UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

(RULE 14a-101)

INFORMATION REQUIRED IN PROXY STATEMENT

SCHEDULE 14A INFORMATION

PROXY STATEMENT PURSUANT TO SECTION 14(a) OF THE

SECURITIES EXCHANGE ACT OF 1934

| Filed by the Registrant | x | |

| Filed by a Party other than the Registrant | ¨ |

Check the appropriate box:

| ¨ | Preliminary Proxy Statement | |

| ¨ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) | |

| ¨ | Definitive Proxy Statement | |

| x | Definitive Additional Materials | |

| ¨ | Soliciting Material Pursuant to Rule 14a-11(c) or Rule 14a-12 |

TICC Capital Corp.

(Name of Registrant as Specified in Its Charter)

(Name of Person(s) Filing Proxy Statement if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

| x | No fee required. | |||

| ¨ | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. | |||

| (1) | Title of each class of securities to which transaction applies: | |||

| (2) | Aggregate number of securities to which transaction applies: | |||

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (Set forth the amount on which the filing fee is calculated and state how it was determined): | |||

| (4) | Proposed maximum aggregate value of transaction: | |||

| (5) | Total fee paid: | |||

| ¨ | Fee paid previously with preliminary materials. | |||

| ¨ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the form or schedule and the date of its filing. | |||

| (1) | Amount previously Paid: | |||

| (2) | Form, schedule or registration statement No.: | |||

| (3) | Filing party: | |||

| (4) | Date filed: | |||

TICC Capital Corp. (the "Company") has filed with the Securities and Exchange Commission (the “SEC”), and disseminated to its stockholders, a proxy statement and accompanying WHITE proxy card to be used to solicit votes for the Company's proposal to approve a new advisory agreement between the Company and TICC Management, LLC, to take effect upon a change of control of TICC Management, LLC, and certain related proposals, at a special meeting of stockholders of the Company scheduled to be held on October 27, 2015.

On October 9, 2015, representatives of the Company will give a presentation to representatives of Institutional Shareholder Services Inc. regarding the Company (the "ISS Presentation"). Slides for the ISS Presentation are attached hereto.

October 2015 Investor Presentation

2 Additional Information and Where to Find It In connection with the approval of the proposed new investment advisory agreement with Benefit Street Partners L.L.C. (“BSP”), TICC Capital Corp. ("TICC", "TICC Capital", the "Company", "us", "we" or "our") has filed relevant materials with the SEC, including a definitive proxy statement on Schedule 14A. The Company has distributed the definitive proxy statement and a proxy card to each stockholder entitled to vote at the special meeting relating to the approval of the proposed new investment advisory agreement and the election of six directors nominated by the Company. INVESTORS AND SECURITY HOLDERS OF THE COMPANY ARE URGED TO READ THESE MATERIALS (INCLUDING ANY AMENDMENTS OR SUPPLEMENTS THERETO), AND ANY OTHER RELEVANT DOCUMENTS IN CONNECTION WITH THE APPROVAL OF THE PROPOSED NEW INVESTMENT ADVISORY AGREEMENT AND THE APPROVAL OF ITS DIRECTOR NOMINEES THAT THE COMPANY FILES WITH THE SEC, BECAUSE THESE MATERIALS CONTAIN IMPORTANT INFORMATION ABOUT THE COMPANY AND THE APPROVAL OF THESE MATTERS. The definitive proxy statement and other relevant materials in connection with the approval of these matters, and any other documents filed by the Company with the SEC, may be obtained free of charge at the SEC's website (http://www.sec.gov), at the Company's website (http://www.ticc.com), or by writing to the Company at 8 Sound Shore Drive, Suite 255, Greenwich, CT 06830 (telephone number 203- 983-5275). Participants in the Solicitation The Company and its directors and executive officers may be deemed to be participants in the solicitation of proxies from the Company's stockholders with respect to the approval of the proposed new investment advisory agreement and the election of six directors nominated by the Company. Information about the Company's directors and executive officers and their ownership of the Company's common stock is set forth in the proxy statement on Schedule 14A filed with the SEC on September 3, 2015, and the Annual Report on Form 10-K for the fiscal year ended December 31, 2014. Information regarding the identity of the potential participants, and their direct or indirect interests in the approval of the proposed new investment advisory agreement, by security holdings or otherwise, are set forth in the proxy statement and other materials filed or to be filed with SEC in connection therewith. Forward Looking Statements This press release contains forward-looking statements subject to the inherent uncertainties in predicting future results and conditions. Any statements that are not statements of historical fact (including statements containing the words "believes," "plans," "anticipates," "expects," "estimates" and similar expressions) should also be considered to be forward-looking statements. Certain factors could cause actual results and conditions to differ materially from those projected in these forward-looking statements. These factors are identified from time to time in our filings with the Securities and Exchange Commission. We undertake no obligation to update such statements to reflect subsequent events.

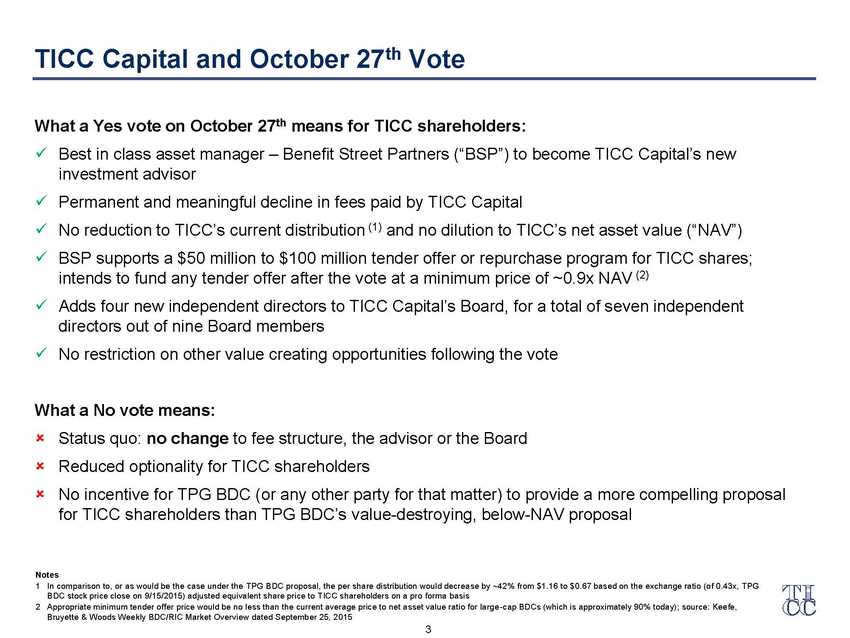

3 What a Yes vote on October 27th means for TICC shareholders: „Ï Best in class asset manager ¡V Benefit Street Partners (¡§BSP¡¨) to become TICC Capital¡¦s new investment advisor „Ï Permanent and meaningful decline in fees paid by TICC Capital „Ï No reduction to TICC¡¦s current distribution (1) and no dilution to TICC¡¦s net asset value (¡§NAV¡¨) „Ï BSP supports a $50 million to $100 million tender offer or repurchase program for TICC shares; intends to fund any tender offer after the vote at a minimum price of ~0.9x NAV (2) „Ï Adds four new independent directors to TICC Capital¡¦s Board, for a total of seven independent directors out of nine Board members „Ï No restriction on other value creating opportunities following the vote What a No vote means: „Î Status quo: no change to fee structure, the advisor or the Board „Î Reduced optionality for TICC shareholders „Î No incentive for TPG BDC (or any other party for that matter) to provide a more compelling proposal for TICC shareholders than TPG BDC¡¦s value-destroying, below-NAV proposal TICC Capital and October 27th Vote Notes 1 In comparison to, or as would be the case under the TPG BDC proposal, the per share distribution would decrease by ~42% from $1.16 to $0.67 based on the exchange ratio (of 0.43x, TPG BDC stock price close on 9/15/2015) adjusted equivalent share price to TICC shareholders on a pro forma basis 2 Appropriate minimum tender offer price would be no less than the current average price to net asset value ratio for large-cap BDCs (which is approximately 90% today); source: Keefe, Bruyette & Woods Weekly BDC/RIC Market Overview dated September 25, 2015

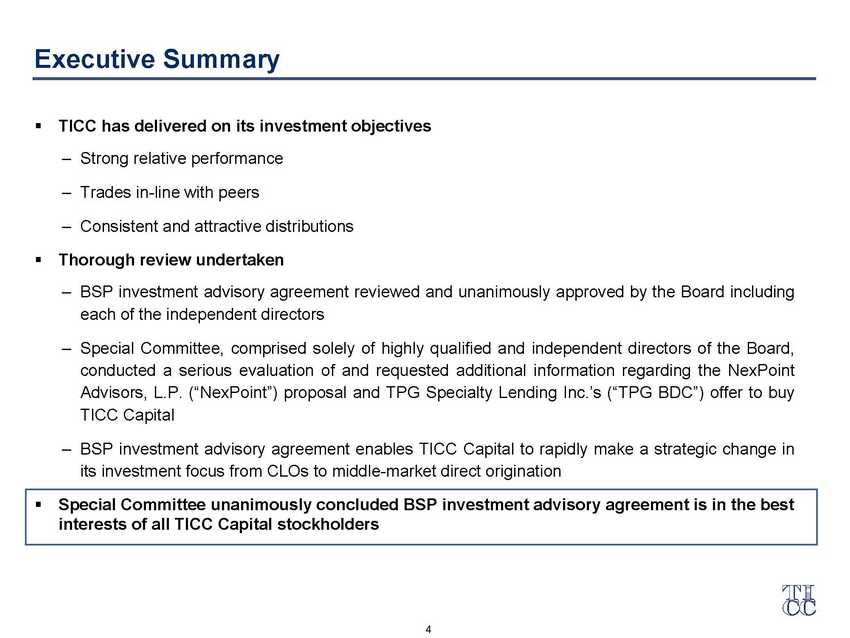

4 „X TICC has delivered on its investment objectives ¡V Strong relative performance ¡V Trades in-line with peers ¡V Consistent and attractive distributions „X Thorough review undertaken ¡V BSP investment advisory agreement reviewed and unanimously approved by the Board including each of the independent directors ¡V Special Committee, comprised solely of highly qualified and independent directors of the Board, conducted a serious evaluation of and requested additional information regarding the NexPoint Advisors, L.P. (¡§NexPoint¡¨) proposal and TPG Specialty Lending Inc.¡¦s (¡§TPG BDC¡¨) offer to buy TICC Capital ¡V BSP investment advisory agreement enables TICC Capital to rapidly make a strategic change in its investment focus from CLOs to middle-market direct origination „X Special Committee unanimously concluded BSP investment advisory agreement is in the best interests of all TICC Capital stockholders Executive Summary

5 „X Completed IPO in November 2003 as Technology Investment Capital Corp. ¡V Newly formed Business Development Company (¡§BDC¡¨) ¡V Initially created to invest in the debt and/or equity securities of technology-related companies ¡V Raised $150 million „X TICC Capital today: ¡V $956 million portfolio composed of 96 portfolio company and CLO investments ¡V 70% of the portfolio is in senior secured debt ¡V No investments on non-accrual ¡V Investment portfolio marked to fair market value „X Since IPO, TICC has paid $12.01 per share in total distributions to investors { Represents approximately 1.4x TICC¡¦s current NAV per share TICC Capital¡¦s History

6 TICC Has Performed Favorably Relative to its BDC Peers 7-Year Total Return Comparison ¡V TICC Has Outperformed Average = 12% (%) Price / NAV Differential: TICC vs. Pre-2007 BDC IPO Peers (1) (20%) 0% 20% 40% 60% Oct-10 Apr-11 Oct-11 Apr-12 Oct-12 May-13 Nov-13 May-14 Nov-14 May-15 „X TICC has traded at a 5-year average Price / NAV of 0.99x versus other pre-2007 BDC IPO peers (1) at 0.88x, demonstrating the prudent management approach of TICC¡¦s investment advisor „X TICC has outperformed TPG BDC from a total returns perspective in three of the last six quarters (since TPG BDC¡¦s IPO) TICC Pre-2007 BDC IPO Peers (1) (%) (2) (1) Source: SNL Financial; market data as of 10/6/2015 Notes 1 Represents BDCs that went public before 1/1/2007; includes ACAS, AINV, ARCC, BKCC, CSWC, EQS, GAIN, GLAD, HTGC, KCAP, MVC, OHAI, PNNT, PSEC, RAND, SAR, TAXI, TCAP and TINY 2 Includes externally-managed BDCs and is based on medians. Peer group includes ABDC, AINV, ARCC, BKCC, CMFN, CPTA, FDUS, FSC, FSIC, FULL, GAIN, GARS, GBDC, GLAD, GSBD, HCAP, HRZN, MCC, MRCC, MVC, NMFC, OFS, OHAI, PNNT, PSEC, SAR, SCM, SLRC, TCPC, TCRD, TSLX, TPVG and WHF TICC has traded at a 12% average Price / NAV premium to peers over the last 5 years 20% 47% 338% 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% Externally Managed BDC Peers Pre-2007 BDC IPO Peers TICC

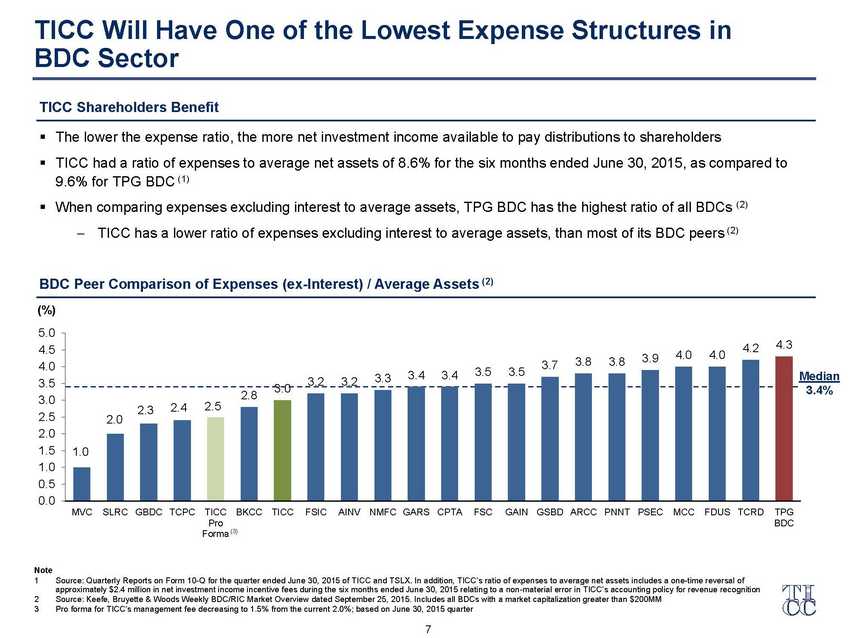

7 TICC Will Have One of the Lowest Expense Structures in BDC Sector „X The lower the expense ratio, the more net investment income available to pay distributions to shareholders „X TICC had a ratio of expenses to average net assets of 8.6% for the six months ended June 30, 2015, as compared to 9.6% for TPG BDC (1) „X When comparing expenses excluding interest to average assets, TPG BDC has the highest ratio of all BDCs (2) { TICC has a lower ratio of expenses excluding interest to average assets, than most of its BDC peers (2) TICC Shareholders Benefit Note 1 Source: Quarterly Reports on Form 10-Q for the quarter ended June 30, 2015 of TICC and TSLX. In addition, TICC¡¦s ratio of expenses to average net assets includes a one-time reversal of approximately $2.4 million in net investment income incentive fees during the six months ended June 30, 2015 relating to a non-material error in TICC¡¦s accounting policy for revenue recognition 2 Source: Keefe, Bruyette & Woods Weekly BDC/RIC Market Overview dated September 25, 2015. Includes all BDCs with a market capitalization greater than $200MM 3 Pro forma for TICC¡¦s management fee decreasing to 1.5% from the current 2.0%; based on June 30, 2015 quarter (%) BDC Peer Comparison of Expenses (ex-Interest) / Average Assets (2) 1.0 2.0 2.3 2.4 2.5 2.8 3.0 3.2 3.2 3.3 3.4 3.4 3.5 3.5 3.7 3.8 3.8 3.9 4.0 4.0 4.2 4.3 0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0 4.5 5.0 MVC SLRC GBDC TCPC TICC Pro Forma BKCC TICC FSIC AINV NMFC GARS CPTA FSC GAIN GSBD ARCC PNNT PSEC MCC FDUS TCRD TPG BDC (3) Median 3.4%

BSP Agreement: TICC Process & Considerations

9 „X In accordance with the Section 15 of the 1940 Act, TICC¡¦s Board thoroughly reviewed BSP¡¦s proposal in July and carefully evaluated the potential benefits to stockholders „X TICC¡¦s Board carefully evaluated the following information related to BSP¡¦s proposal: { BSP's expertise in credit origination and investment, and the ability to leverage that knowledge to make a strategic change in TICC Capital's investment focus away from CLOs { Comparative data with respect to services and the advisory fees paid to investment advisers of other BDCs { Questionnaires completed and extensive materials provided by BSP in response to the Board¡¦s requests { BSP¡¦s operations and financial conditions, including its $10 billion of assets under management { BSP¡¦s philosophy of management, historical performance and methods of operation { The favorable performance record of BSP and the quality of services { Education and experience of BSP¡¦s 60 investment and research professionals { The base management fees and incentive fees associated with the BSP agreement { The expected profitability of BSP¡¦s affiliate in relation to the services „X The non-interested directors consulted with independent legal counsel regarding the approval of the BSP agreement „X Ultimately, the Board of Directors determined that the BSP agreement was in the best interests of the Company and its stockholders The Review Undertaken to Protect Stockholder Interests

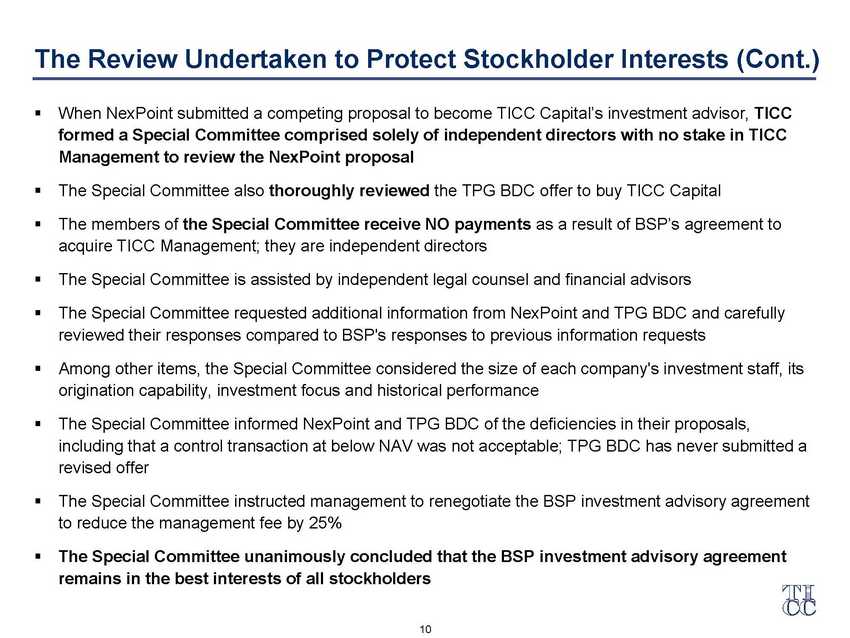

10 „X When NexPoint submitted a competing proposal to become TICC Capital¡¦s investment advisor, TICC formed a Special Committee comprised solely of independent directors with no stake in TICC Management to review the NexPoint proposal „X The Special Committee also thoroughly reviewed the TPG BDC offer to buy TICC Capital „X The members of the Special Committee receive NO payments as a result of BSP¡¦s agreement to acquire TICC Management; they are independent directors „X The Special Committee is assisted by independent legal counsel and financial advisors „X The Special Committee requested additional information from NexPoint and TPG BDC and carefully reviewed their responses compared to BSP's responses to previous information requests „X Among other items, the Special Committee considered the size of each company's investment staff, its origination capability, investment focus and historical performance „X The Special Committee informed NexPoint and TPG BDC of the deficiencies in their proposals, including that a control transaction at below NAV was not acceptable; TPG BDC has never submitted a revised offer „X The Special Committee instructed management to renegotiate the BSP investment advisory agreement to reduce the management fee by 25% „X The Special Committee unanimously concluded that the BSP investment advisory agreement remains in the best interests of all stockholders The Review Undertaken to Protect Stockholder Interests (Cont.)

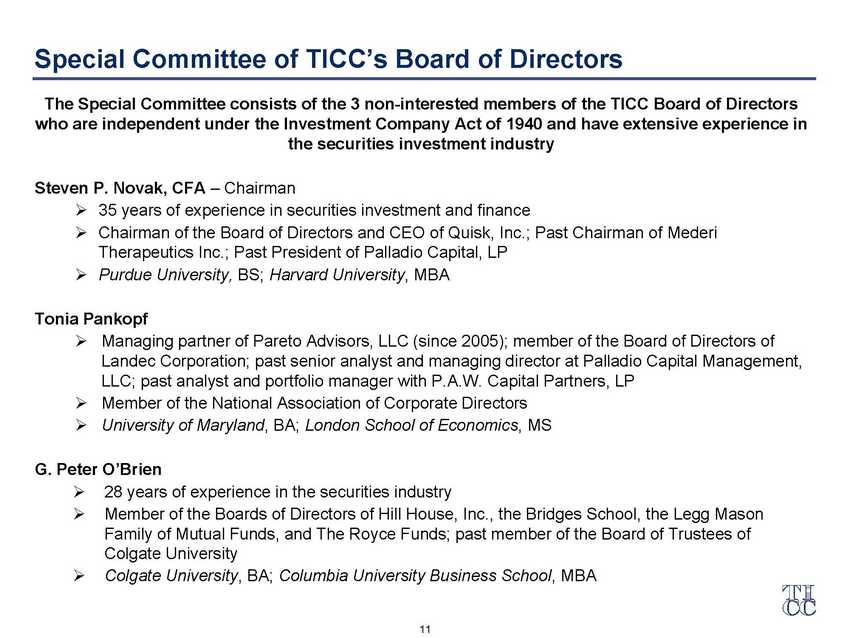

11 The Special Committee consists of the 3 non-interested members of the TICC Board of Directors who are independent under the Investment Company Act of 1940 and have extensive experience in the securities investment industry Steven P. Novak, CFA ¡V Chairman „« 35 years of experience in securities investment and finance „« Chairman of the Board of Directors and CEO of Quisk, Inc.; Past Chairman of Mederi Therapeutics Inc.; Past President of Palladio Capital, LP „« Purdue University, BS; Harvard University, MBA Tonia Pankopf „« Managing partner of Pareto Advisors, LLC (since 2005); member of the Board of Directors of Landec Corporation; past senior analyst and managing director at Palladio Capital Management, LLC; past analyst and portfolio manager with P.A.W. Capital Partners, LP „« Member of the National Association of Corporate Directors „« University of Maryland, BA; London School of Economics, MS G. Peter O¡¦Brien „« 28 years of experience in the securities industry „« Member of the Boards of Directors of Hill House, Inc., the Bridges School, the Legg Mason Family of Mutual Funds, and The Royce Funds; past member of the Board of Trustees of Colgate University „« Colgate University, BA; Columbia University Business School, MBA Special Committee of TICC¡¦s Board of Directors

12 BSP Agreement is the Right Outcome for TICC Shareholders BSP is a World Class Manager TICC Fees Will Decrease Under the BSP Agreement Notes 1 Returns referenced are for BSP¡¦s three private debt flagship funds and do not account for returns of certain clients BSP has determined are not managed in a substantially similar manner to its three private debt flagship funds; past performance is not a guarantee of future results ¡V any investment entails a risk of loss 2 Source: Keefe, Bruyette & Woods Weekly BDC/RIC Market Overview dated September 25, 2015 3 In comparison to, or as would be the case under the TPG BDC proposal, the per share distribution would decrease by ~42% from $1.16 to $0.67 based on the exchange ratio (of 0.43x, TPG BDC stock price close on 9/15/2015) adjusted equivalent share price to TICC shareholders on a pro forma basis „Ï BSP is a world class credit manager with over $10 billion of assets under management, achieving superior investment performance (1) at their existing private debt funds while utilizing substantially less leverage than the BDC industry average (2) „Ï NO reduction to TICC¡¦s current distribution (3) and NO dilution to TICC¡¦s NAV „Ï Substantially lower management fees and larger investment staff „Ï Superior loan origination capability: BSP committed to a more diversified and higher yielding portfolio over time for TICC „Ï BSP has spent more than 9 months in due diligence studying the TICC portfolio to find opportunities for increasing value „Ï BSP plans to attract meaningful institutional ownership into TICC's shareholder base

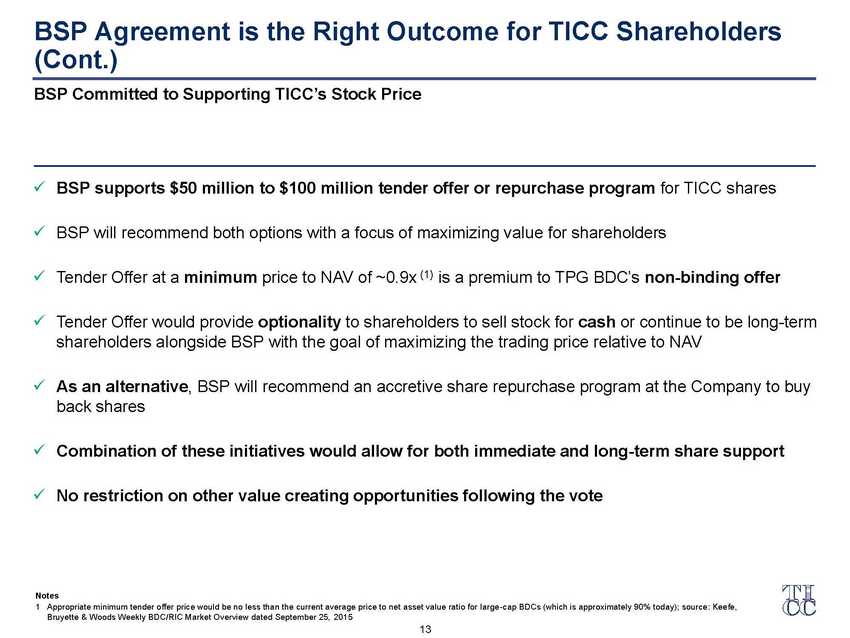

13 BSP Agreement is the Right Outcome for TICC Shareholders (Cont.) Notes 1 Appropriate minimum tender offer price would be no less than the current average price to net asset value ratio for large-cap BDCs (which is approximately 90% today); source: Keefe, Bruyette & Woods Weekly BDC/RIC Market Overview dated September 25, 2015 „Ï BSP supports $50 million to $100 million tender offer or repurchase program for TICC shares „Ï BSP will recommend both options with a focus of maximizing value for shareholders „Ï Tender Offer at a minimum price to NAV of ~0.9x (1) is a premium to TPG BDC¡¦s non-binding offer „Ï Tender Offer would provide optionality to shareholders to sell stock for cash or continue to be long-term shareholders alongside BSP with the goal of maximizing the trading price relative to NAV „Ï As an alternative, BSP will recommend an accretive share repurchase program at the Company to buy back shares „Ï Combination of these initiatives would allow for both immediate and long-term share support „Ï No restriction on other value creating opportunities following the vote BSP Committed to Supporting TICC¡¦s Stock Price

TICC’s Agreement with BSP is Far Superior to TPG BDC’s Self-Serving Proposal

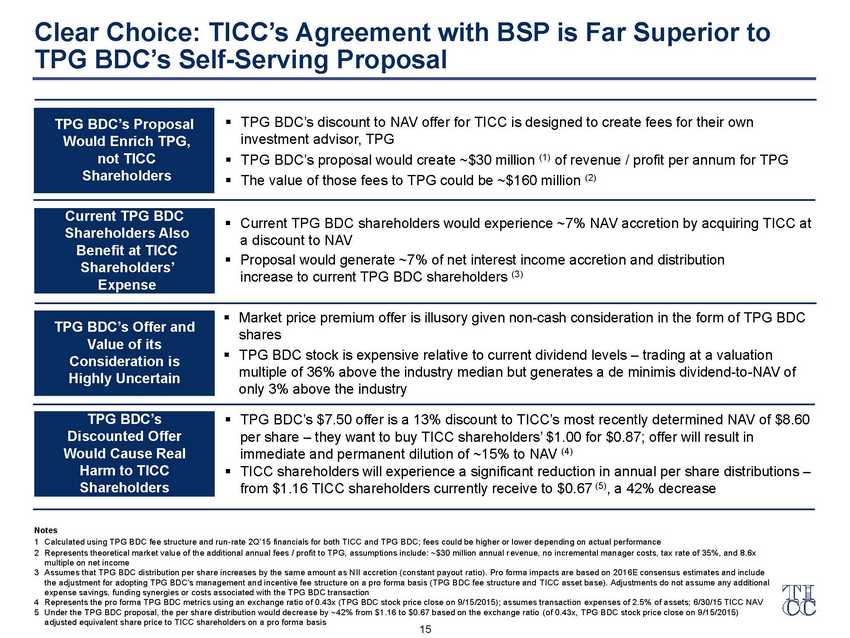

15 Clear Choice: TICC¡¦s Agreement with BSP is Far Superior to TPG BDC¡¦s Self-Serving Proposal TPG BDC¡¦s Proposal Would Enrich TPG, not TICC Shareholders „X Current TPG BDC shareholders would experience ~7% NAV accretion by acquiring TICC at a discount to NAV „X Proposal would generate ~7% of net interest income accretion and distribution increase to current TPG BDC shareholders (3) TPG BDC¡¦s Offer and Value of its Consideration is Highly Uncertain „X TPG BDC¡¦s $7.50 offer is a 13% discount to TICC¡¦s most recently determined NAV of $8.60 per share ¡V they want to buy TICC shareholders¡¦ $1.00 for $0.87; offer will result in immediate and permanent dilution of ~15% to NAV (4) „X TICC shareholders will experience a significant reduction in annual per share distributions ¡V from $1.16 TICC shareholders currently receive to $0.67 (5), a 42% decrease Notes 1 Calculated using TPG BDC fee structure and run-rate 2Q¡¦15 financials for both TICC and TPG BDC; fees could be higher or lower depending on actual performance 2 Represents theoretical market value of the additional annual fees / profit to TPG, assumptions include: ~$30 million annual revenue, no incremental manager costs, tax rate of 35%, and 8.6x multiple on net income 3 Assumes that TPG BDC distribution per share increases by the same amount as NII accretion (constant payout ratio). Pro forma impacts are based on 2016E consensus estimates and include the adjustment for adopting TPG BDC¡¦s management and incentive fee structure on a pro forma basis (TPG BDC fee structure and TICC asset base). Adjustments do not assume any additional expense savings, funding synergies or costs associated with the TPG BDC transaction 4 Represents the pro forma TPG BDC metrics using an exchange ratio of 0.43x (TPG BDC stock price close on 9/15/2015); assumes transaction expenses of 2.5% of assets; 6/30/15 TICC NAV 5 Under the TPG BDC proposal, the per share distribution would decrease by ~42% from $1.16 to $0.67 based on the exchange ratio (of 0.43x, TPG BDC stock price close on 9/15/2015) adjusted equivalent share price to TICC shareholders on a pro forma basis Current TPG BDC Shareholders Also Benefit at TICC Shareholders¡¦ Expense „X Market price premium offer is illusory given non-cash consideration in the form of TPG BDC shares „X TPG BDC stock is expensive relative to current dividend levels ¡V trading at a valuation multiple of 36% above the industry median but generates a de minimis dividend-to-NAV of only 3% above the industry TPG BDC¡¦s Discounted Offer Would Cause Real Harm to TICC Shareholders „X TPG BDC¡¦s discount to NAV offer for TICC is designed to create fees for their own investment advisor, TPG „X TPG BDC¡¦s proposal would create ~$30 million (1) of revenue / profit per annum for TPG „X The value of those fees to TPG could be ~$160 million (2)

16 TPG BDC¡¦s Proposal Would Enrich TPG, not TICC Shareholders „X TPG BDC¡¦s discounted NAV offer for TICC isn¡¦t motivated by wealth creation for TICC shareholders; rather their proposal is designed to create fees for their own investment advisor, TPG ¡V at the expense of TICC shareholders who would be harmed ¡V TPG BDC¡¦s CEOs and executives are employees of, and compensated by, the investment advisor, TPG ¡V enriching themselves at TICC shareholders¡¦ expense „X TPG BDC has a shareholder unfriendly ¡§catch-up¡¨ provision and low fixed hurdle rate of only 6% ¡V If TPG BDC adopted TICC¡¦s proposed fee structure under the BSP agreement, TPG BDC shareholders would save ~$8 million in annual incentive fees(1) representing a ~8% increase in distributions per share(1) „X TPG BDC¡¦s proposal creates ~$30 million(2) of revenue / profit per annum for their investment advisor, TPG ¡V NOT TICC shareholders ¡V TPG incurs no additional costs yet creates significant wealth for themselves „X The value of those fees to TPG could be ~$160 million(3) „X TPG BDC is also asking TICC shareholders to pay for all expenses associated with their campaign against the BSP proposal Proposal is Self-Motivated ¡V by TPG BDC¡¦s Investment Advisor, TPG Notes 1 Calculated assuming a 6.65% hurdle rate with no catch-up provision using 2Q¡¦15 financials for TPG BDC (assumes a constant payout ratio) 2 Calculated using TPG BDC fee structure and run-rate 2Q¡¦15 financials for both TICC and TPG BDC; fees could be higher or lower depending on actual performance 3 Represents theoretical market value of the additional annual fees / profit to TPG, assumptions include: ~$30 million annual revenue, no incremental manager costs, tax rate of 35%, and 8.6x multiple on net income

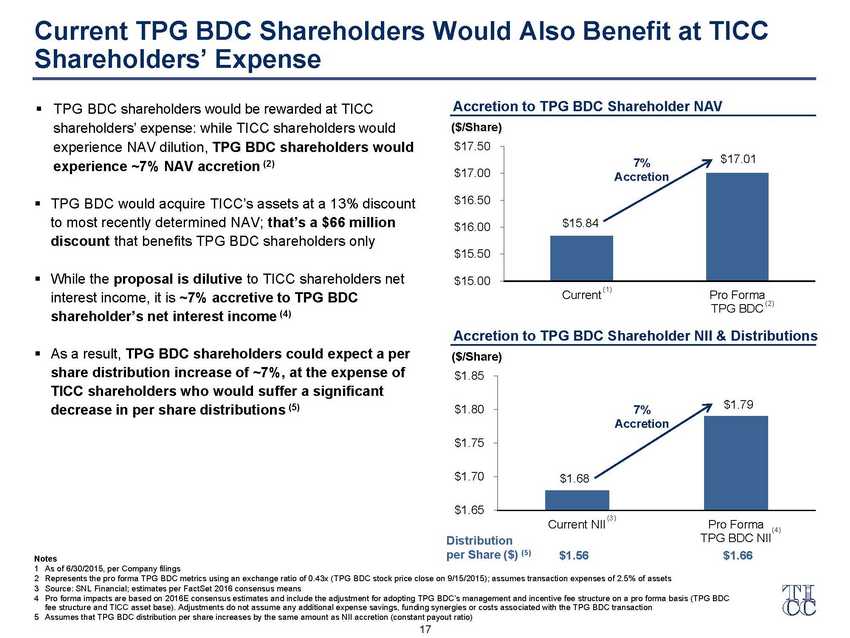

17 Current TPG BDC Shareholders Would Also Benefit at TICC Shareholders¡¦ Expense Notes 1 As of 6/30/2015, per Company filings 2 Represents the pro forma TPG BDC metrics using an exchange ratio of 0.43x (TPG BDC stock price close on 9/15/2015); assumes transaction expenses of 2.5% of assets 3 Source: SNL Financial; estimates per FactSet 2016 consensus means 4 Pro forma impacts are based on 2016E consensus estimates and include the adjustment for adopting TPG BDC¡¦s management and incentive fee structure on a pro forma basis (TPG BDC fee structure and TICC asset base). Adjustments do not assume any additional expense savings, funding synergies or costs associated with the TPG BDC transaction 5 Assumes that TPG BDC distribution per share increases by the same amount as NII accretion (constant payout ratio) 17% Dividend Yield „X TPG BDC shareholders would be rewarded at TICC shareholders¡¦ expense: while TICC shareholders would experience NAV dilution, TPG BDC shareholders would experience ~7% NAV accretion (2) „X TPG BDC would acquire TICC¡¦s assets at a 13% discount to most recently determined NAV; that¡¦s a $66 million discount that benefits TPG BDC shareholders only „X While the proposal is dilutive to TICC shareholders net interest income, it is ~7% accretive to TPG BDC shareholder¡¦s net interest income (4) „X As a result, TPG BDC shareholders could expect a per share distribution increase of ~7%, at the expense of TICC shareholders who would suffer a significant decrease in per share distributions (5) (2) $15.84 $17.01 $15.00 $15.50 $16.00 $16.50 $17.00 $17.50 Current Pro Forma TPG BDC ($/Share) Accretion to TPG BDC Shareholder NAV (1) 7% Accretion (4) $1.68 $1.79 $1.65 $1.70 $1.75 $1.80 $1.85 Current NII Pro Forma TPG BDC NII ($/Share) Accretion to TPG BDC Shareholder NII & Distributions (3) 17% Dividend Yield 7% Accretion Distribution per Share ($) (5) $1.56 $1.66

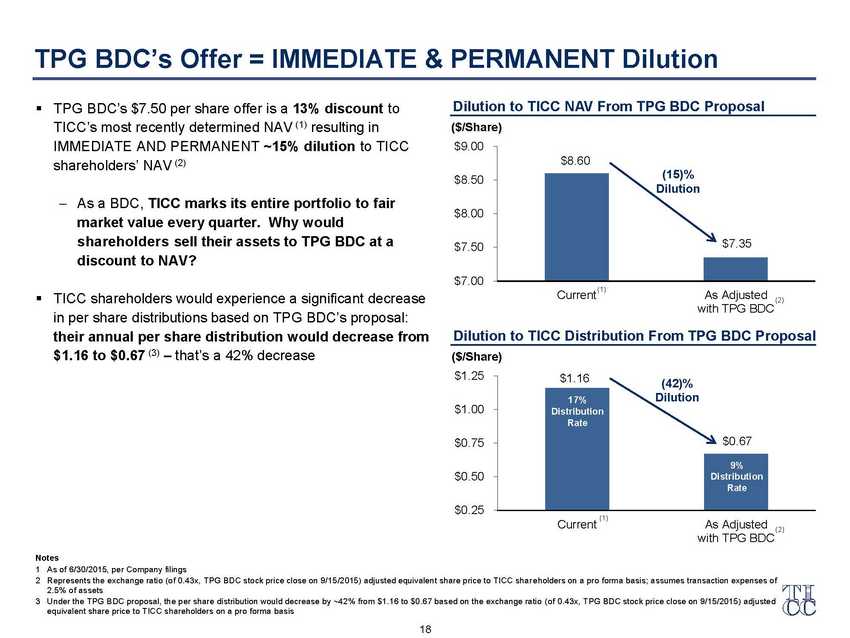

18 TPG BDC¡¦s Offer = IMMEDIATE & PERMANENT Dilution „X TPG BDC¡¦s $7.50 per share offer is a 13% discount to TICC¡¦s most recently determined NAV (1) resulting in IMMEDIATE AND PERMANENT ~15% dilution to TICC shareholders¡¦ NAV (2) { As a BDC, TICC marks its entire portfolio to fair market value every quarter. Why would shareholders sell their assets to TPG BDC at a discount to NAV? „X TICC shareholders would experience a significant decrease in per share distributions based on TPG BDC¡¦s proposal: their annual per share distribution would decrease from $1.16 to $0.67 (3) ¡V that¡¦s a 42% decrease Notes 1 As of 6/30/2015, per Company filings 2 Represents the exchange ratio (of 0.43x, TPG BDC stock price close on 9/15/2015) adjusted equivalent share price to TICC shareholders on a pro forma basis; assumes transaction expenses of 2.5% of assets 3 Under the TPG BDC proposal, the per share distribution would decrease by ~42% from $1.16 to $0.67 based on the exchange ratio (of 0.43x, TPG BDC stock price close on 9/15/2015) adjusted equivalent share price to TICC shareholders on a pro forma basis (2) $8.60 $7.35 $7.00 $7.50 $8.00 $8.50 $9.00 Current As Adjusted with TPG BDC ($/Share) Dilution to TICC NAV From TPG BDC Proposal (1) (15)% Dilution (2) $1.16 $0.67 $0.25 $0.50 $0.75 $1.00 $1.25 Current As Adjusted with TPG BDC ($/Share) Dilution to TICC Distribution From TPG BDC Proposal (1) (42)% 17% Dilution Distribution Rate 9% Distribution Rate

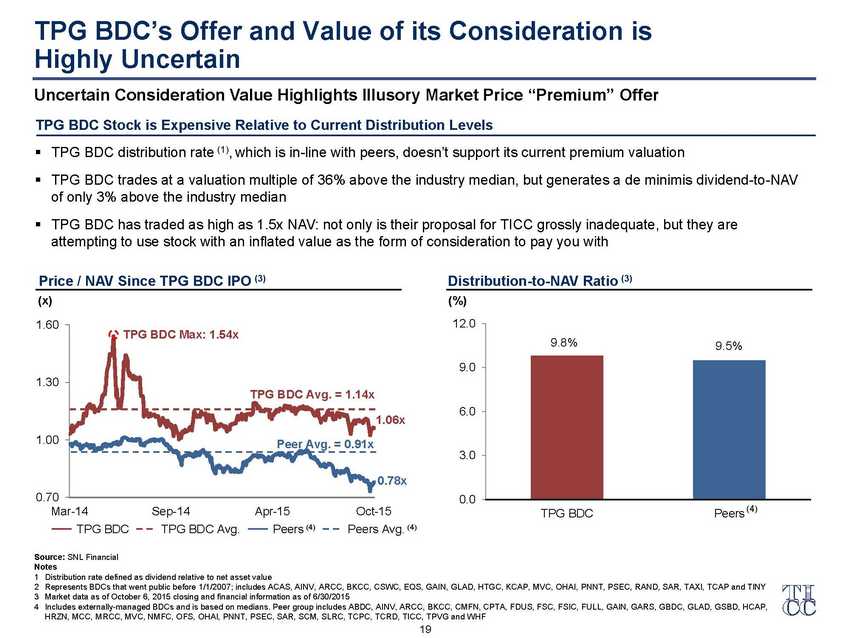

19 TPG BDC¡¦s Offer and Value of its Consideration is Highly Uncertain (x) Price / NAV Since TPG BDC IPO (3) (%) Source: SNL Financial Notes 1 Distribution rate defined as dividend relative to net asset value 2 Represents BDCs that went public before 1/1/2007; includes ACAS, AINV, ARCC, BKCC, CSWC, EQS, GAIN, GLAD, HTGC, KCAP, MVC, OHAI, PNNT, PSEC, RAND, SAR, TAXI, TCAP and TINY 3 Market data as of October 6, 2015 closing and financial information as of 6/30/2015 4 Includes externally-managed BDCs and is based on medians. Peer group includes ABDC, AINV, ARCC, BKCC, CMFN, CPTA, FDUS, FSC, FSIC, FULL, GAIN, GARS, GBDC, GLAD, GSBD, HCAP, HRZN, MCC, MRCC, MVC, NMFC, OFS, OHAI, PNNT, PSEC, SAR, SCM, SLRC, TCPC, TCRD, TICC, TPVG and WHF Distribution-to-NAV Ratio (3) „X TPG BDC distribution rate (1), which is in-line with peers, doesn¡¦t support its current premium valuation „X TPG BDC trades at a valuation multiple of 36% above the industry median, but generates a de minimis dividend-to-NAV of only 3% above the industry median „X TPG BDC has traded as high as 1.5x NAV: not only is their proposal for TICC grossly inadequate, but they are attempting to use stock with an inflated value as the form of consideration to pay you with TPG BDC Stock is Expensive Relative to Current Distribution Levels Uncertain Consideration Value Highlights Illusory Market Price ¡§Premium¡¨ Offer 9.8% 9.5% 0.0 3.0 6.0 9.0 12.0 TPG BDC Peers(4) Peers (4) 0.70 1.00 1.30 1.60 Mar-14 Sep-14 Apr-15 Oct-15 TPG BDC 1.06x 0.78x TPG BDC Max: 1.54x TPG BDC Avg. Peers Avg. (4) TPG BDC Avg. = 1.14x Peer Avg. = 0.91x

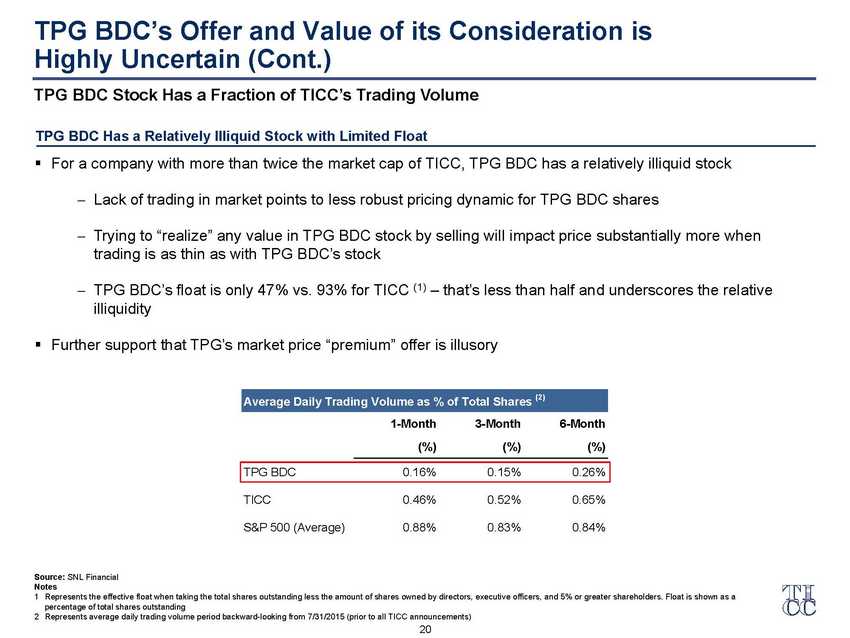

20 TPG BDC Stock Has a Fraction of TICC¡¦s Trading Volume Source: SNL Financial Notes 1 Represents the effective float when taking the total shares outstanding less the amount of shares owned by directors, executive officers, and 5% or greater shareholders. Float is shown as a percentage of total shares outstanding 2 Represents average daily trading volume period backward-looking from 7/31/2015 (prior to all TICC announcements) „X For a company with more than twice the market cap of TICC, TPG BDC has a relatively illiquid stock { Lack of trading in market points to less robust pricing dynamic for TPG BDC shares { Trying to ¡§realize¡¨ any value in TPG BDC stock by selling will impact price substantially more when trading is as thin as with TPG BDC¡¦s stock { TPG BDC¡¦s float is only 47% vs. 93% for TICC (1) ¡V that¡¦s less than half and underscores the relative illiquidity „X Further support that TPG¡¦s market price ¡§premium¡¨ offer is illusory TPG BDC Has a Relatively Illiquid Stock with Limited Float TPG BDC¡¦s Offer and Value of its Consideration is Highly Uncertain (Cont.) Average Daily Trading Volume as % of Total Shares (2) 1-Month 3-Month 6-Month (%) (%) (%) TPG BDC 0.16% 0.15% 0.26% TICC 0.46% 0.52% 0.65% S&P 500 (Average) 0.88% 0.83% 0.84%

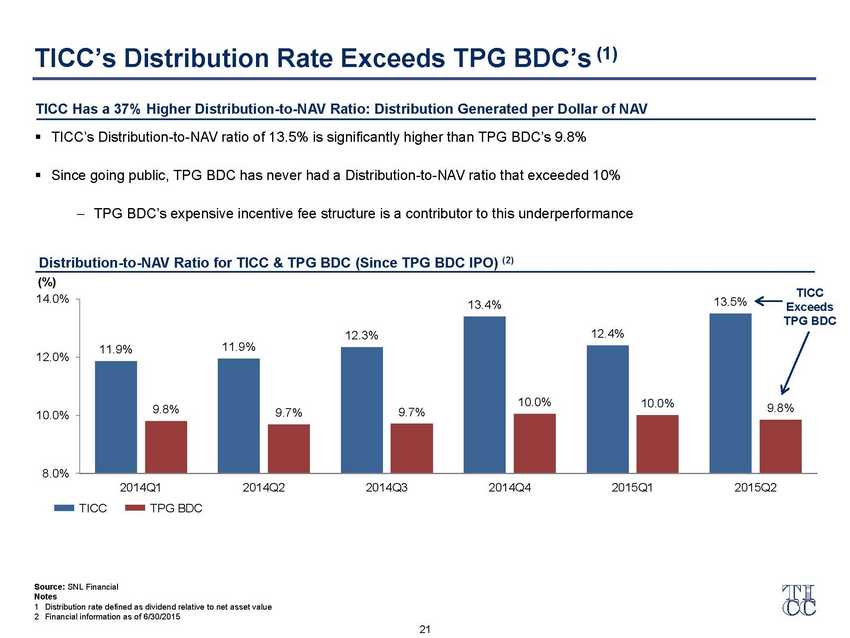

21 TICC¡¦s Distribution Rate Exceeds TPG BDC¡¦s (1) (%) Distribution-to-NAV Ratio for TICC & TPG BDC (Since TPG BDC IPO) (2) Source: SNL Financial Notes 1 Distribution rate defined as dividend relative to net asset value 2 Financial information as of 6/30/2015 „X TICC¡¦s Distribution-to-NAV ratio of 13.5% is significantly higher than TPG BDC¡¦s 9.8% „X Since going public, TPG BDC has never had a Distribution-to-NAV ratio that exceeded 10% { TPG BDC¡¦s expensive incentive fee structure is a contributor to this underperformance TICC TPG BDC TICC Has a 37% Higher Distribution-to-NAV Ratio: Distribution Generated per Dollar of NAV 11.9% 11.9% 12.3% 13.4% 12.4% 13.5% 9.8% 9.7% 9.7% 10.0% 10.0% 9.8% 8.0% 10.0% 12.0% 14.0% 2014Q1 2014Q2 2014Q3 2014Q4 2015Q1 2015Q2 TICC Exceeds TPG BDC

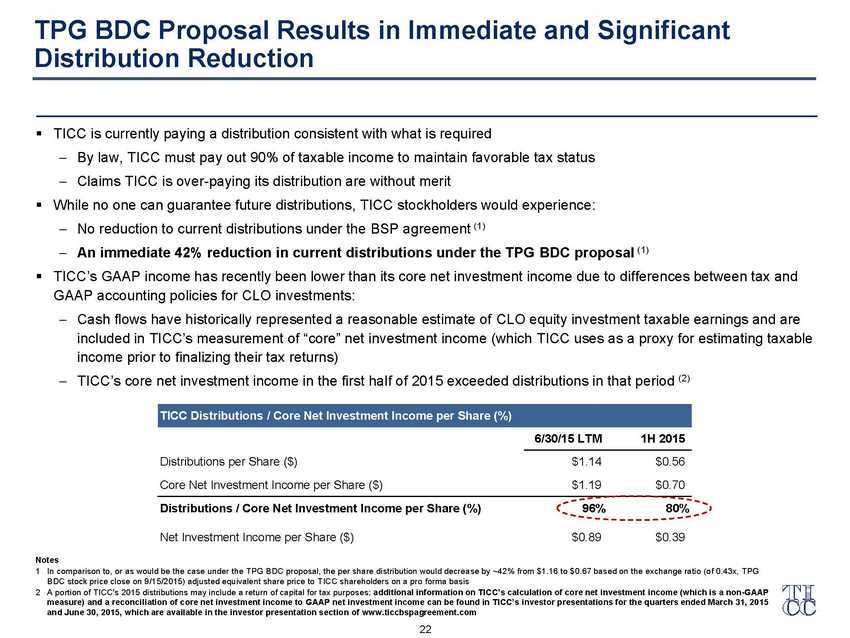

22 TPG BDC Proposal Results in Immediate and Significant Distribution Reduction „X TICC is currently paying a distribution consistent with what is required { By law, TICC must pay out 90% of taxable income to maintain favorable tax status { Claims TICC is over-paying its distribution are without merit „X While no one can guarantee future distributions, TICC stockholders would experience: { No reduction to current distributions under the BSP agreement (1) { An immediate 42% reduction in current distributions under the TPG BDC proposal (1) „X TICC¡¦s GAAP income has recently been lower than its core net investment income due to differences between tax and GAAP accounting policies for CLO investments: { Cash flows have historically represented a reasonable estimate of CLO equity investment taxable earnings and are included in TICC¡¦s measurement of ¡§core¡¨ net investment income (which TICC uses as a proxy for estimating taxable income prior to finalizing their tax returns) { TICC¡¦s core net investment income in the first half of 2015 exceeded distributions in that period (2) Notes 1 In comparison to, or as would be the case under the TPG BDC proposal, the per share distribution would decrease by ~42% from $1.16 to $0.67 based on the exchange ratio (of 0.43x, TPG BDC stock price close on 9/15/2015) adjusted equivalent share price to TICC shareholders on a pro forma basis 2 A portion of TICC's 2015 distributions may include a return of capital for tax purposes; additional information on TICC¡¦s calculation of core net investment income (which is a non-GAAP measure) and a reconciliation of core net investment income to GAAP net investment income can be found in TICC¡¦s investor presentations for the quarters ended March 31, 2015 and June 30, 2015, which are available in the investor presentation section of www.ticcbspagreement.com TICC Distributions / Core Net Investment Income per Share (%) 6/30/15 LTM 1H 2015 Distributions per Share ($) $1.14 $0.56 Core Net Investment Income per Share ($) $1.19 $0.70 Distributions / Core Net Investment Income per Share (%) 96% 80% Net Investment Income per Share ($) $0.89 $0.39

Appendix I – New Members of TICC’s Board Following the BSP Transaction

24 Upon the consummation of the Transaction, Mr. Gahan will be appointed as the Chairman of the Board of Directors and Mr. Byrne will be appointed as the President and Chief Executive Officer of the Company. Mr. Gahan will be an interested person of the Company as defined in the 1940 Act due to his position as chief executive officer of the Adviser. Mr. Byrne will be an interested person of the Company as defined in the 1940 Act due to his positions as the Chief Executive Officer and President of the Company. Thomas J. Gahan „« Chief Executive Officer of Benefit Street Partners „« Previously was CEO of Deutsche Bank Securities Inc. and Head of Corporate and Investment Banking in the Americas; was also the Global Head of Capital Markets, chairman of the principal investment committee and a member of the global banking executive committee and the global markets executive committee „« Before joining Deutsche Bank, spent 11 years at Merrill Lynch, most recently as Global Head of Credit Trading within the fixed income division „« Brown University, BA Richard J. Byrne „« President of Benefit Street Partners „« Previously was CEO of Deutsche Bank Securities Inc. and Global Co-Head of Capital Markets; before joining Deutsche Bank, Mr. Byrne was Global Co-Head of the Leveraged Finance Group and Global Head of Credit Research at Merrill Lynch & Co „« Member of the Board of Directors of New York Road Runners and the Board of Directors of MFA Financial, Inc. „« Binghamton University, BA; Kellogg School of Management, MBA New Members of TICC¡¦s Board of Directors Following the BSP Transaction

25 Upon consummation of the BSP transaction, the TICC Board of Directors will be 75% independent, with the addition of 4 well-qualified directors who are not interested persons under the Investment Company Act of 1940 Dennis Schaney „« Member of the Board of Directors of Griffin-Benefit Street Partners BDC Corp.; past Managing Director and Head of High Yield and Leveraged Loans at Morgan Stanley Investment Management; past Co-Head of Morgan Stanley Credit Partners „« Founder of BlackRock Financial Management¡¦s Leveraged Finance Group „« University of Bridgeport, BS; Fairfield University, MS Gary Katcher „« Chairman of GRK Partners LP; past Executive Vice President and Global Head of Institutional Fixed Income and Global Capital Markets of Knight Capital Group „« Founder and past CEO of Libertas Capital Partners „« SUNY Oneonta, BS; NYU, MBA New Members of TICC¡¦s Board of Directors Following the BSP Transaction (Cont.)

26 Ronald Kramer „« CEO and Vice Chairman of the Board of Directors of Griffon Corporation; past President and member of the Board of Directors of Wynn Resorts, Ltd „« Chairman of the Board of The Undergraduate Division of the Wharton School, University of Pennsylvania; member of the Board of Mt. Sinai Children¡¦s Center, New York „« Wharton School of the University of Pennsylvania, BS; NYU, MBA Lee Hillman „« President of Liberation Advisory Group; CEO of Performance Health Systems, LLC; member of the Board of Directors of Lawson Products Inc.; Trustee of the Adelphia Recovery Trust; past member of the Boards of Directors of HealthSouth Corporation, Wyndham International, and RCN Corporation „« The University of Pennsylvania, BS; The University of Chicago, MBA New Members of TICC¡¦s Board of Directors Following the BSP Transaction (Cont.)

Appendix II – TICC Portfolio Overview

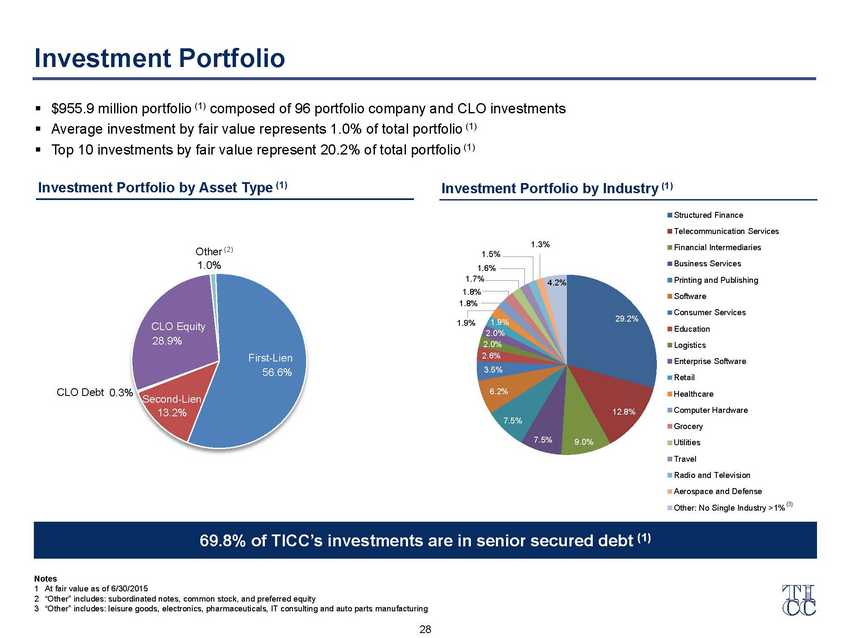

28 Investment Portfolio „X $955.9 million portfolio (1) composed of 96 portfolio company and CLO investments „X Average investment by fair value represents 1.0% of total portfolio (1) „X Top 10 investments by fair value represent 20.2% of total portfolio (1) Investment Portfolio by Asset Type (1) Investment Portfolio by Industry (1) First-Lien 69.8% of TICC¡¦s investments are in senior secured debt (1) Notes 1 At fair value as of 6/30/2015 2 ¡§Other¡¨ includes: subordinated notes, common stock, and preferred equity 3 ¡§Other¡¨ includes: leisure goods, electronics, pharmaceuticals, IT consulting and auto parts manufacturing (3) 29.2% 12.8% 7.5% 9.0% 7.5% 6.2% 3.5% 2.6% 2.0% 2.0% 1.9% 1.9% 1.8% 1.8% 1.7% 1.6% 1.5% 1.3% 4.2% Structured Finance Telecommunication Services Financial Intermediaries Business Services Printing and Publishing Software Consumer Services Education Logistics Enterprise Software Retail Healthcare Computer Hardware Grocery Utilities Travel Radio and Television Aerospace and Defense Other: No Single Industry >1% 1.0% 56.6% 13.2% 0.3% 28.9% Other (2) CLO Debt CLO Equity First-Lien Second-Lien

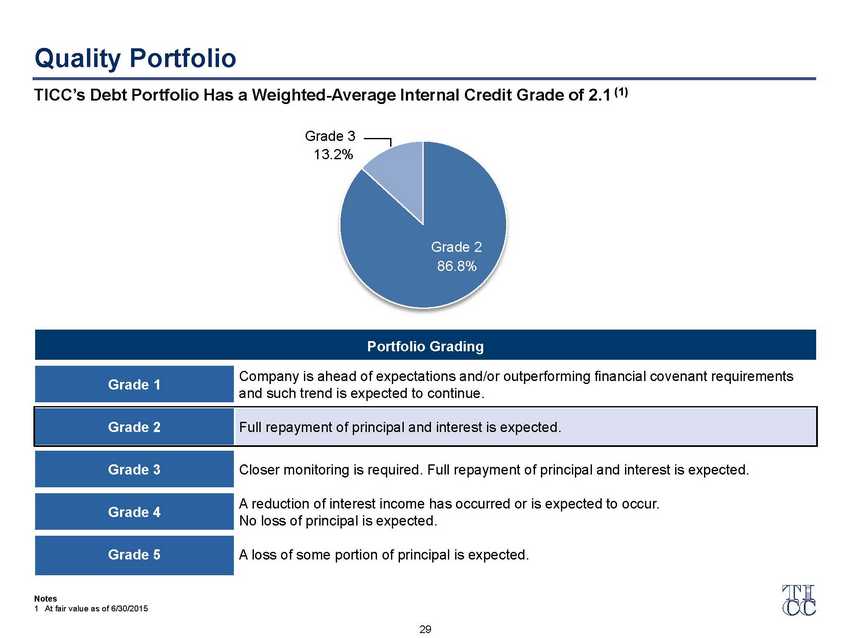

29 Quality Portfolio TICC’s Debt Portfolio Has a Weighted-Average Internal Credit Grade of 2.1 (1) Portfolio Grading Grade 1 Company is ahead of expectations and/or outperforming financial covenant requirements and such trend is expected to continue. Grade 2 Full repayment of principal and interest is expected. Grade 3 Closer monitoring is required. Full repayment of principal and interest is expected. Grade 4 A reduction of interest income has occurred or is expected to occur. No loss of principal is expected. Grade 5 A loss of some portion of principal is expected. 86.8% 13.2% Grade 3 Grade 2 Notes 1 At fair value as of 6/30/2015

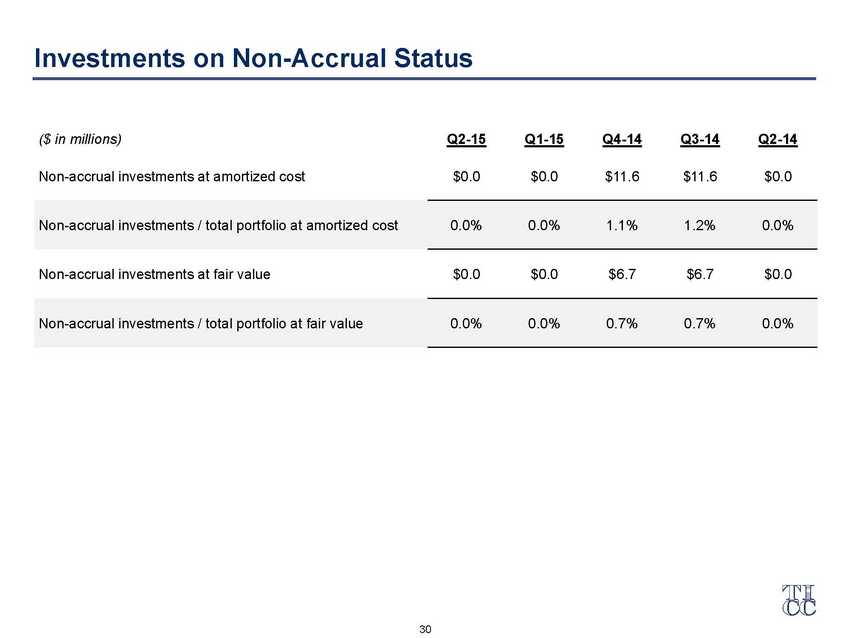

30 Investments on Non-Accrual Status ($ in millions) Q2-15 Q1-15 Q4-14 Q3-14 Q2-14 Non-accrual investments at amortized cost $0.0 $0.0 $11.6 $11.6 $0.0 Non-accrual investments / total portfolio at amortized cost 0.0% 0.0% 1.1% 1.2% 0.0% Non-accrual investments at fair value $0.0 $0.0 $6.7 $6.7 $0.0 Non-accrual investments / total portfolio at fair value 0.0% 0.0% 0.7% 0.7% 0.0%