UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-21422 | |||||||

| ||||||||

Trust for Advised Portfolios | ||||||||

(Exact name of registrant as specified in charter) | ||||||||

| ||||||||

615 East Michigan Street Milwaukee, Wisconsin |

| 53202 | ||||||

(Address of principal executive offices) |

| (Zip code) | ||||||

| ||||||||

Christopher E. Kashmerick Trust for Advised Portfolios 2020 East Financial Way, Suite 100 Glendora, CA 91741 | ||||||||

(Name and address of agent for service) | ||||||||

| ||||||||

Registrant’s telephone number, including area code: | (626) 914-7385 |

| ||||||

| ||||||||

Date of fiscal year end: | December 31 |

| ||||||

| ||||||||

Date of reporting period: | December 31, 2020 |

| ||||||

Item 1. Reports to Stockholders.

(a)

Annual Report

December 31, 2020

Miller Opportunity Trust

Class A LGOAX

Class C LMOPX

Class FI LMOFX

Class R LMORX

Class I LMNOX

Class IS MVISX

Important Notice: The U.S. Securities and Exchange Commission will permit funds to make shareholder reports available electronically beginning January 1, 2021. Accordingly, paper copies will no longer be mailed. Instead, at that time, the Miller Opportunity Trust will send a notice, either by mail or e-mail, each time an updated report is available on the Fund's website (www.millervaluefunds.com). Investors enrolled in electronic delivery will receive the notices by e-mail, with links to the updated report and will not need to take any action. Investors who are not enrolled in electronic delivery by January 1, 2021 will receive the notices in the mail.

All investors who prefer to receive shareholder reports in a printed format may, at any time, choose that option free of charge. Contact your financial intermediary to make this election, or direct investors can call 1-888-593-5110.

Table of contents

Miller Opportunity Trust | |||||||

Manager commentary | 1 | ||||||

Fund at a glance | 13 | ||||||

Fund expenses | 14 | ||||||

Fund performance | 16 | ||||||

Schedule of investments | 17 | ||||||

Statement of assets and liabilities | 21 | ||||||

Statement of operations | 23 | ||||||

Statements of changes in net assets | 24 | ||||||

Financial highlights | 25 | ||||||

Notes to financial statements | 31 | ||||||

Report of independent registered public accounting firm | 44 | ||||||

Approval of investment advisory agreement | 46 | ||||||

Additional information | 49 | ||||||

Privacy notice | 52 | ||||||

Directory of Fund's service providers | Back Cover | ||||||

Miller Opportunity Trust 2020 Annual Report

Miller Opportunity Trust manager commentary (unaudited)

Miller Opportunity Trust ended the year on a strong note, notching a 35.85%1 gain in the quarter versus the S&P 500's 12.15%. This brought the 2020 annual return to 38.91%1, more than doubling the market's 18.40% return. The gains were driven by a strong market recovery from the COVID crash earlier in the year, along with good old fashion stock picking. Performance in the quarter benefited from a rebound in "value" more broadly. Over the year, we benefited from diversification between different types of values: longer-term, more growth-oriented compounders as well as classic value holdings.

Average Annual Total Returns and Expenses (%) as of 12/31/2020

Without Sales Charges | |||||||||||||||||||||||||||||||

YTD | 1 Yr | 3 Yr | 5 Yr | 10 Yr | Inception* | Inception Date | |||||||||||||||||||||||||

Class A | 38.61 | 38.61 | 18.75 | 16.04 | 13.78 | 19.47 | 2/3/2009 | ||||||||||||||||||||||||

Class C | 37.56 | 37.56 | 17.86 | 15.16 | 12.91 | 7.74 | 12/30/1999 | ||||||||||||||||||||||||

Class FI | 38.50 | 38.50 | 18.68 | 15.99 | 13.73 | 8.02 | 2/13/2004 | ||||||||||||||||||||||||

Class R | 38.22 | 38.22 | 18.42 | 15.70 | 13.37 | 6.98 | 12/28/2006 | ||||||||||||||||||||||||

Class I | 38.91 | 38.91 | 19.06 | 16.35 | 14.10 | 8.83 | 6/26/2000 | ||||||||||||||||||||||||

Class IS | 39.02 | — | — | — | — | 14.16 | 8/22/2018 | ||||||||||||||||||||||||

S&P 500 | 18.40 | 18.40 | 14.18 | 15.22 | 13.88 | 9.50 | — | ||||||||||||||||||||||||

With Max Sales Charges | |||||||||||||||||||||||||||||||

YTD | 1 Yr | 3 Yr | 5 Yr | 10 Yr | Inception | ||||||||||||||||||||||||||

Class A | 30.64 | 30.64 | 16.43 | 14.67 | 13.11 | 18.87 | 2/3/2009 | ||||||||||||||||||||||||

Class C | 36.56 | 36.56 | 17.86 | 15.16 | 12.91 | 7.74 | 12/30/1999 | ||||||||||||||||||||||||

* S&P 500 since inception return represented from 12/30/99, the Fund's oldest share class.

Gross (Net) Expenses (%): Class A 1.49 (1.49); Class C 2.23 (2.23); Class FI 1.55 (1.55); Class I 1.25 (1.22), Class R 1.77 (1.77) and Class IS 1.15 (1.15). Miller Value Partners, LLC (the "Adviser") has agreed to waive fees and/or reimburse operating expenses (other than front-end or contingent deferred loads, taxes, interest expense, brokerage commissions, acquired fund fees and expenses, expenses incurred in connection with any merger or reorganization, portfolio transaction expenses, dividends paid on short sales, extraordinary expenses such as litigation, Rule 12b-1 fees, intermediary servicing fees, or any other class-specific expenses) through April 30, 2021, so that such annual operating expenses will not exceed 0.88%. Separately, with respect to Class I only, the Adviser has agreed to waive fees and/or reimburse operating expenses such that the previously described annual operating expenses, plus intermediary servicing fees and other class-specific expenses, will not exceed 0.93%. Net expense ratios are current to the most recent prospectus dated 4/30/20 and are applicable to investors.

Performance shown represents past performance and is no guarantee of future results. Current performance may be higher or lower than the performance shown. Investment return and principal value will fluctuate so shares, when redeemed, may be worth more or less than the original cost. Class A shares have a maximum front-end sales charge of 5.75%. Class C shares have a one-year contingent deferred sales charge (CDSC) of 1.0%. If sales charges were included, performance shown would be lower. Total returns assume the reinvestment of all distributions at net asset value and the deduction of all Fund expenses. Total return figures are based on the NAV per share applied to shareholder subscriptions and redemptions, which may differ from the NAV per share disclosed in Fund shareholder reports. Performance would have been lower if fees had not been waived in various periods. YTD is calculated from January 1 of the reporting year. All classes of shares may not be available to all investors or through all distribution channels. For the most recent month-end information, please call 888-593-5110 or visit millervaluefunds.com.

1 Class I — LMNOX

Miller Opportunity Trust 2020 Annual Report

1

Miller Opportunity Trust manager commentary (unaudited) (cont'd)

The only bad news about such strong returns: they aren't sustainable. We just made in a quarter what we might expect to earn over numerous years. Huge market bursts can't endure forever. Many take this line of reasoning a step further, projecting a major pullback. We disagree. We think the market can continue to be stronger than many expect providing a window to earn strong returns. We estimate the portfolio currently has greater than 60%2 upside to our calculation of its intrinsic value offering strong return potential.

Market pullbacks happen frequently, and no one can consistently predict them accurately. We wouldn't be surprised by a modest one after such a strong move. However, we believe we are in a bull market and the market can continue to move higher driven by a continuing economic recovery, attractive equity valuations relative to bonds and over a decade of underinvestment in equities relative to bonds.

There are two key points we think aren't well understood. First, this economic hit is more akin to a natural disaster than endogenous economic malaise. This has important implications on many levels. First, the sudden dramatic nature of the pandemic caught everyone's attention garnering unprecedented resources and support. The Fed expanded its balance sheet by $3T over a few months. During the financial crisis, it took more than 5 years for a comparable dollar expansion. Likewise, we've seen two rounds of fiscal stimulus totaling just shy of $3T and with a Democratic-controlled Congress, more appears to be on the way. During the 2008-09 financial crisis, total stimulus was just over $1T, so a fraction of the size. In addition, corporations, universities, and the broad population have marshaled unprecedented levels of resources to combat the problem.

During and after a natural disaster, the economy behaves differently than a normal recession. The economic hit is sudden, dramatic, and extreme, but so is the ensuing recovery. After Hurricane Katrina, employment fell off a cliff but it had fully recovered a couple years later. It took nearly a decade after the financial crisis for unemployment to reach pre-crisis levels. So far, employment trends are tracking much closer to Katrina than the financial crisis.

The pandemic, lasting many months, is more prolonged than a typical disaster, but the natural disaster analogy implies a quicker and stronger recovery once we reach the other side. A combination of greater infection rates and vaccine distribution will help get us there over the coming months. This implies gains could continue to be faster and stronger than many expect.

2 As of 1/12/21. A proprietary calculation of the central tendency of value for the portfolio based on our assessment of the intrinsic value of individual holdings.

Miller Opportunity Trust 2020 Annual Report

2

Second, we are in a bull market. This definitely isn't news to anyone, but I think people underappreciate the importance of the point. My partner Bill Miller writes fantastic market letters. For roughly the past decade he's started with this statement. Why? It provides the broad context you need to know how to behave optimally.

The market's reaction function (how prices respond to news and events) differs completely in bull markets than in bear markets. How can the market mostly ignore protestors storming the capital and temporarily disrupting the smooth transition of power? A bull market can look through to economic implications, while a bear won't.

Investors often focus on the problem of losing money during pullbacks, but over the past decade investors' biggest mistake has been missing out on massive gains due to overwhelming risk aversion. Likewise, bubble fears caused many people to exit the market in 1998, years before the top. One of Bill's best all-time moves was his near-perfect timing when exiting technology stocks in 2000. He pulled this off partially by being a keen observer of the market environment.

Bull markets typically don't peak during a strong economic recovery with accommodative monetary and fiscal policy. We think it's optimal to play offense in a bull market driven by a recovering economy. If this changes, we can adjust accordingly.

Our favorite relevant quote from Sir John Templeton (which we repeat A LOT) is: "Bull markets are born on pessimism, grow on skepticism, mature on optimism and die on euphoria." Understanding sentiment in this way helps us frame the opportunity set along with the risks. Greater pessimism implies higher future returns, while the opposite is true of euphoria. The depths of panics, like March 2020, provide the best buying opportunities. When no one sees risks, run for the door. So where are we now?

It's hard to be precise but we're somewhere in the later stages of the bull market. While this implies we are closer to the end, it's important to note that the latest stages of bull markets typically generate some of the best returns. Lazlo Birinyi is a market strategist with an excellent long-term investing record. His team divides bull markets into four stages (similar to Templeton): reluctance, consolidation, acceptance and exuberance. The first (reversal off bear market lows) and last (euphoria kicks in) stages offer the best returns. They think we might be somewhere in the acceptance phase.

I like to joke with Bill about how he's usually right, just sometimes early. During the financial crisis, he shorted oil based on his view that it was economically sensitive and the world was falling apart so the price shouldn't be rising. He nailed it

Miller Opportunity Trust 2020 Annual Report

3

Miller Opportunity Trust manager commentary (unaudited) (cont'd)

fundamentally but that didn't stop the price from continuing its rapid ascent before falling apart. A few years ago, a client asked about risks. Bill replied bonds were expensive and if stocks rose to comparable levels, it would produce massive gains but then it would be difficult to make money anywhere. That scenario seems more likely now. If true, the good news is there's still a window to make nice returns. The bad news is that it might be followed by some ugly times. We will do our best to adapt as circumstances change.

In more growthy areas of the market, euphoria seems to abound. We aren't optimistic about the long-term return prospects for certain growth names where elevated prices make it increasingly difficult to meet market embedded expectations. We know from history that the very best companies drive the overall market's returns. When the rarefied company, like an Amazon or Apple, sustains high growth rates for extended periods of time, high multiples on current revenues and earnings are justified, while still offering attractive returns. But most companies priced to achieve this type of growth fail to do so. Currently, many growth companies trade at significant premiums to even Amazon's historical valuations, outside of the peak of the tech bubble.

The market is pricing more and more companies as if they will achieve Amazon or Apple type growth. We estimate current market expectations imply Apple-level growth for Peloton and Amazon-level growth for insurance company Lemonade. In the past few weeks alone, we've heard numerous companies pitch themselves as the Amazon of this or that area. There are far more Amazon aspirants than actual Amazons.

We recently exited Peloton because of heightened risk of falling short of elevated expectations, along with our belief that other names offered better opportunities. We bought Peloton in the low $20's right after the IPO believing it was a misunderstood disruptor with a powerful brand that could change the way large numbers of people exercise. We still see significant potential for Peloton to grow the business over the long term.

However, we estimate current market expectations imply Peloton will grow at a slightly greater rate than Apple did3 from a comparable level of revenue for the next 22 YEARS. Very few companies have a shot at this type of performance. Work by Michael Mauboussin4 shows companies' competitive advantage periods (the period over which it can earn excess returns) average 10-15 years. Alternatively, Peloton will need to grow topline 38% annually over the next 10 years to justify the current price, well ahead of Netflix's 28% topline growth from a comparable revenue level. Not a bet we want to make.

3 Apple grew 19% annually on average from a comparable revenue level

4 http://people.stern.nyu.edu/adamodar/pdfiles/eqnotes/cap.pdf

Miller Opportunity Trust 2020 Annual Report

4

Part of our initial bull case on Peloton compared the brand power to Apple's. But the analogy only goes so far. Most people can't put down their phones. On the other hand, most can't get off their duffs to exercise! Peloton is an amazing company, but we don't want to bet its Apple-level amazing, especially as extremely tough comps in the back half of 2021 could present near-term risk.

A couple points: not all growth companies have elevated expectations. Despite the significant moves up we still believe Farfetch, Amazon, Stitch Fix, along with the other high growth names we still own are undervalued. Our primary job is to do the company-by-company work of sifting through market expectations relative to our assessment of fundamentals. We make bets when we think those two sides of the equation are out of whack. We think through the opportunities relative to the risks. We believe our flexibility to migrate as the opportunity set dictates offers us a significant competitive advantage relative to investors forced to stay in a more restricted area.

Since we own some high growth names, we often get asked if we are truly a value manager. The answer: absolutely! We only purchase a name is if we think it's a good value. Likewise, we use valuations to make sell decisions (which has not helped us in this market where no valuation is too high for beloved companies!). We do believe this discipline will pay off over time.

Many people equate low accounting-based metrics (P/E, P/B, etc) with good value, but that's simply not the case. Low accounting metrics are markers of low expectations, but fundamentals must outperform those expectations for stocks to do well. The value of any investment is the present value of future free cash flows. Those may be difficult to forecast, but they will drive the value of any investment. We spend our time understanding business values in different scenarios and what historical precedents imply on the likelihood of outcomes. We want a favorable skew between returns in the base or best case scenario relative to the worst case.

As in everything with markets, value investing evolves over time. I recently read a post saying the founder of value investing, Ben Graham, would have been very uncomfortable with Warren Buffett's method of projecting earnings to derive a value. It's certainly true that the cone of uncertainty widens with time. Ben Graham himself spoke of this in The Intelligent Investor:

The better a company's record and prospects, the less relationship the price of shares will have to their book value. But the greater premium above book value, the less certain the basis of determining its intrinsic value — i.e., the more this "value" will depend on the changing moods and measurements of the stock market. Thus, we reach the final paradox, that the more successful the company, the greater are likely to be the fluctuations in the price of its

Miller Opportunity Trust 2020 Annual Report

5

Miller Opportunity Trust manager commentary (unaudited) (cont'd)

shares. This means in a very real sense, the better the quality of a common stock, the more speculative it is likely to be.

So relevant to our current environment! Innovation and growth have fueled returns, but that's led to valuations of those companies disconnecting dramatically from current revenue and earnings streams. As long as belief states about future growth prospects hold, it's not a problem. With disappointment comes great loss.

We can look back at the great Nifty Fifty growth stocks of the 70s to understand they actually weren't all that overpriced, but that didn't stop them from suffering a huge crash. Likewise, buying Amazon in 1999 was a great move long term but that didn't protect you from losing a ton of money over the next couple years. While we don't see near term risk to growth stocks broadly, we do think there's a good chance this euphoria won't end well. In the past, it's taken a recession to end these sorts of moves. A significant move up in rates is another threat to long duration assets.

We try to think through these risks carefully. We manage them in the portfolio through security selection and portfolio diversification. We also want to understand these darling companies well enough to take advantage of any opportunity that arises from price weakness.

The key behind all value approaches, though, is a strict reckoning between what you are paying and what you are getting. That's our lifeblood. Most sell-side analysts don't even run long term discounted cash flows, and I don't remember ever seeing a model that looks at numerous future scenarios. I love that because it means our approach isn't in high demand from those on the buy side either. This means it's a potential edge versus others.

We really love the current portfolio. It trades at a steep discount to the market (roughly 12x next 12 months earnings versus the SPX at 23x5). Even with our higher multiple growth names, we think the portfolio is very attractively valued even on near-term metrics. We constantly work to see if we can improve our risk-adjusted returns and we continue to find attractive investment opportunities. I will highlight a couple examples.

Desktop Metal is a name that made it into our top holdings at the end of year due to strong performance since our purchase. The company is a second generation industrial printing company led by a great team. It came public through a merger with a SPAC led by Leo Hindery, Jr. who we've known from his successful history at Telecommunications, Inc (TCI) where they excelled at capital allocation. One of the unique benefits of structure is that it helps us get access to unique opportunities.

5 Source FactSet as of 12/31/20

Miller Opportunity Trust 2020 Annual Report

6

Here, we were able to invest in the PIPE (private investment in public equity) to take the company public based on industry relationships.

Desktop Metal is early in its commercialization, but we think the company has great potential over the next five years with a stellar list of customer partners and potential applications. We bought on the deal at a $1.8B enterprise value or 6.7x the EBITDA management estimates it can earn in 5 years before any acquisitions. For a company capable of growing at such high rates (triple digits for next couple years), with a great business with high moats and a fantastic team, this was a great deal. It's doubled since the deal. This is a great example of an undervalued, long-term, growth-oriented opportunity that we were still able to source in this market.

In the squarely value camp, we bought Norwegian Cruise Lines in the quarter as well. The sector has obviously been one of the hardest hit by COVID with business shut down. It should be one of the biggest beneficiaries of a normalization due to vaccines and infections helping us reach herd immunity at some point. As we got clarity around vaccine efficiency and potential timelines for disbursement, it enabled us to analyze the ability of cruise lines to make it through and what the potential balance sheet and earnings power might look like on the other side. We think Norwegian is worth somewhere in the $40s with a good ability to withstand the crisis. We think the recovery in travel is more likely to beat current recovery expectations than it is to fall short, setting up a nice risk-reward.

We also bought Diamondback Energy. For the first time in decades, we find energy to be quite attractive. Companies are finally focusing on cash flow and returns. Diamondback is a low-cost shale producer that screened well on a number of metrics we pay attention to (dividend yield, free cash flow yield, discounted cash flow, and insider buying). They recently added Return on Invested Capital (ROIC) to their management incentive compensation. They plan to continue to pay down debt and maintain the dividend. The company is obviously levered to increasing oil prices.

Green Thumb, another new name, is a cannabis company that we have watched for a while. The company is the best capital allocator in the space with a focus on profitable growth in limited license states, while also building national brands. We believe there's a long growth runway due to state adoption driven by budgetary needs. We believe that GTBIF is undervalued based on their current licenses alone, while state expansion is virtually guaranteed.

Another name we're very excited about is WW (formerly known as Weight Watchers). We've followed it for awhile. CEO Mindy Grossman, joined in 2017, is excellent. While the company has looked cheap in the past, we think the digital transition has reached an important inflection the market is not reflecting. We

Miller Opportunity Trust 2020 Annual Report

7

Miller Opportunity Trust manager commentary (unaudited) (cont'd)

expect improving revenue growth and margin expansion and believe the stock can double.

Lastly, we added a small position to Netflix after the disappointment following 3Q results. Overall, it's getting more difficult to find investment opportunities in the very high growth areas that meet our standards for attractive value. On the other hand, we continue to find opportunities in more value-oriented areas of the market. We would expect the portfolio to migrate in this direction.

We appreciate your interest in the Fund. We continue to work hard to earn attractive returns for our investors and thank you for your support.

| Samantha McLemore, CFA January 15, 2021 | |||

Supplemental Questions:

What is the Fund's investment strategy?

The Fund seeks long-term growth of capital. The Fund normally invests in securities, derivatives, and other financial instruments that, in the portfolio managers' opinion, offer the opportunity for long-term growth of capital. The portfolio managers exercise a flexible strategy when selecting investments, not limited by investment style or asset class. The investment strategy typically involves identifying instances where the manager believes the capital markets have mispriced investment opportunities and exploiting price discrepancies and inefficiencies in the market. The Fund may invest in the common stock of U.S. and foreign securities, debt securities, derivatives and other financial instruments. The Fund may also engage to a substantial degree in short sales of securities and other instruments, and can borrow money for investment purposes in amounts up to 10% of its net assets, a practice known as "leveraging." Although the portfolio managers consider ratings in determining whether securities convertible into common stock or debt securities are appropriate investments for the Fund, such securities may include investments rated below investment grade, commonly known as "junk" bonds, and unrated securities.

What were the overall conditions during the Fund's reporting period?

All major indices and asset classes had a strong finish to 2020 despite how the year began. The Nasdaq Composite finished the year up 45.1% followed by the S&P500 gaining 18.4% and the Dow Jones Industrial Average closing out the year with a return of 9.7%. Eight out of the eleven sectors in the S&P 500 posted positive returns for the year, with Information Technology and Consumer Discretionary gaining the most with returns of 43.9% and 33.3%, respectively. On the other hand, Energy and Real Estate lost the most with returns of -33.7% and -2.2%, respectively. Large-caps continued to outperform Small-caps, which

Miller Opportunity Trust 2020 Annual Report

8

beat Mid-cap names. Specifically, the large-cap Russell 1000 Index gained 21.0%, ahead of the small-cap Russell 2000 Index's 19.9% return for the year followed by the Russell MidCap Index's 17.1% return. Growth stocks outperformed value stocks with the Russell 1000 Growth returning 38.5% compared with the Russell 1000 Value Index's gain of 2.8% over the year. Bonds lagged stocks, with the Barclays U.S. Aggregate underperforming all equity benchmarks with a 7.5% return. Long-dated US Treasuries performed better with the Barclays Long-Term Treasury Index gaining 18.1%. Commodities fell, with the Bloomberg Commodity Index declining 3.5% while the dollar lost 6.69% while gold gain 21.9% and Bitcoin took off to a new all-time-high returning 305.1%. Oil prices partially recovered from their declines earlier in the year ending the year down 20.5%. All major developed countries except for France, United Kingdom and Hong Kong ended the year up in local currency terms, with the US being the best market with a total return of 18.4% followed closely by Japan at 18.2%. Emerging market countries had a strong year helped by the dollar decline with India and Shanghai posting the largest gains in local currency terms, 16.6% and 16.6%, respectively.

How did we respond to these changing market conditions?

Short-term periods of high uncertainty, such as what we experienced in early 2020, often present buying opportunities for the Fund, as we aim to capitalize on favorable price dislocations relative to strong fundamentals. The Fund aims to monetize volatility in the market by paring back winners and adding to names where the market does not appropriately reflect the embedded intrinsic value. We also sold securities of companies we believed might be impaired by the COVID crisis to manage risk. Overall, our activity aimed to improve the risk-adjusted return potential of the portfolio. The Fund initiated 27 new positions and eliminated 20 in the year as we used the volatility opportunistically to improve the return potential of the portfolio.

Growth drove much of the market's returns in 2020, with the Russell 1000 Growth outperforming the Russell 1000 Value in 3 of the 4 quarters. The Fund, however, continues to invest in a mix of mispriced secular (long-term compounders) and cyclical (class value) companies, a positioning that enabled the Fund to respond favorably to the shifting market environment as we slowly recovered from the early 2020 disruption. The Fund trades attractively relative to the S&P 500 benchmark, with a forward Price-to-Earnings at 12.5x versus the S&P 500's 23.1x (as of 12/31/20).

What were the leading contributors to performance?

Farfetch Ltd. (FTCH), Amazon.com, Inc. (AMZN), and Peloton Interactive, Inc. (PTON) were the top contributors for the year based on contribution to total return.

Miller Opportunity Trust 2020 Annual Report

9

Miller Opportunity Trust manager commentary (unaudited) (cont'd)

What were the leading detractors from performance?

American Airlines Group Inc. (AAL), Delta Air Lines Inc. (DAL), and Flexion Therapeutics (FLXN) were the top detractors for the year based on contribution to total return.

Were there any significant changes to the Fund during the reporting period?

As discussed above, during the year we initiated 27 new positions while eliminating 20 holdings, bringing the Fund's total names to 47 as of December 31. The Fund's top 10 represent 41.8%% of total assets compared to 27.4% for the index, and maintained its meaningful active share of 94.3%. The manager provides a quarterly letter discussing portfolio changes at http://millervaluefunds.com.

The S&P 500 Index is a market capitalization-weighted index of 500 widely held common stocks. An investor cannot invest directly in an index. Unmanaged index returns do not reflect any fees, expenses or sales charges. The NASDAQ Composite Index is a market capitalization-weighted index that is designed to represent the performance of NASDAQ securities and it includes over 3,000 stocks. The Dow Jones Industrial Average (DJIA) is an unmanaged index composed of 30 blue-chip stocks, each with annual sales exceeding $7 billion. The DJIA is price-weighted, reflects large-cap companies representative of U.S. industry, and historically has moved in tandem with other major market indexes, such as the S&P 500. The Russell 1000® Index measures the performance of the 1,000 largest companies in the Russell 3000 Index, which represents approximately 92% of the total market capitalization of the Russell 3000 Index. The Russell Midcap Index, an unmanaged index, measures the performance of the 800 smallest companies in the Russell 1000 Index. The Russell 1000® Growth Index measures the performance of those Russell 1000 Index companies with higher price-to-book ratios and higher forecasted growth values. The Russell 1000® Value Index measures the performance of those Russell 1000 Index companies with lower price-to-book ratios and lower forecasted growth values. The Barclays U.S. Aggregate Bond Index tracks the daily price, coupon, pay-downs, and total return performance of fixed-rate, publicly placed, dollar-denominated, and nonconvertible investment grade debt issues with at least $250 million par amount outstanding and with at least one year to final maturity. The Barclays Long-Term Treasury Index includes publicly issued U.S. Treasury securities that have a remaining maturity of 10 or more years, are rated investment grade, and have $250 million or more of outstanding face value. An investor cannot invest directly in an index. Unmanaged index returns do not reflect any fees, expenses or sales charges. The Bloomberg Commodity Index is a highly liquid and diversified benchmark for commodity investments. Price-to-Earnings is the market price per share divided by earnings per share. The Russell 2000 index measures

Miller Opportunity Trust 2020 Annual Report

10

the performance of the 2,000 smallest-cap companies in the Russell 3000 Index. Free cash flow is earnings before depreciation, amortization, and non-cash charges minus maintenance capital expenditures. Book value is the value at which an asset is carried on a balance sheet. Duration is a measure of the sensitivity of a bond price or other debt instrument price to a change in interest rates. Dividend yield is the ratio of a company's annual dividend compared to its share price. Price-to-book ratio is used to compare a stock's market value to its book value. It is calculated by dividing the current closing price of the stock by the latest quarter's book value per share. Discounted cash flows is a valuation methodology used to estimate the value of an investment based on its expected future cash flows. Enterprise value (EV) is a measure of a company's total value. Return on invested capital (ROIC) is a ratio that is used to assess a company's efficiency at allocating the capital under its control to profitable investments. EBITDA is earnings before interest, taxes, depreciation and amortization and is a calculation of a company's financial health. SPX is the S&P 500 Index.

Must be preceded or accompanied by a current prospectus.

The views expressed are those of the portfolio managers as of the date indicated, are subject to change, and may differ from the views of other portfolio managers or the firm as a whole. These opinions are not intended to be a forecast of future events, a guarantee of future results, or investment advice. All data referenced are from sources deemed to be reliable but cannot be guaranteed.

Discussions of individual securities are intended to inform shareholders as to the basis (in whole or in part) for previously made decisions by a portfolio manager to buy, sell or hold a security in a portfolio. References to specific securities are not intended and should not be relied upon as the basis for anyone to buy, sell or hold any security. Portfolio holdings and sector allocations may not be representative of the portfolio manager's current or future investment and are subject to change at any time. Please refer to the schedule of investments in this report for complete holdings information.

Equity securities are subject to price fluctuation and possible loss of principal. Small- and mid-cap stocks involve greater risks and volatility than large-cap stocks. Real estate investment trusts (REITs) are closely linked to the performance of the real estate markets. REITs are subject to illiquidity, credit and interest rate risks, and risks associated with small and mid-cap investments. Asset-backed, mortgage-backed or mortgage-related securities are subject to prepayment and extension risks. Investments in MLP securities are subject to unique risks, including the risks of MLPs and the energy sector,

Miller Opportunity Trust 2020 Annual Report

11

Miller Opportunity Trust manager commentary (unaudited) (cont'd)

including the risks of declines in energy and commodity prices, decreases in energy demand, adverse weather conditions, natural or other disasters, changes in government regulation, and changes in tax laws. Short selling is a speculative strategy. Unlike the possible loss on a security that is purchased, there is no limit on the amount of loss on an appreciating security that is sold short. International investments are subject to special risks, including currency fluctuations and social, economic and political uncertainties, which could increase volatility. These risks are magnified in emerging markets. Fixed income securities involve interest rate, credit, inflation, and reinvestment risks; and possible loss of principal. As interest rates rise, the value of fixed-income securities falls. High yield bonds are subject to greater price volatility, illiquidity, and possibility of default. As a non-diversified Fund, it is permitted to invest a higher percentage of its assets in any one issuer than a diversified fund, which may magnify the Fund's losses from events affecting a particular issuer. Derivatives, such as options and futures, can be illiquid, may disproportionately increase losses, and have a potentially large impact on Fund performance.

Earnings growth is not representative of the Fund's future performance.

The Miller Value Funds are distributed by Quasar Distributors, LLC.

Miller Opportunity Trust 2020 Annual Report

12

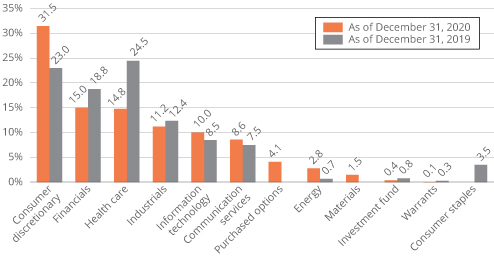

Fund at a glance+ (unaudited)

Investment breakdown (%) as a percentage of total investments

+ The bar graph above represents the composition of the Fund's investments as of December 31, 2020 and December 31, 2019. The Fund is actively managed. As a result, the composition of the Fund's investments is subject to change at any time.

Miller Opportunity Trust 2020 Annual Report

13

Fund expenses (unaudited)

As a shareholder of the Fund, you may incur two types of costs: (1) transaction costs, including front-end and back-end sales charges (loads) on purchase payments; and (2) ongoing costs, including management fees; service and/or distribution (12b-1) fees; and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The example is based on an investment of $1,000 invested on July 1, 2020 and held for the six months ended December 31, 2020.

Actual Expenses

The table below titled "Based on total actual return" provides information about actual account values and actual expenses. You may use the information provided in this table, together with the amount you invested, to estimate the expenses that you paid over the period. To estimate the expenses you paid on your account, divide your ending account value by $1,000 (for example, an $8,600 ending account value divided by $1,000 = 8.6), then multiply the result by the number under the heading entitled "Expenses Paid During the Period".

Hypothetical Example for Comparison Purposes

The table below titled "Based on hypothetical actual return" provides information about hypothetical account values and hypothetical expenses based on the actual expense ratio and an assumed rate of return of 5.00% per year before expenses, which is not the Fund's actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information provided in this table to compare the ongoing costs of investing in the Fund and other funds. To do so, compare the 5.00% hypothetical example relating to the Fund with the 5.00% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table below are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as front-end or back-end sales charges (loads). Therefore, the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs could have been higher.

Miller Opportunity Trust 2020 Annual Report

14

Based on total actual return1

| Actual Total Return Without Sales Charges2 | Beginning Account Value | Ending Account Value | Annualized Expense Ratio | Expenses Paid During the Period3 | |||||||||||||||||||

Class A | 53.99 | % | $ | 1,000.00 | $ | 1,539.90 | 1.24 | % | $ | 7.93 | |||||||||||||

Class C | 53.39 | 1,000.00 | 1,533.90 | 1.99 | 12.67 | ||||||||||||||||||

Class FI | 53.92 | 1,000.00 | 1,539.20 | 1.31 | 8.36 | ||||||||||||||||||

Class R | 53.75 | 1,000.00 | 1,537.50 | 1.48 | 9.44 | ||||||||||||||||||

Class I | 54.14 | 1,000.00 | 1,541.40 | 1.00 | 6.36 | ||||||||||||||||||

Class IS | 54.24 | 1,000.00 | 1,542.40 | 0.93 | 5.94 | ||||||||||||||||||

Based on hypothetical actual return1

| Hypothetical Annualized Total Return | Beginning Account Value | Ending Account Value | Annualized Expense Ratio | Expenses Paid During the Period3 | |||||||||||||||||||

Class A | 5.00 | % | $ | 1,000.00 | $ | 1,018.89 | 1.24 | % | $ | 6.30 | |||||||||||||

Class C | 5.00 | 1,000.00 | 1,015.13 | 1.99 | 10.08 | ||||||||||||||||||

Class FI | 5.00 | 1,000.00 | 1,018.55 | 1.31 | 6.65 | ||||||||||||||||||

Class R | 5.00 | 1,000.00 | 1,017.69 | 1.48 | 7.51 | ||||||||||||||||||

Class I | 5.00 | 1,000.00 | 1,020.13 | 1.00 | 5.06 | ||||||||||||||||||

Class IS | 5.00 | 1,000.00 | 1,020.46 | 0.93 | 4.72 | ||||||||||||||||||

1 For the six months ended December 31, 2020.

2 Assumes the reinvestment of all distributions, including returns of capital, if any, at net asset value or does not reflect the deduction of the applicable sales charge with respect to Class A shares or the applicable contingent deferred sales charge ("CSDC") with respect to Class C shares. Total return is not annualized, as it may not be representative of the total return for the year. Performance figures may reflect compensating balance arrangements, fee waivers and/or expense reimbursements. In the absence of compensating balance arrangements, fee waivers and/or expense reimbursements, the total return would have been lower. Past performance is no guarantee of future results.

3 Expenses (net of compensating balance arrangements, fee waivers and/or expense reimbursements) are equal to each class' respective annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year (184), then divided by 366.

Miller Opportunity Trust 2020 Annual Report

15

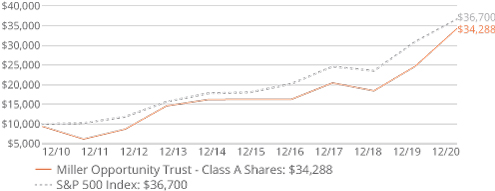

Fund performance (unaudited)

Historical Performance

Value of $10,000 invested in

Class A Shares of Miller Opportunity Trust vs. S&P 500 Index† — December 2010 - December 2020

All figures represent past performance and are not a guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Performance figures may reflect compensating balance arrangements, fee waivers and/or expense reimbursements. In the absence of compensating balance arrangements, fee waivers and/or expense reimbursements, the total return would have been lower.

† Hypothetical illustration of $10,000 invested in Class A shares of Miller Opportunity Trust on December 31, 2010, assuming the maximum sales charge at purchase and reinvestment of all distributions, including returns of capital, if any, at net asset value through December 31, 2020. The hypothetical illustration also assumes a $10,000 investment in the S&P 500 Index. The S&P 500 Index is an unmanaged index of 500 stocks and is generally representative of the performance of larger companies in the U.S. The index is unmanaged and is not subject to the same management and trading expenses as a mutual fund. Please note that an investor cannot invest directly in an index. The performance of the Fund's other classes may be greater or less than the Class A shares' performance indicated on this chart, depending on whether greater or lesser sales charges and fees were incurred by shareholders investing in the other classes.

Miller Opportunity Trust 2020 Annual Report

16

Schedule of investments

December 31, 2020

Miller Opportunity Trust

Security | Shares | Value | |||||||||

Common Stocks — 101.2% | |||||||||||

Communication Services — 9.1% | |||||||||||

Entertainment — 1.2% | |||||||||||

Netflix Inc. * | 50,000 | $ | 27,036,500 | ||||||||

Interactive Media & Services — 6.2% | |||||||||||

Alphabet Inc. *(a) | 37,500 | 65,724,000 | |||||||||

Facebook Inc., Class A Shares *(a) | 270,000 | 73,753,200 | |||||||||

Total Interactive Media & Services | 139,477,200 | ||||||||||

Media — 1.7% | |||||||||||

Discovery Inc., Class A Shares * | 1,300,000 | 39,117,000 | |||||||||

Total Communication Services | 205,630,700 | ||||||||||

Consumer Discretionary — 33.4% | |||||||||||

Diversified Consumer Services — 2.2% | |||||||||||

WW International Inc. * | 2,000,000 | 48,800,000 | |||||||||

Hotels, Restaurants & Leisure — 2.3% | |||||||||||

Norwegian Cruise Line Holdings Ltd. * | 2,000,000 | 50,860,000 | |||||||||

Household Durables — 2.8% | |||||||||||

Taylor Morrison Home Corp. * | 2,450,000 | 62,842,500 | |||||||||

Internet & Direct Marketing Retail — 21.3% | |||||||||||

Alibaba Group Holding Ltd. — ADR * | 300,000 | 69,819,000 | |||||||||

Amazon.com Inc. *(a) | 30,000 | 97,707,900 | |||||||||

Farfetch Ltd. *(a) | 1,800,000 | 114,858,000 | |||||||||

Quotient Technology Inc. *(b) | 4,900,000 | 46,158,000 | |||||||||

RealReal Inc./The * | 2,900,000 | 56,666,000 | |||||||||

Stitch Fix Inc., Class A Shares * | 1,600,000 | 93,952,000 | |||||||||

Total Internet & Direct Marketing Retail | 479,160,900 | ||||||||||

Specialty Retail — 2.9% | |||||||||||

Vroom Inc. * | 1,600,000 | 65,552,000 | |||||||||

Textiles, Apparel & Luxury Goods — 1.9% | |||||||||||

Canada Goose Holdings Inc. *(a) | 1,450,000 | 43,166,500 | |||||||||

Total Consumer Discretionary | 750,381,900 | ||||||||||

Energy — 2.9% | |||||||||||

Oil, Gas & Consumable Fuels — 2.9% | |||||||||||

Diamondback Energy Inc. | 450,000 | 21,780,000 | |||||||||

Energy Transfer LP | 7,100,000 | 43,878,000 | |||||||||

Total Oil, Gas & Consumable Fuels | 65,658,000 | ||||||||||

Total Energy | 65,658,000 | ||||||||||

Financials — 15.9% | |||||||||||

Banks — 6.5% | |||||||||||

Bank of America Corp. | 1,700,000 | 51,527,000 | |||||||||

Citigroup Inc. (a) | 700,000 | 43,162,000 | |||||||||

JPMorgan Chase & Co. | 400,000 | 50,828,000 | |||||||||

Total Banks | 145,517,000 | ||||||||||

Miller Opportunity Trust 2020 Annual Report

17

Schedule of investments (cont'd)

December 31, 2020

Miller Opportunity Trust

Security | Shares | Value | |||||||||

Consumer Finance — 5.9% | |||||||||||

Capital One Financial Corp. | 525,000 | $ | 51,896,250 | ||||||||

OneMain Holdings Inc.(a) | 1,700,000 | 81,872,000 | |||||||||

Total Consumer Finance | 133,768,250 | ||||||||||

Insurance — 1.0% | |||||||||||

Genworth Financial Inc., Class A Shares *(a) | 6,000,000 | 22,680,000 | |||||||||

Thrifts & Mortgage Finance — 2.5% | |||||||||||

Rocket Cos Inc. * | 2,800,000 | 56,616,000 | |||||||||

Total Financials | 358,581,250 | ||||||||||

Health Care — 15.7% | |||||||||||

Biotechnology — 5.1% | |||||||||||

Flexion Therapeutics Inc. *(b) | 3,200,000 | 36,928,000 | |||||||||

Precigen Inc. * | 5,400,000 | 55,080,000 | |||||||||

ZIOPHARM Oncology Inc. *(b) | 9,400,000 | 23,688,000 | |||||||||

Total Biotechnology | 115,696,000 | ||||||||||

Health Care Providers & Services — 2.0% | |||||||||||

Tivity Health Inc. * | 2,300,000 | 45,057,000 | |||||||||

Life Sciences Tools & Services — 2.0% | |||||||||||

PureTech Health Plc * | 8,000,000 | 43,760,085 | |||||||||

Pharmaceuticals — 6.6% | |||||||||||

Bausch Health Cos Inc. *(a) | 2,600,000 | 54,080,000 | |||||||||

Green Thumb Industries Inc. * | 1,700,000 | 41,650,000 | |||||||||

Teva Pharmaceutical Industries Ltd. — ADR * | 5,400,000 | 52,110,000 | |||||||||

Total Pharmaceuticals | 147,840,000 | ||||||||||

Total Health Care | 352,353,085 | ||||||||||

Industrials — 11.9% | |||||||||||

Aerospace & Defense — 1.9% | |||||||||||

Boeing Co/The * | 200,000 | 42,812,000 | |||||||||

Airlines — 2.0% | |||||||||||

Delta Air Lines Inc. (a) | 1,100,000 | 44,231,000 | |||||||||

Commercial Services & Supplies — 3.3% | |||||||||||

ADT Inc. (a) | 9,500,000 | 74,575,000 | |||||||||

Electrical Equipment — 2.7% | |||||||||||

Acuity Brands Inc. | 500,000 | 60,545,000 | |||||||||

Road & Rail — 2.0% | |||||||||||

Uber Technologies Inc. * | 900,000 | 45,900,000 | |||||||||

Total Industrials | 268,063,000 | ||||||||||

Information Technology — 10.7% | |||||||||||

IT Services — 4.6% | |||||||||||

DXC Technology Co. (a) | 4,000,000 | 103,000,000 | |||||||||

Miller Opportunity Trust 2020 Annual Report

18

Miller Opportunity Trust

Security | Shares | Value | |||||||||||||||||||||

Software — 2.0% | |||||||||||||||||||||||

GTY Technology Holdings Inc. * | 1,500,000 | $ | 7,770,000 | ||||||||||||||||||||

Workday Inc. * | 150,000 | 35,941,500 | |||||||||||||||||||||

Total Software | 43,711,500 | ||||||||||||||||||||||

Technology Hardware, Storage & Peripherals — 4.1% | |||||||||||||||||||||||

Desktop Metal Inc. *(c)(d) | 6,000,000 | 92,880,000 | |||||||||||||||||||||

Total Information Technology | 239,591,500 | ||||||||||||||||||||||

Materials — 1.6% | |||||||||||||||||||||||

Chemicals — 1.6% | |||||||||||||||||||||||

Chemours Co/The | 1,400,000 | 34,706,000 | |||||||||||||||||||||

Total Materials | 34,706,000 | ||||||||||||||||||||||

| Total Common Stocks (Cost — $1,793,297,098) | 2,274,965,435 | ||||||||||||||||||||||

Investment Fund — 0.5% | |||||||||||||||||||||||

Pangaea One, LP (b)(c)(d) | 1 | 10,096,002 | |||||||||||||||||||||

| Total Investment Fund (Cost — $33,993,989) | 10,096,002 | ||||||||||||||||||||||

| Maturity Date | Strike Price | Contracts | Notional ($) | ||||||||||||||||||||

Purchased Options — 4.4% | |||||||||||||||||||||||

CVS Health Corp. | Jan. 20, 2023 | $ | 60.00 | 6,500 | 44,395,000 | 8,726,250 | |||||||||||||||||

Uber Technologies Inc. | Jan. 21, 2022 | 32.00 | 42,000 | 214,200,000 | 90,195,000 | ||||||||||||||||||

| Total Purchased Options (Cost — $40,066,752) | 98,921,250 | ||||||||||||||||||||||

| Expiration Date | Exercise Price | Shares | |||||||||||||||||||||

Warrants — 0.1% | |||||||||||||||||||||||

| GTY Technology Holdings Inc. * | Feb. 19, 2024 | $ | 11.50 | 482,500 | 168,875 | ||||||||||||||||||

| ZIOPHARM Oncology Inc. *(b)(c)(d) | Jul. 26, 2024 | 7.00 | 3,787,879 | 1,846,591 | |||||||||||||||||||

| Total Warrants (Cost — $1,678,957) | 2,015,466 | ||||||||||||||||||||||

| Total Investments — 106.2% (Cost — $1,869,036,796) | $ | 2,385,998,153 | |||||||||||||||||||||

Liabilities in Excess of Other Assets — (6.2)% | (139,017,765 | ) | |||||||||||||||||||||

Total Net Assets — 100.0% | $ | 2,246,980,388 | |||||||||||||||||||||

* Non-income producing security.

(a) All or a portion of this security is pledged as collateral pursuant to the loan agreement.

(b) In this instance, as defined in the Investment Company Act of 1940, an "Affiliated Company" represents Fund ownership of at least 5% of the outstanding voting securities of an issuer, or outstanding capital for Pangaea One, LP. At December 31, 2020, the total market value

Miller Opportunity Trust 2020 Annual Report

19

Schedule of investments (cont'd)

December 31, 2020

Miller Opportunity Trust

of investments in Affiliated Companies was $118,716,593 and the cost was $183,394,212. (See Note 8).

(c) Security is valued in good faith in accordance with procedures approved by the Board of Trustees (See Note 2).

(d) Restricted security (See Note 9).

The Global Industry Classification Standard (GICS®) was developed by and/or is the exclusive property of Morgan Stanley International, Inc. ("MSCI") and Standard & Poor's Financial Services LLC ("S&P"). GICS is a service mark of MSCI and S&P and has been licensed for use by U.S. Bancorp Fund Services, LLC.

The Accompanying Notes are an Integral Part of these Financial Statements.

Miller Opportunity Trust 2020 Annual Report

20

Statement of assets and liabilities

December 31, 2020

Assets: | |||||||

Investments in unaffiliated securities, at value (Cost $1,685,642,584) | $ | 2,267,281,560 | |||||

Investments in affiliated securities, at value (Cost $183,394,212) | 118,716,593 | ||||||

Cash | 4,724,361 | ||||||

Receivable for securities sold | 6,594,557 | ||||||

Receivable for Fund shares sold | 2,231,303 | ||||||

Dividends and interest receivable | 332,500 | ||||||

Prepaid expenses | 54,394 | ||||||

Total Assets | 2,399,935,268 | ||||||

Liabilities: | |||||||

Line of credit payable (Note 6) | 145,000,000 | ||||||

Payable for securities purchased | 2,453,945 | ||||||

Payable for Fund shares repurchased | 2,761,647 | ||||||

Investment management fee payable | 1,457,192 | ||||||

Distribution and service fees payable | 683,201 | ||||||

Interest payable | 102,944 | ||||||

Accrued other expenses | 495,951 | ||||||

Total Liabilities | 152,954,880 | ||||||

Total Net Assets | $ | 2,246,980,388 | |||||

Net Assets: | |||||||

Paid-in capital | $ | 1,704,635,371 | |||||

Total accumulated earnings | 542,345,017 | ||||||

Total Net Assets | $ | 2,246,980,388 | |||||

The Accompanying Notes are an Integral Part of these Financial Statements.

Miller Opportunity Trust 2020 Annual Report

21

Statement of assets and liabilities (cont'd)

December 31, 2020

Net Assets: | |||||||

Class A | $ | 941,941,856 | |||||

Class C | $ | 204,213,513 | |||||

Class FI | $ | 14,458,308 | |||||

Class R | $ | 8,194,811 | |||||

Class I | $ | 1,077,437,575 | |||||

Class IS | $ | 734,325 | |||||

Shares Outstanding: | |||||||

Class A | 23,556,910 | ||||||

Class C | 5,531,541 | ||||||

Class FI | 351,051 | ||||||

Class R | 205,778 | ||||||

Class I | 24,638,593 | ||||||

Class IS | 16,759 | ||||||

Net Asset Value: | |||||||

Class A (and redemption price) | $ | 39.99 | |||||

Class C (redemption price* and offering price per share) | $ | 36.92 | |||||

Class FI (redemption price and offering price per share) | $ | 41.19 | |||||

Class R (redemption price and offering price per share) | $ | 39.82 | |||||

Class I (redemption price and offering price per share) | $ | 43.73 | |||||

Class IS (redemption price and offering price per share) | $ | 43.82 | |||||

Maximum Public Offering Price Per Share: | |||||||

Class A (based on maximum initial sales charge of 5.75%) | $ | 42.43 | |||||

* Redemption price per share of Class C shares is NAV reduced by a 1.00% CDSC if shares are redeemed within one year of purchase (See Note 3).

The Accompanying Notes are an Integral Part of these Financial Statements.

Miller Opportunity Trust 2020 Annual Report

22

Statement of operations

For the Year Ended December 31, 2020

Investment Income: | |||||||

Dividends from unaffiliated investments (Net of foreign tax of $56,250) | $ | 19,355,449 | |||||

Dividends from affiliated investments | 393,306 | ||||||

Total Investment Income | 19,748,755 | ||||||

Expenses: | |||||||

Investment management fee (Note 3) | 12,221,941 | ||||||

Distribution fees (Note 5) | 3,446,535 | ||||||

Interest expense (Note 6) | 1,574,264 | ||||||

Shareholder servicing fee (Note 5) | 1,021,038 | ||||||

Administration and fund accounting fees (Note 3) | 839,797 | ||||||

Transfer agent expenses (Note 3) | 358,247 | ||||||

Registration fees | 113,659 | ||||||

Custody fees (Note 3) | 99,381 | ||||||

Shareholder reports | 96,392 | ||||||

Legal fees | 37,600 | ||||||

Audit and tax fees | 20,613 | ||||||

Insurance | 14,897 | ||||||

Trustees' fees (Note 3) | 14,326 | ||||||

Compliance fees (Note 3) | 13,279 | ||||||

Miscellaneous expenses | 78,635 | ||||||

Total Expenses | 19,950,604 | ||||||

Less: Fee waivers and/or expense reimbursement (Note 3) | (77,684 | ) | |||||

Net Expenses | 19,872,920 | ||||||

Net Investment loss | (124,165 | ) | |||||

Realized and Unrealized Gain (Loss) on Investments (Note 2): | |||||||

Net Realized Gain (Loss) From: | |||||||

Investments in unaffiliated securities | 136,627,305 | ||||||

Investments in affiliated securities | (5,118,375 | ) | |||||

Net Realized Gain | 131,508,930 | ||||||

Net Change in Unrealized Appreciation (Depreciation) From: | |||||||

Investments in unaffiliated securities | 535,782,567 | ||||||

Investments in affiliated securities | (50,938,179 | ) | |||||

Net Change in Unrealized Appreciation (Depreciation) | 484,844,388 | ||||||

Net Gain on Investments | 616,353,318 | ||||||

Increase in Net Assets from Operations | $ | 616,229,153 | |||||

The Accompanying Notes are an Integral Part of these Financial Statements.

Miller Opportunity Trust 2020 Annual Report

23

Statements of changes in net assets

For the Year Ended December 31, | 2020 | 2019 | |||||||||

Operations: | |||||||||||

Net investment loss | $ | (124,165 | ) | $ | (5,584,331 | ) | |||||

Net realized gain (loss) | 131,508,930 | (52,466,487 | ) | ||||||||

Change in unrealized appreciation | 484,844,388 | 491,729,797 | |||||||||

Increase in Net Assets from Operations | 616,229,153 | 433,678,979 | |||||||||

Fund Share Transactions (Note 7): | |||||||||||

Net proceeds from sale of shares | 386,734,000 | 611,530,990 | |||||||||

Cost of shares repurchased | (435,939,749 | ) | (683,295,174 | ) | |||||||

| (Decrease) in Net Assets from Fund Share Transactions | (49,205,749 | ) | (71,764,184 | ) | |||||||

Increase in Net Assets | 567,023,404 | 361,914,795 | |||||||||

Net Assets: | |||||||||||

Beginning of year | 1,679,956,984 | 1,318,042,189 | |||||||||

End of year | $ | 2,246,980,388 | $ | 1,679,956,984 | |||||||

The Accompanying Notes are an Integral Part of these Financial Statements.

Miller Opportunity Trust 2020 Annual Report

24

Financial highlights

For a share of beneficial interest outstanding throughout each year ended December 31:

Class A Shares | 2020 | 2019 | 2018 | 2017 | 2016 | ||||||||||||||||||

Net asset value, beginning of year | $ | 28.85 | $ | 21.54 | $ | 23.88 | $ | 18.96 | $ | 19.01 | |||||||||||||

Income (loss) from operations: | |||||||||||||||||||||||

Net investment income (loss)1 | (0.01 | ) | 0.002 | (0.13 | ) | (0.14 | ) | (0.09 | ) | ||||||||||||||

Net realized and unrealized gain (loss) | 11.15 | 7.31 | (2.21 | ) | 5.06 | 0.043 | |||||||||||||||||

| Total income (loss) from operations | 11.14 | 7.31 | (2.34 | ) | 4.92 | (0.05 | ) | ||||||||||||||||

Net asset value, end of year | $ | 39.99 | $ | 28.85 | $ | 21.54 | $ | 23.88 | $ | 18.96 | |||||||||||||

Total return4 | 38.61 | %5 | 33.94 | %5 | -9.80 | %5 | 25.95 | % | -0.26 | %5 | |||||||||||||

Net assets, end of year (000s) | $ | 941,942 | $ | 705,372 | $ | 221,842 | $ | 266,560 | $ | 216,974 | |||||||||||||

Ratios to average net assets: | |||||||||||||||||||||||

Gross expenses6 | 1.28 | % | 1.47 | % | 1.39 | % | 1.34 | % | 1.31 | % | |||||||||||||

Net expenses6 | 1.287 | 1.477 | 1.397 | 1.347 | 1.31 | ||||||||||||||||||

Net investment income (loss) | (0.04 | ) | 0.02 | (0.49 | ) | (0.64 | ) | (0.52 | ) | ||||||||||||||

Portfolio turnover rate | 64 | % | 35 | % | 30 | % | 120 | % | 85 | %8 | |||||||||||||

1 Per share amounts have been calculated using the average shares method.

2 Amount is less than $0.01 per share.

3 Calculation of the net gain per share (both realized and unrealized) does not correlate to the aggregate realized and unrealized losses presented in the Statement of Operations due to the timing of sales and repurchases of Fund shares in relation to fluctuating market values of the investments of the Fund.

4 Performance figures, exclusive of sales charges, may reflect fee waivers and/or expense reimbursements. In the absence of fee waivers and/or expense reimbursements, the total return would have been lower. Past performance is no guarantee of future results. Total returns for periods of less than one year are not annualized.

5 The total return includes gains from settlement of security litigations. Without these gains, the total return would have been 38.51%, 33.89%, -9.84% and -0.37% for the years ended December 31, 2020, 2019, 2018 and 2016, respectively.

6 Does not include fees and expenses of the Underlying Funds in which the Fund invests.

7 Effective April 30, 2020, the Adviser agreed to waive fees and/or reimburse operating expenses, (other than front-end or contingent deferred loads, taxes, interest expense, brokerage commissions, acquired fund fees and expenses, expenses incurred in connection with any merger or reorganization, portfolio transaction expenses, dividends paid on short sales, extraordinary expenses such as litigation, Rule 12b-1 fees, intermediary servicing fees, or any other class-specific expenses) through April 30, 2021, so that such annual operating expenses will not exceed 0.88%. Prior to April 30, 2020, the limit was 1.20% and established at the class level (inclusive of 12b-1 and shareholder servicing fees). Interest expenses were 0.10%, 0.28%, 0.21% and 0.16% for the years ended December 31, 2020, 2019, 2018 and 2017, respectively. Excluding interest, the expense ratios were 1.18%, 1.19%, 1.18% and 1.18% for the years ended December 31, 2020, 2019, 2018 and 2017, respectively (See Note 3).

8 Excludes securities delivered as a result of a redemption in-kind.

The Accompanying Notes are an Integral Part of these Financial Statements.

Miller Opportunity Trust 2020 Annual Report

25

Financial highlights (cont'd)

For a share of beneficial interest outstanding throughout each year ended December 31:

Class C Shares | 2020 | 2019 | 2018 | 2017 | 2016 | ||||||||||||||||||

Net asset value, beginning of year | $ | 26.84 | $ | 20.19 | $ | 22.55 | $ | 18.04 | $ | 18.23 | |||||||||||||

Income (loss) from operations: | |||||||||||||||||||||||

Net investment loss1 | (0.23 | ) | (0.29 | ) | (0.30 | ) | (0.29 | ) | (0.21 | ) | |||||||||||||

Net realized and unrealized gain (loss) | 10.31 | 6.94 | (2.06 | ) | 4.80 | 0.022 | |||||||||||||||||

| Total income (loss) from operations | 10.08 | 6.65 | (2.36 | ) | 4.51 | (0.19 | ) | ||||||||||||||||

Net asset value, end of year | $ | 36.92 | $ | 26.84 | $ | 20.19 | $ | 22.55 | $ | 18.04 | |||||||||||||

Total return3 | 37.56 | %4 | 32.94 | %4 | -10.47 | %4 | 25.00 | % | -1.04 | %4 | |||||||||||||

Net assets, end of year (000s) | $ | 204,214 | $ | 216,364 | $ | 559,251 | $ | 694,001 | $ | 657,038 | |||||||||||||

Ratios to average net assets: | |||||||||||||||||||||||

Gross expenses5 | 2.03 | % | 2.22 | % | 2.13 | % | 2.11 | % | 2.09 | % | |||||||||||||

Net expenses5 | 2.036 | 2.226 | 2.136 | 2.116 | 2.09 | ||||||||||||||||||

Net investment loss | (0.88 | ) | (1.25 | ) | (1.24 | ) | (1.42 | ) | (1.30 | ) | |||||||||||||

Portfolio turnover rate | 64 | % | 35 | % | 30 | % | 120 | % | 85 | %7 | |||||||||||||

1 Per share amounts have been calculated using the average shares method.

2 Calculation of the net gain per share (both realized and unrealized) does not correlate to the aggregate realized and unrealized losses presented in the Statement of Operations due to the timing of sales and repurchases of Fund shares in relation to fluctuating market values of the investments of the Fund.

3 Performance figures, exclusive of CDSC, may reflect fee waivers and/or expense reimbursements. In the absence of fee waivers and/or expense reimbursements, the total return would have been lower. Past performance is no guarantee of future results. Total returns for periods of less than one year are not annualized.

4 The total return includes gains from settlement of security litigations. Without these gains, the total return would have been 37.44%, 32.69%, -10.51% and -1.15% for the years ended December 31, 2020, 2019, 2018 and 2016, respectively.

5 Does not include fees and expenses of the Underlying Funds in which the Fund invests.

6 Effective April 30, 2020, the Adviser agreed to waive fees and/or reimburse operating expenses, (other than front-end or contingent deferred loads, taxes, interest expense, brokerage commissions, acquired fund fees and expenses, expenses incurred in connection with any merger or reorganization, portfolio transaction expenses, dividends paid on short sales, extraordinary expenses such as litigation, Rule 12b-1 fees, intermediary servicing fees, or any other class-specific expenses) through April 30, 2021, so that such annual operating expenses will not exceed 0.88%. Prior to April 30, 2020, the limit was 1.97% and established at the class level (inclusive of 12b-1 and shareholder servicing fees). Interest expenses were 0.10%, 0.28%, 0.21% and 0.16% for the years ended December 31, 2020, 2019, 2018 and 2017, respectively. Excluding interest, the expense ratios were 1.93%, 1.94%, 1.92% and 1.95% for the years ended December 31, 2020, 2019, 2018 and 2017, respectively (See Note 3).

7 Excludes securities delivered as a result of a redemption in-kind.

The Accompanying Notes are an Integral Part of these Financial Statements.

Miller Opportunity Trust 2020 Annual Report

26

For a share of beneficial interest outstanding throughout each year ended December 31:

Class FI Shares | 2020 | 2019 | 2018 | 2017 | 2016 | ||||||||||||||||||

Net asset value, beginning of year | $ | 29.74 | $ | 22.22 | $ | 24.64 | $ | 19.57 | $ | 19.62 | |||||||||||||

Income (loss) from operations: | |||||||||||||||||||||||

Net investment income (loss)1 | (0.05 | ) | (0.09 | ) | (0.14 | ) | (0.16 | ) | (0.10 | ) | |||||||||||||

Net realized and unrealized gain (loss) | 11.50 | 7.61 | (2.28 | ) | 5.23 | 0.052 | |||||||||||||||||

| Total income (loss) from operations | 11.45 | 7.52 | (2.42 | ) | 5.07 | (0.05 | ) | ||||||||||||||||

Net asset value, end of year | $ | 41.19 | $ | 29.74 | $ | 22.22 | $ | 24.64 | $ | 19.57 | |||||||||||||

Total return3 | 38.50 | %4 | 33.84 | %4 | -9.82 | %4 | 25.91 | % | -0.25 | %4 | |||||||||||||

Net assets, end of year (000s) | $ | 14,458 | $ | 14,026 | $ | 13,278 | $ | 24,394 | $ | 22,474 | |||||||||||||

Ratios to average net assets: | |||||||||||||||||||||||

Gross expenses5 | 1.35 | % | 1.53 | % | 1.41 | % | 1.39 | % | 1.35 | % | |||||||||||||

Net expenses5 | 1.356 | 1.536 | 1.416 | 1.396 | 1.35 | ||||||||||||||||||

Net investment loss | (0.19 | ) | (0.34 | ) | (0.53 | ) | (0.70 | ) | (0.56 | ) | |||||||||||||

Portfolio turnover rate | 64 | % | 35 | % | 30 | % | 120 | % | 85 | %7 | |||||||||||||

1 Per share amounts have been calculated using the average shares method.

2 Calculation of the net gain per share (both realized and unrealized) does not correlate to the aggregate realized and unrealized losses presented in the Statement of Operations due to the timing of sales and repurchases of Fund shares in relation to fluctuating market values of the investments of the Fund.

3 Performance figures may reflect fee waivers and/or expense reimbursements. In the absence of fee waivers and/or expense reimbursements, the total return would have been lower. Past performance is no guarantee of future results. Total returns for periods of less than one year are not annualized.

4 The total return includes gains from settlement of security litigations. Without these gains, the total return would have been 38.40%, 33.71%, -9.90% and -0.36% for the years ended December 31, 2020, 2019, 2018 and 2016, respectively.

5 Does not include fees and expenses of the Underlying Funds in which the Fund invests.

6 Effective April 30, 2020, the Adviser agreed to waive fees and/or reimburse operating expenses, (other than front-end or contingent deferred loads, taxes, interest expense, brokerage commissions, acquired fund fees and expenses, expenses incurred in connection with any merger or reorganization, portfolio transaction expenses, dividends paid on short sales, extraordinary expenses such as litigation, Rule 12b-1 fees, intermediary servicing fees, or any other class-specific expenses) through April 30, 2021, so that such annual operating expenses will not exceed 0.88%. Prior to April 30, 2020, the limit was 1.26% and established at the class level (inclusive of 12b-1 and shareholder servicing fees). Interest expenses were 0.10%, 0.28%, 0.21% and 0.16% for the years ended December 31, 2020, 2019, 2018 and 2017, respectively. Excluding interest, the expense ratios were 1.25%, 1.25%, 1.20% and 1.23% for the years ended December 31, 2020, 2019, 2018 and 2017, respectively (See Note 3).

7 Excludes securities delivered as a result of a redemption in-kind.

The Accompanying Notes are an Integral Part of these Financial Statements.

Miller Opportunity Trust 2020 Annual Report

27

Financial highlights (cont'd)

For a share of beneficial interest outstanding throughout each year ended December 31:

Class R Shares | 2020 | 2019 | 2018 | 2017 | 2016 | ||||||||||||||||||

Net asset value, beginning of year | $ | 28.81 | $ | 21.57 | $ | 23.98 | $ | 19.10 | $ | 19.21 | |||||||||||||

Income (loss) from operations: | |||||||||||||||||||||||

Net investment loss1 | (0.09 | ) | (0.14 | ) | (0.21 | ) | (0.21 | ) | (0.15 | ) | |||||||||||||

Net realized and unrealized gain (loss) | 11.10 | 7.38 | (2.20 | ) | 5.09 | 0.042 | |||||||||||||||||

| Total income (loss) from operations | 11.01 | 7.24 | (2.41 | ) | 4.88 | (0.11 | ) | ||||||||||||||||

Net asset value, end of year | $ | 39.82 | $ | 28.81 | $ | 21.57 | $ | 23.98 | $ | 19.10 | |||||||||||||

Total return3 | 38.22 | %4 | 33.57 | %4 | -10.05 | %4 | 25.55 | % | -0.57 | %4 | |||||||||||||

Net assets, end of year (000s) | $ | 8,195 | $ | 7,122 | $ | 5,778 | $ | 8,367 | $ | 7,708 | |||||||||||||

Ratios to average net assets: | |||||||||||||||||||||||

Gross expenses5 | 1.53 | % | 1.76 | % | 1.67 | % | 1.66 | % | 1.66 | % | |||||||||||||

Net expenses5 | 1.536 | 1.766 | 1.676 | 1.666 | 1.66 | ||||||||||||||||||

Net investment loss | (0.32 | ) | (0.54 | ) | (0.79 | ) | (0.97 | ) | (0.86 | ) | |||||||||||||

Portfolio turnover rate | 64 | % | 35 | % | 30 | % | 120 | % | 85 | %7 | |||||||||||||

1 Per share amounts have been calculated using the average shares method.

2 Calculation of the net gain per share (both realized and unrealized) does not correlate to the aggregate realized and unrealized losses presented in the Statement of Operations due to the timing of sales and repurchases of Fund shares in relation to fluctuating market values of the investments of the Fund.

3 Performance figures may reflect fee waivers and/or expense reimbursements. In the absence of fee waivers and/or expense reimbursements, the total return would have been lower. Past performance is no guarantee of future results. Total returns for periods of less than one year are not annualized.

4 The total return includes gains from settlement of security litigations. Without these gains, the total return would have been 38.11%, 33.43%, -10.13% and -0.68% for the years ended December 31, 2020, 2019, 2018 and 2016, respectively.

5 Does not include fees and expenses of the Underlying Funds in which the Fund invests.

6 Effective April 30, 2020, the Adviser agreed to waive fees and/or reimburse operating expenses, (other than front-end or contingent deferred loads, taxes, interest expense, brokerage commissions, acquired fund fees and expenses, expenses incurred in connection with any merger or reorganization, portfolio transaction expenses, dividends paid on short sales, extraordinary expenses such as litigation, Rule 12b-1 fees, intermediary servicing fees, or any other class-specific expenses) through April 30, 2021, so that such annual operating expenses will not exceed 0.88%. Prior to April 30, 2020, the limit was 1.55% and established at the class level (inclusive of 12b-1 and shareholder servicing fees). Interest expenses were 0.10%, 0.28%, 0.21% and 0.16% for the years ended December 31, 2020, 2019, 2018 and 2017, respectively. Excluding interest, the expense ratios were 1.43%, 1.48%, 1.46% and 1.50% for the years ended December 31, 2020, 2019, 2018 and 2017, respectively (See Note 3).

7 Excludes securities delivered as a result of a redemption in-kind.

The Accompanying Notes are an Integral Part of these Financial Statements.

Miller Opportunity Trust 2020 Annual Report

28

For a share of beneficial interest outstanding throughout each year ended December 31:

Class I Shares | 2020 | 2019 | 2018 | 2017 | 2016 | ||||||||||||||||||

Net asset value, beginning of year | $ | 31.48 | $ | 23.44 | $ | 25.91 | $ | 20.53 | $ | 20.51 | |||||||||||||

Income (loss) from operations: | |||||||||||||||||||||||

Net investment income (loss)1 | 0.07 | 0.01 | (0.07 | ) | (0.09 | ) | (0.06 | ) | |||||||||||||||

Net realized and unrealized gain (loss) | 12.18 | 8.03 | (2.40 | ) | 5.47 | 0.082 | |||||||||||||||||

| Total income (loss) from operations | 12.25 | 8.04 | (2.47 | ) | 5.38 | 0.02 | |||||||||||||||||

Net asset value, end of year | $ | 43.73 | $ | 31.48 | $ | 23.44 | $ | 25.91 | $ | 20.53 | |||||||||||||

Total return3 | 38.91 | %4 | 34.30 | %4 | -9.53 | %4 | 26.21 | % | 0.10 | %4 | |||||||||||||

Net assets, end of year (000s) | $ | 1,077,438 | $ | 736,467 | $ | 517,820 | $ | 480,451 | $ | 388,872 | |||||||||||||

Ratios to average net assets: | |||||||||||||||||||||||

Gross expenses5 | 1.04 | % | 1.23 | % | 1.15 | % | 1.12 | % | 1.05 | % | |||||||||||||

Net expenses5 | 1.036 | 1.216 | 1.146 | 1.096 | 1.05 | ||||||||||||||||||

Net investment income (loss) | 0.23 | 0.02 | (0.23 | ) | (0.39 | ) | (0.30 | ) | |||||||||||||||

Portfolio turnover rate | 64 | % | 35 | % | 30 | % | 120 | % | 85 | %7 | |||||||||||||

1 Per share amounts have been calculated using the average shares method.

2 Calculation of the net gain per share (both realized and unrealized) does not correlate to the aggregate realized and unrealized losses presented in the Statement of Operations due to the timing of sales and repurchases of Fund shares in relation to fluctuating market values of the investments of the Fund.

3 Performance figures may reflect fee waivers and/or expense reimbursements. In the absence of fee waivers and/or expense reimbursements, the total return would have been lower. Past performance is no guarantee of future results. Total returns for periods of less than one year are not annualized.

4 The total return includes gains from settlement of security litigations. Without these gains, the total return would have been 38.82%, 34.17%, -9.61% and -0.05% for the years ended December 31, 2020, 2019, 2018 and 2016, respectively.

5 Does not include fees and expenses of the Underlying Funds in which the Fund invests.

6 Effective April 30, 2020, the Adviser agreed to waive fees and/or reimburse operating expenses, (other than front-end or contingent deferred loads, taxes, interest expense, brokerage commissions, acquired fund fees and expenses, expenses incurred in connection with any merger or reorganization, portfolio transaction expenses, dividends paid on short sales, extraordinary expenses such as litigation, Rule 12b-1 fees, intermediary servicing fees, or any other class-specific expenses) through April 30, 2021, so that such annual operating expenses will not exceed 0.88%. Separately, the Adviser has agreed to waive fees and/or reimburse operating expenses such that the previously described annual operating expenses, plus intermediary servicing fees and other class-specific expenses, will not exceed 0.93% for Class I. Interest expenses were 0.10%, 0.28%, 0.21% and 0.16% for the years ended December 31, 2020, 2019, 2018 and 2017, respectively. Excluding interest, the net expense ratios were 0.93%, 0.93% for the years ended December 31, 2020, 2019, 2018 and 2017 (See Note 3).

7 Excludes securities delivered as a result of a redemption in-kind.

The Accompanying Notes are an Integral Part of these Financial Statements.

Miller Opportunity Trust 2020 Annual Report

29

Financial highlights (cont'd)

For a share of beneficial interest outstanding throughout each period ended December 31:

Class IS Shares | 2020 | 2019 | 2018** | ||||||||||||

Net asset value, beginning of period | $ | 31.52 | $ | 23.44 | $ | 32.06 | |||||||||

Income (loss) from operations: | |||||||||||||||

Net investment income1 | 0.08 | 0.23 | 0.01 | ||||||||||||

Net realized and unrealized gain (loss) | 12.22 | 7.85 | (8.63 | ) | |||||||||||

Total gain (loss) from operations | $ | 12.30 | $ | 8.08 | (8.62 | ) | |||||||||