EXHIBIT 1

| Daniel J. Donoghue | |||

| Managing Partner | |||

| 1 312 265 9605 | |||

| ddonoghue@thediscoverygroup.com |

March 4, 2010

The Board of Directors

c/o Mr. David M. Young, Corporate Secretary

TESSCO Technologies Incorporated

11126 McCormick Road

Hunt Valley, MD 21031

Dear Directors:

As you know, Discovery Group is a long-term investor in TESSCO Technologies, Inc. and is also the largest, non-management owner of the Company holding 14.2% of the outstanding stock. We are writing to bring to your attention certain inquiries we have received recently from private equity firms and large distribution companies interested in acquiring TESSCO.

It is unusual for a public shareholder to be contacted regarding such matters. These parties have told us that they have attempted on multiple occasions to contact Mr. Bob Barnhill, Chairman and Chief Executive Officer, to discuss possible transactions, and that they have received no constructive response. They have therefore contacted Discovery Group, as a significant TESSCO shareholder, in the hope that perhaps we could draw the Board’s attention to their interest.

Why Is TESSCO An Acquisition Target?

It is not surprising to learn that there is so much interest in a takeover of TESSCO Technologies. The Company operates in an attractive growth sector of the economy, has demonstrated profitability that we believe can be substantially improved through consolidation with a larger firm, and trades at an extremely cheap valuation in the public market.

The wireless industry is one of the most vibrant sectors of the economy and TESSCO is admirably positioned as the market-leading distributor of end-to-end wireless system products. TESSCO has a strong breadth and depth of product offerings. In its supply-chain function TESSCO is protected against the vagaries of technological obsolescence. For these reasons, large, wholesale, industrial distribution companies would benefit by adding TESSCO’s specialization to their business platforms.

Would-be acquirers of TESSCO also see an opportunity to create incremental value by optimizing procurement, storage, shipping and administration costs. Distribution businesses drive profitability through economies of scale. TESSCO is a relatively small distribution company, which in part accounts for its chronically sub-standard profitability. Publicly-traded distribution companies in comparable lines of business typically generate operating margins in the range of 5%.

Mr. David M. Young

March 4, 2010

Page 2

Over the past five years TESSCO’S operating margin averaged just 2%. In an industry where competitiveness is driven by efficiency, it is crippling for a company of TESSCO’s size to bear the sizable costs of public ownership. A combination with a larger organization would enhance TESSCO’s competitiveness leading to better service to customers, expanded career opportunities for employees and greater value to shareholders.

The business elements of TESSCO’s takeover appeal are complemented by its attractive (low) stock market valuation. Larger publicly-traded distribution companies trade at enterprise valuations of 7.5-10X EBITDA. Even after the recent run-up in TESSCO’s stock price, the public market valuation of the Company is only 5.1X our projected 2010 EBITDA. The difference between TESSCO’s valuation and that of its likely acquirers leaves plenty of room for a transaction that is both accretive to the purchaser and rewarding to TESSCO’s owners, simply based on the differences in valuation multiples, before taking into account any cost redundancies that can be eliminated immediately following a transaction.

Why Is TESSCO Shunned By The Stock Market?

Microcap stocks are chronically undervalued due to systemic issues associated with that segment of the public equity market but TESSCO’s situation is exacerbated by what we believe is poor corporate governance that casts an additional pall over its stock market valuation.

We define microcaps as companies that have market capitalization between $25-$500 million. TESSCO’s current market capitalization is approximately $100 million. Microcap companies make up 60% of the universe of all U.S. public companies. However, while microcaps are large in number, they only account for 3% of the market value of all publicly-traded firms. As a result, microcaps have a difficult time attracting Wall Street’s attention and very few maintain an appropriate valuation for their stock.

We further parse market capitalization data by breaking public companies into deciles, where the top decile is the largest 10% of the public companies and the 10th decile is the smallest 10 percent of public companies. TESSCO ranks in the 8th decile. Trading liquidity of public stocks becomes significantly impaired at about the 5th decile and below. Not coincidentally, valuations as measured by price-to-earnings multiples fall off precipitously after the 5th decile. So while most microcap companies suffer valuation discounts associated with their size, TESSCO’s situation is acutely problematic because it is small even by microcap standards.

Repeatedly, Discovery Group has presented this information to TESSCO’s management and its directors, petitioning them to consider alternative solutions that could boost shareholder value. It is our impression that management and the Board refuse to acknowledge the data and the implications for the Company’s owners. In our view, this failure, and the associated governance practices we discuss below, is interpreted by the stock market as evidence of management entrenchment. Management entrenchment is the intentional construction of barriers designed to protect management from losing control of the company. We believe that in the case of TESSCO, the negative stigma of management entrenchment extracts a substantial toll from the valuation of its shares.

Mr. David M. Young

March 4, 2010

Page 3

The evidence of this entrenchment can be found in the Board’s apparent apathy with respect to management’s missed operating targets, the Board’s adoption of anti-takeover mechanisms, the maintenance of staggered director terms that make it difficult for shareholders to recast the Board, and the repeated rebuffing of takeover overtures from well-financed strategic parties.

| ● | Missed Operating Targets. When Discovery Group first began investing in TESSCO in 2005, management had an operating plan, characterized by Mr. Barnhill as “taken to the Board”, that would improve operating margins to 4-5% and double earnings per share (“EPS”) every year for five years. The string of operating margins from 2005 to 2009 turned out to be; 2.0%, 1.8%, 2.5%, 1.6%, 2.3%. The 2005 EPS was $.92 and the 2009 EPS was $1.26. Obviously, management’s performance was woefully short of plan. It is our understanding that management has recently hatched a new plan to double revenues and double margins within a few short years. It is common practice among entrenched management teams to have an operating plan, often grandiose in scope, which can be used to defend against unwanted takeover inquiries. While we would be thrilled by such outstanding performance, the Board must not ignore the clear and relevant history of over-promising by this management team when evaluating shareholder alternatives. | |

| ● | Adoption of a “Poison Pill”. In 2008, the Board adopted a poison pill rights plan in response to the accumulation of 9.9% of TESSCO’s shares by Brightpoint, Inc. As a large distributor of cellular equipment, Brightpoint is a credible strategic acquirer of TESSCO. We believe that the threat that management might lose control of the Company to Brightpoint was the catalyst for establishing the poison pill. The Board’s action signaled to Brightpoint, and all other potential suitors, that the leadership at TESSCO was not amenable to a transaction. We believe the proper response would have been to engage in an exploratory dialogue with Brightpoint. At last year’s annual shareholder meeting we submitted a proposal to eliminate the poison pill. We demonstrated that TESSCO’s poison pill runs counter to modern corporate governance practices. Our proposal received the endorsement of Riskmetrics, the leading proxy advisor to institutional investors. An overwhelming 75% of non-management shareholders voted for our proposal yet the TESSCO Board ignored this important request of its constituency. |

Related links to Edgar Archive:

Discovery’s SEC Filing to Eliminate Poison Pill

www.sec.gov/Archives/edgar/data/927355/000110465909004863/a09-4099_1sc13da.htm

Discovery’s Letter to Board After Poison Pill Vote www.sec.gov/Archives/edgar/data/927355/000118811209001635/ex1.htm

| ● | Staggered Director Elections. For this year’s annual shareholder meeting, Discovery Group has submitted a proposal to eliminate TESSCO’s staggered director terms, so that each director must stand for reelection every year. Like the poison pill, TESSCO’s staggered board terms are not, in our view, consistent with good governance practices and trends among public companies. The best corrective action would be for the Board to embrace our proposal without putting it up for shareholder vote. |

Mr. David M. Young

March 4, 2010

Page 4

Discovery’s SEC Filing to Eliminate Staggered Director Elections

www.sec.gov/Archives/edgar/data/927355/000118811210000179/t67056_sc13da.htm

| ● | Rebuffing Takeover Overtures. Several well-intentioned and credible private equity firms and public corporations have contacted us to express their frustration about not being able to get a sincere response to their calls to Mr. Barnhill. They interpret Mr. Barnhill’s unresponsiveness as a clear signal that he is not interested in discussing potential transactions, regardless of the benefit to the public shareholders. The Board’s reaction to Brightpoint, which included the adoption of a poison pill and the “greenmail” tactic of repurchasing Brightpoint’s shares, pursuant to an offer that was not likewise extended to other shareholders, suggests that the Board stands behind Mr. Barnhill’s unresponsiveness. |

Discovery’s Letter to Board Regarding Brightpoint’s Interest

www.sec.gov/Archives/edgar/data/927355/000110465908044602/a08-18259_1ex1.htm

It is imperative that the Board recognizes that its position on these issues is transparent to the stock market. As demonstrated earlier in this letter, the competition for investor capital is fierce among public companies, and among microcaps in particular. TESSCO has an additional size disadvantage even among microcaps. On top of all that, what we believe amounts to a governance crisis at TESSCO essentially rules out a fair market valuation for its shares.

How Much Shareholder Value Is Being Forsaken?

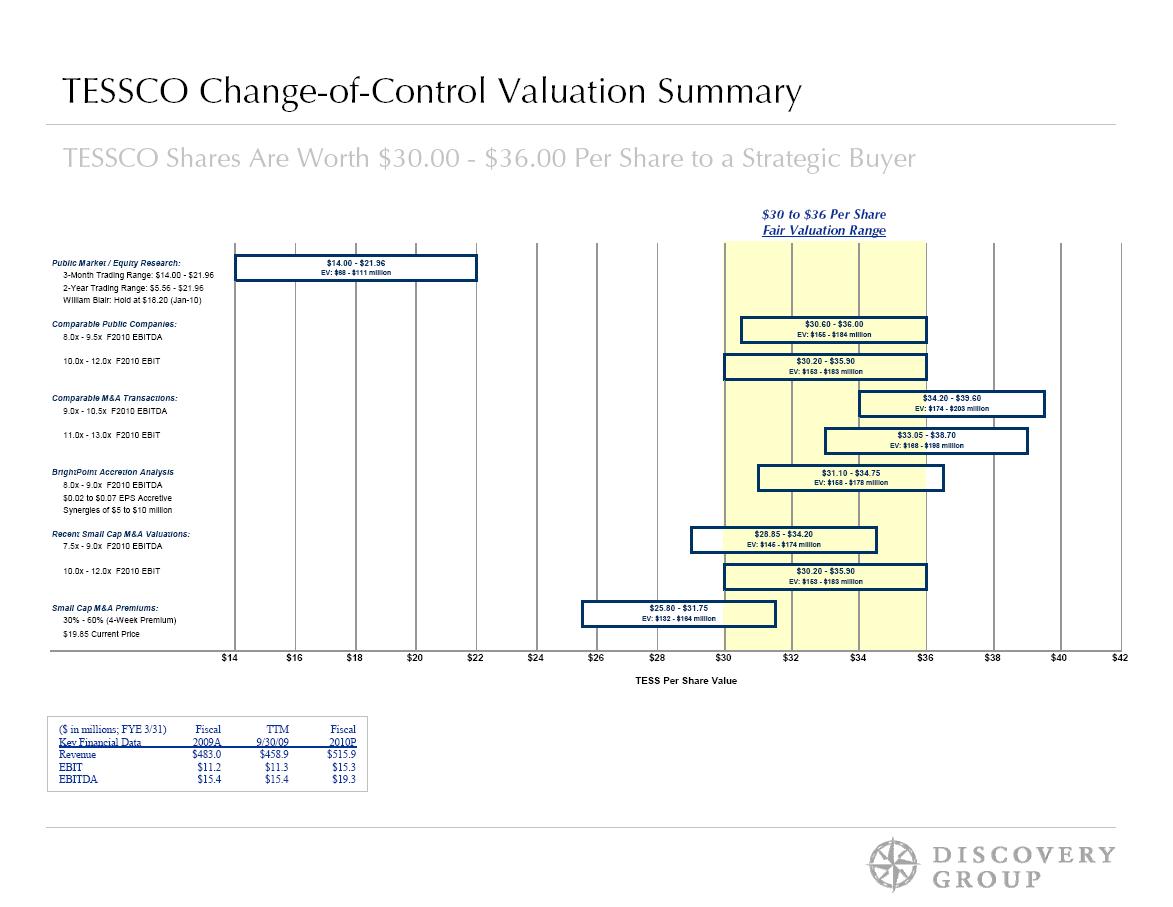

At a meeting at the TESSCO offices on January 20, 2010 with Mr. Barnhill and Mr. John Beletic, lead Director, Discovery Group presented specific quantitative data that predicts the valuation TESSCO would obtain in a competitive company sale process. The analysis is based on conventional investment banking methodology as the principals at Discovery Group are former investment bankers with considerable expertise in the field of mergers and acquisitions. A current summary of the work is provided in an appendix to this letter.

At the time of this writing, the TESSCO share price of $19.96 reflects a total enterprise value of $99.6 million, after taking into account the Company’s cash, debt, and fully-diluted shares. Discovery Group projects that earnings before interest, taxes, and depreciation (“EBITDA”) for fiscal 2010, which ends March 31, 2010, will be $19.3 million. Thus, TESSCO trades at only 5.1 times our projected fiscal 2010 EBITDA.

It is interesting to note that the historical range of TESSCO’s EBITDA valuation over the past 10 years has a median of 6.0X. While that historical valuation is low relative to industry standards, TESSCO shares are currently trading at a discount to its own historical norm. We suspect that the actions of the Board in discouraging expressions of interest from potential suitors and not addressing other serious governance shortcomings has pushed away enough investors as to cause the excessively depressed valuation of late.

Mr. David M. Young

March 4, 2010

Page 5

Discovery Group‘s change-of-control valuation indicates that TESSCO’s shares are worth between $30-$36. That conclusion is based on a comprehensive set of quantitative valuation criteria and assumes a professionally managed process for identifying ownership alternatives. Among other things, we analyzed comparable public company valuations, comparable M&A transactions in the industry, recent small-cap M&A valuations, recent premiums paid relative to pre-existing stock prices for public, small-cap takeovers, and an accretion/dilution analysis with Brightpoint, Inc.

As to the process, the key to obtaining full shareholder value is to move TESSCO from an inefficient public marketplace, where micro-caps are ignored and valuations are steeply discounted, to a more competitive private marketplace, where bidders can readily compute the true economic value that can be obtained through complete ownership and assimilation of a business. It is critical, therefore, that potential suitors for TESSCO not be discouraged but rather embraced and ultimately organized into an open and fair process. We are concerned that the defensive approach that TESSCO management has taken toward potential bidders in the past will leave the impression that management would never cooperate in a sale to those or other parties in the future.

It is, therefore, incumbent on the Board to address the opportunity to engage with interested acquirers of TESSCO given the large financial opportunity for its owners. We strongly believe, on the basis of comprehensive and relevant analysis, that a company sale would yield at least a 50% premium for shareholders relative to the current market valuation. Discovery Group is concerned, however, that Mr. Barnhill’s sway over this Board, as well as the directors’ own lack of incentives to maximize shareholder value, stand in the way of proper and assertive Board action.

What Is Motivating Board Complacency?

The governance crisis at TESSCO is a textbook case of misalignment of incentives and conflicts of interest. TESSCO’s non-management directors have personally invested their own funds in an inconsequential amount of stock while enjoying significant cash compensation and other prerequisites. The most current SEC filings indicate that non-management directors have beneficial ownership in 5.3% of the outstanding TESSCO shares. However, excluding equity securities that the directors essentially gave each other, at the expense of the public shareholders, the ownership level is not even 1%. Even more discouraging, the ownership level would be higher except that many of the directors have sold vested equity awards in the past.

A perfect example is Mr. Dennis J. Shaughnessy, one of the two directors that will likely be standing for re-election at this year’s annual shareholder meeting. According to SEC filings, Mr. Shaughnessy has beneficial ownership of 27,068 TESSCO common shares. However, a closer analysis of the data reveals that none of those shares was purchased in the open market by Mr. Shaughnessy. We can find no record of Mr. Shaughnessy ever buying a share of TESSCO stock with his own funds. All his TESSCO shares have been given to him by the Company. Mr. Shaughnessy has been a director since 1989 and over that period we estimate that he has collected roughly $500,000 in cash directors’ fees, in addition to perhaps another half million dollars worth of stock awards, yet has never cared to reinvest any of the cash remuneration back into the Company’s stock. Further, Mr. Shaughnessy has actually sold some of his awarded stock.

Mr. David M. Young

March 4, 2010

Page 6

This lack of personal investment suggests to us that Mr. Shaughnessy may not believe in TESSCO’s prospects, may not consider the stock undervalued, and may not be the best person to represent the interests of shareholders like Discovery Group that put their capital at risk in this Company.

Interestingly, the only other director standing for reelection this year is Mr. Jay G. Baitler. Mr. Baitler has been a director since 2007 and has been employed since 1995 by Staples, Inc. Staples has exceptional governance standards outlined in a straightforward and accessible Corporate Governance statement in its annual proxy. Unlike TESSCO, Staples does not have a staggered Board, does not have a poison pill, requires minimum levels of equity ownership by its directors, and requires that directors be elected by a majority of the shareholders. It must be challenging for Mr. Baitler to reconcile Staples’ approach to stewardship, which is very shareholder-focused, with that of TESSCO, which seems to us so blatantly management-centric.

It is worth mentioning at this point that at the upcoming 2010 annual meeting of TESSCO shareholders, Discovery Group plans to withhold its votes for Messrs. Shaughnessy and Baitler due to our view that they have demonstrated a lack of regard for the interests of non-management shareholders.

Mr. Barnhill, the Chairman and Chief Executive Officer, greatly augments the insider ownership of the TESSCO Board. But therein lies the problem, we believe. Mr. Barnhill appears to exert tremendous influence over the Board but he has personal interests at stake in any proposed sale of the Company that may not be consistent with the public shareholders, including a history of what we view as exorbitant personal compensation as well as employment benefits for several family members. Total compensation for Mr. Barnhill shown in last year’s proxy statement was $1.6 million, which we consider egregiously higher than the median CEO compensation of $625,000 for the public companies in TESSCO’s 8th decile size range. It is probably not a coincidence that TESSCO directors receive compensation that is substantially higher than directors at similarly-sized public companies. The Company has also employed Mr. Barnhill’s wife and son, as reported in the 2008 proxy statement. Meanwhile, Mr. Barnhill uses his large stock position to vote counter to the great majority of the public shareholders on matters like the poison pill, which he led the Board to adopt in the face of a takeover threat that could have cost him these benefits.

In both a great irony and a great insult to shareholders, Mr. Barnhill is a steady seller of TESSCO stock, which puts pressure on an already illiquid market and destabilizes investor confidence in the Company, yet his ownership stake is regularly replenished through equity securities given to him by the Board. Apparently the Board does not appreciate the illogic of using equity incentives to motivate a CEO that is selling stock.

In the face of an extremely low Company valuation and multiple expressions of acquisition interest by credible parties, the time is long past due for this Board of Directors to put aside these various conflicts and disincentives in order to properly fulfill its fiduciary duty.

Our Recommendation: Immediately Hire an Investment Banker

When a company is the subject of takeover interest, and its directors and management have potential conflicts of interest in considering those expressions of interest, there is a well-established protocol to address the situation. Public companies with well meaning and well

Mr. David M. Young

March 4, 2010

Page 7

advised Boards sort out these matters by forming a special committee of the Board comprised of only independent directors. That Special Independent Committee typically engages its own advisers, both legal and financial.

A nationally-recognized investment banking firm is then charged with coordinating a dialogue between the Special Independent Committee and TESSCO’s potential suitors. At the conclusion of the process the investment banker will have adequate information to advise the Special Independent Committee, and ultimately the Board, on the best course of action for all its shareholders, which may be to sell the company or to continue to operate independently. Please notice that there is no downside to such a process. The Board maintains flexibility in charting the proper course for the Company and the directors are endowed with significantly more information with which to do so.

As the largest non-management shareholder in TESSCO, Discovery Group considers any expression of interest in acquiring TESSCO to be friendly and believes that other public shareholders would likewise want management to be responsive to inquiries. It is only management’s rebuffing of expressions of interest, without appropriate consideration by disinterested directors, which we find to be hostile to the Company’s owners. Until the Board takes the corrective action of forming a Special Independent Committee and engaging an investment banker, Discovery Group will continue to make the Board aware of any opportunities to enhance shareholder value, including any expressions of interest from potential suitors that we learn are meeting resistance from management.

Respectfully submitted,

DISCOVERY GROUP, LLC.

/s/ Daniel J. Donoghue

Daniel J. Donoghue

Managing Member

TESSCO Change-of-Control Valuation Summary TESSCO Shares Are Worth $30.00 -$36.00 Per Share to a Strategic Buyer$30 to $36 Per Share Fair Valuation Range Public Market / Equity Research: 3-Month Trading Range: $14.00 - $21.96 2-Year Trading Range: $5.56 - $21.96 William Blair: Hold at $18.20 (Jan-10) $14.00 - $21.96EV: $68 - $111 million Comparable Public Companies: 8.0x - 9.5x F2010 EBITDA $30.60 - - $36.00EV: $155 - $184 million 10.0x - 12.0x F2010 EBIT $30.20 - $35.90 EV: $153 - $183 million Comparable M&A Transactions: 9.0x - 10.5x F2010 EBITDA $34.20 -$39.60EV: $174 - $203 million 11.0x - 13.0x F2010 EBIT $33.05 -$38.70 EV: $168 - $198 million BrightPoint Accretion Analysis 8.0x - 9.0x F2010 EBITDA $0.02 to $0.07 EPS Accretive Synergies of $5 to $10 million $31.10 - $34.75EV: $158 - $178 million Recent Small Cap M&A Valuations: 7.5x - 9.0x F2010 EBITDA $28.85 - $34.20EV: $145 - $174 million 10.0x - 12.0x F2010 EBIT $30.20 - $35.90 EV: $153 - $183 million Small Cap M&A Premiums: 30% - 60% (4-Week Premium) $19.85 Current Price $25.80 - $31.75EV: $132 - $164 million$14 $16 $18 $20 $22 $24 $26 $28 $30 $32 $34 $36 $38 $40 $42 TESS Per Share Value ($ in millions; FYE 3/31) Fiscal TTM Fiscal Key Financial Data 2009A 9/30/09 2010P Revenue $483.0 $458.9 $515.9 EBIT $11.2 $11.3 $15.3 EBITDA $15.4 $15.4 $19.3