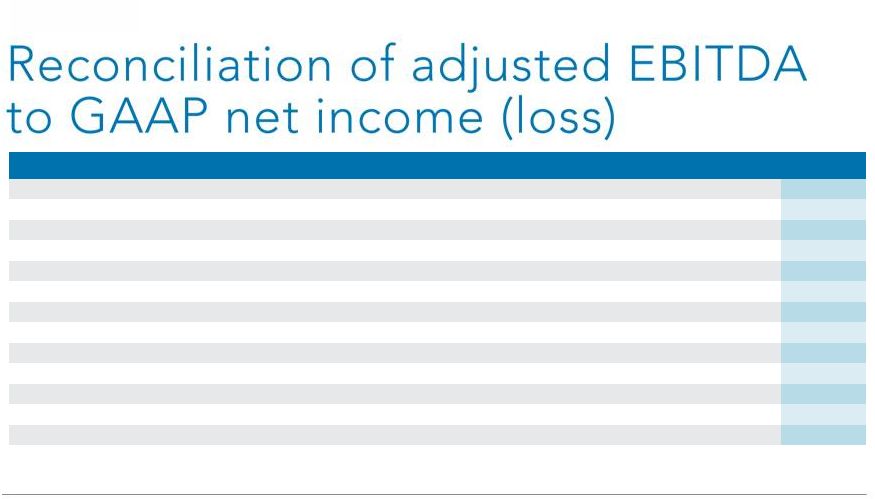

10 Quarterly earnings summary: Q2 2014 This document includes the non-GAAP financial measure of “Adjusted EBITDA” which we define as net income (loss) excluding: provision for income taxes; interest and other income (expense), net; depreciation; amortization; stock based compensation charges; gain or loss on derivatives’ revaluation, net income (loss) from discontinued operations; gain on sale of Rovion; impairment charges; LEC receivables reserve; finance related charges; accrued lease liability/asset; and severance charges. Adjusted EBITDA, as defined above, is not a measurement under GAAP. Adjusted EBITDA is reconciled to net income (loss) which we believe is the most comparable GAAP measure. A reconciliation of net income (loss) to Adjusted EBITDA is set forth within this presentation. Management believes that Adjusted EBITDA provides useful information to investors about the company’s performance because it eliminates the effects of period-to-period changes in income from interest on the company’s cash and marketable securities, expense from the company’s financing transactions and the costs associated with income tax expense, capital investments, stock-based compensation expense, LEC receivables reserve, warrant revaluation charges; finance related charges; accrued lease liability; and severance charges which are not directly attributable to the underlying performance of the company’s business operations. Management uses Adjusted EBITDA in evaluating the overall performance of the company’s business operations. A limitation of non-GAAP Adjusted EBITDA is that it excludes items that often have a material effect on the company’s net income and earnings per common share calculated in accordance with GAAP. Therefore, management compensates for this limitation by using Adjusted EBITDA in conjunction with net income (loss) and net income (loss) per share measures. The company believes that Adjusted EBITDA provides investors with an additional tool for evaluating the company’s core performance, which management uses in its own evaluation of overall performance, and as a base-line for assessing the future earnings potential of the company. While the GAAP results are more complete, the company prefers to allow investors to have this supplemental metric since, with reconciliation to GAAP; it may provide greater insight into the company’s financial results. The non-GAAP measures should be viewed as a supplement to, and not as a substitute for, or superior to, GAAP net income (loss) or earnings (loss) per share. |