Table of Contents

As filed with the Securities and Exchange Commission on October 9, 2007

Registration No. 333-140240

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

POST-EFFECTIVE AMENDMENT NO. 1

TO

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

THE FRONTIER FUND

(a Delaware Statutory Trust)

BALANCED SERIES; GRAHAM SERIES; WINTON SERIES; CAMPBELL/GRAHAM SERIES;

CURRENCY SERIES; LONG ONLY COMMODITY SERIES;

LONG/SHORT COMMODITY SERIES; MANAGED FUTURES INDEX SERIES

(Exact Name of Registrant as Specified in its Charter)

| Delaware | 6799 | 38-6815533 | ||

| (State of Organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification Number) |

c/o Equinox Fund Management, LLC 1660 Lincoln Street, Suite 100 Denver, Colorado 80264 (303) 837-0600 (Address and telephone number of registrant’s principal executive offices) | Robert J. Enck, President & Chief Executive Officer Equinox Fund Management, LLC 1660 Lincoln Street, Suite 100 Denver, Colorado 80264 (303) 837-0600 (Name, address and telephone number of agent for service) |

Copies to:

Michael F. Griffin, Esq.

Arnold & Porter LLP

399 Park Avenue New York, New York 10022 (212) 715-1136

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, as amended, check the following box. x

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If delivery of the prospectus is expected to be made pursuant to Rule 434, please check the following box. ¨

CALCULATION OF REGISTRATION FEE

| Title of Each Series of Securities to be Registered | Maximum Aggregate Number of Securities to be Offered | Proposed Maximum Aggregate Offering† | Amount of Registration Fee‡ | |||||

Balanced Series-2 | 1,000,000 | $ | 116,850,000 | $ | 12,502.95 | |||

Long/Short Commodity Series-1 | 1,000,000 | $ | 99,420,000 | $ | 10,637.94 | |||

Long/Short Commodity Series-2 | 200,000 | $ | 20,420,000 | $ | 2,184.94 | |||

Total Units of Beneficial Interest | 2,200,000 | $ | 236,690,000 | $ | 25,325.83 | |||

| † | The proposed maximum aggregate offering for the Balanced Series Class 2, Long/Short Commodity Series Class 1 and Long/Short Commodity Series Class 2 Units has been calculated assuming that all Units were sold are sold at the Net Asset Value per Unit as of January 22, 2007. |

| ‡ | The amount of the registration fee for the Balanced Series, Long Only Commodity Series, Long/Short Commodity Series and Managed Futures Index Series of Units is calculated in reliance upon Rule 457(o) under the Securities Act and using the proposed maximum aggregate offering as described above. The amount of the registration fee has been calculated at the recently-enacted rate of $107 per million dollars of registered securities. |

Pursuant to the provisions of Rule 429 of the rules and regulations of the Commission under the Securities Act, the form of prospectus herein also relates to 2,500,000 Units registered under the Registrant’s Registration Statement on Form S-1 (Reg. No. 333-108397) declared effective on June 28, 2004, 460,000 Units registered under the Registrant’s Registration Statement on Form S-1MEF (Reg. No. 333-116949) declared effective on June 29, 2004, 11,000,000 Units registered under the Registrant’s Registration Statement on Form S-1 (Reg. No. 333-119596) declared effective on February 8, 2005, and 1,620,000 Units registered under the Registrant’s Registration Statement on Form S-1 (Reg. No. 333-129701) declared effective on February 9, 2006.

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act or until this Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

THE FRONTIER FUND

| Minimum Number of Units to be Sold during the Initial Offering Period† | Maximum Number of Units to be Offered | Price to the Public Per Unit‡ | Upfront Selling Commissions* | Proceeds to The Frontier Fund** | |||||||

Balanced Series-1: | N/A | 7,820,000 | Net Asset Value | None | 100 | % | |||||

Balanced Series-2: | 1,930,000 | Net Asset Value | None | 100 | % | ||||||

Balanced Series-1a: | N/A | 200,000 | Net Asset Value | None | 100 | % | |||||

Balanced Series-2a: | 70,000 | Net Asset Value | None | 100 | % | ||||||

Graham Series-1: | N/A | 980,000 | Net Asset Value | None | 100 | % | |||||

Graham Series-2: | 120,000 | Net Asset Value | None | 100 | % | ||||||

Winton Series-1: | N/A | 560,000 | Net Asset Value | None | 100 | % | |||||

Winton Series-2: | 90,000 | Net Asset Value | None | 100 | % | ||||||

Campbell/Graham Series-1: | N/A | 2,500,000 | Net Asset Value | None | 100 | % | |||||

Campbell/Graham Series-2: | 500,000 | Net Asset Value | None | 100 | % | ||||||

Currency Series-1: | N/A | 200,000 | Net Asset Value | None | 100 | % | |||||

Currency Series-2: | 30,000 | Net Asset Value | None | 100 | % | ||||||

Long Only Commodity Series-1: | N/A | 250,000 | Net Asset Value | None | 100 | % | |||||

Long Only Commodity Series-2: | 100,000 | Net Asset Value | None | 100 | % | ||||||

Long/Short Commodity Series-1: | N/A | 1,200,000 | Net Asset Value | None | 100 | % | |||||

Long/Short Commodity Series-2: | 250,000 | Net Asset Value | None | 100 | % | ||||||

Managed Futures Index Series-1: | N/A | 500,000 | Net Asset Value | None | 100 | % | |||||

Managed Futures Index Series-2: | 250,000 | Net Asset Value | None | 100 | % | ||||||

| 17,550,000 |

| † | The Initial Offering Period for the Balanced Series, Winton Series and Currency Series ended in September 2004, the Initial Offering Period for the Graham Series ended in November 2004, the Initial Offering Period for the Campbell/Graham Series ended in February 2005, the Initial Offering Period for the Long Only Commodity Series and the Long/Short Commodity Series ended in March 2006, the Initial Offering Period for the Managed Futures Index Series ended in April 2006 and the Initial Offering Period for the Class 1a and Class 2a of the Balanced Series ended in May 2006. |

| ‡ | During the Continuous Offering Period, Units may be purchased, and, subject to certain restrictions, Units of one Series may be exchanged for Units of another Series, at the then-current Net Asset Value per Unit of the applicable Series. |

| * | Each Series of Units is offering Units designated as Class 1 Units and Class 2 Units. In addition, the Balanced Series is offering Units designated as Class 1a Units and Class 2a Units. The Selling Agents will receive (i) with respect to all Class 1 Units and Class 1a Units sold by them, an initial service fee of up to 3.0% of the purchase price of your Units and annual on-going service fees of up to 3.0% of the Net Asset Value of your Units, and (ii) with respect to all Class 2 Units and Class 2a Units sold by them, on-going service fees of up to 0.5% of the Net Asset Value of your Units. The initial service fee will be prepaid by the Managing Owner. |

| ** | During the Continuous Offering Period, the proceeds will be turned over to such Series for trading. See “Series Subscription Minimums” on page 8 of this Prospectus. Because Equinox Fund Management, LLC will be responsible for payment of the organization and offering expenses of The Frontier Fund, except for the initial service fee, if any, 100% of the proceeds raised during the Continuous Offering Period will be initially available for each Series’ trading activities. During the Continuous Offering Period, the proceeds will be turned over to such Series for trading. See “Series Subscription Minimums” on page 8 of this Prospectus. Because Equinox Fund Management, LLC will be responsible for payment of the organization and offering expenses of The Frontier Fund, except for the initial service fee, if any, 100% of the proceeds raised during the Continuous Offering Period will be initially available for each Series’ trading activities. |

| • | The Initial Offering Period for the Balanced Series, Winton Series and Currency Series closed in September 2004, the Initial Offering Period for the Graham Series closed in November 2004, the Initial Offering Period for the Campbell/Graham Series closed in February 2005, the Initial Offering Period for the Long Only Commodity Series and the Long/Short Commodity Series closed in March 2006, the Initial Offering Period for the Managed Futures Index Series ended in April 2006 and the Initial Offering Period for the Class 1a and Class 2a of the Balanced Series ended in May 2006. Currently, Units in the Balanced Series, Graham Series, Winton Series, Campbell/Graham Series, Currency Series, Long Only Commodity Series, Long/Short Commodity Series and Managed Futures Index Series are being offered as of each day of each week and will continue to be offered until the maximum amount of each such Series’ Units which are registered are sold. The Managing Owner may terminate the Continuous Offering Period at any time. |

| • | The Selling Agents, including Bornhoft Group Securities Corporation, an affiliate of the Managing Owner, will use their “best efforts” to sell Units. This means that the Selling Agents are not required to sell any specific number or dollar amount of Units but will use their best efforts to sell the Units offered. |

| • | The Units of each Series are speculative securities and their purchase involves a high degree of risk.You should consider all risk factors before investing in any Series of The Frontier Fund. Please refer to “Risk Factors” beginning on page 22 of this Prospectus.Specifically, you should be aware that: |

| – | Futures, forward and options trading is volatile and highly leveraged |

| – | Past performance is not necessarily indicative of future results |

| – | Each Series will rely on its Trading Advisor(s) for success |

| – | You could lose a substantial portion, or even all, of your investment |

| – | Your annual tax liability is anticipated to exceed cash distributions to you |

| – | If you redeem all or a portion of your Units in Class 1 of any Series on or before the end of twelve (12) full months following the effective date of the purchase of the Units being redeemed, you will be charged a redemption fee of up to 3.0% of the Net Asset Value at which your Units are redeemed |

| – | Transfers are restricted; no market exists or is expected to exist for the Units of any Series |

| • | The Frontier Fund is not a mutual fund and is not subject to regulation under the Investment Company Act of 1940, as amended. |

NEITHER THE SECURITIES AND EXCHANGE COMMISSION NOR ANY STATE SECURITIES COMMISSION HAS APPROVED OR DISAPPROVED THESE SECURITIES, OR DETERMINED IF THIS PROSPECTUS IS TRUTHFUL OR COMPLETE. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

THE COMMODITY FUTURES TRADING COMMISSION HAS NOT PASSED UPON THE MERITS OF PARTICIPATING IN THIS POOL NOR HAS THE COMMISSION PASSED ON THE ADEQUACY OR ACCURACY OF THIS DISCLOSURE DOCUMENT.

The date of this Prospectus is October 9, 2007.

Table of Contents

| • | Each Series of Units of The Frontier Fund will engage in the speculative trading of a diversified portfolio of futures, forward (including interbank foreign currencies) and options contracts and other derivative instruments. Each Series is being separately offered, and the assets of each Series will be segregated from the other Series and separately valued. |

Series: | Units of Beneficial Interest: | Trading Advisor: | Program(s): | |||

Balanced | 10,020,000 | Major Advisors: Campbell & Company, Inc Quantitative Investment Management, LLC |

Financial, Metal & Energy Large Portfolio Diversified 2XL International Value Program

Global | |||

| Winton Capital Management Ltd. | DTP/Enhanced Risk USD | |||||

| Non-Major Commodity Trading Advisors | Various Programs | |||||

| Emerging Managers (allocation of <5%) | Various Programs | |||||

| Strategic Allocations | Various Programs | |||||

| Swaps | Renaissance Technologies Corp.-RIFF trading program Transtrend B.V - DTP-Enhanced Risk (USD) Diversified Program | |||||

Graham | 1,100,000 | Graham Capital Management, L.P. | K-4 Program at 150% leverage | |||

Winton | 650,000 | Winton Capital Management Ltd. | Diversified Program | |||

Campbell/Graham | 3,000,000 | Campbell & Company, Inc. Graham Capital Management, L.P. | Financial, Metal & Energy Large Portfolio K-4 Program at 150% leverage | |||

Currency | 230,000 | C-View International Limited | Currency Program | |||

| Gain Capital Asset Management LLC | Gain MAC-2x Program | |||||

| Swap | FX Concepts, Inc.-Global Currency Program; Developed Markets Currency program | |||||

Long Only Commodity | 350,000 | Swaps | Reuters/Jefferies CRB Index Jefferies Commodity Performance Index | |||

Long/Short Commodity | 1,450,000 | AIS Futures Management, LLC Cornerstone Quantitative Investment Group, Inc. Kottke Associates, LLC Red Oak Commodity Advisors, Inc. | MAAP Program International Value Program; Real Commodity Analysis Program Swinford Program; JVPT Program Fundamental Trading Program | |||

| Non-Major Commodity Trading Advisors | Various Programs | |||||

Managed Futures Index | 750,000 | Conquest Capital, LLC | Conquest Managed Futures Select Program |

| • | Once trading commences for the Series in which you have invested, you may purchase additional Units in such Series, Exchange your Units in one Series for Units in another Series which has also commenced trading or may redeem your Units on a daily basis. Exchanges will be available between the various Class 1 Units of the Series of Units, and Exchanges will be available between the various Class 2 Units. However, it is important to note that Exchanges will not be allowed from Class 1 to Class 2 or vice versa. In addition, you will only be allowed to Exchange your Units in one Series for Units in another Series which is registered for sale in your State. Furthermore, Exchanges will be allowed out of the Graham Series, but Exchanges into the Graham Series will be restricted to those investors that have purchased their Units through a Selling Agent that acts as a selling agent for the Graham Series. |

| • | In general, your minimum initial subscription is $1,000, or, if you are a Plan (including an IRA), an employee or family member of an employee of the Managing Owner or its affiliates or a charitable organization, you have no minimum initial subscription requirements. Your minimum initial purchase in any one Series is $1,000, and, if you are an existing Limited Owner, you will be able to purchase additional Units in increments of $100. If you are a Plan (including an IRA), an employee or family member of an employee of the Managing Owner or its affiliates or a charitable organization, you have no minimum on the amount of additional Units that may be purchased. |

Table of Contents

COMMODITY FUTURES TRADING COMMISSION

YOU SHOULD CAREFULLY CONSIDER WHETHER YOUR FINANCIAL CONDITION PERMITS YOU TO PARTICIPATE IN A COMMODITY POOL. IN SO DOING, YOU SHOULD BE AWARE THAT FUTURES AND OPTIONS TRADING CAN QUICKLY LEAD TO LARGE LOSSES AS WELL AS GAINS. SUCH TRADING LOSSES CAN SHARPLY REDUCE THE NET ASSET VALUE OF THE POOL AND CONSEQUENTLY THE VALUE OF YOUR INTEREST IN THE POOL. IN ADDITION, RESTRICTIONS ON REDEMPTIONS MAY AFFECT YOUR ABILITY TO WITHDRAW YOUR PARTICIPATION IN THE POOL.

FURTHER, COMMODITY POOLS MAY BE SUBJECT TO SUBSTANTIAL CHARGES FOR MANAGEMENT, AND ADVISORY AND BROKERAGE FEES. IT MAY BE NECESSARY FOR THOSE POOLS THAT ARE SUBJECT TO THESE CHARGES TO MAKE SUBSTANTIAL TRADING PROFITS TO AVOID DEPLETION OR EXHAUSTION OF THEIR ASSETS. THIS DISCLOSURE DOCUMENT CONTAINS A COMPLETE DESCRIPTION OF EACH EXPENSE TO BE CHARGED THIS POOL AT PAGES 53 THROUGH 60 AS WELL AS IN THE APPENDICES ATTACHED TO THIS PROSPECTUS FOR EACH SERIES OF UNITS AND A STATEMENT OF THE PERCENTAGE RETURN NECESSARY TO BREAK EVEN, THAT IS, TO RECOVER THE AMOUNT OF YOUR INITIAL INVESTMENT IN THE SUPPLEMENT TO THIS PROSPECTUS FOR EACH INDIVIDUAL SERIES.

THIS BRIEF STATEMENT CANNOT DISCLOSE ALL THE RISKS AND OTHER FACTORS NECESSARY TO EVALUATE YOUR PARTICIPATION IN THIS COMMODITY POOL. THEREFORE, BEFORE YOU DECIDE TO PARTICIPATE IN THIS COMMODITY POOL, YOU SHOULD CAREFULLY STUDY THIS DISCLOSURE DOCUMENT, INCLUDING A DESCRIPTION OF THE PRINCIPAL RISK FACTORS OF THIS INVESTMENT AT PAGES 18 THROUGH 33.

YOU SHOULD ALSO BE AWARE THAT THIS COMMODITY POOL MAY TRADE FOREIGN FUTURES OR OPTIONS CONTRACTS. TRANSACTIONS ON MARKETS LOCATED OUTSIDE THE UNITED STATES, INCLUDING MARKETS FORMALLY LINKED TO A UNITED STATES MARKET, MAY BE SUBJECT TO REGULATIONS WHICH OFFER DIFFERENT OR DIMINISHED PROTECTION TO THE POOL AND ITS PARTICIPANTS. FURTHER, UNITED STATES REGULATORY AUTHORITIES MAY BE UNABLE TO COMPEL THE ENFORCEMENT OF THE RULES OF REGULATORY AUTHORITIES OR MARKETS IN NON UNITED STATES JURISDICTIONS WHERE TRANSACTIONS FOR THE POOL MAY BE EFFECTED.

THIS POOL HAS A LIMITED PERFORMANCE HISTORY.

| • | You should rely only on the information contained in this Prospectus or incorporated by reference which legally forms a part of the Prospectus. We have not authorized anyone to provide you with information that is different. |

| • | This Prospectus is in two parts: a disclosure document and a statement of additional information attached as Part II to this Prospectus, or the Statement of Additional Information. These parts are bound together, and both parts contain important information. |

| • | This Prospectus is not an offer to sell, nor is it seeking an offer to buy these securities in any jurisdiction where the offer or sale is not permitted. |

| • | There is no guarantee that information in this Prospectus is correct as of any time after the date appearing on the cover. |

| • | The Trust is not a mutual fund or any other type of investment company within the meaning of the Investment Company Act of 1940, as amended, and is not subject to the regulations under the Investment Company Act. |

Table of Contents

| • | This Prospectus must be accompanied by a recent monthly report of the Trust. |

| • | The Selling Agents of the Trust must deliver any supplemented or amended Prospectus issued by the Trust. |

| • | You should not invest more than 10% of your net worth (exclusive of home, furnishings and automobiles in the case of individuals; or readily marketable securities in the case of entities) in any Series of Units of the Trust, or in the Trust as a whole. |

Table of Contents

Page | ||

PART I: | ||

| 1 | ||

| 22 | ||

| 42 | ||

| 43 | ||

| 44 | ||

DESCRIPTION OF THE TRUST, TRUSTEE, MANAGING OWNER AND AFFILIATES | 47 | |

| 58 | ||

| 60 | ||

| 61 | ||

| 61 | ||

| 63 | ||

| 66 | ||

| 66 | ||

| 76 | ||

| 80 | ||

| 81 | ||

| 84 | ||

| 85 | ||

| 103 | ||

| 106 | ||

| 107 | ||

| 107 | ||

| 107 | ||

| 107 | ||

| Fin. - 1 | ||

APPENDICES TO PART I | ||

| Balanced App. – 1 | ||

| Graham App. – 1 | ||

| Winton App. – 1 | ||

| Campbell/Graham App. – 1 | ||

| Currency App. – 1 | ||

| Long Only Commodity App. – 1 | ||

| Long/Short Commodity App. – 1 | ||

| Managed Futures Index App. – 1 | ||

PART II: STATEMENT OF ADDITIONAL INFORMATION | ||

| SAI-1 | ||

| SAI-7 | ||

| SAI-11 | ||

| SAI-15 | ||

| SAI-16 | ||

| SAI-35 | ||

| SAI-66 | ||

Table of Contents

Page | ||

EXHIBITS: | ||

Exhibit A – Amended and Restated Declaration of Trust and Trust Agreement | A-1 | |

| B-1 | ||

| C-1 | ||

| D-1 | ||

| E-1 | ||

Exhibit F – Application for Transfer of Ownership / Re-registration Form | F-1 | |

| G-1 | ||

Table of Contents

This summary of all material information provided in this Prospectus is intended for quick reference only. The remainder of this Prospectus contains more detailed information; you should read the entire Prospectus, including the Statement of Additional Information and all exhibits to the Prospectus, before deciding to invest in any Series of Units. This Prospectus is intended to be used beginning , 2007.

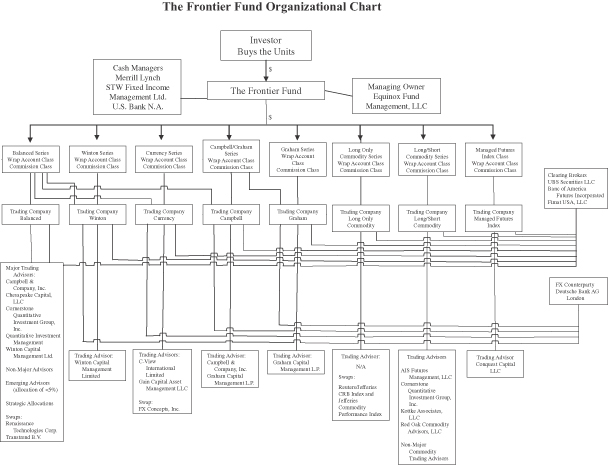

The Trust | The Frontier Fund, or the Trust, was formed as a Delaware statutory trust on August 8, 2003, with separate series, or each, a Series, of units of beneficial interest, or the Units. Its term will expire on December 31, 2053 (unless terminated earlier in certain circumstances). The principal offices of the Trust and Equinox Fund Management, LLC, or the Managing Owner, are located at 1660 Lincoln Street, Suite 100, Denver, Colorado 80264, and their telephone number is (303) 837-0600. See “Trust Agreement.” The Trust is a multi-advisor commodity pool as described in Commodity Futures Trading Commission, or CFTC, Regulation § 4.10(d)(2). |

The Series | The Trust’s Units are being offered in eight (8) separate and distinct Series: Balanced Series, Graham Series, Winton Series, Campbell/Graham Series, Currency Series, Long Only Commodity Series, Long/Short Commodity Series and Managed Futures Index Series. The Trust may issue future Series of Units. The Units of the Graham Series, Winton Series, Campbell/Graham Series, Currency Series, Long Only Commodity Series, Long/Short Commodity Series and Managed Futures Index Series will be separated into two sub-classes, or each, a Sub-Class, of Units, and the Units of the Balanced Series will be separated into four Sub-Classes of Units. The Trust, with respect to each Series, will: |

• engage in the speculative trading of a diversified portfolio of futures, forward (including interbank foreign currencies) and options contracts and other derivative instruments and may, from time to time, engage in cash and spot transactions; |

• allocate funds, directly or indirectly, to a subsidiary trading vehicle or managed account or invest in a limited liability company, limited partnership or other investment vehicle, or each, a Trading Company. Except for the Trading Company established for the Long Only Commodity Series, each Trading Company will have one-year renewable contracts with its own independent commodity trading advisor(s), or each, a Trading Advisor, that will manage all or a portion of such Trading Company’s assets, make the trading decisions for the assets of each Series vested in such Trading Company, segregate its assets from any other Trading Company and maintain separate, distinct records for each Series, and account for its assets separately from the other Series and the other Trust assets; |

• calculate the net assets, or the Net Asset Value, of its Units separately from the other Series; |

• have an investment objective of increasing the value of your Units over the long term (capital appreciation), while controlling risk and volatility; further, to offer exposure to the investment programs of |

1

Table of Contents

individual Trading Advisors and to specific instruments (e.g., currencies); |

• offer Units in the Graham Series, Winton Series, Campbell/Graham Series, Currency Series, Long Only Commodity Series, Long/Short Commodity Series and Managed Futures Index Series in two Sub-Classes—Class 1 and Class 2; and |

• offer Units in the Balanced Series in four Sub-Classes—Class 1, Class 2, Class 1a and Class 2a. |

Class 1 Units, Class 2 Units, Class 1a Units and Class 2a Units | • Investors who purchase Class 1 Units of the Balanced Series, Winton Series, Campbell/Graham Series, Currency Series, Graham Series or Long/Short Commodity Series, as well as investors who purchase Class 1a Units of the Balanced Series, will be charged an initial service fee up to three percent (3.0%) of the Net Asset Value of each Unit purchased, for the benefit of Selling Agents selling Class 1 Units, or Class 1a Units, as applicable. The Managing Owner will prepay the initial service fee for bona fide transactions, which initial service fee will be amortized monthly at an annual rate of up to three percent (3.0%) of the average daily Net Asset Value of Class 1 or Class 1a, as applicable, of such Series, provided, however, that investors who redeem all or a portion of their Class 1 Units or Class 1a Units of any Series during the first twelve (12) months following the effective date of their purchase will be subject to a redemption fee of up to three percent (3.0%) of the Net Asset Value at which such investor redeemed to reimburse the Managing Owner for the then-unamortized balance of the prepaid initial service fee. In addition, after the expiration of twelve (12) months following the purchase of Class 1 Units of the Balanced Series, Winton Series, Campbell/Graham Series, Currency Series or Graham Series, investors who purchased Class 1 Units of such Series will be charged an annual on-going service fee of up to three percent (3.0%) of the Net Asset Value of each Unit purchased, for the benefit of Selling Agents selling Class 1 Units for on-going services provided to the Trust and the Limited Owners by the Selling Agents. |

• After the expiration of twelve (12) months following the purchase of Class 1 Units of the Long/Short Commodity Series or Class 1a Units of the Balanced Series, investors who purchased Class 1 Units or Class 1a Units, as applicable, of such Series will be charged an annual on-going service fee of up to three percent (3.0%) of the Net Asset Value of each Unit purchased, for the benefit of Selling Agents selling Class 1 Units or Class 1a Units, as applicable, for on-going services provided to the Trust and the Limited Owners by the Selling Agents. The on-going service fee with respect to the Class 1 Units of the Long/Short Commodity Series or Class 1a Units of the Balanced Series will continue only until the aggregate initial service fees and on-going service fees received by the Selling Agent with respect to such Units total ten percent (10%) of the purchase price of such Class 1 Units of such Series. |

2

Table of Contents

• Investors who purchase Class 1 Units of the Long Only Commodity Series or the Managed Futures Index Series will be charged an initial service fee up to two percent (2.0%) of the Net Asset Value of each Unit purchased, for the benefit of Selling Agents selling Class 1 Units. The Managing Owner will prepay the initial service fee for bona fide transactions, which initial service fee will be amortized monthly at an annual rate of up to two percent (2.0%) of the average daily Net Asset Value of Class 1 of such Series, provided, however, that investors who redeem all or a portion of their Class 1 Units of such Series during the first twelve (12) months following the effective date of their purchase will be subject to a redemption fee of up to two percent (2.0%) of the Net Asset Value at which such investor redeemed to reimburse the Managing Owner for the then-unamortized balance of the prepaid initial service fee. |

• After the expiration of twelve (12) months following the purchase of Class 1 Units of the Long Only Commodity Series or the Managed Futures Index Series, investors who purchased Class 1 Units of such Series will be charged an annual on-going service fee of up to two percent (2.0%) of the Net Asset Value of each Unit purchased, for the benefit of Selling Agents selling Class 1 Units for on-going services provided to the Trust and the Limited Owners by the Selling Agents. The on-going service fee with respect to the Class 1 Units of the Long Only Commodity Series or the Managed Futures Index Series will continue only until the aggregate initial service fees and on-going service fees received by the Selling Agent with respect to such Units total ten percent (10%) of the purchase price of such Class 1 Units of such Series. |

• Class 2 Units and Class 2a Units may only be offered to investors who are represented by approved Selling Agents who are directly compensated by the investor for services rendered in connection with an investment in the Trust (such arrangements commonly referred to as “wrap-accounts”). Investors who purchase Class 2 Units of any Series or Class 2a Units of the Balanced Series will be charged no initial service fee. However, the Managing Owner may pay the Selling Agents an on-going service fee of up to 0.5% annually of the Net Asset Value of each Class 2 Unit or Class 2a Unit sold by them for certain administrative services. The on-going service fee payable to the Selling Agents with respect to the Class 2 Units of the Long Only Commodity Series, the Long/Short Commodity Series and the Managed Futures Index Series and the Class 2a Units of the Balanced Series will continue until the aggregate initial service fees and on-going service fees received by the Selling Agent with respect to such Units total ten percent (10%) of the purchase price of such Class 2 Units or Class 2a Units of such Series. The on-going service fee payable to the Selling Agents with respect to the Class 2 Units of the Balanced Series sold on or after November 10, 2007, will continue until the aggregate initial service fees and on-going service fees received by the Selling Agent with respect to such Units total ten percent (10%) of the purchase price of such Class 2 Units of such |

3

Table of Contents

Series. The on-going service fee payable to the Selling Agents with respect to the Class 2 Units of the Winton Series sold on or after November 10, 2007, will continue until the aggregate initial service fees and on-going service fees received by the Selling Agent with respect to such Units total ten percent (10%) of the purchase price of such Class 2 Units of such Series. The Managing Owner will pay such on-going service fee out of brokerage commissions and fees paid to the Managing Owner and the Clearing Brokers. See “Fees and Expenses—Charges to be paid by the Trust—Brokerage Commissions and Fees.” |

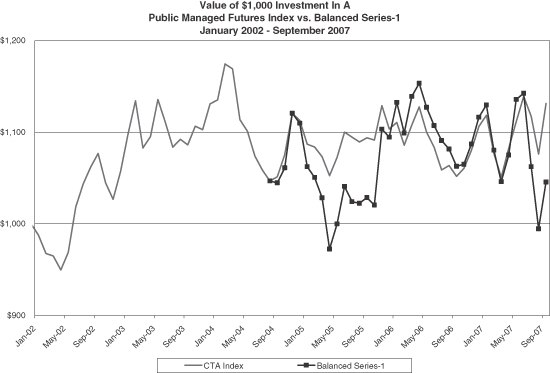

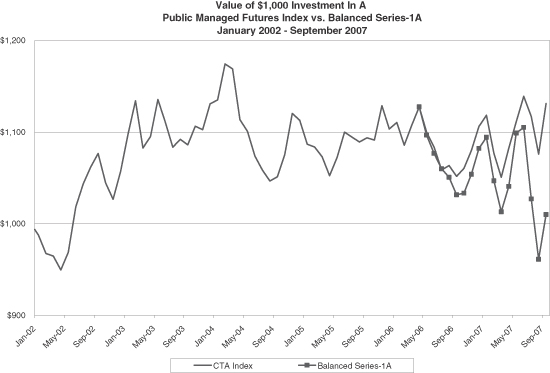

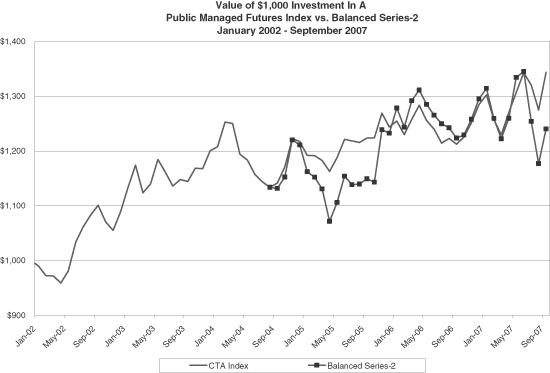

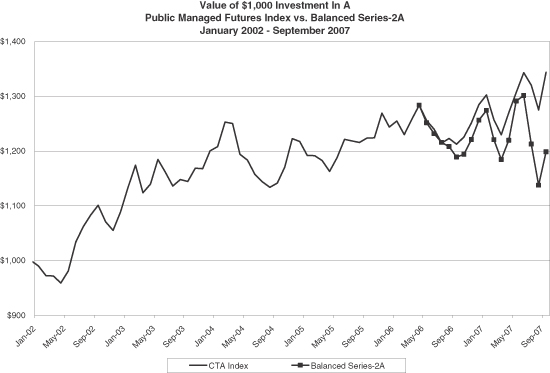

Balanced Series | Trading for the Balanced Series will be directed by a group of Trading Advisors, including Campbell & Company, Inc., or Campbell, Chesapeake Capital Corporation, or Chesapeake, Cornerstone Quantitative Investment Group, Inc., or Cornerstone; Quantitative Investment Management, LLC, or QIM, Winton Capital Management Ltd., or Winton, one or more Trading Advisors designated as “non-major commodity trading advisors” to the Balanced Series; and one or more Trading Advisors designated as “Emerging Managers” to the Balanced Series. The Managing Owner anticipates that between ten percent (10%) and twenty percent (20%) of the Balanced Series’ assets will be allocated to each Trading Advisor designated as a “major commodity trading advisor” that is trading in such Series and that less than ten percent (10%) of the Balanced Series’ assets will be allocated to each Trading Advisor described as a “non-major commodity trading advisor” or an “Emerging Manager” that is trading in such Series. In addition, a portion of the assets of the Balanced Series will be allocated to the Trading Company for the Currency Series, the Trading Company for the Long Only Commodity Series, the Trading Company for the Long/Short Commodity Series and the Trading Company for the Managed Futures Index Series. The actual allocation of the Balanced Series’ assets will vary based upon the trading performance of the Trading Advisors and the Managing Owner’s asset allocation activities. The Managing Owner may appoint additional, replacement or substitute Trading Advisors, subject to its review and due diligence. Other or additional trading programs and Trading Advisors may be used in the future. The Balanced Series will also strategically invest assets in one or more swap contracts, or Swaps, including a Swap that references Renaissance Technologies Corp.’s, or Renaissance’s, RIFF trading program and a Swap that references Transtrend B.V.’s, or Transtrend’s, DTP-Enhanced Risk (USD) Diversified Program. The Trading Company in which the assets of the Balanced Series will be invested will not own any of the investments or indices referenced by any Swap entered into by the Balanced Series, and Renaissance and Transtrend therefore are not and will not be Trading Advisors to the Balanced Series. See the appendix for the Balanced Series Units attached to Part I of this Prospectus, or the Balanced Series Appendix. |

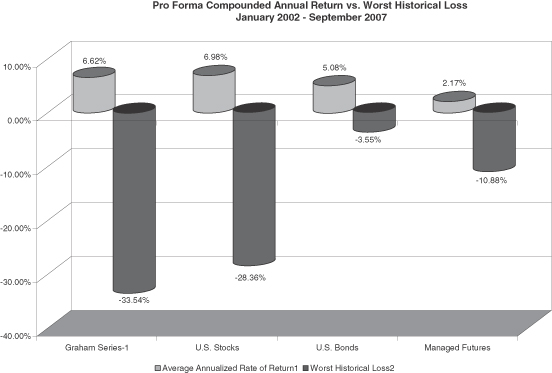

Graham Series | Trading for the Graham Series will be directed by Graham Capital Management, L.P., or Graham. Graham will trade 100% of Graham Series’ assets pursuant to its K-4 program at 150% leverage. Other or |

4

Table of Contents

additional trading programs may be used in the future. See the appendix for the Graham Series Units attached to Part I of this Prospectus, or the Graham Series Appendix. |

Winton Series | The Winton Series was originally designated as the “Beach Series,” and trading for the Winton Series was directed by Beach Capital Management Ltd. As the Series will be directed by Winton, its name was changed to the “Winton Series.” Trading for the Winton Series will be directed by Winton. Winton will trade 100% of Winton Series’ assets pursuant to its diversified program. Other or additional trading programs may be used in the future. See the appendix for the Winton Series Units attached to Part I of this Prospectus, or the Winton Series Appendix. |

Campbell/Graham Series | Trading for the Campbell/Graham Series will be directed by Campbell and Graham. The Managing Owner anticipates that each of Campbell and Graham will be allocated approximately 50% of Campbell/Graham Series’ assets. The actual allocation of the Campbell/Graham Series’ assets may vary based upon the trading performance of the Trading Advisors and the Managing Owner’s asset allocation activities. Campbell will trade the portion of Campbell/Graham Series’ assets allocated to it pursuant to its Financial, Metal & Energy Large Portfolio and Graham will trade the portion of Campbell/Graham Series’ assets allocated to it pursuant to its K-4 program at 150% leverage. The Managing Owner may appoint additional, replacement or substitute Trading Advisors, subject to its review and due diligence. Other or additional trading programs and Trading Advisors may be used in the future. See the appendix for the Campbell/Graham Series Units attached to Part I of this Prospectus, or the Campbell/Graham Series Appendix. |

Currency Series | The Currency Series was originally a single-advisor Series designated as the “C-View Currency Series.” As trading for the Series is now directed by multiple Trading Advisors, its name was changed to the “Currency Series.” Trading for the Currency Series will be directed by a group of Trading Advisors, including C-View International Limited, or C-View and GAIN Capital Asset Management LLC, or Gain. The Managing Owner anticipates that between ten percent (10%) and fifty percent (50%) of the Currency Series’ assets will be allocated to each Trading Advisor designated as a “major FX trading advisor” that is trading in such Series. The actual allocation of the Currency Series’ assets will vary based upon the trading performance of the Trading Advisors and the Managing Owner’s asset allocation activities. The Managing Owner may appoint additional, replacement or substitute Trading Advisors, subject to its review and due diligence. Other or additional trading programs may be used in the future. The Currency Series will also strategically invest assets in one or more Swaps including a Swap that references FX Concepts, Inc.’s, or FX Concepts’, Global Currency Program and Developed Markets Currency program. The Trading Company in which the assets of the Currency Series will be invested will not own any of the investments or indices referenced by any Swap entered into by the Currency Series, and FX Concepts therefore is not and will not be a Trading Advisor to the Currency Series. See the appendix for the |

5

Table of Contents

Currency Series Units attached to Part I of this Prospectus, or the Currency Series Appendix. |

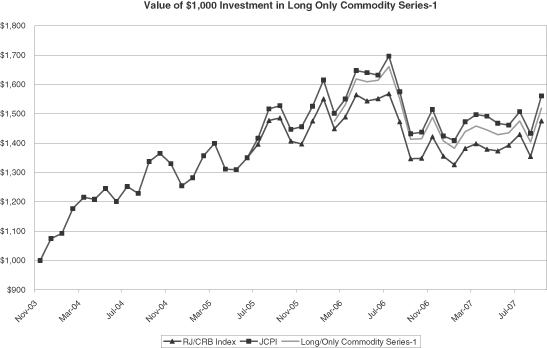

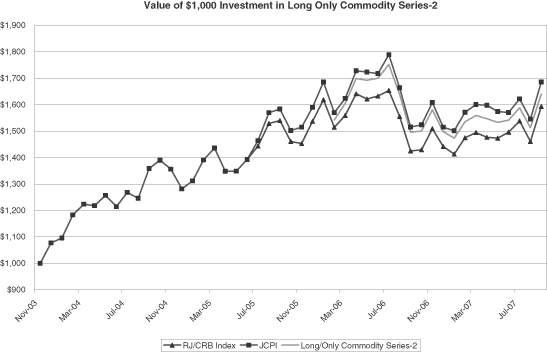

Long Only Commodity Series | Trading for the Long Only Commodity Series will be directed by the Managing Owner, pursuant to the limited liability company agreement governing the Trading Company to which assets of the Long Only Commodity Series will be allocated. 50% of the Long Only Commodity Series’ assets will be invested in a swap which will track the performance, positive or negative, of the Reuters/Jefferies CRB Index and 50% of the Long Only Commodity Series’ assets will be invested in Swaps which will track the performance, positive or negative, of the Jefferies Commodity Performance Index, in each case less the costs of the Swaps. Other or additional trading programs may be used in the future. See the appendix for the Long Only Commodity Series Units attached to Part I of this Prospectus, or the Long Only Commodity Series Appendix. |

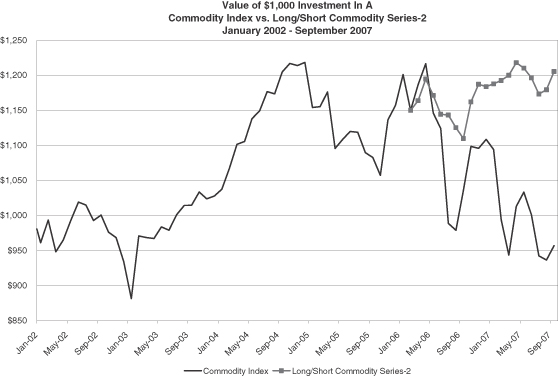

Long/Short Commodity Series | Trading for the Long/Short Commodity Series will be directed by a group of Trading Advisors, including AIS Futures Management, LLC, or AIS, Cornerstone, Kottke Associates, LLC, or Kottke, Red Oak Commodity Advisors, Inc., or Red Oak, and a group of non-major commodity trading advisors to the Long/Short Commodity Series. The Managing Owner anticipates that between ten percent (10%) and twenty percent (20%) of the Long/Short Commodity Series’ assets will be allocated to each Trading Advisor designated as a “major commodity trading advisor” that is trading in such Series and less than ten percent (10%) of the Long/Short Commodity Series’ assets will be allocated to each Trading Advisor designated as a “non-major commodity trading advisor.” The actual allocation of the Long/Short Commodity Series’ assets will vary based upon the trading performance of the Trading Advisors and the Managing Owner’s asset allocation activities. The Managing Owner may appoint additional, replacement or substitute trading advisors, subject to its review and due diligence. Other or additional trading programs and Trading Advisors may be used in the future. See the appendix for the Long Short Commodity Series Units attached to Part I of this Prospectus, or the Long/Short Commodity Series Appendix. |

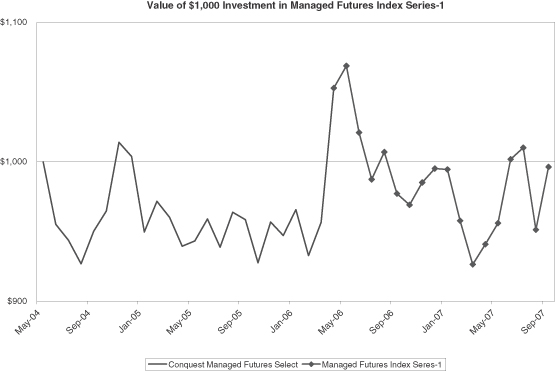

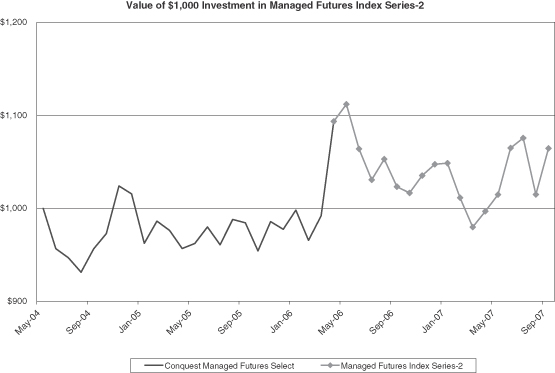

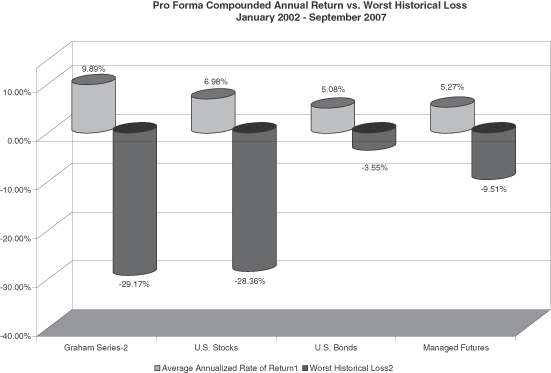

Managed Futures Index Series | Trading for the Managed Futures Index Series will be directed by Conquest. Conquest will trade 100% of Managed Futures Index Series’ assets pursuant to its Conquest Managed Futures Select program. Other or additional trading programs may be used in the future. See the appendix for the Managed Futures Index Series Units attached to Part I of this Prospectus, or the Managed Futures Index Series Appendix. |

Appendices | The Balanced Series Appendix, the Graham Series Appendix, the Winton Series Appendix, the Campbell/Graham Series Appendix, the Currency Series Appendix, the Long Only Commodity Series Appendix, the Long/Short Commodity Series Appendix and the Managed Futures Index Series Appendix are individually referred to in the abstract as an Appendix and collectively referred to as the Appendices. |

6

Table of Contents

Investment Risks | UNITS IN EACH SERIES ARE SPECULATIVE SECURITIES AND AN INVESTMENT IN ANY SERIES OF THE TRUST INVOLVES A HIGH DEGREE OF RISK. YOU SHOULD BE AWARE THAT: |

• The Trust has a limited operating history; |

• With respect to all Series, the Trading Advisors may use additional trading programs that are not identified in this Prospectus and, with respect to the Balanced Series, the Campbell/Graham Series, the Currency Series and the Long/Short Commodity Series, the Managing Owner may appoint additional or replacement Trading Advisors that are not identified in this Prospectus, in each case without the approval of the holders of Units in such Series; |

• Purchasers of Class 1 Units or Class 1a Units in any Series will have to pay a redemption fee of up to 3% of the Net Asset Value of any such Units redeemed during the first twelve (12) months after purchase; |

• The incentive nature of the compensation to be paid to the Trading Advisors may encourage the Trading Advisors to take riskier or more speculative positions; |

• Futures, forward and options trading is speculative, volatile and highly leveraged. Due to the volatile nature of the commodities markets and the high degree of leverage to the employed by the Trust, a relatively small change in the price of a contract can cause significant losses for the Trust. |

• The Trading Advisors’ programs may not perform for each Series as they have performed in the past; |

• Each of the Trust’s Series relies on its Trading Advisor(s) for success; |

• There is no guarantee that the Trust, with respect to any Series, will meet its intended objective; accordingly, you could lose a substantial portion, or even all, of your investment; |

• Your annual tax liability may exceed cash distributions to you; |

• Substantial expenses will be incurred by the investors in each Series, regardless of the performance of that Series. We estimate that the Trust, with respect to each Series, will have to achieve net trading profits (after taking interest income into account) of between from -2.13% to 4.22% each year for investors to break-even on their investments; |

• Transfers are restricted. No trading market exists or is expected to exist for the Units of any Series; |

• Actual and potential conflicts of interest exist among the Managing Owner and the Trading Advisors. The full attention and efforts of the Managing Owner and the Trading Advisors will not be devoted to the activities of the Trust. The Managing Owner and some of the Trading Advisors may have business arrangements between them that do not |

7

Table of Contents

directly relate to the Trust’s business. The Managing Owner and the Trading Advisors may trade in commodities for their own accounts. The Managing Owner does not intend to effect any distributions by the Trust, thus increasing the management fees payable to it and the Trading Advisors; |

• You will have limited voting rights and no control over the Trust’s business; and |

• Unless the Series in which you invest is successful—and we cannot assure you that it will be—it cannot serve as a beneficial diversification for your portfolio. |

The Trustee | Wilmington Trust Company, or the Trustee, a Delaware banking corporation, is the Trust’s sole trustee. The Trustee delegated to the Managing Owner all of the power and authority to manage the business and affairs of the Trust and has only nominal duties and liabilities to the Trust. |

The Managing Owner | Equinox Fund Management, LLC is a limited liability company formed in the state of Delaware in June 2003. The Managing Owner is the Trust’s and each Series’ commodity pool operator, or CPO, and will administer the business and affairs of each Series (excluding commodity trading decisions, except in certain limited, and essentially emergency, situations). See “Actual and Potential Conflicts of Interest.” The Managing Owner will make a contribution to Series of the Trust necessary to maintain at least a 1% interest in the aggregate profits and losses of all Series at all times. See “Managing Owner’s Commitments—Minimum Purchase Commitment” and “Managing Owner’s Commitments—Net Worth Commitment.” Under the Trust Agreement, the Managing Owner has agreed to accept liability for the obligations of each Series that exceed that Series’ net assets. See “Trust Agreement.” |

The Clearing Brokers | UBS Securities LLC, or UBS Securities, Banc of America Securities LLC, or Banc of America Securities and Fimat USA, LLC, or Fimat USA, act as certain of the Trading Company’s futures clearing brokers, or the Futures Clearing Brokers. Deutsche Bank AG London, or Deutsche Bank, serves certain Trading Companies which trade over-the-counter foreign currencies as the foreign exchange counterparty, or the FX Counterparty. The Futures Clearing Brokers and the FX Counterparty are collectively referred to as the Clearing Brokers. The Clearing Brokers will execute and clear the Trading Company’s futures, options and over-the-counter foreign currency transactions, as applicable, and will perform certain administrative services for each Trading Company. |

The Selling Agents | Bornhoft Group Securities Corporation, an affiliate of the Managing Owner, acts as a selling agent of the Trust. The Managing Owner intends to appoint certain other broker-dealers registered under the Securities Exchange Act of 1934, as amended, and members of the Financial Industry Regulatory Authority, or FINRA, as the Trust’s selling agents (collectively with Bornhoft Group Securities Corporation, the Selling Agents). The Selling Agents will use their “best efforts” to sell Units. This means that the Selling Agents are not required to sell any specific |

8

Table of Contents

number or dollar amount of Units but will use their best efforts to sell the Units offered. |

Liabilities You Assume | Although the Managing Owner has unlimited liability for any obligations of a Series that exceed that Series’ net assets, your investment in a Series is part of the assets of that Series, and it will therefore be subject to the risks of that Series’ trading. You cannot lose more than your investment in any Series in which you invest, and you will not be subject to the losses or liabilities of any Series in which you have not invested. We have received an opinion of counsel that each Series shall be entitled to the benefits of the limitation on interseries liability set forth in Section 3804(a) of the Trust Act. See “Trust Agreement—Liabilities” for a more complete explanation. |

Limitation of Liabilities | The debts, liabilities, obligations, claims and expenses of a particular Series shall be enforceable against the assets of that Series only, and not against the assets of the Trust generally or the assets of any other Series, and, unless otherwise provided in the Trust Agreement, none of the debts, liabilities, obligations and expenses incurred, contracted for or otherwise existing with respect to the Trust generally or any other Series thereof shall be enforceable against the assets of such Series. |

Who May Subscribe | An investment in the Trust is speculative and involves a high degree of risk. The Trust is not suitable for all investors. The Managing Owner offers the Trust as a diversification opportunity for an investor’s entire investment portfolio, and therefore an investment in the Trust should only represent a limited portion of your overall portfolio. To subscribe in the Units of any Series: |

• You must have at a minimum (1) a net worth (exclusive of your home, home furnishings and automobiles) of at least $150,000 or (2) a net worth, similarly calculated, of at least $45,000 and an annual gross income of at least $45,000. A significant number of states impose on their residents substantially higher suitability standards than the minimums described above. Before investing, you should review the minimum suitability requirements for your state of residence which are described in “State Suitability Requirements” in “SUBSCRIPTION INFORMATION” attached as Exhibit B to the Statement of Additional Information. These suitability requirements are, in each case, regulatory minimums only, and just because you meet such requirements does not mean that an investment in the Units is suitable for you; |

• You may not invest more than 10% of your net worth, exclusive of your home, furnishings and automobiles, in any Series or combination of Series; |

• IRAs, Keogh plans covering no common law employees and employee benefit plans not subject to the Employee Retirement Income Security Act of 1974, as amended, or ERISA, may not invest more than 10% of the subscriber’s and their participants’ net worth (exclusive of home, home furnishings and automobiles) in any Series or combination of Series. |

9

Table of Contents

• Employee benefit plans subject to ERISA are subject to special suitability requirements and should not invest more than 10% of their assets in any Series or combination of Series. |

See “Who May Subscribe” beginning on page 61 of this Prospectus. |

What You Must Understand Before You Subscribe | You should not subscribe for Units unless you understand: |

• the fundamental risks and possible financial hazards of the investment; |

• the trading strategies to be followed in the Series in which you will invest; |

• the tax consequences of this investment; |

• that if you decide to sell securities to subscribe for Units, you may have income tax consequences from that sale; |

• the fees and expenses to which you will be subject; |

• your rights and obligations as a Limited Owner. |

See “Risk Factors,” “Fees and Expenses,” “Federal Income Tax Consequences” and the appendix attached to this Prospectus for the Series of Units in which you wish to invest. |

Your Minimum Subscription and Unit Pricing | Minimum required subscriptions and Unit prices are as follows: |

Your minimum initial subscription is $1,000 and your minimum initial purchase in any one Series is $1,000, or, if you are a Plan (including an IRA), an employee or family member of an employee of the Managing Owner or its affiliates or a charitable organization, you have no minimum initial subscription requirements;

During the Continuous Offering Period, each Series’ Units will be offered and sold at their daily Net Asset Value, and existing Limited Owners will be able to purchase additional Units in increments of $100, or, if you are a Plan (including an IRA), an employee or family member of an employee of the Managing Owner or its affiliates or a charitable organization, you have no minimum additional subscription requirements; |

If you are a resident of Texas, your minimum initial subscription requirement is $5,000, or, if you are a Plan, an employee or family member of an employee of the Managing Owner or its affiliates or a charitable organization, your minimum initial subscription requirement is $1,000; |

No front-end sales charges or selling commissions will be charged to any Series of Units; and |

No Series’ Net Asset Value will be diluted by the Trust’s organization and offering expenses. |

How to Subscribe | To subscribe for any Series’ Units: |

10

Table of Contents

You will be required to complete and submit to the Trust a Subscription Agreement. |

Any subscription may be rejected in whole or in part by the Managing Owner for any reason. |

Initial Offering Period | The Units of each Series were offered for an initial offering period of limited duration, or the Initial Offering Period. The Initial Offering Period for the Winton Series and Currency Series as well as the Class 1 and Class 2 of the Balanced Series ended in September 2004, the Initial Offering Period for the Graham Series ended in November 2004, the Initial Offering Period for the Campbell/Graham Series ended in February 2005, the Initial Offering Period for the Long Only Commodity Series and the Long/Short Commodity Series ended in March 2006, the Initial Offering Period for the Managed Futures Index Series ended in April 2006 and the Initial Offering Period for the Class 1a and Class 2a of the Balanced Series ended in May 2006. Following the close of the Initial Offering Period for any Series, Units in such Series will be continuously offered. |

Series Subscription Minimums | Because the Initial Offering Period for the Winton Series and Currency Series as well as the Class 1 and Class 2 of the Balanced Series ended in September 2004, the Initial Offering Period for the Graham Series ended in November 2004, the Initial Offering Period for the Campbell/Graham Series ended in February 2005, the Initial Offering Period for the Long Only Commodity Series and the Long/Short Commodity Series ended in March 2006, the Initial Offering Period for the Managed Futures Index Series ended in April 2006 and the Initial Offering Period for the Class 1a and Class 2a of the Balanced Series ended in May 2006 and each such Series has begun trading, none of such Series has a Subscription Minimum. |

Continuous Offering Period | As trading has commenced for the Balanced Series, Graham Series, Winton Series, Campbell/Graham Series, Currency Series, Long Only Commodity Series, Long/Short Commodity Series and Managed Futures Index Series, we will offer Units of such Series as of each day of each week and will continue to offer Units in each Series until the maximum amount of each Series’ Units which are registered are sold, such period being referred to as the Continuous Offering Period. The Managing Owner may terminate the Continuous Offering Period at any time. |

Subscription Effective Dates During Continuous Offering Period | The effective date of all accepted subscriptions during the Continuous Offering Period, whether you are a new subscriber to a Series, or an existing Limited Owner in a Series who is purchasing additional Units in that Series or exchanging Units in one Series for Units in a different Series, is the day of the week two (2) Business Days after the day in which your Subscription Agreement or Exchange Request is received by the Managing Owner on a timely basis by 4:00 PM New York City Time, or NYT. The Managing Owner in its sole and absolute discretion may change such notice requirement upon written notice to you. |

11

Table of Contents

Segregated Accounts/Interest Income | Except for that portion of each Trading Company’s assets used as margin to maintain that Trading Company’s forward currency contract or swap positions and that portion of each Series’ assets maintained at the Trust level for cash management, the proceeds of the offering for each Series will be deposited in cash in segregated accounts in the name of each Trading Company maintained for each Trading Company at the Clearing Brokers in accordance with CFTC segregation requirements. The Clearing Brokers credit each Trading Company with 80%-100% of the interest earned on its average net assets (other than those assets held in the form of U.S. Government securities) on deposit with the Clearing Brokers each week. With respect to the Balanced Series, Graham Series, Winton Series, Campbell/Graham Series, Currency Series, Long Only Commodity Series, Long/Short Commodity Series and Managed Futures Index Series, interest income is currently estimated at 4.86%. In an attempt to increase interest income earned, the Managing Owner also may invest non-margin assets in U.S. government securities which include any security issued or guaranteed as to principal or interest by the United States, or by a person controlled by or supervised by and acting as an instrumentality of the government of the United States pursuant to authority granted by Congress of the United States or any certificate of deposit for any of the foregoing, including U.S. treasury bonds, U.S. treasury bills and issues of agencies of the United States government, and certain cash items such as money market funds, certificates of deposit (under nine months) and time deposits. The Managing Owner has selected Merrill Lynch, STW Fixed Income Management Ltd. and U.S. Bank N.A. to serve as the cash managers for the Trust, and the Managing Owner, in its sole and absolute discretion, may appoint additional or substitute cash managers for the Trust. With respect to the Graham Series, Winton Series, Campbell/Graham Series, Currency Series and the Class 1 and Class 2 of the Balanced Series, interest income up to 2.0% will be paid to the Managing Owner. With respect to the Long Only Commodity Series, Long/Short Commodity Series, Managed Futures Index Series and the Class 1a and Class 2a of the Balanced Series, twenty percent (20%) of interest income earned per annum by the Trust will be paid to the Managing Owner, and the remaining eighty percent (80%) of interest income earned per annum by the Trust will be retained by the Trust for the benefit of such Series. |

Organization and Offering Expenses | The Managing Owner is responsible for the payment of all of the ordinary expenses associated with the organization of the Trust and the offering of each Series of Units, except for the initial service fee, if any, and no Series will be required to reimburse these expenses. As a result, 100% of each Series’ offering proceeds will be initially available for that Series’ trading activities. See “The Structure of the Trust—Overview of the Series” and “Fees and Expenses.” |

12

Table of Contents

Summary Table of Fees and Expenses

| Amount of Expense† | ||||||||||||||||||||

Balanced Series-1 | Balanced Series-2‡ | Balanced Series-1a | Balanced Series-2a‡ | |||||||||||||||||

| $ | % | $ | % | $ | % | $ | % | |||||||||||||

Syndication and Selling Expense | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | ||||||||||||

Trust Operating Expenses | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | ||||||||||||

Management Fee | 5.00 | 0.50 | 5.00 | 0.50 | 10.00 | 1.00 | 10.00 | 1.00 | ||||||||||||

Service Fee | 30.00 | 3.00 | 0.00 | 0.00 | 30.00 | 3.00 | 0.00 | 0.00 | ||||||||||||

Incentive Fee (expressed as a percentage of New High Net Trading Profits) | N/A | * | 25.00 | N/A | * | 25.00 | N/A | * | 25.00 | N/A | * | 25.00 | ||||||||

Interest income** | 48.60 | 4.86 | 48.60 | 4.86 | 48.60 | 4.86 | 48.60 | 4.86 | ||||||||||||

Brokerage Commissions and Trading Fees*** | 16.10 | 1.61 | 16.10 | 1.61 | 25.80 | 2.58 | 25.80 | 2.58 | ||||||||||||

| Amount of Expense† | ||||||||||||||||||||

Graham Series-1 | Graham Series-2‡ | Winton Series-1 | Winton Series-2‡ | |||||||||||||||||

| $ | % | $ | % | $ | % | $ | % | |||||||||||||

Syndication and Selling Expense | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | ||||||||||||

Trust Operating Expenses | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | ||||||||||||

Management Fee | 25.00 | 2.50 | 25.00 | 2.50 | 20.00 | 2.00 | 20.00 | 2.00 | ||||||||||||

Service Fee | 30.00 | 3.00 | 0.00 | 0.00 | 30.00 | 3.00 | 0.00 | 0.00 | ||||||||||||

Incentive Fee (expressed as a percentage of New High Net Trading Profits) | N/A | * | 20.00 | N/A | * | 20.00 | N/A | * | 20.00 | N/A | * | 20.00 | ||||||||

Interest income** | 48.60 | 4.86 | 48.60 | 4.86 | 48.60 | 4.86 | 48.60 | 4.86 | ||||||||||||

Brokerage Commissions and Trading Fees*** | 13.10 | 1.31 | 13.10 | 1.31 | 20.80 | 2.08 | 20.80 | 2.08 | ||||||||||||

| Amount of Expense† | ||||||||||||||||||||

| Campbell/Graham Series-1 | Campbell/Graham Series-2‡ | Currency Series-1 | Currency Series-2‡ | |||||||||||||||||

| $ | % | $ | % | $ | % | $ | % | |||||||||||||

Syndication and Selling Expense | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | ||||||||||||

Trust Operating Expenses | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | ||||||||||||

Management Fee | 25.00 | 2.50 | 25.00 | 2.50 | 20.00 | 2.00 | 20.00 | 2.00 | ||||||||||||

Service Fee | 30.00 | 3.00 | 0.00 | 0.00 | 30.00 | 3.00 | 0.00 | 0.00 | ||||||||||||

Incentive Fee (expressed as a percentage of New High Net Trading Profits) | N/A | * | 20.00 | N/A | * | 20.00 | N/A | * | 20.00 | N/A | * | 20.00 | ||||||||

Interest income** | 48.60 | 4.86 | 48.60 | 4.86 | 48.60 | 4.86 | 48.60 | 4.86 | ||||||||||||

Brokerage Commissions and Trading Fees*** | 12.30 | 1.23 | 12.30 | 1.23 | 5.00 | 0.50 | 5.00 | 0.50 | ||||||||||||

| Amount of Expense† | ||||||||||||||||||||

| Long Only Commodity Series-1 | Long Only Commodity Series-2‡ | Long/Short Commodity Series-1 | Long/Short Commodity Series-2‡ | |||||||||||||||||

| $ | % | $ | % | $ | % | $ | % | |||||||||||||

Syndication and Selling Expense | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | ||||||||||||

Trust Operating Expenses | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | ||||||||||||

Management Fee | 12.50 | 1.25 | 12.50 | 1.25 | 35.00 | 3.50 | 35.00 | 3.50 | ||||||||||||

Service Fee | 20.00 | 2.00 | 0.00 | 0.00 | 30.00 | 3.00 | 0.00 | 0.00 | ||||||||||||

Incentive Fee (expressed as a percentage of New High Net Trading Profits) | N/A | * | 0.00 | N/A | * | 0.00 | N/A | * | 20.00 | N/A | * | 20.00 | ||||||||

Interest income** | 48.60 | 4.86 | 48.60 | 4.86 | 48.60 | 4.86 | 48.60 | 4.86 | ||||||||||||

Brokerage Commissions and Trading Fees*** | 5.00 | 0.50 | 5.00 | 0.50 | 18.60 | 1.86 | 18.60 | 1.86 | ||||||||||||

13

Table of Contents

| Amount of Expense† | ||||||||||

| Managed Futures Index Series-1 | Managed Futures Index Series-2‡ | |||||||||

| $ | % | $ | % | |||||||

Syndication and Selling Expense | 0.00 | 0.00 | 0.00 | 0.00 | ||||||

Trust Operating Expenses | 0.00 | 0.00 | 0.00 | 0.00 | ||||||

Management Fee | 20.00 | 2.00 | 20.00 | 2.00 | ||||||

Service Fee | 20.00 | 2.00 | 0.00 | 0.00 | ||||||

Incentive Fee (expressed as a percentage of New High Net Trading Profits) | N/A | * | 0.00 | N/A | * | 0.00 | ||||

Interest income** | 48.60 | 4.86 | 48.60 | 4.86 | ||||||

Brokerage Commissions and Trading Fees*** | 8.50 | 0.85 | 8.50 | 0.85 | ||||||

| † | The dollar value for each fee and expense presented is calculated on the basis of a $1,000 investment in the Trust. |

| ‡ | Class 2 Units may only be offered to investors who are represented by approved Selling Agents who are directly compensated by the investor for services rendered in connection with an investment in the Trust (such arrangements commonly referred to as “wrap-accounts”). |

| * | Because the incentive fee is based upon New High Net Trading Profits, it is impossible to estimate a dollar value for such fee. |

| ** | With respect to the Balanced Series, Graham Series, Winton Series, Campbell/Graham Series, Currency Series, Long Only Commodity Series, Long/Short Commodity Series and Managed Futures Index Series, interest income is currently estimated at 4.86%. With respect to the Graham Series, Winton Series, Campbell/Graham Series, Currency Series and the Class 1 and Class 2 of the Balanced Series, the first two percent (2.0%) of interest income earned per annum by the Trust on each Series will be paid to the Managing Owner. In addition, if interest rates fall below 0.75% (calculated daily based on each Series’ Net Asset Value), the Managing Owner will be paid the difference between the Trust’s annualized income interest and 0.75%. Interest income above two percent (2.0%) per Series (calculated daily based on each Series’ Net Asset Value) is retained by the Trust. With respect to the Long Only Commodity Series, Long/Short Commodity Series, Managed Futures Index Series and the Class 1a and Class 2a of the Balanced Series, twenty percent (20%) of interest income earned per annum by the Trust will be paid to the Managing Owner, and the remaining eighty percent (80%) of interest income earned per annum by the Trust will be retained by the Trust. |

| *** | The amount of brokerage commissions and trading fees to be incurred will vary on a Series by Series basis. Although the actual rates of brokerage commissions and transaction related fees and expenses are the same for all Trading Advisors, the total amount of brokerage commissions and trading fees varies from Series to Series based upon the trading frequency of such Series’ Trading Advisor (or Trading Advisors, in the case of the Balanced Series, Campbell/Graham Series, Currency Series and Long/Short Commodity Series) and the types of instruments traded. The estimates presented in the table above are prepared using historical data about the Trading Advisors’ trading activities. |

14

Table of Contents

Fees and Expenses | Charges to be paid by the Trust include: |

• Each Series will pay to the Managing Owner a monthly management fee equal to a certain percentage of each Series’ Net Asset Value. For the actual percentage of the Net Asset Value of a Series payable to the Managing Owner as a management fee, please see the Appendix for such Series. The Managing Owner may pay all or a portion of such management fees to the Trading Advisor(s) for such Series; |

• Each Series will pay to the Managing Owner an incentive fee of a certain percentage (between 0% and 25%) of profits net of fees and expenses generated by such Series, including realized and unrealized |

gains and losses thereon, as of the close of business on the last day of each calendar month or quarter. The Managing Owner will pay all or a portion of such incentive fees to the Trading Advisor(s) for such Series; |

• The Trust, with respect to each Series, will pay the Clearing Brokers and the Managing Owner a fee of approximately 0.50% to 2.58% of each Series’ Net Asset Value annually which will be used to pay all brokerage commissions, including applicable exchange fees, NFA fees, give up fees, pit brokerage fees and other transaction related fees and expenses charged in connection with each Series’ trading activities and on-going service fees of up to 0.75% annually of the Net Asset Value of the Class 2 Units and Class 2a Units for certain administrative services payable to certain Selling Agents selling Class 2 Units and Class 2a Units of any Series; |

• With respect to the Graham Series, Winton Series, Campbell/Graham Series, Currency Series and the Class 1 and Class 2 of the Balanced Series, the first two percent (2.0%) of interest income earned per annum by the Trust on each Series will be paid to the Managing Owner. In addition, if interest rates fall below 0.75% (calculated daily based on each Series’ Net Asset Value), the Managing Owner will be paid the difference between the Trust’s annualized income interest and 0.75%. Interest income above two percent (2.0%) per Series (calculated daily based on each Series’ Net Asset Value) is retained by the Trust; |

• With respect to the Long Only Commodity Series, Long/Short Commodity Series, Managed Futures Index Series and the Class 1a and Class 2a of the Balanced Series, twenty percent (20%) of interest income earned per annum by the Trust will be paid to the Managing Owner, and the remaining eighty percent (80%) of interest income earned per annum by the Trust will be retained by the Trust; |

• The Trust will pay all extraordinary fees and expenses. |

Charges to be paid by the Managing Owner include: |

• Routine operational, administrative and other expenses; and |

• Expenses incurred in connection with the organization of the Trust. |

15

Table of Contents

Charges to be paid by the Limited Owners include: |

• With respect to the Class 1 Units of the Balanced Series, Winton Series, Campbell/Graham Series, Currency Series, Graham Series and Long/Short Commodity Series, as well as the Class 1a Units of the Balanced Series, as compensation, the Selling Agents will receive an initial service fee of up to three percent (3.0%) of the subscription amount. |

• After the expiration of twelve (12) months following the purchase of Class 1 Units of the Balanced Series, Winton Series, Campbell/Graham Series, Currency Series or Graham Series, investors who purchased Class 1 Units of such Series will be charged an annual on-going service fee of up to three percent (3.0%) of the Net Asset Value of each Unit purchased, for the benefit of Selling Agents selling Class 1 Units for on-going services provided to the Trust and the Limited Owners by the Selling Agents. |

• After the expiration of twelve (12) months following the purchase of Class 1 Units of the Long/Short Commodity Series or Class 1a Units of the Balanced Series, investors who purchased Class 1 Units or Class 1a Units, as applicable, of such Series will be charged an annual on-going service fee of up to three percent (3.0%) of the Net Asset Value of each Unit purchased, for the benefit of Selling Agents selling Class 1 Units or Class 1a Units, as applicable, for on-going services provided to the Trust and the Limited Owners by the Selling Agents. The on-going service fee with respect to the Class 1 Units of the Long/Short Commodity Series or Class 1a Units of the Balanced Series will continue only until the aggregate initial service fees and on-going service fees received by the Selling Agent with respect to such Units total ten percent (10%) of the purchase price of such Class 1 Units of such Series; |

• With respect to the Class 1 Units of the Long Only Commodity Series and the Managed Futures Index Series, as compensation, the Selling Agents will receive an initial service fee of up to two percent (2.0%) of the subscription amount. In addition, after the expiration of twelve (12) months following the purchase of Class 1 Units of the Long Only Commodity Series or the Managed Futures Index Series, investors who purchased Class 1 Units of such Series will be charged an annual on-going service fee of up to two percent (2.0%) of the Net Asset Value of each Unit purchased, for the benefit of Selling Agents selling Class 1 Units for on-going services provided to the Trust and the Limited Owners by the Selling Agents. The on-going service fee with respect to the Class 1 Units of the Long Only Commodity Series or the Managed Futures Index Series will continue only until the aggregate initial service fees and on-going service fees received by the Selling Agent with respect to such Units total ten percent (10%) of the purchase price of such Class 1 Units of such Series; |

• Investors who purchase Class 2 Units of any Series or Class 2a Units of the Balanced Series will be charged no initial service fee, but Selling Agents selling Class 2 Units or Class 2a Units may receive an |

16

Table of Contents

on-going service fee of up to 0.5% annually of the Net Asset Value of the Class 2 Units or Class 2a Units sold by them. The on-going service fee payable to the Selling Agents with respect to the Class 2 Units of the Long Only Commodity Series, the Long/Short Commodity Series and the Managed Futures Index Series and the Class 2a Units of the Balanced Series will continue until the aggregate initial service fees and on-going service fees received by the Selling Agent with respect to such Units total ten percent (10%) of the purchase price of such Class 2 Units or Class 2a Units of such Series. The on-going service fee payable to the Selling Agents with respect to the Class 2 Units of the Balanced Series sold on or after November 10, 2007, will continue until the aggregate initial service fees and on-going service fees received by the Selling Agent with respect to such Units total ten percent (10%) of the purchase price of such Class 2 Units of such Series. The on-going service fee payable to the Selling Agents with respect to the Class 2 Units of the Winton Series sold on or after November 10, 2007, will continue until the aggregate initial service fees and on-going service fees received by the Selling Agent with respect to such Units total ten percent (10%) of the purchase price of such Class 2 Units of such Series. |

• Investors who redeem all or a portion of their Class 1 Units of the Balanced Series, Winton Series, Campbell/Graham Series, Currency Series, Graham Series and Long/Short Commodity Series, as well as the Class 1a Units of the Balanced Series, during the first twelve (12) months following the effective date of their purchase will be subject to a redemption fee of up to three percent (3.0%) of the Net Asset Value at which such investor redeemed to reimburse the Managing Owner for the then-unamortized balance of the prepaid initial service fee; |

• Investors who redeem all or a portion of their Class 1 Units of the Long Only Commodity Series and the Managed Futures Index Series during the first twelve (12) months following the effective date of their purchase will be subject to a redemption fee of up to two percent (2.0%) of the Net Asset Value at which such investor redeemed to reimburse the Managing Owner for the then-unamortized balance of the prepaid initial service fee; and |

• There is no redemption fee associated with the Class 2 Units. |

Respective Break-Even Amounts for Each Series | The following summary displays the estimated amount of all fees and expenses which are anticipated to be incurred by a new investor in each Sub-Class of each Series during the first twelve months. In each case, the total estimated cost and expense load is expressed as a percentage of $1,000, the amount of minimum investment in the Trust (other than IRAs, Plans, employees or family members of an employee of the Managing Owner or its affiliates or charitable organizations). |

• Balanced Series-1: 2.25% (or $22.50 for each $1,000 invested); |

17

Table of Contents

• Balanced Series-2: -0.75% (or -$7.50 for each $1,000 invested); |

• Balanced Series-1a: 2.69% (or $26.90 for each $1,000 invested); |

• Balanced Series-2a: -0.31% (or -$3.10 for each $1,000 invested); |

• Graham Series-1: 3.99% (or $39.90 for each $1,000 invested); |

• Graham Series-2: 0.95% (or $9.50 for each $1,000 invested); |

• Winton Series-1: 4.22% (or $42.20 for each $1,000 invested); |

• Winton Series-2: 1.22% (or $12.20 for each $1,000 invested); |

• Campbell/Graham Series -1: 3.90% (or $39.00 for each $1,000 invested); |

• Campbell/Graham Series -2: 0.87% (or $0.87 for each $1,000 invested); |

• Currency Series-1: 2.64% (or $26.40 for each $1,000 invested); |

• Currency Series-2: -0.36% (or -$3.60 for each $1,000 invested); |

• Long Only Commodity Series-1: 0.13% (or $1.30 for each $1,000 invested); |

• Long Only Commodity Series-2: -2.13% (or -$21.30 for each $1,000 invested); |

• Long/Short Commodity Series-1: 4.47% (or $44.70 for each $1,000 invested); |

• Long/Short Commodity Series-2: 1.47% (or $14.47 for each $1,000 invested); |

• Managed Futures Index Series-1: 0.96% (or $9.60 for each $1,000 invested); |

• Managed Futures Index Series-2: -1.04% (or -$10.40 for each $1,000 invested); |

Transfer of Units | The Trust Agreement restricts the transferability and assignability of the Units of each Series. There is not now, nor is there expected to be, a primary or secondary trading market for the Units of any Series. |

Exchange Privilege | Once trading commences for the Series in which you have invested, you may exchange your Units in such Series for Units in another Series which has also commenced trading. Exchanges will be available between the various Classes 1 of the Series and Exchanges will be available between the various Classes 2 of the Series. However, Exchanges will not be allowed from Class 1 to Class 2 or vice versa. In addition, you will only be allowed to Exchange your Units in one Series for Units in another Series which is registered for sale in your State. Furthermore, Exchanges will be allowed out of the Graham Series, but Exchanges into the Graham Series will be restricted to those investors that have purchased their Units through a Selling Agent that acts as a selling agent for the Graham Series. The Exchange of Units will be treated as a redemption of Units in one Series (with the related tax consequences) and the immediate purchase of |

18

Table of Contents

Units in the Series you exchange into. See “Federal Income Tax Consequences.” Exchanges are made at the applicable Series’ then-current Net Asset Value per Unit (which includes, among other things, accrued but unpaid incentive fees due to that Series’ Trading Advisor) at the close of business on each day, or the Valuation Point, immediately preceding the day on which your Exchange will become effective. The effective date of an Exchange will be the day of the week two (2) Business Days following your submission of an Exchange Request to the Managing Owner on a timely basis by 4:00 PM NYT. The Managing Owner, in its sole and absolute discretion, may change the notice |