UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-21374 | |||||||

| ||||||||

PIMCO Floating Rate Income Fund | ||||||||

(Exact name of registrant as specified in charter) | ||||||||

| ||||||||

1345 Avenue of the Americas, New York, NY |

| 10105 | ||||||

(Address of principal executive offices) |

| (Zip code) | ||||||

| ||||||||

Lawrence G. Altadonna - 1345 Avenue of the Americas, New York, NY 10105 | ||||||||

(Name and address of agent for service) | ||||||||

| ||||||||

Registrant’s telephone number, including area code: | 212-739-3371 |

| ||||||

| ||||||||

Date of fiscal year end: | July 31, 2009 |

| ||||||

| ||||||||

Date of reporting period: | July 31, 2009 |

| ||||||

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549-2001. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

ITEM 1: REPORT TO SHAREHOLDERS

| Contents |

|

|

| |

Letter to Shareholders | 1 | |

|

| |

Fund Insights/Performance & Statistics | 2-3 | |

|

| |

Schedules of Investments | 4-16 | |

|

| |

Statements of Assets and Liabilities | 17 | |

|

| |

Statements of Operations | 18 | |

|

| |

Statements of Changes in Net Assets | 19-20 | |

|

| |

Statements of Cash Flows | 21 | |

|

| |

Notes to Financial Statements | 22-41 | |

|

| |

Financial Highlights | 42-43 | |

|

| |

Report of Independent Registered Public Accounting Firm | 44 | |

|

| |

Tax Information/Annual Shareholder Meeting Results | 45 | |

|

| |

Changes to Investment Policies | 46 | |

|

| |

Matters Related to the Trustees’ Consideration of the Investment Management & Portfolio Management Agreements | 47-49 | |

|

| |

Privacy Policy/Proxy Voting Policies & Procedures | 50 | |

|

| |

Divident Reinvestment Plan | 51 | |

|

| |

Board of Trustees | 52-53 | |

|

| |

| Fund Officers | 54 |

|

|

|

|

|

|

|

| |

PIMCO Floating Rate Income/PIMCO Floating Rate Strategy Funds Letter to Shareholders

September 15, 2009

Dear Shareholder:

Please find enclosed the annual reports for PIMCO Floating Rate Income Fund and PIMCO Floating Rate Strategy Fund (collectively, the “Funds”) for the fiscal year ended July 31, 2009.

Corporate credit securities provided modest returns during the 12-month fiscal period as investors showed renewed enthusiasm for risk assets during the second half of the fiscal year. Early signs of improving economic conditions contributed to shifting sentiments away from low yielding U.S. Treasury securities and in favor of corporate stocks and bonds. In this environment, the Barclays Capital U.S. Aggregate Index, a broad credit market measure of government and corporate securities, posted a 7.85% return. The Barclays Capital Investment Grade Credit Index, a measure of high quality corporate bond performance, returned 8.69%. Mortgage-backed securities, as represented by the Barclays Capital Mortgage Index, returned 3.47% and the Barclays Capital U.S. High Yield Bond Index returned 4.94%. Stocks fared worse as the Standard & Poor’s 500 Index, an unmanaged index that is generally representative of the U.S. stock market, declined 19.96% despite having rallied 21.18% during the last six months of the fiscal year.

During the reporting period, the Federal Reserve (the “Fed”) reduced the Federal Funds Rate, the key target rate on loans between member banks, from 2.00% to the record-low target level of 0.00% to 0.25%. The Fed also engaged in quantitative easing, which included purchasing significant amounts of securities from banks in order to add to the supply of cash available for lending.

On April 6, 2009, the Funds issued a press release to make explicit that each Fund’s investment policies allow it to hold common stock received from conversion of other portfolio securities, such that common stocks may represent up to 20% of each Fund’s total assets. The Funds may invest in preferred stock and convertible securities, and these securities may allow for conversion into common stock.

For specific information on the Funds and a review of their performance for the reporting period, please see the following pages. If you have any questions regarding the information provided, we encourage you to contact your financial advisor or call the Funds’ shareholder servicing agent at (800) 254-5197. In addition, a wide range of information and resources is available on our website, www.allianzinvestors.com/closedendfunds.

Together with Allianz Global Investors Fund Management LLC, the Funds’ investment manager, and Pacific Investment Management Company LLC (“PIMCO”), the Funds’ sub-adviser, we thank you for investing with us.

We remain dedicated to serving your investment needs.

Sincerely,

|

|

|

|

|

|

Hans W. Kertess | Brian S. Shlissel |

Chairman | President & Chief Executive Officer |

7.31.09 | PIMCO Floating Rate Income/PIMCO Floating Rate Strategy Funds Annual Report 1

PIMCO Floating Rate Income Fund Fund Insights/Performance & Statistics

July 31, 2009 (unaudited)

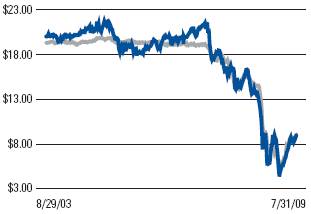

· For the fiscal year ended July 31, 2009, PIMCO Floating Rate Income Fund (the “Fund”) declined 28.97% on net asset value (“NAV”) and 25.78% on market price.

· Exposure to the finance sector, with specific emphasis on banking and insurance where performance came under pressure, was among the most significant detractors from returns.

· Security selection in the telecommunication sector, where the Fund’s focus has predominantly been on fixed-line companies relative to wireless providers, detracted from performance.

· Limited exposure to consumer non-cyclicals, such as food and tobacco, detracted from performance as the sector performed well during the fiscal 12-month reporting period.

· Minimal exposure to retailers, which outperformed during the reporting period despite difficult economic conditions, detracted from the Fund’s return.

· An initial above-market weighting in media cable loans, which was one of the best performing sectors during the reporting period, contributed positively to performance.

· Despite heightened volatility during the reporting period, exposure to auto-related credits benefited performance.

· An emphasis on health care early in the reporting period and a paring back of exposure in early 2009 as valuations richened, benefited returns.

Total Return(1): |

| Market Price |

| NAV |

|

1 Year |

| (25.78)% |

| (28.97)% |

|

5 Year |

| (5.94)% |

| (4.76)% |

|

Commencement of Operations (8/29/03) to 7/31/09 |

| (4.01)% |

| (3.35)% |

|

Market Price/NAV Performance: | Market Price/NAV: |

|

|

|

Commencement of Operations (8/29/03) to 7/31/09 | Market Price |

| $8.98 |

|

| NAV |

| $9.07 |

|

| Discount to NAV |

| (0.99)% |

|

| Market Price Yield(2) |

| 8.77% |

|

|

|

| ||

(1) Past performance is no guarantee of future results. Total return is calculated by determining the percentage change in net asset value or market share price (as applicable) in the specified period. The calculation assumes that all income dividends and capital gain distributions, if any, have been reinvested. Total return does not reflect broker commissions or sales charges. Total return for a period of more than one year represents the average annual total return.

Performance at market price will differ from its results at NAV. Although market price returns typically reflect investment results over time, during shorter periods returns at market price can also be influenced by factors such as changing views about the Fund, market conditions, supply and demand for the Fund’s shares, or changes in Fund distributions.

An investment in the Fund involves risk, including the loss of principal. Total return, market price, market yield and net asset value will fluctuate with changes in market conditions. This data is provided for information only and is not intended for trading purposes. Closed-end funds, unlike open-end funds, are not continuously offered. There is a onetime public offering and once issued, shares of closed-end funds are sold in the open market through a stock exchange. Net asset value is equal to total assets attributable to common shareholders less total liabilities divided by the number of common shares outstanding. Holdings are subject to change daily.

(2) Market Price Yield is determined by dividing the annualized current monthly per share dividend payable to common shareholders by the market price per common share at July 31, 2009.

2 PIMCO Floating Rate Income/PIMCO Floating Rate Strategy Funds Annual Report | 7.31.09

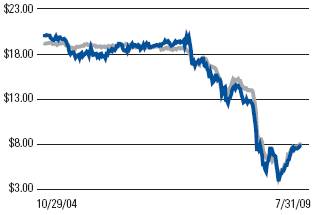

PIMCO Floating Rate Strategy Fund Fund Insights/Performance & Statistics

July 31, 2009 (unaudited)

· For the fiscal year ended July 31, 2009, PIMCO Floating Rate Strategy Fund (the “Fund”) declined 35.35% on net asset value (“NAV”) and 29.85% on market price.

· Exposure to the finance sector, with specific emphasis on banking and insurance where performance came under pressure, was among the most significant detractors from returns.

· Exposure to the non-cable media sector, which underperformed significantly amid a weakening advertising market, detracted from performance.

· Security selection in the telecommunication sector, where the Fund’s focus has predominantly been on fixed-line companies relative to wireless providers, detracted from performance.

· Adding exposure midway through the period to high-quality securitized holdings, such as residential mortgage-backed securities, detracted from the Fund’s return.

· An initial above-market weighting in media cable loans, one of the best performing sectors during the reporting period, contributed positively to performance.

· Despite heightened volatility during the fiscal 12-month reporting period, exposure to auto-related credits benefited performance.

· Limited exposure to the gaming sector, which experienced significant pressure during the reporting period, benefited returns.

Total Return(1): |

| Market Price |

| NAV |

|

1 Year |

| (29.85)% |

| (35.35)% |

|

3 Year |

| (16.11)% |

| (15.49)% |

|

Commencement of Operations (10/29/04) to 7/31/09 |

| (9.24)% |

| (8.07)% |

|

Market Price/NAV Performance: | Market Price/NAV: |

|

|

|

Commencement of Operations (10/29/04) to 7/31/09 | Market Price |

| $7.78 |

|

| NAV |

| $7.98 |

|

| Discount to NAV |

| (2.51)% |

|

| Market Price Yield(2) |

| 9.48% |

|

|

|

| ||

(1) Past performance is no guarantee of future results. Total return is calculated by determining the percentage change in net asset value or market share price (as applicable) in the specified period. The calculation assumes that all income dividends and capital gain distributions, if any, have been reinvested. Total return does not reflect broker commissions or sales charges. Total return for a period of more than one year represents the average annual total return.

Performance at market price will differ from its results at NAV. Although market price returns typically reflect investment results over time, during shorter periods returns at market price can also be influenced by factors such as changing views about the Fund, market conditions, supply and demand for the Fund’s shares, or changes in Fund distributions.

An investment in the Fund involves risk, including the loss of principal. Total return, market price, market yield and net asset value will fluctuate with changes in market conditions. This data is provided for information only and is not intended for trading purposes. Closed-end funds, unlike open-end funds, are not continuously offered. There is a onetime public offering and once issued, shares of closed-end funds are sold in the open market through a stock exchange. Net asset value is equal to total assets attributable to common shareholders less total liabilities divided by the number of common shares outstanding. Holdings are subject to change daily.

(2) Market Price Yield is determined by dividing the annualized current monthly per share dividend payable to common shareholders by the market price per common share at July 31, 2009.

7.31.09 | PIMCO Floating Rate Income/PIMCO Floating Rate Strategy Funds Annual Report 3

PIMCO Floating Rate Income Fund Schedule of Investments

July 31, 2009

Principal Amount |

|

|

| Credit Rating |

| Value |

| |

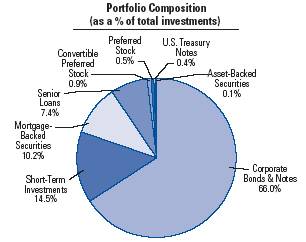

CORPORATE BONDS & NOTES – 66.0% |

|

|

|

|

| |||

|

|

|

|

|

| |||

Apparel & Textiles – 0.3% |

|

|

|

|

| |||

$900 |

| Hanesbrands, Inc., 4.593%, 12/15/14, FRN |

| B2/B |

| $765,000 |

| |

Banking – 26.1% |

|

|

|

|

| |||

1,600 |

| American Express Bank FSB, 0.418%, 5/29/12, FRN (j) |

| A2/A+ |

| 1,457,365 |

| |

2,100 |

| American Express Centurion Bank, 0.446%, 6/12/12, FRN |

| A2/A+ |

| 1,913,279 |

| |

£1,700 |

| BAC Capital Trust VII, 5.25%, 8/10/35 |

| Baa3/B |

| 1,676,943 |

| |

|

| Barclays Bank PLC (g), |

|

|

|

|

| |

$1,200 |

| 7.375%, 12/15/11 (a) (d) |

| Baa2/BBB+ |

| 877,356 |

| |

1,485 |

| 7.434%, 12/15/17 (a) (d) |

| Baa2/BBB+ |

| 1,130,208 |

| |

£4,300 |

| 14.00%, 6/15/19 |

| Baa2/BBB+ |

| 8,910,942 |

| |

$10,000 |

| Comerica Bank, 0.861%, 5/22/12, FRN |

| A1/A+ |

| 9,113,650 |

| |

1,000 |

| Den Norske Bank, 7.729%, 6/29/11 (a) (d) (g) |

| Aa3/BBB+ |

| 806,583 |

| |

600 |

| HBOS PLC, 6.75%, 5/21/18 (a) (d) |

| Baa2/A- |

| 462,245 |

| |

3,000 |

| JPMorgan Chase Bank N.A., 0.959%, 6/13/16, FRN |

| Aa2/A+ |

| 2,454,075 |

| |

|

| M&I Marshall & Ilsley Bank, FRN, |

|

|

|

|

| |

1,600 |

| 0.778%, 6/1/11 |

| A2/BBB |

| 1,392,723 |

| |

3,300 |

| 0.916%, 12/4/12 |

| A3/BBB- |

| 2,234,348 |

| |

1,629 |

| NB Capital Trust II, 7.83%, 12/15/26 |

| Baa3/B |

| 1,392,795 |

| |

€3,000 |

| Northern Rock PLC, 1.377%, 3/13/12, FRN |

| A2/A |

| 3,363,742 |

| |

$10,000 |

| Rabobank Nederland NV, 11.00%, 6/30/19 (a) (d) (g) |

| Aa2/AA- |

| 11,680,930 |

| |

7,200 |

| Regions Financial Corp., 0.774%, 6/26/12, FRN |

| Baa3/BBB+ |

| 5,988,377 |

| |

£1,955 |

| Royal Bank of Scotland PLC, 6.334%, 4/6/11, FRN |

| NR/NR |

| 1,799,194 |

| |

$6,000 |

| Wachovia Bank N.A., 0.959%, 3/15/16, FRN (j) |

| Aa3/AA- |

| 4,992,984 |

| |

4,250 |

| Wells Fargo & Co., 7.98%, 3/15/18 (g) |

| Ba3/A- |

| 3,681,677 |

| |

2,550 |

| Wells Fargo Capital XIII, 7.70%, 3/26/13 (g) |

| Ba3/A- |

| 2,220,180 |

| |

|

|

|

|

|

| 67,549,596 |

| |

Financial Services – 28.5% |

|

|

|

|

| |||

1,200 |

| American Express Credit Corp., 0.405%, 2/24/12, FRN (j) |

| A2/BBB+ |

| 1,088,287 |

| |

|

| American General Finance Corp., FRN, |

|

|

|

|

| |

3,900 |

| 0.879%, 12/15/11 |

| Baa2/BB+ |

| 2,579,300 |

| |

775 |

| 1.134%, 8/17/11 |

| Baa2/BB+ |

| 483,039 |

| |

2,500 |

| Chukchansi Economic Dev. Auth., |

| B3/B+ |

| 1,718,750 |

| |

|

| CIT Group, Inc., |

|

|

|

|

| |

6,200 |

| 0.734%, 4/27/11, FRN |

| Ca/CC |

| 3,713,323 |

| |

1,600 |

| 5.40%, 2/13/12 |

| Ca/CC |

| 878,259 |

| |

100 |

| Citigroup Capital XXI, 8.30%, 12/21/77, |

| Baa3/B+ |

| 84,250 |

| |

5,000 |

| Citigroup, Inc., 0.903%, 6/9/16, FRN |

| Baa1/A- |

| 3,628,850 |

| |

|

| Ford Motor Credit Co. LLC, |

|

|

|

|

| |

10,250 |

| 3.26%, 1/13/12, FRN |

| Caa1/CCC+ |

| 8,725,312 |

| |

2,200 |

| 7.25%, 10/25/11 |

| Caa1/CCC+ |

| 2,066,962 |

| |

|

| GMAC, Inc., |

|

|

|

|

| |

500 |

| 6.00%, 12/15/11 |

| Ca/CCC |

| 443,752 |

| |

1,425 |

| 6.875%, 9/15/11 |

| Ca/CCC |

| 1,298,184 |

| |

1,625 |

| 6.875%, 8/28/12 |

| Ca/CCC |

| 1,451,050 |

| |

2,600 |

| 7.25%, 3/2/11 |

| Ca/CCC |

| 2,420,382 |

| |

2,702 |

| 7.50%, 12/31/13 (a) (d) |

| Ca/CCC |

| 2,323,720 |

| |

|

| International Lease Finance Corp., |

|

|

|

|

| |

600 |

| 4.15%, 1/20/15 |

| Baa2/BBB+ |

| 551,700 |

| |

650 |

| 4.75%, 1/13/12 |

| Baa2/BBB+ |

| 464,129 |

| |

1,350 |

| 4.875%, 9/1/10 |

| Baa2/BBB+ |

| 1,155,492 |

| |

650 |

| 5.125%, 11/1/10 |

| Baa2/BBB+ |

| 543,263 |

| |

4 PIMCO Floating Rate Income/PIMCO Floating Rate Strategy Funds Annual Report | 7.31.09

PIMCO Floating Rate Income Fund Schedule of Investments

July 31, 2009 (continued)

Principal Amount |

|

|

| Credit Rating |

| Value |

| |

|

|

|

|

|

|

|

| |

Financial Services (continued) |

|

|

|

|

| |||

$650 |

| 5.30%, 5/1/12 |

| Baa2/BBB+ |

| $475,615 |

| |

650 |

| 5.35%, 3/1/12 |

| Baa2/BBB+ |

| 477,846 |

| |

650 |

| 5.45%, 3/24/11 |

| Baa2/BBB+ |

| 511,338 |

| |

7,150 |

| 5.625%, 9/15/10 (j) |

| Baa3/AA |

| 6,097,105 |

| |

2,111 |

| 5.625%, 9/20/13 |

| Baa2/BBB+ |

| 1,475,441 |

| |

4,100 |

| 5.75%, 6/15/11 |

| Baa2/BBB+ |

| 3,241,698 |

| |

2,947 |

| 6.625%, 11/15/13 |

| Baa2/BBB+ |

| 2,043,258 |

| |

9,100 |

| JPMorgan Chase & Co., 7.90%, 4/30/18 (g) |

| A2/BBB+ |

| 8,675,740 |

| |

1,500 |

| Lehman Brothers Holdings, Inc., 7.50%, 5/11/38 (e) |

| NR/NR |

| 150 |

| |

4,200 |

| MBNA Capital, 1.828%, 2/1/27, FRN |

| Baa3/B |

| 2,248,491 |

| |

|

| Morgan Stanley, FRN, |

|

|

|

|

| |

2,600 |

| 0.96%, 10/18/16 |

| A2/A |

| 2,253,454 |

| |

3,500 |

| 0.989%, 10/15/15 |

| A2/A |

| 3,108,161 |

| |

9,650 |

| SLM Corp., 0.734%, 10/25/11, FRN |

| Ba1/BBB- |

| 7,370,072 |

| |

|

|

|

|

|

| 73,596,373 |

| |

Insurance – 10.1% |

|

|

|

|

| |||

|

| American International Group, Inc., |

|

|

|

|

| |

5,900 |

| 0.62%, 10/18/11, FRN |

| A3/A- |

| 4,078,074 |

| |

10,000 |

| 0.671%, 9/27/10, FRN (f) |

| A3/A- |

| 6,810,437 |

| |

1,600 |

| 0.709%, 3/20/12, FRN |

| A3/NR |

| 956,990 |

| |

1,500 |

| 4.70%, 10/1/10 |

| A3/A- |

| 1,283,354 |

| |

5,000 |

| 4.95%, 3/20/12 |

| A3/A- |

| 3,445,225 |

| |

6,400 |

| 5.45%, 5/18/17 |

| A3/A- |

| 3,338,976 |

| |

700 |

| 8.175%, 5/15/68, (converts to FRN on 5/15/38) |

| Ba2/BBB |

| 183,750 |

| |

2,200 |

| 8.25%, 8/15/18 |

| A3/A- |

| 1,303,373 |

| |

£1,300 |

| 8.625%, 5/22/68, (converts to FRN on 5/22/18) (b) |

| Baa1/BBB |

| 538,801 |

| |

$4,600 |

| Pricoa Global Funding I, 0.734%, 6/26/12, FRN (a) (d) |

| A2/AA- |

| 4,285,139 |

| |

|

|

|

|

|

| 26,224,119 |

| |

Oil & Gas – 0.2% |

|

|

|

|

| |||

600 |

| SandRidge Energy, Inc., 8.00%, 6/1/18 (a) (d) |

| B3/B- |

| 549,000 |

| |

Paper/Paper Products – 0.5% |

|

|

|

|

| |||

2,500 |

| Verso Paper Holdings LLC, 4.778%, 8/1/14, FRN |

| B2/B- |

| 1,212,500 |

| |

Telecommunications – 0.0% |

|

|

|

|

| |||

2,500 |

| Hawaiian Telcom Communications, Inc., 8.49%, 5/1/13, FRN (b) (e) |

| WR/NR |

| 18,750 |

| |

Utilities – 0.3% |

|

|

|

|

| |||

1,000 |

| CMS Energy Corp., 1.459%, 1/15/13, FRN |

| Ba1/BB+ |

| 827,500 |

| |

Total Corporate Bonds & Notes (cost-$172,594,951) |

|

|

| 170,742,838 |

| |||

|

|

|

|

|

| |||

MORTGAGE-BACKED SECURITIES – 10.2% |

|

|

|

|

| |||

477 |

| Banc of America Commercial Mortgage, Inc., |

| NR/AAA |

| 481,777 |

| |

700 |

| Bear Stearns Commercial Mortgage Securities Inc., |

| NR/AAA |

| 591,260 |

| |

1,500 |

| Citigroup/Deutsche Bank Commercial Mortgage Trust, |

| Aaa/AAA |

| 1,194,295 |

| |

|

| Commercial Mortgage Pass Through Certificates, CMO, |

|

|

|

|

| |

1,900 |

| 5.306%, 12/10/46 |

| Aaa/NR |

| 1,544,777 |

| |

6,550 |

| 6.010%, 12/10/49, VRN |

| Aaa/AAA |

| 5,592,518 |

| |

900 |

| Credit Suisse Mortgage Capital Certificates, |

| NR/AAA |

| 708,742 |

| |

7.31.09 | PIMCO Floating Rate Income/PIMCO Floating Rate Strategy Funds Annual Report 5

PIMCO Floating Rate Income Fund Schedule of Investments

July 31, 2009 (continued)

Principal Amount |

|

|

| Credit Rating |

| Value |

| |

|

|

|

|

|

|

|

| |

$2,330 |

| GS Mortgage Securities Corp. II, 5.56%, 11/10/39, CMO |

| Aaa/NR |

| $2,167,403 |

| |

4,600 |

| JPMorgan Chase Commercial Mortgage Securities Corp., |

| Aaa/AAA |

| 3,760,147 |

| |

3,625 |

| LB-UBS Commercial Mortgage Trust, |

| NR/AAA |

| 2,972,856 |

| |

1,182 |

| Mellon Residential Funding Corp., |

| Aaa/AAA |

| 887,335 |

| |

8,069 |

| Morgan Stanley Capital I, 6.076%, 6/11/49, CMO, VRN |

| NR/AAA |

| 6,449,860 |

| |

Total Mortgage-Backed Securities (cost-$24,826,319) |

|

|

| 26,350,970 |

| |||

|

|

|

|

|

| |||

SENIOR LOANS (a) (c) – 7.4% |

|

|

|

|

| |||

|

|

|

|

|

| |||

Automotive Products – 0.5% |

|

|

|

|

| |||

|

| Delphi Corp. (b), |

|

|

|

|

| |

2,269 |

| 8.50%, 6/30/20 |

|

|

| 1,081,523 |

| |

231 |

| 8.50%, 6/30/20, Term DD |

|

|

| 110,144 |

| |

|

|

|

|

|

| 1,191,667 |

| |

Banking – 0.6% |

|

|

|

|

| |||

|

| Aster Co., Ltd. (b), |

|

|

|

|

| |

1,092 |

| 4.013%, 9/19/13, Term B |

|

|

| 716,916 |

| |

1,132 |

| 4.013%, 9/19/14, Term C |

|

|

| 742,643 |

| |

|

|

|

|

|

| 1,459,559 |

| |

Chemicals – 0.2% |

|

|

|

|

| |||

€287 |

| Brenntag AG, 3.214%, 12/23/13, Term B |

|

|

| 387,986 |

| |

Consumer Products – 0.3% |

|

|

|

|

| |||

$1,000 |

| National Mentor, Inc., 2.901%, 6/29/12 (b) |

|

|

| 858,333 |

| |

Containers & Packaging – 0.0% |

|

|

|

|

| |||

|

| Graphic Packaging International Corp., |

|

|

|

|

| |

3 |

| 2.334%, 5/3/14 |

|

|

| 2,884 |

| |

3 |

| 2.504%, 5/3/14 |

|

|

| 2,628 |

| |

6 |

| 2.504%, 5/3/14, Term B |

|

|

| 5,782 |

| |

3 |

| 2.505%, 5/3/14, Term A |

|

|

| 2,628 |

| |

1 |

| 2.509%, 5/3/14 |

|

|

| 1,066 |

| |

12 |

| 2.597%, 5/3/14 |

|

|

| 11,301 |

| |

|

|

|

|

|

| 26,289 |

| |

Diversified Manufacturing – 0.7% |

|

|

|

|

| |||

4,519 |

| Grant Forest Products, 10.25%, 9/16/13 (b) |

|

|

| 233,495 |

| |

|

| KION Group GmbH (b), |

|

|

|

|

| |

1,250 |

| 2.285%, 12/20/14, Term B |

|

|

| 781,250 |

| |

1,250 |

| 2.785%, 12/20/15, Term C |

|

|

| 781,250 |

| |

|

|

|

|

|

| 1,795,995 |

| |

Drugs & Medical Products – 0.9% |

|

|

|

|

| |||

€985 |

| Bausch & Lomb, Inc., 4.37%, 4/11/15, Term T |

|

|

| 1,328,845 |

| |

€709 |

| Mylan Laboratories, Inc., 3.29%, 10/2/13, Term A |

|

|

| 942,176 |

| |

|

|

|

|

|

| 2,271,021 |

| |

Electronics – 0.4% |

|

|

|

|

| |||

|

| Sensata Technologies, Inc. (b), |

|

|

|

|

| |

€2 |

| 2.706%, 4/21/13 |

|

|

| 2,933 |

| |

€985 |

| 2.892%, 4/27/13 |

|

|

| 1,136,097 |

| |

|

|

|

|

|

| 1,139,030 |

| |

6 PIMCO Floating Rate Income/PIMCO Floating Rate Strategy Funds Annual Report | 7.31.09

PIMCO Floating Rate Income Fund Schedule of Investments

July 31, 2009 (continued)

Principal Amount |

|

|

| Credit Rating |

| Value |

| |

|

|

|

|

|

|

|

| |

Entertainment – 0.3% |

|

|

|

|

| |||

|

| Revolution Studios LLC (b), |

|

|

|

|

| |

$470 |

| 2.79%, 12/21/12, Term A |

|

|

| $427,930 |

| |

419 |

| 4.04%, 12/21/14, Term B |

|

|

| 381,524 |

| |

|

|

|

|

|

| 809,454 |

| |

Financial Services – 0.9% |

|

|

|

|

| |||

935 |

| Chrysler Financial Corp., 4.29%, 8/3/12, Term B |

|

|

| 886,798 |

| |

|

| FCI S.A., Term B (b), |

|

|

|

|

| |

100 |

| 3.406%, 3/9/13 |

|

|

| 68,043 |

| |

2,083 |

| 3.406%, 3/8/14 |

|

|

| 1,416,303 |

| |

|

|

|

|

|

| 2,371,144 |

| |

Food & Beverage – 0.4% |

|

|

|

|

| |||

|

| Dole Foods Co., |

|

|

|

|

| |

108 |

| 0.505%, 4/12/13 |

|

|

| 108,724 |

| |

23 |

| 7.25%, 4/12/13, Term C |

|

|

| 23,217 |

| |

188 |

| 8.00%, 4/12/13, Term B |

|

|

| 190,060 |

| |

679 |

| 8.00%, 4/12/13, Term C |

|

|

| 684,964 |

| |

|

|

|

|

|

| 1,006,965 |

| |

Healthcare & Hospitals – 0.7% |

|

|

|

|

| |||

|

| Community Health Systems, Inc., |

|

|

|

|

| |

49 |

| 2.535%, 7/25/14 |

|

|

| 45,718 |

| |

68 |

| 2.535%, 7/25/14, Term B |

|

|

| 63,908 |

| |

884 |

| 2.924%, 7/25/14, Term B |

|

|

| 832,249 |

| |

€1,000 |

| ISTA, 5.085%, 6/15/16 |

|

|

| 891,410 |

| |

|

|

|

|

|

| 1,833,285 |

| |

Multi-Media – 0.6% |

|

|

|

|

| |||

|

| Seven Media Group, Term T, |

|

|

|

|

| |

AUD 2,766 |

| 5.365%, 12/28/12 |

|

|

| 1,345,077 |

| |

AUD 662 |

| 5.73%, 12/28/12 |

|

|

| 322,060 |

| |

|

|

|

|

|

| 1,667,137 |

| |

Paper/Paper Products – 0.0% |

|

|

|

|

| |||

|

| Verso Paper Holdings LLC (b), |

|

|

|

|

| |

$448 |

| 6.733%, 2/1/13 |

|

|

| 100,800 |

| |

23 |

| 7.483%, 2/1/13 |

|

|

| 5,202 |

| |

|

|

|

|

|

| 106,002 |

| |

Recreation – 0.0% |

|

|

|

|

| |||

1 |

| Cedar Fair L.P., 2.285%, 8/30/12 |

|

|

| 1,469 |

| |

Telecommunications – 0.6% |

|

|

|

|

| |||

2,556 |

| Hawaiian Telcom Communications, Inc., |

|

|

| 1,571,902 |

| |

Waste Disposal – 0.3% |

|

|

|

|

| |||

€500 |

| AVR-Bedrijven NV, 3.042%, 3/1/15 (b) |

|

|

| 633,851 |

| |

Total Senior Loans (cost-$30,663,276) |

|

|

| 19,131,089 |

| |||

|

|

|

|

|

| |||

CONVERTIBLE PREFERRED STOCK – 0.9% |

|

|

|

|

| |||

|

|

|

|

|

|

|

| |

Shares |

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

| |

Banking – 0.9% |

|

|

|

|

| |||

2,700 |

| Wells Fargo & Co., 7.50%, 12/31/49, Ser. L (cost-$1,869,885) |

| Ba3/A- |

| 2,267,892 |

| |

7.31.09 | PIMCO Floating Rate Income/PIMCO Floating Rate Strategy Funds Annual Report 7

PIMCO Floating Rate Income Fund Schedule of Investments

July 31, 2009 (continued)

Shares |

|

|

|

|

| Value |

| |||||||

PREFERRED STOCK – 0.5% |

|

|

|

|

| |||||||||

|

|

|

|

|

| |||||||||

Financial Services – 0.5% |

|

|

|

|

| |||||||||

30 |

| Richmond Cnty. Capital Corp., 4.381%, Ser. C, FRN (a) (b) (d) (f) |

| NR/NR |

| $1,191,803 |

| |||||||

|

|

|

|

|

| |||||||||

U.S. TREASURY NOTES (h) – 0.4% |

|

|

|

|

| |||||||||

|

|

|

|

|

|

|

| |||||||

Principal |

|

|

|

|

|

|

| |||||||

|

|

|

|

|

|

|

| |||||||

$1,119 |

| U.S. Treasury Notes, 1.13%, 6/30/11 (cost-$1,124,066) |

|

|

| 1,120,402 |

| |||||||

|

|

|

|

|

| |||||||||

ASSET-BACKED SECURITIES – 0.1% |

|

|

|

|

| |||||||||

|

|

|

|

|

| |||||||||

|

| Credit Suisse First Boston Mortgage Securities Corp., FRN, |

|

|

|

|

| |||||||

12 |

| 0.985%, 7/25/32 |

| Aaa/AAA |

| 4,442 |

| |||||||

426 |

| 1.025%, 8/25/32 |

| Aaa/AAA |

| 157,021 |

| |||||||

Total Asset-Backed Securities (cost-$438,358) |

|

|

| 161,463 |

| |||||||||

|

|

|

|

|

| |||||||||

SHORT-TERM INVESTMENTS – 14.5% |

|

|

|

|

| |||||||||

|

|

|

|

|

| |||||||||

Corporate Notes – 13.9% |

|

|

|

|

| |||||||||

Banking – 1.2% |

|

|

|

|

| |||||||||

3,300 |

| M&I Marshall & Ilsley Bank, 0.754%, 6/16/10, FRN |

| A2/BBB |

| 3,153,022 |

| |||||||

Financial Services – 11.8% |

|

|

|

|

| |||||||||

|

| American General Finance Corp., |

|

|

|

|

| |||||||

4,800 |

| 0.706%, 3/2/10, FRN |

| Baa2/BB+ |

| 4,201,497 |

| |||||||

1,000 |

| 3.875%, 10/1/09 |

| Baa2/BB+ |

| 960,563 |

| |||||||

900 |

| 4.875%, 5/15/10 |

| Baa2/BB+ |

| 778,574 |

| |||||||

5,750 |

| CIT Group, Inc., 0.759%, 3/12/10, FRN |

| Ca/CC |

| 3,370,937 |

| |||||||

1,625 |

| Ford Motor Credit Co. LLC, 7.375%, 10/28/09 |

| Caa1/CCC+ |

| 1,622,117 |

| |||||||

1,625 |

| GMAC, Inc., 7.75%, 1/19/10 |

| Ca/CCC |

| 1,606,394 |

| |||||||

|

| International Lease Finance Corp., |

|

|

|

|

| |||||||

2,000 |

| 0.881%, 5/24/10, FRN |

| Baa2/BBB+ |

| 1,741,740 |

| |||||||

4,300 |

| 0.909%, 1/15/10, FRN |

| Baa2/BBB+ |

| 4,105,881 |

| |||||||

900 |

| 4.55%, 10/15/09 |

| Baa2/BBB+ |

| 882,875 |

| |||||||

4,450 |

| 5.00%, 4/15/10 |

| Baa2/BBB+ |

| 4,002,922 |

| |||||||

3,600 |

| SLM Corp., 0.37%, 3/15/10, FRN |

| Ba1/BBB- |

| 3,295,206 |

| |||||||

|

| Universal City Florida Holding Co., |

|

|

|

|

| |||||||

3,500 |

| 5.778%, 5/1/10, FRN |

| Caa2/B- |

| 3,062,500 |

| |||||||

1,000 |

| 8.375%, 5/1/10 |

| Caa2/B- |

| 890,000 |

| |||||||

|

|

|

|

|

| 30,521,206 |

| |||||||

Insurance – 0.9% |

|

|

|

|

| |||||||||

700 |

| AIG Matched Funding Corp., 0.32%, 9/8/09, FRN (a) (d) |

| A3/A- |

| 613,375 |

| |||||||

|

| Residential Reinsurance Ltd., FRN (a) (b) (d), |

|

|

|

|

| |||||||

1,300 |

| 7.918%, 6/7/10 |

| NR/BB |

| 1,249,950 |

| |||||||

500 |

| 8.418%, 6/7/10 |

| NR/BB- |

| 477,650 |

| |||||||

|

|

|

|

|

| 2,340,975 |

| |||||||

Total Corporate Notes (cost-$38,032,103) |

|

|

| 36,015,203 |

| |||||||||

U.S. Treasury Bill (h) – 0.1% |

|

|

|

|

| |||||||||

150 |

| 0.15%, 8/20/09 (cost-$149,988) |

|

|

| 149,988 |

| |||||||

8 PIMCO Floating Rate Income/PIMCO Floating Rate Strategy Funds Annual Report | 7.31.09

PIMCO Floating Rate Income Fund Schedule of Investments

July 31, 2009 (continued)

Principal Amount |

|

|

|

|

| Value |

| |

|

|

|

|

|

|

|

| |

Repurchase Agreement – 0.5% |

|

|

|

|

| |||

$1,366 |

| State Street Bank & Trust Co., dated 7/31/09, 0.01%, due 8/3/09, proceeds $1,366,001; collateralized by U.S. Treasury Bills, 0.09%, due 9/10/09, valued at $1,394,861 including accrued interest (cost-$1,366,000) |

|

|

| $1,366,000 |

| |

Total Short-Term Investments (cost-$39,548,091) |

|

|

| 37,531,191 |

| |||

Total Investments (cost-$274,133,253) – 100.0% |

|

|

| $258,497,648 |

| |||

7.31.09 | PIMCO Floating Rate Income/PIMCO Floating Rate Strategy Funds Annual Report 9

PIMCO Floating Rate Strategy Fund Schedule of Investments

July 31, 2009

Principal |

|

|

| Credit Rating |

| Value |

| ||

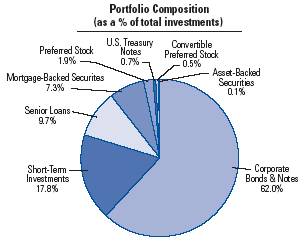

CORPORATE BONDS & NOTES – 62.0% |

|

|

|

|

| ||||

|

|

|

|

|

| ||||

Banking – 24.1% |

|

|

|

|

| ||||

$3,400 |

| American Express Bank FSB, 0.418%, 5/29/12, FRN |

| A2/A+ |

| $3,096,900 |

| ||

£2,100 |

| BAC Capital Trust VII, 5.25%, 8/10/35 |

| Baa3/B |

| 2,071,518 |

| ||

|

| Barclays Bank PLC (g), |

|

|

|

|

| ||

$2,600 |

| 7.375%, 12/15/11 (a) (d) |

| Baa2/BBB+ |

| 1,900,938 |

| ||

3,000 |

| 7.434%, 12/15/17 (a) (d) |

| Baa2/BBB+ |

| 2,283,249 |

| ||

£8,600 |

| 14.00%, 6/15/19 |

| Baa2/BBB+ |

| 17,821,884 |

| ||

$20,000 |

| Comerica Bank, 0.861%, 5/22/12, FRN |

| A1/A+ |

| 18,227,300 |

| ||

2,000 |

| Den Norske Bank, 7.729%, 6/29/11 (a) (d) (g) |

| Aa3/BBB+ |

| 1,613,166 |

| ||

1,400 |

| HBOS PLC, 6.75%, 5/21/18 (a) (d) |

| Baa2/A- |

| 1,078,573 |

| ||

€4,900 |

| Keycorp, 1.444%, 11/22/10, FRN |

| Baa1/BBB+ |

| 6,293,264 |

| ||

|

| M&I Marshall & Ilsley Bank, FRN, |

|

|

|

|

| ||

$3,400 |

| 0.778%, 6/1/11 |

| A2/BBB |

| 2,959,537 |

| ||

6,700 |

| 0.916%, 12/4/12 |

| A3/BBB- |

| 4,536,402 |

| ||

3,500 |

| NB Capital Trust II, 7.83%, 12/15/26 |

| Baa3/B |

| 2,992,500 |

| ||

15,000 |

| Rabobank Nederland NV, 11.00%, 6/30/19 (a) (d) (g) |

| Aa2/AA- |

| 17,521,395 |

| ||

14,900 |

| Regions Financial Corp., 0.774%, 6/26/12, FRN |

| Baa3/BBB+ |

| 12,392,613 |

| ||

£3,911 |

| Royal Bank of Scotland PLC, 6.334%, 4/6/11, FRN |

| NR/NR |

| 3,598,388 |

| ||

$13,000 |

| Wachovia Bank N.A., 0.959%, 3/15/16, FRN |

| Aa3/AA- |

| 10,818,132 |

| ||

6,750 |

| Wells Fargo & Co., 7.98%, 3/15/18 (g) |

| Ba3/A- |

| 5,847,370 |

| ||

9,900 |

| Wells Fargo Capital XIII, 7.70%, 3/26/13 (g) |

| Ba3/A- |

| 8,619,524 |

| ||

|

|

|

|

|

| 123,672,653 |

| ||

Financial Services – 28.5% |

|

|

|

|

| ||||

1,600 |

| AIG SunAmerica Global Financing VI, 6.30%, 5/10/11 (a) (d) |

| A1/A+ |

| 1,533,688 |

| ||

2,570 |

| American Express Credit Corp., 0.405%, 2/24/12, FRN |

| A2/BBB+ |

| 2,330,748 |

| ||

|

| American General Finance Corp., FRN, |

|

|

|

|

| ||

8,450 |

| 0.879%, 12/15/11 |

| Baa2/BB+ |

| 5,588,484 |

| ||

1,625 |

| 1.134%, 8/17/11 |

| Baa2/BB+ |

| 1,012,824 |

| ||

3,500 |

| Chukchansi Economic Dev. Auth., |

|

|

|

|

| ||

|

| 4.913%, 11/15/12, FRN (a) (b) (d) |

| B3/B+ |

| 2,406,250 |

| ||

1,350 |

| CIT Group Funding Co. of Canada, 5.60%, 11/2/11 |

| Ca/CC |

| 944,996 |

| ||

|

| CIT Group, Inc., |

|

|

|

|

| ||

13,000 |

| 0.734%, 4/27/11, FRN (j) |

| Ca/CC |

| 7,785,999 |

| ||

350 |

| 4.75%, 12/15/10 |

| Ca/CC |

| 196,672 |

| ||

1,000 |

| 5.40%, 2/13/12 |

| Ca/CC |

| 548,912 |

| ||

1,350 |

| 5.60%, 4/27/11 |

| Ca/CC |

| 760,716 |

| ||

200 |

| Citigroup Capital XXI, 8.30%, 12/21/77, |

| Baa3/B+ |

| 168,500 |

| ||

|

| Citigroup, Inc., |

|

|

|

|

| ||

15,000 |

| 0.903%, 6/9/16, FRN |

| Baa1/A- |

| 10,886,550 |

| ||

100 |

| 6.50%, 8/19/13 |

| A3/A |

| 102,060 |

| ||

|

| Ford Motor Credit Co. LLC, |

|

|

|

|

| ||

8,400 |

| 3.26%, 1/13/12, FRN |

| Caa1/CCC+ |

| 7,150,500 |

| ||

7,000 |

| 7.25%, 10/25/11 |

| Caa1/CCC+ |

| 6,576,696 |

| ||

3,300 |

| 7.80%, 6/1/12 |

| Caa1/CCC+ |

| 3,104,030 |

| ||

1,400 |

| General Electric Capital Corp., 0.768%, 10/6/15, FRN |

| Aa2/AA+ |

| 1,165,469 |

| ||

4,800 |

| Genworth Global Funding Trusts, 1.023%, 5/15/12, FRN |

| A2/A |

| 4,050,038 |

| ||

|

| GMAC, Inc., |

|

|

|

|

| ||

3,000 |

| 2.868%, 12/1/14, FRN |

| Ca/CCC |

| 2,103,750 |

| ||

5,500 |

| 6.00%, 12/15/11 |

| Ca/CCC |

| 4,881,278 |

| ||

3,000 |

| 6.75%, 12/1/14 |

| Ca/CCC |

| 2,532,744 |

| ||

3,575 |

| 6.875%, 9/15/11 |

| Ca/CCC |

| 3,256,846 |

| ||

3,375 |

| 6.875%, 8/28/12 |

| Ca/CCC |

| 3,013,720 |

| ||

10 PIMCO Floating Rate Income/PIMCO Floating Rate Strategy Funds Annual Report | 7.31.09

PIMCO Floating Rate Strategy Fund Schedule of Investments

July 31, 2009 (continued)

Principal |

|

|

| Credit Rating |

| Value |

| ||

|

|

|

|

|

| ||||

Financial Services (continued) |

|

|

|

|

| ||||

|

| International Lease Finance Corp., |

|

|

|

|

| ||

$1,400 |

| 4.15%, 1/20/15 |

| Baa2/BBB+ |

| $1,287,300 |

| ||

1,350 |

| 4.75%, 1/13/12 |

| Baa2/BBB+ |

| 963,959 |

| ||

2,785 |

| 4.875%, 9/1/10 |

| Baa2/BBB+ |

| 2,383,737 |

| ||

1,350 |

| 5.125%, 11/1/10 |

| Baa2/BBB+ |

| 1,128,316 |

| ||

1,350 |

| 5.30%, 5/1/12 |

| Baa2/BBB+ |

| 987,817 |

| ||

1,350 |

| 5.35%, 3/1/12 |

| Baa2/BBB+ |

| 992,448 |

| ||

1,350 |

| 5.45%, 3/24/11 |

| Baa2/BBB+ |

| 1,062,010 |

| ||

17,560 |

| 5.625%, 9/15/10 |

| Baa3/AA |

| 14,974,150 |

| ||

4,950 |

| 5.625%, 9/20/13 |

| Baa2/BBB+ |

| 3,459,704 |

| ||

5,950 |

| 6.625%, 11/15/13 |

| Baa2/BBB+ |

| 4,125,343 |

| ||

15,900 |

| JPMorgan Chase & Co., 7.90%, 4/30/18 (g) |

| A2/BBB+ |

| 15,158,710 |

| ||

2,500 |

| Lehman Brothers Holdings, Inc., 7.50%, 5/11/38 (e) |

| NR/NR |

| 250 |

| ||

7,450 |

| Morgan Stanley, 0.989%, 10/15/15, FRN |

| A2/A |

| 6,615,943 |

| ||

|

| SLM Corp., FRN, |

|

|

|

|

| ||

19,350 |

| 0.734%, 10/25/11 |

| Ba1/BBB- |

| 14,778,330 |

| ||

10,000 |

| 1.413%, 9/15/15 |

| Ba1/BBB- |

| 6,569,000 |

| ||

|

|

|

|

|

| 146,588,487 |

| ||

Insurance – 8.7% |

|

|

|

|

| ||||

5,000 |

| AIG Life Holdings U.S., Inc., 7.50%, 8/11/10 |

| A3/A- |

| 4,854,260 |

| ||

|

| American International Group, Inc., |

|

|

|

|

| ||

12,600 |

| 0.62%, 10/18/11, FRN |

| A3/A- |

| 8,709,107 |

| ||

10,000 |

| 0.671%, 9/27/10, FRN (f) |

| A3/A- |

| 6,810,437 |

| ||

3,400 |

| 0.709%, 3/20/12, FRN |

| A3/A- |

| 2,033,605 |

| ||

2,500 |

| 4.70%, 10/1/10 |

| A3/A- |

| 2,138,922 |

| ||

3,200 |

| 4.95%, 3/20/12 |

| A3/A- |

| 2,204,944 |

| ||

13,600 |

| 5.45%, 5/18/17 |

| A3/A- |

| 7,095,324 |

| ||

1,450 |

| 8.175%, 5/15/68, (converts to FRN on 5/15/38) |

| Ba2/BBB |

| 380,625 |

| ||

£2,400 |

| 8.625%, 5/22/68, (converts to FRN on 5/22/18) (b) |

| Baa1/BBB |

| 994,710 |

| ||

$10,000 |

| Pricoa Global Funding I, 0.734%, 6/26/12, FRN (a) (d) |

| A2/AA- |

| 9,315,520 |

| ||

|

|

|

|

|

| 44,537,454 |

| ||

Paper/Paper Products – 0.7% |

|

|

|

|

| ||||

7,500 |

| Verso Paper Holdings LLC, 4.778%, 8/1/14, FRN |

| B2/B- |

| 3,637,500 |

| ||

Telecommunications – 0.0% |

|

|

|

|

| ||||

8,750 |

| Hawaiian Telcom Communications, Inc., |

| WR/NR |

| 65,625 |

| ||

Total Corporate Bonds & Notes (cost-$329,354,370) |

|

|

| 318,501,719 |

| ||||

|

|

|

|

|

| ||||

SENIOR LOANS (a) (c) – 9.7% |

|

|

|

|

| ||||

|

|

|

|

|

| ||||

Automotive – 0.1% |

|

|

|

|

| ||||

|

| Ford Motor Corp., Term B, |

|

|

|

|

| ||

51 |

| 3.29%, 12/16/13 |

|

|

| 43,622 |

| ||

734 |

| 3.51%, 12/16/13 |

|

|

| 627,023 |

| ||

|

|

|

|

|

| 670,645 |

| ||

Automotive Products – 0.8% |

|

|

|

|

| ||||

|

| Delphi Corp. (b), |

|

|

|

|

| ||

7,261 |

| 8.50%, 6/30/20 |

|

|

| 3,460,873 |

| ||

739 |

| 8.50%, 6/30/20, Term DD |

|

|

| 352,463 |

| ||

311 |

| 9.25%, 9/30/09 |

|

|

| 311,246 |

| ||

|

|

|

|

|

| 4,124,582 |

| ||

7.31.09 | PIMCO Floating Rate Income/PIMCO Floating Rate Strategy Funds Annual Report 11

PIMCO Floating Rate Strategy Fund Schedule of Investments

July 31, 2009 (continued)

Principal |

|

|

| Value |

| ||

|

|

|

|

|

| ||

Banking – 1.1% |

|

|

| ||||

|

| Aster Co., Ltd. (b), |

|

|

| ||

€1,800 |

| 3.945%, 9/19/13, Term B |

| $1,735,326 |

| ||

$2,137 |

| 4.013%, 9/19/13, Term B |

| 1,402,661 |

| ||

1,500 |

| 4.013%, 9/19/14, Term B |

| 984,375 |

| ||

2,214 |

| 4.013%, 9/19/14, Term C |

| 1,452,995 |

| ||

|

|

|

| 5,575,357 |

| ||

Chemicals – 0.4% |

|

|

| ||||

€287 |

| Brenntag AG, 3.214%, 12/23/13, Term B |

| 387,986 |

| ||

€1,457 |

| MacDermid, Inc., 2.754%, 4/12/14 (b) |

| 1,497,092 |

| ||

|

|

|

| 1,885,078 |

| ||

Consumer Products – 0.5% |

|

|

| ||||

$3,000 |

| National Mentor, Inc., 2.901%, 6/29/12 (b) |

| 2,574,999 |

| ||

Containers & Packaging – 0.0% |

|

|

| ||||

|

| Graphic Packaging International Corp., |

|

|

| ||

3 |

| 2.334%, 5/3/14 |

| 2,884 |

| ||

3 |

| 2.504%, 5/3/14 |

| 2,628 |

| ||

6 |

| 2.504%, 5/3/14, Term B |

| 5,782 |

| ||

3 |

| 2.505%, 5/3/14, Term A |

| 2,628 |

| ||

1 |

| 2.509%, 5/3/14 |

| 1,066 |

| ||

12 |

| 2.597%, 5/3/14 |

| 11,301 |

| ||

|

|

|

| 26,289 |

| ||

Diversified Manufacturing – 0.9% |

|

|

| ||||

9,684 |

| Grant Forest Products, 10.25%, 9/16/13 (b) |

| 500,346 |

| ||

|

| KION Group GmbH (b), |

|

|

| ||

3,000 |

| 2.285%, 12/20/14, Term B |

| 1,875,000 |

| ||

3,000 |

| 2.785%, 12/20/15, Term C |

| 1,875,000 |

| ||

|

| Linpac Mouldings Ltd. (b), |

|

|

| ||

1,016 |

| 2.76%, 4/16/12, Term B |

| 248,847 |

| ||

1,277 |

| 3.26%, 4/16/12, Term C |

| 312,901 |

| ||

|

|

|

| 4,812,094 |

| ||

Electronics – 0.2% |

|

|

| ||||

|

| Sensata Technologies, Inc., (b) |

|

|

| ||

€3 |

| 2.706%, 4/21/13 |

| 2,933 |

| ||

€985 |

| 2.892%, 4/27/13 |

| 1,136,097 |

| ||

|

|

|

| 1,139,030 |

| ||

Financial Services – 1.7% |

|

|

| ||||

$1,819 |

| Chrysler Financial Corp., 4.29%, 8/3/12, Term B |

| 1,724,126 |

| ||

|

| FCI S.A., Term B (b), |

|

|

| ||

173 |

| 3.406%, 3/9/13 |

| 117,529 |

| ||

3,598 |

| 3.406%, 3/8/14 |

| 2,446,341 |

| ||

|

| One (b), |

|

|

| ||

€2,000 |

| 3.292%, 2/4/16, Term B |

| 2,268,400 |

| ||

€2,000 |

| 3.792%, 2/4/17, Term C |

| 2,268,400 |

| ||

|

|

|

| 8,824,796 |

| ||

Food & Beverage – 0.2% |

|

|

| ||||

|

| Dole Foods Co., |

|

|

| ||

$108 |

| 0.505%, 4/12/13 |

| 108,724 |

| ||

23 |

| 7.25%, 4/12/13, Term C |

| 23,217 |

| ||

188 |

| 8.00%, 4/12/13, Term B |

| 190,060 |

| ||

679 |

| 8.00%, 4/12/13, Term C |

| 684,964 |

| ||

|

|

|

| 1,006,965 |

| ||

12 PIMCO Floating Rate Income/PIMCO Floating Rate Strategy Funds Annual Report | 7.31.09

PIMCO Floating Rate Strategy Fund Schedule of Investments

July 31, 2009 (continued)

Principal |

|

|

| Credit Rating |

| Value |

| ||||

|

|

|

|

|

| ||||||

Healthcare & Hospitals – 0.5% |

|

|

|

|

| ||||||

€3,000 |

| ISTA, 5.085%, 6/15/16 |

|

|

| $2,674,231 |

| ||||

Manufacturing – 0.5% |

|

|

|

|

| ||||||

|

| Bombardier, Inc., Term B (b), |

|

|

|

|

| ||||

$2,028 |

| 3.33%, 6/26/13 |

|

|

| 1,449,886 |

| ||||

1,586 |

| 4.11%, 6/26/13 |

|

|

| 1,134,070 |

| ||||

|

|

|

|

|

| 2,583,956 |

| ||||

Multi-Media – 1.4% |

|

|

|

|

| ||||||

4,328 |

| Insight Communications, 6.25%, 4/23/15, Term B (b) |

|

|

| 2,683,293 |

| ||||

|

| Seven Media Group, Term T, |

|

|

|

|

| ||||

AUD 7,150 |

| 5.365%, 12/28/12 |

|

|

| 3,477,328 |

| ||||

AUD 1,712 |

| 5.73%, 12/28/12 |

|

|

| 832,599 |

| ||||

|

|

|

|

|

| 6,993,220 |

| ||||

Printing/Publishing – 0.7% |

|

|

|

|

| ||||||

|

| Tribune Co. (b) (e), |

|

|

|

|

| ||||

$4,151 |

| 5.00%, 6/4/24, Term X |

|

|

| 1,698,509 |

| ||||

4,975 |

| 5.25%, 6/4/24, Term B |

|

|

| 1,919,212 |

| ||||

|

|

|

|

|

| 3,617,721 |

| ||||

Recreation – 0.0% |

|

|

|

|

| ||||||

3 |

| Cedar Fair L.P., 2.285%, 8/30/12 |

|

|

| 3,427 |

| ||||

Telecommunications – 0.7% |

|

|

|

|

| ||||||

5,675 |

| Hawaiian Telcom Communications, Inc., |

|

|

| 3,490,183 |

| ||||

Total Senior Loans (cost-$85,980,073) |

|

|

| 50,002,573 |

| ||||||

|

|

|

|

|

| ||||||

MORTGAGE-BACKED SECURITIES – 7.3% |

|

|

|

|

| ||||||

1,450 |

| Bear Stearns Commercial Mortgage Securities Inc., |

| NR/AAA |

| 1,224,754 |

| ||||

8,226 |

| Citigroup Commercial Mortgage Trust, |

| Aaa/AAA |

| 7,048,318 |

| ||||

2,900 |

| Citigroup/Deutsche Bank Commercial Mortgage Trust, |

| Aaa/AAA |

| 2,308,971 |

| ||||

|

| Commercial Mortgage Pass Through Certificates, CMO, |

|

|

|

|

| ||||

4,000 |

| 5.306%, 12/10/46 |

| Aaa/NR |

| 3,252,161 |

| ||||

11,900 |

| 6.010%, 12/10/49, VRN |

| Aaa/AAA |

| 10,160,453 |

| ||||

1,900 |

| Credit Suisse Mortgage Capital Certificates, |

| NR/AAA |

| 1,496,233 |

| ||||

4,865 |

| GS Mortgage Securities Corp. II, 5.56%, 11/10/39, CMO |

| Aaa/NR |

| 4,525,501 |

| ||||

3,155 |

| JPMorgan Chase Commercial Mortgage Securities Corp., |

| Aaa/AAA |

| 2,578,970 |

| ||||

|

| Morgan Stanley Capital I, CMO, VRN, |

|

|

|

|

| ||||

3,360 |

| 5.447%, 2/12/44 |

| Aaa/AAA |

| 2,740,151 |

| ||||

2,800 |

| 6.076%, 6/11/49 |

| NR/AAA |

| 2,238,147 |

| ||||

Total Mortgage-Backed Securities (cost-$33,455,609) |

|

|

| 37,573,659 |

| ||||||

|

|

|

|

|

| ||||||

PREFERRED STOCK – 1.9% |

|

|

|

|

| ||||||

|

|

|

|

|

| ||||||

| Shares |

|

|

|

|

|

|

| |||

|

|

|

|

|

|

|

| ||||

Automotive Products – 0.0% |

|

|

|

|

| ||||||

20,275 |

| Dura Automotive Systems, Inc., 20.00%, 12/31/49 (b) (f) (i) |

| NR/NR |

| 10,137 |

| ||||

7.31.09 | PIMCO Floating Rate Income/PIMCO Floating Rate Strategy Funds Annual Report 13

PIMCO Floating Rate Strategy Fund Schedule of Investments

July 31, 2009 (continued)

Shares |

|

|

|

|

| Value |

| ||||

|

|

|

|

|

| ||||||

Insurance – 1.9% |

|

|

|

|

| ||||||

21,655 |

| ABN AMRO North America Capital Funding Trust I, |

| B3/B |

| $9,555,269 |

| ||||

Total Preferred Stock (cost-$11,257,512) |

|

|

| 9,565,406 |

| ||||||

|

|

|

|

|

|

|

| ||||

U.S. TREASURY NOTES – 0.7% |

|

|

|

|

| ||||||

|

|

|

|

|

| ||||||

Principal |

|

|

|

|

|

|

| ||||

| (000) |

|

|

|

|

|

|

| |||

|

|

|

|

|

|

|

| ||||

$3,697 |

| U.S. Treasury Notes, 1.13%, 6/30/11 (cost-$3,713,737) |

|

|

| 3,701,632 |

| ||||

|

|

|

|

|

|

|

| ||||

CONVERTIBLE PREFERRED STOCK – 0.5% |

|

|

|

|

| ||||||

|

|

|

|

|

|

|

| ||||

| Shares |

|

|

|

|

|

|

| |||

|

|

|

|

|

|

|

| ||||

Banking – 0.5% |

|

|

|

|

| ||||||

3,000 |

| Wells Fargo & Co., 7.50%, 12/31/49, Ser. L (cost-$2,077,650) |

| Ba3/A- |

| 2,519,880 |

| ||||

|

|

|

|

|

|

|

| ||||

ASSET-BACKED SECURITIES – 0.1% |

|

|

|

|

| ||||||

|

|

|

|

|

|

|

| ||||

Principal |

|

|

|

|

|

|

| ||||

| (000) |

|

|

|

|

|

|

| |||

|

|

|

|

|

|

|

| ||||

$410 |

| CIT Group Home Equity Loan Trust, 0.555%, 6/25/33, FRN |

| Aaa/AAA |

| 251,361 |

| ||||

|

|

|

|

|

|

|

| ||||

COMMON STOCK – 0.0% |

|

|

|

|

| ||||||

|

|

|

|

|

|

|

| ||||

| Shares |

|

|

|

|

|

|

| |||

|

|

|

|

|

| ||||||

Automotive Products – 0.0% |

|

|

|

|

| ||||||

81,383 |

| Dura Automotive Systems, Inc. (b) (f) (i) (cost-$1,317,433) |

|

|

| 81,383 |

| ||||

|

|

|

|

|

|

|

| ||||

SHORT-TERM INVESTMENTS – 17.8% |

|

|

|

|

| ||||||

|

|

|

|

|

| ||||||

Principal |

|

|

|

|

|

|

| ||||

| (000) |

|

|

|

|

|

|

| |||

|

|

|

|

|

| ||||||

Corporate Notes – 14.9% |

|

|

|

|

| ||||||

Banking – 2.3% |

|

|

|

|

| ||||||

$5,000 |

| Bank of Scotland PLC, 0.31%, 6/28/10, FRN (a) (b) (d) |

| Aa3/A+ |

| 4,831,740 |

| ||||

6,700 |

| M&I Marshall & Ilsley Bank, 0.754%, 6/16/10, FRN |

| A2/BBB |

| 6,401,589 |

| ||||

700 |

| UBS AG, 2.158%, 7/1/10 |

| NR/NR |

| 699,994 |

| ||||

|

|

|

|

|

| 11,933,323 |

| ||||

Financial Services – 11.6% |

|

|

|

|

| ||||||

|

| American General Finance Corp., |

|

|

|

|

| ||||

14,200 |

| 0.706%, 3/2/10, FRN |

| Baa2/BB+ |

| 12,429,430 |

| ||||

2,000 |

| 3.875%, 10/1/09 |

| Baa2/BB+ |

| 1,921,126 |

| ||||

12,250 |

| CIT Group, Inc., 0.759%, 3/12/10, FRN |

| Ca/CC |

| 7,181,563 |

| ||||

8,755 |

| Ford Motor Credit Co. LLC, 7.375%, 10/28/09 |

| Caa1/CCC+ |

| 8,739,469 |

| ||||

|

| International Lease Finance Corp., |

|

|

|

|

| ||||

3,000 |

| 0.881%, 5/24/10, FRN |

| Baa2/BBB+ |

| 2,612,610 |

| ||||

9,900 |

| 0.909%, 1/15/10, FRN |

| Baa2/BBB+ |

| 9,453,074 |

| ||||

1,932 |

| 4.55%, 10/15/09 |

| Baa2/BBB+ |

| 1,895,238 |

| ||||

5,550 |

| 5.00%, 4/15/10 |

| Baa2/BBB+ |

| 4,992,408 |

| ||||

14 PIMCO Floating Rate Income/PIMCO Floating Rate Strategy Funds Annual Report | 7.31.09

PIMCO Floating Rate Strategy Fund Schedule of Investments

July 31, 2009 (continued)

Principal |

|

|

| Credit Rating |

| Value |

| ||

|

|

|

|

|

| ||||

Financial Services (continued) |

|

|

|

|

| ||||

$1,400 |

| SLM Corp., 0.37%, 3/15/10, FRN |

| Ba1/BBB- |

| $1,281,469 |

| ||

|

| Universal City Florida Holding Co., |

|

|

|

|

| ||

9,000 |

| 5.778%, 5/1/10, FRN |

| Caa2/B- |

| 7,875,000 |

| ||

1,000 |

| 8.375%, 5/1/10 |

| Caa2/B- |

| 890,000 |

| ||

|

|

|

|

|

| 59,271,387 |

| ||

Insurance – 1.0% |

|

|

|

|

| ||||

1,381 |

| AIG Matched Funding Corp., 0.32%, 9/8/09, FRN (a) (d) |

| A3/A- |

| 1,210,101 |

| ||

|

| Residential Reinsurance Ltd., FRN (a) (b) (d), |

|

|

|

|

| ||

3,000 |

| 7.918%, 6/7/10 |

| NR/BB |

| 2,884,500 |

| ||

1,200 |

| 8.418%, 6/7/10 |

| NR/BB- |

| 1,146,360 |

| ||

|

|

|

|

|

| 5,240,961 |

| ||

Total Corporate Notes (cost-$80,458,669) |

|

|

| 76,445,671 |

| ||||

|

|

|

|

|

| ||||

U.S. Treasury Bills (h) – 1.1% |

|

|

|

|

| ||||

5,567 |

| 0.13%-0.15%, 8/6/09-8/13/09 (cost-$5,566,738) |

|

|

| 5,566,739 |

| ||

|

|

|

|

|

|

|

| ||

Repurchase Agreements – 1.8% |

|

|

|

|

| ||||

9,000 |

| JPMorgan Securities, Inc., dated 7/31/09, 0.21%, due 8/3/09, proceeds $9,000,158; collateralized by Fannie Mae, 7.125%, due 06/15/10, valued at $9,186,486 including accrued interest |

|

|

| 9,000,000 |

| ||

489 |

| State Street Bank & Trust Co., dated 7/31/09, 0.01%, due 8/3/09, proceeds $489,000; collateralized by U.S. Treasury Bills, 0.09%, due 9/10/09, valued at $499,950 including accrued interest |

|

|

| 489,000 |

| ||

Total Repurchase Agreements (cost-$9,489,000) |

|

|

| 9,489,000 |

| ||||

Total Short-Term Investments (cost-$95,514,407) |

|

|

| 91,501,410 |

| ||||

Total Investments (cost-$563,081,518) – 100.0% |

|

|

| $513,699,023 |

| ||||

7.31.09 | PIMCO Floating Rate Income/PIMCO Floating Rate Strategy Funds Annual Report 15

PIMCO Floating Rate Strategy Fund Schedule of Investments

July 31, 2009 (continued)

| ||||

Notes to Schedule of Investments: | ||||

* | Unaudited |

| ||

(a) | Private Placement–Restricted as to resale and may not have a readily available market. Securities with an aggregate value of $46,497,798 and $107,283,322, representing 18.0% and 20.9% of total investments in Floating Rate Income and Floating Rate Strategy, respectively. |

| ||

(b) | Illiquid security. |

| ||

(c) | These securities generally pay interest at rates which are periodically pre-determined by reference to a base lending rate plus a premium. These base lending rates are generally either the lending rate offered by one or more major European banks, such as the “LIBOR” or the prime rate offered by one or more major United States banks, or the certificate of deposit rate. These securities are generally considered to be restricted as the Funds are ordinarily contractually obligated to receive approval from the Agent bank and/or borrower prior to disposition. Remaining maturities of senior loans may be less than the stated maturities shown as a result of contractual or optional payments by the borrower. Such prepayments cannot be predicted with certainty. The interest rate disclosed reflects the rate in effect on July 31, 2009. |

| ||

(d) | 144A Security–Exempt from registration under Rule 144A of the Securities Act of 1933. These securities may be resold in transactions exempt from registration, typically only to qualified institutional buyers. Unless otherwise indicated, these securities are not considered to be illiquid. |

| ||

(e) | In default. |

| ||

(f) | Fair-Valued–Securities with an aggregate value of $8,002,240 and $6,901,957, representing 3.1% and 1.3% of total investments in Floating Rate Income and Floating Rate Strategy, respectively. See Note 1(a) in the Notes to Financial Statements. |

| ||

(g) | Perpetual maturity security. Maturity date shown is the first call date. Interest rate is fixed until the first call date and variable thereafter. |

| ||

(h) | All or partial amount segregated as collateral for swaps. |

| ||

(i) | Non-income producing. |

| ||

(j) | All or partial amount segregated as collateral for reverse repurchase agreements. |

| ||

|

|

| ||

Glossary: |

| |||

AUD | - | Australian Dollar |

| |

£ | - | British Pound |

| |

CMO | - | Collateralized Mortgage Obligation |

| |

€ | - | Euro |

| |

FRN | - | Floating Rate Note. The interest rate disclosed reflects the rate in effect on July 31, 2009. |

| |

LIBOR | - | London Inter-Bank Offered Rate |

| |

NR | - | Not Rated |

| |

VRN | - | Variable Rate Note. Instruments whose interest rates change on specified date (such as a coupon date or interest payment date) and/or whose interest rates vary with changes in a designated base rate (such as the prime interest rate). The interest rate disclosed reflects the rate in effect on July 31, 2009. |

| |

WR | - | Withdrawn Rating |

| |

16 PIMCO Floating Rate Income/PIMCO Floating Rate Strategy Funds Annual Report | 7.31.09 | See accompanying Notes to Financial Statements.

PIMCO Floating Rate Income/PIMCO Floating Rate Strategy Funds | ||||||

|

|

|

| |||

|

| Floating Rate |

| Floating Rate | ||

Assets: |

|

|

|

|

|

|

Investments, at value (cost—$274,133,253 and $563,081,518, respectively) |

| $258,497,648 |

|

| $513,699,023 |

|

Cash (including foreign currency of $300,225 and $544,780 with a cost of $289,091 and $554,483, respectively) |

| 337,677 |

|

| 565,776 |

|

Receivable for investments sold |

| 5,963,526 |

|

| 13,439,822 |

|

Unrealized appreciation of swaps |

| 2,737,638 |

|

| 5,770,882 |

|

Interest receivable |

| 2,685,455 |

|

| 5,503,581 |

|

Unrealized appreciation of forward foreign currency contracts |

| 28,826 |

|

| 325,980 |

|

Receivable for terminated swaps |

| 692 |

|

| 789 |

|

Premium for swaps purchased |

| – |

|

| 17,500 |

|

Receivable from broker |

| – |

|

| 94,272 |

|

Prepaid expenses |

| 16,337 |

|

| 28,349 |

|

Total Assets |

| 270,267,799 |

|

| 539,445,974 |

|

|

|

|

|

|

|

|

Liabilities: |

|

|

|

|

|

|

Payable for reverse repurchase agreements |

| 12,104,750 |

|

| 442,000 |

|

Payable for investments purchased |

| 7,856,876 |

|

| 24,125,251 |

|

Premium for swaps sold |

| 2,053,750 |

|

| 4,145,250 |

|

Dividends payable to common and preferred shareholders |

| 1,208,625 |

|

| 2,656,408 |

|

Unrealized depreciation of swaps |

| 1,131,457 |

|

| 2,743,228 |

|

Unrealized depreciation of forward foreign currency contracts |

| 236,520 |

|

| 854,611 |

|

Unrealized depreciation of unfunded loan commitments |

| 179,166 |

|

| 358,332 |

|

Investment management fees payable |

| 152,876 |

|

| 312,005 |

|

Payable to broker |

| 138,890 |

|

| – |

|

Interest payable |

| 1,590 |

|

| 32 |

|

Payable to broker for collateral |

| – |

|

| 570,000 |

|

Accrued expenses |

| 246,614 |

|

| 289,593 |

|

Total Liabilities |

| 25,311,114 |

|

| 36,496,710 |

|

Preferred shares ($0.00001 par value and $25,000 liquidation |

| 78,975,000 |

|

| 161,000,000 |

|

Net Assets Applicable to Common Shareholders |

| $165,981,685 |

|

| $341,949,264 |

|

|

|

|

|

|

|

|

Composition of Net Assets Applicable to Common Shareholders: |

|

|

|

|

|

|

Common Stock: |

|

|

|

|

|

|

Par value ($0.00001 per share) |

| $183 |

|

| $429 |

|

Paid-in-capital in excess of par |

| 350,123,066 |

|

| 808,275,004 |

|

Undistributed net investment income |

| 18,110,199 |

|

| 31,899,814 |

|

Accumulated net realized loss |

| (188,131,915 | ) |

| (451,000,333 | ) |

Net unrealized depreciation of investments, swaps, |

| (14,119,848 | ) |

| (47,225,650 | ) |

Net Assets Applicable to Common Shareholders |

| $165,981,685 |

|

| $341,949,264 |

|

Common Shares Issued and Outstanding |

| 18,307,756 |

|

| 42,875,265 |

|

Net Asset Value Per Common Share |

| $9.07 |

|

| $7.98 |

|

See accompanying Notes to Financial Statements. | 7.31.09 | PIMCO Floating Rate Income/PIMCO Floating Rate Strategy Funds Annual Report 17

PIMCO Floating Rate Income/PIMCO Floating Rate Strategy Funds

Statements of Operations

Year ended July 31, 2009

|

|

|

| |||

|

| Floating Rate |

| Floating Rate | ||

Investment Income: |

|

|

|

|

|

|

Interest |

| $30,982,955 |

|

| $66,978,160 |

|

Dividends |

| 474,202 |

|

| 508,034 |

|

Facility and other fee income |

| 373,633 |

|

| 1,107,574 |

|

Total Investment Income |

| 31,830,790 |

|

| 68,593,768 |

|

|

|

|

|

|

|

|

Expenses: |

|

|

|

|

|

|

Investment management fees |

| 2,323,031 |

|

| 5,018,086 |

|

Auction agent fees and commissions |

| 322,490 |

|

| 701,918 |

|

Excise tax expense |

| 261,531 |

|

| 53,014 |

|

Custodian and accounting agent fees |

| 219,821 |

|

| 304,730 |

|

Interest expense |

| 175,780 |

|

| 410,191 |

|

Audit and tax services |

| 158,809 |

|

| 159,212 |

|

Shareholder communications |

| 90,046 |

|

| 161,004 |

|

Legal fees |

| 75,556 |

|

| 150,091 |

|

Trustees’ fees and expenses |

| 40,750 |

|

| 81,248 |

|

Transfer agent fees |

| 31,639 |

|

| 32,806 |

|

New York Stock Exchange listing fees |

| 21,545 |

|

| 35,084 |

|

Insurance expense |

| 10,375 |

|

| 21,989 |

|

Miscellaneous |

| 19,626 |

|

| 22,839 |

|

Total expenses |

| 3,750,999 |

|

| 7,152,212 |

|

Less: custody credits earned on cash balances |

| (1,310 | ) |

| (1,936 | ) |

Net expenses |

| 3,749,689 |

|

| 7,150,276 |

|

|

| 28,081,101 |

|

| 61,443,492 |

|

|

|

|

|

|

|

|

Net realized gain (loss) on: |

|

|

|

|

|

|

Investments |

| (128,645,012 | ) |

| (308,481,570 | ) |

Swaps |

| (11,502,339 | ) |

| (38,618,695 | ) |

Foreign currency transactions |

| 15,081,271 |

|

| 36,936,652 |

|

Net change in unrealized appreciation/depreciation of: |

| 15,943,929 |

|

| 25,933,153 |

|

Swaps |

| 4,022,954 |

|

| 14,850,253 |

|

Unfunded loan commitments |

| (192,023 | ) |

| (371,840 | ) |

Foreign currency transactions |

| (994,680 | ) |

| (3,670,031 | ) |

Net realized and change in unrealized loss on investments, swaps, unfunded loan commitments and foreign currency transactions |

| (106,285,900 | ) |

| (273,422,078 | ) |

Net Decrease in Net Assets Resulting from Investment Operations |

| (78,204,799 | ) |

| (211,978,586 | ) |

Dividends on Preferred Shares from Net Investment Income |

| (3,784,254 | ) |

| (8,434,704 | ) |

Net Decrease in Net Assets Applicable to Common |

| $(81,989,053 | ) |

| $(220,413,290 | ) |

18 PIMCO Floating Rate Income/PIMCO Floating Rate Strategy Funds Annual Report | 7.31.09 | See accompanying Notes to Financial Statements.

PIMCO Floating Rate Income Fund |

|

|

|

| |||

|

| 2009 |

|

| 2008 |

|

Investment Operations: |

|

|

|

|

|

|

Net investment income |

| $28,081,101 |

|

| $33,021,100 |

|

Net realized loss on investments, futures contracts, swaps and |

| (125,066,080 | ) |

| (43,985,922 | ) |

Net change in unrealized appreciation/depreciation of |

| 18,780,180 |

|

| 6,157,349 |