Table of Contents

Filed Pursuant to Rule 424(b)(3)

Registration No. 333-128662

Prospectus

CNL INCOME PROPERTIES, INC.

200,000,000 Shares of Common Stock - Maximum Offering. Minimum Purchase - 500 Shares.

We are a Maryland corporation sponsored by CNL Financial Group, Inc. (our “Sponsor”) and formed to acquire lifestyle properties primarily in the United States and Canada. We will either acquire these properties directly or through joint ventures or other real estate operating companies. We are offering 195 million shares of our common stock at a price of $10.00 per share on a “best efforts” basis through our affiliate, CNL Securities Corp. “Best efforts” means that CNL Securities Corp., our managing dealer and affiliate (the “Managing Dealer”), is not obligated, and does not intend, to purchase any specific number or dollar amount of shares. We also are offering up to five million shares of our common stock at a price of $9.50 per share to stockholders who elect to participate in our reinvestment plan. In each case, the offering price was subjectively determined by our board of directors. As of December 31, 2006, we have issued and sold a total of 116,066,598 shares of our common stock pursuant to our offerings.

We believe that we are qualified and have operated for federal income tax purposes as a real estate investment trust (“REIT”).

This investment involves a high degree of risk. You should purchase these securities only if you can afford a complete loss of your investment.See “Risk Factors” beginning on page19 of this prospectus for a discussion of material risks that you should consider before you invest in our common stock, including:

| • | We have a limited operating history and limited financing sources. |

| • | Our investment policies and strategies are very broad and permit us to invest in many types of real estate and to make loans and other investments. |

| • | The number of properties that we will acquire or loans we can make and the diversification of our investments will depend on the total proceeds raised in this offering. |

| • | We rely on CNL Income Corp., our advisor (the “Advisor”) and our affiliate, subject to approval by our board of directors, to make our investment decisions. Our Advisor was formed in 2003 and has limited experience in certain of the asset classes in which we will invest. Our Advisor and its affiliates have limited or no experience investing in certain of the types of properties in which we may invest, which could result in a failure to meet our investment objectives. |

| • | The advisory agreement was not negotiated at arm’s length and we will pay our Advisor and its affiliates substantial fees. |

| • | Certain officers and directors of our Advisor also serve as our officers and directors, resulting in conflicts of interest. Those persons could take actions that are more favorable to other entities than to us. |

| • | To the extent consistent with our investment objectives and limitations, our investment policies and strategies may be altered by a majority of our directors, including a majority of our independent directors, without stockholder consent. |

| • | There is no market for our shares and we do not expect to list our shares in the near future. If we do not list our shares by December 31, 2015, we will take steps to liquidate our assets or merge with another entity to provide our stockholders with cash or securities of a publicly traded company. |

| • | We may borrow up to 300% of the value of our net assets, which may reduce the cash available for distributions to stockholders. |

| • | Our articles of incorporation prohibit individual stockholders from owning more than 9.8% of our common stock. |

| • | Redemption of our shares shall be at our sole option. |

| • | If we do not qualify and remain qualified as a REIT, we would be subject to taxation on our income at regular corporate rates. |

| Per Share | Total Maximum | |||||

Public Offering Price | $ | 10.00 | $ | 2,000,000,000 | ||

Selling Commissions and Marketing Support Fee* | $ | 1.00 | $ | 195,000,000 | ||

Proceeds to CNL Income Properties | $ | 9.00 | $ | 1,805,000,000 | ||

| * | The selling commissions and marketing support fee will not be paid in connection with purchases of shares pursuant to our reinvestment plan and will not be charged in connection with certain purchases. A portion of these fees will be reduced with respect to volume purchases. |

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. In addition, the Attorney General of the State of New York has not passed on or endorsed the merits of this offering. Any representation to the contrary is a criminal offense.

This offering will end no later than April 4, 2008.

No one is authorized to make any statements about the offering that differ from those that appear in this prospectus. You should also be aware that the description of our company contained in this prospectus was accurate on April 6, 2007, but may no longer be accurate. We will amend or supplement this prospectus, however, if there is a material change in the affairs of our company.

We will only use proceeds from this offering for the purposes stated in the “Use of Proceeds” section of the prospectus. Subscription funds will initially be held in an interest-bearing escrow account for our benefit.

The use of forecasts in this offering is prohibited. Any representations to the contrary and any predictions, written or oral, as to the amount or certainty of any present or future cash benefit or tax consequence which may flow from an investment in our shares is not permitted.

April 20, 2007

Table of Contents

SUITABILITY STANDARDS AND HOW TO SUBSCRIBE

We have established financial suitability standards for investors interested in purchasing shares of our common stock. In addition, residents of Arizona, California, Kansas, Maine, Massachusetts, Michigan, Missouri, North Carolina, Ohio and Pennsylvania have established suitability standards different from those established by us. These standards require you to meet the applicable criteria set forth below. In determining your net worth, do not include the value of your home, furnishings or personal automobile.

You must have:

| • | a net worth of at least $150,000, or |

| • | a gross annual income of at least $45,000 and a net worth of at least $45,000. |

Our suitability standards also require that you:

| • | can reasonably benefit from an investment in our common stock based on your overall investment objectives and portfolio structure; |

| • | are able to bear the economic risk of the investment based on your overall financial situation; and |

| • | have apparent understanding of: |

| • | the fundamental risks of your investment, |

| • | the risk that you may lose your entire investment, |

| • | the lack of liquidity of your shares, |

| • | the restrictions on transferability of your shares, |

| • | the background and qualifications of our Advisor, and |

| • | the tax consequences of your investment. |

Initially, we do not expect that there will be, and there has not been a market for our shares, which means that it may be difficult for you to sell your shares.

ARIZONA, CALIFORNIA, MASSACHUSETTS, MICHIGAN AND NORTH CAROLINA — you must have either:

| • | a net worth (not including home, furnishings and personal automobiles) of at least $60,000 and a gross annual income of at least $60,000, or |

| • | a net worth (not including home, furnishings and personal automobiles) of at least $225,000. |

MAINE — you must have either:

| • | a net worth (not including home, furnishings and personal automobiles) of at least $50,000 and a gross annual income of at least $50,000, or |

i

Table of Contents

| • | a net worth (not including home, furnishings and personal automobiles) of at least $225,000. |

KANSAS — you must:

| • | have either (a) a net worth (not including home, furnishings, and personal automobiles) of at least $70,000 and a gross annual income of at least $70,000 or (b) a net worth (not including home, furnishings and personal automobiles) of at least $250,000. |

| • | It is recommended that you limit your aggregate investment in our stock and other non-exchange traded REITs to not more than 10% of your liquid net worth. “Liquid net worth” means the portion of net worth (total assets minus total liabilities) that is comprised of cash, cash equivalents and readily marketable securities as determined in accordance with generally accepted accounting principles. |

OHIO — you must:

| • | invest no more than 10% of your net worth (not including home, furnishings and personal automobiles) in us, and |

| • | have either (a) a net worth (not including home, furnishings and personal automobiles) of at least $70,000 and a gross annual income of at least $70,000 or (b) a net worth (not including home, furnishings and personal automobiles) of at least $250,000. |

MISSOURI — you must:

| • | invest no more than 10% of your net worth (not including home, furnishings and personal automobiles) in us, and |

| • | have either (a) a net worth (not including home, furnishings, and personal automobiles) of at least $60,000 and a gross annual income of at least $60,000 or (b) a net worth (not including home, furnishings and personal automobiles) of at least $225,000. |

PENNSYLVANIA — you must:

| • | invest no more than 10% of your net worth (not including home, furnishings and personal automobiles) in us, and |

| • | have either (a) a net worth (not including home, furnishings and personal automobiles) of at least $45,000 and a gross annual income of at least $45,000 or (b) a net worth (not including home, furnishings and personal automobiles) of at least $150,000. |

The foregoing suitability standards must be met by each investor who purchases shares. If the investment is being made for a fiduciary account (such as an IRA, Keogh plan or a pension, profit-sharing, stock bonus plan or other plan (including a plan described in Section 4975(e)(1) of Code) collectively “Plans”), the beneficiary, the fiduciary account, or any donor or grantor that is the fiduciary of the account who directly or indirectly supplies the investment funds must meet such suitability standards.

Before authorizing an investment in shares, fiduciaries of Plans should consider, among other matters, (a) fiduciary standards imposed by ERISA or governing state or other law, if applicable, (b) whether the purchase of shares satisfies the prudence and diversification requirements of ERISA and governing state or other law, if applicable, taking into account any applicable Plan investment policy and the composition of the Plan’s portfolio, and the limitations on the marketability of shares, (c) whether such fiduciaries have authority to hold shares under the applicable Plan investment policies and governing instruments, (d) rules relating to the periodic valuation of Plan assets, and (e) prohibitions under ERISA, the Code and/or governing state or other law relating to Plans engaging in

ii

Table of Contents

certain transactions involving “plan assets” with persons who are “disqualified persons” under the Code or “parties in interest” under ERISA or governing state or other law, if applicable. See “The Offering - ERISA Considerations.”

Participating broker-dealers that are members of the National Association of Securities Dealers, Inc. (“NASD”) or other entities exempt from broker-dealer registration, who are engaged by our Managing Dealer to sell shares, have the responsibility to make every reasonable effort to determine that the purchase of shares is a suitable and appropriate investment for an investor. In making this determination, the participating broker-dealers will rely on relevant information provided by the investor, including information as to the investor’s age, investment objectives, investment experience, income, net worth, financial situation, other investments and any other pertinent information. Executed subscription agreements will be maintained in our records for six years.

If you meet the suitability standards described above and wish to subscribe for shares prior to May 15, 2007, complete and execute the subscription agreement and deliver it to your broker-dealer, together with a check payable to “WBNA Escrow Agent for CNL Income Properties, Inc.” for the full purchase price of the shares. Beginning May 15, 2007, our Escrow Agent will be Wells Fargo Bank, National Association (“Wells Fargo Bank”). If you wish to subscribe for shares on or after May 15, 2007, complete and execute the subscription agreement and deliver it to your broker-dealer, together with a check payable to “CNL Income Properties, Inc.” for the full purchase price of the shares. Certain participating broker-dealers who have “net capital,” as defined in the applicable federal securities regulations, of $250,000 or more may instruct their customers to make their checks for shares for which they have subscribed payable directly to them. Partnerships, individual fiduciaries signing on behalf of trusts, estates, and in other capacities, and persons signing on behalf of corporations and corporate trustees may be required to provide additional documents to participating broker-dealers. We may reject any subscription in whole or in part, regardless of whether you meet the minimum suitability standards.

Individuals must initially invest at least $5,000. Plans must initially invest at least $4,000. If you have previously invested $5,000/$4,000 as applicable, either in this offering or in our prior offering, you may purchase additional shares in $10.00 increments.

iii

Table of Contents

i

Table of Contents

ii

Table of Contents

iii

Table of Contents

iv

Table of Contents

| 59 | ||

| 61 | ||

| 61 | ||

| 62 | ||

| 64 | ||

| 64 | ||

| 65 | ||

| 66 | ||

| 67 | ||

Recent Demographic Trends That May Enhance Demand for Certain of Our Investments | 67 | |

| 70 | ||

| 71 | ||

| 101 | ||

| 104 | ||

| 105 | ||

| 109 | ||

| 109 | ||

| 109 | ||

| 113 | ||

| 115 | ||

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 117 | |

| 117 | ||

| 117 | ||

| 118 | ||

| 125 | ||

| 126 | ||

| 127 | ||

| 130 | ||

| 134 | ||

| 136 | ||

| 136 | ||

| 138 | ||

| 139 | ||

| 139 | ||

| 140 | ||

| 141 | ||

| 142 | ||

| 142 | ||

| 142 | ||

| 145 | ||

| 147 | ||

| 147 | ||

| 151 | ||

| 152 | ||

v

Table of Contents

| 152 | ||

| 152 | ||

| 153 | ||

| 153 | ||

Advance Notice for Stockholder Nominations for Directors and Proposals of New Business | 154 | |

| 154 | ||

| 154 | ||

| 155 | ||

| 156 | ||

| 156 | ||

| 156 | ||

| 158 | ||

| 158 | ||

| 159 | ||

| 159 | ||

| 160 | ||

| 161 | ||

| 161 | ||

| 168 | ||

| 172 | ||

| 173 | ||

| 173 | ||

| 174 | ||

| 174 | ||

| 175 | ||

| 179 | ||

| 179 | ||

| 180 | ||

| 181 | ||

| 182 | ||

| 182 | ||

| 183 | ||

| 183 | ||

| 185 | ||

| 186 | ||

| F-1 | ||

| Appendix A | ||

| Appendix B | ||

| Appendix C | ||

vi

Table of Contents

This summary highlights the material information contained elsewhere in this prospectus. Because this is a summary, it does not contain all information that may be important to you. You should read this entire prospectus and its appendices carefully before you decide to invest in shares of our common stock.

CNL Income Properties, Inc. CNL Income Properties, Inc. is a Maryland corporation organized on August 11, 2003. We operate as a real estate investment trust, or a REIT. In general, a REIT is a company that combines the capital of many investors to acquire or provide financing for real estate. Typically REITs:

| • | do not pay federal corporate income taxes on income they distribute to their shareholders as long as they distribute at least 90% of their taxable income to their stockholders. Such treatment substantially eliminates the “double taxation” (taxation at both the corporate and stockholder levels) that generally results from investing in a corporation; and |

| • | offer the benefit of a real estate portfolio under professional management. |

In the course of our business, various wholly owned subsidiaries, unconsolidated and consolidated entities have been and/or will be formed in the future for the purpose of acquiring interests in properties, loans and other permitted investments. The terms “us,” “we,” “our,” “our company” and “CNL Income Properties” include CNL Income Properties, Inc. and our subsidiaries. Our address is CNL Center at City Commons, 450 South Orange Avenue, Orlando, Florida 32801, and our telephone number is (407) 650-1000 or toll free (866) 650-0650.

General. We invest in lifestyle properties in the United States and Canada that we lease on a long-term basis (generally 5 to 20 years, plus multiple renewal options) to tenants or operators who are significant industry leaders. We define lifestyle properties as those properties that reflect or are impacted by the social, consumption and entertainment values and choices of our society. We also offer mortgage, mezzanine and other financing related to interests in lifestyle real estate.

As of April 6, 2007, we had a portfolio of 65 lifestyle properties, including interests in retail and commercial properties at seven resort villages, one merchandise mart, two waterpark resorts, five waterparks, one sky lift attraction, one dealership, 21 golf courses, seven ski properties, 11 family entertainment centers, five marinas and four theme parks. We had made eleven loans, ten of which were outstanding, and committed to make one additional loan. We have also committed to acquire four marina properties and the retail and commercial properties at one resort village. As of December 31, 2006, we had total assets of approximately $1.1 billion.

Our tenants and operators.We generally attempt to lease our properties to tenants and operators who are significant industry tenants and leaders. We consider an operator to be a “significant industry leader” if it has one or more of the following traits:

| • | many years of experience operating in a particular industry as compared with other operators in that industry, as a company or through the experience of its senior management; |

| • | many assets managed in a particular industry as compared with other operators in that industry; and/or |

| • | is deemed by us to be a dominant operator in a particular industry for reasons other than those listed above. |

Our leases and ventures. As part of our net lease investment strategy, we plan to either acquire properties directly or purchase interests in entities that own the properties we acquire. Once we acquire properties, we will either lease them back to the original seller or to a third-party operator. These leases are usually triple-net leases which means our tenants are generally responsible for repairs, maintenance, property taxes, ground lease or permit

1

Table of Contents

expenses (where applicable), utilities and insurance for the properties that they lease. Our joint ventures will lease properties either to our venture partner or to third-party operators, generally on a triple-net or gross basis. We generally structure our leases to provide for the payment of a minimum annual base rent with periodic increases in rent over the lease term. In addition, our leases provide for the payment of percentage rent generally based on a percentage of gross revenues at the property over certain thresholds.

To a lesser extent, when beneficial to our venture structure, certain properties may be leased to wholly-owned tenants that are taxable REIT subsidiaries or that are owned through taxable REIT subsidiaries (referred to as “TRS” entities). Under this structure, we engage third-party managers to conduct day-to-day operations. Under the TRS leasing structure, our results of operations will include the operating results of the underlying properties as opposed to rental income from operating leases that is recorded for properties leased to third-party tenants.

Further, we have entered into joint ventures where our partners may subordinate their returns to our minimum return. This structure provides us with some protection against the risk of downturns in performance but may allow our partners to obtain a higher rate of return on their investment than we receive if the underlying performance of the properties exceeds certain thresholds.

Key investment factors.We have and will continue to focus our investment activities on and use the proceeds of our offerings primarily for the acquisition, development and ownership of lifestyle properties that we believe possess some or all of the following characteristics:

| • | are part of an asset class in which the supply of developed, specific-use real estate is typically greater than the demand for the intended use of such real estate; |

| • | have historically shown consistent revenue and income trends or have the potential for increased performance due to a change in operational control or additional investment in improvements; |

| • | are part of an industry that is experiencing constraints on the availability of new capital, which we believe typically has the effect of lowering the purchase price of such properties; and/or |

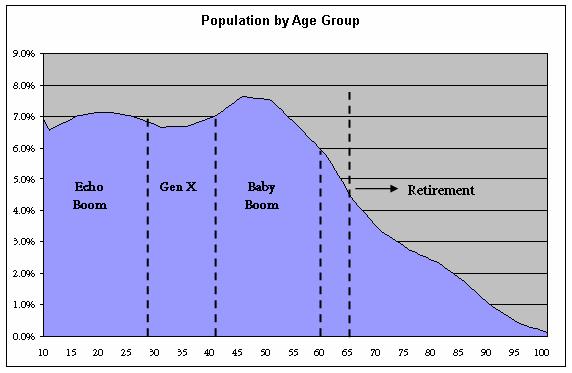

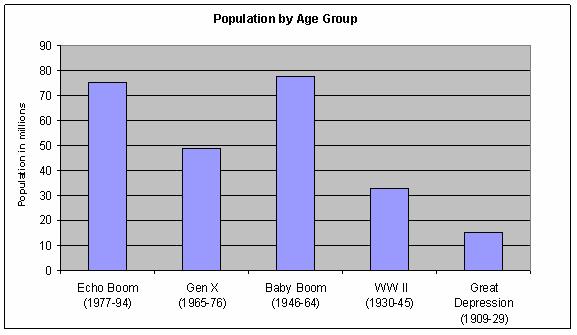

| • | have the potential for long-term revenue generation based upon certain demographic data, including an aging baby boomer population and associated concentrations of wealth. |

Asset classes. We have invested or intend to invest in properties in the following asset classes (in no order of priority):

| • | property leased to dealerships including, for example, automobile, motorcycle, recreational vehicle and boat dealerships; |

| • | campgrounds, recreational vehicle (“RV”) parks whose operators rent lots and offer other services; |

| • | health clubs, athletic training facilities, wellness centers and spa facilities; |

| • | parking lots whose operators offer monthly and daily parking space rentals in urban areas; |

| • | merchandise marts whose operators lease showrooms and host tradeshows for merchandise manufacturers and wholesalers in major metropolitan areas; |

| • | destination retail and entertainment centers whose operators develop and lease properties featuring entertainment-oriented stores, restaurants and/or attractions; |

| • | marinas whose operators offer recreational boat slip rentals and other services; |

| • | ski resorts, including real estate in and around ski resorts such as ski-in/ski-out alpine villages, townhouses, lodging and other related properties; |

2

Table of Contents

| • | golf courses and golf resorts, including real estate in and around golf courses and golf resorts such as retail villages, townhouses, lodges and other related properties; |

| • | amusement parks, waterparks and family entertainment centers, which may include lodging facilities; |

| • | real estate in and around lifestyle communities; |

| • | vacation ownership interests, which entitle a purchaser of the interests to exclusive use of resort accommodations at a resort property or properties for a particular period of time each year; and |

| • | other attractions, such as sports-related venues and cultural facilities, visual and performing arts centers, zoological parks or aquariums. |

Although we have invested or intend to invest in these asset classes, we may acquire or invest in other types of properties which are not listed above that we believe have the potential to generate long-term revenue. Our activities will continue to focus on property acquisitions and other investments with increased focus on the management and oversight of our existing assets. We will also look to our existing assets and partners for additional investment opportunities.

We may obtain debt financing or sell additional shares of our stock in the future to finance acquisitions. Proceeds received from this offering generally will be temporarily invested in short-term, highly liquid investments pending investment of such proceeds in properties, loans or other Permitted Investments.

Our loans. As part of our lending strategy, we have made and may continue to make or to acquire loans (including mortgage, mezzanine or other loans) with respect to any of the asset classes in which we are permitted to invest. We generally make loans to the owners of properties to enable them to acquire land, buildings or both or to develop property. In exchange, the owner generally grants us a first-lien or collateralized interest in a participating mortgage collateralized by the property or by partnership interests in a partnership that owns the property. Our loans generally require fixed interest payments and may provide for variable participating interest based on the amount of revenue generated at the encumbered property. We expect that the interest rate and terms for long-term mortgage loans (generally, 10 to 20 years) will be similar to the rate of returns on our long-term net leases. Mezzanine loans and other financings for which we have a secondary lien or collateralized interest will generally have shorter terms (one to two years) and higher interest rates than our net leases and long-term mortgage loans. With respect to the loans that we make, we generally seek loans with collateral values resulting in a loan-to-value ratio of not more than 85%.

Ancillary businesses. In addition to acquiring properties and making loans, we may invest up to 10% of our total assets in businesses that provide services to, or are otherwise ancillary to, the types of properties in which we are permitted to invest. Any ancillary investments that we may make must be consistent with our intent to remain qualified as a REIT.

Intended borrowings. We have borrowed, and intend to borrow in the future, to acquire properties, to make or acquire loans and other Permitted Investments and to pay certain fees, and intend to encumber properties in connection with these borrowings.

Lines of credit. We plan to obtain one or more lines of credit and anticipate that the aggregate amount of any lines of credit we carry will be $100 million; however, our board of directors is permitted to increase the amount we may borrow under lines of credit. We may repay lines of credit we obtain with offering proceeds, proceeds from the sale of assets, working capital or permanent financing. We currently have a $20 million unsecured revolving line of credit, but there is no assurance that we will obtain additional lines of credit on satisfactory terms.

Permanent financing. In addition to lines of credit, we anticipate obtaining permanent financing (generally, long term debt financing secured by mortgages on our properties.) The aggregate amount of

3

Table of Contents

our permanent financing is not expected to exceed 50% of our total assets on an annual basis. Our articles of incorporation limit the maximum amount of our borrowings in relation to our net assets to an amount equal to 300% of our net assets, in the absence of a satisfactory showing that a higher level of borrowing is appropriate. For us to borrow an amount in excess of 300% of our net assets, a majority of the independent directors on our board of directors must approve the borrowing, and the borrowing must be disclosed and explained to our stockholders in our first quarterly report after such approval occurs.

Duration and listing. Under our articles of incorporation, we will automatically terminate and dissolve on December 31, 2015, unless our common stock is listed on a national securities exchange or quoted on the National Market System of the NASDAQ Stock Market. If our shares are listed or quoted by that time, we will automatically become a perpetual life company. Prior to or in conjunction with listing, we anticipate merging with our Advisor and becoming self-advised.

If our shares are not listed or quoted by December 31, 2015, we will sell our assets and distribute the net sales proceeds to our stockholders or we will merge with another entity in a transaction which provides our stockholders with cash or securities of a publicly traded company, unless our stockholders owning a majority of our shares elect to extend the duration of CNL Income Properties by amendment of our articles of incorporation.

In making a determination of whether listing or quotation is in the best interest of our stockholders, our board of directors may consider a variety of criteria, including, but not limited to, market capitalization, the number of properties owned, portfolio diversification, portfolio performance, our financial condition, potential access to capital as a listed company and the potential for stockholder liquidity.

Our common stock offerings. As of December 31, 2006, we had raised approximately $1.2 billion (116.1 million shares) through our public offerings. We have and will continue to use the net proceeds from our offerings to acquire properties and make loans and other Permitted Investments.

Tax status. We currently operate and have elected to be taxed as a REIT for federal income tax purposes beginning with the taxable year ended December 31, 2004. As a REIT, we generally will not be subject to federal income tax at corporate level to the extent we distribute at least 90% of our taxable income. If we fail to qualify as a REIT in any taxable year, we will be subject to federal income tax on our taxable income at regular corporate rates and will not be permitted to qualify for treatment as a REIT for federal income tax purposes for four years following the year in which our qualification is lost.

Properties. Through separate limited partnerships and limited liability companies, we own or own interests in the following real estate investment properties (dollars are in millions). The Initial Purchase Price for properties owned through partnerships or joint ventures represents only our proportionate share of the underlying assets.

Property | Property Description | Operator | Initial Purchase Price | Date Acquired | |||||

Marinas | |||||||||

Lake Front Marina – Port Clinton, Ohio | 470 floating slips and storage facilities | Marinas International affiliate | $ | 5.6 | 12/22/06 | ||||

Sandusky Harbor Marina – Sandusky, Ohio | 660 floating slips, storage and yacht club | Marinas International affiliate | $ | 9.0 | 12/22/06 | ||||

Beaver Creek Resort – Somerset, Kentucky | 275 floating slips and boat rental | Marinas International affiliate | $ | 10.5 | 12/22/06 | ||||

4

Table of Contents

Property | Property Description | Operator | Initial Purchase Price | Date Acquired | |||||

Burnside Marina – Monticello, Kentucky | 400 floating slips and boat rental | Marinas International affiliate | $ | 7.1 | 12/22/06 | ||||

Pier 121 Marina and Easthill Park – Lewisville, Texas | 1,007 wet slips, 250 dry slips and floating restaurant | Marinas International affiliate | $ | 37.2 | 12/22/06 | ||||

Ski and Mountain Lifestyle Properties | |||||||||

Cypress Mountain – Vancouver, British Columbia | 358 skiable acres, five chairlifts, base lodge and skier service facilities | Boyne USA | $ | 27.5 | 5/30/06 | ||||

Bretton Woods Mountain Resort – Bretton Woods, New Hampshire | 434 skiable acres, nine chairlifts, base lodge and three lodging facilities | National Resort Management | $ | 45.0 | 6/23/06 | ||||

Brighton Ski Resort Brighton, Utah | 1,050 skiable acres, seven chairlifts, lodge, restaurants, skier services facility and small retail village | Boyne USA | $ | 35.0 | 1/8/07 | ||||

Northstar-at-Tahoe™ Resort Lake Tahoe, California | 2,480 skiable acres, 16 chairlifts, lodge, restaurants, shops, skier services facilities and ski school | Booth Creek Resort Properties | $ | 80.1 | 1/19/07 | ||||

Sierra-at-Tahoe® Resort South Lake Tahoe, California | 1,680 skiable acres, 12 chairlifts and full-service lodge | Booth Creek Resort Properties | $ | 39.9 | 1/19/07 | ||||

Summit-at-Snoqualmie Resort Snoqualmie Pass, Washington | 1,697 skiable acres, 26 chairlifts, ten lodges and skier services facilities | Booth Creek Resort Properties | $ | 34.5 | 1/19/07 | ||||

Loon® Mountain Resort Lincoln, New Hampshire | 275 skiable acres, ten chairlifts, base lodge, restaurants and skier services facilities | Booth Creek Resort Properties | $ | 15.5 | 1/19/07 | ||||

Destination Retail | |||||||||

Village at Blue Mountain – Ontario, Canada | 23 tenant units in 6 buildings | Intrawest | $ | 8.6 | 12/3/04 | ||||

Whistler Creekside – British Columbia, Canada | 26 tenant units in 8 buildings | Intrawest | $ | 15.6 | 12/3/04 | ||||

5

Table of Contents

Property | Property Description | Operator | Initial Purchase Price | Date Acquired | |||||

Village at Copper Mountain – Copper Mountain, Colorado | 48 tenant units in 10 buildings | Intrawest | $ | 18.6 | 12/16/04 | ||||

Village at Mammoth Mountain – Mammoth Lakes, California | 33 tenant units in 4 buildings | Intrawest | $ | 18.6 | 12/16/04 | ||||

Village of Baytowne Wharf – Destin, Florida | 30 tenant units in 14 buildings | Intrawest | $ | 13.7 | 12/16/04 | ||||

Village of Snowshoe Mountain – Snowshoe, West Virginia | 16 tenant units in 4 buildings | Intrawest | $ | 6.7 | 12/16/04 | ||||

Village at Stratton – Stratton, Vermont | 23 tenant units in 11 buildings | Intrawest | $ | 7.6 | 12/16/04 | ||||

Golf Courses | |||||||||

Palmetto Hall Plantation Club – Hilton Head, South Carolina | Two 18-hole public courses | Heritage Golf Group | $ | 7.6 | 4/27/06 | ||||

Raven Golf Club at South Mountain™ –Phoenix, Arizona | 18-hole public course | I.R.I. Golf Group | $ | 12.8 | 6/9/06 | ||||

Bear Creek Golf Club – Dallas, Texas | Two 18-hole public courses | Billy Casper Golf | $ | 11.1 | 9/8/06 | ||||

Weston Hills Country Club – Weston, Florida | Two 18-hole private courses | Heritage Golf Group | $ | 35.0 | 10/16/06 | ||||

Talega Golf Club – San Clemente, California | 18-hole public course | Heritage Golf Group | $ | 18.0 | 10/16/06 | ||||

Valencia Country Club – Santa Clarita, California | 18-hole private course | Heritage Golf Group | $ | 39.5 | 10/16/06 | ||||

Canyon Springs Golf Club – San Antonio, Texas | 18-hole public course | EAGL Golf | $ | 13.0 | 11/16/06 | ||||

Mansfield National Golf Club – Dallas-Fort Worth, Texas | 18-hole public course | EAGL Golf | $ | 7.1 | 11/16/06 | ||||

Plantation Golf Club – Dallas-Fort Worth, Texas | 18-hole public course | EAGL Golf | $ | 4.4 | 11/16/06 | ||||

Lake Park Golf Club – Dallas-Fort Worth, Texas | 18-hole semi-private course | EAGL Golf | $ | 5.6 | 11/16/06 | ||||

6

Table of Contents

Property | Property Description | Operator | Initial Purchase Price | Date Acquired | |||||

Golf Club at Fossil Creek – Fort Worth, Texas | 18-hole public course | EAGL Golf | $ | 7.7 | 11/16/06 | ||||

The Golf Club at Cinco Ranch – Houston, Texas | 18-hole public course | EAGL Golf | $ | 7.3 | 11/16/06 | ||||

Cowboys Golf Club – Grapevine, Texas | 18-hole public course | EAGL Golf | $ | 25.0 | 12/26/06 | ||||

Mesa del Sol Golf Club – Yuma, Arizona | 18-hole public course | EAGL Golf | $ | 6.9 | 12/22/06 | ||||

LakeRidge Country Club – Lubbock, Texas | 18-hole private course | EAGL Golf | $ | 7.9 | 12/22/06 | ||||

Fox Meadow Country Club – Medina, Ohio | 18-hole private course | EAGL Golf | $ | 9.4 | 12/22/06 | ||||

Painted Hills Golf Club – Kansas City, Kansas | 18-hole public course | EAGL Golf | $ | 3.9 | 12/22/06 | ||||

Signature Golf Course – Solon, Ohio | 18-hole private course | EAGL Golf | $ | 17.1 | 12/22/06 | ||||

Weymouth Country Club – Medina, Ohio | 18-hole private course | EAGL Golf | $ | 10.5 | 12/22/06 | ||||

Royal Meadows Golf Course – Kansas City, Missouri | 18-hole public course | EAGL Golf | $ | 2.4 | 12/22/06 | ||||

Clear Creek Golf Club Houston, Texas | 18-hole public course | EAGL Golf | $ | 1.9 | 1/11/07 | ||||

Merchandise Marts | |||||||||

Dallas Market Center – Dallas, Texas | 4.8 million leasable square feet | Market Center Management Company | $ | 199.2 | 2/14/05- 5/25/05 | ||||

Attractions | |||||||||

Great Wolf Lodge – Wisconsin Dells –Wisconsin Dells, Wisconsin | 76,000 square-foot waterpark, 309 guest rooms, 77 condominium units with 128 rooms and 64,000 square-foot indoor entertainment area | Great Wolf Resorts | $ | 42.0 | 10/4/05 | ||||

7

Table of Contents

Property | Property Description | Operator | Initial Purchase Price | Date Acquired | |||||

Great Wolf Lodge – Sandusky –Sandusky, Ohio | 42,000 square-foot indoor entertainment area with waterpark, 271 guest rooms, 6,000 square feet of meeting space, fitness center, arcade and gift shop | Great Wolf Resorts | $ | 38.2 | 10/4/05 | ||||

Hawaiian Falls – Garland – Garland, Texas | 11-acre waterpark | HFE Horizon | $ | 6.3 | 4/21/06 | ||||

Hawaiian Falls – The Colony – The Colony, Texas | 12-acre waterpark | HFE Horizon | $ | 5.8 | 4/21/06 | ||||

White Water Bay – Oklahoma City, Oklahoma | 21-acre waterpark | PARC Management | $ | 20.0 | 4/6/07 | ||||

Splashtown – Houston, Texas | 53-acre waterpark | PARC Management | $ | 13.7 | 4/6/07 | ||||

WaterWorld – Concord, California | 23-acre waterpark | PARC Management | $ | 10.8 | 4/6/07 | ||||

Zuma Fun Center – Charlotte, North Carolina | Miniature golf course, batting cages, bumper boats and go-karts | Trancas | $ | 7.4 | 10/6/06 | ||||

Zuma Fun Center – Knoxville, Tennessee | Miniature golf course, batting cages, bumper boats, rock climbing and go-karts | Trancas | $ | 2.0 | 10/6/06 | ||||

Zuma Fun Center – North Houston, Texas | Miniature golf course, batting cages, bumper boats and go-karts | Trancas | $ | .9 | 10/6/06 | ||||

Mountasia Family Fun Center – North Richland Hills, Texas | Two miniature golf courses, go-karts, bumper boats, batting cages, paintball fields and arcade | Trancas | $ | 1.8 | 10/6/06 | ||||

Zuma Fun Center – South Houston, Texas | Miniature golf course, batting cages, bumper boats and go-karts | Trancas | $ | 4.9 | 10/6/06 | ||||

Grand Prix Tampa – Tampa, Florida | Miniature golf course, go-kart and batting cages | Grand Prix | $ | 3.3 | 10/6/06 | ||||

Fiddlesticks Fun Center – Tempe, Arizona | Miniature golf course, bumper boats, batting cages and go-karts | Trancas | $ | 5.0 | 10/6/06 | ||||

8

Table of Contents

Property | Property Description | Operator | Initial Purchase Price | Date Acquired | |||||

Funtasticks Fun Center – Tucson, Arizona | Miniature golf course, go-karts, batting cages, bumper boats and kiddie land with rides | Trancas | $ | 6.4 | 10/6/06 | ||||

Putt Putt Fun Center – Lubbock, Texas | Batting cages, go-karts and bumper boats | Putt Putt Investments | $ | 1.8 | 10/6/06 | ||||

Putt Putt Fun Center – Raleigh, North Carolina | Batting cages, go-karts and bumper boats | Putt Putt Investments | $ | .8 | 10/6/06 | ||||

Camelot Park – Bakersfield, California | Miniature golf course, go-karts, batting cages and arcade | Trancas | $ | .9 | 10/6/06 | ||||

Gatlingburg Sky Lift – Gatlinburg, Tennessee | Scenic chairlift | Boyne USA | $ | 19.9 | 12/22/05 | ||||

Darien Lake – Buffalo, New York | 978-acre theme park and waterpark | PARC Management | $ | 109.0 | 4/6/07 | ||||

Elitch Gardens – Denver, Colorado | 62-acre theme park and waterpark | PARC Management | $ | 109.0 | 4/6/07 | ||||

Frontier City – Oklahoma City, Oklahoma | 113-acre theme park | PARC Management | $ | 17.8 | 4/6/07 | ||||

Wild Waves and Enchanted Village – Seattle, Washington | 67-acre theme park and waterpark | PARC Management | $ | 31.8 | 4/6/07 | ||||

Dealerships | |||||||||

Route 66 Harley-Davidson – Tulsa, Oklahoma | 46,000 square-foot retail and service facility with restaurant | Route 66 Real Estate | $ | 6.5 | 4/27/06 | ||||

An investment in our common stock is subject to significant risks. We summarize some of the more important risks below. A more detailed description of the risk factors is found in the section of this prospectus entitled “Risk Factors.” You should read and understand all of these risk factors before making your decision to invest our common stock.

| • | The price of our shares is subjective and may not bear any relationship to what a stockholder could receive if their shares were resold. |

| • | There is currently no market for our shares, and there is no assurance that one will develop. If our shares of common stock are not listed on a national securities exchange or quoted on the National Market System of the NASDAQ Stock Market on or before December 31, 2015, we will sell our assets and distribute the proceeds to our stockholders or merge with another entity in a transaction which provides our stockholders with cash or securities of a publicly traded company. In such instances, we will engage only in activities related to our orderly liquidation or merger, unless our stockholders owning a majority of our shares elect to extend the duration of CNL Income Properties by amending of our articles of incorporation. |

9

Table of Contents

| • | Both the number of properties that we will acquire and the diversification of our investments may be reduced to the extent that the total proceeds of the offering are substantially less than the maximum amount of the offering. |

| • | Subject to the approval of a majority of our directors, including a majority of our independent directors, we may purchase properties from or sell properties to our affiliates. |

| • | We will rely on CNL Income Corp., our Advisor and affiliate, subject to approval by our board of directors, with respect to all investment decisions. Our Advisor was formed in 2003 and has limited experience as the Advisor to a public REIT. Our Advisor and its affiliates have no previous experience investing in certain of the asset classes in which we may invest, which could result in a failure to meet our investment objectives. |

| • | Certain officers and directors of our Advisor also serve as our officers and directors, resulting in conflicts of interest. Those persons could take actions that are more favorable to other entities than to us. The Advisory Agreement was not negotiated at arm’s length and we will pay our Advisor and its affiliates substantial fees, including fees in connection with the acquisition, management and sale of our properties and fees based on permanent financing that we obtain. The fee on permanent financing may create an incentive to secure more debt despite the risk that increased debt may decrease distributions to stockholders. |

| • | To the extent consistent with our investment objectives and limitations, our investment policies and strategies may be altered by a majority of our directors, including a majority of our independent directors, without stockholder consent. |

| • | We have multiple leases and loans with certain tenants or borrowers. As a result, a default by, or the financial failure of, a tenant or borrower could cause more than one property to become vacant or more than one lease or loan to become non-performing. Vacancies would reduce our cash receipts and funds available for distribution, the repayment of outstanding debt and could decrease the resale value of affected properties until they can be re-leased. |

| • | We may, without the approval of a majority of our independent directors, incur debt totaling up to 300% of the value of our net assets, including debt to make distributions to stockholders in order to maintain our status as a REIT or otherwise. If we are unable to meet our debt service obligations, we may lose our investment in any properties that secure underlying indebtedness on which we have defaulted. |

| • | Ownership, transferability and redemption of our shares are subject to certain limitations. Our articles of incorporation generally limit the ownership by any single stockholder of any class of our capital stock to 9.8% of the outstanding shares of that class. Any transfer of shares of our capital stock that would jeopardize our REIT status shall be null and void. Redemption of our shares shall be at our sole option. |

| • | Our board of directors will have significant flexibility regarding our operations, including, for example, the ability to issue additional shares that may dilute our stockholders’ equity interests, the ability to change the compensation of our Advisor and to employ and compensate our affiliates. Our board of directors can take these actions solely on its own authority and without our stockholders’ approval. |

| • | We may make investments that will not appreciate in value over time, such as investments in building-only properties like the Dallas Market Center with the land owned by a third-party, as well as loans. |

| • | Many of the businesses associated with the properties in which we have invested and in which we seek to invest, such as ski resorts and related properties, marinas and golf courses, are seasonal in |

10

Table of Contents

nature and susceptible to periods of unprofitability resulting from adverse weather conditions which may affect the amount of revenue we receive from such tenants. |

| • | We have acquired and may continue to acquire specific-use properties, such as ski resorts and related properties, marinas and golf courses, which may not lend themselves to alternative uses. This may make it more difficult to obtain tenants in the event a property sector or class is negatively affected by poor economic trends or an existing tenant failure, which could adversely impact our cash available to pay our outstanding debt and to make distributions, as well as our liquidation value. |

| • | If we do not obtain additional lines of credit or permanent financing, we may not be able to acquire as many properties or make as many loans as we anticipate, which could limit the diversification of our investment portfolio and our ability to achieve our investment objectives. |

| • | Our loans may be affected by unfavorable real estate market conditions. When we make loans, we are at risk of default on those loans caused by many conditions beyond our control, including local and other economic conditions affecting real estate values and interest rate levels. We do not know whether the values of the properties securing mortgage loans will remain at the levels existing on the dates of origination of the loans. If the values of the underlying properties drop or in some instances fail to rise, our risk will increase and the value of our interests may decrease. |

| • | The vote of our stockholders owning at least a majority but less than all of our shares of common stock will bind all of our stockholders as to matters such as the amendment of our governing documents. Stockholders holding a majority of the shares voting at a meeting at which a quorum is present may bind all of our stockholders regarding the election of directors. |

| • | Restrictions on ownership of more than 9.8% of the outstanding shares of our common stock by any single stockholder or certain related stockholders may have the effect of inhibiting a change in control of CNL Income Properties, even if such a change is in the best interest of a majority of our stockholders. |

| • | Because we must annually distribute at least 90% of our taxable income, excluding net capital gains, to maintain our qualification as a REIT, our ability to rely upon income or cash flows from operations to finance our growth and acquisition activities may be limited. In addition, if our income or cash flow available from operations is not sufficient to cover our distribution requirement, we would need to incur borrowings to meet our distribution requirement and there is no assurance that we would be able to do so. |

| • | If we do not qualify and remain qualified as a REIT for federal income tax purposes, we would be subject to taxation on our income at regular corporate rates, which would reduce the amount of funds available for distributions to stockholders and could adversely affect the value of our securities. |

| • | We expect to pay substantial fees to our Advisor and its affiliates, which will reduce the amount of cash available for investment in properties, loans and other permitted investments, or for distribution to our stockholders. As a result of such substantial fees, we expect that approximately 85.76% to 86.07% of the total proceeds received in the offering will be available for investment in properties, loans and other permitted investments. |

We believe we are qualified and have operated as a REIT for federal income tax purposes. As a REIT, we generally will not be subject to federal income tax on income that we distribute to our stockholders. To maintain REIT status, we must meet a number of highly technical and complex organizational and operational requirements, including a requirement that we distribute at least 90% of our taxable income, as determined on an annual basis. No

11

Table of Contents

assurance can be provided that we qualify or will continue to qualify as a REIT or that new legislation, Treasury Regulations, administrative interpretations or court decisions will not significantly change the tax laws with respect to our qualification as a REIT or the federal income tax consequences of such qualification. If we fail to qualify for taxation as a REIT in any year, our income will be taxed at regular corporate rates, and we may not be able to qualify for treatment as a REIT for that year and the next four years. Even if we qualify as a REIT for federal income tax purposes, we may be subject to some federal, state and local taxes on some of our income and property, and would be subject to federal income and excise taxes on our undistributed income. In addition, some of our subsidiaries are subject to corporate income taxes. A more complete discussion of our tax status is provided under the heading “Federal Income Tax Considerations.”

The members of our board of directors oversee our business. The majority of our directors are independent of our Advisor and have responsibility for reviewing our Advisor’s performance. Our directors are elected annually by our stockholders. Although we have executive officers, all of our executive officers are also executive officers of, and employed by, our Advisor. Our executive officers have extensive previous experience investing in real estate on a triple-net lease basis. Our Chairman of the Board and Vice Chairman of the Board have over 33 and 28 years of experience, respectively, with other affiliates of CNL Holdings, Inc. We have retained our Advisor to provide us with management, acquisition, advisory and administrative services. Our Advisor has responsibility for:

| • | selecting the investments that we will make, formulating and evaluating the terms of each proposed acquisition, and arranging for the acquisition of properties; |

| • | identifying potential tenants for and/or operators of our properties and potential borrowers for our loans, and formulating, evaluating and negotiating the terms of each of our lease, loan and operating agreements; and |

| • | negotiating the terms of any borrowing by us, including lines of credit and any long-term, permanent financing. |

12

Table of Contents

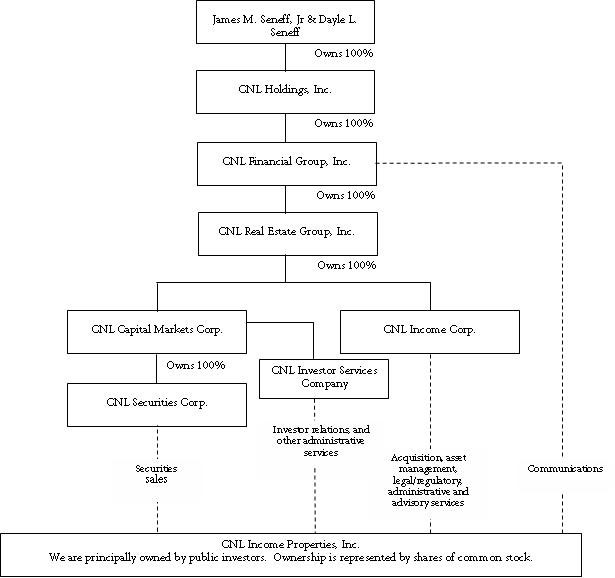

The following chart indicates the relationship between us and our Advisor, our Sponsor, and certain of our other affiliates that provide services to us.

| • | James M. Seneff, Jr. is our Chairman of the Board. He shares ownership of CNL Holdings, Inc. with his wife, Dayle L. Seneff. |

| • | James M. Seneff, Jr. and Robert A. Bourne serve as directors and/or executive officers of CNL Income Properties, Inc. In addition, they serve as directors and/or officers of various CNL entities, including CNL Income Corp., our Advisor, and CNL Securities Corp., our Managing Dealer. |

| • | CNL Real Estate Group, Inc. is the parent company of various entities that provide advisory services to us and other CNL-sponsored investment programs. |

13

Table of Contents

Conflicts of interest may exist between us and some of our affiliates. Some of our officers and directors, who are also officers or directors of our Advisor, may experience conflicts of interest in their management of us. These arise principally from their involvement in other activities that may conflict with our business and interests. Some of the conflicts that may exist between us and some of our affiliates include:

| • | competition for properties and other investments with existing affiliates, including CNL Real Estate Group, Inc., or future affiliates sponsored or controlled by James M. Seneff, Jr.; |

| • | competition for the time and services of certain persons who serve as officers and directors of our company and for our affiliates, including James M. Seneff Jr. and Robert A. Bourne, which may limit the amount of time they spend on our business matters; |

| • | the possibility that we may acquire properties that require development where our Advisor or its affiliates would receive a development fee; |

| • | substantial compensation, including fees in connection with the acquisition, management and sale of our properties and fees based on permanent financing that we obtain, will be paid to our Advisor and its affiliates, including the Managing Dealer; |

| • | the fee on permanent financing payable to our Advisor may create an incentive for our Advisor to recommend that we obtain more debt despite the risk that increased debt may decrease distributions to our stockholders; |

| • | the Asset Management fee, payable to our Advisor, may encourage the purchase and discourage the sale of investments, some of which may be speculative; |

| • | the deferred, subordinated disposition fee that may be payable to our Advisor may encourage the premature sale of properties, loans and other permitted investments; |

| • | our ability to enter into agreements with affiliates that will not be negotiated at “arms length” and, accordingly, may be less advantageous to us than if similar agreements were negotiated with non-affiliated third parties; |

| • | our Managing Dealer, CNL Securities Corp., and our Advisor will not independently review us or the offering; and |

| • | our securities and tax counsel also may serve as securities and tax counsel for some of our affiliates, including CNL Securities Corp. and CNL Financial Group, Inc., and we will not have separate counsel. |

The “Prior Performance Information” section of this prospectus contains a narrative discussion of the other real estate programs sponsored by our affiliates and our Advisor’s affiliates in the past. During the twenty-one year period ending on December 31, 2006, these entities, which invest in properties that are leased primarily on a “triple-net” lease basis or are leased to taxable REIT subsidiaries but do not invest in the types of properties in which we intend to invest, had purchased (or purchased interests in), directly or indirectly, approximately 2,100 fast-food, family-style, and casual-dining restaurant properties, 137 hotel properties and 280 retirement and other health care-related properties, including in each case properties which were sold during such period. Based on an analysis of the operating results of such prior public programs in which Mr. Seneff, our Chairman, and Mr. Bourne, our Vice Chairman and Treasurer, have served, individually or with others, as general partners or officers and directors, Messrs. Seneff and Bourne believe that each of such prior public programs has met, or is in the process of meeting,

14

Table of Contents

its principal investment objectives. Statistical data relating to certain of the public limited partnerships and the unlisted public REITs are contained in Appendix B — Prior Performance Tables.

Our primary investment objectives are to preserve, protect and enhance our assets, while:

| • | paying distributions at an increasing rate; |

| • | obtaining fixed income primarily through the receipt of base rent and providing protection against inflation primarily through periodic increases in rent and the payment of percentage rent; |

| • | owning a diversified portfolio primarily of triple-net leased real estate that will increase in value; |

| • | qualifying and remaining qualified as a REIT for federal income tax purposes; and |

| • | providing you with liquidity for your investment on or before December 31, 2015. |

COMPENSATIONTO BE PAIDTO OUR ADVISORAND AFFILIATES

We will pay to our Advisor and other affiliates of our Advisor compensation for services they will perform for us. We will also reimburse them for expenses they pay on our behalf. The following pages summarize the more significant items of compensation and reimbursement payable to our Advisor and other affiliates.

Type of Compensation and Recipient | Method of Computation and | |

| FEESPAIDINCONNECTIONWITHOUROFFERING | ||

| Selling commissions to our Managing Dealer and to participating broker-dealers | Up to 7.0% per share on all shares sold in this offering (a portion of which up to 6.5% may be re-allowed to participating broker-dealers; 0.5% to our Managing Dealer), subject to reduction in connection with certain purchases.

Estimated maximum: $136.5 million | |

| Marketing support fee to our Managing Dealer and to participating broker-dealers | 3.0% of gross offering proceeds payable to our Managing Dealer, a portion of which up to 2.5% may be re-allowed to participating broker-dealers. This 3.0% marketing support fee is subject to reduction in connection with certain purchases.

Estimated maximum: $58.5 million | |

| Other offering expenses to our Advisor | Actual expenses incurred in connection with this offering such as filing fees, printing, legal, mailing, and advertising expenses.

Estimated maximum: $16.4 million | |

| * | For purposes of calculating the “estimated maximum fees payable,” we have made assumptions as to the number of shares (and the corresponding price per share) that would be sold net of selling commissions, the marketing support fee and reduced acquisition fees. Because these figures cannot be precisely calculated at this time, the actual fees payable may exceed these estimates. |

15

Table of Contents

Type of Compensation and Recipient | Method of Computation and | |

| Due diligence expense reimbursements to participating broker-dealers | Actual expenses incurred in connection with the due diligence of CNL Income Properties, Inc. and this offering.

Estimated maximum: $2.0 million | |

| FEESPAIDINCONNECTIONWITHACQUISITIONS,INVESTMENTSORLOANS | ||

| Acquisition Fee to our Advisor | 3.0% of gross offering proceeds for services provided in connection with the selection, purchase, development or construction of real property or other investments. Estimated maximum acquisition fee: $59.9 million. Advisory fee is not determinable at this time. | |

| Acquisition Fee to our Advisor on loan proceeds | 3.0% of loan proceeds for services in connection with the incurrence of debt, from our lines of credit and permanent financing that are used to acquire properties or to make or acquire loans and other permitted investments.

Estimated maximum: $51.9 million if our permanent financing equals $1.729 billion | |

| Reimbursement to our Advisor and its affiliates for acquisition expenses | Actual expenses incurred on our behalf in connection with the selection and acquisition of properties, loans and other permitted investments.

Expenses are not determinable at this time. | |

| FEESPAIDINCONNECTIONWITHASSETMANAGEMENT | ||

| Asset Management Fee to our Advisor | Monthly payment of 0.08334% of an amount equal to the total amount invested in our properties, loans and other permitted investments (exclusive of acquisition fees and acquisition expenses), as of the end of the preceding month.

Fee is not determinable at this time. | |

FEESPAIDINCONNECTIONWITHPROPERTYSALES, LIQUIDATIONOROTHERSIGNIFICANTEVENTS | ||

| Deferred, subordinated disposition fee payable to our Advisor from the sale of our properties, loans or other permitted investments, in liquidation of CNL Income Properties, Inc. or otherwise1 | The lesser of one-half of a competitive real estate commission (generally, a fee which is reasonable, customary and competitive in light of the size, type and location of the property, as determined by our board of directors) or 3.0% of the gross sales price of the property (or comparable competitive fee in the case of a sale of a loan or other Permitted Investment).

Fee is not determinable at this time. | |

1 | We will not pay these fees until we have paid distributions to our stockholders equal to or greater than the sum of an aggregate, annual, cumulative, non-compounded 8% return on the stockholders’ aggregate invested capital plus 100% of the stockholders’ aggregate invested capital, which is what we mean when we call a fee “subordinated.” In general, we calculate our stockholders’ aggregate invested capital by multiplying the total number of shares issued and outstanding by the offering price per share, reduced by the portion of any distributions paid to our stockholders that are attributable to the sale of our properties, loans or other permitted investments. |

16

Table of Contents

Type of Compensation and Recipient | Method of Computation and | |

| Deferred, subordinated share of net sales proceeds from the sale of our assets payable to our Advisor from the sale of our properties, loans or other permitted investments, in liquidation of CNL Income Properties, Inc. or otherwise1 | 10% of the net sales proceeds from the sale of our properties, loans or other permitted investments.

Fee is not determinable at this time. | |

| Subordinated incentive fee payable to our Advisor at such time, if any, as the listing of our shares for trading on a national securities exchange or the inclusion of its common stock for quotation on the National Market System of the NASDAQ Stock Market occurs | 10% of the amount by which (i) our market value plus the total distributions made to stockholders from our inception until the date of any listing of our shares for trading on a national securities exchange or the inclusion of our common stock for quotation on the National Market System of the NASDAQ Stock Market exceeds (ii) the sum of (a) their invested capital and (b) the total distributions required to be made to our stockholders in order to pay the stockholders’ 8% return from inception through the date the market value is determined.

Fee is not determinable at this time. | |

| Performance fee payable to our Advisor upon termination of the Advisory Agreement, if the listing of our shares for trading on a national securities exchange or the inclusion of our common stock for quotation on the National Market System of the NASDAQ Stock Market has not occurred and our Advisor has met applicable performance standards | 10% of the amount by which (i) the appraised value of our assets on the date of termination of the Advisory Agreement, less any indebtedness secured by such assets, plus total distributions paid to stockholders from our inception through the termination date, exceeds (ii) the sum of 100% of invested capital plus an amount equal to the stockholders’ 8% return from inception through the termination date.

Fee is not determinable at this time. | |

Our obligation to pay some fees may be subject to conditions and restrictions or may change in some instances. We will reimburse our Advisor and its affiliates for out-of-pocket expenses that they incur on our behalf, subject to certain expense limitations.

Appropriateness of investment.An investment in our shares may provide:

| • | regular distributions because we intend to make regular cash distributions to our stockholders on a quarterly basis. |

| • | a hedge against inflation because we intend to enter into leases with tenants that provide for scheduled rent increases. |

| • | preservation of your capital with appreciation because we intend to acquire a portfolio of diverse commercial real estate assets that offer appreciation potential. |

However, we can make no assurances that these objectives will be achieved.

1 | We will not pay these fees until we have paid distributions to our stockholders equal to or greater than the sum of an aggregate, annual, cumulative, non-compounded 8% return on the stockholders’ aggregate invested capital plus 100% of the stockholders’ aggregate invested capital, which is what we mean when we call a fee “subordinated.” In general, we calculate our stockholders’ aggregate invested capital by multiplying the total number of shares issued and outstanding by the offering price per share, reduced by the portion of any distributions paid to our stockholders that are attributable to the sale of our properties, loans or other permitted investments. |

17

Table of Contents

Distribution policy.Our board of directors intends to declare distributions monthly and pay distributions quarterly during the offering period and thereafter. However, our board of directors, in its sole discretion, may determine to declare or pay distributions on another basis. We may borrow, and have borrowed, as necessary to pay distributions. The amount of distributions will generally depend on the expected and actual net cash from operations for the year, our financial condition, a balanced analysis of value creation reflective of both current and long-term stabilized cash flows from our properties, the actual operating results of each quarter, avoidance of volatility of distributions, and other factors.

Taxation of distributions.Generally, distributions that you receive will be considered ordinary income to the extent they are from current and accumulated earnings and profits. In addition, because depreciation expense reduces taxable income but does not reduce cash available for distribution, we expect that a portion of your distributions will be considered a return of capital for tax purposes. These amounts will not be subject to tax immediately but will instead reduce the tax basis of your investment. This in effect defers a portion of your tax until your investment is sold or until we liquidate or merge with another company (if such merger is treated as a taxable merger), at which time the gain will, generally, be taxable as capital gains. However, because each investor’s tax implications are different, we suggest you consult with your tax advisor before investing in our common stock. Form 1099-DIV tax information will be mailed to investors by January 31 of each year or such other deadline prescribed by the Internal Revenue Service.

Estimated use of proceeds. Approximately 86.07% (maximum offering); 85.76 % (assuming 100 million shares are sold as described in the “Estimated Use of Proceeds” section of this prospectus), to acquire properties and make loans and other investments. The balance 13.93% (maximum offering); 14.24% (assuming 100 million shares are sold) will be used to pay fees and expenses in connection with the offering, some of which are payable to our affiliates, the Managing Dealer and/or participating brokers.

Reinvestment plan.We have adopted a reinvestment plan that will allow our stockholders to have the full amount of their distributions reinvested in additional shares that may be available. We initially have registered five million shares of our common stock for this purpose.

Redemption plan.We have adopted a discretionary redemption plan that allows our stockholders who hold shares for at least one year to request that we redeem all or a portion of their shares equal to at least 25% of their shares. If we have sufficient funds available to do so and if we choose, in our sole discretion, to redeem shares, the number of shares redeemed in any calendar year and the price at which they are redeemed are subject to conditions and limitations including:

| • | no more than $100,000 of proceeds from sale of shares pursuant to any offering in any calendar quarter may be used to redeem shares (but the full amount of the proceeds from the sale of shares under the reinvestment plan attributable to any calendar quarter may be used to redeem shares presented for redemption during such quarter and any subsequent quarter); |

| • | no more than 5% of the number of shares of our common stock (outstanding at the beginning of any 12-month period) may be redeemed during such 12-month period; and |

| • | redemption pricing ranging from $9.25 per share for stockholders who have owned their shares for at least one year to $10.00 for stockholders who have owned their shares for at least four years. |

Further, our board of directors has the ability, in its sole discretion, to amend or suspend the plan, if it is deemed to be in our best interest. If we have sufficient funds and if we choose to redeem shares, the redemption price will be on such terms as our board of directors determines.

Who can help answer your questions? If you have more questions about the offering or if you would like additional copies of this prospectus, you should contact your registered representative or CNL Sales Department, Post Office Box 4920, Orlando, Florida 32802-4920; phone (866) 650-0650 or (407) 650-1000.

18

Table of Contents

An investment in our shares involves significant risks and is suitable only for those persons who understand the following material risks and who are able to bear the risk of losing their entire investment. You should consider the following material risks in addition to other information set forth elsewhere in this prospectus before making your investment decision.

The price of our shares is subjective and may not bear any relationship to what a stockholder could receive if their shares were resold.We determined the offering price of our shares in our sole discretion based on:

| • | the price at which we believed investors would pay for the shares, |

| • | estimated fees that would be paid to third parties and to our Advisor and its affiliates, |

| • | the expenses of this offering and the funds we believed should be available to invest in properties, loans and other permitted investments. |

There is no public market for the shares onwhich to base market value and there can be no assurance that one will develop.

There may be a delay in investing the proceeds from this offering due to the inability of our Advisor to find suitable properties, loans or other Permitted Investments, or tenants and operators for those investments, and therefore delay the receipt of any returns from such investments. We may delay investing the proceeds of this offering for up to the later of two years from the commencement of this offering or one year after termination of the offering, although we expect to invest substantially all of the net offering proceeds by the end of that period. Until we invest in properties, make loans or other Permitted Investments, our investment returns on offering proceeds will be limited to the rates of return available on short-term, highly liquid investments that provide appropriate safety of principal. We expect the rates of return on our investments, which affect the amount of cash available to make distributions to stockholders, to be lower than we would receive for property investments, loans or other permitted investments. These delays may be due to the inability of our Advisor to find suitable properties, loans or other permitted investments. Delays may also be caused by our Advisor’s or its affiliates’ employees who may be simultaneously trying to find suitable investments both for us and for other entities. In addition, we may be unable to find suitable tenants or operators in some sectors which could further delay the investment of proceeds. If we have not invested or committed for investment the net offering proceeds or reserved those funds for company purposes within the later of two years from the initial date of this prospectus, or one year after the termination of this offering, we will distribute the remaining funds, including accrued interest which has not been previously distributed, pro rata to the persons who are our stockholders at that time.

Selling your shares will be difficult, because there is no market for our common stock. Currently, there is no market for our shares, so stockholders may not be able to sell their shares promptly at a desired price. You should consider purchasing our shares as a long-term investment only. Although we anticipate applying for listing or quotation on or before December 31, 2015, we do not know if we will ever apply to list our shares on a national securities exchange or be included for quotation on the National Market System of the NASDAQ Stock Market or, if we do apply for listing or quotation, when such application would be made or whether it would be accepted. If our shares are listed, we cannot assure you a public trading market will develop. Further, our articles of incorporation provide that we will not apply for listing before the completion or termination of this offering. We cannot assure you that the price you would receive in a sale on a national securities exchange or on the National Market System of the NASDAQ Stock Market would be representative of the value of the assets we own or that it would equal or exceed the amount you paid for our shares. In addition, although we have adopted a redemption plan, we have discretion to not redeem your shares, to suspend the plan and to cease redemptions. The plan has many limitations and you should not rely upon it as a method of selling shares promptly and at a desired price.

19

Table of Contents

You cannot evaluate the types of properties or the specific properties that we will acquire or the loans or other permitted investments that we may make in the future. Because we have not identified all of the specific assets that we will acquire in the future, we cannot provide you with information that you may want to evaluate before deciding to invest in our shares. Our board has absolute discretion in implementing the investment policies set forth in our articles of incorporation. See “Business – Investment Focus” for discussion regarding our investment policies and strategies. While we have targeted certain types of properties in the past and will continue to do so, our investment policies and strategies are very broad and permit us to invest in many types of real estate including developed and undeveloped properties, regardless of geographic location or property type. As of April 6, 2007, we had a portfolio of 65 lifestyle properties, including interests in retail and commercial properties at seven resort villages, one merchandise mart, two waterpark resorts, five waterparks, one sky lift attraction, one dealership, 21 golf courses, seven ski properties, 11 family entertainment centers marinas and four theme parks. We have made eleven loans, ten of which are outstanding. There can be no assurance that we will invest in like properties or make similar loans in the future.

We cannot assure you that we will obtain suitable investments. We cannot be certain that we will be successful in obtaining suitable investments on financially attractive terms or that, if we make investments, our objectives will be achieved. If we are unable to find suitable investments, our financial condition and ability to pay distributions or increase the distribution rate could be adversely affected.

Our Managing Dealer has not made an independent review of us. Our Managing Dealer is an affiliate of ours and will not independently review us or this offering. Accordingly, you do not have the benefit of an independent review of the terms of this offering.

We have a limited operating history which hinders your ability to evaluate this investment. We commenced active operations in June 2004, are still in the early stages of growth and have limited performance history. As a result, you cannot be sure how we will be operated, whether we will achieve the objectives described in this prospectus or how we will perform financially. You should not rely on our past performance or the past performance of other real estate investment programs sponsored by CNL to predict our future results.