UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

(RULE 14a-101)

INFORMATION REQUIRED IN PROXY STATEMENT

SCHEDULE 14A INFORMATION

PROXY STATEMENT PURSUANT TO SECTION 14(a) OF THE

SECURITIES EXCHANGE ACT OF 1934

| Filed by the Registrant | x |

| Filed by a Party other than the Registrant | ¨ |

Check the appropriate box:

| ¨ | Preliminary Proxy Statement | |

| ¨ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) | |

| ¨ | Definitive Proxy Statement | |

| x | Definitive Additional Materials | |

| ¨ | Soliciting Material Pursuant to Rule 14a-11(c) or Rule 14a-12 |

TICC Capital Corp.

(Name of Registrant as Specified in Its Charter)

(Name of Person(s) Filing Proxy Statement if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

| x | No fee required. | ||

| ¨ | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. | ||

| (1) | Title of each class of securities to which transaction applies: | ||

| (2) | Aggregate number of securities to which transaction applies: | ||

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (Set forth the amount on which the filing fee is calculated and state how it was determined): | ||

| (4) | Proposed maximum aggregate value of transaction: | ||

| (5) | Total fee paid: | ||

| ¨ | Fee paid previously with preliminary materials. | ||

| ¨ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the form or schedule and the date of its filing. | ||

| (1) | Amount previously Paid: | ||

| (2) | Form, schedule or registration statement No.: | ||

| (3) | Filing party: | ||

| (4) | Date filed: | ||

TICC Capital Corp. (the "Company") has filed with the Securities and Exchange Commission (the “SEC”), and disseminated to its stockholders, a proxy statement and accompanying WHITE proxy card to be used to solicit votes for the Company's proposal to approve a new advisory agreement between the Company and TICC Management, LLC, to take effect upon a change of control of TICC Management, LLC, and certain related proposals, at a special meeting of stockholders of the Company scheduled to be held on October 27, 2015.

This Schedule 14A filing consists of a press release that was issued by the Company on October 16, 2015 and slides from a related presentation, which reflect content not previously filed with the SEC. The content of this presentation is available at: http://WWW.TICCBSPAGREEMENT.COM, a website established by the Company that contains information regarding the above solicitation.

TICC ISSUES PRESENTATION DETAILING HOW TPG IS MISLEADING TICC STOCKHOLDERS

GREENWICH, CT– October 16, 2015 – TICC Capital Corp. (NASDAQ: TICC) (the "Company," "TICC," "we," or "our") today issued a presentation entitled “How TPG is Misleading TICC Stockholders” to highlight how TPG Specialty Lending, Inc. (“TSLX” or “TPG BDC”) is attempting to deceive and take advantage of TICC’s retail stockholders.

Key issues detailed include:

| · | The truth about TICC’s performance relative to its BDC peers; |

| · | Why TPG BDC’s offer and the value of its consideration is inadequate and highly uncertain; and |

| · | Why TPG BDC proposal is self-motivated – by their investment advisor, TPG |

The presentation can be found atwww.ticcbspagreement.com.

Morgan Stanley & Co. LLC and Wachtell, Lipton, Rosen & Katz are advising the Special Committee.

About TICC Capital Corp.

TICC Capital Corp. is a publicly-traded business development company principally engaged in providing capital to established businesses, investing in syndicated bank loans and purchasing debt and equity tranches of collateralized loan obligations.

Additional Information and Where to Find It

In connection with the approval of the proposed new investment advisory agreement, the Company has filed relevant materials with the SEC, including a definitive proxy statement on Schedule 14A. The Company has distributed the definitive proxy statement and a proxy card to each stockholder entitled to vote at the special meeting relating to the approval of the proposed new investment advisory agreement. INVESTORS AND SECURITY HOLDERS OF THE COMPANY ARE URGED TO READ THESE MATERIALS (INCLUDING ANY AMENDMENTS OR SUPPLEMENTS THERETO), AND ANY OTHER RELEVANT DOCUMENTS IN CONNECTION WITH THE APPROVAL OF THE PROPOSED NEW INVESTMENT ADVISORY AGREEMENT THAT THE COMPANY FILES WITH THE SEC, BECAUSE THESE MATERIALS CONTAIN IMPORTANT INFORMATION ABOUT THE COMPANY AND THE APPROVAL OF THE PROPOSED NEW INVESTMENT ADVISORY AGREEMENT. The definitive proxy statement and other relevant materials in connection with the approval of the proposed new investment advisory agreement, and any other documents filed by the Company with the SEC, may be obtained free of charge at the SEC's website (http://www.sec.gov), at the Company's website (http://www.ticc.com), or by writing to the Company at 8 Sound Shore Drive, Suite 255, Greenwich, CT 06830 (telephone number 203-983-5275).

Participants in the Solicitation

The Company and its directors and executive officers may be deemed to be participants in the solicitation of proxies from the Company's stockholders with respect to the approval of the proposed new investment advisory agreement. Information about the Company's directors and executive officers and their ownership of the Company's common stock is set forth in the proxy statement on Schedule 14A filed with the SEC on September 3, 2015, and the Annual Report on Form 10-K for the fiscal year ended December 31, 2014. Information regarding the identity of the potential participants, and their direct or indirect interests in the approval of the proposed new investment advisory agreement, by security holdings or otherwise, are set forth in the proxy statement and other materials filed or to be filed with SEC in connection therewith.

Forward Looking Statements

This press release contains forward-looking statements subject to the inherent uncertainties in predicting future results and conditions. Any statements that are not statements of historical fact (including statements containing the words "believes," "plans," "anticipates," "expects," "estimates" and similar expressions) should also be considered to be forward-looking statements. Certain factors could cause actual results and conditions to differ materially from those projected in these forward-looking statements. These factors are identified from time to time in our filings with the Securities and Exchange Commission. We undertake no obligation to update such statements to reflect subsequent events.

_______________

TICC Contacts

Media:Brandy Bergman/Meghan Gavigan

Sard Verbinnen & Co

212-687-8080

Stockholders:

Bruce Goldfarb/Tony Vecchio

Okapi Partners LLC

877-566-1922

October 2015 How TPGis Misleading TICCStockholders

2 Additional Information and Where to Find It In connection with the approval of the proposed new investment advisory agreement with Benefit Street Partners L.L.C. (“BSP”), TICC Capital Corp. ("TICC", "TICC Capital", the "Company", "us", "we" or "our") has filed relevant materials with the SEC, including a definitive proxy statement on Schedule 14A. The Company has distributed the definitive proxy statement and a proxy card to each stockholder entitled to vote at the special meeting relating to the approval of the proposed new investment advisory agreement and the election of six directors nominated by the Company. INVESTORS AND SECURITY HOLDERS OF THE COMPANY ARE URGED TO READ THESE MATERIALS (INCLUDING ANY AMENDMENTS OR SUPPLEMENTS THERETO), AND ANY OTHER RELEVANT DOCUMENTS IN CONNECTION WITH THE APPROVAL OF THE PROPOSED NEW INVESTMENT ADVISORY AGREEMENT AND THE APPROVAL OF ITS DIRECTOR NOMINEES THAT THE COMPANY FILES WITH THE SEC, BECAUSE THESE MATERIALS CONTAIN IMPORTANT INFORMATION ABOUT THE COMPANY AND THE APPROVAL OF THESE MATTERS. The definitive proxy statement and other relevant materials in connection with the approval of these matters, and any other documents filed by theCompany with the SEC, may be obtained free of charge at the SEC's website (http://www.sec.gov), at the Company's website (http://www.ticc.com), or by writing to the Company at 8 Sound Shore Drive, Suite 255, Greenwich, CT 06830 (telephone number 203- 983-5275). Participants in the Solicitation The Company and its directors and executive officers may be deemed to be participants in the solicitation of proxies from the Company's shareholders with respect to the approval of the proposed new investment advisory agreement and the election of six directors nominated by the Company. Information about the Company's directors and executive officers and their ownership of the Company's common stock is set forth in the proxy statement on Schedule 14A filed with the SEC on September 3, 2015, and the Annual Report on Form 10-K for the fiscal year ended December 31, 2014. Information regarding the identity of the potential participants, and their direct or indirect interests in the approval of the proposed new investment advisory agreement, by security holdings or otherwise, are set forth in the proxy statement and other materials filed or to be filed with SEC in connection therewith. Forward Looking Statements This press release contains forward-looking statements subject to the inherent uncertainties in predicting future results and conditions. Any statements that are not statements of historical fact (including statements containing the words "believes," "plans," "anticipates," "expects," "estimates" and similar expressions) should also be considered to be forward-looking statements. Certain factors could cause actual results and conditions to differ materially from those projected in these forward-looking statements. These factorsare identified from time to time in our filings with the Securities and Exchange Commission. We undertake no obligation to updatesuch statements to reflect subsequent events.

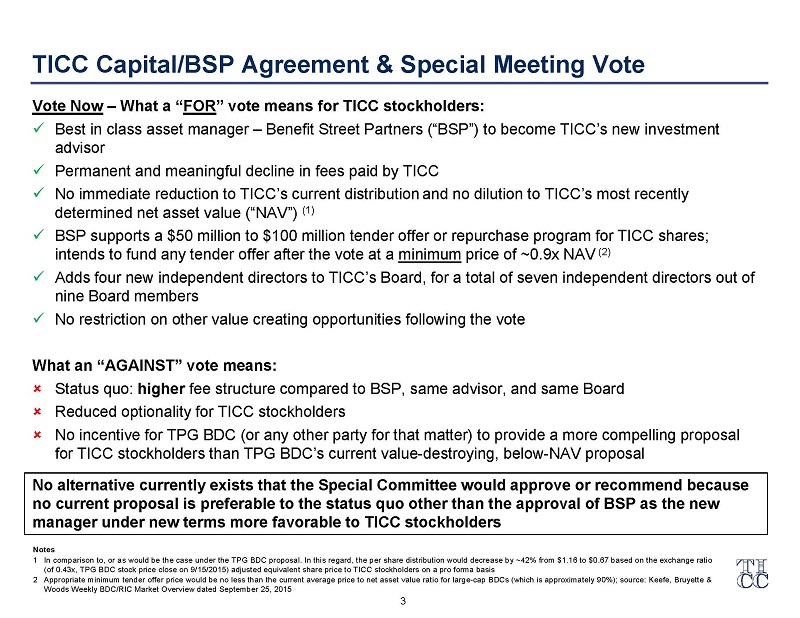

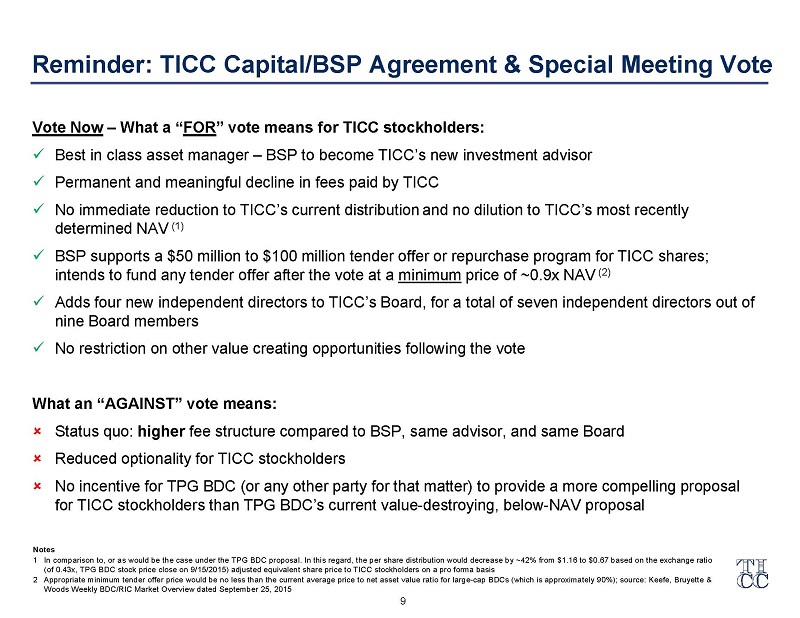

3 Vote Now–What a “FOR” vote means for TICC stockholders: x Best in class asset manager –Benefit Street Partners (“BSP”) to become TICC’s new investment advisor x Permanent and meaningful decline in fees paid by TICC x No immediate reduction to TICC’s current distributionand no dilution to TICC’s most recently determined net asset value (“NAV”) (1) x BSP supports a $50 million to $100 million tender offer or repurchase program for TICC shares; intends to fund any tender offer after the vote at a minimumprice of ~0.9x NAV (2) x Adds four new independent directors to TICC’s Board, for a total of seven independent directors out of nine Board members x No restriction on other value creating opportunities following the vote What an “AGAINST” vote means: Status quo: higher fee structure compared to BSP, same advisor, and same Board Reduced optionality for TICC stockholders No incentive for TPG BDC (or any other party for that matter) to provide a more compelling proposal for TICC stockholders than TPG BDC’s current value-destroying, below-NAV proposal No alternative currently exists that the Special Committee would approve or recommend because no current proposal is preferable to the status quo other than the approval of BSP as the new manager under new terms more favorable to TICC stockholders TICC Capital/BSP Agreement & Special Meeting Vote Notes 1 In comparison to, or as would be the case under the TPG BDC proposal. In this regard, the per share distribution would decrease by ~42% from $1.16 to $0.67 based on the exchange ratio (of 0.43x, TPG BDC stock price close on 9/15/2015) adjusted equivalent share price to TICC stockholders on a pro forma basis 2 Appropriate minimum tender offer price would be no less than the current average price to net asset value ratio for large -cap BDCs (which is approximately 90 %); source: Keefe, Bruyette & Woods Weekly BDC/RIC Market Overview dated September 25, 2015

4 ▪ Don’t be fooled, TPG’ssole motivations are driven by greed: acquire TICCassets at a big discount to NAV, charge higher fees and hope to earn even more fees in a rising rate environment ▪ TICChas performed favorably vs. BDCpeers – TICChas a strong return profile relative to peers, including outperforming TPG BDC50% of the time (1) – BSPfocused on reducing any trading discount to NAVfor TICC ▪ TPG BDC’soffer and value of its consideration is highly uncertain – Uncertain consideration value highlights illusory market price “premium” offer – TPG BDCstock is expensive relative to current distribution levels and is a relatively illiquid stock with which TPGwants to pay TICCstockholders ▪ TPG’sfocus on TICC’smanager’s compensation is a ruse solely seeking to deceive you into blocking a more favorable economic transaction for TICCstockholders (the BSPProposal) with a “hope” to enrich themselves and current TPG BDCstockholders at your expense (the TPG BDCProposal) – TPG BDConly became a TICCstockholder following announcement of the BSPProposal in August 2015 in order to, among other things, create the illusion of commonality of interest with TICC’sstockholders – The sale of TICC’smanager does not reduce the value of TICC’sassets or create any liabilities for TICC or its stockholders – This fleeting “Robin Hood rhetoric” by TPG is simply a ruse to block the BSPProposal in hopes that you will subsequently capitulate to the inferior TPG BDCproposal thereby enriching themselves TPG Attempting to Deceive and Take Advantage of TICC’s Retail Stockholders Notes 1 Based on the comparison of TICCand TPGBDCtotal return performance by quarter for the six quarters since TPGBDC’sIPO. TICChas had higher total returns in three of the last six quarters since TPGBDC’sIPO

5 Source:SNLFinancial; market data as of 10/6/2015 Notes 1 Represents BDCsthat went public before 1/1/2007; includes ACAS, AINV, ARCC, BKCC, CSWC, EQS, GAIN, GLAD, HTGC, KCAP, MVC, OHAI, PNNT, PSEC, RAND, SAR, TAXI, TCAPand TINY 2 Includes externally-managed BDCs and is based on medians. Peer group includes ABDC, AINV, ARCC, BKCC, CMFN, CPTA, FDUS, FSC, FSIC, FULL, GAIN, GARS, GBDC, GLAD, GSBD, HCAP, HRZN, MCC, MRCC, MVC, NMFC, OFS, OHAI, PNNT, PSEC, SAR, SCM, SLRC, TCPC, TCRD, TPVG, TSLX and WHF 3 Appropriate minimum tender offer price would be no less than the current average price to net asset value ratio for large -cap BDCs(which is approximately 90%); source: Keefe, Bruyette& Woods Weekly BDC/RICMarket Overview dated September 25, 2015 BSPInitiatives to Close the NAVGap TICCHas Performed Favorably Relative to BDCPeers Average = 12% (%) Price / NAVDifferential: TICCvs. Pre-2007 BDCIPO Peers (1) (20%) 0% 20% 40% 60% Oct-10 Apr-11 Oct-11 Apr-12 Oct-12 May-13 Nov-13 May-14 Nov-14 May-15 TICC Pre-2007 BDC IPO Peers (1) TICChas traded at a 12% average Price / NAVpremiumto peers over the last 5 years ▪ TICChas traded at a 5-year average Price / NAVof 0.99x versus other pre-2007 BDCIPO peers (1) at 0.88x, significantly outperforming peers, and demonstrating the prudent management approach of TICC’sadvisor In fact, TICChas outperformed all externally managed BDCs (2) –over the same 5-year period they have traded at an average of 0.97x vs. TICCat 0.99x ▪ BSPfocused on reducing any trading discount to NAV: BSPsupports $50 million to $100 million tender offer or repurchase program for TICCshares; any tender offer would be funded by BSP Tender Offer at a minimumprice to NAVof ~0.9x (3) is a premium to TPG BDC’snon-binding offer Tender Offer would provide optionality to stockholders to sell stock for cash or continue to be long-term stockholders alongside BSPwith the goal of maximizing the trading price relative to NAV Norestriction on other value creating opportunities following the vote

6 TICCHas Performed Favorably Relative to BDCPeers (Cont.) 7-Year Total Return Comparison –TICCHas Outperformed ▪ Post-financial crisis, TICChas generated an attractive return profile, significantly outperforming peers Not only has TICCoutperformed their pre-2007 peers, but all externally managed BDCsas well ▪ TICChas also OUTPERFORMED TPG BDCfrom a total return perspective in three of the last six quarters (since TPG BDC’sIPO) (%) (2) (1) Source:SNLFinancial; market data as of 10/6/2015 Notes 1 Represents BDCsthat went public before 1/1/2007; includes ACAS, AINV, ARCC, BKCC, CSWC, EQS, GAIN, GLAD, HTGC, KCAP, MVC, OHAI, PNNT, PSEC, RAND, SAR, TAXI, TCAPand TINY 2 Includes externally-managed BDCs and is based on medians. Peer group includes ABDC, AINV, ARCC, BKCC, CMFN, CPTA, FDUS, FSC, FSIC, FULL, GAIN, GARS, GBDC, GLAD, GSBD, HCAP, HRZN, MCC, MRCC, MVC, NMFC, OFS, OHAI, PNNT, PSEC, SAR, SCM, SLRC, TCPC, TCRD, TSLX, TPVGand WHF 20% 47% 338% 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% Externally Managed BDC Peers Pre-2007 BDC IPO Peers TICC Total Return Outperformance Post-Crisis

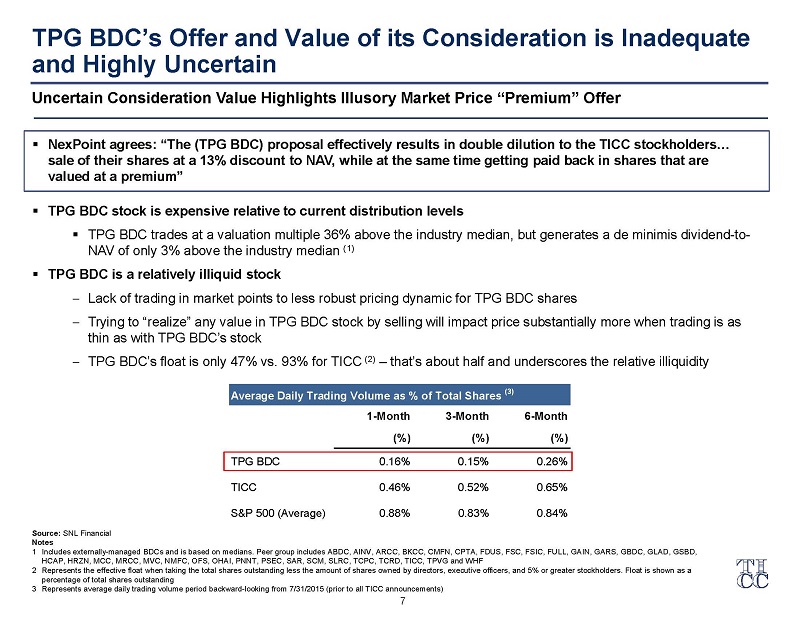

7 Average Daily Trading Volume as % of Total Shares (3) 1-Month 3-Month 6-Month (%) (%) (%) TPG BDC 0.16% 0.15% 0.26% TICC 0.46% 0.52% 0.65% S&P 500 (Average) 0.88% 0.83% 0.84% Source:SNL Financial Notes 1 Includes externally-managed BDCsand is based on medians. Peer group includes ABDC, AINV, ARCC, BKCC, CMFN, CPTA, FDUS, FSC, FSIC, FULL, GAIN, GARS, GBDC, GLAD, GSBD, HCAP, HRZN, MCC, MRCC, MVC, NMFC, OFS, OHAI, PNNT, PSEC, SAR, SCM, SLRC, TCPC, TCRD, TICC, TPVGand WHF 2 Represents the effective float when taking the total shares outstanding less the amount of shares owned by directors, executive officers , and 5% or greater stockholders. Float is shown as a percentage of total shares outstanding 3 Represents average daily trading volume period backward-looking from 7/31/2015 (prior to all TICCannouncements) ▪ NexPointagrees: “The (TPG BDC) proposal effectively results in double dilution to the TICCstockholders… sale of their shares at a 13% discount to NAV, while at the same time getting paid back in shares that are valued at a premium” ▪ TPG BDCstock is expensive relative to current distribution levels ▪ TPG BDCtrades at a valuation multiple 36% above the industry median, but generates a de minimisdividend-to- NAVof only 3% above the industry median (1) ▪ TPG BDCis a relatively illiquid stock Lack of trading in market points to less robust pricing dynamic for TPG BDCshares Trying to “realize” any value in TPG BDCstock by selling will impact price substantially more when trading is as thin as with TPG BDC’sstock TPG BDC’sfloat is only 47% vs. 93% for TICC (2) –that’s about half and underscores the relative illiquidity TPG BDC’s Offer and Value of its Consideration is Inadequate and Highly Uncertain Uncertain Consideration Value Highlights Illusory Market Price “Premium” Offer

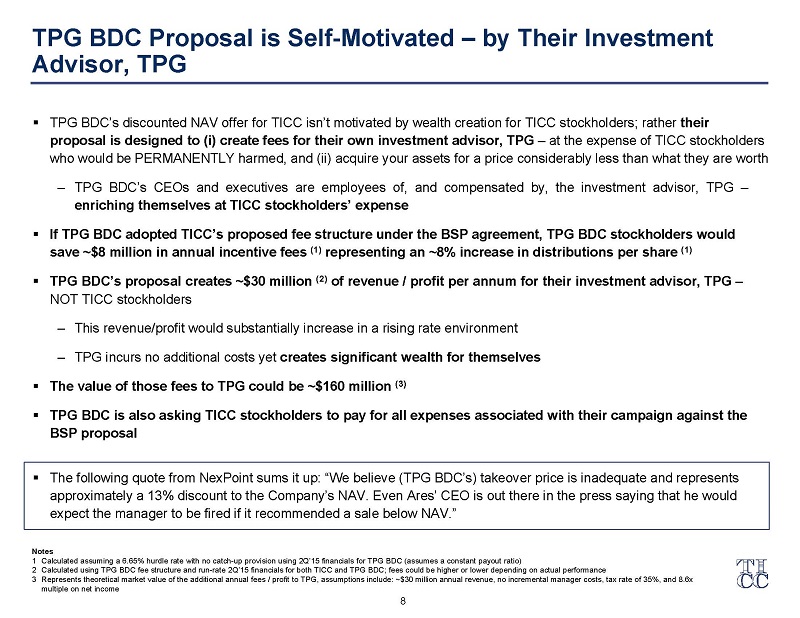

8 TPGBDCProposal is Self-Motivated –by Their Investment Advisor, TPG ▪ TPG BDC’s discounted NAV offer for TICC isn’t motivated by wealth creation for TICCstockholders; rather their proposal is designed to (i) create fees for their own investment advisor, TPG –at the expense of TICCstockholders who would be PERMANENTLY harmed, and (ii) acquire your assets for a price considerably less than what they are worth – TPG BDC’s CEOs and executives are employees of, and compensated by, the investment advisor, TPG – enrichingthemselvesatTICCstockholders’expense ▪ If TPG BDC adopted TICC’s proposed fee structure under the BSP agreement, TPG BDCstockholders would save ~$8 million in annual incentive fees (1) representing an ~8% increase in distributions per share (1) ▪ TPGBDC’sproposalcreates~$30million (2) of revenue / profitperannumfortheirinvestment advisor, TPG– NOTTICCstockholders – Thisrevenue/profitwouldsubstantiallyincreaseinarisingrateenvironment – TPGincursnoadditionalcostsyetcreatessignificantwealthforthemselves ▪ The value of those fees to TPG could be ~$160 million (3) ▪ TPGBDCis also askingTICCstockholderstopay forall expenses associated with their campaign against the BSPproposal ▪ The following quote from NexPointsums it up: “We believe (TPG BDC’s) takeover price is inadequate and represents approximately a 13% discount to the Company’s NAV. Even Ares’ CEO is out there in the press saying that he would expect the manager to be fired if it recommended a sale below NAV.” Notes 1 Calculated assuming a 6.65% hurdle rate with no catch-up provision using 2Q’15 financials for TPG BDC (assumes a constant payout ratio) 2 Calculated using TPG BDC fee structure and run-rate 2Q’15 financials for both TICC and TPG BDC; fees could be higher or lower depending on actual performance 3 Represents theoretical market value of the additional annual fees / profit to TPG, assumptions include: ~$30 million annual revenue, no incremental manager costs, tax rate of 35%, and 8.6x multiple on net income

9 Vote Now–What a “FOR” vote means for TICC stockholders: x Best in class asset manager –BSPto become TICC’s new investment advisor x Permanent and meaningful decline in fees paid by TICC x No immediate reduction to TICC’s current distributionand no dilution to TICC’s most recently determined NAV (1) x BSP supports a $50 million to $100 million tender offer or repurchase program for TICC shares; intends to fund any tender offer after the vote at a minimumprice of ~0.9x NAV (2) x Adds four new independent directors to TICC’s Board, for a total of seven independent directors out of nine Board members x No restriction on other value creating opportunities following the vote What an “AGAINST” vote means: Status quo: higher fee structure compared to BSP, same advisor, and same Board Reduced optionality for TICC stockholders No incentive for TPG BDC (or any other party for that matter) to provide a more compelling proposal for TICC stockholders than TPG BDC’s current value-destroying, below-NAV proposal Reminder: TICC Capital/BSP Agreement & Special Meeting Vote Notes 1 In comparison to, or as would be the case under the TPG BDC proposal. In this regard, the per share distribution would decrease by ~42% from $1.16 to $0.67 based on the exchange ratio (of 0.43x, TPG BDC stock price close on 9/15/2015) adjusted equivalent share price to TICC stockholders on a pro forma basis 2 Appropriate minimum tender offer price would be no less than the current average price to net asset value ratio for large -cap BDCs (which is approximately 90 %); source: Keefe, Bruyette & Woods Weekly BDC/RIC Market Overview dated September 25, 2015