| FREE WRITING PROSPECTUS | ||

| FILED PURSUANT TO RULE 433 | ||

| REGISTRATION FILE NO.: 333-207132-10 | ||

January 23, 2017

Free Writing Prospectus

Structural and Collateral Term Sheet

$1,327,484,158

(Approximate Initial Mortgage Pool Balance)

$1,115,061,000

(Offered Certificates)

CD 2017-CD3 Mortgage Trust

As Issuing Entity

Citigroup Commercial Mortgage Securities Inc.

As Depositor

CD 2017-CD3 Mortgage Trust Commercial Mortgage Pass-Through

Certificates, Series 2017-CD3

Citigroup Global Markets Realty Corp.

German American Capital Corporation

As Sponsors and Mortgage Loan Sellers

STATEMENT REGARDING THIS FREE WRITING PROSPECTUS

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-207132) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Deutsche Bank Securities Inc., Drexel Hamilton, LLC, or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

IMPORTANT NOTICE RELATING TO AUTOMATICALLY GENERATED EMAIL DISCLAIMERS

Any legends, disclaimers or other notices that may appear at the bottom of the email communication to which this free writing prospectus is attached relating to (1) these materials not constituting an offer (or a solicitation of an offer), (2) no representation being made that these materials are accurate or complete and that these materials may not be updated or (3) these materials possibly being confidential, are, in each case, not applicable to these materials and should be disregarded. Such legends, disclaimers or other notices have been automatically generated as a result of these materials having been sent via Bloomberg or another system.

| Citigroup | Deutsche Bank Securities | |

| Co-Lead Managers and Joint Bookrunners | ||

| Drexel Hamilton | ||

| Co-Manager | ||

The securities offered by this structural and collateral term sheet (this “Term Sheet”) are described in greater detail in the preliminary prospectus, dated on or about January 24, 2017, included as part of our registration statement (SEC File No. 333-207132) (the “Preliminary Prospectus”). The Preliminary Prospectus contains material information that is not contained in this Term Sheet (including, without limitation, a detailed discussion of risks associated with an investment in the offered securities under the heading“Risk Factors” in the Preliminary Prospectus). The Preliminary Prospectus is available upon request from Citigroup Global Markets Inc., Deutsche Bank Securities Inc. or Drexel Hamilton, LLC. This Term Sheet is subject to change.

For information regarding certain risks associated with an investment in this transaction, refer to “Risk Factors” in the Preliminary Prospectus. Capitalized terms used but not otherwise defined in this Term Sheet have the respective meanings assigned to those terms in the Preliminary Prospectus.

The Securities May Not Be a Suitable Investment for You

The securities offered by this Term Sheet are not suitable investments for all investors. In particular, you should not purchase any class of securities unless you understand and are able to bear the prepayment, credit, liquidity and market risks associated with that class of securities. For those reasons and for the reasons set forth under the heading “Risk Factors” in the Preliminary Prospectus, the yield to maturity of, the aggregate amount and timing of distributions on and the market value of the offered securities are subject to material variability from period to period and give rise to the potential for significant loss over the life of those securities. The interaction of these factors and their effects are impossible to predict and are likely to change from time to time. As a result, an investment in the offered securities involves substantial risks and uncertainties and should be considered only by sophisticated institutional investors with substantial investment experience with similar types of securities and who have conducted appropriate due diligence on the mortgage loans and the securities. Potential investors are advised and encouraged to review the Preliminary Prospectus in full and to consult with their legal, tax, accounting and other advisors prior to making any investment in the offered securities described in this Term Sheet.

The securities offered by these materials are being offered when, as and if issued. This Term Sheet is not to be construed as an offer to sell or the solicitation of any offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal. The information contained in this Term Sheet may not pertain to any securities that will actually be sold. The information contained in this Term Sheet may be based on assumptions regarding market conditions and other matters as reflected in this Term Sheet. We make no representations regarding the reasonableness of such assumptions or the likelihood that any of such assumptions will coincide with actual market conditions or events, and this Term Sheet should not be relied upon for such purposes. We and our affiliates, officers, directors, partners and employees, including persons involved in the preparation or issuance of this Term Sheet may, from time to time, have long or short positions in, and buy or sell, the securities mentioned in this Term Sheet or derivatives thereof (including options). Information contained in this Term Sheet is current as of the date appearing on this Term Sheet only. Information in this Term Sheet regarding the securities and the mortgage loans backing any securities discussed in this Term Sheet supersedes all prior information regarding such securities and mortgage loans. None ofCitigroup Global Markets Inc., Deutsche Bank Securities Inc. or Drexel Hamilton, LLC provides accounting, tax or legal advice.

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-207132) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Deutsche Bank Securities Inc., Drexel Hamilton, LLC, or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

| 2 |

The issuing entity will be relying on an exclusion or exemption from the definition of “investment company” under the Investment Company Act of 1940, as amended (the “Investment Company Act”), contained in Section 3(c)(5) of the Investment Company Act or Rule 3a-7 under the Investment Company Act, although there may be additional exclusions or exemptions available to the issuing entity. The issuing entity is being structured so as not to constitute a “covered fund” for purposes of the Volcker Rule under the Dodd-Frank Act (both as defined in “Risk Factors—Legal and Regulatory Provisions Affecting Investors Could Adversely Affect the Liquidity of the Offered Certificates” in the Preliminary Prospectus). See also “Legal Investment” in the Preliminary Prospectus.

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-207132) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Deutsche Bank Securities Inc., Drexel Hamilton, LLC, or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

| 3 |

| CERTIFICATE SUMMARY |

| OFFERED CERTIFICATES |

| Offered Classes | Expected Ratings (Moody’s / Fitch / KBRA)(1) | Approximate Initial Certificate Balance or Notional Amount(2) | Approximate Initial Credit Support(3) | Initial Pass- Through Rate(4) | Pass- Through Rate Description | Expected Wtd. Avg. Life (Yrs)(5) | Expected Principal Window(5) | |||||||

| Class A-1 | Aaa(sf) / AAAsf / AAA(sf) | $ 29,155,000 | 30.000% | [ ]% | (6) | 2.62 | 3/17 - 10/21 | |||||||

| Class A-2 | Aaa(sf) / AAAsf / AAA(sf) | $ 38,347,000 | 30.000% | [ ]% | (6) | 4.72 | 10/21 - 12/21 | |||||||

| Class A-3 | Aaa(sf) / AAAsf / AAA(sf) | $ 200,000,000 | 30.000% | [ ]% | (6) | 9.35 | 8/25 - 11/26 | |||||||

| Class A-4 | Aaa(sf) / AAAsf / AAA(sf) | $ 589,293,000 | 30.000% | [ ]% | (6) | 9.82 | 11/26 - 1/27 | |||||||

| Class A-AB | Aaa(sf) / AAAsf / AAA(sf) | $ 54,788,000 | 30.000% | [ ]% | (6) | 7.28 | 12/21 - 10/26 | |||||||

| Class X-A | Aa1(sf) / AAAsf / AAA(sf) | $ 989,719,000(7) | N/A | [ ]% | Variable IO(8) | N/A | N/A | |||||||

| Class X-B | NR / AA-sf / AAA(sf) | $ 61,857,000(7) | N/A | [ ]% | Variable IO(8) | N/A | N/A | |||||||

| Class X-C | NR / A-sf / AAA(sf) | $ 63,485,000(7) | N/A | [ ]% | Variable IO(8) | N/A | N/A | |||||||

| Class A-S | Aa2(sf) / AAAsf / AAA(sf) | $ 78,136,000 | 24.000% | [ ]% | (6) | 9.91 | 1/27 - 1/27 | |||||||

| Class B | NR / AA-sf / AA(sf) | $ 61,857,000 | 19.250% | [ ]% | (6) | 9.91 | 1/27 - 1/27 | |||||||

| Class C | NR / A-sf / A(sf) | $ 63,485,000 | 14.375% | [ ]% | (6) | 9.91 | 1/27 - 1/27 |

| NON-OFFERED CERTIFICATES |

| Non-Offered Classes | Expected Ratings (Moody’s / Fitch / KBRA)(1) | Approximate Initial Certificate Balance or Notional Amount(2) | Approximate Initial Credit Support | Initial Pass-Through Rate(4) | Pass-Through Rate Description | Expected Wtd. Avg. Life (Yrs)(5) | Expected Principal Window(5) | |||||||

| Class X-D | NR / BBB-sf / BBB-(sf) | $ 76,508,000(7) | N/A | [ ]% | Variable IO(8) | N/A | N/A | |||||||

| Class D | NR / BBB-sf / BBB-(sf) | $ 76,508,000 | 8.500% | [ ]% | (6) | 9.91 | 1/27 - 1/27 | |||||||

| Class E(9) | NR / BB-sf / BB-(sf) | $ 35,812,000 | 5.750% | [ ]% | (6) | 9.91 | 1/27 - 1/27 | |||||||

| Class F(9) | NR / B-sf / B(sf) | $ 14,651,000 | 4.625% | [ ]% | (6) | 9.91 | 1/27 - 1/27 | |||||||

| Class G(9) | NR / NR / NR | $ 60,229,959 | 0.000% | [ ]% | (6) | 9.98 | 1/27 - 2/27 | |||||||

| Class S(10) | N/A | N/A | N/A | N/A | N/A | N/A | N/A | |||||||

| Class R(10) | N/A | N/A | N/A | N/A | N/A | N/A | N/A |

| NON-OFFERED VERTICAL RISK RETENTION INTEREST |

| Non-Offered Eligible Vertical Interest | Expected Ratings (Moody’s / Fitch / KBRA)(1) | Approximate Initial Certificate Balance or Notional Amount(2) | Approximate Initial Credit Support | Initial Pass-Through Rate(4) | Pass-Through Rate Description | Expected Wtd. Avg. Life (Yrs)(5) | Expected Principal Window(5) | |||||||

| VRR Interest(11) | NR / NR / NR | $ 25,222,199 | N/A | [ ]% | WAC(12) | 9.36 | 3/17 - 2/27 |

| (1) | It is a condition of issuance that the offered certificates and certain classes of non-offered certificates receive the ratings set forth above. The anticipated ratings shown are those of Moody’s Investors Service, Inc. (“Moody’s”), Fitch Ratings, Inc. (“Fitch”) and Kroll Bond Rating Agency, Inc. (“KBRA”). Subject to the discussion under “Ratings” in the Preliminary Prospectus, the ratings on the certificates address the likelihood of the timely receipt by holders of all payments of interest to which they are entitled on each distribution date and, except in the case of the interest only certificates, the ultimate receipt by holders of all payments of principal to which they are entitled on or before the applicable rated final distribution date. Certain nationally recognized statistical rating organizations, as defined in Section 3(a)(62) of the Securities Exchange Act of 1934, as amended, that were not hired by the depositor may use information they receive pursuant to Rule 17g-5 under the Securities Exchange Act of 1934, as amended, or otherwise to rate the offered certificates. We cannot assure you as to what ratings a non-hired nationally recognized statistical rating organization would assign. See “Risk Factors—Nationally Recognized Statistical Rating Organizations May Assign Different Ratings to the Certificates; Ratings of the Certificates Reflect Only the Views of the Applicable Rating Agencies as of the Dates Such Ratings Were Issued; Ratings May Affect ERISA Eligibility; Ratings May Be Downgraded” in the Preliminary Prospectus. Moody’s, Fitch and KBRA have informed us that the “sf” designation in the ratings represents an identifier of structured finance product ratings. For additional information about this identifier, prospective investors can go to the related rating agency’s website. The depositor and the underwriters have not verified, do not adopt and do not accept responsibility for any statements made by the rating agencies on those websites. Credit ratings referenced throughout this Term Sheet are forward-looking opinions about credit risk and express a rating agency’s opinion about the willingness and ability of an issuer of securities to meet its financial obligations in full and on time. Ratings are not indications of investment merit and are not buy, sell or hold recommendations, a measure of asset value or an indication of the suitability of an investment. |

| (2) | Approximate, subject to a variance of plus or minus 5%, including in connection with any variation in the certificate balances of the VRR Interest and/or the HRR Certificates following calculation of the actual fair value of all of the ABS interests (as such term is defined in Regulation RR) issued by the issuing entity, as described under “Credit Risk Retention” in the Preliminary Prospectus. The certificate balance of the VRR Interest is not included in the certificate balance or notional amount of any class of offered certificates or non-offered certificates listed in the table above, and the VRR Interest is not offered hereby. |

| (3) | The approximate initial credit support percentages set forth for the Class A-1, Class A-2, Class A-3, Class A-4 and Class A-AB certificates are represented in the aggregate. The approximate initial credit support percentages shown in the table above do not take into account the VRR Interest. However, losses incurred on the mortgage loans will be allocated between the VRR Interest, on the one hand, and the Non-Vertically Retained Certificates (exclusive of the Class X, Class S and Class R certificates), on the other hand,pro rata in accordance with their respective outstanding certificate balances. See “Credit Risk Retention” and “Description of the Certificates” in the Preliminary Prospectus. |

| (4) | Approximateper annum rate as of the Closing Date. |

| (5) | Determined assuming no prepayments prior to the maturity date or any anticipated repayment date, as applicable, for any mortgage loan and based on the modeling assumptions described under “Yield, Prepayment and Maturity Considerations” in the Preliminary Prospectus. |

| (6) | For any distribution date, the pass-through rates on the Class A-1, Class A-2, Class A-3, Class A-4, Class A-AB, Class A-S, Class B, Class C, Class D, Class E, Class F and Class G certificates (collectively, and together with the VRR Interest, the “principal balance certificates”) will generally be equal to one of (i) a fixedper annum rate, (ii) the weighted average of the net interest rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) as in effect from time to time, (iii) a rate equal to the lesser of a specifiedper annum rate and the weighted average rate described in clause (ii), or (iv) the weighted average rate described in clause (ii) less a specified percentage, but no less than 0.000%, as described under “Description of the Certificates—Distributions—Pass Through Rates” in the Preliminary Prospectus. |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-207132) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Deutsche Bank Securities Inc., Drexel Hamilton, LLC, or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

| 4 |

| (7) | The Class X-A, Class X-B, Class X-C and Class X-D certificates (collectively, the “Class X certificates”) will not have certificate balances and will not be entitled to receive distributions of principal. Interest will accrue on the Class X-A, Class X-B, Class X-C and Class X-D certificates at their respective pass-through rates based upon their respective notional amounts. The notional amount of the Class X-A certificates will be equal to the aggregate of the certificate balances of the Class A-1, Class A-2, Class A-3, Class A-4, Class A-AB and Class A-S certificates from time to time. The notional amount of the Class X-B certificates will be equal to the certificate balance of the Class B certificates from time to time. The notional amount of the Class X-C certificates will be equal to the certificate balance of the Class C certificates from time to time. The notional amount of the Class X-D certificates will be equal to the certificate balance of the Class D certificates from time to time. |

| (8) | The pass-through rate on each class of Class X certificates will generally be equal to aper annum rate equal to the excess, if any, of (i) the weighted average of the net interest rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) as in effect from time to time, over (ii) the pass-through rate (or the weighted average of the pass-through rates, as applicable) on the class (or classes, as applicable) of principal balance certificates with the certificate balance(s) upon which the notional amount of such class of Class X certificates is based, as described in the Preliminary Prospectus. |

| (9) | In satisfaction of a portion of the retaining sponsor’s risk retention obligations with respect to this transaction, all of the Class E, Class F and Class G certificates, in the aggregate initial certificate balance of approximately $110,692,959, are expected to represent approximately 3.1% of the fair value, as of the Closing Date, of all ABS interests issued by the issuing entity, and to constitute an “eligible horizontal residual interest” (as such term is defined in Regulation RR, collectively, the “HRR Certificates”), to be purchased and retained by KKR Real Estate Credit Opportunity Partners Aggregator I L.P. (or an affiliate) in accordance with the credit risk retention rules applicable to this securitization transaction. See “Credit Risk Retention” in the Preliminary Prospectus. |

| (10) | The Class S certificates and the Class R certificates will not have a certificate balance, notional amount, pass-through rate, rating or rated final distribution date. The Class R certificates will represent the residual interests in each of two separate REMICs, as further described in the Preliminary Prospectus. The Class R certificates will not be entitled to distributions of principal or interest. Excess interest accruing after the related anticipated repayment date on any mortgage loan with an anticipated repayment date will, to the extent collected, be allocated to the Class S certificates and the VRR Interest as set forth in “Description of the Certificates—Distributions—Excess Interest” in the Preliminary Prospectus. |

| (11) | Citigroup Global Markets Realty Corp., as the retaining sponsor, is expected to purchase from the depositor, on the Closing Date, an “eligible vertical interest” (as such term is defined in Regulation RR, the “VRR Interest”) in the form of a single vertical security with an aggregate initial certificate balance of approximately $25,222,199, which is expected to represent approximately 1.9% of the aggregate initial certificate balance of all of the ABS interests issued by the issuing entity. The VRR Interest will be retained by certain retaining parties in accordance with the credit risk retention rules applicable to this securitization transaction. See “Credit Risk Retention” in the Preliminary Prospectus. The VRR Interest is a class of certificates. |

| (12) | Although it does not have a specified pass-through rate (other than for tax reporting purposes), the effective interest rate for the VRR Interest will be the weighted average of the net mortgage interest rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) for the related distribution date. |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-207132) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Deutsche Bank Securities Inc., Drexel Hamilton, LLC, or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

| 5 |

| MORTGAGE POOL CHARACTERISTICS |

| Mortgage Pool Characteristics(1) | |

| Initial Pool Balance(2) | $1,327,484,158 |

| Number of Mortgage Loans | 52 |

| Number of Mortgaged Properties | 59 |

| Average Cut-off Date Balance | $25,528,542 |

| Weighted Average Mortgage Rate | 4.57758% |

| Weighted Average Remaining Term to Maturity/ARD (months)(3) | 116 |

| Weighted Average Remaining Amortization Term (months)(4) | 353 |

| Weighted Average Cut-off Date LTV Ratio(5) | 57.9% |

| Weighted Average Maturity Date/ARD LTV Ratio(3)(5) | 53.4% |

| Weighted Average UW NCF DSCR(6) | 1.95x |

| Weighted Average Debt Yield on Underwritten NOI(7) | 10.7% |

| % of Initial Pool Balance of Mortgage Loans that are Amortizing Balloon | 21.8% |

| % of Initial Pool Balance of Mortgage Loans that are Interest Only then Amortizing Balloon | 27.1% |

| % of Initial Pool Balance of Mortgage Loans that are Interest Only | 51.1% |

| % of Initial Pool Balance of Mortgaged Properties with Single Tenants | 13.6% |

| % of Initial Pool Balance of Mortgage Loans with Mezzanine or Subordinate Debt | 23.5% |

| (1) | With respect to each mortgage loan that is part of a loan combination (as identified under “Collateral Overview—Loan Combination Summary” below), the Cut-off Date LTV Ratio, Maturity Date/ARD LTV Ratio, UW NCF DSCR, Debt Yield on Underwritten NOI and Cut-off Date Balance Per SF / Rooms / Units are calculated based on both that mortgage loan and any related pari passu companion loan(s), but without regard to any related subordinate companion loan(s), unless otherwise indicated. Other than as specifically noted, the Cut-off Date LTV Ratio, Maturity Date/ARD LTV Ratio, UW NCF DSCR, Debt Yield on Underwritten NOI and Cut-off Date Balance Per SF / Rooms / Units information for each mortgage loan is presented in this Term Sheet without regard to any other indebtedness (whether or not secured by the related mortgaged property, ownership interests in the related borrower or otherwise) that currently exists or that may be incurred by the related borrower or its owners in the future. |

| (2) | Subject to a permitted variance of plus or minus 5%. |

| (3) | Unless otherwise indicated, mortgage loans with anticipated repayment dates are presented as if they were to mature on the anticipated repayment date. |

| (4) | Excludes mortgage loans that are interest-only for the entire term. |

| (5) | The Cut-off Date LTV Ratios and Maturity Date/ARD LTV Ratios presented in this Term Sheet are generally based on the “as-is” appraised values of the related mortgaged properties (as set forth on Annex A to the Preliminary Prospectus), provided, that such LTV ratios may be (i) based on “as-complete”, “as-stabilized” or similar values in certain cases where the completion of certain hypothetical conditions or other events at the property are assumed and/or where reserves have been established at origination to satisfy the applicable condition or event that is expected to occur, or (ii) calculated based on the Cut-off Date Balance or Balloon Balance, as applicable, net of a related earnout or holdback reserve, in each case as further described in the definitions of “Appraised Value”, “Cut-off Date LTV Ratio” and “Maturity Date/ARD LTV Ratio” under “Certain Definitions” in this Term Sheet and under “Description of the Mortgage Pool—Certain Calculations and Definitions” in the Preliminary Prospectus. |

| (6) | The UW NCF DSCR for each mortgage loan is generally calculated by dividing the UW NCF for the related mortgaged property or mortgaged properties by the annual debt service for such mortgage loan, as adjusted in the case of (i) mortgage loans with a partial interest only period by using the first 12 amortizing payments due instead of the actual interest only payment due or (ii) in certain cases calculated based on the annual debt service for such mortgage loan, net of a related earnout or holdback reserve. With respect to the Moffett Place Google and Key Vista Apartments mortgage loans, the UW NCF DSCR is calculated based on the annual debt service equal to the aggregate of the first 12 payments on the respective mortgage loan (and the relatedpari passucompanion loans in the case of the Moffett Place Google mortgage loan) following the Closing Date as set forth in the respective non-standard amortization schedules set forth in Annex G-1 and Annex G-2 to the Preliminary Prospectus. See the definition of “UW NCF DSCR” under “Description of the Mortgage Pool—Certain Calculations and Definitions”in the Preliminary Prospectus. |

| (7) | The Debt Yield on Underwritten NOI for each mortgage loan is generally calculated as the related mortgaged property’s Underwritten NOI divided by the Cut-off Date Balance of such mortgage loan, and the Debt Yield on Underwritten NCF for each mortgage loan is generally calculated as the related mortgaged property’s Underwritten NCF divided by the Cut-off Date Balance of such mortgage loan; provided, that such Debt Yields may be calculated based on the Cut-off Date Balance net of a related earnout or holdback reserve, as further described in the definitions of “Debt Yield on Underwritten NOI” and “Debt Yield on Underwritten NCF” under“Description of the Mortgage Pool—Certain Calculations and Definitions” in the Preliminary Prospectus. |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-207132) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Deutsche Bank Securities Inc., Drexel Hamilton, LLC, or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

| 6 |

| KEY FEATURES OF THE CERTIFICATES |

| Co-Lead Managers and Joint Bookrunners: | Citigroup Global Markets Inc. Deutsche Bank Securities Inc. |

| Co-Manager: | Drexel Hamilton, LLC |

| Depositor: | Citigroup Commercial Mortgage Securities Inc. |

| Initial Pool Balance: | $1,327,484,158 |

| Master Servicer: | Midland Loan Services, a Division of PNC Bank, National Association |

| Special Servicer: | Midland Loan Services, a Division of PNC Bank, National Association |

| Certificate Administrator: | Wells Fargo Bank, National Association |

| Trustee: | Wells Fargo Bank, National Association |

| Operating Advisor: | Park Bridge Lender Services LLC |

| Asset Representations Reviewer: | Park Bridge Lender Services LLC |

| Risk Retention Consultation Parties: | Citigroup Global Markets Realty Corp. and Deutsche Bank AG, New York Branch |

| Credit Risk Retention: | For a discussion on the manner in which the U.S. credit risk retention requirements are being satisfied by Citigroup Global Markets Realty Corp., as retaining sponsor, see “Credit Risk Retention” in the Preliminary Prospectus. Note that this securitization transaction is not structured to satisfy the EU risk retention and due diligence requirements. |

| Closing Date: | On or about February 14, 2017 |

| Cut-off Date: | With respect to each mortgage loan, the due date in February 2017 for that mortgage loan (or, in the case of any mortgage loan that has its first due date subsequent to February 2017, the date that would have been its due date in February 2017 under the terms of that mortgage loan if a monthly payment were scheduled to be due in that month) |

| Determination Date: | The 6th day of each month or next business day, commencing in March 2017 |

| Distribution Date: | The 4th business day after the Determination Date, commencing in March 2017 |

| Interest Accrual: | Preceding calendar month |

| ERISA Eligible: | The offered certificates are expected to be ERISA eligible, subject to the exemption conditions described in the Preliminary Prospectus |

| SMMEA Eligible: | No |

| Payment Structure: | Sequential Pay |

| Day Count: | 30/360 |

| Tax Structure: | REMIC |

| Rated Final Distribution Date: | February 2050 |

| Cleanup Call: | 1.0% |

| Minimum Denominations: | $10,000 minimum for the offered certificates (except with respect to the Class X-A, Class X-B and Class X-C certificates: $1,000,000 minimum); integral multiples of $1 thereafter for all the offered certificates |

| Delivery: | Book-entry through DTC |

| Bond Information: | Cash flows are expected to be modeled by TREPP, INTEX and BLOOMBERG |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-207132) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Deutsche Bank Securities Inc., Drexel Hamilton, LLC, or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

| 7 |

| TRANSACTION HIGHLIGHTS |

| ■ | $1,327,484,158 (Approximate) New-Issue Multi-Borrower CMBS: |

| — | Overview: The mortgage pool consists of 52 fixed-rate commercial mortgage loans that have an aggregate Cut-off Date Balance of $1,327,484,158 (the “Initial Pool Balance”), have an average mortgage loan Cut-off Date Balance of $25,528,542 and are secured by 59 mortgaged properties located throughout 25 states |

| — | LTV: 57.9% weighted average Cut-off Date LTV Ratio |

| — | DSCR: 1.95x weighted average Underwritten Debt Service Coverage Ratio |

| — | Debt Yield: 10.7% weighted average Debt Yield on Underwritten NOI |

| — | Credit Support:30.000% credit support to Class A-1 / A-2 / A-3 / A-4 / A-AB |

| ■ | Loan Structural Features: |

| — | Amortization:48.9% of the mortgage loans by Initial Pool Balance have scheduled amortization: |

| – | 21.8% of the mortgage loans by Initial Pool Balance have amortization for the entire term with a balloon payment due at maturity |

| – | 27.1 % of the mortgage loans by Initial Pool Balance have scheduled amortization following a partial interest only period with a balloon payment due at maturity |

| — | Hard Lockboxes:77.7% of the mortgage loans by Initial Pool Balance have a Hard Lockbox in place |

| — | Cash Traps: 100.0% of the mortgage loans by Initial Pool Balance have cash traps triggered by certain declines in cash flow, all at levels equal to or greater than a 1.15x coverage, that fund an excess cash flow reserve |

| — | Reserves: The mortgage loans require amounts to be escrowed for reserves as follows: |

| – | Real Estate Taxes: 43 mortgage loans representing 76.9% of the Initial Pool Balance |

| – | Insurance: 25 mortgage loans representing 36.0% of the Initial Pool Balance |

| – | Replacement Reserves (Including FF&E Reserves): 42 mortgage loans representing 79.4% of the Initial Pool Balance |

| – | Tenant Improvements / Leasing Commissions: 23 mortgage loans representing 72.0% of the portion of the Initial Pool Balance that is secured by retail, office, mixed use and industrial properties |

| — | Predominantly Defeasance Mortgage Loans: 86.6% of the mortgage loans by Initial Pool Balance permit defeasance only after an initial lockout period |

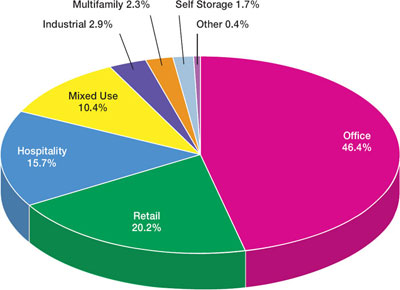

| ■ | Multiple-Asset Types > 5.0% of the Initial Pool Balance: |

| — | Office: 46.4% of the mortgaged properties by allocated Initial Pool Balance are office properties |

| — | Retail: 20.2% of the mortgaged properties by allocated Initial Pool Balance are retail properties (15.0% are anchored retail properties) |

| — | Hospitality:15.7% of the mortgaged properties by allocated Initial Pool Balance are hospitality properties |

| — | Mixed Use: 10.4% of the mortgaged properties by allocated Initial Pool Balance are mixed use properties |

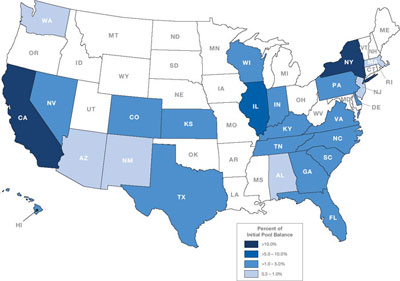

| ■ | Geographic Diversity:The 59 mortgaged properties are located throughout 25 states, with only two states having greater than 10.0% of the allocated Initial Pool Balance: New York (31.3%), and California (19.6%) |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-207132) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Deutsche Bank Securities Inc., Drexel Hamilton, LLC, or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

| 8 |

| COLLATERAL OVERVIEW |

Mortgage Loans by Loan Seller

| Mortgage Loan Seller | Mortgage Loans | Mortgaged Properties |

Aggregate Cut-off | % of Initial Pool Balance | ||||||||

| German American Capital Corporation | 23 | 27 | $641,199,782 | 48.3 | % | |||||||

| Citigroup Global Markets Realty Corp. | 27 | 30 | 519,284,377 | 39.1 | ||||||||

| German American Capital Corporation & Citigroup Global Markets Realty Corp.(1)(2) | 2 | 2 | 167,000,000 | 12.6 | ||||||||

| Total | 52 | 59 | $1,327,484,158 | 100.0 | % | |||||||

| (1) | The 229 West 43rd Street Retail Condo mortgage loan was originated by Deutsche Bank AG, New York Branch. Such mortgage loan is evidenced by four promissory notes: (i) notes A-4-B and A-5, with an aggregate outstanding principal balance of $50,000,000 as of the Cut-off Date, as to which Citigroup Global Markets Realty Corp. is acting as mortgage loan seller; and (ii) notes A-7 and A-8, with an aggregate outstanding principal balance of $50,000,000 as of the Cut-off Date, as to which German American Capital Corporation is acting as mortgage loan seller. |

| (2) | The 111 Livingston Street mortgage loan was co-originated by Citigroup Global Markets Realty Corp. and Deutsche Bank AG, New York Branch. Such mortgage loan is evidenced by two promissory notes: (i) note A-1, with an outstanding principal balance of $38,000,000 as of the Cut-off Date, as to which Citigroup Global Markets Realty Corp. is acting as mortgage loan seller; and (ii) note A-3, with an outstanding principal balance of $29,000,000 as of the Cut-off Date, as to which German American Capital Corporation is acting as mortgage loan seller. |

Ten Largest Mortgage Loans(1)(2)

# | Mortgage Loan Name | Cut-off Date Balance | % of Initial Pool Balance | Property Type | Property Size | Cut-off Date Balance Per SF / Rooms | UW NCF | UW | Cut-off Date LTV Ratio | ||||||||||||||||

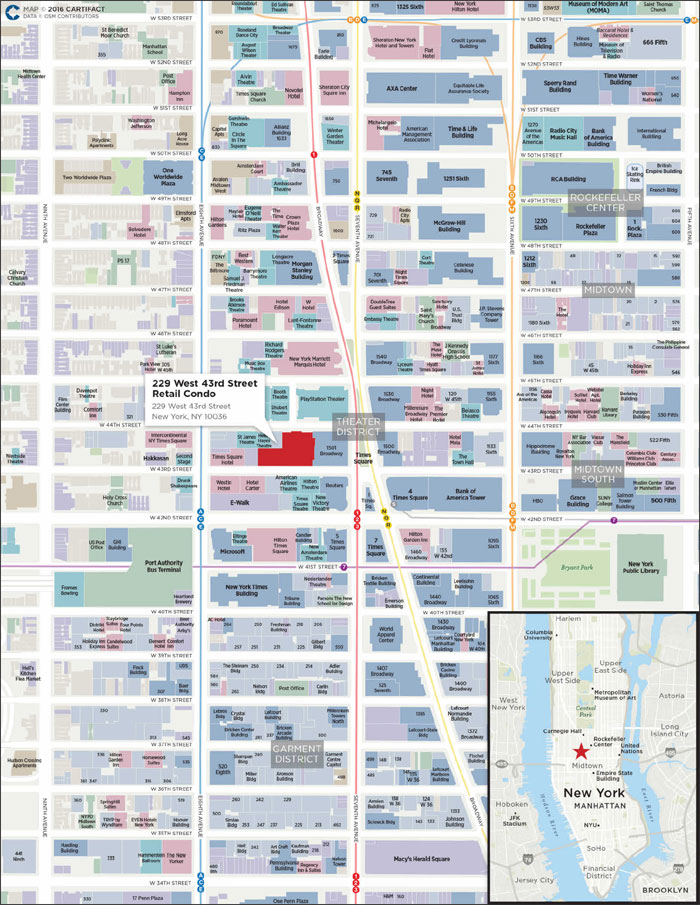

| 1 | 229 West 43rd Street Retail Condo | $100,000,000 | 7.5 | % | Retail | 248,457 | $1,147 | 1.75 | x | 7.5 | % | 60.6 | % | ||||||||||||

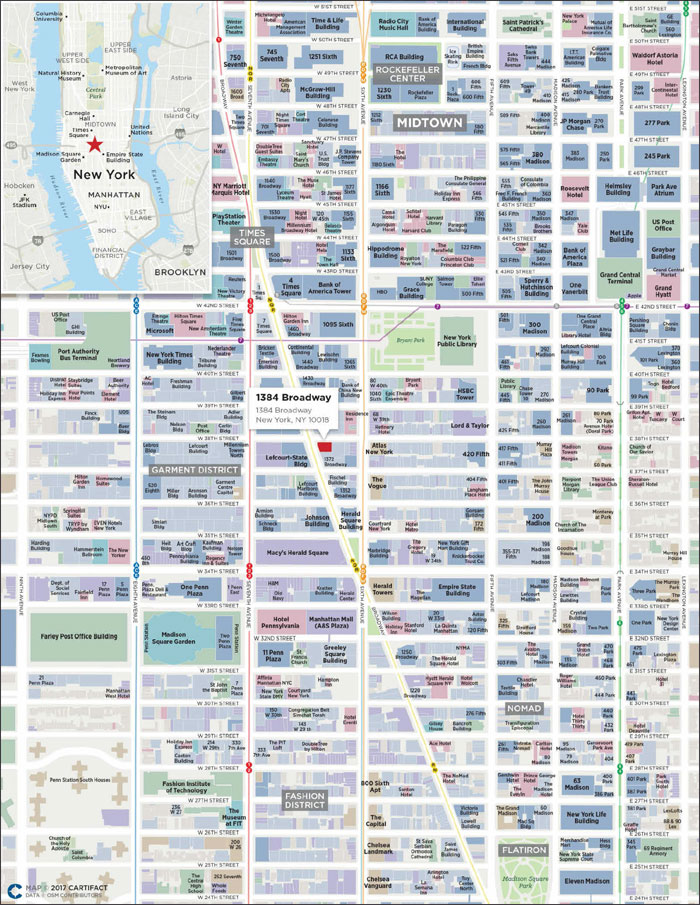

| 2 | 1384 Broadway | 88,000,000 | 6.6 | Office | 213,450 | $412 | 1.50 | x | 7.8 | % | 55.0 | % | |||||||||||||

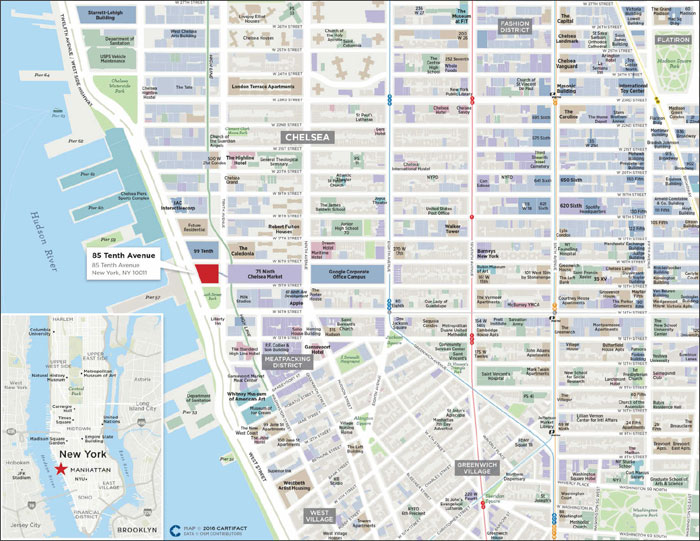

| 3 | 85 Tenth Avenue | 75,000,000 | 5.6 | Mixed Use | 632,584 | $403 | 3.66 | x | 14.5 | % | 30.5 | % | |||||||||||||

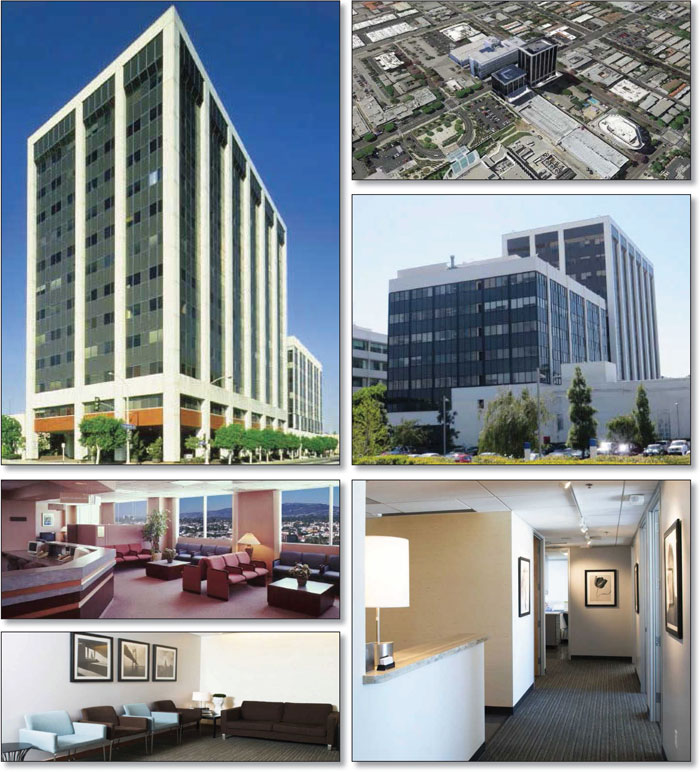

| 4 | Medical Centre of Santa Monica | 71,000,000 | 5.3 | Office | 204,414 | $347 | 3.04 | x | 13.3 | % | 47.3 | % | |||||||||||||

| 5 | Prudential Plaza | 70,000,000 | 5.3 | Office | 2,269,632 | $183 | 1.33 | x | 9.1 | % | 59.3 | % | |||||||||||||

| 6 | Moffett Place Google | 70,000,000 | 5.3 | Office | 314,352 | $589 | 1.38 | x | 8.3 | % | 59.5 | % | |||||||||||||

| 7 | 111 Livingston Street | 67,000,000 | 5.0 | Office | 434,000 | $277 | 1.56 | x | 8.1 | % | 54.8 | % | |||||||||||||

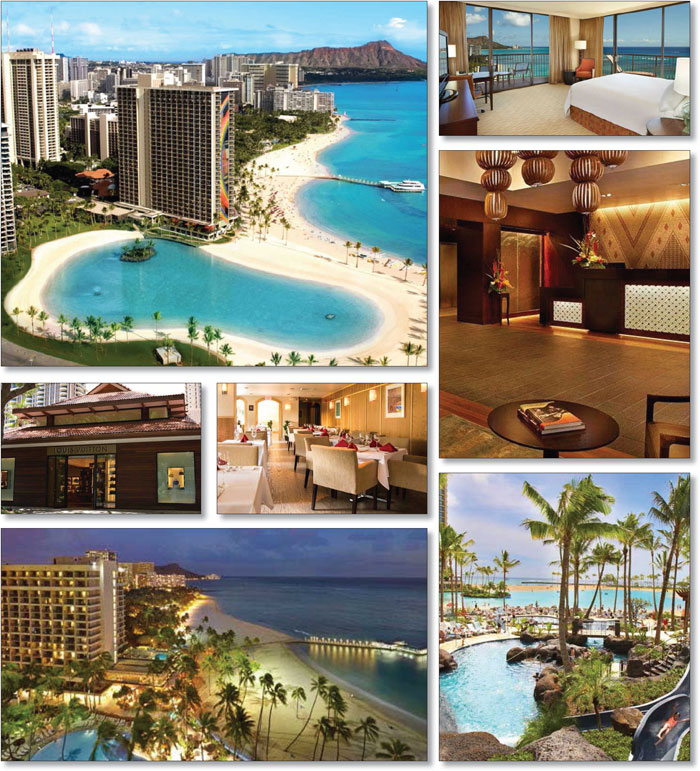

| 8 | Hilton Hawaiian Village Waikiki Beach Resort | 60,000,000 | 4.5 | Hospitality | 2,860 | $243,566 | 4.47 | x | 21.2 | % | 31.2 | % | |||||||||||||

| 9 | State Farm Data Center | 55,000,000 | 4.1 | Office | 193,953 | $412 | 2.42 | x | 11.4 | % | 62.5 | % | |||||||||||||

| 10 | Courtyard Century City | 40,839,616 | 3.1 | Hospitality | 136 | $300,291 | 2.17 | x | 13.9 | % | 62.9 | % | |||||||||||||

| Top 10 Total / Wtd. Avg. | $696,839,616 | 52.5 | % | 2.27 | x | 11.0 | % | 52.3 | % | ||||||||||||||||

| Remaining Total / Wtd. Avg. | 630,644,542 | 47.5 | 1.60 | x | 10.2 | % | 64.1 | % | |||||||||||||||||

| Total / Wtd. Avg. | $1,327,484,158 | 100.0 | % | 1.95 | x | 10.7 | % | 57.9 | % | ||||||||||||||||

| (1) | See footnotes to table entitled“Mortgage Pool Characteristics” above. |

| (2) | With respect to each mortgage loan that is part of a loan combination (as identified under “Collateral Overview—Loan Combination Summary” below), the UW NCF DSCR, UW NOI Debt Yield and Cut-off Date LTV Ratio are calculated based on both that mortgage loan and any related pari passu companion loan(s), but without regard to any related subordinate companion loan(s) or other indebtedness. With respect to the 85 Tenth Avenue mortgage loan, the mortgaged property is also encumbered by subordinate companion loans with an aggregate outstanding principal balance as of the Cut-off Date of $141,000,000. The UW NCF DSCR, UW NOI Debt Yield and Cut-off Date LTV Ratio for the 85 Tenth Avenue mortgage loan inclusive of the subordinate companion loans are 2.36x, 9.3% and 47.4% respectively. With respect to the Hilton Hawaiian Village Waikiki Beach Resort mortgage loan, the mortgaged property is also encumbered by subordinate companion loans with an aggregate outstanding principal balance as of the Cut-off Date of $578,400,000. The UW NCF DSCR, UW NOI Debt Yield and Cut-off Date LTV Ratio for the Hilton Hawaiian Village Waikiki Beach Resort mortgage loan inclusive of the subordinate companion loans are 2.44x, 11.6% and 57.2% respectively. |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-207132) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Deutsche Bank Securities Inc., Drexel Hamilton, LLC, or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

| 9 |

| COLLATERAL OVERVIEW (continued) |

Loan Combination Summary

Mortgaged Property Name(1) | Mortgage Loan Cut-off Date Balance | Mortgage Loan as Approx. % of Initial Pool Balance | Aggregate Pari Passu Companion Loan Cut-off Date Balance | Aggregate Subordinate Companion Loan Cut-off Date Balance | Loan Combination Cut-off Date Balance |

Controlling Pooling/Trust and Servicing Agreement (“Controlling PSA”)(2) | Master Servicer / Outside Servicer | Special Servicer / Outside Special Servicer | ||||||||||||

| 229 West 43rd Street Retail Condo | $100,000,000 | 7.5 | % | $185,000,000 | — | $285,000,000 | CD 2016-CD2 | Wells Fargo | KeyBank | |||||||||||

| 85 Tenth Avenue | $75,000,000 | 5.6 | % | $180,000,000 | $141,000,000 | $396,000,000 | DBWF 2016-85T | Wells Fargo | AEGON USA Realty | |||||||||||

| Prudential Plaza | $70,000,000 | 5.3 | % | $345,000,000 | — | $415,000,000 | COMM 2015-CCRE26 | Wells Fargo | CWCAM | |||||||||||

| Moffett Place Google | $70,000,000 | 5.3 | % | $115,000,000 | — | $185,000,000 | CD 2017-CD3 | Midland | Midland | |||||||||||

| 111 Livingston Street | $67,000,000 | 5.0 | % | $53,000,000 | — | $120,000,000 | CD 2017-CD3 | Midland | Midland | |||||||||||

| Hilton Hawaiian Village Waikiki Beach Resort | $60,000,000 | 4.5 | % | $636,600,000 | $578,400,000 | $1,275,000,000 | Hilton USA Trust 2016-HHV | Wells Fargo | AEGON USA Realty | |||||||||||

| State Farm Data Center | $55,000,000 | 4.1 | % | $25,000,000 | — | $80,000,000 | CD 2017-CD3 | Midland | Midland | |||||||||||

| Summit Place Wisconsin | $40,000,000 | 3.0 | % | $32,000,000 | — | $72,000,000 | CD 2017-CD3 | Midland | Midland | |||||||||||

| 681 Fifth Avenue | $28,500,000 | 2.1 | % | $186,500,000 | — | $215,000,000 | MSC 2016-UBS12 | Midland | Rialto | |||||||||||

| 8 Times Square & 1460 Broadway | $25,000,000 | 1.9 | % | $175,000,000 | — | $200,000,000 | CD 2016-CD2 | Wells Fargo | KeyBank | |||||||||||

| Marriott Hilton Head Resort & Spa | $14,903,575 | 1.1 | % | $82,466,449 | — | $97,370,024 | WFCM 2016-LC25 | Wells Fargo | CWCAM | |||||||||||

| Parts Consolidation Center | $12,750,000 | 1.0 | % | $10,000,000 | — | $22,750,000 | CD 2017-CD3 | Midland | Midland | |||||||||||

| (1) | Each of the mortgage loans included in the issuing entity that is secured by a mortgaged property identified in the table above, together with the related companion loan(s) (each of which is not included in the issuing entity), is referred to in this Term Sheet as a “loan combination”. See “Description of the Mortgage Pool—The Loan Combinations” in the Preliminary Prospectus. |

| (2) | Each loan combination will be serviced under the related Controlling PSA, and the controlling class representative (or an equivalent entity), if any, under the related Controlling PSA (or such other party as is designated under the related Controlling PSA and/or the related co-lender agreement) will be entitled to exercise the rights of controlling note holder for the subject loan combination. |

Mortgage Loans with Existing Mezzanine Debt(1)

Mortgaged Property Name | Mortgage Loan Cut-off Date Balance | Pari Passu Companion Loan Cut-off Date Balance | Subordinate Companion Loan Cut-off Date Balance | Mezzanine Debt Cut-off Date Balance | Cut-off Date Total Debt Balance | Wtd. Avg Cut-off Date Total Debt Interest Rate | Cut-off Date Mortgage Loan LTV | Cut-off Date Total Debt LTV | Cut-off Date Mortgage Loan UW NCF DSCR | Cut-off Date Total Debt UW NCF DSCR | ||||||||||||||||||

| 229 West 43rd Street Retail Condo | $100,000,000 | $185,000,000 | — | $85,000,000 | $370,000,000 | 4.90478 | % | 60.6 | % | 78.7 | % | 1.75 | x | 1.10 | x | |||||||||||||

| 85 Tenth Avenue(2) | $75,000,000 | $180,000,000 | $141,000,000 | $229,000,000 | $625,000,000 | 4.55001 | % | 30.5 | % | 74.9 | % | 3.66 | x | 1.26 | x | |||||||||||||

| Moffett Place Google | $70,000,000 | $115,000,000 | — | $40,000,000 | $225,000,000 | 4.89650 | % | 59.5 | % | 72.3 | % | 1.38 | x | 1.07 | x | |||||||||||||

| Key Vista Apartments | $6,826,000 | — | — | $1,124,000 | $7,950,000 | 6.53004 | % | 54.2 | % | 63.1 | % | 1.73 | x | 1.24 | x | |||||||||||||

| (1) | See footnotes to table entitled “Mortgage Pool Characteristics” above. |

| (2) | All “Total Debt” calculations set forth in the table above include the related subordinate companion loans and the related mezzanine debt. |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-207132) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Deutsche Bank Securities Inc., Drexel Hamilton, LLC, or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

| 10 |

| COLLATERAL OVERVIEW (continued) |

Loan Combination Controlling Notes and Non-Controlling Notes

Mortgaged Property Name / | Controlling | Current Holder of | Current or Anticipated Holder | Cut-off Date Balance |

| 229 West 43rd Street Retail Condo | ||||

| Notes A-1 and A-6 | Yes (Note A-1) | — | CD 2016-CD2 | $75,000,000 |

| Notes A-2 and A-3 | No | Deutsche Bank AG, New York Branch | Not identified | $80,000,000 |

| Note A-4-A | No | CGMRC | Not identified | $30,000,000 |

| Notes A-4-B and A-5 | No | CGMRC | CD 2017-CD3 | $50,000,000 |

| Notes A-7 and A-8 | No | Deutsche Bank AG, New York Branch | CD 2017-CD3 | $50,000,000 |

| 85 Tenth Avenue | ||||

| Notes A-1-S and A-2-S | (5) | — | DBWF 2016-85T | $130,000,000 |

| Notes A-1-C1 and A-1-C2 | No | Deutsche Bank AG, New York Branch | CD 2017-CD3 | $75,000,000 |

| Notes A-2-C1 and A-2-C2 | No | Wells Fargo Bank, National Association | Not identified | $50,000,000 |

| Notes B-1 and B-2 | (5) | — | DBWF 2016-85T | $141,000,000 |

| Prudential Plaza | ||||

| Note A-1 | Yes | — | COMM 2015-CCRE26 | $115,000,000 |

| Note A-2-1 | No | — | CD 2016-CD1 | $50,000,000 |

| Notes A-2-2 and A-3-3 | No | — | CD 2016-CD2 | $75,000,000 |

| Note A-3-1 | No | — | COMM 2016-COR1 | $40,000,000 |

| Notes A-3-2 and A-4-1 | No | Deutsche Bank AG, New York Branch | CD 2017-CD3 | $70,000,000 |

| Note A-4-2 | No | Deutsche Bank AG, New York Branch | Not identified | $65,000,000 |

| Moffett Place Google | ||||

| Notes A-1 and A-3 | Yes (Note A-1) | Deutsche Bank AG, New York Branch | CD 2017-CD3 | $70,000,000 |

| Notes A-2, A-4, A-5 and A-6 | No | Deutsche Bank AG, New York Branch | Not identified | $115,000,000 |

| 111 Livingston Street | ||||

| Note A-1 | Yes | CGMRC | CD 2017-CD3 | $38,000,000 |

| Note A-2 | No | CGMRC | Not identified | $29,000,000 |

| Note A-3 | No | Deutsche Bank AG, New York Branch | CD 2017-CD3 | $29,000,000 |

| Note A-4 | No | Deutsche Bank AG, New York Branch | Not identified | $24,000,000 |

| Hilton Hawaiian Village Waikiki Beach Resort | ||||

| Notes A-1-A, A-1-B, A-1-C, A-1-D and A-1-E | Yes (Note A-1-A) | — | Hilton USA Trust 2016-HHV | $171,600,000 |

| Note A-2-A-1 | No | — | JPMCC 2016-JP4 | $94,000,000 |

| Notes A-2-A-2, A-2-A-3 and A-2-A-4 | No | JPMorgan Chase Bank, National Association | Not identified | $142,250,000 |

| Note A-2-B-1 | No | Deutsche Bank, AG, New York Branch | CD 2017-CD3 | $60,000,000 |

| Note A-2-B-2 | No | Deutsche Bank, AG, New York Branch | Not identified | $56,625,000 |

| Note A-2-B-3 | No | — | CFCRE 2016-C7 | $56,625,000 |

| Notes A-2-D-1 and A-2-D-2 | No | — | MSBAM 2016-C32 | $63,000,000 |

| Notes A-2-E-1 and A-2-E-2 | No | — | WFCM 2016-C37 | $52,500,000 |

| Notes B-1, B-2, B-3, B-4 and B-5 | No | — | Hilton USA Trust 2016-HHV | $578,400,000 |

| State Farm Data Center | ||||

| Note A-1 | Yes | Deutsche Bank, AG, New York Branch | CD 2017-CD3 | $55,000,000 |

| Note A-2 | No | Deutsche Bank, AG, New York Branch | Not identified | $25,000,000 |

| Summit Place Wisconsin | ||||

| Note A-1 | Yes | Deutsche Bank, AG, New York Branch | CD 2017-CD3 | $40,000,000 |

| Note A-2 | No | Deutsche Bank, AG, New York Branch | Not identified | $32,000,000 |

| 681 Fifth Avenue | ||||

| Note A-1 | Yes | — | MSC 2016-UBS12 | $80,000,000 |

| Notes A-2 and A-4 | No | — | CFCRE 2016-C7 | $34,000,000 |

| Note A-3 | No | — | CSMC 2016-NXSR | $15,000,000 |

| Note A-5 | No | — | CGCMT 2016-P6 | $57,500,000 |

| Note A-6 | No | CGMRC | CD 2017-CD3 | $28,500,000 |

| 8 Times Square & 1460 Broadway | ||||

| Note A-1 | Yes | — | CD 2016-CD2 | $100,000,000 |

| Note A-2-1 | No | — | CGCMT 2016-P6 | $75,000,000 |

| Note A-2-2 | No | CGMRC | CD 2017-CD3 | $25,000,000 |

| Marriott Hilton Head Resort & Spa | ||||

| Note A-1 | Yes | — | WFCM 2016-LC25 | $42,723,582 |

| Note A-2A | No | CGMRC | CD 2017-CD3 | $4,967,858 |

| Notes A-2B and A-4 | No | — | CGCMT 2016-C3 | $29,807,150 |

| Note A-3A | No | — | CD 2016-CD2 | $9,935,717 |

| Note A-3B | No | CGMRC | CD 2017-CD3 | $9,935,717 |

| Parts Consolidation Center | ||||

| Note A-1 | Yes | CGMRC | CD 2017-CD3 | $12,750,000 |

| Note A-2 | No | CGMRC | Not identified | $10,000,000 |

| (1) | The holder(s) of one or more specified controlling notes (collectively, the “Controlling Note“) will be entitled (directly or through a representative) to (a) approve or, in some cases, direct material servicing decisions involving the related loan combination (while the remaining such holder(s) generally are only entitled to non-binding consultation rights in such regard), and (b) in some cases, replace the applicable special servicer with respect to such loan combination with or without cause. See “Description of the Mortgage Pool—The Loan Combinations” and “The Pooling and Servicing Agreement—Directing Holder” in the Preliminary Prospectus. |

| (2) | The holder(s) of the note(s) other than the Controlling Note (each, a “Non-Controlling Note”) will be generally entitled (directly or through a representative) to certain non-binding consultation rights with respect to any decisions as to which the holder of the Controlling Note has consent rights involving the related loan combination, subject to certain exceptions, including that in certain cases such consultation rights will not be afforded to the holder(s) of the Non-Controlling Notes until after a control trigger event has occurred with respect to either the Control Note or certain certificates backed thereby, in each case as set forth in the related co-lender agreement. See “Description of the Mortgage Pool—The Loan Combinations“ in the Preliminary Prospectus. |

| (3) | Unless otherwise specified, with respect to each loan combination, any related unsecuritized Controlling Note and/or Non-Controlling Note may be further split, modified, combined and/or reissued (prior to its inclusion in a securitization transaction) as one or multiple Controlling Notes or Non-Controlling Notes, as the case may be, subject to the terms of the related co-lender agreement (including that the aggregate principal balance, weighted average interest rate and certain other material terms cannot be changed). In connection with the foregoing, any such split, modified or combined Controlling Note or Non-Controlling Note, as the case may be, may be transferred to one or multiple parties (not identified in the table above) prior to its inclusion in a future commercial mortgage securitization transaction. |

| (4) | Unless otherwise specified, with respect to each loan combination, each related unsecuritized pari passu Companion Note (both controlling and non-controlling) is expected to be contributed to one or more future commercial mortgage securitization transactions. Under the column “Current or Anticipated Holder of Securitized Note”, (i) the identification of a securitization trust means we have identified an outside securitization that has closed or as to which a preliminary prospectus or final prospectus has printed that has or is expected to include the subject Controlling Note or Non-Controlling Note, as the case may be, (ii) “Not identified” means no preliminary prospectus or final prospectus has printed that identifies the future outside securitization that is expected to include the subject Controlling Note or Non-Controlling Note, and (iii) “Not applicable” means the subject Controlling Note or Non-Controlling Note is not intended to be contributed to a future commercial mortgage securitization transaction. Under the column “Current Holder of Unsecuritized Note”, “—“ means the subjectControlling Note or Non-Controlling Note is not an unsecuritized note and is currently held by the securitization trust referenced under the “Current or Anticipated Holder of Securitized Note” column. |

| (5) | With respect to the 85 Tenth Avenue loan combination, under the related co-lender agreement, the DBWF 2016-85T Mortgage Trust is the designated “controlling holder”, but there is no “controlling class” or “directing holder” under the related outside servicing agreement. See “Description of the Mortgage Pool—The Loan Combinations—The 85 Tenth Avenue Loan Combination—Consultation and Control” in the Preliminary Prospectus. |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-207132) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Deutsche Bank Securities Inc., Drexel Hamilton, LLC, or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

| 11 |

| COLLATERAL OVERVIEW (continued) |

Previously Securitized Mortgaged Properties(1)

Mortgaged Property Name | Mortgage Loan Seller | City | State | Property |

Cut-off Date | % of | Previous Securitization | |||||||

| 1384 Broadway | CGMRC | New York | New York | Office | $88,000,000 | 6.6% | WBCMT 2007-C30 | |||||||

| 85 Tenth Avenue | GACC | New York | New York | Mixed Use | $75,000,000 | 5.6% | COMM 2007-C9; CD 2007-CD5 | |||||||

| Medical Centre of Santa Monica - West | CGMRC | Santa Monica | California | Office | $48,329,400 | 3.6% | MLCFC 2007-5 | |||||||

| Medical Centre of Santa Monica - East | CGMRC | Santa Monica | California | Office | $22,670,600 | 1.7% | MLCFC 2007-5 | |||||||

| Prudential Plaza | GACC | Chicago | Illinois | Office | $70,000,000 | 5.3% | JPMCC 2006-LDP7; JPMCC 2006-CB16 | |||||||

| 111 Livingston Street | CGMRC, GACC | Brooklyn | New York | Office | $67,00,000 | 5.0% | GECMC 2007-C1 | |||||||

| Hilton Hawaiian Village Waikiki Beach Resort | GACC | Honolulu | Hawaii | Hospitality | $60,000,000 | 4.5% | Hilton 2013-HLT: Hilton Portfolio; Hilton 2013-HLF:Hilton Portfolio | |||||||

| Courtyard Century City | GACC | Los Angeles | California | Hospitality | $40,839,616 | 3.1% | CGCMT 2006-C5 | |||||||

| Silverado Ranch | CGMRC | Las Vegas | Nevada | Retail | $40,000,000 | 3.0% | JPMCC 2007-LDPX | |||||||

| Summit Place Wisconsin | GACC | West Allis | Wisconsin | Office | $40,000,000 | 3.0% | BSCMS 2007-PW15 | |||||||

| 16 E 40th Street | GACC | New York | New York | Office | $31,500,000 | 2.4% | JPMCC 2006-LDP9 | |||||||

| 681 Fifth Avenue | CGMRC | New York | New York | Mixed Use | $28,500,000 | 2.1% | DBUBS 2011-LC1A | |||||||

| 166 Geary Street | CGMRC | San Francisco | California | Retail | $28,500,000 | 2.1% | LMRET 2006-1A | |||||||

| Residence Inn - Chattanooga | GACC | Chattanooga | Tennessee | Hospitality | $13,863,205 | 1.0% | JPMCC 2011-C3 | |||||||

| Marriott Hilton Head Resort & Spa | CGMRC | Hilton Head Island | South Carolina | Hospitality | $14,903,575 | 1.1% | JPMCC 2007-CB18 | |||||||

| Parts Consolidation Center | CGMRC | Vance | Alabama | Industrial | $12,750,000 | 1.0% | WFCM 2014-LC16 | |||||||

| Olivewood Plaza | GACC | Lindsay | California | Retail | $9,050,000 | 0.7% | MLCFC 2006-3 | |||||||

| Kingsville Pointe Apartments | CGMRC | Kingsville | Texas | Multifamily | $8,625,000 | 0.6% | FNA 2014-M13 | |||||||

| Hampton Inn & Suites Surprise | CGMRC | Surprise | Arizona | Hospitality | $7,277,095 | 0.5% | MSC 2007-IQ15 | |||||||

| Orangecrest Self Storage | CGMRC | Riverside | California | Self Storage | $5,743,524 | 0.4% | CD 2007-CD4 | |||||||

| 180 Main Avenue | GACC | Clifton | New Jersey | Other | $5,300,000 | 0.4% | BSCMS 2007-PW15 | |||||||

| Walgreens Dorchester | CGMRC | Dorchester | Massachusetts | Retail | $3,375,000 | 0.3% | WBCMT 2004-C12 | |||||||

| Walgreens Walterboro | CGMRC | Walterboro | South Carolina | Retail | $3,300,000 | 0.2% | WBCMT 2007-C33 |

| (1) | The table above includes mortgaged properties securing mortgage loans for which the most recent prior financing of all or a significant portion of such mortgaged property was included in a securitization. Information under “Previous Securitization” represents the most recent such securitization with respect to each of those mortgaged properties. The information in the above table is based solely on information provided by the related borrower or obtained through searches of a third-party database, and has not otherwise been confirmed by the mortgage loan sellers. |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-207132) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Deutsche Bank Securities Inc., Drexel Hamilton, LLC, or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

| 12 |

| COLLATERAL OVERVIEW (continued) |

Property Types

Property Type / Detail | Number of Mortgaged Properties | Aggregate | % of Initial | Wtd. Avg. | Wtd. Avg. Cut-off | Wtd. Avg. | |||||

| Office | 17 | $615,731,616 | 46.4% | 1.73x | 59.0% | 9.7% | |||||

| CBD | 5 | 326,500,000 | 24.6 | 1.48x | 56.5% | 8.3% | |||||

| Suburban | 9 | 163,231,616 | 12.3 | 1.43x | 68.0% | 10.4% | |||||

| Medical Office | 2 | 71,000,000 | 5.3 | 3.04x | 47.3% | 13.3% | |||||

| Data Center | 1 | 55,000,000 | 4.1 | 2.42x | 62.5% | 11.4% | |||||

| Retail | 15 | $267,863,746 | 20.2% | 1.66x | 63.2% | 8.5% | |||||

| Anchored | 7 | 199,690,442 | 15.0 | 1.69x | 63.8% | 8.6% | |||||

| Unanchored | 3 | 36,987,281 | 2.8 | 1.51x | 63.1% | 8.1% | |||||

| Shadow Anchored | 1 | 16,000,000 | 1.2 | 1.76x | 53.3% | 7.9% | |||||

| Single Tenant | 4 | 15,186,023 | 1.1 | 1.42x | 65.4% | 9.4% | |||||

| Hospitality | 13 | $208,875,627 | 15.7% | 2.67x | 55.3% | 16.0% | |||||

| Limited Service | 7 | 95,326,351 | 7.2 | 1.98x | 64.4% | 13.9% | |||||

| Full Service | 2 | 74,903,575 | 5.6 | 3.87x | 36.9% | 19.4% | |||||

| Extended Stay | 3 | 28,200,344 | 2.1 | 2.06x | 70.9% | 14.0% | |||||

| Select Service | 1 | 10,445,357 | 0.8 | 1.94x | 62.5% | 15.0% | |||||

| Mixed Use | 4 | $137,486,755 | 10.4% | 2.74x | 40.9% | 11.4% | |||||

| Office/Retail/Storage | 1 | 75,000,000 | 5.6 | 3.66x | 30.5% | 14.5% | |||||

| Office/Retail | 2 | 53,500,000 | 4.0 | 1.69x | 52.0% | 7.3% | |||||

| Flex/Office | 1 | 8,986,755 | 0.7 | 1.25x | 60.7% | 9.9% | |||||

| Industrial | 3 | $39,045,000 | 2.9% | 1.67x | 66.8% | 10.7% | |||||

| Warehouse/Distribution | 2 | 34,970,000 | 2.6 | 1.60x | 68.3% | 10.6% | |||||

| Flex | 1 | 4,075,000 | 0.3 | 2.21x | 53.7% | 11.5% | |||||

| Multifamily (Garden) | 3 | $30,451,000 | 2.3% | 1.38x | 69.3% | 10.0% | |||||

| Self Storage | 3 | $22,730,414 | 1.7% | 1.41x | 60.9% | 9.4% | |||||

| Other (Leased Fee) | 1 | $5,300,000 | 0.4% | 2.03x | 60.9% | 9.9% | |||||

| Total | 59 | $1,327,484,158 | 100% | 1.95x | 57.9% | 10.7% |

| (1) | Calculated based on the mortgaged property’s allocated loan amount for mortgage loans secured by more than one mortgaged property. |

| (2) | Weighted average based on the mortgaged property’s allocated loan amount for mortgage loans secured by more than one mortgaged property. |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-207132) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Deutsche Bank Securities Inc., Drexel Hamilton, LLC, or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

| 13 |

| COLLATERAL OVERVIEW (continued) |

Geographic Distribution

Property Location | Number of | Aggregate | % of Initial | Aggregate | % of Total | Underwritten | % of Total | |||||||

| New York | 7 | $415,000,000 | 31.3% | $2,545,000,000 | 35.6% | $108,202,258 | 26.7% | |||||||

| California | 10 | 260,586,662 | 19.6 | 656,639,999 | 9.2 | 37,585,002 | 9.3 | |||||||

| Illinois | 2 | 74,450,000 | 5.6 | 706,530,000 | 9.9 | 37,977,476 | 9.4 | |||||||

| Hawaii | 1 | 60,000,000 | 4.5 | 2,230,000,000 | 31.2 | 147,564,484 | 36.5 | |||||||

| Kansas | 1 | 55,000,000 | 4.1 | 128,000,000 | 1.8 | 9,133,746 | 2.3 | |||||||

| Colorado | 4 | 52,079,929 | 3.9 | 82,250,000 | 1.1 | 5,412,181 | 1.3 | |||||||

| Wisconsin | 1 | 40,000,000 | 3.0 | 99,000,000 | 1.4 | 6,983,106 | 1.7 | |||||||

| Nevada | 1 | 40,000,000 | 3.0 | 60,000,000 | 0.8 | 3,588,503 | 0.9 | |||||||

| Texas | 4 | 32,490,183 | 2.4 | 46,970,000 | 0.7 | 3,090,157 | 0.8 | |||||||

| Indiana | 3 | 32,333,556 | 2.4 | 48,000,000 | 0.7 | 4,195,808 | 1.0 | |||||||

| Georgia | 2 | 31,110,442 | 2.3 | 43,700,000 | 0.6 | 3,141,604 | 0.8 | |||||||

| Virginia | 1 | 29,670,000 | 2.2 | 46,600,000 | 0.7 | 3,024,953 | 0.7 | |||||||

| Florida | 4 | 28,777,543 | 2.2 | 44,700,000 | 0.6 | 3,995,316 | 1.0 | |||||||

| Pennsylvania | 2 | 26,695,357 | 2.0 | 41,700,000 | 0.6 | 3,564,848 | 0.9 | |||||||

| Delaware | 1 | 26,223,908 | 2.0 | 35,200,000 | 0.5 | 2,837,832 | 0.7 | |||||||

| Tennessee | 2 | 21,124,883 | 1.6 | 29,500,000 | 0.4 | 3,020,852 | 0.7 | |||||||

| North Carolina | 1 | 21,000,000 | 1.6 | 30,000,000 | 0.4 | 1,847,189 | 0.5 | |||||||

| South Carolina | 2 | 18,203,575 | 1.4 | 168,700,000 | 2.4 | 12,000,925 | 3.0 | |||||||

| Kentucky | 1 | 15,000,000 | 1.1 | 20,250,000 | 0.3 | 1,399,753 | 0.3 | |||||||

| Alabama | 1 | 12,750,000 | 1.0 | 36,000,000 | 0.5 | 2,427,087 | 0.6 | |||||||

| New Jersey | 2 | 9,300,000 | 0.7 | 14,500,000 | 0.2 | 857,809 | 0.2 | |||||||

| Massachusetts | 2 | 7,436,023 | 0.6 | 11,520,000 | 0.2 | 700,120 | 0.2 | |||||||

| Arizona | 1 | 7,277,095 | 0.5 | 13,400,000 | 0.2 | 1,119,122 | 0.3 | |||||||

| Washington | 2 | 6,475,000 | 0.5 | 12,060,000 | 0.2 | 747,542 | 0.2 | |||||||

| New Mexico | 1 | 4,500,000 | 0.3 | 7,000,000 | 0.1 | 375,180 | 0.1 | |||||||

| Total | 59 | $1,327,484,158 | 100.0% | $7,157,219,999 | 100.0% | $404,792,853 | 100.0% |

| (1) | Calculated based on the mortgaged property’s allocated loan amount for mortgage loans secured by more than one mortgaged property. |

| (2) | Aggregate Appraised Values and Underwritten NOI reflect the aggregate values without any reduction for thepari passu companion loan(s). |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-207132) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Deutsche Bank Securities Inc., Drexel Hamilton, LLC, or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

| 14 |

| COLLATERAL OVERVIEW (continued) |

| Distribution of Cut-off Date Balances | |||||||||||

| Range of Cut-off Date Balances ($) | Number of Mortgage Loans | Cut-off Date Balance | % of Initial Pool Balance | ||||||||

| 3,300,000- 4,999,999 | 6 | $23,686,023 | 1.8 | % | |||||||

| 5,000,000 - 9,999,999 | 14 | 100,606,343 | 7.6 | ||||||||

| 10,000,000 - 19,999,999 | 9 | 122,041,669 | 9.2 | ||||||||

| 20,000,000 - 29,999,999 | 8 | 208,510,241 | 15.7 | ||||||||

| 30,000,000 - 39,999,999 | 3 | 95,800,267 | 7.2 | ||||||||

| 40,000,000 - 49,999,999 | 3 | 120,839,616 | 9.1 | ||||||||

| 50,000,000 - 59,999,999 | 1 | 55,000,000 | 4.1 | ||||||||

| 60,000,000 - 100,000,000 | 8 | 601,000,000 | 45.3 | ||||||||

| Total | 52 | $1,327,484,158 | 100.0 | % | |||||||

| Distribution of UW NCF DSCRs(1) | |||||||||||

| Range of UW DSCR (x) | Number of Mortgage Loans | Cut-off Date Balance | % of Initial Pool Balance | ||||||||

| 1.25 - 1.35 | 9 | $191,477,072 | 14.4 | % | |||||||

| 1.36 - 1.50 | 15 | 364,233,171 | 27.4 | ||||||||

| 1.51 - 1.65 | 6 | 128,442,478 | 9.7 | ||||||||

| 1.66 - 1.80 | 8 | 227,153,081 | 17.1 | ||||||||

| 1.81 - 2.00 | 4 | 53,722,452 | 4.0 | ||||||||

| 2.01 - 3.00 | 7 | 156,455,904 | 11.8 | ||||||||

| 3.01 - 4.47 | 3 | 206,000,000 | 15.5 | ||||||||

| Total | 52 | $1,327,484,158 | 100.0 | % | |||||||

| (1) See footnotes (1) and (6) to the table entitled “Mortgage Pool Characteristics” above. | |||||||||||

| Distribution of Amortization Types(1) | |||||||||||

| Amortization Type | Number of Mortgage Loans | Cut-off Date Balance | % of Initial Pool Balance | ||||||||

| Interest Only | 15 | $623,025,000 | 46.9 | % | |||||||

| Interest Only, Then Amortizing(2) | 16 | 360,266,000 | 27.1 | ||||||||

| Amortizing (30 Years) | 14 | 230,628,605 | 17.4 | ||||||||

| Interest Only — ARD | 1 | 55,000,000 | 4.1 | ||||||||

| Amortizing (25 Years) | 5 | 52,097,922 | 3.9 | ||||||||

| Amortizing (20 Years) | 1 | 6,466,631 | 0.5 | ||||||||

| Total | 52 | $1,327,484,158 | 100.0 | % | |||||||

(1) All of the mortgage loans will have balloon payments at maturity date or anticipated repayment date. (2) Original partial interest only periods range from 12 to 60 months. | |||||||||||

| Distribution of Lockboxes | |||||||||||

| Lockbox Type | Number of Mortgage Loans | Cut-off Date Balance | % of Initial Pool Balance | ||||||||

| Hard | 31 | $1,031,761,710 | 77.7 | % | |||||||

| Springing | 18 | 265,105,302 | 20.0 | ||||||||

| Soft | 2 | 21,826,000 | 1.6 | ||||||||

| Soft Springing | 1 | 8,791,147 | 0.7 | ||||||||

| Total | 52 | $1,327,484,158 | 100.0 | % | |||||||

| Distribution of Cut-off Date LTV Ratios(1) | |||||||||||

| Range of Cut-off Date LTV (%) | Number of Mortgage Loans | Cut-off Date Balance | % of Initial Pool Balance | ||||||||

| 30.5 - 50.0 | 4 | $234,500,000 | 17.7 | % | |||||||

| 50.1 - 55.0 | 8 | 228,821,619 | 17.2 | ||||||||

| 55.1 - 60.0 | 4 | 179,903,575 | 13.6 | ||||||||

| 60.1 - 65.0 | 21 | 409,882,154 | 30.9 | ||||||||

| 65.1 - 74.5 | 15 | 274,376,810 | 20.7 | ||||||||

| Total | 52 | $1,327,484,158 | 100.0 | % | |||||||

| (1) See footnotes (1) and (5) to the table entitled “Mortgage Pool Characteristics” above. | |||||||||||

| Distribution of Maturity Date/ARD LTV Ratios(1) | |||||||||||

| Range of Maturity Date/ARD LTV (%) | Number of Mortgage Loans | Cut-off Date Balance | % of Initial Pool Balance | ||||||||

| 30.5 - 50.0 | 11 | $298,808,077 | 22.5 | % | |||||||

| 50.1 - 55.0 | 15 | 468,070,903 | 35.3 | ||||||||

| 55.1 - 60.0 | 12 | 173,536,270 | 13.1 | ||||||||

| 60.1 - 65.0 | 13 | 372,068,908 | 28.0 | ||||||||

| 65.1 – 69.8 | 1 | 15,000,000 | 1.1 | ||||||||

| Total | 52 | $1,327,484,158 | 100.0 | % | |||||||

| (1) See footnotes (1), (3) and (5) to the table entitled “Mortgage Pool Characteristics” above. | |||||||||||

| Distribution of Loan Purpose | |||||||||||

| Loan Purpose | Number of Mortgage Loans | Cut-off Date Balance | % of Initial Pool Balance | ||||||||

| Refinance | 30 | $1,000,335,725 | 75.4 | % | |||||||

| Acquisition | 21 | 272,148,434 | 20.5 | ||||||||

| Acquisition/Refinance | 1 | 55,000,000 | 4.1 | ||||||||

| Total | 52 | $1,327,484,158 | 100.0 | % | |||||||

| Distribution of Mortgage Rates | |||||||||||

| Range of Mortgage Rates (%) | Number of Mortgage Loans | Cut-off Date Balance | % of Initial Pool Balance | ||||||||

| 3.821 - 4.000 | 2 | $91,250,000 | 6.9% | ||||||||

| 4.001 - 4.500 | 13 | 430,538,380 | 32.4 | ||||||||

| 4.501 - 5.000 | 21 | 600,513,436 | 45.2 | ||||||||

| 5.001 - 5.550 | 16 | 205,182,342 | 15.5 | ||||||||

| Total | 52 | $1,327,484,158 | 100.0 | % | |||||||

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-207132) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Deutsche Bank Securities Inc., Drexel Hamilton, LLC, or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

| 15 |

| COLLATERAL OVERVIEW (continued) |

| Distribution of Debt Yield on Underwritten NOI(1) | |||||||||||

| Range of Debt Yields on Underwritten NOI (%) | Number of Mortgage Loans | Cut-off Date Balance | % of Initial Pool Balance | ||||||||

| 7.3 - 7.9 | 6 | $286,000,000 | 21.5 | % | |||||||

| 8.0 - 8.9 | 7 | 215,877,332 | 16.3 | ||||||||

| 9.0 - 9.9 | 14 | 220,077,570 | 16.6 | ||||||||

| 10.0 - 10.9 | 7 | 137,365,290 | 10.3 | ||||||||

| 11.0 - 11.9 | 4 | 83,745,707 | 6.3 | ||||||||

| 12.0 - 12.9 | 3 | 37,979,575 | 2.9 | ||||||||

| 13.0 - 21.2 | 11 | 346,438,683 | 26.1 | ||||||||

| Total | 52 | $1,327,484,158 | 100.0 | % | |||||||

| (1) See footnotes (1) and (7) to the table entitled “Mortgage Pool Characteristics” above. | |||||||||||

| Distribution of Debt Yield on Underwritten NCF(1) | |||||||||||

| Range of Debt Yields on Underwritten NCF (%) | Number of Mortgage Loans | Cut-off Date Balance | % of Initial Pool Balance | ||||||||

| 7.0 - 7.9 | 7 | $353,000,000 | 26.6 | % | |||||||

| 8.0 - 8.9 | 15 | 348,723,271 | 26.3 | ||||||||

| 9.0 - 9.9 | 11 | 152,324,104 | 11.5 | ||||||||

| 10.0 - 10.9 | 5 | 48,922,100 | 3.7 | ||||||||

| 11.0 - 11.9 | 4 | 110,409,556 | 8.3 | ||||||||

| 12.0 - 12.9 | 4 | 128,791,387 | 9.7 | ||||||||

| 13.0 - 19.0 | 6 | 185,313,740 | 14.0 | ||||||||

| Total | 52 | $1,327,484,158 | 100.0 | % | |||||||

| (1) See footnotes (1) and (7) to the table entitled “Mortgage Pool Characteristics” above. | |||||||||||

| Mortgage Loans with Original Partial Interest Only Periods | |||||||||||

| Original Partial Interest Only Period (months) | Number of Mortgage Loans | Cut-off Date Balance | % of Initial Pool Balance | ||||||||

| 12 | 2 | $23,625,000 | 1.8 | % | |||||||

| 18 | 1 | $6,826,000 | 0.5 | % | |||||||

| 24 | 2 | $26,220,000 | 2.0 | % | |||||||

| 36 | 5 | $63,875,000 | 4.8 | % | |||||||

| 48 | 1 | $70,000,000 | 5.3 | % | |||||||

| 60 | 5 | $169,720,000 | 12.8 | % | |||||||

| Distribution of Original Terms to Maturity/ARD(1) | |||||||||||

| Original Term to Maturity/ARD (months) | Number of Mortgage Loans | Cut-off Date Balance | % of Initial Pool Balance | ||||||||

| 60 | 3 | $38,076,000 | 2.9 | % | |||||||

| 120 | 49 | 1,289,408,158 | 97.1 | ||||||||

| Total | 52 | $1,327,484,158 | 100.0 | % | |||||||

| (1) See footnote (3) to the table entitled “Mortgage Pool Characteristics” above. | |||||||||||

| Distribution of Remaining Terms to Maturity/ARD(1) | |||||||||||

| Range of Remaining Terms to Maturity/ARD (months) | Number of Mortgage Loans | Cut-off Date Balance | % of Initial Pool Balance | ||||||||

| 56 - 58 | 3 | $38,076,000 | 2.9 | % | |||||||

| 102 | 1 | 70,000,000 | 5.3 | ||||||||

| 116 - 120 | 48 | 1,219,408,158 | 91.9 | ||||||||

| Total | 52 | $1,327,484,158 | 100.0 | % | |||||||

(1) See footnote (3) to the table entitled “Mortgage Pool Characteristics” above.

| |||||||||||

| Distribution of Original Amortization Terms(1) | |||||||||||

| Original Amortization Term (months) | Number of Mortgage Loans | Cut-off Date Balance | % of Initial Pool Balance | ||||||||

| Interest Only | 16 | $678,025,000 | 51.1 | % | |||||||

| 240 | 1 | 6,466,631 | 0.5 | ||||||||

| 300 | 5 | 52,097,922 | 3.9 | ||||||||

| 360 | 30 | 590,864,605 | 44.5 | ||||||||

| Total | 52 | $1,327,484,158 | 100.0 | % | |||||||

| (1) All of the mortgage loans will have balloon payments at maturity or have an anticipated repayment date. | |||||||||||

| Distribution of Remaining Amortization Terms(1) | |||||||||||

| Range of Remaining Amortization Terms (months) | Number of Mortgage Loans | Cut-off Date Balance | % of Initial Pool Balance | ||||||||

| Interest Only | 16 | $678,025,000 | 51.1 | % | |||||||

| 238 | 1 | 6,466,631 | 0.5 | ||||||||

| 296 - 299 | 5 | 52,097,922 | 3.9 | ||||||||

| 357 - 360 | 30 | 590,894,605 | 44.5 | ||||||||

| Total | 52 | $1,327,484,158 | 100.0 | % | |||||||

| (1) All of the mortgage loans will have balloon payments at maturity or have an anticipated repayment date. | |||||||||||

| Distribution of Prepayment Provisions | |||||||||||

| Prepayment Provision | Number of Mortgage Loans | Cut-off Date Balance | % of Initial Pool Balance | ||||||||

| Defeasance | 46 | $1,090,202,268 | 82.1 | % | |||||||

| Yield Maintenance | 5 | 177,281,890 | 13.4 | ||||||||

| Defeasance or Yield Maintenance | 1 | 60,000,000 | 4.5 | ||||||||

| Total | 52 | $1,327,484,158 | 100.0 | % | |||||||

| Distribution of Escrow Types | |||||||||||

| Escrow Type | Number of Mortgage Loans | Cut-off Date Balance | % of Initial Pool Balance | ||||||||

| Replacement Reserves(1) | 42 | $1,053,881,803 | 79.4 | % | |||||||

| Real Estate Tax | 43 | $1,020,339,158 | 76.9 | % | |||||||

| TI/LC(2) | 23 | $763,746,094 | 72.0 | % | |||||||

| Insurance | 25 | $477,509,739 | 36.0 | % | |||||||