| FILED PURSUANT TO RULE 424(b)(2) | ||

| REGISTRATION FILE NO.: 333-207132-21 | ||

PROSPECTUS

$728,129,000 (Approximate)

BENCHMARK 2019-B9 MORTGAGE TRUST

(Central Index Key number0001764759)

Issuing Entity

Citigroup Commercial Mortgage Securities Inc.

(Central Index Key number 0001258361)

Depositor

Citi Real Estate Funding Inc.

(Central Index Key number 0001701238)

German American Capital Corporation

(Central Index Key number 0001541294)

JPMorgan Chase Bank, National Association

(Central Index Key number 0000835271)

Sponsors and Mortgage Loan Sellers

Commercial Mortgage Pass-Through Certificates, Series 2019-B9

The Benchmark 2019-B9 Mortgage Trust, Commercial Mortgage Pass-Through Certificates, Series 2019-B9, will consist of multiple classes of certificates, including those identified on the table below which are being offered by this prospectus. The offered certificates (together with the classes of non-offered certificates of the same series and the VRR Interest) will represent the beneficial ownership interests in the issuing entity identified above. The issuing entity’s primary assets will be a pool of fixed rate commercial mortgage loans secured by first liens on various types of commercial and multifamily properties. The mortgage loans will generally be the sole source of payment on the certificates. Credit enhancement will be provided solely by certain classes of subordinate certificates that will be subordinate to certain classes of senior certificates as described under “Description of the Certificates—Subordination; Allocation of Realized Losses”. Each class of offered certificates will entitle holders to receive monthly distributions of interest and/or principal on the 4th business day following the 11th day of each month (or if the 11th is not a business day, the next business day), commencing in March 2019. The rated final distribution date for the offered certificates isMarch 2052.

Classes of Offered Certificates | Approximate Initial Certificate | Initial Pass-Through Rate(3) | Pass-Through Rate Description | |||||

| Class A-1 | $ | 15,600,000 | 3.015% | Fixed | ||||

| Class A-2 | $ | 15,800,000 | 3.952% | Fixed | ||||

| Class A-3 | $ | 8,867,000 | 3.746% | Fixed | ||||

| Class A-4 | $ | 130,000,000 | 3.750% | Fixed | ||||

| Class A-5 | $ | 385,272,000 | 4.015% | Fixed | ||||

| Class A-AB | $ | 32,000,000 | 3.932% | Fixed | ||||

| Class X-A | $ | 649,440,000 | (5) | 1.049% | Variable IO(6) | |||

| Class A-S | $ | 61,901,000 | 4.266% | Fixed | ||||

| Class B | $ | 38,820,000 | 4.468% | Fixed | ||||

| Class C | $ | 39,869,000 | 4.970% | WAC Cap(7) | ||||

(Footnotes to table begin on page 3)

You should carefully consider the risk factors beginning onpage 61 of this prospectus.

Neither the Series 2019-B9 certificates nor the underlying mortgage loans are insured or guaranteed by any governmental agency or instrumentality or any other person or entity.

The Series 2019-B9 certificates will represent interests in and obligations of the issuing entity only and will not represent the obligations of or interests in the depositor, the sponsors or any of their respective affiliates. |

NEITHER THE SECURITIES AND EXCHANGE COMMISSION NOR ANY STATE SECURITIES COMMISSION HAS APPROVED OR DISAPPROVED OF THE OFFERED CERTIFICATES OR DETERMINED IF THIS PROSPECTUS IS TRUTHFUL OR COMPLETE. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE. THE DEPOSITOR WILL NOT LIST THE OFFERED CERTIFICATES ON ANY SECURITIES EXCHANGE OR ANY AUTOMATED QUOTATION SYSTEM OF ANY NATIONAL SECURITIES ASSOCIATION.

The offered certificates will be offered by Citigroup Global Markets Inc., Deutsche Bank Securities Inc., J.P. Morgan Securities LLC, Academy Securities, Inc. and The Williams Capital Group, L.P., the underwriters, when, as and if issued by the issuing entity, delivered to and accepted by the underwriters and subject to each underwriter’s right to reject orders in whole or in part. The underwriters will purchase the offered certificates from Citigroup Commercial Mortgage Securities Inc. and will offer the offered certificates to prospective investors from time to time in negotiated transactions or otherwise at varying prices, plus, in certain cases, accrued interest, determined at the time of sale. Citigroup Global Markets Inc., Deutsche Bank Securities Inc. and J.P. Morgan Securities LLC are acting as co-lead managers and joint bookrunners in the following manner: Citigroup Global Markets Inc. is acting as sole bookrunning manager with respect to approximately 49.9% of each class of offered certificates, Deutsche Bank Securities Inc. is acting as sole bookrunning manager with respect to approximately 28.9% of each class of offered certificates, and J.P. Morgan Securities LLC is acting as sole bookrunning manager with respect to approximately 21.2% of each class of offered certificates. Academy Securities, Inc. and The Williams Capital Group, L.P. are acting as co-managers.

The underwriters expect to deliver the offered certificates to purchasers in book-entry form only through the facilities of The Depository Trust Company in the United States and Clearstream Banking, société anonyme and Euroclear Bank SA/NV, as operator of the Euroclear System, in Europe against payment in New York, New York on or about February 14, 2019. Citigroup Commercial Mortgage Securities Inc. expects to receive from this offering approximately 109.97% of the aggregate principal balance of the offered certificates, plus accrued interest from February 1, 2019, before deducting expenses payable by the depositor.

The issuing entity will be relying on an exclusion or exemption from the definition of “investment company” under the Investment Company Act of 1940, as amended (the “Investment Company Act”), contained in Section 3(c)(5) of the Investment Company Act or Rule 3a-7 under the Investment Company Act, although there may be additional exclusions or exemptions available to the issuing entity. The issuing entity is being structured so as not to constitute a “covered fund” for purposes of the Volcker Rule under the Dodd-Frank Act (both as defined in“Risk Factors—Legal and Regulatory Provisions Affecting Investors Could Adversely Affect the Liquidity and Other Aspects of the Offered Certificates”). See also“Legal Investment”.

CALCULATION OF REGISTRATION FEE

Title of Each Class of Securities to Be Registered | Amount to Be Registered | Proposed Maximum Offering Price Per Unit(1) | Proposed Maximum Aggregate Offering Price(1) | Amount of Registration Fee(2) |

| Commercial Mortgage Pass-Through Certificates | $728,129,000 | 100% | $728,129,000 | $88,249.23 |

(1) Estimated solely for the purpose of calculating the registration fee.

(2) Calculated according to Rule 457(s) of the Securities Act of 1933.

| Citigroup | J.P. Morgan | Deutsche Bank Securities |

Co-Lead Managers and Joint Bookrunners

Academy Securities Co-Manager | The Williams Capital Group, L.P. Co-Manager | |

| February 1, 2019 |

Certificate Summary

Set forth below are the indicated characteristics of the respective classes of the Series 2019-B9 certificates, including the non-offered VRR Interest discussed in footnote (10) below.

| Classes of Certificates | Approximate Initial | Approximate | Initial | Pass-Through Rate Description | Expected Weighted | Expected Principal Window(4) | ||||||||||

| Offered Certificates | ||||||||||||||||

| Class A-1 | $ | 15,600,000 | 30.000 | % | 3.015% | Fixed | 2.86 | 3/19-11/23 | ||||||||

| Class A-2 | $ | 15,800,000 | 30.000 | % | 3.952% | Fixed | 4.81 | 11/23-12/23 | ||||||||

| Class A-3 | $ | 8,867,000 | 30.000 | % | 3.746% | Fixed | 7.00 | 2/26-2/26 | ||||||||

| Class A-4 | $ | 130,000,000 | 30.000 | % | 3.750% | Fixed | 9.71 | 7/28-12/28 | ||||||||

| Class A-5 | $ | 385,272,000 | 30.000 | % | 4.015% | Fixed | 9.85 | 12/28-1/29 | ||||||||

| Class A-AB | $ | 32,000,000 | 30.000 | % | 3.932% | Fixed | 7.30 | 12/23-9/28 | ||||||||

| Class X-A | $ | 649,440,000 | (5) | N/A | 1.049% | Variable IO(6) | N/A | N/A | ||||||||

| Class A-S | $ | 61,901,000 | 22.625 | % | 4.266% | Fixed | 9.92 | 1/29-1/29 | ||||||||

| Class B | $ | 38,820,000 | 18.000 | % | 4.468% | Fixed | 9.92 | 1/29-1/29 | ||||||||

| Class C | $ | 39,869,000 | 13.250 | % | 4.970% | WAC Cap(7) | 9.92 | 1/29-1/29 | ||||||||

| Non-Offered Certificates | ||||||||||||||||

| Class X-B | $ | 78,689,000 | (5) | N/A | 0.279% | Variable IO(6) | N/A | N/A | ||||||||

| Class X-D | $ | 46,163,000 | (5) | N/A | 2.002% | Variable IO(6) | N/A | N/A | ||||||||

| Class X-F | $ | 20,984,000 | (5) | N/A | 1.250% | Fixed IO(6) | N/A | N/A | ||||||||

| Class X-G | $ | 9,443,000 | (5) | N/A | 1.250% | Fixed IO(6) | N/A | N/A | ||||||||

| Class X-H | $ | 9,442,000 | (5) | N/A | 1.250% | Fixed IO(6) | N/A | N/A | ||||||||

| Class X-J | $ | 25,180,928 | (5) | N/A | 1.250% | Fixed IO(6) | N/A | N/A | ||||||||

| Class D | $ | 26,229,000 | 10.125 | % | 3.000% | Fixed | 9.92 | 1/29-1/29 | ||||||||

| Class E | $ | 19,934,000 | 7.750 | % | 3.000% | Fixed | 9.95 | 1/29-2/29 | ||||||||

| Class F | $ | 20,984,000 | 5.250 | % | 3.752% | WAC – 1.250%(8) | 10.00 | 2/29-2/29 | ||||||||

| Class G | $ | 9,443,000 | 4.125 | % | 3.752% | WAC – 1.250%(8) | 10.00 | 2/29-2/29 | ||||||||

| Class H | $ | 9,442,000 | 3.000 | % | 3.752% | WAC – 1.250%(8) | 10.00 | 2/29-2/29 | ||||||||

| Class J | $ | 25,180,928 | 0.000 | % | 3.752% | WAC – 1.250%(8) | 10.00 | 2/29-2/29 | ||||||||

| Class S(9) | N/A | N/A | N/A | N/A | N/A | N/A | ||||||||||

| Class R(9) | N/A | N/A | N/A | N/A | N/A | N/A | ||||||||||

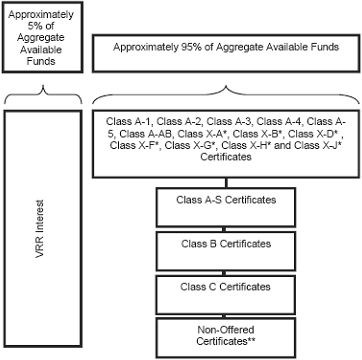

| Non-Offered Vertical Risk Retention Interest | ||||||||||||||||

| VRR Interest(10) | $ | 44,175,891 | N/A | 5.002%(11) | WAC(11) | 9.50 | 3/19-2/29 | |||||||||

| (1) | Approximate, subject to a variance of plus or minus 5%. |

| (2) | The approximate initial credit support percentages set forth for the Class A-1, Class A-2, Class A-3, Class A-4, Class A-5 and Class A-AB certificates are represented in the aggregate. The approximate initial credit support percentages shown in the table above do not take into account the VRR Interest. However, losses incurred on the mortgage loans will be allocated between the VRR Interest, on the one hand, and the Class A-1, Class A-2, Class A-3, Class A-4, Class A-5, Class A-AB, Class A-S, Class B, Class C, Class D, Class E, Class F, Class G, Class H and Class J certificates (collectively, the “non-vertically retained principal balance certificates”), on the other hand,pro rata in accordance with their respective outstanding certificate balances. See “Credit Risk Retention” and “Description of the Certificates”. The VRR Interest and the non-vertically retained principal balance certificates are collectively referred to in this prospectus as the “principal balance certificates”. |

| (3) | Approximateper annum rate as of the closing date. |

| (4) | Determined assuming no prepayments prior to the maturity date or any anticipated repayment date, as applicable, for any mortgage loan and based on the modeling assumptions described under “Yield, Prepayment and Maturity Considerations.” |

| (5) | The Class X-A, Class X-B, Class X-D, Class X-F, Class X-G, Class X-H and Class X-J certificates (collectively, the “Class X certificates”) will not have certificate balances and will not be entitled to receive distributions of principal. Interest will accrue on each class of Class X certificates at the related pass-through rate based upon the related notional amount. The notional amount of each class of the Class X certificates will be equal to the certificate balance or the aggregate of the certificate balances, as applicable, from time to time of the class or classes of the non-vertically retained principal balance certificates identified in the same row as such class of Class X certificates in the chart below (as to such class of Class X certificates, the “corresponding principal balance certificates”): |

| Class of Class X Certificates | Class(es) of Corresponding Principal Balance Certificates |

| Class X-A | Class A-1, Class A-2, Class A-3, Class A-4, Class A-5, Class A-AB and Class A-S |

| Class X-B | Class B and Class C |

| Class X-D | Class D and Class E |

| Class X-F | Class F |

| Class X-G | Class G |

| Class X-H | Class H |

| Class X-J | Class J |

| (6) | The pass-through rate for the Class X-A, Class X-B and Class X-D certificates will generally be aper annum rate equal to the excess, if any, of (i) the weighted average of the net interest rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a |

3

360-day year consisting of twelve 30-day months) as in effect from time to time, over (ii) the pass-through rate (or, if applicable, the weighted average of the pass-through rates) of the class or classes of corresponding principal balance certificates as in effect from time to time, as described in this prospectus. The pass-through rate for the Class X-F, Class X-G, Class X-H and Class X-J certificates will be a fixedper annum rate equal to 1.250%.

| (7) | The pass-through rate for the Class C certificates will generally be aper annum rate equal to the lesser of (a) the initial pass-through rate for such class specified in the table above and (b) the weighted average of the net interest rates on the mortgage loans (in each case, adjusted, if necessary to accrue on the basis of a 360-day year consisting of twelve 30-day months) as in effect from time to time, as described in this prospectus. |

| (8) | The pass-through rates for the Class F, Class G, Class H and Class J certificates will each generally be aper annum rate equal to the weighted average of the net interest rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) as in effect from time to time, minus 1.250%, as described in this prospectus. |

| (9) | Neither the Class S certificates nor the Class R certificates will have a certificate balance, notional amount, pass-through rate, rating or rated final distribution date. Excess interest accruing after the related anticipated repayment date on any mortgage loan with an anticipated repayment date will, to the extent collected, be allocated to the Class S certificates as set forth in “Description of the Certificates—Distributions—Excess Interest”. The Class R certificates will represent the residual interests in each of two separate REMICs, as further described in this prospectus. The Class R certificates will not be entitled to distributions of principal or interest. |

| (10) | German American Capital Corporation, as retaining sponsor, is expected to acquire (or cause one or more other retaining parties to acquire) from the depositor, on the closing date for this transaction, portions of an “eligible vertical interest” (as such term is defined in Regulation RR) in the form of a “single vertical security” (as defined in Regulation RR) with an initial certificate balance of approximately $44,175,891 (the “VRR Interest”), representing at least 5.0% of the aggregate initial certificate balance of all of the ABS interests issued by the issuing entity on the closing date. The VRR Interest will be retained by certain retaining parties in accordance with the credit risk retention rules applicable to this securitization transaction. See “Credit Risk Retention”. The VRR Interest is a class of certificates. |

| (11) | Although it does not have a specified pass-through rate (other than for tax reporting purposes), the effective interest rate for the VRR Interest will be the weighted average of the net mortgage interest rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) as in effect from time to time. |

The Class X-B,Class X-D, Class X-F, Class X-G, Class X-H, Class X-J, Class D, Class E, Class F, Class G, Class H, Class J, Class S and Class R certificates and the VRR Interest are not offered by this prospectus. Any information in this prospectus concerning certificates other than the offered certificates or concerning the VRR Interest is presented solely to enhance your understanding of the offered certificates.

4

Table of Contents

| Certificate Summary | 3 |

| Important Notice Regarding the Offered Certificates | 10 |

| IMPORTANT NOTICE ABOUT INFORMATION PRESENTED IN THIS PROSPECTUS | 10 |

| Summary of Terms | 17 |

| Risk Factors | 61 |

| The Offered Certificates May Not Be a Suitable Investment for You | 61 |

| Combination or “Layering” of Multiple Risks May Significantly Increase Risk of Loss | 61 |

| The Offered Certificates Are Limited Obligations; If Assets Are Not Sufficient, You May Not Be Paid | 61 |

| Any Credit Support for Your Offered Certificates May Be Insufficient to Protect You Against All Potential Losses | 62 |

| Your Yield May Be Affected by Defaults, Prepayments and Other Factors | 62 |

| Payments Allocated to the VRR Interest Will Not Be Available to Make Payments on the Non-Vertically Retained Certificates, and Payments Allocated to the Non-Vertically Retained Certificates Will Not Be Available to Make Payments on the VRR Interest | 67 |

| Release, Casualty and Condemnation of Collateral May Reduce the Yield on Your Certificates | 67 |

| Pro RataAllocation of Principal Between and Among the Subordinate Companion Loan and the Related Mortgage Loan Prior to a Material Mortgage Loan Event Default | 67 |

| Certain Classes of the Offered Certificates Are Subordinate to, and Are Therefore Riskier Than, Other Classes | 67 |

| A Rapid Rate of Principal Prepayments, Liquidations and/or Principal Losses on the Mortgage Loans Could Result in the Failure to Recoup the Initial Investment in the Class X-A Certificates | 68 |

| Book-Entry Registration Will Mean You Will Not Be Recognized as a Holder of Record | 68 |

| The Volatile Economy, Credit Crisis and Downturn in the Real Estate Market Have Adversely Affected and May Continue to Adversely Affect the Value of CMBS | 68 |

| Legal and Regulatory Provisions Affecting Investors Could Adversely Affect the Liquidity and Other Aspects of the Offered Certificates | 69 |

| Other External Factors May Adversely Affect the Value and Liquidity of Your Investment; Global, National and Local Economic Factors | 72 |

| The Certificates May Have Limited Liquidity and the Market Value of the Certificates May Decline | 72 |

| Nationally Recognized Statistical Rating Organizations May Assign Different Ratings to the Certificates; Ratings of the Certificates Reflect Only the Views of the Applicable Rating Agencies as of the Dates Such Ratings Were Issued; Ratings May Affect ERISA Eligibility; Ratings May Be Downgraded | 73 |

| Commercial and Multifamily Lending Is Dependent on Net Operating Income; Information May Be Limited or Uncertain | 76 |

| Mortgage Loans Are Non-Recourse and Are Not Insured or Guaranteed | 76 |

| Underwritten Net Cash Flow Could Be Based on Incorrect or Failed Assumptions | 77 |

| Frequent and Early Occurrence of Borrower Delinquencies and Defaults May Adversely Affect Your Investment | 77 |

| The Mortgage Loans Have Not Been Reviewed or Reunderwritten by Us; Some Mortgage Loans May Not Have Complied With Another Originator’s Underwriting Criteria | 78 |

| Historical Information Regarding the Mortgage Loans May Be Limited | 79 |

| Ongoing Information Regarding the Mortgage Loans and the Offered Certificates May Be Limited | 79 |

| Static Pool Data Would Not Be Indicative of the Performance of This Pool | 79 |

| Performance of the Certificates Will Be Highly Dependent on the Performance of Tenants and Tenant Leases | 79 |

| A Tenant Concentration May Result in Increased Losses | 80 |

| Mortgaged Properties Leased to Multiple Tenants Also Have Risks | 81 |

| Mortgaged Properties Leased to Borrowers or Borrower Affiliated Entities Also Have Risks | 81 |

5

| Tenant Bankruptcy Could Result in a Rejection of the Related Lease | 81 |

| Leases That Are Not Subordinated to the Lien of the Mortgage or Do Not Contain Attornment Provisions May Have an Adverse Impact at Foreclosure | 81 |

| Early Lease Termination Options May Reduce Cash Flow | 82 |

| Mortgaged Properties Leased to Not-for-Profit Tenants Also Have Risks | 82 |

| Certain Aspects of Co-Lender, Intercreditor and Similar Agreements Executed in Connection with Mortgage Loans Underlying Your Offered Certificates May Be Unenforceable | 82 |

| Mezzanine Debt May Reduce the Cash Flow Available to Reinvest in a Mortgaged Property and may Increase the Likelihood that a Borrower Will Default on a Mortgage Loan Underlying Your Offered Certificates | 83 |

| Concentrations Based on Property Type, Geography, Related Borrowers and Other Factors May Disproportionately Increase Losses | 83 |

| Repayment of a Commercial or Multifamily Mortgage Loan Depends Upon the Performance and Value of the Underlying Real Property, Which May Decline Over Time, and the Related Borrower’s Ability to Refinance the Property, of Which There Is No Assurance | 84 |

| The Types of Properties That Secure the Mortgage Loans Present Special Risks | 90 |

| Any Analysis of the Value or Income Producing Ability of a Commercial or Multifamily Property Is Highly Subjective and Subject to Error | 106 |

| Changes in Pool Composition Will Change the Nature of Your Investment | 109 |

| Tenancies-in-Common May Hinder Recovery | 109 |

| Risks Relating to Enforceability of Cross-Collateralization Arrangements | 109 |

| Inadequacy of Title Insurers May Adversely Affect Payments on Your Certificates | 110 |

| The Performance of a Mortgage Loan and Its Related Mortgaged Property Depends in Part on Who Controls the Borrower and Mortgaged Property | 110 |

| Risks of Anticipated Repayment Date Loans | 111 |

| The Absence of Lockboxes Entails Risks That Could Adversely Affect Distributions on Your Certificates | 111 |

| Various Other Laws Could Affect the Exercise of Lender’s Rights | 111 |

| A Borrower May Be Unable to Repay Its Remaining Principal Balance on the Maturity Date or Anticipated Repayment Date; Longer Amortization Schedules and Interest-Only Provisions Increase Risk | 112 |

| Some Provisions in the Mortgage Loans Underlying Your Offered Certificates May Be Challenged as Being Unenforceable | 113 |

| Jurisdictions with One Action or Security First Rules and/or Anti-Deficiency Legislation May Limit the Ability of the Special Servicer to Foreclose on a Real Property or to Realize on Obligations Secured by a Real Property | 115 |

| Appraisals May Not Reflect Current or Future Market Value of Each Property | 115 |

| Risks Related to Redevelopment, Expansion and Renovation at Mortgaged Properties | 116 |

| Risks Relating to Costs of Compliance with Applicable Laws and Regulations | 117 |

| Increases in Real Estate Taxes and Assessments May Reduce Available Funds | 117 |

| Risks Relating to Tax Credits | 117 |

| Condemnation of a Mortgaged Property May Adversely Affect Distributions on Certificates | 118 |

| Some Mortgaged Properties May Not Be Readily Convertible to Alternative Uses | 118 |

| Lending on Condominium Units Creates Risks for Lenders That Are Not Present When Lending on Non-Condominiums | 119 |

| Lending on Ground Leases Creates Risks for Lenders That Are Not Present When Lending on a Fee Ownership Interest in a Real Property | 119 |

| Leased Fee Properties Have Special Risks | 121 |

| Risks Related to Zoning Non-Compliance and Use Restrictions | 121 |

| Risks Relating to Inspections of Properties | 122 |

| State and Local Mortgage Recording Taxes May Apply Upon a Foreclosure or Deed-in-Lieu of Foreclosure and Reduce Net Proceeds | 122 |

| Earthquake, Flood and Other Insurance May Not Be Available or Adequate | 122 |

6

| Lack of Insurance Coverage Exposes the Trust to Risk for Particular Special Hazard Losses | 123 |

| Terrorism Insurance May Not Be Available for All Mortgaged Properties | 124 |

| Risks Associated with Blanket Insurance Policies or Self-Insurance | 125 |

| The Mortgage Loan Sellers, the Sponsors and the Depositor Are Subject to Bankruptcy or Insolvency Laws That May Affect the Issuing Entity’s Ownership of the Mortgage Loans | 125 |

| The Borrower’s Form of Entity May Cause Special Risks | 126 |

| Other Debt of the Borrower or Ability to Incur Other Financings Entails Risk | 129 |

| Litigation and Other Legal Proceedings May Adversely Affect a Borrower’s Ability to Repay Its Mortgage Loan | 130 |

| Reserves to Fund Certain Necessary Expenditures Under the Mortgage Loans May Be Insufficient for the Purpose for Which They Were Established | 130 |

| A Bankruptcy Proceeding May Result in Losses and Delays in Realizing on the Mortgage Loans | 131 |

| Bankruptcy of a Servicer May Adversely Affect Collections on the Mortgage Loans and the Ability to Replace the Servicer | 131 |

| Interests and Incentives of the Underwriter Entities May Not Be Aligned with Your Interests | 132 |

| Interests and Incentives of the Originators, the Sponsors and Their Affiliates May Not Be Aligned with Your Interests | 133 |

| Potential Conflicts of Interest of the Master Servicer, the Special Servicer, the Trustee, any Outside Servicer and any Outside Special Servicer | 135 |

| Additional Compensation to the Master Servicer and the Special Servicer and Interest on Advances Will Affect Your Right to Receive Distributions on Your Offered Certificates | 138 |

| Inability to Replace the Master Servicer Could Affect Collections and Recoveries on the Mortgage Loans | 138 |

| Potential Conflicts of Interest of the Operating Advisor | 138 |

| Potential Conflicts of Interest of the Asset Representations Reviewer | 139 |

| Potential Conflicts of Interest of a Directing Holder, any Outside Controlling Class Representative and any Companion Loan Holder | 139 |

| Potential Conflicts of Interest in the Selection of the Underlying Mortgage Loans | 141 |

| Conflicts of Interest May Occur as a Result of the Rights of the Controlling Class Representative, an Outside Controlling Class Representative or a Controlling Note Holder to Terminate the Special Servicer of the Related Loan Combination | 142 |

| Other Potential Conflicts of Interest May Affect Your Investment | 142 |

| Your Lack of Control Over the Issuing Entity and Servicing of the Mortgage Loans Can Create Risks | 143 |

| The Servicing of the Servicing Shift Loan Combination Will Shift to Other Servicers | 144 |

| Rights of the Directing Holder, the Risk Retention Consultation Parties and the Operating Advisor Could Adversely Affect Your Investment | 144 |

| Realization on a Mortgage Loan That Is Part of a Serviced Loan Combination May Be Adversely Affected by the Rights of the Related Serviced Companion Loan Holder | 145 |

| Rights of any Outside Controlling Class Representative or Other Controlling Note Holder with Respect to an Outside Serviced Loan Combination Could Adversely Affect Your Investment | 146 |

| You Will Not Have Any Control Over the Servicing of Any Outside Serviced Mortgage Loan | 147 |

| Sponsors May Not Make Required Repurchases or Substitutions of Defective Mortgage Loans | 147 |

| Any Loss of Value Payment Made by a Sponsor May Not Be Sufficient to Cover All Losses on a Defective Mortgage Loan | 147 |

| Adverse Environmental Conditions at or Near Mortgaged Properties May Result in Losses | 147 |

| Environmental Liabilities Will Adversely Affect the Value and Operation of the Contaminated Property and May Deter a Lender from Foreclosing | 148 |

| Certain Types of Operations Involved in the Use and Storage of Hazardous Materials May Lead to an Increased Risk of Issuing Entity Liability | 149 |

| Tax Matters and Changes in Tax Law May Adversely Impact the Mortgage Loans or Your Investment | 149 |

| State, Local and Other Tax Considerations | 151 |

7

| Changes to REMIC Restrictions on Loan Modifications May Impact an Investment in the Certificates | 151 |

| Description of the Mortgage Pool | 153 |

| General | 153 |

| Certain Calculations and Definitions | 154 |

| Statistical Characteristics of the Mortgage Loans | 163 |

| Delinquency Information | 174 |

| Environmental Considerations | 174 |

| Litigation and Other Legal Considerations | 177 |

| Redevelopment, Expansion and Renovation | 178 |

| Default History, Bankruptcy Issues and Other Proceedings | 179 |

| Tenant Issues | 180 |

| Insurance Considerations | 191 |

| Zoning and Use Restrictions | 191 |

| Non-Recourse Carveout Limitations | 192 |

| Real Estate and Other Tax Considerations | 193 |

| Certain Terms of the Mortgage Loans | 195 |

| Additional Indebtedness | 206 |

| The Loan Combinations | 211 |

| Additional Mortgage Loan Information | 222 |

| Transaction Parties | 224 |

| The Sponsors and the Mortgage Loan Sellers | 224 |

| Compensation of the Sponsors | 247 |

| The Depositor | 247 |

| The Issuing Entity | 248 |

| The Trustee | 249 |

| The Certificate Administrator | 250 |

| Servicers | 252 |

| The Operating Advisor and the Asset Representations Reviewer | 269 |

| Certain Affiliations, Relationships and Related Transactions Involving Transaction Parties | 270 |

| Credit Risk Retention | 273 |

| General | 273 |

| Qualifying CRE Loans; Required Credit Risk Retention Percentage | 274 |

| The VRR Interest | 274 |

| Hedging, Transfer and Financing Restrictions | 276 |

| Description of the Certificates | 278 |

| General | 278 |

| Distributions | 280 |

| Allocation of Yield Maintenance Charges and Prepayment Premiums | 292 |

| Assumed Final Distribution Date; Rated Final Distribution Date | 294 |

| Prepayment Interest Shortfalls | 294 |

| Subordination; Allocation of Realized Losses | 295 |

| Reports to Certificateholders; Certain Available Information | 297 |

| Voting Rights | 306 |

| Delivery, Form, Transfer and Denomination | 307 |

| Certificateholder Communication | 310 |

| The Mortgage Loan Purchase Agreements | 311 |

| Sale of Mortgage Loans; Mortgage File Delivery | 311 |

| Representations and Warranties | 316 |

| Cures, Repurchases and Substitutions | 316 |

| Dispute Resolution Provisions | 319 |

| Asset Review Obligations | 319 |

| The Pooling and Servicing Agreement | 320 |

| General | 320 |

| Certain Considerations Regarding the Outside Serviced Loan Combinations | 323 |

| Assignment of the Mortgage Loans | 324 |

| Servicing of the Mortgage Loans | 325 |

| Subservicing | 331 |

| Advances | 331 |

| Accounts | 335 |

| Withdrawals from the Collection Account | 337 |

| Application of Loss of Value Payments | 339 |

| Servicing and Other Compensation and Payment of Expenses | 339 |

| Application of Penalty Charges and Modification Fees | 353 |

| Enforcement of Due-On-Sale and Due-On-Encumbrance Clauses | 354 |

| Appraisal Reduction Amounts | 356 |

| Inspections | 361 |

| Evidence as to Compliance | 361 |

| Limitation on Liability; Indemnification | 362 |

| Servicer Termination Events | 365 |

| Rights Upon Servicer Termination Event | 367 |

| Waivers of Servicer Termination Events | 368 |

| Termination of the Special Servicer Other Than in Connection With a Servicer Termination Event | 369 |

| Resignation of the Master Servicer, the Special Servicer and the Operating Advisor | 372 |

| Qualification, Resignation and Removal of the Trustee and the Certificate Administrator | 372 |

| Amendment | 374 |

| Realization Upon Mortgage Loans | 376 |

| Directing Holder | 383 |

| Operating Advisor | 390 |

| Asset Status Reports | 397 |

| The Asset Representations Reviewer | 398 |

| Limitation on Liability of the Risk Retention Consultation Parties | 405 |

| Repurchase Requests; Enforcement of Mortgage Loan Seller’s Obligations Under the Mortgage Loan Purchase Agreement | 406 |

| Dispute Resolution Provisions | 407 |

| Rating Agency Confirmations | 410 |

8

| Termination; Retirement of Certificates | 412 |

| Optional Termination; Optional Mortgage Loan Purchase | 412 |

| Servicing of the Outside Serviced Mortgage Loans | 413 |

| Use of Proceeds | 419 |

| Yield, Prepayment and Maturity Considerations | 419 |

| Yield | 419 |

| Yield on the Class X-A Certificates | 422 |

| Weighted Average Life of the Offered Certificates | 422 |

| Price/Yield Tables | 427 |

| Material Federal Income Tax Consequences | 432 |

| General | 432 |

| Qualification as a REMIC | 432 |

| Status of Offered Certificates | 434 |

| Taxation of the Regular Interests | 434 |

| Taxes That May Be Imposed on a REMIC | 440 |

| Bipartisan Budget Act of 2015 | 440 |

| Taxation of Certain Foreign Investors | 441 |

| FATCA | 442 |

| Backup Withholding | 442 |

| Information Reporting | 442 |

| 3.8% Medicare Tax on “Net Investment Income” | 442 |

| Reporting Requirements | 443 |

| Tax Return Disclosure and Investor List Requirements | 443 |

| Certain State, Local and Other Tax Considerations | 443 |

| ERISA Considerations | 444 |

| General | 444 |

| Plan Asset Regulations | 445 |

| Prohibited Transaction Exemptions | 446 |

| Underwriter Exemption | 447 |

| Exempt Plans | 450 |

| Insurance Company General Accounts | 450 |

| Ineligible Purchasers | 450 |

| Further Warnings | 450 |

| Consultation with Counsel | 451 |

| Tax Exempt Investors | 451 |

| Legal Investment | 451 |

| Certain Legal Aspects of the Mortgage Loans | 452 |

| General | 453 |

| Types of Mortgage Instruments | 453 |

| Installment Contracts | 454 |

| Leases and Rents | 454 |

| Personalty | 455 |

| Foreclosure | 455 |

| Bankruptcy Issues | 460 |

| Environmental Considerations | 466 |

| Due-On-Sale and Due-On-Encumbrance Provisions | 469 |

| Junior Liens; Rights of Holders of Senior Liens | 470 |

| Subordinate Financing | 470 |

| Default Interest and Limitations on Prepayments | 470 |

| Applicability of Usury Laws | 471 |

| Americans with Disabilities Act | 471 |

| Servicemembers Civil Relief Act | 471 |

| Anti-Money Laundering, Economic Sanctions and Bribery | 472 |

| Potential Forfeiture of Assets | 472 |

| Ratings | 473 |

| Plan of Distribution (Underwriter Conflicts of Interest) | 475 |

| Incorporation of Certain Information by Reference | 477 |

| Where You Can Find More Information | 477 |

| Financial Information | 477 |

| Legal Matters | 477 |

| Index of Certain Defined Terms | 478 |

| ANNEX A – CERTAIN CHARACTERISTICS OF THE MORTGAGE LOANS AND MORTGAGED PROPERTIES | A-1 |

| ANNEX B – SIGNIFICANT LOAN SUMMARIES | B-1 |

| ANNEX C – MORTGAGE POOL INFORMATION | C-1 |

| ANNEX D – FORM OF DISTRIBUTION DATE STATEMENT | D-1 |

| ANNEX E-1A – SPONSOR REPRESENTATIONS AND WARRANTIES (CREFI AND GACC) | E-1A-1 |

| ANNEX E-1B – EXCEPTIONS TO SPONSOR REPRESENTATIONS AND WARRANTIES (CREFI AND GACC) | E-1B-1 |

| ANNEX E-2A – SPONSOR REPRESENTATIONS | |

| AND WARRANTIES (JPMCB) | E-2A-1 |

| ANNEX E-2B – EXCEPTIONS TO SPONSOR REPRESENTATIONS AND WARRANTIES (JPMCB) | E-2B-1 |

| ANNEX F – CLASS A-AB SCHEDULED PRINCIPAL BALANCE SCHEDULE | F-1 |

9

Important Notice Regarding the OfferedCertificates

WE HAVE FILED WITH THE SECURITIES AND EXCHANGE COMMISSION A REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933, AS AMENDED, WITH RESPECT TO THE OFFERED CERTIFICATES. THIS PROSPECTUS WILL FORM A PART OF THAT REGISTRATION STATEMENT, BUT THE REGISTRATION STATEMENT INCLUDES ADDITIONAL INFORMATION. SEE “WHERE YOU CAN FIND MORE INFORMATION” IN THIS PROSPECTUS.

THERE IS CURRENTLY NO SECONDARY MARKET FOR THE OFFERED CERTIFICATES. WE CANNOT ASSURE YOU THAT A SECONDARY MARKET WILL DEVELOP OR, IF A SECONDARY MARKET DOES DEVELOP, THAT IT WILL PROVIDE HOLDERS OF THE OFFERED CERTIFICATES WITH LIQUIDITY OF INVESTMENT OR THAT IT WILL CONTINUE FOR THE TERM OF THE OFFERED CERTIFICATES. THE UNDERWRITERS CURRENTLY INTEND TO MAKE A MARKET IN THE OFFERED CERTIFICATES, BUT ARE UNDER NO OBLIGATION TO DO SO. ACCORDINGLY, PURCHASERS MUST BE PREPARED TO BEAR THE RISKS OF THEIR INVESTMENTS FOR AN INDEFINITE PERIOD. SEE “RISK FACTORS—THE CERTIFICATES MAY HAVE LIMITED LIQUIDITY AND THE MARKET VALUE OF THE CERTIFICATES MAY DECLINE”.

THIS PROSPECTUS IS NOT AN OFFER TO SELL OR A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY STATE OR OTHER JURISDICTION WHERE SUCH OFFER, SOLICITATION OR SALE IS NOT PERMITTED.

THE OFFERED CERTIFICATES DO NOT REPRESENT AN INTEREST IN OR OBLIGATION OF THE DEPOSITOR, THE SPONSORS, THE ORIGINATORS, THE MASTER SERVICER, THE SPECIAL SERVICER, THE TRUSTEE, THE CERTIFICATE ADMINISTRATOR, THE OPERATING ADVISOR, THE ASSET REPRESENTATIONS REVIEWER, THE CONTROLLING CLASS REPRESENTATIVE, THE RISK RETENTION CONSULTATION PARTIES, THE COMPANION LOAN HOLDERS (OR THEIR REPRESENTATIVES), THE UNDERWRITERS OR ANY OF THEIR RESPECTIVE AFFILIATES. NEITHER THE OFFERED CERTIFICATES NOR THE MORTGAGE LOANS ARE INSURED OR GUARANTEED BY ANY GOVERNMENTAL AGENCY OR INSTRUMENTALITY OR PRIVATE INSURER.

IMPORTANT NOTICE ABOUT INFORMATION PRESENTED IN THIS PROSPECTUS

You should rely only on the information contained in this prospectus. We have not authorized anyone to provide you with information that is different from that contained in this prospectus. The information contained in this prospectus is accurate only as of the date of this prospectus.

■ This prospectus begins with two introductory sections describing the certificates and the issuing entity in abbreviated form:

| ● | the “Certificate Summary”, which sets forth important statistical information relating to the certificates; and |

| ● | the “Summary of Terms”, which gives a brief introduction to the key features of the certificates and a description of the underlying mortgage loans. |

Additionally, “Risk Factors” describes the material risks that apply to the certificates.

This prospectus includes cross-references to other sections in this prospectus where you can find further related discussions. The Table of Contents in this prospectus identifies the pages where these sections are located.

Certain capitalized terms are defined and used in this prospectus to assist you in understanding the terms of the offered certificates and this offering. The capitalized terms used in this prospectus are defined on the pages indicated under the caption “Index of Certain Defined Terms”.

■ In this prospectus:

| ● | the terms “depositor,” “we,” “us” and “our” refer to Citigroup Commercial Mortgage Securities Inc. |

10

| ● | references to “lender” or “mortgage lender” with respect to the mortgage loans generally should be construed to mean, from and after the date of initial issuance of the offered certificates, the trustee on behalf of the issuing entity as the holder of record title to the mortgage loans or the master servicer or the special servicer, as applicable, with respect to the obligations and rights of the lender as described under “The Pooling and Servicing Agreement”. |

| ● | unless otherwise specified or otherwise indicated by the context, (i) references to a mortgaged property (or portfolio of mortgaged properties) by name refer to such mortgaged property (or portfolio of mortgaged properties) so identified on Annex A, (ii) references to a mortgage loan by name refer to such mortgage loan secured by the related mortgaged property (or portfolio of mortgaged properties) so identified on Annex A, (iii) any parenthetical with a percentage next to the name of a mortgaged property (or the name of a portfolio of mortgaged properties) indicates the approximate percentage (or approximate aggregate percentage) that the outstanding principal balance of the related mortgage loan (or, if applicable, the allocated loan amount with respect to such mortgaged property) represents of the aggregate outstanding principal balance of the pool of mortgage loans as of the cut-off date for this securitization (the foregoing will also apply to the identification of multiple mortgaged properties by name or as a group), and (iv) any parenthetical with a percentage next to the name of a mortgage loan or a group of mortgage loans indicates the approximate percentage (or approximate aggregate percentage) that the outstanding principal balance of such mortgage loan or the aggregate outstanding principal balance of such group of mortgage loans, as applicable, represents of the aggregate outstanding principal balance of the pool of mortgage loans as of the cut-off date for this securitization (the foregoing will also apply to the identification of multiple mortgage loans by name or as a group). |

The Annexes attached to this prospectus are incorporated into and made a part of this prospectus.

THE UNITED KINGDOM SELLING RESTRICTIONS

EACH UNDERWRITER HAS REPRESENTED AND AGREED THAT:

(A) IN THE UNITED KINGDOM, IT HAS ONLY COMMUNICATED OR CAUSED TO BE COMMUNICATED AND WILL ONLY COMMUNICATE OR CAUSE TO BE COMMUNICATED AN INVITATION OR INDUCEMENT TO ENGAGE IN INVESTMENT ACTIVITY (WITHIN THE MEANING OF SECTION 21 OF THE FINANCIAL SERVICES AND MARKETS ACT 2000 (AS AMENDED, THE “FSMA”)) RECEIVED BY IT IN CONNECTION WITH THE ISSUE OR SALE OF THE OFFERED CERTIFICATES IN CIRCUMSTANCES IN WHICH SECTION 21(1) OF THE FSMA DOES NOT APPLY TO THE DEPOSITOR OR THE ISSUING ENTITY; AND

(B) IT HAS COMPLIED AND WILL COMPLY WITH ALL APPLICABLE PROVISIONS OF THE FSMA WITH RESPECT TO ANYTHING DONE BY IT IN RELATION TO THE OFFERED CERTIFICATES IN, FROM OR OTHERWISE INVOLVING THE UNITED KINGDOM.

NOTICE TO UNITED KINGDOM INVESTORS

THE ISSUING ENTITY MAY CONSTITUTE A “COLLECTIVE INVESTMENT SCHEME” AS DEFINED BY SECTION 235 OF THE FSMA THAT IS NOT A “RECOGNISED COLLECTIVE INVESTMENT SCHEME” FOR THE PURPOSES OF THE FSMA AND THAT HAS NOT BEEN AUTHORIZED, REGULATED OR OTHERWISE RECOGNIZED OR APPROVED. AS AN UNREGULATED SCHEME, THE OFFERED CERTIFICATES CANNOT BE MARKETED IN THE UNITED KINGDOM TO THE GENERAL PUBLIC, EXCEPT IN ACCORDANCE WITH THE FSMA.

THE DISTRIBUTION OF THIS PROSPECTUS (A) IF MADE BY A PERSON WHO IS NOT AN AUTHORIZED PERSON UNDER THE FSMA, IS BEING MADE ONLY TO, OR DIRECTED ONLY AT, PERSONS WHO (I) ARE OUTSIDE THE UNITED KINGDOM, OR (II) HAVE PROFESSIONAL EXPERIENCE IN MATTERS RELATING TO INVESTMENTS AND QUALIFY AS INVESTMENT PROFESSIONALS IN ACCORDANCE WITH ARTICLE 19(5) OF THE FINANCIAL SERVICES AND MARKETS ACT 2000 (FINANCIAL PROMOTION) ORDER 2005 (AS AMENDED, THE “FINANCIAL PROMOTION ORDER”), OR (III) ARE PERSONS FALLING WITHIN ARTICLE 49(2)(A) THROUGH (D) (“HIGH NET WORTH COMPANIES, UNINCORPORATED ASSOCIATIONS, ETC.”) OF THE FINANCIAL PROMOTION ORDER OR (IV) ARE ANY OTHER PERSONS TO WHOM IT MAY OTHERWISE LAWFULLY BE DISTRIBUTED OR DIRECTED UNDER THE FINANCIAL PROMOTION ORDER (ALL SUCH PERSONS TOGETHER BEING REFERRED TO AS “FPO PERSONS”); AND (B) IF MADE BY A PERSON WHO IS AN AUTHORIZED PERSON UNDER THE FSMA, IS BEING MADE ONLY

11

TO, OR DIRECTED ONLY AT, PERSONS WHO (I) ARE OUTSIDE THE UNITED KINGDOM, OR (II) HAVE PROFESSIONAL EXPERIENCE OF PARTICIPATING IN UNREGULATED SCHEMES (AS DEFINED FOR PURPOSES OF THE FINANCIAL SERVICES AND MARKETS ACT 2000 (PROMOTION OF COLLECTIVE INVESTMENT SCHEMES) (EXEMPTIONS) ORDER 2001 (AS AMENDED, THE “PROMOTION OF COLLECTIVE INVESTMENT SCHEMES EXEMPTIONS ORDER”) AND QUALIFY AS INVESTMENT PROFESSIONALS IN ACCORDANCE WITH ARTICLE 14(5) OF THE PROMOTION OF COLLECTIVE INVESTMENT SCHEMES EXEMPTIONS ORDER, OR (III) ARE PERSONS FALLING WITHIN ARTICLE 22(2)(A) THROUGH (D) (“HIGH NET WORTH COMPANIES, UNINCORPORATED ASSOCIATIONS, ETC.”) OF THE PROMOTION OF COLLECTIVE INVESTMENT SCHEMES EXEMPTIONS ORDER, OR (IV) PERSONS TO WHOM THE ISSUING ENTITY MAY LAWFULLY BE PROMOTED IN ACCORDANCE WITH SECTION 4.12 OF THE UK FINANCIAL CONDUCT AUTHORITY’S CONDUCT OF BUSINESS SOURCEBOOK (ALL SUCH PERSONS TOGETHER BEING REFERRED TO AS “PCIS PERSONS” AND, TOGETHER WITH THE FPO PERSONS, THE “RELEVANT PERSONS”).

THIS PROSPECTUS MUST NOT BE ACTED ON OR RELIED ON BY PERSONS WHO ARE NOT RELEVANT PERSONS. ANY INVESTMENT OR INVESTMENT ACTIVITY TO WHICH THIS PROSPECTUS RELATES, INCLUDING THE OFFERED CERTIFICATES, IS AVAILABLE ONLY TO RELEVANT PERSONS AND WILL BE ENGAGED IN ONLY WITH RELEVANT PERSONS.

POTENTIAL INVESTORS IN THE UNITED KINGDOM ARE ADVISED THAT ALL, OR MOST, OF THE PROTECTIONS AFFORDED BY THE UNITED KINGDOM REGULATORY SYSTEM WILL NOT APPLY TO AN INVESTMENT IN THE OFFERED CERTIFICATES AND THAT COMPENSATION WILL NOT BE AVAILABLE UNDER THE UNITED KINGDOM FINANCIAL SERVICES COMPENSATION SCHEME.

NOTICE TO RESIDENTS WITHIN EUROPEAN ECONOMIC AREA

THIS PROSPECTUS IS NOT A PROSPECTUS FOR THE PURPOSES OF THE PROSPECTUS DIRECTIVE (AS DEFINED BELOW).

THE OFFERED CERTIFICATES ARE NOT INTENDED TO BE OFFERED, SOLD OR OTHERWISE MADE AVAILABLE TO, AND SHOULD NOT BE OFFERED, SOLD OR OTHERWISE MADE AVAILABLE TO, ANY RETAIL INVESTOR IN THE EUROPEAN ECONOMIC AREA (“EEA”). FOR THESE PURPOSES, A RETAIL INVESTOR MEANS A PERSON WHO IS ONE (OR MORE) OF: (I) A RETAIL CLIENT AS DEFINED IN POINT (11) OF ARTICLE 4(1) OF DIRECTIVE 2014/65/EU (AS AMENDED, “MIFID II”); OR (II) A CUSTOMER WITHIN THE MEANING OF DIRECTIVE (EU) 2016/97, AS AMENDED (THE INSURANCE DISTRIBUTION DIRECTIVE), WHERE THAT CUSTOMER WOULD NOT QUALIFY AS A PROFESSIONAL CLIENT AS DEFINED IN POINT (10) OF ARTICLE 4(1) OF MIFID II; OR (III) NOT A QUALIFIED INVESTOR AS DEFINED IN THE PROSPECTUS DIRECTIVE.

CONSEQUENTLY NO KEY INFORMATION DOCUMENT REQUIRED BY REGULATION (EU) NO 1286/2014 (AS AMENDED, THE “PRIIPS REGULATION”) FOR OFFERING OR SELLING THE OFFERED CERTIFICATES OR OTHERWISE MAKING THEM AVAILABLE TO RETAIL INVESTORS IN THE EEA HAS BEEN PREPARED AND THEREFORE OFFERING OR SELLING THE OFFERED CERTIFICATES OR OTHERWISE MAKING THEM AVAILABLE TO ANY RETAIL INVESTOR IN THE EEA MAY BE UNLAWFUL UNDER THE PRIIPS REGULATION.

THIS PROSPECTUS HAS BEEN PREPARED ON THE BASIS THAT ANY OFFER OF CERTIFICATES IN ANY MEMBER STATE OF THE EEA WHICH HAS IMPLEMENTED THE PROSPECTUS DIRECTIVE (EACH, A “RELEVANT MEMBER STATE”) WILL ONLY BE MADE TO A LEGAL ENTITY WHICH IS A QUALIFIED INVESTOR UNDER THE PROSPECTUS DIRECTIVE (“QUALIFIED INVESTORS”). ACCORDINGLY ANY PERSON MAKING OR INTENDING TO MAKE AN OFFER IN THAT RELEVANT MEMBER STATE OF CERTIFICATES WHICH ARE THE SUBJECT OF THE OFFERING CONTEMPLATED IN THIS PROSPECTUS MAY ONLY DO SO WITH RESPECT TO QUALIFIED INVESTORS. NONE OF THE ISSUING ENTITY, THE DEPOSITOR OR ANY OF THE UNDERWRITERS HAVE AUTHORISED, NOR DO THEY AUTHORISE, THE MAKING OF ANY OFFER OF CERTIFICATES OTHER THAN TO QUALIFIED INVESTORS. THE EXPRESSION “PROSPECTUS DIRECTIVE” MEANS DIRECTIVE 2003/71/EC (AS AMENDED OR SUPERSEDED), AND INCLUDES ANY RELEVANT IMPLEMENTING MEASURE IN THE RELEVANT MEMBER STATE.

ANY DISTRIBUTOR SUBJECT TO MIFID II THAT IS OFFERING, SELLING OR RECOMMENDING THE OFFERED CERTIFICATES IS RESPONSIBLE FOR UNDERTAKING ITS OWN TARGET MARKET

12

ASSESSMENT IN RESPECT OF THE OFFERED CERTIFICATES AND DETERMINING ITS OWN DISTRIBUTION CHANNELS FOR THE PURPOSES OF THE MIFID II PRODUCT GOVERNANCE RULES UNDER COMMISSION DELEGATED DIRECTIVE (EU) 2017/593 (AS AMENDED, THE “DELEGATED DIRECTIVE”). NEITHER THE ISSUER, THE DEPOSITOR NOR ANY INITIAL PURCHASER MAKES ANY REPRESENTATIONS OR WARRANTIES AS TO A DISTRIBUTOR’S COMPLIANCE WITH THE DELEGATED DIRECTIVE.

EUROPEAN ECONOMIC AREA SELLING RESTRICTIONS

EACH UNDERWRITER HAS REPRESENTED AND AGREED THAT IT HAS NOT OFFERED, SOLD OR OTHERWISE MADE AVAILABLE, AND WILL NOT OFFER, SELL OR OTHERWISE MAKE AVAILABLE, ANY OFFERED CERTIFICATES TO ANY RETAIL INVESTOR IN THE EEA. FOR THE PURPOSES OF THIS PROVISION:

| ● | THE EXPRESSION “RETAIL INVESTOR” MEANS A PERSON WHO IS ONE (OR MORE) OF THE FOLLOWING: |

(A) A RETAIL CLIENT AS DEFINED IN POINT (11) OF ARTICLE 4(1) OF MIFID II;

(B) A CUSTOMER WITHIN THE MEANING OF THE INSURANCE DISTRIBUTION DIRECTIVE, WHERE THAT CUSTOMER WOULD NOT QUALIFY AS A PROFESSIONAL CLIENT AS DEFINED IN POINT (10) OF ARTICLE 4(1) OF MIFID II; OR

(C) NOT A QUALIFIED INVESTOR AS DEFINED IN THE PROSPECTUS DIRECTIVE; AND

| ● | THE EXPRESSION “OFFER” INCLUDES THE COMMUNICATION IN ANY FORM AND BY ANY MEANS OF SUFFICIENT INFORMATION ON THE TERMS OF THE OFFER AND THE CERTIFICATES TO BE OFFERED SO AS TO ENABLE AN INVESTOR TO DECIDE TO PURCHASE OR SUBSCRIBE THE OFFERED CERTIFICATES. |

PEOPLE’S REPUBLIC OF CHINA

THE OFFERED CERTIFICATES WILL NOT BE OFFERED OR SOLD IN THE PEOPLE’S REPUBLIC OF CHINA (EXCLUDING HONG KONG, MACAU AND TAIWAN, THE “PRC”) AS PART OF THE INITIAL DISTRIBUTION OF THE OFFERED CERTIFICATES BUT MAY BE AVAILABLE FOR PURCHASE BY INVESTORS RESIDENT IN THE PRC FROM OUTSIDE THE PRC.

THIS PROSPECTUS DOES NOT CONSTITUTE AN OFFER TO SELL OR THE SOLICITATION OF AN OFFER TO BUY ANY SECURITIES IN THE PRC TO ANY PERSON TO WHOM IT IS UNLAWFUL TO MAKE THE OFFER OR SOLICITATION IN THE PRC.

THE DEPOSITOR DOES NOT REPRESENT THAT THIS PROSPECTUS MAY BE LAWFULLY DISTRIBUTED, OR THAT ANY OFFERED CERTIFICATES MAY BE LAWFULLY OFFERED, IN COMPLIANCE WITH ANY APPLICABLE REGISTRATION OR OTHER REQUIREMENTS IN THE PRC, OR PURSUANT TO AN EXEMPTION AVAILABLE THEREUNDER, OR ASSUME ANY RESPONSIBILITY FOR FACILITATING ANY SUCH DISTRIBUTION OR OFFERING. IN PARTICULAR, NO ACTION HAS BEEN TAKEN BY THE DEPOSITOR WHICH WOULD PERMIT AN OFFERING OF ANY OFFERED CERTIFICATES OR THE DISTRIBUTION OF THIS PROSPECTUS IN THE PRC. ACCORDINGLY, THE OFFERED CERTIFICATES ARE NOT BEING OFFERED OR SOLD WITHIN THE PRC BY MEANS OF THIS PROSPECTUS OR ANY OTHER DOCUMENT. NEITHER THIS PROSPECTUS NOR ANY ADVERTISEMENT OR OTHER OFFERING MATERIAL MAY BE DISTRIBUTED OR PUBLISHED IN THE PRC, EXCEPT UNDER CIRCUMSTANCES THAT WILL RESULT IN COMPLIANCE WITH ANY APPLICABLE LAWS AND REGULATIONS.

HONG KONG

NO PERSON HAS ISSUED OR DISTRIBUTED OR HAD IN ITS POSSESSION FOR THE PURPOSES OF ISSUE OR DISTRIBUTION, OR WILL ISSUE OR DISTRIBUTE OR HAVE IN ITS POSSESSION FOR THE PURPOSES OF ISSUE OR DISTRIBUTION, WHETHER IN HONG KONG OR ELSEWHERE, ANY ADVERTISEMENT, INVITATION OR DOCUMENT RELATING TO THE OFFERED CERTIFICATES, WHICH IS DIRECTED AT, OR THE CONTENTS OF WHICH ARE LIKELY TO BE ACCESSED OR READ BY, THE PUBLIC

13

OF HONG KONG (EXCEPT IF PERMITTED TO DO SO UNDER THE SECURITIES LAWS OF HONG KONG) OTHER THAN WITH RESPECT TO OFFERED CERTIFICATES WHICH ARE OR ARE INTENDED TO BE DISPOSED OF (A) ONLY TO PERSONS OUTSIDE HONG KONG OR (B) ONLY TO “PROFESSIONAL INVESTORS” WITHIN THE MEANING OF THE SECURITIES AND FUTURES ORDINANCE (CAP. 571 OF THE LAWS OF HONG KONG) (THE “SFO”) AND ANY RULES OR REGULATIONS MADE UNDER THE SFO.

THE OFFERED CERTIFICATES (IF THEY ARE NOT A “STRUCTURED PRODUCT” AS DEFINED IN THE SECURITIES AND FUTURES ORDINANCE (CAP. 571 OF THE LAWS OF HONG KONG) HAVE NOT BEEN OFFERED OR SOLD AND WILL NOT BE OFFERED OR SOLD, BY MEANS OF ANY DOCUMENT, OTHER THAN (A) TO “PROFESSIONAL INVESTORS” AS DEFINED IN THE SFO AND ANY RULES OR REGULATIONS MADE UNDER THE SFO, OR (B) IN OTHER CIRCUMSTANCES WHICH DO NOT RESULT IN THE DOCUMENT CONSTITUTING A “PROSPECTUS” AS DEFINED IN THE COMPANIES (WINDING UP AND MISCELLANEOUS PROVISIONS) ORDINANCE (CAP. 32 OF THE LAWS OF HONG KONG) OR WHICH DO NOT CONSTITUTE AN OFFER TO THE PUBLIC WITHIN THE MEANING OF THE COMPANIES ORDINANCE (CAP. 622 OF THE LAWS OF HONG KONG). FURTHER, THE CONTENTS OF THIS PROSPECTUS HAVE NOT BEEN REVIEWED OR APPROVED BY THE SECURITIES AND FUTURES COMMISSION OF HONG KONG OR ANY OTHER REGULATORY AUTHORITY IN HONG KONG. YOU ARE ADVISED TO EXERCISE CAUTION IN RELATION TO THE OFFERING CONTEMPLATED IN THIS PROSPECTUS. IF YOU ARE IN ANY DOUBT ABOUT ANY OF THE CONTENTS OF THIS PROSPECTUS, YOU SHOULD OBTAIN INDEPENDENT PROFESSIONAL ADVICE.

NOTICE TO PROSPECTIVE INVESTORS IN SINGAPORE

NEITHER THIS PROSPECTUS NOR ANY OTHER DOCUMENT OR MATERIAL IN CONNECTION WITH ANY OFFER OF THE OFFERED CERTIFICATES HAS BEEN OR WILL BE LODGED OR REGISTERED AS A PROSPECTUS WITH THE MONETARY AUTHORITY OF SINGAPORE (“MAS”) UNDER THE SECURITIES AND FUTURES ACT (CAP. 289) OF SINGAPORE (THE “SFA”). ACCORDINGLY, MAS ASSUMES NO RESPONSIBILITY FOR THE CONTENTS OF THIS PROSPECTUS. THIS PROSPECTUS IS NOT A PROSPECTUS AS DEFINED IN THE SFA AND STATUTORY LIABILITY UNDER THE SFA IN RELATION TO THE CONTENTS OF PROSPECTUSES WOULD NOT APPLY. PROSPECTIVE INVESTORS SHOULD CONSIDER CAREFULLY WHETHER THE INVESTMENT IS SUITABLE FOR IT.

THIS PROSPECTUS AND ANY OTHER DOCUMENTS OR MATERIALS IN CONNECTION WITH THE OFFER OR SALE, OR INVITATION FOR SUBSCRIPTION OR PURCHASE, OF THE OFFERED CERTIFICATES MAY NOT BE DIRECTLY OR INDIRECTLY ISSUED, CIRCULATED OR DISTRIBUTED, NOR MAY THE OFFERED CERTIFICATES BE OFFERED OR SOLD, OR BE MADE THE SUBJECT OF AN INVITATION FOR SUBSCRIPTION OR PURCHASE, WHETHER DIRECTLY OR INDIRECTLY, TO PERSONS IN SINGAPORE OTHER THAN (I) TO AN INSTITUTIONAL INVESTOR (AS DEFINED IN SECTION 4A(1)(C) OF THE SFA (“INSTITUTIONAL INVESTOR”)) PURSUANT TO SECTION 304 OF THE SFA.

UNLESS SUCH OFFERED CERTIFICATES ARE OF THE SAME CLASS AS OTHER OFFERED CERTIFICATES OF THE ISSUING ENTITY THAT ARE LISTED FOR QUOTATION ON AN APPROVED EXCHANGE (AS DEFINED IN SECTION 2(1) OF THE SFA) (“APPROVED EXCHANGE”) AND IN RESPECT OF WHICH ANY OFFER, INFORMATION, STATEMENT, INTRODUCTORY DOCUMENT, SHAREHOLDERS’ CIRCULAR FOR A REVERSE TAKE-OVER DOCUMENT ISSUED FOR THE PURPOSES OF A TRUST SCHEME OR ANY OTHER SIMILAR DOCUMENT APPROVED BY AN APPROVED EXCHANGE WAS ISSUED IN CONNECTION WITH AN OFFER OR THE LISTING FOR QUOTATION OF THOSE CERTIFICATES, ANY SUBSEQUENT OFFERS IN SINGAPORE OF OFFERED CERTIFICATES ACQUIRED PURSUANT TO AN INITIAL OFFER MADE HEREUNDER MAY ONLY BE MADE, PURSUANT TO THE REQUIREMENTS OF SECTION 304A, TO PERSONS WHO ARE INSTITUTIONAL INVESTORS.

AS THE OFFERED CERTIFICATES ARE ONLY OFFERED TO PERSONS IN SINGAPORE WHO QUALIFY AS AN INSTITUTIONAL INVESTOR, THE ISSUING ENTITY IS NOT REQUIRED TO DETERMINE THE CLASSIFICATION OF THE OFFERED CERTIFICATES PURSUANT TO SECTION 309B OF THE SFA.

NOTHING SET OUT IN THIS NOTICE SHALL BE CONSTRUED AS LEGAL ADVICE AND EACH PROSPECTIVE INVESTOR SHOULD CONSULT ITS OWN LEGAL COUNSEL. THIS NOTICE IS FURTHER SUBJECT TO THE PROVISIONS OF THE SFA AND ITS REGULATIONS AS THE SAME MAY BE AMENDED OR CONSOLIDATED FROM TIME TO TIME AND DOES NOT PURPORT TO BE EXHAUSTIVE IN ANY RESPECT.

14

NOTICE TO RESIDENTS OF THE REPUBLIC OF KOREA

THIS PROSPECTUS IS NOT, AND UNDER NO CIRCUMSTANCES IS THIS PROSPECTUS TO BE CONSTRUED AS, A PUBLIC OFFERING OF SECURITIES IN KOREA. NEITHER THE ISSUER NOR ANY OF ITS AGENTS MAKE ANY REPRESENTATION WITH RESPECT TO THE ELIGIBILITY OF ANY RECIPIENTS OF THIS PROSPECTUS TO ACQUIRE THE OFFERED CERTIFICATES UNDER THE LAWS OF KOREA, INCLUDING, BUT WITHOUT LIMITATION, THE FOREIGN EXCHANGE TRANSACTION LAW AND REGULATIONS THEREUNDER (THE “FETL”). THE OFFERED CERTIFICATES HAVE NOT BEEN REGISTERED WITH THE FINANCIAL SERVICES COMMISSION OF KOREA FOR PUBLIC OFFERING IN KOREA, AND NONE OF THE OFFERED CERTIFICATES MAY BE OFFERED, SOLD OR DELIVERED, DIRECTLY OR INDIRECTLY, OR OFFERED OR SOLD TO ANY PERSON FOR RE-OFFERING OR RESALE, DIRECTLY OR INDIRECTLY IN KOREA OR TO ANY RESIDENT OF KOREA EXCEPT PURSUANT TO THE FINANCIAL INVESTMENT SERVICES AND CAPITAL MARKETS ACT AND THE DECREES AND REGULATIONS THEREUNDER (THE “FSCMA”), THE FETL AND ANY OTHER APPLICABLE LAWS, REGULATIONS AND MINISTERIAL GUIDELINES IN KOREA. WITHOUT PREJUDICE TO THE FOREGOING, THE NUMBER OF OFFERED CERTIFICATES OFFERED IN KOREA OR TO A RESIDENT OF KOREA SHALL BE LESS THAN FIFTY AND FOR A PERIOD OF ONE YEAR FROM THE ISSUE DATE OF THE OFFERED CERTIFICATES, NONE OF THE OFFERED CERTIFICATES MAY BE DIVIDED RESULTING IN AN INCREASED NUMBER OF OFFERED CERTIFICATES. FURTHERMORE, THE OFFERED CERTIFICATES MAY NOT BE RESOLD TO KOREAN RESIDENTS UNLESS THE PURCHASER OF THE OFFERED CERTIFICATES COMPLIES WITH ALL APPLICABLE REGULATORY REQUIREMENTS (INCLUDING, BUT NOT LIMITED TO, GOVERNMENT REPORTING APPROVAL REQUIREMENTS UNDER THE FETL AND ITS SUBORDINATE DECREES AND REGULATIONS) IN CONNECTION WITH THE PURCHASE OF THE OFFERED CERTIFICATES.

JAPAN

THE OFFERED CERTIFICATES HAVE NOT BEEN AND WILL NOT BE REGISTERED UNDER THE FINANCIAL INSTRUMENTS AND EXCHANGE LAW OF JAPAN, AS AMENDED (THE “FIEL”), AND DISCLOSURE UNDER THE FIEL HAS NOT BEEN AND WILL NOT BE MADE WITH RESPECT TO THE OFFERED CERTIFICATES. ACCORDINGLY, EACH UNDERWRITER HAS REPRESENTED AND AGREED THAT IT HAS NOT, DIRECTLY OR INDIRECTLY, OFFERED OR SOLD AND WILL NOT, DIRECTLY OR INDIRECTLY, OFFER OR SELL ANY OFFERED CERTIFICATES IN JAPAN OR TO, OR FOR THE BENEFIT OF, ANY RESIDENT OF JAPAN (WHICH TERM AS USED IN THIS PROSPECTUS MEANS ANY PERSON RESIDENT IN JAPAN, INCLUDING ANY CORPORATION OR OTHER ENTITY ORGANIZED UNDER THE LAWS OF JAPAN) OR TO OTHERS FOR RE-OFFERING OR RE-SALE, DIRECTLY OR INDIRECTLY, IN JAPAN OR TO, OR FOR THE BENEFIT OF, ANY RESIDENT OF JAPAN EXCEPT PURSUANT TO AN EXEMPTION FROM THE REGISTRATION REQUIREMENTS OF, AND OTHERWISE IN COMPLIANCE WITH, THE FIEL AND OTHER RELEVANT LAWS, REGULATIONS AND MINISTERIAL GUIDELINES OF JAPAN.

NOTICE TO RESIDENTS OF CANADA

THE OFFERED CERTIFICATES MAY BE SOLD IN CANADA ONLY TO PURCHASERS PURCHASING, OR DEEMED TO BE PURCHASING, AS PRINCIPAL THAT ARE ACCREDITED INVESTORS, AS DEFINED IN NATIONAL INSTRUMENT 45-106 PROSPECTUS EXEMPTIONS OR SUBSECTION 73.3(1) OF THE SECURITIES ACT (ONTARIO), AND ARE PERMITTED CLIENTS, AS DEFINED IN NATIONAL INSTRUMENT 31-103 REGISTRATION REQUIREMENTS, EXEMPTIONS AND ONGOING REGISTRANT OBLIGATIONS. ANY RESALE OF THE OFFERED CERTIFICATES MUST BE MADE IN ACCORDANCE WITH AN EXEMPTION FROM, OR IN A TRANSACTION NOT SUBJECT TO, THE PROSPECTUS REQUIREMENTS OF APPLICABLE SECURITIES LAWS.

SECURITIES LEGISLATION IN CERTAIN PROVINCES OR TERRITORIES OF CANADA MAY PROVIDE A PURCHASER WITH REMEDIES FOR RESCISSION OR DAMAGES IF THIS PROSPECTUS (INCLUDING ANY AMENDMENT THERETO) CONTAINS A MISREPRESENTATION, PROVIDED THAT THE REMEDIES FOR RESCISSION OR DAMAGES ARE EXERCISED BY THE PURCHASER WITHIN THE TIME LIMIT PRESCRIBED BY THE SECURITIES LEGISLATION OF THE PURCHASER’S PROVINCE OR TERRITORY. THE PURCHASER SHOULD REFER TO ANY APPLICABLE PROVISIONS OF THE SECURITIES LEGISLATION OF THE PURCHASER’S PROVINCE OR TERRITORY FOR PARTICULARS OF THESE RIGHTS OR CONSULT WITH A LEGAL ADVISOR.

15

PURSUANT TO SECTION 3A.3 OF NATIONAL INSTRUMENT 33-105 UNDERWRITING CONFLICTS (“NI 33-105”), THE UNDERWRITERS ARE NOT REQUIRED TO COMPLY WITH THE DISCLOSURE REQUIREMENTS OF NI 33-105 REGARDING UNDERWRITER CONFLICTS OF INTEREST IN CONNECTION WITH THIS OFFERING.

FORWARD-LOOKING STATEMENTS

In this prospectus, we use certain forward-looking statements. These forward-looking statements are found in the material, including each of the tables, set forth under “Risk Factors” and “Yield, Prepayment and Maturity Considerations”. Forward-looking statements are also found elsewhere in this prospectus and include words like “expects,” “intends,” “anticipates,” “estimates” and other similar words. These statements are intended to convey our projections or expectations as of the date of this prospectus. These statements are inherently subject to a variety of risks and uncertainties. Actual results could differ materially from those we anticipate due to changes in, among other things:

| ● | economic conditions and industry competition, |

| ● | political and/or social conditions, and |

| ● | the law and government regulatory initiatives. |

We will not update or revise any forward-looking statement to reflect changes in our expectations or changes in the conditions or circumstances on which these statements were originally based.

16

Summary of Terms

The following is only a summary of selected information in this prospectus. It does not contain all of the information you need to consider in making your investment decision. More detailed information appears elsewhere in this prospectus. To understand all of the terms of the offered certificates, carefully read this entire document. See“Index of Certain Defined Terms”for definitions of capitalized terms.

General

| Title of Certificates | Benchmark 2019-B9 Mortgage Trust, Commercial Mortgage Pass-Through Certificates, Series 2019-B9. |

Relevant Parties

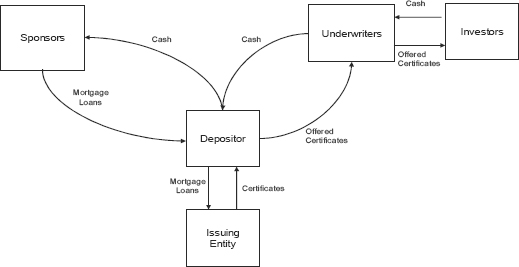

| Depositor | Citigroup Commercial Mortgage Securities Inc., a Delaware corporation and an indirect, wholly-owned subsidiary of Citigroup Global Markets Holdings Inc. As depositor, Citigroup Commercial Mortgage Securities Inc. will acquire the mortgage loans from the sponsors and transfer them to the issuing entity. The depositor’s address is 388 Greenwich Street, New York, New York 10013 and its telephone number is (212) 816-5343. See “Transaction Parties—The Depositor.” |

| Issuing Entity | Benchmark 2019-B9 Mortgage Trust, a New York common law trust to be established on the closing date of this securitization transaction under the pooling and servicing agreement, to be dated as of February 1, 2019, between the depositor, the master servicer, the special servicer, the trustee, the certificate administrator, the operating advisor and the asset representations reviewer. See “Transaction Parties—The Issuing Entity”. |

| Sponsors | The sponsors will be transferring the mortgage loans to the depositor for inclusion in the issuing entity. The sponsors of this transaction are: |

| ● | Citi Real Estate Funding Inc., a New York corporation (25 mortgage loans (49.9%)); |

| ● | German American Capital Corporation, a Maryland corporation (14 mortgage loans (28.9%)); and |

| ● | JPMorgan Chase Bank, National Association, a national banking association organized under the laws of the United States of America (11 mortgage loans (21.2%)). |

| The sponsors are sometimes also referred to in this prospectus as the “mortgage loan sellers”. |

17

| Originators | The sponsors originated (or co-originated) the mortgage loans or acquired (or, on or prior to the closing date, will acquire) the mortgage loans, directly or indirectly, from the originators as set forth in the following chart: |

| Originator | Sponsor | Number Mortgage Loans | Aggregate Balance of Loans | Approx. % of Initial Pool Balance | ||||||||

| Citi Real Estate Funding Inc. | Citi Real Estate Funding Inc. | 25 | $441,277,378 | 49.9 | % | |||||||

| JPMorgan Chase Bank, National Association | JPMorgan Chase Bank, National Association | 11 | (1) | 187,240,118 | 21.2 | |||||||

| Deutsche Bank AG, acting through its New York Branch | German American Capital Corporation(2) | 8 | 151,893,323 | 17.2 | ||||||||

| German American Capital Corporation | German American Capital Corporation | 6 | 103,107,000 | 11.7 | ||||||||

| Total | 50 | $883,517,820 | 100.0 | % | ||||||||

| (1) | Includes the Aventura Mall mortgage loan (1.7%), which is part of a loan combination that was co-originated by JPMorgan Chase Bank, National Association, Wells Fargo Bank, National Association, Deutsche Bank AG, acting through its New York Branch, and Morgan Stanley Bank, N.A., and is evidenced by the promissory note designated as note A-2-A-5-B, with an outstanding principal balance of $15,000,000 as of the cut-off date. |

| (2) | German American Capital Corporation has acquired or will acquire the mortgage loans that were originated or co-originated by Deutsche Bank AG, acting through its New York Branch, on or prior to the closing date. |

| See “Transaction Parties—The Sponsors and the Mortgage Loan Sellers”. |

| Master Servicer | Wells Fargo Bank, National Association, a national banking association, will be the master servicer. The master servicer will, in general, be responsible for the master servicing and administration of the serviced mortgage loans and the related companion loans pursuant to the pooling and servicing agreement for this transaction (excluding those mortgage loans and companion loans that are or become part of outside serviced loan combinations and that are currently, or become in the future, serviced under an outside servicing agreement as indicated in the table titled “Outside Serviced Mortgage Loans Summary” under “—Relevant Parties—Outside Servicers, Outside Special Servicers, Outside Trustees and Outside Custodians”below). The principal west coast commercial mortgage master servicing offices of Wells Fargo Bank, National Association are located at MAC-A0227-020, 1901 Harrison Street, Oakland, California 94612. The principal east coast commercial mortgage master servicing offices of Wells Fargo Bank, National Association are located at Three Wells Fargo, MAC D1050-084, 401 South Tryon Street, Charlotte, North Carolina 28202. See “Transaction Parties—Servicers—The Master Servicer” and “The Pooling and Servicing Agreement—Servicing of the Mortgage Loans”. |

| See “—The Mortgage Pool—The Loan Combinations”below for a discussion of the mortgage loans included in the issuing entity that are part of a loan combination and have one or more related companion loans held outside the issuing entity. |

18

| The mortgage loans transferred to the issuing entity, any related companion loans and any related loan combinations that are, in each case, serviced under the pooling and servicing agreement for this securitization transaction are referred to in this prospectus as “serviced mortgage loans,” “serviced companion loans” and “serviced loan combinations,” respectively. A serviced mortgage loan and a serviced companion loan may each also be referred to as a “serviced loan”. Any mortgage loans transferred to the issuing entity, related companion loans and related loan combinations that are not serviced under the pooling and servicing agreement, but are instead serviced under a separate servicing agreement (an “outside servicing agreement”) governing the securitization of one or more related companion loans, are referred to as “outside serviced mortgage loans,” “outside serviced companion loans,” and “outside serviced loan combinations,” respectively. An outside serviced mortgage loan and an outside serviced companion loan may each also be referred to as an “outside serviced loan”. |

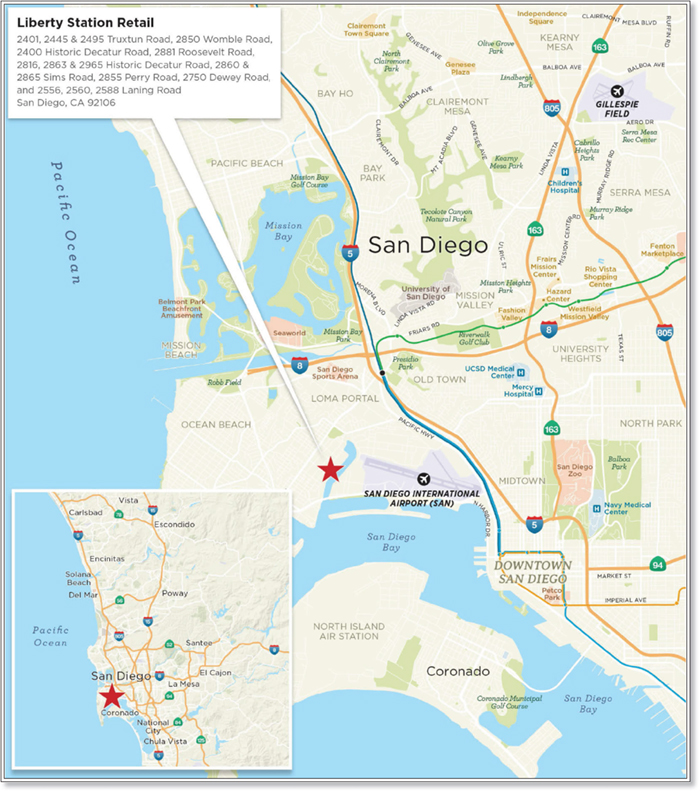

| The Liberty Station Retail mortgage loan is part of a loan combination that will initially be serviced pursuant to the pooling and servicing agreement for this securitization transaction. However, upon the inclusion of the related controlling pari passu companion loan in a future securitization transaction, the servicing of the related loan combination will shift to the servicing agreement (which will then become an outside servicing agreement) governing that future securitization transaction. Accordingly, the Liberty Station Retail mortgage loan, the related companion loan(s) and the related loan combination will be: (i) a serviced mortgage loan, serviced companion loan(s) and a serviced loan combination, respectively, prior to any such shift in servicing; and (ii) an outside serviced mortgage loan, outside serviced companion loan(s) and an outside serviced loan combination, respectively, after the related shift in servicing occurs. The Liberty Station Retail mortgage loan, the related companion loan(s) and the related loan combination are sometimes referred to as a “servicing shift mortgage loan”, “servicing shift companion loan(s)” and a “servicing shift loan combination”, respectively. |

| See the chart entitled “Loan Combination Summary” under “The Mortgage Pool—Loan Combinations” below in this summary and the chart entitled “Servicing of the Loan Combinations” under “The Pooling and Servicing Agreement—General” below for a listing of the serviced loan combinations, outside serviced loan combinations and servicing shift loan combinations. |

| The servicer(s) of the outside serviced mortgage loan(s) (to the extent definitively identified) are set forth in the table titled “Outside Serviced Mortgage Loans Summary” under “—Relevant Parties—Outside Servicers, Outside Special Servicers, Outside Trustees and Outside Custodians” below. See “Transaction Parties—Servicers—The Outside Servicers and the Outside Special Servicers”and“The Pooling and Servicing Agreement—Servicing of the Outside Serviced Mortgage Loans”. |

| Special Servicer | LNR Partners, LLC, a Florida limited liability company, will be the initial special servicer with respect to the serviced mortgage loans (other than any excluded special servicer mortgage loan) and any related serviced companion loans pursuant to the pooling and servicing agreement. The special servicer will be primarily responsible for (i) making decisions and performing certain servicing functions with respect to the serviced mortgage loans and any related companion loans as to which a special servicing transfer event (such as a default or an imminent default) has |

19

| occurred, as well as any related REO properties acquired on behalf of the issuing entity and any related companion loan holders, and (ii) reviewing, evaluating, processing and/or providing or withholding consent as to certain major decisions and certain other matters identified as “special servicer decisions” relating to such serviced mortgage loans and any related companion loans for which a special servicing transfer event has not occurred, in each case pursuant to the pooling and servicing agreement for this transaction. The principal special servicing offices of the special servicer are located at 1601 Washington Avenue, Suite 700, Miami Beach, Florida 33139, and its telephone number is (305) 695-5600. See “Transaction Parties—Servicers—The Special Servicer”, and “The Pooling and Servicing Agreement—Servicing of the Mortgage Loans” and “—Servicing and Other Compensation and Payment of Expenses”. |

| If the special servicer, to its knowledge, becomes a borrower party (as defined under “—Directing Holder / Controlling Class Representative” below) with respect to any mortgage loan (such mortgage loan, an “excluded special servicer mortgage loan”), it will be required to resign with respect to the servicing of that mortgage loan. The controlling class representative (prior to the occurrence and continuance of a control termination event (as described under“—Directing Holder / Controlling Class Representative” below)) will be entitled to appoint a separate special servicer that is not a borrower party with respect to such excluded special servicer mortgage loan (such special servicer, an “excluded mortgage loan special servicer”) unless such excluded special servicer mortgage loan is also an excluded mortgage loan (as defined under“—Directing Holder / Controlling Class Representative” below), in which case the largest controlling class certificateholder (by certificate balance) that is not an excluded controlling class holder with respect to that mortgage loan will be entitled to appoint the excluded mortgage loan special servicer. A controlling class certificateholder that is a borrower party with respect to any mortgage loan will be an “excluded controlling class holder” with respect to that mortgage loan. See“—Directing Holder / Controlling Class Representative” below. Any excluded mortgage loan special servicer will be required to perform all of the obligations of the special servicer for the related excluded special servicer mortgage loan and will be entitled to all special servicing compensation with respect to such excluded special servicer mortgage loan earned during such time as the related mortgage loan is an excluded special servicer mortgage loan. If neither the controlling class representative nor any controlling class certificateholder is entitled to appoint an excluded mortgage loan special servicer for an excluded special servicer mortgage loan, an excluded mortgage loan special servicer will be appointed in the manner described in this prospectus and as provided under the pooling and servicing agreement. See “The Pooling and Servicing Agreement—Termination of the Special Servicer Other Than in Connection With a Servicer Termination Event” in this prospectus. |

| LNR Partners, LLC, was selected to be the initial special servicer by Prime Finance Long Duration (B-Piece) II, L.P., one or more affiliates of which are expected to : (a) purchase a majority interest in the Class F, Class G, Class H, Class J, Class X-F, Class X-G, Class X-H, Class X-J and Class S certificates on the closing date; and (b) appoint Prime Finance Long Duration (B-Piece) II, L.P. or an affiliate as the initial controlling class representative and the initial directing holder with respect to the serviced loans other than any serviced outside controlled loan combination and any excluded mortgage loan. See “—Directing |

20

| Holder / Controlling Class Representative” below and “The Pooling and Servicing Agreement—Directing Holder”. LNR Securities Holding, LLC, an affiliate of LNR Partners, LLC, or an affiliate is expected to purchase a minority interest in the Class F, Class G, Class H, Class J, Class X-F, Class X-G, Class X-H, Class X-J and Class S certificates equal to approximately 40% of the initial certificate balance or notional amount of each such class (or, in the case of the Class S certificates, equal to an approximately 40% percentage interest in such class). |

| The special servicer (but not the special servicer with respect to any outside serviced mortgage loan) may be removed in such capacity under the pooling and servicing agreement, with or without cause, as set forth under (and subject to certain conditions described under) “The Pooling and Servicing Agreement—Termination of the Special Servicer Other Than in Connection With a Servicer Termination Event”, “—Servicer Termination Events” and “—Rights Upon Servicer Termination Event.” |

| A special servicer with respect to any outside serviced mortgage loan may only be removed in such capacity in accordance with the terms and provisions of the applicable outside servicing agreement and the co-lender agreement governing the related outside serviced loan combination. |

| The special servicer(s) of the outside serviced mortgage loan(s) (to the extent definitively identified) are set forth in the table below titled “Outside Serviced Mortgage Loans Summary” under “—Relevant Parties—Outside Servicers, Outside Special Servicers, Outside Trustees and Outside Custodians” below.See“Transaction Parties—Servicers—The Outside Servicers and the Outside Special Servicers” and “The Pooling and Servicing Agreement—Servicing of the Outside Serviced Mortgage Loans”. |

| Significant Primary Servicer | Midland Loan Services, a Division of PNC Bank, National Association, will act as primary servicer with respect to the serviced mortgage loans sold to the depositor by JPMorgan Chase Bank, National Association. See “Transaction Parties—Servicers—Significant Primary Servicer—Midland Loan Services, a Division of PNC Bank, National Association”. |

| The master servicer (or related outside servicer, in the case of an outside serviced mortgage loan) will be responsible to pay the fees of Midland Loan Services and each other primary servicer out of the servicing fees payable under the pooling and servicing agreement for this transaction or the related outside servicing agreement, as applicable. |

| Trustee | Wilmington Trust, National Association, a national banking association, will act as trustee. The corporate trust office of the trustee is located at 1100 North Market Street, Wilmington, Delaware 19890, Attention: Benchmark 2019-B9. Following the transfer of the mortgage loans, the trustee, on behalf of the issuing entity, will become the mortgagee of record for each serviced mortgage loan and any related companion loans; except that, with respect to each servicing shift loan combination, the trustee will not become the mortgagee of record unless the related servicing shift does not occur within 180 days after the closing date or the loan combination becomes specially serviced prior to the related servicing shift. Upon the occurrence of the related servicing shift with respect to any servicing shift loan combination, the trustee of the securitization of the related controlling pari passu companion loan will become the mortgagee of record. In addition, subject to the terms of the pooling and servicing agreement, the trustee will be primarily responsible |

21

| for back-up advancing. See “Transaction Parties—The Trustee” and “The Pooling and Servicing Agreement”. |

| The trustee(s) with respect to the outside serviced mortgage loan(s) (to the extent definitively identified) are set forth in the table titled “Outside Serviced Mortgage Loans Summary” under “—Relevant Parties—Outside Servicers, Outside Special Servicers, Outside Trustees and Outside Custodians” below. See“The Pooling and Servicing Agreement—Servicing of the Outside Serviced Mortgage Loans”. |

| Certificate Administrator | Citibank, N.A., a national banking association organized under the laws of the United States, will initially act as certificate administrator. The certificate administrator will also be required to act as custodian, certificate registrar, REMIC administrator, 17g-5 information provider, paying agent and authenticating agent. The corporate trust offices of the certificate administrator are located at 388 Greenwich Street, New York, New York 10013, Attention: Global Transaction Services – Benchmark 2019-B9, and for certificate transfer purposes are located at 480 Washington Boulevard, 30th Floor, Jersey City, New Jersey 07310, Attention: Securities Window. See “Transaction Parties—The Certificate Administrator” and“The Pooling and Servicing Agreement”. |