| FREE WRITING PROSPECTUS | ||

| FILED PURSUANT TO RULE 433 | ||

| REGISTRATION FILE NO.: 333-207132-17 | ||

March 19, 2018

Free Writing Prospectus

Structural and Collateral Term Sheet

$1,092,537,712

(Approximate Initial Mortgage Pool Balance)

$949,142,000

(Offered Certificates)

Benchmark 2018-B3 Commercial Mortgage Trust

As Issuing Entity

Citigroup Commercial Mortgage Securities Inc.

As Depositor

Commercial Mortgage Pass-Through Certificates, Series 2018-B3

German American Capital Corporation

JPMorgan Chase Bank, National Association

Citi Real Estate Funding Inc.

As Sponsors and Mortgage Loan Sellers

STATEMENT REGARDING THIS FREE WRITING PROSPECTUS

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-207132) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Deutsche Bank Securities Inc., J.P. Morgan Securities LLC, Drexel Hamilton, LLC or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

IMPORTANT NOTICE RELATING TO AUTOMATICALLY GENERATED EMAIL DISCLAIMERS

Any legends, disclaimers or other notices that may appear at the bottom of the email communication to which this free writing prospectus is attached relating to (1) these materials not constituting an offer (or a solicitation of an offer), (2) no representation being made that these materials are accurate or complete and that these materials may not be updated or (3) these materials possibly being confidential, are, in each case, not applicable to these materials and should be disregarded. Such legends, disclaimers or other notices have been automatically generated as a result of these materials having been sent via Bloomberg or another system.

| Citigroup | J.P. Morgan | Deutsche Bank Securities |

Co-Lead Managers and Joint Bookrunners

Drexel Hamilton

Co-Manager

The securities offered by this structural and collateral term sheet (this “Term Sheet”) are described in greater detail in the preliminary prospectus, dated on or about March 19, 2018, included as part of our registration statement (SEC File No. 333-207132) (the “Preliminary Prospectus”). The Preliminary Prospectus contains material information that is not contained in this Term Sheet (including, without limitation, a detailed discussion of risks associated with an investment in the offered securities under the heading“Risk Factors” in the Preliminary Prospectus). The Preliminary Prospectus is available upon request from Citigroup Global Markets Inc., Deutsche Bank Securities Inc., J.P. Morgan Securities LLC or Drexel Hamilton, LLC. This Term Sheet is subject to change.

For information regarding certain risks associated with an investment in this transaction, refer to “Risk Factors” in the Preliminary Prospectus. Capitalized terms used but not otherwise defined in this Term Sheet have the respective meanings assigned to those terms in the Preliminary Prospectus.

The Securities May Not Be a Suitable Investment for You

The securities offered by this Term Sheet are not suitable investments for all investors. In particular, you should not purchase any class of securities unless you understand and are able to bear the prepayment, credit, liquidity and market risks associated with that class of securities. For those reasons and for the reasons set forth under the heading “Risk Factors” in the Preliminary Prospectus, the yield to maturity of, the aggregate amount and timing of distributions on and the market value of the offered securities are subject to material variability from period to period and give rise to the potential for significant loss over the life of those securities. The interaction of these factors and their effects are impossible to predict and are likely to change from time to time. As a result, an investment in the offered securities involves substantial risks and uncertainties and should be considered only by sophisticated institutional investors with substantial investment experience with similar types of securities and who have conducted appropriate due diligence on the mortgage loans and the securities. Potential investors are advised and encouraged to review the Preliminary Prospectus in full and to consult with their legal, tax, accounting and other advisors prior to making any investment in the offered securities described in this Term Sheet.

The securities offered by these materials are being offered when, as and if issued. This Term Sheet is not to be construed as an offer to sell or the solicitation of any offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal. The information contained in this Term Sheet may not pertain to any securities that will actually be sold. The information contained in this Term Sheet may be based on assumptions regarding market conditions and other matters as reflected in this Term Sheet. We make no representations regarding the reasonableness of such assumptions or the likelihood that any of such assumptions will coincide with actual market conditions or events, and this Term Sheet should not be relied upon for such purposes. We and our affiliates, officers, directors, partners and employees, including persons involved in the preparation or issuance of this Term Sheet may, from time to time, have long or short positions in, and buy or sell, the securities mentioned in this Term Sheet or derivatives thereof (including options). Information contained in this Term Sheet is current as of the date appearing on this Term Sheet only. Information in this Term Sheet regarding the securities and the mortgage loans backing any securities discussed in this Term Sheet supersedes all prior information regarding such securities and mortgage loans. None ofCitigroup Global Markets Inc., Deutsche Bank Securities Inc., J.P. Morgan Securities LLC or Drexel Hamilton, LLCprovides accounting, tax or legal advice.

| The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-207132) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Deutsche Bank Securities Inc., J.P. Morgan Securities LLC, Drexel Hamilton, LLC or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146. |

2

The issuing entity will be relying on an exclusion or exemption from the definition of “investment company” under the Investment Company Act of 1940, as amended (the “Investment Company Act”), contained in Section 3(c)(5) of the Investment Company Act or Rule 3a-7 under the Investment Company Act, although there may be additional exclusions or exemptions available to the issuing entity. The issuing entity is being structured so as not to constitute a “covered fund” for purposes of the Volcker Rule under the Dodd-Frank Act (both as defined in “Risk Factors—Legal and Regulatory Provisions Affecting Investors Could Adversely Affect the Liquidity and Other Aspects of the Offered Certificates” in the Preliminary Prospectus). See also “Legal Investment” in the Preliminary Prospectus.

| The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-207132) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Deutsche Bank Securities Inc., J.P. Morgan Securities LLC, Drexel Hamilton, LLC or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146. |

3

| CERTIFICATE SUMMARY |

| OFFERED CERTIFICATES | |||||||||

Offered Classes | Expected Ratings | Approximate Initial Certificate Balance or Notional Amount(2) | Approximate Initial Credit Support(3) | Initial | Pass-Through Rate Description | Expected | Expected Principal Window(5) | ||

| Class A-1 | AAA(sf) / AAAsf / AAA(sf) | $25,000,000 | 30.000% | % | (6) | 2.42 | 5/18 - 6/22 | ||

| Class A-2 | AAA(sf) / AAAsf / AAA(sf) | $162,100,000 | 30.000% | % | (6) | 4.73 | 6/22 - 4/23 | ||

| Class A-3 | AAA(sf) / AAAsf / AAA(sf) | $66,600,000 | 30.000% | % | (6) | 6.68 | 12/24 - 2/25 | ||

| Class A-4 | AAA(sf) / AAAsf / AAA(sf) | (7) | 30.000% | % | (6) | (7) | 11/27 - 1/28 | ||

| Class A-5 | AAA(sf) / AAAsf / AAA(sf) | (7) | 30.000% | % | (6) | (7) | 1/28 - 2/28 | ||

| Class A-AB | AAA(sf) / AAAsf / AAA(sf) | $46,000,000 | 30.000% | % | (6) | 7.37 | 4/23 - 11/27 | ||

| Class X-A | NR / AAAsf / AAA(sf) | $849,448,000(8) | N/A | % | Variable IO(9) | N/A | N/A | ||

| Class X-B | NR / A-sf / AAA(sf) | $99,694,000(8) | N/A | % | Variable IO(9) | N/A | N/A | ||

| Class A-S | NR / AAAsf / AAA(sf) | $84,672,000 | 22.250% | % | (6) | 9.90 | 2/28 - 3/28 | ||

| Class B | NR / AA-sf / AA(sf) | $49,164,000 | 17.750% | % | (6) | 9.92 | 3/28 - 3/28 | ||

| Class C | NR / A-sf / A-(sf) | $50,530,000 | 13.125% | % | (6) | 9.92 | 3/28 - 3/28 | ||

| NON-OFFERED CERTIFICATES | |||||||||

Non-Offered Classes | Expected Ratings | Approximate Initial Certificate Balance | Approximate | Initial | Pass- | Expected | Expected Principal Window(5) | ||

| Class X-D | NR / BBB-sf / BBB(sf) | $36,873,000(8)(10) | N/A | % | Variable IO(9) | N/A | N/A | ||

| Class D | NR / BBB-sf / BBB(sf) | $36,873,000(10) | 9.750%(10) | % | (6) | 9.92 | 3/28 - 3/28 | ||

| Class E-RR(11) | NR / BBB-sf / BBB-(sf) | $21,851,000(10) | 7.750% | % | (6) | 9.92 | 3/28 - 3/28 | ||

| Class F-RR(11) | NR / BB+sf / BB+(sf) | $12,291,000 | 6.625% | % | (6) | 9.92 | 3/28 - 3/28 | ||

| Class G-RR(11) | NR / BB-sf / BB-(sf) | $12,291,000 | 5.500% | % | (6) | 9.92 | 3/28 - 3/28 | ||

| Class H-RR(11) | NR / B-sf / B-(sf) | $15,022,000 | 4.125% | % | (6) | 9.92 | 3/28 - 3/28 | ||

| Class NR-RR(11) | NR / NR / NR | $45,067,711 | 0.000% | % | (6) | 9.96 | 3/28 - 4/28 | ||

| Class S(12) | N/A | N/A | N/A | N/A | N/A | N/A | N/A | ||

| Class R(12) | N/A | N/A | N/A | N/A | N/A | N/A | N/A | ||

| (1) | It is a condition of issuance that the offered certificates and certain classes of non-offered certificates receive the ratings set forth above. The anticipated ratings shown are those of S&P Global Ratings, a Standard & Poor’s Financial Services LLC business (“S&P”), Fitch Ratings, Inc. (“Fitch”) and Kroll Bond Rating Agency, Inc. (“KBRA”). Subject to the discussion under “Ratings” in the Preliminary Prospectus, the ratings on the certificates address the likelihood of the timely receipt by holders of all payments of interest to which they are entitled on each distribution date and, except in the case of the interest only certificates, the ultimate receipt by holders of all payments of principal to which they are entitled on or before the applicable rated final distribution date. Certain nationally recognized statistical rating organizations, as defined in Section 3(a)(62) of the Securities Exchange Act of 1934, as amended, that were not hired by the depositor may use information they receive pursuant to Rule 17g-5 under the Securities Exchange Act of 1934, as amended, or otherwise to rate the offered certificates. We cannot assure you as to what ratings a non-hired nationally recognized statistical rating organization would assign. See “Risk Factors—Nationally Recognized Statistical Rating Organizations May Assign Different Ratings to the Certificates; Ratings of the Certificates Reflect Only the Views of the Applicable Rating Agencies as of the Dates Such Ratings Were Issued; Ratings May Affect ERISA Eligibility; Ratings May Be Downgraded” in the Preliminary Prospectus. S&P, Fitch and KBRA have informed us that the “sf” designation in the ratings represents an identifier of structured finance product ratings. For additional information about this identifier, prospective investors can go to the related rating agency’s website. The depositor and the underwriters have not verified, do not adopt and do not accept responsibility for any statements made by the rating agencies on those websites. Credit ratings referenced throughout this Term Sheet are forward-looking opinions about credit risk and express a rating agency’s opinion about the willingness and ability of an issuer of securities to meet its financial obligations in full and on time. Ratings are not indications of investment merit and are not buy, sell or hold recommendations, a measure of asset value or an indication of the suitability of an investment. |

| (2) | Approximate, subject to a variance of plus or minus 5% and further subject to (i) any variation in the certificate balances of the Class A-4 certificates and the Class A-5 certificates, as described in footnote (7) below, and (ii) any variation in the certificate balances of the Class D certificates and the Class E-RR Certificates following calculation of the actual fair value of all of the “ABS interests” (as such term is defined in Regulation RR) issued by the issuing entity, as described in footnote (10) below and under “Credit Risk Retention” in the Preliminary Prospectus. In addition, the notional amounts of the Class X-A, Class X-B and Class X-D certificates may vary depending upon the final pricing of the classes of Principal Balance Certificates (as defined in footnote (6) below) whose certificate balances comprise such notional amounts, and, if as a result of such pricing the pass-through rate of any class of the Class X-A, Class X-B or Class X-D certificates, as applicable, would be equal to zero at all times, such class of certificates will not be issued on the closing date of this securitization. |

| (3) | The approximate initial credit support percentages set forth for the Class A-1, Class A-2, Class A-3, Class A-4, Class A-5 and Class A-AB certificates are represented in the aggregate. |

| (4) | Approximateper annum rate as of the Closing Date. |

| (5) | Determined assuming no prepayments prior to the maturity date or any anticipated repayment date, as applicable, for anymortgage loan and based on the modeling assumptions describedunder “Yield, Prepayment and Maturity Considerations” in the Preliminary Prospectus. |

| (6) | For any distribution date, the pass-through rate for each class of the Class A-1, Class A-2, Class A-3, Class A-4, Class A-5, Class A-AB, Class A-S, Class B, Class C, Class D, Class E-RR, Class F-RR, Class G-RR, Class H-RR and Class NR-RR certificates (collectively, the “Principal Balance Certificates”) will generally be equal to one of (i) a fixedper annum rate, (ii) the weighted average of the net interest rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) as in effect from time to time, (iii) a rate equal to the lesser of a specifiedper annum rate and the weighted average rate described in clause (ii), or (iv) the weighted average rate described in clause (ii) less a specified percentage, but no less than 0.000%, as describedunder“Description of the Certificates—Distributions—Pass-Through Rates” in the Preliminary Prospectus. |

| The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-207132) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Deutsche Bank Securities Inc., J.P. Morgan Securities LLC, Drexel Hamilton, LLC or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146. |

4

| CERTIFICATE SUMMARY (continued) |

| (7) | The exact initial certificate balances of the Class A-4 and Class A-5 certificates are unknown and will be determined based on the final pricing of those classes of certificates. However, the respective initial certificate balances and weighted average lives of the Class A-4 and Class A-5 certificates are expected to be within the applicable ranges reflected in the following chart. The aggregate initial certificate balance of the Class A-4 and Class A-5 certificates is expected to be approximately $465,076,000, subject to a variance of plus or minus 5%. |

Class of | Expected Range of Initial | Expected Range of Weighted Avg. Life (Yrs) | ||

| Class A-4 | $75,000,000 - $175,000,000 | 9.60 – 9.69 | ||

| Class A-5 | $290,076,000 - $390,076,000 | 9.79 – 9.78 |

(8) | The Class X-A, Class X-B and Class X-D certificates (collectively, the “Class X Certificates”) will not have certificate balances and will not be entitled to receive distributions of principal. Interest will accrue on each class of Class X Certificates at the related pass-through rate based upon the related notional amount. The notional amount of each class of the Class X Certificates will be equal to the certificate balance or the aggregate of the certificate balances, as applicable, from time to time of the class or classes of the Principal Balance Certificates identified in the same row as such class of Class X Certificates in the chart below (as to such class of Class X Certificates, the “Corresponding Principal Balance Certificates”): |

| Class of Class X Certificates | Class(es) of Corresponding Principal Balance Certificates |

| Class X-A | Class A-1, Class A-2, Class A-3, Class A-4, Class A-5, Class A-AB and Class A-S |

| Class X-B | Class B and Class C |

| Class X-D | Class D |

| (9) | The pass-through rate for each class of Class X Certificates will generally be aper annumrate equal to the excess, if any, of (i) the weighted average of the net interest rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) as in effect from time to time, over (ii) the pass-through rate (or, if applicable, the weighted average of the pass-through rates) of the class or classes of Corresponding Principal Balance Certificates as in effect from time to time, as described in the Preliminary Prospectus. |

| (10) | The approximate initial certificate balances of the Class D and Class E-RR certificates are estimated based in part on the estimated ranges of initial certificate balances and estimated fair values described in “Credit Risk Retention” in the Preliminary Prospectus, with the ultimate initial certificate balances of the Class D and Class E-RR certificates determined such that, upon initial issuance, the aggregate fair value of the RR Certificates will equal at least 5% of the estimated fair value of all ABS interests issued by the issuing entity. The respective initial certificate balances of the Class D and Class E-RR certificates and the approximate initial credit support for the Class D certificates are expected to be within the applicable ranges reflected in the following chart. The aggregate initial certificate balance of the Class D and Class E-RR certificates is expected to be approximately $58,724,000, subject to a variance of plus or minus 5%. |

Class of | Expected Range of Initial | Expected Range of Approximate Initial Credit Support | ||

| Class D | $35,015,000 - $38,293,000 | 9.920% - 9.620% | ||

| Class E-RR | $20,431,000 - $23,709,000 | 7.750% |

| (11) | In satisfaction of the risk retention obligations of Citi Real Estate Funding Inc. (as retaining sponsor) with respect to this transaction, all of the Class E-RR, Class F-RR, Class G-RR, Class H-RR and Class NR-RR certificates (collectively, the “RR Certificates”), with an aggregate fair value expected to represent at least 5.0% of the fair value, as of the closing date for this transaction, of all ABS interests issued by the issuing entity, will collectively constitute an “eligible horizontal residual interest” (as such term is defined in Regulation RR) that is to be purchased and retained byKKR Real Estate Credit Opportunity Partners Aggregator I L.P., a Delaware limited partnership, througha “majority-owned affiliate” (as such term is defined in Regulation RR), in accordance with the credit risk retention rules applicable to this securitization transaction. See “Credit Risk Retention” in the Preliminary Prospectus. |

| (12) | Neither the Class S certificates nor the Class R certificates will have a certificate balance, notional amount, pass-through rate, rating or rated final distribution date.Excess interest accruing after the related anticipated repayment date on any mortgage loan with an anticipated repayment date will, to the extent collected, be allocated to the Class S certificates as set forth in “Description of the Certificates—Distributions—Excess Interest” in the Preliminary Prospectus.The Class R certificates will represent the residual interests in each of two separate REMICs, as further described in the Preliminary Prospectus. The Class R certificates will not be entitled to distributions of principal or interest. |

| The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-207132) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Deutsche Bank Securities Inc., J.P. Morgan Securities LLC, Drexel Hamilton, LLC or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146. |

5

| MORTGAGE POOL CHARACTERISTICS |

| Mortgage Pool Characteristics(1) | |

| Initial Pool Balance(2) | $1,092,537,712 |

| Number of Mortgage Loans | 45 |

| Number of Mortgaged Properties | 75 |

| Average Cut-off Date Balance | $24,278,616 |

| Weighted Average Mortgage Rate | 4.57607% |

| Weighted Average Remaining Term to Maturity/ARD (months)(3) | 107 |

| Weighted Average Remaining Amortization Term (months)(4) | 351 |

| Weighted Average Cut-off Date LTV Ratio(5) | 60.0% |

| Weighted Average Maturity Date/ARD LTV Ratio(3)(5) | 55.6% |

| Weighted Average UW NCF DSCR(6) | 1.91x |

| Weighted Average Debt Yield on Underwritten NOI(7) | 10.8% |

| % of Initial Pool Balance of Mortgage Loans that are Amortizing Balloon | 24.6% |

| % of Initial Pool Balance of Mortgage Loans that are Interest Only then Amortizing Balloon | 29.7% |

| % of Initial Pool Balance of Mortgage Loans that are Interest Only | 45.7% |

| % of Initial Pool Balance of Mortgaged Properties with Single Tenants | 12.1% |

| % of Initial Pool Balance of Mortgage Loans with Mezzanine Debt | 17.1% |

| % of Initial Pool Balance of Mortgage Loans with Subordinate Debt | 4.6% |

| (1) | The Cut-off Date LTV Ratio, Maturity Date/ARD LTV Ratio, UW NCF DSCR, Debt Yield on Underwritten NOI and Cut-off Date Balance Per SF / Rooms information for each mortgage loan is presented in this Term Sheet (i) if such mortgage loan is part of a loan combination (as defined under “Collateral Overview—Loan Combination Summary” below), based on both that mortgage loan and any related pari passu companion loan(s) but, unless otherwise specifically indicated, without regard to any related subordinate companion loan(s), and (ii) unless otherwise specifically indicated, without regard to any other indebtedness (whether or not secured by the related mortgaged property, ownership interests in the related borrower or otherwise) that currently exists or that may be incurred by the related borrower or its owners in the future. |

| (2) | Subject to a permitted variance of plus or minus 5%. |

| (3) | Unless otherwise indicated, mortgage loans with anticipated repayment dates are presented as if they were to mature on the anticipated repayment date. |

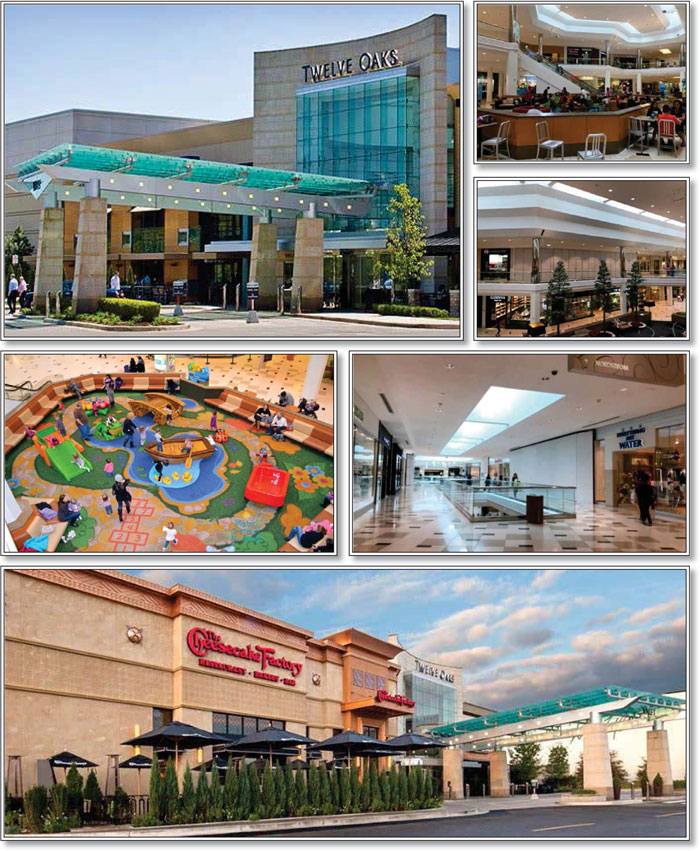

| (4) | Excludes mortgage loans that are interest-only for the entire term. In addition, the Twelve Oaks Mall mortgage loan provides for amortizing debt service payments based on the non-standard amortization schedule set forth on Annex G to the Preliminary Prospectus. Although such mortgage loan is reflected in the table above as having a remaining amortization term of 359 months, the related amortization is non-standard and not straight-line. |

| (5) | The Cut-off Date LTV Ratios and Maturity Date/ARD LTV Ratios presented in this Term Sheet are generally based on the “as-is” appraised values of the related mortgaged properties (as set forth on Annex A to the Preliminary Prospectus),provided that such LTV ratios may be calculated (i) based on “as-stabilized” or similar values in certain cases where the completion of certain hypothetical conditions or other events at the property are assumed and/or where reserves have been established at origination to satisfy the applicable condition or event that is expected to occur or (ii) based on the Cut-off Date Balance net of a related earnout or holdback reserve, in each case as further described in the definitions of “Appraised Value”, “Cut-off Date LTV Ratio” and “Maturity Date/ARD LTV Ratio” under “Description of the Mortgage Pool—Certain Calculations and Definitions” in the Preliminary Prospectus. |

| (6) | The UW NCF DSCR for each mortgage loan is generally calculated by dividing the UW NCF for the related mortgaged property or mortgaged properties by the annual debt service for such mortgage loan, as adjusted in the case of mortgage loans with a partial interest only period by using the first 12 amortizing payments due instead of the actual interest only payment due. With respect to the Twelve Oaks Mall mortgage loan, the UW NCF DSCR is calculated based on the annual debt service equal to the aggregate of the first 12 payments on the mortgage loan following the Closing Date as set forth in the non-standard amortization schedule set forth on Annex G of the Preliminary Prospectus. See the definition of “UW NCF DSCR” under “Description of the Mortgage Pool—Certain Calculations and Definitions” in the Preliminary Prospectus. |

| (7) | The Debt Yield on Underwritten NOI for each mortgage loan is generally calculated as the related mortgaged property’s Underwritten NOI divided by the Cut-off Date Balance of such mortgage loan, and the Debt Yield on Underwritten NCF for each mortgage loan is generally calculated as the related mortgaged property’s Underwritten NCF divided by the Cut-off Date Balance of such mortgage loan;provided, that such Debt Yields may be calculated based on the Cut-off Date Balance net of a related earnout or holdback reserve, as further described in the definitions of “Debt Yield on Underwritten NOI” and “Debt Yield on Underwritten NCF” under“Description of the Mortgage Pool—Certain Calculations and Definitions” in the Preliminary Prospectus. |

| The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-207132) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Deutsche Bank Securities Inc., J.P. Morgan Securities LLC, Drexel Hamilton, LLC or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146. |

6

| KEY FEATURES OF THE CERTIFICATES |

| Co-Lead Managers and Joint Bookrunners: | Citigroup Global Markets Inc. Deutsche Bank Securities Inc. J.P. Morgan Securities LLC |

| Co-Manager: | Drexel Hamilton, LLC |

| Depositor: | Citigroup Commercial Mortgage Securities Inc. |

| Initial Pool Balance: | $1,092,537,712 |

| Master Servicer: | Midland Loan Services, a Division of PNC Bank, National Association |

| Special Servicer: | Midland Loan Services, a Division of PNC Bank, National Association |

| Certificate Administrator: | Citibank, N.A. |

| Trustee: | Wilmington Trust, National Association

|

| Operating Advisor: | Park Bridge Lender Services LLC

|

| Asset Representations Reviewer: | Park Bridge Lender Services LLC

|

| Credit Risk Retention: | For a discussion on the manner in which the U.S. credit risk retention requirements are being satisfied by Citi Real Estate Funding Inc., as retaining sponsor, see “Credit Risk Retention” in the Preliminary Prospectus. Note that this securitization transaction is not structured to satisfy the EU risk retention and due diligence requirements.

|

| Closing Date: | On or about April 10, 2018

|

| Cut-off Date: | With respect to each mortgage loan, the due date in April 2018 for that mortgage loan (or, in the case of any mortgage loan that has its first due date subsequent to April 2018, the date that would have been its due date in April 2018 under the terms of that mortgage loan if a monthly payment were scheduled to be due in that month)

|

| Determination Date: | The 6th day of each month or next business day, commencing in May 2018

|

| Distribution Date: | The 4th business day after the Determination Date, commencing in May 2018

|

| Interest Accrual: | Preceding calendar month

|

| ERISA Eligible: | The offered certificates are expected to be ERISA eligible, subject to the exemption conditions described in the Preliminary Prospectus

|

| SMMEA Eligible: | No |

| Payment Structure: | Sequential Pay |

| Day Count: | 30/360 |

| Tax Structure: | REMIC |

| Rated Final Distribution Date: | April 2051 |

| Cleanup Call: | 1.0% |

| Minimum Denominations: | $10,000 minimum for the offered certificates (other than the Class X-A and Class X-B certificates); $1,000,000 minimum for the Class X-A and Class X-B certificates; and integral multiples of $1 thereafter for all the offered certificates |

| Delivery: | Book-entry through DTC |

| Bond Information: | Cash flows are expected to be modeled by TREPP, INTEX and BLOOMBERG |

| The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-207132) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Deutsche Bank Securities Inc., J.P. Morgan Securities LLC, Drexel Hamilton, LLC or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146. |

7

| TRANSACTION HIGHLIGHTS |

| ■ | $1,092,537,711 (Approximate) New-Issue Multi-Borrower CMBS: |

| — | Overview:The mortgage pool consists of 45 fixed-rate commercial mortgage loans that have an aggregate Cut-off Date Balance of $1,092,537,712 (the “Initial Pool Balance”), have an average mortgage loan Cut-off Date Balance of $24,278,616 and are secured by 75 mortgaged properties located throughout 22 states. |

| — | LTV:60.0% weighted average Cut-off Date LTV Ratio |

| — | DSCR:1.91x weighted average Underwritten Debt Service Coverage Ratio |

| — | Debt Yield: 10.8% weighted average Debt Yield on Underwritten NOI |

| — | Credit Support: 30.000% credit support to Class A-1 / A-2 / A-3 / A-4 / A-5 / A-AB |

| ■ | Loan Structural Features: |

| — | Amortization:54.3% of the mortgage loans by Initial Pool Balance have scheduled amortization: |

–24.6% of the mortgage loans by Initial Pool Balance have amortization for the entire term with a balloon payment due at maturity

–29.7% of the mortgage loans by Initial Pool Balance have scheduled amortization following a partial interest only period with a balloon payment due at maturity

| — | Hard Lockboxes: 62.6% of the mortgage loans by Initial Pool Balance have a Hard Lockbox in place |

| — | Cash Traps: 90.4% of the mortgage loans by Initial Pool Balance have cash traps triggered by certain declines in cash flow, all at levels equal to or greater than a 1.05x coverage, that fund an excess cash flow reserve |

| — | Reserves:The mortgage loans require amounts to be escrowed for reserves as follows: |

–Real Estate Taxes: 32 mortgage loans representing 60.8% of the Initial Pool Balance

–Insurance: 18 mortgage loans representing 27.4% of the Initial Pool Balance

–Replacement Reserves (Including FF&E Reserves): 29 mortgage loans representing 53.0% of the Initial Pool Balance

–Tenant Improvements / Leasing Commissions: 20 mortgage loans representing 67.3% of the portion of the Initial Pool Balance that is secured by office, retail, industrial and mixed use properties

| — | Predominantly Defeasance Mortgage Loans: 74.1% of the mortgage loans by Initial Pool Balance permit defeasance only after an initial lockout period |

| ■ | Multiple-Asset Types > 5.0% of the Initial Pool Balance: |

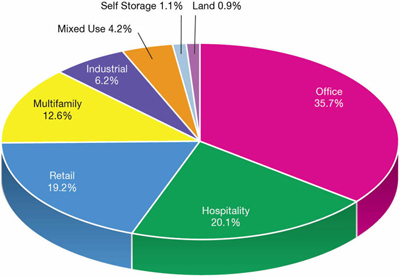

| — | Office:35.7% of the mortgaged properties by allocated Initial Pool Balance are office properties |

| — | Hospitality:20.1% of the mortgaged properties by allocated Initial Pool Balance are hospitality properties |

| — | Retail:19.2% of the mortgaged properties by allocated Initial Pool Balance are retail properties (5.3% are anchored retail properties) |

| — | Multifamily:12.6% of the mortgaged properties by allocated Initial Pool Balance are multifamily properties |

| — | Industrial:6.2% of the mortgaged properties by allocated Initial Pool Balance are industrial properties |

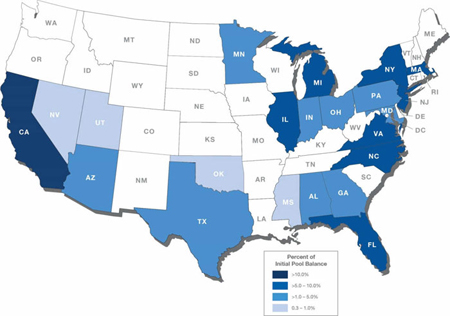

| ■ | Geographic Diversity: The 75 mortgaged properties are located throughout 22 states, with only one state having greater than 10.0% of the allocated Initial Pool Balance: California (23.7%) |

| The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-207132) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Deutsche Bank Securities Inc., J.P. Morgan Securities LLC, Drexel Hamilton, LLC or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146. |

8

| COLLATERAL OVERVIEW |

Mortgage Loans by Loan Seller

Mortgage Loan Seller | Mortgage Loans | Mortgaged Properties | Aggregate Cut-off | % of Initial | ||||||

| German American Capital Corporation | 17 | 20 | $467,894,811 | 42.8 | % | |||||

| JPMorgan Chase Bank, National Association | 12 | 13 | 386,127,961 | 35.3 | ||||||

| Citi Real Estate Funding Inc. | 16 | 42 | 238,514,940 | 21.8 | ||||||

| Total | 45 | 75 | $1,092,537,712 | 100.0 | % | |||||

Ten Largest Mortgage Loans(1)(2)

# | Mortgage Loan Name | Cut-off Date | % of Initial | Property Type | Property | Cut-off Date | UW | UW | Cut-off | ||||||||||||||||

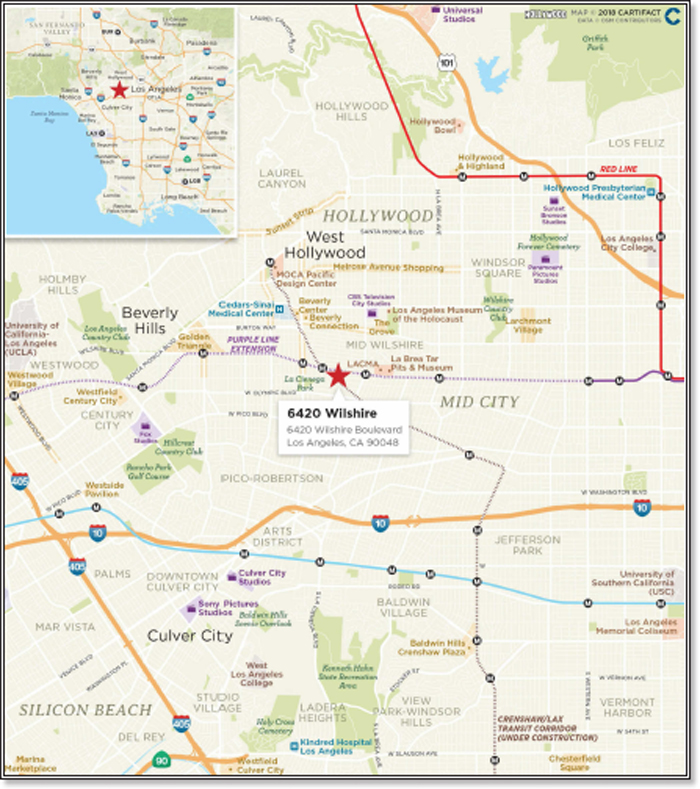

| 1 | 6420 Wilshire | $62,000,000 | 5.7 | % | Office | 204,035 | $304 | 1.98 | x | 9.2 | % | 64.6 | % | ||||||||||||

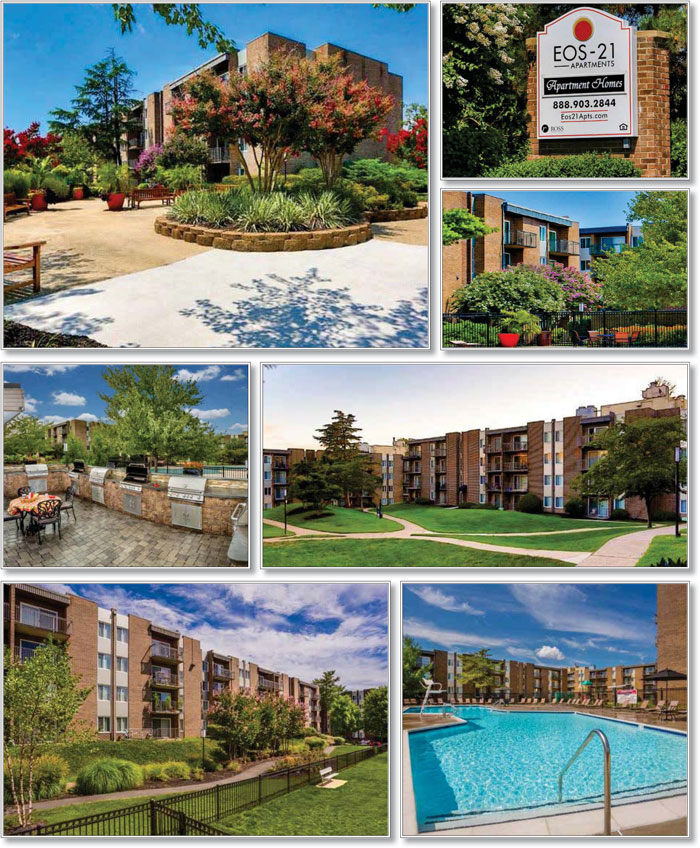

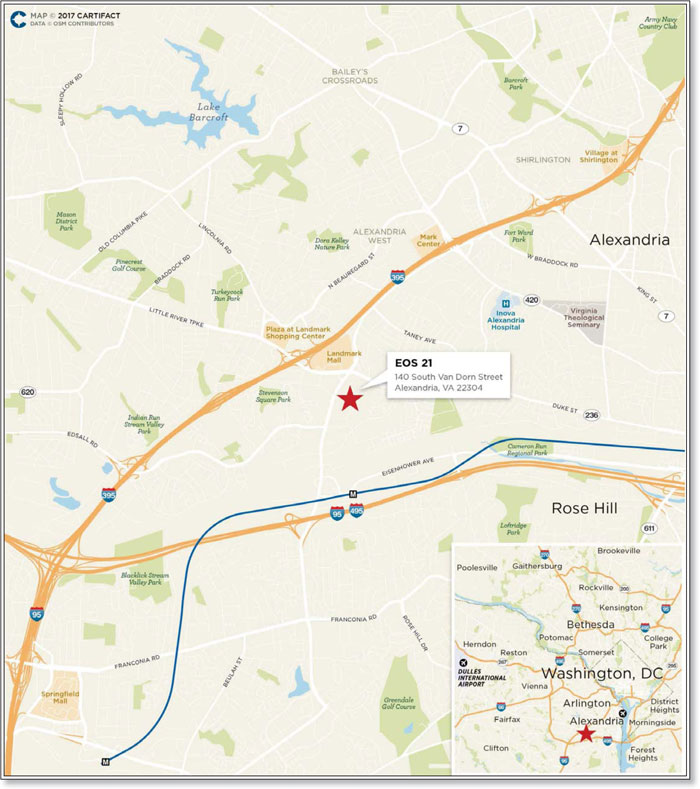

| 2 | EOS 21 | 60,000,000 | 5.5 | Multifamily | 1,180 | $127,119 | 1.87 | x | 7.5 | % | 64.8 | % | |||||||||||||

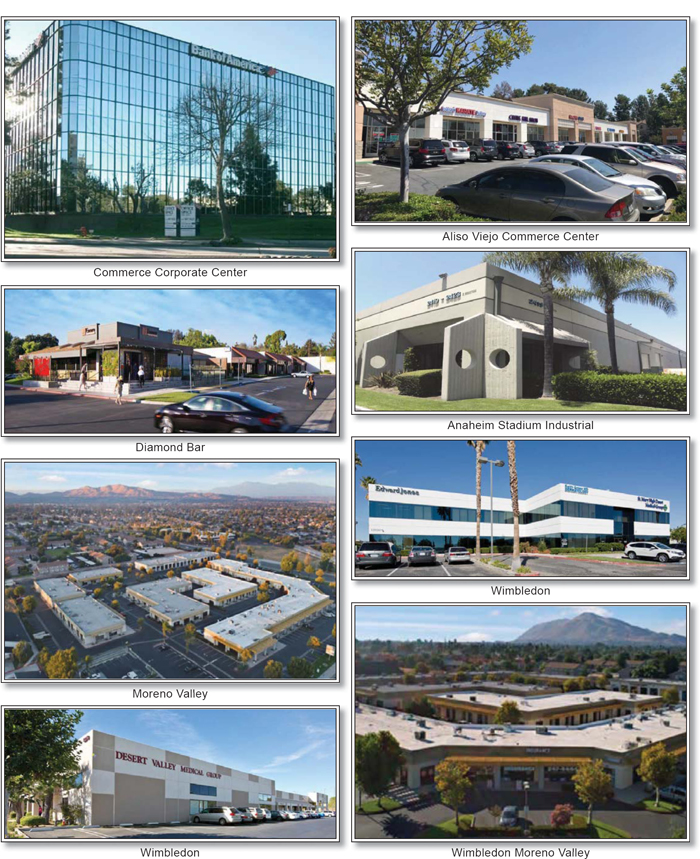

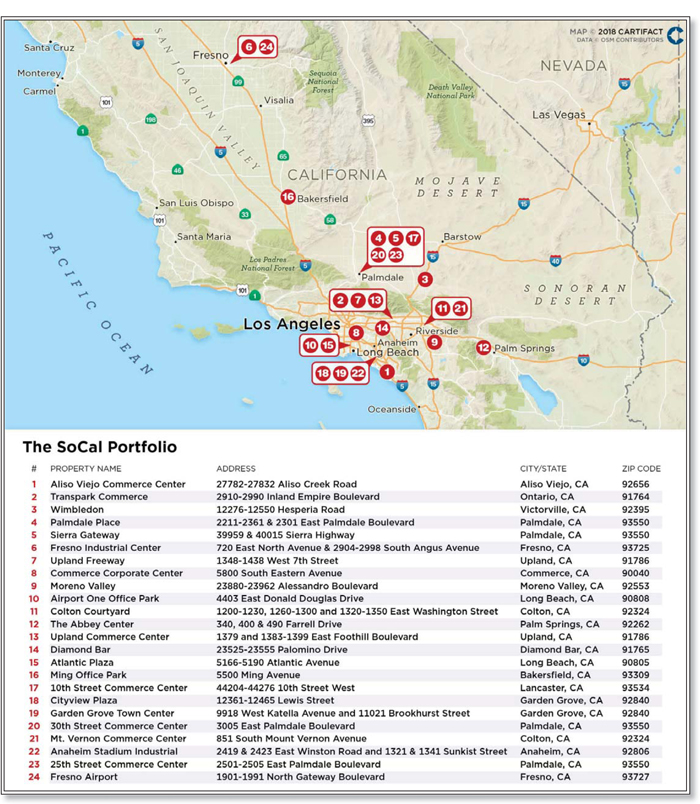

| 3 | The SoCal Portfolio | 50,000,000 | 4.6 | Various | 2,194,425 | $104 | 1.48 | x | 10.2 | % | 59.4 | % | |||||||||||||

| 4 | Twelve Oaks Mall | 49,944,961 | 4.6 | Retail | 709,771 | $281 | 2.55 | x | 15.3 | % | 36.1 | % | |||||||||||||

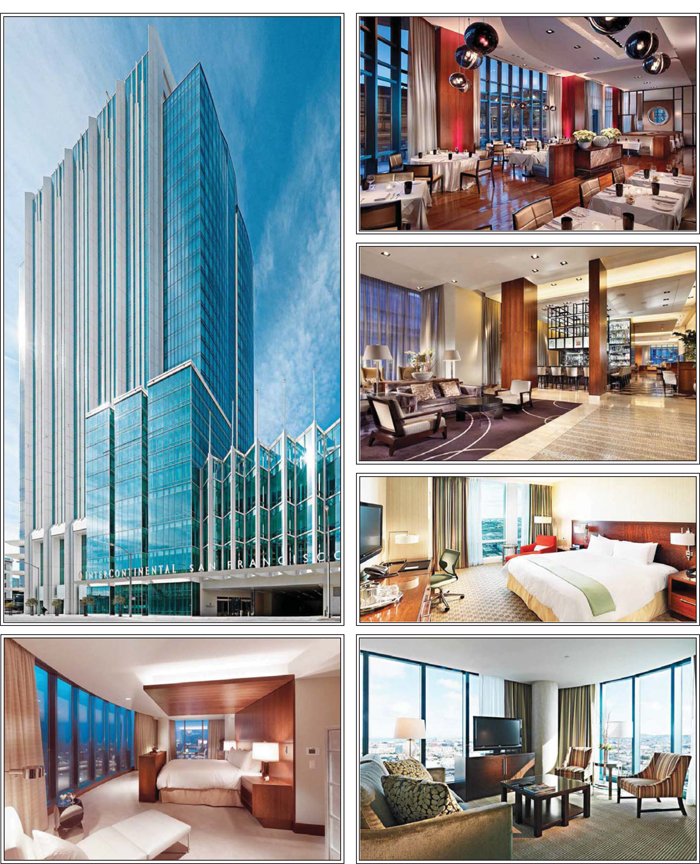

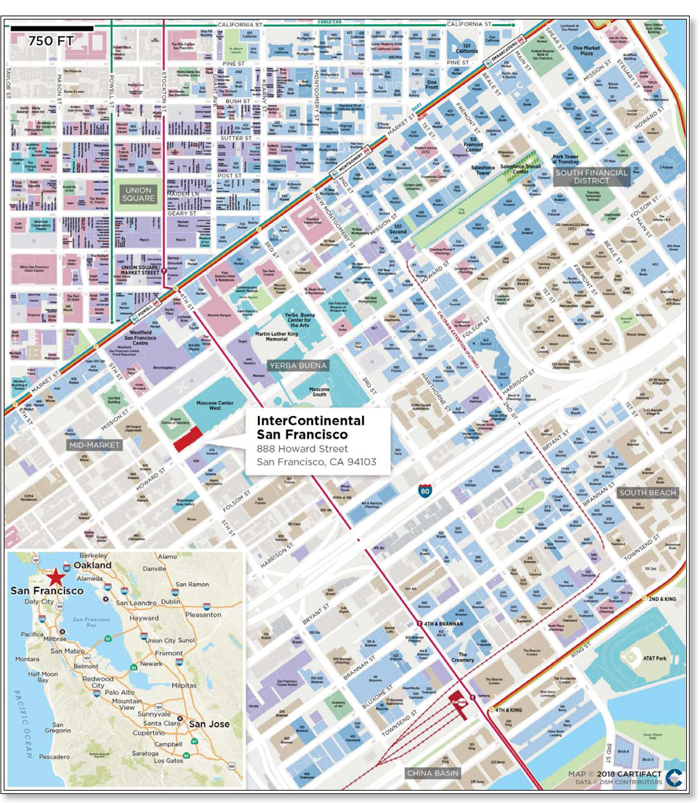

| 5 | InterContinental San Francisco | 49,788,676 | 4.6 | Hospitality | 550 | $199,155 | 2.29 | x | 16.1 | % | 41.8 | % | |||||||||||||

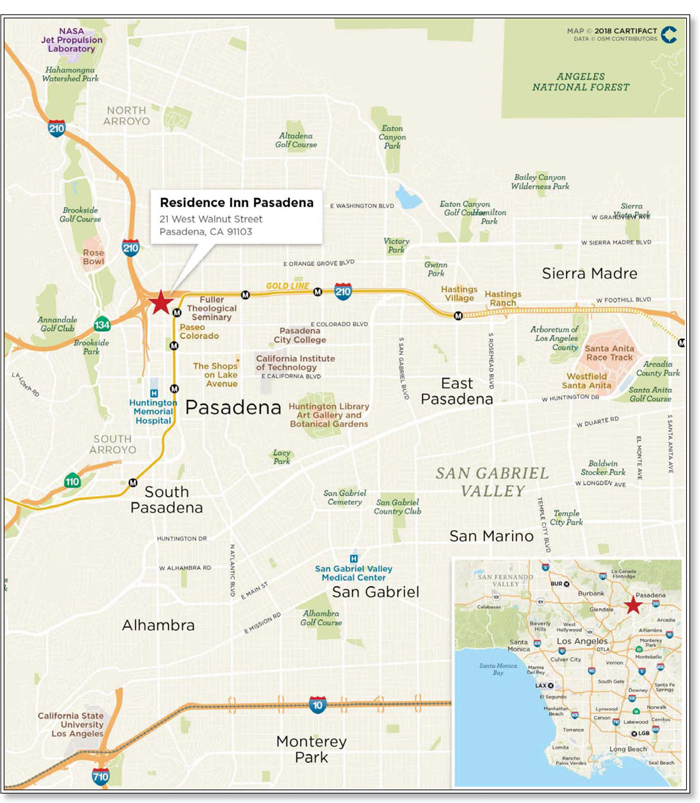

| 6 | Residence Inn Pasadena | 47,322,293 | 4.3 | Hospitality | 144 | $328,627 | 1.77 | x | 12.1 | % | 66.0 | % | |||||||||||||

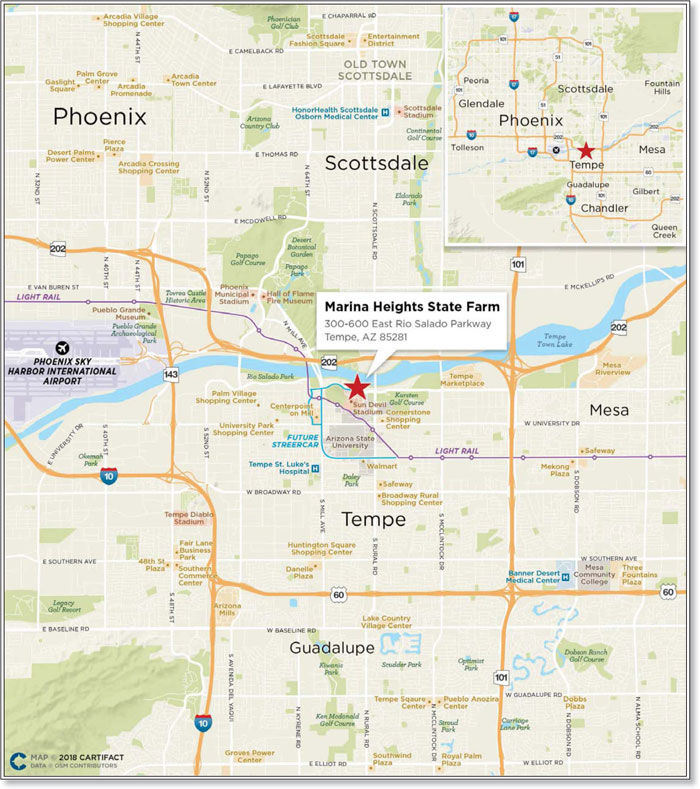

| 7 | Marina Heights State Farm | 45,000,000 | 4.1 | Office | 2,031,293 | $276 | 3.12 | x | 11.3 | % | 58.3 | % | |||||||||||||

| 8 | CrossPoint | 45,000,000 | 4.1 | Office | 1,320,254 | $114 | 2.24 | x | 11.8 | % | 60.0 | % | |||||||||||||

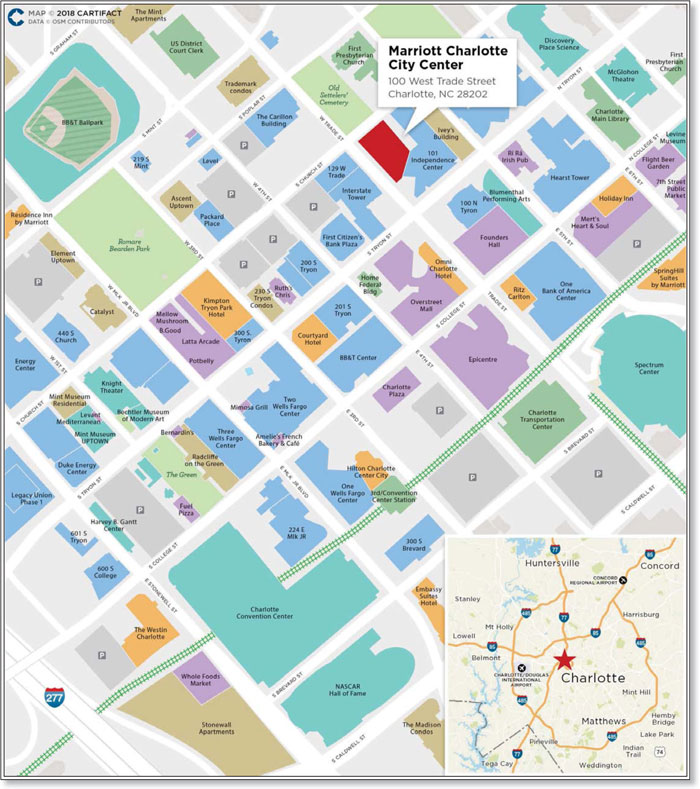

| 9 | Marriott Charlotte City Center | 43,000,000 | 3.9 | Hospitality | 446 | $230,942 | 2.76 | x | 12.7 | % | 60.6 | % | |||||||||||||

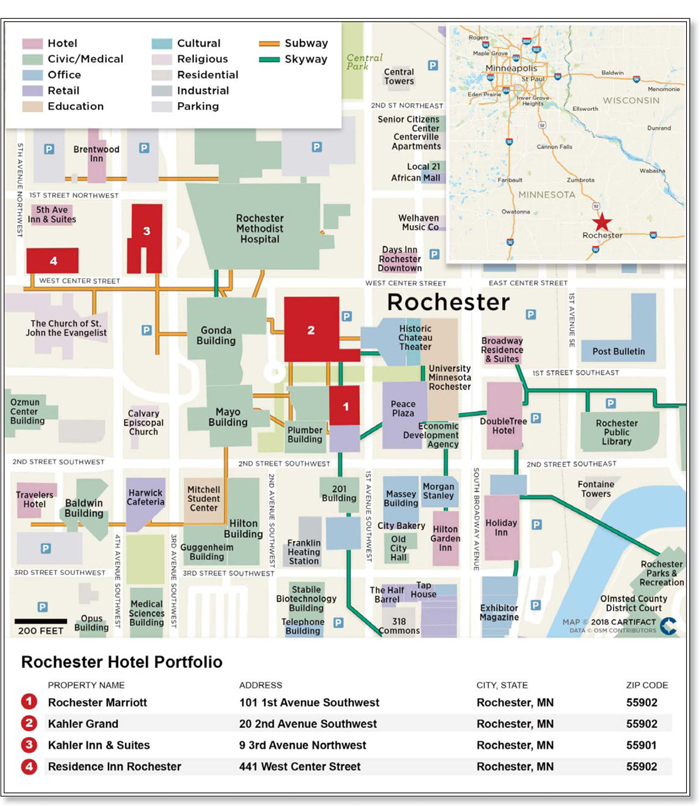

| 10 | Rochester Hotel Portfolio | 40,000,000 | 3.7 | Hospitality | 1,222 | $114,566 | 1.50 | x | 12.2 | % | 66.7 | % | |||||||||||||

| Top 10 Total / Wtd. Avg. | $492,055,929 | 45.0 | % | 2.14 | x | 11.7 | % | 57.9 | % | ||||||||||||||||

| Remaining Total / Wtd. Avg. | 600,481,782 | 55.0 | 1.72 | x | 10.2 | % | 61.7 | % | |||||||||||||||||

| Total / Wtd. Avg. | $1,092,537,712 | 100.0 | % | 1.91 | x | 10.8 | % | 60.0 | % | ||||||||||||||||

| (1) | See footnotes to table entitled“Mortgage Pool Characteristics” above. |

| (2) | With respect to each mortgage loan that is part of a loan combination (as identified under “Collateral Overview—Loan Combination Summary” below), the UW NCF DSCR, UW NOI Debt Yield and Cut-off Date LTV Ratio are calculated based on both that mortgage loan and any related pari passu companion loan(s), but without regard to any related subordinate companion loan(s) or other indebtedness. With respect to the Twelve Oaks Mall mortgage loan, the mortgaged property is also encumbered by 3 subordinate companion loans with an aggregate outstanding principal balance as of the Cut-off Date of $99,889,922. The UW NCF DSCR, UW NOI Debt Yield and Cut-off Date LTV Ratio for the Twelve Oaks Mall mortgage loan, inclusive of the subordinate companion loans, are 1.58x, 10.2% and 54.2%, respectively.] |

| (3) | With respect to certain of the mortgage loans identified above, the Cut-off Date LTV Ratios have been calculated using “as-stabilized”, “portfolio premium” or similar hypothetical values. Such mortgage loans are identified under the definition of “Appraised Value” set forth under “Description of the Mortgage Pool—Certain Calculations and Definitions” in the Preliminary Prospectus. |

| The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-207132) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Deutsche Bank Securities Inc., J.P. Morgan Securities LLC, Drexel Hamilton, LLC or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146. |

9

| COLLATERAL OVERVIEW (continued) |

Loan Combination Summary

Mortgaged Property Name(1) | Mortgage Loan | Mortgage Loan as Approx. % of Initial Pool Balance | Aggregate Pari | Aggregate Subordinate Companion | Loan | Controlling | Master | Special |

| EOS 21 | $60,000,000 | 5.5% | $90,000,000 | — | $150,000,000 | Benchmark 2018-B2 | KeyBank | CWCapital |

| The SoCal Portfolio | $50,000,000 | 4.6% | $179,300,000 | — | $229,300,000 | CGCMT 2018-B2 | Midland | LNR Partners |

| Twelve Oaks Mall | $49,944,961 | 4.6% | $149,834,882 | $99,889,922 | $299,669,765 | GSMS 2018-GS9(3) | Wells Fargo | Rialto |

| Intercontinental San Francisco | $49,788,676 | 4.6% | $59,746,411 | — | $109,535,088 | Benchmark 2018-B2 | KeyBank | CWCapital |

| Marina Heights State Farm | $45,000,000 | 4.1% | $515,000,000 | — | $560,000,000 | GSMS 2017-FARM | KeyBank | AEGON |

| CrossPoint | $45,000,000 | 4.1% | $105,000,000 | — | $150,000,000 | Benchmark 2018-B3 | Midland | Midland |

| Marriott Charlotte City Center | $43,000,000 | 3.9% | $60,000,000 | — | $103,000,000 | Benchmark 2018-B3 | Midland | Midland |

| Rochester Hotel Portfolio | $40,000,000 | 3.7% | $100,000,000 | — | $140,000,000 | Benchmark 2018-B2 | KeyBank | CWCapital |

| 599 Broadway | $35,000,000 | 3.2% | $40,000,000 | — | $75,000,000 | Benchmark 2018-B2 | KeyBank | CWCapital |

| 315 West 36th Street | $30,000,000 | 2.7% | $47,000,000 | — | $77,000,000 | Benchmark 2018-B3(4) | Midland(4) | Midland(4) |

| 90 Hudson | $30,000,000 | 2.7% | $100,000,000 | — | $130,000,000 | Benchmark 2018-B1 | Wells Fargo | Midland |

| Atrium Center | $30,000,000 | 2.7% | $85,000,000 | — | $115,000,000 | Benchmark 2018-B3 | Midland | Midland |

| Oak Portfolio | $24,972,167 | 2.3% | $15,651,306 | — | $40,623,473 | Benchmark 2018-B3 | Midland | Midland |

| Towers at University Town Center | $11,000,000 | 1.0% | $35,000,000 | — | $46,000,000 | Benchmark 2018-B2 | KeyBank | CWCapital |

| (1) | Each of the mortgage loans included in the issuing entity that is secured by a mortgaged property or portfolio of mortgaged properties identified in the table above, together with the related companion loan(s) (none of which is included in the issuing entity), is referred to in this Term Sheet as a “loan combination”. See “Description of the Mortgage Pool—The Loan Combinations” in the Preliminary Prospectus. |

| (2) | Each loan combination will be serviced under the related Controlling PSA, and the controlling class representative (or an equivalent entity), if any, under the related Controlling PSA (or such other party as is designated under the related Controlling PSA) will be entitled to exercise the rights of controlling note holder for the subject loan combination, except as otherwise discussed in footnotes (3) and (4) below. |

| (3) | With respect to the Twelve Oaks Mall mortgage loan, the control rights and the right to replace the applicable special servicer are held by the holder of the subordinate companion loans evidenced by notes B-1, B-2 and B-3 so long as no “note B control appraisal period” under the related co-lender agreement is in effect. If a “note B control appraisal period” under the related co-lender agreement is in effect, then note A-1 will be the controlling note. Unless and until a “note B control appraisal period” is in effect, the controlling class representative (or equivalent entity) under the applicable Controlling PSA will not be entitled to exercise control rights or the right to replace the applicable special servicer for the Twelve Oaks Mall mortgage loan. |

| (4) | The 315 West 36th Street loan combination will initially be serviced by the master servicer and the special servicer pursuant to the Benchmark 2018-B3 pooling and servicing agreement. Upon the inclusion of the related controlling pari passu companion loan in a future securitization transaction, the subject loan combination will be serviced under the pooling and servicing agreement entered into in connection with that future securitization, which will then be the applicable Controlling PSA for such loan combination. Although the Benchmark 2018-B3 pooling and servicing agreement will initially be the Controlling PSA for the 315 West 36th Street loan combination, the holder of the related controlling companion loan for such loan combination will be the Directing Holder of the subject loan combination while it is serviced under the Benchmark 2018-B3 pooling and servicing agreement and, solely as to the subject loan combination, will exercise all rights normally exercised by the Benchmark 2018-B3 controlling class representative with respect to other loan combinations for which the Benchmark 2018-B3 pooling and servicing agreement is the Controlling PSA. |

Mortgage Loans with Existing Mezzanine Debt or Subordinate Debt(1)

Mortgaged Property Name | Mortgage Loan Cut-off Date Balance | Aggregate Pari Passu Companion Loan Cut-off Date Balance | Mezzanine Debt Cut-off Date Balance | Aggregate Subordinate Companion Loan Cut-off Date Balance | Cut-off Date Total Debt Balance(2) | Wtd. Avg Cut-off Date Total Debt Interest Rate(2) | Cut-off Date Mortgage Loan LTV(3) | Cut-off Date Total Debt LTV(2) | Cut-off Date Mortgage Loan UW NCF DSCR(3) | Cut-off Date Total Debt UW NCF DSCR(2) |

| 6420 Wilshire | $62,000,000 | — | $8,000,000 | — | $70,000,000 | 4.69000% | 64.6% | 72.9% | 1.98x | 1.60x |

| Twelve Oaks Mall | $49,944,961 | $149,834,882 | — | $99,889,922 | $299,669,765 | 4.84900% | 36.1% | 54.2% | 2.55x | 1.58x |

| Residence Inn Pasadena | $47,322,293 | — | $4,500,000 | — | $51,822,293 | 5.29000% | 66.0% | 72.3% | 1.77x | 1.54x |

| NJ Distribution Portfolio | $33,000,000 | — | $6,000,000 | — | $39,000,000 | 5.60000% | 54.0% | 63.8% | 1.73x | 1.28x |

| Dellagio Town Center | $28,000,000 | — | $5,000,000 | — | $33,000,000 | 5.93000% | 69.8% | 82.3% | 1.47x | 1.12x |

| Holiday Inn Miami West Airport Area | $16,000,000 | — | $3,000,000 | — | $19,000,000 | 6.35000% | 57.1% | 67.9% | 1.97x | 1.57x |

| (1) | See footnotes to table entitled “Mortgage Pool Characteristics” above. |

| (2) | All “Total Debt” calculations set forth in the table above include any related pari passu companion loan(s), any related subordinate companion loan(s) and any related mezzanine debt. |

| (3) | “Cut-off Date Mortgage Loan LTV” and “Cut-off Date Mortgage Loan UW NCF DSCR” calculations include any related pari passu companion loan(s). |

| The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-207132) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Deutsche Bank Securities Inc., J.P. Morgan Securities LLC, Drexel Hamilton, LLC or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146. |

10

| COLLATERAL OVERVIEW (continued) |

Loan Combination Controlling Notes and Non-Controlling Notes(1)(2)

Mortgaged Property Name / | Controlling Note | Current Holder of | Current or | Cut-off |

| EOS 21 | ||||

| Note A-1 | Yes | — | Benchmark 2018-B2 | $60,000,000 |

| Note A-2 | No | — | Benchmark 2018-B3 | $60,000,000 |

| Note A-3 | No | JPMorgan Chase Bank, National Association | Not Identified | $30,000,000 |

| The SoCal Portfolio | ||||

| Note A-1-1 | Yes | Citi Real Estate Funding Inc. | CGCMT 2018-B2(5) | $50,000,000 |

| Note A-1-2 | No | — | Benchmark 2018-B3 | $35,000,000 |

| Note A-1-3 | No | — | Benchmark 2018-B3 | $15,000,000 |

| Note A-1-4 | No | Cantor Commercial Real Estate Lending, L.P. | UBS 2018-C9(5) | $37,580,000 |

| Note A-2-1 | No | Barclays Bank PLC | WFCM 2018-C43(5) | $45,000,000 |

| Note A-2-2 | No | Barclays Bank PLC | Not Identified | $46,720,000 |

| Twelve Oaks Mall | ||||

| Note A-1 | (6) | Goldman Sachs Mortgage Company | GSMS 2018-GS9(5) | $66,593,282 |

| Note A-2 | No | Wells Fargo Bank, National Association | Not Identified | $66,593,280 |

| Note A-3-1 | No | — | Benchmark 2018-B3 | $49,944,961 |

| Note A-3-2 | No | JPMorgan Chase Bank, National Association | Not Identified | $16,648,320 |

| Note B-1 | Yes(6) | Teachers Insurance Annuity Association of America | Not Applicable | $33,296,640 |

| Note B-2 | Yes(6) | Teachers Insurance Annuity Association of America | Not Applicable | $33,296,641 |

| Note B-3 | Yes(6) | Teachers Insurance Annuity Association of America | Not Applicable | $33,296,640 |

| Intercontinental San Francisco | ||||

| Note A-1 | Yes | — | Benchmark 2018-B2 | $39,830,941 |

| Note A-2 | No | — | Benchmark 2018-B3 | $29,873,206 |

| Note A-3 | No | — | Benchmark 2018-B2 | $19,915,470 |

| Note A-4 | No | — | Benchmark 2018-B3 | $9,957,735 |

| Note A-5 | No | — | Benchmark 2018-B3 | $9,957,735 |

| Marina Heights State Farm | ||||

| Note A-1-S | Yes | — | GSMS 2017-FARM | $264,000,000 |

| Note A-1-C1 | No | Goldman Sachs Mortgage Company | GSMS 2018-GS9(5) | $72,500,000 |

| Note A-1-C2 | No | Goldman Sachs Mortgage Company | Not Identified | $27,500,000 |

| Note A-2-C1 | No | — | Benchmark 2018-B3 | $45,000,000 |

| Note A-2-C2 | No | Deutsche Bank AG, acting through its New York Branch | Not Identified | $60,000,000 |

| Note A-2-C3 | No | Deutsche Bank AG, acting through its New York Branch | Not Identified | $50,000,000 |

| Note A-2-C4 | No | — | Benchmark 2018-B2 | $20,000,000 |

| Note A-2-C5 | No | — | Benchmark 2018-B2 | $21,000,000 |

| CrossPoint | ||||

| Note A-1 | Yes | — | Benchmark 2018-B3 | $30,000,000 |

| Note A-2 | No | — | UBS 2018-C8 | $25,000,000 |

| Note A-3 | No | — | UBS 2018-C8 | $20,000,000 |

| Note A-4 | No | Cantor Commercial Real Estate Lending, L.P. | UBS 2018-C9(5) | $20,000,000 |

| Note A-5 | No | Starwood Mortgage Funding V LLC | CGCMT 2018-B2(5) | $15,000,000 |

| Note A-6 | No | Starwood Mortgage Funding V LLC | CGCMT 2018-B2(5) | $10,000,000 |

| Note A-7 | No | — | Benchmark 2018-B3 | $10,000,000 |

| Note A-8 | No | Cantor Commercial Real Estate Lending, L.P. | UBS 2018-C9(5) | $10,000,000 |

| Note A-9 | No | — | UBS 2018-C8 | $5,000,000 |

| Note A-10 | No | — | Benchmark 2018-B3 | $5,000,000 |

| Marriott Charlotte City Center | ||||

| Note A-1 | No | — | Benchmark 2018-B1 | $30,000,000 |

| Note A-2 | No | — | Benchmark 2018-B2 | $30,000,000 |

| Note A-3 | Yes | — | Benchmark 2018-B3 | $43,000,000 |

| Rochester Hotel Portfolio | ||||

| Note A-1 | Yes | — | Benchmark 2018-B2 | $60,000,000 |

| Note A-2 | No | — | Benchmark 2018-B1 | $30,000,000 |

| Note A-3 | No | — | Benchmark 2018-B3 | $30,000,000 |

| Note A-4-A | No | — | Benchmark 2018-B1 | $10,000,000 |

| Note A-4-B | No | — | Benchmark 2018-B3 | $10,000,000 |

| 599 Broadway | ||||

| Note A-1 | Yes | — | Benchmark 2018-B2 | $40,000,000 |

| Note A-2 | No | — | Benchmark 2018-B3 | $35,000,000 |

| 315 West 36th Street | ||||

| Note A-1 | Yes | Deutsche Bank AG, acting through its New York Branch | Not Identified | $42,000,000 |

| Note A-2 | No | — | Benchmark 2018-B3 | $30,000,000 |

| Note A-3 | No | Deutsche Bank AG, acting through its New York Branch | Not Identified | $5,000,000 |

| 90 Hudson | ||||

| Note A-1 | Yes | — | Benchmark 2018-B1 | $70,000,000 |

| Note A-2-A | No | — | Benchmark 2018-B2 | $30,000,000 |

| Note A-2-B | No | — | Benchmark 2018-B3 | $30,000,000 |

| Atrium Center | ||||

| Note A-1 | No | — | Benchmark 2018-B1 | $50,000,000 |

| Note A-2 | No | — | Benchmark 2018-B2 | $35,000,000 |

| Note A-3 | Yes | — | Benchmark 2018-B3 | $30,000,000 |

| Oak Portfolio | ||||

| Note A-1 | Yes | — | Benchmark 2018-B3 | $24,972,167 |

| Note A-2 | No | Citi Real Estate Funding Inc. | Not Identified | $15,651,306 |

| Towers at University Town Center | ||||

| Note A-1-A | Yes | — | Benchmark 2018-B2 | $15,000,000 |

| Note A-2 | No | — | Benchmark 2018-B1 | $20,000,000 |

| Note A-1-B | No | — | Benchmark 2018-B3 | $11,000,000 |

| (1) | The holder(s) of one or more specified controlling notes (collectively, the “Controlling Note”) will be the “controlling note holder(s)” entitled (directly or through a representative) to (a) approve or, in some cases, direct material servicing decisions involving the related loan combination (while the remaining such holder(s) generally are only entitled to non-binding consultation rights in such regard), and (b) in some cases, replace the applicable special servicer with respect to such loan combination with or without cause. See “Description of the Mortgage Pool—The Loan Combinations” and “The Pooling and Servicing Agreement—Directing Holder” in the Preliminary Prospectus. |

| (2) | The holder(s) of the note(s) other than the Controlling Note (each, a “Non-Controlling Note”) will be the “non-controlling note holder(s)” generally entitled (directly or through a representative) to certain non-binding consultation rights with respect to any decisions as to which the holder of the Controlling Note has consent rights involving the related loan combination, subject to certain exceptions, including that in certain cases where the related Controlling Note is a B- |

| The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-207132) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Deutsche Bank Securities Inc., J.P. Morgan Securities LLC, Drexel Hamilton, LLC or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146. |

11

| COLLATERAL OVERVIEW (continued) |

note such consultation rights will not be afforded to the holder(s) of the Non-Controlling Notes until after a control trigger event has occurred with respect to either such Controlling Note or certain certificates backed thereby, in each case as set forth in the related co-lender agreement. See “Description of the Mortgage Pool—The Loan Combinations” in the Preliminary Prospectus.

| (3) | Unless otherwise specified, with respect to each loan combination, any related unsecuritized Controlling Note and/or Non-Controlling Note may be further split, modified, combined and/or reissued (prior to its inclusion in a securitization transaction) as one or multiple Controlling Notes or Non-Controlling Notes, as the case may be, subject to the terms of the related co-lender agreement (including that the aggregate principal balance, weighted average interest rate and certain other material terms cannot be changed). In connection with the foregoing, any such split, modified or combined Controlling Note or Non-Controlling Note, as the case may be, may be transferred to one or multiple parties (not identified in the table above) prior to its inclusion in a future commercial mortgage securitization transaction. |

| (4) | Unless otherwise specified, with respect to each loan combination, each related unsecuritized pari passu companion loan (whether controlling or non-controlling) is expected to be contributed to one or more future commercial mortgage securitization transactions. Under the column “Current or Anticipated Holder of Securitized Note”, (i) the identification of a securitization trust means we have identified an outside securitization that has closed or as to which a preliminary prospectus or final prospectus has been filed with the SEC that has included or is expected to include the subject Controlling Note or Non-Controlling Note, as the case may be, (ii) “Not Identified” means the subject Controlling Note or Non-Controlling Note, as the case may be, has not been securitized and no preliminary prospectus or final prospectus has been filed with the SEC that identifies the future outside securitization that is expected to include the subject Controlling Note or Non-Controlling Note, and (iii) “Not Applicable” means the subject Controlling Note or Non-Controlling Note is not intended to be contributed to a future commercial mortgage securitization transaction. Under the column “Current Holder of Unsecuritized Note”, “—” means the subjectControlling Note or Non-Controlling Note is not an unsecuritized note and is currently held by the securitization trust referenced under the “Current or Anticipated Holder of Securitized Note” column. |

| (5) | The CGCMT 2018-B2, UBS 2018-C9, WFCM 2018-C43 and GSMS 2018-GS9 transactions have not closed but are expected to close prior to the closing date for the Benchmark 2018-B3 transaction. |

| (6) | With respect to the Twelve Oaks Mall loan combination, pursuant to the related co-lender agreement, (i) the Controlling Note (so long as no “note B control appraisal period” is in effect) are notes B-1, B-2 and B-3, collectively, and (ii) if a note B control appraisal period under the related co-lender agreement is in effect, then note A-1 will be the Controlling Note. |

| The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-207132) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Deutsche Bank Securities Inc., J.P. Morgan Securities LLC, Drexel Hamilton, LLC or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146. |

12

| COLLATERAL OVERVIEW (continued) |

Previously Securitized Mortgaged Properties(1)

Mortgaged Property Name | Mortgage Loan Seller | City | State | Property Type | Cut-off Date Balance / Allocated Cut-off Date Balance | % of Initial Pool Balance | Previous Securitization | |||||||

| Rochester Marriott | GACC | Rochester | Minnesota | Hospitality | $15,214,286 | 1.4% | COMM 2013-CR6 | |||||||

| Kahler Grand | GACC | Rochester | Minnesota | Hospitality | $14,428,571 | 1.3% | COMM 2013-CR6 | |||||||

| Kahler Inn & Suites | GACC | Rochester | Minnesota | Hospitality | $6,071,429 | 0.6% | COMM 2013-CR6 | |||||||

| Residence Inn Rochester | GACC | Rochester | Minnesota | Hospitality | $4,285,714 | 0.4% | COMM 2013-CR6 | |||||||

| Greystone Park | JPMCB | Jacksonville | Florida | Office | $20,000,000 | 1.8% | JPMCC 2016-FL8 | |||||||

| The Meridian at Deerwood Park | JPMCB | Jacksonville | Florida | Office | $20,000,000 | 1.8% | JPMCC 2016-FL8 | |||||||

| 599 Broadway | JPMCB | New York | New York | Retail | $35,000,000 | 3.2% | PRIMA 2011-1 | |||||||

| Chicago Infill Industrial Portfolio | JPMCB | Various | Illinois | Industrial | $30,883,000 | 2.8% | JPMCC 2007-CB20 | |||||||

| Oak Creek Center | CREFI | Lombard | Illinois | Office | $16,068,613 | 1.5% | JPMCC 2013-C10 | |||||||

| Bay Tech North | GACC | Brisbane | California | Office | $13,100,000 | 1.2% | UBSBB 2013-C6 | |||||||

| Towers at University Town Center | JPMCB | Hyattsville | Maryland | Multifamily | $11,000,000 | 1.0% | MLCFC 2007-8 | |||||||

| (1) | The table above includes mortgaged properties securing mortgage loans for which the most recent prior financing of all or a significant portion of such mortgaged properties was included in a securitization. Information under “Previous Securitization” represents the most recent such securitization with respect to each of those mortgaged properties. The information in the above table is based solely on information provided by the related borrower or obtained through searches of a third-party database, and has not otherwise been confirmed by the mortgage loan sellers. |

| The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-207132) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Deutsche Bank Securities Inc., J.P. Morgan Securities LLC, Drexel Hamilton, LLC or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146. |

13

| COLLATERAL OVERVIEW (continued) |

Property Types

Property Type / Detail | Number of Mortgaged Properties | Aggregate Cut-off Date Balance(1) | % of Initial Pool Balance(1) | Wtd. Avg. Underwritten NCF DSCR(2)(3) | Wtd. Avg. Cut-off Date LTV | Wtd. Avg. Debt Yield on Underwritten | ||||||||||||

| Office | 23 | $390,566,138 | 35.7 | % | 2.00 | x | 61.5 | % | 10.6 | % | ||||||||

| Suburban | 17 | 203,066,138 | 18.6 | 2.14 | x | 62.3 | % | 11.9 | % | |||||||||

| CBD | 4 | 150,500,000 | 13.8 | 1.92 | x | 63.2 | % | 9.0 | % | |||||||||

| Medical | 2 | 37,000,000 | 3.4 | 1.57 | x | 50.7 | % | 9.5 | % | |||||||||

| Hospitality | 10 | $220,113,907 | 20.1 | % | 2.04 | x | 58.3 | % | 13.3 | % | ||||||||

| Full Service | 5 | 138,431,533 | 12.7 | 2.23 | x | 54.7 | % | 13.9 | % | |||||||||

| Extended Stay | 3 | 68,590,945 | 6.3 | 1.72 | x | 65.3 | % | 12.1 | % | |||||||||

| Limited Service | 1 | 7,020,000 | 0.6 | 1.95 | x | 54.0 | % | 14.6 | % | |||||||||

| Select Service | 1 | 6,071,429 | 0.6 | 1.50 | x | 66.7 | % | 12.2 | % | |||||||||

| Retail | 21 | $209,433,365 | 19.2 | % | 1.83 | x | 55.7 | % | 10.9 | % | ||||||||

| Unanchored | 11 | 88,445,040 | 8.1 | 1.57 | x | 58.6 | % | 9.0 | % | |||||||||

| Anchored | 6 | 59,310,010 | 5.4 | 1.64 | x | 65.7 | % | 10.1 | % | |||||||||

| Super Regional Mall | 1 | 49,944,961 | 4.6 | 2.55 | x | 36.1 | % | 15.3 | % | |||||||||

| Shadow Anchored | 2 | 8,092,313 | 0.7 | 1.73 | x | 72.0 | % | 10.9 | % | |||||||||

| Single Tenant Retail | 1 | 3,641,041 | 0.3 | 1.36 | x | 55.6 | % | 9.2 | % | |||||||||

| Multifamily | 6 | $138,065,591 | 12.6 | % | 1.64 | x | 66.4 | % | 8.8 | % | ||||||||

| Garden | 4 | 67,065,591 | 6.1 | 1.44 | x | 68.3 | % | 9.7 | % | |||||||||

| Mid-Rise | 1 | 60,000,000 | 5.5 | 1.87 | x | 64.8 | % | 7.5 | % | |||||||||

| Student Housing | 1 | 11,000,000 | 1.0 | 1.55 | x | 63.4 | % | 10.0 | % | |||||||||

| Industrial | 6 | $67,699,939 | 6.2 | % | 1.95 | x | 60.6 | % | 9.8 | % | ||||||||

| Warehouse/Distribution | 3 | 47,051,154 | 4.3 | 2.06 | x | 63.3 | % | 10.2 | % | |||||||||

| Flex | 3 | 20,648,785 | 1.9 | 1.72 | x | 54.2 | % | 9.1 | % | |||||||||

| Mixed Use | 5 | $45,352,914 | 4.2 | % | 1.89 | x | 55.3 | % | 9.1 | % | ||||||||

| Office/Retail | 3 | 37,332,176 | 3.4 | 1.94 | x | 54.7 | % | 8.6 | % | |||||||||

| Retail/Signage | 1 | 4,477,345 | 0.4 | 1.82 | x | 57.0 | % | 12.1 | % | |||||||||

| Retail/Education | 1 | 3,543,393 | 0.3 | 1.48 | x | 59.4 | % | 10.2 | % | |||||||||

| Self Storage | 2 | $11,750,000 | 1.1 | % | 1.31 | x | 68.1 | % | 8.8 | % | ||||||||

| Land | 2 | $9,555,857 | 0.9 | % | 1.33 | x | 44.6 | % | 11.3 | % | ||||||||

| Total | 75 | $1,092,537,712 | 100.0 | % | 1.91 | x | 60.0 | % | 10.8 | % | ||||||||

| (1) | Calculated based on the mortgaged property’s allocated loan amount for mortgage loans secured by more than one mortgaged property. |

| (2) | Weighted average based on the mortgaged property’s allocated loan amount for mortgage loans secured by more than one mortgaged property. |

| (3) | See footnotes to the table entitled “Mortgage Pool Characteristics” above. |

| The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-207132) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Deutsche Bank Securities Inc., J.P. Morgan Securities LLC, Drexel Hamilton, LLC or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146. |

14

| COLLATERAL OVERVIEW (continued) |

Geographic Distribution

Property Location | Number of Mortgaged Properties | Aggregate Cut-off Date Balance(1) | % of Initial Pool Balance(1) | Aggregate Appraised Value(2) | % of Total Appraised Value | Underwritten | % of Total Underwritten NOI | ||||||||||||||

| California | 31 | $258,522,432 | 23.7 | % | $894,240,000 | 18.9 | % | $57,984,948 | 19.7 | % | |||||||||||

| New York | 3 | 90,000,000 | 8.2 | 332,000,000 | 7.0 | 13,213,613 | 4.5 | ||||||||||||||

| Florida | 5 | 86,700,000 | 7.9 | 136,100,000 | 2.9 | 10,478,049 | 3.6 | ||||||||||||||

| Massachusetts | 2 | 75,000,000 | 6.9 | 465,000,000 | 9.8 | 27,128,309 | 9.2 | ||||||||||||||

| Illinois | 6 | 69,340,833 | 6.3 | 128,840,000 | 2.7 | 9,683,653 | 3.3 | ||||||||||||||

| Michigan | 2 | 69,144,961 | 6.3 | 580,800,000 | 12.3 | 32,334,723 | 11.0 | ||||||||||||||

| North Carolina | 2 | 66,100,000 | 6.1 | 203,900,000 | 4.3 | 15,323,854 | 5.2 | ||||||||||||||

| New Jersey | 3 | 63,000,000 | 5.8 | 277,100,000 | 5.8 | 14,896,444 | 5.1 | ||||||||||||||

| Virginia | 1 | 60,000,000 | 5.5 | 231,400,000 | 4.9 | 11,306,236 | 3.8 | ||||||||||||||

| Arizona | 1 | 45,000,000 | 4.1 | 960,000,000 | 20.3 | 63,333,156 | 21.5 | ||||||||||||||

| Minnesota | 5 | 44,477,345 | 4.1 | 217,850,000 | 4.6 | 17,561,819 | 6.0 | ||||||||||||||

| Ohio | 2 | 34,975,070 | 3.2 | 50,700,000 | 1.1 | 3,615,768 | 1.2 | ||||||||||||||

| Pennsylvania | 1 | 28,500,000 | 2.6 | 43,100,000 | 0.9 | 3,081,156 | 1.0 | ||||||||||||||

| Texas | 1 | 25,550,000 | 2.3 | 38,190,000 | 0.8 | 2,631,736 | 0.9 | ||||||||||||||

| Georgia | 1 | 17,280,248 | 1.6 | 26,300,000 | 0.6 | 1,973,168 | 0.7 | ||||||||||||||

| Alabama | 1 | 14,750,000 | 1.4 | 23,100,000 | 0.5 | 1,370,995 | 0.5 | ||||||||||||||

| Indiana | 3 | 14,640,191 | 1.3 | 29,530,000 | 0.6 | 2,070,548 | 0.7 | ||||||||||||||

| Maryland | 1 | 11,000,000 | 1.0 | 72,500,000 | 1.5 | 4,615,001 | 1.6 | ||||||||||||||

| Utah | 1 | 7,200,000 | 0.7 | 10,500,000 | 0.2 | 642,882 | 0.2 | ||||||||||||||

| Mississippi | 1 | 4,315,591 | 0.4 | 6,290,000 | 0.1 | 485,151 | 0.2 | ||||||||||||||

| Oklahoma | 1 | 3,641,041 | 0.3 | 6,550,000 | 0.1 | 334,225 | 0.1 | ||||||||||||||

| Nevada | 1 | 3,400,000 | 0.3 | 5,130,000 | 0.1 | 413,842 | 0.1 | ||||||||||||||

| Total | 75 | $1,092,537,712 | 100.0 | % | $4,739,120,000 | 100.0 | % | $294,479,276 | 100.0 | % | |||||||||||

| (1) | Calculated based on the mortgaged property’s allocated loan amount for mortgage loans secured by more than one mortgaged property. |

| (2) | Aggregate Appraised Values and Underwritten NOI reflect the aggregate values without any reduction for the pari passu companion loan(s). |

| The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-207132) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Deutsche Bank Securities Inc., J.P. Morgan Securities LLC, Drexel Hamilton, LLC or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146. |

15

| COLLATERAL OVERVIEW (continued) |

| Distribution of Cut-off Date Balances | |||||||||||

| Range of Cut-off Date Balances ($) | Number of Mortgage Loans | Cut-off Date Balance | % of Initial Pool Balance | ||||||||

| 2,667,365 - 4,999,999 | 7 | $25,751,343 | 2.4 | % | |||||||

| 5,000,000 - 9,999,999 | 5 | 35,437,017 | 3.2 | ||||||||

| 10,000,000 - 19,999,999 | 10 | 155,288,256 | 14.2 | ||||||||

| 20,000,000 - 29,999,999 | 6 | 155,122,167 | 14.2 | ||||||||

| 30,000,000 - 39,999,999 | 6 | 188,883,000 | 17.3 | ||||||||

| 40,000,000 - 49,999,999 | 8 | 360,055,929 | 33.0 | ||||||||

| 50,000,000 - 59,999,999 | 1 | 50,000,000 | 4.6 | ||||||||

| 60,000,000 - 62,000,000 | 2 | 122,000,000 | 11.2 | ||||||||

| Total | 45 | $1,092,537,712 | 100.0 | % | |||||||

| Distribution of UW NCF DSCRs(1) | |||||||||||

| Range of UW DSCR (x) | Number of Mortgage Loans | Cut-off Date Balance | % of Initial Pool Balance | ||||||||

| 1.21 – 1.50 | 16 | $284,921,968 | 26.1 | % | |||||||

| 1.51 – 2.00 | 20 | 455,499,107 | 41.7 | ||||||||

| 2.01 – 2.50 | 6 | 214,171,676 | 19.6 | ||||||||

| 2.51 – 3.00 | 2 | 92,944,961 | 8.5 | ||||||||

| 3.01 – 3.12 | 1 | 45,000,000 | 4.1 | ||||||||

| Total | 45 | $1,092,537,712 | 100.0 | % | |||||||

| (1) See footnotes (1) and (6) to the table entitled “Mortgage Pool Characteristics” above. | |||||||||||

| Distribution of Amortization Types(1) | |||||||||||

| Amortization Type | Number of Mortgage Loans | Cut-off Date Balance | % of Initial Pool Balance | ||||||||

| Interest Only | 13 | $454,133,000 | 41.6 | % | |||||||

| Interest Only, Then Amortizing(2) | 17 | 324,820,000 | 29.7 | ||||||||

| Amortizing (30 Years) | 12 | 244,721,150 | 22.4 | ||||||||

| Amortizing (25 Years) | 1 | 16,975,070 | 1.6 | ||||||||

| Amortizing (15 Years) | 1 | 6,888,492 | 0.6 | ||||||||

| Interest Only – ARD | 1 | 45,000,000 | 4.1 | ||||||||

| Total | 45 | $1,092,537,712 | 100.0 | % | |||||||

| (1) All of the mortgage loans will have balloon payments at maturity date or have an anticipated repayment date, as applicable. | |||||||||||

| (2) Original partial interest only periods range from 12 to 60 months. | |||||||||||

| Distribution of Lockboxes | |||||||||||

| Lockbox Type | Number of Mortgage Loans | Cut-off Date Balance | % of Initial Pool Balance | ||||||||

| Hard | 23 | $684,323,722 | 62.6 | % | |||||||

| Springing | 18 | 246,891,697 | 22.6 | ||||||||

| Soft | 4 | 161,322,293 | 14.8 | ||||||||

| Total | 45 | $1,092,537,712 | 100.0 | % | |||||||

| Distribution of Cut-off Date LTV Ratios(1) | |||||||||||

| Range of Cut-off Date LTV (%) | Number of Mortgage Loans | Cut-off Date Balance | % of Initial Pool Balance | ||||||||

| 36.1 - 49.9 | 5 | $134,322,129 | 12.3 | % | |||||||

| 50.0 - 59.9 | 11 | 244,238,387 | 22.4 | ||||||||

| 60.0 - 69.9 | 27 | 681,676,504 | 62.4 | ||||||||

| 70.0 - 73.3 | 2 | 32,300,692 | 3.0 | ||||||||

| Total | 45 | $1,092,537,712 | 100.0 | % | |||||||

| (1) See footnotes (1) and (5) to the table entitled “Mortgage Pool Characteristics” above. | |||||||||||

| Distribution of Maturity Date/ARD LTV Ratios(1) | |||||||||||

| Range of Maturity Date/ARD LTV (%) | Number of Mortgage Loans | Cut-off Date Balance | % of Initial Pool Balance | ||||||||

| 15.5 - 49.9 | 8 | $149,460,516 | 13.7 | % | |||||||

| 50.0 - 59.9 | 20 | 428,544,196 | 39.2 | ||||||||

| 60.0 - 67.7 | 17 | 514,533,000 | 47.1 | ||||||||

| Total | 45 | $1,092,537,712 | 100.0 | % | |||||||

| (1) See footnotes (1), (3) and (5) to the table entitled “Mortgage Pool Characteristics” above. | |||||||||||

| Distribution of Loan Purpose | |||||||||||

| Loan Purpose | Number of Mortgage Loans | Cut-off Date Balance | % of Initial Pool Balance | ||||||||

| Acquisition | 22 | $499,150,216 | 45.7 | % | |||||||

| Refinance | 18 | 452,770,368 | 41.4 | ||||||||

| Recapitalization | 3 | 82,644,961 | 7.6 | ||||||||

| Acquisition/Recapitalization | 2 | 57,972,167 | 5.3 | ||||||||

| Total | 45 | $1,092,537,712 | 100.0 | % | |||||||

| Distribution of Mortgage Rates | |||||||||||

| Range of Mortgage Rates (%) | Number of Mortgage Loans | Cut-off Date Balance | % of Initial Pool Balance | ||||||||

| 3.560 - 4.500 | 11 | $389,050,654 | 35.6 | % | |||||||

| 4.501 - 5.000 | 21 | 570,235,052 | 52.2 | ||||||||

| 5.001 - 5.500 | 11 | 114,552,006 | 10.5 | ||||||||

| 5.501 - 5.788 | 2 | 18,700,000 | 1.7 | ||||||||

| Total | 45 | $1,092,537,712 | 100.0 | % | |||||||

| The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-207132) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Deutsche Bank Securities Inc., J.P. Morgan Securities LLC, Drexel Hamilton, LLC or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146. |

16

| COLLATERAL OVERVIEW (continued) |

| Distribution of Debt Yield on Underwritten NOI(1) | |||||||||||

| Range of Debt Yields on Underwritten NOI (%) | Number of Mortgage Loans | Cut-off Date Balance | % of Initial Pool Balance | ||||||||

| 6.8 - 7.9 | 3 | $125,000,000 | 11.4 | % | |||||||

| 8.0 - 8.9 | 5 | 51,417,365 | 4.7 | ||||||||

| 9.0 - 9.9 | 10 | 240,691,041 | 22.0 | ||||||||

| 10.0 - 10.9 | 7 | 176,633,000 | 16.2 | ||||||||

| 11.0 -16.1 | 20 | 498,796,305 | 45.7 | ||||||||

| Total | 45 | $1,092,537,712 | 100.0 | % | |||||||

| (1) See footnotes (1) and (7) to the table entitled “Mortgage Pool Characteristics” above. | |||||||||||

| Distribution of Debt Yield on Underwritten NCF(1) | |||||||||||

| Range of Debt Yields on Underwritten NCF (%) | Number of Mortgage Loans | Cut-off Date Balance | % of Initial Pool Balance | ||||||||

| 6.4 - 7.9 | 3 | $125,000,000 | 11.4 | % | |||||||

| 8.0 - 8.9 | 12 | 240,367,365 | 22.0 | ||||||||

| 9.0 - 9.9 | 8 | 160,416,111 | 14.7 | ||||||||

| 10.0 - 10.9 | 11 | 232,340,302 | 21.3 | ||||||||

| 11.0 - 15.0 | 11 | 334,413,934 | 30.6 | ||||||||

| Total | 45 | $1,092,537,712 | 100.0 | % | |||||||

| (1) See footnotes (1) and (7) to the table entitled “Mortgage Pool Characteristics” above. | |||||||||||

| Mortgage Loans with Original Partial Interest Only Periods | |||||||||||

| Original Partial Interest Only Period (months) | Number of Mortgage Loans | Cut-off Date Balance | % of Initial Pool Balance | ||||||||

| 12 | 1 | $7,200,000 | 0.7 | % | |||||||

| 24 | 3 | $93,550,000 | 8.6 | % | |||||||

| 36 | 9 | $119,870,000 | 11.0 | % | |||||||

| 60 | 4 | $104,200,000 | 9.5 | % | |||||||

| Distribution of Original Terms to Maturity/ARD(1) | |||||||||||

| Original Term to Maturity/ARD (months) | Number of Mortgage Loans | Cut-off Date Balance | % of Initial Pool Balance | ||||||||

| 60 | 6 | $158,133,000 | 14.5 | % | |||||||

| 84 | 2 | 67,000,000 | 6.1 | ||||||||

| 120 | 37 | 867,404,712 | 79.4 | ||||||||

| Total | 45 | $1,092,537,712 | 100.0 | % | |||||||

| (1) See footnote (3) to the table entitled “Mortgage Pool Characteristics“ above. | |||||||||||

| Distribution of Remaining Terms to Maturity/ARD(1) | |||||||||||

| Range of Remaining Terms to Maturity/ARD (months) | Number of Mortgage Loans | Cut-off Date Balance | % of Initial Pool Balance | ||||||||