| FREE WRITING PROSPECTUS | ||

| FILED PURSUANT TO RULE 433 | ||

| REGISTRATION FILE NO.: 333-207132-16 | ||

February 28, 2018

Free Writing Prospectus

Structural and Collateral Term Sheet

$1,062,384,703

(Approximate Initial Mortgage Pool Balance)

$880,584,000

(Offered Certificates)

Citigroup Commercial Mortgage Trust 2018-B2

As Issuing Entity

Citigroup Commercial Mortgage Securities Inc.

As Depositor

Commercial Mortgage Pass-Through Certificates, Series 2018-B2

Morgan Stanley Mortgage Capital Holdings LLC

Citi Real Estate Funding Inc.

Starwood Mortgage Funding V LLC

Bank of America, National Association

As Sponsors and Mortgage Loan Sellers

STATEMENT REGARDING THIS FREE WRITING PROSPECTUS

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-207132) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Morgan Stanley & Co. LLC, Merrill Lynch, Pierce, Fenner & Smith Incorporated, Drexel Hamilton, LLC, The Williams Capital Group, L.P. or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

IMPORTANT NOTICE RELATING TO AUTOMATICALLY GENERATED EMAIL DISCLAIMERS

Any legends, disclaimers or other notices that may appear at the bottom of the email communication to which this free writing prospectus is attached relating to (1) these materials not constituting an offer (or a solicitation of an offer), (2) no representation being made that these materials are accurate or complete and that these materials may not be updated or (3) these materials possibly being confidential, are, in each case, not applicable to these materials and should be disregarded. Such legends, disclaimers or other notices have been automatically generated as a result of these materials having been sent via Bloomberg or another system.

| Citigroup | BofA Merrill Lynch | Morgan Stanley | |

| Co-Lead Managers and Joint Bookrunners | |||

| Drexel Hamilton | The Williams Capital Group, L.P. | ||

| Co-Manager | Co-Manager | ||

The securities offered by this structural and collateral term sheet (this “Term Sheet”) are described in greater detail in the preliminary prospectus, dated on or about February 28, 2018, included as part of our registration statement (SEC File No. 333-207132) (the “Preliminary Prospectus”). The Preliminary Prospectus contains material information that is not contained in this Term Sheet (including, without limitation, a detailed discussion of risks associated with an investment in the offered securities under the heading“Risk Factors” in the Preliminary Prospectus). The Preliminary Prospectus is available upon request from Citigroup Global Markets Inc., Morgan Stanley & Co. LLC, Merrill Lynch, Pierce, Fenner & Smith Incorporated, Drexel Hamilton, LLC or The Williams Capital Group, L.P. This Term Sheet is subject to change.

For information regarding certain risks associated with an investment in this transaction, refer to “Risk Factors” in the Preliminary Prospectus. Capitalized terms used but not otherwise defined in this Term Sheet have the respective meanings assigned to those terms in the Preliminary Prospectus.

The Securities May Not Be a Suitable Investment for You

The securities offered by this Term Sheet are not suitable investments for all investors. In particular, you should not purchase any class of securities unless you understand and are able to bear the prepayment, credit, liquidity and market risks associated with that class of securities. For those reasons and for the reasons set forth under the heading “Risk Factors” in the Preliminary Prospectus, the yield to maturity of, the aggregate amount and timing of distributions on and the market value of the offered securities are subject to material variability from period to period and give rise to the potential for significant loss over the life of those securities. The interaction of these factors and their effects are impossible to predict and are likely to change from time to time. As a result, an investment in the offered securities involves substantial risks and uncertainties and should be considered only by sophisticated institutional investors with substantial investment experience with similar types of securities and who have conducted appropriate due diligence on the mortgage loans and the securities. Potential investors are advised and encouraged to review the Preliminary Prospectus in full and to consult with their legal, tax, accounting and other advisors prior to making any investment in the offered securities described in this Term Sheet.

The securities offered by these materials are being offered when, as and if issued. This Term Sheet is not to be construed as an offer to sell or the solicitation of any offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal. The information contained in this Term Sheet may not pertain to any securities that will actually be sold. The information contained in this Term Sheet may be based on assumptions regarding market conditions and other matters as reflected in this Term Sheet. We make no representations regarding the reasonableness of such assumptions or the likelihood that any of such assumptions will coincide with actual market conditions or events, and this Term Sheet should not be relied upon for such purposes. We and our affiliates, officers, directors, partners and employees, including persons involved in the preparation or issuance of this Term Sheet may, from time to time, have long or short positions in, and buy or sell, the securities mentioned in this Term Sheet or derivatives thereof (including options). Information contained in this Term Sheet is current as of the date appearing on this Term Sheet only. Information in this Term Sheet regarding the securities and the mortgage loans backing any securities discussed in this Term Sheet supersedes all prior information regarding such securities and mortgage loans. None ofCitigroup Global Markets Inc., Morgan Stanley & Co. LLC, Merrill Lynch, Pierce, Fenner & Smith Incorporated, Drexel Hamilton, LLC or The Williams Capital Group, L.P.,provides accounting, tax or legal advice.

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-207132) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Morgan Stanley & Co. LLC, Merrill Lynch, Pierce, Fenner & Smith Incorporated, Drexel Hamilton, LLC, The Williams Capital Group, L.P. or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

2

The issuing entity will be relying on an exclusion or exemption from the definition of “investment company” under the Investment Company Act of 1940, as amended (the “Investment Company Act”), contained in Section 3(c)(5) of the Investment Company Act or Rule 3a-7 under the Investment Company Act, although there may be additional exclusions or exemptions available to the issuing entity. The issuing entity is being structured so as not to constitute a “covered fund” for purposes of the Volcker Rule under the Dodd-Frank Act (both as defined in “Risk Factors—Legal and Regulatory Provisions Affecting Investors Could Adversely Affect the Liquidity and Other Aspects of the Offered Certificates” in the Preliminary Prospectus). See also “Legal Investment” in the Preliminary Prospectus.

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-207132) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Morgan Stanley & Co. LLC, Merrill Lynch, Pierce, Fenner & Smith Incorporated, Drexel Hamilton, LLC, The Williams Capital Group, L.P. or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

3

CERTIFICATE SUMMARY

| OFFERED CERTIFICATES | |||||||

Offered Classes | Expected Ratings | Approximate Initial | Approximate Initial | Initial | Pass-Through | Expected | Expected |

| Class A-1 | Aaa(sf) / AAAsf / AAA(sf) | $28,000,000 | 30.000% | % | (6) | 2.79 | 4/18 - 1/23 |

| Class A-2 | Aaa(sf) / AAAsf / AAA(sf) | $69,000,000 | 30.000% | % | (6) | 4.91 | 1/23 - 3/23 |

| Class A-3 | Aaa(sf) / AAAsf / AAA(sf) | (7) | 30.000% | % | (6) | (7) | (7) |

| Class A-4 | Aaa(sf) / AAAsf / AAA(sf) | (7) | 30.000% | % | (6) | (7) | (7) |

| Class A-AB | Aaa(sf) / AAAsf / AAA(sf) | $49,000,000 | 30.000 % | % | (6) | 7.37 | 3/23 - 10/27 |

| Class X-A | Aa1(sf) / AAAsf / AAA(sf) | $783,442,000(8) | N/A | % | Variable IO(9) | N/A | N/A |

| Class X-B | NR / A-sf / AAA(sf) | $97,142,000(8) | N/A | % | Variable IO(9) | N/A | N/A |

| Class A-S | Aa3(sf) / AAAsf / AAA(sf) | $76,957,000 | 22.375% | % | (6) | 9.93 | 2/28 - 3/28 |

| Class B | NR / AA-sf / AA-(sf) | $49,202,000 | 17.500% | % | (6) | 9.97 | 3/28 - 3/28 |

| Class C | NR / A-sf / A-(sf) | $47,940,000 | 12.750% | % | (6) | 9.97 | 3/28 - 3/28 |

| NON-OFFERED CERTIFICATES | |||||||

Non-Offered Classes | Expected Ratings | Approximate Initial | Approximate Initial | Initial | Pass-Through | Expected | Expected |

| Class X-D | NR / BBB-sf / BBB-(sf) | $52,986,000(8) | N/A | % | Variable IO(9) | N/A | N/A |

| Class X-E | NR / BB-sf / NR | $25,232,000(8) | N/A | % | Variable IO(9) | N/A | N/A |

| Class X-F | NR / B-sf / NR | $10,092,000(8) | N/A | % | Variable IO(9) | N/A | N/A |

| Class X-G | NR / NR / NR | $40,371,466(8) | N/A | % | Variable IO(9) | N/A | N/A |

| Class D | NR / BBB-sf / BBB-(sf) | $52,986,000 | 7.500% | % | (6) | 9.97 | 3/28 - 3/28 |

| Class E | NR / BB-sf / NR | $25,232,000 | 5.000% | % | (6) | 9.97 | 3/28 - 3/28 |

| Class F | NR / B-sf / NR | $10,092,000 | 4.000% | % | (6) | 9.97 | 3/28 - 3/28 |

| Class G | NR / NR / NR | $40,371,466 | 0.000% | % | (6) | 9.97 | 3/28 - 3/28 |

| Class R(10) | N/A | N/A | N/A | N/A | N/A | N/A | N/A |

NON-OFFERED VERTICAL RISK RETENTION INTEREST | |||||||

Non-Offered Eligible Vertical Interest | Expected Ratings | Approximate Initial | Approximate Initial | Initial | Pass-Through | Expected | Expected |

| VRR Interest(11) | NR / NR / NR | $53,119,236 | N/A | % | WAC(12) | 9.22 | 4/18 - 3/28 |

| (1) | It is a condition of issuance that the offered certificates and certain classes of non-offered certificates receive the ratings set forth above. The anticipated ratings shown are those of Moody’s Investors Service, Inc. (“Moody’s”), Fitch Ratings, Inc. (“Fitch”) and Kroll Bond Rating Agency, Inc. (“KBRA”). Subject to the discussion under “Ratings” in the Preliminary Prospectus, the ratings on the certificates address the likelihood of the timely receipt by holders of all payments of interest to which they are entitled on each distribution date and, except in the case of the interest only certificates, the ultimate receipt by holders of all payments of principal to which they are entitled on or before the applicable rated final distribution date. Certain nationally recognized statistical rating organizations, as defined in Section 3(a)(62) of the Securities Exchange Act of 1934, as amended, that were not hired by the depositor may use information they receive pursuant to Rule 17g-5 under the Securities Exchange Act of 1934, as amended, or otherwise to rate the offered certificates. We cannot assure you as to what ratings a non-hired nationally recognized statistical rating organization would assign. See “Risk Factors—Nationally Recognized Statistical Rating Organizations May Assign Different Ratings to the Certificates; Ratings of the Certificates Reflect Only the Views of the Applicable Rating Agencies as of the Dates Such Ratings Were Issued; Ratings May Affect ERISA Eligibility; Ratings May Be Downgraded” in the Preliminary Prospectus. Moody’s, Fitch and KBRA have informed us that the “sf” designation in the ratings represents an identifier of structured finance product ratings. For additional information about this identifier, prospective investors can go to the related rating agency’s website. The depositor and the underwriters have not verified, do not adopt and do not accept responsibility for any statements made by the rating agencies on those websites. Credit ratings referenced throughout this Term Sheet are forward-looking opinions about credit risk and express a rating agency’s opinion about the willingness and ability of an issuer of securities to meet its financial obligations in full and on time. Ratings are not indications of investment merit and are not buy, sell or hold recommendations, a measure of asset value or an indication of the suitability of an investment. |

| (2) | Approximate, subject to a variance of plus or minus 5%, and further subject to the discussion in footnote (7) below. The certificate balance of the VRR Interest (as defined in footnote (11) below) is not included in the certificate balance or notional amount of any other class of certificates listed in the table above, and the VRR Interest is not offered hereby. In addition, the notional amounts of the Class X-A, Class X-B, Class X-D, Class X-E, Class X-F and Class X-G certificates may vary depending upon the final pricing of the classes of Principal Balance Certificates (as defined in footnote (3) below) whose certificate balances comprise such notional amounts, and, if as a result of such pricing the pass-through rate of any class of the Class X-A, Class X-B, Class X-D, Class X-E, Class X-F or Class X-G certificates, as applicable, would be equal to zero at all times, such class of certificates will not be issued on the closing date of this securitization. |

| (3) | The approximate initial credit support percentages set forth for the Class A-1, Class A-2, Class A-3, Class A-4 and Class A-AB certificates are represented in the aggregate. The approximate initial credit support percentages shown in the table above do not take into account the VRR Interest. However, losses incurred on the mortgage loans will be allocated between the VRR Interest, on the one hand, and the Class A-1, Class A-2, Class A-3, Class A-4, Class A-AB, Class A-S, Class B, Class C, Class D, Class E, Class F and Class G certificates (collectively, the “Non-Vertically Retained Principal Balance Certificates”), on the other hand,pro rata in accordance with their respective outstanding certificate balances. See “Credit Risk Retention” and “Description of the Certificates” in the Preliminary Prospectus. The VRR Interest and the Non-Vertically Retained Principal Balance Certificates are collectively referred to in this Term Sheet as the “Principal Balance Certificates”. |

| (4) | Approximateper annum rate as of the Closing Date. |

| (5) | Determined assuming no prepayments prior to the maturity date or any anticipated repayment date, as applicable, for anymortgage loan and based on the modeling assumptions described under“Yield, Prepayment and Maturity Considerations” in the Preliminary Prospectus. |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-207132) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Morgan Stanley & Co. LLC, Merrill Lynch, Pierce, Fenner & Smith Incorporated, Drexel Hamilton, LLC, The Williams Capital Group, L.P. or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

4

CERTIFICATE SUMMARY (continued)

| (6) | For any distribution date, the pass-through rate on each class of the Non-Vertically Retained Principal Balance Certificates will generally be equal to one of (i) a fixedper annumrate, (ii) the weighted average of the net interest rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) as in effect from time to time, (iii) a rate equal to the lesser of a specifiedper annum rate and the weighted average rate described in clause (ii), or (iv) the weighted average rate described in clause (ii) less a specified percentage, but no less than 0.000%, as describedunder“Description of the Certificates—Distributions—Pass Through Rates” in the Preliminary Prospectus. |

| (7) | The exact initial certificate balances of the Class A-3 and Class A-4 certificates are unknown and will be determined based on the final pricing of those classes of certificates. However, the respective initial certificate balances, weighted average lives and principal windows of the Class A-3 and Class A-4 certificates are expected to be within the applicable ranges reflected in the following chart. The aggregate initial certificate balance of the Class A-3 and Class A-4 certificates is expected to be approximately $560,485,000, subject to a variance of plus or minus 5%. |

Class of | Expected Range of Initial | Expected Range of | Expected Range of Principal |

| Class A-3 | $70,000,000 - $170,000,000 | 9.68 - 9.74 | 10/27 - 12/27 / 10/27 - 1/28 |

| Class A-4 | $390,485,000 - $490,485,000 | 9.86 - 9.85 | 1/28 - 2/28 / 12/27 - 2/28 |

| (8) | The Class X-A, Class X-B, Class X-D, Class X-E, Class X-F and Class X-G certificates (collectively, the “Class X Certificates”) will not have certificate balances and will not be entitled to receive distributions of principal. Interest will accrue on each class of Class X Certificates at the related pass-through rate based upon the related notional amount. The notional amount of each class of the Class X Certificates will be equal to the certificate balance or the aggregate of the certificate balances, as applicable, from time to time of the class or classes of the Non-Vertically Retained Principal Balance Certificates identified in the same row as such class of Class X Certificates in the chart below (as to such class of Class X Certificates, the “Corresponding Principal Balance Certificates”): |

| Class of Class X Certificates | Class(es) of Corresponding Principal Balance Certificates |

| Class X-A | Class A-1, Class A-2, Class A-3, Class A-4, Class A-AB and Class A-S |

| Class X-B | Class B and Class C |

| Class X-D | Class D |

| Class X-E | Class E |

| Class X-F | Class F |

| Class X-G | Class G |

| (9) | The pass-through rate on each class of Class X Certificates will generally be aper annum rate equal to the excess, if any, of (i) the weighted average of the net interest rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) as in effect from time to time, over (ii) the pass-through rate (or, if applicable, the weighted average of the pass-through rates) of the class or classes of Corresponding Principal Balance Certificates as in effect from time to time, as described in the Preliminary Prospectus. |

| (10) | The Class R certificates will not have a certificate balance, notional amount, pass-through rate, rating or rated final distribution date. The Class R certificates will represent the residual interests in each of two separate REMICs, as further described in the Preliminary Prospectus. The Class R certificates will not be entitled to distributions of principal or interest. |

| (11) | Citi Real Estate Funding Inc. (as retaining sponsor) is expected to acquire (or cause one or more other retaining parties to acquire) from the depositor, on the Closing Date (as defined below), portions of an “eligible vertical interest” (as defined in Regulation RR) in the form of a “single vertical security” (as defined in Regulation RR) with an initial certificate balance of approximately $53,119,236 (the “VRR Interest”), which is expected to represent approximately 5.0% of the aggregate initial certificate balance of all of the “ABS interests” (as defined in Regulation RR) issued by the issuing entity on the Closing Date. The VRR Interest will be retained by certain retaining parties in accordance with the credit risk retention rules applicable to this securitization transaction. See “Credit Risk Retention” in the Preliminary Prospectus. The VRR Interest is a class of certificates. |

| (12) | Although it does not have a specified pass-through rate (other than for tax reporting purposes), the effective interest rate for the VRR Interest will be the weighted average of the net mortgage interest rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) as in effect from time to time. |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-207132) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Morgan Stanley & Co. LLC, Merrill Lynch, Pierce, Fenner & Smith Incorporated, Drexel Hamilton, LLC, The Williams Capital Group, L.P. or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

5

MORTGAGE POOL CHARACTERISTICS

| Mortgage Pool Characteristics(1) | |

| Initial Pool Balance(2) | $1,062,384,703 |

| Number of Mortgage Loans | 52 |

| Number of Mortgaged Properties | 142 |

| Average Cut-off Date Balance | $20,430,475 |

| Weighted Average Mortgage Rate | 4.69063% |

| Weighted Average Remaining Term to Maturity/ARD (months) | 115 |

| Weighted Average Remaining Amortization Term (months)(3) | 351 |

| Weighted Average Cut-off Date LTV Ratio(4) | 60.1% |

| Weighted Average Maturity Date/ARD LTV Ratio(4) | 54.9% |

| Weighted Average UW NCF DSCR(5) | 1.80x |

| Weighted Average Debt Yield on Underwritten NOI(6) | 10.8% |

| % of Initial Pool Balance of Mortgage Loans that are Amortizing Balloon | 22.4% |

| % of Initial Pool Balance of Mortgage Loans that are Interest Only then Amortizing Balloon | 33.8% |

| % of Initial Pool Balance of Mortgage Loans that are Interest Only | 43.8% |

| % of Initial Pool Balance of Mortgaged Properties with Single Tenants | 8.8% |

| % of Initial Pool Balance of Mortgage Loans with Mezzanine Debt | 0.9% |

| % of Initial Pool Balance of Mortgage Loans with Subordinate Debt | 3.8% |

| (1) | The Cut-off Date LTV Ratio, Maturity Date/ARD LTV Ratio, UW NCF DSCR, Debt Yield on Underwritten NOI and Cut-off Date Balance Per SF / Rooms information for each mortgage loan is presented in this Term Sheet (i) if such mortgage loan is part of a loan combination (as defined under “Collateral Overview—Loan Combination Summary” below), based on both that mortgage loan and any related pari passu companion loan(s) but, unless otherwise specifically indicated, without regard to any related subordinate companion loan(s), and (ii) unless otherwise specifically indicated, without regard to any other indebtedness (whether or not secured by the related mortgaged property, ownership interests in the related borrower or otherwise) that currently exists or that may be incurred by the related borrower or its owners in the future. |

| (2) | Subject to a permitted variance of plus or minus 5%. |

| (3) | Excludes mortgage loans that are interest-only for the entire term. |

| (4) | The Cut-off Date LTV Ratios and Maturity Date/ARD LTV Ratios presented in this Term Sheet are generally based on the “as-is” appraised values of the related mortgaged properties (as set forth on Annex A to the Preliminary Prospectus),provided that such LTV ratios may be calculated (i) based on “as-stabilized” or similar values in certain cases where the completion of certain hypothetical conditions or other events at the property are assumed and/or where reserves have been established at origination to satisfy the applicable condition or event that is expected to occur, (ii) based on an “as-is portfolio value”, which represents the appraised value for a portfolio of mortgaged properties as a whole and not the sum of the appraised values for each of the individual mortgaged properties or (iii) based on the Cut-off Date Balance net of a related earnout or holdback reserve, in each case as further described in the definitions of “Appraised Value”, “Cut-off Date LTV Ratio” and “Maturity Date/ARD LTV Ratio” under “Description of the Mortgage Pool—Certain Calculations and Definitions” in the Preliminary Prospectus. |

| (5) | The UW NCF DSCR for each mortgage loan is generally calculated by dividing the UW NCF for the related mortgaged property or mortgaged properties by the annual debt service for such mortgage loan, as adjusted in the case of mortgage loans with a partial interest only period by using the first 12 amortizing payments due instead of the actual interest only payment due. |

| (6) | The Debt Yield on Underwritten NOI for each mortgage loan is generally calculated as the related mortgaged property’s Underwritten NOI divided by the Cut-off Date Balance of such mortgage loan, and the Debt Yield on Underwritten NCF for each mortgage loan is generally calculated as the related mortgaged property’s Underwritten NCF divided by the Cut-off Date Balance of such mortgage loan;provided, that such Debt Yields may be calculated based on the Cut-off Date Balance net of a related earnout or holdback reserve, as further described in the definitions of “Debt Yield on Underwritten NOI” and “Debt Yield on Underwritten NCF” under“Description of the Mortgage Pool—Certain Calculations and Definitions” in the Preliminary Prospectus. |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-207132) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Morgan Stanley & Co. LLC, Merrill Lynch, Pierce, Fenner & Smith Incorporated, Drexel Hamilton, LLC, The Williams Capital Group, L.P. or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

6

KEY FEATURES OF THE CERTIFICATES

| Co-Lead Managers and Joint Bookrunners: | Citigroup Global Markets Inc. Morgan Stanley & Co. LLC Merrill Lynch, Pierce, Fenner & Smith Incorporated

|

| Co-Managers: | Drexel Hamilton, LLC The Williams Capital Group, L.P.

|

| Depositor: | Citigroup Commercial Mortgage Securities Inc.

|

| Initial Pool Balance: | $1,062,384,703 |

| Master Servicer: | Midland Loan Services, a Division of PNC Bank, National Association

|

| Special Servicer: | LNR Partners, LLC

|

| Certificate Administrator: | Citibank, N.A.

|

| Trustee: | Wilmington Trust, National Association

|

| Operating Advisor: | Park Bridge Lender Services LLC

|

| Asset Representations Reviewer: | Park Bridge Lender Services LLC

|

| Risk Retention Consultation Party: | Citi Real Estate Funding Inc.

|

| Credit Risk Retention: | For a discussion on the manner in which the U.S. credit risk retention requirements are being satisfied by Citi Real Estate Funding Inc., as retaining sponsor, see “Credit Risk Retention” in the Preliminary Prospectus. Note that this securitization transaction is not structured to satisfy the EU risk retention and due diligence requirements.

|

| Closing Date: | On or about March 20, 2018

|

| Cut-off Date: | With respect to each mortgage loan, the due date in March 2018 for that mortgage loan (or, in the case of any mortgage loan that has its first due date subsequent to March 2018, the date that would have been its due date in March 2018 under the terms of that mortgage loan if a monthly payment were scheduled to be due in that month) |

| Determination Date: | The 6th day of each month or next business day, commencing in April 2018 |

| Distribution Date: | The 4th business day after the Determination Date, commencing in April 2018 |

| Interest Accrual: | Preceding calendar month

|

| ERISA Eligible: | The offered certificates are expected to be ERISA eligible, subject to the exemption conditions described in the Preliminary Prospectus

|

| SMMEA Eligible: | No |

| Payment Structure: | Sequential Pay |

| Day Count: | 30/360 |

| Tax Structure: | REMIC |

| Rated Final Distribution Date: | March 2051 |

| Cleanup Call: | 1.0% |

| Minimum Denominations: | $10,000 minimum for the offered certificates (other than the Class X-A and Class X-B certificates); $1,000,000 minimum for the Class X-A and Class X-B certificates; and integral multiples of $1 thereafter for all the offered certificates |

| Delivery: | Book-entry through DTC |

| Bond Information: | Cash flows are expected to be modeled by TREPP, INTEX and BLOOMBERG |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-207132) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Morgan Stanley & Co. LLC, Merrill Lynch, Pierce, Fenner & Smith Incorporated, Drexel Hamilton, LLC, The Williams Capital Group, L.P. or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

7

TRANSACTION HIGHLIGHTS

| ■ | $1,062,384,702 (Approximate) New-Issue Multi-Borrower CMBS: |

| — | Overview: The mortgage pool consists of 52 fixed-rate commercial mortgage loans that have an aggregate Cut-off Date Balance of $1,062,384,703 (the “Initial Pool Balance”), have an average mortgage loan Cut-off Date Balance of $20,430,475 and are secured by 142 mortgaged properties located throughout 30 states and the District of Columbia. |

| — | LTV: 60.1% weighted average Cut-off Date LTV Ratio |

| — | DSCR: 1.80x weighted average Underwritten Debt Service Coverage Ratio |

| — | Debt Yield: 10.8% weighted average Debt Yield on Underwritten NOI |

| — | Credit Support: 30.000% credit support to Class A-1 / A-2 / A-3 / A-4 / A-AB |

| ■ | Loan Structural Features: |

| — | Amortization: 56.2% of the mortgage loans by Initial Pool Balance have scheduled amortization: |

| – | 22.4% of the mortgage loans by Initial Pool Balance have amortization for the entire term with a balloon payment due at maturity |

| – | 33.8% of the mortgage loans by Initial Pool Balance have scheduled amortization following a partial interest only period with a balloon payment due at maturity |

| — | Hard Lockboxes: 35.1% of the mortgage loans by Initial Pool Balance have a Hard Lockbox in place |

| — | Cash Traps: 98.3% of the mortgage loans by Initial Pool Balance have cash traps triggered by certain declines in cash flow, all at levels equal to or greater than a 1.05x coverage, that fund an excess cash flow reserve |

| — | Reserves: The mortgage loans require amounts to be escrowed for reserves as follows: |

| – | Real Estate Taxes: 45 mortgage loans representing 77.6% of the Initial Pool Balance |

| – | Insurance: 31 mortgage loans representing 54.1% of the Initial Pool Balance |

| – | Replacement Reserves (Including FF&E Reserves): 44 mortgage loans representing 78.7% of the Initial Pool Balance |

| – | Tenant Improvements / Leasing Commissions: 29 mortgage loans representing 80.8% of the portion of the Initial Pool Balance that is secured by office, retail, industrial and mixed use properties |

| — | Predominantly Defeasance Mortgage Loans: 84.4% of the mortgage loans by Initial Pool Balance permit defeasance only after an initial lockout period |

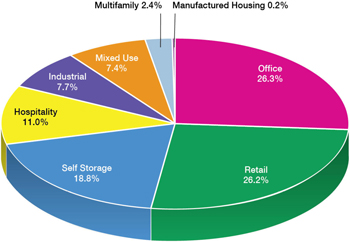

| ■ | Multiple-Asset Types > 5.0% of the Initial Pool Balance: |

| — | Office: 26.3% of the mortgaged properties by allocated Initial Pool Balance are office properties |

| — | Retail: 26.2% of the mortgaged properties by allocated Initial Pool Balance are retail properties (21.9% are anchored retail properties) |

| — | Self Storage: 18.8% of the mortgaged properties by allocated Initial Pool Balance are self-storage properties |

| — | Hospitality: 11.0% of the mortgaged properties by allocated Initial Pool Balance are hospitality properties |

| — | Industrial: 7.7% of the mortgaged properties by allocated Initial Pool Balance are industrial properties |

| — | Mixed Use: 7.4% of the mortgaged properties by allocated Initial Pool Balance are mixed use properties |

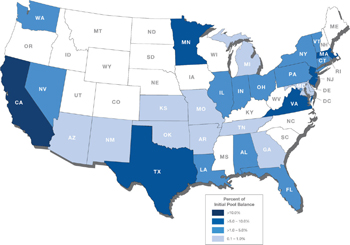

| ■ | Geographic Diversity: The 142 mortgaged properties are located throughout 30 states and the District of Columbia, with only one state having greater than 10.0% of the allocated Initial Pool Balance: California (19.7%) |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-207132) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Morgan Stanley & Co. LLC, Merrill Lynch, Pierce, Fenner & Smith Incorporated, Drexel Hamilton, LLC, The Williams Capital Group, L.P. or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

8

| COLLATERAL OVERVIEW |

Mortgage Loans by Loan Seller

Mortgage Loan Seller | Mortgage Loans | Mortgaged Properties | Aggregate Cut-off | % of Initial | ||||||||

| Morgan Stanley Mortgage Capital Holdings LLC | 12 | 48 | $299,400,517 | 28.2 | % | |||||||

| Citi Real Estate Funding Inc. | 13 | 40 | 292,166,622 | 27.5 | ||||||||

| Starwood Mortgage Funding V LLC | 18 | 20 | 256,817,564 | 24.2 | ||||||||

| Bank of America, National Association | 9 | 34 | 214,000,000 | 20.1 | ||||||||

| Total | 52 | 142 | $1,062,384,703 | 100.0 | % | |||||||

Ten Largest Mortgage Loans(1)(2)

# | Mortgage Loan Name | Cut-off Date | % of | Property | Property | Cut-off Date Balance Per SF/Rooms | UW | UW | Cut-off Date LTV | |||||||||||||||||

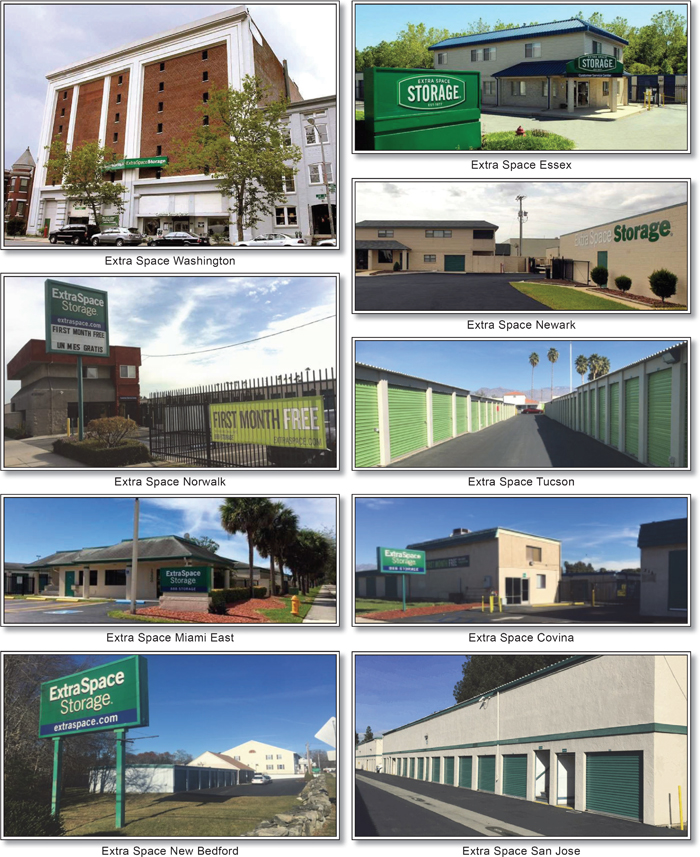

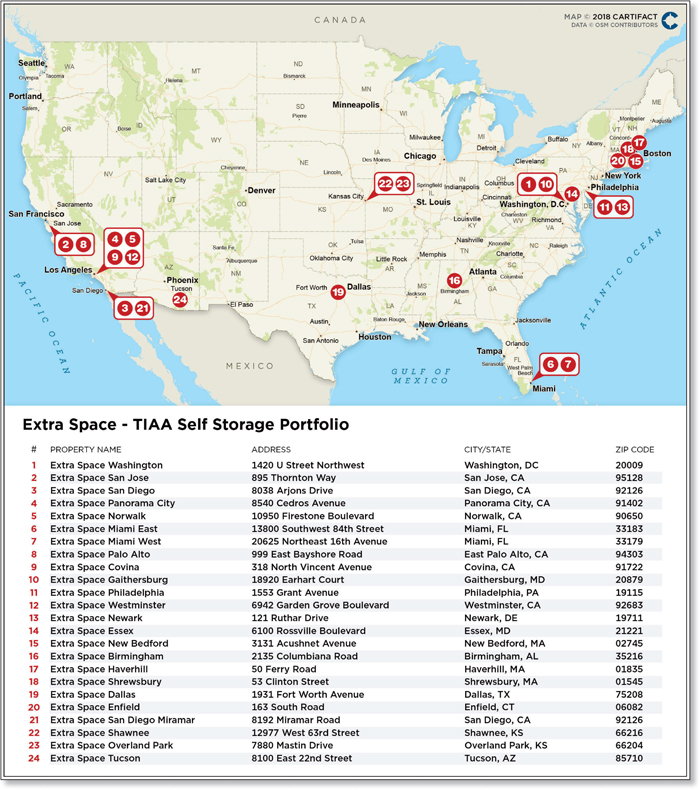

| 1 | Extra Space - TIAA Self Storage Portfolio | $105,000,000 | 9.9 | % | Self Storage | 1,614,702 | $142 | 1.97 | x | 9.2 | % | 58.1 | % | |||||||||||||

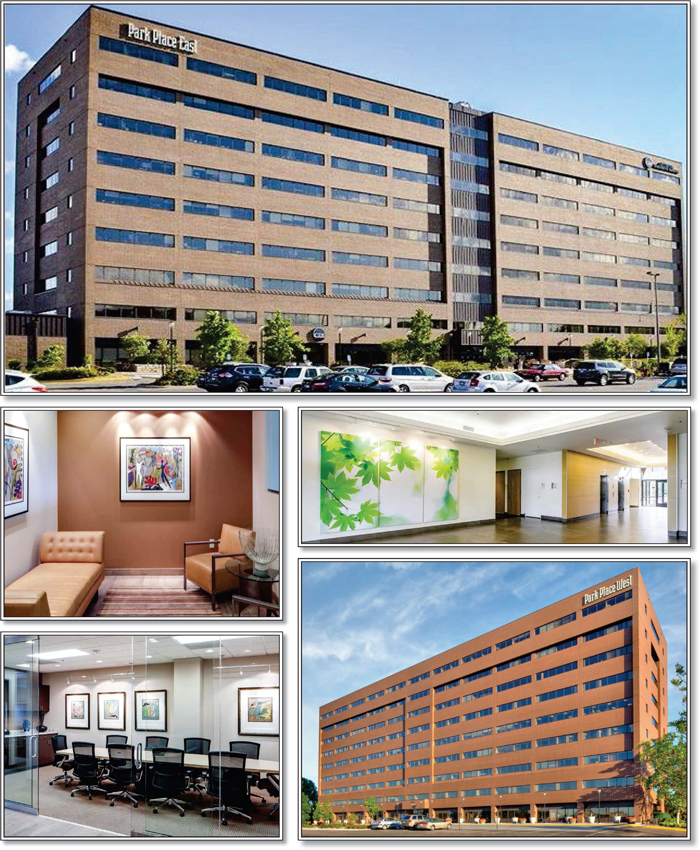

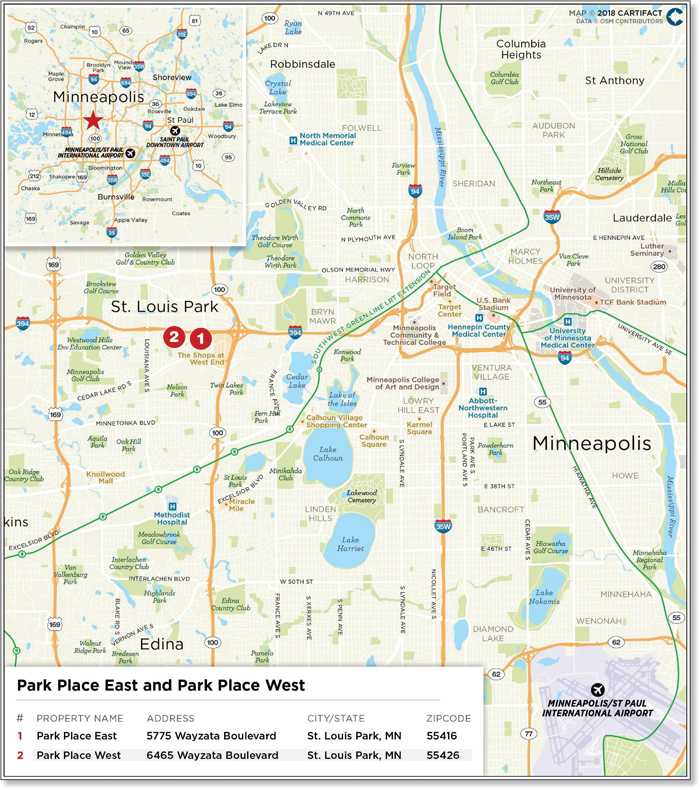

| 2 | Park Place East and Park Place West | 54,250,000 | 5.1 | Office | 397,968 | $136 | 1.32 | x | 9.7 | % | 68.9 | % | ||||||||||||||

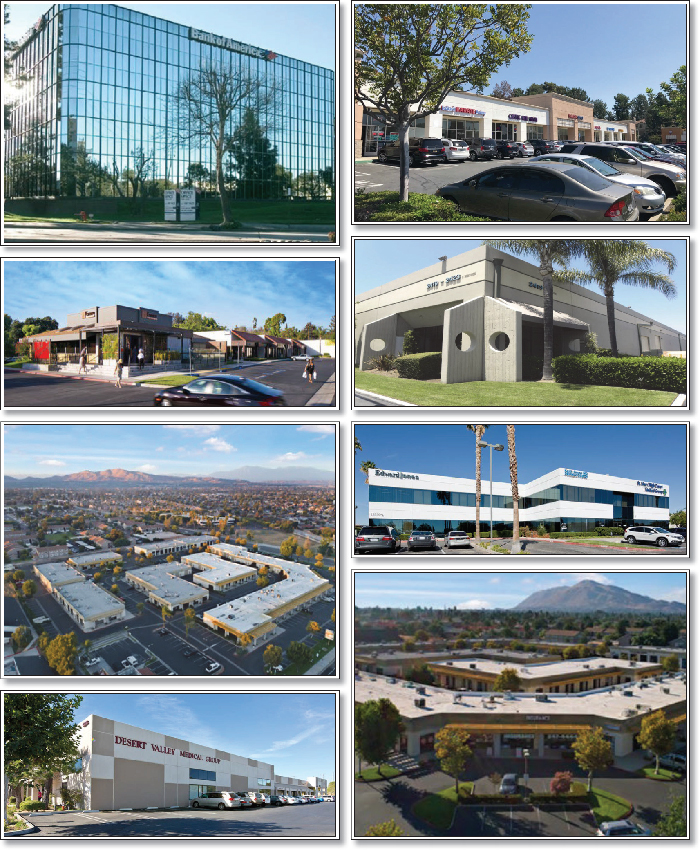

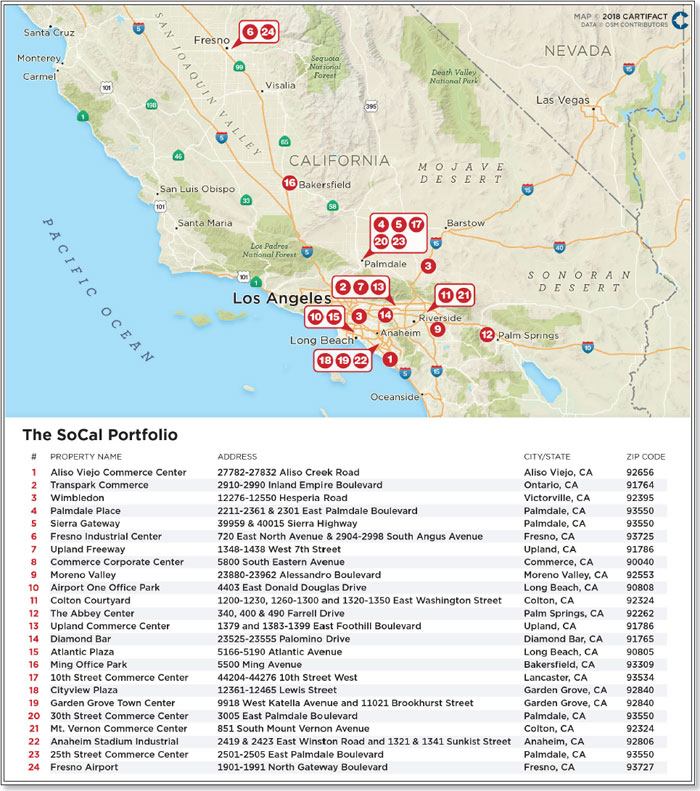

| 3 | The SoCal Portfolio | 50,000,000 | 4.7 | Various | 2,194,425 | $104 | 1.48 | x | 10.2 | % | 59.4 | % | ||||||||||||||

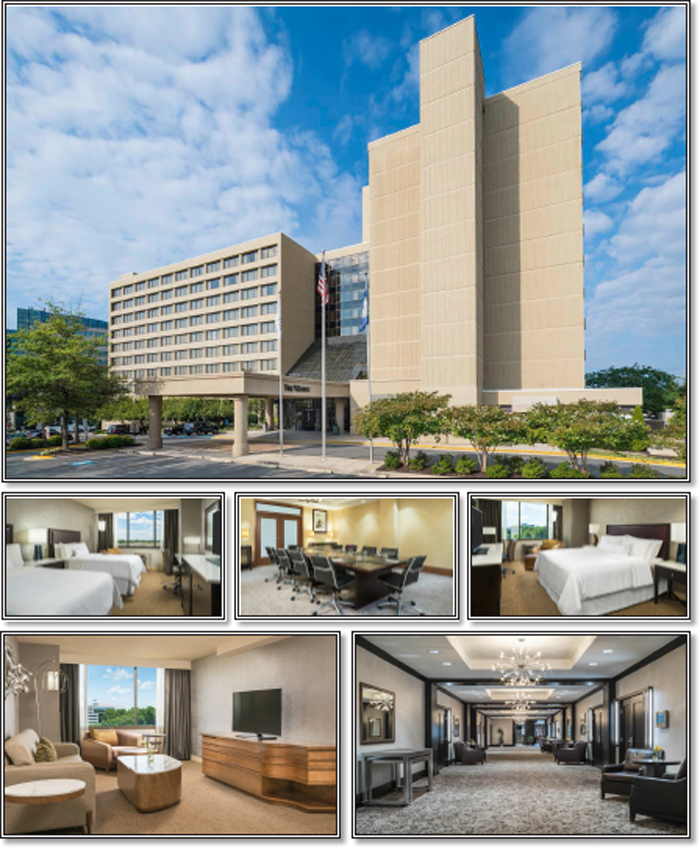

| 4 | Westin Tysons Corner | 48,000,000 | 4.5 | Hospitality | 407 | $117,936 | 1.61 | x | 12.5 | % | 60.8 | % | ||||||||||||||

| 5 | Extra Space Self Storage Portfolio | 42,400,000 | 4.0 | Self Storage | 2,668,218 | $73 | 2.01 | x | 8.7 | % | 65.0 | % | ||||||||||||||

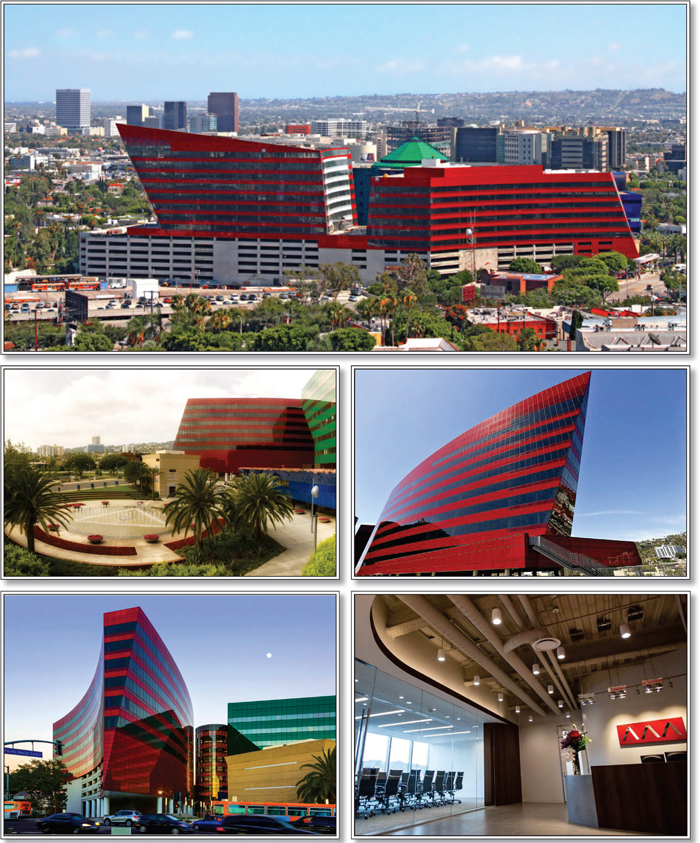

| 6 | Red Building | 40,000,000 | 3.8 | Office | 411,547 | $194 | 3.31 | x | 16.1 | % | 27.9 | % | ||||||||||||||

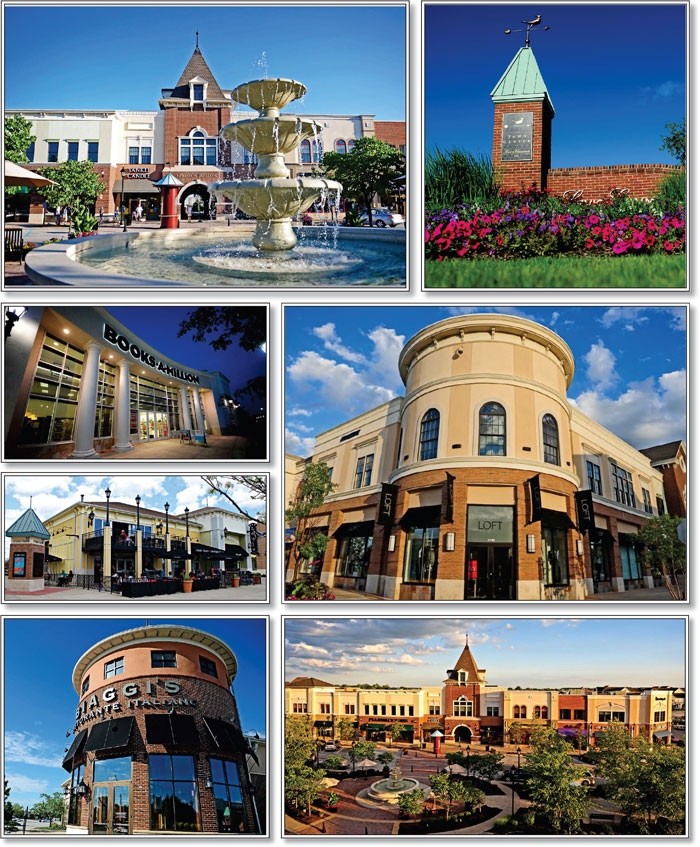

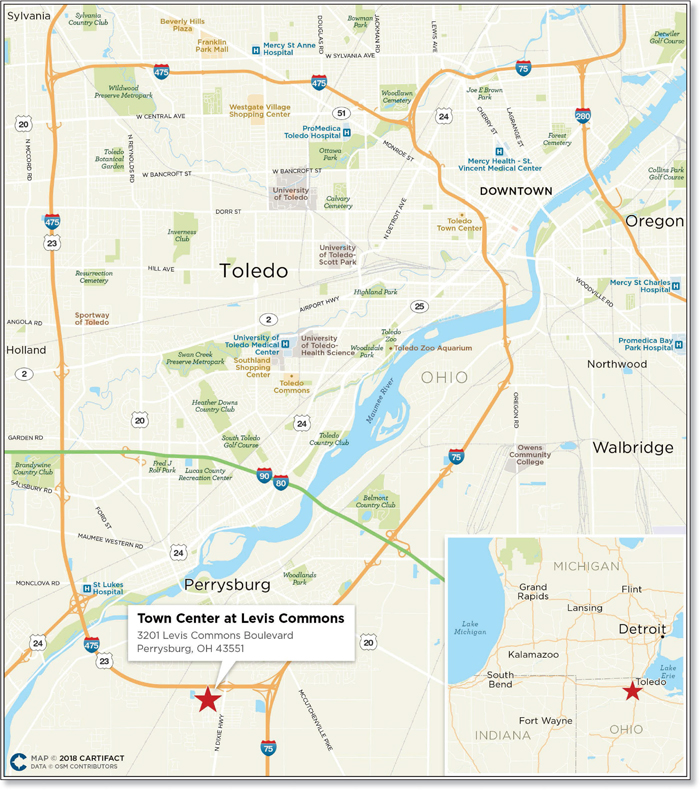

| 7 | Town Center at Levis Commons | 37,000,000 | 3.5 | Retail | 309,532 | $120 | 1.98 | x | 10.6 | % | 62.2 | % | ||||||||||||||

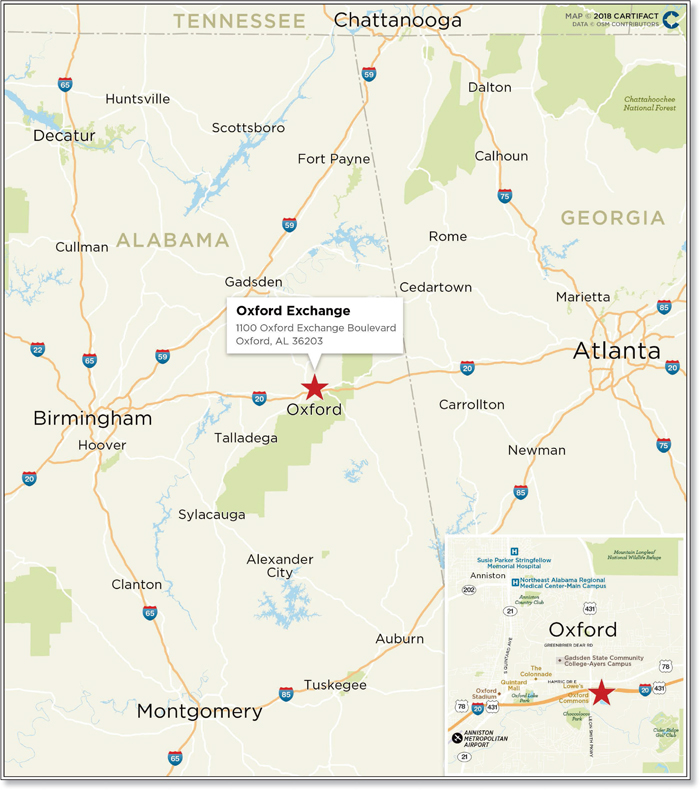

| 8 | Oxford Exchange | 36,900,000 | 3.5 | Retail | 333,866 | $111 | 1.63 | x | 10.4 | % | 68.3 | % | ||||||||||||||

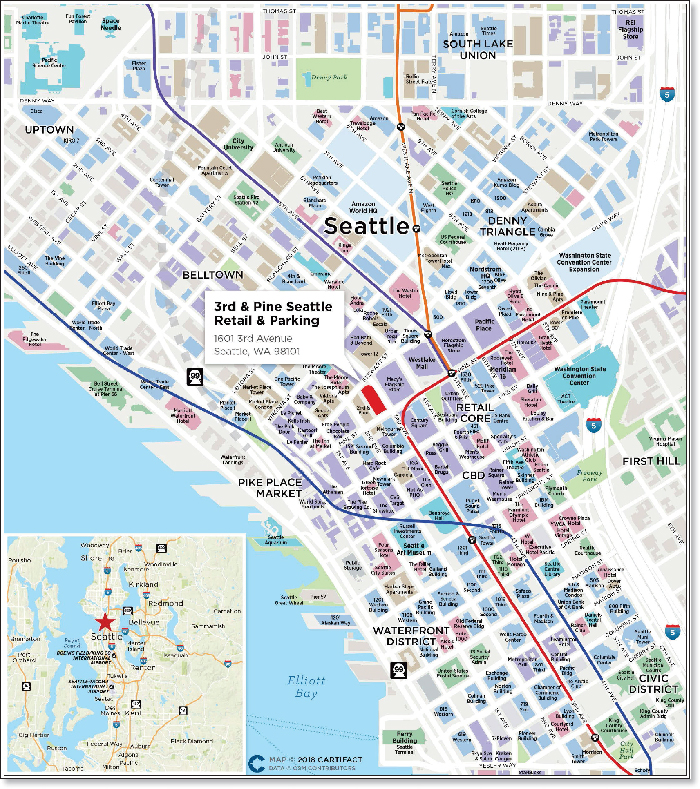

| 9 | 3rd & Pine Seattle Retail & Parking | 35,200,000 | 3.3 | Mixed Use | 349,184 | $101 | 1.78 | x | 8.4 | % | 59.7 | % | ||||||||||||||

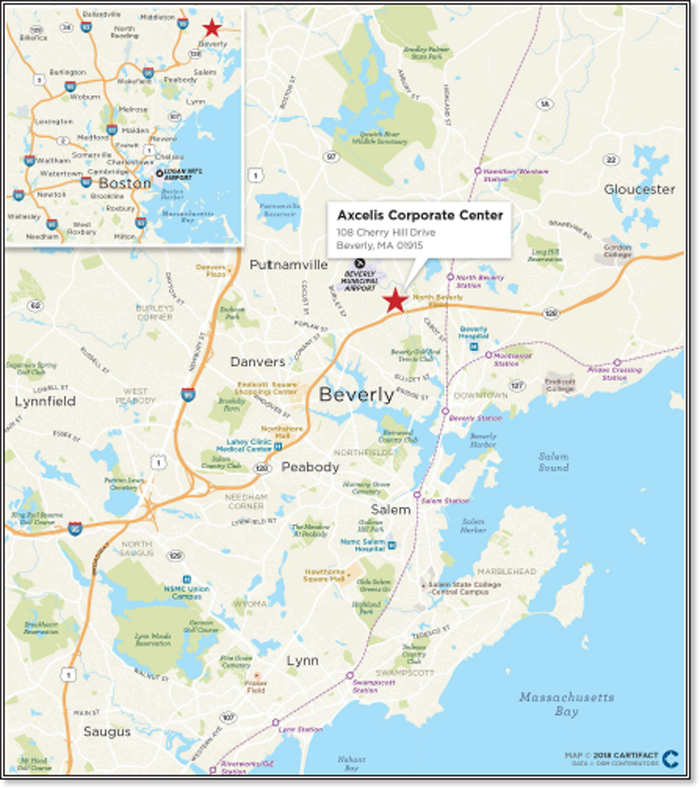

| 10 | Axcelis Corporate Center | 33,932,928 | 3.2 | Industrial | 417,313 | $122 | 1.33 | x | 10.2 | % | 62.0 | % | ||||||||||||||

| Top 10 Total / Wtd. Avg. | $482,682,928 | 45.4 | % | 1.84 | x | 10.4 | % | 59.3 | % | |||||||||||||||||

| Remaining Total / Wtd. Avg. | 579,701,775 | 54.6 | 1.77 | x | 11.1 | % | 60.7 | % | ||||||||||||||||||

| Total / Wtd. Avg. | $1,062,384,703 | 100.0 | % | 1.80 | x | 10.8 | % | 60.1 | % | |||||||||||||||||

| (1) | See footnotes to table entitled“Mortgage Pool Characteristics” above. |

| (2) | With respect to each mortgage loan that is part of a loan combination (as identified under “Collateral Overview—Loan Combination Summary” below), the UW NCF DSCR, UW NOI Debt Yield and Cut-off Date LTV Ratio are calculated based on both that mortgage loan and any related pari passu companion loan(s), but without regard to any related subordinate companion loan(s) or other indebtedness. With respect to the Red Building mortgage loan, the mortgaged property is also encumbered by three subordinate companion loans with an aggregate outstanding principal balance as of the Cut-off Date of $116,000,000. The UW NCF DSCR, UW NOI Debt Yield and Cut-off Date LTV Ratio for the Red Building mortgage loan, inclusive of the subordinate companion loans, are 1.15x, 6.6% and 68.4%, respectively. |

| (3) | With respect to certain of the mortgage loans identified above, the Cut-off Date LTV Ratios have been calculated using “as-stabilized”, “portfolio premium” or similar hypothetical values. Such mortgage loans are identified under the definition of “Appraised Value” set forth under “Description of the Mortgage Pool—Certain Calculations and Definitions” in the Preliminary Prospectus. |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-207132) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Morgan Stanley & Co. LLC, Merrill Lynch, Pierce, Fenner & Smith Incorporated, Drexel Hamilton, LLC, The Williams Capital Group, L.P. or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

9

COLLATERAL OVERVIEW (continued) |

Loan Combination Summary

Mortgaged Property Name(1) | Mortgage Loan | Mortgage | Aggregate Pari Passu | Aggregate Subordinate Companion Loan Cut-off Date Balance | Loan | Controlling | Master | Special | ||||||||||||

| Extra Space - TIAA Self Storage Portfolio | $105,000,000 | 9.9 | % | $124,000,000 | — | $229,000,000 | CGCMT 2018-B2 | Midland | LNR Partners | |||||||||||

| The SoCal Portfolio | $50,000,000 | 4.7 | % | $179,300,000 | — | $229,300,000 | CGCMT 2018-B2 | Midland | LNR Partners | |||||||||||

| Extra Space Self Storage Portfolio | $42,400,000 | 4.0 | % | $152,000,000 | — | $194,400,000 | MSC 2017-HR2 | Wells Fargo | LNR Partners | |||||||||||

| Red Building | $40,000,000 | 3.8 | % | $40,000,000 | $116,000,000 | $196,000,000 | Benchmark 2018-B2(3) | KeyBank | CWCapital | |||||||||||

| Axcelis Corporate Center | $33,932,928 | 3.2 | % | $16,966,464 | — | $50,899,391 | CGCMT 2018-B2 | Midland | LNR Partners | |||||||||||

| One Newark Center | $32,000,000 | 3.0 | % | $34,580,000 | — | $66,580,000 | BANK 2018-BNK10 | Wells Fargo | Torchlight | |||||||||||

| Braddock Metro Center | $30,000,000 | 2.8 | % | $44,200,000 | — | $74,200,000 | Benchmark 2018-B2 | KeyBank | CWCapital | |||||||||||

| Cross Point | $25,000,000 | 2.4 | % | $125,000,000 | — | $150,000,000 | UBS 2018-C8(4) | Midland(4) | Midland(4) | |||||||||||

| Fort Knox Executive Park | $19,000,000 | 1.8 | % | $16,000,000 | — | $35,000,000 | CGCMT 2018-B2 | Midland | LNR Partners | |||||||||||

| Warwick Mall | $17,500,000 | 1.6 | % | $57,500,000 | — | $75,000,000 | BANK 2017-BNK9 | Wells Fargo | Rialto | |||||||||||

| Two Harbor Point Square | $10,000,000 | 0.9 | % | $39,500,000 | — | 49,500,000 | CGCMT 2018-B2 | Midland | LNR Partners | |||||||||||

| (1) | Each of the mortgage loans included in the issuing entity that is secured by a mortgaged property or portfolio of mortgaged properties identified in the table above, together with the related companion loan(s) (none of which is included in the issuing entity), is referred to in this Term Sheet as a “loan combination”. See “Description of the Mortgage Pool—The Loan Combinations” in the Preliminary Prospectus. |

| (2) | Each loan combination will be serviced under the related Controlling PSA, and the controlling class representative (or an equivalent entity), if any, under the related Controlling PSA (or such other party as is designated under the related Controlling PSA) will be entitled to exercise the rights of controlling note holder for the subject loan combination, except as otherwise discussed in footnotes (3) and (4) below. |

| (3) | With respect to the Red Building mortgage loan, the control rights and the right to replace the applicable special servicer are held by the holder of the subordinate companion loan evidenced by note C so long as no “note C control appraisal period” under the related co-lender agreement is in effect. If a “note C control appraisal period” under the related co-lender agreement is in effect and no “note B control appraisal period” is in effect, then note B-1 will be the controlling note. If a “note B control appraisal period” under the related co-lender agreement is in effect, then note A-1 will be the controlling note. Unless and until a “note B control appraisal period” is in effect, the controlling class representative (or equivalent entity) under the applicable Controlling PSA will not be entitled to exercise control rights or the right to replace the applicable special servicer for the Red Building mortgage loan. |

| (4) | The Cross Point loan combination is expected to be initially serviced pursuant to the UBS 2018-C8 pooling and servicing agreement (which will be the initial Controlling PSA for such loan combination), by the outside servicer and outside special servicer set forth in the table above. Notwithstanding the foregoing, upon the inclusion of the related controlling pari passu companion loan in a future securitization transaction, such loan combination will be serviced under the pooling and servicing agreement entered into in connection with that future securitization, which will then be the applicable Controlling PSA for such loan combination. With respect to the Cross Point mortgage loan, the controlling class representative (or equivalent entity) under the initial Controlling PSA will only have non-binding consultation rights regarding major servicing decisions. The holder of the related controlling pari passu companion loan currently has consent rights regarding major servicing decisions, and termination rights with respect to the related outside special servicer, in connection with such mortgage loan. |

Mortgage Loans with Existing Mezzanine Debt or Subordinate Debt(1)

Mortgaged Property Name | Mortgage | Aggregate | Aggregate | Mezzanine | Cut-off Date | Wtd. Avg Cut-off | Cut-off Date | Cut-off | Cut-off | Cut-off | |||||||||||||

| Red Building | $40,000,000 | $40,000,000 | $116,000,000 | — | $196,000,000 | 5.14600 | % | 27.9 | % | 68.4 | % | 3.31x | 1.15x | ||||||||||

| Two Harbor Point Square | $10,000,000 | $39,500,000 | — | $11,500,000 | $61,000,000 | 5.26003 | %(4) | 61.9 | % | 76.3 | % | 1.78x | 1.28x | ||||||||||

| (1) | See footnotes to table entitled “Mortgage Pool Characteristics” above. |

| (2) | All “Total Debt” calculations set forth in the table above include any related pari passu companion loan(s), any related subordinate companion loan(s) and any related mezzanine debt. |

| (3) | “Cut-off Date Mortgage Loan LTV” and “Cut-off Date Mortgage Loan UW NCF DSCR” calculations include any related pari passu companion loan(s). |

| (4) | The Two Harbor Point Square Wtd. Avg. Cut-off Date Total Debt Interest Rate to full precision is 5.26002540983607%. |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-207132) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Morgan Stanley & Co. LLC, Merrill Lynch, Pierce, Fenner & Smith Incorporated, Drexel Hamilton, LLC, The Williams Capital Group, L.P. or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

10

COLLATERAL OVERVIEW (continued) |

Loan Combination Controlling Notes and Non-Controlling Notes

Mortgaged Property Name / | Controlling | Current Holder of | Current or Anticipated Holder | Cut-off Date Balance |

| Extra Space - TIAA Self Storage Portfolio | ||||

| Note A-1 | Yes | — | CGCMT 2018-B2 | $105,000,000 |

| Note A-2 | No | Bank of America, National Association | Not Identified | $80,000,000 |

| Note A-3 | No | Bank of America, National Association | Not Identified | $44,000,000 |

| The SoCal Portfolio | ||||

| Note A-1-1 | Yes | — | CGCMT 2018-B2 | $50,000,000 |

| Note A-1-2 | No | Citi Real Estate Funding Inc. | Not Identified | $35,000,000 |

| Note A-1-3 | No | Citi Real Estate Funding Inc. | Not Identified | $15,000,000 |

| Note A-1-4 | No | Citi Real Estate Funding Inc. | Not Identified | $37,580,000 |

| Note A-2-1 | No | Barclays Bank PLC | Not Identified | $45,000,000 |

| Note A-2-2 | No | Barclays Bank PLC | Not Identified | $46,720,000 |

| Extra Space Self Storage Portfolio | ||||

| Note A-1 | Yes | — | MSC 2017-HR2 | $92,000,000 |

| Note A-2 | No | — | BANK 2018-BNK10 | $60,000,000 |

| Note A-3 | No | — | CGCMT 2018-B2 | $42,400,000 |

| Red Building | ||||

| Note A-1 | (5) | — | Benchmark 2018-B2 | $40,000,000 |

| Note A-2 | No | — | CGCMT 2018-B2 | $40,000,000 |

| Note B-1 | (5) | Athene Annuity and Life Company | Not Applicable | $40,800,000 |

| Note B-2 | No | American Equity Investment Life Insurance Company | Not Applicable | $10,200,000 |

| Note C | (5) | Senior Real Estate Finance Account (N) LP | Not Applicable | $65,000,000 |

| Axcelis Corporate Center | ||||

| Note A-1 | Yes | — | CGCMT 2018-B2 | $33,932,928 |

| Note A-2 | No | Morgan Stanley Bank, N.A. | Not Identified | $16,966,464 |

| One Newark Center | ||||

| Note A-1 | No | — | CGCMT 2018-B2 | $32,000,000 |

| Note A-2 | Yes | — | BANK 2018-BNK10 | $20,000,000 |

| Note A-3 | No | — | BANK 2018-BNK10 | $14,580,000 |

| Braddock Metro Center | ||||

| Note A-1 | Yes | — | Benchmark 2018-B2 | $44,200,000 |

| Note A-2 | No | — | CGCMT 2018-B2 | $30,000,000 |

| Cross Point | ||||

| Note A-1 | Yes | Cantor Commercial Real Estate Lending, L.P. | Not Identified | $30,000,000 |

| Note A-2 | No | — | UBS 2018-C8 | $25,000,000 |

| Note A-3 | No | — | UBS 2018-C8 | $20,000,000 |

| Note A-4 | No | Cantor Commercial Real Estate Lending, L.P. | Not Identified | $20,000,000 |

| Note A-5 | No | — | CGCMT 2018-B2 | $15,000,000 |

| Note A-6 | No | — | CGCMT 2018-B2 | $10,000,000 |

| Note A-7 | No | Cantor Commercial Real Estate Lending, L.P. | Not Identified | $10,000,000 |

| Note A-8 | No | Cantor Commercial Real Estate Lending, L.P. | Not Identified | $10,000,000 |

| Note A-9 | No | — | UBS 2018-C8 | $5,000,000 |

| Note A-10 | No | Cantor Commercial Real Estate Lending, L.P. | Not Identified | $5,000,000 |

| Fort Knox Executive Park | ||||

| Note A-1 | Yes | — | CGCMT 2018-B2 | $19,000,000 |

| Note A-2 | No | Starwood Mortgage Funding II LLC | Not Identified | $16,000,000 |

| Warwick Mall | ||||

| Note A-1 | Yes | — | BANK 2017-BNK9 | $30,000,000 |

| Note A-2 | No | — | BANK 2018-BNK10 | $27,500,000 |

| Note A-3 | No | — | CGCMT 2018-B2 | $17,500,000 |

| Two Harbor Point Square | ||||

| Note A-1-A | Yes | — | CGCMT 2018-B2 | $10,000,000 |

| Note A-1-B | No | — | Benchmark 2018-B1 | $14,750,000 |

| Note A-2 | No | — | Benchmark 2018-B2 | $24,750,000 |

| (1) | The holder(s) of one or more specified controlling notes (collectively, the “Controlling Note”) will be the “controlling note holder(s)” entitled (directly or through a representative) to (a) approve or, in some cases, direct material servicing decisions involving the related loan combination (while the remaining such holder(s) generally are only entitled to non-binding consultation rights in such regard), and (b) in some cases, replace the applicable special servicer with respect to such loan combination with or without cause. See “Description of the Mortgage Pool—The Loan Combinations” and “The Pooling and Servicing Agreement—Directing Holder” in the Preliminary Prospectus. |

| (2) | The holder(s) of the note(s) other than the Controlling Note (each, a “Non-Controlling Note”) will be the “non-controlling note holder(s)” generally entitled (directly or through a representative) to certain non-binding consultation rights with respect to any decisions as to which the holder of the Controlling Note has consent rights involving the related loan combination, subject to certain exceptions, including that in certain cases where the related Controlling Note is a B-note or C-note such consultation rights will not be afforded to the holder(s) of the Non-Controlling Notes until after a control trigger event has occurred with respect to either such Controlling Note or certain certificates backed thereby, in each case as set forth in the related co-lender agreement. See “Description of the Mortgage Pool—The Loan Combinations“ in the Preliminary Prospectus. |

| (3) | Unless otherwise specified, with respect to each loan combination, any related unsecuritized Controlling Note and/or Non-Controlling Note may be further split, modified, combined and/or reissued (prior to its inclusion in a securitization transaction) as one or multiple Controlling Notes or Non-Controlling Notes, as the case may be, subject to the terms of the related co-lender agreement (including that the aggregate principal balance, weighted average interest rate and certain other material terms cannot be changed). In connection with the foregoing, any such split, modified or combined Controlling Note or Non-Controlling Note, as the case may be, may be transferred to one or multiple parties (not identified in the table above) prior to its inclusion in a future commercial mortgage securitization transaction. |

| (4) | Unless otherwise specified, with respect to each loan combination, each related unsecuritized pari passu companion loan (whether controlling or non-controlling) is expected to be contributed to one or more future commercial mortgage securitization transactions. Under the column “Current or Anticipated Holder of Securitized Note”, (i) the identification of a securitization trust means we have identified an outside securitization that has closed or as to which a preliminary prospectus or final prospectus has printed that has included or is expected to include the subject Controlling Note or Non-Controlling Note, as the case may be, (ii) “Not Identified” means the subject Controlling Note or Non-Controlling Note, as the case may be, has not been securitized and no preliminary prospectus or final prospectus has printed that identifies the future outside securitization that is expected to include the subject Controlling Note or Non-Controlling Note, and (iii) “Not Applicable” means the subject Controlling Note or Non-Controlling Note is not intended to be contributed to a future commercial mortgage securitization transaction. Under the column “Current Holder of Unsecuritized Note”, “—” means the subjectControlling Note or Non-Controlling Note is not an unsecuritized note and is currently held by the securitization trust referenced under the “Current or Anticipated Holder of Securitized Note” column. |

| (5) | With respect to the Red Building loan combination, pursuant to the related co-lender agreement, (i) the Controlling Note (so long as no “note C control appraisal period” is in effect) is note C, (ii) if a note C control appraisal period under the related co-lender agreement is in effect and no “note B control appraisal period” is in effect, then note B-1 will be the Controlling Note, and (iii) if a note B control appraisal period under the related co-lender agreement is in effect, then note A-1 will be the Controlling Note. |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-207132) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Morgan Stanley & Co. LLC, Merrill Lynch, Pierce, Fenner & Smith Incorporated, Drexel Hamilton, LLC, The Williams Capital Group, L.P. or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

11

COLLATERAL OVERVIEW (continued) |

Previously Securitized Mortgaged Properties(1)

Mortgaged Property Name | Mortgage | City | State | Property Type | Cut-off Date Balance / | % of Initial Pool | Previous | |||||||||

| Westin Tysons Corner | SMF V | Falls Church | Virginia | Hospitality | $48,000,000 | 4.5 | % | WBCMT 2006-C28 | ||||||||

| Oxford Exchange | SMF V | Oxford | Alabama | Retail | $36,900,000 | 3.5 | % | WFCG 2015-BXRP | ||||||||

| Axcelis Corporate Center | MSMCH | Beverly | Massachusetts | Industrial | $33,932,928 | 3.2 | % | COMM 2015-DC1 | ||||||||

| One Newark Center | MSMCH | Newark | New Jersey | Office | $32,000,000 | 3.0 | % | BSCMS 2006-PW14 | ||||||||

| Ingram Festival Shopping Center | SMF V | San Antonio | Texas | Retail | $27,424,564 | 2.6 | % | BSCMS 2007-PW18 | ||||||||

| Willows Hotel | CREFI | Chicago | Illinois | Hospitality | $8,828,031 | 0.8 | % | LBUBS 2008-C1 | ||||||||

| Majestic Hotel | CREFI | Chicago | Illinois | Hospitality | $8,678,404 | 0.8 | % | LBUBS 2008-C1 | ||||||||

| City Suites Hotel | CREFI | Chicago | Illinois | Hospitality | $6,683,368 | 0.6 | % | LBUBS 2008-C1 | ||||||||

| Stor-All Tchoupitoulas | BANA | New Orleans | Louisiana | Self Storage | $13,350,000 | 1.3 | % | CGCMT 2013-GC11 | ||||||||

| Stor-All Gentilly Woods | BANA | New Orleans | Louisiana | Self Storage | $10,150,000 | 1.0 | % | CGCMT 2013-GC11 | ||||||||

| Fort Knox Executive Park | SMF V | Tallahassee | Florida | Office | $19,000,000 | 1.8 | % | JPMCC 2005-LDP2 | ||||||||

| 8800 Queen Avenue South | CREFI | Bloomington | Minnesota | Mixed Use | $18,500,000 | 1.7 | % | LSPT 2015-LSMZ; LSPT 2015-LSP | ||||||||

| Boulder Ridge Apartments | SMF V | Tulsa | Oklahoma | Multifamily | $6,450,000 | 0.6 | % | FNA 2015-M10 | ||||||||

| (1) | The table above includes mortgaged properties securing mortgage loans for which the most recent prior financing of all or a significant portion of such mortgaged properties was included in a securitization. Information under “Previous Securitization” represents the most recent such securitization with respect to each of those mortgaged properties. The information in the above table is based solely on information provided by the related borrower or obtained through searches of a third-party database, and has not otherwise been confirmed by the mortgage loan sellers. |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-207132) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Morgan Stanley & Co. LLC, Merrill Lynch, Pierce, Fenner & Smith Incorporated, Drexel Hamilton, LLC, The Williams Capital Group, L.P. or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

12

(THIS PAGE INTENTIONALLY LEFT BLANK)

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-207132) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Morgan Stanley & Co. LLC, Merrill Lynch, Pierce, Fenner & Smith Incorporated, Drexel Hamilton, LLC, The Williams Capital Group, L.P. or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

13

COLLATERAL OVERVIEW (continued) |

Property Types

Property Type / Detail | Number of Mortgaged Properties | Aggregate | % of Initial | Wtd. Avg. | Wtd. Avg. | Wtd. Avg. Debt Yield on | ||||||||||||||||||

| Office | 20 | $279,665,327 | 26.3 | % | 1.88 | x | 59.1 | % | 11.8 | % | ||||||||||||||

| Suburban | 17 | 197,665,327 | 18.6 | 1.66 | x | 63.3 | % | 11.0 | % | |||||||||||||||

| CBD | 3 | 82,000,000 | 7.7 | 2.42 | x | 48.8 | % | 13.6 | % | |||||||||||||||

| Retail | 27 | $278,804,818 | 26.2 | % | 1.74 | x | 61.2 | % | 10.4 | % | ||||||||||||||

| Anchored | 12 | 177,913,679 | 16.7 | 1.74 | X | 62.0 | % | 10.5 | % | |||||||||||||||

| Lifestyle Center | 1 | 37,000,000 | 3.5 | 1.98 | x | 62.2 | % | 10.6 | % | |||||||||||||||

| Unanchored | 10 | 36,627,351 | 3.4 | 1.50 | x | 62.6 | % | 9.0 | % | |||||||||||||||

| Regional Mall | 1 | 17,500,000 | 1.6 | 2.01 | x | 47.5 | % | 13.3 | % | |||||||||||||||

| Single Tenant Retail | 2 | 9,000,000 | 0.8 | 1.30 | x | 63.5 | % | 7.6 | % | |||||||||||||||

| Shadow Anchored | 1 | 763,788 | 0.1 | 1.48 | x | 59.4 | % | 10.2 | % | |||||||||||||||

| Self Storage | 64 | $199,550,000 | 18.8 | % | 1.96 | x | 59.7 | % | 9.1 | % | ||||||||||||||

| Hospitality | 7 | $116,991,622 | 11.0 | % | 1.68 | x | 59.4 | % | 12.9 | % | ||||||||||||||

| Limited Service | 5 | 54,166,622 | 5.1 | 1.68 | x | 59.9 | % | 12.8 | % | |||||||||||||||

| Full Service | 1 | 48,000,000 | 4.5 | 1.61 | x | 60.8 | % | 12.5 | % | |||||||||||||||

| Extended Stay | 1 | 14,825,000 | 1.4 | 1.92 | x | 53.5 | % | 14.5 | % | |||||||||||||||

| Industrial | 10 | $81,762,367 | 7.7 | % | 1.70 | x | 58.8 | % | 10.9 | % | ||||||||||||||

| Flex | 8 | 60,709,598 | 5.7 | 1.62 | x | 58.2 | % | 11.1 | % | |||||||||||||||

| Warehouse/Distribution | 2 | 21,052,769 | 2.0 | 1.93 | x | 60.6 | % | 10.1 | % | |||||||||||||||

| Mixed Use | 7 | $78,400,569 | 7.4 | % | 1.72 | x | 61.6 | % | 9.9 | % | ||||||||||||||

| Parking/Retail | 2 | 45,700,000 | 4.3 | 1.67 | x | 60.4 | % | 8.5 | % | |||||||||||||||

| Office/Education | 1 | 18,500,000 | 1.7 | 1.77 | x | 69.5 | % | 12.6 | % | |||||||||||||||

| Office/Retail | 2 | 7,332,176 | 0.7 | 1.48 | x | 59.4 | % | 10.2 | % | |||||||||||||||

| Retail/Education | 1 | 3,543,393 | 0.3 | 1.48 | x | 59.4 | % | 10.2 | % | |||||||||||||||

| Multifamily/Retail | 1 | 3,325,000 | 0.3 | 3.02 | x | 41.8 | % | 14.0 | % | |||||||||||||||

| Multifamily (Garden) | 6 | $25,210,000 | 2.4 | % | 1.65 | x | 63.4 | % | 10.8 | % | ||||||||||||||

| Manufactured Housing | 1 | $2,000,000 | 0.2 | % | 1.30 | x | 69.7 | % | 10.4 | % | ||||||||||||||

| Total | 142 | $1,062,384,703 | 100.0 | % | 1.80 | x | 60.1 | % | 10.8 | % | ||||||||||||||

| (1) | Calculated based on the mortgaged property’s allocated loan amount for mortgage loans secured by more than one mortgaged property. |

| (2) | Weighted average based on the mortgaged property’s allocated loan amount for mortgage loans secured by more than one mortgaged property. |

| (3) | See footnotes to the table entitled “Mortgage Pool Characteristics” above. |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-207132) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Morgan Stanley & Co. LLC, Merrill Lynch, Pierce, Fenner & Smith Incorporated, Drexel Hamilton, LLC, The Williams Capital Group, L.P. or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

14

COLLATERAL OVERVIEW (continued) |

Geographic Distribution

Property Location | Number of Mortgaged Properties | Aggregate Cut-off Date Balance(1) | % of Initial | Aggregate Appraised Value(2) | % of Total Appraised | Underwritten NOI(2) | % of Total Underwritten NOI | ||||||||||||||

| California | 45 | $209,152,086 | 19.7 | % | $1,001,980,000 | 31.0 | % | $53,930,603 | 26.6 | % | |||||||||||

| Texas | 11 | 79,275,179 | 7.5 | 131,880,000 | 4.1 | 9,175,459 | 4.5 | ||||||||||||||

| Virginia | 2 | 78,000,000 | 7.3 | 190,140,000 | 5.9 | 13,049,610 | 6.4 | ||||||||||||||

| Minnesota | 3 | 72,750,000 | 6.8 | 105,300,000 | 3.3 | 7,612,240 | 3.8 | ||||||||||||||

| New Jersey | 9 | 70,779,362 | 6.7 | 203,200,000 | 6.3 | 14,527,312 | 7.2 | ||||||||||||||

| Massachusetts | 6 | 70,041,470 | 6.6 | 373,400,000 | 11.6 | 25,412,651 | 12.5 | ||||||||||||||

| Ohio | 4 | 49,423,493 | 4.7 | 81,920,000 | 2.5 | 6,565,951 | 3.2 | ||||||||||||||

| Florida | 5 | 49,113,576 | 4.6 | 130,700,000 | 4.0 | 8,575,863 | 4.2 | ||||||||||||||

| Nevada | 5 | 45,988,397 | 4.3 | 86,480,000 | 2.7 | 6,477,489 | 3.2 | ||||||||||||||

| Illinois | 6 | 41,739,804 | 3.9 | 73,300,000 | 2.3 | 4,118,794 | 2.0 | ||||||||||||||

| Alabama | 2 | 40,199,017 | 3.8 | 63,250,000 | 2.0 | 4,519,852 | 2.2 | ||||||||||||||

| Pennsylvania | 5 | 37,689,806 | 3.5 | 94,590,000 | 2.9 | 5,623,724 | 2.8 | ||||||||||||||

| Washington | 1 | 35,200,000 | 3.3 | 59,000,000 | 1.8 | 2,958,191 | 1.5 | ||||||||||||||

| New York | 4 | 33,718,724 | 3.2 | 79,500,000 | 2.5 | 4,537,569 | 2.2 | ||||||||||||||

| Louisiana | 2 | 23,500,000 | 2.2 | 37,850,000 | 1.2 | 2,167,950 | 1.1 | ||||||||||||||

| Connecticut | 4 | 19,869,587 | 1.9 | 111,480,000 | 3.5 | 7,673,201 | 3.8 | ||||||||||||||

| Rhode Island | 1 | 17,500,000 | 1.6 | 158,000,000 | 4.9 | 9,999,062 | 4.9 | ||||||||||||||

| Indiana | 3 | 15,560,000 | 1.5 | 23,080,000 | 0.7 | 1,717,915 | 0.8 | ||||||||||||||

| District of Columbia | 1 | 14,141,070 | 1.3 | 47,490,000 | 1.5 | 2,768,131 | 1.4 | ||||||||||||||

| Vermont | 1 | 12,750,000 | 1.2 | 18,600,000 | 0.6 | 1,762,581 | 0.9 | ||||||||||||||

| Maryland | 2 | 7,854,825 | 0.7 | 25,690,000 | 0.8 | 1,574,865 | 0.8 | ||||||||||||||

| Oklahoma | 1 | 6,450,000 | 0.6 | 11,100,000 | 0.3 | 686,807 | 0.3 | ||||||||||||||

| Georgia | 3 | 6,254,177 | 0.6 | 28,250,000 | 0.9 | 1,636,879 | 0.8 | ||||||||||||||

| Arkansas | 1 | 5,750,000 | 0.5 | 8,860,000 | 0.3 | 560,664 | 0.3 | ||||||||||||||

| Michigan | 1 | 4,000,000 | 0.4 | 6,380,000 | 0.2 | 315,176 | 0.2 | ||||||||||||||

| Delaware | 1 | 3,756,616 | 0.4 | 12,590,000 | 0.4 | 748,464 | 0.4 | ||||||||||||||

| Tennessee | 6 | 3,500,617 | 0.3 | 21,900,000 | 0.7 | 1,396,158 | 0.7 | ||||||||||||||

| Kansas | 2 | 3,273,799 | 0.3 | 11,290,000 | 0.3 | 670,852 | 0.3 | ||||||||||||||

| Arizona | 2 | 2,673,220 | 0.3 | 13,570,000 | 0.4 | 785,446 | 0.4 | ||||||||||||||

| New Mexico | 2 | 1,714,321 | 0.2 | 11,400,000 | 0.4 | 688,636 | 0.3 | ||||||||||||||

| Missouri | 1 | 765,556 | 0.1 | 5,100,000 | 0.2 | 304,396 | 0.2 | ||||||||||||||

| Total | 142 | $1,062,384,703 | 100.0 | % | $3,227,270,000 | 100.0 | % | $202,542,492 | 100.0 | % | |||||||||||

| (1) | Calculated based on the mortgaged property’s allocated loan amount for mortgage loans secured by more than one mortgaged property. |

| (2) | Aggregate Appraised Values and Underwritten NOI reflect the aggregate values without any reduction for the pari passu companion loan(s). |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-207132) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Morgan Stanley & Co. LLC, Merrill Lynch, Pierce, Fenner & Smith Incorporated, Drexel Hamilton, LLC, The Williams Capital Group, L.P. or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

15

| COLLATERAL OVERVIEW (continued) |

| Distribution of Cut-off Date Balances | ||||||||||

| Number | % of | |||||||||

| of | Initial | |||||||||

| Range of Cut-off Date | Mortgage | Cut-off Date | Pool | |||||||

| Balances ($) | Loans | Balance | Balance | |||||||

| 2,000,000 – 4,999,999 | 6 | $18,525,000 | 1.7 | % | ||||||

| 5,000,000 – 9,999,999 | 12 | 82,884,237 | 7.8 | |||||||

| 10,000,000 – 19,999,999 | 14 | 219,681,818 | 20.7 | |||||||

| 20,000,000 – 29,999,999 | 8 | 196,610,720 | 18.5 | |||||||

| 30,000,000 – 39,999,999 | 6 | 205,032,928 | 19.3 | |||||||

| 40,000,000 – 49,999,999 | 3 | 130,400,000 | 12.3 | |||||||

| 50,000,000 – 59,999,999 | 2 | 104,250,000 | 9.8 | |||||||

| 60,000,000 – 105,000,000 | 1 | 105,000,000 | 9.9 | |||||||

| Total | 52 | $1,062,384,703 | 100.0 | % | ||||||

| Distribution of UW NCF DSCRs(1) | ||||||||||

| Number | % of | |||||||||

| of | Initial | |||||||||

| Mortgage | Cut-off Date | Pool | ||||||||

| Range of UW DSCR (x) | Loans | Balance | Balance | |||||||

| 1.17 – 1.20 | 1 | $4,000,000 | 0.4 | % | ||||||

| 1.21 – 1.50 | 9 | 195,915,239 | 18.4 | |||||||

| 1.51 – 2.00 | 30 | 647,044,464 | 60.9 | |||||||

| 2.01 – 2.50 | 9 | 166,600,000 | 15.7 | |||||||

| 2.51 – 3.00 | 1 | 5,500,000 | 0.5 | |||||||

| 3.01 – 3.31 | 2 | 43,325,000 | 4.1 | |||||||

| Total | 52 | $1,062,384,703 | 100.0 | % | ||||||

| (1) See footnotes (1) and (5) to the table entitled “Mortgage Pool Characteristics” above. | ||||||||||

| Distribution of Amortization Types(1) | ||||||||||

| Number | % of | |||||||||

| of | Initial | |||||||||

| Mortgage | Cut-off Date | Pool | ||||||||

| Amortization Type | Loans | Balance | Balance | |||||||

| Amortizing (15 Years) | 1 | $9,958,925 | 0.9 | % | ||||||

| Amortizing (22 Years) | 1 | 2,000,000 | 0.2 | |||||||

| Amortizing (25 Years) | 2 | 52,932,928 | 5.0 | |||||||

| Amortizing (30 Years) | 8 | 173,094,851 | 16.3 | |||||||

| Interest Only, Then Amortizing(2) | 20 | 358,623,000 | 33.8 | |||||||

| Interest Only | 20 | 465,775,000 | 43.8 | |||||||

| Total | 52 | $1,062,384,703 | 100.0 | % | ||||||

| (1) All of the mortgage loans will have balloon payments at maturity date or have an anticipated repayment date, as applicable. | ||||||||||

| (2) Original partial interest only periods range from 12 to 60 months. | ||||||||||

| Distribution of Lockboxes | ||||||||||

| Number | % of | |||||||||

| of | Initial | |||||||||

| Mortgage | Cut-off Date | Pool | ||||||||

| Lockbox Type | Loans | Balance | Balance | |||||||

| Springing | 32 | $632,710,153 | 59.6 | % | ||||||

| Hard | 17 | 373,224,550 | 35.1 | |||||||

| Soft | 1 | 48,000,000 | 4.5 | |||||||

| None | 2 | 8,450,000 | 0.8 | |||||||

| Total | 52 | $1,062,384,703 | 100.0 | % | ||||||

| Distribution of Cut-off Date LTV Ratios(1) | ||||||||||

| Number | % of | |||||||||

| of | Initial | |||||||||

| Range of Cut-off Date | Mortgage | Cut-off Date | Pool | |||||||

| LTV (%) | Loans | Balance | Balance | |||||||

| 27.9 – 49.9 | 6 | $76,775,000 | 7.2 | % | ||||||

| 50.0 – 59.9 | 16 | 384,856,729 | 36.2 | |||||||

| 60.0 – 69.9 | 27 | 545,990,663 | 51.4 | |||||||

| 70.0 – 74.1 | 3 | 54,762,312 | 5.2 | |||||||

| Total | 52 | $1,062,384,703 | 100.0 | % | ||||||

| (1) See footnotes (1) and (4) to the table entitled “Mortgage Pool Characteristics” above. | ||||||||||

| Distribution of Maturity Date/ARD LTV Ratios(1) | ||||||||||

| Number | % of | |||||||||

| of | Initial | |||||||||

| Range of Maturity | Mortgage | Cut-off Date | Pool | |||||||

| Date/ARD LTV (%) | Loans | Balance | Balance | |||||||

| 25.0 – 49.9 | 13 | $205,681,656 | 19.4 | % | ||||||

| 50.0 – 59.9 | 25 | 529,540,735 | 49.8 | |||||||

| 60.0 – 66.8 | 14 | 327,162,312 | 30.8 | |||||||

| Total | 52 | $1,062,384,703 | 100.0 | % | ||||||

| (1) See footnotes (1) and (4) to the table entitled “Mortgage Pool Characteristics” above. | ||||||||||

| Distribution of Loan Purpose | ||||||||||

| Number | % of | |||||||||

| of | Initial | |||||||||

| Mortgage | Cut-off Date | Pool | ||||||||

| Loan Purpose | Loans | Balance | Balance | |||||||

| Refinance | 24 | $559,914,220 | 52.7 | % | ||||||

| Acquisition | 24 | 444,210,483 | 41.8 | |||||||

| Recapitalization | 4 | 58,260,000 | 5.5 | |||||||

| Total | 52 | $1,062,384,703 | 100.0 | % | ||||||

| Distribution of Mortgage Rates | ||||||||||

| Number | % of | |||||||||

| of | Initial | |||||||||

| Range of Mortgage | Mortgage | Cut-off Date | Pool | |||||||

| Rates (%) | Loans | Balance | Balance | |||||||

| 4.073 – 4.490 | 13 | $237,305,000 | 22.3 | % | ||||||

| 4.491 – 4.999 | 27 | 650,838,081 | 61.3 | |||||||

| 5.000 – 5.499 | 10 | 154,514,804 | 14.5 | |||||||

| 5.500 – 5.890 | 2 | 19,726,818 | 1.9 | |||||||

| Total | 52 | $1,062,384,703 | 100.0 | % | ||||||

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-207132) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Morgan Stanley & Co. LLC, Merrill Lynch, Pierce, Fenner & Smith Incorporated, Drexel Hamilton, LLC, The Williams Capital Group, L.P. or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

16

| COLLATERAL OVERVIEW (continued) |

| Distribution of Debt Yield on Underwritten NOI(1) | ||||||||||

| Number | % of | |||||||||

| Range of | of | Initial | ||||||||

| Debt Yields on | Mortgage | Cut-off Date | Pool | |||||||

| Underwritten NOI (%) | Loans | Balance | Balance | |||||||

| 7.4 – 7.9 | 3 | $26,550,000 | 2.5 | % | ||||||

| 8.0 – 8.9 | 4 | 108,650,000 | 10.2 | |||||||

| 9.0 – 9.9 | 9 | 252,782,312 | 23.8 | |||||||

| 10.0 – 10.9 | 15 | 306,250,492 | 28.8 | |||||||

| 11.0 – 22.5 | 21 | 368,151,900 | 34.7 | |||||||

| Total | 52 | $1,062,384,703 | 100.0 | % | ||||||

| (1) See footnotes (1) and (6) to the table entitled “Mortgage Pool Characteristics” above. | ||||||||||

| Distribution of Debt Yield on Underwritten NCF(1) | ||||||||||

| Number | % of | |||||||||

| Range of | of | Initial | ||||||||

| Debt Yields on | Mortgage | Cut-off Date | Pool | |||||||

| Underwritten NCF (%) | Loans | Balance | Balance | |||||||

| 7.1 – 7.9 | 3 | $26,550,000 | 2.5 | % | ||||||

| 8.0 – 8.9 | 8 | 190,450,000 | 17.9 | |||||||

| 9.0 – 9.9 | 17 | 437,232,803 | 41.2 | |||||||

| 10.0 – 10.9 | 14 | 265,566,156 | 25.0 | |||||||

| 11.0 – 18.6 | 10 | 142,585,743 | 13.4 | |||||||

| Total | 52 | $1,062,384,703 | 100.0 | % | ||||||

| (1) See footnotes (1) and (6) to the table entitled “Mortgage Pool Characteristics” above. | ||||||||||

| Mortgage Loans with Original Partial Interest Only Periods | ||||||||||

| Number | % of | |||||||||

| Original Partial | of | Initial | ||||||||

| Interest Only Period | Mortgage | Cut-off Date | Pool | |||||||

| (months) | Loans | Balance | Balance | |||||||

| 12 | 2 | $40,400,000 | 3.8 | % | ||||||

| 24 | 4 | $41,030,000 | 3.9 | % | ||||||

| 36 | 6 | $128,560,000 | 12.1 | % | ||||||

| 60 | 8 | $148,633,000 | 14.0 | % | ||||||

| Distribution of Original Terms to Maturity/ARD | ||||||||||

| Number | % of | |||||||||

| of | Initial | |||||||||

| Original Term to | Mortgage | Cut-off Date | Pool | |||||||

| Maturity/ARD (months) | Loans | Balance | Balance | |||||||

| 60 | 4 | $72,756,818 | 6.8 | % | ||||||

| 120 | 48 | 989,627,885 | 93.2 | |||||||

| Total | 52 | $1,062,384,703 | 100.0 | % | ||||||

| Distribution of Remaining Terms to Maturity/ARD | ||||||||||

| Number | % of | |||||||||

| Range of Remaining | of | Initial | ||||||||

| Terms to Maturity/ARD | Mortgage | Cut-off Date | Pool | |||||||

| (months) | Loans | Balance | Balance | |||||||

| 58 – 60 | 4 | $72,756,818 | 6.8 | % | ||||||

| 115 – 120 | 48 | 989,627,885 | 93.2 | |||||||

| Total | 52 | $1,062,384,703 | 100.0 | % | ||||||

| Distribution of Original Amortization Terms(1) | ||||||||||

| Number | % of | |||||||||

| of | Initial | |||||||||

| Original Amortization | Mortgage | Cut-off Date | Pool | |||||||

| Term (months) | Loans | Balance | Balance | |||||||

| Interest Only | 20 | $465,775,000 | 43.8 | % | ||||||

| 180 – 180 | 1 | 9,958,925 | 0.9 | |||||||

| 264 – 264 | 1 | 2,000,000 | 0.2 | |||||||

| 300 – 300 | 2 | 52,932,928 | 5.0 | |||||||