UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

☑ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2018

OR

☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number: 000-55195

GI DYNAMICS, INC.

(Exact name of registrant as specified in its charter)

Delaware |

| 84-1621425 |

(State or other jurisdiction of incorporation or organization) |

| (I.R.S. Employer Identification Number) |

|

| |

PO Box 51915 |

|

|

Boston, Massachusetts |

| 02205 |

(Address of Principal Executive Offices) |

| (Zip Code) |

(781) 357-3300

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Exchange Act: None

Securities registered pursuant to Section 12(g) of the Exchange Act: Common Stock, $0.01 par value per share

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ☐ No ☒

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days: Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files): Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ☐ |

| Accelerated filer ☐ |

| Non-accelerated filer ☐ |

| Smaller reporting company ☒ |

|

|

|

|

|

| Emerging growth company ☒ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act): ☐ Yes ☒ No

The aggregate market value of the registrant’s common stock, in the form of CHESS Depositary Interests, or CDIs, held by non-affiliates of the registrant (without admitting that any person whose shares are not included in such calculation is an affiliate), computed by reference to the price at which the CDIs were last sold prior to December 31 2018, the last business day of the registrant’s most recently completed fiscal year, as reported on the Australian Securities Exchange, was $10,829,647 (A$15,343,790).

As of March 8, 2019, there were 19,277,545 shares of common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE:

Portions of the definitive proxy statement for our 2019 Annual Meeting of Stockholders are incorporated by reference into Part III of this report.

NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements concerning our business, operations, financial performance and condition as well as our plans, objectives and expectations for our business, operations and financial performance and condition. Any statements contained in this Annual Report on Form 10-K that are not of historical facts may be deemed to be forward-looking statements. The forward-looking statements are contained principally in the section entitled “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” Forward-looking statements include, but are not limited to, statements about:

| • | our ability to raise sufficient capital to continue operations beyond March 2019; |

| • | our expectations with respect to regulatory submissions and approvals; |

| • | our expectations with respect to our planned clinical trials; |

| • | our expectations with respect to our intellectual property position; |

| • | our ability to develop and commercialize EndoBarrier; |

| • | our ability to attract and retain talented professionals with the relevant experience; |

| • | our ability to develop and commercialize new products; |

| • | our expectation with regard to inventory; and |

| • | our estimates regarding our capital requirements and our need for additional financing. |

In some cases, you can identify forward-looking statements by terms such as “may,” “will,” “should,” “could,” “would,” “expects,” “plans,” “anticipates,” “believes,” “estimates,” “projects,” “predicts,” “aims,” “assumes,” “goal,” “intends,” “objective,” “potential,” “positioned,” “target,” “continue,” “seek” and similar expressions intended to identify forward-looking statements.

These forward-looking statements are based on current expectations, estimates, forecasts and projections about our business and the industry in which we operate and our management’s beliefs and assumptions. These forward-looking statements are not guarantees of future performance or development and involve known and unknown risks, uncertainties and other factors that are in some cases beyond our control. As a result, any or all of our forward-looking statements in this Annual Report on Form 10-K may later become inaccurate. We may not actually achieve the plans, intentions or expectations disclosed in our forward-looking statements, and actual results or events could differ materially from the plans, intentions and expectations disclosed in the forward-looking statements we make. We have included important factors in the cautionary statements included in this Annual Report on Form 10-K, particularly in the “Risk Factors” section, that could cause actual results or events to differ materially from the forward-looking statements that we make.

You are urged to consider these factors carefully in evaluating the forward-looking statements and are cautioned not to place undue reliance on the forward-looking statements. You should read this Annual Report on Form 10-K and the documents that we have filed as exhibits to our Form 10-K completely and with the understanding that our actual future results may be materially different from what we expect. These forward-looking statements speak only as at the date of this Annual Report on Form 10-K. Unless required by law, we do not intend to publicly update or revise any forward-looking statements to reflect new information or future events or otherwise. You should, however, review the factors and risks we describe in the reports we will file from time to time with the SEC after the date of this Annual Report on Form 10-K.

ANNUAL REPORT ON FORM 10-K

FOR THE YEAR ENDED DECEMBER 31, 2018

|

|

|

| Page |

| |

|

| |||||

PART I |

|

|

|

| ||

|

|

| ||||

Item 1. |

|

|

| 5 |

| |

Item 1A. |

|

|

| 16 |

| |

Item 1B. |

|

|

| 31 |

| |

Item 2. |

|

|

| 31 |

| |

Item 3. |

|

|

| 31 |

| |

Item 4. |

|

|

| 31 |

| |

|

| |||||

|

|

|

| |||

|

|

| ||||

Item 5. |

|

|

| 32 |

| |

Item 6. |

|

|

| 32 |

| |

Item 7. |

| Management’s Discussion and Analysis of Financial Condition and Results of Operations |

|

| 33 |

|

Item 7A. |

|

|

| 45 |

| |

Item 8. |

|

|

| 45 |

| |

Item 9. |

| Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

|

| 45 |

|

Item 9A. |

|

|

| 46 |

| |

Item 9B. |

|

|

| 47 |

| |

|

| |||||

|

|

|

| |||

|

|

| ||||

Item 10. |

|

|

| 48 |

| |

Item 11. |

|

|

| 65 |

| |

Item 12. |

| Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

|

| 66 |

|

Item 13 |

| Certain Relationships and Related Transactions, and Director Independence |

|

| 66 |

|

Item 14 |

|

|

| 66 |

| |

|

| |||||

|

|

|

| |||

|

|

| ||||

Item 15. |

|

|

| 67 |

| |

|

|

|

| 70 |

| |

|

|

|

| F-1 |

| |

4

Overview

We are a clinical stage medical device company focused on the development and commercialization of EndoBarrier, a medical device system intended for treatment of patients with type 2 diabetes and obesity. EndoBarrier is a medical implant designated for the treatment of co-occurring type 2 diabetes and obesity, is approaching 4,000 implants since inception, and is the subject of an approved FDA pivotal trial in the United States which we plan to initiate in 2019. We believe that EndoBarrier represents a paradigm-breaking approach to traditional management of type 2 diabetes, which has focused historically on lifestyle intervention and diabetes medications. According to the article “Adherence to Therapies in Patients with Type 2 Diabetes,” by Luis-Emilio Garcia-Perez, these historical treatments for type 2 diabetes and obesity are limited in efficacy, with less than 50% of patients achieving glycemic control.

EndoBarrier represents the first material departure from this historical approach. We believe that EndoBarrier offers an adjunct to non-insulin diabetes pharmacotherapy, while providing patients a chance to significantly reduce or eliminate insulin and increase the likelihood of avoiding invasive and permanent bariatric or metabolic surgery. EndoBarrier is designed to mimic the mechanism of action of the duodenal-jejunal exclusion currently created by gastric bypass surgery (which is referred to as Roux-en-Y Gastric Bypass, or RYGB), as explained in the article “EndoBarrier: A Safe and Effective Novel Treatment for Obesity and Type 2 Diabetes?” by Nisha Patel. After implanting EndoBarrier, the patient’s food that exits the stomach will flow through the inside of the EndoBarrier Liner, and therefore not contact the wall of the upper intestine (duodenum and jejunum). The food will also not mix with fluids from the pancreas and bile duct until these fluids and the food reach the far end of the EndoBarrier Liner. It is believed that, in a similar fashion to RYGB, shunting the food to a more distant location in the upper intestines triggers hormonal responses that regulate key factors that help control hunger, satiety, and insulin sensitivity, which is also explained in the article by Nisha Patel.

EndoBarrier has been shown in multiple independent clinical studies to lower blood sugar levels (hemoglobin A1c or HbA1c), reduce excess body weight, increase insulin sensitivity, and positively affect other health metrics and comorbidities. Because it has been utilized in approximately 4,000 procedures, EndoBarrier has a thoroughly characterized benefit-risk profile. A recent independent meta-analysis published in American Diabetes Association (ADA) Diabetes Care, “Effects of the Duodenal-Jejunal Bypass Liner on Glycemic Control in Patients with Type 2 Diabetes with Obesity: A Meta-Analysis with Secondary Analysis on Weight Loss and Hormonal Changes,” by Pichamol Jirapinyo, MD provides the most comprehensive review and meta-analysis of EndoBarrier clinical data to date. In addition, two ongoing EndoBarrier registries in the UK and Germany have captured more than 800 patients between the two databases. These registries as well as other investigator-initiated trials continue to release clinical data on a regular basis, largely centered around the annual meetings hosted by Digestive Disease Week (DDW) in May, ADA in June, and EASD (European Association for the Study of Diabetes) in October.

Business Strategy

Our goal is to become the leading provider of alternative treatment options for type 2 diabetes and obesity. Our corporate priorities include:

1) | US Clinical Operations: Conduct Stage 1 of the EndoBarrier 18-1 clinical trial in the United States. |

The Company is focused on the successful execution of the 18-1 clinical trial in the United States. In August 2018, we received notification from the FDA that it had approved the Investigational Device Exemption (IDE) application for EndoBarrier, pending Institutional Review Board (IRB) approval, which was received in February 2019. The approved EndoBarrier IDE represents the pivotal clinical trial for EndoBarrier.

The 18-1 clinical trial is a randomized, controlled, double blinded trial with 3:1 randomization between patients who receive the EndoBarrier implant (3) and the control group made up of patients who will receive a sham procedure and not receive the EndoBarrier implant (1). Both arms will maintain pharmacotherapy in conjunction with ADA guidelines and lifestyle and nutritional counseling consistent with ADA guidelines. The primary endpoint of the trial is reduction of HbA1c from baseline to removal of the EndoBarrier at twelve months as compared to the control group. The study includes numerous secondary endpoints, including weight, insulin resistance, cardiovascular metrics, as well as NAFLD (non-alcoholic fatty liver disease) and NASH (non-alcoholic steatohepatitis).

5

The 18-1 clinical trial consists of two stages. The first stage consists of 50 EndoBarrier patients and approximately 17 control patients. At the end of stage 1, the Company will submit four DMC (Data Monitoring Committee) reports to the FDA for review. Upon a successful completion of the stage 1 review, we will submit a request to the FDA to complete the study by completing stage 2, which we anticipate will be comprised of 130 EndoBarrier patients and approximately 43 control patients for a study total of 240 patients (180 EndoBarrier and 60 control patients). There is no guarantee that this will be the final composition of the study, as the number of remaining stages or remaining patients may vary based on the stage 1 clinical data and the outcome of the stage 1 review with FDA. In addition to the multiple staged study, the FDA has mandated certain stopping rules which, if triggered, could result in the 18-1 study having enrollment or treatment delayed or stopped.

Assuming the successful completion of sufficient financing to ensure funds will be available at the start of the trial to ensure completion of the trial in a safe and patient-focused manner, we expect to begin enrolling patients in the 18-1 clinical trial and to complete the enrollment within 6 months of initiation of enrollment.

2) | India Partnership: Conduct the EndoBarrier clinical trial in India as part of the Apollo Sugar partnership. |

We are focused on the successful execution of the EndoBarrier trial in India as part of our partnership with Apollo Sugar, which was announced on November 27, 2018.

The EndoBarrier India study is also a randomized, controlled, double blinded trial with 3:1 randomization between patients who receive the EndoBarrier implant (3) and the control group made up of patients who will not receive the EndoBarrier implant (1). The primary endpoint of the trial is reduction of HbA1c from baseline to removal of the EndoBarrier at twelve months as compared to the control group. The study includes numerous secondary endpoints, including weight, insulin resistance, cardiovascular metrics, as well as NAFLD and NASH. The study includes 100 patients total, which consists of 75 patients who will receive the EndoBarrier implant and 25 control patients. Five clinical sites in India will participate in the study.

Apollo Sugar is a collaboration between Apollo Health & Lifestyle Limited and Sanofi. Apollo Sugar is a division of Apollo Hospitals Group (Apollo) focused on the treatment of metabolic disorders and operates an integrated network of centers of excellence for diabetes, obesity and endocrinology. Apollo is the largest private hospital system in India and has emerged as Asia’s foremost integrated healthcare services provider, maintaining a robust presence of hospitals, pharmacies, primary care and diagnostic clinics across the healthcare ecosystem. Since its inception, Apollo has treated over 65 million patients from 141 countries.

The Company and Apollo Sugar intend to conduct the clinical trial and seek regulatory approval in India and, in parallel, finalize the terms of a partnership that will focus on the marketing, distribution and clinical support of EndoBarrier to appropriate patients in India and Southeast Asia. Final terms of the proposed collaboration are subject to negotiation and will be disclosed upon completion.

3) | Gain CE Mark: Work with Intertek to gain EndoBarrier CE mark. |

CE Marking on a product is a manufacturer’s declaration that a product meets the applicable health, safety, and environmental requirements outlined in the appropriate European product legislation and has undergone the relevant conformity assessment procedure. A CE Mark is required before we can market EndoBarrier in the EU and certain Middle Eastern countries.

We have entered into an agreement with Intertek to serve as our notified body and to assist us with obtaining CE Marking for EndoBarrier as described in our announcement released on October 5, 2018. A notified body evaluates the conformity of products and the associated quality systems for manufacturers that seek to sell products in Europe.

4) | Ongoing clinical data: Support continued release of clinical data from registries and investigator-initiated clinical trials. |

We continue to support the ongoing efforts of multiple clinicians as they develop new EndoBarrier clinical data. Multiple investigator-initiated clinical trials released clinical data in 2018. It is expected that these clinical trials will continue to release data into 2019, 2020, and beyond.

6

We also support two primary registries that continue to release clinical data. The Association of British Clinical Diabetologists (ABCD) Worldwide EndoBarrier Registry contains over 500 patient data points with the goal of registering and gathering data on 1,000 patients. The German EndoBarrier Registry contains over 300 patient data points. The patients within these two registries are non-overlapping. Both registries are expected to continue releasing clinical data highlighting the EndoBarrier treatment effect on an annual basis.

Multiple studies continue to release data supporting the long-term treatment durability that now stands at two years after EndoBarrier implant and one year after EndoBarrier removal.

The clinical data releases have historically focused, and are expected to continue focusing, on the annual data releases associated with Digestive Disease Week (DDW) in May, The American Diabetes Association (ADA) in June, The European Association for the Study of Diabetes (EASD) in October, and Obesity Week in November.

5) | Development of Intellectual Property: Continue developing our intellectual property and protecting our patents. |

We will continue to invest in expanding our intellectual property portfolio. Our current patent portfolio is composed of 93 issued and pending U.S. and non-U.S. patents. We have been issued 60 U.S. patents and maintain 9 pending U.S. patent applications. We have also sought intellectual property protection outside the U.S. and have been issued 20 patents across Canada, China, the European Patent Convention region (including Germany and the United Kingdom), Hong Kong, Japan, Israel and India, and we have 7 pending PCT applications and 17 pending foreign patent applications.

As a result of a settled 2013 legal action, we granted W.L. Gore & Associates, Inc., or Gore, a nonexclusive, royalty-free license to use our patents within the vascular system. Gore is not licensed to use our patents for any applications in the gastrointestinal tract.

Our current issued patents expire between 2023 and 2031. We also actively monitor our intellectual property by regularly reviewing new developments to identify extensions to our patent portfolio. We employ external patent attorneys to assist us in managing our intellectual property portfolio.

Summary

In summary, we believe that EndoBarrier represents the most effective new treatment option in a market dominated by pharmaceutical companies generating annual revenue in excess $40 billion. We believe that EndoBarrier is poised to have a transformative and disruptive effect on the type 2 diabetes and obesity market. EndoBarrier is one of the few treatment options that treats type 2 diabetes concurrently with obesity and continues to show lasting treatment effects post treatment in many patients. As the duration of the EndoBarrier treatment effect continues to increase in published literature and because, to date, there has been minimal observed clinical risk after EndoBarrier removal, the EndoBarrier risk-benefit balance continues to evolve in an increasingly positive manner.

Background of the Disease

Diabetes mellitus type 2 (also known as type 2 diabetes) is a long-term progressive metabolic disorder characterized by high blood sugar, insulin resistance, and reduced insulin production. People with type 2 diabetes represent 90-95% of the worldwide diabetes population; only 5-10% of this population is diagnosed with type 1 diabetes (a form of diabetes mellitus wherein little to no insulin is produced).

Being overweight is a condition where the patient’s body mass index (BMI) is greater than 25 (kg/m2); obesity is a condition where the patient’s BMI is greater than 30. Obesity and its comorbidities contribute to the progression of type 2 diabetes. Many experts believe obesity contributes to higher levels of insulin resistance, which creates a feedback loop that increases the severity of type 2 diabetes.

When considering treatment for type 2 diabetes, it is optimal to address obesity concurrently with diabetes. According to the article “Mechanisms of Insulin Resistance in Obesity,” by Jianping Ye, absent the concurrent treatment of obesity with the treatment of type 2 diabetes, obesity will likely continue to contribute to the progressive nature of type 2 diabetes. It is our belief that the inability of the current pharmacologic options to fully treat type 2 diabetes is due to the fact that diabetes medications generally treat blood sugar levels only and do not contribute substantially to weight loss.

7

According to the American Diabetes Association 2018 Standards of Medical Care in Diabetes, the current treatment paradigm for type 2 diabetes is lifestyle therapy combined with pharmacological treatment, whereby treating clinicians prescribe a treatment regimen of one to four concurrent medications that could include insulin. Insulin usage carries a significant risk of increased mortality and may contribute to weight gain, which in turn may lead to higher levels of insulin resistance and increased levels of blood sugar, as explained in the article “Insulin-associated weight gain in diabetes--causes, effects and coping strategies,” by Russel-Jones D . Fewer than 50% of patients treated pharmacologically for type 2 diabetes are adequately managed, meaning that medication does not lower blood sugar adequately and does not halt the progressive nature of diabetes for these patients, as explained in the article “Adherence to Therapies in Patients with Type 2 Diabetes,” by Luis-Emilio Garcia-Perez.

The current pharmacological treatment algorithms for type 2 diabetes fall short of ideal, creating a large and unfilled treatment gap. We believe that EndoBarrier, which is designed to mimic the mechanism of action of duodenal-jejunal exclusion currently created by RYGB gastric bypass surgery and operates in a relatively similar manner by reducing both weight and long-term blood sugar levels, can fill this gap by treating type 2 diabetes and obesity in a unique minimally invasive and reversible manner.

Market Opportunity

Unmet Clinical Needs in the Treatment of Type 2 Diabetes and Obesity.

In 2017, the International Diabetes Federation estimated there were 425 million adults with diabetes worldwide, with ~90% diagnosed with type 2 diabetes. Diabetes is the leading cause of cardiovascular disease, kidney failure, blindness, and lower-limb amputation in almost all countries.

Three years after initial diagnosis, over half of patients with type 2 diabetes require multiple drug therapies. Studies have shown that less than 50% of the type 2 diabetes population is adequately managed pharmacologically, as explained in the article “Adherence to Therapies in Patients with Type 2 Diabetes,” by Luis-Emilio Garcia-Perez. . At ten years post diagnosis, most patients, despite insulin use in many, struggle to reach their hemoglobin A1c (HbA1c) treatment goals. HbA1c is a glycosylated hemoglobin molecule found in the bloodstream that is formed when red blood cells are exposed to blood glucose. HbA1c has become the generally accepted gold standard biomarker for measuring levels of diabetes control in clinical practice and in human trials.

Many patients and health care systems struggle to meet the financial burden imposed by the numerous concurrent medications required to attempt to control the progressive nature of type 2 diabetes.

According to the World Health Organization, in 2016 more than 1.9 billion adults 18 and older were overweight. Of these, 650 million people worldwide are diagnosed with obesity (BMI ³ > 30 kg/m 2), a condition often leading to serious health consequences such as cardiovascular disease, diabetes, musculoskeletal disorders, and some cancers.

Those suffering from both type 2 diabetes and obesity, also referred to as diabesity, total more than 169 million worldwide, represent as enormous public health problem not only in the United States (US) but also globally, as explained in the article “Epidemiology of Obesity and Diabetes and Their Cardiovascular Complications,” by Bhupathiraju, S. We believe that the unchecked worldwide rate of growth of the type 2 diabetes and obesity patient population represents one of the greatest unmanaged health risks in all of health care.

We believe EndoBarrier can treat patients with type 2 diabetes and obesity in a safe, effective, nonpharmacological, and nonpermanent manner.

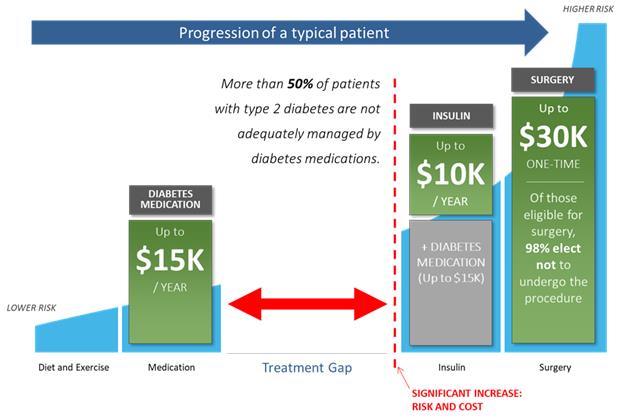

The Treatment Gap

Our intent in developing and seeking regulatory approval for EndoBarrier is to help clinicians deliver a unique treatment option to those patients suffering from type 2 diabetes and obesity, a disease state that sorely lacks innovative new treatment options.

8

We and our scientific advisors feel there must be a change in how the medical establishment currently treats patients suffering from type 2 diabetes and obesity because current treatment options are not effective. According to the International Diabetes Federation, the number of patients progressing to later stages of type 2 diabetes and obesity continues to grow at an alarming rate. Yet less than half of all type 2 diabetes patients are adequately managed by pharmacotherapy, and insulin carries serious risks and may in many cases contribute to the further progression of obesity. At the extreme end of the treatment spectrum, the treatment options are limited to different types of bariatric or metabolic surgery, which are highly invasive and irreversible procedures. Less than 1% of patients who are eligible for bariatric or metabolic surgery opt to undergo the procedure, as explained in the Gut article “Recent advances in clinical practice challenges and opportunities in the management of obesity,” by Acosta A.

The graphic above illustrates the multiple treatment options during the course of progression of type 2 diabetes:

| • | Risk associated with treatment increases from left to right. |

| • | Progression of diabetes and obesity increases vertically. |

| • | Lifestyle therapy (lifestyle counseling including nutrition and exercise) is the first line of defense against the progression of type 2 diabetes and obesity. |

| • | Pharmacotherapy |

| o | Oral monotherapy follows lifestyle therapy, often with metformin as the first line of treatment. |

| o | Multiple combinations may then be administered, as recommended by the American Diabetes Association and other diabetes associations around the world. |

| o | Ultimately, as disease progression continues, injected insulin may be prescribed. |

| • | Bariatric or metabolic gastric bypass surgery may represent a final option. |

9

A significant and rapidly growing patient population falls into the treatment gap, wherein the patient is inadequately managed by medication yet unwilling to undergo gastric bypass surgery. For patients who elect to undergo bariatric or metabolic surgery, the clinical gains may not be permanent, while the risk associated with the procedure is permanent, according to the article “Gastric bypass surgery: Who is it for?” from the Mayo Clinic. These risks include, but are not limited to, excessive bleeding, blood clots, infection and in some cases death. We believe that because EndoBarrier is minimally invasive, can mimic the effects of gastric bypass, and has minimal side-effects, EndoBarrier can uniquely fill this treatment gap, as explained in the article “EndoBarrier: A Safe and Effective Novel Treatment for Obesity and Type 2 Diabetes?” by Nisha Patel.

The EndoBarrier Solution

EndoBarrier is intended for the treatment of type 2 diabetes and obesity in a minimally invasive and reversible manner. EndoBarrier is designed to mimic the mechanism of action of duodenal-jejunal exclusion created by gastric bypass surgery.

The EndoBarrier System consists of three primary components:

| • | EndoBarrier — The EndoBarrier or EndoBarrier Liner is a 60-cm-long implant consisting of a thin, flexible, impermeable fluoropolymer sleeve coupled to a proprietary nitinol anchor assembly. A gastroenterologist (GI clinician) implants the EndoBarrier Liner into the patient’s duodenum in a minimally invasive manner using the EndoBarrier Delivery System. The EndoBarrier Liner is placed via endoscopy (through the mouth and esophagus and into the stomach without cutting tissue) during a procedure that typically takes less than twenty minutes. Once the EndoBarrier Liner is properly positioned in the patient’s upper intestine just below the stomach, the EndoBarrier Delivery System is removed and EndoBarrier Liner remains, held in place by a proprietary anchoring mechanism. EndoBarrier remains in the body for a maximum intended duration of twelve months until removal, again via a minimally invasive endoscopic procedure using the EndoBarrier Retrieval System. The effect of EndoBarrier Liner begins promptly after device placement. |

| • | EndoBarrier Delivery System — EndoBarrier is delivered using our proprietary single-use delivery system. This includes a sterile custom-made delivery catheter 300 cm in length that is sufficiently flexible to be passed through the patient’s mouth, through the stomach, and into the intestine. The EndoBarrier Liner is provided pre-packed in the EndoBarrier Delivery System within the capsule at the distal end of the delivery catheter. The EndoBarrier Liner is deployed by the clinician using the delivery system controls at the proximal or near end of the system. The delivery procedure is brief, typically taking less than twenty minutes, during which the patient is either anaesthetized or semi-sedated. |

10

EndoBarrier has been shown in multiple company-sponsored and independent clinical studies to lower blood sugar levels (hemoglobin A1c or HbA1c), reduce excess body weight, and positively affect other health metrics and comorbidities.

EndoBarrier is not currently approved or commercially available in any jurisdiction. In August 2018, we received notification from the FDA that it had approved the IDE application, pending IRB approval which was received in February 2019. To gain regulatory approval to commercialize EndoBarrier in the United States, we must submit a pre-market authorization (PMA) application for review and approval by the FDA.

The EndoBarrier Effect

Obesity has been shown to exacerbate insulin resistance and contribute to the progression of type 2 diabetes. In situations where lifestyle modification and pharmacotherapy have failed and surgery is not an option or is considered a therapy of last resort, EndoBarrier is intended to reduce blood sugar and weight. In clinical trials in both the United States and outside of the United States, EndoBarrier has been shown to:

| • | significantly lower glucose levels; |

| • | significantly lower body weight; |

| • | lower cardiovascular-related risk factors. |

EndoBarrier utilization accomplishes this in many patients by affecting key hormones involved in insulin sensitivity, glucose metabolism, satiety, and food intake. (See the section titled “How EndoBarrier Works: EndoBarrier Mechanism of Action.”)

Our intent in positioning EndoBarrier to fill the type 2 diabetes and obesity treatment gap is to help patients and clinicians avoid the initiation of insulin therapy by helping many patients maintain lower HbA1c levels and slow or halt the progression of type 2 diabetes. Furthermore, for those patients whose type 2 diabetes has progressed to the point where insulin therapy is necessary, EndoBarrier has been shown in many cases to lower HbA1c levels to the point where insulin is no longer needed. Finally, if the progression of type 2 diabetes is severe enough to warrant gastric bypass surgery, we expect that EndoBarrier either may serve as an opportunity to control type 2 diabetes so that surgery may not be needed, or at least better prepare the patient for bariatric surgery by lowering weight and helping control other comorbidities prior to surgery.

How EndoBarrier Works: EndoBarrier Mechanism of Action

The EndoBarrier mechanism of action is thought to be based on its functional similarities in many ways to Roux-en-Y gastric bypass surgery (RYGB). Once the EndoBarrier is implanted into the duodenum and proximal jejunum, ingested food passing through the EndoBarrier during the normal digestive process is prevented from interacting with the epithelium, microbiota, mucosal layer, or biliopancreatic secretions within the duodenum and proximal jejunum. In addition, EndoBarrier acts as a physical barrier that prevents the interaction of food with pancreatic enzymes and bile until reaching the end of the EndoBarrier Liner. Pancreatic enzymes and bile pass outside EndoBarrier and mix with the food at the distal end of the liner, where absorption ultimately takes place in the intestine. Thus, EndoBarrier creates a functional but reversible bypass of the upper intestine. Unlike RYGB surgery, EndoBarrier does not require an invasive and permanent surgical procedure or permanent physical modification of the stomach and exclusion of the distal stomach from the alimentary flow.

11

Our scientific team and advisors have postulated the following EndoBarrier mechanisms of action, based on scientific evidence from such articles as the “Effects of the Duodenal-Jejunal Bypass Liner on Glycemic Control in Patients with Type 2 Diabetes with Obesity: A Meta-Analysis with Secondary Analysis on Weight Loss and Hormonal Changes,” by Pichamol Jirapinyo and “The EndoBarrier: Duodenal-Jejunal Bypass Liner for Diabetes and Weight Loss,” by Aruchuna Ruban.:

| • | Exclusion of the duodenum — This may offset an abnormality of gastrointestinal physiology responsible for insulin resistance and type 2 diabetes. |

| • | Increased nutrient delivery to the distal small bowel — Additional findings suggest that the exclusion of the proximal intestine (foregut theory) and increase in nutrient delivery to the distal small bowel (hindgut theory) created by EndoBarrier likely induce neuro-hormonal changes and nutrient sensing that affect energy balance and glucose homeostasis. |

| • | Secretion of GLP-1 — Partially digested nutrients reach the distal ileum, which stimulates the secretion of GLP-1 by L-cells located in this area. GLP-1 is known to regulate insulin secretion and action. |

| • | Increase in gut hormones — This contributes to the restoration of energy and glucose homeostasis. |

| • | Elevated GLP-1 and PYY levels — Both levels are elevated as quickly as one-week post-implantation. Both hormones may play a role in satiety and body weight control. |

| • | Increased levels of bile acids — This stimulates thermogenesis and gut hormone secretions. |

| • | Decreased caloric intake— Studies have demonstrated that patients with EndoBarrier, aided by increased satiety from GLP-1, eat less and feel full longer, leading to a decrease in caloric intake. |

There is no known evidence of occurrence of clinically significant caloric malabsorption with EndoBarrier. EndoBarrier covers only 60 cm of duodenal and proximal jejunal mucosa, which most likely represents less than 10% of the length of the small intestine and leaves almost the entire jejunum and ileum for digestion and absorption.

We began selling EndoBarrier in Europe and South America in 2010 and in Australia in 2011. Since inception, the Company has distributed almost 4,000 units of EndoBarrier and generated a total of $7.8 million in revenue. We have incurred net losses in each year since our inception.

We signed an agreement with our manufacturing partner, Proven Process Medical Devices (“PPMD”, “the Manufacturer”) on July 26, 2017.

We have five subsidiaries: GI Dynamics Securities Corporation, a Massachusetts-incorporated nontrading entity; GID Europe Holding B.V., a Netherlands-incorporated nontrading holding company; GID Europe B.V., a Netherlands-incorporated company that conducts certain of our European business operations; GID Germany GmbH, a German-incorporated company that conducts certain of our European business operations; and GI Dynamics Australia Pty Ltd, an Australia-incorporated company that conducts our Australian business operations.

We have raised net proceeds of approximately $264.0 million through sales of our equity of which $6.6 million was raised through our 2018 private placement offerings. We generated $75.7 million in proceeds, net of expenses, through the sale of convertible preferred stock to a number of US venture capital firms, two global medical device manufacturers, and individuals prior to going public. In June 2011, we issued convertible term promissory notes to several of our shareholders totaling $6.0 million, which were repaid concurrently with the closing of our IPO in September 2011 with the associated gross proceeds. In September 2011, we raised approximately $72.5 million, net of expenses, and repaid $6.0 million of convertible term promissory notes in our IPO in Australia and simultaneous private placement of Chess Depository Interests (CDIs) to accredited investors in the United States. In connection with the IPO, all our existing shares of preferred stock were converted into common stock.

In July and August 2013, we raised approximately $52.5 million, net of expenses, in an offering of our CDIs to sophisticated, professional, and accredited investors in Australia, the United States, and certain other jurisdictions. In May 2014, we raised approximately $30.8 million, net of expenses, in an offering of our CDIs to sophisticated, professional, and accredited investors in Australia, Hong Kong, the United Kingdom, and certain other jurisdictions.

12

In December 2016, we raised approximately $1.0 million, net of expenses, in an offering of our CDIs to sophisticated and professional investors in Australia and certain other jurisdictions.

In January 2017, we raised approximately $0.2 million, net of expenses, in an offering of our CDIs to eligible shareholders under a Security Purchase Plan (SPP) available to security holders with registered addresses in Australia or New Zealand.

In June 2017, we completed a Convertible Term Promissory Note (the “2017 Note”) secured financing for a gross amount of $5.0 million, which 2017 Note accrues interest at 5% per annum compounded annually. In December 2018, the maturity date of the 2017 Note was extended from December 31, 2018 to March 31, 2019 in exchange for payment of approximately $394 thousand, which was the total accrued interest on the 2017 Note at December 31, 2018.

In July 2017, we signed an agreement with our manufacturing partner Proven Process Medical Devices (“PPMD”, “the Manufacturer”).

In February and March 2018, we raised approximately $1.6 million in an offering of our CDIs to sophisticated and professional investors, including certain existing investors, in Australia, the United States and the United Kingdom.

In May 2018, we completed a Convertible Term Promissory Note and Warrant (the “2018 Note and Warrant”) for a gross amount of $1.75 million. The $1.75 million 10% per annum convertible note can convert to CDI’s at A$ 0.018 per CDI and matures on May 30, 2023. The warrants consist of the right to purchase 97,222,200 CDIs for A$ 0.018 per CDI with anti-dilution protections.

In September and November 2018, we raised approximately $5.0 million in an offering of our CDIs to sophisticated and professional investors, including certain existing investors, in Australia, the United States and the United Kingdom.

In October 2018, we announced that we signed an agreement with our new notified body Intertek to pursue CE marking of EndoBarrier in Europe.

In November 2018, we signed a clinical trial agreement and a memorandum of understanding with our clinical and potential commercial partner Apollo Sugar, a division of Apollo Hospitals Group located in India.

In December 2018, we announced the appointment of Charles Carter as the Company’s Chief Financial Officer and Secretary.

The rights of our shareholders are governed by Delaware general corporation law.

We are headquartered in Boston, Massachusetts, where the majority of the Company’s employees work. We have subsidiaries in the Netherlands, Germany, and Australia, with employees in Germany and Australia.

2018 in Review

For us, 2018 was a year primarily focused on working with the FDA to gain approval for a new EndoBarrier pivotal clinical trial in the United States and planning and preparing to initiate the clinical trial (18-1). We also focused on a critical partnership in India with Apollo Sugar with the intent of conducting a clinical trial in India leading to regulatory approval and EndoBarrier distribution through a partnership with Apollo Sugar. Additionally, we focused on stabilizing the Company and continuing to address operational issues, continuing to reduce cash burn, working with non-United States regulatory bodies and continuing to develop our intellectual property.

We applied for, and received, an Investigational Device Exemption (IDE) authorizing us to conduct a pivotal trial in the United States designed to support our Pre-Market Authorization application.

We executed a clinical trial agreement and memorandum of understanding for a partnership in India with Apollo Sugar, the joint venture formed by Sanofi and Apollo Hospital Systems.

13

We executed an agreement with Intertek, our new Notified Body in order to pursue a CE mark for EndoBarrier and work towards commercial sales in the European Union and select countries in the Middle East.

We announced the release of clinically significant data from independent investigator-initiated trials and two ongoing Registries throughout the year.

We continued to develop our intellectual property position.

We hired key staff and moved to a new office location in Boston, Massachusetts.

Strategic Focus in 2019: The Path Forward

Our goal is to become the leading provider of alternative treatment options in type 2 diabetes and obesity. We intend to do this by conducting the following activities:

1) U.S. clinical operations: | Conduct Stage 1 of the EndoBarrier 18-1 pivotal trial in the United States. |

2) India partnership: | Conduct the EndoBarrier pivotal trial in India as part of the Apollo Sugar partnership. |

3) Gain CE Mark: | Work with our notified body to gain the EndoBarrier CE mark. |

4) Ongoing clinical data: | Support continued release of clinical data from registries and investigator- initiated clinical trials. |

5) Development of Intellectual Property: | Continue developing our intellectual property and protecting our patents. |

We will need to raise additional capital in 2019.

As of December 31, 2018, the Company’s primary source of liquidity is its cash and cash equivalents balances. We are currently focused primarily on our pivotal trial, which will support future regulatory submissions and potential commercialization activities. Until we are successful in gaining regulatory approvals, we are unable to sell our product in any market at this time. Without revenues, we are reliant on funding obtained from investment in the Company to maintain our business operations until we can generate positive cash flows from operations. We cannot predict the extent of our future operating losses and accumulated deficit, and we may never generate sufficient revenues to achieve or sustain profitability.

The Company has incurred operating losses since inception and at December 31, 2018, had an accumulated deficit of approximately $267 million and a working capital deficit of $3.3 million. The Company expects to incur significant operating losses for the next several years. At December 31, 2018, the Company had approximately $3.8 million in cash and cash equivalents.

The Company will need to raise additional capital and restructure the terms of the 2017 Note before March 31, 2019 in order to continue to pursue its current business objectives as planned and to continue to fund its operations. The Company is looking to raise additional funds through any combination of additional equity and debt financings or from other sources. However, the Company has no guarantee that the 2017 Note will not mature on March 31, 2019 and has no guaranteed source of capital that will sustain operations into the second quarter of 2019. There can be no assurance that any such potential financing opportunities will be available on acceptable terms, if at all. If the Company is unable to raise sufficient capital on the Company’s required timelines and on acceptable terms to shareholders and the Board of Directors, it could be forced to cease operations, including activities essential to support regulatory applications to commercialize EndoBarrier. If access to capital is not achieved in the near term, it will materially harm the Company’s business, financial condition and results of operations to the extent that the Company may be required to cease operations altogether, file for bankruptcy, or undertake any combination of the foregoing. In such event, our shareholders may lose their entire investment in our company.

These factors raise substantial doubt about the Company’s ability to continue as a going concern within one year after the date that the financial statements are issued.

See “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations — Liquidity and Capital Resources” for further information regarding our funding requirements.

14

Implications of Being an Emerging Growth Company and a Smaller Reporting Company

As a company with less than $1.07 billion in revenue during our most recently completed fiscal year, we qualify as an “emerging growth company” as defined in Section 2(a) of the Securities Act of 1933, as amended, which we refer to as the Securities Act, as modified by the Jumpstart Our Business Startups Act of 2012, or the JOBS Act. Additionally, Section Rule 12b-2 of the Securities Exchange Act of 1934, as amended, or the Exchange Act, establishes a class of company called a “smaller reporting company,” which effective September 10, 2018, was amended to include companies with a public float of less than $250 million as of the last business day of its most recently completed second fiscal quarter or, if such public float is less than $700 million, had annual revenues of less than $100 million during the most recently completed fiscal year for which audited financial statements are available. For the year ended December 31, 2018, we qualify as both an emerging growth company and as a smaller reporting company.

As an emerging growth company and/or smaller reporting company, we may take advantage of specified reduced disclosure and other requirements that are otherwise applicable, in general, to public companies that do not qualify for these classifications. These provisions include:

| • | Any requirement that may be adopted by the Public Company Accounting Oversight Board regarding mandatory audit firm rotation or a supplement to the auditor’s report providing additional information about the audit and financial statements, commonly known as an “auditor discussion and analysis”; |

| • | Reduced disclosure about our executive compensation arrangements; |

| • | No non-binding shareholder advisory votes on executive compensation or golden parachute arrangements; and |

| • | Exemption from the auditor attestation requirement in the assessment of our internal control over financial reporting. |

Emerging growth companies may take advantage of these exemptions for up to five years or such earlier time that we are no longer an emerging growth company. For as long as we continue to be an emerging growth company and/or a smaller reporting company, we expect that we will take advantage of the reduced disclosure obligations available to us as a result of those respective classifications. We would cease to be an emerging growth company if we have more than $1.07 billion in annual revenues as of the end of a fiscal year, if we are deemed to be a large-accelerated filer under the rules of the Securities and Exchange Commission, or the SEC, or if we issue more than $1.0 billion of non-convertible debt over a three-year-period. We will remain a smaller reporting company until we have a public float of $250.0 million or more as of the last business day of our most recently completed second fiscal quarter, and we could retain our smaller reporting company status indefinitely depending on the size of our public float.

The JOBS Act permits an emerging growth company to take advantage of an extended transition period to comply with new or revised accounting standards applicable to public companies. We are choosing to “opt out” of this provision.

Employees

As of March 1, 2019, we have 19 employees and contractors, 9 of which are full-time employees. None of our employees are represented by labor unions or covered by collective bargaining agreements.

Available Information

Financial and other information about us is available on our website. Our website address is www.gidynamics.com. We make available on our website, free of charge, copies of our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act as soon as reasonably practicable after we electronically file such material with, or furnish it to, the U.S. Securities and Exchange Commission, or the SEC. The information contained in our website is not intended to be part of this filing.

15

Our business faces many risks. We believe the risks described below are the material risks that we face. However, the risks described below may not be the only risks that we face. Additional unknown risks or risks that we currently consider immaterial, may also impair our business operations. If any of the events or circumstances described below actually occur, our business, financial condition or results of operations could suffer, and the trading price of our CDIs could decline significantly. You should consider the specific risk factors discussed below together with the cautionary statements under the caption “Forward-Looking Statements” and the other information and documents that we file from time to time with the Securities and Exchange Commission, or SEC.

Risks Related to Our Business

We will need substantial additional funding and may be unable to raise capital when needed, which could force us to delay, reduce, or eliminate planned activities or result in our inability to operate as a going concern.

As of December 31, 2018, the Company’s primary source of liquidity is its cash and cash equivalents balances. We are currently focused primarily on our clinical trials, which will support future regulatory submissions and potential commercialization activities. Until we are successful in gaining regulatory approvals, we are unable to sell our product in any market at this time. Without revenues, we are reliant on funding obtained from investment in our Company to maintain our business operations until we can generate positive cash flows from operations. We cannot predict the extent of our future operating losses and accumulated deficit, and we may never generate sufficient revenues to achieve or sustain profitability.

The Company has incurred operating losses since inception and at December 31, 2018, had an accumulated deficit of approximately $267 million and a working capital deficit of $3.3 million. The Company expects to incur significant operating losses for the next several years. At December 31, 2018 the Company had approximately $3.8 million in cash and cash equivalents.

The Company will need to raise additional capital and restructure the terms of the 2017 Note before March 31, 2019 in order to continue to pursue its current business objectives as planned and to continue to fund its operations. The Company is looking to raise additional funds through any combination of additional equity and debt financings or from other sources. However, the Company has no guarantee that the 2017 Note will not mature on March 31, 2019 and has no guaranteed source of capital that will sustain operations into the second quarter of 2019. There can be no assurance that any such potential financing opportunities will be available on acceptable terms, if at all. If the Company is unable to raise sufficient capital on the Company’s required timelines and on acceptable terms to shareholders and the Board of Directors, it could be forced to cease operations, including activities essential to support regulatory applications to commercialize EndoBarrier. If access to capital is not achieved in the near term, it will materially harm the Company’s business, financial condition and results of operations to the extent that the Company may be required to cease operations altogether, file for bankruptcy, or undertake any combination of the foregoing. In such event, our shareholders may lose their entire investment in our company.

These factors raise substantial doubt about the Company’s ability to continue as a going concern within one year after the date that the financial statements are issued.

In addition, if we do not meet our payment obligations to third parties as they become due, we may be subject to litigation claims and our credit worthiness would be adversely affected. Even if we are successful in defending against these claims, litigation could result in substantial costs and would be a distraction to management and may have other unfavorable results that could further adversely impact our financial condition.

As a result of the factors described above, our financial statements include a going-concern disclosure.

16

The terms of our indebtedness, in particular the terms of the 2017 Note, may result in the liquidation or winding down of our business, which would have a negative impact on holders of our CDIs and common stock.

In June 2017, we completed our 2017 Note secured financing for a gross amount of $5.0 million that accrues interest of 5% per annum compounded annually. In December 2018, the maturity date of the 2017 Note was extended from December 31, 2018 to March 31, 2019 in exchange for payment of approximately $394 thousand, which was the total accrued interest on the 2017 Note at December 31, 2018.

As of February 28, 2019, we currently have outstanding debt obligations of $7.3 million, including interest accrued through February 28, 2019. Approximately $5.5 million of this amount is due and payable on or before March 31, 2019 under the terms of the 2017 Note, unless (i) the 2017 Note is converted to equity prior to March 31, 2019 or (ii) we restructure the 2017 Note to extend the maturity date, as we did in December 2018. Our debt obligations are secured by all of our assets such that upon an event of default, we may be forced to sell some or all of our assets in order to make payment against the debt obligation when due. The proceeds from the sale of all of our assets may be insufficient to satisfy our debt obligations in full. As a result, it is unlikely that any proceeds would be available for distribution to holders of our CDIs or common stock on a sale of our assets or on a liquidation or winding down of our business.

Failure to achieve a positive outcome in the U.S. clinical trial of EndoBarrier could negatively impact our ability to raise additional capital and obtain regulatory approval in other countries.

We intend to conduct the U.S. pivotal trial of EndoBarrier under the FDA’s Investigational Device Exemption. We refer to this trial as 18-1 clinical trial in our statements and filings. Failure to achieve a positive outcome in this clinical trial could result in the failure of EndoBarrier to gain regulatory approval in the U. S. This outcome could negatively impact our ability to raise additional capital and obtain regulatory approval in other countries.

In order to complete the 18-1 clinical trial, we will need to enroll patients. If we are unable to enroll patients, or if the enrollment pace is slower than anticipated, it could have a negative effect on our ability to complete the clinical trial, which could adversely affect our business, operating results and prospects.

Conducting successful clinical studies will require the enrollment of patients, and suitable patients may be difficult to identify and recruit. Patient enrollment in clinical trials and completion of patient participation and follow-up depends on many factors, including the size of the patient population, the nature of the trial protocol, the desirability of, or the discomforts and risks associated with, the treatments received by enrolled subjects, the availability of appropriate clinical trial investigators and support staff, the proximity of patients to clinical sites, the ability of patients to comply with the eligibility and exclusion criteria for participation in the clinical trial and patient compliance. For example, patients may be discouraged from enrolling in our clinical trials if the trial protocol requires them to undergo extensive post-treatment procedures or follow-up to assess the safety and effectiveness of our product or if they determine that the treatments received under the trial protocols are not desirable or involve unacceptable risk or discomfort.

Development of sufficient and appropriate clinical protocols to demonstrate safety and efficacy are required and we may not adequately develop such protocols to support clearance or approval. Further, the FDA may require us to submit data on a greater number of patients than we originally anticipated and/or for a longer follow-up period or change the data collection requirements or data analysis applicable to our clinical trials. Delays in patient enrollment or failure of patients to continue to participate in a clinical trial may cause an increase in costs and delays in the approval or clearance and attempted commercialization of our product or result in the failure of the clinical trial. In addition, despite considerable time and expense invested in clinical trials, the FDA may not consider our data adequate to demonstrate safety and efficacy. Such increased costs and delays or failures could adversely affect our business, operating results and prospects.

The FDA has mandated certain stopping rules in the 18-1 clinical trial. If the stopping rules are triggered or other unanticipated adverse issues occur during the 18-1 clinical trial, the FDA may not permit the trial to continue. If that were to happen, our business, operating results and prospects would be materially and adversely affected.

Clinical trials involve the administration of the biological product candidate to patients under the supervision of qualified investigators, generally physicians not employed by or under the trial sponsor’s control. Clinical trials are conducted under protocols detailing, among other things, the objectives of the clinical trial, dosing procedures, subject selection and exclusion criteria, and the parameters to be used to monitor subject safety, including stopping rules that assure a clinical trial will be stopped if certain adverse events should occur. In the context of our 18-1 clinical trial, hepatic bleeding is an example of an adverse event that would be investigated and could trigger such stopping rules.

17

If, during the 18-1 clinical trial, the stopping rules are triggered or other unanticipated adverse issues occur, the FDA may prevent us from enrolling additional patients in the clinical trial or may not permit the clinical trial to be completed. If that were to happen, our business, operating results and prospects would be materially and adversely affected.

In order to commercialize our product in the U.S. and certain other countries, we will need to obtain regulatory and other approvals. Our inability to achieve, or a delay in achieving, such approvals could lead to the denial of marketing approval for EndoBarrier® or any of our other products.

At present, we have no regulatory approvals for marketing and sale of EndoBarrier. In November 2017, we received notification from SGS, the Company’s now former notified body in Europe, that they were withdrawing the Certificate of Conformity for EndoBarrier. The Certificate of Conformity is required for the sale of any product under CE marking. As a result, we are not permitted to supply the EndoBarrier, EndoBarrier Delivery System and EndoBarrier Retrieval System in Europe.

There is no guarantee that we will obtain additional approvals from regulatory bodies in the future, including the FDA in the U.S. In the U.S., we stopped our pivotal trial of EndoBarrier in 2015. We will not be able to obtain FDA approval to commercialize EndoBarrier in the U.S. until the 18-1 clinical trial is successfully completed and regulatory approval is obtained from the FDA through the PMA review process. The 18-1 trial will be conducted in two stages. At the end of the first stage, the FDA will review data collected to date from the 18-1 trial and must approve the continuation of the 18-1 trial to the second stage. There can be no assurance that the FDA will approve continuation of the trial at the end of the first stage.

Regulatory authorities in other countries may also require additional clinical trials. Any such clinical trials may be delayed, suspended or prematurely terminated because costs are greater than we anticipate or for a variety of other reasons, including: delay or failure in reaching agreement with the foreign regulatory authority(ies), on a trial design that we are able to execute; delay or failure in obtaining authorization to commence a trial or inability to comply with conditions imposed by a regulatory authority regarding the scope or design of a clinical trial; or regulators may require that we suspend or terminate our clinical trials for various reasons, including noncompliance with regulatory requirements, unforeseen safety issues or adverse side effects, or a finding that the participants are being exposed to unacceptable health risks. Any of the factors that cause, or lead to, a delay in the commencement or completion of clinical trials may also ultimately lead to the denial of marketing approval for EndoBarrier or any of our other products. Necessary regulatory approvals could also be delayed, which could significantly impact our ability to commercialize our technology in the U.S. and other countries.

We have a history of net losses and we may never achieve or maintain profitability.

We are a medical device company with a limited history of operations and have limited commercial experience with our product. As of December 31, 2018, the Company’s primary source of liquidity is its cash and cash equivalents balances. The Company continues to evaluate which markets are appropriate to continue pursuing reimbursement, market awareness and general market development and selling efforts, and continue to restructure its business and costs, establish new priorities, and evaluate strategic options. We expect to continue to incur significant operating losses for the foreseeable future as we incur costs, including those associated with commercializing our products, conducting clinical trials to test our products, attempting to secure regulatory approvals for our products (in the U.S. and other countries) and increased costs associated with being a public company in the U.S. As a result, if the Company remains in business, it expects to incur significant operating losses for the next several years.

The Company has incurred operating losses since inception and at December 31, 2018, had an accumulated deficit of approximately $267 million and a working capital deficit of $3.3 million. The Company expects to incur significant operating losses for the next several years. At December 31, 2018, the Company had approximately $3.8 million in cash and cash equivalents.

We cannot predict the extent of our future operating losses and accumulated deficit, and we may never generate sufficient revenues to achieve or sustain profitability.

18

We depend heavily on the success of our product, EndoBarrier. We cannot give any assurance that EndoBarrier will receive regulatory approval, which is necessary before it can be commercialized.

Our ability to generate product revenues will depend heavily on the successful commercialization of our product, EndoBarrier, if approved by regulatory agencies in the U.S. or abroad. We cannot be certain that EndoBarrier will be successful in clinical trials or receive regulatory approval. Further, EndoBarrier may not receive regulatory approval even if it is successful in clinical trials. If we do not receive regulatory approvals for EndoBarrier, we may not be able to continue our operations.

If we can obtain the required regulatory approvals in the U.S. and certain other countries, we expect to derive substantially all our revenue from sales of EndoBarrier. Accordingly, our ability to generate revenues in the future relies on our ability to market and sell this product.

The degree of market acceptance for EndoBarrier will depend on a number of factors, including:

| • | the efficacy, ease of use and perceived advantages and disadvantages of EndoBarrier over other available treatments and technologies for managing type 2 diabetes and obesity; |

| • | the prevalence and severity of any adverse events or side effects of EndoBarrier; |

| • | the extent to which physicians adopt EndoBarrier (which may be influenced by our ability to provide additional clinical data regarding the potential long-term benefits provided by EndoBarrier and the strength of our sales and marketing initiatives); |

| • | the price of EndoBarrier and the third-party coverage and reimbursement for procedures using EndoBarrier; |

| • | the extent to which reimbursement may be secured for each country in which EndoBarrier is commercialized; and |

| • | our ability to attract and retain professional sales personnel to drive EndoBarrier revenue. |

We cannot predict the outcome and timing of our current and future human clinical trials of EndoBarrier products. If the trials do not produce positive results, the commercial prospects for EndoBarrier will be impaired.

The results of current and future human clinical trials, whether investigator initiated, or Company sponsored, cannot be predicted. If EndoBarrier or new products that we develop and test in the future cause serious adverse events in future human clinical trials, these trials may need to be delayed or stopped. For example, we stopped our U.S. pivotal trial (ENDO) in 2015 because of adverse events associated with EndoBarrier in that trial. In addition, these clinical trials may not produce positive safety or efficacy results or may produce results that are not as favorable as those seen in previous clinical trials.

Negative safety or efficacy results of any future human clinical trials could require that we attempt to modify the EndoBarrier device or the treatment guidelines to address these issues and there is no guarantee that any potential modifications would be successfully developed.

If future human clinical trials of EndoBarrier products do not meet the required clinical specifications or cause serious adverse or unexpected events, such as those experienced in our U.S. pivotal trial, then these results could affect regulatory approvals and adoption and materially impact potential product sales and reimbursement. If we are not able to adequately address any adverse or unexpected events through training, education, changes in product design or product claims, this may significantly impair the commercial prospects for EndoBarrier.

19

Doctors may not accept EndoBarrier as a treatment option, which would harm our business and future revenues, if any.

The commercial success of EndoBarrier will require acceptance by physicians, who may be slow to adopt our product for the following reasons (among others):

| • | lack of long-term clinical data supporting patient benefits or cost savings over existing alternative treatments; |

| • | lack of experience with EndoBarrier and training time required before it can be used, which may drive preferences for other products or procedures; |

| • | lack of adequate payment to the physician for implanting the device or caring for the patient (driven by availability of adequate coverage and reimbursement for hospitals and implanting physicians); |

| • | perceived strength of products, procedures or pharmacotherapies as alternatives to EndoBarrier; and |

| • | perceived liability risks associated generally with the use of new products and procedures. |

Although we have developed relationships with physicians who are key opinion leaders in certain countries, we cannot assure that these existing relationships and arrangements can be maintained or that new relationships will be established in support of our products. If physicians do not consider our products to be adequate for the treatment of type 2 diabetes and obesity or if a sufficient number of physicians recommend and use competing products or pharmacotherapies, it could harm our business and future revenues, if any.

We have limited sales, marketing and distribution experience; therefore, we may be unable to successfully commercialize our products.

There can be no guarantee that we will be able to effectively commercialize our products. Developing direct sales, distribution and marketing capabilities will require the devotion of significant resources and require us to ensure compliance with all legal and regulatory requirements for sales, marketing and distribution. Failure to develop these capabilities and meet these requirements could jeopardize our ability to market our products or could subject us to substantial liability. In addition, for those countries where we commercialize our products through distributors or other third parties, we will rely heavily on the ability of our partners to effectively market and sell our products to physicians and other end users in those countries. We cannot guarantee that distributors or other third parties will be effective in commercializing our products.

We may compete against companies that have longer operating histories, more established or approved products, and greater resources than we do, which may prevent us from achieving market penetration with our products.

Competition in the medical device industry is intense and EndoBarrier will likely compete in part against more established procedures and products for the treatment of type 2 diabetes and obesity. Bariatric surgery, including gastric bypass surgery and the gastric band, have been used for many years with extensive publication histories on clinical effectiveness. Large multinational medical device companies sell supplies for these procedures and are formidable competitors to us. In addition, certain drugs have been approved, and are used, for the treatment of type 2 diabetes and obesity. Pharmaceutical companies with significantly greater resources than us market these drugs, and we may be unable to compete effectively against these companies.

Many of our competitors have significantly greater sales, marketing, financial and manufacturing capabilities than we have and have established reputations and/or significantly greater name recognition. Accordingly, there is no assurance that we will be able to win market share from these competitors or that these competitors will not succeed in developing products that are more effective or economic.

Additionally, we are likely to compete with companies offering new technologies in the future. We may also face competition from other medical therapies, which may focus on our target market as well as competition from manufacturers of pharmaceutical and other devices that have not yet been developed. Competition from these companies could adversely affect our business.

20

We do not have data regarding the long-term benefits of EndoBarrier, which may affect market acceptance. Furthermore, if the long-term data, once obtained, does not indicate that EndoBarrier is as safe or effective as other treatment options, our business would be harmed.

An important factor that may be relevant to market acceptance of EndoBarrier is whether it improves or maintains glycemic control and maintains weight loss over extended periods of time after removal of the device. While we have tested and evaluated our technology in several clinical trials with hundreds of patients which, in the aggregate, have shown that EndoBarrier is an effective treatment for type 2 diabetes and obesity, we do not yet have sufficient data to demonstrate any longer-term benefits of our product in the treatment of type 2 diabetes and obesity following removal of the device from the patient.

We are continuing to monitor some patients who participated in our clinical trials after device removal to determine the ongoing effects and longevity of results, however, we do not currently have long-term data that supports the safety and efficacy of EndoBarrier. Accordingly, we cannot provide assurance that the long-term data, once obtained, will prove lower HbA1c levels compared to alternative treatment options for type 2 diabetes. If the results obtained from our clinical trials indicate that EndoBarrier is not as safe or effective as other treatment options or as effective as our current short-term data would suggest, EndoBarrier may not be approved, or its adoption may suffer, and our business would be harmed.

If we fail to obtain and maintain adequate levels of reimbursement for our products by health insurers and other third-party payers, there may be no commercially viable markets for our products, or the markets may be much smaller than expected.

If our products are approved for sale, health care providers, including hospitals and physicians that may purchase our products, generally rely on third-party payers, particularly government-sponsored health care and private health insurance providers, to pay for all or a portion of the costs of the procedures, including the cost of the products used in such procedures. Reimbursement and health care payment systems vary significantly by country. Third-party payers may attempt to limit coverage and the level of reimbursement of new therapeutic products.

If we fail to obtain and maintain adequate levels of reimbursement for our products by health insurers and other third-party payers, there may be few commercially viable markets for our products, or the markets may be much smaller than expected. Third-party payers may demand additional clinical data requiring new clinical trials or economic models showing the cost savings of using our product, each of which would consume resources and may delay the decision on reimbursement. If the results of such studies are not satisfactory to third-party payers, then reimbursement may not be received in an acceptable amount or at all. In addition, the efficacy, safety, performance and cost-effectiveness of our products in comparison to any competing products or therapies may determine the availability and level of reimbursement.