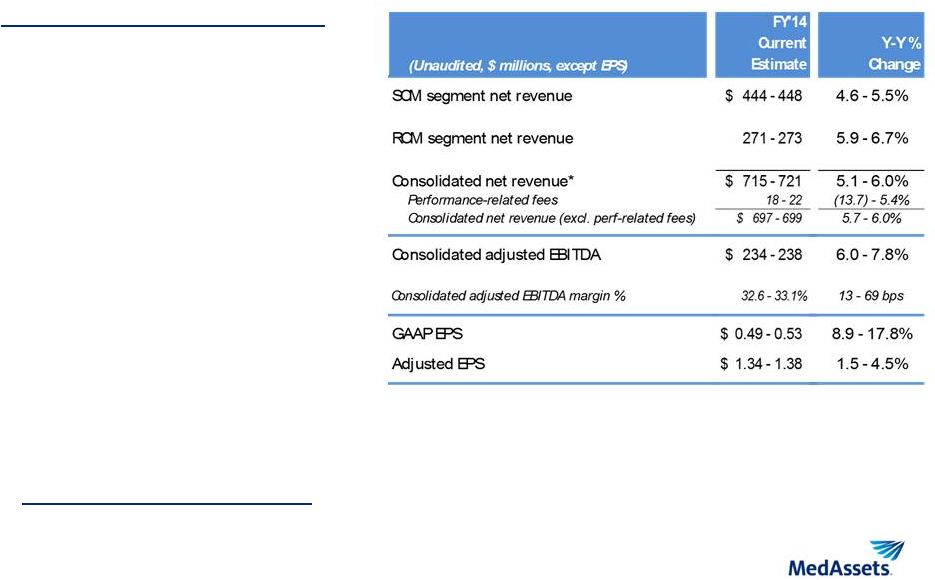

29 Use of Non-GAAP Financial Measures In order to provide investors with greater insight, promote transparency and allow for a more comprehensive understanding of the information used by management and the board of directors in their financial and operational decision-making, the Company supplements its condensed consolidated financial statements presented on a GAAP basis herein with the following non-GAAP financial information: gross fees; gross administrative fees; revenue share obligation; EBITDA; adjusted EBITDA; adjusted EBITDA margin; adjusted net income; diluted adjusted EPS; and free cash flow. These non-GAAP financial measures may have limitations as analytical tools and should not be considered in isolation or as a substitute for analysis of the Company’s results as reported under GAAP. The Company compensates for such limitations by relying primarily on the Company’s GAAP results and using non-GAAP financial measures only supplementally. Where possible, the Company provides reconciliations of non-GAAP financial measures to the most directly comparable GAAP measures. Investors are encouraged to carefully review those reconciliations. In addition, because these non-GAAP measures are not measures of financial performance under GAAP and are susceptible to varying calculations, these measures, as defined by the Company, may differ from and may not be comparable to similarly titled measures used by other companies. Gross fees include gross administrative fees the Company receives pursuant to its vendor contracts and all other fees the Company receives from clients. The Company's revenue share obligation represents the portion of the gross administrative fees the Company is contractually obligated to share with certain of its GPO clients. Net administrative fees (a GAAP measure) are the Company's gross administrative fees net of its revenue share obligation. Total net revenue (a GAAP measure) reflects the Company's gross fees net of its revenue share obligation. These non-GAAP measures assist management and the board of directors and may be helpful to investors in analyzing the Company's growth in its Spend and Clinical Resource Management segment given that administrative fees constitute a material portion of the Company's revenue and are paid to the Company by approximately 1,150 suppliers and other vendors contracted by its GPO, and that the Company's revenue share obligation constitutes a significant outlay to certain of its GPO clients. The Company defines: EBITDA as net income (loss) before net interest expense, income tax expense (benefit), depreciation and amortization; and adjusted EBITDA as net income (loss) before net interest expense, income tax expense (benefit), depreciation and amortization and other non-recurring, non-cash or non-operating items. EBITDA and adjusted EBITDA are used by the Company to facilitate a comparison of its operating performance on a consistent basis from period to period and provides for a more complete understanding of factors and trends affecting our business. These measures assist management and the board of directors and may be useful to investors in comparing the Company's operating performance consistently over time as it removes the impact of its capital structure (primarily interest charges and amortization of debt issuance costs), asset base (primarily depreciation and amortization) and items outside the control of the management team (taxes), as well as other non-cash (purchase accounting adjustments and imputed rental income) and non-recurring items, from the Company’s operational results. Adjusted EBITDA also removes the impact of non- cash share-based compensation expense and certain restructuring, acquisition and integration-related charges. EBITDA and adjusted EBITDA are not measures of liquidity under GAAP, or otherwise, and are not alternatives to cash flow from continuing operating activities. The Company defines adjusted net income as earnings excluding non-cash acquisition-related intangible amortization and non-recurring expense items on a tax-adjusted basis, non-cash tax-adjusted shared-based compensation expense, certain restructuring, acquisition and integration-related expenses on a tax-adjusted basis, purchase accounting adjustments on a tax-adjusted basis and diluted adjusted EPS as earnings per share excluding non-cash acquisition-related intangible amortization, depreciation and non-recurring expense items on a tax-adjusted basis, non-cash tax-adjusted shared-based compensation expense and certain restructuring, acquisition and integration- related expenses on a tax-adjusted basis. Adjusted net income and diluted adjusted EPS are not measures of liquidity under GAAP, or otherwise, and are not alternatives to cash flow from continuing operating activities. Use of this measure for this purpose allows management and the board of directors to analyze the Company’s operating performance on a consistent basis by removing the impact of certain non-cash and non-recurring items from our operations, and by rewarding organic growth and accretive business transactions. As a significant portion of senior management’s incentive based compensation has historically been based on the achievement of certain diluted adjusted EPS growth over time, investors may find such information useful. The Company defines free cash flow as cash provided by operating activities less purchases of property, equipment and software and capitalized software development costs. Management believes free cash flow is an important measure because it represents the cash that the Company is able to generate after spending capital on infrastructure to maintain its business and investing in new and upgraded products and services to support future growth. Free cash flow is important because it allows the Company to pursue opportunities that are intended to enhance shareholder value, which could include debt reduction, share repurchases, partnerships, alliances and acquisitions, and/or dividend payments. The Company's definition of free cash flow does not consider non-discretionary cash payments, such as debt. |