| FREE WRITING PROSPECTUS | ||

| FILED PURSUANT TO RULE 433 | ||

| REGISTRATION FILE NO.: 333-228597-09 | ||

| June 14, 2021 |

BENCHMARK 2021-B27 Commercial Mortgage Trust | ||||

Free Writing Prospectus Structural and Collateral Term Sheet | ||||

$1,093,912,985 (Approximate Initial Mortgage Pool Balance) | ||||

| $899,351,000 | ||||

| (Approximate Offered Certificates) | ||||

Citigroup Commercial Mortgage Securities Inc. Depositor | ||||

Commercial Mortgage Pass-Through Certificates Series 2021-B27 | ||||

Citi Real Estate Funding Inc. Goldman Sachs Mortgage Company JPMorgan Chase Bank, National Association German American Capital Corporation | ||||

| As Sponsors and Mortgage Loan Sellers | ||||

| Citigroup | J.P. Morgan | Deutsche Bank Securities | Goldman Sachs & | ||||

| Co-Lead Managers and Joint Bookrunners | |||||||

| Academy Securities | Siebert Williams Shank | ||||||

| Co-Managers | |||||||

STATEMENT REGARDING THIS FREE WRITING PROSPECTUS

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-228597) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Goldman Sachs & Co. LLC, Deutsche Bank Securities Inc., J.P. Morgan Securities LLC, Academy Securities, Inc., Siebert Williams Shank & Co., LLC or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

IMPORTANT NOTICE RELATING TO AUTOMATICALLY GENERATED EMAIL DISCLAIMERS

Any legends, disclaimers or other notices that may appear at the bottom of the email communication to which this free writing prospectus is attached relating to (1) these materials not constituting an offer (or a solicitation of an offer), (2) no representation being made that these materials are accurate or complete and that these materials may not be updated or (3) these materials possibly being confidential, are, in each case, not applicable to these materials and should be disregarded. Such legends, disclaimers or other notices have been automatically generated as a result of these materials having been sent via Bloomberg or another system.

| ||

| CERTIFICATE SUMMARY |

The securities offered by this structural and collateral term sheet (this “Term Sheet”) are described in greater detail in the preliminary prospectus, dated on or about June 14, 2021, included as part of our registration statement (SEC File No. 333-228597) (the “Preliminary Prospectus”). The Preliminary Prospectus contains material information that is not contained in this Term Sheet (including, without limitation, a summary of risks associated with an investment in the offered securities under the heading “Summary of Risk Factors” and a detailed discussion of such risks under the heading “Risk Factors”). The Preliminary Prospectus is available upon request from Citigroup Global Markets Inc., Goldman Sachs & Co. LLC, J.P. Morgan Securities LLC, Deutsche Bank Securities Inc., Academy Securities, Inc. or Siebert Williams Shank & Co., LLC. This Term Sheet is subject to change.

For information regarding certain risks associated with an investment in this transaction, refer to “Summary of Risk Factors” and “Risk Factors” in the Preliminary Prospectus. Capitalized terms used but not otherwise defined in this Term Sheet have the respective meanings assigned to those terms in the Preliminary Prospectus.

The Securities May Not Be a Suitable Investment for You

The securities offered by this Term Sheet are not suitable investments for all investors. In particular, you should not purchase any class of securities unless you understand and are able to bear the prepayment, credit, liquidity and market risks associated with that class of securities. For those reasons and for the reasons set forth under the headings “Summary of Risk Factors” and “Risk Factors” in the Preliminary Prospectus, the yield to maturity of, the aggregate amount and timing of distributions on and the market value of the offered securities are subject to material variability from period to period and give rise to the potential for significant loss over the life of those securities. The interaction of these factors and their effects are impossible to predict and are likely to change from time to time. As a result, an investment in the offered securities involves substantial risks and uncertainties and should be considered only by sophisticated institutional investors with substantial investment experience with similar types of securities and who have conducted appropriate due diligence on the mortgage loans and the securities. Potential investors are advised and encouraged to review the Preliminary Prospectus in full and to consult with their legal, tax, accounting and other advisors prior to making any investment in the offered securities described in this Term Sheet.

The securities offered by these materials are being offered when, as and if issued. This Term Sheet is not to be construed as an offer to sell or the solicitation of any offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal. The information contained in this Term Sheet may not pertain to any securities that will actually be sold. The information contained in this Term Sheet may be based on assumptions regarding market conditions and other matters as reflected in this Term Sheet. We make no representations regarding the reasonableness of such assumptions or the likelihood that any of such assumptions will coincide with actual market conditions or events, and this Term Sheet should not be relied upon for such purposes. We and our affiliates, officers, directors, partners and employees, including persons involved in the preparation or issuance of this Term Sheet may, from time to time, have long or short positions in, and buy or sell, the securities mentioned in this Term Sheet or derivatives thereof (including options). Information contained in this Term Sheet is current as of the date appearing on this Term Sheet only. Information in this Term Sheet regarding the securities and the mortgage loans backing any securities discussed in this Term Sheet supersedes all prior information regarding such securities and mortgage loans. None of Citigroup Global Markets Inc., Goldman Sachs & Co. LLC, J.P. Morgan Securities LLC, Deutsche Bank Securities Inc., Academy Securities, Inc. or Siebert Williams Shank & Co., LLC provides accounting, tax or legal advice.

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-228597) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Goldman Sachs & Co. LLC, J.P. Morgan Securities LLC, Deutsche Bank Securities Inc., Academy Securities, Inc., Siebert Williams Shank & Co., LLC or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

2

| CERTIFICATE SUMMARY |

The issuing entity will be relying on an exclusion or exemption from the definition of “investment company” under the Investment Company Act of 1940, as amended (the “Investment Company Act”), contained in Section 3(c)(5) of the Investment Company Act or Rule 3a-7 under the Investment Company Act, although there may be additional exclusions or exemptions available to the issuing entity. The issuing entity is being structured so as not to constitute a “covered fund” for purposes of the Volcker Rule under the Dodd-Frank Act (both as defined in “Risk Factors—General Risk Factors—Legal and Regulatory Provisions Affecting Investors Could Adversely Affect the Liquidity and Other Aspects of the Offered Certificates” in the Preliminary Prospectus). See also “Legal Investment” in the Preliminary Prospectus.

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-228597) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Goldman Sachs & Co. LLC, J.P. Morgan Securities LLC, Deutsche Bank Securities Inc., Academy Securities, Inc., Siebert Williams Shank & Co., LLC or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

3

| CERTIFICATE SUMMARY |

| OFFERED CERTIFICATES | |||||||||||||||||

| Offered Classes | Expected Ratings | Approximate Initial Certificate Balance or Notional | Approximate Initial Credit Support(3) | Initial Pass-Through Rate(4) | Pass-Through Rate Description | Expected | Expected Principal Window(5) | ||||||||||

| Class A-1 | AAA(sf) / AAAsf / AAA(sf) | $18,655,000 | 30.000 | % | % | (6) | 2.75 | 07/21 – 05/26 | |||||||||

| Class A-2 | AAA(sf) / AAAsf / AAA(sf) | $37,990,000 | 30.000 | % | % | (6) | 4.96 | 05/26 – 07/26 | |||||||||

| Class A-3 | AAA(sf) / AAAsf / AAA(sf) | $83,071,000 | 30.000 | % | % | (6) | 6.83 | 04/28 – 06/28 | |||||||||

| Class A-4 | AAA(sf) / AAAsf / AAA(sf) | (7) | 30.000 | % | % | (6) | (7) | (7) | |||||||||

| Class A-5 | AAA(sf) / AAAsf / AAA(sf) | (7) | 30.000 | % | % | (6) | (7) | (7) | |||||||||

| Class A-AB | AAA(sf) / AAAsf / AAA(sf) | $26,294,000 | 30.000 | % | % | (6) | 7.43 | 07/26 – 04/31 | |||||||||

| Class X-A | AAA(sf) / AAAsf / AAA(sf) | $808,494,000 (8) | N/A | % | Variable IO(9) | N/A | N/A | ||||||||||

| Class A-S | AAA(sf) / AAAsf / AAA(sf) | $71,105,000 | 23.250 | % | % | (6) | 9.96 | 06/31 – 06/31 | |||||||||

| Class B | AA(sf) / AA-sf / AA+(sf) | $42,136,000 | 19.250 | % | % | (6) | 9.96 | 06/31 – 06/31 | |||||||||

| Class C | A-(sf) / A-sf / A+(sf) | $48,721,000 | 14.625 | % | % | (6) | 9.96 | 06/31 – 06/31 | |||||||||

NON-OFFERED CERTIFICATES(10)

Non-Offered Classes | Expected Ratings | Approximate Initial Certificate Balance or Notional | Approximate Initial Credit Support(3) | Initial Pass-Through Rate(4) | Pass-Through Rate Description | Expected | Expected Principal Window(5) |

| Class X-B | A-(sf) / A-sf / AAA(sf) | $90,857,000(8) | N/A | % | Variable IO(9) | N/A | N/A |

| Class X-D | NR / BBB-sf / AAA(sf) | $64,521,000(8) | N/A | % | Variable IO(9) | N/A | N/A |

| Class X-F | NR / BB+sf / BBB-(sf) | $15,802,000(8) | N/A | % | Variable IO(9) | N/A | N/A |

| Class X-G | NR / BB-sf / BB(sf) | $14,484,000(8) | N/A | % | Variable IO(9) | N/A | N/A |

| Class D | NR / BBBsf / A-(sf) | $35,553,000 | 11.250% | % | (6) | 9.98 | 06/31 – 07/31 |

| Class E | NR / BBB-sf / BBB(sf) | $28,968,000 | 8.500% | % | (6) | 10.04 | 07/31 – 07/31 |

| Class F | NR / BB+sf / BBB-(sf) | $15,802,000 | 7.000% | % | (6) | 10.04 | 07/31 – 07/31 |

| Class G | NR / BB-sf / BB(sf) | $14,484,000 | 5.625% | % | (6) | 10.04 | 07/31 – 07/31 |

| Class J-RR(11) | NR / B-sf / B+(sf) | $11,851,000 | 4.500% | % | (6) | 10.04 | 07/31 – 07/31 |

| Class K-RR(11) | NR / NR / NR | $47,403,985 | 0.000% | % | (6) | 10.04 | 07/31 – 07/31 |

| Class S(12) | N/A | N/A | N/A | N/A | N/A | N/A | N/A |

| Class R(12) | N/A | N/A | N/A | N/A | N/A | N/A | N/A |

| NON-OFFERED VERTICAL RISK RETENTION INTEREST(10) | |||||||

Non-Offered Eligible Vertical Interest | Expected Ratings | Approximate Initial Combined VRR Interest Balance(2) | Approximate Initial Credit Support(3) | Initial Effective Interest Rate(4) | Effective Interest Rate Description | Expected | Expected Principal Window(5) |

| Combined VRR Interest(13) | NR / NR / NR | $40,500,000 | N/A(14) | %(15) | (15) | 9.19 | 07/21 – 07/31 |

| (1) | It is a condition of issuance that the offered certificates and certain classes of non-offered certificates receive the ratings set forth above. The anticipated ratings shown are those of S&P Global Ratings, a Standard & Poor’s Financial Services LLC business (“S&P”), Fitch Ratings, Inc. (“Fitch”) and Kroll Bond Rating Agency, LLC (“KBRA”). Subject to the discussion under “Ratings” in the Preliminary Prospectus, the ratings on the certificates address the likelihood of the timely receipt by holders of all payments of interest to which they are entitled on each distribution date and, except in the case of the interest only certificates, the ultimate receipt by holders of all payments of principal to which they are entitled on or before the applicable rated final distribution date. Certain nationally recognized statistical rating organizations, as defined in Section 3(a)(62) of the Securities Exchange Act of 1934, as amended, that were not hired by the depositor may use information they receive pursuant to Rule 17g-5 under the Securities Exchange Act of 1934, as amended, or otherwise to rate the offered certificates. We cannot assure you as to what ratings a non-hired nationally recognized statistical rating organization would assign. See “Risk Factors—Other Risks Relating to the Certificates—Nationally Recognized Statistical Rating Organizations May Assign Different Ratings to the Certificates; Ratings of the Certificates Reflect Only the Views of the Applicable Rating Agencies as of the Dates Such Ratings Were Issued; Ratings May Affect ERISA Eligibility; Ratings May Be Downgraded” in the Preliminary Prospectus. S&P, Fitch and KBRA have informed us that the “sf” designation in the ratings represents an identifier of structured finance product ratings. For additional information about this identifier, prospective investors can go to the related rating agency’s website. The depositor and the underwriters have not verified, do not adopt and do not accept responsibility for any statements made by the rating agencies on those websites. Credit ratings referenced throughout this Term Sheet are forward-looking opinions about credit risk and express a rating agency’s opinion about the willingness and ability of an issuer of securities to meet its financial obligations in full and on time. Ratings are not indications of investment merit and are not buy, sell or hold recommendations, a measure of asset value or an indication of the suitability of an investment. |

| (2) | Approximate, subject to a variance of plus or minus 5% and further subject to any additional variances described in the footnotes below. In addition, the notional amounts of the Class X-A, Class X-B, Class X-D, Class X-F, and Class X-G certificates (collectively, the “Class X Certificates”) may vary depending upon the final pricing of the classes of Principal Balance Certificates (as defined in footnote (14) below) whose certificate balances comprise such notional amounts, and, if as a result of such pricing (a) the pass-through rate of any class of Class X Certificates, would be equal to zero at all times, such class of Class X Certificates will not be issued on the closing date of this securitization (the “Closing Date”) or (b) the pass-through rate of any class of Principal Balance Certificates whose certificate balance comprises such notional amount is at all times equal to the weighted average of the net interest rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) as in effect from time to time (the “WAC Rate”), the certificate balance of such class of Principal Balance Certificates may not be part of, and there would be a corresponding reduction in, such notional amount of the related class of Class X Certificates. |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-228597) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Goldman Sachs & Co. LLC, J.P. Morgan Securities LLC, Deutsche Bank Securities Inc., Academy Securities, Inc., Siebert Williams Shank & Co., LLC or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

4

| CERTIFICATE SUMMARY |

| (3) | "Approximate Initial Credit Support" means, with respect to any class of Non-Vertically Retained Principal Balance Certificates (as defined in footnote (6) below), the quotient, expressed as a percentage, of (i) the aggregate of the initial certificate balances of all classes of Non-Vertically Retained Principal Balance Certificates, if any, junior to such class of Non-Vertically Retained Principal Balance Certificates, divided by (ii) the aggregate of the initial certificate balances of all classes of Non-Vertically Retained Principal Balance Certificates. The approximate initial credit support percentages set forth for the Class A-1, Class A-2, Class A-3, Class A-4, Class A-5 and Class A-AB certificates are represented in the aggregate. The approximate initial credit support percentages shown in the table above do not take into account the Combined VRR Interest (as defined in footnote (13) below). |

| (4) | Approximate per annum rate as of the Closing Date. |

| (5) | Determined assuming no prepayments prior to the maturity date or any anticipated repayment date, as applicable, for any mortgage loan and based on the modeling assumptions described under “Yield, Prepayment and Maturity Considerations” in the Preliminary Prospectus. |

| (6) | For any distribution date, the pass-through rate for each class of the Class A-1, Class A-2, Class A-3, Class A-4, Class A-5, Class A-AB, Class A-S, Class B, Class C, Class D, Class E, Class F, Class G, Class J-RR and Class K-RR certificates (collectively, the “Non-Vertically Retained Principal Balance Certificates”, and collectively with the Class X, Class S and Class R certificates, the “Non-Vertically Retained Certificates”, and the Non-Vertically Retained Certificates, collectively with the Class VRR certificates, the “Certificates”) will generally be equal to one of (i) a fixed per annum rate, (ii) the WAC Rate, (iii) a rate equal to the lesser of a specified per annum rate and the WAC Rate, or (iv) the WAC Rate less a specified percentage, but no less than 0.000%. The Non-Vertically Retained Certificates, other than the Class S and Class R certificates, are collectively referred to in this term sheet as the “Non-Vertically Retained Regular Certificates”. See “Description of the Certificates—Distributions—Pass-Through Rates” in the Preliminary Prospectus. |

| (7) | The exact initial certificate balances of the Class A-4 and Class A-5 certificates are unknown and will be determined based on the final pricing of those classes of certificates. However, the respective initial certificate balances, weighted average lives and principal windows of the Class A-4 and Class A-5 certificates are expected to be within the applicable ranges reflected, in the following chart. The aggregate initial certificate balance of the Class A-4 and Class A-5 certificates is expected to be approximately $571,379,000, subject to a variance of plus or minus 5%. |

Class of Certificates | Expected Range of Initial Certificate Balances | Expected Range of Weighted Avg. Lives (Yrs) | Expected Range of Principal Windows |

| Class A-4 | $0 – $265,000,000 | NAP – 9.31 | NAP / 02/30 – 05/31 |

| Class A-5 | $306,379,000 – $571,379,000 | 9.96 – 9.66 | 05/31 – 06/31 / 02/30 – 06/31 |

| (8) | The Class X Certificates will not have certificate balances and will not be entitled to receive distributions of principal. Interest will accrue on each class of Class X Certificates at the related pass-through rate based upon the related notional amount. The notional amount of each class of the Class X Certificates will be equal to the certificate balance or the aggregate of the certificate balances, as applicable, from time to time of the class or classes of the Non-Vertically Retained Principal Balance Certificates identified in the same row as such class of Class X Certificates in the chart below (as to such class of Class X Certificates, the “Corresponding Principal Balance Certificates”): |

| Class of Class X Certificates | Class(es) of Corresponding Principal Balance Certificates |

| Class X-A | Class A-1, Class A-2, Class A-3, Class A-4, Class A-5, Class A-AB and Class A-S |

| Class X-B | Class B and Class C |

| Class X-D | Class D and Class E |

| Class X-F | Class F |

| Class X-G | Class G |

| (9) | The pass-through rate for each class of Class X Certificates will generally be a per annum rate equal to the excess, if any, of (i) the WAC Rate over (ii) the pass-through rate (or, if applicable, the weighted average of the pass-through rates) of the class or classes of Corresponding Principal Balance Certificates as in effect from time to time, as described in the Preliminary Prospectus. See “Description of the Certificates—Distributions—Pass-Through Rates” in the Preliminary Prospectus. |

| (10) | The classes of certificates set forth below “Non-Offered Certificates” and “Non-Offered Vertical Risk Retention Interest” in the table are not offered by this Term Sheet. |

| (11) | In partial satisfaction of the risk retention obligations of Citi Real Estate Funding Inc. (“CREFI”) (as “retaining sponsor” with respect to this securitization transaction), all of the Class J-RR and Class K-RR certificates (collectively, the “HRR Certificates”), with an aggregate fair value expected to represent at least 1.31% of the fair value, as of the closing date for this securitization transaction, of all of the “ABS interests” (i.e. all of the certificates (other than the Class R certificates) and the Uncertificated VRR Interest) issued by the issuing entity, will collectively constitute an “eligible horizontal residual interest” that is to be purchased and retained by KKR CMBS II Aggregator Type 1 L.P., a Delaware limited partnership, or its affiliate in accordance with the credit risk retention rules applicable to this securitization transaction. “Retaining sponsor,” “ABS interests” and “eligible horizontal residual interest” have the meanings given to such terms in Regulation RR. See “Credit Risk Retention” in the Preliminary Prospectus. |

| (12) | Neither the Class S certificates nor the Class R certificates will have a certificate balance, notional amount, pass-through rate, rating or rated final distribution date. A specified portion of the “excess interest” accruing after the related anticipated repayment date on any mortgage loan with an anticipated repayment date will, to the extent collected, be allocated to the Class S certificates as set forth in “Description of the Certificates—Distributions—Excess Interest” in the Preliminary Prospectus. The Class R certificates will represent the residual interests in each of four separate REMICs, as further described in the Preliminary Prospectus. The Class R certificates will not be entitled to distributions of principal or interest. |

| (13) | In partial satisfaction of CREFI’s remaining risk retention obligations as retaining sponsor for this securitization transaction, CREFI is expected to acquire (or cause one or more other retaining parties to acquire) from the depositor, on the closing date for this securitization transaction, portions of an “eligible vertical interest” in the form of a “single vertical security” with an initial principal balance of approximately $40,500,000 (the “Combined VRR Interest”), which is expected to represent approximately 3.70% of all of the “ABS interests” (i.e. of the sum of the aggregate initial certificate balance of all of the certificates (other than the Class R certificates) and the initial principal balance of the Uncertificated VRR Interest) issued by the issuing entity on the closing date for this securitization transaction, subject to any variation in the initial principal balance of the Combined VRR Interest following calculation of the actual fair value of the HRR Certificates, all of the other classes of certificates (other than the Class R certificates) and the Uncertificated VRR Interest, as described under “Credit Risk Retention” in the Preliminary Prospectus. The Combined VRR Interest will consist of the “Uncertificated VRR Interest” and the “Class VRR Certificates” (each as defined under “Credit Risk Retention” in the Preliminary Prospectus). The Combined VRR Interest will be retained by certain retaining parties in accordance with the credit risk retention rules applicable to this securitization transaction. “Eligible vertical interest” and “single vertical security” have the meanings given to such terms in Regulation RR. See “Credit Risk Retention” in the Preliminary Prospectus. The Combined VRR Interest is not offered hereby. |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-228597) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Goldman Sachs & Co. LLC, J.P. Morgan Securities LLC, Deutsche Bank Securities Inc., Academy Securities, Inc., Siebert Williams Shank & Co., LLC or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

5

| CERTIFICATE SUMMARY |

| (14) | Although the approximate initial credit support percentages shown in the table above with respect to the Non-Vertically Retained Principal Balance Certificates do not take into account the Combined VRR Interest, losses incurred on the mortgage loans will be allocated between the Combined VRR Interest, on the one hand, and the Non-Vertically Retained Principal Balance Certificates, on the other hand, pro rata in accordance with the principal balance of the Combined VRR Interest (the “Combined VRR Interest Balance”) and the aggregate outstanding certificate balance of the Non-Vertically Retained Principal Balance Certificates, respectively. See “Credit Risk Retention” and “Description of the Certificates” in the Preliminary Prospectus. The Class VRR certificates and the Non-Vertically Retained Principal Balance Certificates are collectively referred to in this Term Sheet as the “Principal Balance Certificates”. |

| (15) | Although it does not have a specified pass-through rate (other than for tax reporting purposes), the effective interest rate for the Combined VRR Interest will be the WAC Rate. |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-228597) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Goldman Sachs & Co. LLC, J.P. Morgan Securities LLC, Deutsche Bank Securities Inc., Academy Securities, Inc., Siebert Williams Shank & Co., LLC or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

6

| MORTGAGE POOL CHARACTERISTICS |

| Mortgage Pool Characteristics(1) | ||

| Initial Pool Balance(2) | $1,093,912,985 | |

| Number of Mortgage Loans | 47 | |

| Number of Mortgaged Properties | 170 | |

| Average Cut-off Date Balance | $23,274,744 | |

| Weighted Average Mortgage Rate | 3.50333% | |

| Weighted Average Remaining Term to Maturity/ARD (months)(3)(5) | 113 | |

| Weighted Average Remaining Amortization Term (months)(4) | 346 | |

| Weighted Average Cut-off Date LTV Ratio(6)(7) | 56.1% | |

| Weighted Average Maturity Date/ARD LTV Ratio(3)(6) | 53.2% | |

| Weighted Average UW NCF DSCR(8) | 2.82x | |

| Weighted Average Debt Yield on Underwritten NOI(7)(9) | 10.9% | |

| % of Initial Pool Balance of Mortgage Loans that are Amortizing Balloon | 8.8% | |

| % of Initial Pool Balance of Mortgage Loans that are Interest Only then Amortizing Balloon | 12.5% | |

| % of Initial Pool Balance of Mortgage Loans that are Interest Only | 58.9% | |

| % of Initial Pool Balance of Mortgage Loans that are Interest Only – ARD | 16.2% | |

| % of Initial Pool Balance of Mortgage Loans that are Amortizing Balloon – ARD | 3.7% | |

| % of Initial Pool Balance of Mortgaged Properties with Single Tenants | 37.6% | |

| % of Initial Pool Balance of Mortgage Loans with Mezzanine Debt | 23.0% | |

| % of Initial Pool Balance of Mortgage Loans with Subordinate Debt | 18.6% | |

| (1) | The Cut-off Date LTV Ratio, Maturity Date/ARD LTV Ratio, UW NCF DSCR, Debt Yield on Underwritten NOI and Cut-off Date Balance Per SF / Unit / Room information for each mortgage loan is presented in this Term Sheet (i) if such mortgage loan is part of a loan combination (as defined under “Collateral Overview—Loan Combination Summary” below), based on both that mortgage loan and any related pari passu companion loan(s) but, unless otherwise specifically indicated, without regard to any related subordinate companion loan(s), and (ii) unless otherwise specifically indicated, without regard to any other indebtedness (whether or not secured by the related mortgaged property, ownership interests in the related borrower or otherwise) that currently exists or that may be incurred by the related borrower or its owners in the future. |

| (2) | Subject to a permitted variance of plus or minus 5%. |

| (3) | Unless otherwise indicated, mortgage loans with anticipated repayment dates are presented as if they were to mature on the anticipated repayment date. |

| (4) | Excludes mortgage loans that are interest-only for the entire term. |

| (5) | With respect to six mortgage loans, representing approximately 15.6% of the initial pool balance, the initial due dates for such mortgage loans occur after July 2021. On the Closing Date, the related mortgage loan seller(s) will contribute an initial interest deposit amount to the issuing entity to cover an amount that represents one month’s interest that would have accrued with respect to each such mortgage loan at the related interest rate with respect to the assumed July 2021 payment date. Information presented in this Term Sheet reflects the contractual loan terms; however, each such mortgage loan is being treated as having an initial due date in July 2021. |

| (6) | The Cut-off Date LTV Ratios and Maturity Date/ARD LTV Ratios presented in this Term Sheet are generally based on the “as-is” appraised values of the related mortgaged properties (as set forth on Annex A to the Preliminary Prospectus), provided that such LTV ratios may be calculated based on (i) “as-stabilized” or similar values in certain cases where the completion of certain hypothetical conditions or other events at the property are assumed and/or where reserves have been established at origination to satisfy the applicable condition or event that is expected to occur, or (ii) the Cut-off Date Balance or Balloon Balance, as applicable, net of a related earnout or holdback reserve, or (iii) the “as-is” appraised value for a portfolio of mortgaged properties that includes a premium relating to the valuation of the portfolio of mortgaged properties as a whole rather than as the sum of individually valued mortgaged properties, in each case as further described in the definitions of “Appraised Value”, “Cut-off Date LTV Ratio” and “Maturity Date/ARD LTV Ratio” under “Description of the Mortgage Pool—Certain Calculations and Definitions” in the Preliminary Prospectus. |

| (7) | The Cut-off Date LTV Ratio, Debt Yield on Underwritten NOI and Debt Yield on Underwritten NCF with respect to the Mission Promenade mortgage loan are each calculated net of a $750,000 holdback reserve. |

| (8) | The UW NCF DSCR for each mortgage loan is generally calculated by dividing the Underwritten NCF for the related mortgaged property or mortgaged properties by the annual debt service for such mortgage loan, as adjusted in the case of mortgage loans with a partial interest only period by using the first 12 amortizing payments due instead of the actual interest only payment due. |

| (9) | The Debt Yield on Underwritten NOI for each mortgage loan is generally calculated as the related mortgaged property’s Underwritten NOI divided by the Cut-off Date Balance of such mortgage loan, and the Debt Yield on Underwritten NCF for each mortgage loan is generally calculated as the related mortgaged property’s Underwritten NCF divided by the Cut-off Date Balance of such mortgage loan. |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-228597) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Goldman Sachs & Co. LLC, J.P. Morgan Securities LLC, Deutsche Bank Securities Inc., Academy Securities, Inc., Siebert Williams Shank & Co., LLC or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

7

| MORTGAGE POOL CHARACTERISTICS |

| COVID-19 Updates | |||||||||||||||||

| Loan No. | Property Name | Mortgage Loan Seller | Property Type | Information as of Date | First Payment Date | March Debt Service Payment Received (Y/N) | April Debt Service Payment Received (Y/N) | May Debt Service Payment Received (Y/N) | Forbearance or Other Debt Service Relief Requested | Other Loan Modification Requested (Y/N) | Lease Modification or Rent Relief Requested (Y/N) | Occupied SF or Unit Count Making Full March Rent Payment (%) | UW March Base Rent Paid (%) | Occupied SF or Unit Count Making Full April Rent Payment (%) | UW April Base Rent Paid (%) | Occupied SF or Unit Count Making Full May Rent Payment (%) | UW May Base Rent Paid (%) |

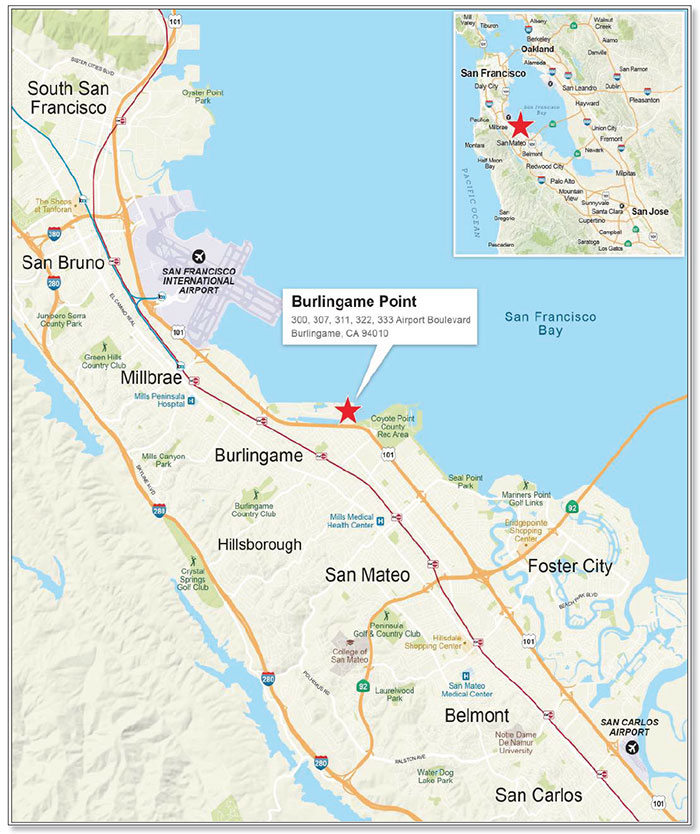

| 1 | Burlingame Point | GSMC, GACC, JPMCB | Office | 6/8/2021 | 5/6/2021 | NAP | NAP | Yes | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% |

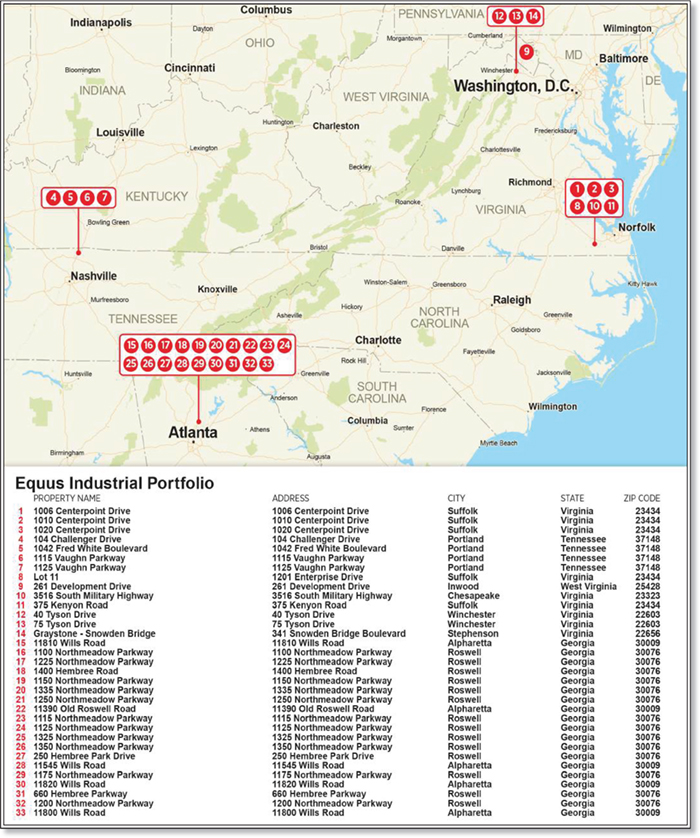

| 2 | Equus Industrial Portfolio | GSMC | Industrial | 6/8/2021 | 5/9/2021 | NAP | NAP | NAP | No | No | No | 96.5% | 96.5% | 99.8% | 99.8% | 99.8% | 99.8% |

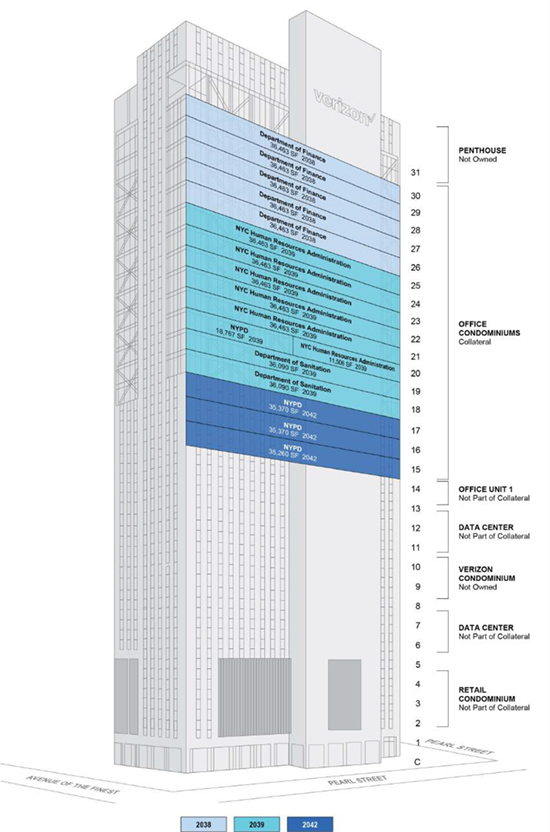

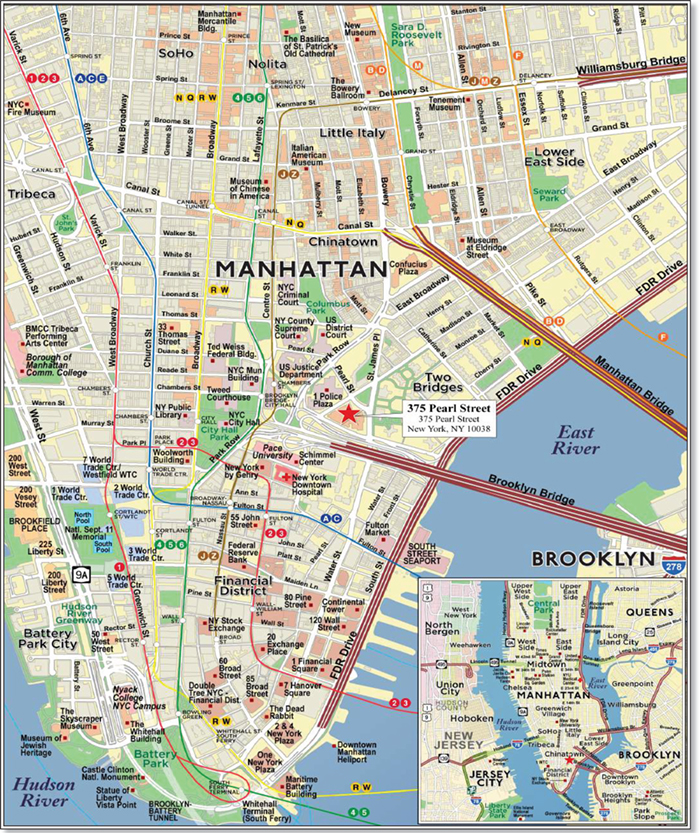

| 3 | 375 Pearl Street | JPMCB | Office | 6/2/2021 | 7/11/2021 | NAP | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% |

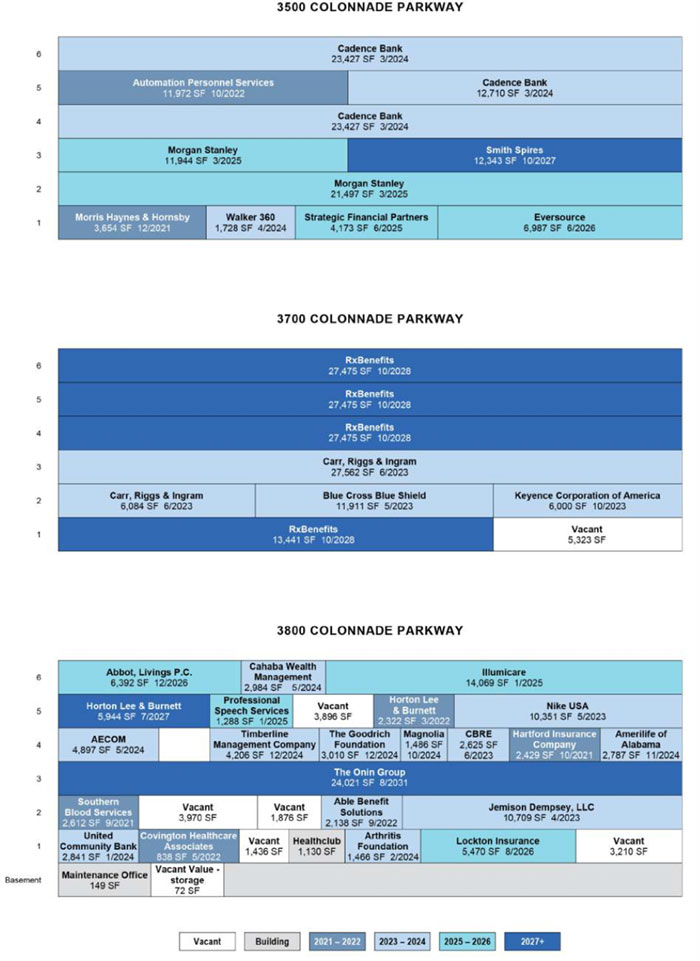

| 4 | Colonnade Corporate Center | JPMCB | Office | 6/2/2021 | 7/5/2021 | NAP | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% |

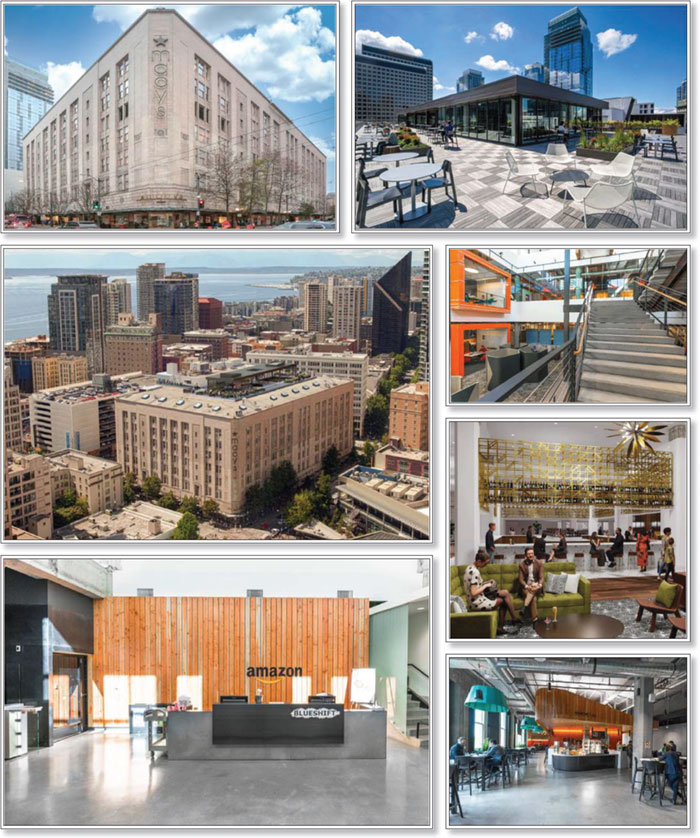

| 5 | Amazon Seattle(1) | GACC | Office | 6/3/2021 | 5/6/2021 | NAP | NAP | Yes | No | No | Yes | 99.6% | 99.6% | 100.0% | 100.0% | 100.0% | 100.0% |

| 6 | 4500 Academy Road Distribution Center | CREFI | Industrial | 6/6/2021 | 7/6/2021 | NAP | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% |

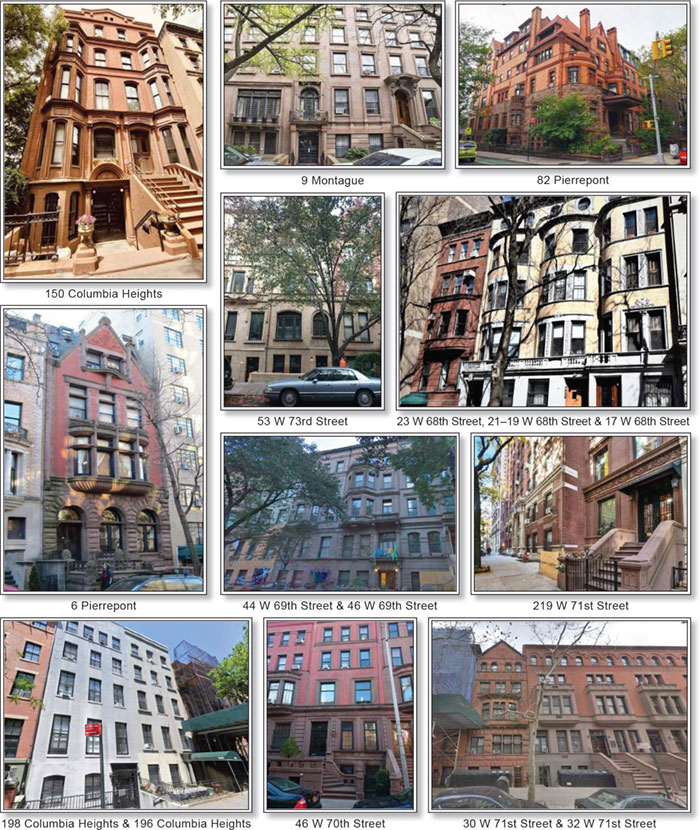

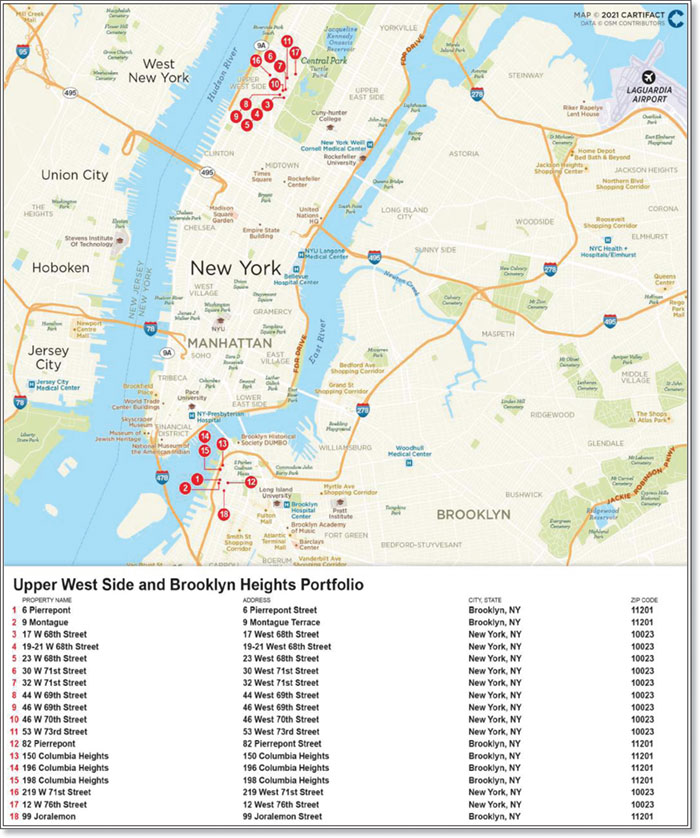

| 7 | Upper West Side and Brooklyn Heights Portfolio | CREFI | Multifamily | 6/6/2021 | 7/6/2021 | NAP | NAP | NAP | No | No | No | 97.0% | 97.0% | 97.0% | 97.0% | 97.0% | 97.0% |

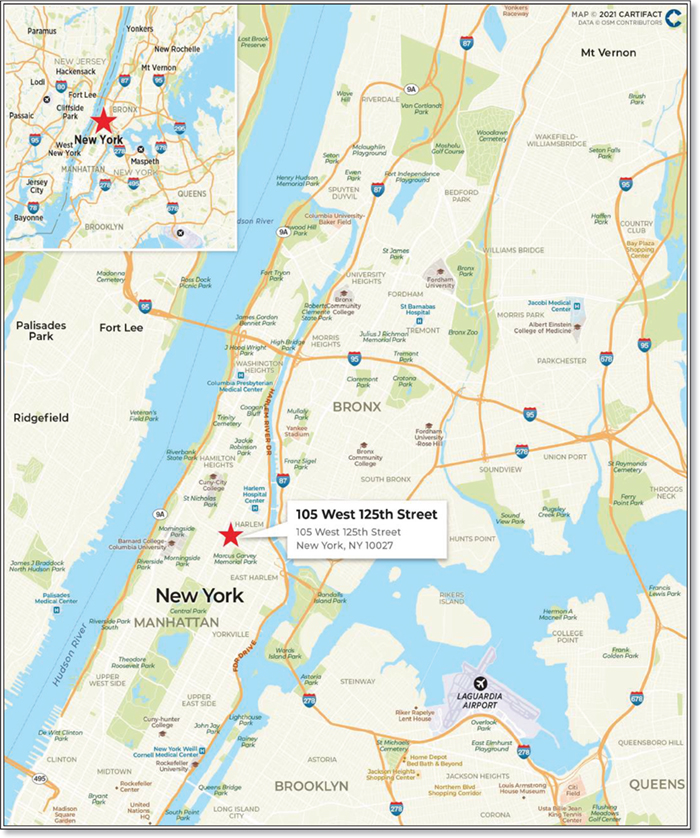

| 8 | 105 West 125th Street | GSMC | Office | 6/8/2021 | 7/6/2021 | NAP | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% |

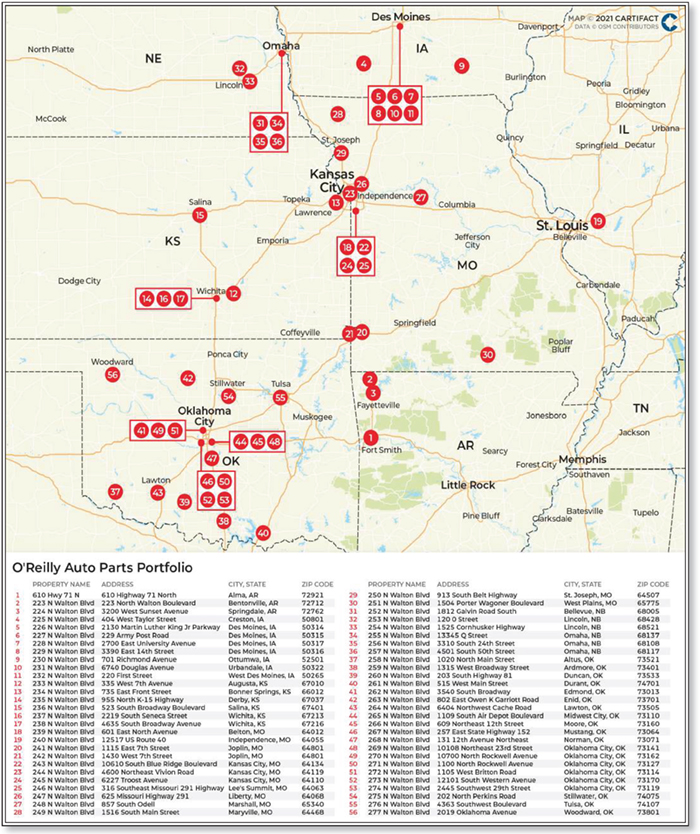

| 9 | O'Reilly Auto Parts Portfolio | GACC | Retail | 6/3/2021 | 5/6/2021 | NAP | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% |

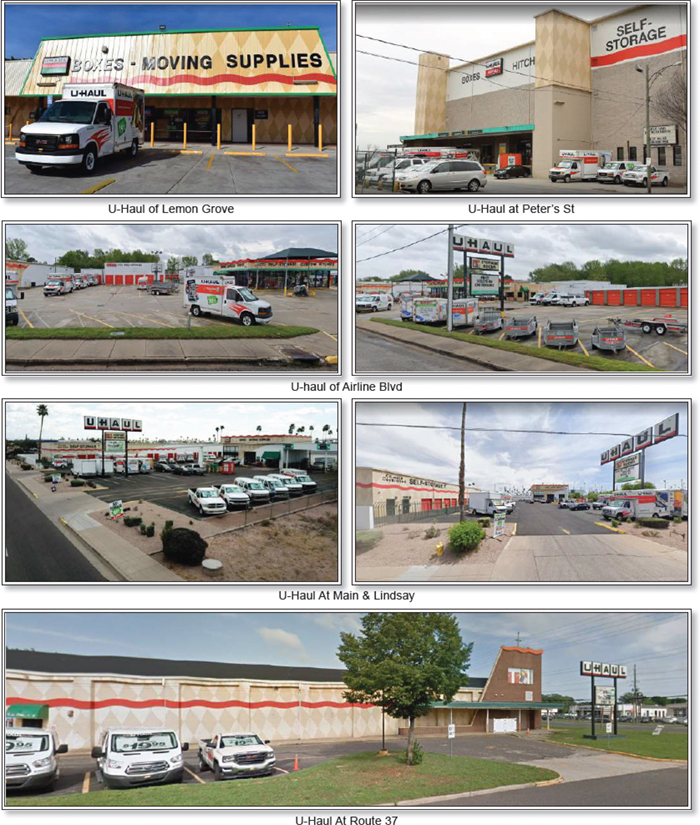

| 10 | U-Haul SAC 20 | JPMCB | Self Storage | 6/2/2021 | 7/1/2021 | NAP | NAP | NAP | No | No | NAP | NAP | NAP | NAP | NAP | NAP | NAP |

| 11 | 335 West 16th Street | CREFI | Office | 6/6/2021 | 7/6/2021 | NAP | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% |

| 12 | Culver City Fee | CREFI | Other | 6/6/2021 | 7/6/2021 | NAP | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% |

| 13 | Union Square Mixed Use Portfolio(2) | CREFI | Various | 6/6/2021 | 7/6/2021 | NAP | NAP | NAP | No | No | Yes | 99.0% | 99.0% | 99.0% | 99.0% | 99.0% | 99.0% |

| 14 | Fisker Corporate Headquarters | GSMC | Office | 6/13/2021 | 6/6/2021 | NAP | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% |

| 15 | Chase Tower | JPMCB | Office | 6/2/2021 | 7/1/2021 | NAP | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% |

| 16 | iPark 84 Innovation Center | CREFI | Industrial | 6/6/2021 | 6/6/2021 | NAP | NAP | Yes | No | No | Yes | 96.6% | 97.4% | 96.6% | 97.4% | 96.6% | 97.4% |

| 17 | 100 East California Ave | CREFI | Office | 6/6/2021 | 7/6/2021 | NAP | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% |

| 18 | 252 Atlantic Avenue(3) | CREFI | Retail | 6/6/2021 | 7/6/2021 | NAP | NAP | NAP | No | No | Yes | 100.0% | 99.3% | 100.0% | 99.3% | 100.0% | 99.3% |

| 19 | Holiday Inn Express San Diego | GSMC | Hospitality | 6/8/2021 | 7/6/2021 | NAP | NAP | NAP | No | No | No | NAP | NAP | NAP | NAP | NAP | NAP |

| 20 | 1985 Marcus | GSMC | Office | 6/8/2021 | 5/6/2021 | NAP | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% |

| 21 | Truax Office(4) | GACC | Mixed Use | 6/9/2021 | 7/6/2021 | NAP | NAP | NAP | No | No | Yes | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% |

| 22 | Alabama Hilton Portfolio(5) | CREFI | Hospitality | 6/6/2021 | 3/6/2020 | Yes | Yes | Yes | Yes | Yes | No | NAP | NAP | NAP | NAP | NAP | NAP |

| 23 | Accenture San Antonio | CREFI | Office | 6/6/2021 | 7/6/2021 | NAP | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% |

| 24 | All World Storage Romeoville | CREFI | Self Storage | 6/6/2021 | 7/6/2021 | NAP | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% |

| 25 | 1-11 South Market Street | CREFI | Industrial | 6/6/2021 | 6/6/2021 | NAP | NAP | NAP | No | No | Yes | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% |

| 26 | DoubleTree Spokane | JPMCB | Hospitality | 6/2/2021 | 7/1/2021 | NAP | NAP | NAP | No | No | NAP | NAP | NAP | NAP | NAP | NAP | NAP |

| 27 | 475 Oakmead | GSMC | Office | 6/13/2021 | 7/6/2021 | NAP | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% |

| 28 | Fordham Road | JPMCB | Retail | 6/2/2021 | 7/1/2021 | NAP | NAP | NAP | No | No | Yes | 88.3% | 95.7% | 88.3% | 95.7% | 88.3% | 95.7% |

| 29 | 500 W 190th | CREFI | Office | 6/6/2021 | 7/6/2021 | NAP | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% |

| 30 | University Blvd MOB(6) | JPMCB | Office | 6/2/2021 | 7/1/2021 | NAP | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% |

| 31 | Bonanza Shopping Center(7) | GACC | Retail | 6/9/2021 | 7/11/2021 | NAP | NAP | NAP | No | No | Yes | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% |

| 32 | Mission Promenade | GACC | Mixed Use | 6/3/2021 | 7/6/2021 | NAP | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% |

| 33 | Residence Inn Florence(8) | GACC | Hospitality | 6/3/2021 | 4/6/2020 | Yes | Yes | Yes | No | No | No | NAP | NAP | NAP | NAP | NAP | NAP |

| 34 | 5550 Macadam(9) | GSMC | Office | 5/7/2021 | 7/6/2021 | NAP | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% | NAV | NAV |

| 35 | Pepsi Distribution Center | CREFI | Industrial | 6/6/2021 | 7/6/2021 | NAP | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% |

| 36 | Palmetto Self Storage | CREFI | Self Storage | 6/6/2021 | 6/6/2021 | NAP | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% |

| 37 | Bowie Commons | GSMC | Retail | 5/31/2021 | 7/6/2021 | NAP | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% |

| 38 | Greenpoint Portfolio | GACC | Multifamily | 6/3/2021 | 7/6/2021 | NAP | NAP | NAP | No | No | No | 100% | 100% | 100.0% | 99.0% | 100% | 100.0% |

| 39 | 654 Broadway | GSMC | Mixed Use | 6/2/2021 | 7/6/2021 | NAP | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% |

| 40 | 135 Brown Place | CREFI | Multifamily | 6/6/2021 | 7/6/2021 | NAP | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% |

| 41 | El Sueno Portfolio | GACC | Manufactured Housing | 6/3/2021 | 7/6/2021 | NAP | NAP | NAP | No | No | No | 99.6% | 100.0% | 99.6% | 100.0% | 100.0% | 100.0% |

| 42 | 20 Carter Drive | CREFI | Industrial | 6/6/2021 | 7/6/2021 | NAP | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% |

| 43 | NJ Flex Portfolio | CREFI | Industrial | 6/6/2021 | 7/6/2021 | NAP | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% |

| 44 | 2530 North Orchard Street | CREFI | Multifamily | 6/6/2021 | 7/6/2021 | NAP | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-228597) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Goldman Sachs & Co. LLC, J.P. Morgan Securities LLC, Deutsche Bank Securities Inc., Academy Securities, Inc., Siebert Williams Shank & Co., LLC or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

8

| MORTGAGE POOL CHARACTERISTICS |

| COVID-19 Updates | |||||||||||||||||

| Loan No. | Property Name | Mortgage Loan Seller | Property Type | Information as of Date | First Payment Date | March Debt Service Payment Received (Y/N) | April Debt Service Payment Received (Y/N) | May Debt Service Payment Received (Y/N) | Forbearance or Other Debt Service Relief Requested | Other Loan Modification Requested (Y/N) | Lease Modification or Rent Relief Requested (Y/N) | Occupied SF or Unit Count Making Full March Rent Payment (%) | UW March Base Rent Paid (%) | Occupied SF or Unit Count Making Full April Rent Payment (%) | UW April Base Rent Paid (%) | Occupied SF or Unit Count Making Full May Rent Payment (%) | UW May Base Rent Paid (%) |

| 45 | ABC Self Storage | CREFI | Self Storage | 6/6/2021 | 6/6/2021 | NAP | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% |

| 46 | Walgreens Snellville | CREFI | Retail | 6/6/2021 | 7/6/2021 | NAP | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% |

| 47 | Walgreens - Newberg OR | CREFI | Retail | 6/6/2021 | 7/6/2021 | NAP | NAP | NAP | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% |

| (1) | Amazon Seattle – One tenant (2,418 SF; 0.3% of NRA; 0.3% of UW Base Rent), requested and was granted rent relief for the months of April through July 2020, and the abated period was extended for a total of twelve months through March 31, 2021. |

| (2) | Union Square Mixed Use Portfolio – Three retail tenants at the Union Square Mixed Use Portfolio properties received rent abatements due to the COVID-19 pandemic. Two of the three tenants are currently paying full unabated rent, with the third tenant beginning to pay full unabated rent beginning in July 2021. The Union Square Mixed Use Portfolio loan is structured with an upfront rent reserve of $26,000, which will be released upon the tenant commencing full unabated rent payments. |

| (3) | 252 Atlantic Avenue – One tenants at the 252 Atlantic Avenue property received a temporary rent deferral due to the COVID-19 pandemic. The tenant is back to paying 100% of their base rent and will begin repaying deferred months in July 2021. Another tenant received a rent abatement through October 2021 and will resume paying full base rent thereafter. The 252 Atlantic Avenue loan was structured with an upfront rent reserve totaling $594,000, which is equal to six months of debt service. The reserve will be incrementally disbursed to the borrower beginning in December 2021 in the event that all conditions under the loan agreement have been met. |

| (4) | Truax Office – Five tenants (47.0% of NRA) requested rent relief and four tenants (16.5% of NRA) received relief due to the COVID-19 pandemic. As of May 2021, the four tenants are current on all contractual rents, additional rents and deferred rents (if applicable). |

| (5) | Alabama Hilton Portfolio – With respect to the Alabama Hilton Portfolio Mortgage Loan (1.5%), a forbearance and modification agreement was entered into as of September 1, 2020 in connection with certain payment delinquencies resulting in commencement of foreclosure of the related Mortgaged Properties, which proceeding was withdrawn due to the execution and delivery of the forbearance and modification agreement. The forbearance and modification agreement, among other things, provided for (i) a forbearance from the exercise of any remedies available under the related loan documents with respect to certain specified defaults for a forbearance period extending (unless earlier terminated pursuant to certain provisions of such forbearance and modification agreement) through and including June 1, 2021, (ii) the deferral of payment of the principal component of monthly debt service payments, and the deferral of payment of monthly FF&E reserve deposits, during the forbearance period, (iii) the deferral of any cash management requirements resulting from the specified defaults during the forbearance period, and the commencement of full cash management thereafter, with an excess cash flow sweep of funds to be applied to the deferred principal and deferred FF&E deposits until such deferred principal and FF&E deposits are fully funded, (iv) in the event any deferred principal and/or deferred FF&E deposits remain after the application of excess cash flow through the December, 2021 monthly payment date, such deficiencies must be funded by the borrower no later than December 31, 2021, (v) the deferral of the related borrower’s obligation to pay default interest and late fees resulting from the specified defaults provided that no default occurs under the forbearance and modification agreement or the loan documents, and the waiver of such default interest and late fees on December 31, 2021 so long as no default or event of default has occurred, and (vi) consent to the related borrower’s having obtained an unsecured loan pursuant to the Paycheck Protection Program administered by the United States Small Business Administration in accordance with the Coronavirus Aid, Relief, and Economic Security Act of 2020, in the amount of approximately $502,294, and agreement that such loan will not constitute a breach of certain applicable provisions of the loan documents so long as such loan is completely forgiven within two years of having been incurred or the related borrower otherwise pays such loan in full prior to its maturity date. |

| (6) | University Blvd MOB – One tenant (accounting for 4.2% of underwritten base rent) is delinquent with respect to certain rental payments with a total of $126,667 in rent outstanding due to being closed during the COVID-19 pandemic. According to the loan sponsor, the tenant is expected to re-pay $100,000, with the Loan Sponsor writing off the balance. The tenant is now open and expected to make full rental payments. |

| (7) | Bonanza Shopping Center – Eight tenants (44.0% of NRA) requested rent relief and six tenants (37.8% of NRA) received relief due to the COVID-19 pandemic. As of May 2021, the six tenants are current on all contractual rents, additional rents, and deferred rents (if applicable). |

| (8) | Residence Inn Florence – As of April 2021, the occupancy and average daily rate per room were 67.6% and $110.81, respectively. The Mortgage Loan has been in a cash management period and cash sweep period since November 2020 as a result of the debt service coverage ratio falling below 1.40x. The Mortgage Loan documents provide for a cash management and cash trap period to occur if as of the last day of any calendar quarter occurring prior to the May 2021 monthly payment date, the debt service coverage ratio is less than 1.40x (which is cured if the debt service coverage ratio is subsequently at least 1.42x as of the last day of any calendar quarter), and if as of the last day of any calendar quarter thereafter, the debt service coverage ratio is less than 1.35x (which is cured if the debt service coverage ratio is subsequently at least 1.37x as of the last day of any calendar quarter). Prior to the May 2021 monthly payment date, the Mortgage Loan documents require the debt service coverage ratio to be calculated based on annualized revenues and expenses for the three months preceding the calculation. The debt service coverage ratios for the Residence Inn Florence Mortgage Loan as of the Q2 2020, Q3 2020, Q4 2020 and Q1 2021 periods, based on the calculations as required under the mortgage loan documents, were 0.49x, 1.27x, 1.08x and 0.92x, respectively. The debt service coverage ratio for the Residence Inn Florence Mortgage Loan as of the trailing twelve months, trailing six months and trailing three months ending April 30, 2021 was 1.25x, 1.23x and 1.33x, respectively. |

| (9) | 5550 Macadam - More recent historical financials are unavailable as the Mortgaged Property was acquired at origination and the seller did not provide the borrower with such information. |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-228597) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Goldman Sachs & Co. LLC, J.P. Morgan Securities LLC, Deutsche Bank Securities Inc., Academy Securities, Inc., Siebert Williams Shank & Co., LLC or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

9

| KEY FEATURES OF THE CERTIFICATES |

| Co-Lead Managers and Joint Bookrunners: | Citigroup Global Markets Inc. Goldman Sachs & Co. LLC J.P. Morgan Securities LLC Deutsche Bank Securities Inc. |

| Co-Managers: | Academy Securities, Inc. Siebert Williams Shank & Co., LLC |

| Depositor: | Citigroup Commercial Mortgage Securities Inc. |

| Initial Pool Balance: | $1,093,912,985 |

| Master Servicer: | Midland Loan Services, a Division of PNC Bank, National Association |

| Special Servicer: | Midland Loan Services, a Division of PNC Bank, National Association |

| Certificate Administrator: | Citibank, N.A. |

| Trustee: | Wilmington Trust, National Association |

| Operating Advisor: | Park Bridge Lender Services LLC |

| Asset Representations Reviewer: | Park Bridge Lender Services LLC |

| Risk Retention Consultation Parties: | Citi Real Estate Funding Inc., Goldman Sachs Mortgage Company and JPMorgan Chase Bank, National Association |

| Credit Risk Retention: | For a discussion on the manner in which the U.S. credit risk retention requirements are being satisfied by Citi Real Estate Funding Inc., as retaining sponsor for this securitization transaction, see “Credit Risk Retention” in the Preliminary Prospectus. Note that this securitization transaction is not structured to satisfy European or United Kingdom risk retention and due diligence requirements. |

| Closing Date: | On or about June 29, 2021 |

| Cut-off Date: | With respect to each mortgage loan, the due date in June 2021 for that mortgage loan (or, in the case of any mortgage loan that has its first due date subsequent to June 2021, the date that would have been its due date in June 2021 under the terms of that mortgage loan if a monthly payment were scheduled to be due in that month) |

| Determination Date: | The 11th day of each month or next business day, commencing in July 2021 |

| Distribution Date: | The 4th business day after the Determination Date, commencing in July 2021 |

| Interest Accrual: | Preceding calendar month |

| ERISA Eligible: | The offered certificates are expected to be ERISA eligible, subject to the exemption conditions described in the Preliminary Prospectus |

| SMMEA Eligible: | No |

| Payment Structure: | Sequential Pay |

| Day Count: | 30/360 |

| Tax Structure: | REMIC |

| Rated Final Distribution Date: | July 2054 |

| Cleanup Call: | 1.0% |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-228597) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Goldman Sachs & Co. LLC, J.P. Morgan Securities LLC, Deutsche Bank Securities Inc., Academy Securities, Inc., Siebert Williams Shank & Co., LLC or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

10

| KEY FEATURES OF THE CERTIFICATES |

| Minimum Denominations: | $10,000 minimum for the offered certificates (other than the Class X-A certificates); $1,000,000 minimum for the Class X-A certificates; and integral multiples of $1 thereafter for all the offered certificates |

| Delivery: | Book-entry through DTC |

| Bond Information: | Cash flows are expected to be modeled by TREPP, INTEX, BLOOMBERG and Moody’s Analytics

|

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-228597) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Goldman Sachs & Co. LLC, J.P. Morgan Securities LLC, Deutsche Bank Securities Inc., Academy Securities, Inc., Siebert Williams Shank & Co., LLC or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

11

| TRANSACTION HIGHLIGHTS |

| ■ | $899,351,000 (Approximate) New-Issue Multi-Borrower CMBS: |

| — | Overview: The mortgage pool consists of 47 fixed-rate commercial mortgage loans that have an aggregate Cut-off Date Balance of $1,093,912,985 (the “Initial Pool Balance”), have an average mortgage loan Cut-off Date Balance of $23,274,744 and are secured by 170 mortgaged properties located throughout 25 states. |

| — | LTV: 56.1% weighted average Cut-off Date LTV Ratio |

| — | DSCR: 2.82x weighted average Underwritten NCF Debt Service Coverage Ratio |

| — | Debt Yield: 10.9% weighted average Debt Yield on Underwritten NOI |

| — | Credit Support: 30.000% credit support to Class A-1 / A-2 / A-3/ A-4/ A-5 / A-AB |

| ■ | Loan Structural Features: |

| — | Amortization: 25.0% of the mortgage loans by Initial Pool Balance have scheduled amortization: |

| – | 12.5% of the mortgage loans by Initial Pool Balance have amortization for the entire term with a balloon payment due at maturity |

| – | 12.5% of the mortgage loans by Initial Pool Balance have scheduled amortization following a partial interest only period with a balloon payment due at maturity |

| — | Hard Lockboxes: 73.1% of the mortgage loans by Initial Pool Balance have a Hard Lockbox in place |

| — | Cash Traps: 86.0% of the mortgage loans by Initial Pool Balance have cash traps triggered by certain declines in cash flow, all at levels equal to or greater than (i) a 1.10x coverage or (ii) a 5.25% debt yield, that fund an excess cash flow reserve |

| — | Reserves: The mortgage loans require amounts to be escrowed for reserves as follows: |

| – | Real Estate Taxes: 35 mortgage loans representing 58.0% of the Initial Pool Balance |

| – | Insurance: 19 mortgage loans representing 30.8% of the Initial Pool Balance |

| – | Replacement Reserves (Including FF&E Reserves): 37 mortgage loans representing 62.0% of the Initial Pool Balance |

| – | Tenant Improvements / Leasing Commissions: 20 mortgage loans representing 36.8% secured by office, industrial, retail, self storage (with commercial tenants), mixed use and multifamily (with commercial tenants) properties |

| — | Predominantly Defeasance Mortgage Loans: 71.0% of the mortgage loans by Initial Pool Balance permit defeasance only after an initial lockout period |

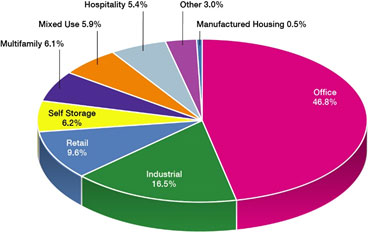

| ■ | Multiple-Asset Types > 5.0% of the Initial Pool Balance: |

| — | Office: 46.8% of the mortgaged properties by allocated Initial Pool Balance are office properties |

| — | Industrial: 16.5% of the mortgaged properties by allocated Initial Pool Balance are industrial properties |

| — | Retail: 9.6% of the mortgaged properties by allocated Initial Pool Balance are retail properties (5.3% are anchored retail properties) |

| — | Self Storage: 6.2% of the mortgaged properties by allocated Initial Pool Balance are self storage properties |

| — | Multifamily: 6.1% of the mortgaged properties by allocated Initial Pool Balance are multifamily properties (5.1% are mid rise multifamily properties |

| — | Mixed Use: 5.9% of the mortgaged properties by allocated Initial Pool Balance are mixed use properties |

| — | Hospitality: 5.4% of the mortgaged properties by allocated Initial Pool Balance are hospitality properties |

| ■ | Geographic Diversity: The 170 mortgaged properties are located throughout 25 states, with only two states having greater than 10.0% of the allocated Initial Pool Balance: New York (30.6%) and California (23.1%). |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-228597) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Goldman Sachs & Co. LLC, J.P. Morgan Securities LLC, Deutsche Bank Securities Inc., Academy Securities, Inc., Siebert Williams Shank & Co., LLC or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

12

| COLLATERAL OVERVIEW |

Mortgage Loans by Loan Seller

Mortgage Loan Seller | Mortgage Loans | Mortgaged Properties | Aggregate Cut-off Date Balance | % of Initial Pool Balance |

| Citi Real Estate Funding Inc. | 22 | 45 | $405,825,154 | 37.1% |

| JPMorgan Chase Bank, National Association | 7 | 14 | 232,310,000 | 21.2 |

| Goldman Sachs Mortgage Company | 9 | 41 | 218,572,228 | 20.0 |

| German American Capital Corporation | 8 | 69 | 153,205,603 | 14.0 |

Goldman Sachs Mortgage Company, German American Capital Corporation, JPMorgan Chase Bank, National Association(1) | 1 | 1 | 84,000,000 | 7.7 |

| Total | 47 | 170 | $1,093,912,985 | 100.0% |

| (1) | Goldman Sachs Mortgage Company, German American Capital Corporation and JPMorgan Chase Bank, National Association and are co-sponsors with respect to the Burlingame Point mortgage loan (7.7%), which mortgage loan is evidenced by five (5) promissory notes: (i) notes A-1-C-4 and A-1-C-5, with an aggregate outstanding principal balance of $40,000,000 as of the cut-off date, as to which Goldman Sachs Mortgage Company is acting as mortgage loan seller; (ii) notes A-2-C-3 and A-2-C-4, with an aggregate outstanding principal balance of $26,000,000 as of the cut-off date, as to which German American Capital Corporation is acting as mortgage loan seller; and (iii) note A-3-C-3, with an outstanding principal balance of $18,000,000 as of the cut-off date, as to which JPMorgan Chase Bank, National Association is acting as mortgage loan seller. |

Ten Largest Mortgage Loans(1)(2)

# | Mortgage Loan Name | Cut-off Date Balance | % of Initial Pool Balance | Property Type | Property Size | Cut-off Date Balance Per SF/Unit/Room | UW NCF | UW | Cut-off Date LTV Ratio(3) | |||||||||

| 1 | Burlingame Point | $84,000,000 | 7.7% | Office | 805,118 | $472 | 4.72x | 14.6% | 38.0% | |||||||||

| 2 | Equus Industrial Portfolio | 68,109,030 | 6.2 | Industrial | 5,959,157 | $39 | 5.10x | 14.0% | 37.8% | |||||||||

| 3 | 375 Pearl Street | 66,000,000 | 6.0 | Office | 573,083 | $384 | 2.67x | 9.2% | 60.3% | |||||||||

| 4 | Colonnade Corporate Center | 60,000,000 | 5.5 | Office | 419,650 | $198 | 1.28x | 8.2% | 72.5% | |||||||||

| 5 | Amazon Seattle | 51,900,000 | 4.7 | Office | 774,412 | $303 | 4.27x | 13.1% | 35.1% | |||||||||

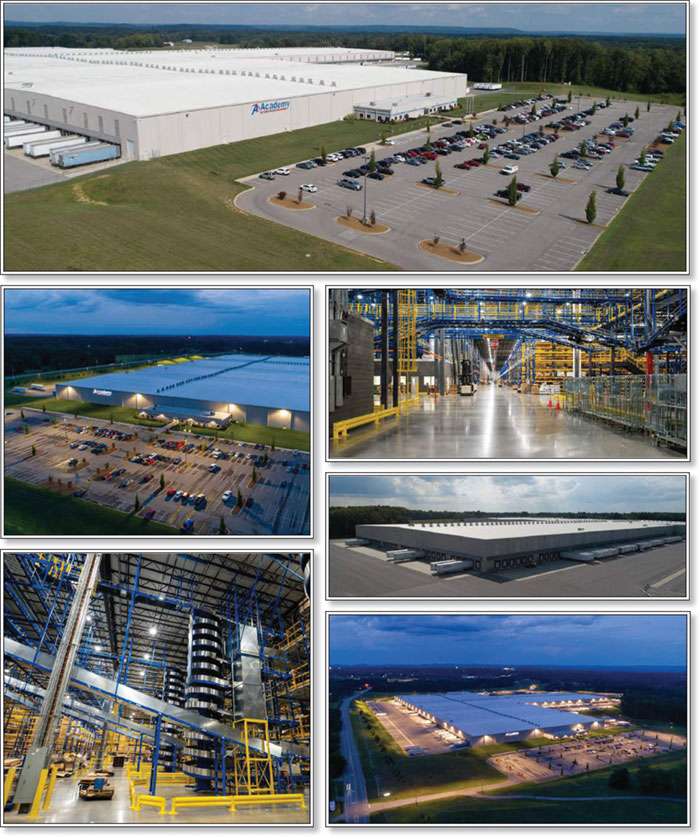

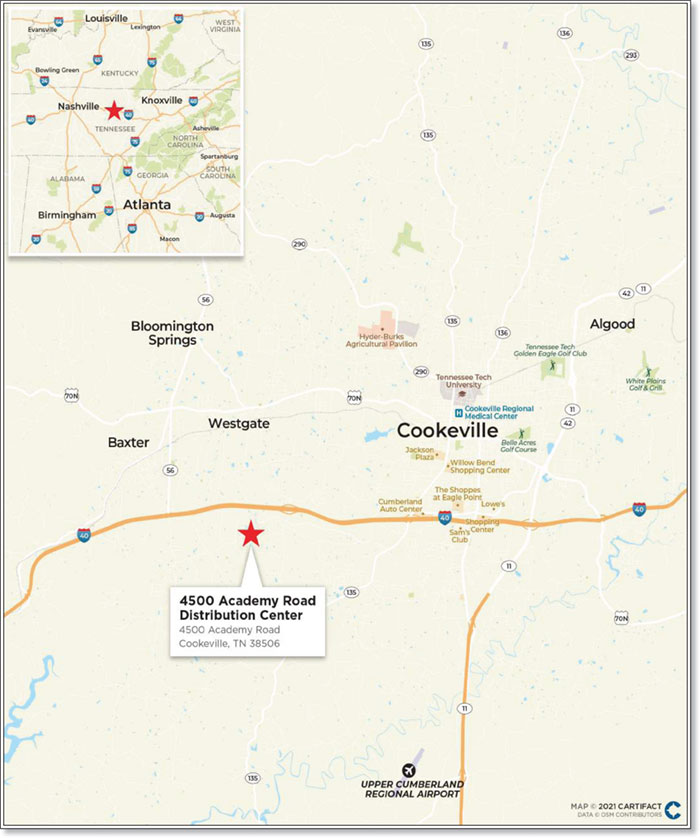

| 6 | 4500 Academy Road Distribution Center | 50,000,000 | 4.6 | Industrial | 1,600,000 | $45 | 2.63x | 10.0% | 59.0% | |||||||||

| 7 | Upper West Side and Brooklyn Heights Portfolio | 50,000,000 | 4.6 | Multifamily | 190 | $263,158 | 2.13x | 8.0% | 52.2% | |||||||||

| 8 | 105 West 125th Street | 45,000,000 | 4.1 | Office | 151,316 | $297 | 3.14x | 11.1% | 62.2% | |||||||||

| 9 | O'Reilly Auto Parts Portfolio | 41,000,000 | 3.7 | Retail | 406,186 | $101 | 2.24x | 9.9% | 56.5% | |||||||||

| 10 | U-Haul SAC 20 | 40,500,000 | 3.7 | Self Storage | 359,998 | $113 | 1.94x | 10.8% | 59.1% | |||||||||

| Top 10 Total / Wtd. Avg. | $556,509,030 | 50.9% | 3.18x | 11.1% | 52.1% | |||||||||||||

| Remaining Total / Wtd. Avg. | 537,403,955 | 49.1 | 2.45x | 10.6%(4) | 60.2%(4) | |||||||||||||

| Total / Wtd. Avg. | $1,093,912,985 | 100.0% | 2.82x | 10.9% | 56.1% |

| (1) | See footnotes to table entitled “Mortgage Pool Characteristics” above. |

| (2) | With respect to each mortgage loan that is part of a loan combination (as identified under “Collateral Overview—Loan Combination Summary” below), the Cut-off Date Balance Per SF/Unit/Room, UW NCF DSCR, UW NOI Debt Yield and Cut-off Date LTV Ratio are calculated based on both that mortgage loan and any related pari passu companion loan(s), but without regard to any related subordinate companion loan(s) or other indebtedness. |

| (3) | With respect to certain of the mortgage loans identified above, the Cut-off Date LTV Ratios have been calculated using “as-stabilized”, “portfolio premium” or similar hypothetical values. Such mortgage loans are identified under the definition of “Appraised Value” set forth under “Description of the Mortgage Pool—Certain Calculations and Definitions” in the Preliminary Prospectus. |

| (4) | The UW NOI Debt Yield and Cut-off Date LTV Ratio with respect to the Mission Promenade mortgage loan are each calculated net of a $750,000 holdback reserve. |

.

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-228597) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Goldman Sachs & Co. LLC, J.P. Morgan Securities LLC, Deutsche Bank Securities Inc., Academy Securities, Inc., Siebert Williams Shank & Co., LLC or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

13

| COLLATERAL OVERVIEW (continued) |

Loan Combination Summary

Mortgage Loan Name(1) | Mortgage Loan Cut-off Date Balance | Mortgage Loan as Approx. % of Initial Pool Balance | Aggregate Pari Passu Companion Loan Cut-off Date Balance | Aggregate Subordinate Companion Loan Cut-off Date Balance | Loan Combination Cut-off Date Balance | Controlling Pooling/Trust and Servicing Agreement (“Controlling PSA”)(2) | Master Servicer / Outside Servicer | Special Servicer / Outside Special Servicer |

| Burlingame Point | $84,000,000 | 7.7% | $296,000,000 | $240,000,000 | $620,000,000 | BGME 2021-VR | KeyBank | Situs |

| Equus Industrial Portfolio | $68,109,030 | 6.2% | $164,903,870 | $154,000,000 | $387,012,900 | Benchmark 2021-B26 | KeyBank | Situs |

| 375 Pearl Street | $66,000,000 | 6.0% | $154,000,000 | - | $220,000,000 | BANK 2021-BNK34 | Wells | Greystone |

| Colonnade Corporate Center | $60,000,000 | 5.5% | $23,000,000 | - | $83,000,000 | Benchmark 2021-B27 | Midland | Midland |

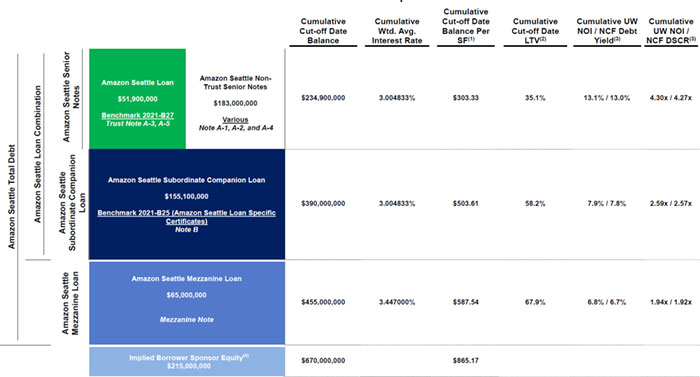

| Amazon Seattle | $51,900,000 | 4.7% | $183,000,000 | $155,100,000 | $390,000,000 | Benchmark 2021-B25 | Midland | Situs |

| 4500 Academy Road Distribution Center | $50,000,000 | 4.6% | $22,000,000 | - | $72,000,000 | Benchmark 2021-B27 | Midland | Midland |

| iPark 84 Innovation Center | $28,000,000 | 2.6% | $60,000,000 | - | $88,000,000 | Benchmark 2021-B26 | KeyBank | KeyBank |

| 1985 Marcus | $18,447,198 | 1.7% | $36,894,396 | - | $55,341,595 | Benchmark 2021-B25 | Midland | Rialto |

| Alabama Hilton Portfolio | $16,491,979 | 1.5% | $11,641,397 | - | $28,133,377 | Benchmark 2021-B27 | Midland | Midland |

| (1) | Each of the mortgage loans included in the issuing entity that is secured by a mortgaged property or portfolio of mortgaged properties identified in the table above, together with the related companion loan(s) (none of which is included in the issuing entity), is referred to in this Term Sheet as a “loan combination”. See “Description of the Mortgage Pool—The Loan Combinations” in the Preliminary Prospectus. |

| (2) | Each loan combination will be serviced under the related Controlling PSA and, in the event the Controlling Note is included in the related securitization transaction, the controlling class representative (or an equivalent entity) under such Controlling PSA will generally be entitled to exercise the rights of the controlling note holder for the subject loan combination. See, however, the chart entitled “Loan Combination Controlling Notes and Non-Controlling Notes” below and “Description of the Mortgage Pool—The Loan Combinations” in the Preliminary Prospectus for information regarding the party that will be entitled to exercise such rights in the event the Controlling Note is held or deemed to be held by a third party or included in a separate securitization transaction. |

Mortgage Loans with Existing Mezzanine Debt or Subordinate Debt(1)

Mortgage Loan Name | Mortgage Loan Cut-off Date Balance | Aggregate Pari Passu Companion Loan Cut-off Date Balance | Aggregate Mezzanine Debt Cut-off Date Balance | Aggregate Subordinate Companion Loan Cut-off Date Balance | Cut-off Date Total Debt Balance(2) | Wtd. Avg Cut-off Date Total Debt Interest Rate(2) | Cut-off Date Mortgage Loan LTV(3) | Cut-off Date Total Debt LTV(2) | Cut-off Date Mortgage Loan UW NCF DSCR(3) | Cut-off Date Total Debt UW NCF DSCR(2) | Cut-off Date Mortgage Loan UW NOI Debt Yield(3) | Cut-off Date Total Debt UW NOI Debt Yield(2) |

| Burlingame Point | $84,000,000 | $296,000,000 | $130,000,000 | $240,000,000 | $750,000,000 | 3.27389% | 38.0% | 75.0% | 4.72x | 1.33x | 14.6% | 7.4% |

| Equus Industrial Portfolio | $68,109,030 | $164,903,870 | — | $154,000,000 | $387,012,900 | 3.11498% | 37.8% | 62.9% | 5.10x | 2.45x | 14.0% | 8.4% |

| 375 Pearl Street | $66,000,000 | $154,000,000 | $30,000,000 | — | $250,000,000 | 3.80400% | 60.3% | 68.5% | 2.67x | 2.08x | 9.2% | 8.1% |

| Amazon Seattle | $51,900,000 | $183,000,000 | $65,000,000 | $155,100,000 | $455,000,000 | 3.44700% | 35.1% | 67.9% | 4.27x | 1.92x | 13.1% | 6.8% |

| 4500 Academy Road Distribution Center | $50,000,000 | $22,000,000 | $12,000,000 | — | $84,000,000 | 4.35000% | 59.0% | 68.9% | 2.63x | 1.83x | 10.0% | 8.6% |

| (1) | See footnotes to table entitled “Mortgage Pool Characteristics” above. |

| (2) | All “Total Debt” calculations set forth in the table above include any related pari passu companion loan(s), any related subordinate companion loan(s) and any related mezzanine debt. |

| (3) | “Cut-off Date Mortgage Loan LTV”, “Cut-off Date Mortgage Loan UW NCF DSCR” and “Cut-off Date Mortgage Loan UW NOI Debt Yield” calculations include any related pari passu companion loan(s) and exclude any related subordinate companion loan(s). |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-228597) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Goldman Sachs & Co. LLC, J.P. Morgan Securities LLC, Deutsche Bank Securities Inc., Academy Securities, Inc., Siebert Williams Shank & Co., LLC or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

14

| COLLATERAL OVERVIEW (continued) |

Loan Combination Controlling Notes and Non-Controlling Notes(1)(2)

Mortgaged Property Name | Servicing of Loan Combination | Note Detail | Controlling Note | Current Holder of | Current or | Aggregate Cut-off |

| Burlingame Point | Outside Serviced | Notes A-1-C-4, A-1-C-5, A-2-C-3, A-2-C-4, A-3-C-3 | No | — | Benchmark 2021-B27 | $84,000,000 |

| Notes A-1, A-2, A-3 | Yes (Note A-1) | — | BGME 2021-VR | $20,000,000 | ||

| Note A-1-C-1 | No | WFB | Not Identified | $60,000,000 | ||

| Notes A-1-C-2, A-2-C-1, A-2-C-5, A-3-C-1, A-3-C-5 | No | — | Benchmark 2021-B25 | $120,000,000 | ||

| Notes A-1-C-3, A-2-C-2, A-3-C-2, A-3-C-4 | No | — | Benchmark 2021-B26 | $96,000,000 | ||

| Notes B-1, B-2, B-3 | No | — | BGME 2021-VR | $240,000,000 | ||

| Equus Industrial Portfolio(6) | Outside Serviced | Note A-1-A | No (Control Shift Note)(6) | — | Benchmark 2021-B26 | $95,000,000 |

| Note A-1-B | No | — | Benchmark 2021-B27 | $68,109,030 | ||

| Note A-2 | No | — | BANK 2021-BNK33 | $69,903,870 | ||

| Note B-1-A | Yes(6) | Prima Mortgage Investment Trust, LLC | Not Identified | $43,400,000 | ||

| Note B-1-B | No | New York State Teachers’ Retirement System | Not Identified | $43,400,000 | ||

| Note B-1-C | No | Wilton Reassurance Company | Not Identified | $8,750,000 | ||

| Note B-1-D | No | Highmark, Inc. | Not Identified | $8,750,000 | ||

| Note B-1-E | No | Wilcac Life Insurance Company | Not Identified | $3,500,000 | ||

| Note B-2-A | No | Prima Mortgage Investment Trust, LLC | Not Identified | $18,600,000 | ||

| Note B-2-B | No | New York State Teachers’ Retirement System | Not Identified | $18,600,000 | ||

| Note B-2-C | No | Wilton Reassurance Company | Not Identified | $3,750,000 | ||

| Note B-2-D | No | Highmark, Inc. | Not Identified | $3,750,000 | ||

| Note B-2-E | No | Wilcac Life Insurance Company | Not Identified | $1,500,000 | ||

| 375 Pearl St. | Outside Serviced | Notes A-1, A-4 | Yes | — | BANK 2021-BNK34 | $100,000,000 |

| Note A-2 | No | — | Benchmark 2021-B27 | $66,000,000 | ||

| Note A-3 | No | WFB | Not Identified | $54,000,000 | ||

| Colonnade Corporate Center | Serviced | Note A-1 | Yes | — | Benchmark 2021-B27 | $60,000,000 |

| Note A-2 | No | JPMCB | Not Identified | $23,000,000 | ||

| Amazon Seattle | Outside Serviced | Note A-1 | No (Control Shift Note)(6) | — | Benchmark 2021-B25 | $90,000,000 |

| Notes A-2, A-4 | No | — | Benchmark 2021-B26 | $93,000,000 | ||

| Notes A-3, A-5 | No | — | Benchmark 2021-B27 | $51,900,000 | ||

| Note B | Yes(6) | — | Benchmark 2021-B25 | $155,100,000 | ||

| 4500 Academy Road Distribution Center | Serviced | Note A-1 | Yes | — | Benchmark 2021-B27 | $50,000,000 |

| Note A-2 | No | CREFI | Not Identified | $22,000,000 | ||

| iPark 84 Innovation Center | Outside Serviced | Note A-1 | Yes | — | Benchmark 2021-B26 | $60,000,000 |

| Note A-2 | No | — | Benchmark 2021-B27 | $28,000,000 | ||

| 1985 Marcus | Outside Serviced | Note A-1 | Yes | — | Benchmark 2021-B25 | $36,894,396 |

| Note A-2 | No | — | Benchmark 2021-B27 | $18,447,198 | ||

| Alabama Hilton Portfolio | Serviced | Note A-1 | No | — | Benchmark 2020-B17 | $11,641,397 |

| Note A-2 | Yes | — | Benchmark 2021-B27 | $16,491,979 |

| (1) | The holder(s) of one or more specified controlling notes (collectively, the “Controlling Note”) will be the “controlling note holder(s)” (collectively, the “Controlling Note Holder”) entitled (directly or through a representative) to (a) approve or, in some cases, direct material servicing decisions involving the related loan combination (while the remaining such holder(s) generally are only entitled to non-binding consultation rights in such regard), and (b) in some cases, replace the applicable special servicer with respect to such loan combination with or without cause. See “Description of the Mortgage Pool—The Loan Combinations” and “The Pooling and Servicing Agreement—Directing Holder” in the Preliminary Prospectus. |

| (2) | The holder(s) of the note(s) other than the Controlling Note (each, a “Non-Controlling Note”) will be the “non-controlling note holder(s)” generally entitled (directly or through a representative) to certain non-binding consultation rights with respect to any decisions as to which the holder of the Controlling Note has consent rights involving the related loan combination, subject to certain exceptions, including that in certain cases where the related Controlling Note is a B-note, C-note or other subordinate note, such consultation rights will not be afforded to the holder(s) of the Non-Controlling Notes until after a control trigger event has occurred with respect to either such Controlling Note(s) or certain certificates backed thereby, in each case as set forth in the related co-lender agreement. See “Description of the Mortgage Pool—The Loan Combinations” in the Preliminary Prospectus. |