| FREE WRITING PROSPECTUS | ||

| FILED PURSUANT TO RULE 433 | ||

| REGISTRATION FILE NO.: 333-262701-04 | ||

June 15, 2023

BENCHMARK 2023-B39

Commercial Mortgage Trust

Free Writing Prospectus

Structural and Collateral Term Sheet

$906,483,263

(Approximate Initial Mortgage Pool Balance)

$[ ]

(Approximate Offered Certificates)

| Citigroup Commercial Mortgage Securities Inc. Depositor |

Commercial Mortgage Pass-Through Certificates,

Series 2023-B39

| Citi Real Estate Funding Inc. |

| Goldman Sachs Mortgage Company |

| German American Capital Corporation |

| JPMorgan Chase Bank, National Association |

As Sponsors and Mortgage Loan Sellers

| Citigroup | Deutsche Bank Securities | J.P. Morgan | Goldman Sachs & Co. LLC |

Co-Lead Managers and Joint Bookrunners

| Academy Securities | Drexel Hamilton |

Co-Managers

STATEMENT REGARDING THIS FREE WRITING PROSPECTUS

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-262701) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Deutsche Bank Securities Inc., Goldman Sachs & Co. LLC, J.P. Morgan Securities LLC, Academy Securities, Inc., Drexel Hamilton, LLC or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

IMPORTANT NOTICE RELATING TO AUTOMATICALLY GENERATED EMAIL DISCLAIMERS

Any legends, disclaimers or other notices that may appear at the bottom of the email communication to which this free writing prospectus is attached relating to (1) these materials not constituting an offer (or a solicitation of an offer), (2) no representation being made that these materials are accurate or complete and that these materials may not be updated or (3) these materials possibly being confidential, are, in each case, not applicable to these materials and should be disregarded. Such legends, disclaimers or other notices have been automatically generated as a result of these materials having been sent via Bloomberg or another system.

The information in this free writing prospectus is preliminary and may be supplemented or changed. This free writing prospectus is not an offering to sell these securities and is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

THIS FREE WRITING PROSPECTUS, DATED June 15, 2023

MAY BE AMENDED OR SUPPLEMENTED PRIOR TO TIME OF SALE

BMARK 2023-B39

The depositor has filed a registration statement (including a prospectus) with the SEC (SEC File No. 333- 262701) for the offering to which this free writing prospectus relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Goldman Sachs & Co. LLC, Deutsche Bank Securities Inc., J.P. Morgan Securities LLC, Academy Securities, Inc., Drexel Hamilton, LLC, or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

The securities to which these collateral materials (“Materials”) relate will be described in greater detail in the preliminary prospectus expected to be dated in June 2023 (the “Preliminary Prospectus”) that will be included as part of our registration statement. The Preliminary Prospectus will contain material information that is not contained in these Materials (including, without limitation, a summary of risks associated with an investment in the offered securities under the heading “Summary of Risk Factors” and a detailed discussion of such risks under the heading “Risk Factors”).

These Materials are preliminary and subject to change. The information in these Materials supersedes all prior such information delivered to you and will be superseded by any subsequent information delivered prior to the time of sale.

Neither these Materials nor anything contained in these Materials shall form the basis for any contract or commitment whatsoever. These Materials are not to be construed as an offer to sell or the solicitation of any offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal.

The information contained in these Materials may not pertain to any securities that will actually be sold. The information contained in these Materials may be based on assumptions regarding market conditions and other matters as reflected in these Materials. We make no representations regarding the reasonableness of such assumptions or the likelihood that any of such assumptions will coincide with actual market conditions or events, and these Materials should not be relied upon for such purposes. We and our affiliates, officers, directors, partners and employees, including persons involved in the preparation or issuance of these Materials may, from time to time, have long or short positions in, and buy or sell, the securities mentioned in these Materials or derivatives thereof (including options). Information contained in these Materials is current as of the date appearing on these Materials only.

IMPORTANT NOTICE RELATING TO AUTOMATICALLY GENERATED EMAIL DISCLAIMERS

Any legends, disclaimers or other notices that may appear at the bottom of the email communication to which this free writing prospectus is attached relating to (1) these Materials not constituting an offer (or a solicitation of an offer), (2) no representation being made that these Materials are accurate or complete and that these Materials may not be updated or (3) these Materials possibly being confidential, are, in each case, not applicable to these Materials and should be disregarded. Such legends, disclaimers or other notices have been automatically generated as a result of these Materials having been sent via Bloomberg or another system.

| 3 |

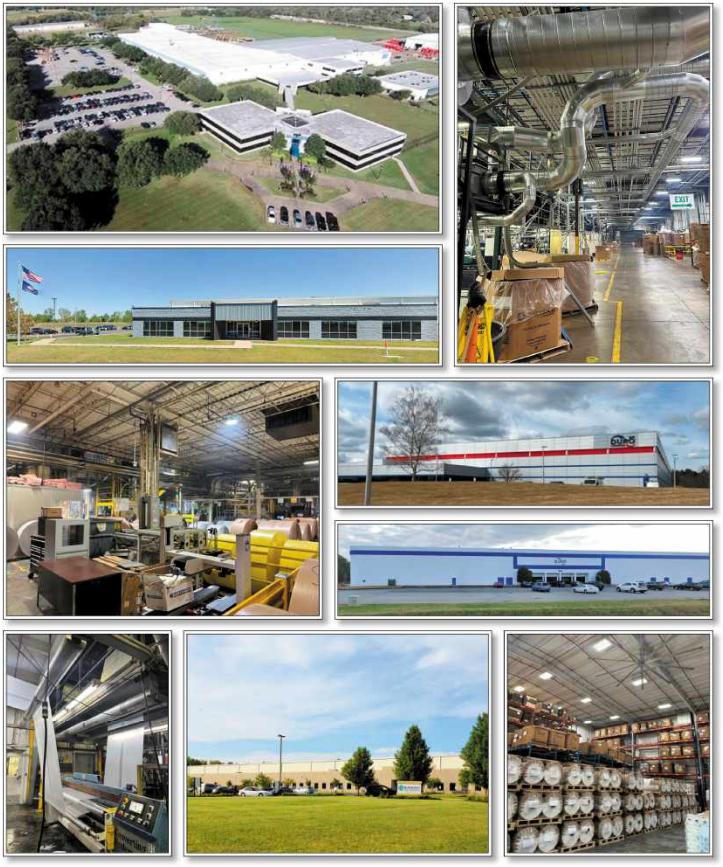

| LOAN #1: NOVOLEX PORTFOLIO |

| The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-262701) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Deutsche Bank Securities Inc., Goldman Sachs & Co. LLC, J.P. Morgan Securities LLC, Drexel Hamilton, LLC, Academy Securities, Inc. or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146. | ||

| 4 | ||

| LOAN #1: NOVOLEX PORTFOLIO |

| The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-262701) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Deutsche Bank Securities Inc., Goldman Sachs & Co. LLC, J.P. Morgan Securities LLC, Drexel Hamilton, LLC, Academy Securities, Inc. or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146. | ||

| 5 | ||

| LOAN #1: NOVOLEX PORTFOLIO |

| Mortgaged Property Information | Mortgage Loan Information | ||||

| Number of Mortgaged Properties | 17 | Loan Seller | GACC, GSMC | ||

| Location (City / State)(1) | Various / Various | Cut-off Date Balance | $89,500,000 | ||

| Property Type(1) | Industrial | Cut-off Date Balance per SF(2) | $49.68 | ||

| Size (SF) | 2,516,274 | Percentage of Initial Pool Balance | 9.9% | ||

| Total Occupancy as of 7/6/2023 | 100.0% | Number of Related Mortgage Loans | None | ||

| Owned Occupancy as of 7/6/2023 | 100.0% | Type of Security | Fee | ||

| Year Built / Latest Renovation(1) | Various / Various | Mortgage Rate | 6.22650% | ||

| Appraised Value(1) | $207,300,000 | Original Term to Maturity (Months) | 120 | ||

| Appraisal Date | 4/1/2023 | Original Amortization Term (Months) | NAP | ||

| Borrower Sponsor | New Mountain Net Lease Partners II Corporation | Original Interest Only Period (Months) | 120 | ||

| Property Management | Self-Managed | First Payment Date | 7/6/2023 | ||

| Maturity Date | 6/6/2033 | ||||

| Underwritten Revenues | $15,224,795 | ||||

| Underwritten Expenses | $456,744 | Escrows(3) | |||

| Underwritten Net Operating Income (NOI) | $14,768,052 | Upfront | Monthly | ||

| Underwritten Net Cash Flow (NCF) | $14,315,122 | Taxes | $0 | Springing | |

| Cut-off Date LTV Ratio(2) | 60.3% | Insurance | $0 | Springing | |

| Maturity Date LTV Ratio(2) | 60.3% | Replacement Reserve | $0 | Springing | |

| DSCR Based on Underwritten NOI / NCF(2) | 1.87x / 1.81x | TI / LC | $0 | Springing | |

| Debt Yield Based on Underwritten NOI / NCF(2) | 11.8% / 11.5% | EIL Policy Reserve | $0 | Springing | |

| Sources and Uses | ||||||

| Sources | $ | % | Uses | $ | % | |

| Whole Loan Amount(2) | $125,000,000 | 100.0% | Return of Equity | $120,571,062 | 96.5 | % |

| Closing Costs | 4,428,938 | 3.5 | ||||

| Total Sources | $125,000,000 | 100.0% | Total Uses | $125,000,000 | 100.0 | % |

| (1) | See the "Portfolio Summary" chart below for Location (City / State), Property Type, Year Built / Latest Renovation and Appraised Values of the individual Novolex Portfolio Properties (as defined below). |

| (2) | The Novolex Portfolio Mortgage Loan (as defined below) is part of the Novolex Portfolio Whole Loan (as defined below), which is evidenced by eight pari passu notes with an aggregate outstanding principal balance of $125.0 million. LTV Ratios, DSCR, Debt Yield and Cut-off Date Balance per SF set forth above are calculated based on the outstanding principal balance of the Novolex Portfolio Whole Loan. |

| (3) | See “—Escrows” below. |

| ■ | The Mortgage Loan. The mortgage loan (the “Novolex Portfolio Mortgage Loan”) is part of a whole loan (the “Novolex Portfolio Whole Loan”) with an aggregate principal balance as of the Cut-off Date of $125,000,000, which is secured by a first mortgage lien encumbering the borrower’s fee interests in a portfolio of 17 industrial properties totaling 2,516,274 SF located in 11 states (each, individually, a “Novolex Portfolio Property”, and collectively, the “Novolex Portfolio” or the “Novolex Portfolio Properties”). The Novolex Portfolio Mortgage Loan is evidenced by the controlling note A-1 and the non-controlling note A-3, A-4, A-5, A-6 and A-7-1 with an aggregate outstanding principal balance as of the Cut-off Date of $89,500,000, representing approximately 9.9% of the Initial Pool Balance. The Novolex Portfolio Whole Loan is comprised of eight pari passu notes with an aggregate principal balance as of the Cut-off Date of $125,000,000, as detailed in the “Whole Loan Summary” table below. |

The Novolex Portfolio Whole Loan was co-originated by DBR Investments Co. Limited (“DBRI”) and Goldman Sachs Bank USA (“GSBI”) on May 19, 2023. DBRI will be contributing the controlling note A-1 and non-controlling notes A-3, A-4 and A-5 with an aggregate outstanding principal balance as of the Cut-off Date of $62,500,000 and GSBI will be contributing notes A-6 and A-7-1 with an outstanding principal balance as of the Cut-off Date of $27,000,000. The Novolex Portfolio Whole Loan requires interest-only payments during its entire term and accrues interest at a rate of 6.22650% per annum. The Novolex Portfolio Whole Loan proceeds were used to recapitalize the borrower following its acquisition of the Novolex Portfolio Properties in a sale-leaseback transaction in February 2023 and pay closing costs.

The Novolex Portfolio Whole Loan has an initial term of 120 months and a remaining term of 119 months as of the Cut-off Date. The scheduled maturity date of the Novolex Portfolio Whole Loan is the payment date in June 2033. Voluntary prepayment of the Novolex Portfolio Whole Loan in whole is permitted at any time on or after June 6, 2025 with payment of a prepayment fee equal to the greater of (i) 1% of the outstanding principal balance as of the prepayment date and (ii) the present value of the remaining scheduled principal and interest payments discounted by the lesser of the treasury rate or the swap rate, less the amount of principal being repaid. Voluntary prepayment of the Novolex Portfolio Whole Loan in whole is permitted on or after the payment date occurring in December 2032 without payment of any prepayment fee. Defeasance of the Novolex Portfolio Whole Loan in whole is permitted at any time after the earlier of (i) the second anniversary of the closing date of the securitization that includes the last pari passu note of the Novolex Portfolio Whole Loan to be securitized and (ii) May 19, 2026. The assumed defeasance lockout period of 25 payments is based on the expected closing date of the Benchmark 2023-B39 securitization in July 2023. The actual lockout period may be longer. In addition, releases of Novolex Portfolio Properties are permitted in connection with a partial prepayment, a partial

| The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-262701) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Deutsche Bank Securities Inc., Goldman Sachs & Co. LLC, J.P. Morgan Securities LLC, Drexel Hamilton, LLC, Academy Securities, Inc. or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146. | ||

| 6 | ||

| LOAN #1: NOVOLEX PORTFOLIO |

defeasance or a property substitution, as described below under “—Release of Collateral”. In connection with a partial release, a prepayment may be made at any time following the origination date.

The table below summarizes the promissory notes that comprise the Novolex Portfolio Whole Loan. The relationship between the holders of the Novolex Portfolio Whole Loan is governed by a co-lender agreement as described under “Description of the Mortgage Pool—The Whole Loans—The Serviced Pari Passu Whole Loans” in the Preliminary Prospectus.

| Whole Loan Summary | ||||

| Note | Original Balance | Cut-off Date Balance | Note Holder(s) | Controlling Piece |

| A-1 | $30,000,000 | $30,000,000 | Benchmark 2023-B39 | Yes |

| A-2 | 25,000,000 | 25,000,000 | DBRI(1) | No |

| A-3 | 15,000,000 | 15,000,000 | Benchmark 2023-B39 | No |

| A-4 | 10,000,000 | 10,000,000 | Benchmark 2023-B39 | No |

| A-5 | 7,500,000 | 7,500,000 | Benchmark 2023-B39 | No |

| A-6 | 25,000,000 | 25,000,000 | Benchmark 2023-B39 | No |

| A-7-1 | 2,000,000 | 2,000,000 | Benchmark 2023-B39 | No |

| A-7-2 | 10,500,000 | 10,500,000 | GSBI(1) | No |

| Whole Loan | $125,000,000 | $125,000,000 | ||

| (1) | Expected to be contributed to one or more future securitization transactions. | |

| ■ | The Mortgaged Properties. The Novolex Portfolio consists of 17 industrial manufacturing, warehouse and distribution properties that total 2,516,274 SF located in Ohio (five properties / 29.8% of NRA), Georgia (two properties / 12.1% of NRA), Indiana (two properties / 11.2% of NRA), Kansas (one property / 10.8% of NRA), Idaho (one property / 7.5% of NRA), Texas (one property / 6.0% of NRA), Illinois (one property / 5.8% of NRA), Connecticut (one property / 5.8% of NRA), New York (one property / 4.8% of NRA), Tennessee (one property / 3.3% of NRA), and Wisconsin (one property / 2.8% of NRA). The Novolex Portfolio Properties are 100% occupied by subsidiaries of Novolex Holdings LLC (“Novolex”). Novolex (Moody’s: Caa2 S&P: B) is a North American manufacturer of high-volume packaging solutions. Novolex holds a top three market position across approximately 75% of product lines. Product line categories include paper bags (approximately 21% of revenues) folding cartons (approximately 17% of revenues), plastic food packaging (approximately 15% of revenues), plastic bags (approximately 15% of revenues) and compostable packaging items (approximately 9% of revenues). |

The following table presents certain information relating to the individual Novolex Portfolio Properties:

Portfolio Summary

Property Name | City, State | Property Sub-Type | Year Built / Renovated | SF | Allocated Whole Loan Cut-off Date Balance | % of Allocated Whole Loan Cut-off Date Balance | Appraised Value | % of Appraised Value | Base Rent |

| 2000 Commerce Center Drive | Franklin, OH | Manufacturing/Warehouse | 2003 / NAP | 275,345 | $14,893,874 | 11.9% | $24,700,000 | 11.9%% | $1,796,626 |

| 1200 Northrop Road | Meriden, CT | Warehouse/Distribution | 1987 / 2021-2022 | 145,819 | 11,034,732 | 8.8 | 18,300,000 | 8.8% | 1,137,388 |

| 3400 Bagcraft Boulevard | Baxter Springs, KS | Manufacturing | 1994 / NAP | 272,330 | 10,100,097 | 8.1 | 16,750,000 | 8.1% | 1,487,306 |

| 690 Unisia Drive | Monroe, GA | Manufacturing | 2001 / NAP | 160,925 | 9,828,751 | 7.9 | 16,300,000 | 7.9% | 1,126,475 |

| 800 Koomey Road | Brookshire, TX | Manufacturing | 1983 / 2023 | 151,748 | 9,346,358 | 7.5 | 15,500,000 | 7.5% | 1,166,153 |

| 3900 West 43rd Street | Chicago, IL | Manufacturing | 1956 / 1967 | 147,117 | 8,863,965 | 7.1 | 14,700,000 | 7.1% | 1,029,819 |

| 540 West Nez Perce | Jerome, ID | Manufacturing/Warehouse | 1973, 2004 / NAP | 187,617 | 8,260,974 | 6.6 | 13,700,000 | 6.6% | 945,121 |

| 4255 Thunderbird Lane | West Chester, OH | Manufacturing | 1991, 2000, 2013 / NAP | 195,280 | 8,049,928 | 6.4 | 13,350,000 | 6.4% | 870,000 |

| 1001 North Madison Avenue | North Vernon, IN | Manufacturing | 1959 / 1999 | 167,926 | 7,507,236 | 6.0 | 12,450,000 | 6.0% | 930,390 |

| 17153 Industrial Highway | Caldwell, OH | Manufacturing | 1958, 1995, 2002 / 2001 | 123,120 | 6,813,796 | 5.5 | 11,300,000 | 5.5% | 883,805 |

| 999 North Madison Avenue | North Vernon, IN | Manufacturing | 2005 / NAP | 114,509 | 5,276,170 | 4.2 | 8,750,000 | 4.2% | 652,347 |

| 407 Sangamore Road | Bremen, GA | Manufacturing | 1975-2000 / NAP | 144,060 | 5,125,422 | 4.1 | 8,500,000 | 4.1% | 637,380 |

| 88 Nesbitt Drive | Holley, NY | Manufacturing | 2002 / 2003, 2006, 2010 | 120,101 | 5,125,422 | 4.1 | 8,500,000 | 4.1% | 632,897 |

| 310 Hartmann Drive | Lebanon, TN | Warehouse/Distribution | 1968 / 1986, 1999 | 84,221 | 4,160,637 | 3.3 | 6,900,000 | 3.3% | 473,743 |

| 101 Commerce Drive | Mount Vernon, OH | Manufacturing | 1972, 1991 / NAP | 82,103 | 4,130,487 | 3.3 | 6,850,000 | 3.3% | 523,560 |

| 620 Hardin Street | Coldwater, OH | Manufacturing | 1997 / NAP | 74,369 | 3,678,244 | 2.9 | 6,100,000 | 2.9% | 474,102 |

| 3100 East Richmond Street | Shawano, WI | Manufacturing | 1983 / 1993, 2013 | 69,684 | 2,803,907 | 2.2 | 4,650,000 | 2.2% | 348,768 |

| Total | 2,516,274 | $125,000,000 | 100.0% | $207,300,000 | 100.0%% | $15,115,880 |

| The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-262701) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Deutsche Bank Securities Inc., Goldman Sachs & Co. LLC, J.P. Morgan Securities LLC, Drexel Hamilton, LLC, Academy Securities, Inc. or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146. | ||

| 7 | ||

| LOAN #1: NOVOLEX PORTFOLIO |

The Novolex Portfolio Properties are responsible for approximately 25% of Novolex’s annual production volume and generate approximately $1.2 billion of annual revenue for Novolex. A majority of the Novolex Portfolio Properties serve Novolex’s largest customers, running seven days per week and employing over 1,000 people. On average, Novolex has been a tenant at the Novolex Portfolio Properties for approximately 25 years. In connection with a sale-leaseback transaction in February 2023, certain subsidiaries of Novolex (collectively, the “Novolex Tenant”) executed a 20-year, triple net master lease with the borrower expiring February 14, 2043 (the “Novolex Lease”). The lease is guaranteed by Clydesdale Acquisition Holdings, Inc, the parent company of Novolex. In April 2022, funds managed by Apollo Global Management, an alternative asset management firm with approximately $598 billion in assets under management (as of March 31, 2023), acquired an 86% majority stake in Novolex from The Carlyle Group, injecting $1.3 billion of new cash equity in Novolex.

Novolex produces flexible packaging with differentiated scale and breadth of product offerings. Novolex produces approximately 25,000 SKUs across paper and plastic products. Currently, the company has over 80 new projects in its innovation pipeline. Approximately 75% of the company’s products are sold to food and delivery users with a focus on quick service restaurant and fast-food operators. Novolex operates 57 manufacturing facilities in North America and Europe, including two recycling facilities.

Novolex maintains a diversified customer base with long tenured relationships. Novolex has direct relationships with its largest accounts, with the top 10 customers comprising approximately 32% of revenue. The average tenure of the company’s largest customers (including BUNZL, McDonald’s, Sysco and Kroger) is over 20 years. Novolex’s customers typically buy from multiple product lines (across both food and delivery and commercial/industrial product lines), making the company a “one-stop-shop” for flexible packaging.

The following table presents certain information relating to the sole tenant at the Novolex Portfolio Properties:

Sole Tenant Summary(1)

| Credit Rating (Fitch/MIS/S&P)(2) | Tenant GLA | % of GLA | UW Base Rent | % of Total UW Base Rent | UW Base Rent $ per SF | Lease Expiration | Renewal / Extension Options |

| Novolex Tenant | NR/Caa2/B | 2,516,274 | 100.0% | $15,115,880 | 100.0% | $6.01 | 2/14/2043 | 4, 5-year options |

| Total Occupied | 2,516,274 | 100.0% | $15,115,880 | 100.0% | $6.01 | |||

| Vacant | 0 | 0.0% | ||||||

| Total / Wtd. Avg. | 2,516,274 | 100.0% |

| (1) | Based on the underwritten rent roll as of July 6, 2023. | |

| (2) | In some instances, ratings provided are those of the parent company of the entity shown, whether or not the parent company guarantees the lease. |

The Novolex Lease permits a sale of one or more of the Novolex Portfolio Properties leased under the Novolex Lease to a Credit Entity (as defined below) that acquires all or substantially all of the assets (either directly or through the acquisition of equity interests) of a divisional business unit that operates at the premises leased under the Novolex Lease (such sale, a “Divisional Sale”).

A “Credit Entity” means any third party entity which is not an affiliate of Novolex or its lease guarantor that, on a proforma basis, after giving effect to the applicable transaction, (a) has a minimum EBITDA (as defined in any Senior Credit Facility (as defined below)) of 35 multiplied by the then-current annual base rent under the Novolex Lease, combined with a maximum Total Net Leverage Ratio (as defined in any Senior Credit Facility) of 6.5x; (b) has a credit rating of B or better from Standard and Poor's (or the equivalent rating from Moody's Investors Services, Fitch Group or any other nationally recognized rating agency); (c) has a minimum net worth of 80 multiplied by the then current annual base rent under the Novolex Lease; or (d) has posted a letter of credit in an amount equal to 12 months of the then current base rent, provided, however, that in any such case such entity has the expertise to operate the facility (either directly or through the engagement of a manager).

“Senior Credit Facility” means a credit facility secured by all or substantially all of the assets of Novolex and/or its lease guarantor and/or their affiliates then in effect, or if none is in effect, most recently in effect.

In connection with a Divisional Sale, the Novolex Lease may be split into more than one lease (any such additional lease, a “Separate Lease”), which leases will not be cross-defaulted. The Novolex Lease provides that no more than one such Separate Lease may be entered into during any 10-year period during the term of the Novolex Lease, and any such Separate Lease may not include more than five individual leased premises or leased premises for which the base rent exceeds 25% of the aggregate base rent under the Novolex Lease.

| The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-262701) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Deutsche Bank Securities Inc., Goldman Sachs & Co. LLC, J.P. Morgan Securities LLC, Drexel Hamilton, LLC, Academy Securities, Inc. or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146. | ||

| 8 | ||

| LOAN #1: NOVOLEX PORTFOLIO |

The following table presents certain information relating to the lease rollover schedule at the Novolex Portfolio Properties, based on initial lease expiration dates:

Lease Expiration Schedule(1)

Year Ending December 31 | Expiring Owned GLA | % of Owned GLA | Cumulative % of Owned GLA | UW Base Rent | % of Total UW Base Rent | UW Base Rent $ per SF | # of Expiring Tenants | ||||

| MTM & 2023 | 0 | 0.0 | % | 0.0% | $0 | 0.0 | % | $0.00 | 0 | ||

| 2024 | 0 | 0.0 | % | 0.0% | 0 | 0.0 | % | $0.00 | 0 | ||

| 2025 | 0 | 0.0 | % | 0.0% | 0 | 0.0 | % | $0.00 | 0 | ||

| 2026 | 0 | 0.0 | % | 0.0% | 0 | 0.0 | % | $0.00 | 0 | ||

| 2027 | 0 | 0.0 | % | 0.0% | 0 | 0.0 | % | $0.00 | 0 | ||

| 2028 | 0 | 0.0 | % | 0.0% | 0 | 0.0 | % | $0.00 | 0 | ||

| 2029 | 0 | 0.0 | % | 0.0% | 0 | 0.0 | % | $0.00 | 0 | ||

| 2030 | 0 | 0.0 | % | 0.0% | 0 | 0.0 | % | $0.00 | 0 | ||

| 2031 | 0 | 0.0 | % | 0.0% | 0 | 0.0 | % | $0.00 | 0 | ||

| 2032 | 0 | 0.0 | % | 0.0% | 0 | 0.0 | % | $0.00 | 0 | ||

| 2033 | 0 | 0.0 | % | 0.0% | 0 | 0.0 | % | $0.00 | 0 | ||

| 2034 & Thereafter | 2,516,274 | 100.0 | 100.0% | 15,115, 880 | 100.0 | $6.01 | 1 | ||||

| Vacant | 0 | 0.0 | % | 100.0% | NAP | NAP |

| NAP | NAP |

| |

| Total / Wtd. Avg. | 2,516,274 | 100.0 | % | $15,115, 880 | 100.0 | % | $6.01 | 1 | |||

| (1) | Based on the underwritten rent roll as of July 6, 2023. |

The following table presents certain information relating to historical occupancy at the Novolex Portfolio Properties:

Historical Leased %(1)

2020 | 2021 | 2022 | As of 7/6/2023(2) |

| 100.0% | 100.0% | 100.0% | 100.0% |

| (1) | As provided by the borrower and reflects year-end occupancy for the indicated year ended December 31 unless specified otherwise. The Novolex Portfolio was 100% owner occupied prior to the borrower sponsor’s acquisition in February 2023. | |

| (2) | Based on the underwritten rent roll as of July 6, 2023. |

| ■ | Underwritten Net Cash Flow. The following table presents certain information relating to the Underwritten Net Cash Flow at the Novolex Portfolio Properties: |

Cash Flow Analysis(1)(2)(3)

Underwritten | Underwritten $ per SF | ||

| Rents In Place | $15,115,880 | $6.01 | |

| Rent Steps | 453,476 | $0.18 | |

| Vacant Income | 0 | $0.00 |

|

| Gross Potential Rent | $15,569,357 | $6.19 | |

| CAM | 456,744 | $0.18 | |

| Other Income | 0 | $0.00 |

|

| Total Gross Income | $16,026,100 | $6.37 | |

| Vacancy / Credit Loss | (801,305) | ($0.32 | ) |

| Effective Gross Income | $15,224,795 | $6.05 | |

| Total Expenses | 456,744 | $0.18 |

|

| Net Operating Income | $14,768,052 | $5.87 | |

| TI/LC | 0 | $0.00 | |

| Capital Expenditures | 452,929 | $0.18 |

|

| Net Cash Flow | $14,315,122 | $5.69 | |

| Occupancy(4) | 95.0% | ||

| NOI Debt Yield(5) | 11.8% | ||

| NCF DSCR(5) | 1.81x | ||

| (1) | Certain items such as interest expense, interest income, lease cancellation income, depreciation, amortization, debt service payments and any other non-recurring items were excluded from the historical presentation and are not considered for the underwritten cash flow. | |

| (2) | Based on the in-place rent roll as of July 6, 2023. |

| (3) | Historical cash flows are unavailable due to the recent acquisition of the Novolex Portfolio in a sale-leaseback transaction. |

| (4) | Represents the underwritten economic occupancy. |

| (5) | Based on the Novolex Portfolio Whole Loan. |

| The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-262701) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Deutsche Bank Securities Inc., Goldman Sachs & Co. LLC, J.P. Morgan Securities LLC, Drexel Hamilton, LLC, Academy Securities, Inc. or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146. | ||

| 9 | ||

| LOAN #1: NOVOLEX PORTFOLIO |

| ■ | Appraisal. According to the portfolio appraisal, the Novolex Portfolio Properties have an aggregate “as is” appraised value of $207,300,000 as of April 1, 2023. |

| ■ | Environmental Matters. According to the Phase I environmental reports dated December 12, 2022 through February 16, 2023, the environmental consultant identified recognized environmental conditions at the following Novolex Portfolio Properties: 3400 Bagcraft Boulevard, 3100 East Richmond Street, 800 Koomey Road, 3900 West 43rd Street, 17153 Industrial Highway and 101 Commerce Drive, and also identified controlled recognized environmental conditions and/or business environmental risks at the 1001 North Madison Avenue, 3900 West 43rd Street and 540 West Nez Perce properties. The borrower has obtained a premises environmental liability insurance policy from Great American E&S Insurance Company with respect to certain of the Novolex Portfolio Properties (the “EIL Policy”), which expires February 14, 2033 (prior to the maturity date of the Novolex Portfolio Whole Loan). See “Description of the Mortgage Pool—Environmental Considerations” in the Preliminary Prospectus and “Escrows—EIL Policy Reserve” below. |

| ■ | Market Overview and Competition. The Novolex Portfolio is located across thirteen different markets in the United States with the largest markets by square foot being Cincinnati (18.7%), Atlanta (12.1%) and Indianapolis (11.2%). The portfolio markets are outlined below: |

Market Overview(1)

Market | # of Properties | SF | Market Vacancy | Market Availability | Market Rent |

| Cincinnati – OH | 2 | 470,625 | 3.0% | 6.2% | $6.87 |

| Atlanta – GA | 2 | 304,985 | 4.3% | 7.8% | $8.53 |

| Indianapolis – IN | 2 | 282,435 | 5.9% | 9.4% | $7.11 |

| Joplin – MO | 1 | 272,330 | 1.8% | 1.3% | $5.12 |

| Columbus – OH | 2 | 205,223 | 5.0% | 8.5% | $7.55 |

| Idaho Falls – ID | 1 | 187,617 | 2.3% | 3.0% | $9.25 |

| Houston – TX | 1 | 151,748 | 5.6% | 10.5% | $8.63 |

| Chicago – IL | 1 | 147,117 | 3.9% | 7.4% | $9.00 |

| New Haven – CT | 1 | 145,819 | 4.1% | 5.6% | $9.09 |

| Rochester – NY | 1 | 120,101 | 5.1% | 5.2% | $7.67 |

| Nashville – TN | 1 | 84,221 | 3.3% | 5.4% | $10.40 |

| Lima – OH | 1 | 74,369 | 1.7% | 3.0% | $4.89 |

| Green Bay – WI | 1 | 69,684 | 1.5% | 3.1% | $5.88 |

| Total / Wtd. Avg. | 17 | 2,516,274 | 3.8% | 6.2% | $7.57 |

| (1) | Source: Third-party market research report. |

| ■ | The Borrower. The borrower is NM NVLX, L.P., a newly formed special purpose, bankruptcy-remote, single member Delaware limited partnership with two independent directors. Legal counsel to the borrower delivered a non-consolidation opinion in connection with the origination of the Novolex Portfolio Whole Loan. The borrower sponsor and non-recourse carveout guarantor is New Mountain Net Lease Partners II Corporation, which is a subsidiary of New Mountain Capital, LLC. |

New Mountain Capital, LLC is a New York, New York based alternative investment firm. As of January 2023, the firm managed private equity, public equity, credit, and real estate funds with $37 billion and approximately 17 million SF in assets under management. New Mountain Net Lease uses a private markets strategy that seeks to create a diversified portfolio of cash flowing, long-term leased real estate assets. New Mountain Net Lease closed its first net lease real estate fund, New Mountain Net Lease Partners, L.P. (“NMNLP”), with $533 million of equity capital commitments in April 2019. NMNLP’s investors include pension funds, insurance companies, asset managers, family offices, high net worth individuals and endowments. Since 2016, NMNLP has completed 46 net lease transactions representing more than $1.7 billion in acquisition value across NMNLP and New Mountain Net Lease Corporation. The borrower sponsor for the Novolex Portfolio Whole Loan is New Mountain’s second net lease real estate fund, which had raised approximately $800 million of commitments as of March 2023.

| ■ | Escrows. |

Real Estate Tax Reserve. On each monthly payment date, the borrower is required to deposit an amount equal to 1/12 of the estimated annual real estate taxes into the tax reserve account; provided that such deposits are waived so long as the Reserve Waiver Conditions (as defined below) are satisfied.

| The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-262701) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Deutsche Bank Securities Inc., Goldman Sachs & Co. LLC, J.P. Morgan Securities LLC, Drexel Hamilton, LLC, Academy Securities, Inc. or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146. | ||

| 10 | ||

| LOAN #1: NOVOLEX PORTFOLIO |

Insurance Reserve. On each monthly payment date, the borrower is required to deposit 1/12 of estimated insurance premiums, unless an event of default has occurred; provided that such deposits are waived so long as the Tenant Insurance Conditions (as defined below) are satisfied.

Replacement Reserve. On each monthly payment date, the borrower is required to deposit $37,744.11 into a replacement reserve, subject to a cap of approximately $22,673,820; provided that such deposits are waived so long as the Reserve Waiver Conditions are satisfied.

TI/LC Reserve. On each monthly payment date, the borrower is required to deposit $209,689.50 into a TI/LC reserve, subject to a cap of $22,673,820; provided that such deposits are waived so long as the Reserve Waiver Conditions are satisfied.

EIL Policy Reserve. On each monthly payment date during the existence of an EIL Policy Trigger Period (defined below), the borrower is required to deposit all available cash into the EIL policy reserve for the purpose of purchasing a renewal or replacement of the EIL Policy that was in effect at origination.

An “EIL Policy Trigger Period” will commence nine months prior to the expiration of the current EIL Policy and will end on the earlier of (i) the date the borrower obtains an additional environmental liability insurance that satisfies the conditions set forth in the Novolex Portfolio Whole Loan documents or (ii) the date on which an amount equal to the cost of an additional environmental liability insurance policy has accumulated in the EIL policy reserve account.

“Tenant Insurance Conditions” means collectively, (i) no event of default has occurred and is continuing, and (ii) an insurance policy that satisfies the insurance requirements in the Novolex Portfolio Whole Loan documents is in effect with respect to all of the insurance policies required by the Novolex Portfolio Whole Loan documents.

“Reserve Waiver Conditions” mean, collectively, (i) the Novolex Lease (or (1) any Separate Lease entered into in connection with a Divisional Sale or (2) a replacement of the Novolex Lease which is entered into in accordance with the terms of the Novolex Portfolio Whole Loan documents) is in full force and effect, the entirety of each of the Novolex Portfolio Properties is demised pursuant to said lease, and the applicable lease is a “triple net” lease, (ii) no Trigger Period (as defined below) has occurred and is then continuing, (iii) the tenant under the Novolex Lease (or a replacement lease which is entered into in accordance with the terms of the Novolex Portfolio Whole Loan documents) is obligated, pursuant to its lease, to (w) pay all taxes, other charges, and any other assessments (if any), directly to the applicable governmental authority, (x) maintain insurance on all of the Novolex Portfolio Properties under an acceptable tenant policy, (y) perform and pay for all capital expenditures at the Novolex Portfolio Properties and (z) perform and pay for all other ongoing recurring property related operating expenses, (iv) such tenant performs all of such obligations in a timely manner (which, with respect to the obligations described in clause (iii)(w) means prior to the date that either such obligations become delinquent or any interest or penalties are incurred thereon, with respect to the obligations in clause (iii)(x) means in accordance with the timeframes set forth in the Novolex Whole Loan documents and with respect to the obligations described in clauses (iii)(y) and (iii)(z) means in accordance with the timeframes set forth in the Novolex Lease (or the applicable replacement lease)), and (v) upon the lender’s request, the borrower provides evidence of such timely performance by such tenant to the lender in a form acceptable to the lender in its reasonable discretion.

| ■ | Lockbox and Cash Management. The Novolex Portfolio Whole Loan is structured with a hard lockbox and springing cash management. All funds in the lockbox accounts are required to be swept on a daily basis to an account designated by the borrower, unless a Trigger Period is continuing, in which case such funds are required to be swept on a daily basis into a cash management account controlled by the lender, and, provided no event of default is continuing under the Novolex Portfolio Whole Loan, applied to make required deposits (if any) to the tax and insurance reserves, pay debt service on the Novolex Portfolio Whole Loan, make required deposits (if any) to the replacement and TI/LC reserves, pay operating expenses and extraordinary operating expenses, and then to deposit excess cash flow (i) if an EIL Policy Trigger Period exists and no other Trigger Period, then exists, into the EIL policy reserve, (ii) if a Lease Sweep Period (as defined below) exists, into a lease sweep reserve, and (iii) during any other Trigger Period, into an excess cash flow reserve. |

A “Trigger Period” will commence upon the occurrence of (a) an event of default, (b) if the debt service coverage ratio of the Novolex Portfolio Whole Loan falls below 1.20x, (c) the commencement of a Lease Sweep Period or (d) the commencement of an EIL Policy Trigger Period and will end if, (i) with respect to a Trigger Period continuing pursuant to clause (a), the event of default commencing the Trigger Period has been cured, (ii) with respect to a Trigger Period continuing due to clause (b), the debt service coverage ratio is at least 1.25x for two consecutive quarters, (iii) with

| The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-262701) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Deutsche Bank Securities Inc., Goldman Sachs & Co. LLC, J.P. Morgan Securities LLC, Drexel Hamilton, LLC, Academy Securities, Inc. or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146. | ||

| 11 | ||

| LOAN #1: NOVOLEX PORTFOLIO |

respect to a Trigger Period continuing due to clause (c), such Lease Sweep Period has ended or (iv) with respect to a Trigger Period continuing due to clause (d), such EIL Policy Trigger Period has ended.

A “Lease Sweep Period” will commence on the first monthly payment date following the occurrence of any of the following: (i) upon the date required under a Lease Sweep Lease (as defined below) by which the tenant thereunder is required to give notice of its exercise of a renewal option thereunder, (ii) the date that a Lease Sweep Lease is surrendered, cancelled or terminated prior to its then current expiration date or the receipt by the borrower or the property manager of notice from any tenant under a Lease Sweep Lease of its intent to surrender, cancel or terminate such Lease Sweep Lease, (iii) the date that any tenant under a Lease Sweep Lease “goes dark” or gives notice that it intends to discontinue its business (other than (i) a temporary discontinuance of business for a commercially reasonable time as the result of the performance of standard and customary alterations at the applicable Novolex Portfolio Property, (ii) any temporary discontinuance of business relating to an ongoing restoration at the applicable Novolex Portfolio Property pursuant to the terms of the loan agreement, or (iii) any temporary discontinuance of business as a result of (or in order to comply with) governmental restrictions on the use or occupancy of any Novolex Portfolio Property as a result of, or otherwise in connection with, any declared state of emergencies or any other pandemic or epidemic (including the COVID-19 pandemic) or any other government mandated quarantines, closures or disruptions, provided that the tenant resumes operations in its leased space within a reasonable period of time relative to other similarly situated tenants in the geographic area where the applicable Novolex Portfolio Property is located after such government restrictions are lifted) at an aggregate portion of the Novolex Portfolio Properties exceeding the lesser of (A) three individual Novolex Portfolio Properties or (B) one or more Novolex Portfolio Properties (or portions of Novolex Portfolio Properties on a pro rata basis) that, in the aggregate, account for 25% or more of the base rent under the applicable Lease Sweep Leases of the Novolex Portfolio Properties (provided that, from and after the occurrence of a Divisional Sale, the foregoing clause (A) will be deemed not to apply), (iv) upon a default in (x) payment of monthly base rent or (y) any other material monetary default (which continues for 60 days beyond any applicable notice and cure period) under a Lease Sweep Lease by the tenant thereunder; (v) the occurrence of a bankruptcy or insolvency of any tenant or its direct or indirect parent company (if any) under a Lease Sweep Lease, (vi) to the extent the applicable Lease Sweep Lease is set to expire on or before the date that is three years following the stated maturity date, a Lease Sweep Period will commence on the date that is 12 months prior to the stated maturity date or (vii) upon a decline in the credit rating of the tenant under a Lease Sweep Lease at or below “CCC-” or equivalent by any rating agency.

A Lease Sweep Period will end if: (a) in the case of all clauses above, the entirety of the Lease Sweep Lease space is leased pursuant to one or more replacement leases acceptable to the lender, as more fully described in the Novolex Portfolio Whole Loan documents (the “Acceptable Replacement Leases”) and, in the lender’s judgment, sufficient funds have been accumulated in the lease sweep reserve (during the continuance of the subject Lease Sweep Period) to cover all anticipated approved Lease Sweep Lease space leasing expenses, free rent periods, and/or rent abatement periods set forth in all such Acceptable Replacement Leases and any shortfalls in required payments under the Novolex Portfolio Whole Loan documents or operating expenses as a result of any anticipated down time prior to the commencement of payments under such Acceptable Replacement Leases; (b) in the case of clause (i) above, the date on which the subject tenant under the Lease Sweep Lease irrevocably exercises its renewal or extension option with respect to all of its Lease Sweep Lease space, and in the lender’s judgment, sufficient funds have been accumulated in the lease sweep reserve (during the continuance of the subject Lease Sweep Period) to cover all anticipated Lease Sweep Space leasing expenses approved by the lender, free rent periods and/or rent abatement periods in connection with such renewal or extension; (c) in the case of clause (ii) above, the tenant irrevocably rescinds its notice to surrender, cancel or terminate the Lease Sweep Lease, (d), in the case of clause (iii) above, the tenant reopens for business in the entirety of the Lease Sweep Lease space (or a portion thereof sufficient to avoid the trigger thresholds set forth in such clause (iii)), or rescinds its notice to discontinue its business, as applicable and continuously operates thereafter for at least 30 days; (e) in the case of clause (iv) above, the date on which (x) with respect to a default in the payment of base rent, the subject default has been cured, all arrearages in rent have been brought current and the applicable tenant has timely made the rental payment due for the calendar month immediately following the date of such cure and (y) with respect to any other material monetary default, the date on which the subject default has been cured, and no other monetary default under such Lease Sweep Lease occurs for a period of 30 days following such cure; (f) in the case of clause (v) above, either (x) the applicable bankruptcy or insolvency proceeding has terminated and the applicable Lease Sweep Lease has been affirmed, assumed or assigned in a manner reasonably satisfactory to the lender or (y) the applicable Lease Sweep Lease space has been assumed and assigned to a third party in a manner reasonably satisfactory to the lender, (g) in the case of clauses (iii) or (vii) above, the date that an amount equal to 18 months’ rent (in the case of clause (iii), for the applicable Lease Sweep Lease space that has gone dark) is deposited into the lease sweep reserve, and (h) in the case of clause (vii) above, if the credit rating of the tenant (or its parent entity) has been restored to at least “CCC” or its equivalent by the relevant rating agencies, (i) the date on which each of the following conditions is satisfied: (a) less than the entirety of the Lease Sweep Lease space (or applicable portion

| The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-262701) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Deutsche Bank Securities Inc., Goldman Sachs & Co. LLC, J.P. Morgan Securities LLC, Drexel Hamilton, LLC, Academy Securities, Inc. or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146. | ||

| 12 | ||

| LOAN #1: NOVOLEX PORTFOLIO |

thereof) is leased pursuant to one or more qualified leases and paying full, unabated rent (which allows the Novolex Portfolio Properties to achieve a debt service coverage ratio of 1.20x) (such space, the “Tenanted Space”), (ii) sufficient funds have been accumulated in the lease sweep reserve account to cover all anticipated approved leasing expenses, free rent periods, and/or rent abatement periods in the Tenanted Space, and (iii) the funds in the lease sweep reserve are equal to 18 months’ rent applicable to the Untenanted Space (for purposes hereof, “Untenanted Space” means any portion of the applicable Lease Sweep Space which does not qualify as the Tenanted Space; and (j) with respect to any Lease Sweep Period commencing with respect to any divisional sweep lease, the date on which the lease sweep funds in the lease sweep reserve collected with respect to the divisional sweep lease (including any lease termination payments with respect to such divisional sweep lease deposited into the lease sweep reserve) is equal to 18 months of rent under such Lease Sweep Lease, unless the applicable Lease Sweep Lease space has been leased pursuant to one or more leases which, in the aggregate, (x) require the borrower to incur expenses, including the payment of brokerage commissions, completion of tenant improvements or payment of tenant allowances, and/or (y) provide for free rent periods and/or rent abatement periods with respect to rent amounts, which, in the lender’s determination, exceed an amount equal to 18 months of rent under such lease (in which case the Lease Sweep Period in question will continue until the borrower satisfies clause (A) above).

"Lease Sweep Lease" means (i) the Novolex lease, (ii) any Separate Lease created pursuant to a Divisional Sale, provided that the Novolex Portfolio Properties subject to such Separate Lease comprise 15% or more of the aggregate base rent under all leases at the Novolex Portfolio Properties, and (iii) any replacement lease covering the lesser of (A) five or more individual Novolex Portfolio Properties or (B) one or more Novolex Portfolio Properties that, in the aggregate, exceed 15% of the base rent of the Novolex Portfolio Properties.

| ■ | Property Management. The Novolex Portfolio is currently self-managed. |

| ■ | Current Mezzanine or Subordinate Indebtedness. None. |

| ■ | Permitted Future Mezzanine or Subordinate Indebtedness. Not permitted. |

| ■ | Release of Collateral. The borrower may obtain the release of any Lease Sweep Defaulted Property (as defined below), Defaulted Individual Property (as defined below) and/or (subject to the lender's prior written consent) Divisional Sale Property (as defined below) upon satisfaction of the following conditions, among others: (i) either defeasance (if the release is on or after the defeasance lockout expiration date) or prepayment of a release amount equal to 110% of the allocated loan amount of such Novolex Portfolio Property, together with, in the case of a prepayment, payment of a prepayment fee equal to the greater of 1.0% of the amount prepaid and a yield maintenance premium, (ii) the sale of such Novolex Portfolio Property is (x) related to a default by the tenant under a Lease Sweep Lease, which default relates solely to the Novolex Portfolio Property being released (the “Lease Sweep Defaulted Property”) and after giving effect to the applicable release, no default will be ongoing with respect to any Lease Sweep Lease which demises any portion of the remaining Novolex Portfolio Properties (in which case, said sale may be either to a third party or to an affiliate of the borrower) or (y) pursuant to an arm’s-length agreement to a bona fide third party or (z) with respect to release of a Divisional Sale Property, a Divisional Sale has occurred and all Divisional Sale Properties are being released in connection therewith, (iii) the debt service coverage ratio of the remaining Novolex Portfolio Properties after such release is no less than the greater of (x) the debt service coverage ratio immediately prior to such release and (y) 1.81x, (iv) the loan-to-value ratio of the remaining Novolex Portfolio Properties after such release is no more than the lesser of (x) the loan-to-value ratio immediately prior to such release and (y) 60.3%, (v) the Novolex Portfolio Property being released is removed from the Novolex Lease, (vi) no event of default exists, except in connection with the release of a Defaulted Individual Property as to which the Defaulted Individual Property Conditions (as defined below) are satisfied, (vii) satisfaction of REMIC related conditions and (viii) with respect to a release of either (but not both) Novolex Portfolio Property located in Indiana (each an “Indiana Novolex Portfolio Property”), which are adjacent to each other, the released Novolex Portfolio Property is legally subdivided and on a separate tax lot from the remaining Indiana Novolex Portfolio Property, and satisfaction of conditions related to the remaining Indiana Novolex Portfolio Property's compliance with zoning and the execution of easements allowing for the continued use of any shared facilities, access or parking. |

"Defaulted Individual Property Conditions" will be deemed to exist with respect to an individual Novolex Portfolio Property securing the Novolex Portfolio Mortgage Loan (the "Defaulted Individual Property") to the extent that: (i) an event of default exists with respect to the related individual Novolex Portfolio Property that relates solely to the Defaulted Individual Property and would not exist but for such Defaulted Individual Property being an individual Novolex Portfolio

| The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-262701) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Deutsche Bank Securities Inc., Goldman Sachs & Co. LLC, J.P. Morgan Securities LLC, Drexel Hamilton, LLC, Academy Securities, Inc. or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146. | ||

| 13 | ||

| LOAN #1: NOVOLEX PORTFOLIO |

Property under the Novolex Portfolio Whole Loan documents; (ii) either the lender has delivered notice to the borrower with respect to such event of default or has commenced exercising remedies in connection therewith; (iii) the borrower has demonstrated to the lender's reasonable satisfaction that it has promptly and diligently pursued a cure of such event of default; (iv) the borrower has been unable to effect a cure of such default; (v) after giving effect to a defeasance or prepayment in connection with the release of such Novolex Portfolio Property no event of default or material default will thereafter be continuing and (vi) after the release of such Novolex Portfolio Property, the borrower will not be subject to any material contingent liabilities relating to such Novolex Portfolio Property.

"Divisional Sale Property" means any Novolex Portfolio Novolex Portfolio Property subject to a Divisional Sale.

In addition, the Novolex Lease allows the Novolex Tenant, following the end of the third lease year (or, if permitted by the borrower’s mortgagee, following the end of the second lease year), and for each ten lease year period thereafter during the term of the Novolex Lease, to substitute one or more of the leased premises for which the base rent allocated to such leased premises does not exceed 10% of the aggregate base rent of all leased premises under the Novolex Lease at the time the substitution request is made. The Novolex Lease provides that the tenant’s right to effect such a substitution is conditioned on, among other things, (i) the substitute property must be a property as to which the landlord will hold fee title and be of “like kind and quality” as the relinquished property, as reasonably determined by the landlord, (ii) the substitute property must have a fair market value equal to or greater than that of the relinquished property, based on appraisals prepared by an independent MAI professional appraiser reasonably acceptable to both the landlord and Novolex Tenant (and the landlord will not be required to accept the substitute property unless its appraised value is equal to the greater of the allocated purchase price of the relinquished property and the appraised value of the relinquished property as of the date of substitution), (iii) upon the substitution), the relinquished property will be removed from the Novolex Lease and the substitute property will be added to the Novolex Lease, and the rent allocation for the substitute property cannot be less than that of the relinquished property and (iv) any customer and commercially reasonable requirements of the landlord’s mortgagee (i.e. the lender) must be satisfied in all respects.

In connection with such substitution rights under the Novolex Lease, the borrower may obtain the release of any one or more Novolex Portfolio Properties (each a “Novolex Release Property”) that do not represent more than 10% in the aggregate of the base rent of all of the Novolex Portfolio Properties, by substituting therefor another property as to which the fee interest is acquired by the borrower (each, a “Novolex Substitute Property”), provided that the following conditions, among others, are satisfied: (i) the lender is satisfied that the Novolex Substitute Property is of like kind and quality with the Novolex Release Property, including, without limitation, with respect to the age of the improvements, location and use, (ii) the number of Novolex Portfolio Properties remains the same after the substitution, (iii) the sale of the Novolex Release Property is (x) pursuant to an arm’s-length agreement to a third party not affiliated with the borrower or (ii) to an affiliate of the borrower pursuant to terms and conditions that would be set forth in a bona fide arm’s-length third-party transaction, (iv) after the substitution, each remaining borrower will be a special purpose bankruptcy remote entity, (v) the lender receives a current appraisal of the Novolex Substitute Property, in form and substance reasonably acceptable to it, showing a fair market value no less than the fair market value of the Novolex Release Property as of such date, (vi) the underwritten net cash flow of the Novolex Substitute Property is no less than the greater of (x) the underwritten net cash flow of the Novolex Release Property immediately preceding such substitution and (y) the underwritten net cash flow attributable to the Novolex Release Property as of the origination date of the Novolex Portfolio Whole Loan (as determined by the lender in its sole discretion); (vii) the debt service coverage ratio of the remaining Novolex Portfolio Properties (including the Novolex Substitute Property) after such substitution is no less than the greater of (x) the debt service coverage ratio immediately prior to such substitution and (y) 1.81x, (viii) the loan-to-value ratio of the remaining Novolex Portfolio Properties (including the Novolex Substitute Property) after such substitution is no more than the lesser of (x) the loan-to-value ratio immediately prior to such substitution and (y) 60.3%, (ix) the Novolex Release Property is removed from, and the Novolex Substitute Property is added to, the Lease Sweep Lease, on the same terms and conditions, except as required by the following clause (x), and the tenant of the Novolex Substitute Property is in possession of, and open and operating in the entirety of such Novolex Portfolio Property, (x) the rent payable under the lease at the Novolex Substitute Property is not materially greater than the rent for comparable space in the market in which such Novolex Substitute Property is located, (xi) no event of default exists, except in connection with the substitution of a Novolex Release Property that is a Defaulted Individual Property as to which the Defaulted Individual Property Conditions are satisfied, (xii) satisfaction of REMIC related conditions, (xiii) a rating agency confirmation is obtained, and (xiv) the borrower has executed and delivered to the lender all additional information and documentation as would be reasonably acceptable to a reasonably prudent lender contemplating such a property release and substitution.

| The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-262701) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Deutsche Bank Securities Inc., Goldman Sachs & Co. LLC, J.P. Morgan Securities LLC, Drexel Hamilton, LLC, Academy Securities, Inc. or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146. | ||

| 14 | ||

| LOAN #1: NOVOLEX PORTFOLIO |

| ■ | Terrorism Insurance. The borrower is required to maintain terrorism insurance in an amount equal to the full replacement cost of the Novolex Portfolio Properties plus the cost of rental loss and/or business interruption coverage for 24 months. For so long as TRIPRA is in effect and continues to cover both foreign and domestic acts, the lender must accept terrorism insurance with coverage against acts which are “certified” within the meaning of TRIPRA. See “Risk Factors—Risks Relating to the Mortgage Loans—Terrorism Insurance May Not Be Available for All Mortgaged Properties” in the Preliminary Prospectus. |

| The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-262701) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Deutsche Bank Securities Inc., Goldman Sachs & Co. LLC, J.P. Morgan Securities LLC, Drexel Hamilton, LLC, Academy Securities, Inc. or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146. | ||

| 15 | ||

| LOAN #2: SEAGATE CAMPUS |

| The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-262701) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Deutsche Bank Securities Inc., Goldman Sachs & Co. LLC, J.P. Morgan Securities LLC, Drexel Hamilton, LLC, Academy Securities, Inc. or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146. | ||

| 16 | ||

| LOAN #2: SEAGATE CAMPUS |

| The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-262701) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Deutsche Bank Securities Inc., Goldman Sachs & Co. LLC, J.P. Morgan Securities LLC, Drexel Hamilton, LLC, Academy Securities, Inc. or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146. | ||

| 17 | ||

| LOAN #2: SEAGATE CAMPUS |

| Mortgaged Property Information | Mortgage Loan Information | ||||

| Number of Mortgaged Properties | 1 | Loan Seller(2) | CREFI | ||

| Location (City / State) | Fremont, California | Cut-off Date Balance(2) | $86,000,000 | ||

| Property Type | Industrial | Cut-off Date Balance per SF(1) | $299.25 | ||

| Size (SF) | 574,775 | Percentage of Initial Pool Balance | 9.5% | ||

| Total Occupancy as of 7/6/2023 | 100.0% | Number of Related Mortgage Loans | None | ||

| Owned Occupancy as of 7/6/2023 | 100.0% | Type of Security | Fee | ||

| Year Built / Latest Renovation | 2010 / 2016 | Mortgage Rate | 7.04000% | ||

| Appraised Value | $260,000,000 | Original Term to Maturity (Months) | 120 | ||

| Appraisal Date | 4/13/2023 | Original Amortization Term (Months) | NAP | ||

| Borrower Sponsor | Kato Road Cypress Holdings, LLC | Original Interest Only Period (Months) | 120 | ||

| Property Management | Self-Managed | First Payment Date | 7/6/2023 | ||

| Maturity Date | 6/6/2033 | ||||

| Underwritten Revenues | $28,021,697 | ||||

| Underwritten Expenses | $4,631,757 | Escrows(3) | |||

| Underwritten Net Operating Income (NOI) | $23,389,940 | Upfront | Monthly | ||

| Underwritten Net Cash Flow (NCF) | $22,468,077 | Taxes | $0 | Springing | |

| Cut-off Date LTV Ratio(1) | 66.2% | Insurance | $0 | Springing | |

| Maturity Date LTV Ratio(1) | 66.2% | Replacement Reserve | $0 | $0 | |

| DSCR Based on Underwritten NOI / NCF(1) | 1.91x / 1.83x | TI / LC | $0 | $0 | |

| Debt Yield Based on Underwritten NOI / NCF(1) | 13.6% / 13.1% | Other(4) | $0 | Springing | |

| Sources and Uses | |||||||

| Sources | $ | % | Uses | $ | % | ||

| Whole Loan Amount | $172,000,000 | 65.4 | % | Purchase Price | $260,000,000 | 98.9 | % |

| Borrower Sponsor Equity | 90,443,933 | 34.4 | Closing Costs | 2,963,085 | 1.1 | ||

| Other Sources(5) | 519,152 | 0.2 | |||||

| Total Sources | $262,963,085 | 100.0 | % | Total Uses | $262,963,085 | 100.0 | % |

| (1) | Calculated based on the aggregate outstanding principal balance as of the Cut-off Date of the Seagate Campus Whole Loan (as defined below). |

| (2) | The Seagate Campus Mortgage Loan (as defined below) is part of the Seagate Campus Whole Loan, which is comprised of seven pari passu promissory notes with an aggregate original balance of $172,000,000. The Seagate Campus Whole Loan was co-originated by Citi Real Estate Funding Inc. (“CREFI”), UBS AG and Wells Fargo Bank, National Association (“WFBNA”). |

| (3) | See “—Escrows” below. |

| (4) | Other monthly reserves include a springing free rent reserve. See “—Escrows” below. |

| (5) | Other Sources consist of prorated rent of approximately $519,152 from May 24, 2023 through May 31, 2023. |

| ■ | The Mortgage Loan. The Seagate Campus mortgage loan (the “Seagate Campus Mortgage Loan”) is part of a whole loan (the “Seagate Campus Whole Loan”) secured by the borrower’s fee interest in a 574,775 SF research and development / advanced manufacturing industrial property located in Fremont, California (the “Seagate Campus Property”). The Seagate Campus Whole Loan is comprised of seven pari passu notes with an aggregate outstanding principal balance as of the Cut-off Date of $172,000,000. The Seagate Campus Mortgage Loan is evidenced by controlling Note A-1 and non-controlling Note A-2 and Note A-3, with an aggregate outstanding principal balance as of the Cut-off Date of $86,000,000, and represents approximately 9.5% of the Initial Pool Balance. |

The Seagate Campus Whole Loan was co-originated on May 24, 2023 by CREFI, UBS AG and WFBNA and accrues interest at a fixed rate of 7.04000% per annum. The Seagate Campus Whole Loan has an initial term of 120 months, a remaining term of 119 months and is interest-only for the full term. The scheduled maturity date of the Seagate Campus Whole Loan is June 6, 2033.

Voluntary prepayment of the Seagate Campus Whole Loan is prohibited prior to December 6, 2032 but may be freely prepaid in whole (but not in part) thereafter. Defeasance of the Seagate Campus Whole Loan in whole (but not in part) is permitted at any time after the earlier of (i) May 24, 2026 and (ii) the second anniversary of the closing date of the securitization that includes the last note of the Seagate Campus Whole Loan to be securitized.

| The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-262701) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Deutsche Bank Securities Inc., Goldman Sachs & Co. LLC, J.P. Morgan Securities LLC, Drexel Hamilton, LLC, Academy Securities, Inc. or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146. | ||

| 18 | ||

| LOAN #2: SEAGATE CAMPUS |

The table below summarizes the promissory notes that comprise the Seagate Campus Whole Loan. The relationship between the holders of the Seagate Campus Whole Loan is governed by a co-lender agreement as described under “Description of the Mortgage Pool—The Whole Loans—The Serviced Pari Passu Whole Loans” in the Preliminary Prospectus.”

| Whole Loan Summary | ||||||

| Note | Original Balance | Cut-off Date Balance | Note Holder | Controlling Piece | ||

| A-1 | $50,000,000 | $50,000,000 | Benchmark 2023-B39 | Yes | ||

| A-2 | 20,000,000 | 20,000,000 | Benchmark 2023-B39 | No | ||

| A-3 | 16,000,000 | 16,000,000 | Benchmark 2023-B39 | No | ||

| A-4 | 20,000,000 | 20,000,000 | BBCMS 2023-C20 | No | ||

| A-5-1 | 12,000,000 | 12,000,000 | BBCMS 2023-C20 | No | ||

| A-5-2 | 11,000,000 | 11,000,000 | UBS AG(1) | No | ||

| A-6 | 43,000,000 | 43,000,000 | WFBNA(1) | No | ||

| Whole Loan | $172,000,000 | $172,000,000 | ||||

| (1) | Expected to be contributed to one or more future securitization transactions. | |

| ■ | The Mortgaged Property. The Seagate Campus Property is a two-story, Class A, LEED-Gold Certified, research and development / advanced manufacturing facility totaling 574,775 SF and is situated on approximately 30.0-acres in Fremont, California. The Seagate Campus Property was built in 2010 and is 100.0% leased to Seagate Technology LLC (“Seagate”) (NASDAQ: STX). The Seagate Campus Property features 103,000 SF of class 10 to 1,000 clean rooms, a 260,000-gallon ultrapure water system, 21 kV of power, 6,000 tons of HVAC capacity, 25,000 SF of warehouse space, rooftop solar panels, a full-service cafeteria and an on-site fitness center. The warehouse space at the Seagate Campus Property features 24’ ceiling heights, 13 dock-high doors, one drive-in loading door, and six grade-level loading doors. The Seagate Campus Property has 705 parking stalls on site, resulting in a parking ratio of approximately 1.23 spaces per 1,000 SF. Seagate invested approximately $200,000,000 into the Seagate Campus Property in 2016 to construct the R&D labs and manufacturing clean rooms for their hard disk drive manufacturing operations. |

The sole tenant at the Seagate Campus Property is Seagate (574,775 SF; 100.0% of net rentable area; 100.0% of UW Base Rent). Founded in 1979, Seagate is a provider of data storage technology and infrastructure solutions. Seagate’s principal product is hard disk drives. Seagate also produces a range of data storage products including solid state drives, solid state hybrid drives, storage subsystems, and an edge-to-cloud mass data platform that includes data transfer shuttles and a storage-as-a-service cloud. Seagate has over 40,000 employees and uses the Seagate Campus Property as its operational headquarters.

Seagate’s lease at the Seagate Campus Property commenced in May 2023 and has a lease expiration in May 2028 with no termination options. Seagate is contractually obligated to renew its lease upon expiration of the initial five-year lease term and has two renewal options: (i) five years, with starting rent equal to the contractual fifth year rent plus 3.0%, with 3.0% annual increases thereafter, and, to the extent that Seagate elects such five-year extension option, Seagate will have a subsequent renewal option for ten years, or (ii) ten years, with rent to reset to the greater of (a) the contractual fifth year rent plus 3.0%, with 3.0% annual increases thereafter or (b) 90.0% of the then-fair market value rent, with 3.0% annual increases thereafter.

The following table presents certain information relating to the sole tenant at the Seagate Campus Property:

Sole Tenant Based on Underwritten Base Rent(1)

Tenant Name | Credit Rating (Fitch/MIS/S&P)(2) | Tenant GLA | % of GLA | UW Base Rent(3) | % of Total UW Base Rent(3) | UW Base Rent $ per SF(3) | Lease Expiration | Renewal / Extension Options | ||

| Seagate | BB+/Ba2/BB | 574,775 | 100.0% | $24,864,767 | 100.0% | $43.26 | 5/18/2028(4) | Various(4) | ||

| Total Occupied | 574,775 |

| 100.0% | $24,864,767 |

| 100.0% | $43.26 | |||

| Vacant Space | 0 | 0 | 0 | 0.0 | $0.00 | |||||

| Total / Wtd. Avg. | 574,775 |

| 100.0% | $24,864,767 |

| 100.0% | $43.26 | |||

| (1) | Based on the underwritten rent roll as of July 6, 2023. |

| (2) | Credit Ratings are those of the parent company whether or not the parent guarantees the lease. |

| (3) | UW Base Rent, % of Total UW Base Rent and UW Base Rent $ per SF include contractual rent steps totaling approximately $724,217 that are underwritten through June 1, 2024. |