UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORMN-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number811-21403

Western Asset Inflation-Linked Income Fund

(Exact name of registrant as specified in charter)

620 Eighth Avenue, 49th Floor, New York, NY 10018

(Address of principal executive offices) (Zip code)

Robert I. Frenkel, Esq.

Legg Mason & Co., LLC

100 First Stamford Place

Stamford, CT 06902

(Name and address of agent for service)

Registrant’s telephone number, including area code: (888)777-0102

Date of fiscal year end: November 30

Date of reporting period: May 31, 2019

| ITEM 1. | REPORT TO STOCKHOLDERS. |

TheSemi-Annual Report to Stockholders is filed herewith.

| | |

| Semi-Annual Report | | May 31, 2019 |

WESTERN ASSET

INFLATION-LINKED

INCOME FUND (WIA)

Beginning in January 2021, as permitted by regulations adopted by the Securities and Exchange Commission, the Fund intends to no longer mail paper copies of the Fund’s shareholder reports like this one, unless you specifically request paper copies of the reports from the Fund or from your financial intermediary (such as a broker-dealer or bank). Instead, the reports will be made available on a website, and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you invest through a financial intermediary and you already elected to receive shareholder reports electronically(“e-delivery”), you will not be affected by this change and you need not take any action. If you have not already electede-delivery, you may elect to receive shareholder reports and other communications from the Fund electronically by contacting your financial intermediary.

You may elect to receive all future reports in paper free of charge. If you invest through a financial intermediary, you can contact your financial intermediary to request that you continue to receive paper copies of your shareholder reports. That election will apply to all Legg Mason funds held in your account at that financial intermediary. If you are a direct shareholder with the Fund, you can call the Fund at1-888-888-0151, or write to the Fund by regular mail at P.O. Box 505000, Louisville, KY 40233 or by overnight delivery to Computershare, 462 South 4th Street, Suite 1600, Louisville, KY 40202 to let the Fund know you wish to continue receiving paper copies of your shareholder reports. That election will apply to all Legg Mason Funds held in your account held directly with the fund complex.

|

| INVESTMENT PRODUCTS: NOT FDIC INSURED • NO BANK GUARANTEE • MAY LOSE VALUE |

Fund objectives

The Fund’s primary investment objective is to provide current income. Capital appreciation, when consistent with current income, is a secondary investment objective.

Letter from the president

Dear Shareholder,

We are pleased to provide the semi-annual report of Western Asset Inflation-Linked Income Fund for thesix-month reporting period ended May 31, 2019. Please read on for Fund performance information during the Fund’s reporting period.

As always, we remain committed to providing you with excellent service and a full spectrum of investment choices. We also remain committed to supplementing the support you receive from your financial advisor. One way we accomplish this is through our website, www.lmcef.com. Here you can gain immediate access to market and investment information, including:

| • | | Fund prices and performance, |

| • | | Market insights and commentaries from our portfolio managers, and |

| • | | A host of educational resources. |

We look forward to helping you meet your financial goals.

Sincerely,

Jane Trust, CFA

President

June 28, 2019

| | |

| II | | Western Asset Inflation-Linked Income Fund |

Performance review

For the six months ended May 31, 2019, Western Asset Inflation-Linked Income Fund returned 6.67% based on its net asset value (“NAV”)1 and 7.23% based on its New York Stock Exchange (“NYSE”) market price per share. The Fund’s unmanaged benchmarks, the Bloomberg Barclays U.S. Government Inflation-Linked1-10 Year Index2 and the Bloomberg Barclays U.S. Government Inflation-Linked All Maturities Index3, returned 4.64% and 6.11%, respectively, for the same period. The Bloomberg Barclays World Government Inflation-Linked All Maturities Index4 and the Fund’s Custom Benchmark5 returned 6.01% and 6.35%, respectively, over the same time frame.

During thissix-month period, the Fund made distributions to shareholders totaling $0.21 per share. As of May 31, 2019, the Fund estimates that all of the distributions were sourced from net investment income*. The performance table shows the Fund’ssix-month total return based on its NAV and market price as of May 31, 2019.Past performance is no guarantee of future results.

| | | | |

Performance Snapshotas of May 31, 2019

(unaudited) | |

| Price Per Share | | 6-Month

Total Return** | |

| $12.96 (NAV) | | | 6.67 | %† |

| $11.25 (Market Price) | | | 7.23 | %‡ |

All figures represent past performance and are not a guarantee of future results. Performance figures for periods shorter than one year represent cumulative figures and are not annualized.

** Total returns are based on changes in NAV or market price, respectively. Returns reflect the deduction of all Fund expenses, including management fees, operating expenses, and other Fund expenses. Returns do not reflect the deduction of brokerage commissions or taxes that investors may pay on distributions or the sale of shares.

† Total return assumes the reinvestment of all distributions, including returns of capital, if any, at NAV.

| * | These estimates are not for tax purposes. The Fund will issue a Form 1099 with final composition of the distributions for tax purposes after year end. A return of capital is not taxable and results in a reduction in the tax basis of a shareholder’s investment. For more information about a distribution’s composition, please refer to the Fund’s distribution press release or, if applicable, the Section 19 notice located in the press release section of our website www.lmcef.com (click on the name of the Fund). |

| 1 | Net asset value (“NAV”) is calculated by subtracting total liabilities, including liabilities associated with financial leverage (if any), from the closing value of all securities held by the Fund (plus all other assets) and dividing the result (total net assets) by the total number of the common shares outstanding. The NAV fluctuates with changes in the market prices of securities in which the Fund has invested. However, the price at which an investor may buy or sell shares of the Fund is the Fund’s market price as determined by supply of and demand for the Fund’s shares. |

| 2 | The Bloomberg Barclays U.S. Government Inflation-Linked1-10 Year Index measures the performance of the intermediate U.S. Treasury Inflation-Protected Securities (“TIPS”) market. |

| 3 | The Bloomberg Barclays U.S. Government Inflation-Linked All Maturities Index measures the performance of the U.S. TIPS market. The Index includes TIPS with one or more years remaining maturity with total outstanding issue size of $500 million or more. |

| 4 | The Bloomberg Barclays World Government Inflation-Linked All Maturities Index measures the performance of the major government inflation-linked bond markets. |

| 5 | The Custom Benchmark is comprised of 90% Bloomberg Barclays U.S. Government Inflation-Linked All Maturities Index and 10% Bloomberg Barclays U.S. Credit Index. The Bloomberg Barclays U.S. Credit Index is an index composed of corporate andnon-corporate debt issues that are investment grade (ratedBaa3/BBB- or higher). |

| | |

| Western Asset Inflation-Linked Income Fund | | III |

Performance review (cont’d)

‡ Total return assumes the reinvestment of all distributions, including returns of capital, if any, in additional shares in accordance with the Fund’s Dividend Reinvestment Plan.

One of the distinguishing features ofclosed-end funds compared to other investment vehicles is the ability to trade at a premium or discount to NAV. Since the Fund is listed on the NYSE, the share price may trade above (premium) or below (discount) its NAV. Whereas the NAV is reflective of the Fund’s underlying investments, the share price is reflective of the overall supply and demand in the marketplace. Historically, the majority ofclosed-end funds have traded at a discount to NAV. This Fund was no exception to the phenomenon. We believe the Fund’s discount may be driven by a number of factors, including the overallclosed-end fund market, current distribution rate and muted demand for inflation-linked investment products. While there are actions that may temporarily reduce the discount to NAV, which we discuss with the Board of Trustees, we believe that if investor demand for inflation-linked investments increased, that development, among other factors, may help reduce the Fund’s share price discount to NAV over time. Western Asset Management Company, LLC, the Fund’s investment adviser, continues to believe the Fund offers investors the opportunity for long-term inflation protection while providing a source of diversification for investors’ fixed-income portfolios.

Looking for additional information?

The Fund is traded under the symbol “WIA” and its closing market price is available in most newspapers under the NYSE listings. The daily NAV is availableon-line under the symbol “XWIAX” on most financial websites. Barron’s and the Wall Street Journal’s Monday edition both carryclosed-end fund tables that provide additional information. In addition, the Fund issues a quarterly press release that can be found on most major financial websites as well as www.lmcef.com (click on the name of the Fund).

In a continuing effort to provide information concerning the Fund, shareholders may call1-888-777-0102 (toll free), Monday through Friday from 8:00 a.m. to 5:30 p.m. Eastern Time, for the Fund’s current NAV, market price and other information.

Thank you for your investment in Western Asset Inflation-Linked Income Fund. As always, we appreciate that you have chosen us to manage your assets and we remain focused on achieving the Fund’s investment goals.

Sincerely,

Western Asset Management Company, LLC

June 28, 2019

RISKS: Bonds are subject to a variety of risks, including interest rate, credit and inflation risks. As interest rates rise, bond prices fall, reducing the value of a fixed-income investment’s price. The Fund is subject to the additional risks associated with inflation protected securities, including liquidity risk, prepayment risk, extension risk and deflation risk. Investments in foreign companies, including emerging markets, involve risks beyond those inherent solely in domestic investments. Leverage may cause a fund to be more volatile than if the fund had not been leveraged, which may increase the risk of investment loss. Derivatives, such as options, futures, forwards and swaps, can be illiquid, create counterparty risk, may disproportionately increase losses, and may have a potentially

| | |

| IV | | Western Asset Inflation-Linked Income Fund |

large impact on fund performance. To the extent that the Fund invests in asset-backed, mortgage-backed or mortgage-related securities, its exposure to prepayment and extension risks may be greater than if it invested in other fixed-income securities. International investments are subject to currency fluctuations, as well as social, economic and political risks. These risks are magnified in emerging markets.

An investment in the Fund is subject to the following additional risks. Lower grade securities, or equivalent unrated securities, which are commonly known as “junk bonds,” typically entail greater potential price volatility and may be less liquid than higher-rated securities. The Fund may have to apply a greater degree of judgment in establishing a price for lower grade securities for purposes of valuing fund shares. Changes in economic conditions or developments regarding the individual issuer are more likely to cause price volatility and weaken the capacity of such securities to make principal and interest payments than is the case for higher grade securities. Lower grade securities are regarded as having predominantly speculative characteristics with respect to the issuer’s capacity to pay interest and repay principal. These securities may also be more susceptible to real or perceived adverse economic and competitive industry conditions than higher rated securities. Lower grade and unrated securities are generally issued by less creditworthy issuers that may have a larger amount of outstanding debt relative to their assets than issuers of higher grade securities. In the event of an issuer’s bankruptcy, claims of other creditors may have priority over the claims of lower grade security holders, leaving few or no assets available to repay lower grade security holders. The Fund may incur expenses to the extent necessary to seek recovery upon default or to negotiate new terms with a defaulting issuer. Lower grade securities frequently have redemption features that permit an issuer to repurchase the security from the Fund before it matures. If the issuer redeems lower grade securities, the Fund may have to invest the proceeds in securities with lower yields and may lose income. Lower grade and unrated securities involve the risk that the Fund’s investment manager may not accurately evaluate the security’s comparative rating. Analysis of the creditworthiness of issuers of lower grade and unrated securities may be more complex than for issuers of higher-quality securities. To the extent that the Fund holds lower grade and/or unrated securities, the Fund’s success in achieving its investment objectives may depend more heavily on the Fund’s investment manager’s credit analysis than if the Fund held exclusively higher-quality and rated securities. If changes in the currency exchange rates do not occur as anticipated, the Fund may lose money on currency transactions. The Fund’s ability to use currency transactions successfully depends on a number of factors, including the currency transactions being available at prices that are not too costly, the availability of liquid markets and the ability of the Fund to accurately predict the direction of changes in currency exchange rates. Currency exchange rates may be volatile. Currency transactions are subject to counterparty risk, which is the risk that the other party in the transaction will not fulfill its contractual obligation. The Fund may gain exposure to the commodities markets by investing a portion of its assets in a wholly-owned subsidiary, Western Asset Inflation-Linked Income Fund CFC (the “Subsidiary”), organized under the laws of the Cayman Islands. The Fund and the Subsidiary are deemed “commodity pools” and the investment adviser is considered a “commodity pool operator” with respect to the Fund under the Commodity Exchange Act. The

| | |

| Western Asset Inflation-Linked Income Fund | | V |

Performance review (cont’d)

investment adviser, directly or through its affiliates, is therefore subject to dual regulation by the Securities and Exchange Commission (the “SEC”) and the Commodity Futures Trading Commission (the “CFTC”).

Due to recent regulatory changes, additional regulatory requirements may be imposed, and additional expenses may be incurred by the Fund. The regulatory requirements governing the use of commodity futures (which include futures on broad-based securities indexes, interest rate futures and currency futures), options on commodity futures, certain swaps or certain other investments could change at any time. Investments by the Fund in commodity-linked derivatives may subject the Fund to greater volatility than investments in traditional securities. The value of commodity-linked derivatives may be affected by changes in overall market movements, commodity index volatility, prolonged or intense speculation by investors, changes in interest rates or factors affecting a particular industry or commodity, such as drought, floods, other weather phenomena, livestock disease, embargoes, tariffs and international economic, political and regulatory developments. By investing in the Subsidiary, the Fund is indirectly exposed to the risks associated with the Subsidiary’s investments. The investments held by the Subsidiary are generally similar to those that are permitted to be held by the Fund and are subject to the same risks that apply to similar investments if held directly by the Fund. The Subsidiary is not registered as an investment company and is not subject to all of the investor protections of the Investment Company Act of 1940 (the “1940 Act”). Changes in the laws of the United States and/or the Cayman Islands could adversely affect the Fund. For example, the Cayman Islands does not currently impose any income, corporate or capital gains tax, estate duty, inheritance tax, gift tax or withholding tax on the Subsidiary. If Cayman Islands law changes such that the Subsidiary must pay Cayman Islands taxes, shareholders would likely suffer decreased investment returns. The Fund’s exposure to commodities markets, including through the Subsidiary, may be limited by its intention to qualify as a regulated investment company for U.S. federal income tax purposes, and may interfere with its ability to qualify as such.

This material is not intended as a recommendation or as investment advice of any kind, including in connection with rollovers, transfers, and distributions. Such material is not provided in a fiduciary capacity, may not be relied upon for or in connection with the making of investment decisions, and does not constitute a solicitation of an offer to buy or sell securities. All content has been provided for informational or educational purposes only and is not intended to be and should not be construed as legal or tax advice and/or a legal opinion. Always consult a financial, tax and/or legal professional regarding your specific situation.

All investments are subject to risk including the possible loss of principal. Past performance is no guarantee of future results. All index performance reflects no deduction for fees, expenses or taxes. Please note that an investor cannot invest directly in an index.

| | |

| VI | | Western Asset Inflation-Linked Income Fund |

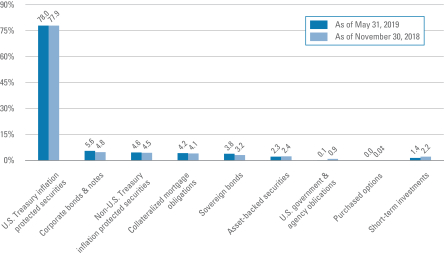

Fund at a glance†(unaudited)

Investment breakdown(%) as a percent of total investments

| † | The bar graph above represents the composition of the Fund’s investments as of May 31, 2019 and November 30, 2018 and does not include derivatives such as forward foreign currency contracts, futures contracts and swap contracts. The Fund is actively managed. As a result, the composition of the Fund’s investments is subject to change at any time. |

| ‡ | Represents less than 0.1%. |

| | |

| Western Asset Inflation-Linked Income Fund 2019 Semi-Annual Report | | 1 |

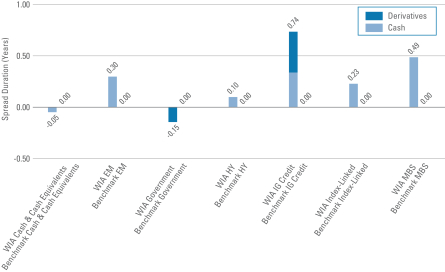

Spread duration(unaudited)

Economic exposure— May 31, 2019

Spread duration measures the sensitivity to changes in spreads. The spread over Treasuries is the annual risk-premium demanded by investors to holdnon-Treasury securities. Spread duration is quantified as the % change in price resulting from a 100 basis points change in spreads. For a security with positive spread duration, an increase in spreads would result in a price decline and a decline in spreads would result in a price increase. This chart highlights the market sector exposure of the Fund’s sectors relative to the selected benchmark sectors as of the end of the reporting period.

| | |

| |

| Benchmark | | — Bloomberg Barclays U.S. Government Inflation-Linked All Maturities Index |

| |

| EM | | — Emerging Markets |

| |

| HY | | — High Yield |

| |

| IG Credit | | — Investment Grade Credit |

| |

| MBS | | — Mortgage-Backed Securities |

| |

| WIA | | — Western Asset Inflation-Linked Income Fund |

| | |

| 2 | | Western Asset Inflation-Linked Income Fund 2019 Semi-Annual Report |

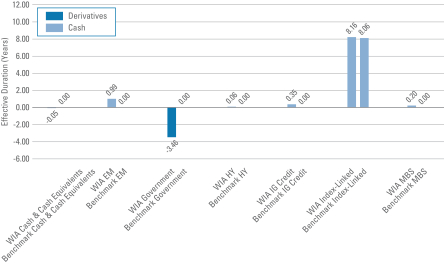

Effective duration(unaudited)

Interest rate exposure— May 31, 2019

Effective duration measures the sensitivity to changes in relevant interest rates. Effective duration is quantified as the % change in price resulting from a 100 basis points change in interest rates. For a security with positive effective duration, an increase in interest rates would result in a price decline and a decline in interest rates would result in a price increase. This chart highlights the interest rate exposure of the Fund’s sectors relative to the selected benchmark sectors as of the end of the reporting period.

| | |

| |

| Benchmark | | — Bloomberg Barclays U.S. Government Inflation-Linked All Maturities Index |

| |

| EM | | — Emerging Markets |

| |

| HY | | — High Yield |

| |

| IG Credit | | — Investment Grade Credit |

| |

| MBS | | — Mortgage-Backed Securities |

| |

| WIA | | — Western Asset Inflation-Linked Income Fund |

| | |

| Western Asset Inflation-Linked Income Fund 2019 Semi-Annual Report | | 3 |

Consolidated schedule of investments(unaudited)

May 31, 2019

Western Asset Inflation-Linked Income Fund

| | | | | | | | | | | | | | | | |

| Security | | Rate | | | Maturity

Date | | | Face

Amount† | | | Value | |

| U.S. Treasury Inflation Protected Securities — 111.9% | | | | | | | | | | | | | | | | |

U.S. Treasury Bonds, Inflation Indexed | | | 2.375 | % | | | 1/15/25 | | | | 10,788,560 | | | $ | 12,010,457 | |

U.S. Treasury Bonds, Inflation Indexed | | | 2.000 | % | | | 1/15/26 | | | | 55,917,982 | | | | 61,987,162 | (a) |

U.S. Treasury Bonds, Inflation Indexed | | | 1.750 | % | | | 1/15/28 | | | | 33,853,860 | | | | 37,752,471 | (a) |

U.S. Treasury Bonds, Inflation Indexed | | | 3.625 | % | | | 4/15/28 | | | | 157,167 | | | | 201,036 | |

U.S. Treasury Bonds, Inflation Indexed | | | 2.500 | % | | | 1/15/29 | | | | 7,210,499 | | | | 8,630,740 | |

U.S. Treasury Bonds, Inflation Indexed | | | 3.875 | % | | | 4/15/29 | | | | 32,472,300 | | | | 43,279,954 | (a) |

U.S. Treasury Bonds, Inflation Indexed | | | 2.125 | % | | | 2/15/40 | | | | 3,528,300 | | | | 4,522,927 | |

U.S. Treasury Bonds, Inflation Indexed | | | 2.125 | % | | | 2/15/41 | | | | 4,747,631 | | | | 6,135,034 | |

U.S. Treasury Bonds, Inflation Indexed | | | 1.375 | % | | | 2/15/44 | | | | 22,108,894 | | | | 25,255,593 | (a) |

U.S. Treasury Bonds, Inflation Indexed | | | 0.750 | % | | | 2/15/45 | | | | 15,285,720 | | | | 15,242,034 | |

U.S. Treasury Bonds, Inflation Indexed | | | 1.000 | % | | | 2/15/48 | | | | 3,092,520 | | | | 3,283,492 | |

U.S. Treasury Bonds, Inflation Indexed | | | 1.000 | % | | | 2/15/49 | | | | 3,040,702 | | | | 3,244,138 | |

U.S. Treasury Notes, Inflation Indexed | | | 0.125 | % | | | 4/15/20 | | | | 52,212,550 | | | | 51,797,501 | (a) |

U.S. Treasury Notes, Inflation Indexed | | | 0.125 | % | | | 4/15/21 | | | | 23,596,100 | | | | 23,368,618 | |

U.S. Treasury Notes, Inflation Indexed | | | 0.625 | % | | | 7/15/21 | | | | 15,790,040 | | | | 15,884,778 | |

U.S. Treasury Notes, Inflation Indexed | | | 0.125 | % | | | 1/15/22 | | | | 11,905,072 | | | | 11,825,122 | |

U.S. Treasury Notes, Inflation Indexed | | | 0.125 | % | | | 4/15/22 | | | | 44,214,498 | | | | 43,833,720 | (a) |

U.S. Treasury Notes, Inflation Indexed | | | 0.125 | % | | | 7/15/22 | | | | 25,313,660 | | | | 25,219,667 | (a) |

U.S. Treasury Notes, Inflation Indexed | | | 0.125 | % | | | 1/15/23 | | | | 6,607,740 | | | | 6,556,106 | |

U.S. Treasury Notes, Inflation Indexed | | | 0.625 | % | | | 1/15/26 | | | | 22,134,576 | | | | 22,537,227 | |

Total U.S. Treasury Inflation Protected Securities (Cost — $414,188,970) | | | | | | | | 422,567,777 | |

| Corporate Bonds & Notes — 8.1% | | | | | | | | | | | | | | | | |

| Consumer Staples — 0.0% | | | | | | | | | | | | | | | | |

Tobacco — 0.0% | | | | | | | | | | | | | | | | |

Pyxus International Inc., Secured Notes | | | 9.875 | % | | | 7/15/21 | | | | 160,000 | | | | 136,400 | |

| Energy — 4.6% | | | | | | | | | | | | | | | | |

Energy Equipment & Services — 0.1% | | | | | | | | | | | | | | | | |

Halliburton Co., Senior Notes | | | 3.800 | % | | | 11/15/25 | | | | 200,000 | | | | 206,073 | |

Oil, Gas & Consumable Fuels — 4.5% | | | | | | | | | | | | | | | | |

Anadarko Petroleum Corp., Senior Notes | | | 5.550 | % | | | 3/15/26 | | | | 110,000 | | | | 122,117 | |

Anadarko Petroleum Corp., Senior Notes | | | 6.200 | % | | | 3/15/40 | | | | 1,330,000 | | | | 1,597,259 | |

Apache Corp., Senior Notes | | | 2.625 | % | | | 1/15/23 | | | | 115,000 | | | | 113,333 | |

Apache Corp., Senior Notes | | | 5.250 | % | | | 2/1/42 | | | | 440,000 | | | | 452,619 | |

Apache Corp., Senior Notes | | | 4.250 | % | | | 1/15/44 | | | | 1,310,000 | | | | 1,175,466 | |

BP Capital Markets America Inc., Senior Notes | | | 3.119 | % | | | 5/4/26 | | | | 200,000 | | | | 200,593 | |

Exxon Mobil Corp., Senior Notes | | | 3.043 | % | | | 3/1/26 | | | | 200,000 | | | | 204,350 | |

Gazprom OAO Via Gaz Capital SA, Senior Notes | | | 5.150 | % | | | 2/11/26 | | | | 1,830,000 | | | | 1,884,183 | (b) |

KazTransGas JSC, Senior Notes | | | 4.375 | % | | | 9/26/27 | | | | 2,000,000 | | | | 2,002,484 | (b) |

See Notes to Consolidated Financial Statements.

| | |

| 4 | | Western Asset Inflation-Linked Income Fund 2019 Semi-Annual Report |

Western Asset Inflation-Linked Income Fund

| | | | | | | | | | | | | | | | |

| Security | | Rate | | | Maturity

Date | | | Face

Amount† | | | Value | |

Oil, Gas & Consumable Fuels — continued | | | | | | | | | | | | | | | | |

MEG Energy Corp., Secured Notes | | | 6.500 | % | | | 1/15/25 | | | | 30,000 | | | $ | 28,978 | (b) |

MEG Energy Corp., Senior Notes | | | 7.000 | % | | | 3/31/24 | | | | 50,000 | | | | 44,875 | (b) |

Noble Energy Inc., Senior Notes | | | 3.900 | % | | | 11/15/24 | | | | 200,000 | | | | 205,404 | |

Noble Energy Inc., Senior Notes | | | 4.950 | % | | | 8/15/47 | | | | 1,590,000 | | | | 1,627,567 | |

Oasis Petroleum Inc., Senior Notes | | | 6.875 | % | | | 1/15/23 | | | | 450,000 | | | | 433,125 | |

Occidental Petroleum Corp., Senior Notes | | | 3.000 | % | | | 2/15/27 | | | | 810,000 | | | | 787,090 | |

Petrobras Global Finance BV, Senior Notes | | | 5.999 | % | | | 1/27/28 | | | | 1,820,000 | | | | 1,876,420 | |

Transcontinental Gas Pipe Line Co. LLC, Senior Notes | | | 7.850 | % | | | 2/1/26 | | | | 200,000 | | | | 253,913 | |

Whiting Petroleum Corp., Senior Notes | | | 6.250 | % | | | 4/1/23 | | | | 2,000,000 | | | | 1,942,500 | |

Williams Cos. Inc., Senior Notes | | | 5.750 | % | | | 6/24/44 | | | | 1,340,000 | | | | 1,463,124 | |

YPF Sociedad Anonima, Senior Notes | | | 8.500 | % | | | 7/28/25 | | | | 800,000 | | | | 752,000 | (c) |

Total Oil, Gas & Consumable Fuels | | | | | | | | | | | | | | | 17,167,400 | |

Total Energy | | | | | | | | | | | | | | | 17,373,473 | |

| Financials — 0.9% | | | | | | | | | | | | | | | | |

Banks — 0.7% | | | | | | | | | | | | | | | | |

Barclays Bank PLC, Subordinated Notes | | | 7.625 | % | | | 11/21/22 | | | | 2,440,000 | | | | 2,648,888 | |

Diversified Financial Services — 0.2% | | | | | | | | | | | | | | | | |

ILFCE-Capital Trust II, Ltd. Gtd. ((Highest of 3 mo. USD LIBOR, 10 year U.S. Treasury Constant Maturity Rate and 30 year U.S. Treasury Constant Maturity Rate) + 1.800%) | | | 4.850 | % | | | 12/21/65 | | | | 1,010,000 | | | | 762,550 | (b)(d) |

Total Financials | | | | | | | | | | | | | | | 3,411,438 | |

| Health Care — 1.0% | | | | | | | | | | | | | | | | |

Pharmaceuticals — 1.0% | | | | | | | | | | | | | | | | |

Bausch Health Americas Inc., Senior Notes | | | 9.250 | % | | | 4/1/26 | | | | 550,000 | | | | 596,922 | (b) |

Bausch Health Americas Inc., Senior Notes | | | 8.500 | % | | | 1/31/27 | | | | 970,000 | | | | 1,020,624 | (b) |

Bausch Health Cos. Inc., Senior Notes | | | 6.125 | % | | | 4/15/25 | | | | 840,000 | | | | 820,575 | (b) |

Bausch Health Cos. Inc., Senior Notes | | | 9.000 | % | | | 12/15/25 | | | | 1,280,000 | | | | 1,382,400 | (b) |

Total Health Care | | | | | | | | | | | | | | | 3,820,521 | |

| Materials — 1.6% | | | | | | | | | | | | | | | | |

Metals & Mining — 1.6% | | | | | | | | | | | | | | | | |

Alcoa Nederland Holding BV, Senior Notes | | | 6.125 | % | | | 5/15/28 | | | | 720,000 | | | | 725,400 | (b) |

Anglo American Capital PLC, Senior Notes | | | 4.000 | % | | | 9/11/27 | | | | 800,000 | | | | 785,152 | (b) |

ArcelorMittal, Senior Notes | | | 6.125 | % | | | 6/1/25 | | | | 350,000 | | | | 387,216 | |

Barrick Gold Corp., Senior Notes | | | 5.250 | % | | | 4/1/42 | | | | 200,000 | | | | 213,066 | |

Glencore Funding LLC, Senior Notes | | | 4.125 | % | | | 3/12/24 | | | | 370,000 | | | | 377,624 | (b) |

Glencore Funding LLC, Senior Notes | | | 4.000 | % | | | 3/27/27 | | | | 200,000 | | | | 195,264 | (b) |

Glencore Funding LLC, Senior Notes | | | 3.875 | % | | | 10/27/27 | | | | 800,000 | | | | 777,240 | (b) |

Southern Copper Corp., Senior Notes | | | 5.250 | % | | | 11/8/42 | | | | 1,670,000 | | | | 1,729,883 | |

See Notes to Consolidated Financial Statements.

| | |

| Western Asset Inflation-Linked Income Fund 2019 Semi-Annual Report | | 5 |

Consolidated schedule of investments(unaudited) (cont’d)

May 31, 2019

Western Asset Inflation-Linked Income Fund

| | | | | | | | | | | | | | | | |

| Security | | Rate | | | Maturity

Date | | | Face

Amount† | | | Value | |

Metals & Mining — continued | | | | | | | | | | | | | | | | |

Yamana Gold Inc., Senior Notes | | | 4.625 | % | | | 12/15/27 | | | | 670,000 | | | $ | 673,599 | |

Total Materials | | | | | | | | | | | | | | | 5,864,444 | |

Total Corporate Bonds & Notes (Cost — $29,695,109) | | | | | | | | 30,606,276 | |

| Non-U.S. Treasury Inflation Protected Securities — 6.6% | | | | | | | | | | | | | | | | |

Brazil — 3.1% | | | | | | | | | | | | | | | | |

Brazil Notas do Tesouro Nacional Serie B, Notes | | | 6.000 | % | | | 8/15/30 | | | | 13,033,322 | BRL | | | 3,956,818 | |

Brazil Notas do Tesouro Nacional Serie B, Notes | | | 6.000 | % | | | 8/15/50 | | | | 22,927,796 | BRL | | | 7,704,103 | |

Total Brazil | | | | | | | | | | | | | | | 11,660,921 | |

Italy — 3.5% | | | | | | | | | | | | | | | | |

Italy Buoni Poliennali Del Tesoro | | | 3.100 | % | | | 9/15/26 | | | | 10,826,762 | EUR | | | 13,352,090 | (c) |

TotalNon-U.S. Treasury Inflation Protected Securities (Cost — $23,697,417) | | | | | | | | 25,013,011 | |

| Collateralized Mortgage Obligations (e) — 6.0% | | | | | | | | | | | | | | | | |

Alternative Loan Trust, 2007-12T1 A3 | | | 6.000 | % | | | 6/25/37 | | | | 1,606,950 | | | | 1,199,041 | |

BCAP LLC Trust,2011-RR5 11A4 (1 mo. USD LIBOR + 0.150%) | | | 2.627 | % | | | 5/28/36 | | | | 823,991 | | | | 821,233 | (b)(d) |

Bear Stearns ARM Trust,2004-9 24A1 | | | 4.836 | % | | | 11/25/34 | | | | 24,771 | | | | 24,800 | (d) |

Chase Mortgage Finance Trust,2007-A1 2A3 | | | 4.591 | % | | | 2/25/37 | | | | 5,775 | | | | 5,946 | (d) |

CSMC Trust,2014-11R 9A2 (1 mo. USD LIBOR + 0.140%) | | | 2.617 | % | | | 10/27/36 | | | | 2,430,000 | | | | 1,927,455 | (b)(d) |

Federal Home Loan Mortgage Corp. (FHLMC) Multifamily Structured Pass-Through Certificates, K721 X1, IO | | | 0.330 | % | | | 8/25/22 | | | | 149,119,821 | | | | 1,458,526 | (d) |

Federal Home Loan Mortgage Corp. (FHLMC) REMIC, 4057 UI, IO | | | 3.000 | % | | | 5/15/27 | | | | 923,082 | | | | 66,406 | |

Federal Home Loan Mortgage Corp. (FHLMC) REMIC, 4085 IO, IO | | | 3.000 | % | | | 6/15/27 | | | | 2,479,048 | | | | 180,143 | |

Federal Home Loan Mortgage Corp. (FHLMC) Structured Agency Credit Risk Debt Notes, 2017-DNA2 M2 (1 mo. USD LIBOR + 3.450%) | | | 5.880 | % | | | 10/25/29 | | | | 1,300,000 | | | | 1,399,241 | (d) |

Federal National Mortgage Association (FNMA) — CAS,2014-C04 1M2 (1 mo. USD LIBOR + 4.900%) | | | 7.330 | % | | | 11/25/24 | | | | 962,874 | | | | 1,082,359 | (b)(d) |

Federal National Mortgage Association (FNMA) — CAS,2016-C04 1M1 (1 mo. USD LIBOR + 1.450%) | | | 3.880 | % | | | 1/25/29 | | | | 282,036 | | | | 283,090 | (b)(d) |

Federal National Mortgage Association (FNMA) — CAS,2017-C03 1B1 (1 mo. USD LIBOR + 4.850%) | | | 7.280 | % | | | 10/25/29 | | | | 1,340,000 | | | | 1,494,395 | (b)(d) |

Federal National Mortgage Association (FNMA) — CAS,2017-C03 1M2 (1 mo. USD LIBOR + 3.000%) | | | 5.430 | % | | | 10/25/29 | | | | 1,310,000 | | | | 1,377,997 | (b)(d) |

Federal National Mortgage Association (FNMA) — CAS,2019-R02 1M1 (1 mo. USD LIBOR + 0.850%) | | | 3.280 | % | | | 8/25/31 | | | | 1,321,021 | | | | 1,324,572 | (b)(d) |

GMACM Mortgage Loan Trust,2005-AF2 A1 | | | 6.000 | % | | | 12/25/35 | | | | 1,161,541 | | | | 1,139,440 | |

Government National Mortgage Association (GNMA),2011-142 IO, IO | | | 0.229 | % | | | 9/16/46 | | | | 3,380,896 | | | | 27,330 | (d) |

Government National Mortgage Association (GNMA),2012-44 IO, IO | | | 0.407 | % | | | 3/16/49 | | | | 1,058,129 | | | | 13,012 | (d) |

See Notes to Consolidated Financial Statements.

| | |

| 6 | | Western Asset Inflation-Linked Income Fund 2019 Semi-Annual Report |

Western Asset Inflation-Linked Income Fund

| | | | | | | | | | | | | | | | |

| Security | | Rate | | | Maturity

Date | | | Face

Amount† | | | Value | |

| Collateralized Mortgage Obligations (e) — continued | | | | | | | | | | | | | | | | |

Government National Mortgage Association (GNMA),2012-112 IO, IO | | | 0.278 | % | | | 2/16/53 | | | | 1,820,706 | | | $ | 35,062 | (d) |

Government National Mortgage Association (GNMA),2012-152 IO, IO | | | 0.789 | % | | | 1/16/54 | | | | 5,978,690 | | | | 309,868 | (d) |

Government National Mortgage Association (GNMA),2013-145 IO, IO | | | 1.065 | % | | | 9/16/44 | | | | 2,485,796 | | | | 119,108 | (d) |

Government National Mortgage Association (GNMA),2014-47 IA, IO | | | 0.126 | % | | | 2/16/48 | | | | 551,450 | | | | 10,927 | (d) |

Government National Mortgage Association (GNMA),2014-50 IO, IO | | | 0.836 | % | | | 9/16/55 | | | | 1,580,530 | | | | 84,765 | (d) |

Government National Mortgage Association (GNMA),2014-169 IO, IO | | | 0.825 | % | | | 10/16/56 | | | | 13,739,062 | | | | 672,053 | (d) |

Government National Mortgage Association (GNMA),2015-101 IO, IO | | | 0.825 | % | | | 3/16/52 | | | | 21,617,835 | | | | 1,135,213 | (d) |

Government National Mortgage Association (GNMA),2015-183 IO, IO | | | 0.946 | % | | | 9/16/57 | | | | 26,421,481 | | | | 1,769,679 | (d) |

GSR Mortgage Loan Trust,2004-11 1A1 | | | 4.674 | % | | | 9/25/34 | | | | 61,228 | | | | 64,194 | (d) |

Merrill Lynch Mortgage Investors Trust Series MLMI,2004-A1 2A1 | | | 4.613 | % | | | 2/25/34 | | | | 8,795 | | | | 8,927 | (d) |

New Residential Mortgage Loan Trust,2014-1A A | | | 3.750 | % | | | 1/25/54 | | | | 820,311 | | | | 840,018 | (b)(d) |

Nomura Resecuritization Trust,2015-4R 2A2 (1 mo. USD LIBOR + 0.306%) | | | 2.617 | % | | | 10/26/36 | | | | 2,763,895 | | | | 2,374,176 | (b)(d) |

RAMP Series Trust,2004-SL4 A5 | | | 7.500 | % | | | 7/25/32 | | | | 54,722 | | | | 40,707 | |

WaMu Mortgage Pass-Through Certificates Trust,2007-OA2 1A (Federal Reserve US 12 mo. Cumulative Avg 1 Year CMT + 0.700%) | | | 3.181 | % | | | 3/25/47 | | | | 1,404,268 | | | | 1,293,323 | (d) |

Washington Mutual MSC Mortgage Pass-Through Certificates Series Trust,2004-RA1 2A | | | 7.000 | % | | | 3/25/34 | | | | 7,587 | | | | 8,320 | |

Total Collateralized Mortgage Obligations (Cost — $23,546,799) | | | | | | | | 22,591,326 | |

| Sovereign Bonds �� 5.5% | | | | | | | | | | | | | | | | |

Argentina — 0.4% | | | | | | | | | | | | | | | | |

Argentina POM Politica Monetaria, Bonds (Argentina Central Bank 7 Day Repo Reference Rate) | | | 68.804 | % | | | 6/21/20 | | | | 64,160,000 | ARS | | | 1,431,296 | (d) |

Chile — 1.0% | | | | | | | | | | | | | | | | |

Bonos de la Tesoreria de la Republica en pesos, Bonds | | | 5.000 | % | | | 3/1/35 | | | | 2,330,000,000 | CLP | | | 3,695,458 | |

Ecuador — 0.6% | | | | | | | | | | | | | | | | |

Ecuador Government International Bond, Senior Notes | | | 10.500 | % | | | 3/24/20 | | | | 1,520,000 | | | | 1,597,915 | (b) |

Ecuador Government International Bond, Senior Notes | | | 7.950 | % | | | 6/20/24 | | | | 520,000 | | | | 527,155 | (c) |

Total Ecuador | | | | | | | | | | | | | | | 2,125,070 | |

Indonesia — 1.1% | | | | | | | | | | | | | | | | |

Indonesia Government International Bond, Senior Notes | | | 5.125 | % | | | 1/15/45 | | | | 200,000 | | | | 217,159 | (b) |

See Notes to Consolidated Financial Statements.

| | |

| Western Asset Inflation-Linked Income Fund 2019 Semi-Annual Report | | 7 |

Consolidated schedule of investments(unaudited) (cont’d)

May 31, 2019

Western Asset Inflation-Linked Income Fund

| | | | | | | | | | | | | | | | |

| Security | | Rate | | | Maturity

Date | | | Face

Amount† | | | Value | |

Indonesia — continued | | | | | | | | | | | | | | | | |

Indonesia Government International Bond, Senior Notes | | | 4.750 | % | | | 7/18/47 | | | | 400,000 | | | $ | 414,074 | (b) |

Indonesia Government International Bond, Senior Notes | | | 4.350 | % | | | 1/11/48 | | | | 290,000 | | | | 292,403 | |

Indonesia Treasury Bond, Senior Notes | | | 7.000 | % | | | 5/15/27 | | | | 49,188,000,000 | IDR | | | 3,262,687 | |

Total Indonesia | | | | | | | | | | | | | | | 4,186,323 | |

Mexico — 1.0% | | | | | | | | | | | | | | | | |

Mexican Bonos, Senior Notes | | | 7.750 | % | | | 11/13/42 | | | | 10,990,000 | MXN | | | 523,216 | |

Mexican Bonos, Senior Notes | | | 8.000 | % | | | 11/7/47 | | | | 25,110,000 | MXN | | | 1,220,519 | |

Mexico Government International Bond, Senior Notes | | | 4.500 | % | | | 4/22/29 | | | | 1,830,000 | | | | 1,902,303 | |

Total Mexico | | | | | | | | | | | | | | | 3,646,038 | |

Nigeria — 0.0% | | | | | | | | | | | | | | | | |

Nigeria Government International Bond, Senior Notes | | | 6.500 | % | | | 11/28/27 | | | | 200,000 | | | | 189,726 | (b) |

Qatar — 0.5% | | | | | | | | | | | | | | | | |

Qatar Government International Bond, Senior Notes | | | 4.000 | % | | | 3/14/29 | | | | 1,850,000 | | | | 1,950,893 | (b) |

Russia — 0.9% | | | | | | | | | | | | | | | | |

Russian Federal Bond — OFZ | | | 7.050 | % | | | 1/19/28 | | | | 236,150,000 | RUB | | | 3,465,658 | |

Total Sovereign Bonds (Cost — $23,772,980) | | | | | | | | | | | | | | | 20,690,462 | |

| Asset-Backed Securities — 3.3% | | | | | | | | | | | | | | | | |

Ameriquest Mortgage Securities Inc., Asset-BackedPass-Through Certificates Series,2005-R7 M2 (1 mo. USD LIBOR + 0.500%) | | | 2.930 | % | | | 9/25/35 | | | | 1,300,000 | | | | 1,306,101 | (d) |

Ameriquest Mortgage Securities Inc., Asset-BackedPass-Through Certificates Series,2005-R10 M5 (1 mo. USD LIBOR + 0.630%) | | | 3.060 | % | | | 1/25/36 | | | | 4,660,000 | | | | 4,427,087 | (d) |

CWHEQ Revolving Home Equity Loan Trust Series,2005-C 2A (1 mo. USD LIBOR + 0.180%) | | | 2.620 | % | | | 7/15/35 | | | | 604,247 | | | | 589,792 | (d) |

CWHEQ Revolving Home Equity Loan Trust Series,2006-I 2A (1 mo. USD LIBOR + 0.140%) | | | 2.580 | % | | | 1/15/37 | | | | 882,703 | | | | 844,558 | (d) |

First Franklin Mortgage Loan Trust, 2006-FF15 A5 (1 mo. USD LIBOR + 0.160%) | | | 2.590 | % | | | 11/25/36 | | | | 1,342,340 | | | | 1,316,954 | (d) |

Legacy Mortgage Asset Trust,2019-GS1 A1 | | | 4.000 | % | | | 1/25/59 | | | | 1,268,237 | | | | 1,288,701 | (b) |

Structured Asset Securities Corp. Mortgage Loan Trust,2005-WF4 M8 (1 mo. USD LIBOR + 2.625%) | | | 5.055 | % | | | 11/25/35 | | | | 2,600,000 | | | | 2,714,784 | (d) |

Total Asset-Backed Securities (Cost — $10,852,223) | | | | | | | | | | | | | | | 12,487,977 | |

| U.S. Government & Agency Obligations — 0.1% | | | | | | | | | | | | | | | | |

U.S. Government Obligations — 0.1% | | | | | | | | | | | | | | | | |

U.S. Treasury Notes (Cost — $499,386) | | | 2.125 | % | | | 5/31/26 | | | | 500,000 | | | | 503,047 | |

Total Investments before Short-Term Investments (Cost — $526,252,884) | | | | | | | | 534,459,876 | |

See Notes to Consolidated Financial Statements.

| | |

| 8 | | Western Asset Inflation-Linked Income Fund 2019 Semi-Annual Report |

Western Asset Inflation-Linked Income Fund

| | | | | | | | | | | | | | | | |

| Security | | Rate | | | | | | Shares | | | Value | |

| Short-Term Investments — 2.0% | | | | | | | | | | | | | | | | |

Dreyfus Government Cash Management, Institutional Shares (Cost — $7,540,484) | | | 2.318 | % | | | | | | | 7,540,484 | | | $ | 7,540,484 | |

Total Investments — 143.5% (Cost — $533,793,368) | | | | | | | | | | | | | | | 542,000,360 | |

Liabilities in Excess of Other Assets — (43.5)% | | | | | | | | | | | | | | | (164,221,634 | ) |

Total Net Assets — 100.0% | | | | | | | | | | | | | | $ | 377,778,726 | |

| † | Face amount denominated in U.S. dollars, unless otherwise noted. |

| (a) | All or a portion of this security is held by the counterparty as collateral for open reverse repurchase agreements. |

| (b) | Security is exempt from registration under Rule 144A of the Securities Act of 1933. This security may be resold in transactions that are exempt from registration, normally to qualified institutional buyers. This security has been deemed liquid pursuant to guidelines approved by the Board of Trustees. |

| (c) | Security is exempt from registration under Regulation S of the Securities Act of 1933. Regulation S applies to securities offerings that are made outside of the United States and do not involve direct selling efforts in the United States. This security has been deemed liquid pursuant to guidelines approved by the Board of Trustees. |

| (d) | Variable rate security. Interest rate disclosed is as of the most recent information available. Certain variable rate securities are not based on a published reference rate and spread but are determined by the issuer or agent and are based on current market conditions. These securities do not indicate a reference rate and spread in their description above. |

| (e) | Collateralized mortgage obligations are secured by an underlying pool of mortgages or mortgage pass-through certificates that are structured to direct payments on underlying collateral to different series or classes of the obligations. The interest rate may change positively or inversely in relation to one or more interest rates, financial indices or other financial indicators and may be subject to an upper and/or lower limit. |

| | |

Abbreviations used in this schedule: |

| |

| ARM | | — Adjustable Rate Mortgage |

| |

| ARS | | — Argentine Peso |

| |

| BRL | | — Brazilian Real |

| |

| CAS | | — Connecticut Avenue Securities |

| |

| CLP | | — Chilean Peso |

| |

| CMT | | — Constant Maturity Treasury |

| |

| EUR | | — Euro |

| |

| IDR | | — Indonesian Rupiah |

| |

| IO | | — Interest Only |

| |

| JSC | | — Joint Stock Company |

| |

| LIBOR | | — London Interbank Offered Rate |

| |

| MXN | | — Mexican Peso |

| |

| REMIC | | — Real Estate Mortgage Investment Conduit |

| |

| RUB | | — Russian Ruble |

| |

| USD | | — United States Dollar |

See Notes to Consolidated Financial Statements.

| | |

| Western Asset Inflation-Linked Income Fund 2019 Semi-Annual Report | | 9 |

Consolidated schedule of investments(unaudited) (cont’d)

May 31, 2019

Western Asset Inflation-Linked Income Fund

At May 31, 2019, the Fund had the following open reverse repurchase agreements:

| | | | | | | | | | | | | | | | | | | | | | |

| Counterparty | | Rate | | | Effective

Date | | | Maturity

Date | | Face Amount

of Reverse

Repurchase

Agreements | | | Asset Class of Collateral* | | | Collateral

Value | |

| Deutsche Bank | | | 2.600% | | | | 4/11/2019 | | | 7/10/2019 | | $ | 171,526,300 | | | | U.S. Treasury Inflation Protected Securities | | | $ | 177,356,096 | |

| | | | | | | | | | | | | $ | 171,526,300 | | | | | | | $ | 177,356,096 | |

| * | Refer to the Consolidated Schedule of Investments for positions held at the counterparty as collateral for reverse repurchase agreements. At May 31, 2019, the Fund held non-cash collateral from Deutsche Bank in the amount of $602,280. |

At May 31, 2019, the Fund had the following open futures contracts:

| | | | | | | | | | | | | | | | | | | | |

| | | Number of

Contracts | | | Expiration

Date | | | Notional

Amount | | | Market

Value | | | Unrealized

Appreciation

(Depreciation) | |

| Contracts to Buy: | | | | | | | | | | | | | | | | | | | | |

| 90-Day Eurodollar | | | 92 | | | | 12/19 | | | $ | 22,367,666 | | | $ | 22,518,150 | | | $ | 150,484 | |

| Copper | | | 165 | | | | 7/19 | | | | 12,020,662 | | | | 10,890,000 | | | | (1,130,662) | |

| Euro | | | 83 | | | | 6/19 | | | | 11,760,276 | | | | 11,606,512 | | | | (153,763) | |

| Gold 100 Ounce | | | 54 | | | | 8/19 | | | | 6,974,775 | | | | 7,079,940 | | | | 105,165 | |

| Japanese Yen | | | 35 | | | | 6/19 | | | | 3,962,525 | | | | 4,040,969 | | | | 78,444 | |

| Mexican Peso | | | 104 | | | | 6/19 | | | | 2,639,948 | | | | 2,638,480 | | | | (1,469) | |

| U.S. Treasury2-Year Notes | | | 57 | | | | 9/19 | | | | 12,225,708 | | | | 12,236,297 | | | | 10,589 | |

| U.S. Treasury Long-Term Bonds | | | 179 | | | | 9/19 | | | | 26,948,544 | | | | 27,515,656 | | | | 567,112 | |

| WTI Crude | | | 72 | | | | 12/19 | | | | 4,058,739 | | | | 3,855,600 | | | | (203,139) | |

| WTI Crude | | | 142 | | | | 12/21 | | | | 7,916,511 | | | | 7,254,780 | | | | (661,731) | |

| | | | | | | | | | | | | | | | | | | | (1,238,970) | |

| Contracts to Sell: | | | | | | | | | | | | | | | | | | | | |

| British Pound | | | 33 | | | | 6/19 | | | | 2,744,634 | | | | 2,607,619 | | | | 137,016 | |

| Euro-Bund | | | 35 | | | | 6/19 | | | | 6,369,853 | | | | 6,582,136 | | | | (212,283) | |

| Euro-Bund | | | 71 | | | | 9/19 | | | | 13,539,562 | | | | 13,545,868 | | | | (6,307) | |

| Gasoline | | | 19 | | | | 12/19 | | | | 1,378,961 | | | | 1,200,591 | | | | 178,370 | |

| U.S. Treasury5-Year Notes | | | 1,051 | | | | 9/19 | | | | 122,500,058 | | | | 123,352,917 | | | | (852,859) | |

| U.S. Treasury10-Year Notes | | | 127 | | | | 9/19 | | | | 15,843,030 | | | | 16,097,250 | | | | (254,220) | |

| U.S. Treasury Ultra Long-Term Bonds | | | 268 | | | | 9/19 | | | | 46,279,848 | | | | 47,109,375 | | | | (829,527) | |

| WTI Crude | | | 69 | | | | 7/19 | | | | 4,292,317 | | | | 3,691,500 | | | | 600,818 | |

| | | | | | | | | | | | | | | | | | | | (1,238,992) | |

| Net unrealized depreciation on open futures contracts | | | | | | | $ | (2,477,962) | |

See Notes to Consolidated Financial Statements.

| | |

| 10 | | Western Asset Inflation-Linked Income Fund 2019 Semi-Annual Report |

Western Asset Inflation-Linked Income Fund

At May 31, 2019, the Fund had the following open forward foreign currency contracts:

| | | | | | | | | | | | | | | | | | | | |

Currency

Purchased | | | Currency

Sold | | | Counterparty | | Settlement

Date | | | Unrealized

Appreciation

(Depreciation) | |

| BRL | | | 7,730,000 | | | USD | | | 1,959,393 | | | Barclays Bank PLC | | | 7/17/19 | | | $ | 2,468 | |

| GBP | | | 1,928,058 | | | USD | | | 2,534,683 | | | Barclays Bank PLC | | | 7/17/19 | | | | (91,195) | |

| INR | | | 508,118,791 | | | USD | | | 7,206,132 | | | Barclays Bank PLC | | | 7/17/19 | | | | 47,397 | |

| MYR | | | 18,766,939 | | | USD | | | 4,591,749 | | | Barclays Bank PLC | | | 7/17/19 | | | | (116,579) | |

| RUB | | | 443,400,000 | | | USD | | | 6,671,231 | | | Barclays Bank PLC | | | 7/17/19 | | | | 60,445 | |

| USD | | | 26,476,660 | | | EUR | | | 23,338,609 | | | Barclays Bank PLC | | | 7/17/19 | | | | 298,650 | |

| USD | | | 78,247 | | | EUR | | | 70,000 | | | BNP Paribas SA | | | 7/17/19 | | | | (269) | |

| BRL | | | 60,000 | | | USD | | | 15,375 | | | Citibank N.A. | | | 7/17/19 | | | | (147) | |

| BRL | | | 4,802,309 | | | USD | | | 1,230,604 | | | Citibank N.A. | | | 7/17/19 | | | | (11,786) | |

| BRL | | | 12,490,000 | | | USD | | | 3,201,579 | | | Citibank N.A. | | | 7/17/19 | | | | (31,638) | |

| COP | | | 47,489,378,331 | | | USD | | | 15,016,404 | | | Citibank N.A. | | | 7/17/19 | | | | (996,753) | |

| IDR | | | 26,052,151,242 | | | USD | | | 1,802,668 | | | Citibank N.A. | | | 7/17/19 | | | | 11,875 | |

| JPY | | | 880,310 | | | USD | | | 7,954 | | | Citibank N.A. | | | 7/17/19 | | | | 201 | |

| RUB | | | 363,768,911 | | | USD | | | 5,511,224 | | | Citibank N.A. | | | 7/17/19 | | | | 11,496 | |

| USD | | | 229,845 | | | AUD | | | 322,519 | | | Citibank N.A. | | | 7/17/19 | | | | 5,789 | |

| USD | | | 56,113 | | | EUR | | | 50,000 | | | Citibank N.A. | | | 7/17/19 | | | | 30 | |

| USD | | | 1,487,412 | | | MXN | | | 29,003,786 | | | Citibank N.A. | | | 7/17/19 | | | | 19,571 | |

| BRL | | | 2,470,000 | | | USD | | | 632,984 | | | JPMorgan Chase & Co. | | | 7/17/19 | | | | (6,103) | |

| USD | | | 9,791,883 | | | TWD | | | 301,120,000 | | | JPMorgan Chase & Co. | | | 7/17/19 | | | | 240,251 | |

| Total | | | | | | | | | $ | (556,297) | |

| | |

Abbreviations used in this table: |

| |

| AUD | | — Australian Dollar |

| |

| BRL | | — Brazilian Real |

| |

| COP | | — Colombian Peso |

| |

| EUR | | — Euro |

| |

| GBP | | — British Pound |

| |

| IDR | | — Indonesian Rupiah |

| |

| INR | | — Indian Rupee |

| |

| JPY | | — Japanese Yen |

| |

| MXN | | — Mexican Peso |

| |

| MYR | | — Malaysian Ringgit |

| |

| RUB | | — Russian Ruble |

| |

| TWD | | — Taiwan Dollar |

| |

| USD | | — United States Dollar |

See Notes to Consolidated Financial Statements.

| | |

| Western Asset Inflation-Linked Income Fund 2019 Semi-Annual Report | | 11 |

Consolidated schedule of investments(unaudited) (cont’d)

May 31, 2019

Western Asset Inflation-Linked Income Fund

At May 31, 2019, the Fund had the following open swap contracts:

| | | | | | | | | | |

| CENTRALLY CLEARED INTEREST RATE SWAPS |

Notional

Amount | | Termination

Date | | Payments

Made by

the Fund† | | Payments

Received by

the Fund† | | Upfront

Premiums

Paid

(Received) | | Unrealized

(Depreciation) |

| $19,547,000 | | 8/31/23 | | 2.500% semi-annually | | 3-Month LIBOR quarterly | | $(1,219) | | $(466,080) |

| | | | | | | | | | | | | | | | | | | | | | |

| OTC INTEREST RATE SWAPS | |

| Swap Counterparty | | Notional

Amount | | | Termination

Date | | | Payments

Made by

the Fund† | | Payments

Received by

the Fund† | | | Upfront

Premiums

Paid

(Received) | | | Unrealized

Depreciation | |

| Barclays Bank PLC | | $ | 47,000,000 | | | | 5/3/20 | | | 2.023%* | | | CPURNSA | * | | | — | | | $ | (73,259) | |

| | | | | | | | | | | | | | | | | | | | | | |

| CENTRALLY CLEARED CREDIT DEFAULT SWAPS ON CREDIT INDICES — SELL PROTECTION1 | |

| Reference Entity | | Notional

Amount2 | | | Termination Date | | | Periodic

Payments

Received by

the Fund† | | Market

Value3 | | | Upfront

Premiums

Paid

(Received) | | | Unrealized

Depreciation | |

| Markit CDX.NA.IG.32 Index | | $ | 32,170,000 | | | | 6/20/24 | | | 1.000% quarterly | | $ | 451,249 | | | $ | 501,035 | | | $ | (49,786) | |

| 1 | If the Fund is a seller of protection and a credit event occurs, as defined under the terms of that particular swap agreement, the Fund will either (i) pay to the buyer of protection an amount equal to the notional amount of the swap and take delivery of the referenced obligation or underlying securities comprising the referenced index or (ii) pay a net settlement amount in the form of cash or securities equal to the notional amount of the swap less the recovery value of the referenced obligation or underlying securities comprising the referenced index. |

| 2 | The maximum potential amount the Fund could be required to pay as a seller of credit protection or receive as a buyer of credit protection if a credit event occurs as defined under the terms of that particular swap agreement. |

| 3 | The quoted market prices and resulting values for credit default swap agreements on asset-backed securities and credit indices serve as an indicator of the current status of the payment/performance risk and represent the likelihood of an expected loss (or profit) for the credit derivative had the notional amount of the swap agreement been closed/sold as of the period end. Decreasing market values (sell protection) or increasing market values (buy protection) when compared to the notional amount of the swap, represent a deterioration of the referenced entity’s credit soundness and a greater likelihood or risk of default or other credit event occurring as defined under the terms of the agreement. |

| † | Percentage shown is an annual percentage rate. |

| * | One time payment made at termination date. |

| | |

Abbreviations used in this table: |

| |

| CPURNSA | | — U.S. CPI Urban Consumers NSA Index |

| |

| LIBOR | | — London Interbank Offered Rate |

See Notes to Consolidated Financial Statements.

| | |

| 12 | | Western Asset Inflation-Linked Income Fund 2019 Semi-Annual Report |

Consolidated statement of assets and liabilities(unaudited)

May 31, 2019

| | | | |

| |

| Assets: | | | | |

Investments, at value (Cost — $533,793,368) | | $ | 542,000,360 | |

Foreign currency, at value (Cost — $2,078,190) | | | 2,032,582 | |

Deposits with brokers for open futures contracts | | | 2,644,472 | |

Interest receivable | | | 2,583,296 | |

Deposits with brokers for OTC derivatives | | | 1,050,000 | |

Deposits with brokers for centrally cleared swap contracts | | | 971,868 | |

Foreign currency collateral for open futures contracts, at value (Cost — $802,009) | | | 803,303 | |

Unrealized appreciation on forward foreign currency contracts | | | 698,173 | |

Prepaid expenses | | | 1,803 | |

Total Assets | | | 552,785,857 | |

| |

| Liabilities: | | | | |

Payable for open reverse repurchase agreements (Note 3) | | | 171,526,300 | |

Unrealized depreciation on forward foreign currency contracts | | | 1,254,470 | |

Payable to broker — variation margin on open futures contracts | | | 1,039,719 | |

Interest payable | | | 631,789 | |

Investment management fee payable | | | 162,469 | |

Payable to broker — variation margin on centrally cleared swap contracts | | | 143,178 | |

OTC swaps, at value (premiums received — $0) | | | 73,259 | |

Administration fee payable | | | 23,210 | |

Trustees’ fees payable | | | 15,060 | |

Accrued expenses | | | 137,677 | |

Total Liabilities | | | 175,007,131 | |

| Total Net Assets | | $ | 377,778,726 | |

| |

| Net Assets: | | | | |

Common shares, no par value, unlimited number of shares authorized, 29,152,820 shares issued and outstanding | | $ | 381,524,996 | |

Total distributable earnings (loss) | | | (3,746,270) | |

| Total Net Assets | | $ | 377,778,726 | |

| |

| Shares Outstanding | | | 29,152,820 | |

| |

| Net Asset Value | | | $12.96 | |

See Notes to Consolidated Financial Statements.

| | |

| Western Asset Inflation-Linked Income Fund 2019 Semi-Annual Report | | 13 |

Consolidated statement of operations(unaudited)

For the Six Months Ended May 31, 2019

| | | | |

| |

| Investment Income: | | | | |

Interest | | $ | 7,615,547 | |

Less: Foreign taxes withheld | | | (42,283) | |

Total Investment Income | | | 7,573,264 | |

| |

| Expenses: | | | | |

Interest expense (Note 3) | | | 2,255,172 | |

Investment management fee (Note 2) | | | 937,940 | |

Legal fees | | | 155,118 | |

Administration fees (Note 2) | | | 133,991 | |

Trustees’ fees | | | 44,300 | |

Fund accounting fees | | | 39,490 | |

Transfer agent fees | | | 36,056 | |

Audit and tax fees | | | 24,752 | |

Stock exchange listing fees | | | 14,147 | |

Commodity pool reports | | | 13,463 | |

Custody fees | | | 12,276 | |

Shareholder reports | | | 10,551 | |

Insurance | | | 3,570 | |

Miscellaneous expenses | | | 7,822 | |

Total Expenses | | | 3,688,648 | |

| Net Investment Income | | | 3,884,616 | |

| |

Realized and Unrealized Gain (Loss) on Investments, Futures Contracts,

Written Options, Swap Contracts, Forward Foreign Currency Contracts

and Foreign Currency Transactions (Notes 1, 3 and 4): | | | | |

Net Realized Gain (Loss) From: | | | | |

Investment transactions | | | (129,882) | |

Futures contracts | | | (3,141,361) | |

Written options | | | 115,719 | |

Swap contracts | | | 155,675 | |

Forward foreign currency contracts | | | 1,538,785 | |

Foreign currency transactions | | | (206,044) | |

Net Realized Loss | | | (1,667,108) | |

Change in Net Unrealized Appreciation (Depreciation) From: | | | | |

Investments | | | 22,596,933 | |

Futures contracts | | | (615,117) | |

Swap contracts | | | (393,611) | |

Forward foreign currency contracts | | | (34,474) | |

Foreign currencies | | | 119,537 | |

Change in Net Unrealized Appreciation (Depreciation) | | | 21,673,268 | |

| Net Gain on Investments, Futures Contracts, Written Options, Swap Contracts, Forward Foreign Currency Contracts and Foreign Currency Transactions | | | 20,006,160 | |

| Increase in Net Assets From Operations | | $ | 23,890,776 | |

See Notes to Consolidated Financial Statements.

| | |

| 14 | | Western Asset Inflation-Linked Income Fund 2019 Semi-Annual Report |

Consolidated statements of changes in net assets

| | | | | | | | |

For the Six Months Ended May 31, 2019 (unaudited)

and the Year Ended November 30, 2018 | | 2019 | | | 2018 | |

| | |

| Operations: | | | | | | | | |

Net investment income | | $ | 3,884,616 | | | $ | 9,740,317 | |

Net realized gain (loss) | | | (1,667,108) | | | | 1,911,903 | |

Change in net unrealized appreciation (depreciation) | | | 21,673,268 | | | | (21,272,346) | |

Increase (Decrease) in Net Assets From Operations | | | 23,890,776 | | | | (9,620,126) | |

| | |

| Distributions to Shareholders From (Note 1): | | | | | | | | |

Total distributable earnings | | | (6,034,634) | | | | (12,069,268) | |

Decrease in Net Assets From Distributions to Shareholders | | | (6,034,634) | | | | (12,069,268) | |

Increase (Decrease) in Net Assets | | | 17,856,142 | | | | (21,689,394) | |

| | |

| Net Assets: | | | | | | | | |

Beginning of period | | | 359,922,584 | | | | 381,611,978 | |

End of period | | $ | 377,778,726 | | | $ | 359,922,584 | |

See Notes to Consolidated Financial Statements.

| | |

| Western Asset Inflation-Linked Income Fund 2019 Semi-Annual Report | | 15 |

Consolidated statement of cash flows(unaudited)

For the Six Months Ended May 31, 2019

| | | | |

| |

| Increase (Decrease) in Cash: | | | | |

| Cash Provided (Used) by Operating Activities: | | | | |

Net increase in net assets resulting from operations | | $ | 23,890,776 | |

Adjustments to reconcile net increase in net assets resulting from operations to net cash provided (used) by operating activities: | | | | |

Purchases of portfolio securities | | | (93,923,697) | |

Sales of portfolio securities | | | 90,780,096 | |

Net purchases, sales and maturities of short-term investments | | | 4,113,609 | |

Net inflation adjustment | | | (2,946,182) | |

Net amortization of premium (accretion of discount) | | | 1,418,578 | |

Decrease in receivable for securities sold | | | 4,193,743 | |

Increase in interest receivable | | | (148,971) | |

Decrease in prepaid expenses | | | 13,065 | |

Increase in payable to broker — variation margin on centrally cleared swap contracts | | | 127,021 | |

Decrease in payable for securities purchased | | | (5,699,026) | |

Increase in investment management fee payable | | | 12,318 | |

Increase in Trustees’ fees payable | | | 1,236 | |

Increase in administration fee payable | | | 1,760 | |

Increase in interest payable | | | 442,120 | |

Decrease in accrued expenses | | | (55,850) | |

Increase in payable to broker — variation margin on open futures contracts | | | 964,923 | |

Net realized loss on investments | | | 129,882 | |

Change in net unrealized appreciation (depreciation) of investments, OTC swap contracts and forward foreign currency contracts | | | (22,489,200) | |

Net Cash Provided by Operating Activities* | | | 826,201 | |

| |

| Cash Flows From Financing Activities: | | | | |

Distributions paid on common stock | | | (6,034,634) | |

Decrease in due to custodian | | | (6,597) | |

Increase in payable for reverse repurchase agreements | | | 5,473,375 | |

Net Cash Used in Financing Activities | | | (567,856) | |

| Net Increase in Cash and Restricted Cash | | | 258,345 | |

Cash and restricted cash at beginning of period | | | 7,243,880 | |

Cash and restricted cash at end of period | | $ | 7,502,225 | |

| * | Included in operating expenses is cash of $1,813,052 paid for interest on borrowings. |

| | The following table provides a reconciliation of cash and restricted cash reported with the Consolidated Statement of Assets and Liabilities that sums to the total of the such amounts shown on the Consolidated Statement of Cash Flows. |

| | | | |

| | | May 31, 2019 | |

| Cash | | $ | 2,032,582 | |

| Restricted cash | | | 5,469,643 | |

| Total cash and restricted cash shown in the Consolidated Statement of Cash Flows | | $ | 7,502,225 | |

| | Restricted cash consists of cash that has been segregated to cover the Fund’s collateral or margin obligations under derivative contracts. It is separately reported on the Consolidated Statement of Assets and Liabilities as Deposits with brokers. |

See Notes to Consolidated Financial Statements.

| | |

| 16 | | Western Asset Inflation-Linked Income Fund 2019 Semi-Annual Report |

Consolidated financial highlights

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

For a share of capital stock outstanding throughout each year ended November 30,

unless otherwise noted: | |

| | | 20191,2 | | | 20181 | | | 20171 | | | 20161,3 | | | 20151,4 | | | 20141,4 | | | 20131,4 | |

| | | | | | | |

| Net asset value, beginning of period | | | $12.35 | | | | $13.09 | | | | $12.66 | | | | $12.47 | | | | $13.21 | | | | $13.14 | | | | $14.73 | |

| | | | | | | |

| Income (loss) from operations: | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | 0.13 | | | | 0.33 | | | | 0.34 | | | | 0.27 | | | | 0.07 | | | | 0.29 | | | | 0.10 | |

Net realized and unrealized gain (loss) | | | 0.69 | | | | (0.66) | | | | 0.48 | | | | 0.27 | | | | (0.46) | | | | 0.20 | | | | (1.31) | |

Total income (loss) from operations | | | 0.82 | | | | (0.33) | | | | 0.82 | | | | 0.54 | | | | (0.39) | | | | 0.49 | | | | (1.21) | |

| | | | | | | |

| Less distributions from: | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | (0.21) | 6 | | | (0.41) | | | | (0.40) | | | | (0.23) | | | | (0.10) | | | | (0.35) | | | | (0.11) | |

Net realized gains | | | — | | | | — | | | | — | | | | — | | | | (0.00) | 5 | | | (0.07) | | | | (0.27) | |

Return of capital | | | — | | | | — | | | | — | | | | (0.12) | | | | (0.26) | | | | — | | | | — | |

Total distributions | | | (0.21) | | | | (0.41) | | | | (0.40) | | | | (0.35) | | | | (0.35) | | | | (0.42) | | | | (0.38) | |

Payment by servicing agent | | | — | | | | — | | | | 0.01 | | | | — | | | | — | | | | — | | | | — | |

| | | | | | | |

| Net asset value, end of period | | | $12.96 | | | | $12.35 | | | | $13.09 | | | | $12.66 | | | | $12.47 | | | | $13.21 | | | | $13.14 | |

| | | | | | | |

| Market price, end of period | | | $11.25 | | | | $10.69 | | | | $11.62 | | | | $11.23 | | | | $10.57 | | | | $11.60 | | | | $11.42 | |

Total return, based on NAV7,8 | | | 6.67 | % | | | (2.49) | % | | | 6.77 | %9 | | | 4.28 | % | | | (3.00) | % | | | 3.68 | % | | | (8.29) | % |

Total return, based on Market Price10 | | | 7.23 | % | | | (4.61) | % | | | 7.15 | % | | | 9.61 | % | | | (5.95) | % | | | 5.20 | % | | | (10.15) | % |

| | | | | | | |

| Net assets, end of period (millions) | | | $378 | | | | $360 | | | | $382 | | | | $369 | | | | $363 | | | | $385 | | | | $383 | |

| | | | | | | |

| Ratios to average net assets: | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Gross expenses | | | 2.00 | %11 | | | 1.83 | % | | | 1.44 | % | | | 1.33 | %11 | | | 1.10 | % | | | 0.89 | % | | | 0.74 | % |

Net expenses | | | 2.00 | 11 | | | 1.62 | 12 | | | 1.44 | | | | 1.33 | 11 | | | 1.10 | | | | 0.89 | | | | 0.74 | |

Net investment income | | | 2.11 | 11 | | | 2.60 | | | | 2.63 | | | | 2.33 | 11 | | | 0.50 | | | | 2.17 | | | | 0.72 | |

| | | | | | | |

| Portfolio turnover rate | | | 18 | % | | | 45 | % | | | 59 | % | | | 88 | % | | | 59 | % | | | 30 | % | | | 65 | % |

See Notes to Consolidated Financial Statements.

| | |

| Western Asset Inflation-Linked Income Fund 2019 Semi-Annual Report | | 17 |

Consolidated financial highlights (cont’d)

| 1 | Per share amounts have been calculated using the average shares method. |

| 2 | For the six months ended May 31, 2019 (unaudited). |

| 3 | For the period January 1, 2016 through November 30, 2016. |

| 4 | For the year ended December 31. |

| 5 | Amount represents less than $0.005 per share. |

| 6 | The actual source of the Fund’s current fiscal year distributions may be from net investment income, return of capital or combination of both. Shareholders will be informed of the tax characteristics of the distributions after the close of the fiscal year. |

| 7 | Performance figures may reflect compensating balance arrangements, fee waivers and/or expense reimbursements. In the absence of compensating balance arrangements, fee waivers and/or expense reimbursements, the total return would have been lower. Past performance is no guarantee of future results. Total returns for periods of less than one year are not annualized. |

| 8 | The total return calculation assumes that distributions are reinvested at NAV. Past performance is no guarantee of future results. Total returns for periods of less than one year are not annualized. |

| 9 | The total return includes payment by the servicing agent. Without this payment, the total return would have been 6.69% for the year ended November 30, 2017. |

| 10 | The total return calculation assumes that distributions are reinvested in accordance with the Fund’s dividend reinvestment plan. Past performance is no guarantee of future results. Total returns for periods of less than one year are not annualized. |

See Notes to Consolidated Financial Statements.

| | |

| 18 | | Western Asset Inflation-Linked Income Fund 2019 Semi-Annual Report |

Notes to consolidated financial statements(unaudited)

1. Organization and significant accounting policies

Western Asset Inflation-Linked Income Fund (the “Fund”) is registered under the Investment Company Act of 1940, as amended (“1940 Act”), as a diversified,closed-end management investment company. The Fund commenced operations on September 26, 2003.

The Fund’s primary investment objective is to provide current income for its shareholders. Capital appreciation, when consistent with current income, is a secondary investment objective. If a security is rated by multiple nationally recognized statistical rating organizations (“NRSROs”) and receives different ratings, the Fund will treat the security as being rated in the highest rating category received from an NRSRO.

The Fund may gain exposure to the commodities markets by investing a portion of its assets in a wholly-owned subsidiary, Western Asset Inflation-Linked Income Fund CFC (the “Subsidiary”), organized under the laws of the Cayman Islands. Among other investments, the Subsidiary may invest in commodity-linked instruments. The Fund may invest up to 25% of its total assets in the Subsidiary; although 10% of total managed assets may be utilized for commodity-related strategies. These financial statements are consolidated financial statements of the Fund and the Subsidiary.

The following are significant accounting policies consistently followed by the Fund and are in conformity with U.S. generally accepted accounting principles (“GAAP”). Estimates and assumptions are required to be made regarding assets, liabilities and changes in net assets resulting from operations when financial statements are prepared. Changes in the economic environment, financial markets and any other parameters used in determining these estimates could cause actual results to differ. Subsequent events have been evaluated through the date the financial statements were issued.

(a) Investment valuation.The valuations for fixed income securities (which may include, but are not limited to, corporate, government, municipal, mortgage-backed, collateralized mortgage obligations and asset-backed securities) and certain derivative instruments are typically the prices supplied by independent third party pricing services, which may use market prices or broker/dealer quotations or a variety of valuation techniques and methodologies. The independent third party pricing services use inputs that are observable such as issuer details, interest rates, yield curves, prepayment speeds, credit risks/spreads, default rates and quoted prices for similar securities. Investments inopen-end funds are valued at the closing net asset value per share of each fund on the day of valuation. Futures contracts are valued daily at the settlement price established by the board of trade or exchange on which they are traded. Equity securities for which market quotations are available are valued at the last reported sales price or official closing price on the primary market or exchange on which they trade. When the Fund holds securities or other assets that are denominated in a foreign currency, the Fund will normally use the currency exchange rates as of 4:00 p.m. (Eastern Time). If independent third party pricing services are unable to supply prices for a portfolio investment, or if the prices supplied are deemed by the manager to be unreliable, the market price may be determined by the manager using quotations from one or more broker/dealers or at the transaction price if the security has recently

| | |

| Western Asset Inflation-Linked Income Fund 2019 Semi-Annual Report | | 19 |

Notes to financial statements(unaudited) (cont’d)

been purchased and no value has yet been obtained from a pricing service or pricing broker. When reliable prices are not readily available, such as when the value of a security has been significantly affected by events after the close of the exchange or market on which the security is principally traded, but before the Fund calculates its net asset value, the Fund values these securities as determined in accordance with procedures approved by the Fund’s Board of Trustees.

The Board of Trustees is responsible for the valuation process and has delegated the supervision of the daily valuation process to the Legg Mason North Atlantic Fund Valuation Committee (the “Valuation Committee”). The Valuation Committee, pursuant to the policies adopted by the Board of Trustees, is responsible for making fair value determinations, evaluating the effectiveness of the Fund’s pricing policies, and reporting to the Board of Trustees. When determining the reliability of third party pricing information for investments owned by the Fund, the Valuation Committee, among other things, conducts due diligence reviews of pricing vendors, monitors the daily change in prices and reviews transactions among market participants.

The Valuation Committee will consider pricing methodologies it deems relevant and appropriate when making fair value determinations. Examples of possible methodologies include, but are not limited to, multiple of earnings; discount from market of a similar freely traded security; discounted cash-flow analysis; book value or a multiple thereof; risk premium/yield analysis; yield to maturity; and/or fundamental investment analysis. The Valuation Committee will also consider factors it deems relevant and appropriate in light of the facts and circumstances. Examples of possible factors include, but are not limited to, the type of security; the issuer’s financial statements; the purchase price of the security; the discount from market value of unrestricted securities of the same class at the time of purchase; analysts’ research and observations from financial institutions; information regarding any transactions or offers with respect to the security; the existence of merger proposals or tender offers affecting the security; the price and extent of public trading in similar securities of the issuer or comparable companies; and the existence of a shelf registration for restricted securities.

For each portfolio security that has been fair valued pursuant to the policies adopted by the Board of Trustees, the fair value price is compared against the last available and next available market quotations. The Valuation Committee reviews the results of such back testing monthly and fair valuation occurrences are reported to the Board of Trustees quarterly.

The Fund uses valuation techniques to measure fair value that are consistent with the market approach and/or income approach, depending on the type of security and the particular circumstance. The market approach uses prices and other relevant information generated by market transactions involving identical or comparable securities. The income approach uses valuation techniques to discount estimated future cash flows to present value.

| | |

| 20 | | Western Asset Inflation-Linked Income Fund 2019 Semi-Annual Report |

GAAP establishes a disclosure hierarchy that categorizes the inputs to valuation techniques used to value assets and liabilities at measurement date. These inputs are summarized in the three broad levels listed below:

| • | | Level 1 — quoted prices in active markets for identical investments |

| • | | Level 2 — other significant observable inputs (including quoted prices for similar investments, interest rates, prepayment speeds, credit risk, etc.) |

| • | | Level 3 — significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of investments) |

The inputs or methodologies used to value securities are not necessarily an indication of the risk associated with investing in those securities.

The following is a summary of the inputs used in valuing the Fund’s assets and liabilities carried at fair value:

| | | | | | | | | | | | | | | | |

| ASSETS | |

| Description | | Quoted Prices

(Level 1) | | | Other Significant

Observable Inputs

(Level 2) | | | Significant

Unobservable

Inputs

(Level 3) | | | Total | |

| Long-term investments†: | | | | | | | | | | | | | | | | |

U.S. treasury inflation protected securities | | | — | | | $ | 422,567,777 | | | | — | | | $ | 422,567,777 | |

Corporate bonds & notes | | | — | | | | 30,606,276 | | | | — | | | | 30,606,276 | |

Non-U.S. treasury inflation protected securities | | | — | | | | 25,013,011 | | | | — | | | | 25,013,011 | |

Collateralized mortgage obligations | | | — | | | | 22,591,326 | | | | — | | | | 22,591,326 | |

Sovereign bonds | | | — | | | | 20,690,462 | | | | — | | | | 20,690,462 | |

Asset-backed securities | | | — | | | | 12,487,977 | | | | — | | | | 12,487,977 | |

U.S. government & agency obligations | | | — | | | | 503,047 | | | | — | | | | 503,047 | |

| Total long-term investments | | | — | | | | 534,459,876 | | | | — | | | | 534,459,876 | |

| Short-term investments† | | $ | 7,540,484 | | | | — | | | | — | | | | 7,540,484 | |

| Total investments | | $ | 7,540,484 | | | $ | 534,459,876 | | | | — | | | $ | 542,000,360 | |

| Other financial instruments: | | | | | | | | | | | | | | | | |

Futures contracts | | $ | 1,827,998 | | | | — | | | | — | | | $ | 1,827,998 | |

Forward foreign currency contracts | | | — | | | $ | 698,173 | | | | — | | | | 698,173 | |

| Total other financial instruments | | $ | 1,827,998 | | | $ | 698,173 | | | | — | | | $ | 2,526,171 | |