207 | 214 | 8 | YB78696 | YB78703 | 17-Mar-07 | Watson Lake | 105-G-08 | |

| NHL | 1 | 30 | 30 | YB60677 | YB60706 | 17-Mar-05 | Watson Lake | 105-G-07 | |

| NHL | 31 | 144 | 114 | YB60707 | YB60820 | 17-Mar-10 | Watson Lake | 105-G-07 | |

| NHL | 145 | 148 | 4 | YB60821 | YB60824 | 17-Mar-05 | Watson Lake | 105-G-07 | |

| NHL | 149 | 152 | 4 | YB68845 | YB68848 | 17-Mar-05 | Watson Lake | 105-G-07 | |

| NHL | 153 | 158 | 6 | YB68831 | YB68836 | 17-Mar-05 | Watson Lake | 105-G-07 | |

| NHL | 159 | 166 | 8 | YB68837 | YB68844 | 17-Mar-10 | Watson Lake | 105-G-08 | |

| NHL | 167 | 176 | 10 | YB89561 | YB89570 | 17-Mar-10 | Watson Lake | 105-G-08 | |

| NL | 1 | 30 | 30 | YC22607 | YC22636 | 21-Nov-03 | Watson Lake | 105-G-10 | |

| NS | 1 | 40 | 40 | YC22547 | YC22586 | 21-Nov-03 | Watson Lake | 105-G-06 | |

| OC | 1 | 16 | 16 | YB94385 | YB94400 | 21-Nov-04 | Watson Lake | 105-G-11 | |

| OC | 17 | 62 | 46 | YC22501 | YC22546 | 21-Nov-04 | Watson Lake | 105-G-11 | |

| Overtime | 1 | 50 | 50 | YB60534 | YB60583 | 17-Mar-07 | Watson Lake | 105-G-07 | |

| Overtime | 51 | 86 | 36 | YB61522 | YB61557 | 17-Mar-07 | Watson Lake | 105-G-07 | |

| Play | 1 | 64 | 64 | YB59183 | YB59246 | 17-Mar-07 | Watson Lake | 105-G-13 | |

| Play | 65 | 68 | 4 | YB60911 | YB60914 | 17-Mar-07 | Watson Lake | 105-G-13 | |

| Play | 69 | 76 | 8 | YB60915 | YB60922 | 17-Mar-05 | Watson Lake | 105-G-13 | |

| Play | 77 | 80 | 4 | YB60923 | YB60926 | 17-Mar-07 | Watson Lake | 105-G-13 | |

| Play | 81 | 88 | 8 | YB60927 | YB60934 | 17-Mar-05 | Watson Lake | 105-G-13 | |

| Play | 98 | 1 | YB77007 | 17-Mar-06 | Watson Lake | 105-G-13 | |||

| Play | 100 | 1 | YB77009 | 17-Mar-06 | Watson Lake | 105-G-13 | |||

| Play | 102 | 1 | YB77011 | 17-Mar-06 | Watson Lake | 105-G-13 | |||

| Play | 104 | 1 | YB77013 | 17-Mar-06 | Watson Lake | 105-G-13 | |||

| Play | 106 | 1 | YB77015 | 17-Mar-06 | Watson Lake | 105-G-13 | |||

| Play | 108 | 1 | YB77017 | 17-Mar-06 | Watson Lake | 105-G-13 | |||

| Play | 110 | 1 | YB77019 | 17-Mar-06 | Watson Lake | 105-G-13 | |||

| Play | 112 | 1 | YB77021 | 17-Mar-06 | Watson Lake | 105-G-13 | |||

| Play | 114 | 1 | YB77023 | 17-Mar-06 | Watson Lake | 105-G-13 | |||

| Play | 116 | 1 | YB77025 | 17-Mar-06 | Watson Lake | 105-G-13 | |||

| Play | 118 | 1 | YB77027 | 17-Mar-06 | Watson Lake | 105-G-13 | |||

| Play | 120 | 1 | YB77029 | 17-Mar-06 | Watson Lake | 105-G-13 | |||

| Play | 122 | 1 | YB77031 | 17-Mar-06 | Watson Lake | 105-G-13 | |||

| Play | 124 | 1 | YB77033 | 17-Mar-06 | Watson Lake | 105-G-13 | |||

| Play | 126 | 1 | YB77035 | 17-Mar-06 | Watson Lake | 105-G-13 | |||

| Play | 140 | 147 | F | 8 | YB89332 | YB89339 | 17-Mar-06 | Watson Lake | 105-G-13 |

| Play | 152 | 154 | 3 | YB89390 | YB89392 | 17-Mar-06 | Watson Lake | 105-G-14 | |

| Play | 155 | 1 | YB89607 | 17-Mar-06 | Watson Lake | 105-G-14 | |||

| Puck | 1 | 80 | 80 | YB55979 | YB56058 | 17-Mar-09 | Watson Lake | 105-G-08 | |

| Red Line | 1 | 12 | 12 | YB60825 | YB60836 | 17-Mar-06 | Watson Lake | 105-G-08 | |

| Red Line | 13 | 28 | 16 | YB70624 | YB70639 | 17-Mar-06 | Watson Lake | 105-G-08 | |

| Ref | 1 | 16 | 16 | YB77069 | YB77084 | 20-Feb-06 | Watson Lake | 105-G-14 | |

| Ref | 51 | 61 | 11 | YB79627 | YB79637 | 20-Feb-06 | Watson Lake | 105-G-14 | |

| Ref | 63 | 1 | YB79639 | 20-Feb-06 | Watson Lake | 105-G-14 | |||

| Ref | 65 | 1 | YB79641 | 20-Feb-06 | Watson Lake | 105-G-14 | |||

| Ref | 67 | 1 | YB79643 | 20-Feb-06 | Watson Lake | 105-G-14 |

16

| Ref | 69 | 1 YB79645 | 20-Feb-06 | Watson Lake | 105-G-14 | ||||

| Ref | 71 | 1 YB79647 | 20-Feb-06 | Watson Lake | 105-G-14 | ||||

| Ref | 86 | 1 YB79662 | 20-Feb-06 | Watson Lake | 105-G-14 | ||||

| Ref | 88 | 1 YB79664 | 20-Feb-06 | Watson Lake | 105-G-14 | ||||

| Ref | 90 | 1 YB79666 | 20-Feb-06 | Watson Lake | 105-G-14 |

17

| Claim | Claim | Number | Record | Record | |||||

| Claim | Number | Number | of | Number | Number | Mining | |||

| Group | From | To | Fractions | claims | From | To | Expiry Date | District | Map Sheet |

| Ref | 92 | 1 | YB79668 | 20-Feb-06 | Watson Lake | 105-G-14 | |||

| Ref | 94 | 110 | 17 | YB79670 | YB79686 | 20-Feb-06 | Watson Lake | 105-G-14 | |

| Ref | 113 | 120 | 8 | YB79689 | YB79696 | 20-Feb-06 | Watson Lake | 105-G-14 | |

| Ref | 121 | 125 | 5 | YB79697 | YB79701 | 20-Feb-06 | Watson Lake | 105-G-14 | |

| Ref | 127 | 1 | YB79703 | 20-Feb-06 | Watson Lake | 105-G-14 | |||

| Ref | 130 | 1 | YB79706 | 20-Feb-06 | Watson Lake | 105-G-14 | |||

| Ref | 132 | 1 | YB79708 | 20-Feb-06 | Watson Lake | 105-G-14 | |||

| Ref | 134 | 150 | 17 | YB79710 | YB79726 | 20-Feb-06 | Watson Lake | 105-G-14 | |

| Replay | 1 | 20 | 20 | YB77111 | YB77130 | 20-Feb-06 | Watson Lake | 105-G-13 | |

| Shot | 1 | 36 | 36 | YB56059 | YB56094 | 17-Mar-07 | Watson Lake | 105-G-07 | |

| Shutout | 1 | 14 | 14 | YB58953 | YB58966 | 17-Mar-08 | Watson Lake | 105-G-01 | |

| Shutout | 15 | 22 | 8 | YB58967 | YB58974 | 17-Mar-12 | Watson Lake | 105-G-01 | |

| Shutout | 23 | 26 | 4 | YB58975 | YB58978 | 17-Mar-08 | Watson Lake | 105-G-01 | |

| Shutout | 27 | 36 | 10 | YB58979 | YB58988 | 17-Mar-12 | Watson Lake | 105-G-01 | |

| Shutout | 37 | 38 | 2 | YB58989 | YB58990 | 17-Mar-08 | Watson Lake | 105-G-01 | |

| Shutout | 39 | 48 | 10 | YB58991 | YB59000 | 17-Mar-12 | Watson Lake | 105-G-01 | |

| Shutout | 49 | 50 | 2 | YB59001 | YB59002 | 17-Mar-08 | Watson Lake | 105-G-01 | |

| Shutout | 51 | 60 | 10 | YB59003 | YB59012 | 17-Mar-12 | Watson Lake | 105-G-01 | |

| Shutout | 61 | 66 | 6 | YB59013 | YB59018 | 17-Mar-08 | Watson Lake | 105-G-01 | |

| Shutout | 67 | 72 | 6 | YB59019 | YB59024 | 17-Mar-12 | Watson Lake | 105-G-01 | |

| Shutout | 73 | 80 | 8 | YB59025 | YB59032 | 17-Mar-08 | Watson Lake | 105-G-01 | |

| Shutout | 81 | 84 | 4 | YB59033 | YB59036 | 17-Mar-12 | Watson Lake | 105-G-01 | |

| Shutout | 85 | 94 | 10 | YB59037 | YB59046 | 17-Mar-08 | Watson Lake | 105-G-01 | |

| Shutout | 95 | 96 | 2 | YB59047 | YB59048 | 17-Mar-12 | Watson Lake | 105-G-01 | |

| Shutout | 97 | 108 | 12 | YB59049 | YB59060 | 17-Mar-08 | Watson Lake | 105-G-01 | |

| Shutout | 109 | 133 | 25 | YB77893 | YB77917 | 17-Mar-05 | Watson Lake | 105-G-01 | |

| Shutout | 134 | F | 1 | YB77918 | 17-Mar-05 | Watson Lake | 105-G-01 | ||

| Shutout | 135 | 158 | 24 | YB77919 | YB77942 | 17-Mar-05 | Watson Lake | 105-G-01 | |

| Skate | 1 | 54 | 54 | YB68933 | YB68986 | 17-Mar-05 | Watson Lake | 105-F-16 | |

| Stick | 1 | 30 | 30 | YB60484 | YB60513 | 17-Mar-05 | Watson Lake | 105-G-06 | |

| WC | 1 | 20 | 20 | YC22587 | YC22606 | 21-Nov-04 | Watson Lake | 105-G-11 | |

| Winger | 8 | 1 | YB77138 | 20-Feb-08 | Watson Lake | 105-G-06 | |||

| Winger | 15 | 16 | 2 | YB77145 | YB77146 | 20-Feb-08 | Watson Lake | 105-G-06 | |

| Total | 2626 |

18

Our claims comprise a total of 135,000 acres or 54,600 hectares. In order to retain the claims past the expiry date, the claimholder must either pay $100 on or before the expiry date or perform work thereon.

In September 2003, the Company contracted the services of Amerlin Exploration Services Ltd. and Mr. Carl G. Verley, P. Geo and a member of the YK Group and a "qualified person" as defined in Canadian Mining "National Policy 43-101. The following is a brief summary of Amerlin Explorations Services' work program.

During the 2003 field season $176,000 was expended on a program of prospecting, geological mapping and soil sampling conducted on 6 claim blocks collectively covering 52,000 acres or only 40% of the overall claim holdings. As a result of this work a new beryl occurrence was discovered in ultramafic rocks on the Goal Net claim block a few kilometers to the north of the Regal Ridge emerald discovery. In addition a number of known beryllium soil anomalies were reconfirmed and several new beryllium soil anomalies were located on Goal Net. On the Light claim block soil sample results outlined a lithology with a high Be background and beryl-bearing quartz vein float

Geochemical soil sampling (484 samples) was undertaken during the course of the fieldwork. The results of this work indicate that Be anomalies in soils are in some cases (Light claims), but not all associated with known beryl mineralization. Therefore detailed, systematic prospecting is required to fully evaluate anomalous areas. In addition, Be soil geochemistry outlined lithologies having a high Be background. These lithologies could provide sources of Be under the right conditions and therefore should be examined closely. Other areas anomalous in Be on the Goal Net and Light claim blocks warrant further follow-up prospecting and sampling. Areas of quartz-tourmaline vein must also be followed up with further prospecting and sampling.

19

Based on the results to date further work is warranted and strongly recommended. Follow-up should include detailed prospecting, sampling and mapping on the known beryl showing and beryllium soil anomalies. In addition trenching and initial drill testing of significant showings should be undertaken. . In addition, further work should also be directed to the area of quartz-tourmaline veining on the west side of the Light property. A greater number of claims should be looked at during the 2004 program in order to assess their potential for hosting emerald deposits. The estimated cost of the recommended program ranges from $200,000 to $500,000. The broad range is provided for foul weather contingencies particularly in the event that drilling takes place late in the season.

The complete report on the 2003 exploration program is available on the Company website at www.entouragemining.com/ A detailed overview of the Finlayson Lake property is outlined below.

Location and access

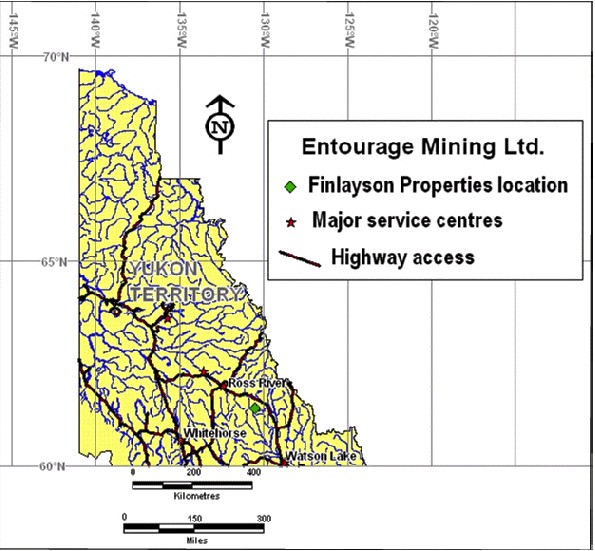

The properties are located in a northwesterly trending belt approximately 220 km in length by 35 km in width centered at latitude 61 degrees 31 minutes North, longitude 131 degrees 08 minutes West in southeastern Yukon Territory. The Finlayson Properties are located in the northern Pelly Mountains of the Yukon Plateau. The project area is 260 km east-northeast of Whitehorse and 180 km northwest of Watson Lake by air. The community of Ross River is located at the northwest end of the area.

Access to the Finlayson Properties is via helicopter from the Finlayson Lake airstrip. The Robert Campbell Highway, an all weather, chip sealed or gravel road, transects the Finlayson Properties project area. A number of the claim groups listed, including the Assist, Box, Breakaway, Bug, Puck, Goal Net, Ice, League, Red Line, Replay and Skate, are within 20 kilometers of the Robert Campbell Highway. The highway connects with the Alaska Highway at Watson Lake, approximately 170 kilometers to the southeast, and the Klondike Highway at Carmacks, approximately 320 kilometers to the northwest. The town of Ross River is located 120 kilometers to the northwest and, 34 kilometers further to the northwest is the town of Faro. The center of the properties holdings are about 230 air kilometers northeast of Whitehorse. An all-weather privately owned access road extends from the Robert Campbell Highway to the Kudz Ze Kayah Deposit in the center of the southern half of the project area. Private gravel airstrips are located immediately south of Wolverine Lake and near the Kudz Ze Kayah Deposit. There are several lakes in the area that are large enough to accommodate float planes up to a DHC-6 (Twin Otter). Helicopter charter services are available in Ross River and Watson Lake. Fixed wing charter is available from Watson Lake and Whitehorse.

The area around the properties has been explored since 1981. The Finlayson Properties have no history of previous exploration for emeralds. There is no evidence of mining on the properties and there is no plant or equipment located on the properties. There are no material engineering or geological reports concerning the emerald potential of the properties, other than governmental regional geological reports and the Report of Aurora Geoscience Ltd. dated March 21, 2003, filed with the Company's original Registration Statement dated June 6th, 2003, which are known or available to us. There is no power source on the properties.

Based upon the recommendations of the Amerlin Exploration 2003 report, the Company plans to initiate a $200,000-$500,000 staged work program, subject to us securing financing and subject to prevailing weather conditions, to begin in the last week of June 2004. There is no guarantee that the Company will be able to raise sufficient funding or that the weather conditions will permit prospecting, trenching and sampling of the property.

Physiography

The properties are located in the northern Pelly Mountains of the Yukon Plateau. The area is covered by glacial -fluvial deposits at elevations below 1,700 meters and contain rocky outcropping and talus at higher elevations. Outcropping is sparse except along ridge crests, in north-facing cirques, and along actively eroding creek cuts. The League, Red Line and Puck claims are on the northern flank of the Pelly Mountains in undulating terrain at elevations ranging from 1,100 to 1,700 meters. The Goal Net claim is located in the Pelly Mountains proper with elevations ranging from 1,500 to 2,350 meters.

The League, Red Line and Puck claims drain to the north via the Big Campbell, Wolverine and several smaller, unnamed creeks. The Goal Net Property is at the height of land and drains south via the North River and northeast via

20

Money Creek. North Lakes at an elevation of 1,500 meters and Wolverine Lake at an elevation of 1,150 meters are the only significant bodies of water in the area.

The tree line occurs at approximately 1,400 meters throughout the area and tree cover below this elevation consists of sparse black spruce, willow and alder. Tree cover is locally thick near Wolverine Lake and at lower elevations along the creeks. At higher elevations, alders and dwarf willow give way to grass on south-facing slopes. Discontinuous permafrost occurs throughout the project area is extensive on north facing slopes.

The main rock types occurring in the area are nearly flat lying layered metamorphic rocks belonging to the Yukon-Tanana Terrane. The Yukon-Tanana Terrane can be subdivided into several thrust faults bound in succession ranging in age from Devonian to Triassic. The rocks record the transition from continental margin sedimentation through continental arc magmatism to final submarine rifting. Intrusive into Yukon-Tanana successions are rocks ranging in age from late Devonian to Tertiary and ranging in composition from ultramafic to felsic. The foregoing was observed by Michael A. Power, M.Sc., P.Geo., when he visited the properties. We have been advised by Aurora Geosciences Ltd. that emeralds may be found in some parts of the Grass Lakes succession, the lowest member of the Yukon-Tanana Terrane. Not all members of the Yukon-Tanana Terrane contains emeralds. We do not know if there are potentially significant occurrences of economic mineralization on the properties.

We are prospecting for emeralds. Our target is mineralized material. Our success depends upon finding mineralized material. Mineralized material is a mineralized body which has been delineated by appropriate spaced drilling or underground sampling to support sufficient tonnage and average grade of metals to justify removal. If we do not find mineralized material or we cannot remove mineralized material, either because we do not have the money to do it or because it is not economically feasible to do it, we will cease operations and you will lose your investment.

21

In addition, we may not have enough money to complete the exploration of our properties. If it turns out that we have not raised enough money to complete our exploration program, we will try to raise additional funds from a public offering, a private placement or loansIf we are unable to raise additional money we will have to suspend or cease operations.

We must conduct exploration to determine what amount of minerals, if any, exist on our properties and if any emerald mineralization that is found can be economically extracted and profitably processed.

Our properties are undeveloped raw land. Limited exploration and surveying has been initiated and further exploration will not be initiated until we raise money in an offering. That is because we do not have sufficient capital to complete our 2004 exploration program. Once an offering is concluded, we intend to start exploration operations at the end of June 2004. To our knowledge, the properties have never been mined. The only event that has occurred is the staking of the properties by Expatriate Resources Ltd., a physical examination of the properties and the 2003 exploration activities of Amerlin Exploration Services Ltd.. Before emerald retrieval can begin, we must explore for and find mineralized material. After that has occurred we have to determine if it is economically feasible to remove the mineralized material. Economically feasible means that the costs associated with the removal of the mineralized material will not exceed the price at which we can sell the mineralized material. We cannot predict what that will be until we find mineralized material.

We do not know if we will find mineralized material. We believe that activities occurring on adjoining properties are not material to our activities. The reason is that what ever is located under the adjoining properties may or may not be located under our properties.

Our exploration program is designed to economically explore and evaluate our properties.

We do not claim to have any minerals or reserves whatsoever at this time on any of our properties.

We intend to continue our staged exploration program which initially consisted of prospecting to identify emerald mineralization on the Finlayson Properties as described in the Amerlin Explorations Services report. Once emerald mineralization is located a more detailed exploration of the emerald-bearing areas will be the focus of ensuing exploration programs. These programs will initially consist of trenching and bulk sampling. Some core drilling may be undertaken from time to time based on the recommendations of the Company's consultants.

In 2003, the YK Group paid the sum of $5,283.80 to Aurora Geosciences Ltd. in order to obtain independent recommendations for the exploration of the Finlayson Properties.

The breakdown of estimated times and dollars was made by Aurora Geosciences Ltd. in consultation with John Poloni a director.

We do not intend to interest other companies in the properties if we find mineralized materials. We intend to try to develop the reserves ourselves.

If we are unable to complete exploration because we do not have enough money, we will cease operations until we raise more money. If we cannot or do not raise more money, we will cease operations. If we cease operations, we don't know what we will do and we don't have any plans to do anything else.

We cannot provide you with a more detailed discussion of how our exploration program will work and what we expect will be our likelihood of success. That is because we have a piece of raw land and we intend to look for mineralized material. We may or may not find any mineralized material. We hope we do, but it is impossible to predict the likelihood of such an event.

We do not have any plan to generate revenue. That is because we have not found economicmineralization yet and it is impossible to project revenue generation from nothing.

Prospecting methods will essentially be visual inspection of the ground where anomalous beryllium analysis in soils have been determined from previous soil sampling work by conducted on behalf of Expatriate Resources by Archer Cathro and Associates and by Amerlin Exploration Services Ltd. in 2003. The visual inspection process will rely on Entourage's prospecting team's expertise in recognizing beryl and the associated rock formations within which beryl may occur, such as quartz tourmaline veins. Beryl and thus emerald does not have any easily utilizable geophysical properties that can be adapted to the search for emerald. However the geochemistry of beryllium and associated elements can be effectively utilized to outline where there is a high probability for locating beryllium minerals, among which beryl and emerald could be present. Because beryllium soil anomalies having the same intensity as those found on ground where emeralds were originally discovered in the Finlayson Lake area, it is believed that there is a high probability for finding mineralized material in the anomalous areas on Entourage's optioned ground. The prospecting work will include further

22

geochemical sampling of selected areas. In additional, rock sampling of beryl/emerald material located during the course of prospecting will be taken and representative samples of emerald will be sent out to qualified gemologists for evaluation.

Timing, scope and expected costs of planned exploration program:

For 2004:

Exploration planned for 2004 will commence in late June continuing on for approximately 65-75 days toward mid-or the end of September.

The 2004 exploration should include detailed prospecting, sampling and mapping on the known beryl showing and beryllium soil anomalies. In addition trenching and initial drill testing of significant showings should be undertaken. In addition, further work should also be directed to the area of quartz-tourmaline veining on the west side of the Light property. A greater number of the Finlayson Property claims should be looked at during the 2004 program in order to assess their potential for hosting emerald deposits. The estimated cost of the recommended program ranges from $200,000 to $500,000. The broad range is provided for foul weather contingencies particularly in the event that drilling takes place late in the season.

| 1) | Physical showings of white beryl and quartz-tourmaline veins require close scrutiny. It is recommended that both locations be soil sampled, mapped and prospected on 10 metre centres. Beryl in float should be further investigated by hand excavating short trenches perpendicular to local stratigraphy. |

Particular attention should be paid to structural control of vein and fault features in proximity to the zones of interest.

| 2) | The soil anomalies within the five areas outlined should be closed-off to determine ultimate dimensions with additional soil sampling. The zones within the anomalous areas that contain coincident anomalous copper, beryllium and tungsten values should be targeted with close-spaced soil sampling (10 m centers) and detailed prospecting and mapping. Areas with anomalous beryllium and either tungsten or copper values should be sampled at 25 meter spacing and carefully mapped and prospected. |

| 3) | Claim blocks not yet sampled should be examined by stream sediment sampling on creeks draining prospective stratigraphy; mapping and prospecting across stratigraphy; and soil/talus sampling along talus slopes to develop targets for follow-up work. |

The program will require approximately 75 field days for a crew consisting of a 4-person technical team. The 2004 fieldwork will be conducted from the nearby Inconnu Lodge where helicopter services and board and room for the field crew can be secured.

23

A listing of the major cost components of the 2004 phase of the exploration program is tabulated below:

| Item | Estimated Cost | ||||

| Field expense | |||||

| Communications | 5,000 | ||||

| Camp equipment | 30,000 | ||||

| Equipment rental | 20,000 | ||||

| Expediting | 6,000 | ||||

| Freight & Fuel | 12,500 | ||||

| Food | 12,000 | ||||

| Hotel | 2,000 | ||||

| Permitting | 3,000 | ||||

| Truck rental | 5,350 | ||||

| Travel | 12,000 | ||||

| Analytical Costs | Soils 1,000 samples | 17,000 | |||

| Diamond drilling | 1,000 metres | 120,000 | |||

| Excavator rental | 15 days | 18,750 | |||

| Helicopter Support | 70 hours | 73,500 | |||

| Gemological consulting | 20,000 | ||||

| Reporting | 6,000 | ||||

| Wages & Salaries | 104,000 | ||||

| Project management | @10% | 46,710 | |||

| GST | 35,967 | ||||

| Total Cost | $ | 503,067 |

Competitive factors

The emerald mining industry is fragmented. We are a start up venture and compete with other exploration companies looking for emeralds. We are one of the smaller exploration companies in existence. While we compete with other exploration companies, there is no competition for the exploration or removal of minerals from our properties. Readily available emerald markets exist in Canada and around the world for the sale of emeralds. Therefore, we will be able to sell any emeralds that we are able to recover.

RegulationsOur mineral exploration program is subject to the Yukon Quartz Mining Act. This act sets forth rules for

| * | locating claims | |

| * | posting claims | |

| * | working claims | |

| * | reporting work performed |

24

We must comply with these laws to operate our business. Compliance with these rules and regulations will not adversely affect our operations.

We have no experience in complying with these rules and regulations. One of directors, John Poloni, has had experience in dealing with similar rules and regulations in the provinces of British Columbia. As a result, we believe we will be able to comply with these rules and regulations. In the event that it becomes too difficult for us to comply with the regulations, we intend to hire professional engineers or and/or geologists to assist us with compliance. As of the date of December 31, 2003, we have spent $-0- complying with these regulations.

Environmental law

We are also subject to the Quartz Mining Land Use Regulations in the Yukon. This code deals with environmental matters relating to the exploration and development of mining properties. Its goals are to protect the environment through a series of regulations affecting:

| 1. | Health and Safety | |

| 2. | Archaeological Sites | |

| 3. | Exploration Access |

We are required to provide a safe working environment, not disrupt archaeological sites, and conduct our activities to prevent unnecessary damage to the properties.

We will secure all necessary permits for exploration and, if development is warranted on the properties, will file final plans of operation before we start any mining operations. We anticipate no discharge of water into active stream, creek, river, lake or any other body of water regulated by environmental law or regulation. No endangered species will be disturbed. Restoration of the disturbed land will be completed according to law. All holes, pits and shafts will be sealed upon abandonment of the properties. It is difficult to estimate the cost of compliance with the environmental law since the full nature and extent of our proposed activities cannot be determined at this time.

Under the Quartz Mining Use Regulations, varying classes of land use permits are issued depending upon the level of exploration activity. Permit applications are submitted to the Mining Recorder's office in the regional mining district. Review of the permit application takes up to thirty days. Fees for the permit applications can be as high as $500.00. We believe our continued activities for the 2004 season will fall into Class I for which there is no application fee. Beyond this, we will make application for the appropriate permit in advance of further exploration work. We do not foresee any obstacles to obtaining the permits.

We are in compliance with the act and will continue to comply with the act in the future. We believe that compliance with the act will not adversely affect our business operations in the future.

Exploration stage companies have no need to discuss environmental matters, except as they relate to exploration activities. The only costs of compliance with environmental regulations in the Yukon Territory is returning the surface to its previous condition upon abandonment of the properties. We cannot speculate on those costs in light of our ongoing plans for exploration.

25

Other Properties

In June 2004, we signed a definitive agreement with Goodsprings Development Corp., a Nevada based corporation, whereby we may earn a 100% interest in the GBW project in Esmeralda County, Nevada. The project comprises patented and unpatented mineral claims in the Walker Lane mineral belt.

The agreement with Goodsprings Development Corp. is described more fully in Material Agreements and was filed as an attachment to a report on Form 6-K dated June 29, 2004.

Labor

Initially, we intend to use the services of subcontractors for manual labor exploration work on our properties. Our only technical assistants will be our officers and directors.

Employees and employment agreementsAt present, we have no employees, other than our president and director Greg Kennedy. Mr. Kennedy has a management agreement with us. Mr. Kennedy is reimbursed for his out of pocket expenses In February 2004, we adopted a stock option plan for our employees, officers, directors and consultants. We presently do not have pension, health, annuity, insuranceprofit sharing or similar benefit plans; however, we may adopt plans in the future. There are presently no personal benefits available to Mr. Kennedy. Mr. Kennedy will handle our administrative duties. Because Mr. Kennedy is inexperienced with exploration, he will hire qualified persons to perform the surveying, exploration, and excavating of our properties. As of today, we have talked to two geologists who will perform work for us in the future.

C. ORGANIZATIONAL STRUCTURE

Not applicable

D. PROPERTY, PLANTS AND EQUIPMENT

We are a natural resource company engaged in the acquisition and exploration of natural resource properties. We commenced operations in 1996 and currently have an interest in the Finlayson properties consisting of 2626 un- surveyed quartz claims described below and intend to seek and acquire additional properties worthy of exploration and development.

Disclosure required of an extractive enterprise is contained in Item 4, Part B above. As the Company's properties are not at an advanced stage of exploration, no reserve estimates are made nor as of yet certain what if any reserves will be on the properties

ITEM 5. OPERATING AND FINANCIAL REVIEW AND PROSPECTS

A. Operating ResultsWe are a start-up, exploration stage corporation and have not yet generated or realized any revenues from our business operations.

Our auditors have issued a going concern opinion. This means that there is substantial doubt that we can continue as an on-going business for the next twelve months unless we obtain additional capital to pay our bills. This is because we have not generated any revenues and no revenues are anticipated until we begin removing and selling minerals. Accordingly, we must raise cash from sources other than the sale of minerals found on the properties. That cash must be raised from other sources. Our only other source for cash at this time is investments by others in Entourage Mining Ltd. We must raise cash to implement our project and stay in business. Even if we raise money, we do not know how long the money will last. It depends upon the amount of exploration we conduct and the cost thereof. We won't know that information until we begin exploring our properties. We will not be able to complete the exploration of our properties until we raise money.

If we find mineralized material and it is economically feasible to remove the mineralized material, we will attempt to raise additional money through a subsequent private placement, public offering or through loans. If we do not raise all of the money we need, we will have to find alternative sources of funding, like a public offering, a private placement of securities, or loans from our officers or others.

26

We have discussed this matter with our officers and directors, however, our officers and directors are unwilling to make any commitment to loan us any significant amounts of money at this time. At the present time, we have limited cash reserves and we are seeking to raise additional cash. If we need additional cash and can't raise it we will either have to suspend operations until we do raise the cash, or cease operations entirely.

Our exploration program is explained in as much detail as possible in the business section of this registration statement. We are not going to buy or sell any plant or significant equipment during the next twelve months. We will not buy any equipment until we have located a body of minerals and we have determined they are economical to extract from the land.

We do not intend to interest other companies in the properties if we find mineralized materials. We intend to try to develop the reserves ourselves.

If we are unable to complete any phase of exploration because we don't have enough money, we will cease operations until we raise more money. If we can't or don't raise more money, we will cease operations. If we cease operations, we don't know what we will do and we don't have any plans to do anything.

We do not intend to hire additional employees at this time. All of the work on the properties will be conducted by unaffiliated independent contractors that we will hire. The independent contractors will be responsible for surveying, geology, engineering, exploration, and excavation. The geologists will evaluate the information derived from the exploration and excavation and the engineers will advise us on the economic feasibility of removing the mineralized material.

Fiscal year ended December 31, 2003 ("fiscal 2003") compared to fiscal year ended December 31, 2002 ("fiscal2002")

During fiscal 2003 the Company spent $246,628 on exploration work on its Yukon property. Part of this expenditure has been paid from the $219,450 raised during February 2004 through a private placement of 997,500 shares at $0.22 per share. No exploration costs were incurred during the years ended December 31, 2002, 2001 and 2000.

During fiscal 2003 the total loss (as well as expenses) was $319,515 as compared to $59,428 during fiscal 2002. The main reason for the increase in losses were: the exploration costs during fiscal 2003 were $246,628 (nil during fiscal 2002); accounting and legal expenses were $49,399 as compared to $4,855 during fiscal 2002; and office and sundry expenses were $18,832 as compared to $32 during fiscal 2002. The main reason for the increased expenses was because the Company was listed on the OTC-BB and was more active during the fiscal 2003 as compared to fiscal 2002.

Fiscal year ended December 31, 2002 ("fiscal 2002") compared to fiscal year ended December 31, 2001 ("fiscal2001")

The total loss (as well as the total expenses) during the fiscal 2002 was $59,428 as compared to $58,749 during the fiscal 2001. During each of the years the main expenses were $30,000 for management fees and $24,000 for the rent. The Company was very inactive during both the years.

27

B. Liquidity and Capital Resources

As of the date of this report, we have yet to generate any revenues from our business operations.